Embed Size (px)

Citation preview

Stainless Steel Materials

South African Fund Manager Presentation : June 2003

Dr Chris Pointon – President, Stainless Steel Materials Customer Sector Group

SSM SA Fund Manager Presentation June 2003Page 2

SSM already has a established production and marketing presence

NewIndonesia

AustraliaWestern

Operations

Exploration

Ni/Cr marketing office

Caledonia

Cerro MatosoColombia

South AfricaSamancor Chrome

QNIYabulu

Refinery

Philippines

The Hague - Marketing

SSM SA Fund Manager Presentation June 2003Page 3

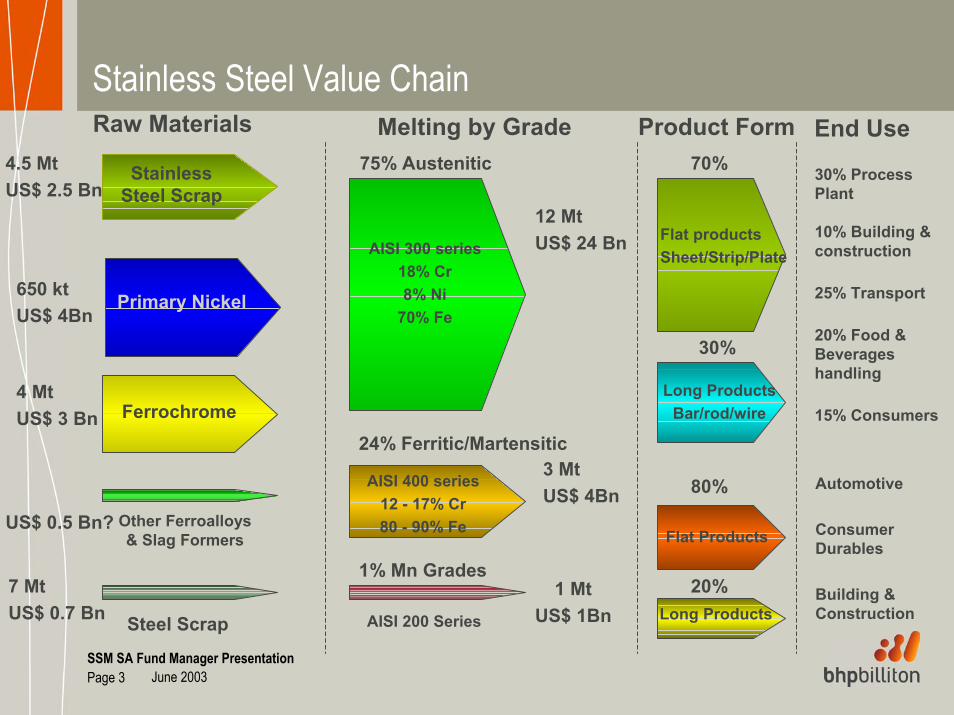

Stainless Steel Value Chain

Steel Scrap AISI 200 Series

Automotive

Consumer Durables

Building &Construction

StainlessSteel Scrap

Primary Nickel

Ferrochrome

Other Ferroalloys & Slag Formers

75% Austenitic

AISI 300 series18% Cr8% Ni

70% Fe

24% Ferritic/Martensitic

AISI 400 series12 - 17% Cr80 - 90% Fe

1% Mn Grades

4.5 MtUS$ 2.5 Bn

650 ktUS$ 4Bn

4 MtUS$ 3 Bn

US$ 0.5 Bn?

7 MtUS$ 0.7 Bn

70%

80%

30%

20%

Flat productsSheet/Strip/Plate

Long ProductsBar/rod/wire

Flat Products

Long Products

30% Process Plant

10% Building & construction

25% Transport

20% Food & Beverageshandling

15% Consumers

12 MtUS$ 24 Bn

3 MtUS$ 4Bn

1 MtUS$ 1Bn

Raw Materials Melting by Grade Product Form End Use

SSM SA Fund Manager Presentation June 2003Page 4

Stainless Steel is the fastest growing major use of metals, and will continue to grow strongly

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000

W. Europe

USA

Japan

Russia Other

China

Stainless Slab Production – million tonnes

SSM SA Fund Manager Presentation June 2003Page 5

Chrome Value Chain – >80% of ore converted to FeCr, and 75% of FeCr used in stainless steels

OreOreProductionProduction

Chemical Chemical ProducersProducers

Integrated Integrated Alloyers Alloyers

85%85%

Independent Independent Alloyers Alloyers

15%15%

10%10%

8%8%

82%82%

LowLow--carboncarbonferrochromeferrochrome Other usesOther uses 25%25%

5%

MediumMedium--carboncarbonferrochromeferrochrome 3%

Stainless SteelStainless SteelProductionProduction 75%75%

HighHigh--carboncarbonferrochrome &ferrochrome &Charge chromeCharge chrome 92%

* Percentages based oncontained chrome units

RefractoriesRefractories& Foundries

Ferrochrome production 2000LCFeCr = 240 ktMCFeCr = 140 ktHCFeCr = 4900 kt

& FoundriesTotal = 13 Mtpa

Source: Samancor

SSM SA Fund Manager Presentation June 2003Page 6

Austenitic Stainless has maintained a strong growth trend. Primary Ni and FeCr inputs will grow proportionately faster as scrap supply is constrained

CAGR1989-2002

Projections2003-2010

>4.5%

5.4%

6.7%

4.4%

>5%

3.1% >5.0%

>5%

Primary Growth - Rising to 5%paSecondary Growth - Exceeding Primary

0

1,000

2,000

3,000

4,000

5,000

6,000

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 20020

2000

4000

6000

8000

10000

12000

14000

16000

Austenitic Steel Production(Right Hand Scale)

Primary Nickel production

High Carbon Ferrochrome Production

Stainless Steel Scrap (*)

kt

Note: * Excludes internal scrap

SSM SA Fund Manager Presentation June 2003Page 7

The primary nickel supply business has high financial and technical barriers to entry

Buyer power

LOW

Threat ofsubstitution

Industryrivalry

MODERATE TO HIGH

Market demand growing @ 4-5%pa

MODERATE TO HIGH

High Capital Intensity, Technical

Complexity

Capital Efficient Growth

Barriers to entryHIGH

Supplier power

HIGH

Growth Sustainability

SSM SA Fund Manager Presentation June 2003Page 8

A primary nickel supply gap is set to emerge over the present decade. Only three major projects at Feasibility. Lead times for new projects are 7-10 years. The majority of current production is from sulphide mines, but most new nickel projects will be from laterite ores.

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Use

GoroVBN

Brownfield expansions

Capacity in 2002 less sulphide depletion

BHPBilliton

“Supply Gap”

Market surplus

Nickel reserves Nickel production

oxide 75%

sulphide 25% oxide40%

sulphide 60%

Mt

SSM SA Fund Manager Presentation June 2003Page 9

Cerro Matoso Project – Colombia – 99.8% OwnershipProduction History

Reserves : 46.9Mt @ 1.93% NiResources : 65.4Mt @ 1.75% NiNB based on 1.1% Ni cut-off

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

83 88 93 98 2000 2001 2002 2003

1.00

1.50

2.00

2.50

1998 1999 2000 2001 2002 2003

Year Ending June

US$/l

b Ni

(Rea

l 200

3)

C1 Cost C3 CostLost Time Injury Frequency Rate

012345

1998 1999 2000 2001 2002 2003

LTIF

R

Year Ending June

SSM SA Fund Manager Presentation June 2003Page 10

The QNI strategy

Stabilise Yabulu operation

• Zero harm • Catch-up maintenance. • Commence installation of

modern management practices.

Utilities due forcompletion in FY04

Ore processing plants at world class orebodies with expansion of refinery part of Yabulu

• Phase I:Concurrently develop Ravensthorpe and Yabulu Extension Projects.

• Phase II:Develop 2nd Ore Processing project at suitable orebody with no further expansion of Yabulu

Feasibility Study

Optimise Yabulu margins

• Incremental value-added product development.

• Incremental Ni and Co production increases:

•YOI quick payback project suite

•LGSO strategy• Cost reduction initiatives:

•Small group projects•Capitalise on gas at Yabulu site

•Best management practices, particularly Maintenance

• Establish own mine for up to one third of ore supply.

In Progress

SSM SA Fund Manager Presentation June 2003Page 11

QNI Yabulu – Australia - 100% Ownership

25,000

26,000

27,000

28,000

29,000

30,000

31,000

32,000

1998 1999 2000 2001 2002 2003

Year Ending June

Tonn

esNi

0123456789

LTIF

R

Nickel - Tonnes

LTIFR

Yabulu Site Cash Cost of Production after Cobalt Credits

2.50

2.75

3.00

3.25

FY00 FY01 FY02 FY03

US$

/ lb

Site Cash Cost of Production after Cobalt CreditsLinear (Site Cash Cost of Production after Cobalt Credits)

Normalised on FY03 Assumptions:LME $3.44 US$/A$ 0.584 Oil A$301/t Coal A$60/tLMB $7.34 Insurance A$5.7m Naphtha A$734/t

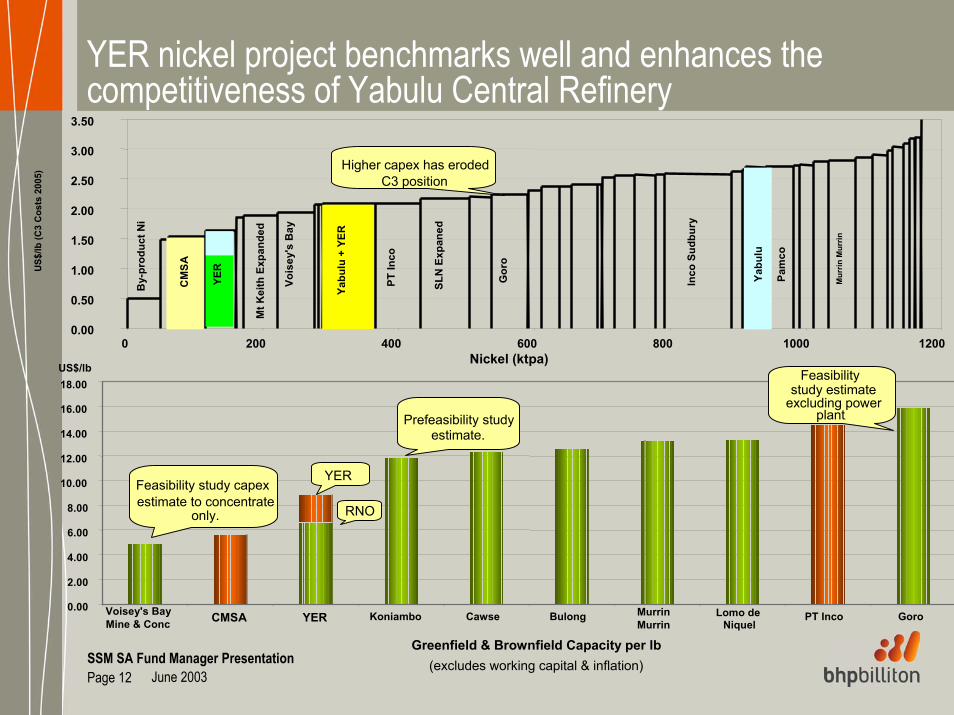

SSM SA Fund Manager Presentation June 2003Page 12

Greenfield & Brownfield Capacity per lb(excludes working capital & inflation)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Voisey's BayMine & Conc CMSA YER Koniambo Cawse Bulong Murrin

MurrinLomo de

NiquelPT Inco Goro

US$/lb

YER

RNO

Feasibilitystudy estimate

excluding power plant.

Feasibility study capex estimate to concentrate

only.

Prefeasibility study estimate.

Nickel (ktpa)

US$/

lb (C

3 C

osts

200

5)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

0 200 400 600 800 1000 1200

CM

SA

Mt K

eith

Exp

ande

d

Vois

ey's

Bay

YER

Yabu

lu+

YER

PT In

co

SLN

Exp

aned

Gor

o

Inco

Sudb

ury

Yabu

lu

Pam

co

Mur

rin M

urrin

Higher capex has eroded C3 position

By-

prod

uct N

i

YER nickel project benchmarks well and enhances the competitiveness of Yabulu Central Refinery

SSM SA Fund Manager Presentation June 2003Page 13

The FeCr industry has high internal rivalry, low barriers to entry, but growth is strong and there is no substitute, except for scrap

Low capital cost per tonne FeCr capacity

Threat ofsubstitution

LOW

Barriers to Entry

LOW

Buyer power

HIGH/CYCLICAL

Depends upon SS cycle and scrap availability

IndustryrivalryHIGH

SA to remain ore-long

Supplier power

HIGH

No substitute for Cr, but scrap cyclical

SSM SA Fund Manager Presentation June 2003Page 14

Ferrochrome demand growth outlook is robust – supply side is thus the issue

0

2,000

4,000

6,000

8,000

10,000

12,000

14,00019

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000Ferrochrome Demand (LHS)Stainless Steel Production (RHS)

(kt) (kt)

•Stainless growth 2005 – 2020: assumed 5% per annum•Ferrochrome demand = Stainless + other uses consumption•Growth rate of secondary chrome units decline from 2005 onwards

Growth Rates1990-1995

1995-2000

2000-2005

2005-2010

2010-2020

Total Ferrochrome demand growth (%) 4.7% 3.0% 4.0% 4.7% 5.2%No. of standard 120 kt furnaces required per annum 1.3 1.0 1.6 2.4 3.8

SSM SA Fund Manager Presentation June 2003Page 15

South Africa dominates the primary FeCr sector and will have the major share of future expansions

Zimbabwe19%

India1%

Finland1%

Kazakhstan7% Other

2%

South Africa70%

Source: Samancor

World Chrome Ore Reserves

Scandinavia9% Kazchrome

15%

Zimbabwe7%

Asia12%

Other8% Samancor

16%

ASA1%

Feralloys5%

Hernic5%

Xstrata20%

SA Chrome1%

World Primary Chrome Supply

SSM SA Fund Manager Presentation June 2003Page 16

Ferrochrome falling price trend is a continuing challenge to theindustry

20

40

60

80

100

120

140

160

1980

1985

1990

1995

2000

USc/lb (Real)

CAGR Price (80 - 00) = -3.24%

CAGR Cost (80 - 00) = -4.3%

Source: CRU, Samancor Analysis

Largest risk s to cost

•Reductants

•Electricity

SSM SA Fund Manager Presentation June 2003Page 17

South Africa has failed to create industry discipline for FeCrgrowth, and has exported most of the value of its dominant supplier position

60%

80%

100%

120%

140%

160%

180%

1996 1997 1998 1999 2000 2001 2002

SA FeCr Production

SA FeCr Revenue

Revenue in real US$ based on CRU US Import list price – 50-55%

CAGRProduction + 6.6%Revenue -2.0%

Xstrata 620 ktHernic 260 kt - new entrantSA Chrome 230 kt – new entranAssmang 200 ktSamancor 160 ktASA 60 kt – new entrant

SA has been the price setter in the industry in the past 7 years

But the total revenue to SA industry declined in real terms since 1996

SA Accounted for the 100% of net increase in FeCr world capacity since 1995 (1.53Mt)

Index SA production and Revenue (1996-2002)

SSM SA Fund Manager Presentation June 2003Page 18

BEE and the Ferrochrome business

3500

4000

4500

5000

5500

6000

(kt)

0

100

200

300

400

500

600

700

Capacityadditions

Demand

Supply

Capacity additions 40 220 260 348 482 336Demand 4530 4599 4409 4717 5011 5076 5374Supply 4622 4918 4040 4350 4976 5458 5794

1999 2000 2001 2002 2003 2004 2005

• The historic trend in SA capacity growth will continue. Entry barriers will be lower, as producers will not be able to retain unutilised resources.

• However, costs will rise - Rand, reductantcosts, increased electricity prices, social obligations for South African producers.

• Will HDSA participation in FeCr Smelters be profitable?

Hence HSDA business focus will likely center on:

• Procurement

• Mining and ore preparation

• Community development

• New smelting where there is a genuine low cost position

SA Project IRR ~ 12.5% Real

20

22

24

26

28

30

32

34

36

38

0.08 0.1 0.12 0.14 0.16 0.18 0.2 0.22 0.24Electricity Price R c/kWh

Cr R

ealiz

ed p

rice

CIF

US

c/lb

8 R:US$ 9 R :US$ 10 R:US$

SSM SA Fund Manager Presentation June 2003Page 19

Samancor Chrome (60% Ownership) : a Turnaround Asset

Reserves : 40Mt @ 42.4% CrResources : 570Mt @ 43.3% CrNB based on 38% Cr cut-off

PRODUCTION FACILITIES SOUTH AFRICA

Chrome OreFerrochrome

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

WCM Tubatse (incl ECM)

Ferrometals/IC3 MFC/MTC

SSM SA Fund Manager Presentation June 2003Page 20

Restructuring of Chrome Division by a 3 Horizon Strategy

Manufacturing mindset to reposition chrome at the bottom of the cost curve

• Zero harm • People lynchpin everything. • Eliminate waste.• ETG, furnace and mine stability, Procurement & contractor management, maintenance, GSAP&MES, Six Sigma. • Site specific cost reductions.

Reposition in Future Industry Context•Understand emerging industry dynamics. •Understand SA Government approach to FeCr industry.•Understand new product requirements in advance of the rest of the producers by working with customers.

•Increasing business maturity•Improving market / production interface

Optimise value chain through prudent investment•Understand future customer requirements.•Implementing high IRR capacity creep projects at the works.•Rationalise the mines with the value chain as the driver.

SSM SA Fund Manager Presentation June 2003Page 21

Variable cost drivers + results against benchmark show positive trends.

3.903.794.083.98SEC (k/Wh/ton)

50.976.510.642.49

FY03

50.951.151.3Cr content (%)74.172.2379.24Cr Recovery (%)0.630.650.64Reductant (t/t)2.542.582.43Ore (t/t)

FY02FY01FY00Cost Driver

Smelter Cost (R/t Real 2000)1700

1600

1400

1500

1300FY00 FY01 FY02 FY03

Samancor Benchmark

SSM SA Fund Manager Presentation June 2003Page 22

800

900

1000

1100

1200

1300

1400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2000 2000 2000 2000 2001 2001 2001 2001 2002 2002 2002 2002 2003 2003 2003 2003 2004 2004 2004 2004

-200

-100

0

100

200

300

400

500

600

700

800

900Cumulative Balance (Right-hand scale) Production Demand

Supply and demand balance – Samancor production

Forecast

(000

’t)

(000

’t)(0

00’t)

250

270Samancor Production

230

210

190

170

150

SSM SA Fund Manager Presentation June 2003Page 23

Conclusion

• Stainless steel – the highest growth major use of metals – provides a strong market for primary FeCr and Nickel

• A looming nickel supply gap is becoming apparent, a result of high entry barriers and inadequate returns on capital in 1990s

• SA will provide new FeCr capacity to meet the strong, but volatile, demand growth

• Uncontrolled FeCr capacity growth in SA has led, and may continue to lead, to significant value transfer to overseas customers.

• For Samancor Chrome, cost-efficiency is key, as input costs in SA are likely to increase

• BHP Billiton is a mature nickel producer, customer-focused with options for further capital-efficient growth