Embed Size (px)

Citation preview

Standards in market infrastructures…and beyond

17th XBRL Europe Day

1 June 2016, Frankfurt

François Laurent

DG Market Infrastructure & Payments

European Central Bank

Rubric

www.ecb.europa.eu

Standardisation and market infrastructures1

New regulatory landscape2

Table of contents

Issues to consider3

2

Rubric

www.ecb.europa.eu

Standardisation and market infrastructures1

New regulatory landscape2

Table of contents

Issues to consider3

3

Rubric

www.ecb.europa.eu

Market Infrastructures challenges

Integration of European market infrastructure a political

priority for EU governments

Further integration of market infrastructures in Europe

Three actions possible for ECB/Eurosystem:

Regulations

Catalyst for change

Operator of market infrastructure

4

Standardisation and market infrastructures

Use of global standards is a must

Rubric

www.ecb.europa.eu

ECB experience with standardisation in market infrastructures

Efficient and reliable real-time straight-through processing

of payment and securities settlement transactions

Major efforts to facilitate integration, through

harmonisation and interoperability

Development of more and more interoperable platforms

globally

5

Standardisation and market infrastructures

Rubric

www.ecb.europa.eu

3 areas addressed from a market infrastructure perspective:

Retail payments (SEPA)

Large value payments (TARGET2)

Securities settlement (T2S)

6

Standardisation and market infrastructures

Rubric

www.ecb.europa.eu

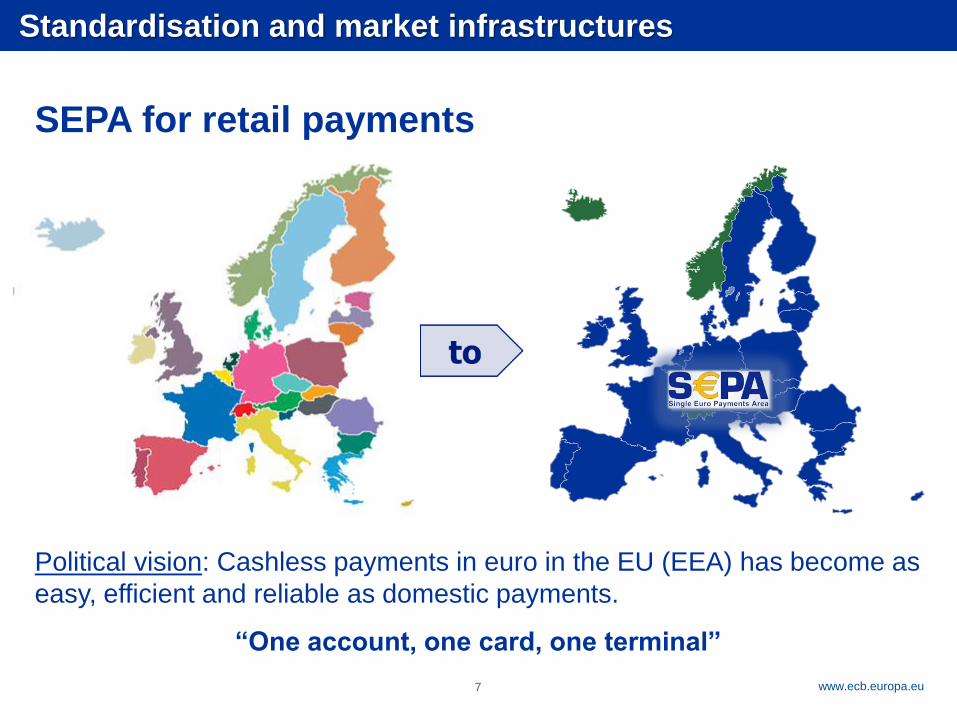

Political vision: Cashless payments in euro in the EU (EEA) has become as

easy, efficient and reliable as domestic payments.

“One account, one card, one terminal”

SEPA for retail payments

Standardisation and market infrastructures

7

Rubric

www.ecb.europa.eu

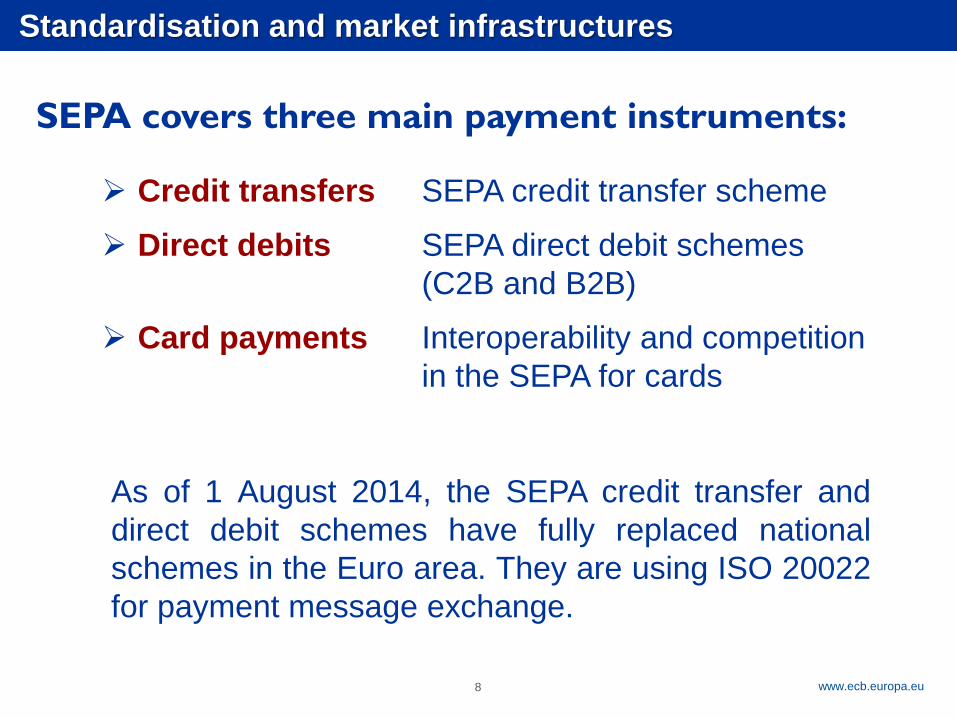

Standardisation and market infrastructures

SEPA covers three main payment instruments:

8

Credit transfers SEPA credit transfer scheme

Direct debits SEPA direct debit schemes

(C2B and B2B)

Card payments Interoperability and competition

in the SEPA for cards

As of 1 August 2014, the SEPA credit transfer and

direct debit schemes have fully replaced national

schemes in the Euro area. They are using ISO 20022

for payment message exchange.

Rubric

www.ecb.europa.eu

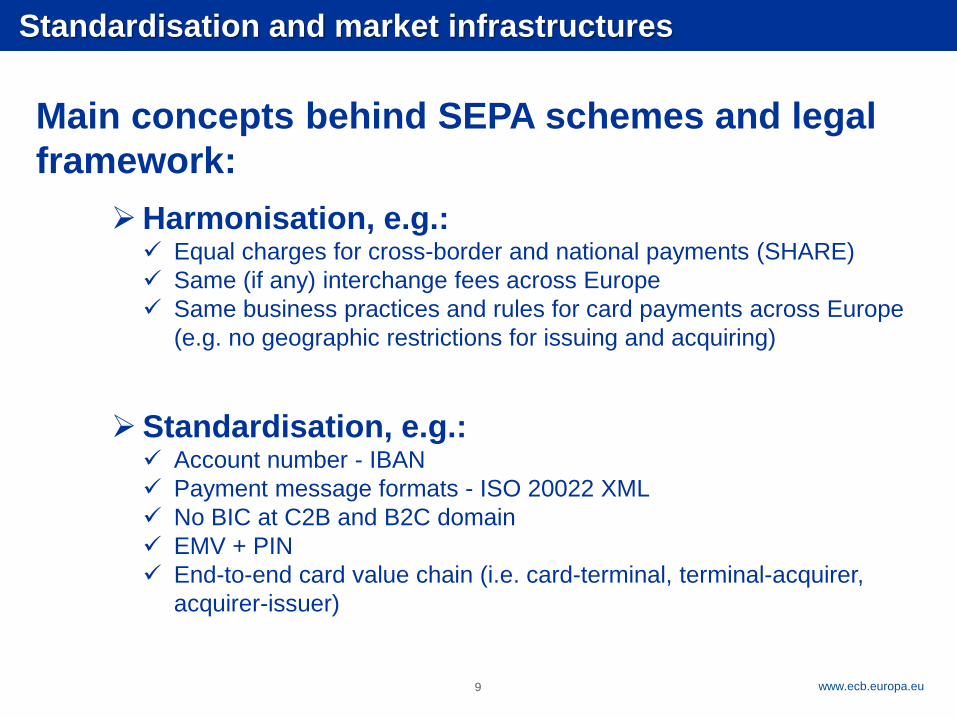

Standardisation and market infrastructures

Main concepts behind SEPA schemes and legal

framework:

9

Harmonisation, e.g.: Equal charges for cross-border and national payments (SHARE)

Same (if any) interchange fees across Europe

Same business practices and rules for card payments across Europe

(e.g. no geographic restrictions for issuing and acquiring)

Standardisation, e.g.: Account number - IBAN

Payment message formats - ISO 20022 XML

No BIC at C2B and B2C domain

EMV + PIN

End-to-end card value chain (i.e. card-terminal, terminal-acquirer,

acquirer-issuer)

Rubric

www.ecb.europa.eu

Real-time gross settlement (RTGS) system for

the euro.

Processing and settlement of payments takes

place in real time (i.e. continuously).

Each transfer is settled individually (gross

settlement).

Enables transactions to be settled using central

bank money and with immediate finality.

Operated by the Eurosystem.

Offers the highest standards of reliability and

resilience.

What is TARGET2?

Standardisation and market infrastructures

10

Rubric

www.ecb.europa.eu

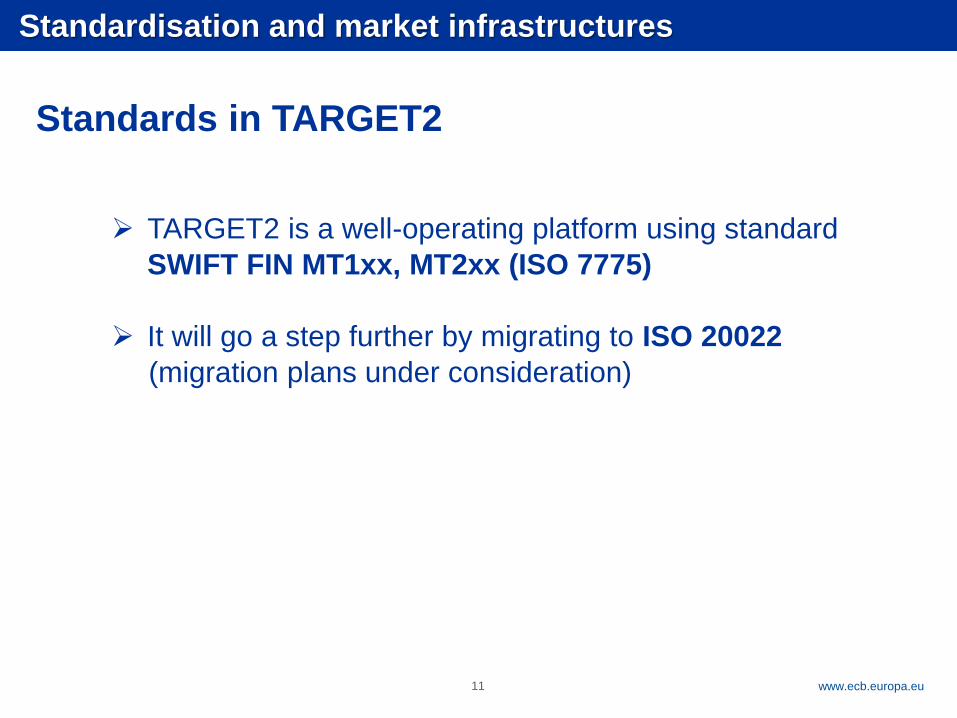

TARGET2 is a well-operating platform using standard

SWIFT FIN MT1xx, MT2xx (ISO 7775)

It will go a step further by migrating to ISO 20022

(migration plans under consideration)

Standards in TARGET2

11

Standardisation and market infrastructures

Rubric

www.ecb.europa.eu

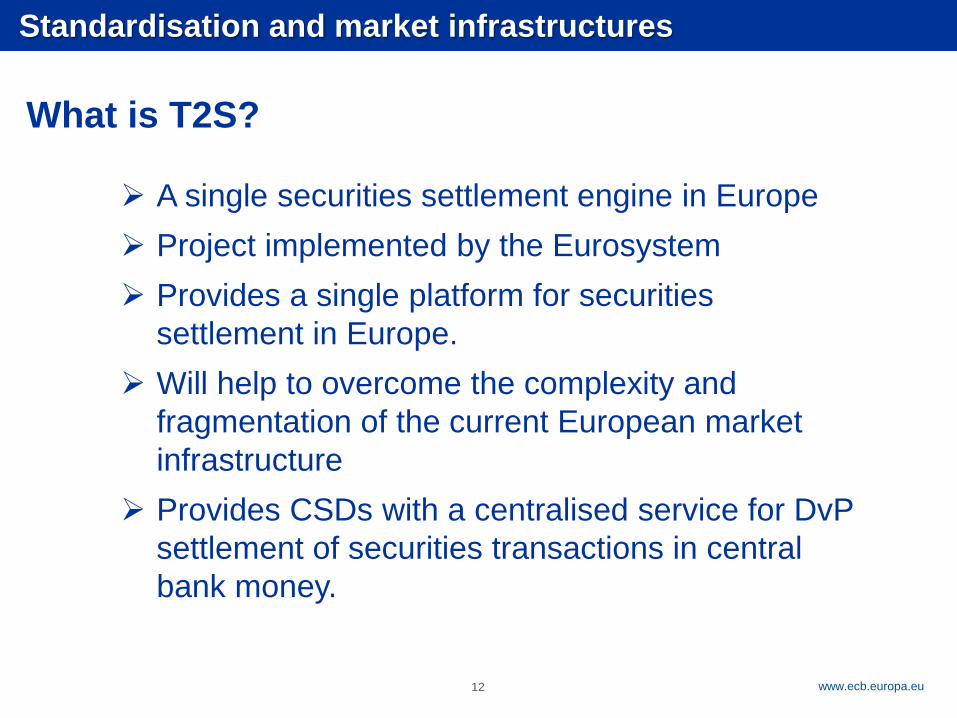

A single securities settlement engine in Europe

Project implemented by the Eurosystem

Provides a single platform for securities

settlement in Europe.

Will help to overcome the complexity and

fragmentation of the current European market

infrastructure

Provides CSDs with a centralised service for DvP

settlement of securities transactions in central

bank money.

What is T2S?

Standardisation and market infrastructures

12

Rubric

www.ecb.europa.eu

Process of both debt securities and equities.

Settlement, at low cost, of both domestic and

cross-border transactions.

Single set of rules, standards and fees applied to

all transactions across all T2S markets.

Multicurrency system.

Integration onto a single IT platform of both the

market participants’ securities accounts, and their

dedicated central bank cash accounts.

Trigger of significant liquidity and collateral

savings.

T2S main characteristics

Standardisation and market infrastructures

13

Rubric

www.ecb.europa.eu

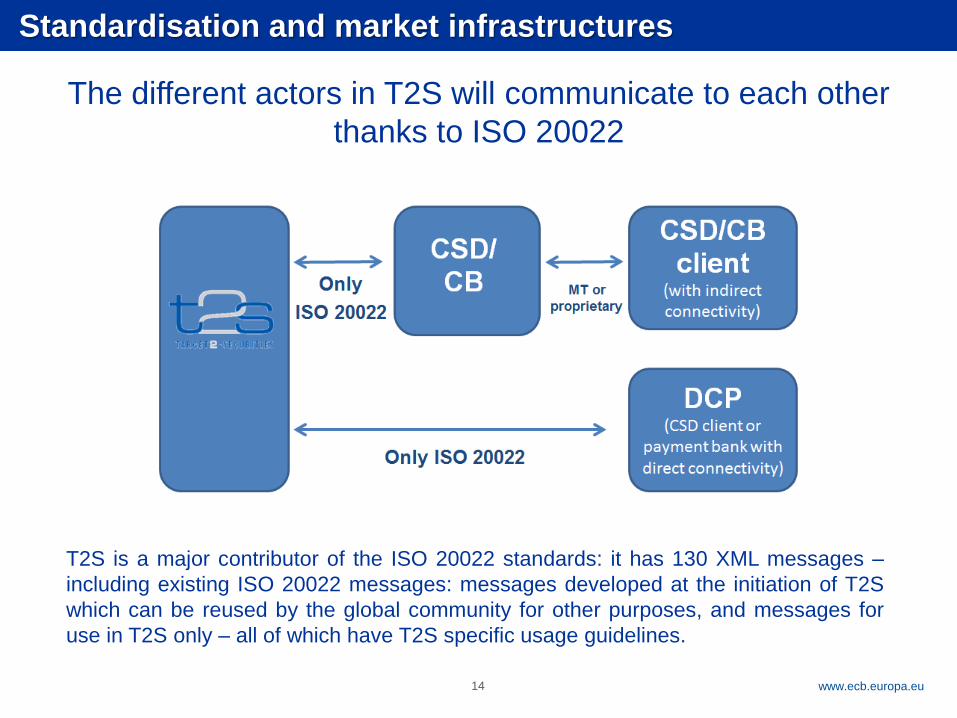

The different actors in T2S will communicate to each other

thanks to ISO 20022

T2S is a major contributor of the ISO 20022 standards: it has 130 XML messages –

including existing ISO 20022 messages: messages developed at the initiation of T2S

which can be reused by the global community for other purposes, and messages for

use in T2S only – all of which have T2S specific usage guidelines.

14

Standardisation and market infrastructures

Rubric

www.ecb.europa.eu15

Standardisation and market infrastructures

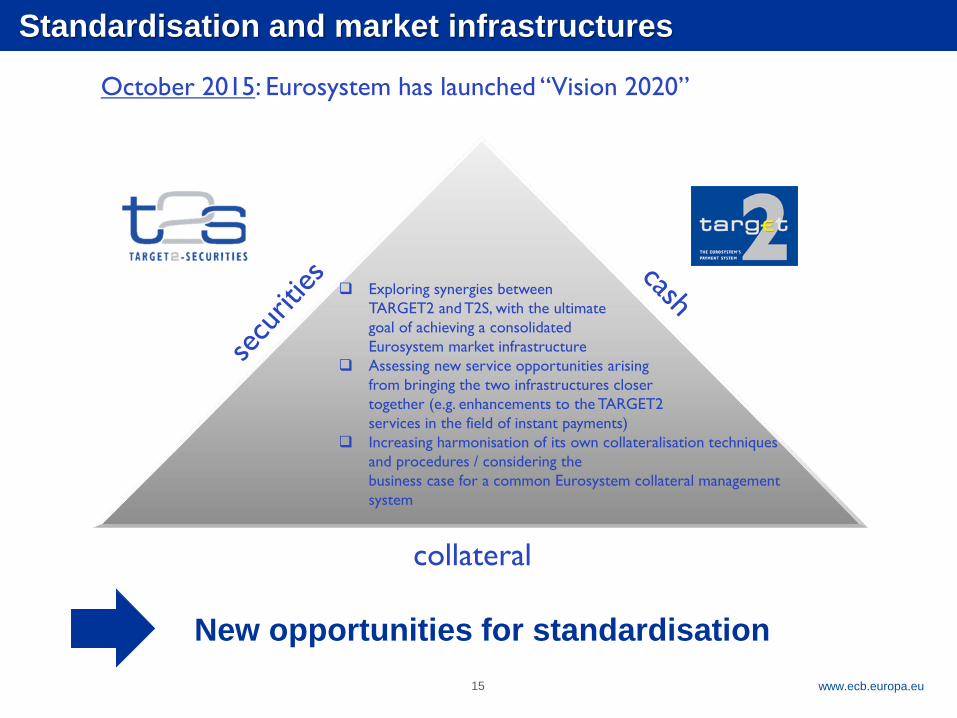

Exploring synergies between

TARGET2 and T2S, with the ultimate

goal of achieving a consolidated

Eurosystem market infrastructure

Assessing new service opportunities arising

from bringing the two infrastructures closer

together (e.g. enhancements to the TARGET2

services in the field of instant payments)

Increasing harmonisation of its own collateralisation techniques

and procedures / considering the

business case for a common Eurosystem collateral management

system

October 2015: Eurosystem has launched “Vision 2020”

collateral

New opportunities for standardisation

Rubric

www.ecb.europa.eu

Standardisation and market infrastructures1

New regulatory landscape2

Issues to consider3

16

Table of contents

Rubric

www.ecb.europa.eu

CSDR

EMIR

SSMMiFID2/MiFIR

New regulatory landscape

ESMA

TR

17

EBAFSB

EIOPA

CPMI

AnaCredit

FinRep/CoRep

IOSCO

Rubric

www.ecb.europa.eu

Supervisory

Leveraging standardisation experience

New regulatory landscape

Statistics &

Analysis

Operations &

Transactions

18

Rubric

www.ecb.europa.eu

Example: MMSR (Money Market Statistical Reporting)

• ECB Regulation (OJ 16/12/2014): larger Credit Institutions need to report daily data on money market transactions to the Eurosystem

• Data collected: related to Secured Market, Unsecured Market, Foreign Exchange Swaps and Euro Overnight Index Swaps

• First reporting: as of 1 April 2016 (50 largest credit Institutions)

• Reporting Instructions:

• Will be established to set up a standardised/highly automated reporting framework

• Aligned with ISO 20022 standards, or expand them where appropriate to be easier to implement by the banking industry

• Will identify the taxonomy of the variables across the different market segments as unique reference for NCBs and credit institutions

New regulatory landscape

19

Rubric

www.ecb.europa.eu

Example: SFT (Secured Financing Transactions)

• Lack of transparency in the secured financing market: FSB Recommendations on shadow banking and European Commission proposal for a EU regulation to enhance transparency in the SFTs market

• Daily trade-level reporting - Granular reporting required for monitoring and analysis:

• To facilitate more effective macro-prudential monitoring of the possible systemic risks and vulnerabilities arising from SFTs

• To enhance the micro-prudential supervision (facilitating the monitoring of liquidity risk and credit risks arising from SFTs)

• To enhance oversight of financial market infrastructures (FMIs) that process SFTs

• To achieve a better and more in-depth understanding of the SFT market segments relevant for monetary policy implementation

• To support the monitoring and analysis of developments related to financial integration

New regulatory landscape

20

Rubric

www.ecb.europa.eu

Benefits

Quality of information

• Greater consistency

• Less necessity for ex post data reconciliations

Avoiding duplications in data requests

• Reducing reporting burden

More powerful services for users

• Faster reply to new data requests

• Richer information

• Higher data sharing

New regulatory landscape

21

Economies of scale in data management

and supporting IT solutions

Rubric

www.ecb.europa.eu

Standardisation and market infrastructures1

New regulatory landscape2

Issues to consider3

22

Table of contents

Rubric

www.ecb.europa.eu

Global challenges

Opportunities for standardisation

Issues to consider

23

How to handle increasingly interrelated business

segments (e.g. collateral and payments)?

How to manage high volume of business information

from multiple sources?

How to effectively address the increasing need for

(regulatory) reporting to multiple parties for multiple

purposes?

How to address market participants ever increasing

requests for efficient and effective non-proprietary

solutions?

How to manage globalising markets?

Rubric

www.ecb.europa.eu

Consideration, awareness and commitment

at all levels

Involvement of all relevant stakeholders

(market participants, public authorities,

regulators)

Need for a common reference model (incl.

Data Dictionary) with key reference data,

e.g. Legal Entity Identifier (LEI), Unique

Transaction Identifier (UTI) and Unique

Product Identifier (UPI)

24

Issues to consider

Rubric

www.ecb.europa.eu

Many thanks for your attention!

http://www.ecb.europa.eu/paym/html/index.en.html

25

![DCP AUTHORIZATION TEST CASES T2S PROJECT · Target2 Securities - DCP AUTHORIZATION TEST v. 3.0 final [T2S –208] 5 . 1 DOCUMENT MANAGEMENT 1.1 Document History Date Version Details](https://img.pdfslide.us/doc/110x75/60047388b0a06f54cd229a62/dcp-authorization-test-cases-t2s-project-target2-securities-dcp-authorization.jpg)