Embed Size (px)

Citation preview

Standard Insurance CompanyPortland, OR

The policy discussed in this presentation has exclusions and limitations and terms under which the policy may be continued in force or discontinued. For costs and complete details of coverage, contact your Standard Insurance Company representative or The Standard at 800.992.4446. Policy Form B152. This presentation is not for use in California or Georgia.

The Impact of DisabilityA Presentation for Associations aboutThe Need for Individual Disability Income Insurance

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Agenda

• Company Information

• Disability Facts

• The Problem

• The Solution

• Our Promise

• In Closing

• Associations

• Other Products from The Standard

Information About The Standard

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Who is The Standard?

• Standard Insurance Company

– 4th largest in Group Long Term Disability Insurance Nationwide*

– 4th largest in Group Short Term Disability Insurance Nationwide*

– 8th largest in Individual Disability Insurance Nationwide*

• StanCorp Financial Group, Inc.

• Specialty carrier in disability and other lines of insurance

• Over 30 consecutive years of profits in disability on a statutory basis

*Based on 2004 in force premium statistics from JHA and LIMRA.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Ratings

Financial Strength Ratings, December 2004

A.M. Best Company A (Excellent) 3rd of 13 rankings

Fitch AA- (Very Strong) 4th of 16 rankings

Standard & Poor’s A+ (Strong) 5th of 16 rankings

Moody’s A1 (Good) 5th of 16 rankings

Disability Facts

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

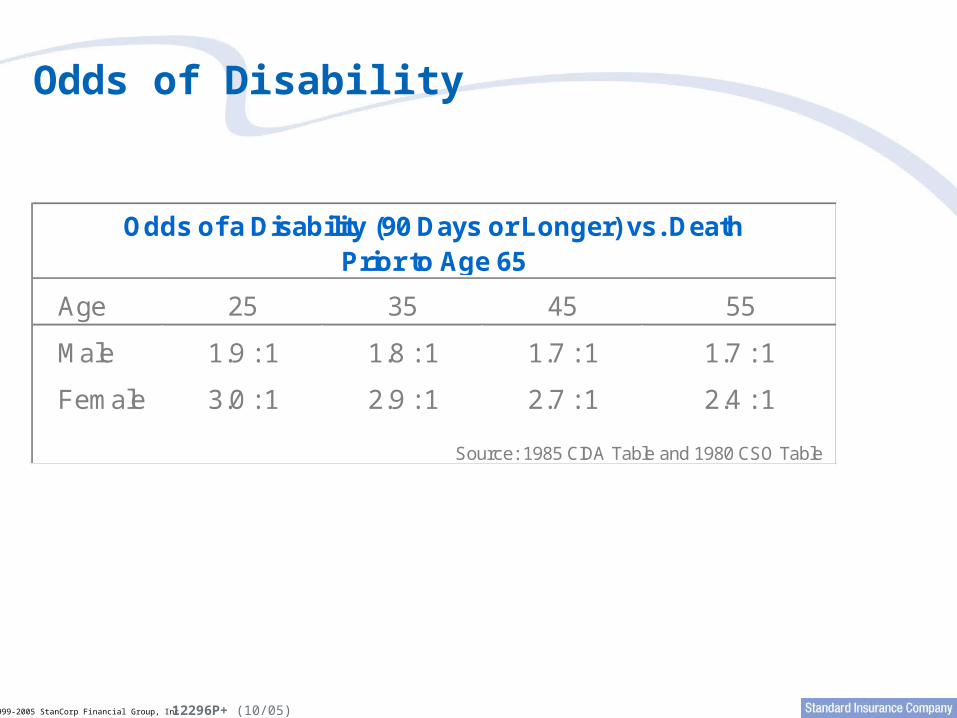

Odds of Disability

Age 25 35 45 55

Male 1.9 : 1 1.8 : 1 1.7 : 1 1.7 : 1

Female 3.0 : 1 2.9 : 1 2.7 : 1 2.4 : 1

Odds of a Disability (90 Days or Longer) vs. Death Prior to Age 65

Source: 1985 CIDA Table and 1980 CSO Table

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

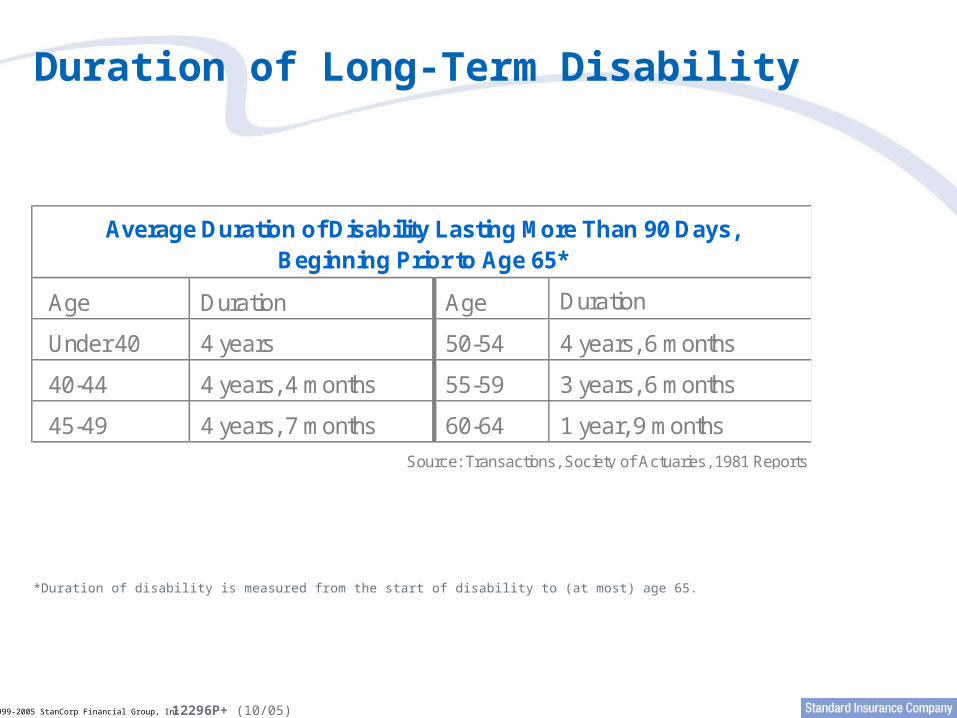

Age Duration Age

Under 40 4 years 50-54 4 years, 6 months

40-44 4 years, 4 months 55-59 3 years, 6 months

45-49 4 years, 7 months 60-64 1 year, 9 months

Average Duration of Disability Lasting More Than 90 Days,Beginning Prior to Age 65*

Source: Transactions, Society of Actuaries, 1981 Reports

Duration

Duration of Long-Term Disability

*Duration of disability is measured from the start of disability to (at most) age 65.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Current Causes of Disability

Source: Standard Insurance Company

Breakdown of diagnoses for The Standard’s disability claims from 1/1/04 to 12/31/04

The conditions listed above do not establish disability. Each claim is evaluated on its own merits and according to the terms of the policy.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

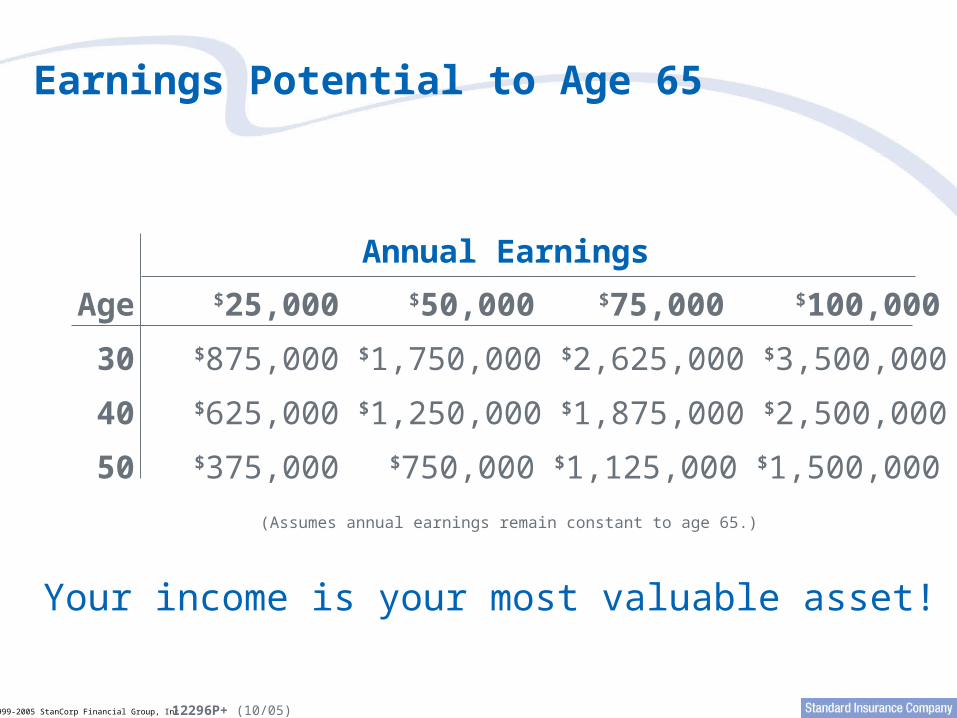

Annual Earnings

Earnings Potential to Age 65

Age $25,000 $50,000 $75,000 $100,000

30 $875,000 $1,750,000 $2,625,000 $3,500,000

40 $625,000 $1,250,000 $1,875,000 $2,500,000

50 $375,000 $750,000 $1,125,000 $1,500,000

(Assumes annual earnings remain constant to age 65.)

Your income is your most valuable asset!

The Problem

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Three Aspects of Disability

What can happen?

– Presumptive Total Disability – Even if the insured can still perform some or all of his occupation, he is presumed fully disabled and entitled to full benefits under specified conditions which include loss of sight, speech, hearing or use of two limbs

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Three Aspects of Disability

What can happen?

– Presumptive Disability – Even if you can still perform some or all of your occupation, you are presumed fully disabled and entitled to full benefits under specified conditions which include loss of sight, speech, hearing or use of two limbs.

– Total Disability – If, due to injury or sickness, the insured is unable to perform the substantial and material duties of his occupation, is not working in another occupation, and is under a physician’s care

– Residual Disability – If, due to injury or sickness, you can perform some of the substantial and material duties of your occupation, or all of these duties but not for as long or as effectively as before, your monthly earnings are reduced by at least 20%; you are under a doctor’s care and you are not totally disabled.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Three Aspects of Disability

What can happen?

– Presumptive Disability – Even if you can still perform some or all of your occupation, you are presumed fully disabled and entitled to full benefits under specified conditions which include loss of sight, speech, hearing or use of two limbs.

– Total Disability – If, due to injury or sickness, you are unable to

– Residual Disability – If, due to injury or sickness: the insured can perform some of the substantial and material duties of his occupation, or all of these duties but not for as long or as effectively as before; his monthly earnings are reduced by at least 20%; and he is under a physician’s care. Also, he may not be totally disabled

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state.

The Solution

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Benefits

The Protector+SM – an individual disability insurance policy

– Guaranteed Renewable to Age 66/67

– Benefit for Total Disability

– Benefit for Presumptive Total Disability

– Rehabilitation Benefit

– Premium Waiver Benefit

– Disability due to Cosmetic or Transplant Surgery Benefit

– Survivor Benefit (not available in all states)

The policy discussed in this presentation has exclusions and limitations and terms under which the policy may be continued in force or discontinued. For costs and complete details of coverage, contact your Standard Insurance Company representative or The Standard at 800.992.4446. Policy Form B152.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Policy Definition of Total Disability/Totally Disabled

Because of Your Injury or Sickness:

1. You are unable to perform the substantial and material duties of Your Regular Occupation; and

2. You are not engaged in any other gainful occupation; and

3. You are under the regular care of a Physician appropriate for Your Injury or Sickness. This Physician’s care requirement will be waived when We receive written proof, satisfactory to Us, that further care would be of no benefit to You.

This is generic language only. Actual contract provisions and availability of certain benefits and riders may vary by state.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Optional Riders

• Available to all occupation classes

– Residual Disability Rider

– Indexed Cost of Living Rider

– Supplemental Social Insurance Rider

– Future Purchase Option Rider

– Noncancelable Rider

– Catastrophic Disability Benefit Rider

• Available to select occupation classes

– Own Occupation Rider

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Residual Disability Rider

Residual disability means the insured is not totally disabled, but because of his injury or sickness:

1. His monthly earnings are reduced by 20% or more of his indexed prior monthly earnings; and

2. He is under the regular care of a physician appropriate for his injury or sickness; and

3. He is able:

a. To do some, but not all, of the substantial and material duties of his regular occupation; or

b. To do all of the substantial and material duties of his regular occupation, but not for as long a time or as effectively as he did immediately prior to his injury or sickness.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Indexed Cost of Living Rider

This rider helps provide a cushion against inflation during a lengthy disability.

For each year of disability after the first, the rider pays an amount in addition to the policy benefit based on the average annual change in the Consumer Price Index for All Urban Consumers (CPI-U), subject to a cap of either 3% or 6%, whichever is chosen on the application.

Payment is subject to the policy’s benefit period and other requirements. The amount payable under the rider will not decrease even if the CPI-U decreases.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Supplemental Social Insurance Rider

This rider pays a benefit if the policy’s total disability benefit is payable and no legislated benefits are payable for the disability.

The insured must apply for legislated benefits for which he may be eligible and meet other requirements in the rider.

A reduced benefit is available if legislated benefits are payable that are less than the rider benefit amount.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Future Purchase Option Rider

This rider allows for the purchase of benefit increases on each policy anniversary subject only to financial underwriting. Evidence of the insured’s good health is not required to purchase an increase.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Noncancelable Rider

This rider changes the policy and all riders made part of the policy from guaranteed renewable to noncancelable and guaranteed renewable.

The Standard cannot change the policy terms or premium until the termination date.

This rider also changes the policy to provide that, if the maximum benefit period is longer than five years and the insured becomes eligible for the benefit for presumptive total disability, total disability payments will be payable for his lifetime as long as the presumptive disability continues.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Catastrophic Disability Benefit Rider

This rider pays an additional benefit if you are receiving the benefit for total disability and you are unable to perform at least two activities of daily living (ADLs), have a severe cognitive impairment, or are presumptively totally disabled.

ADLs include: bathing, continence, dressing, eating, toileting and transferring (moving into and out of a bed, chair or wheelchair).

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Own Occupation Rider1

This rider changes the policy definition of Total Disability2 to read:

“Because of your Injury or Sickness:

1. You are unable to perform the substantial and material duties of Your Regular Occupation; and

2. You are under the regular care of a Physician appropriate for your Injury or Sickness. This physician’s care requirement will be waived when We receive written proof, satisfactory to Us, that further care would be of no benefit to You.”

Not available for all occupation classes

1. This rider is issued with a two year mental disorder and substance abuse limitation

2. This rider removes the following sentence from the definition of Total Disability: “You are not engaged in any other gainful occupation”

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Mental Disorder/Substance Abuse Limitation

Two year benefit period limitation for disability caused by mental disorder or substance abuse.

This limitation endorsement is added to each policy that has the Own Occupation Rider.

This endorsement may also be used at underwriter discretion.

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Exclusions from Coverage

The Standard will not pay benefits for:

1. Disability due to war. War means any:

a. War, declared or undeclared, whether civil or international;

b. Act of war;

c. Act incident to war;

d. Insurrection; and

e. Substantial armed conflict with organized forces of a military nature

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Exclusions from Coverage (continued)

2. The first 90 days of the insured’s disability due to pregnancy or childbirth

3. Disability caused or contributed to by the insured:

a. Committing or attempting to commit an assault or felony; or

b. Actively participating in a violent disorder or riot. "Actively participating" does not include the insured being at the scene of a violent disorder or riot while performing his official duties

4. Disability while the insured is confined for any reason to a penal or correctional institution

5. Intentionally self-inflicted injury

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Miscellaneous Policy Provisions

• The policy is guaranteed renewable until the policy termination date

– The Standard cannot change the policy, except for its premium, until that date. The premium can be changed only after the policy is three years old

• Renewal Option

– After the termination date, you may ask that the policy be renewed, but only if you are working at least 30 hours per week and are not disabled at the time of your request. Only the total disability benefit will be available, and limited benefit periods will apply

This is a general description only and is not specific policy language. Contract provisions and availability of certain benefits and riders may vary by state. Policy Form B152. Riders are available at extra cost.

Our Promise

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

Claims Philosophy and Practices

• We deliver on our promises

• We know that claimants need both financial and emotional support

• Our claims management approach is:

– Responsive

– Ethical

– Fair

Associations

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

• Members of approved associations may be eligible to receive a discount of 10%* on The Standard’s individual disability policies

• Discuss the conditions and eligibility for an association discount with a licensed representative of The Standard

• The Standard has issued disability policies to members of several hundred associations nationwide

*No discount in Florida.

Other Products from The Standard

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

The Protector SeriesSM

• The Business ProtectorSM

Reimbursement of business overhead expenses incurred during disability

• The Business Equity ProtectorSM

Funding for buy/sell agreements triggered due to disability

These policies have exclusions and limitations and terms under which the policy may be continued in force or discontinued. For costs and complete details of coverage, contact your Standard Insurance Company representative or The Standard at 800.992.4446. Policy Form Nos. B123 and B128.

In Closing

This presentation is not for use in California or Georgia.

©1999-2005 StanCorp Financial Group, Inc. 12296P+ (10/05)

The goose that laid the golden egg ~

Which would you insure?

… the goose?

… or the egg?

You insure your home, your car, your valuable assets …

Do you insure your income?

Thank you!

This presentation is not for use in California or Georgia.