Embed Size (px)

Citation preview

• Statement of Cash Flows• Purpose of the Statement of Cash Flows• Reports cash flows

– Cash flows from operating activities – transactions that affect net income.

– Cash flows from investing activities – transactions that affect noncurrent assets.

– Cash flows from financing activities – transactions that affect equity and debt of the entity.

1

• Noncash Investing and Financing Activities• Operating Activities, Investing Activities &

Financing Activities• Cash and Cash Equivalents• Direct Method

– Cash Received from Customers– Interest and Dividends Received– Cash Paid for Merchandise– Cash Payments for Expenses

2

STATEMENT OF CASH FLOWS –Indirect Method

Chapter

13

3

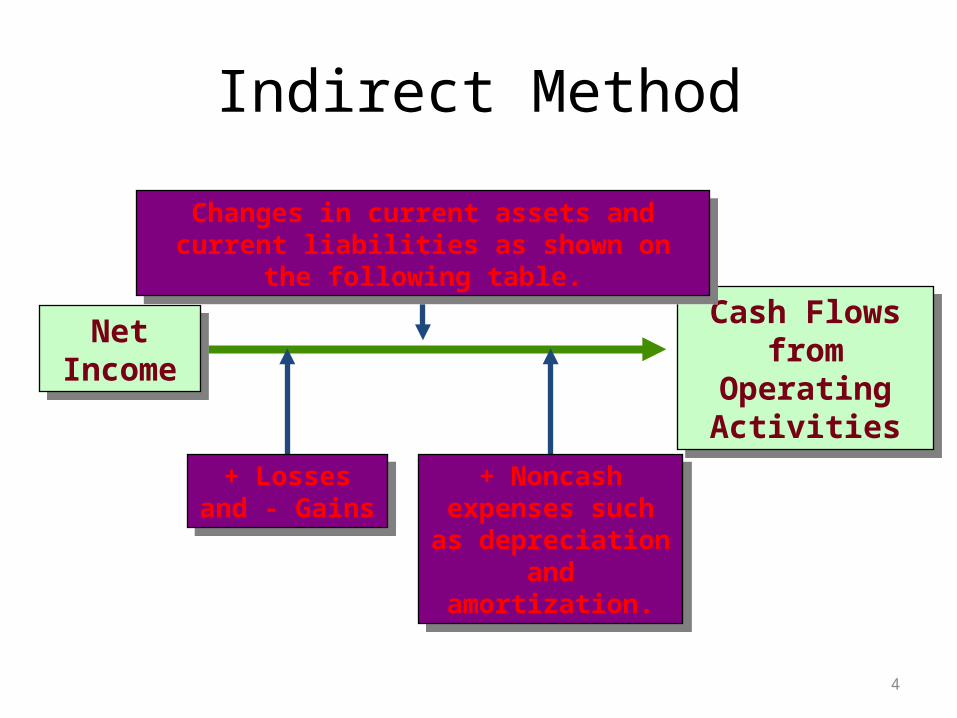

Net Income

Net Income

Cash Flows from Operating

Activities

Cash Flows from Operating

Activities

Indirect Method

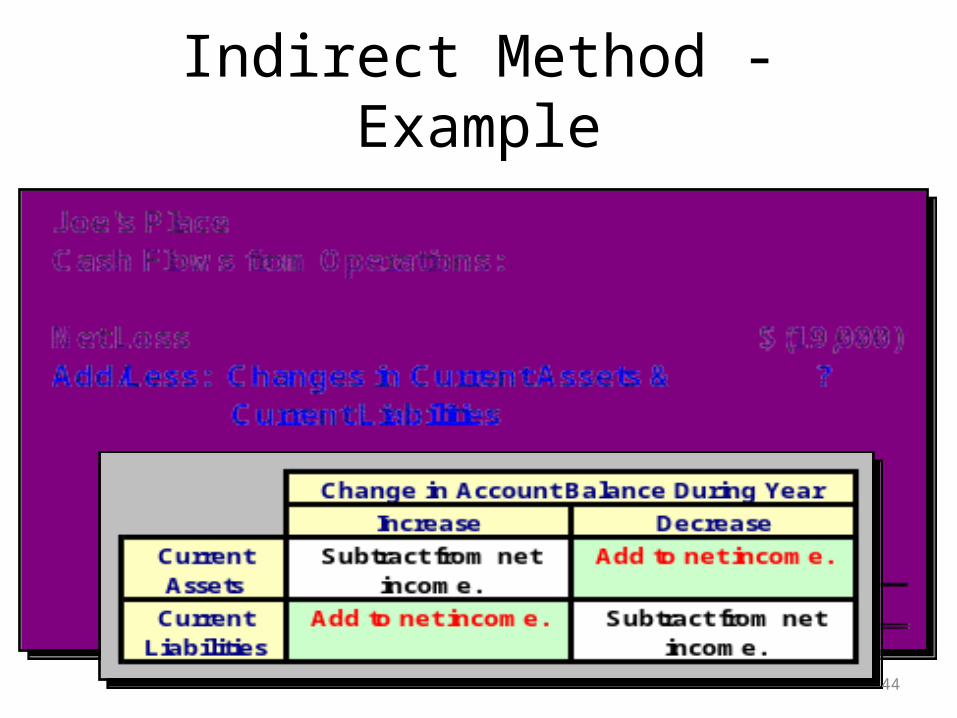

Changes in current assets and current liabilities as shown on the following table.

Changes in current assets and current liabilities as shown on the following table.

+ Losses and - Gains

+ Losses and - Gains

+ Noncash expenses such as depreciation and

amortization.

+ Noncash expenses such as depreciation and

amortization.

4

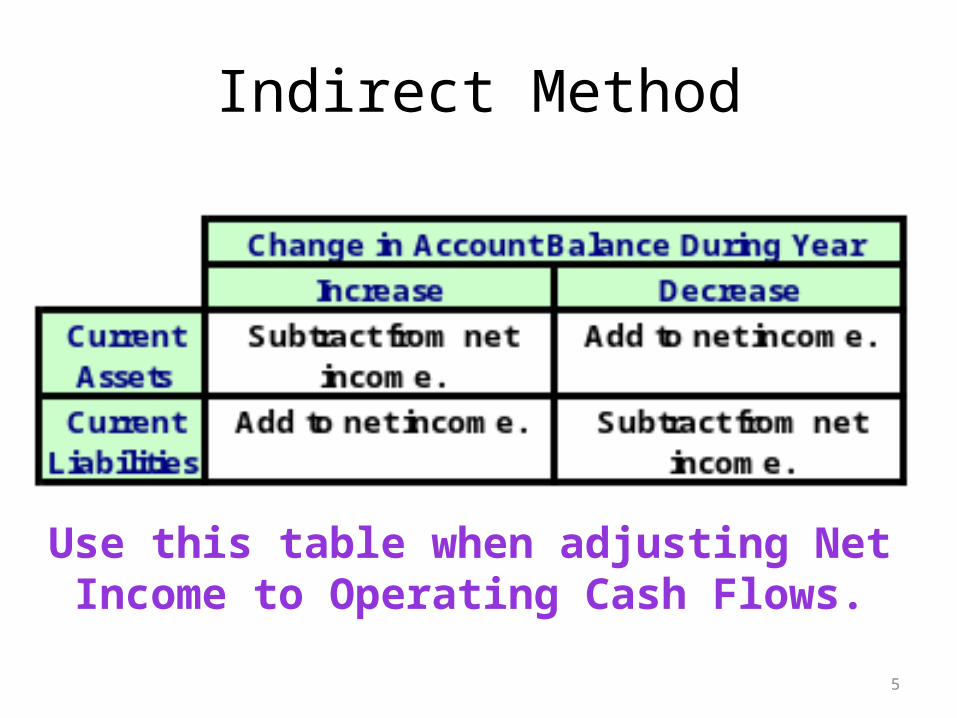

Use this table when adjusting Net Income to Operating Cash Flows.

Indirect Method

5

6

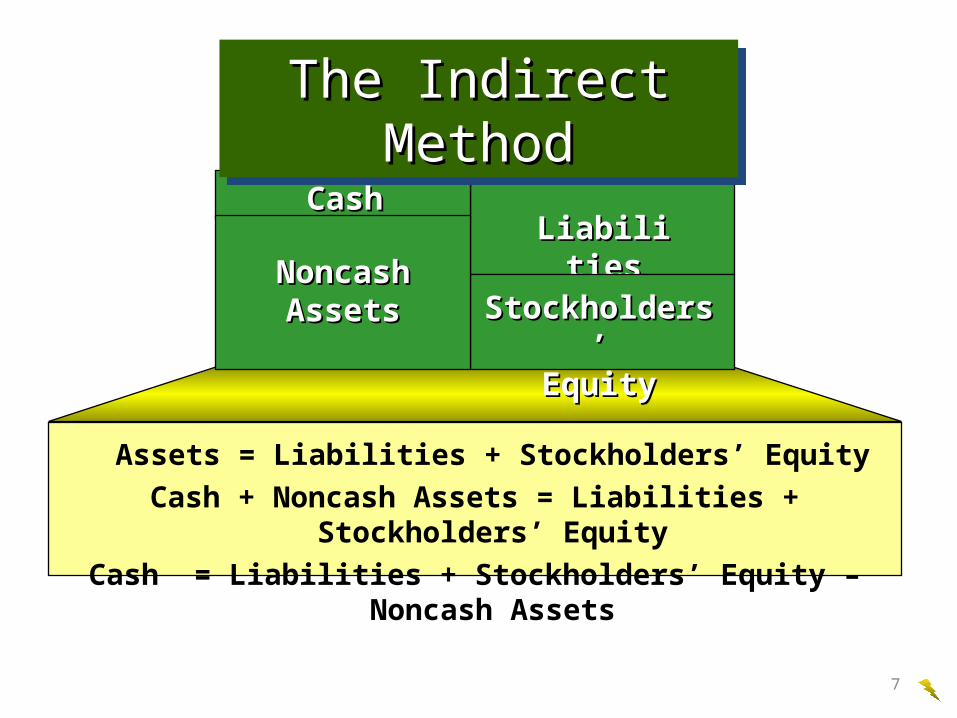

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Cash + Noncash Assets = Liabilities + Stockholders’ Equity

Cash = Liabilities + Stockholders’ Equity – Noncash Assets

CashCashLiabilitiesLiabilities

Stockholders’Stockholders’EquityEquity

NoncashNoncashAssetsAssets

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

7

CashLiabilitiesLiabilities

Stockholders’Stockholders’EquityEquity

Balance Sheet

NoncashNoncashAssetsAssets

Assets = Liabilities + Stockholders’ Equity

Cash + Noncash Assets = Liabilities + Stockholders’ Equity

Cash = Liabilities + Stockholders’ Equity – Noncash Assets

22 3311

The cash flows are determined by analyzing liabilities, The cash flows are determined by analyzing liabilities, stockholders’ equity, and noncash assets.stockholders’ equity, and noncash assets.

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

8

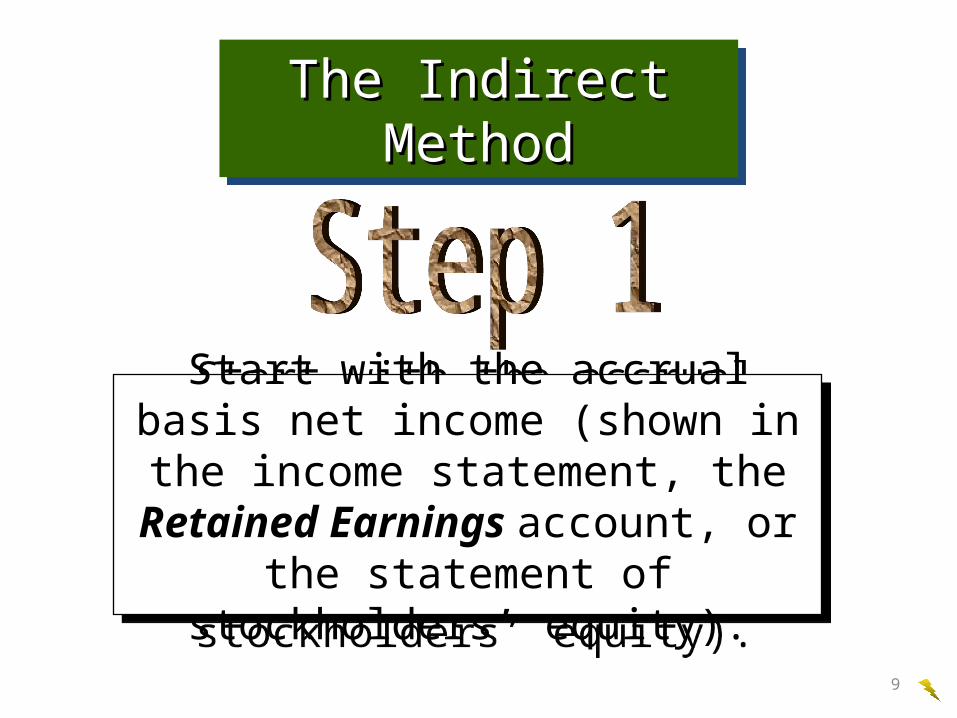

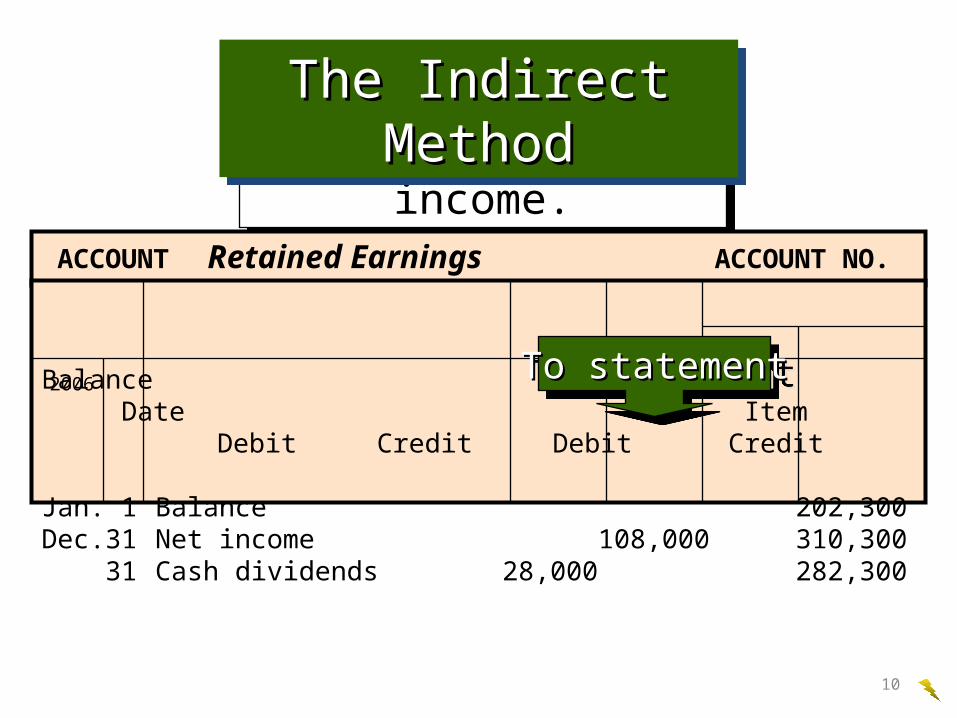

Start with the accrual basis net income (shown in the income statement, the Retained Earnings account, or the statement of stockholders’ equity).

Start with the accrual basis net income (shown in the income statement, the Retained Earnings account, or the statement of stockholders’ equity).

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

9

Find the net income.Find the net income.

ACCOUNT Retained Earnings ACCOUNT NO. 32

Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 202,300Dec. 31 Net income 108,000 310,300

31 Cash dividends 28,000 282,300

To statementTo statementTo statementTo statement

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

2006

10

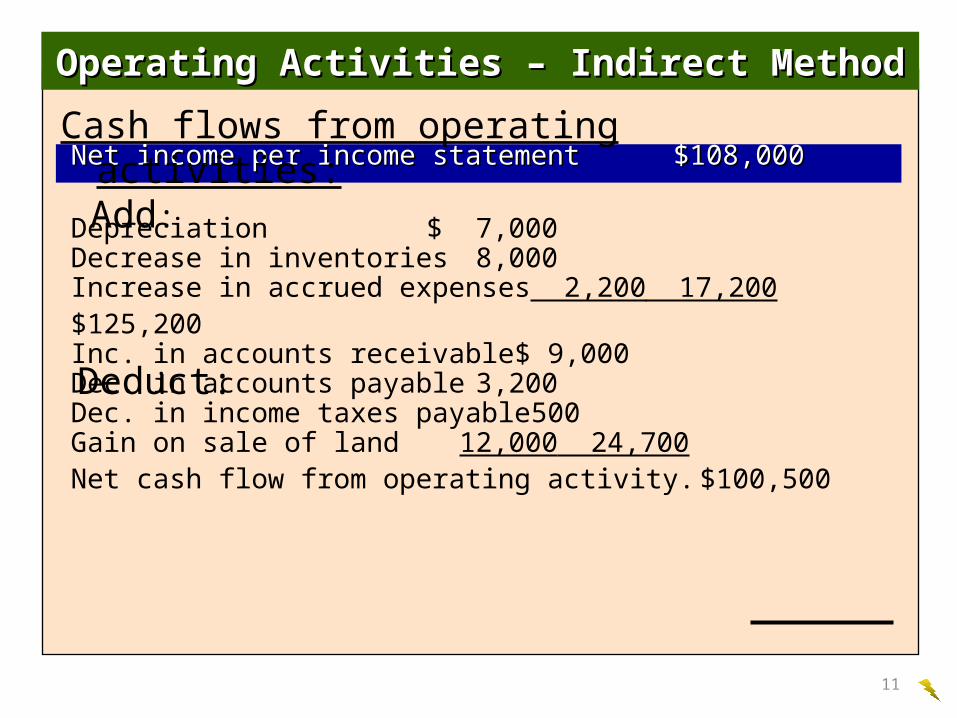

Net income per income statementNet income per income statement $108,000$108,000

Depreciation $ 7,000Decrease in inventories 8,000Increase in accrued expenses 2,200 17,200

$125,200Inc. in accounts receivable $ 9,000Dec. in accounts payable 3,200Dec. in income taxes payable 500Gain on sale of land 12,000 24,700

Net cash flow from operating activity. $100,500

Cash flows from operating activities:

Operating Activities – Indirect MethodOperating Activities – Indirect Method

Deduct:

Add:

11

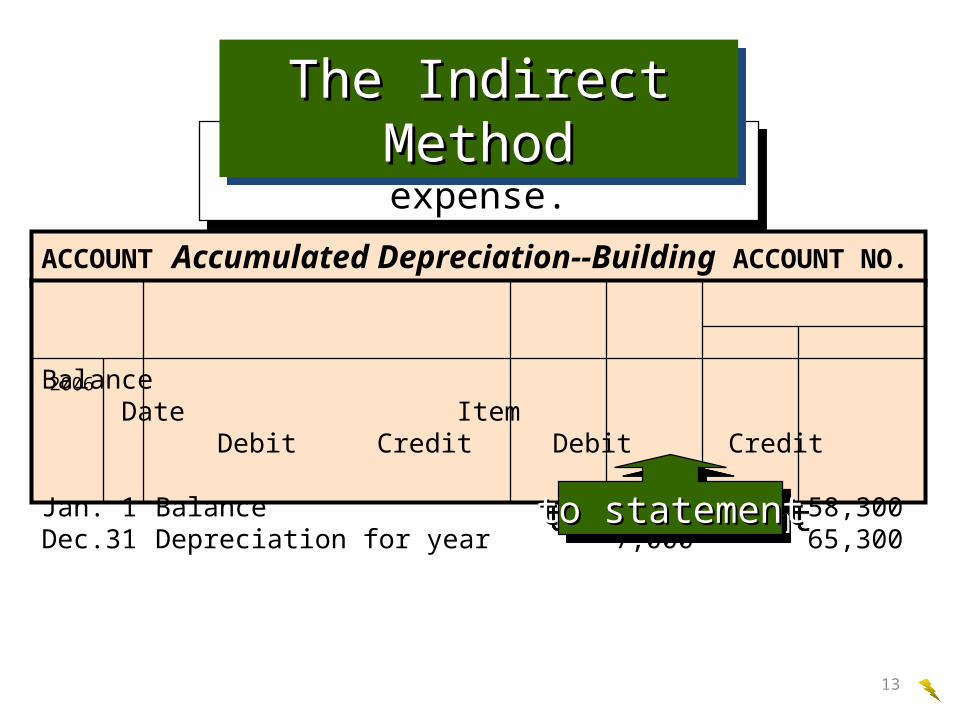

Next, we need to determine depreciation expense for the year. If it isn’t given on the income

statement, sometimes it can be found by analyzing the Accumulated Depreciation account.

Next, we need to determine depreciation expense for the year. If it isn’t given on the income

statement, sometimes it can be found by analyzing the Accumulated Depreciation account.

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

12

Determine depreciation expense.Determine depreciation expense.

ACCOUNT Accumulated Depreciation--Building ACCOUNT NO. 17

Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 58,300Dec. 31 Depreciation for year 7,000 65,300

to statementto statementto statementto statement

2006

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

13

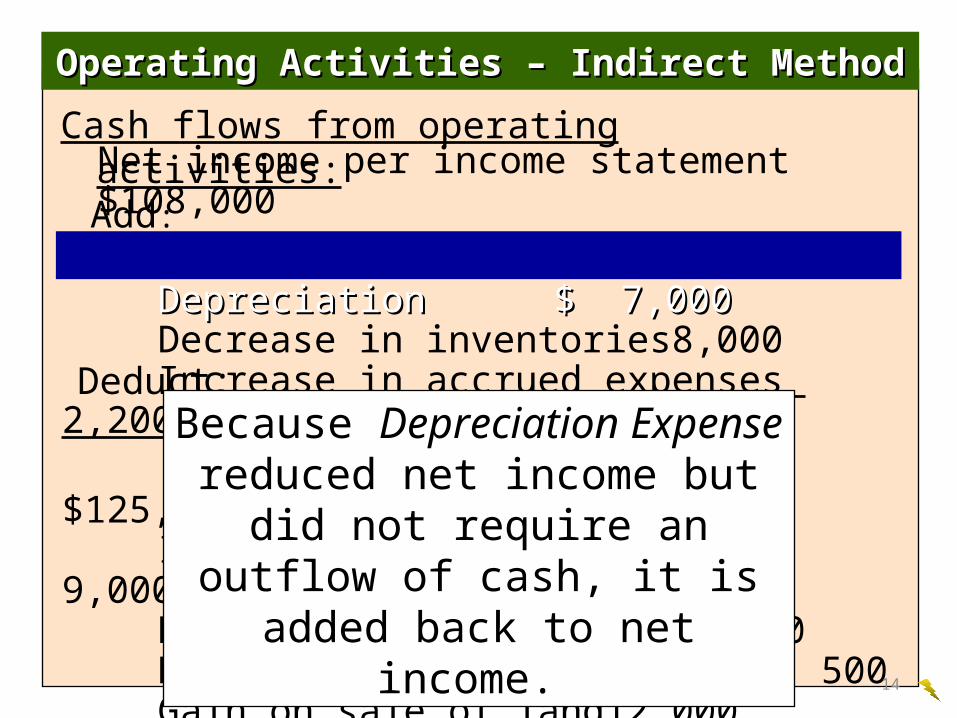

Cash flows from operating activities:

Operating Activities – Indirect MethodOperating Activities – Indirect Method

Deduct:

Add:

Net income per income statement $108,000

DepreciationDepreciation $ 7,000$ 7,000Decrease in inventories 8,000Increase in accrued expenses 2,200 17,200

$125,200Inc. in accounts receivable $ 9,000Dec. in accounts payable 3,200Dec. in income taxes payable 500Gain on sale of land 12,000 24,700

Net cash flow from operating activities $100,500

Because Depreciation Expense reduced net income but did not require an outflow of cash, it is

added back to net income.

14

Select current assets and current liabilities that impact cash flow and

determine the increases and decreases.

Select current assets and current liabilities that impact cash flow and

determine the increases and decreases.

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

15

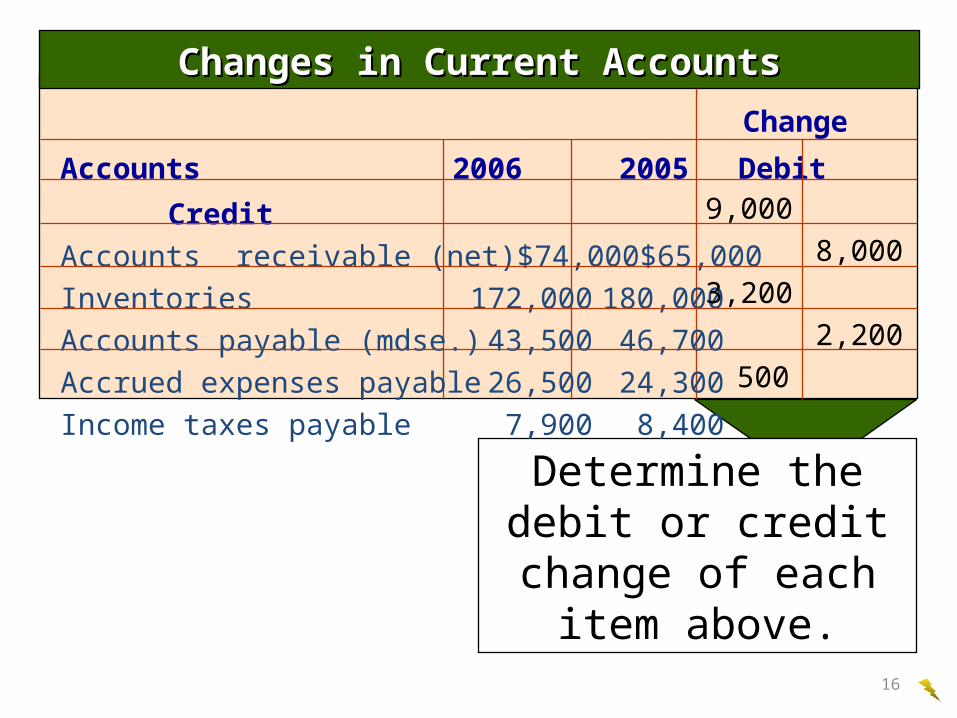

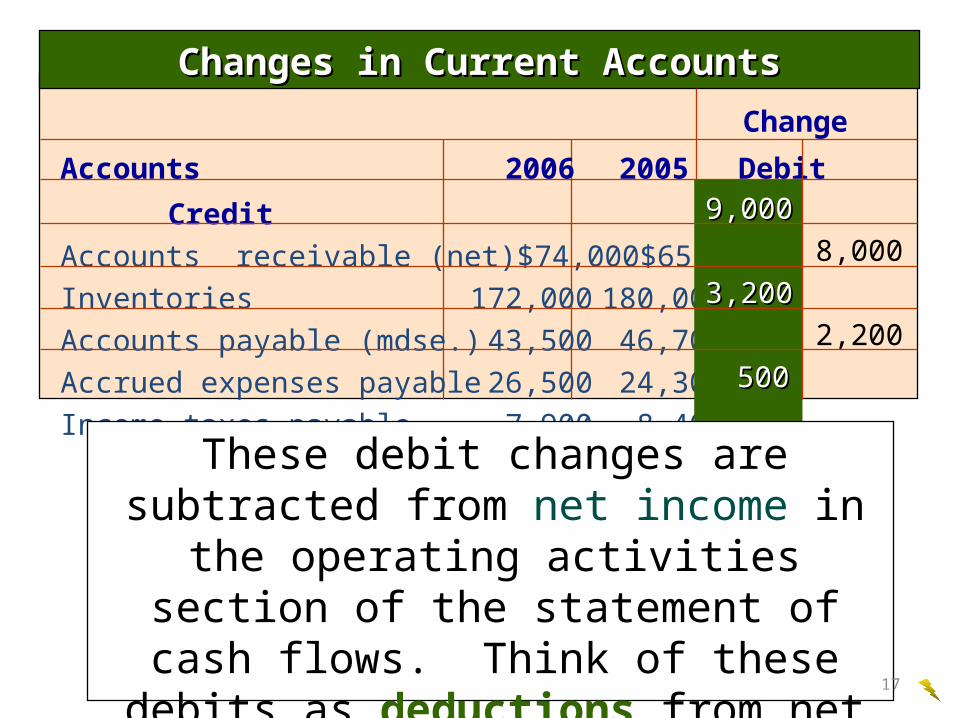

Determine the debit or credit change of each

item above.

Changes in Current AccountsChanges in Current Accounts

Change

Accounts 2006 2005 Debit Credit

Accounts receivable (net) $74,000 $65,000

Inventories 172,000 180,000

Accounts payable (mdse.) 43,500 46,700

Accrued expenses payable 26,500 24,300

Income taxes payable 7,900 8,400

9,000

8,000

3,200

2,200

500

16

Changes in Current AccountsChanges in Current Accounts

Change

Accounts 2006 2005 Debit Credit

Accounts receivable (net) $74,000 $65,000

Inventories 172,000 180,000

Accounts payable (mdse.) 43,500 46,700

Accrued expenses payable 26,500 24,300

Income taxes payable 7,900 8,400

These debit changes are subtracted from net income in the operating activities section of the statement of cash flows. Think of these

debits as deductions from net income in arriving at net cash flow from operations.

9,0009,000

8,000

3,2003,200

2,200

500500

17

Changes in Current AccountsChanges in Current Accounts

Change

Accounts 2006 2005 Debit Credit

Accounts receivable (net) $74,000 $65,000

Inventories 172,000 180,000

Accounts payable (mdse.) 43,500 46,700

Accrued expenses payable 26,500 24,300

Income taxes payable 7,900 8,400

9,000

8,0008,000

3,200

2,2002,200

500

These credit changes are added to net income in the operating activities section of the statement of cash

flows. Think of these credits as additions to net income in arriving at net cash flow from operations.

18

Cash flows from operating activities:

Operating ActivitiesOperating Activities——Indirect MethodIndirect Method

Add:

Net income per income statement $108,000

Depreciation $ 7,000Decrease in inventoriesDecrease in inventories 8,0008,000Increase in accrued expensesIncrease in accrued expenses 2,200 2,200 17,200

$125,200Inc. in accounts receivableInc. in accounts receivable $ 9,000$ 9,000Dec. in accounts payableDec. in accounts payable 3,2003,200Dec. in income taxes payableDec. in income taxes payable 500500Gain on sale of land 12,000 24,700

Net cash flow from operating activities $100,500

19

Analyze the income statement to determine if there are any gains or losses from selling

investments, equipment, etc.

Analyze the income statement to determine if there are any gains or losses from selling

investments, equipment, etc.

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

20

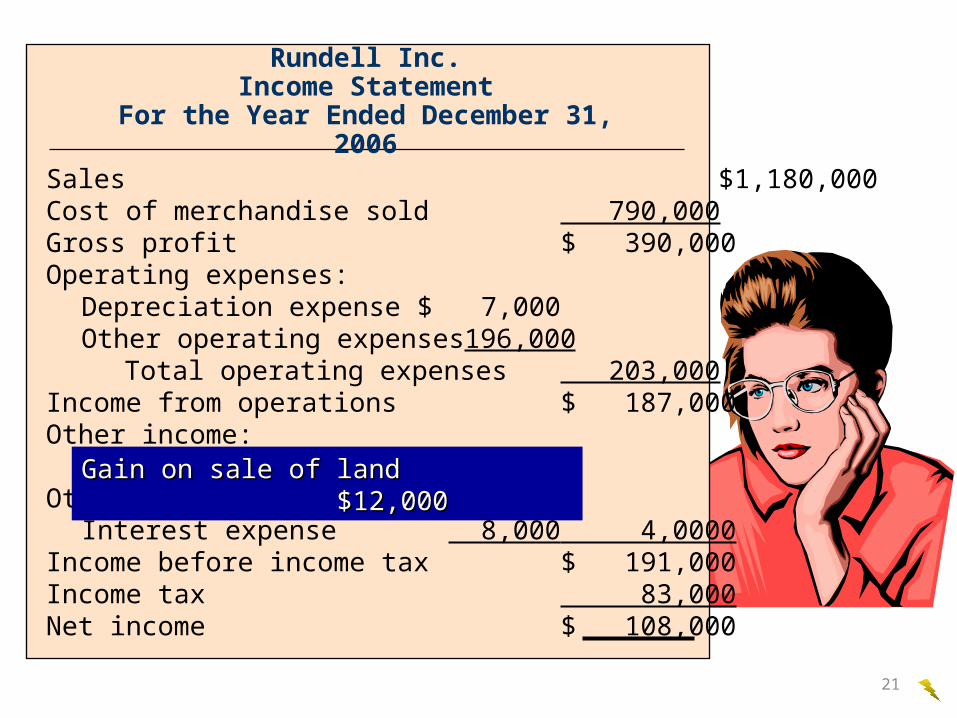

Rundell Inc.Income Statement

For the Year Ended December 31, 2006

Sales $1,180,000Cost of merchandise sold 790,000 Gross profit $ 390,000Operating expenses:

Depreciation expense $ 7,000 Other operating expenses 196,000

Total operating expenses 203,000Income from operations $ 187,000Other income:

Gain on sale of land $12,000 Other expense:

Interest expense 8,000 4,0000 Income before income tax $ 191,000Income tax 83,000 Net income $ 108,000

Gain on sale of land $12,000Gain on sale of land $12,000

21

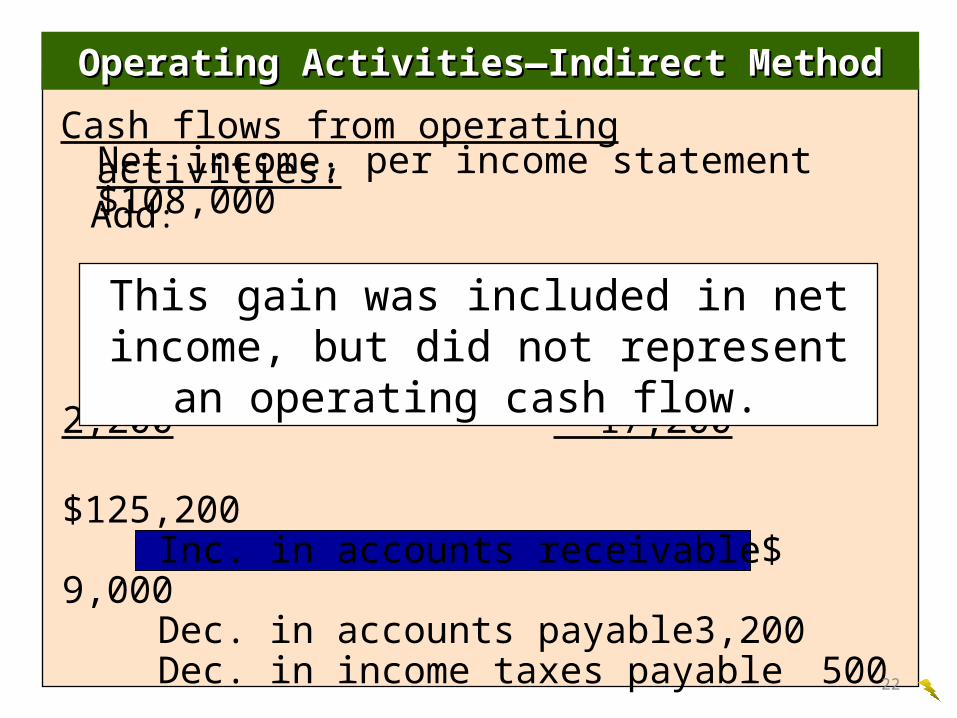

Cash flows from operating activities:

Operating ActivitiesOperating Activities——Indirect MethodIndirect Method

Add:

Net income, per income statement $108,000

Depreciation $ 7,000Decrease in inventories 8,000Increase in accrued expenses 2,200 17,200

$125,200Inc. in accounts receivable $ 9,000Dec. in accounts payable 3,200Dec. in income taxes payable 500Gain on sale of land 12,000 24,700

Net cash flow from operating activities $100,500

This gain was included in net income, but did not represent an operating cash flow.

22

If there had been a loss on this sale, the loss would have been

added to net income.

If there had been a loss on this sale, the loss would have been

added to net income.

The Indirect MethodThe Indirect MethodThe Indirect MethodThe Indirect Method

23

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

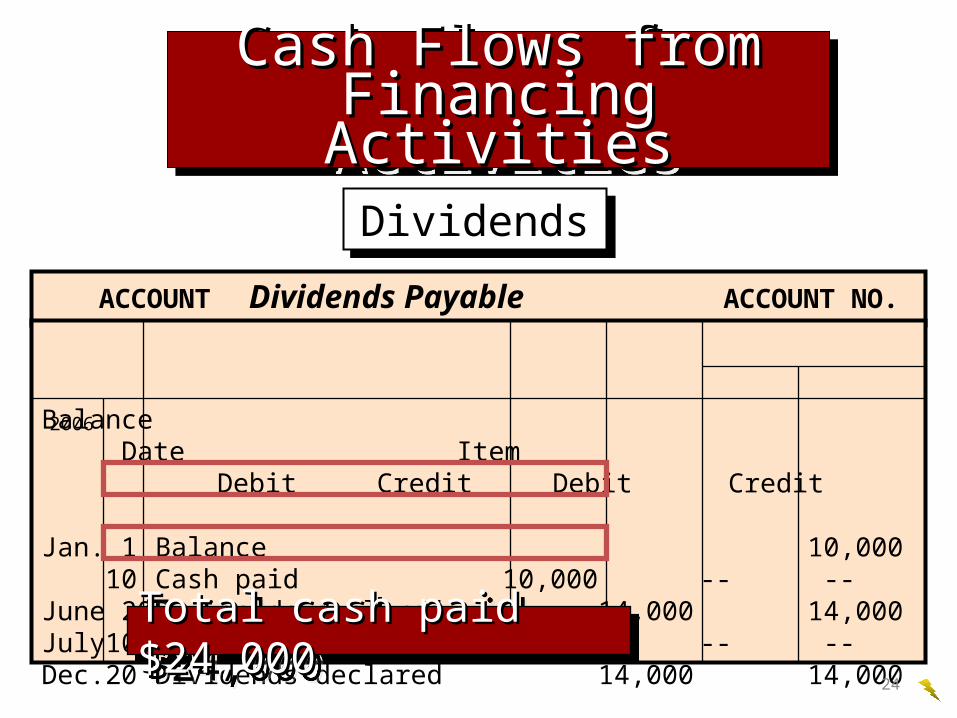

ACCOUNT Dividends Payable ACCOUNT NO. 23

Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 10,00010 Cash paid 10,000 -- --

June 20 Dividends declared 14,000 14,000July 10 Cash paid 14,000 -- -- Dec. 20 Dividends declared 14,000 14,000

Total cash paidTotal cash paid $24,000$24,000Total cash paidTotal cash paid $24,000$24,000

DividendsDividends

2006

24

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

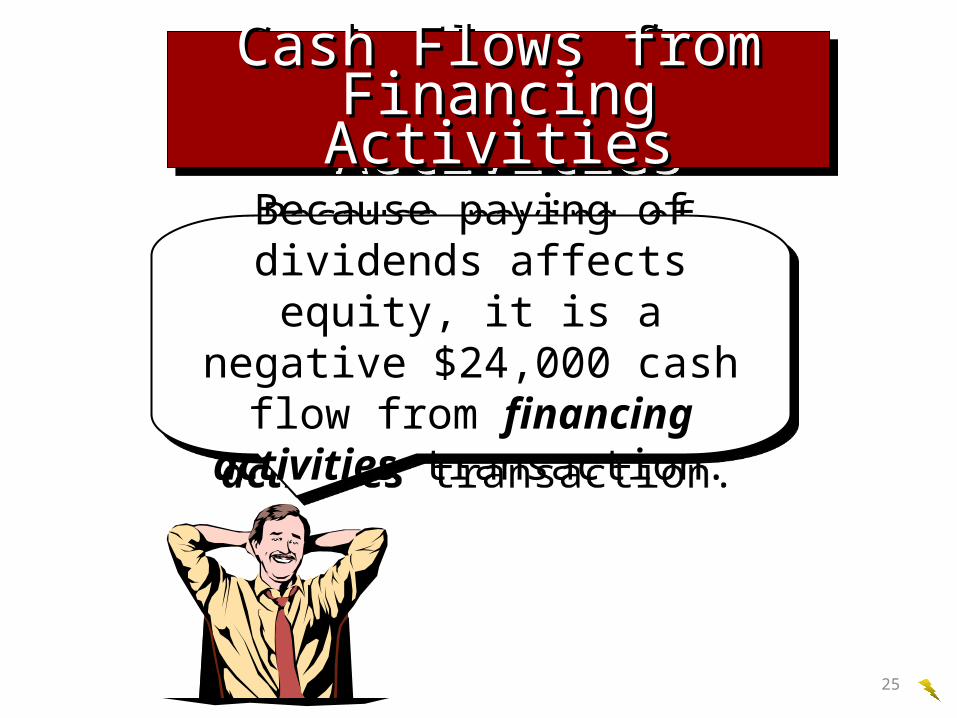

Because paying of dividends affects equity, it is a negative

$24,000 cash flow from financing activities transaction.

Because paying of dividends affects equity, it is a negative

$24,000 cash flow from financing activities transaction.

25

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

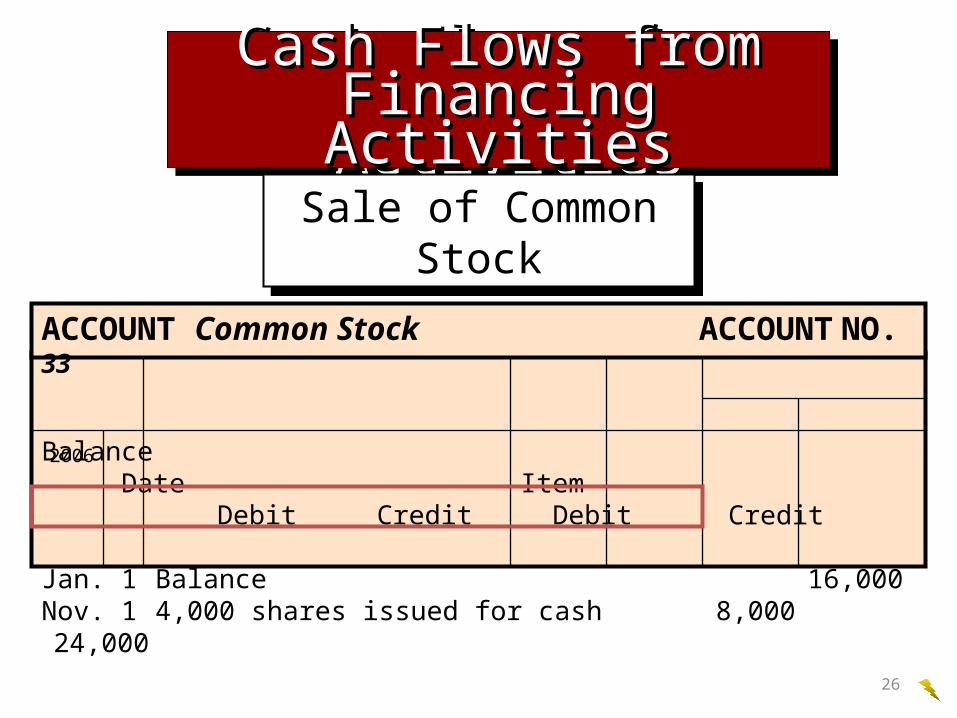

Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 16,000Nov. 1 4,000 shares issued for cash 8,000 24,000

Sale of Common StockSale of Common Stock

2006

ACCOUNT Common Stock ACCOUNT NO. 33

26

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

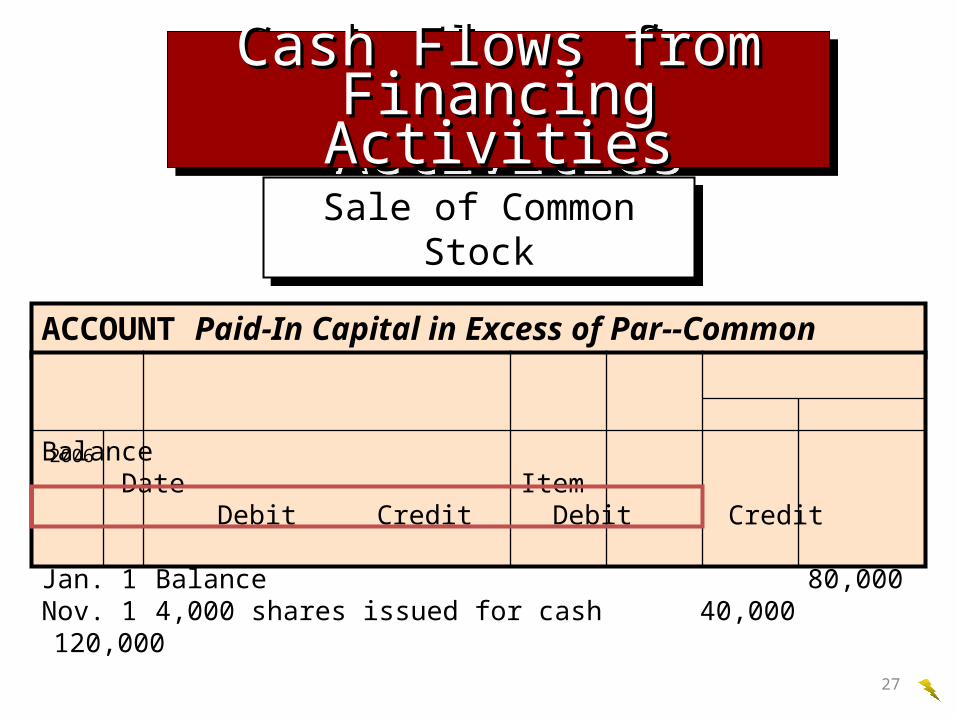

ACCOUNT Paid-In Capital in Excess of Par--Common ACCT. NO. 34 Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 80,000Nov. 1 4,000 shares issued for cash 40,000 120,000

Sale of Common StockSale of Common Stock

2006

27

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

Issuing common stock affects equity; therefore, we have a total positive cash

flow of $48,000 from this financing activities transaction.

Issuing common stock affects equity; therefore, we have a total positive cash

flow of $48,000 from this financing activities transaction.

28

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

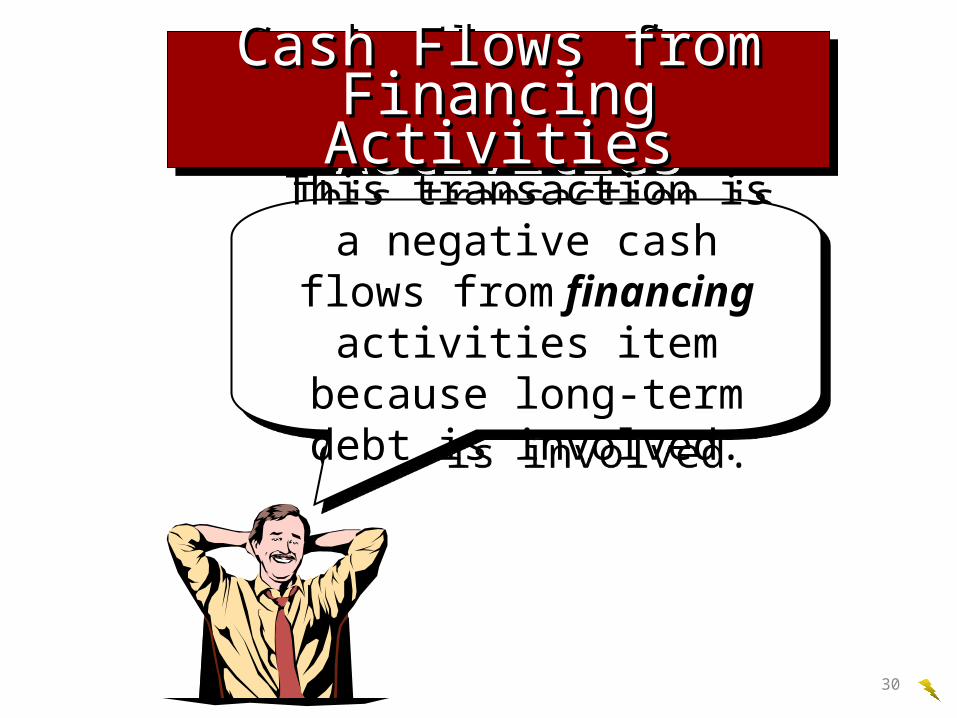

ACCOUNT Bonds Payable ACCOUNT. NO. 25 Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 150,000June 30 Retired by payment of cash

at face amount 50,000 100,000

Retirement of Bonds PayableRetirement of Bonds Payable

2006

29

Cash Flows from Cash Flows from Financing ActivitiesFinancing ActivitiesCash Flows from Cash Flows from

Financing ActivitiesFinancing Activities

This transaction is a negative cash flows from financing

activities item because long-term debt is involved.

This transaction is a negative cash flows from financing

activities item because long-term debt is involved.

30

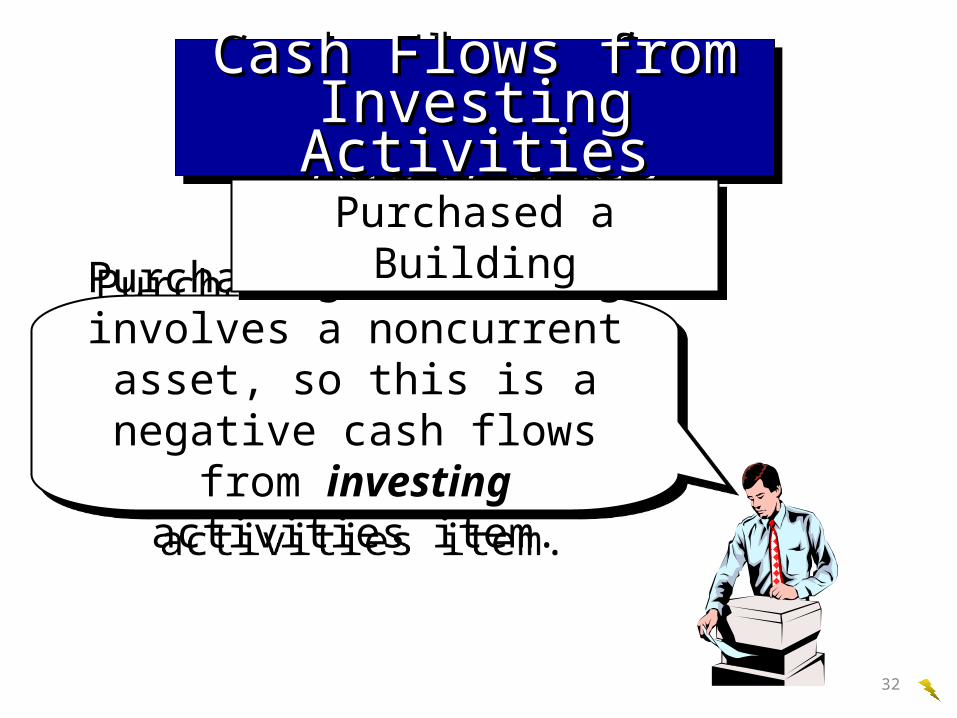

ACCOUNT Building ACCOUNT NO. 18 Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 200,000Dec. 27 Purchased for cash 60,000 260,000

2006

Cash Flows from Cash Flows from Investing ActivitiesInvesting ActivitiesCash Flows from Cash Flows from

Investing ActivitiesInvesting Activities

Purchased a BuildingPurchased a Building

31

Cash Flows from Cash Flows from Investing ActivitiesInvesting ActivitiesCash Flows from Cash Flows from

Investing ActivitiesInvesting Activities

Purchasing a building involves a noncurrent asset, so this is a

negative cash flows from investing activities item.

Purchasing a building involves a noncurrent asset, so this is a

negative cash flows from investing activities item.

Purchased a BuildingPurchased a Building

32

Cash Flows from Cash Flows from Investing ActivitiesInvesting ActivitiesCash Flows from Cash Flows from

Investing ActivitiesInvesting Activities

ACCOUNT Land ACCOUNT NO. 16 Balance Date Item Debit Credit Debit Credit

Jan. 1 Balance 125,000June 8 Sold for $72,000 cash 60,000 65,000Oct. 12 Purchased for $15,000 cash 15,000 80,000

Land TransactionsLand Transactions

2006

33

Cash Flows from Cash Flows from Investing ActivitiesInvesting ActivitiesCash Flows from Cash Flows from

Investing ActivitiesInvesting Activities

The first transaction, the sale of land, results in a positive cash flow from investing activities because

land is a noncash asset.

The first transaction, the sale of land, results in a positive cash flow from investing activities because

land is a noncash asset.

Land TransactionsLand Transactions

34

Cash Flows from Cash Flows from Investing ActivitiesInvesting ActivitiesCash Flows from Cash Flows from

Investing ActivitiesInvesting Activities

The $12,000 gain was recorded earlier on previous slide as an operating activity. The

purchase of land also is an investing activity.

The $12,000 gain was recorded earlier on previous slide as an operating activity. The

purchase of land also is an investing activity.

Land TransactionsLand Transactions

35

Rundell Inc.Statement of Cash Flows

For the Year Ended December 31, 2006

Cash flows from operating activities:Net income $108,000Add: Depreciation $ 7,000 Decrease in inventor. 8,000 Increase in accrued exp. 2,200 17,200

$125,000Deduct: Increase in A/R $9,000 Decrease in accts. Pay. 3,200

Decrease in ITP 500 Gain on sale of land 12,000 24,700Net cash flow from operating act. $100,500

Cash flows from investing activities:Cash from sale of land $72,000Less: Cash paid to pur. land $15,000

Cash paid for bldg. 60,000 75,000(3,000)Cash flows from financing activities:

Cash received from sale of c.s. $48,000Less: Cash paid to retire b. $50,000 Cash paid for divid. 24,000 74,000Net cash flow for financing (26,000)

Increase in cash $71,500Cash at beginning of year 26,000Cash at end of year $97,500

Refer to Exhibit 6 in your textbook to see the formal

statement of cash flows using the indirect approach.

Refer to Exhibit 6 in your textbook to see the formal

statement of cash flows using the indirect approach.

36

Let’s prepare another

Statement of Cash Flows

using the Indirect Method.

37

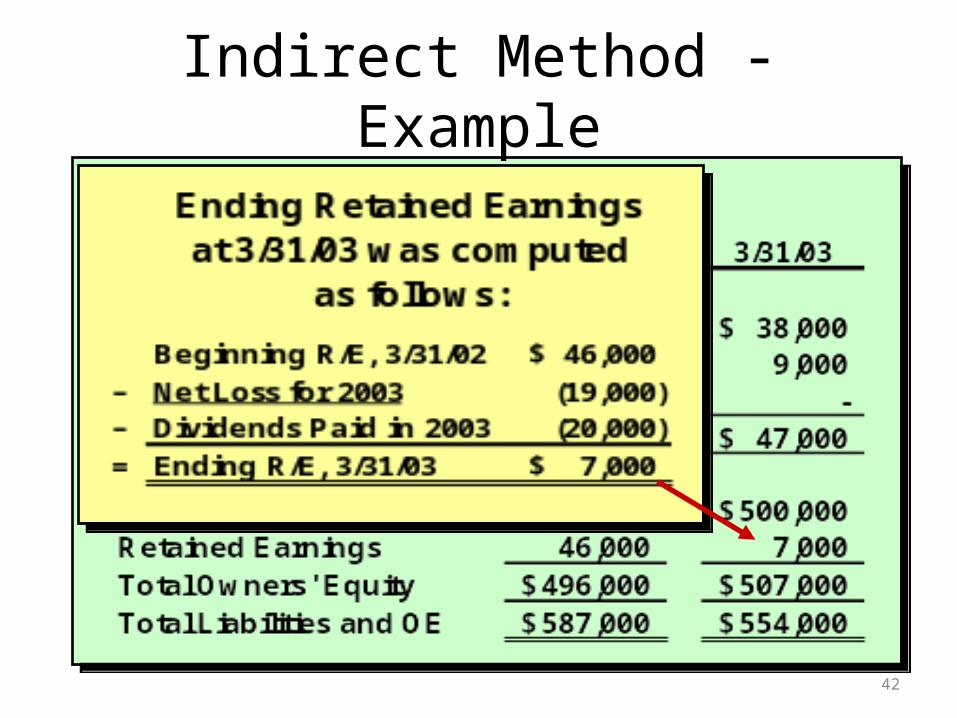

Indirect Method - Example

Joe’s Place has prepared the Balance Sheet as of March 31, 2003, and March 31, 2002. The Income Statement for the year ended

3/31/03 has also been prepared. Joe needs help preparing the Statement of

Cash Flows.

Joe’s Place has prepared the Balance Sheet as of March 31, 2003, and March 31, 2002. The Income Statement for the year ended

3/31/03 has also been prepared. Joe needs help preparing the Statement of

Cash Flows.

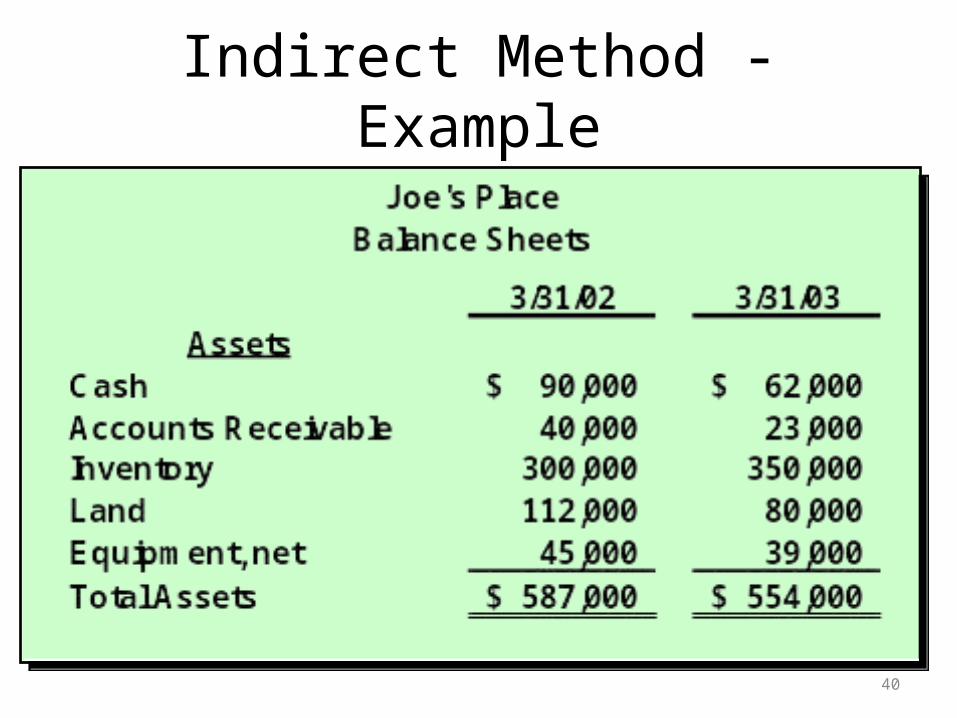

Joe’s Place

38

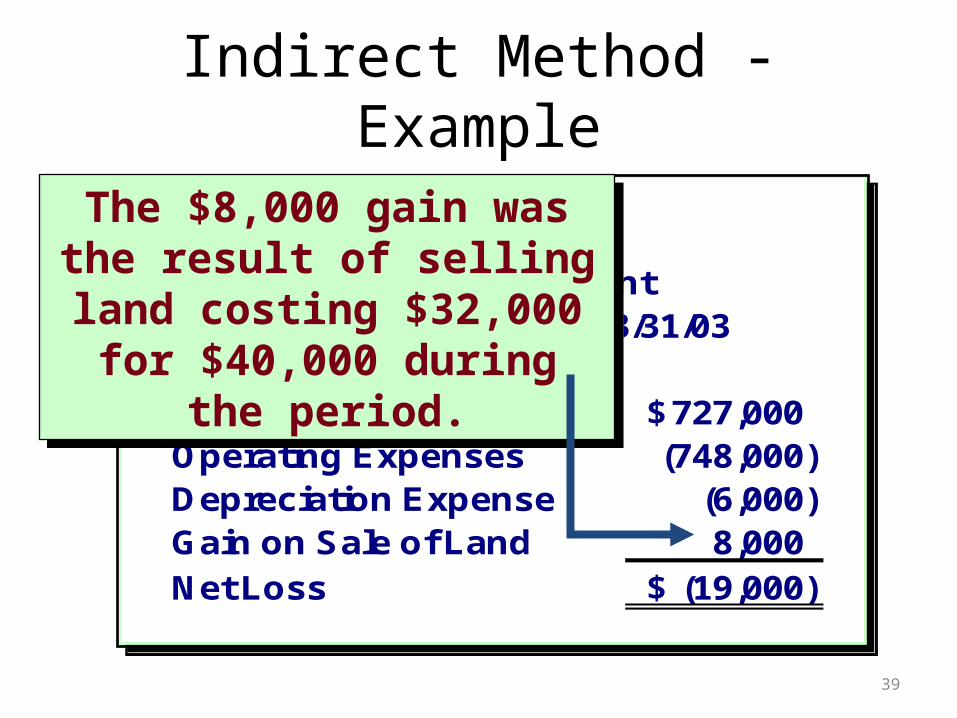

Joe's PlaceIncome Statement

For the Year Ending 3/31/03

Revenues 727,000$ Operating Expenses (748,000) Depreciation Expense (6,000) Gain on Sale of Land 8,000 Net Loss (19,000)$

Joe's PlaceIncome Statement

For the Year Ending 3/31/03

Revenues 727,000$ Operating Expenses (748,000) Depreciation Expense (6,000) Gain on Sale of Land 8,000 Net Loss (19,000)$

The $8,000 gain was the result of selling land

costing $32,000 for $40,000 during the period.

The $8,000 gain was the result of selling land

costing $32,000 for $40,000 during the period.

Indirect Method - Example

39

Indirect Method - Example

40

Joe’s Place issued $50,000 of no par common stock to

settle the $50,000 note payable.

Joe’s Place issued $50,000 of no par common stock to

settle the $50,000 note payable.

Indirect Method - Example

41

Indirect Method - Example

42

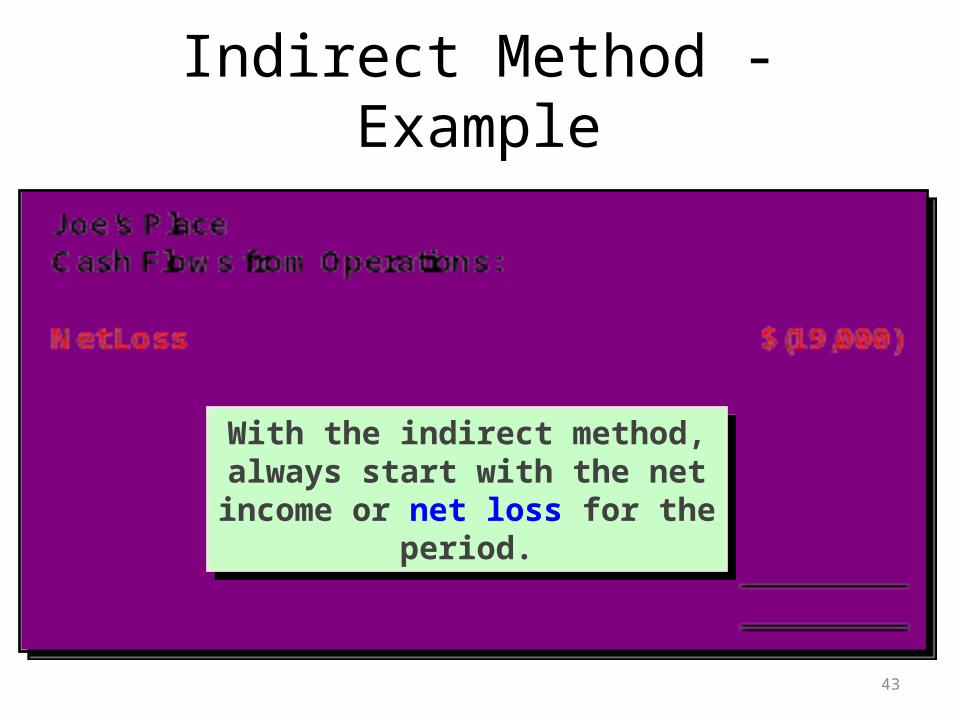

With the indirect method, always start with the net income or net

loss for the period.

With the indirect method, always start with the net income or net

loss for the period.

Indirect Method - Example

43

Indirect Method - Example

44

Accounts receivable decreased.

3/31/03 3/31/02

$23,000 - $40,000 = $(17,000)

Accounts receivable decreased.

3/31/03 3/31/02

$23,000 - $40,000 = $(17,000)

Indirect Method - Example

45

Accounts payable increased.

3/31/03 3/31/02

$38,000 - $27,000 = $11,000

Accounts payable increased.

3/31/03 3/31/02

$38,000 - $27,000 = $11,000

Indirect Method - Example

46

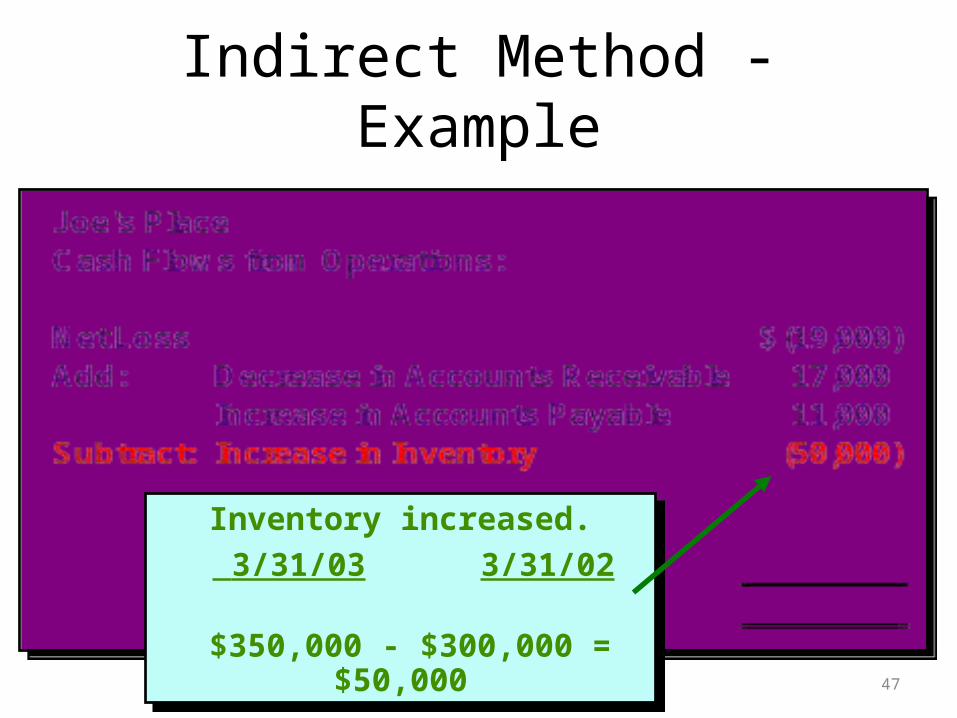

Inventory increased.

3/31/03 3/31/02

$350,000 - $300,000 = $50,000

Inventory increased.

3/31/03 3/31/02

$350,000 - $300,000 = $50,000

Indirect Method - Example

47

Salaries payable decreased.

3/31/03 3/31/02

$ 9,000 - $14,000 = $(5,000)

Salaries payable decreased.

3/31/03 3/31/02

$ 9,000 - $14,000 = $(5,000)

Indirect Method - Example

48

Add back non-cash expenses. Add back non-cash expenses.

Indirect Method - Example

49

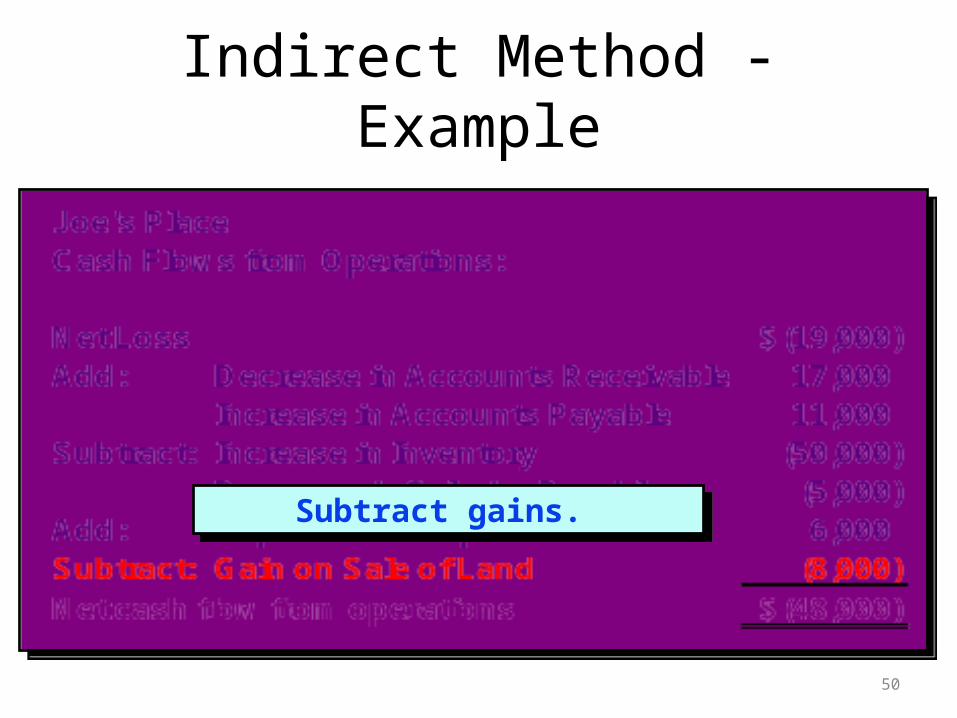

Subtract gains. Subtract gains.

Indirect Method - Example

50

The operating cash flows amount comes

from the schedule just prepared.

The operating cash flows amount comes

from the schedule just prepared.

Indirect Method - Example

51

Land originally costing $32,000 was sold for $40,000.

Land originally costing $32,000 was sold for $40,000.

Indirect Method - Example

52

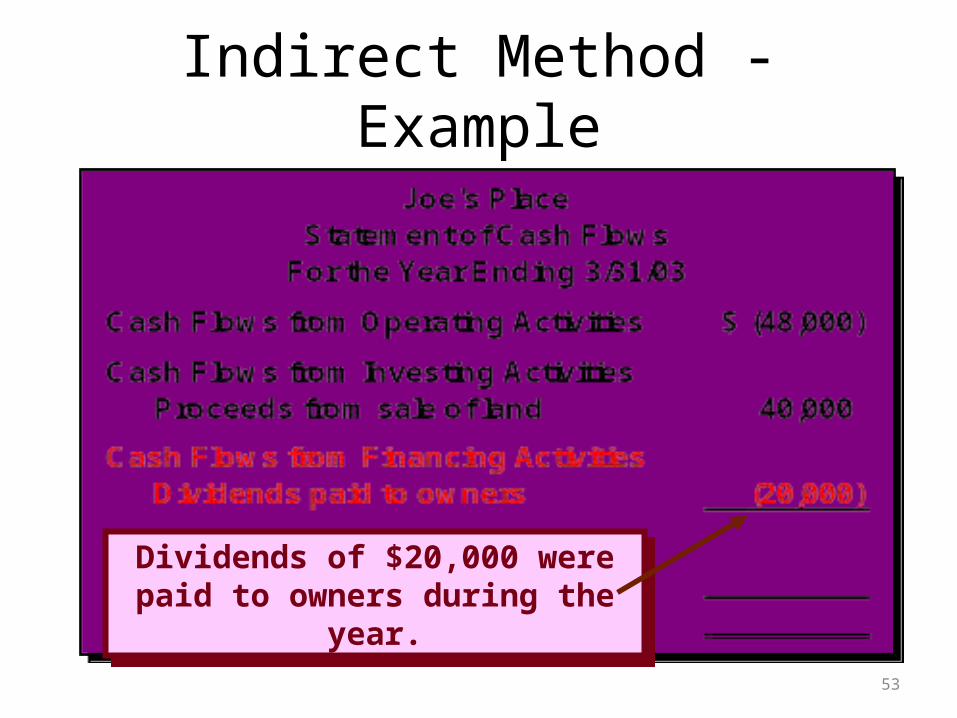

Dividends of $20,000 were paid to owners during the year.

Dividends of $20,000 were paid to owners during the year.

Indirect Method - Example

53

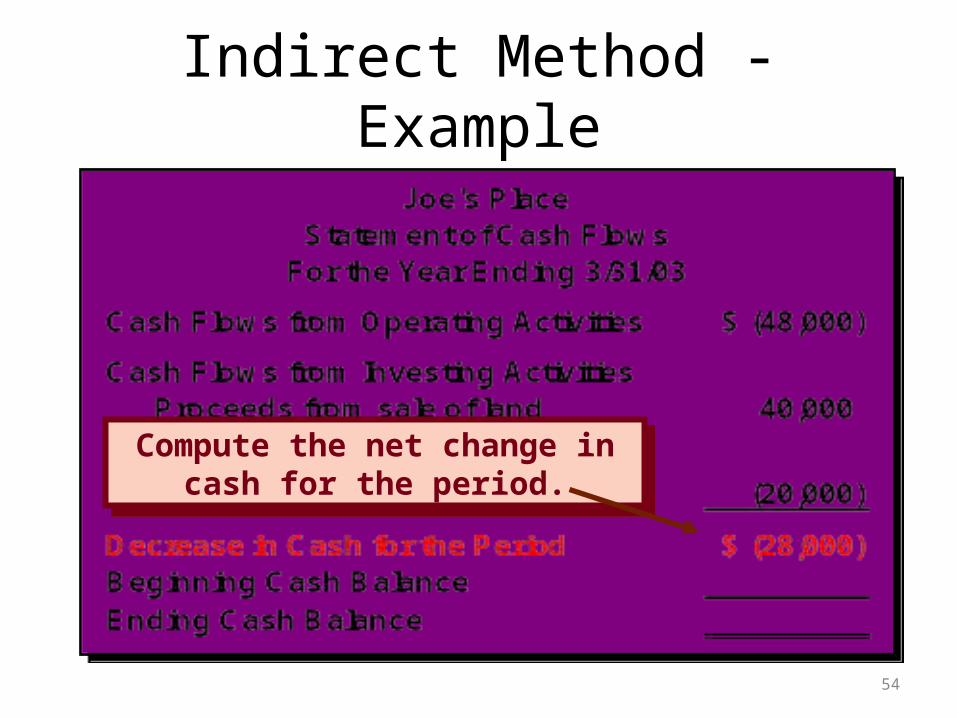

Compute the net change in cash for the period.

Compute the net change in cash for the period.

Indirect Method - Example

54

Complete the Statement of Cash Flows by reconciling beginning

cash to ending cash.

Complete the Statement of Cash Flows by reconciling beginning

cash to ending cash.

Indirect Method - Example

55

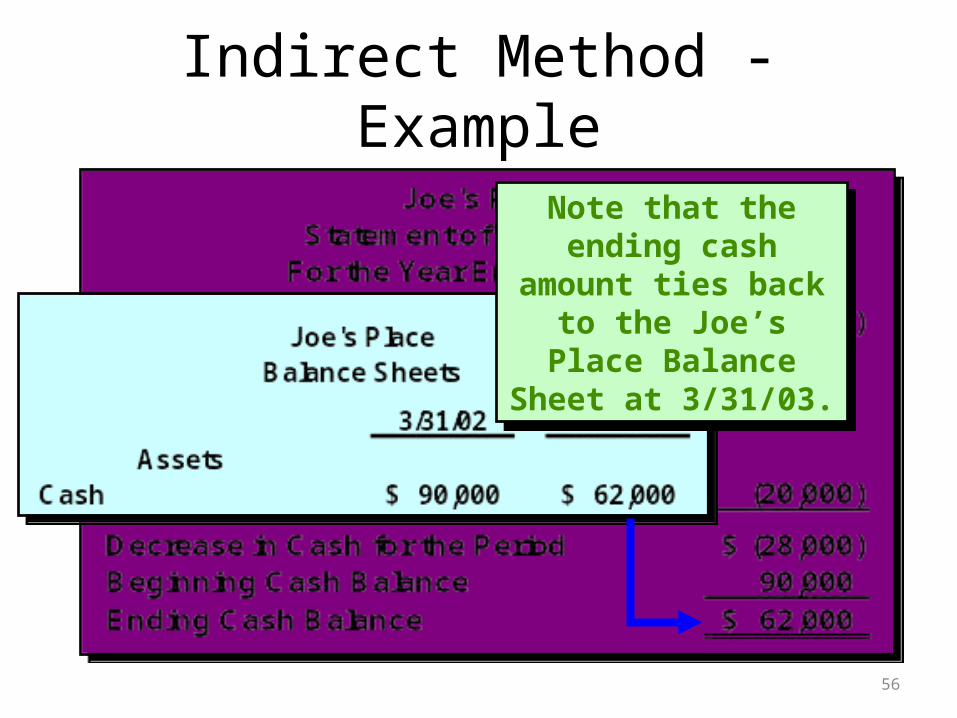

Note that the ending cash amount ties back to the Joe’s

Place Balance Sheet at 3/31/03.

Note that the ending cash amount ties back to the Joe’s

Place Balance Sheet at 3/31/03.

Indirect Method - Example

56

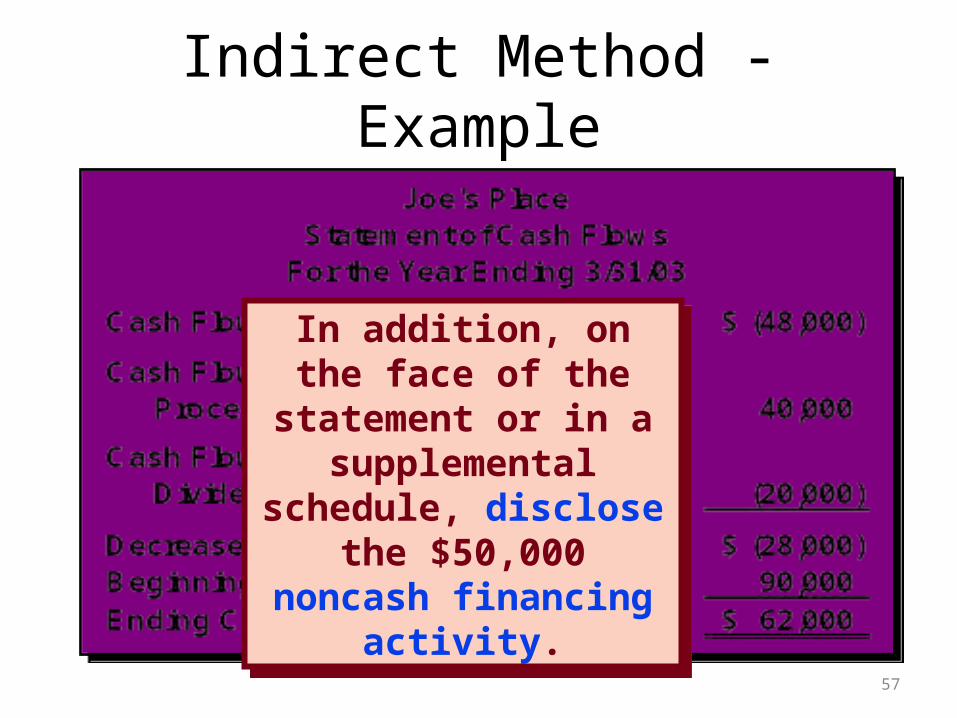

In addition, on the face of the statement or in a

supplemental schedule, disclose the

$50,000 noncash financing activity.

In addition, on the face of the statement or in a

supplemental schedule, disclose the

$50,000 noncash financing activity.

Indirect Method - Example

57

In addition, cash interest payments and

cash tax payments must also be disclosed

separately.

In addition, cash interest payments and

cash tax payments must also be disclosed

separately.

Indirect Method - Example

58

Cash Budgets are used by management to plan and forecast future cash flows.

Cash Budgets are used by management to plan and forecast future cash flows.

Force m anagem ent to coordinate activities.

Provide m anagers w ith advance notice of available resources.

Provide targets useful in evaluating perform ance.

Provide advance w arnings of potential cash shortages.

A C ash Budget can be used to:

Managing Cash Flows

59

Managing Cash Flows

• Increase collection of accounts receivables.

• Keep inventory low.• Delay payment of liabilities.• Plan timing of major expenditures.• Invest idle cash.

• Increase collection of accounts receivables.

• Keep inventory low.• Delay payment of liabilities.• Plan timing of major expenditures.• Invest idle cash.

60

Cash Budgeting

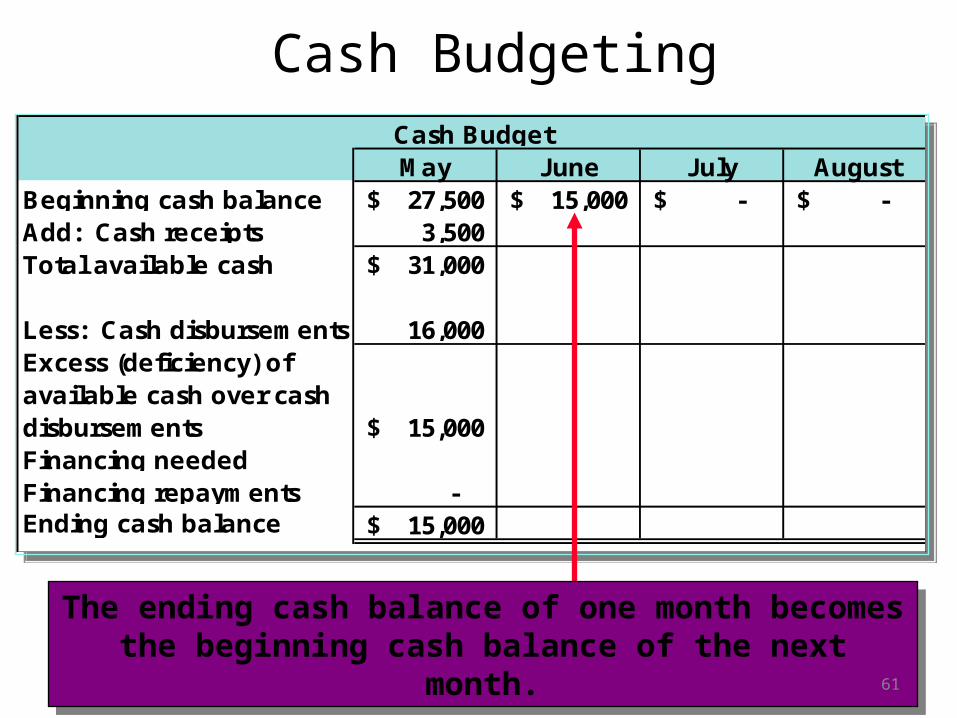

Cash BudgetMay June July August

Beginning cash balance 27,500$ 15,000$ -$ -$ Add: Cash receipts 3,500 Total available cash 31,000$

Less: Cash disbursements 16,000 Excess (deficiency) of available cash over cash disbursements 15,000$ Financing neededFinancing repayments - Ending cash balance 15,000$

Cash BudgetMay June July August

Beginning cash balance 27,500$ 15,000$ -$ -$ Add: Cash receipts 3,500 Total available cash 31,000$

Less: Cash disbursements 16,000 Excess (deficiency) of available cash over cash disbursements 15,000$ Financing neededFinancing repayments - Ending cash balance 15,000$

The ending cash balance of one month becomes the beginning cash balance of the next month.

The ending cash balance of one month becomes the beginning cash balance of the next month.

61

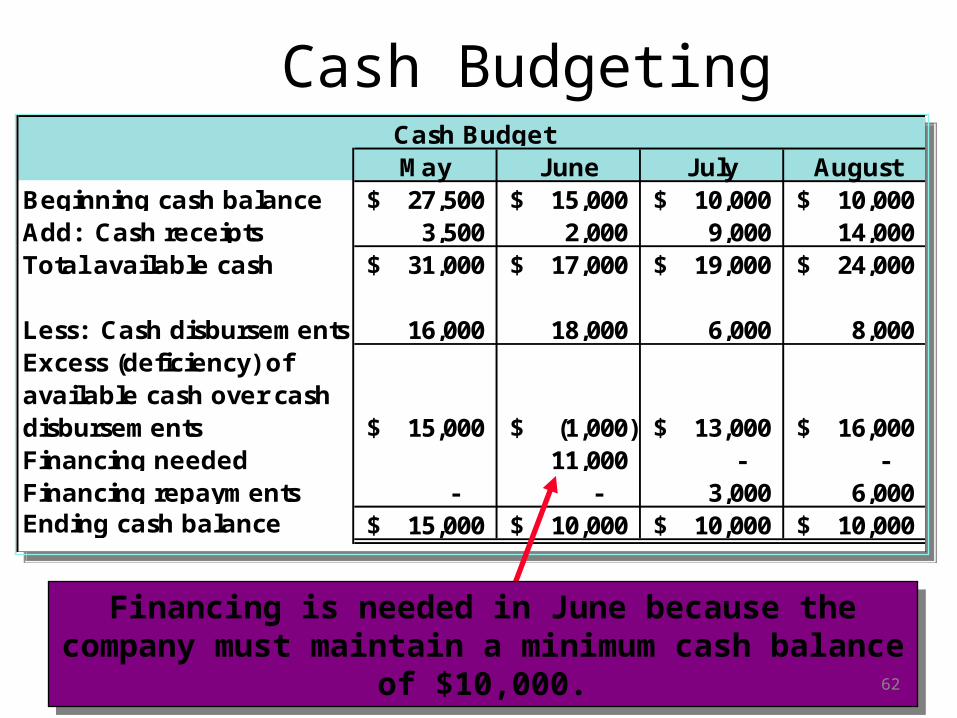

Cash BudgetingCash BudgetMay June July August

Beginning cash balance 27,500$ 15,000$ 10,000$ 10,000$ Add: Cash receipts 3,500 2,000 9,000 14,000 Total available cash 31,000$ 17,000$ 19,000$ 24,000$

Less: Cash disbursements 16,000 18,000 6,000 8,000 Excess (deficiency) of available cash over cash disbursements 15,000$ (1,000)$ 13,000$ 16,000$ Financing needed 11,000 - - Financing repayments - - 3,000 6,000 Ending cash balance 15,000$ 10,000$ 10,000$ 10,000$

Cash BudgetMay June July August

Beginning cash balance 27,500$ 15,000$ 10,000$ 10,000$ Add: Cash receipts 3,500 2,000 9,000 14,000 Total available cash 31,000$ 17,000$ 19,000$ 24,000$

Less: Cash disbursements 16,000 18,000 6,000 8,000 Excess (deficiency) of available cash over cash disbursements 15,000$ (1,000)$ 13,000$ 16,000$ Financing needed 11,000 - - Financing repayments - - 3,000 6,000 Ending cash balance 15,000$ 10,000$ 10,000$ 10,000$

Financing is needed in June because the company must maintain a minimum cash balance of $10,000.

Financing is needed in June because the company must maintain a minimum cash balance of $10,000.

62

End of Chapter 13

63