Embed Size (px)

Citation preview

STABILITY AND SUSTAINABILITYIN BANKING REFORM

in association with

Are environmental risks missing in Basel III?

2

Copyright © 2014 University of CambridgeInstitute for Sustainability Leadership (CISL).Some rights reserved. The material featuredin this publication is licensed under theCreative Commons Attribution-NonCommercial-ShareAlike License. The details of this license may be viewed infull at http://creativecommons.org/licenses/by-nc-sa/4.0/legalcode.Cover image: Getty Images

ReferencePlease refer to this paper as Stability andSustainability in Banking Reform: AreEnvironmental Risks Missing in Basel III? (CISL& UNEP FI, 2014).

DisclaimerThe opinions expressed in this report are theauthor’s own and do not represent an officialposition of CISL, the BEI or UNEP, or of any oftheir individual members.

CopiesThis full document can be downloaded inEnglish, and its Executive Briefing in a range of different languages, from the CISL andUNEP FI websites: www.cisl.cam.ac.uk &www.unepfi.org.

ContactTo obtain more information on the report,please contact the Cambridge Institute forSustainability Leadership (CISL) or the UnitedNations Environment Programme FinanceInitiative (UNEP FI):

Andrew Voysey, University of CambridgeInstitute for Sustainability Leadership

Careen Abb, UNEP Finance Initiative

Manuscript completed August 2014.Cambridge and Geneva, 2014.

This report aims to trigger a deeper reflection amongst financial policymakers and regulatorsconcerning the relevance of systemic environmental risks to banking sector stability. Recent historydemonstrates linkages between risks arising both from the environment itself (e.g. extremeweather events) and from humanity’s management of environmental resources (e.g. soil quality)and banking instability. Evidence suggests this trend will become more pronounced and complex ashumanity breaches more planetary boundaries.

However, international banking regulation (i.e. the Basel Capital Accord or ‘Basel III’) does notaddress the financial stability risks associated with systemic environmental risks. Nevertheless, agroup of countries including Brazil, China and Peru, along with their banking industries, haveadopted regulatory and governance practices to address systemic environmental risks. The BaselCommittee should learn more from their experiences and consider reforms to the Basel III Pillar 2Supervisory Review framework and the Pillar 3 Market Discipline framework that would involverecognising systemic environmental risks as material risks that potentially threaten banking stability.

In addition to Basel III, certain financial policies should be considered. Central bank monetary policymeasures could enhance the provision of bank credit to environmentally sustainable economicactivity. Also, the role of financial innovation should be considered as it relates to an array of creditrisk transfer instruments that can be used to enhance the amount and quality of funding availablefor environmentally sustainable economic activity. Finally, financial policy and regulation should bealigned with environmental policy and regulation and coordinated so that the objectives andunderstanding of each area of expertise can be shared between the relevant agencies. This wouldcreate synergies for policy development and regulatory practices and standards.

Abstract

3

Foreword 4

Executive briefing 7

1. Introduction 9

2. Are systemic environmental risks and banking instability linked? 11

3. Does Basel III adequately address systemic environmental risks? 13

a) How does Basel III currently treat systemic environmental risks? 15

b) Do Basel III’s Pillar 1 ‘Minimum Capital Requirements’ discourage the financing of environmentally sustainable economic activities? 15

c) Are there existing regulatory and market practices outside of Basel III that are relevant to this study? 16

d) How might the Basel Committee take forward the lessons of this study? 18

4. What other financial policy options are available? 22

a) Monetary policy 22

b) Financial innovation 23

c) Joining up banking regulation with environmental policy 23

5. Conclusions and recommendations for financial policymakers and regulators 25

Appendices

a) Planetary boundaries explained 27

b) Overview of current frameworks to include environmental risks in banking 28

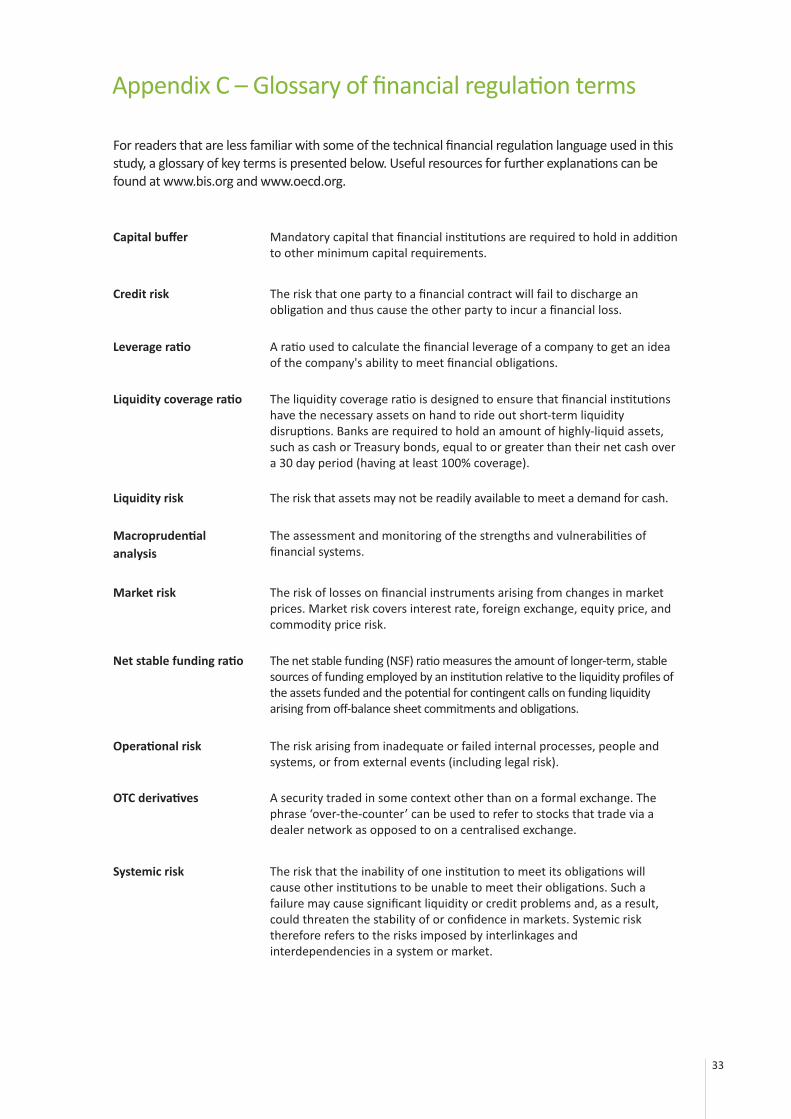

c) Glossary of financial regulation terms 33

References 34

Interviews and seminars 38

About us 39

Contents

4

Foreword – The Banking Environment Initiative andCambridge Institute for Sustainability LeadershipThe Banking Environment Initiative (BEI) wasfounded by a group of leading bank ChiefExecutives in 2010 and is convened by theUniversity of Cambridge Institute forSustainability Leadership (CISL). It was formed outof the belief that a fresh approach was needed bybanks to help support socially andenvironmentally sustainable economicactivity.

The BEI’s initial focus has been threefold: first,developing customer partnerships to re-alignbanks’ goals with those of the real economy;second, driving industry-level consensus onstandards to accelerate what banks can doindividually, and third, supporting innovation inproducts and services to stimulate the marketthrough commercially viable action.

With the help of CISL’s networks of corporateleaders and its ability to drive learning andchange across diverse groups, the BEI hasdemonstrated how this model can be applied tofinancing activities that support commoditysupply chains. The BEI’s ‘Soft Commodities’Compact with the Consumer Goods Forum istriggering an evolution in how banks and theircorporate customers, through trade financeproduct and services, direct capital towardssustainable practices in agricultural supply chains.

However, we have always known that it takesmore than strong corporate leadership to changepractices at an industry level; those who set therules that govern the system also have a role.

Since the financial crisis of 2008, we havewitnessed some regulators, especially in thefaster-growth economies, concluding that

financial stability may not only emanate fromwithin the financial system itself. As waspowerfully demonstrated at the China-focusedBEI Forum 2014 in Hong Kong, some countriesare already acting on their view that systemicenvironmental risks can also affect stability.

In anticipation that momentum behind this trendwould only build – as well as the simple fact thatsome of the emerging economies where thisthinking is already further progressed will beincreasingly influential on the global stage – theBEI decided, on behalf of its members, to initiatean independent process to look at these issuesand how regulators around the world areaddressing them. We were delighted thatProfessor Kern Alexander, a CISL Fellow and Chairin Law and Finance at the University of Zurich,agreed to lead the study. We were also verypleased that UNEP FI, with its uniqueperspective at the interface betweengovernments and the finance sector, alsorecognised the value of this inquiry anddecided to co-commission the work with us.

This study assesses the links between systemicenvironmental risks and financial stability andoffers insights into how some members of theBasel Committee are already acting on such links.Building on this leadership at a national level, thefocus then turns to how such approaches mightbe harmonised internationally.

As the report itself says, this is a study thatclearly has profound implications. Furtheranalysis will certainly be required to assessthe feasibility of implementing its variousrecommendations and we look forward toplaying an active role in that debate.

Polly Courtice LVODirector, University of Cambridge Institutefor Sustainability Leadership (CISL)

Jeremy Wilson Chair – Banking Environment Initiative(BEI) Working Group

5

Foreword – United Nations Environment Programme– Finance Initiative

While the global economy continues to beaffected by the profound financial crisis of 2008,the world faces the twin challenges of dealingwith the consequences of climate change and anunsustainable path for economic growth.

These trends are not unrelated and, since itsinception in 1992, UNEP Finance Initiative (UNEPFI) has been a firm believer in the role of thefinance sector in setting a new course towards agreener economic model.

UNEP FI, the UN’s unique and dedicated financeand sustainability partnership, was initiated by apioneering group of commercial banks and nowcounts a strong, international bankingmembership that coalesced in 2010 as theInitiative’s Banking Commission.

The Banking Commission has pursued an agendawith a strong focus on catalytic action on theground - it has supported, and continues tosupport, many of the country frameworks onsustainable finance alluded to in this report.

UNEP FI’s Position Paper at Rio+20 and thesubsequent holding of its Global Roundtable inBeijing in 2013 with a focus on policy andregulation have been instrumental in bringingthis topic to an international audience.

Professor Alexander’s report is the natural andnecessary next step in exploring the role thatfinancial – and in particular banking – regulationcan play in the transition to a green economy.

Not only does this report provide clarity on thelinks between environmental sustainability andeconomic stability; clarity that is needed toestablish the pertinence of addressingenvironmental risk in banking regulation. It alsoshows that in today’s world, practitioners andtheir regulators can be found to be willing toengage constructively in the global policy debateon how to build ‘the future we want’.

Indeed, while a banking regulatory regime whichis cogniscent of environmental challenges andwhich as a consequence provides appropriateguidance to banks is important, of greaterimportance still is the emergence of a robust andcontinuous dialogue between financial andenvironmental policy-makers. The changesrequired will not be possible without greaterpolicy coherence and cohesion between thesetwo constituencies.

We are proud to have partnered with the BEIand CISL for this first research piece oninternational financial regulation andenvironmental risks, harnessing the full power ofCambridge’s academic excellence. ProfessorAlexander’s paper is intended to provoke debate,and it is our aspiration that the content, theconclusions and the recommendations will serveto inspire the financial policy community to anew way of thinking about the interdependenceof finance and sustainability. We look forward toparticipating in the engagement which willfollow, and in the further research and analysiswhich will contribute to this dialogue.

Charles Anderson Head, UNEP FI Secretariat

Dag Arne Kristensen Chair, UNEP FI Banking Commission

This report was made possible by a partnership between the Banking Environment Initiative(BEI), which is convened by CISL, and UNEP FI’s Banking Commission, with additional supportfrom Bloomberg LP.

The principal investigator and lead author of the report was Professor Kern Alexander, Facultyof Law, University of Zurich and CISL Fellow. Professor Alexander led a research team at theUniversity of Zurich that included Thomas Strahm and Alexandra Balmer.

The study design and editorial process were led by Andrew Voysey (Director – Finance SectorPlatforms, CISL), Dr Jake Reynolds (Director – Business Platforms, CISL) and Careen Abb (BankingCommission Coordinator, UNEP FI). Rosie Jennings (CISL) managed the production process.

The study was further supported by the valuable guidance of an Advisory Group made up ofBEI and UNEP FI members.

Acknowledgements

6

7

In the wake of the 2007-08 financial crisis, anextensive reform of banking regulation wasinitiated to “generate strong, sustainable andbalanced global growth”. At the same time,the Earth’s planetary boundaries – defined asthresholds that, if crossed, could generateunacceptable environmental changes forhumanity – are under increasing stress andrepresent a source of increasing cost to theglobal economy. Experts argue that such‘systemic environmental risks’ may beamongst the biggest risks that humanity facestoday. This study analyses whether the BaselCapital Accord (‘Basel III’) adequatelyaddresses systemic environmental risks in thecontext of its overriding objective of bankingstability.

Core FindingsThe analysis presented in this report suggeststhat the regulatory framework that governstoday’s banking system may not be being used toits full capacity; with some notable exceptions,systemic environmental risks appear to be in thecollective blind spot of bank supervisors.

Despite the fact that history demonstrates directand indirect links between systemicenvironmental risks and banking sector stabilityand that evidence suggests this trend willbecome more pronounced and complex ashumanity breaches more planetary boundaries,the current Basel Capital Accord does not takeexplicit account of, and therefore only marginallyaddresses, these issues.

By failing to addresses systemic environmentalrisks, Basel III is arguably overlooking animportant source of risk to the financial system

and broader economy, despite its overridingobjective of guaranteeing banking stability.

However, this report also offers insights thatsolutions are within reach, should regulators andindustry practitioners work together proactively.

A number of national authorities, especially inemerging markets such as Brazil, China and Peru,are already acting to use the existing regulatoryframework to address these links. Opportunitiesexist within the current Basel Capital Accord tolearn from these practices and to raise thestandard of how systemic environmental risksare managed internationally.

Additional options relating to monetary policyand measures to increase the potential for long-term investors to allocate capital toenvironmentally sustainable activities are alsoavailable to regulators.

Executive briefing

The role of the financial system in the economy and broader society is toprovide the necessary financing and liquidity for human and economicactivity to thrive – not only today but also tomorrow. In other words, itsrole is to fund a stable and sustainable economy. The role of financialregulators is to ensure that excessive risks that would threaten the stabilityof the financial system – and hence imperil the stability and sustainabilityof the economy – are not taken.

“ ...the regulatory frameworkthat governs today’sbanking system may not bebeing used to its fullcapacity […] Basel III isarguably overlooking animportant source of risk tothe financial system andbroader economy”

8

Next stepsThese findings and recommendations clearly have profound implications. Further research isnecessary to assess the feasibility of their implementation. CISL and UNEP FI are keen toengage a multi-disciplinary and international process to this effect. This would include learninglessons from those national authorities that have already taken leadership steps and workingwith market actors to establish the most appropriate roles for them to play.

Recommendations1. The Basel Committee should explicitly acknowledge environmental risks and their

increasing impact on the stability and sustainability of the economy as an emerging sourceof systemic risk for banks and banking stability. On this basis it should encourage andsupport bank regulators to work with banks to adopt current best practice in themanagement of environmental issues, and to collect the necessary data and conductanalysis to refine the banking sectors' understanding of, and ability to address, systemicenvironmental risk in the future.

2. Bank supervisors should then explore the feasibility of incorporating forward-lookingscenarios that estimate the potential financial stability impact of supplying credit toenvironmentally unsustainable or sustainable activities over time into their Pillar 2 –Supervisory Review stress tests.

3. Bank supervisors should also examine Pillar 3 – Market Discipline to assess the feasibility ofbanks disclosing information about their exposure to, and management of, systemicenvironmental risks in a standardised manner across countries.

4. National financial authorities should consider their role in developing targeted monetarypolicy measures, such as accepting certain high-quality ‘green’ assets from banks as collateralfor central bank loans that would assist banks in providing more funding for environmentallysustainable economic activity.

5. As financial regulators are assessing standards and rules that allow banks and otherfinancial institutions to use simple and transparent financial instruments and investmentstructures to facilitate longer-term investment, they should aim to encourage moreinvestment in 'green’ assets and other forms of environmentally sustainable economicactivity. For instance, sustainable asset-backed securities issued in transparent and simplestructures could increase long-term investment in ‘green’ credit and related assets.

6. Finally, far greater effort must be made to ensure that financial and environmental policiesand regulations are coordinated across government agencies and departments in theirpromulgation, implementation and enforcement.

9

The role of the financial system in the economyand broader society is to provide the necessaryfinancing and liquidity for human and economicactivity to thrive – not only today but alsotomorrow. In other words, its role is to fund astable and sustainable economy. The role offinancial regulators is to ensure that excessiverisks that would threaten the stability of thefinancial system – and hence imperil thestability and sustainability of the economy – arenot taken.

In the wake of the financial crisis of 2007-08that resulted in trillions of dollars in losses andbank bail-outs, banking regulation hasundergone, and continues to go through, anextensive reform process, the core aim ofwhich is to “generate strong, sustainable andbalanced global growth” (G20 Summit Leaders’Statement 2009).

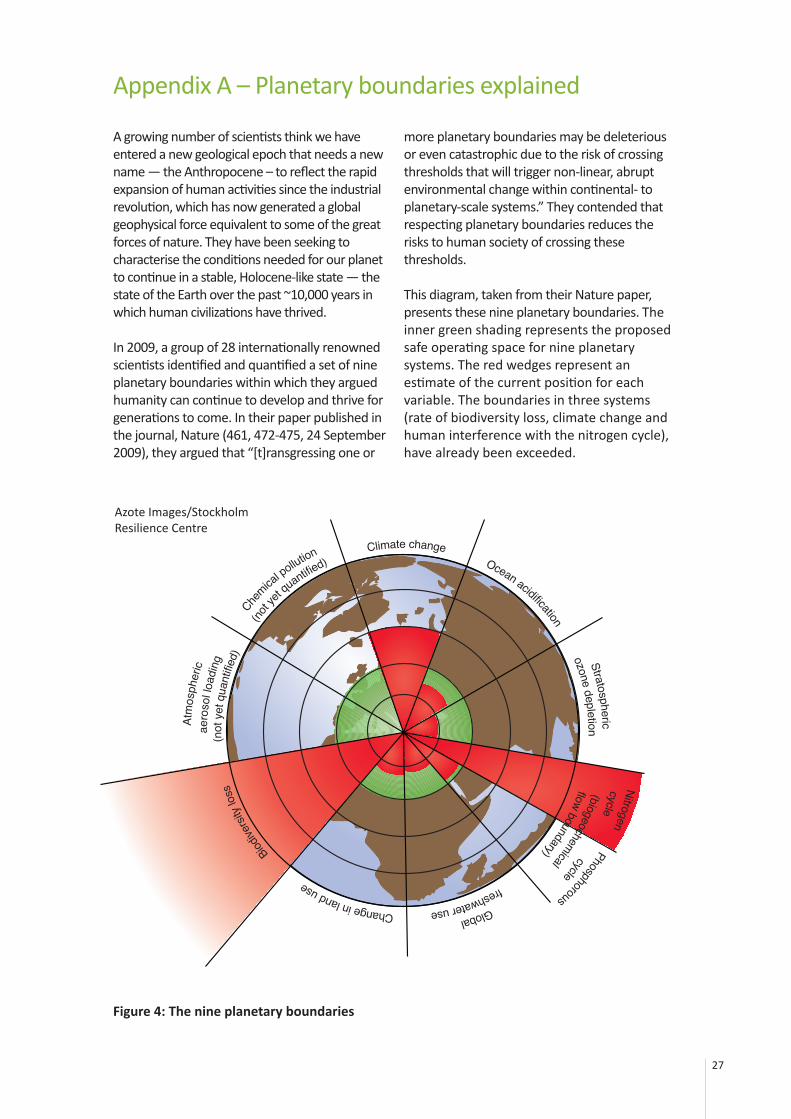

At the same time, the Earth’s planetaryboundaries – defined as thresholds that, ifcrossed, could undermine “the safe space forhuman development” (Rockström et al 2009) –are under increasing stress, and represent asource of increasing cost to the globaleconomy. Appendix A explains the concept ofplanetary boundaries in more detail. Expertsargue that such ‘systemic environmental risks’may be amongst the biggest risks thathumanity faces today.1 The scale of theeconomic and social impacts of such risks andof the economic transformation required toaddress them are both significant. A study bythe United Nations estimates that the annualcost to the global economy of maintaining thecurrent scale of unsustainable economicactivity will reach nearly $28.6 trillion by 2050,equivalent to 18 per cent of global GDP.2

Meanwhile, estimates indicate that around $1trillion of additional investment in new greeninfrastructure in energy, transport, buildingsand industry is needed annually to 2030 *(WEF,2013).

This study analyses whether the Basel CapitalAccord (‘Basel III’) adequately addressessystemic environmental risks in the context ofits overriding objective of banking stability. Itexamines the hypothesis that banking reform,despite its best intentions, could actually beoverlooking – and even aggravating – animportant source of risk to the financial systemand broader economy, namely systemicenvironmental risks.

Origins and rationale for the studyThis report was made possible by a partnershipbetween the Banking Environment Initiative(BEI), which is convened by CISL, and UNEP FI’sBanking Commission, with additional supportfrom Bloomberg LP. CISL and UNEP FI havebeen working together with partners in thebanking industry for many years to addressissues on finance and sustainability. In thecontext of this work, the role of financialregulation and policy in maintainingenvironmental sustainability has becomeincreasingly apparent. CISL and UNEP FI arekeen to promote research on this complex andunder-studied topic as part of their worktowards a financial sector that fullyunderstands, and plays its role in achieving,environmentally sustainable, financially stableand socially inclusive economic development.

This work arrives at a critical moment. InJanuary 2014, the United Nations EnvironmentProgramme launched its two-year Inquiry intothe alignment of the global financial systemwith long-term, sustainable development.3 Thiscomes in the wake of Rio+20, in which contextthe United Nations is striving to establish a setof Sustainable Development Goals (SDGs), andis exploring the means of implementing andfinancing them. In parallel, in 2012, theInternational Finance Corporation (IFC) startedgathering financial policymakers and regulatorsaround sustainability issues via the newlycreated Sustainable Banking Network.

Introduction

1 World Economic Forum ‘Global Risks 2010’: “The biggest risks facing the world today may be from slow failures or creeping risk...These are riskslinked to big shifts that are recognized....For example, global population growth, ageing and the ensuing rise in consumption, have implications forresources, climate change, health and fiscal policy”. http://www3.weforum.org/docs/WEF_GlobalRisks_Report_2010.pdf (accessed 07.08.2014)2 United Nations Environment Programme Finance Initiative 'Universal Ownership: Why environmental externalities matter to institutional investors’www.unepfi.org/fileadmin/documents/universal_ownership_full.pdf (accessed 07.08.2014)3 See United Nations Environment Programme (UNEP) Background Paper: ‘Inquiry: Design of a Sustainable Financial System’ (2014) http://www.unep.org/greeneconomy/financialinquiry/portals/50215/Inquiry_expanded.pdf (accessed 07.08.2014)

1

10

MethodologyThe report is based on research that involvedinterviews and written questionnaires forpractitioners in the banking industry, bankregulators from selected developed andemerging-market economies, officials frominternational organisations, and representativesfrom non-governmental organisations (detailsare listed at the end of the report). Theresearch also consisted of analysis of theprovisions of Basel III and selected nationalbanking laws and regulations along with theofficial publications of internationalorganisations on systemic environmental risks,such as the reports of the UN InternationalPanel on Climate Change. The analysis andrecommendations in the report wereconsidered and debated by members of thestudy’s advisory group, consisting of academics,financial sector and legal practitioners,regulators and representatives of governmentalbodies and the banking industry.

Report structurePart 2 explores the evidence relating to thequestion of whether systemic environmentalrisks and banking sector stability are linked. Itreviews the experience of recent history as wellas a selection of available evidence to showthat systemic environmental risks areassociated with banking sector instability.

Part 3 examines how Basel III currentlyaddresses systemic environmental risks. Thequestion of whether Basel III creates a biasagainst finance for environmentally sustainableeconomic activities is explored and examples ofsome countries that have already incorporatedsystemic environmental risks into bank capitalregulation are highlighted. Part 3 then considerswhat the Basel Committee might learn from theexample of these jurisdictions and identifieshow these lessons might be taken forward bythe Basel Committee, focusing on Basel III’sPillar 2 ‘Supervisory Review’ and Pillar 3‘Market Discipline’ frameworks.

Part 4 considers what other financial policyoptions are available outside of Basel III. Thisincludes an examination of the utility of certainother monetary policy measures and the use ofinnovative financial instruments – such as‘green’ asset-backed securities (ABS) – toenhance the flow of bank funds toenvironmentally sustainable economic activity.

Part 5 presents specific recommendations forfinancial policymakers and regulators abouthow Basel III and related areas of monetary andfinancial policy can be used more effectively toaddress systemic environmental risks. Finally,Part 5 sets out the conclusions of this studyoverall, and identifies next steps. It presentsspecific recommendations for financialpolicymakers and regulators about how Basel IIIand related areas of monetary and financialpolicy can be used more effectively to addresssystemic environmental risks.

11

Are systemic environmental risks and bankinginstability linked?2Economic historians have demonstratedrelationships between weather, agriculturalmarkets and financial markets to show thatthere are linkages between natural disasters(e.g. drought) and financial market instability.4

For example, the British economist WilliamJevons (1884) famously argued that financialcrises were produced by sunspots, whichcould be shown to cause drought and poorharvests in key agricultural producingcountries, which led to a downturn ininternational trade resulting in significantbank losses and related financial marketstresses. The United States suffered from dustbowls in the farm belt states in the 1880s and1890s and again in the 1930s due to soilerosion caused by unsustainable farmingmethods.5 The ensuing economic downturnsduring these periods resulted in substantiallosses on bank loans and related financialmarket distress which spread contagion-likethrough the regional economy.6

More recently, in the late twentieth and earlytwenty-first century, increased hurricaneactivity in the Caribbean and south easternUnited States caused huge bank losses tobusinesses and individuals directly impactedby these high wind storms. Hurricane Andrewcaused $24 billion in damages to the southFlorida economy in 1992, while hurricanesRita, Wilma and Katrina each causedwidespread and extensive damage toCaribbean economies and to the southeastern United States. Hurricane Katrina cameashore in south Florida in August 2005,causing in excess of $200 billion in damagesand ranks as one of the costliest naturaldisasters in U.S. history (Lambert, Noth andSchüwer 2011). The damages led to high loanlosses and provisioning for banks that werebased in the impacted areas. The bank lossesled US regulators to review the adequacy ofbank risk models regarding credit risk andhurricane damage.

Geological disasters such as earthquakes andvolcanoes can also result in banking andfinancial market distress. The Great KantoEarthquake of 1923, which struck the southpart of the Kato district in Japan, is among thecauses of the 1927 Showa financial crisiswhich culminated in the closure of numerousbanks (Shimizu & Fujimura 2010). Similarly,the series of earthquakes which hit Turkey in1999 required international financialassistance to rebuild the economy and avoidthe collapse of the banking system (Brinke2013). Finally, the eruption of the SoufriereHills volcano on the island of Montserrat in1998 destroyed Plymouth, the capital, andforced 90 per cent of the inhabitants to leavethe island. The financial system was severelyimpacted, as the most important bank on theisland, the Montserrat Building Society (MBS)collapsed due to a bank run (Clay et al 1999).

Clearly, not all of these examples relate toenvironmental risks that have been mademore likely or severe by human activity –sunspot activity and geological disasters beingcases in point. However, there are conceptualparallels between these natural disasters andthose that can be aggravated by humanactivity in that, while inevitable in theiroccurrence, specific incidents are difficult topredict and can have significant impacts onbanking instability unless sufficientprecautions are taken. History therefore raisesthe fundamental question of how bankregulation can take into account the financialstability risks that can arise fromenvironmentally unsustainable practices.

4 See generally for a review of the literature, J. Landon-Lane, H Rockoff, R.H Steckel, (2011) The Economics of Climate Change: Adaptations Past andPresent pp 73-84.5 See R Hornbeck, ‘The Enduring Impact of the American Dust Bowl : Short and Long Run Adjustments to Environmental Catastrophe’ (2012)American Economic Review 102 (4), 1477-1507 6 The United States economy was suffering a severe depression in the 1930s that had already caused hundreds of banks to fail across the country.Economists have demonstrated how some of the banking sector distress experienced in these farm belt states can be attributed to the dustbowlphenomenon. Hornbeck (2012) pp 1481-1483.

12

Further, scientists have now identified ninebiophysical thresholds for the Earth, which, ifcrossed, could undermine “the safe space forhuman development”. These thresholds –known colloquially as ‘planetary boundaries’ –represent “the ‘planetary playing field’ forhumanity if we want to be sure of avoidingmajor human-induced environmental changeon a global scale” (Rockström et al 2009).Three of these boundaries (namely climatechange, biological diversity and nitrogen inputto the biosphere) are thought to have beencrossed already.

Climate change is the boundary about whichwe know the most. The International Panel on Climate Change (2007, 2013, 2014) hasdocumented the scientific evidence in support of the proposition that global warmingand ocean acidification are caused by thecarbon-intensive activities of humans. Carbon-intensive activities lead in the longer-term toglobal warming, rising sea levels, and oceanacidification. More immediately, they can leadto increasingly volatile weather patterns,including extreme temperatures andintensified flooding of coastal and low-lyingareas, water shortages, and the health costs ofpollution. Existing extreme weather risk istherefore being exacerbated by human activity;moreover climate systems (in manneranalogous to financial systems) are likely toshow non-linear responses to increased stress.

Some believe these externalities arecontrolled and even mitigated throughadaptations in the economy, such asalternative production processes, or re-directing transport routes to avoid floodedcoastlines (Nordhaus 2013). According to thisview, investors, aware of the scientificevidence on the risks of climate change,would be expected to discount the value ofhigh-carbon assets and increase the value oflow carbon assets, resulting in investmentshifting over time to low carbon assets (Bankof England 2012). Nevertheless, the history offinancial crises demonstrates that financialmarkets suffer from serious over and under-estimation of risks because of asymmetric

information and moral hazard. These riskstranslate into large externalities for theeconomy and society (Kindleberger andAliber, 2011, 29-33; Schinasi, 2006, 47-66;Eichengreen, 1999, 80-82). Moreover,financial stability is a public good; marketparticipants do not have the incentive toinvest the necessary capital to provide itthemselves because the benefits of stabilityspill over to free-riders who do not pay for it.

The absence of regulatory intervention toaddress such market failures has beencriticised by some internationalorganisations.7 In January 2014 World BankPresident Jim Yong Kim, speaking at the WorldEconomic Forum, recognised the regulatorygap in this area by stating that “financialregulators must take the lead in addressingclimate change risks”, and that they shoulduse pricing mechanisms to more effectivelycontrol negative externalities or systemic risksassociated with global warming.8

Therefore, the key questions addressed in thefollowing sections are:

• To what extent are the economic andfinancial costs associated with systemicenvironmental risks currently beingconsidered in banking regulation, and

• How might existing banking regulationframeworks be utilised better to ensurethat systemic environmental risks areappropriately managed and do notcontribute to banking sector instability inthe future?

7 OECD (2013) p 128 OECD (2013) p 12See World Bank Group President: ‘This Is the Year of Climate Action’: http://www.worldbank.org/en/news/speech/2014/01/23/world-bank-group-president-jim-yong-kim-remarks-at-davos-press-conference (accessed 06.08.2014)

“ ...the history of financial crisesdemonstrates that financialmarkets suffer from seriousover and under-estimation ofrisks […] These risks translateinto large externalities for theeconomy and society”

13

Does Basel III adequately address systemicenvironmental risks?3By way of introduction, Basel III represents themost important international financialregulation agreement. The first Accord (Basel I)was adopted in 1988 with two main objectives:1) that internationally active banks hold aminimum amount of capital against their risk-based assets, and 2) to promote aninternationally level playing field for cross-border banking (Norton 1995). Although BaselIII is not legally binding under international law,it is remarkable that most countries haveadopted it and claim to have implemented it.The IMF observed that countries and bankinginstitutions which demonstrate that they haveimplemented the Accord benefit from a lowercost of capital than countries and banks thathave not done so (Financial Stability Forum2000). Some countries implement the Accordfaithfully and strictly enforce its requirements.9

However, the Accord is not mandatory; somecountries pick and choose what provisions tocomply with, while others impose stricterstandards.

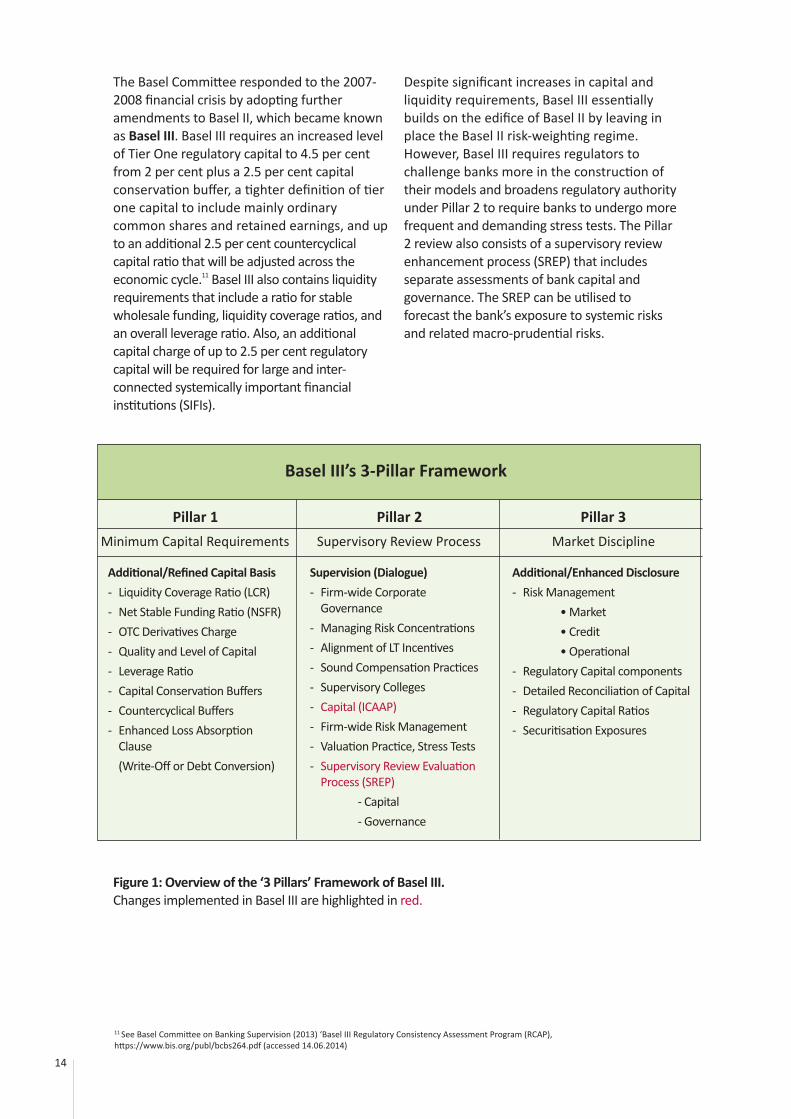

Although Basel I achieved its main objective ofincreasing the level of regulatory capital in theinternational banking system, it containedmany national discretions, loopholes andincentives for banks to make riskier short-termloans and to transfer less risky assets off theirbalance sheets (Goodhart 2011). Basel II wasproposed in 1999 to address many of thesegaps and weaknesses. In doing so, Basel IIintroduced the ‘three pillars’ concept – 1)Minimum Capital, 2) Supervisory Review, and3) Market Discipline. The three pillars aredesigned to reinforce each other and to createincentives for banks to enhance their riskmeasurement and management. Thisframework is represented in Figure 1.

Pillar 1 (Minimum Capital) allows banks tocalculate their regulatory capital by using

statistical models that rely mainly on their ownhistoric default and loss data to estimate theircredit, market, and operational risks. Pillar 2sets forth principles of supervisory review thatauthorise regulators to require banks tocomply with broad principles of corporategovernance and to adopt an internal capitaladequacy assessment process (ICAAP)designed to enhance risk measurement andmanagement. Pillar 3 uses market discipline torequire banks to provide more information tothe market so shareholders and creditors canmonitor bank management more effectively toensure the bank’s soundness and futureprospects.

Basel II expanded the use of risk weightings forbanks to estimate the riskiness of their assets.A number of parameters determine an asset’srisk weighting, including the maturity of theloan, the probability of default, and the bank’sloss and exposure given default. Assets withlower risk weightings generally attract lowercapital charges, whereas assets with higher riskweightings generally attract higher capitalcharges. Corporate loans with short-termmaturities attract lower risk weightings (lowercapital charges), while corporate loans withlong-term maturities (7 years or more) attracthigher risk weightings (higher capital charges).

Basel II allowed banks to use their ownestimates of credit and market risks to lowertheir risk weightings for certain asset classes.This risk management approach was shown tobe seriously flawed when the global financialcrisis began in August 2007; the risk weightingsof most European and US banks were shown tobe poor indicators of the financial risks towhich banks were exposed.10

9 For example, the South African Reserve Bank (South Africa’s Bank Regulator) strictly implements and enforces the Basel Accord. See South AfricanReserve Bank, 'South Africa's implementation of Basel II and Basel III'www.resbank.co.za/RegulationAndSupervision/BankSupervision/TheBaselCapitalAccordper cent28Baselper cent20IIpercent29/Pages/AccordImplementationForumper cent28AIFper cent29.aspx (accessed 24.07.2014) and South African Reserve Bank, 'Guidance Note 9/2012issued in terms of section 6(5) of the Banks Act, 1990- Capital Framework for South Africa based on the Basel III Framework',www.resbank.co.za/Lists/Newsper cent20andper cent20Publications/Attachments/ 5154/G9per cent20ofper cent202012.pdf (accessed 24.07.2014)10 Specifically, bank models to estimate their counter-party credit and liquidity risks in the asset-backed securities and derivatives markets underestimatedcorrelations across asset classes. Moreover, the opaqueness of the risk-weightings in the banking book made it very difficult, if not impossible, forinvestors to understand the true risk exposure of a bank. These factors contributed significantly to an undercapitalisation of the banking system whichweakened its ability to absorb losses in the crisis.

14

The Basel Committee responded to the 2007-2008 financial crisis by adopting furtheramendments to Basel II, which became knownas Basel III. Basel III requires an increased levelof Tier One regulatory capital to 4.5 per centfrom 2 per cent plus a 2.5 per cent capitalconservation buffer, a tighter definition of tierone capital to include mainly ordinarycommon shares and retained earnings, and upto an additional 2.5 per cent countercyclicalcapital ratio that will be adjusted across theeconomic cycle.11 Basel III also contains liquidityrequirements that include a ratio for stablewholesale funding, liquidity coverage ratios, andan overall leverage ratio. Also, an additionalcapital charge of up to 2.5 per cent regulatorycapital will be required for large and inter-connected systemically important financialinstitutions (SIFIs).

Despite significant increases in capital andliquidity requirements, Basel III essentiallybuilds on the edifice of Basel II by leaving inplace the Basel II risk-weighting regime.However, Basel III requires regulators tochallenge banks more in the construction oftheir models and broadens regulatory authorityunder Pillar 2 to require banks to undergo morefrequent and demanding stress tests. The Pillar2 review also consists of a supervisory reviewenhancement process (SREP) that includesseparate assessments of bank capital andgovernance. The SREP can be utilised toforecast the bank’s exposure to systemic risksand related macro-prudential risks.

Figure 1: Overview of the ‘3 Pillars’ Framework of Basel III.Changes implemented in Basel III are highlighted in red.

11 See Basel Committee on Banking Supervision (2013) ‘Basel III Regulatory Consistency Assessment Program (RCAP),https://www.bis.org/publ/bcbs264.pdf (accessed 14.06.2014)

Pillar 1 Pillar 2 Pillar 3

Additional/Refined Capital Basis- Liquidity Coverage Ratio (LCR)- Net Stable Funding Ratio (NSFR)- OTC Derivatives Charge- Quality and Level of Capital- Leverage Ratio- Capital Conservation Buffers- Countercyclical Buffers- Enhanced Loss Absorption

Clause (Write-Off or Debt Conversion)

Supervision (Dialogue)- Firm-wide Corporate

Governance- Managing Risk Concentrations- Alignment of LT Incentives- Sound Compensation Practices- Supervisory Colleges - Capital (ICAAP)- Firm-wide Risk Management- Valuation Practice, Stress Tests- Supervisory Review Evaluation

Process (SREP)- Capital- Governance

Additional/Enhanced Disclosure- Risk Management

• Market• Credit• Operational

- Regulatory Capital components- Detailed Reconciliation of Capital - Regulatory Capital Ratios- Securitisation Exposures

Minimum Capital Requirements Supervisory Review Process Market Discipline

Basel III’s 3-Pillar Framework

15

a) How does Basel III currently treat systemicenvironmental risks?

Pillar 1 of Basel II (now Basel III) does requirebanks to assess the impact of specificenvironmental risks on the bank’s credit andoperational risk exposures, but these are mainlytransaction-specific risks that affected theborrower’s ability to repay a loan or address the‘deep pockets’ doctrine of lender liability fordamages and cost of property clean-up. Forexample, paragraph 510 of Basel II and III (Pillar1) requires banks to ‘appropriately monitor therisk of environmental liability arising in respectof the collateral, such as the presence of toxicmaterial on a property’. This would involve thebank in due diligence and transaction screeningto mitigate the credit and operational risksassociated with this type of lending. Thesetransaction-specific risks are narrowly definedand do not constitute broader macro-prudentialor portfolio-wide risks for the bank.

b) Do Basel III’s Pillar 1 ‘Minimum CapitalRequirements’ discourage the financing ofenvironmentally sustainable economicactivities?

A concern that has arisen in relation to Pillar 1 ofBasel III is the extent to which higher capitalcharges on longer-term project finance loansmight have had the unintended consequence ofundermining finance for environmentallysustainable economic activities, particularlylending for long-term endeavours such asinfrastructure. Commentators holding this viewargue that unless capital and liquidityrequirements are relaxed, long-term project

finance for environmentally sustainableeconomic activities will be severely restricted.This study has investigated this concern.

Basel II and III apply a lower risk weighting toshort-term (1-3 year) recourse balance sheetcorporate loans in comparison to longer-term (7years or more) project finance loans to off-balance-sheet entities because the latter type ofloans are riskier due to their longer maturity andnon-recourse structure. The risk-weightingframework therefore results in higher capitalrequirements for bank lending in countries thatrely mainly on longer-term specialised lendingarrangements as opposed to countries that relymainly on short-term corporate loans for suchcredit.

However, the form of bank lending forenvironmentally sustainable economic activitiesvaries substantially between countries. In somecountries (e.g. Brazil and China), this takes placealmost wholly through recourse balance sheetshort-term corporate lending, while in othercountries (e.g. Peru and South Africa), it ismostly long-term non-recourse off-balance-sheet specialised lending (i.e. project finance).Across most countries, however, most bankexposures to financing environmentallysustainable economic activities will be throughshort-term corporate lending. A much smallerpercentage of lending will be long-term (7 yearsor more), which will mainly be specialised (i.e.project finance) lending for large-scalerenewable energy projects.

Do capital requirements matter?

Christopher Wells, Senior Vice President for Environmental and Social Risk for Santander’sBrazilian subsidiary, explained in an interview for this study that as far as bank riskmanagement is concerned, managing a bank’s environmental risk exposure in respect of short-term corporate loans was not a capital allocation issue, as broader governance issues wereimplicated and outweighed in importance the calculation of regulatory capital.

In Brazil, a major systemic environmental risk for small and medium-sized farmers isdeforestation of the Amazon and related soil erosion and productivity decline. Most Brazilianbank lending to mitigate these risks takes the form of recourse balance sheet loans, which aretypically short-term corporate (1-3 years) whilst longer-term maturities are up to 3 to 5 years.In conclusion, the importance of capital requirements depends on the market context.

16

Based on interviews with regulators and bankpractitioners from Brazil, China, India and Peru,it was uniformly observed that Basel III’sstricter capital and liquidity requirementswould have only a marginal impact on lendingto support environmentally sustainable activity.This is not least because bank financing ofinfrastructure projects, such as those relatingto renewable energy, is influenced by anumber of factors that relate to the economicand political riskiness of the project. Thesecriteria are much more important indetermining whether the bank lends than theregulatory capital or liquidity requirements. Infact, regulatory capital is considered by projectfinance specialists to be an insignificant factorin influencing the bank’s pricing of the loan orits willingness to lend.

Moreover, interviewees stated that loweringcapital and liquidity requirements to benefitenvironmentally sustainable economicactivities may create an undesirable trade-offbetween financial stability and environmentalsustainability,12 and that Pillar 1’s primary roleshould be to support a sound financial systemthrough higher capital and liquidityrequirements. There was also a concern thatlowering capital requirements for the financingof environmentally sustainable economicactivities may lead to arbitrage and poorincentives for banks.13

Further, the Financial Stability Board (2013) hasobserved in a research paper that “The Basel IIIreform package does not specifically targetlong-term bank finance, although it may affectit…[as Basel III does] alter the incentives fordifferent types of financial institutions toparticipate in this market.” The FSB furthernotes that “pre-crisis models and levels offinancing were unsustainable and should notbe the appropriate benchmark for assessingthe impact of reforms on the availability andcost of longer-term finance” (FSB 2013).

Based on the above, the evidence suggeststhat regulatory capital and liquidityrequirements as currently set forth in Basel III’s

Pillar 1 approach play at most a marginal rolein influencing a bank’s decision to providespecialised lending on project finance forenvironmentally sustainable economicactivities such as renewable energyinfrastructure projects.

c) Are there existing regulatory and marketpractices outside of Basel III that are relevantto this study?

Despite little action at the international level,some countries have already engaged in avariety of regulatory and market practices toassess systemic environmental risks and adoptpractices to mitigate the banking sector’sexposure to environmentally unsustainableactivity.

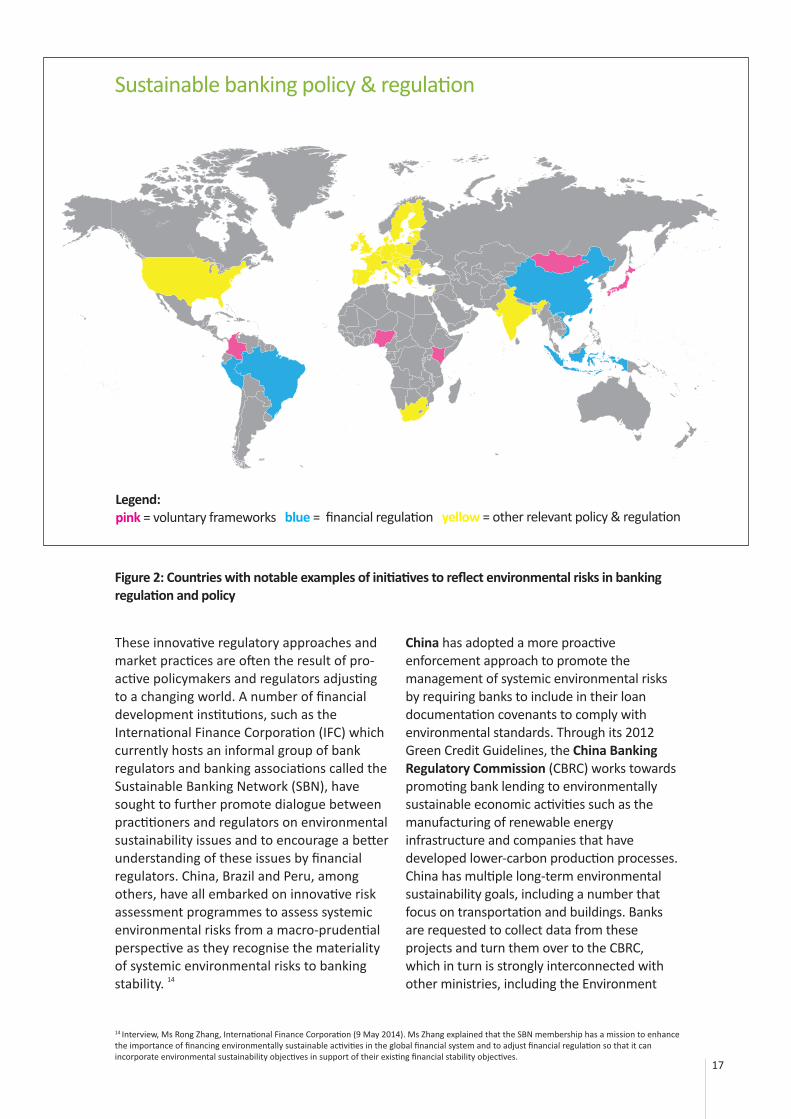

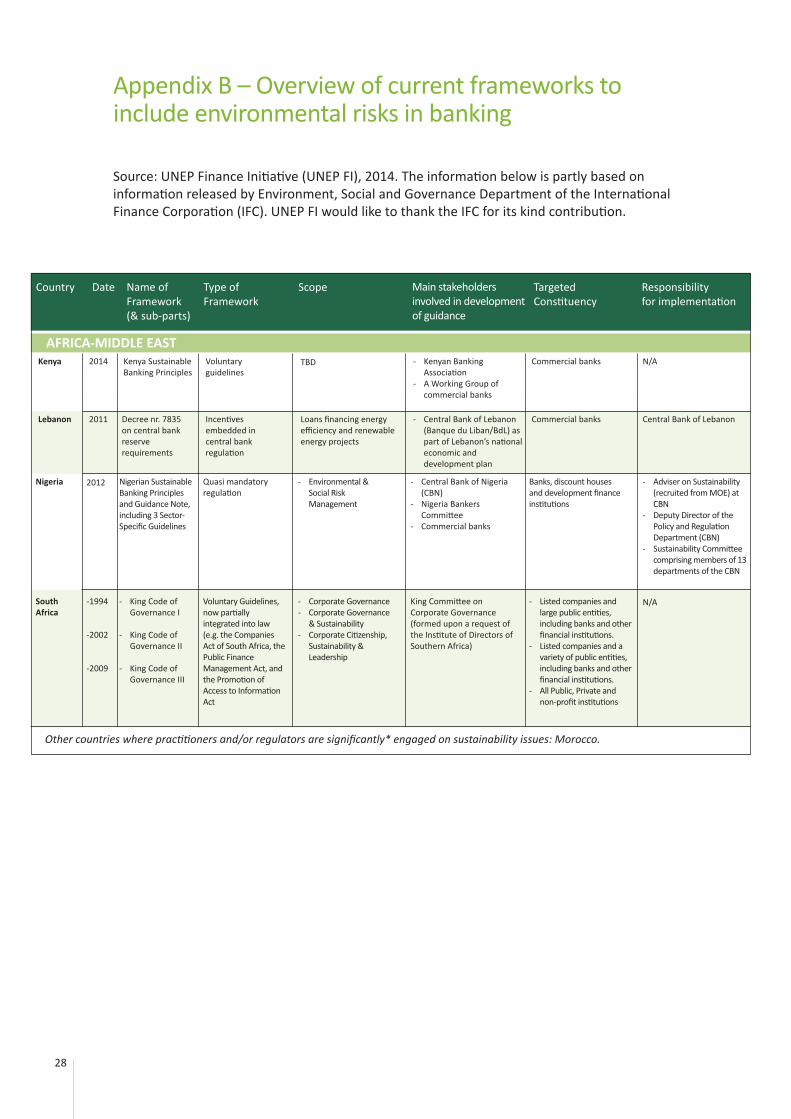

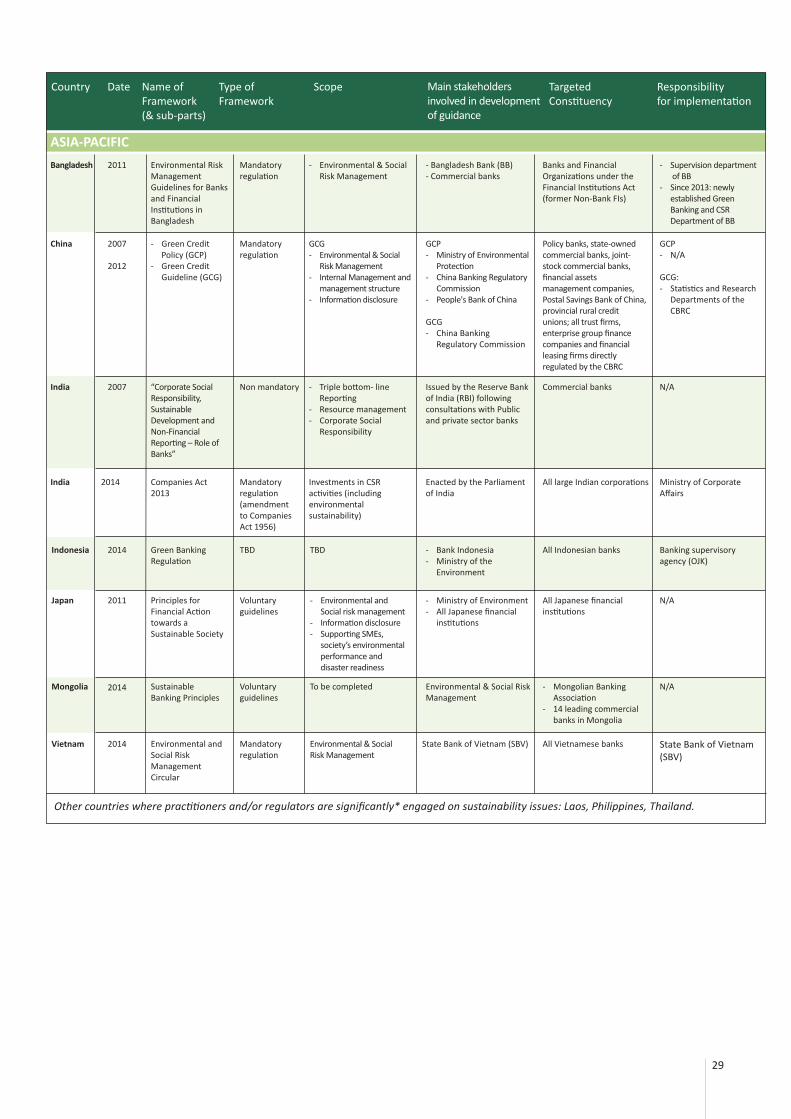

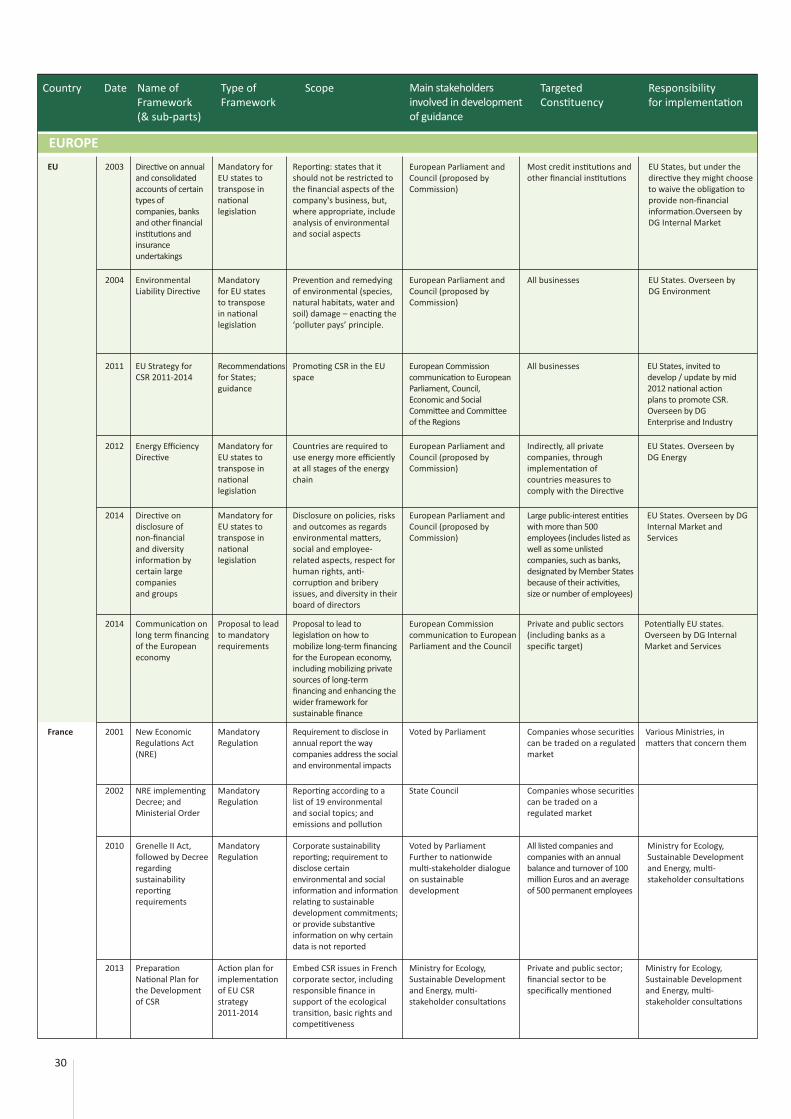

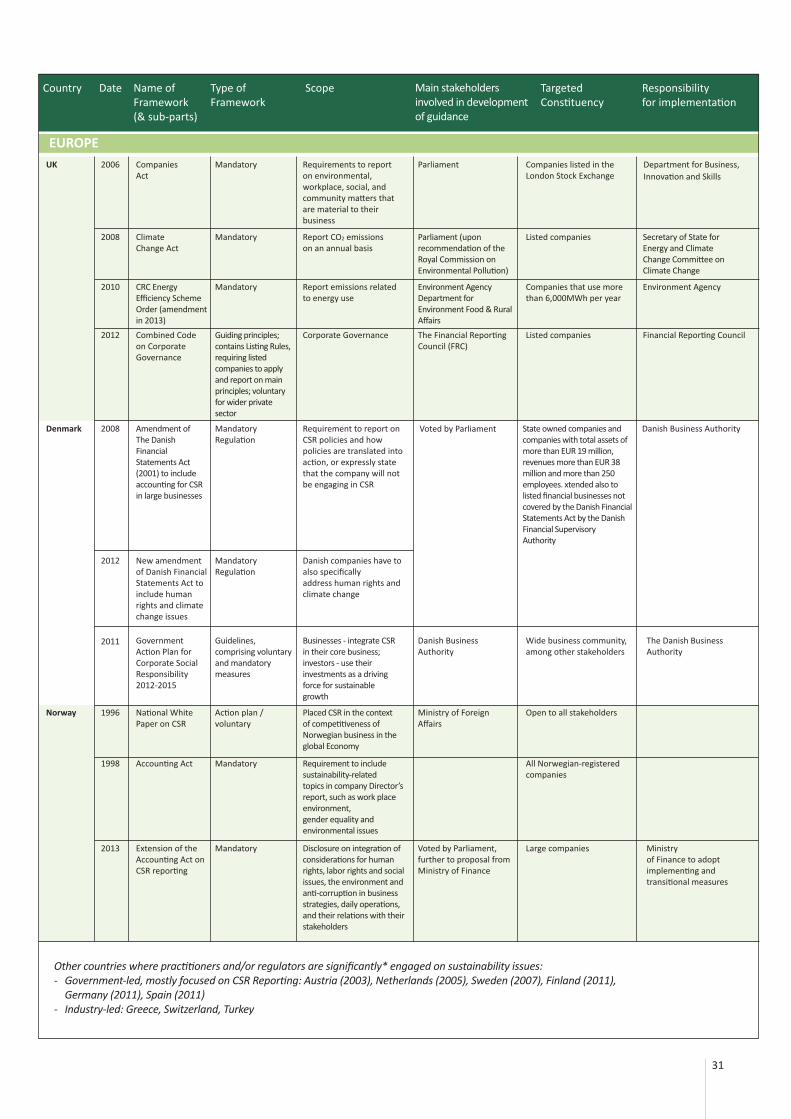

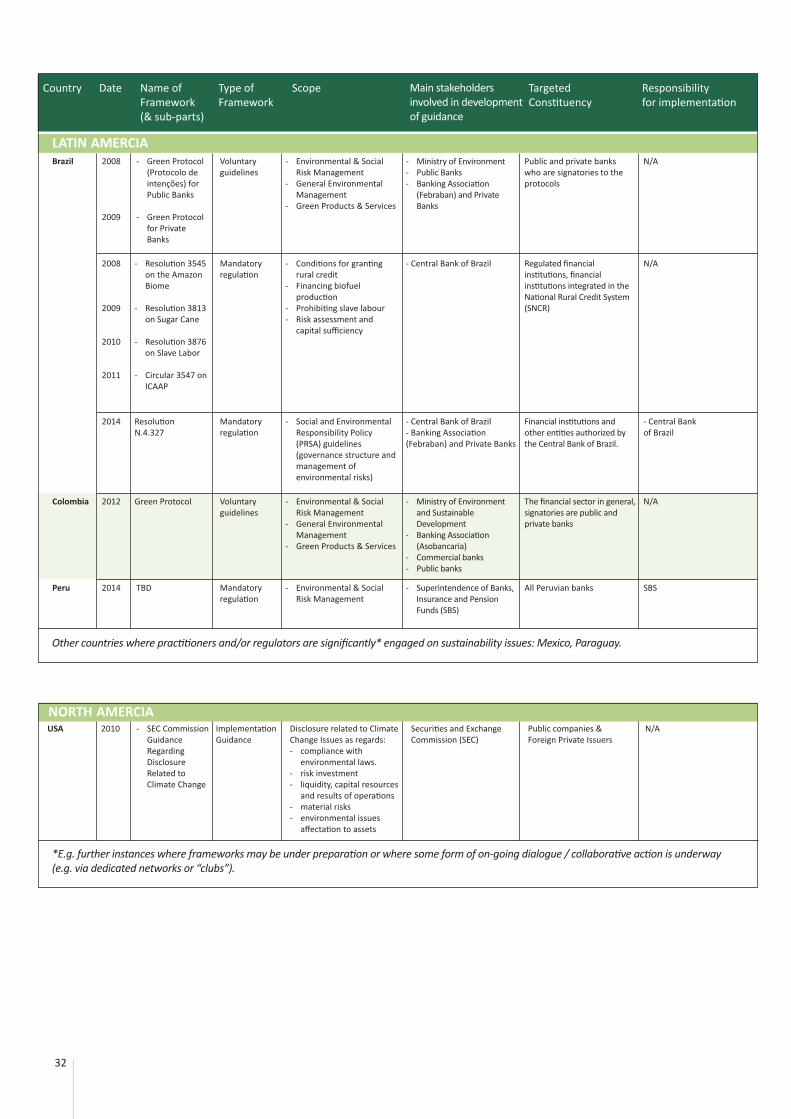

These initiatives have been based on existingregulatory mandates to promote financialstability by acting through the existing Basel IIIframework to identify and manage bankingrisks both at the transaction-specific level andat the broader portfolio level. What issignificant about these various country andmarket practices is that the regulatoryapproaches used to enhance the bank’s riskassessment fall into two areas: 1) Greaterinteraction between the regulator and thebank in assessing wider portfolio level financial,social and political risks, and 2) Banks’enhanced disclosure to the market regardingtheir exposures to systemic environmentalrisks. Figure 2 highlights countries wherenotable innovation is taking place. For a fullreview of current regulatory and voluntaryframeworks aiming to promote theconsideration of sustainability issues in banks,please see Appendix B.

12 Interviews with Christopher Wells, Banco Santander Brazil (30 May 2014), Dr Rubens Sardenberg, Brazilian Federation of Banks (17 June 2014) andMalcolm Athaide, YES Bank (10 July 2014).13 Interview, Mr Paul Collazos, Superintendencia de Banca, Seguros y AFP, (20 May 2014).

“ Despite little action at theinternational level, somecountries have alreadyengaged in regulatory andmarket practices to assesssystemic environmental risks”

17

These innovative regulatory approaches andmarket practices are often the result of pro-active policymakers and regulators adjustingto a changing world. A number of financialdevelopment institutions, such as theInternational Finance Corporation (IFC) whichcurrently hosts an informal group of bankregulators and banking associations called theSustainable Banking Network (SBN), havesought to further promote dialogue betweenpractitioners and regulators on environmentalsustainability issues and to encourage a betterunderstanding of these issues by financialregulators. China, Brazil and Peru, amongothers, have all embarked on innovative riskassessment programmes to assess systemicenvironmental risks from a macro-prudentialperspective as they recognise the materialityof systemic environmental risks to bankingstability. 14

China has adopted a more proactiveenforcement approach to promote themanagement of systemic environmental risksby requiring banks to include in their loandocumentation covenants to comply withenvironmental standards. Through its 2012Green Credit Guidelines, the China BankingRegulatory Commission (CBRC) works towardspromoting bank lending to environmentallysustainable economic activities such as themanufacturing of renewable energyinfrastructure and companies that havedeveloped lower-carbon production processes.China has multiple long-term environmentalsustainability goals, including a number thatfocus on transportation and buildings. Banksare requested to collect data from theseprojects and turn them over to the CBRC,which in turn is strongly interconnected withother ministries, including the Environment

Legend: pink = voluntary frameworks blue = financial regulation yellow = other relevant policy & regulation

14 Interview, Ms Rong Zhang, International Finance Corporation (9 May 2014). Ms Zhang explained that the SBN membership has a mission to enhancethe importance of financing environmentally sustainable activities in the global financial system and to adjust financial regulation so that it canincorporate environmental sustainability objectives in support of their existing financial stability objectives.

Sustainable banking policy & regulation

Figure 2: Countries with notable examples of initiatives to reflect environmental risks in bankingregulation and policy

18

Ministry which can use the information toinitiate an investigation of environmentalregulation violations. In 2012, the CBRC beganrequiring banks to monitor its borrowers’compliance with environmental regulationsand to begin implementing loan contractchanges that either allows the bank toaccelerate loan repayments of a customer inviolation of environmental laws or else todemonstrate compliance in a certaintimeframe. If compliance cannot be shown, thebank could suspend further lending and triggeraccelerated loan repayment.

In 2014, Brazil adopted similar requirementsrelating to the financing of sustainable activity,as well as disclosure, that are mandatory forbanks as part of their Pillar 2 SupervisoryAssessment and Pillar 3 Market Disclosurerequirements. Unlike the supervisory practicesof most other Basel Committee members, theBanco Central do Brasil (the Central Bank ofBrazil) has utilised the Pillar 2 Internal CapitalAdequacy and Assessment Process (ICAAP) toencourage banks to assess their individualexposures to carbon risk. Moreover, the BancoCentral do Brasil implemented a regulation in2014 15 which establishes guidelines forfinancial institutions in connection with thePillar 2 Supervisory Review and EvaluationProcess (SREP) to consider the bank’s “degreeof exposure to the social and environmentalrisk of the activities and transactions of theinstitution”. 16 This regulation also requires thebank to publicly disclose its environmental andsocial risks (with penalties if disregarded) aspart of the market discipline disclosure rules ofPillar 3 of Basel III.

The Peruvian regulators’ approach has been todevelop the principle of due diligence as themost effective way to persuade projectmanagers to rethink how they go about projectdevelopment. The due diligence processrequires banks to require the project managerto complete a due diligence report on theproject, which must be approved by the bankbefore it makes credit available. In using thisapproach, the regulator is not primarilyimposing pressure on the company overwhether or not to invest in the project, or on

the bank to decide whether or not to make theloan. Instead, the company is required to moredeeply analyse the underlying social,environmental and economic risks related tothe loan, and to recognise these before theymanifest during project development. Longbefore substantial amounts are invested, thedeveloper is asked to assess the risk factors –social, environmental, economic and financial –relevant for planning, building and operatingthe project. The bank oversees this assessmentin order to determine at a deeper level theriskiness of the loan and the extent to which itshould provide credit for the project.

According to senior management at Peru’sFinancial Regulation Authority, since thisinnovation was introduced, social conflictshave decreased markedly and affectedstakeholders and community groups feel theynow have more influence in shaping theinvestment decision. This has also resulted inimproved financial risk management for banks,as defaults and restructurings on such loanshave fallen dramatically. 17 This has enhancedbanks’ financial risk management and alsoimproved broader macro-economicdevelopment for communities and the countryas a whole. Based on such due diligence riskassessments, banks can obtain moreinformation and can therefore act sooner andmore effectively in managing their own risk by,for example, requiring higher quality collateraland sensitising the manager to potential socialunrest because of the project and its relatedsystemic environmental risks.

d) How might the Basel Committee takeforward the lessons of this study?

The evidence assessed during this studysuggests that systemic environmental risks arematerial to banking stability. The study hasfound that the existing Basel Capital Accorddoes require banks to assess the impact ofspecific environmental risks on the bank’scredit and operational risk exposures, but thatthese transaction-specific risks are narrowlydefined and do not constitute broader macro-prudential or portfolio-wide risks for the bank.

15 Regulation No. 4,327 (28 April 2014).16 Ibid. 17 Interview, Dr Daniel Schydlowsky, Director Peru’s Financial Regulation Authority, and Paul Collazos, Economist, Peru’s Financial Regulation Authority(4 June2014).

19

The impact of Basel III’s Pillar 1 MinimumCapital Requirements was explored with theconclusion that regulatory capital and liquidityrequirements, as currently set forth in BaselIII’s Pillar 1, play at most a marginal role ininfluencing a bank’s decision to providespecialised lending on project finance forenvironmentally sustainable economicactivities. In addition, it is thought thatlowering capital and liquidity requirements tobenefit environmentally sustainable economicactivities may create an undesirable trade-offbetween financial stability and environmentalsustainability.

How, then, might the Basel Committeeimprove the banking sector’s management ofsystemic environmental risks in keeping with itsresponsibility to safeguard banking sectorstability and sustainability? Supervisory Reviewunder Pillar 2 and Market Discipline underPillar 3 offer some promising avenues.

Using Pillar 2 – Supervisory Review

The Pillar 2 Supervisory Review process isdesigned to complement Pillar 1 and concernsrisk management. Risk management is aboutdiversification of risk exposures by reducing,for instance, concentration risk exposures tocertain asset classes or economic sectors.

Pillar 2 of Basel III requires banks to measureand manage risks at the broader portfolio levelby applying the “fundamental principles ofsound capital assessment”, including “policiesand procedures designed to ensure that thebank identifies, measures, and reports allmaterial risks” (i.e. stress tests) across itsportfolio. 18 Pillar 2 allows the supervisors tohave wide powers of oversight to test thebank’s corporate governance structures and itsrisk management practices in assessingtransaction-specific risks as well as broaderportfolio-level risks. Based on theseassessments, modifications can be made to thePillar 1 capital and liquidity calculationprocesses.

Banks should address all ‘material’ risks in thecapital assessment process and, while it isrecognised that not all risks can be measured

precisely, the process should be developed toestimate risks by making a list of risk exposuresthat should “by no means constitute acomprehensive list of all risks”. 19 This studyargues that exposure to economic activity thatis environmentally unsustainable falls withinthe scope of Pillar 2.

To be incorporated in the Pillar 2 portfolio riskassessment framework, risks must beconsidered ‘material’ and included in thebank’s list of material risks. However, the BaselCommittee has not been addressing systemicenvironmental risks, nor has it beenencouraging national regulators to ask bankrisk officers whether they are measuring thebank’s exposure to environmentallyunsustainable activities. For example, mostbank supervisors have not utilised Pillar 2’ssupervisory approaches to incorporateforward-looking models that estimate thepotential stability impact of supplying credit toenvironmentally unsustainable or sustainableactivities over time into their stress tests. Suchan approach could equally be applied torecognise the positive impact of bank lendingfor environmentally sustainably activity as thenegative impact for environmentallyunsustainable activity.

This very limited approach to addressingbanking risks that can arise fromenvironmentally unsustainable activity couldpose serious longer-term risks to the stabilityof the banking sector. It is an omission that isunsupported by the economic and scientificdata and that is within the mandate of theBasel Committee to address. Recent studiesshow that the cost of environmentallyunsustainable activity to the economy isbecoming increasingly material in terms offinancial risk exposure for banking institutions.The World Bank estimates that the averageannual economic cost of human-inducedenvironmental depletion was approximately$6.6 trillion in 2008, equivalent to 11 per centof global GDP. The same study estimates that ifenvironmentally unsustainable activitycontinues at this scale, the annual costs for theglobal economy will reach nearly $28.6 trillionby 2050, equivalent to 18 per cent of globalGDP (UNEP FI 2011).

18 Basel II Pillar 2, para 731.19 Basel II Pillar 2, para 732.

20

The evidence therefore suggests that systemicenvironmental risks are material for bankregulation purposes and therefore should beexpressly incorporated into Pillar 2’s list ofmaterial risks. This would provide aninternationally level playing field to guide bankrisk officers and regulators in assessing theportfolio-level risks of bank lending forenvironmentally sustainable and unsustainableactivities. This could potentially involveregulators and risk officers developing, amongother things, exclusion lists, phase-out or phase-in targets for certain types of activities (e.g.replace high-carbon assets with low-carbonassets), and conduct impact screening – bothnegative and positive – to develop a betterunderstanding of banks’ risk exposure toenvironmentally unsustainable activity.

Using Pillar 3 – Market Discipline

The Pillar 3 ─ Market Discipline – element ofBasel III could also play an important role inenhancing risk management in respect ofsystemic environmental risks. It largely relies ondeveloping a set of disclosure requirementswhich will allow market participants to assessrelevant information about a bank’s capital, riskexposures, risk assessment processes, and hencethe capital adequacy of the institution. Byproviding disclosures to the capital markets, it isintended that investors should learn fully of therisks to which banking institutions are exposed –including the bank’s exposure to systemicenvironmental risks.

Public disclosure of these risks raises a numberof questions. Firstly, whether or not the public isable to comprehend the long-term effects oftheir investment choices. Regulators in bothBrazil and Peru doubt the willingness of theindividual investor to question the long-term riskexposure to carbon and other systemicenvironmental risks of a short-term investment,or to differentiate between a stock doing badlydue to its exposure to environmentallysustainable or unsustainable activity ascompared to other bad business choices. Peru’sbank regulator also questioned the usefulness of

requiring banks to disclose publicly theirexposure to systemic environmental risks on thegrounds that this could expose banks topotential legal liability for mis-stating such risksin their disclosures. Secondly, the effectivenessof these kinds of disclosures was questionedbased on the availability of data and relatedinformation, and the difficulty of forecastingsystemic environmental risk exposures far intothe future.

That said, the market discipline approach hasbeen utilised by shareholders of some USbanks to require the bank’s board to disclosethe institution’s exposure to high-carbonactivities. This has been criticised as a ratherad hoc and inflexible approach to obtaininginformation on a bank’s carbon exposure. 20

Instead, our findings suggest that the marketdiscipline approach in Pillar 3 could beenhanced to include rules on both qualitativedisclosures (e.g. voluntary codes and industrystandards) and quantitative disclosures (asdefined by the financial regulator). This wouldprovide an effective and a more economicallyefficient tool which would also improveaccountability through further clarifying thefiduciary duties of the bank board toundertake risk assessments to obtain thisinformation. 21

Pillar 3’s market discipline framework should beconsidered as another lever to enhance thebanks’ governance frameworks with respect tosystemic environmental risks. Basel III, however,does not require or encourage banks to discloseinformation about systemic environmental risksor risk management practices. In somecountries, such as France, 22 all environmentaland social risk exposures must be publiclydisclosed by listed companies and financialinstitutions. The Basel Committee shouldconsider how Pillar 3 can be used to encourageor require banks to disclose, on a harmonisedand standardised basis, information aboutexposure to systemic environmental risks andconsequent management practices that couldbe useful for investors in assessing the bank’slonger-term soundness and profitability.

20 According to a recent WSJ report, shareholder resolutions have become increasingly political and less relevant to average shareholders with respectto climate risk reporting, as ‘special-interest groups’ have allegedly hijacked the shareholder resolution process, as the guidance (on disclosingemissions stemming from fossil-fuel related loans) released by regulators has not led to an increase in the quality or quantity of the disclosures.21 What exactly could amount to a breach of fiduciary duty is, in itself, a widely contested area. Trustees who do not act on Environmental and SocialGovernance issues arguably increase the risk of a long-term portfolio and therefore may not be acting in the best interest of the beneficiaries. Theproblem is that, in practice, various financial managers believe that considering issues other than financial returns could constitute a breach. Thefindings of a UNEP FI legal study issued in 2005 (A legal framework for the integration of environmental, social and governance issues intoinstitutional investment, UNEP FI, 2005), found that fiduciary duty is inclusive rather than exclusive of environmental, social and governanceconsiderations, however differences of opinion persist in the market as regulation continues to be permissive rather than obligatory.22 France has adopted legislation mandating banking and financial institutions to publicly disclose their environmental and social risks as they relate tothe company’s financial performance and soundness. See Conseil d’Etat Decree, Regulation, Article 225. The disclosure of social and environmental

21

Pillar 1 Pillar 2 Pillar 3

Additional/Refined Capital Basis- Liquidity Coverage Ratio (LCR)- Net Stable Funding Ratio (NSFR)- OTC Derivatives Charge- Quality and Level of Capital- Leverage Ratio- Capital Conservation Buffers- Countercyclical Buffers- Enhanced Loss Absorption

Clause (Write-Off or Debt Conversion)

Supervision (Dialogue)- Firm-wide Corporate

Governance- Managing Risk Concentrations- Alignment of LT Incentives- Sound Compensation Practices- Supervisory Colleges - Capital (ICAAP)- Firm-wide Risk Management- Valuation Practice, Stress Tests- Supervisory Review Evaluation

Process (SREP)- Capital- Governance

Additional/Enhanced Disclosure- Risk Management

• Market• Credit• Operational

- Regulatory Capital components- Detailed Reconciliation of Capital - Regulatory Capital Ratios- Securitisation Exposures

Minimum Capital Requirements Supervisory Review Process Market Discipline

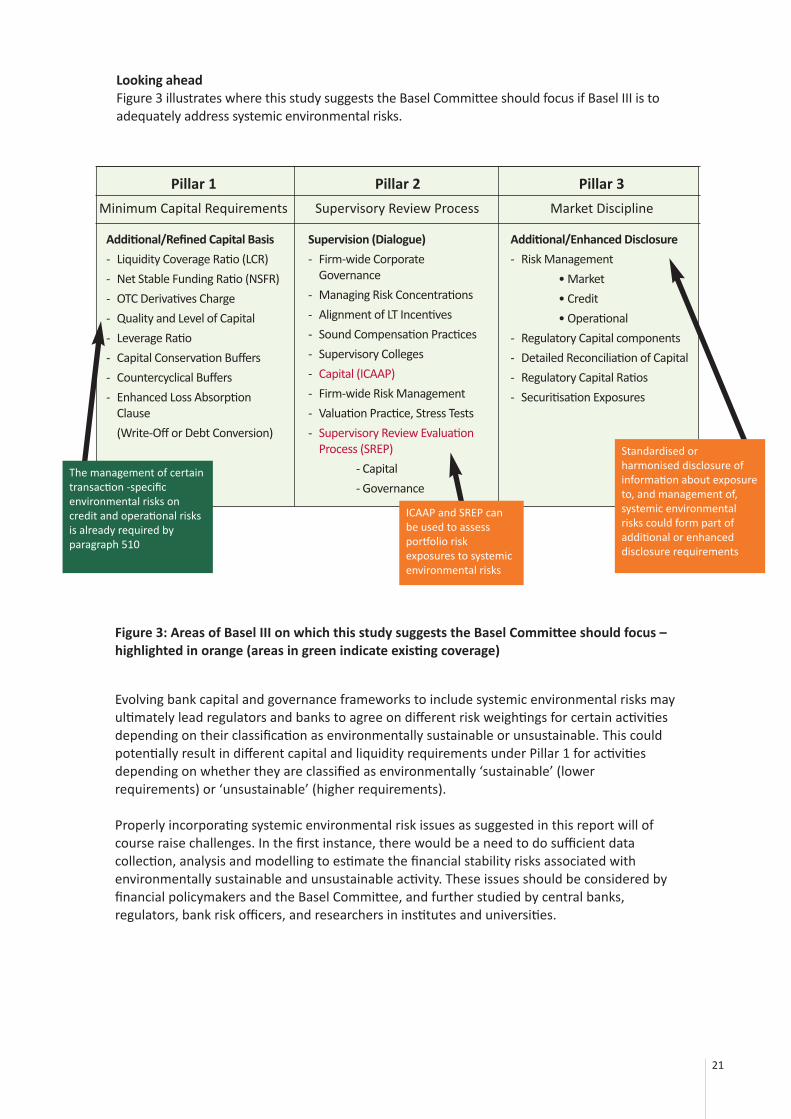

Evolving bank capital and governance frameworks to include systemic environmental risks mayultimately lead regulators and banks to agree on different risk weightings for certain activitiesdepending on their classification as environmentally sustainable or unsustainable. This couldpotentially result in different capital and liquidity requirements under Pillar 1 for activitiesdepending on whether they are classified as environmentally ‘sustainable’ (lowerrequirements) or ‘unsustainable’ (higher requirements).

Properly incorporating systemic environmental risk issues as suggested in this report will ofcourse raise challenges. In the first instance, there would be a need to do sufficient datacollection, analysis and modelling to estimate the financial stability risks associated withenvironmentally sustainable and unsustainable activity. These issues should be considered byfinancial policymakers and the Basel Committee, and further studied by central banks,regulators, bank risk officers, and researchers in institutes and universities.

Figure 3: Areas of Basel III on which this study suggests the Basel Committee should focus –highlighted in orange (areas in green indicate existing coverage)

The management of certaintransaction -specificenvironmental risks oncredit and operational risksis already required byparagraph 510

ICAAP and SREP canbe used to assessportfolio riskexposures to systemicenvironmental risks

Standardised orharmonised disclosure ofinformation about exposureto, and management of,systemic environmentalrisks could form part ofadditional or enhanceddisclosure requirements

Looking aheadFigure 3 illustrates where this study suggests the Basel Committee should focus if Basel III is toadequately address systemic environmental risks.

22

What other financial policy options are available?4 Part 2 of this study has considered how BaselIII could adequately take account of systemicenvironmental risks. However, there are otherfinancial policy options available topolicymakers and regulators, which are alsoworth exploring.

a) Monetary policy

Monetary policy could play a role insupporting liquidity provision for finance tosupport environmentally sustainableeconomic activities.

In recent history, central bank monetarypolicy has revolved around the targeting ofretail price inflation at a low rate of around 2per cent and using an array of measures toensure that the target is achieved and thatthe monetary policy transmission mechanismworks effectively throughout the economyand banking system. The economic slowdownin Europe, the US and Japan in the aftermathof the financial crisis has led the world’s mostinfluential central banks – the US FederalReserve, the European Central Bank, theJapanese Central Bank, and the Bank ofEngland – to follow extraordinarily loosemonetary policies involving quantitativeeasing and generous liquidity and otherfinancial support for the banking sector with aview to encouraging banks to lend more tothe broader economy.

For example, between 2009 and 2014, theBank of England followed a ‘funding forlending’ scheme that involved the Britishcentral bank lending money at a zero-interestrate to banks with the hope that the bankswould then lend the funds on to homebuyersto support the British housing market. Bankswere not obliged to lend the money, but wereobliged to report the amount of funds theyprovided for home mortgage loans.

Experts are divided over the effectiveness ofthe policy. In the context of this report,however, it raises the question of whethercentral banks should make funding available

to banks on generous terms in order topromote lending to environmentallysustainable economic activities. An exampleof this has been demonstrated by theLebanese Central Bank through its Decreenumber 7835 to support financing forinvestment in environmentally sustainableprojects, including green buildings andrenewable energy projects.

Brazilian and Peruvian authorities and bankersexplained that their central banks are veryconservative and would probably not agree tothe use of loose monetary policy measures toincrease such lending because it might send asignal to the global capital markets that theywere following an undisciplined monetarypolicy that could lead to higher inflation. Theyfurther asserted that monetary policyconditions in most emerging-marketeconomies were not greatly affected by therecent financial crisis and monetary policyshould therefore remain conservative andorthodox.

That said, Dr Rubens Sardenberg, ChiefEconomist of the Brazilian Federation ofBanks, expressed the personal view that hethought there were ways that central bankscould facilitate financial support for lending toenvironmentally sustainable economicactivities, These could involve, for example,the central bank accepting ‘green bonds’ orasset-backed securities that were AAA ratedas collateral for liquidity support . DrSardenberg also emphasised that Brazilianbanks are largely well-capitalised andfinanced at this time and would not needsuch liquidity support from central banks toprovide more lending to environmentallysustainable economic activities.

In contrast, Mr Han Fe of the CBRC statedthat, because of recent banking stresses in2013 in the inter-bank loan market, theChinese central bank (the People’s Bank ofChina – PBOC) was considering moreproactive measures to provide additionalliquidity support to Chinese banks, such as

23

the acceptance of ‘green’ asset-backedsecurities as collateral for liquidity support forChinese banks.

b) Financial innovation

Financial innovation could play a furtherimportant role in identifying sources offinance for bank lending to supportenvironmentally sustainable economicactivity.

Chinese regulators are already acting inaccordance with this view. Because China’scapital markets are evolving and becomingmore sophisticated, credit risk transferinstruments, such as asset-backed securities,are increasingly viewed by regulators andbankers as potential sources of additionalfinance for the Chinese economy. This couldperhaps play an important role in allowingChinese banks to make more fundingavailable for initiatives that targetenvironmentally sustainable economicactivity.

This view was supported by Dr Sardenberg,who emphasised how fast the Brazilianwholesale debt and secondary tradingmarkets are evolving and the growing interestby banks in utilising credit risk transferinstruments that are subject to regulatorycontrols to attract more investment in ‘greencredit’. He observed that the Brazilian marketwas not quite ready for these instruments yet,but when the time comes there will be a quicktransition because Brazil has already beenthrough a painful regulatory reform of itsbanking sector in the 1990s after a crisis thatresulted in the Banco Central do Brasilobtaining broad macro-prudential supervisorypowers to control and monitor the so-called‘shadow banking’ sector. Therefore, any newfinancing instruments or ABS green assetswould be subject to central bank oversight.

As discussed above, the involvement ofcentral bank oversight may not be a bad thingas demonstrated in the case of the Chineseauthorities considering the merits of allowingthe PBOC to accept certain simple andtransparent green asset-backed securities

(ABS) as collateral for bank liquidity supportmeasures. This could potentially lead to muchgreater bank lending for environmentallysustainable economic activities and providemore sustainable sources of funding for suchinitiatives.

Even without central bank acceptance ofgreen ABS as collateral, however, Chineseregulators are considering more favourableregulatory treatment to be applied to certaininnovative financial instruments, such asgreen asset-backed securities. Underconsideration are proposals that would allowcompanies to issue ‘green bonds’ and forbanks to securitise ‘green assets’ as a way togenerate more funding for environmentallysustainable economic activity. The CBRCconsiders simple and transparent asset-backed securities as an important source offinance for such economic activity. Moreover,the CBRC hopes that the Chinese central bankwill approve the use of certain monetarypolicy tools to increase green lending, such asthe central bank accepting green bonds orhigh quality asset-backed securities ascollateral for providing liquidity support tobanks.

In addition, the growing sophistication ofChina’s wholesale securities and debt marketscreates the potential for increased investmentin green assets by institutional investors alongwith the creation of a secondary market fortrading these securities. All of which wouldbode well for increased investment intoChinese green credit.

c) Joining up banking regulation withenvironmental policy

A major weakness with existing approaches tofinancial and environmental policy andregulation has been lack of coordination indeveloping, implementing and enforcing rulesand standards. The problem of a lack ofcoordination and mutual recognition ofstandards arises all the way to theinternational level, involving the G20 andinternational environmental initiatives. Therehas been a failure of policymakers at thehighest level to join up financial policy and

24

environmental policy with respect to puttingthe global economy on a more stable andsustainable footing. For instance, many banksupervisors do not believe that they have apolicy mandate from their Finance Ministriesto require banks and financial institutions tomanage or report their systemicenvironmental risks.

Although the G20 has failed to recognise theimportance of the linkage between financialpolicy and environmental policy, somecountries have made much progress inestablishing institutional and legal linkagesbetween environmental and financialregulation.

The efforts of China and Peru should benoted, as they have adopted coordinationmechanisms between environmental andfinance ministries and banking regulators toensure the exchange of information, data andmutual support in the investigation andenforcement of environmental laws. Both thebank and environmental regulator arerequired to coordinate their regulatorypractices and supervision whereenvironmental regulatory compliance andfinancial regulatory compliance implicate oneanother. Other countries, such as Brazil, haveembarked on similar coordination policies byensuring that databases of infringements ofenvironmental laws and regulations are madepublicly available, enabling banks to accessthem.

Most advanced developed countries, however– including most members of the BaselCommittee – have no policy to coordinateenvironmental and banking regulation.Moreover, in EU states and the United Statesbank regulators and supervisors do not havean official mandate to take account ofsystemic environmental risks when applyingand implementing their own regulatoryframeworks.

Many central banks in the SustainableBanking Network have developed nationalapproaches that could serve as a model forthe G20 and other international bodies torecommend to all countries although, of

course, country-specific approaches may notbe wholly transferable. Successful approachesgenerally involve countries developing astrong dialogue between their environmentaland the financial ministries with respect tofinancial exposures to systemic environmentalrisk. It is certainly necessary as a first step forfinance ministries to provide bank regulatorswith a mandate to supervise the bankingsector’s exposure to systemic environmentalrisks. This will ultimately enhance bank riskmanagement in the areas of credit, market,liquidity and operational risk.

“ Most advanced, developedcountries – includingmembers of the BaselCommittee – have no policyto coordinate environmentaland banking regulation”

25

Conclusions and recommendations for financialpolicymakers and regulators5The role of the financial system in theeconomy and broader society is to providethe necessary financing and liquidity forhuman and economic activity to thrive – notonly today, but also tomorrow. In otherwords, its role is to fund a stable andsustainable economy. The role of financialregulators is to ensure that excessive risksthat would threaten the stability of thefinancial system – and hence imperil thestability and sustainability of the economy –are not taken.

The analysis presented in this report suggeststhat the regulatory framework that governstoday’s banking system may not be being used toits full capacity; with some notable exceptions,systemic environmental risks appear to be in thecollective blind spot of bank supervisors.

Despite the fact that history demonstrates directand indirect links between systemicenvironmental risks and banking sector stability,and that evidence suggests this trend willbecome more pronounced and complex ashumanity breaches more planetary boundaries,the current Basel Capital Accord does not takeexplicit account of, and therefore only marginallyaddresses, these issues. Although Basel IIIprovides a flexible framework for regulatorsand bank risk management to assess andmeasure the financial stability risks associatedwith environmental risks, this has not beenutilised by most bank regulators in theirsupervisory frameworks.

By failing to addresses systemic environmentalrisks, Basel III is arguably overlooking animportant source of risk to the financial systemand broader economy, despite its overridingobjective of guaranteeing banking stability andsustainability. Because financial stability is apublic good, regulation has a role to play toensure that environmental risks do not threatenfinancial stability.

However this report also offers insights thatsolutions are within reach, should regulators andindustry practitioners work together proactively.