Embed Size (px)

Citation preview

3rd EUROPEAN ELECTROMOBILITY STAKEHOLDER FORUM

MAKING THE CONNECTION

#eMSF2015

@eMobilityForum

3rd E-MOBILITY STAKEHOLDER FORUM

Strategies for widespread uptake of heavy duty EV’s

(Zero Emission Urban bus Systems)

Gert Miedema, Sales Director, ABB, PG EVCI

Agenda

o Main market drivers for widespread uptake of EV’s o Clean(er) air o High energy efficiency (‘well-to-wheel’) solutions o EV Battery prices are falling o Standardization is a must o Strong incentives: Norway

o Strategies for widespread uptake of heavy duty EV’s o Follow the passenger EV’s: Standardization & Volumes o Governments should set ZE targets & challenge industry

Strategies for widespread uptake of heavy duty EV’s

See also the site: http://aqicn.org/

But also Paris,

March 17th, 2014

China has no choice, Zero Emission is needed….

Mega-Cities are turning into smog-centers

Well-to-wheel efficiency: ‘electric‘ transportation most efficient

Biofuel: 7km

Hydrogen: 160km

Electric: 380km

A solar panel delivers 105 kWh/m².

A solar panel delivers 105 kWh/m².

After distribution, charging and storage in the battery, 77kWh is available to the motor.

An EV drives 5km/kWh, so 77kWh gives 380km range.

After electrolysis, compression and distribution 63kWh goes into the tank.

The fuel cell generates 31.5kWh of electricity. The vehicle drives 5km/kWh, so 31.5kWh gives 160km range.

Most efficient energy crops (palm oil, sugar cane) deliver 0.5L/m² including sowing, fertilizing, harvesting, refinement and distribution.

A vehicle drives 15km/L, so 0.5L gives 7km range.

Original source: Auke Hoekstra, Eindhoven University of Technology. Data was modified due to improved performance of biofuel and hydrogen.

Range per year per m² of land for alternative fuels

As this graph below shows, EV battery prices have fallen 40% since 2010.

Regarding the future, BMW board member Ian Robertson says, “in the next three to four years there will be more progress in battery development than in the previous 100 years.”

Source: http://cleantechnica.com/2013/07/08/40-drop-in-ev-battery-prices-from-2010-to-2012/#EpKMkZKxlOlD52Y8.99

Steeply falling EV-Battery prices & increasing volumes

40% Drop in EV Battery Prices from 2010 To 2012

More than 40 000 fully electric cars on the road (Dec 2014) - PHEV: Approx. 2 300

New sales approx 1 600 – 1 800 per month for the last 8 months

Very favourable incentives for buying fully electric cars

Incentives to be reviewed when more than 50 000 cars

Incentives being planned for electric transportation (Ruter)

0

5,000

10,000

15,000

20,000

25,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total 2014

Total 2012

Total 2013

Fast charging Stations Installed: 128 Planned: 54 (‘15)

Highest penetration EV market: Norway

Driven by targets & strong incentives

BEV sales / year 2012 - 2014

CHAdeMO / AC type 2/ CCS

EV car charging has 3 OEM Fast Charging standards in EU

Q4-2013 50 kW CCS

2010 50 kW CHAdeMO

Q4-2012 22-43 kW AC

& Tesla……

EU decision: after 31-12-’17 AC type 2 CCS

(Strategies for widespread uptake of heavy EV’s: follow the EV’s!

ZE bus/truck solution

Infra structure & maintenance cost

HD EV cost

Flexibility/ Roll-out speed

Reliability/maturity bus + infra

Range Energy Efficiency

(Passenger) capacity

(Initial) Impact on city traffic

Synergy ZE passenger cars

Fuel cells

(Only)

overnight

AC charging

Trolley/

Catenary

Inductive

Battery

swapping

Opportunity

DC Fast

Charging

Standard Fast DC charging: the solution towards ZE bus/truck

3/9/2015 | Slide 9 © ABB Group

= strongest option

Consumers/voters (should) ask for clean air & low noise (be willing to pay a small premium during the transition)

Governments should •Set (Zero) Emission & budget targets (2020/2030)

•Cities & Countries •Euro 7 norm definition (2018)

•Define & share (local) plans towards these targets •Challenge the industry to propose transition solutions

•Short term: City pilot projects •Medium/long term: volume roll-out projects

•Strongly encourage standardization •Help managing residential value of infrastructure

Governments should set ZE targets & challenge industry

E-bus & Fast Charging Industry should offer solutions: •Current requirements like bus timetables & routes •Standardized, •Cost effective (in volumes), • Implementable

3rd E-MOBILITY STAKEHOLDER FORUM

Moving forward with e-mobility integration into Smart Grids

Giovanni Coppola, Enel SpA

Smart Grids vision

13

Renewables

Dispatching

Network Automation

Forecast

Storage

Smart Secondary Substation

Electric Mobility

Interoperability

Smart Charging

Fast-Charge

Active Demand

Market Services

Smart-Info

Energy-Box

Load Balancing

Public Lighting

LED Technology

Remote Control

Gas Smart Metering

New Strategic Roles of the Infrastructures

Electricity Smart Metering

E-mobility business space

14

The research leading to these results has received funding from the European Union Seventh Framework Programme (FP7/2007 – 2013) under grant agreement No. 265499.

A seamless customer experience is built on IT system harmonized interfaces

B2C

DSO

LV/MV Electricity Grid

EV Service Provider

B2C service

B2B service

EVSE Operator

EVSE EV

RENs Production

search

access

pay ?

EV Customer

E-mobility standardization

select – your location

select – your connector

Type 2 AC

DC CHAdeMO

Combo 2

search

access

pay Alternative Fuels directive 94/2014

POI e-mobility interface

The research leading to these results has received funding from the European Union Seventh Framework Programme (FP7/2007 – 2013) under grant agreement No. 265499.

Smart Charging: turning risk into opportunity

16

Smart Charging could be a service sold by OEMs

Increasing flexibility burden for the DSOs

The increase of battery capacity could lead OEMs to step into virtual utility marketplace

Smart Charging: the customer’s perspective

17

Enabling customers to trade time flexibility with money savings,

while enhancing DERs hosting capacity

Smart charging

State Of Charge

Time of departure

EV tracking

EVSE Op.

EVSE

18

DSO

LV/MV Electricity Grid

EV Service Provider

B2C service

B2B service

Charging Station Operator

Charging Station EVs

RENs Production

Smart charging

State Of Charge

Time of departure

EV tracking

A wide set of B2B / M2M interfaces needs to be established for product implementation

and service execution

Load Management

LV/MV Grid monitoring

RENs integration

Smart Charging: IT interfaces

Page 19

DSO

DMS

EV Smart-Grids Integration

EVSE Operator

Load Area IT-ENE-001-0001

RENs Traceability & Forecast

0

10

20

30

40

50

60

1 3 5 7 9 11 13 15 17 19 21 23

Desired Load Area Target Curve

kW

hours

Customer Preferences

DER Operator

{ Smart charging State Of Charge

Time of departure

EV tracking

0

10

20

30

40

50

60

1 3 5 7 9 11 13 15 17 19 21 23

Effective vs Ideal Target Curve

Ideal

Effective

hours

po

we

r

Smart Charging: Projects exploitation

po

we

r

09.03.2015 Page 20

Smart Charging: next steps in EU

A position paper over Smart Charging from EU electricity industry, released on March 24th

To go forward with smart charging research and development within H2020 calls

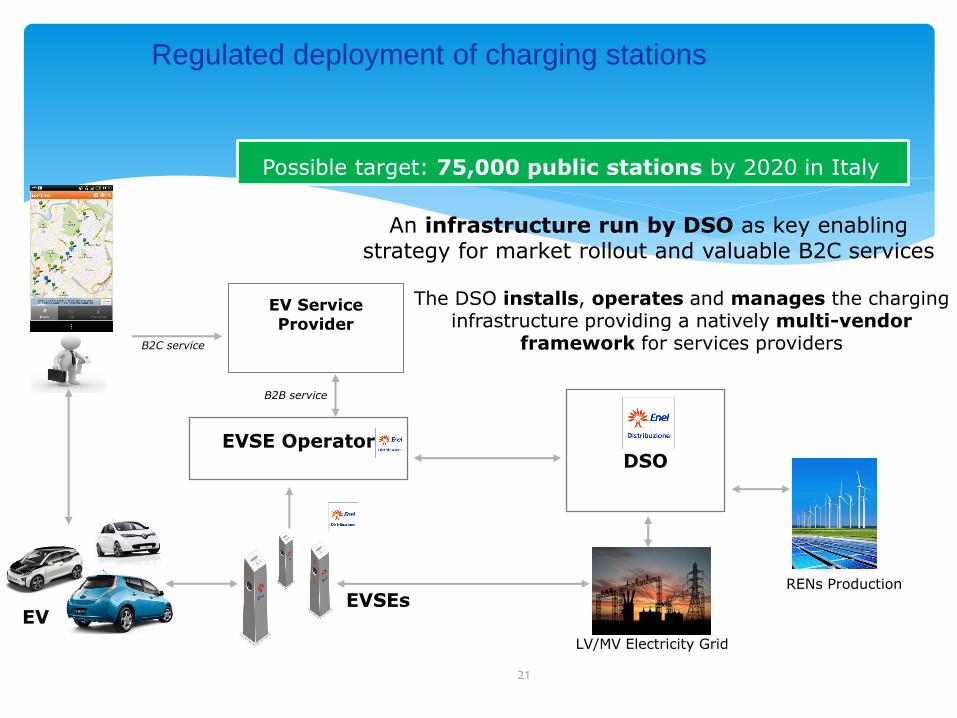

Regulated deployment of charging stations

21

B2C

DSO

LV/MV Electricity Grid

EV Service Provider

B2C service

B2B service

EVSE Operator

EVSEs EV

RENs Production

An infrastructure run by DSO as key enabling strategy for market rollout and valuable B2C services

The DSO installs, operates and manages the charging infrastructure providing a natively multi-vendor

framework for services providers

Possible target: 75,000 public stations by 2020 in Italy

Thank you

Giovanni COPPOLA Product Manager of Enel SpA

End-Customer Application & New Technologies

3rd E-MOBILITY STAKEHOLDER FORUM

Charging Infrastructure Effects of Electrifying Rotterdam’s City Fleet

Jos Streng Roland Steinmetz (Traffic & Transport Planner, City of Rotterdam) (EV Consult)

Rotterdam

Stakeholder Forum

Historical development of City and Port

Contents

o Overview

o Brainstorming objectives

An attractive place to be…

EC-sources abroad

rest of NL

local traffic

industry shipping

consumers

…but it should and could even be better….

How the city tries to clear the air

Ecostars (fleet recognition scheme for companies & organisations, more Ecostars means more sustainable –public- image and more traffic-related privileges)

Green Deal Zero Emission Urban Distribution 2020 (declaration of intent, signed by city, companies and TNO research institute)

FREVUE (demonstrating the use of E-trucks & vans for Urban Distribution, and investigating conditions for large scale introduction)

Minimizing emission from our duty vehicles (replacement of vehicles by fully electric, unless…)

Basic figures

o 614.00 inhabitants, 319 km2, (113 km2 water)

o Captive fleet of 1343 four-wheeled duty vehicles:

(63% diesel, 20% hybrid, 14% gasoline, 3% electric)

- 470 passenger cars - 270 small vans - 196 pickups with various equipment (cranes, compressors, etc.) - 400 trucks & special vehicles (refuse, sewage suction)

o 222 scooters, bicycles and segways (96% E)

60% of passenger cars and light vans can be electrified

XYZ

o Text here

o Text here

Where do these cars spend the night?

Property Rented locations Number of vehicles

Small (1 to 4)

Medium (5 to 9)

Large (10 to 19)

Super (20 or more)

Total

Analyzed scenarios

Standard: all vehicles charge overnight at 11 kW Power Connections upgraded when necessary

Smart: locations with 5 or more vehicles get 70% occupation, vehicles with more than 120 km/day get 11 kW, other vehicles 3,7kW

Fast and Smart: 1 fast charger per 8 vehicles at locations with 20 or more vehicles

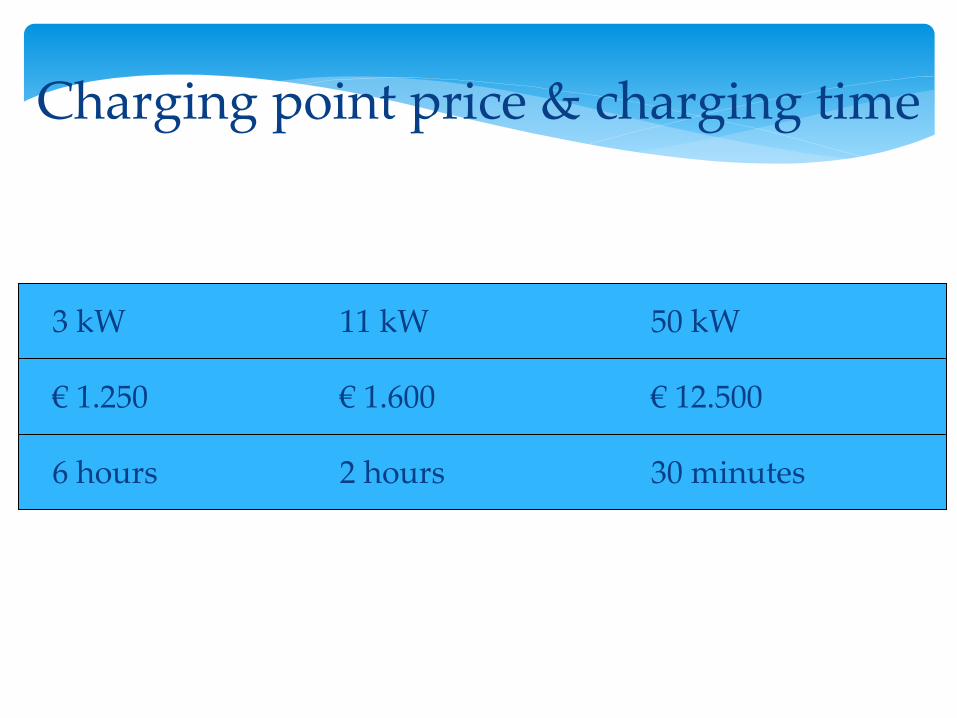

Charging point price & charging time

3 kW 11 kW 50 kW

€ 1.250 € 1.600 € 12.500

6 hours 2 hours 30 minutes

Fuel savings (238 vehicles)

Current annual Corresponding Annual savings fuel expense electricity cost

€ 390.000 € 70.000 € 320.000

Interesting detail: those who pay the fuel don’t pay the electricity bill

Avoided PM10 emission (238 vehicles)

Average PM10 Average annual Annual savings emission per km mileage (km) (g PM 10)

0,0025 g/km 16.592 10.086

Charging infrastructure requirements (per scenario)

Standard: 238 charging points 11 kW 14 connection upgrade of 175 kVA 1 connection upgrade of 300 kVA

Smart: 167 charging points 3,7 kW 12 charging points 11 kW 4 connection upgrade 175 kVA

Fast and Smart: 127 charging point 3,7 kW 10 charging points 11 kW 8 fast chargers 50 kW 4 connection upgrade 175 kVA

Financial implications (indicative)

Hardware (as indicated)

Installation (about the same cost as charging point, based on experience over the last year with 50 points)

Power connection upgrade (Stedin estimate)

Charging point exploitation (offer by supplier)

Periodic costs

Depreciation in 8 years

15% contingencies

Show me the money…..

Scenario Hardware Installation Connection

upgrade Total

Annual

(8 years)

Standard 382.400 382.400 84.312 976.479 180.000

Smart 227.950 286.400 15.368 609.176 105.000

Fast and Smart 274.750 214.400 15.368 600.436 100.000

Perspective o Taking fuel savings into account, 50-75 € per vehicle per month would

be available to improve the business case for the vehicle

o Final decision on scenario and speed of introduction is being prepared (e.g. facility managers include maintenance cost in regular budget).

o For one fleet owner, the implications are far reaching but overseeable.

o But if FREVUE would be succesfull, and our Green Deal would become reality (hence all business trucks and vanselectric by 2020), the grid operator should prepare for a huge strategy adaptation.

o Therefore, a joint research project to determine the match between projected demand and current grid capacity is being prepared.

o If all vehicle kilometers in Rotterdam would be electric, an additional 200 MW of continuous electric power would be required.

3rd E-MOBILITY STAKEHOLDER FORUM

Making the connection

Kai Tullius European Commission

DG ENERGY

Directive on the deployment of alternative fuels infrastructure (AFID)

Facilitate development of a single market for alternative fuels vehicles (electricity, natural gas, LNG, CNG, hydrogen) and infrastructures

Focus on the "missing links" – infrastructure and standards

Remove technical and regulatory barriers across the EU

• "Appropriate number" of recharging points accessible to the public at least in urban agglomerations → MSs national policy frameworks

• Number of EVs estimated to be registered by 2020

• Best practices and recommendations by the Commission

• As an indication: 10 cars per recharging point

• Additional recharging points to be put in place by 31/12/2025 could be proposed by the Commission

• Measures to facilitate private recharging points

Minimum infrastructure by 2020

Charging Infrastructure

• Publicly recharging points shall, if technically feasible and economically reasonable, make use of intelligent metering systems

Integration in the electricity system

The use of intelligent metering systems: 1) Contributes to the stability of the grid 2) Enhances consumer protection and demand response 3) Incentivizes the development of new business models 4) It is an affordable investment 5) Reinforces the coherence of EU energy policy (Third Energy Market Package)

Integration

• "Ad-hoc" charging without contract

• Consumers can contract electricity simultaneous with several suppliers

• Prices at publicly accessible recharging points reasonable, easily and clearly comparable, transparent and non-discriminatory

More flexibility for consumers

• Any person can establish or operate publicly accessible recharging points

• Operators are free to purchase electricity from any EU electricity supplier

• DSOs cooperate on a non-discriminatory basis with recharging point owners or operators

Recharging service – market driven

Market Rules

• AC normal and fast recharging points with connectors of type 2

• DC fast recharging points with connector of type "Combo 2"

EU common standards for charging plugs

Standards

Coordination

National

• National policy frameworks (NPF):targets and actions for development of market and deployment of infrastructure

• Population density and geographical characteristics to consider

• Notification to the Commission 2 years after entry into force of AFID

Regional

• Cooperation with neighbouring countries by means of consultations or joint policy frameworks

EU

• The Commission shall facilitate the exchange of information and best practices

• Responsible for the publication and updating of information on the national targets

• It shall assess the coherence of NPF and assist MSs in the cooperation process

• Adoption of guidelines concerning the reporting on the implementation of NPF

Thank you

Kai Tullius European Commission

DG ENERGY

![“While there’s life, there’s hope .” — Marcus Tullius Cicero [Add an image]](https://img.pdfslide.us/doc/110x75/56813424550346895d9b1068/while-theres-life-theres-hope-marcus-tullius-cicero-add.jpg)