Embed Size (px)

Citation preview

© 2009 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein may be the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified,or distributed in any form or manner without the prior written permission of Experian Information Solutions, Inc.

State of the Automotive Finance MarketThird Quarter 2009

Melinda Zabritski, Director of Automotive Credit

2© 2009 Experian Information Solutions, Inc. All rights reserved.

Presentation Overview

Third quarter 2009 Automotive Finance Market Overview► All open automotive loans by risk tier► Automotive loan delinquencies► Source: Experian-Oliver Wyman Market Intelligence Reports. For more

information, please visit www.marketintelligencereports.comAutomotive Financing in the third quarter of 2009► Financing by geography► New versus Used vehicles► Top Lender report► Loan characteristics► Source: Experian Automotive

National Vehicle Database sourced from DMV title registrations. For more information, please visit www.autocount.com

Risk TiersCategory Scorex

PLUSSMVantageScore

Super Prime 740+ 801 – 990

Prime 680 – 739 701 – 800

Nonprime 620 – 679 641 – 700

Subprime 550 – 619 601 – 640

Deep Subprime <550 501 - 600

© 2009 Experian Information Solutions, Inc. All rights reserved. 3

Automotive Finance MarketHow has the market been changing?

-0.09%

2.25%

0.35%

-3.74%

-1.33%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

Super Prime Prime Nonprime Subprime Deep Subprime

Change in Risk Distribution from 3Q2008

37.0%37.0%37.9%

23.9%23.4%23.8%

15.3%15.2%15.1%

8.8%9.1%9.0%

15.1%15.3%14.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q093Q083Q07

Risk Distribution of Open Auto Loans

Super Prime Prime Nonprime Subprime Deep Subprime

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2009 Experian Information Solutions, Inc. All rights reserved. 4

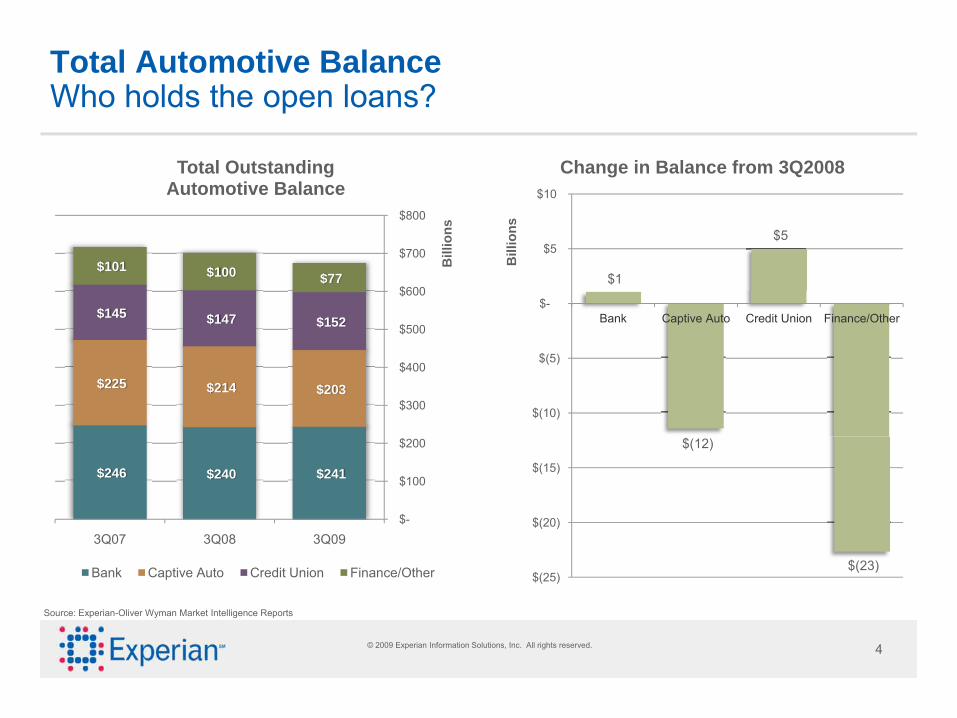

Total Automotive BalanceWho holds the open loans?

$241 $240 $246

$203 $214 $225

$152 $147 $145

$77 $100 $101

$-

$100

$200

$300

$400

$500

$600

$700

$800

3Q093Q083Q07

Bill

ions

Total Outstanding Automotive Balance

Bank Captive Auto Credit Union Finance/Other

$1

$(12)

$5

$(23)$(25)

$(20)

$(15)

$(10)

$(5)

$-

$5

$10

Bank Captive Auto Credit Union Finance/Other

Bill

ions

Change in Balance from 3Q2008

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2009 Experian Information Solutions, Inc. All rights reserved. 5

Recent Automotive Delinquency: 30 Day DelinquencyHow are automotive loans performing?

2.18%

3.04%

1.43%

6.19%

2.86%2.52%

3.24%

1.65%

6.55%

3.14%3.07%3.52%

1.72%

6.55%

3.32%

0%

1%

2%

3%

4%

5%

6%

7%

Banks Captive Auto Credit Union Finance/Other TOTAL

30 Day Delinquency

3Q07 3Q08 3Q09

5.8%

-0.1%

8.7%

4.5%

21.7%

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2009 Experian Information Solutions, Inc. All rights reserved. 6

0.65% 0.60%

0.38%

1.96%

0.77%0.77%

0.59%0.42%

2.02%

0.84%0.89%0.77%

0.49%

2.33%

0.95%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Bank Captive Auto Credit Union Finance/Other TOTAL

60 Day Delinquency

3Q07 3Q08 3Q09

Recent Automotive Delinquency: 60 Day DelinquencyHow are automotive loans performing?

14.5% 13.4%29.2%

16.7%

15.5%

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2009 Experian Information Solutions, Inc. All rights reserved. 7

Recent 30 and 60 Day Automotive DelinquencyWhat’s at stake?

$7,104

$2,026

$6,913

$1,524

$2,472

$687

$5,286

$1,803

$-

$5,000

$10,000

$15,000

$20,000

$25,000

30 Day Delinquency 60 Day Delinquency

Mill

ions

Balance of 3Q2009 Delinquent Auto Loans

Bank Captive Auto Credit Union Finance/Other

$995

$141

$332 $281

$138 $124

$(1,550)

$(147)$(85)

$400

$(2,000)

$(1,500)

$(1,000)

$(500)

$-

$500

$1,000

$1,500

30 Day Delinquency 60 Day Delinquency

Mill

ions

Change in Delinquency from 3Q2008

Bank Captive Auto Credit Union Finance/Other TOTAL

Source: Experian-Oliver Wyman Market Intelligence Reports

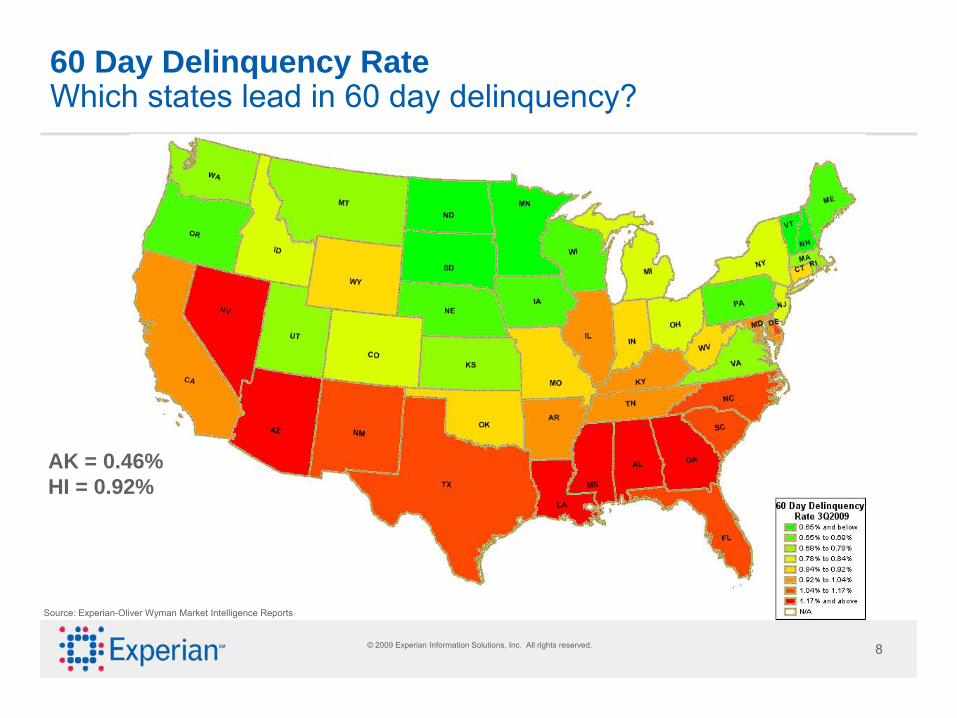

© 2009 Experian Information Solutions, Inc. All rights reserved. 8

60 Day Delinquency Rate Which states lead in 60 day delinquency?

Source: Experian-Oliver Wyman Market Intelligence Reports

AK = 0.46%HI = 0.92%

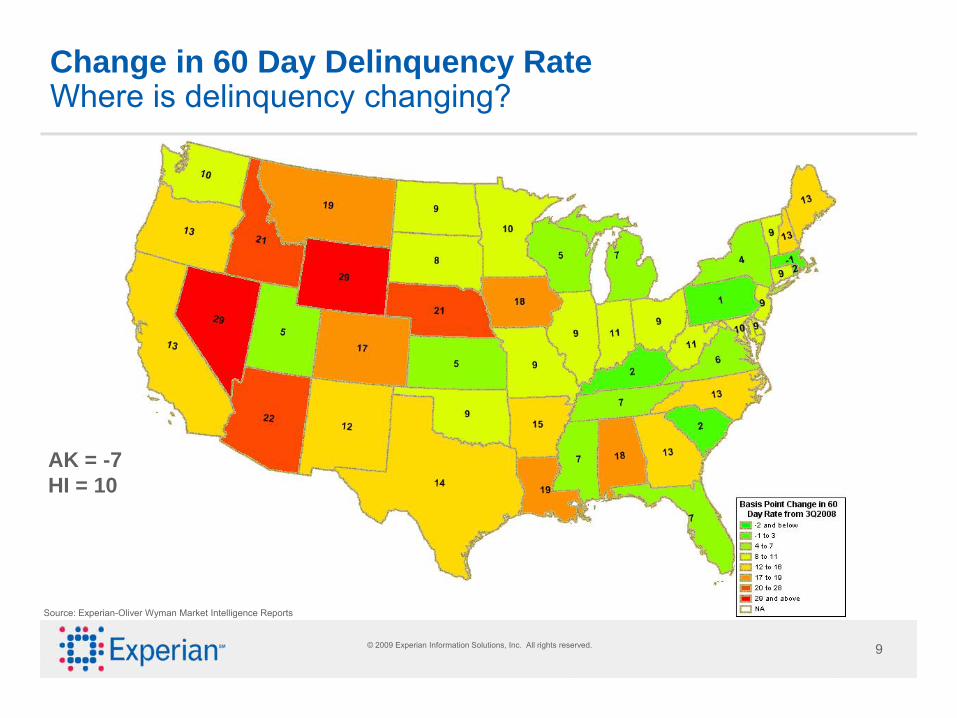

© 2009 Experian Information Solutions, Inc. All rights reserved. 9

Change in 60 Day Delinquency Rate Where is delinquency changing?

Source: Experian-Oliver Wyman Market Intelligence Reports

AK = -7HI = 10

© 2009 Experian Information Solutions, Inc. All rights reserved. 10

AUTOMOTIVE FINANCINGTHIRD QUARTER 2009

© 2009 Experian Information Solutions, Inc. All rights reserved. 11

Average Credit Score on New Vehicles Financed 3Q2009Which states have higher credit scores?

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 12

Average Credit Score on Used Vehicles Financed 3Q2009Which states have higher credit scores?

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 13

Quarterly Financing for New and Used VehiclesHow has credit changed for new and used financing?

14.4%

-3.3%

-12.8%

-21.0%

-12.6%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Super Prime

Prime Nonprime Subprime Deep Subprime

Change in Vehicle Financing from 3Q2008

52.71%46.06%42.84%

13.29%13.74%

13.76%

12.15%13.94%

14.48%

10.55%13.34%15.32%

11.29%12.92%13.60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q20093Q20083Q2007

Vehicle Financing by Credit Tier

Super Prime Prime Nonprime Subprime Deep Subprime

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 14

Quarterly Financing for New and Used VehiclesHow has financing on vehicles changed?

42.08% 39.24% 35.64% 38.90% 41.17% 36.28% 31.85% 36.02%42.77%

57.92% 60.76% 64.36% 61.10% 58.83% 63.72% 68.15% 63.98%57.23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q2007 4Q2007 1Q2008 2Q2008 3Q2008 4Q2008 1Q2009 2Q2009 3Q2009

Market Share by Vehicle Type

New Used

-2.72%

3.89%

© 2009 Experian Information Solutions, Inc. All rights reserved. 15

Credit Scores on Vehicle FinancingHow have scores changed?

749 749 753 755762 766

773 774 775

663 661653

668 670 668661

677684

580

600

620

640

660

680

700

720

740

760

780

800

3Q2007 4Q2007 1Q2008 2Q2008 3Q2008 4Q2008 1Q2009 2Q2009 3Q2009

Average Credit Score

New Score Used Score

14

13

© 2009 Experian Information Solutions, Inc. All rights reserved. 16

Quarterly Financing for New and Used VehiclesHow has credit changed for new and used financing?

Super Prime

Prime

Nonprime

Subprime

Deep Subprime

Source: Experian Automotive

69.88%63.15%58.51%

13.21%14.45%14.52%

9.79%12.05%12.75%5.66%7.98%10.29%1.46%2.37%3.93%

0%

20%

40%

60%

80%

100%

3Q20093Q20083Q2007

New Vehicle Financing

39.89%34.11%31.46%

13.35%13.25%13.20%

13.92%15.26%15.73%

14.20%17.09%18.98%

18.64%20.29%20.63%

0%

20%

40%

60%

80%

100%

3Q20093Q20083Q2007

Used Vehicle Financing

10.7%

-8.6%-18.8%

-29.1%-38.3%

16.9%

0.8%

-8.7%-16.9% -8.1%

-50%-40%-30%-20%-10%

0%10%20%

Super Prime Prime Nonprime Subprime Deep Subprime

Change in Vehicle Financing from 2Q2008

CHANGE - NEW CHANGE - USED

© 2009 Experian Information Solutions, Inc. All rights reserved. 17

Used Car Financing by Dealer TypeHow is financing changing by dealer type?

Source: Experian Automotive

30.85%30.10%27.62%

69.15%69.90%72.38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q20093Q20083Q2007

Used Vehicle Financing by Dealer Type

Independent Used Franchise Used

612605606

716

698685

540

560

580

600

620

640

660

680

700

720

740

3Q20093Q20083Q2007

Average Credit Scores on Used Vehicle Financing

Independent Used Franchise Used

-1.07

2.50%

18

7

© 2009 Experian Information Solutions, Inc. All rights reserved. 18

Credit Distribution by Dealer TypeHow has dealer type changed by credit mix?

48.03%

21.62%

15.22%

9.18%

14.64%

12.31%

12.46%

18.09%

9.64%

38.81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Franchise Used Independent Used

Used Vehicle Risk Distributionby Dealer Type

Super Prime Prime Nonprime Subprime Deep Subprime

18.34%

1.09%

-10.15%

-23.11%

-2.73%

13.41%

1.39%

-4.14%

-5.54%

-2.73%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Super Prime Prime Nonprime Subprime Deep Subprime

Change in Used Financing from 3Q2008

Franchise Change Independent Change

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 19

Top 20 Lenders by Market ShareWho gained or lost share?

7.2% 6.3% 5.0% 4.6% 3.6% 3.3% 2.3% 1.9% 1.7% 1.4% 1.4% 1.2% 1.1% 0.9% 0.9% 0.8% 0.7% 0.7% 0.7% 0.6%

93.3%

8.4%

41.1%

-19.6%-25.3%-21.1%

7.1% 12.4%

36.0%

-12.8%

81.3%

48.2%

21.5%

-30.6%

77.6%

10.5%

29.6%

-9.3%

12.1%

121.4%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Top 20 Lenders By Market Share: Total Loan

3Q2009 Share Change in Share from 3Q08

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 20

Top 20 New Lenders by Market ShareWho gained or lost share on New Vehicle Financing?

11.2% 11.1% 9.1% 7.1% 6.9% 3.9% 3.7% 3.3% 2.0% 1.8% 1.6% 1.5% 1.5% 1.3% 1.2% 1.2% 1.2% 1.1% 1.0% 1.0%

10.1%

129.5%

-5.0%-12.0%

-32.3%

103.1%

65.6%

-23.0%

51.9%

75.2%

113.0%

-8.4% -9.1%

84.5%

103.3%

-22.0%-2.5%

35.9%34.2%20.3%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0%

2%

4%

6%

8%

10%

12%

Top 20 New Lenders by Market Share

3Q09 Share Change in Share from 3Q08

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 21

Top 20 Used Lenders by Market ShareWho gained or lost share on Used Vehicle Financing?

5.7% 4.5% 3.0% 1.8% 1.6% 1.3% 1.2% 1.2% 1.2% 1.1% 1.1% 1.1% 1.0% 1.0% 0.9% 0.9% 0.8% 0.8% 0.7% 0.6%

24.6%

50.7%

0.7%7.0%

-51.2%

-2.2%

67.6%

-29.7%

64.3%

-1.8%9.1%

34.2%

6.4%

-21.1%-20.5%

19.4%

36.8%42.6%

-5.5%

-49.6%

-60%

-40%

-20%

0%

20%

40%

60%

80%

0%

1%

2%

3%

4%

5%

6%

7%

Top 20 Used Auto Lenders by Market Share

3Q09 Share Change in Share from 3Q08

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 22

Top 20 Subprime/Nonprime LendersWho’s winning in the high risk space?

6.9% 5.7% 5.6% 5.5% 3.7% 3.7% 2.9% 2.1% 1.5% 1.2% 1.1% 0.9% 0.9% 0.9% 0.9% 0.8% 0.6% 0.5% 0.5% 0.5%

298.42%

505.38%

270.96%

461.93%

150.09%

259.42%231.32%

305.69%

115.13%

402.96%

114.90%

511.63%

430.36%

209.14%168.12%

445.21%

-28.05%

437.89%

292.05%

-100%

0%

100%

200%

300%

400%

500%

600%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Top 20 Subprime/Nonprime Lenders

3Q09 Share Change in Share from 3Q08

6000+%

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 23

Vehicle Financing and Credit ScoresHow has financing changed by credit score?

• High risk segments experiencing greater shifts in amount financed

• Deep Subprime decreased $1,976 on New financing

• Subprime decreased $1,376 on Used financing• Deep Subprime finance on average $8,545 more on

New loans than Used• Super Prime Used financing experienced the only

increase ($114)

$22,317 $23,555 $24,759 $25,307 $23,750

$20,341 $21,561 $22,936 $23,688 $22,623

$10,000

$15,000

$20,000

$25,000

$30,000

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Amount Financed on New Vehicles

3Q2008 3Q2009

$13,076

$15,020$15,832

$16,734 $16,871

$11,796

$13,644$14,855

$16,223

$16,986

$10,000

$12,000

$14,000

$16,000

$18,000

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Amount Financed on Used Vehicles

3Q2008 3Q2009

-$1,976 -$1,994-$1,824

-$1,619

-$1,128-$1,280 -$1,376-$977

-$511

$114

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$

$500

Deep Subprime

Subprime Nonprime Prime Super Prime

Change in Average Amount Financed

CHANGE - NEW CHANGE - USED

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 24

Vehicle Payments and Credit ScoresHow has monthly payment change by credit score?

• Average monthly payments decreased for all risk segments except Super Prime Used financing (up $3)

• Greatest decreases in New payments were seen in the higher risk segments

• At most a $10 difference is seen across New payments by risk while Used payments show more differentiation

$465 $462$455 $450

$444

$431 $428 $424 $423 $421

$400$410$420$430$440$450$460$470

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Monthly Payment on New Vehicles

3Q2008 3Q2009

$355 $352

$335$330 $331

$343$334

$320$325

$334

$300

$310

$320

$330

$340

$350

$360

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Monthly Payment on Used Vehicles

3Q2008 3Q2009

-$34 -$34-$31

-$26-$23

-$12-$18

-$15

-$6

$3

-$40-$35-$30-$25-$20-$15-$10-$5

$$5

Deep Subprime

Subprime Nonprime Prime Super Prime

Change in Average Monthly Payment

CHANGE - NEW CHANGE - USED

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 25

Interest Rate and Credit ScoresHow does rate change by credit score?

• Highest rates are seen in the highest risk segments• Rates increased in higher risk segments• Nonprime Used financing experienced the greatest

decrease in rates (27 bps)• Used rates are 173-225 bps higher than New rates

within the same risk segment

13.49%

11.21%

8.18%6.28%

4.88%

14.00%

11.42%

8.16%6.24%

4.80%

4%

6%

8%

10%

12%

14%

16%

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Rate on New Vehicles

3Q2008 3Q2009

16.04%14.31%

10.91%

8.48%6.63%

16.25%

14.24%

10.64%

8.32%6.54%

5%

7%

9%

11%

13%

15%

17%

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Rate on Used Vehicles

3Q2008 3Q2009

51

21

(2) (4) (8)

21

(6)(27)

(16) (9)(40)

(20)

-

20

40

60

Deep Subprime

Subprime Nonprime Prime Super Prime

Change in Average Rate(Basis Points)

CHANGE - NEW CHANGE - USED

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 26

Vehicle Term and Credit ScoresHow has term change by credit score?

• Steady drop in term across all risk segments for both New and Used financing

• High risk Used financing saw significant decreases in term (-4.29 months in Deep Subprime)

• Super Prime New loans average 1.8 months longer term than Used; Deep Subprime average 20.4 months shorter on Used than New loans

68.21 68.69 67.9266.74

61.43

67.36 67.76 66.9065.67

60.88

56

58

60

62

64

66

68

70

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Term on New Vehicles

3Q2008 3Q2009

51.2559.04 60.49 61.48 59.54

46.9655.53 58.48 60.09 59.08

0

10

20

30

40

50

60

70

Deep Subprime

Subprime Nonprime Prime Super Prime

Average Term on Used Vehicles

3Q2008 3Q2009

(0.85) (0.94) (1.03) (1.07)(0.55)

(4.29)

(3.52)

(2.01)(1.39)

(0.46)

(5.00)(4.50)(4.00)(3.50)(3.00)(2.50)(2.00)(1.50)(1.00)(0.50)

-Deep

SubprimeSubprime Nonprime Prime Super Prime

Change in Average Term

CHANGE - NEW CHANGE - USED

Source: Experian Automotive

© 2009 Experian Information Solutions, Inc. All rights reserved. 27

Third Quarter 2009 In Summary

Relatively steady credit quality in year-over-year comparisonOverall balances have declined to just over $673 billion (-4%)Steady increase in delinquency rates and balances with 30-day balances decreasingNew originations dominating in the Prime+ market (66%) up 10%► Scores on both new and used vehicles continue to increase► Over 83% of new buyers are prime+► Over 53% of used buyers are prime+

Used financing dipped in year-over-year comparisonFinanced amounts and monthly payments dropped year-over-yearRates adjusted by risk while terms decreased in all risk segments

© 2009 Experian Information Solutions, Inc. All rights reserved. 28

Questions?

Thank you for attending our Web seminar

© 2009 Experian Information Solutions, Inc. All rights reserved. 29© 2009 Experian Information Solutions, Inc. All rights reserved.Experian Public.