Embed Size (px)

Citation preview

A R T I C L E S

STATE-OWNED ENTERPRISES AROUND THE WORLD ASHYBRID ORGANIZATIONS

GARRY D. BRUTONTexas Christian University and Sun Yat-sen University

MIKE W. PENGUniversity of Texas at Dallas

DAVID AHLSTROMThe Chinese University of Hong Kong

CIPRIAN STANFlorida Atlantic University

KEHAN XUSun Yat-sen University

State-owned enterprises represent approximately 10% of global gross domestic product.Yet they remain relatively underexplored by management scholars. Firms have often beenviewed dichotomously as either state owned or privately owned. Today, however, weencourage a more nuanced view of state-owned enterprises as hybrid organizations, inwhich the levels of ownership and control by the state can vary. Drawing on 36 cases fromfour industries in 23 countries, we lay the groundwork for a richer understanding ofstate-owned enterprises by management scholars in the future.

The breakup of the Soviet Union more than twodecades ago led many to anticipate the demise ofstate-owned enterprises (SOEs) globally (Kozmin-ski, 1993; Spicer, McDermott, & Kogut, 2000).These predictions, however, have turned out to belargely unfounded. Indeed, SOEs generate approx-imately one tenth of world gross domestic product(GDP) and represent approximately 20% of globalequity market value (Economist, 2010, 2012a). Inaddition, more than 10% of the world’s largestfirms are state owned, with joint sales of $3.6 tril-

lion in 2011 (Kowalski, Büge, Sztajerowska, & Ege-land, 2013). And between 2005 and 2012, SOEsrepresented nine of the 15 largest initial publicofferings (see Table 1). In certain parts of the world,SOEs play a particularly key role in the economy.For example, SOEs in regions as diverse as Africa,Asia, and Latin America currently provide roughly15% of total GDP, often in strategic industries (Budi-man, Lin, & Singham, 2009). State ownership hasbeen credited with helping developed countries suchas France, where the state plays an active role inbusiness, weather the 2008 economic turmoil (Espi-noza, 2008).

Why have SOEs continued to thrive in today’seconomy? We argue that SOEs may have survivedand thrived in part because they have evolved tobecome a type of hybrid organization (Diefenbach &Sillince, 2011; Economist, 2012a; Inoue, Lazzarini,& Musacchio, 2013). Indeed, today’s SOEs are quite

The work in this article was substantially supported bya grant from the RGC Research Grant Direct AllocationScheme (Project no. 2070465, 2011-2012) of The ChineseUniversity of Hong Kong, Hong Kong Special Adminis-trative Region. The authors would also like to thank MarcAhlstrom of Burlington County College for his editorialassistance.

� The Academy of Management Perspectives2015, Vol. 29, No. 1, 92–114.http://dx.doi.org/10.5465/amp.2013.0069

92

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download, or email articles for individual use only.

different from many of their inefficient predeces-sors that proliferated in the last century (Carney &Child, 2012; Economist, 2012a). For example, to-day’s SOEs have much more private ownershipcompared to those of the last century (Economist,2012a). Some hybrid SOEs, such as Brazil’s Petro-bras and Vale, experience high levels of govern-ment ownership but are largely independent intheir operations (Inoue et al., 2013). Conversely,government ownership of other firms, such as En-ergies de Portugal, is relatively low while govern-ment control is high.

The existing research on SOEs has tended toview state ownership in black-and-white terms—that is, a firm is either state owned or it is not(Kornai, 1992; Shleifer, 1998)—and if state owned,its management and governance falls under thegovernment’s complete ownership and control,thus overlooking this new trend toward greaterflexibility. Some limited research has sketched outthis hybrid model, but much of it has a publicadministration orientation (Koppell, 2007). Yet therich contextualization of important aspects of man-agement, including aspects of firm strategy and cor-porate governance, need to be better understoodunder such varying conditions of state ownershipand control (cf. Cooke, 2003; Kowalski et al., 2013).

State ownership reduces the firms’ profit imper-ative while introducing additional governance mat-ters; thus, state ownership offers a wide variety ofrich theoretical issues for study (Liang, Ren & Sun,2014; Young, Peng, Ahlstrom, Bruton, & Jiang,2008). Specifically, because an SOE’s function (Jen-

sen, 2001) is not necessarily one of profit maximi-zation (Ghosh & Whalley, 2008), SOEs often repre-sent a means to contextualize theory more fullythan if private firms alone were being studied. Thatis, if the SOEs’ chief goal is something other thanmaximizing profit, such as increasing market shareor employment levels, then it cannot be assumedthat SOEs will behave (or should be managed) inthe same manner as private firms. This is consistentwith the argument that the firm’s objective functionshould be made clear in theories of the firm (Jen-sen, 2001; Young, Tsai, Wang, Liu, & Ahlstrom,2014) and in terms of the various aspects of theirgovernance (Musacchio & Lazzarini, 2014; Younget al., 2008). Thus, SOEs need to be examined innew ways to better understand this crucial organi-zational form. This suggests two important and un-derexplored research questions. First, what is thenature of SOEs in the 21st century? And second,what contributes to their ability to survive and, insome cases, prosper?

We address these questions by first reviewingrecent SOE literature in leading academic journals.Then, to fill the gaps identified by our review, westudy 36 cases of hybrid SOEs in four specific in-dustries across 23 countries. We specifically look atkey issues in these SOEs, such as leadership andhow the state may affect the firm’s decisions aboutstrategic issues.

Overall, this paper makes four contributions.First, in terms of empirical contribution, the casestudies will provide a fuller analysis of state firms,particularly in terms of the understudied hybrid

TABLE 1State-Owned Enterprises Represent 9 of the 15 Largest IPOs from 2005 to 2012

Company Industry Year Value ($ billion)

Agricultural Bank of China (SOE) Finance 2010 22.1Industrial and Commercial Bank of China (SOE) Finance 2006 21.9AIA (Hong Kong) Insurance 2010 20.5Visa (United States) Finance 2008 19.7General Motors (United States) (SOE) Automotive 2010 18.1Bank of China (SOE) Finance 2006 11.2Dai-ichi Life Insurance (Japan) Insurance 2010 11.1Rosneft (Russia) (SOE) Oil and gas 2006 10.7Glencore International (Switzerland) Mining 2011 10.0China Construction Bank (SOE) Finance 2005 9.2Electricité de France (SOE) Utility and energy 2005 9.0VTB Group (Russia) (SOE) Finance 2007 8.0Banco Santander Brasil Finance 2009 7.5China State Construction Engineering Corp. (SOE) Construction 2009 7.3Iberdrola Renovables (Spain) Utility and energy 2007 6.6

Source: Adapted from the Economist, 2012a, New masters of the universe. Special Report: State Capitalism, January 21, p. 8.

2015 93Bruton, Peng, Ahlstrom, Stan, and Xu

SOEs. Second, this paper also adds to theory andevidence regarding research on the varieties of cap-italism (Hall & Soskice, 2001). Much past theoryand empirical work on varieties of capitalism hasexamined the important differences among na-tional economies and the impact of these varietiesto economies as a whole (Hall & Soskice, 2001;Whitley, 1998). Despite the importance of the sec-tor, this literature has generally paid little attentionto state ownership because it traditionally was notconsidered a type of capitalism (e.g., Ahlstrom,Bruton, & Yeh, 2008; Gourevitch & Shinn, 2005).This paper focuses more on the varied ways inwhich states intervene in the management andownership of firms.

Third, the paper also contributes to practice byfurther identifying the range of stakeholders andthe resulting objective functions with which SOEmanagement must contend. Managers of non-SOEfirms in a developed economy that do businesswith SOEs in countries such as China or Russia, forexample, need to understand such hybrid organi-zations if they are to successfully work with theircounterparts, given that the SOEs’ strategy andgoals can differ significantly from those of non-SOEfirms, such as placing more emphasis on employ-ment levels or on market share (Battilana & Dorado,2010; Young, Ahlstrom, Bruton, & Rubanik, 2011).

Finally, this study also allows us to address theconcern that although there is widespread ac-knowledgment that the state matters significantlyto organizations, the mechanisms by which thestate matters require much more attention (Bai &Wang, 1998; Musacchio & Lazzarini, 2014).

WHAT DOES RECENT SCHOLARSHIP SAYABOUT SOEs?

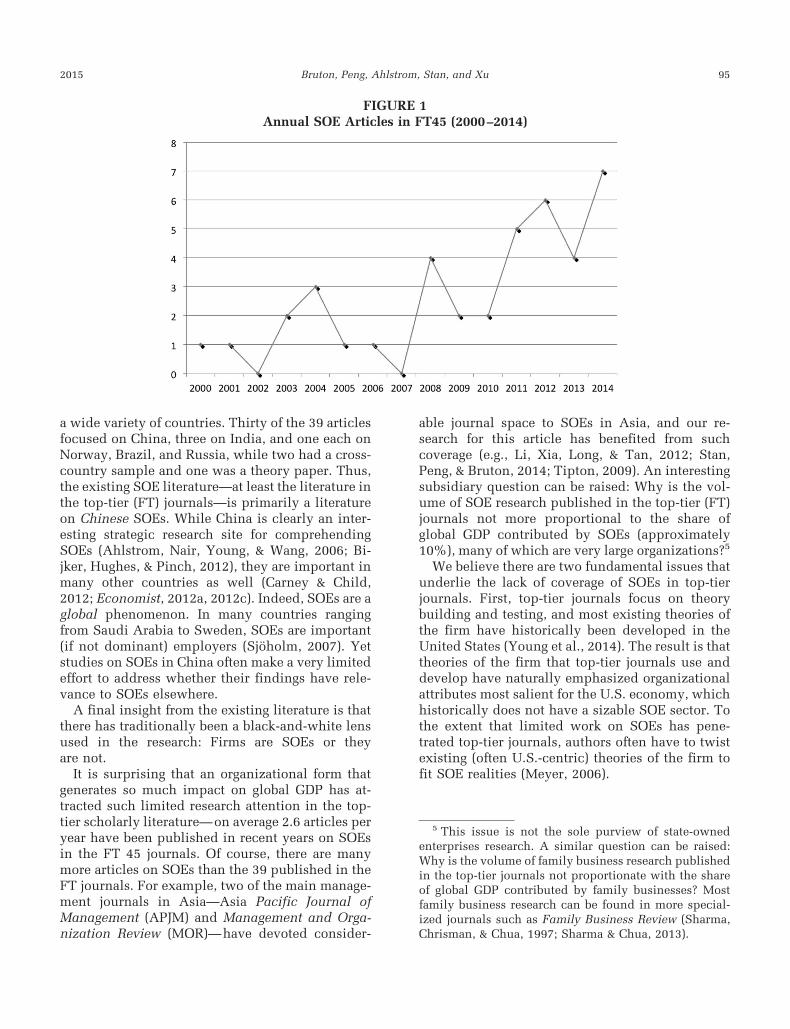

The question of what recent scholarship saysabout SOEs can be answered in two words: notmuch—at least among the top-tier academic jour-nals.1 To date scholars have published only limitedresearch on SOEs in leading journals. In reviewingthis literature, we systematically and comprehen-sively examined the journals of the FinancialTimes’ top 45 list (FT 45)2 from 2000 to 2014,

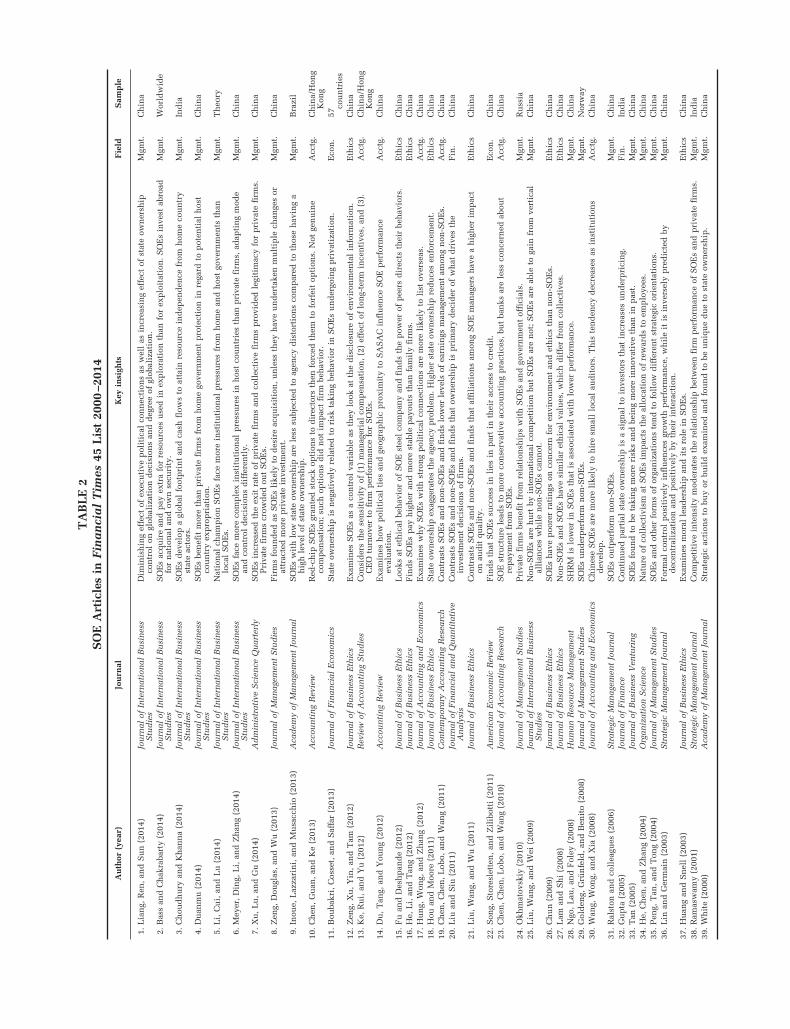

inclusive. Using the search term state-owned enter-prise (or SOE) in the title or abstract, we were ableto identify only 57 articles from that 15-year period.Two of those articles appeared in the more practi-tioner-oriented Harvard Business Review, leaving55 scholarly articles. Sixteen of these 55 articleswere on the privatization of SOEs. As a result, only39 articles out of thousands published by the FT 45top journals during the most recent 15-year periodactually focused on the management of SOEs.3 Al-though inquiry into SOEs is on the rise, as noted inFigure 1, there is still a dearth of research onthe topic.

The 39 SOE articles outlined in Table 2 touch ona wide variety of issues, but with such a limitednumber it is possible to generate only a few com-mon insights. First, almost all 39 articles viewedSOEs dichotomously—that is, firms were labeledas either completely state owned or not. Inone of the few articles whose authors did not holdthe dichotomous view, Gupta (2005) acknowledgedthe potential for mixed ownership structures,with the state maintaining varying levels of owner-ship even in publicly listed companies. It is impor-tant to note that Gupta (2005) is a finance articleand that management and organizational researchdealing with mixed ownership remains verylimited.

A second common insight derived from the 39articles is that researchers have disagreed on theimpact of state ownership on firm performance. Forexample, Ralston, Terpstra-Tong, Terpstra, Wang,and Egri (2006) reported that SOE managers inChina perceived their firms to be more competitivethan private firms. However, Goldeng, Grünfeld,and Benito (2008) found that private firms in Nor-way clearly outperformed SOEs. These and otherconflicting findings may have resulted from theauthors dichotomizing their samples into stateand nonstate entities without considering hybridSOEs.4

A third insight is that the 39 articles on SOEs todate have not examined the topic of SOE hybrids in

1 Even the comprehensive Handbook of Organiza-tional Economics (Gibbons & Roberts, 2013) and one ofthe major texts on growth economics (Acemoglu, 2009)only occasionally mention state ownership of firms.

2 These are the journals the Financial Times uses to

compile its business school research rank. The Academyof Management Perspectives is included in this list.

3 All of those 39 articles are marked with an asterisk(*) in the references section.

4 Recent research in finance has also started to addressthis issue in discussing partial privatization and howgovernment participation can affect the performance ofstate-owned or state-linked firms (e.g., Fan, Wong, &Zhang, 2007).

94 FebruaryThe Academy of Management Perspectives

a wide variety of countries. Thirty of the 39 articlesfocused on China, three on India, and one each onNorway, Brazil, and Russia, while two had a cross-country sample and one was a theory paper. Thus,the existing SOE literature—at least the literature inthe top-tier (FT) journals—is primarily a literatureon Chinese SOEs. While China is clearly an inter-esting strategic research site for comprehendingSOEs (Ahlstrom, Nair, Young, & Wang, 2006; Bi-jker, Hughes, & Pinch, 2012), they are important inmany other countries as well (Carney & Child,2012; Economist, 2012a, 2012c). Indeed, SOEs are aglobal phenomenon. In many countries rangingfrom Saudi Arabia to Sweden, SOEs are important(if not dominant) employers (Sjöholm, 2007). Yetstudies on SOEs in China often make a very limitedeffort to address whether their findings have rele-vance to SOEs elsewhere.

A final insight from the existing literature is thatthere has traditionally been a black-and-white lensused in the research: Firms are SOEs or theyare not.

It is surprising that an organizational form thatgenerates so much impact on global GDP has at-tracted such limited research attention in the top-tier scholarly literature—on average 2.6 articles peryear have been published in recent years on SOEsin the FT 45 journals. Of course, there are manymore articles on SOEs than the 39 published in theFT journals. For example, two of the main manage-ment journals in Asia—Asia Pacific Journal ofManagement (APJM) and Management and Orga-nization Review (MOR)—have devoted consider-

able journal space to SOEs in Asia, and our re-search for this article has benefited from suchcoverage (e.g., Li, Xia, Long, & Tan, 2012; Stan,Peng, & Bruton, 2014; Tipton, 2009). An interestingsubsidiary question can be raised: Why is the vol-ume of SOE research published in the top-tier (FT)journals not more proportional to the share ofglobal GDP contributed by SOEs (approximately10%), many of which are very large organizations?5

We believe there are two fundamental issues thatunderlie the lack of coverage of SOEs in top-tierjournals. First, top-tier journals focus on theorybuilding and testing, and most existing theories ofthe firm have historically been developed in theUnited States (Young et al., 2014). The result is thattheories of the firm that top-tier journals use anddevelop have naturally emphasized organizationalattributes most salient for the U.S. economy, whichhistorically does not have a sizable SOE sector. Tothe extent that limited work on SOEs has pene-trated top-tier journals, authors often have to twistexisting (often U.S.-centric) theories of the firm tofit SOE realities (Meyer, 2006).

5 This issue is not the sole purview of state-ownedenterprises research. A similar question can be raised:Why is the volume of family business research publishedin the top-tier journals not proportionate with the shareof global GDP contributed by family businesses? Mostfamily business research can be found in more special-ized journals such as Family Business Review (Sharma,Chrisman, & Chua, 1997; Sharma & Chua, 2013).

FIGURE 1Annual SOE Articles in FT45 (2000–2014)

2015 95Bruton, Peng, Ahlstrom, Stan, and Xu

TA

BL

E2

SO

EA

rtic

les

inF

ina

nci

al

Tim

es45

Lis

t20

00–2

014

Au

thor

(yea

r)Jo

urn

alK

eyin

sigh

tsF

ield

Sam

ple

1.L

ian

g,R

en,

and

Su

n(2

014)

Jou

rnal

ofIn

tern

atio

nal

Bu

sin

ess

Stu

die

sD

imin

ish

ing

effe

ctof

exec

uti

vep

olit

ical

con

nec

tion

sas

wel

las

incr

easi

ng

effe

ctof

stat

eow

ner

ship

con

trol

ongl

obal

izat

ion

dec

isio

ns

and

deg

ree

ofgl

obal

izat

ion

.M

gmt.

Ch

ina

2.B

ass

and

Ch

akra

bart

y(2

014)

Jou

rnal

ofIn

tern

atio

nal

Bu

sin

ess

Stu

die

sS

OE

sac

quir

ean

dp

ayex

tra

for

reso

urc

esu

sed

inex

plo

rati

onth

anfo

rex

plo

itat

ion

.S

OE

sin

vest

abro

adfo

rn

atio

nal

and

own

secu

rity

.M

gmt.

Wor

ldw

ide

3.C

hou

dh

ury

and

Kh

ann

a(2

014)

Jou

rnal

ofIn

tern

atio

nal

Bu

sin

ess

Stu

die

sS

OE

sd

evel

opa

glob

alfo

otp

rin

tan

dca

shfl

ows

toat

tain

reso

urc

ein

dep

end

ence

from

hom

eco

un

try

stat

eac

tors

.M

gmt.

Ind

ia

4.D

uan

mu

(201

4)Jo

urn

alof

Inte

rnat

ion

alB

usi

nes

sS

tud

ies

SO

Es

ben

efit

mor

eth

anp

riva

tefi

rms

from

hom

ego

vern

men

tp

rote

ctio

nin

rega

rdto

pot

enti

alh

ost

cou

ntr

yex

pro

pri

atio

n.

Mgm

t.C

hin

a

5.L

i,C

ui,

and

Lu

(201

4)Jo

urn

alof

Inte

rnat

ion

alB

usi

nes

sS

tud

ies

Nat

ion

alch

amp

ion

SO

Es

face

mor

ein

stit

uti

onal

pre

ssu

res

from

hom

ean

dh

ost

gove

rnm

ents

than

loca

lS

OE

s.M

gmt.

Th

eory

6.M

eyer

,D

ing,

Li,

and

Zh

ang

(201

4)Jo

urn

alof

Inte

rnat

ion

alB

usi

nes

sS

tud

ies

SO

Es

face

mor

eco

mp

lex

inst

itu

tion

alp

ress

ure

sin

hos

tco

un

trie

sth

anp

riva

tefi

rms,

adap

tin

gm

ode

and

con

trol

dec

isio

ns

dif

fere

ntl

y.M

gmt.

Ch

ina

7.X

u,

Lu

,an

dG

u(2

014)

Ad

min

istr

ativ

eS

cien

ceQ

uar

terl

yS

OE

sin

crea

sed

the

exit

rate

ofp

riva

tefi

rms

and

coll

ecti

vefi

rms

pro

vid

edle

giti

mac

yfo

rp

riva

tefi

rms.

Pri

vate

firm

scr

owd

edou

tS

OE

s.M

gmt.

Ch

ina

8.Z

eng,

Dou

glas

,an

dW

u(2

013)

Jou

rnal

ofM

anag

emen

tS

tud

ies

Fir

ms

fou

nd

edas

SO

Es

like

lyto

des

ire

acqu

isit

ion

,u

nle

ssth

eyh

ave

un

der

take

nm

ult

iple

chan

ges

orat

trac

ted

mor

ep

riva

tein

vest

men

t.M

gmt.

Ch

ina

9.In

oue,

Laz

zari

ni,

and

Mu

sacc

hio

(201

3)A

cad

emy

ofM

anag

emen

tJo

urn

alS

OE

sw

ith

low

stat

eow

ner

ship

are

less

subj

ecte

dto

agen

cyd

isto

rtio

ns

com

par

edto

thos

eh

avin

ga

hig

hle

vel

ofst

ate

own

ersh

ip.

Mgm

t.B

razi

l

10.

Ch

en,

Gu

an,

and

Ke

(201

3)A

ccou

nti

ng

Rev

iew

Red

-ch

ipS

OE

sgr

ante

dst

ock

opti

ons

tod

irec

tors

then

forc

edth

emto

forf

eit

opti

ons.

Not

gen

uin

eco

mp

ensa

tion

;su

chop

tion

sd

idn

otim

pac

tfi

rmbe

hav

ior.

Acc

tg.

Ch

ina/

Hon

gK

ong

11.

Bou

bakr

i,C

osse

t,an

dS

affa

r(2

013)

Jou

rnal

ofF

inan

cial

Eco

nom

ics

Sta

teow

ner

ship

isn

egat

ivel

yre

late

dto

risk

taki

ng

beh

avio

rin

SO

Es

un

der

goin

gp

riva

tiza

tion

.E

con

.57

cou

ntr

ies

12.

Zen

g,X

u,

Yin

,an

dT

am(2

012)

Jou

rnal

ofB

usi

nes

sE

thic

sE

xam

ines

SO

Es

asa

con

trol

vari

able

asth

eylo

okat

the

dis

clos

ure

ofen

viro

nm

enta

lin

form

atio

n.

Eth

ics

Ch

ina

13.

Ke,

Ru

i,an

dY

u(2

012)

Rev

iew

ofA

ccou

nti

ng

Stu

die

sC

onsi

der

sth

ese

nsi

tivi

tyof

(1)

man

ager

ial

com

pen

sati

on,

(2)

effe

ctof

lon

g-te

rmin

cen

tive

s,an

d(3

).C

EO

turn

over

tofi

rmp

erfo

rman

cefo

rS

OE

s.A

cctg

.C

hin

a/H

ong

Kon

g14

.D

u,

Tan

g,an

dY

oun

g(2

012)

Acc

oun

tin

gR

evie

wE

xam

ines

how

pol

itic

alti

esan

dge

ogra

ph

icp

roxi

mit

yto

SA

SA

Cin

flu

ence

SO

Ep

erfo

rman

ceev

alu

atio

n.

Acc

tg.

Ch

ina

15.

Fu

and

Des

hp

and

e(2

012)

Jou

rnal

ofB

usi

nes

sE

thic

sL

ooks

atet

hic

albe

hav

ior

ofS

OE

stee

lco

mp

any

and

fin

ds

the

pow

erof

pee

rsd

irec

tsth

eir

beh

avio

rs.

Eth

ics

Ch

ina

16.

He,

Li,

and

Tan

g(2

012)

Jou

rnal

ofB

usi

nes

sE

thic

sF

ind

sS

OE

sp

ayh

igh

eran

dm

ore

stab

lep

ayou

tsth

anfa

mil

yfi

rms.

Eth

ics

Ch

ina

17.

Hu

ng,

Won

g,an

dZ

han

g(2

012)

Jou

rnal

ofA

ccou

nti

ng

and

Eco

nom

ics

Exa

min

esw

hy

SO

Es

wit

hst

ron

gp

olit

ical

con

nec

tion

sar

em

ore

like

lyto

list

over

seas

.A

cctg

.C

hin

a18

.H

ouan

dM

oore

(201

1)Jo

urn

alof

Bu

sin

ess

Eth

ics

Sta

teow

ner

ship

exag

gera

tes

the

agen

cyp

robl

em.

Hig

her

stat

eow

ner

ship

red

uce

sen

forc

emen

t.E

thic

sC

hin

a19

.C

hen

,C

hen

,L

obo,

and

Wan

g(2

011)

Con

tem

por

ary

Acc

oun

tin

gR

esea

rch

Con

tras

tsS

OE

san

dn

on-S

OE

san

dfi

nd

slo

wer

leve

lsof

earn

ings

man

agem

ent

amon

gn

on-S

OE

s.A

cctg

.C

hin

a20

.L

iuan

dS

iu(2

011)

Jou

rnal

ofF

inan

cial

and

Qu

anti

tati

veA

nal

ysis

Con

tras

tsS

OE

san

dn

on-S

OE

san

dfi

nd

sth

atow

ner

ship

isp

rim

ary

dec

ider

ofw

hat

dri

ves

the

inve

stm

ent

dec

isio

ns

offi

rms.

Fin

.C

hin

a

21.

Liu

,W

ang,

and

Wu

(201

1)Jo

urn

alof

Bu

sin

ess

Eth

ics

Con

tras

tsS

OE

san

dn

on-S

OE

san

dfi

nd

sth

ataf

fili

atio

ns

amon

gS

OE

man

ager

sh

ave

ah

igh

erim

pac

ton

aud

itqu

alit

y.E

thic

sC

hin

a

22.

Son

g,S

tore

slet

ten

,an

dZ

ilib

otti

(201

1)A

mer

ican

Eco

nom

icR

evie

wF

ind

sth

atS

OE

ssu

cces

sin

lies

inp

art

inth

eir

acce

ssto

cred

it.

Eco

n.

Ch

ina

23.

Ch

en,

Ch

en,

Lob

o,an

dW

ang

(201

0)Jo

urn

alof

Acc

oun

tin

gR

esea

rch

SO

Est

ruct

ure

lead

sto

mor

eco

nse

rvat

ive

acco

un

tin

gp

ract

ices

,bu

tba

nks

are

less

con

cern

edab

out

rep

aym

ent

from

SO

Es.

Acc

tg.

Ch

ina

24.

Okh

mat

ovsk

iy(2

010)

Jou

rnal

ofM

anag

emen

tS

tud

ies

Pri

vate

firm

sbe

nef

itfr

omre

lati

onsh

ips

wit

hS

OE

san

dgo

vern

men

tof

fici

als.

Mgm

t.R

uss

ia25

.L

iu,

Wan

g,an

dW

ei(2

009)

Jou

rnal

ofIn

tern

atio

nal

Bu

sin

ess

Stu

die

sN

on-S

OE

sar

eh

urt

byin

tern

atio

nal

com

pet

itio

nbu

tS

OE

sar

en

ot;

SO

Es

are

able

toga

infr

omve

rtic

alal

lian

ces

wh

ile

non

-SO

Es

can

not

.M

gmt.

Ch

ina

26.

Ch

un

(200

9)Jo

urn

alof

Bu

sin

ess

Eth

ics

SO

Es

hav

ep

oore

rra

tin

gson

con

cern

for

envi

ron

men

tan

det

hic

sth

ann

on-S

OE

s.E

thic

sC

hin

a27

.L

aman

dS

hi

(200

8)Jo

urn

alof

Bu

sin

ess

Eth

ics

Non

-SO

Es

and

SO

Es

hav

esi

mil

aret

hic

alva

lues

,w

hic

hd

iffe

rfr

omco

llec

tive

s.E

thic

sC

hin

a28

.N

go,

Lau

,an

dF

oley

(200

8)H

um

anR

esou

rce

Man

agem

ent

SH

RM

islo

wer

inS

OE

sth

atis

asso

ciat

edw

ith

low

erp

erfo

rman

ce.

Mgm

t.C

hin

a29

.G

old

eng,

Grü

nfe

ld,

and

Ben

ito

(200

8)Jo

urn

alof

Man

agem

ent

Stu

die

sS

OE

su

nd

erp

erfo

rmn

on-S

OE

s.M

gmt.

Nor

way

30.

Wan

g,W

ong,

and

Xia

(200

8)Jo

urn

alof

Acc

oun

tin

gan

dE

con

omic

sC

hin

ese

SO

Es

are

mor

eli

kely

toh

ire

smal

llo

cal

aud

itor

s.T

his

ten

den

cyd

ecre

ases

asin

stit

uti

ons

dev

elop

.A

cctg

.C

hin

a

31.

Ral

ston

and

coll

eagu

es(2

006)

Str

ateg

icM

anag

emen

tJo

urn

alS

OE

sou

tper

form

non

-SO

Es.

Mgm

t.C

hin

a32

.G

up

ta(2

005)

Jou

rnal

ofF

inan

ceC

onti

nu

edp

arti

alst

ate

own

ersh

ipis

asi

gnal

toin

vest

ors

that

incr

ease

su

nd

erp

rici

ng.

Fin

.In

dia

33.

Tan

(200

5)Jo

urn

alof

Bu

sin

ess

Ven

turi

ng

SO

Es

fou

nd

tobe

taki

ng

mor

eri

sks

and

bein

gm

ore

inn

ovat

ive

than

inp

ast.

Mgm

t.C

hin

a34

.H

e,C

hen

,an

dZ

han

g(2

004)

Org

aniz

atio

nS

cien

ceN

atu

reof

coll

ecti

vism

atS

OE

sim

pac

tsth

eal

loca

tion

ofre

war

ds

toem

plo

yees

.M

gmt.

Ch

ina

35.

Pen

g,T

an,

and

Ton

g(2

004)

Jou

rnal

ofM

anag

emen

tS

tud

ies

SO

Es

and

oth

erfo

rms

ofor

gan

izat

ion

ste

nd

tofo

llow

dif

fere

nt

stra

tegi

cor

ien

tati

ons.

Mgm

t.C

hin

a36

.L

inan

dG

erm

ain

(200

3)S

trat

egic

Man

agem

ent

Jou

rnal

For

mal

con

trol

pos

itiv

ely

infl

uen

ces

grow

thp

erfo

rman

ce,

wh

ile

itis

inve

rsel

yp

red

icte

dby

dec

entr

aliz

atio

nan

dp

osit

ivel

yby

thei

rin

tera

ctio

n.

Mgm

t.C

hin

a

37.

Hu

ang

and

Sn

ell

(200

3)Jo

urn

alof

Bu

sin

ess

Eth

ics

Exa

min

esm

oral

lead

ersh

ipan

dit

sro

lein

SO

Es.

Eth

ics

Ch

ina

38.

Ram

asw

amy

(200

1)S

trat

egic

Man

agem

ent

Jou

rnal

Com

pet

itiv

ein

ten

sity

mod

erat

esth

ere

lati

onsh

ipbe

twee

nfi

rmp

erfo

rman

ceof

SO

Es

and

pri

vate

firm

s.M

gmt.

Ind

ia39

.W

hit

e(2

000)

Aca

dem

yof

Man

agem

ent

Jou

rnal

Str

ateg

icac

tion

sto

buy

orbu

ild

exam

ined

and

fou

nd

tobe

un

iqu

ed

ue

tost

ate

own

ersh

ip.

Mgm

t.C

hin

a

Second, the ideological nature of the debate onstate ownership has resulted in the difficulties ofincorporating SOEs into (mainstream) theories ofthe firm. Some work has framed the debate as so-cialism versus capitalism, which may have made itmore difficult in terms of theory and ideology forWestern scholars to highlight the merits of SOEs,especially in the last quarter-century. Among mostscholars and policymakers in the West, it has al-most become an article of faith that SOEs are lessefficient than private firms (Dewenter & Malatesta,2001). Thus, instead of studying SOEs on their ownterms, many scholars have viewed them primarilyas targets for privatization (Economist, 2014; Fila-totchev, Buck, & Zhukov, 2000; Kozminski, 1993;Megginson & Netter, 2001; Vickers & Yarrow,1991). The privatization movement throughout theworld since the 1980s seems to suggest that SOEsare a transitional organizational form destined tobecome relics of history (Spicer et al., 2000). But, asdiscussed earlier, this has not happened. Instead,in response to the 2008 economic crisis, even gov-ernments in developed economies such as theUnited States and the United Kingdom partiallynationalized major private firms such as GeneralMotors (GM) and the Royal Bank of Scotland (RBS).

For management and organizational research tofurther build its relevance and insight into impor-tant contemporary issues, we must address the dis-connect between the limited scholarly coverage intop-tier journals and the wide-ranging real-worldrealities of the major organizational form of theSOE (Christensen & Carlile, 2009; Makino &Yiu, 2014).

HYBRID ORGANIZATIONS

A key characteristic of SOEs today—and a reasonwhy they have been able to prosper—is their abilityto adapt and take on a new organizational form(Musacchio & Lazzarini, 2014). This new form,known as hybrid organizations, “incorporate[s] el-ements from different institutional logics” (Pache &Santos, 2013, p. 972). Clearly, state ownership andprivate ownership represent different institutionallogics (Bruton, Ahlstrom, & Li, 2010), thus necessi-tating our consideration of SOEs incorporating bothstate and private ownership as hybrid organiza-tions (Inoue et al., 2013). When managed well, hy-brid organizations can harvest legitimacy-enhanc-ing elements of the different institutional logics,and survive and thrive (Battilana & Dorado, 2010).

One can trace the treatment of ownership andcontrol in the management literature to the seminalwork by Berle and Means (1932), The Modern Cor-poration and Private Property, which argued thatdiffused ownership in modern firms preventedmeaningful control by owners and created poten-tial agency problems. The view of ownership andcontrol as directly related is consistent with the factthat three decades ago scholars typically thought ofSOEs as enterprises operating in command econo-mies, where the state had absolute ownership aswell as control over state enterprises, a belief thatwas understandable given the prevalence of SOEsin these economies (Kornai, 1992; Peng & Heath,1996; Shleifer, 1998).

The setting SOEs face today is more complex.Rather than being simply state owned, most SOEstoday mix private and public ownership (Econo-mist, 2012a; Flores-Macias & Musacchio, 2009;Huang & Orr, 2007; Woetzel, 2008). Facing complexownership and control patterns, investors andother stakeholders need to be sensitive as they lookto partner with or invest in SOEs (Bruton, Ahl-strom, & Wan, 2003; Young et al., 2011). Thus,researchers should also view state ownership as acontinuous variable (Gupta, 2005; Jing & Tyle-cote, 2005).

However, it should also be recognized that own-ership in this setting does not necessarily equate tocontrol (Sheng & Zhao, 2012; Sun & Tong, 2003). InChina, for example, control of the firm comes fromthe offering of different types of shares. Shares thatvote on control issues may be held by the centralgovernment, by various local governments, or byother SOEs (Sheng & Zhao, 2012; Xu & Wang,1999). For example, the Chinese central govern-ment is the controlling shareholder of the Agricul-tural Bank of China, but the bank has governancetraits that allow much participation by private in-vestors. Such patterns can be found in other coun-tries as well (Flinders, 2006; Mishra, 2009; Tipton,2009). It is more appropriate, therefore, to viewSOEs as hybrid organizations that consist of differ-ent mixtures of private ownership and control bythe state (Huang & Orr, 2007; Koppell, 2007). Thus,as we think of our two research questions in thispaper—(1) what is the nature of SOEs today? and(2) why have they been able to survive and pros-per?—the resulting organizational form that SOEshave taken on becomes quite important. Therefore,we focus on defining SOEs as hybrid organizationsand highlighting their strategic and performanceimplications.

2015 97Bruton, Peng, Ahlstrom, Stan, and Xu

Some research published in the 1980s recognizedhybrid organizations that mix public and privateownership. For example, Emmert and Crow (1988)examined hybrid public–private firms in theUnited States such as the Overseas Private Invest-ment Corporation (OPIC), which facilitates U.S. in-vestment in developing countries. This early re-search on hybrids generally sought to understandtraditional government-run activities that wereprivatized, such as trash collection or waterworks.Such hybrids typically did not face competition fortheir services from other firms in the local market-place. In contrast, today’s hybrid SOEs increasinglyoperate in competitive product markets, whichcalls for a new understanding of their rationales,operations, and performance as well as the relevantinstitutional environments.

MARKETS, HIERARCHIES, AGENTS, ANDINSTITUTIONS

Following the earlier SOE research that appearedin top-tier journals (Inoue et al., 2013; Peng &Heath, 1996), we draw on three core managerialtheories that help scholars understand all organiza-tions to develop our understanding of hybrid SOEfirms: transaction cost economics, agency theory,and neoinstitutional theory. These three theoriescan form a foundation for scholars to further de-velop an understanding of the similarities and dif-ferences between SOEs and other organizations.

Transaction Cost Economics

From a transaction cost standpoint, Williamson(1975, 1992) identified two basic forms of eco-nomic organizations: markets and hierarchies. Eachorganizational form has its own rationale (Steier,1998). The self-interested actions of individualsand firms, focusing on issues such as prices andprofits, form the basis for market organizations. Incontrast, the rationale for hierarchical organiza-tions is that “the visible hand of management sup-plants the invisible hand of market in coordinatingsupply and demand” (Powell, 1990, p. 303; see alsoChandler, 1977). Williamson (1985) acknowledgedthat organizations may combine aspects of bothmarket and hierarchy to create a “middle kind” oforganization, and in fact went on to call for greaterattention to such middle kinds of firms and eco-nomic organizations. Huang (1990) found someearly examples of hybrid state firms in China, whilePowell (1990, p. 299) went further, adding that

“[b]y sticking to the twin pillars of markets andhierarchies, our attention is deflected from a diver-sity of organizational designs.”

Thus, from a transaction cost perspective, hy-brids can be viewed as organizations that “combineaspects of market transactions and characteristicsof hierarchies and fall between the two alternativeson a continuum” (Larson, 1992, p. 76). Hybrid or-ganizations are “highly significant features of thecontemporary organizational landscape” (Powell,1987, p. 68). However, the research focus for suchhybrids has been on government agencies (André,2010; Steier, 1998), such as how to make theseagencies act in a more business-like manner (Os-borne & Gaebler, 1992; Pollitt & Bouckaert, 2004).Scholars have also recognized hybrid organizationsin the commercial sector (Battilana & Dorado, 2010;Pache & Santos, 2013; Shane, 1996), but those ex-aminations of business have typically focused onprivate firms performing government services. As aresult, there remains a lack of understanding ofSOEs that are hybrid firms conducting businessactivities.

Agency Theory

Insights on hybrid SOEs can also be drawn fromagency theory as it addresses the conflicting inter-ests between managers (agents) and the owners(principals) on whose behalf they manage organi-zations (Eisenhardt, 1989). Classical agency theoryassumes that both principals and agents are self-interest–seeking utility maximizers, with agentsbeing risk averse and principals, who could di-versify their holdings, being risk neutral (Sha-piro, 2005). However, given the hybrid nature ofmany SOEs, a multiple agency theory perspectiveenables us to see that SOEs have potential con-flicts of interests among different agent groups(Arthurs, Hoskisson, Busenitz, & Johnson, 2008).The result is that SOEs face conflicting choices inregard to which principals’ interests they shouldserve, more so than most private firms, especiallygiven the “conflicting voices” that those princi-pals may have as an outcome of different incen-tives and time horizons (Ghosh & Whalley, 2008;Hoskisson, Hitt, Johnson, & Grossman, 2002; Jen-sen, 2001). Such principal–principal conflicts be-tween controlling and minority shareholders,which may lead to suboptimal strategic deci-sions, are present in SOEs operating in emergingand developing economies (Young et al., 2008).In this setting the fiduciary duty of agents, such

98 FebruaryThe Academy of Management Perspectives

as the boards of directors, is not to any specificgroup of stakeholders such as shareholders. In-stead, the fiduciary duty is to the organizationitself (Lan & Heracleous, 2010; Mehrotra, 2011).

Institutional Theory

Regardless of whether they are wholly state-owned “classical” types or hybrid types, SOEs areclearly products of their institutional environ-ments, thus rendering an institutional lens as ahelpful theoretical tool (DiMaggio & Powell, 1991;Godfrey, 2014). Specifically, neoinstitutional the-ory posits that the taken-for-granted assumptions,laws, rules, norms, and boundaries in establishedorganizational fields strongly affect the behavior ofactors (North, 1990; Peng, Sun, Pinkham, & Chen,2009; Scott, 2014). Much past research has viewedinstitutions, such as societal laws or cultural val-ues, as macro-level variables that affect an entiresociety (Meyer, Estrin, Bhaumik, & Peng, 2009).However, Wicks (2001) argued that institutionsalso occur at the micro level. Specifically, a mind-set can develop that affects the firms in that indus-try or profession in terms of the standards andcommercial conventions in that industry or profes-sion (Eisenhardt, 1988; McCloskey, 1994). Employ-ing such a micro-level perspective, Vermeulen, VanDen Bosch, and Volberda (2007) examined howmicro institutional forces, including the mindset ofmanagers at the business unit level of a firm, affectincremental product innovation efforts in the fi-nancial services industry.

Inspired by such work, we examine both themacro and micro levels of institutions and theirimpact on SOEs. Overall, as driven by transactioncost, agency, and institutional logics, via a series ofcase studies, we focus on how SOEs mix ownershipand control as hybrid organizations, and on howdifferent macro and micro institutions affect differ-ent levels of state ownership and control.

CASE ANALYSIS

Developing a greater understanding of hybridSOEs is a complex and nuanced task. We define theinstitutional field in terms of national boundariesand examine SOEs from a diverse set of countriesand industries to understand how they operate(Greenwood & Suddaby, 2006). The goal is to un-derstand how SOEs behave in a single country andto also understand more broadly the strategic ac-tions that affect such firms across a wide range of

countries and regions of the world. Therefore, weemployed a purposive case selection (Yin, 2013).We thus sought to cover a range of industries gen-erally important in the state sector by selectingcases of SOEs from four specific industry sectors—natural resources/energy, transportation, manufac-turing, and finance—for each of the different mix-tures of ownership and control we examined.

We chose these sectors to ensure our consider-ation of a wide range of firms and industries. Wealso selected these four sectors because they allowus to address specific concerns. First, these sectorsare not directly related to national security, andthus face some market-based competition. Second,the industry concentration is modest in these in-dustries, and therefore monopoly is not a concern.We also wanted to be able to compare firms in thesame industry in different settings of ownershipand control (Brouthers & Bamossy, 2006). Addi-tionally, given that rather narrow geographic scopeis a limitation of current SOE research, we sought abroad set of countries. Thus, our sample includes23 countries. The ability to have some cases fromthe same country in different cells of the matrix,reflecting different levels of ownership and control,however, also allowed us to ensure that the resultswe identified were not due to strictly country-spe-cific factors.

For these cases we wanted to gather a rich rangeof data from the popular and business press, annualreports if available, and reported financial data.Thus, a major requirement in the case-selectionprocess was the availability of a wide variety ofinformation for each company, as there is very lim-ited information released about some SOEs by gov-ernments or by other sources. We also ensured thatthe firms we examined had market-based competi-tors. In selecting the cases we focused in a mannersuggested by established methodology for qualita-tive research to ensure that the cases were clear anddistinct in their nature. Qualitative research gener-ally does not focus on average cases but on thosecases that allow clear contrasts to be emphasized sothat rich understanding can be developed (Ragin,1987; Yin, 2013). As noted earlier, research on hy-brid public–private firms has tended to focus onpublic entities that perform a public function butseek to operate more as private firms. Here ourfocus is on state-owned businesses that face com-petition either locally or internationally to allow usto examine more clearly the strategic decisions thefirms make.

2015 99Bruton, Peng, Ahlstrom, Stan, and Xu

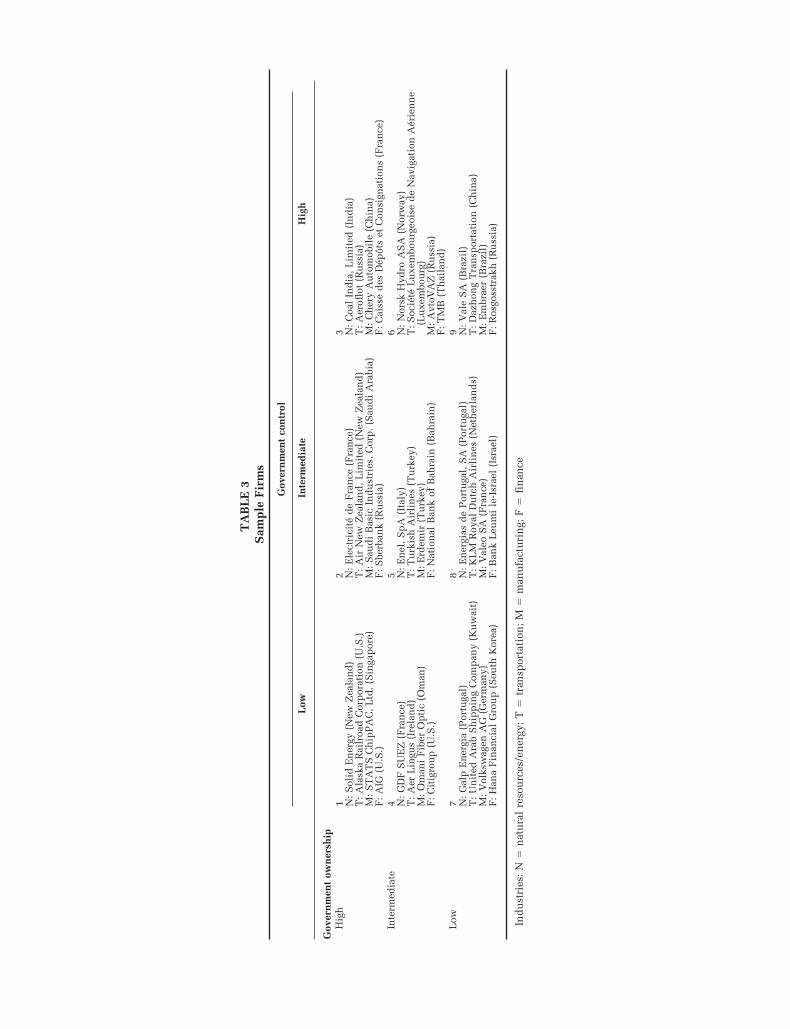

To highlight the hybrid nature of SOEs, we con-structed a 3 � 3 matrix showing levels of govern-ment ownership and government control (see Table3). We defined “high level of government owner-ship” as ownership greater than 50%, “intermedi-ate level” as 25% to 50%, and “low level” as lessthan 25%. These levels were chosen to ensure aclear representation of ownership (Kowalski et al.,2013). The horizontal axis representing the level ofgovernment control is divided into high, middle,and low categories based on case histories of thefirms and a judgment by the authors grounded inreports of government control (Easterby-Smith,Golden-Biddle, & Locke, 2008).

We first examined a large number of SOEs. Wethen selected cases that fit the requirements of eachcell. As noted above, we focused on the cases pro-viding clear and strong examples of the given levelof ownership and desired level of control. If afterfurther examination of these cases a firm’s level ofownership or government control differed from ourexpectations, we selected another case. The authorseventually came to an agreement on the placementof all cases in the cells. Two research assistantsthen reviewed the cases and validated the place-ment. Through this process we developed 36 casesof SOEs that populate the nine cells.

RESULTS

SOEs as Hybrid Organizations

Our rich and diverse set of cases supports theargument that on a worldwide basis a new form ofSOE has developed in which there are variations inownership and control. The traditional SOE, withhigh levels of ownership by government and corre-spondingly high levels of control, still exists (seecell 3 in Table 3). However, the presence of a richrange of cases in which ownership and controlappear to be far more mixed supports our argumentfor the emergence of a new form of organization, inwhich public and private ownership and controlmix to match the needs of the given setting.

These settings vary widely. For example, the Sin-gapore government recognized that while it couldsupply large amounts of investment capital itcould not efficiently manage high-technology firms(Bruton, Ahlstrom, & Singh, 2002). As a result,when Singapore formed STATS ChipPAC througha 2004 merger to provide semiconductor packagingand testing services (cell 1), they encouraged anaggressive market-driven approach to firm manage-

ment, with a Singapore government holding firmsupplying funding (and owning much equity) butproviding little day-to-day direction.6

For some SOEs the state has dramatically re-duced its ownership through privatization, but therealities of the political setting in these locationspushed the state to retain strong control over thefirm (Ahlstrom & Bruton, 2010). For example, theRussian government still holds a single “goldenshare” in more than 180 firms with which the statecan veto major firm actions (Economist, 2012a).Scholars report similar levels of control for SOEs inChina, with the power to veto resting with thegovernment or the controlling councils, such as theState-owned Assets Supervision and Administra-tion Commission (SASAC) of the State Council.

The ability of SOEs to adapt to different settingsin ways specific to the needs in that location in partexplains why some SOEs have not only survivedbut often prospered despite many predictions oftheir demise. If the dichotomous choice of full statecontrol and ownership versus pure private owner-ship were all a government could make, then thedecline of the SOEs may well have occurred. In-stead, SOEs have been able to adapt and change asneeded with the environment and economic situa-tion. As a result, we expect that most SOEs willhave some hybrid features that mix state and pri-vate ownership and control.

Hybrid Organizations and Control

One key area that merits future investigation isthe nature of the control of the SOE and its impacton performance. While the authors of one of the 39SOE articles we reviewed for this article reportedthat managers in China perceived SOEs’ perfor-mance to be better than that of private firms (Ral-ston et al., 2006), researchers (particularly in eco-nomics) have found that state ownership does notgenerate superior firm performance (Bartel & Har-rison, 2005) and is often a drag on both productiv-ity and even national income (Hsieh & Klenow,2009; Kornai, 1992; Shleifer, 1998).

6 STATS ChipPAC was recently sold to Chinese elec-tronics firm Jiangsu Changjiang. The Singapore govern-ment realized a healthy return from the sale (http://finance.burgtelegram.com/news/otc-markets/jiangsu-changjiang-wholly-acquires-stats-chippac/jiangsu-changjiang-wholly-acquires-stats-chippac-13634948.htm, ac-cessed January 22, 2015).

100 FebruaryThe Academy of Management Perspectives

TA

BL

E3

Sam

ple

Fir

ms

Gov

ern

men

tco

ntr

ol

Low

Inte

rmed

iate

Hig

h

Gov

ern

men

tow

ner

ship

Hig

h1 N

:S

olid

En

ergy

(New

Zea

lan

d)

T:

Ala

ska

Rai

lroa

dC

orp

orat

ion

(U.S

.)M

:S

TA

TS

Ch

ipP

AC

,L

td.

(Sin

gap

ore)

F:

AIG

(U.S

.)

2 N:

Ele

ctri

cité

de

Fra

nce

(Fra

nce

)T

:A

irN

ewZ

eala

nd

,L

imit

ed(N

ewZ

eala

nd

)M

:S

aud

iB

asic

Ind

ust

ries

,C

orp

.(S

aud

iA

rabi

a)F

:S

berb

ank

(Ru

ssia

)

3 N:

Coa

lIn

dia

,L

imit

ed(I

nd

ia)

T:

Aer

oflo

t(R

uss

ia)

M:

Ch

ery

Au

tom

obil

e(C

hin

a)F

:C

aiss

ed

esD

épôt

set

Con

sign

atio

ns

(Fra

nce

)In

term

edia

te4 N

:G

DF

SU

EZ

(Fra

nce

)T

:A

erL

ingu

s(I

rela

nd

)M

:O

man

iF

iber

Op

tic

(Om

an)

F:

Cit

igro

up

(U.S

.)

5 N:

En

el,

Sp

A(I

taly

)T

:T

urk

ish

Air

lin

es(T

urk

ey)

M:

Erd

emir

(Tu

rkey

)F

:N

atio

nal

Ban

kof

Bah

rain

(Bah

rain

)

6 N:

Nor

skH

ydro

AS

A(N

orw

ay)

T:

Soc

iété

Lu

xem

bou

rgeo

ise

de

Nav

igat

ion

Aér

ien

ne

(Lu

xem

bou

rg)

M:

Avt

oVA

Z(R

uss

ia)

F:

TM

B(T

hai

lan

d)

Low

7 N:

Gal

pE

ner

gia

(Por

tuga

l)T

:U

nit

edA

rab

Sh

ipp

ing

Com

pan

y(K

uw

ait)

M:

Vol

ksw

agen

AG

(Ger

man

y)F

:H

ana

Fin

anci

alG

rou

p(S

outh

Kor

ea)

8 N:

En

ergi

asd

eP

ortu

gal,

SA

(Por

tuga

l)T

:K

LM

Roy

alD

utc

hA

irli

nes

(Net

her

lan

ds)

M:

Val

eoS

A(F

ran

ce)

F:

Ban

kL

eum

ile

-Isr

ael

(Isr

ael)

9 N:

Val

eS

A(B

razi

l)T

:D

azh

ong

Tra

nsp

orta

tion

(Ch

ina)

M:

Em

brae

r(B

razi

l)F

:R

osgo

sstr

akh

(Ru

ssia

)

Ind

ust

ries

:N

�n

atu

ral

reso

urc

es/e

ner

gy;

T�

tran

spor

tati

on;

M�

man

ufa

ctu

rin

g;F

�fi

nan

ce

One key argument for the finding that higherstate control hurts performance is that state owner-ship is typically associated with soft budget con-straints (Bai & Wang, 1998). Thus, the state willprovide support to a firm with chronic losses,which softens budget constraints and virtuallyeliminates the possibility of its going out of busi-ness or of being properly restructured (Davis, Halti-wanger, Jarmin, Lerner, & Miranda, 2011; Econo-mist, 2012c; Kornai, 1992). Such state support cancome directly from the government or indirectlyfrom government-controlled institutions (such asbanks or other SOEs) that provide loans and re-sources to the troubled business. Soft budget con-straints mean that a firm does not need to respondto the market as it continues to receive resources forcontinued operations (Sheng & Zhao, 2012). Easymoney often causes firms to overinvest in produc-tion equipment and other physical assets, such thatthey wind up with overcapacity (Burlingham,2012; Peng & Heath, 1996). They also tend to ignoremarket signals and many key technologies, partic-ularly during periods of technological ferment (Le-rner, 2008). The result is that soft budget con-straints can turn the focus of management awayfrom the market or keep firms on a technologicalpath that is becoming unviable (Kornai, Maskin, &Roland, 2003).

However, some of our cases appear to suggestthat state control, whether associated with stateownership or not, can result in good performance.Examining the three cells in Table 3 with the high-est levels of government control (cells 3, 6, and 9),we find that two of them—cells 3 and 9—have thehighest levels of return on investment (ROI). Stra-tegically, we could not determine whether this per-formance is the result of soft budget constraints interms of a longer-term outlook or other directlyconferred benefits, such as free land, which canalso represent a major subsidy to SOEs (Economist,2012d; Hsieh & Klenow, 2009).

The research surveyed and data gathered on thecase firms suggest that the impact of state supportmay be significant. For example, Caisse des Dépôtset Consignations is a French bank that describesitself as a state institution whose subsidiaries andaffiliates operate in the competitive sector. Thebank reported a profit for 2010. The largest amountof that income was from the increase in value ofequity in firms that the bank had invested in. Mostof these firms provided services to various levels ofthe government. These results can help researchersto understand how state-controlled firms can uti-

lize the resources the state offers to generate above-average profits or to achieve other goals, such asemployment levels, while minimizing the drag onproductivity (Hsieh & Klenow, 2009). Research inboth economics and strategic management has yetto clarify the balance between having financialslack and a longer-term outlook versus staying toolong with an investment or technological standardwhen enabled by soft budget constraints. The inter-action among these supports and other factors thatcharacterize SOEs suggest a rich topic for futureempirical investigation.

Macro Institutions: Institutional Development

Several studies have recognized the key role ofinstitutional development in the economic successof a country, both in terms of formal (Acemoglu &Robinson, 2012; North, 1990) and informal institu-tions (Godfrey, 2014; McCloskey, 1994, 2010;Mokyr, 2009). This impact partially derives fromsocietal norms that shape the actions of individualsand firms (Greif, 2006; Peng et al., 2009). The soci-etal norms in countries with a tradition of stronggovernment action will exercise stronger influenceover firms in terms of how they behave (Newman,2000). The ability of a society to develop newinstitutional structures that may be supportive ofprivate firms may be weakened by strong institu-tional inertia (Dacin, Goodstein, & Scott, 2002; Mc-Closkey, 2010; Ogilvie, 2011). Thus, the develop-ment of institutions in a country in terms ofsupporting SOEs versus private businesses is criti-cal to SOE performance.

We assessed the nature of institutional develop-ment to support private enterprise. Initially welooked at several sources regarding the variouscountries’ macroeconomic settings and institu-tional development. These ratings concern macroissues in the country, such as whether the countryhas clear, less intrusive, and more inclusive rulesfor doing business (Acemoglu & Robinson, 2012).While there are several economic ranking systemsavailable, here we employed a widely used rankingdeveloped by the Washington, DC–based HeritageFoundation. The Index of Economic Freedomranking system relies on 10 different commercialand economic factors: business freedom, trade free-dom, fiscal freedom, government spending free-dom, monetary freedom, investment freedom, fi-nancial freedom, property rights, freedom fromcorruption, and labor freedom. Each of these vari-

102 FebruaryThe Academy of Management Perspectives

ables describes the level of development of nationalinstitutions that support business.

As with any such measure, different sources willvary in their rankings. However, alternative rank-ing systems show broad agreement. Hong Kong,Singapore, and the United States tend to rankhigher on economic freedom than other countriesrepresented in our cases. The individual rank of agiven country may vary slightly, but the overallview of economic freedom typically does not varymuch in these sources. Thus, we employ the Indexof Economic Freedom for each economy in our 36cases, to determine the strength of institutions thatsupport business in each country.

From our examination of the cases, governmentcontrol in SOEs appears to be negatively correlatedwith the overall institutional development in sup-port of private enterprise. In other words, govern-ment control is more likely to occur in settings withlimited institutional development supporting busi-ness. Cell 1 of Table 3 represents low governmentcontrol and high government ownership. All firmsin the cell are in the top 10 economies that havedeveloped institutional support for private busi-ness, according to the Heritage Foundation. Simi-larly, as we look at cell 3, which represents firmswith high state ownership and control, three of thefour cases come from countries in the bottom thirdin terms of development of institutions to supportprivate business (India, China, and Russia). Look-ing deeper at individual firms, one easily sees thiskind of government intervention in firms such asthe Russian airline Aeroflot, which still looks forgovernment approval of key decisions, such as pur-chasing new aircraft. It is also interesting to notethat the level of government ownership of firmsdoes not correlate positively or negatively to insti-tutional development in support of private enter-prise. Thus, institutional development does notseem to be related to government ownership butseems to be related to government control.

We suggest a caveat that appears to moderate therelationship between the impact of governmentcontrol and economic freedom. The cases demon-strate that as the importance of an SOE’s productsincreases so does the level of governmental control.For example, cell 9 contains a mining firm (Vale)that many believe will ultimately provide greatbenefits to Brazil as offshore oil is developed. Thiscell also contains core industries such as the largestRussian insurance firm. If we look at the cells thatborder cell 9 (cells 6 and 8, which also reflect highlevels of government control), we continue to see

firms that have a disproportionate impact on theircountries, whether economically, strategically, orin terms of GDP and employment (McGregor,2012). Thus, ownership by the state may not behigh, but if the economic and strategic importanceof the industry or firm is great (such as with energyor steel), then the government is much more likelyto assert itself in the management of the firmthrough high levels of control, even when lackinghigh levels of ownership. This suggests that schol-ars should pursue such rich topics as the interac-tion between institutional development for privatebusiness and how that institutional developmentalso affects SOEs. In addition, the impact of thestrategic importance of an industry or firm on thenature of the relationship to the government ap-pears ripe for investigation. Scholars will need torecognize that different countries define differentindustries as strategic, and this will affect the insti-tutional logics facing state firms.

Micro Institutions: CEOs

Neoinstitutional theory argues that institutionsoperate not only at the macro level of analysis butalso at the micro level (Meyer et al., 2009; Scott,2014). Typically, neoinstitutional theory has morecommonly focused on the macro level. However,micro-level institutions shape values and percep-tions of how to do business in a given industry orregion (Wicks, 2001) while shaping key activitiessuch as innovation and several commercial conven-tions (McCloskey, 1994, 2010). Thus, individual ac-tivities can act to build or maintain institutions(Hobsbawm & Ranger, 1992; Nee & Opper, 2012).

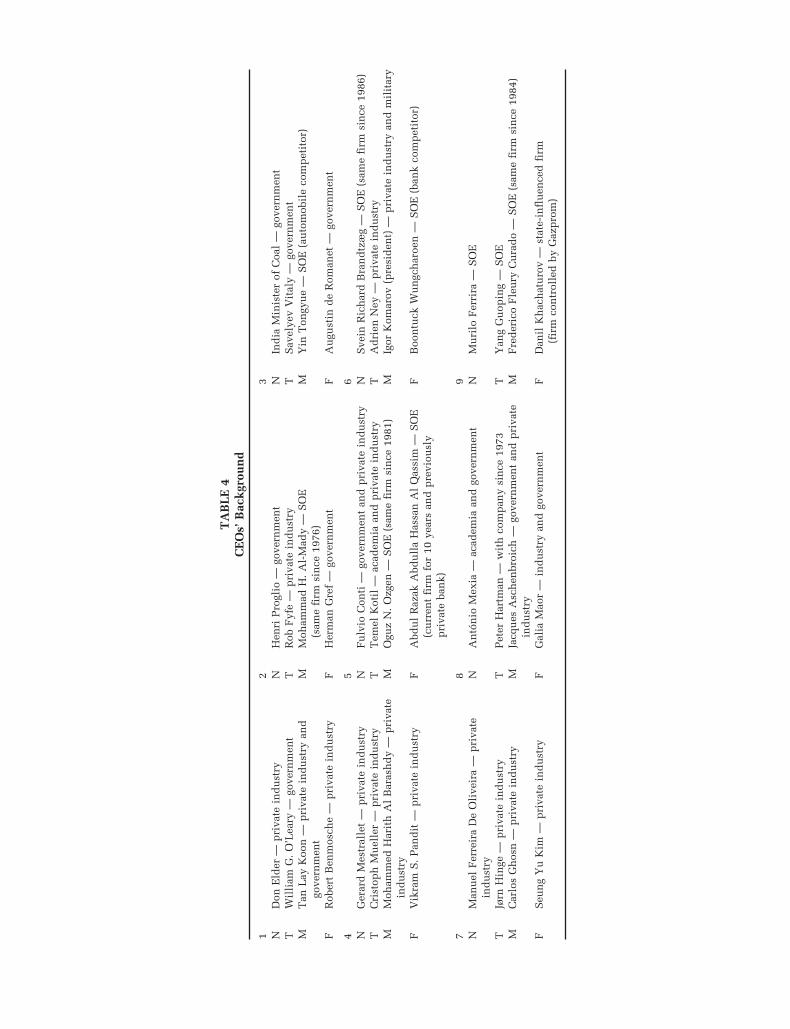

In SOEs, one important type of micro institutionis the office of the CEO, whose authority and mind-set are very important to firm operations. The back-ground and experience of the CEO of the firm iscritical in setting that mindset and driving key be-haviors (McCall, 1998). The main goal of (most)governments is job creation and stability, not nec-essarily economic efficiency. If the CEO of the SOEcomes from the government or has always workedfor the SOE sector, the CEO may be more likely toinherit a mindset that stresses job maintenance andoperations, not necessarily firm efficiency or stra-tegic orientation (Ahlstrom, 2014). The backgroundof such individuals encourages a mindset, or wayof doing things, that is consistent with that of typ-ical government processes and goals—but not nec-essarily with those of private enterprise (McCall,1998; Steinfeld, 1998). Because of this government

2015 103Bruton, Peng, Ahlstrom, Stan, and Xu

mindset, the CEO may willingly comply when agovernment official asks the SOE to acquire an-other firm, redistribute its profits to subsidize thegovernment’s social welfare objectives (e.g., fund-ing local schools or health care), or continue toexpand even in the face of unfavorable market orfactor market conditions or other problems (Lu,2006; Shi, Markoczy, & Stan, 2014).

Table 4 summarizes the backgrounds of the CEOsfor each of our case firms. The CEOs of firms on theleft side of the chart, where government control islow, almost always come from private industry. Onthe right side, where government control is high,we find it common that the executives come fromthe government, or have worked for SOEs consis-tently. To illustrate, in cell 6 of Table 4, the CEO ofthree of the four cases came from some form of gov-ernment background, having previously worked ei-ther for an SOE or for the military.

The institutionalization of new practices requiressome disassociation with the historical context(Barley & Tolbert, 1997). The expectation is that incases where there is a CEO who has worked for thestate or for an SOE and a high level of governmentcontrol, the two may act to reinforce the concern forissues other than economic performance. The CEOwho has worked for the state brings a mindsetconsistent with state goals and not necessarily withthe profit-maximization goals associated with pri-vate firms. The focus of the government and of theCEO (who has a state background) tends to be onthe maintenance of employment and other socialconcerns rather than necessarily firm efficiency(Baron & Kreps, 1999; McCall, 1998). As a result,government control can negatively affect the SOE’seconomic performance or may push the SOE to-ward production maximization as opposed to inno-vation and ROI (Economist, 2012a; Lerner, 2008).

Micro institutions are similar to macro institu-tions in that both have the ability to not only sup-port but also to change and shape institutional de-velopment (Barley & Tolbert, 1997; Greif, 2006;Steinfeld, 2010). Thus, we expect CEOs whosebackgrounds are not in government or in the SOEsector to have more skills and experience to re-shape SOEs to be more innovative and market ori-ented (McCall, 1998). Similarly, CEOs can take overSOEs that have historically had wide latitude tooperate independently to bring these firms backinto greater alignment with the government’s goalsor turn them around (Bruton, Ahlstrom, & Wan,2001). To illustrate, Valeo, a French auto partsmanufacturer in cell 8, changed its CEO in 2009.

The goal was to bring in a CEO who combined bothgovernment experience and private industry back-ground to better manage the firm and address itsstrategic challenges. The new CEO replaced theprevious one, who had had only government expe-rience. The government and other investors wantedsomeone who would have the ability to better turnthe firm around in the given financial crisis, andcut hours or employment if necessary to increasethe firm’s ability to weather the financial crisis.SOE top management attributes and experienceand their link to SOE action and performance ispotentially a rich topic for future research in man-agement (Bruton et al., 2003; Maheshwari & Ahl-strom, 2004).

DISCUSSION

Much of the limited previous research on SOEshas largely assumed a direct correlation betweenstate ownership and control as well as a dichotomybetween state owned and private firms. These as-sumptions appear unwarranted. Today hybrid or-ganizations that mix ownership and control are thedominant form of SOE organizations. Building onthis recognition allows a far more detailed and bet-ter-informed analysis of SOEs than has occurred inthe past. Our first contribution highlights the hy-brid nature of many of today’s SOEs, which areimportant but remain underexplored. Extendingtransaction cost, agency, and neoinstitutional the-ories, this research with an SOE focus also has thepotential to push the frontiers of these theoriesfurther by focusing attention on factors that medi-ate and moderate SOE strategy, structure, and out-comes. For example, the hybrid nature of SOEs inmany countries suggests ways in which state firmscan balance multiple stakeholders effectively interms of legitimacy building with the governmentwhile also seeking to maximize profit for share-holders. Alternatively, SOEs also offer insights onhow strategy must be viewed differently whenprofit maximization is not the top priority.

Moreover, this paper adds to the literature onvarieties of capitalism research (Hall & Soskice,2001). Much past theory and empirical work onvarieties of capitalism has examined the impor-tant differences among national economies andtheir institutions, and the impact of these differ-ences on economies as a whole (Hall & Soskice,2001; Whitley, 1998). This literature has gener-ally paid little attention to state ownershipand generally not at the firm level, despite

104 FebruaryThe Academy of Management Perspectives

TA

BL

E4

CE

Os’

Bac

kgr

oun

d

12

3N

Don

Eld

er—

pri

vate

ind

ust

ryN

Hen

riP

rogl

io—

gove

rnm

ent

NIn

dia

Min

iste

rof

Coa

l—

gove

rnm

ent

TW

illi

amG

.O

’Lea

ry—

gove

rnm

ent

TR

obF

yfe

—p

riva

tein

du

stry

TS

avel

yev

Vit

aly

—go

vern

men

tM

Tan

Lay

Koo

n—

pri

vate

ind

ust

ryan

dgo

vern

men

tM

Moh

amm

adH

.A

l-M

ady

—S

OE

(sam

efi

rmsi

nce

1976

)M

Yin

Ton

gyu

e—

SO

E(a

uto

mob

ile

com

pet

itor

)

FR

ober

tB

enm

osch

e—

pri

vate

ind

ust

ryF

Her

man

Gre

f—

gove

rnm

ent

FA

ugu

stin

de

Rom

anet

—go

vern

men

t

45

6N

Ger

ard

Mes

tral

let

—p

riva

tein

du

stry

NF

ulv

ioC

onti

—go

vern

men

tan

dp

riva

tein

du

stry

NS

vein

Ric

har

dB

ran

dtz

æg

—S

OE

(sam

efi

rmsi

nce

1986

)T

Cri

stop

hM

uel

ler

—p

riva

tein

du

stry

TT

emel

Kot

il—

acad

emia

and

pri

vate

ind

ust

ryT

Ad

rien

Ney

—p

riva

tein

du

stry

MM

oham

med

Har

ith

Al

Bar

ash

dy

—p

riva

tein

du

stry

MO

guz

N.

Ozg

en—

SO

E(s

ame

firm

sin

ce19

81)

MIg

orK

omar

ov(p

resi

den

t)—

pri

vate

ind

ust

ryan

dm

ilit

ary

FV

ikra

mS

.P

and

it—

pri

vate

ind

ust

ryF

Abd

ul

Raz

akA

bdu

lla

Has

san

Al

Qas

sim

—S

OE

(cu

rren

tfi

rmfo

r10

year

san

dp

revi

ousl

yp

riva

teba

nk)

FB

oon

tuck

Wu

ngc

har

oen

—S

OE

(ban

kco

mp

etit

or)

78

9N

Man

uel

Fer

reir

aD

eO

live

ira

—p

riva

tein

du

stry

NA

ntó

nio

Mex

ia—

acad

emia

and

gove

rnm

ent

NM

uri

loF

erri

ra—

SO

E

TJø

rnH

inge

—p

riva

tein

du

stry

TP

eter

Har

tman

—w

ith

com

pan

ysi

nce

1973

TY

ang

Gu

opin

g—

SO

EM

Car

los

Gh

osn

—p

riva

tein

du

stry

MJa

cqu

esA

sch

enbr

oich

—go

vern

men

tan

dp

riva

tein

du

stry

MF

red

eric

oF

leu

ryC

ura

do

—S

OE

(sam

efi

rmsi

nce

1984

)

FS

eun

gY

uK

im—

pri

vate

ind

ust

ryF

Gal

iaM

aor

—in

du

stry

and

gove

rnm

ent

FD

anil

Kh

ach

atu

rov

—st

ate-

infl

uen

ced

firm

(fir

mco

ntr

olle

dby

Gaz

pro

m)

the relevance of the state sector and the impor-tance of understanding its governance and per-formance. Giving additional attention to thestate-owned sector and the range of organizationalstructures that have now developed, particularly atthe firm level, will further add to the varieties ofcapitalism literature.