Embed Size (px)

Citation preview

Accounting for and Tax TreatmentAccounting for and Tax TreatmentAccounting for and Tax Treatment Accounting for and Tax Treatment of Startof Start--up and Development Costsup and Development Costs

Tim Tim WilhelmyWilhelmyDeloitte & Touche LLPDeloitte & Touche LLP

RupeshRupesh VadapalliVadapalliDeloitte Tax LLPDeloitte Tax LLP

AgendaAgenda

• Accounting Treatment of Start-up and DevelopmentAccounting Treatment of Start up and Development Costs

• Tax Treatment of Start-up and Development Costs– Overview of Project Development Activities– Start-up Costs

O i ti l d S di ti C t– Organizational and Syndication Costs– Expansion Costs– Transaction CostsTransaction Costs

Accounting Treatment of gStart-up and Development Costs

Start-up and Development CostsAcco nting TreatmentAccounting Treatment

• Start-up costs are specifically addressed by ASCStart up costs are specifically addressed by ASC 720-15 (formerly Statement of Position 98-5, Reporting on the Cost of Start-Up Activities)– Other literature addressing start-up costs includes

ASC 835-20, ASC 360-20, ASC 970-10 and ASC 805 (formerly FASB Statements 34 66 67 and141805 (formerly FASB Statements 34, 66, 67 and141, respectively)

– ASC 720-15 requires start-up costs to be expensed SC 0 5 equ es s a up cos s o be e pe sedas incurred

Start-up and Development CostsAcco nting DefinitionAccounting Definition

• Start-up activities are defined broadly as activitiesStart up activities are defined broadly as activities related to any of the following: – Opening a new facilityp g y– Introducing a new product or service– Conducting business in a new territory– Conducting business with an entirely new class of

customers or beneficiary

Start p and De elopment CostsStart-up and Development Costs

• Start-up activities include activities related toStart up activities include activities related to organizing a new entity

• Start-up activities also include costs related to pperforming feasibility studies and should be expensed as incurred

Start p and De elopment CostsStart-up and Development Costs

Start-up activities do not include:Start up activities do not include:• Routine ongoing efforts to refine, enrich, or

otherwise improve upon the qualities of an existing p p q gproduct, service, process or facility

• Costs of acquiring or constructing long-lived assets and getting them ready for their intended uses

• Costs of acquiring or producing inventory

Note: This list is not meant to be inclusive of all ti iti th t t id d t t ti itiactivities that are not considered start-up activities

Start up and Development CostsEnd of Capitali ation PeriodEnd of Capitalization Period

• Issue- When does a cost cease to exhibit theIssue When does a cost cease to exhibit the characteristics of a start-up cost?

• Answer: Determining whether a cost is a start-up g pactivity or a development or construction activity is a matter of judgment based upon case specific f t d i tfacts and circumstances

Accounting for Start-up and De elopment Costs O er ieDevelopment Costs – Overview

• Project costs should be capitalized whenProject costs should be capitalized when management believes a specific project is probable (i.e., 50% likelihood) of completion– Conclusion on probability should be based on

achievements of milestones or a combination of milestones and a company’s historical experiencemilestones and a company s historical experience. Examples may include:• Receipt of governmental approval or permitsece p o go e e a app o a o pe s• Execution of power purchase agreement (unless

merchant facility)• Agreement for acquisition of significant plant

components

Business Initiation CostsAcco nting TreatmentAccounting Treatment

• Costs incurred in the normal course of starting aCosts incurred in the normal course of starting a business or project

• Business initiation costs must be expensed prior to p pindentifying a feasible project

Examples of Business Initiation CostsAcco nting TreatmentAccounting Treatment

• Bid preparationBid preparation• Internal costs for analysis, legal research and early

stage engineeringg g g• Costs of a development office• Organizational costs of new legal entitiesg g

Development CostsAcco nting TreatmentAccounting Treatment

• Costs incurred prior to initiating an acquisition orCosts incurred prior to initiating an acquisition or construction of a project, but after initiation

• If not related to a specific property these costs p p p yshould be expensed

• If related to a specific project which management has concluded is probable of completion, costs should be capitalized as project development cost

Development CostsAcco nting E amplesAccounting Examples

• Property acquisition feesProperty acquisition fees• Cost of permits and licenses• Legal and other professional feesLegal and other professional fees• Internal costs related to contract negotiation

Start p and De elopment CostsStart-up and Development Costs

• Construction costsConstruction costs– Costs incurred which are necessary to get the asset

ready for its intended usey– Substantially all costs incurred in the construction

phase are capitalizable– Capitalization should cease at commercial

operations date

Construction of Power Plants E amples of Constr ction Period CostsExamples of Construction Period Costs

• EPC contractor feesEPC contractor fees• Interest paid to third parties• Test power costs (and related income) (for shortTest power costs (and related income) (for short

periods of time)• Internal costs directly related to the projecty p j• Property tax incurred during the construction period• Bonuses to development teamp• Development fees (under certain circumstances)

Late Stage Development CostsAcco nting Treatment and E amplesAccounting Treatment and Examples

• Late stage development costs are not capitalizedLate stage development costs are not capitalized for financial reporting purposes

• Examples:p– Costs to train employees and contractors (unless

complex and unique facilities– Costs incurred to fine tune equipment after

commercial operations dateCosts incurred to negotiate contracts related to– Costs incurred to negotiate contracts related to operations

Construction of Power Plants Capitali ation Iss esCapitalization Issues

• Should costs be capitalized or expensed/deductedShould costs be capitalized or expensed/deducted currently?

• If costs are capitalized, are they a separate p , y pintangible or part of the grant/ITC-eligible plant basis?

• What is the amortization period of any intangible assets created during the start-up period?

Tax Treatment: Overview ofProject Development Activities

Timeline of Project Development Acti itiesActivities

Start-up Phase

Development Phase

Operational PhasePhase

• PPA negotiationLand option

Phase

• Design and engineering of

Phase

• Placing facility in service• Land option

negotiations• Research and

development of

engineering of plant

• Site and ground-work

service• Producing power

for sale under PPAdevelopment of

technologieswork

• Construction of facilities

PPA• Ongoing

maintenance activities

Start p Phase O er ieStart-up Phase Overview

• Start-up phaseStart up phase– Deductible costs are capitalized as start-up costs

under Section 195 if the Company is not engaged in p y g gactive trade or business• Unless expressly deductible

– There may be certain costs that are properly capitalizable to the basis of tangible or intangible assets under Sections 263 and 263Aassets under Sections 263 and 263A• Tangible assets (e.g., land)• Intangible assets (e.g., PPA, certain licenses)g ( g )

De elopment Phase O er ieDevelopment Phase Overview

• Development phaseDevelopment phase– If the Company is engaged in active trade or

business at this phase, ordinary and necessary p y ybusiness expenses are deductible under Section 162Majority of costs typically are related to construction– Majority of costs typically are related to construction of project and capitalized to basis of tangible or intangible assets under Sections 263 and 263Ag• Direct costs (e.g., materials, labor)• Indirect costs (e.g., overheads, engineering)• Interest capitalization

Operational Phase O er ieOperational Phase Overview

• Operational phaseOperational phase– Company is engaged in active trade or business and

ordinary and necessary business expenses are y y pdeductible under Section 162 (e.g., repairs and maintenance costs)If company is constructing other projects the costs– If company is constructing other projects, the costs attributable to the intangible basis of those projects are capitalized under Sections 263 and 263Ap

Other Common De elopment Acti itiesOther Common Development Activities

• Companies developing alternative energy projectsCompanies developing alternative energy projects also commonly engage in other activities for which the associated costs have a specific tax treatment– Organization of business– Syndication of partnership– Expansion of existing business– Acquisition or reorganization of existing business

Tax Treatment: Start-Up Costs

Tax Treatment of Start-up CostsO er ieOverview

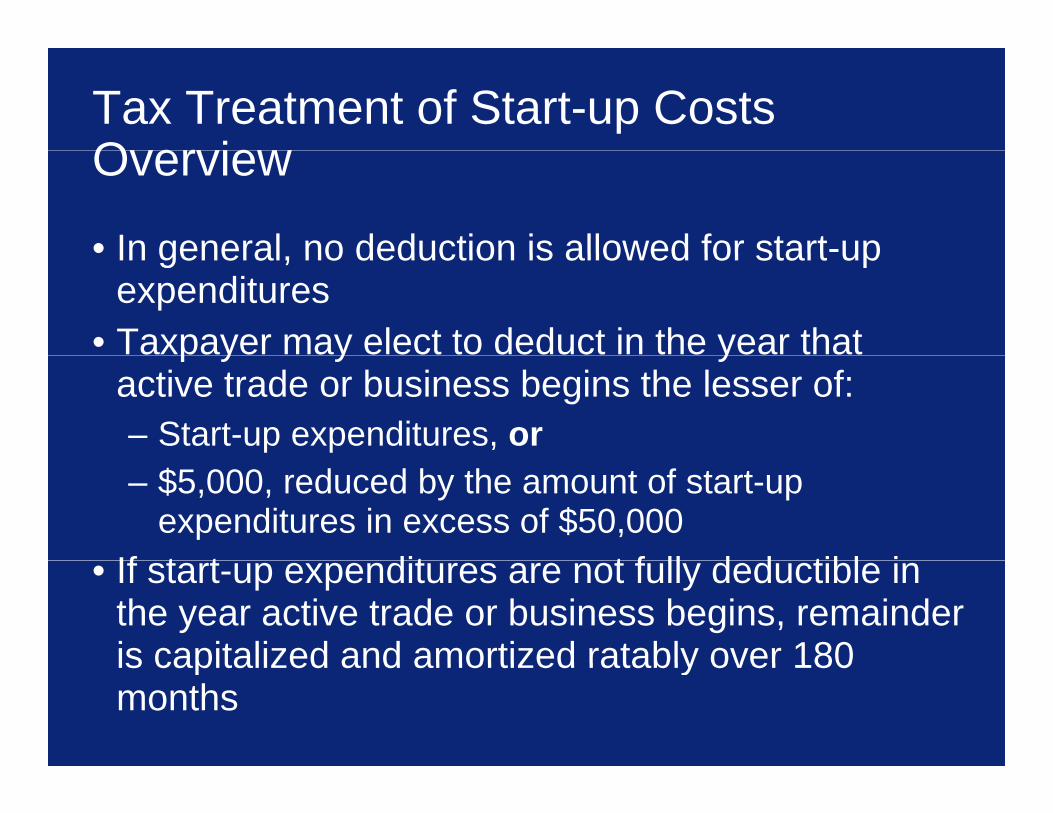

• In general no deduction is allowed for start-upIn general, no deduction is allowed for start up expenditures

• Taxpayer may elect to deduct in the year that p y y yactive trade or business begins the lesser of: – Start-up expenditures, or – $5,000, reduced by the amount of start-up

expenditures in excess of $50,000If t t dit t f ll d d tibl i• If start-up expenditures are not fully deductible in the year active trade or business begins, remainder is capitalized and amortized ratably over 180is capitalized and amortized ratably over 180 months

Tax Treatment of Start-up CostsStat tor Constr ctionStatutory Construction

• Section 195(a) provides, in general, that no deduction shallSection 195(a) provides, in general, that no deduction shall be allowed for start-up expenditures

• Section 195(b)(1) provides that a taxpayer may elect to ded ct in the ta able ear that the acti e trade or b sinessdeduct in the taxable year that the active trade or business begins the lesser of: 1) Its start-up expenditures or ) p p2) $5,000, reduced (but not below zero) by the amount by

which such start-up expenditures exceed $50,000, and to deduct the remainder of such start up expendituresto deduct the remainder of such start-up expenditures ratably over the 180-month period beginning with the month in which the active trade or business begins

Tax Treatment of Start-up CostsStat tor Constr ctionStatutory Construction

• Section 195(c)(1) defines “start-up expenditure” as anySection 195(c)(1) defines start up expenditure as any amount paid or incurred in connection with: 1) Investigating the creation or acquisition of an active trade or business2) Creating an active trade or business or2) Creating an active trade or business, or 3) Any activity engaged in for profit and for the production of income before the

day on which the active trade or business begins, in anticipation of such activity becoming an active trade or business, to the extent that the amount, if paid or incurred in connection with the operation of an existing active trade or business, would be allowable as a deduction for the taxable year in which paid or incurred.

• Section 195(c)(1) further provides that the term “start up• Section 195(c)(1) further provides that the term start-up expenditure” does not include any amount with respect to which a deduction is allowable under Sections 163(a) (interest), 164 (taxes), or 174 (research and experimental expenditures)

What Constitutes a Start-up Cost?Ta CriteriaTax Criteria

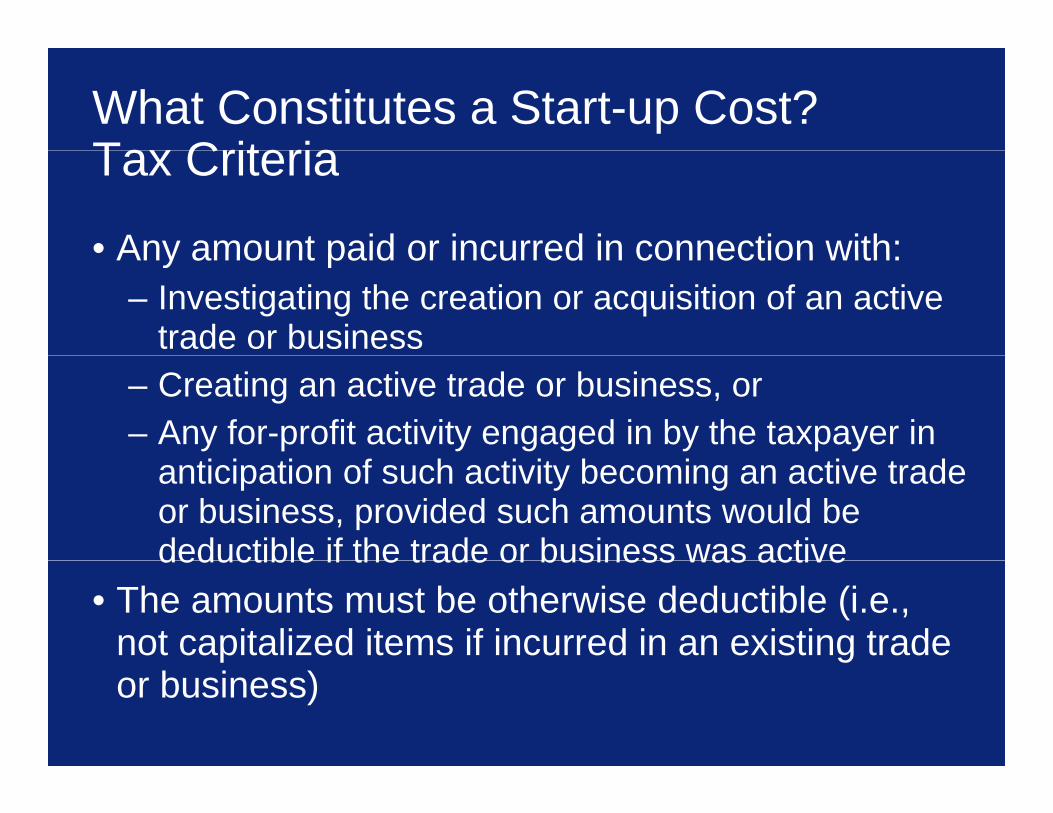

• Any amount paid or incurred in connection with:Any amount paid or incurred in connection with: – Investigating the creation or acquisition of an active

trade or business– Creating an active trade or business, or – Any for-profit activity engaged in by the taxpayer in

anticipation of such activity becoming an active trade or business, provided such amounts would be deductible if the trade or business was activedeductible if the trade or business was active

• The amounts must be otherwise deductible (i.e., not capitalized items if incurred in an existing trade or business)

Examples of Start-up Costs for Tax P rposesPurposes

• AdvertisingAdvertising• Salaries and wages paid to employees who are

being trained and their instructors g• Travel expenses• Salaries and fees paid or incurred for executives, p ,

consultants and similar professional services

Costs Not Subject to Capitalization as Start p Costs for Ta P rposesStart-up Costs for Tax Purposes

• Amounts that are allowable as a deduction may notAmounts that are allowable as a deduction may not be capitalized and amortized as start-up costs– Interest– Taxes– Research & experimental expenditures

• Depreciation expense on fixed assets may not treated as a start-up cost eligible for capitalization

d ti tiand amortization– TAM 9235004

Business expansion costs• Business expansion costs

What Constitutes Active Conduct of Trade or B sinessTrade or Business

• Facts and circumstances analysis based on theFacts and circumstances analysis based on the corporation beginning the business when it starts the business operations for which it was organized– Does not mean “in existence”

• Key factors in analysis include:– Acquisition of all necessary assets– Revenue-producing operations commenced with

th tthose assets• Does not necessarily coordinate with the “start of

trade or business” under Sections 248 709 or 355trade or business under Sections 248, 709 or 355

What Constitutes Active Conduct of Trade or B sinessTrade or Business

• Generally the courts use the tests of RichmondGenerally the courts use the tests of Richmond Television Corp., 345 F2d 901 (4th Cir. 1965)– Costs incurred by the taxpayer for training in years y p y g y

prior to receipt of its FCC broadcasting license are not ordinary business expensesT d b i d d t b i b th t– Trade or business deemed to begin by the court when the taxpayer begins to function as a going concern and performs those activities for which it pwas organized

• When active conduct of trade or business l i dcommences, start-up costs are no longer incurred

Making a Valid Section 195 ElectionMaking a Valid Section 195 Election

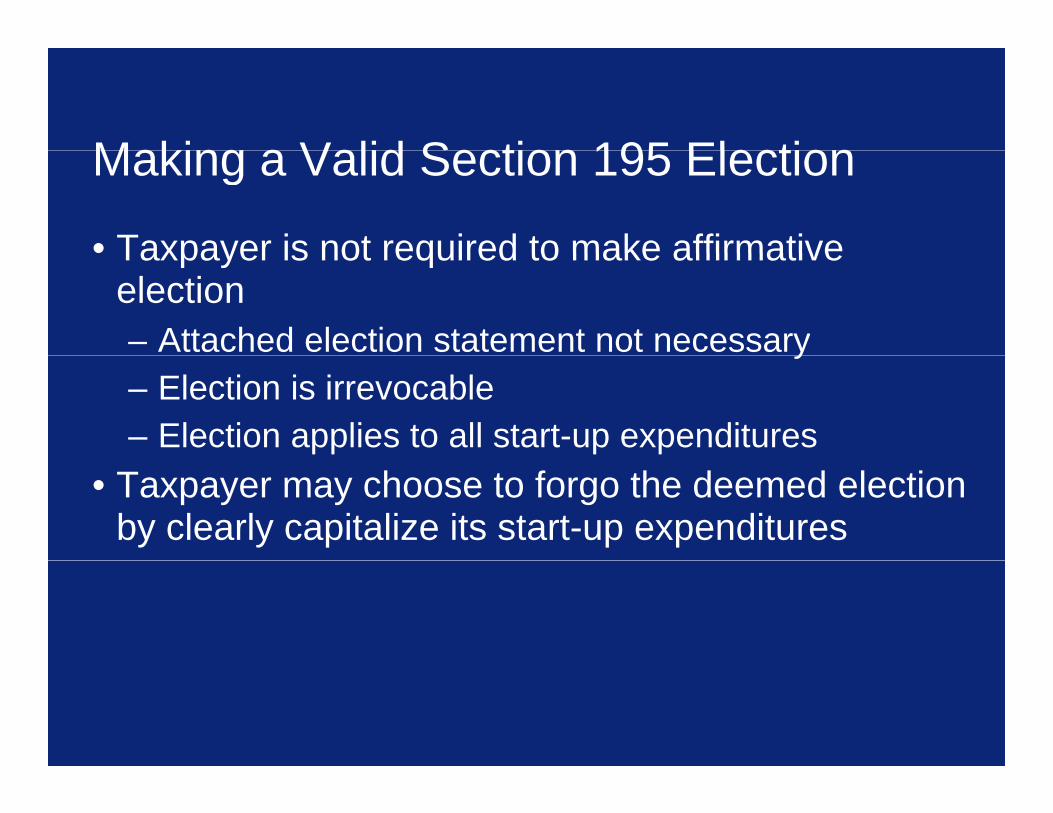

• Taxpayer is not required to make affirmativeTaxpayer is not required to make affirmative election– Attached election statement not necessaryy– Election is irrevocable– Election applies to all start-up expenditures

• Taxpayer may choose to forgo the deemed election by clearly capitalize its start-up expenditures

Partners and PartnershipsTa Treatment of Start p CostsTax Treatment of Start-up Costs

• Generally in a partnership entity the test of activeGenerally in a partnership entity, the test of active trade or business is applied at the entity level– Partners may have been engaged in active trade or y g g

business apart from the flow-through entity• Madison Gas & Electric decision provided that a

j i t t b l tiliti t hijoint venture by several utilities was a partnership, requiring capitalization of the start-up costs of the joint venturejoint venture– Joint venture was not an expansion of the existing

business of the utilities

Failed Start p CostsFailed Start-up Costs

• Costs of investigating trade or businesses that doCosts of investigating trade or businesses that do not commence are not start-up costs– Costs are deductible as a loss under Section 165– Determination is based on available facts and

circumstances• In the case of a technical termination of a

partnership, the trade or business may be considered to be disposedconsidered to be disposed

• Loss deductions in excess of $10M (corporations) or $2M (partnership) may require reporting onor $2M (partnership) may require reporting on Form 8886

ITC or Treas r Grant EligibilitITC or Treasury Grant Eligibility

• Capitalized start-up costs are not tangible propertyCapitalized start up costs are not tangible property and are not depreciable

• Costs eligible for Treasury Grant or ITC must be:g y– Tangible personal property – Other tangible propertyg y

T T t tTax Treatment: Organizational and gSyndication Costs

Organi ational Costs Ta TreatmentOrganizational Costs Tax Treatment

• Rules similar to those for start-up costs reRules similar to those for start up costs re applicable for organizational costs under IRC Sections 248 and 709 that are:– Incident to creation of a corporation or partnership,– Chargeable to a capital account, AND– Of a character which would be amortizable over a

limited life, if the entity had a limited lifeAmounts are generally capitalized and amortized• Amounts are generally capitalized and amortized pursuant to election by taxpayer– If election is foregone amounts are permanentlyIf election is foregone, amounts are permanently

capitalized

Organizational CostsMaking a Valid Ta ElectionMaking a Valid Tax Election

• Taxpayer is not required to make affirmativeTaxpayer is not required to make affirmative election– Attached election statement not necessaryy– Election is irrevocable– Election applies to all organizational expenditures

S ndication Costs Ta TreatmentSyndication Costs Tax Treatment

• Syndication costs are capital costs related toSyndication costs are capital costs related to syndicating a partnership and its related investment units– Cost of marketing of the actual units– Cost of production of any offering memorandums or

ti l t i lpromotional materials– Sales commissions

Syndication costs are capitalized under Section• Syndication costs are capitalized under Section 709– Capitalized amounts are not subject to amortizationCapitalized amounts are not subject to amortization

Tax Treatment: Expansion Costs

B siness E pansion CostsBusiness Expansion Costs

• Ordinary and necessary costs incurred inOrdinary and necessary costs incurred in connection with expanding an existing trade or business are deductible under Section 162– Facts and circumstances analysis has faced

different interpretations by Courts and IRSI B i liff C d C th t l d th t t• In Briarcliff Candy Corp., the court ruled that costs incurred to pursue marketing operations in a different locale and of a different type aredifferent locale and of a different type are deductible– A separate and distinct asset was not createdp

B siness E pansion CostsBusiness Expansion Costs

• In Colorado Springs Nat'l Bank v U S the courtIn Colorado Springs Nat l Bank v. U.S., the court ruled that costs incurred to enter the credit card business by banks that were previously engaged in retail loan making were deductible

• In FMR Corp. v. Comr., the court ruled the mutual f d i d t it li th tfund group was required to capitalize the costs associated with the development of the marketing plan development of the management contractplan, development of the management contract, formation and registration of 82 new mutual funds– Taxpayer expected significant future benefit from the p y p g

new funds

Tax Treatment: Transaction Costs

O er ieOverview

• Transaction costs that facilitate a restructuring orTransaction costs that facilitate a restructuring or reorganization of a business entity or a transaction involving the acquisition of capital, such as stock issuance, borrowing, or recapitalization, are capitalized

T o prong R leTwo-prong Rule

• First prong requires capitalization of costs thatFirst prong requires capitalization of costs that facilitate the taxpayer’s acquisition, creation, or enhancement of intangible asset

• Second prong requires capitalization of costs that facilitate the taxpayer’s restructuring or

i ti f b i tit f ilit treorganization of a business entity or facilitate a transaction involving the acquisition of capital

Including stock issuance borrowing or– Including stock issuance, borrowing, or recapitalization

Facilitate R leFacilitate Rule

• An amount facilitates a transaction if it is paid in theAn amount facilitates a transaction if it is paid in the process of pursuing the transaction, as determined under a facts and circumstances analysis

• The fact that an amount would not have been incurred but for the transaction is relevant but not d t i tideterminative

Inherentl Facilitati eInherently Facilitative

• Certain amounts are considered inherentlyCertain amounts are considered inherently facilitative and must be capitalized without regard to the date such costs are incurred– Determining the value of target (i.e., securing

valuation or formal written evaluation)N ti ti t t i th t ti– Negotiating or structuring the transaction

– Preparing and reviewing transactional documents or regulatory filingsregulatory filings

– Obtaining regulatory approval for the transaction– Securing advice on the tax consequences of theSecuring advice on the tax consequences of the

transaction

“Co ered Transactions”“Covered Transactions”

• An amount paid in the process of investigating orAn amount paid in the process of investigating or otherwise pursuing a “covered transaction” facilitates the transaction only if it relates to activities performed on or after the earlier of the date on which:

A l tt f i t t l i it t i il– A letter of intent, exclusivity agreement, or similar written communication (other than a confidentiality agreement) is executed by both the acquirer and g ) y qtarget; or

– The material terms of the transaction are authorized d b th t ’ b d f di tor approved by the taxpayer’s board of directors

“Co ered Transactions” ( t )“Covered Transactions” (cont.)

• A “Covered Transaction” means/includes:A Covered Transaction means/includes:– A taxable acquisition of assets that constitute a trade

or business– A taxable acquisition of a controlling interest in a

business entity – An “A,” “B,” “C,” or acquisitive “D” reorganization

• A “Covered Transaction” does not mean/include:Di i i “D” i ti d S ti 355– Divisive “D” reorganizations under Section 355, Section 351 transactions, “G” reorganizations

– LBOs Redemptions Recapitalizations StockLBOs, Redemptions, Recapitalizations, Stock Issuances,

Effect on Co ered TransactionsEffect on Covered Transactions

• Deduction or amortization of investigatory costs isDeduction or amortization of investigatory costs is only possible in covered transactions

• All transaction costs in non-covered transactions must be capitalized

Simplif ing Con entionsSimplifying Conventions

• Salaries and OverheadSalaries and Overhead– The regulations provide an assumption that

employee compensation and overhead costs do not p y pfacilitate the acquisition, creation or enhancement of an intangible asset

De Minimis Costs• De Minimis Costs– The regulations provide that de minimis transaction

costs do not facilitate a capital transaction and arecosts do not facilitate a capital transaction and are not required to be capitalized • De minimis costs are defined as costs that do not

exceed $5,000

Special R lesSpecial Rules

• Borrowing CostsBorrowing Costs– An amount paid to facilitate a borrowing does not

facilitate another transaction other than the borrowing

• Asset Sales– An amount paid to facilitate a sale of unwanted

assets does not facilitate another transaction other than the asset salethan the asset sale

Questions?

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiariesstructure of Deloitte LLP and its subsidiaries.

Copyright © 2010 Deloitte Development LLC. All rights reserved.

Member Deloitte Touche Tohmatsu Limited