Embed Size (px)

Citation preview

State ownership in Slovenia and the strategy for management of SOEs

European Semester Conference, 5 June 2015, Ljubljana

Svetoslava GeorgievaDG Economic and Financial Affairs

European Commission

AGENDA

The role of SOEs in the SI economy – why is the strategy important?

Facts & Figures from the strategy

Implications and potential traps

Next steps

2

State involvement in SI is high compared to other member states and in sectors that are typically private owned

SOEs are present across sectors

Book value of equity in SOEs/SCEs (%of GDP) Share of SOEs/SCEs in sectoral value added(% of total sectoral value added), 2013

State ownership among the highest

Source: OECD, 2015 Country report for Slovenia, European Commission

Source: 2015 Country report for Slovenia, European Commission

3

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

ES

BE

DE

PT

DK EL

FR AT

HU NL

SE PL IT IE LT LV FI

CZ

EE SI

Minority holdings Majority holdings

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Co

nsu

me

r st

aple

s

Ch

emic

al a

nd p

har

ma

Met

al p

roce

ssin

g in

dust

ry

Oth

er

man

ufa

ctu

ring

& r

epai

r Ene

rgy

Pub

lic u

tiliti

es

Co

nstr

uctio

n

Tra

nsp

ort

& s

tora

ge

Tou

rism

Pos

tal s

ervi

ces

& I

CT

SI RO HR

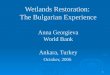

SOEs underperformed compared to peers in SI and in other member states

…and less profitable compared to peers. SOEs are more indebted…

Debt leverage ratio of SOEs/SCEs and privately owned companies in SI (2013)

Source: 2015 Country report for Slovenia, European Commission

Profitability (ROCE) of SOEs/SCEs and foreign owned companies relative to domestic privately owned

companies (2004-2013)

Source: 2015 Country report for Slovenia, European Commission

4

-10x

-5x

0x

5x

10x

15x

20x

Ch

emic

als

and

pha

rma

Co

nstr

uctio

n

Du

rab

les

ICT

Mat

eria

ls

Oth

er

man

ufa

ctu

ring

Ser

vice

s

Co

nsu

me

r st

aple

s

Tou

rism

Tra

de

SOE/ SCE aggregate Foreign aggregate

SOE/ SCE median Foreign median

-20

-15

-10

-5

0

5

10

Ove

rall

Ch

emic

als

and

pha

rma

Mat

eria

ls

No

n-d

urab

les

Du

rab

les

Oth

er

man

ufa

ctu

ring

Co

nstr

uctio

n

ICT

Tou

rism

Tra

de

Oth

er

serv

ice

s

SOEs/ SCEs Foreign

Risks linked to the complex network of state ownership could be reduced by divesting non-core assets

Gorenjska Banka (26%)Prvi Faktor (100%)

(finance)Factor Banka (10%) Abanka (52%)

Probanka (4%) SID Banka (100%)

KAD (100%)(state fund)

SOD (100%)(state fund)

Triglav (67%)(insurance)

PivovarnaUnion(39%)(SOE, retail)

NKBM (51%)(bank)

NLB (57%)(bank)

Mercator (31%)(SOE, retail)

Republic of Slovenia

Lasko (40%)(SOE, brewery)

Source: 2013 Country Focus, Slovenia: State-owned and State-controlled Enterprises in Slovenia, European Commission

5

Indirect state ownership and cross-links between SOEs are not considered in the strategy

15% of state-owned and state-controlled companies reviewed (75% in terms of book value)

5%

1%

(Indirect)32%

3rd Leg of Ownership

(Indirect)

4rd Leg of Ownership(Indirect)

2nd Leg of Ownership

Direct ownership

62%1st Leg of Ownership

(Quasi Direct)

Republic of Slovenia

SOEs/SCEs

Stated-owned banks, other financial and

insurance companies

State management funds (SSH, DSU, KAD, PDP, Modra)

Municipalities

Mutual and Pension Funds

BAMC

SOEs/SCEs

SOEs/SCEs

SOEs/SCEs

SOEs/SCEs

Other entities (ZPIZ, humanitarian foundations)

REVIEWED15% of

companies

NOT REVIEWED

85% of companies

Source: European Commission, SI Chamber of Commerce 6

The majority of the assets reviewed are classified as strategic or important, some sectors remain out of scope

Book value of equity (in EUR 000) by sector Book value of equity (in EUR 000) by sector

Major sectors classified as strategic or important Some sectors were not fully reviewed

Source: European Commission Source: European Commission7

00

1,000

2,000

3,000

4,000

5,000

6,000 Not reviewed

Portfolio

Important

Strategic

00

100

200

300

400

500

600

700

800

900

1,000 Not reviewed

Portfolio

Important

Strategic

New commitments account for 1.5% of the total state assets reviewed

Classification of state assets

Book value of equity (% of total included in strategy)

Strategic assets68.3%

Important assets18.2%

Portfolio -list of 15 &

banks 12.1%

Portfolio -new 1.5%

8

New portfolio assets by sector

Book value of equity (in EUR 000)

0

20

40

60

80

100

120

140

160

180 Telecommunications

Media

Financial services(holdings)Transport

Banking

In bankruptcy

Services and others

Manufacturing

Energy

Tourism & leisure

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Baseline Scenario 1 Scenario 2

Portfolio assets

Important assets

Strategic assets

The classification of assets is largely influenced by the choice of criteria and thresholds

•Highest weight of criteria 11 and 14

•Classification sensitive to selection of criteria and thresholds

•The ranking of companies does not change in the different scenarios

Source: European Commission

Book value of equity (% of total)

Scenario analysis of classification methodology Preliminary conclusions

Scenario 1: Excluding criteria 11 & 14 Scenario 2: Excluding reference to strategic documents which are still work in progress

9

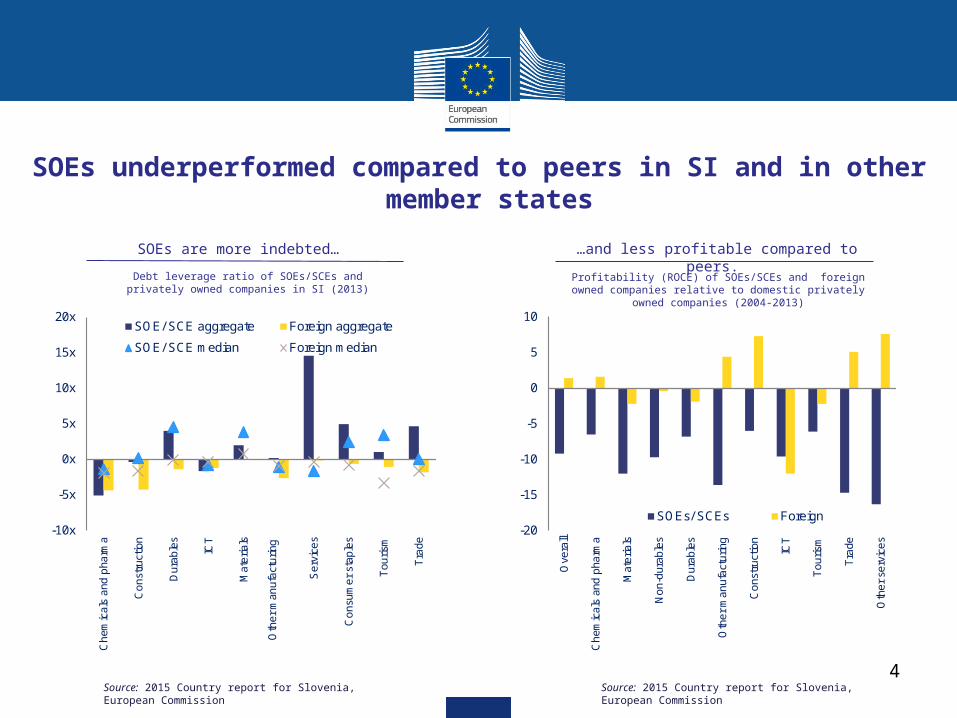

Certain aspects of the strategy may pose some challenges and important implications for the economy…

Potential traps Possible implications

• Only part of the state portfolio reviewed

• Blocking minority in companies

• No strategic investors in important assets

• Keeping value chains under state control

• Social conditions for asset sale

• Updates should be envisaged (OECD guidelines)

• Links between SOEs and the financial sector remain

• Reduced pool of potential investors

• Negative impact on price

• Delays in the process

• Harming competitiveness

• Not compatible with EU state aid rules

• Not taking into account future developments

10

…linked to risks of incurring further costs to the state and slowing down private investment recovery

Private investment dropped below all benchmarks

Source: European Commission

14

16

18

20

22

24

26

02 03 04 05 06 07 08 09 10 11 12 13 14

Priv

ate

inve

stm

ent,

% o

f G

DP

Slovenia EA V4

SI historical average(since 1995)

13bn of direct and indirect costs to SI

Cumulative 2007-2014

EUR bn

Total fiscal and economic implications 13.4

as % of GDP 36%

with direct fiscal impact (debt, deficit or both) 8.3

as % of GDP 22%

with wider economic impact (foregone profits) 5.1

as % of GDP 14%

Source: 2015 Country Report for Slovenia European Commission, SI Chamber of Commerce

11

Next steps

12

June 2015

Sept/ Oct 2015

Nov/ Dec 2015

• CSR on SOEs management adopted

• Monitoring mission

• Report on progress

Hvala!

![Thesis Antoniya Georgieva[1]](https://img.pdfslide.us/doc/110x75/6175bae2bb44291fce118c1d/thesis-antoniya-georgieva1.jpg)