Embed Size (px)

DESCRIPTION

No

Citation preview

Implications of Service TaxPost Union Budget -2012

( effective from 01.07.2012 )

By

CA Uday W. PrabhupatkarB.Com., LLB(Gen.), DTL., DCEXSRC, MFM., ACA.

General Manager – ( Indirect Tax) Tecnimont ICB Pvt. Ltd.,

& Visiting Faculty for Management Institutes

affiliated to University of Mumbai.

Basic Frame Work of Service Tax

Overview of service tax Basic concepts Legal framework Definition of service Charging section Negative list of services Declared services

Overview

It is a Central Government Levy Introduced & governed by Finance Act, 1994 Humble beginning by Taxing 3 services from July’ 94 gathering

revenue of Rs. 407 crores Progressed to Tax 119 Services & whopping collection of Rs.

97,444 crores revenue for the year 2011-12 Till date No Separate Fiscal Legislation Changes are managed by circulars & notifications Certain provisions of Central Excise Act, 1944 are made

applicable to Service Tax Administered by Central Excise Department

Basic Concepts

Rendition/provision of “service” is the subject matter of Taxation

There has to be two entities called “service provider” & “service recipient”

Taxable event for provision of service is prescribed by Point of Taxation Rules, 2011

Tax levied on Gross consideration for service Reimbursement of expenses forms part of Gross

consideration, except in case of a “pure agent” Service Tax is destination based consumption tax

Basic Concepts

Obligation to collect & pay the service tax is on Service Provider

Generally charged on the face of Invoice If not charged separately, Invoice value is presumed to be

inclusive of Service Tax If the contract is silent or does not specifically provide for

Service Tax – it is service provider’s obligation to pay service tax in his hands irrespective of the fact whether he collects or not from service recipient

For recovery of Tax, authorities have recourse only to service provider & not to Service recipient, except in the cases specifically provided for u/s 68(2) read with Rule 2(1)(d)

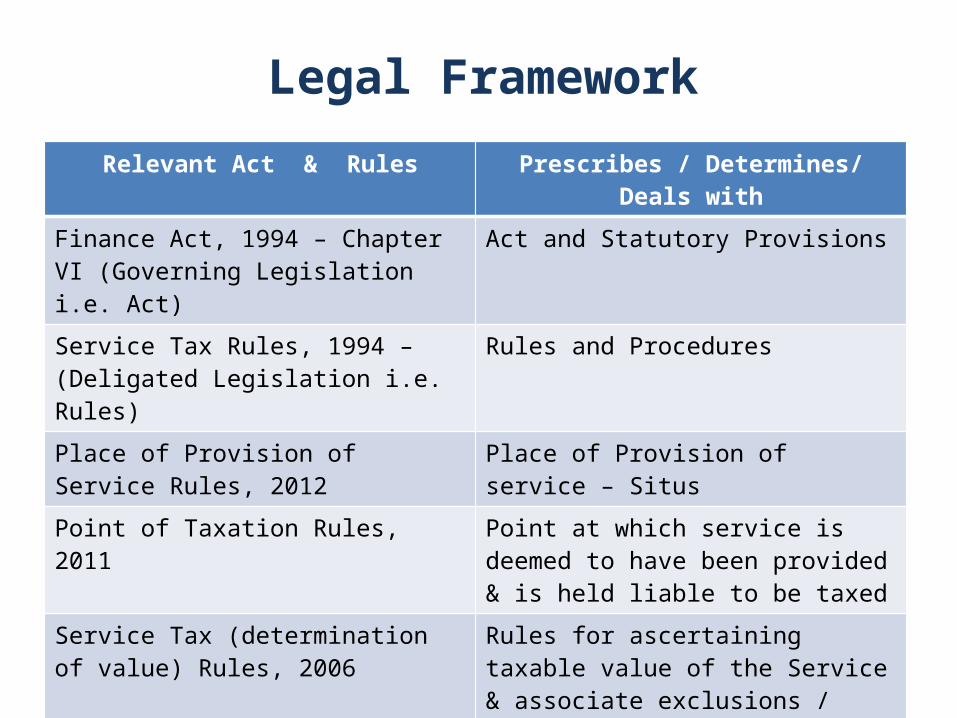

Legal Framework

Relevant Act & Rules Prescribes / Determines/ Deals with

Finance Act, 1994 – Chapter VI (Governing Legislation i.e. Act)

Act and Statutory Provisions

Service Tax Rules, 1994 – (Deligated Legislation i.e. Rules)

Rules and Procedures

Place of Provision of Service Rules, 2012 Place of Provision of service – Situs

Point of Taxation Rules, 2011 Point at which service is deemed to have been provided & is held liable to be taxed

Service Tax (determination of value) Rules, 2006

Rules for ascertaining taxable value of the Service & associate exclusions / inclusions

CENVAT Credit Rules, 2004 Regulations, Procedures & Documents for entitlement, availing and utilisation of in-put tax credit & associate restrictions

Service Tax (Advance Rulings) Rules, 2003 Procedures for Advance Regulations

Service Tax (settlement of cases) Rules, 2012

Procedures for Settlement of cases

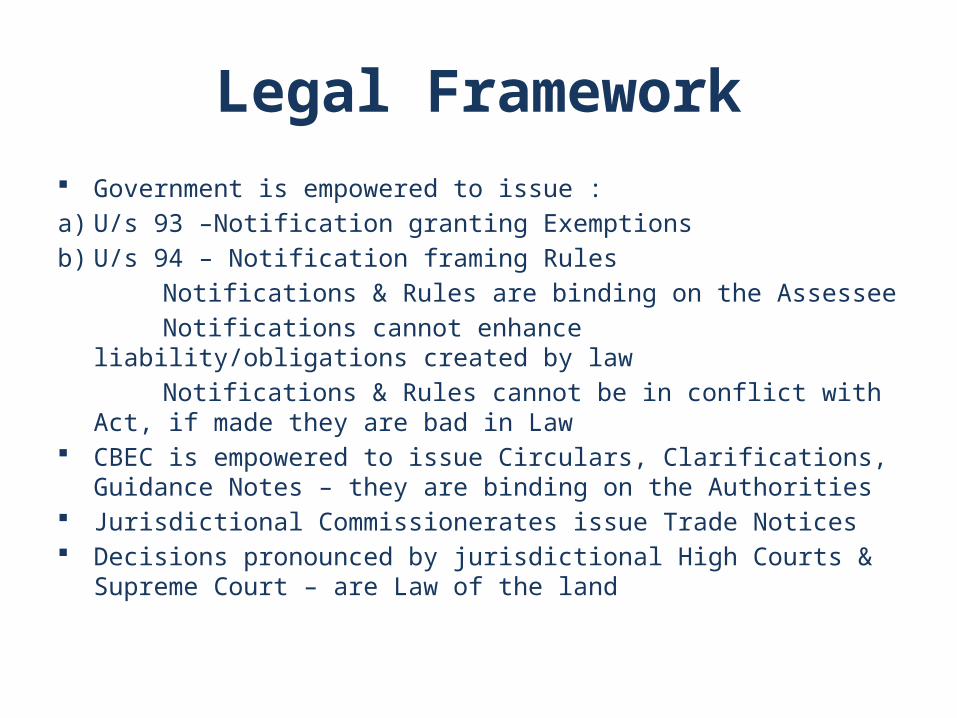

Legal Framework

Government is empowered to issue :a) U/s 93 –Notification granting Exemptionsb) U/s 94 – Notification framing Rules Notifications & Rules are binding on the Assessee Notifications cannot enhance liability/obligations created by law Notifications & Rules cannot be in conflict with Act, if made they

are bad in Law CBEC is empowered to issue Circulars, Clarifications, Guidance

Notes – they are binding on the Authorities Jurisdictional Commissionerates issue Trade Notices Decisions pronounced by jurisdictional High Courts & Supreme

Court – are Law of the land

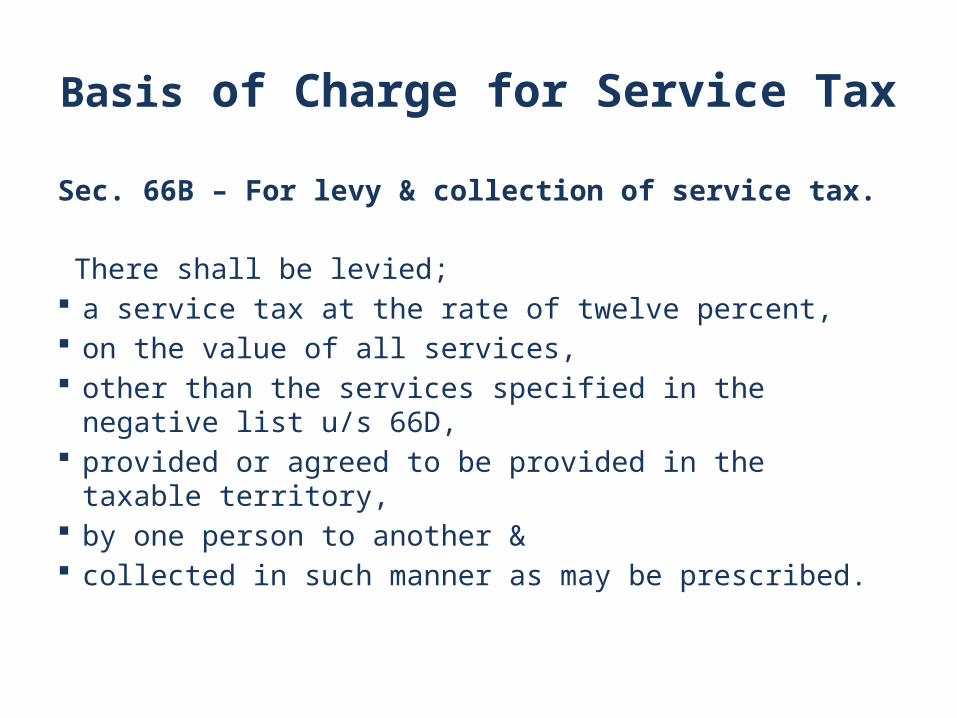

Basis of Charge for Service Tax

Sec. 66B – For levy & collection of service tax.

There shall be levied; a service tax at the rate of twelve percent, on the value of all services, other than the services specified in the negative

list u/s 66D, provided or agreed to be provided in the taxable

territory, by one person to another & collected in such manner as may be prescribed.

Prerequisites of Taxing Provision – is fully satisfied by the charging

provision

Prerequisite of a Taxing provision

Relevant component of Sec. 66B

1. Subject matter of Tax & Taxable event

All services provided or agreed to be provided in Taxable Territory, other than the services specified in negative list.

2. The person on whom Tax is imposed & who is liable to pay Tax

Service provider / service recipient as may be specified

3. Rate of Tax 12 %

4. Quantification / measure of Tax Value of service

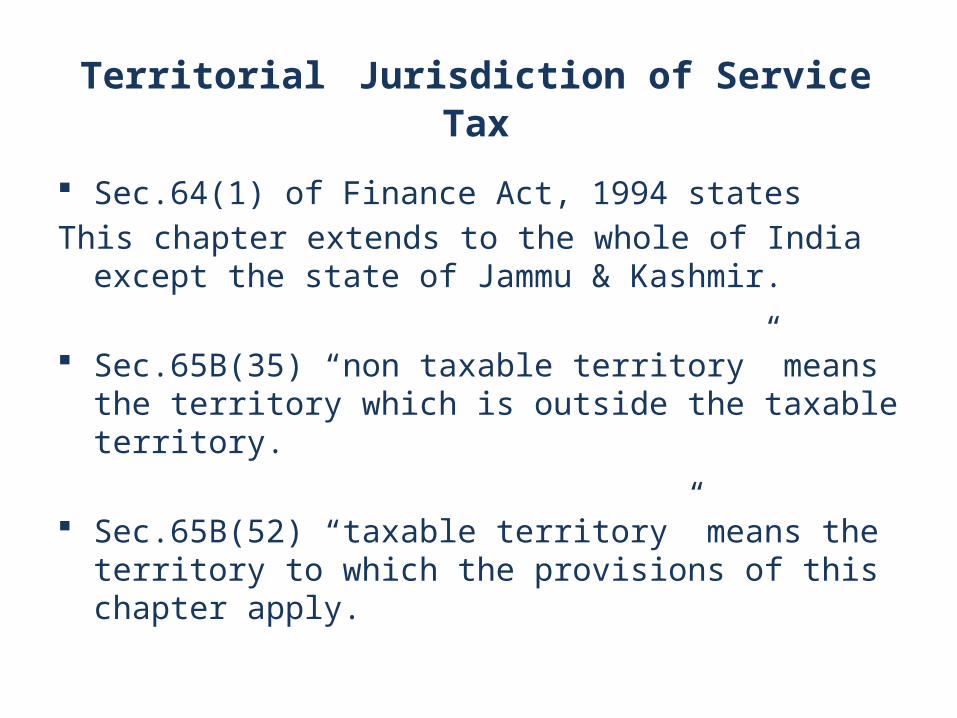

Territorial Jurisdiction of Service Tax

Sec.64(1) of Finance Act, 1994 statesThis chapter extends to the whole of India except

the state of Jammu & Kashmir.

Sec.65B(35) “non taxable territory” means the territory which is outside the taxable territory.

Sec.65B(52) “taxable territory” means the territory to which the provisions of this chapter apply.

Territorial Jurisdiction of Service Tax

Sec. 65B(27) “India” means,

a) The territory of the Union as referred to in the Constitution - Article 1 clause 2 & 3;

b) Its territorial waters, continental shelf, exclusive economic zone or any other maritime zone as defined in the Territorial Waters, Continental Shelf, Exclusive Economic Zone, & Other Maritime Zones Act, 1976;

c) The seabed & the subsoil underlying the territorial waters;d) The air space above its territory & territorial waters; &e) The installations, structures & vessels located in the

continental shelf of India & the exclusive economic zone of India, for the purpose of prospecting or extraction or production of mineral oil & natural gas & supply thereof;

Definition of Service

Sec. 65B (44) “service” means, any activity carried out by a person for another for consideration and includes declared service (u/s 66E), But shall not includea) an activity which constitutes merely-i. a transfer of title in goods or immovable property by way of sale, gift or

in any other manner; orii. Transfer, delivery or supply of any goods, which is a deemed sale under

Article 366(29A) of Constitution of India; andiii. a transaction in money or actionable claim;b) a provision of service by an employee to an employer in the course of

or in relation to his employment;c) Fees taken in any court or tribunal established under any law for the

time being in force.

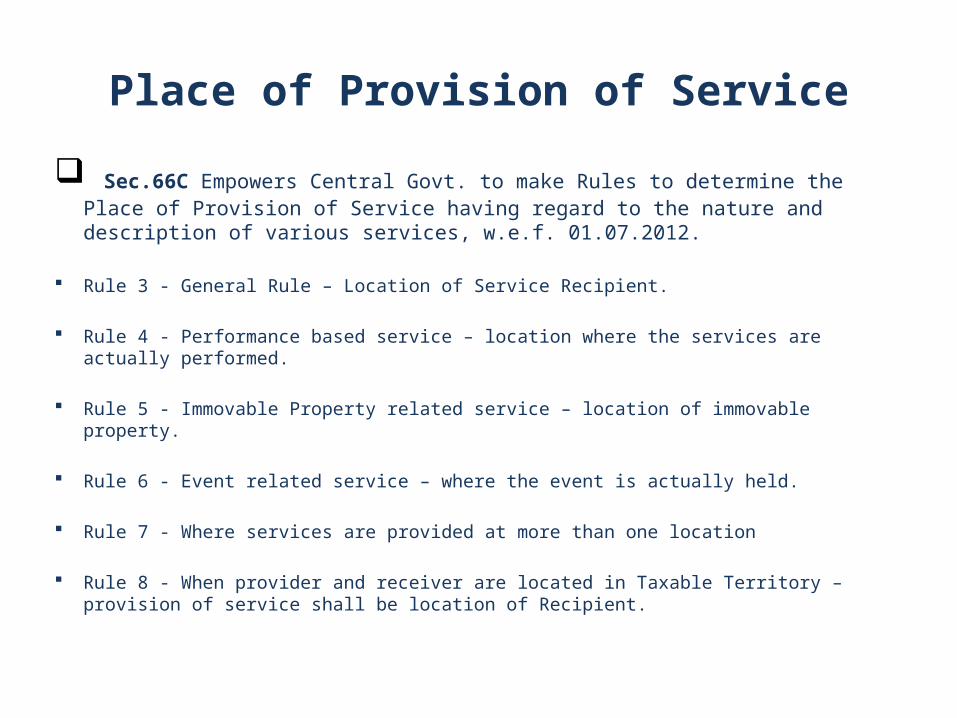

Place of Provision of Service

Sec.66C Empowers Central Govt. to make Rules to determine the Place of Provision of Service having regard to the nature and description of various services, w.e.f. 01.07.2012.

Rule 3 - General Rule – Location of Service Recipient.

Rule 4 - Performance based service – location where the services are actually performed.

Rule 5 - Immovable Property related service – location of immovable property.

Rule 6 - Event related service – where the event is actually held.

Rule 7 - Where services are provided at more than one location

Rule 8 - When provider and receiver are located in Taxable Territory – provision of service shall be location of Recipient.

Place of Provision of Service Rule 9 - Place of provision of “Specified Services” shall be place of service

provider. (Presently 4 services are covered –Banking Co/Fin. Institution/NBFC to it’s

customers, Online information and data base access or retrieval services, Intermediary services, hiring of means of transport up-to a period of one month.)

Rule 10 – Goods transportation service (other than GTA) shall be place of destination of goods.

Rule 11 – Passenger Transportation service – place of embarkation for continuous journey.

Rule 12 – Provision of services provided on board a conveyance.

Rule 13 – Powers to Notify description of Service or circumstances for certain purpose.

Rule 14 – “Tie-Breaker Test” – Later Rule to apply.

Negative List of Services

Sec. 66D Negative List shall comprise the following services:-

a) Services by Government or Local Authority excluding - i)specified postal services, ii) services in relation to aircraft or vessel inside or outside the precincts of a port or an airport, iii) transport of goods or passengers, support services other than the above provided to business entities.

b) Services by Reserve Bank of Indiac) Services by Foreign Diplomatic Mission located in Indiad) Services relating to Agriculture or agricultural producee) Trading of goodsf) any process amounting to manufacture or production of goodsg) Selling of space or time slots for advertisements other than

advertisement broadcast by radio or televisionh) Service by way of access to a road or bridge on payment of toll

charges

Negative List of Services

i) betting, gambling or lotteryj) admission to entertainment events or access to amusement facilitiesk) Transmission or distribution of electricity by the utilityl) pre-school education, approved vocation course, or education as per the

curriculum for obtaining qualification recognized by any law for the time being in force.

m) Renting of residential dwelling for use as residencen) Extending of deposits, loans or advance for consideration by way of

interest or discount & inter-say sale or purchase of foreign currency amongst banks or amongst authorized dealers for foreign exchange or amongst banks & such dealers.

o) Service of transportation of passengers by specified modesp) Services by way of transportation of goods by road except GTA & Courier

by inland waterway & by aircraft or vessel from out of India q) funeral, burial, crematorium or mortuary services including transportation

of the deceased.

Declared Services

Sec. 66E The following shall constitute Declared Services, namely:-

a) Renting of immovable property;b) Construction of a complex, building, civil structure or a part thereof,

wholly or partly, except where the entire consideration is received after issuance of completion certificate by the competent authority;

c) Temporary transfer or permitting the used) or enjoyment of any intellectual property right;e) Development, design, programming, customization, adaptation, up-

gradation, enhancement, implementation of information technology software;

f) Agreeing to the obligation or refrain from an act, or to tolerate an act or a situation, or to do an act;

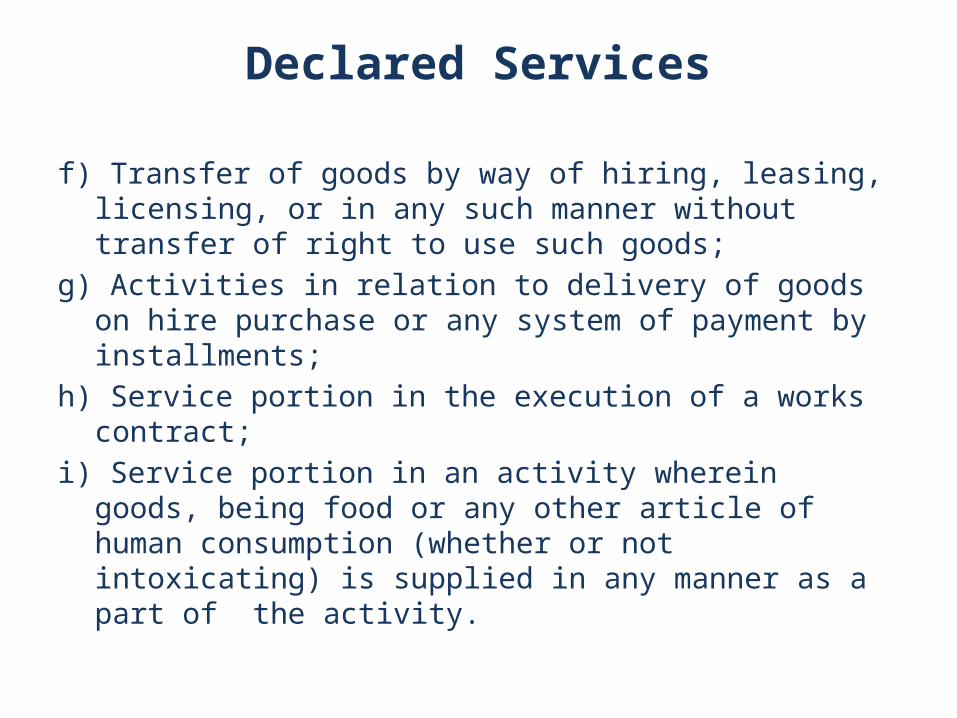

Declared Services

f) Transfer of goods by way of hiring, leasing, licensing, or in any such manner without transfer of right to use such goods;

g) Activities in relation to delivery of goods on hire purchase or any system of payment by installments;

h) Service portion in the execution of a works contract;i) Service portion in an activity wherein goods, being

food or any other article of human consumption (whether or not intoxicating) is supplied in any manner as a part of the activity.

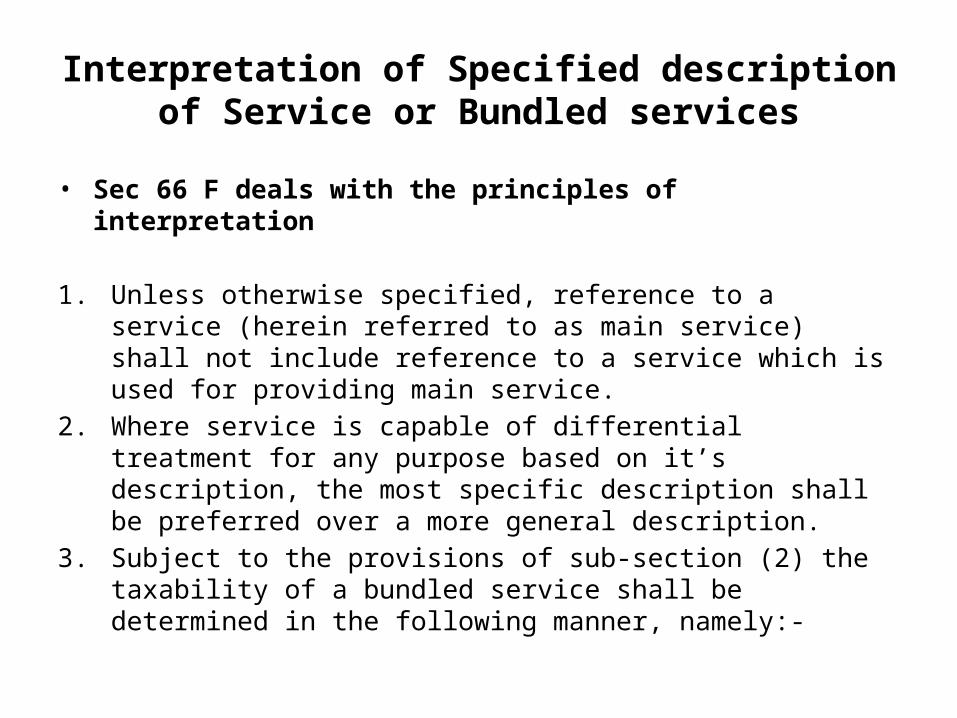

Interpretation of Specified description of Service or Bundled services

• Sec 66 F deals with the principles of interpretation

1. Unless otherwise specified, reference to a service (herein referred to as main service) shall not include reference to a service which is used for providing main service.

2. Where service is capable of differential treatment for any purpose based on it’s description, the most specific description shall be preferred over a more general description.

3. Subject to the provisions of sub-section (2) the taxability of a bundled service shall be determined in the following manner, namely:-

Interpretation of Specified description of Service or Bundled services

a) If various elements of such service are naturally bundled in the ordinary course of business, it shall be treated as provision of the single service which gives such bundle it’s essential character

b) If various elements of such service are not naturally bundled in the ordinary course of business, it shall be treated as provision of single service which results in highest liability of service tax.

Explanation – for the purpose of sub-section (3), the expression “bundled service” means a bundle of provision of various services wherein an element of provision of one service is combined with an element or elements of provision of any other service or services.

Valuation of taxable services for

charging service tax • Sec 67 deals with valuation of taxable services

1. (i) where provision of service is for a consideration in money – the gross amount charged by service provider for such service provided or to be provided by him;(ii) where provision of service is for a consideration not wholly or partly consisting of money, be such amount in money as, with the addition of service tax charged, is equivalent to the consideration;(iii) where provision of service is for a consideration which is not ascertainable, be the amount as may be determined in the prescribed manner

2. Where gross amount charged by service provider is inclusive of service tax payable, value shall be such amount as, with the addition of tax payable, is equal to the gross amount charged.

Valuation of taxable services for charging service tax

3. The gross amount charged for the taxable service shall include any amount received towards the taxable service before, during or after provision of such service.

4. Subject to sub-section (1), (2) and (3), the value shall be determined in such manner as may be prescribed

Explanation – for the purpose of this section:-

a) “consideration” includes any amount that is payable for the taxable services provided or to be provided;

b) “money” – deleted w.e.f.01.07.2012

c) “gross amount charged” includes payment by cheque , credit card, deduction from account and any form of payment by issue of credit notes or debit notes and book adjustment, and any amount credited or debited, as the case may be, to any account, whether called “suspense account” or by any other name, in the books of account of a person liable to pay service tax, where the transaction of taxable service is with any associated enterprise.

Date of determination of rate of tax, value of taxable service and rate of exchange

• Sec 67A statesThe rate of service tax, value of taxable service and

rate of exchange, if any, shall be the rate of service tax or value of taxable service or rate of exchange, as the case may be, in force or as applicable at the time when the taxable service has been provided or agreed to be provided.

Explanation – for the purpose of this section, “rate of exchange means” rate of exchange referred to in Explanation to Sec 14 of the Customs Act, 1962.