Embed Size (px)

Citation preview

1

©A. Alizadeh Shipping Risk Management Slide 1

Shipping Risk Management

Bunker Risk Management

©A. Alizadeh Shipping Risk Management Slide 2

Topics covered

• What is bunker (fuel oil)?

• World bunker market

• Bunker Risk management in liner shipping • Bunker adjustment factor• Long term bunker contracts

• Bunker Risk in Tramp Shipping

• Bunker derivatives

• Petroleum and Product futures

• Forward contracts

• Swaps

• Options

Shipping Risk Management

2

©A. Alizadeh Shipping Risk Management Slide 3

• Bunker fuel is essentially a "Residual" fuel that was originally defined

as whatever liquid was left behind in the petroleum distillation unit after

the removal of more valuable products like kerosene, diesel and naphtha

• There are two basic grades of bunker fuel, IFO 180 and the more widely

used, IFO 380.

• The distinction between the two grades is the distillate content, Grade

180 has 7-15% distillate content, while Grade 380 has 2-5% distillate

content. The higher the distillate content, the more energy the fuel has.

• 60% of world volume in bunkers is IFO380, 30% IFO180 and other

grades, with the remaining 10% in Marine Diesel Oil,

World Bunker Markets

©A. Alizadeh Shipping Risk Management Slide 4

• The IFO380 used in modern ships reflects the technological

advances in the design and efficiency of the engines.

• In general, ships use bunker fuel for propulsion and diesel oil

for manoeuvring in ports and electricity generators.

• Although, recent technological advances enabled ships to use

lower grade bunker fuel more efficiently, high grade bunker is

still used by more sophisticated ships, especially cruise ships

and fast ferries.

World Bunker Markets

3

©A. Alizadeh Shipping Risk Management Slide 5

• Marine bunkers are almost bought and sold in almost every

port in the world

• However, there are a few major bunkering regions in the world

in which the bulk of physical bunkering activities takes place

• These markets are Singapore, Rotterdam and Houston• Singapore has long flourished as a transshipment centre due to its

strategic geographical location.

• Rotterdam (ARA) has been the transshipment centre in Europe

• Houston has been the main bunkering port in the US Gulf

• Other markets include: Hamburg, Fujaira, Yokohama, New

York, Hong Kong, Pusan, etc.

World Bunker Markets

©A. Alizadeh Shipping Risk Management Slide 6

Between 1996 to 2000, roughly 140 million mt of bunker fuels was

consumed per year globally. This has gone up to an estimated

amount of about 200 million mt per year.

• The Singapore bunker market is by far the largest marine fuels market in

the world, with turnover in marine fuel oil 28.5 million mt in 2010

• In Europe, bunker trade volume in Rotterdam reached 13.4 million mt in

2010. However, the combined Amsterdam–Rotterdam–Antwerp (ARA)

region trade is much higher

• Bunkering on the US Gulf coast is dominated by Houston, recording an

estimated annual sales volume of about 5 million mt in year 2010.

World Bunker Markets

4

©A. Alizadeh Shipping Risk Management Slide 7

Historical Bunker prices in major shipping ports

Risk Management in Shipping Operation

Source: Clarkson’s SIN

0

100

200

300

400

500

600

700

800

900

US

$/M

T

Rotterdam Houston Singapore Fujairah Japan

©A. Alizadeh Shipping Risk Management Slide 8

• Bunker fuel is one of the major operating expenses of any shipownerand shipping company, depending on the duration of the voyage accounting for almost 10% to 95% of voyage costs

• The volatility of bunker markets leaves shipowners and operators in a very difficult position as their operating profit may be wiped off very quickly due to sudden changes in bunker prices

• Bunker risk management is important since • It provides greater control over operational costs and secures profit

margins

• Company's creditworthiness can be improved through stabilisation of cash flow and profitability.

Bunker Risk Management

5

©A. Alizadeh Shipping Risk Management Slide 9

Bunker Risk Management

Weekly changes in 380cst bunker prices in Rotterdam, Housmt and Singapore

Average price change and volatility of weekly bunker prices in different

bunkering locations (1990 to 2007)

Rotterdam Houston Singapore Fujairah Japan

Average Price $/mt 158.67 161.98 172.38 169.49 200.34

Min Price $/mt 50.50 48.50 52.00 51.00 59.00Max Price $/mt 707.00 747.00 745.50 736.00 792.50Ave Price Change 0.0509 0.0649 0.0446 0.0456 0.0464Volatility SD 0.4036 0.4329 0.4063 0.3808 0.3142

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

Ja

n-9

0

Ja

n-9

1

Ja

n-9

2

Ja

n-9

3

Ja

n-9

4

Ja

n-9

5

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

US

$/m

t

Rotterdam Houston Singapore

©A. Alizadeh Shipping Risk Management Slide 10

• To see how bunker price fluctuations affect shipowners’ P/L, consider the

following example

• A panamax owner fixes a contract of affreightment (CoA) for 150,000 mt

of cargo today, which requires 3 shipments, one every 2 months, at a rate of

25$/mt.

• The freight contract generates $1,250,000 (25$/mt x 50,000 mt) every two

months.

• If the current bunker price is 300$/mt, and the ship consumes 2500 mt of

bunker per voyage, the expected profit for the shipowner from each voyage,

assuming that port charges are $150,000, will be $350,000.

• Now consider the case where bunker prices increase by 20% to 360$/mt in

two months time. This results in an overall reduction in profits of $450,000

for the entire contract, $150,000 for each voyage.

Bunker Risk Management

6

©A. Alizadeh Shipping Risk Management Slide 11

©A. Alizadeh Shipping Risk Management Slide 12

In order to efficiently and effectively use derivatives to manage

bunker price risk in shipping operations it is essential to know how

these derivatives instruments work

These instruments include

• Petroleum and Petroleum product futures contracts,

• Forward bunker agreements,

• Options on bunker prices

• Bunker swap contracts

There are also other tailor made derivative contracts which are

designed especially to eliminate or control the bunker price risk.

Use of each derivative instrument depends on the need of the shipowner/operator and bunker supplier in terms of costs & benefits

Bunker Risk Management

7

©A. Alizadeh Shipping Risk Management Slide 13

Fuel oil Futures Contracts

• Fuel oil futures were traded in the Singapore Mercantile

Exchange (SIMEX) during the period 1988 to 1992, however,

due to the decline in trading volume and illiquidity of the

contracts, SIMEX withdrew the contract.

• The International Petroleum Exchange attempted to launch a

bunker futures contract in January 1999. This proved

unsuccessful and the contract was withdrawn after six months.

• The reason for the failure of these contracts is that shipowners

and suppliers are exposed to price fluctuations in different

geographical locations while bunker futures were only

available for one location (Rotterdam)

Bunker Risk Management

©A. Alizadeh Shipping Risk Management Slide 14

CONTRACT SIZE QUOTE TICK

NYMEX

1. WTI Crude at Cushing 1000 bbl US$/bbl $ 0.01/bbl=$10/contract

2. HEATING OIL #2 42000 US gl US$/gl $ 0.01/gl=$4.2/contract

3. UNLEADED GAS 42000 US gl US$/gl $0.01/gl=$4.2/contract

IPE

1. Brent Crude oil 1000bbl US$/bbl 0.01/bbl=$10/contract

2. GASOIL 100 mt US$/mt $ 0.25/mt=$25/contract

SIMEX

1.Crude Oil Brent 1000 bbl US$/bbl $0.01/bbl=$100/contract

• Apart from Futures contracts, Options on WTI crude, Heating Oil,

Unleaded Gas and crack spreads are also traded at NYMEX

• In the IPE, options on Brent crude and Gasoil are also available

Bunker Risk Management

8

©A. Alizadeh Shipping Risk Management Slide 15

Rotterdam

IFO380

Singapore

IFO380

Houston

IFO380

NYMEXHO NYMEXCO NYMEXGO IPECO IPEGO

Rotterdam IFO380 1.0000

Singapore IFO380 0.4993 1.0000

Houston IFO380 0.3956 0.4679 1.0000

NYMEXCO 0.4228 0.3527 0.2646 1.0000

NYMEXHO 0.3832 0.3001 0.2272 0.6366 1.0000

NYMEXGO 0.4081 0.3255 0.2242 0.6088 0.6546 1.0000

IPECO 0.4671 0.3249 0.2264 0.6590 0.8007 0.6859 1.0000

IPEGO 0.4991 0.4131 0.2975 0.8231 0.7016 0.6304 0.7194 1.0000

• Since fuel oil is a low derivative of crude oil and one would expect crude

or petroleum prices to move closely together (positive correlation), then

it might be possible to use exchange traded petroleum and petroleum

product derivatives to hedge bunker price risk

• Let us see how strong is the correlation between bunker prices in

different bunker markets and oil futures.

Bunker Risk Management

©A. Alizadeh Shipping Risk Management Slide 16

• Due to the poor effectiveness of cross commodity hedging in the

bunker markets, use of OTC instruments such as forwards, swaps and

options has become increasingly popular.

• In recent years, especially following the wake of development of a

variety of OTC derivative products for fuel oil, such instruments have

become quite popular in bunker price risk management too.

• OTC products are tailor-made and designed to suit the individual

needs of agents involved in the bunker market.

• Nowadays many financial institutions and commodity trading houses

such as Barclays Capital, Morgan Stanley, Calyon etc., offer OTC

bunker derivative products such as forward contracts, swaps and

options.

Bunker Risk Management

9

©A. Alizadeh Shipping Risk Management Slide 17

Forward Bunker Contracts

• Recently, OTC instruments such as forwards, swaps and options have become increasingly popular in the bunker market.

• A forward bunker contract is defined as an agreement between a

seller and a buyer to exchange a specified quantity of fuel oil of

certain quality, at an agreed price, at certain delivery location

and time in the future.

• Forward contracts are usually paper contracts in the sense that

settlement is made on the difference between the contracted

price and the price for bunker at the delivery point, although

physical deliveries are also possible.

©A. Alizadeh Shipping Risk Management Slide 18

Forward Bunker Contracts

• Forward Bunker Contracts are effective tools for bunker price

risk management but they there is credit risk involved

• Many financial institutions and commodity trading houses such

as Barclays Capital, Morgan Stanley, Calyon etc., offer OTC

bunker derivative products such as forward contracts, swaps

and options.

• Imarex launched their Bunker Forward contracts in Dec 2005• Rotterdam 3.5% S Barges FOB

• NWE 1.0% S Cargo FOB

• Singapore HSFO 380 C/St FOB

• Singapore HSFO 180 C/St FOB

• Fujairah IFO380 c/St Bunker FOB

10

©A. Alizadeh Shipping Risk Management Slide 19

Example:• On 8 Jan 2009 a shipowner fixes a voyage charter contract for end of

February 2009.

• The shipowner expects to purchase 5000 tonnes of bunker fuel @ Houston

for this voyage. The current bunker price at Houston is 420$/tonne

• The owner expects the price to increase by February and if the price goes

above 420$/tonne, the shipowner will lose $5000 for every 1$ increase in

prices. If prices go to 450$/tonne, the profit from the voyage will be zero

• Through a broker, he finds that forward bunker prices for 5000 tonnes at

Houston for August is 425$/tonne

• Therefore, he decides to hedge the bunker for the voyage by entering into

(buying) a forward bunker contract for Feb at 425$/tonne

• In this way the owner locks into a bunker price of 425$/tonne.

Forward Bunker Contracts

©A. Alizadeh Shipping Risk Management Slide 20

1-month forward bunker hedge for the period 8 Jan to 28 Feb 2009

Physical Market Forward Market

8 July 2009 Spot bunker price: 420$/tonne Feb 09 Forward bunker price: 425 $/tonne

Total current bunker cost :

$2,100,000 (=5,000*420$/t)

Expected total bunker cost :

$2,125,000 (=5,000 * 425$/t)

Shipowner buys 5000 tonnes of forward bunker expiry 28 Feb 2009 for 425$/t

28 Feb 2009 Spot bunker price: 455$/tonne Feb 2009 forward bunker Settlement: 455 $/tonne

Total bunker cost :

$2,275,000(=5000*455$/t)

Settles the difference between forward bunker price and

Feb market price

$150,000=(455 - 425)*5,000

Loss in the Physical Market Profit from FBA transaction

2,125,000 –2,275,000 = - $150,000 (455- 425)*5,000 = $150,000

Net Result from Hedging = $0

Forward Bunker Contracts

11

©A. Alizadeh Shipping Risk Management Slide 21

Average and standard deviations (volatility) of spot and forward bunker prices in four major bunkering ports

around the world: April 1997 to May 2002

US Gulf

Houston

New York

Harbour

Asia

Singapore

ARA

Rotterdam

Spot

102.40

(29.22)

114.91

(32.93)

110.35

(35.26)

98.60

(27.99)

1 month Forward

102.27

(28.28)

114.73

(31.79)

115.20

(34.78)

100.83

(28.02)

2 month Forward

102.40

(27.25)

115.02

(30.62)

113.93

(32.88)

100.61

(26.68)

3 month Forward

NA

NA

115.35

(29.69)

113.02

(31.48)

100.79

(25.70) All f igures are in $/t

Figures in brackets are standard deviations

We can compare the mean and volatilities of spot and forward bunker prices in different bunkering ports to asses the risk involved in bunker prices

• It can be seen that on average prices are higher in New York, Singapore, compared to

US Gulf and Rotterdam

• Also volatilities decrease as contract maturity increases. This is in line with the

behaviour of forward prices for commodities

• Volatilities are higher in Singapore and New York compared to US Gulf and

Rotterdam

Forward Bunker Contracts

©A. Alizadeh Shipping Risk Management Slide 22

A forward curve (forward bunker curve) is the plot of available forward prices across time. For example plot of 1m, 2m and 3m prices as a percentage of spot prices.

It is also interesting to look at the behaviour (shape) of forward bunker curves and compare them across different bunkering ports

• Forward bunker curves reflects the market’s believe of future bunker prices

• It can be seen that forward bunker curves behave differently at different point

in time and across regions. For example, in September 1997, forward bunker

curve in Rotterdam has show increasing bunker prices over the next few

months

• Whereas, in September 1997, forward bunker prices in Asia signals a drop in

bunker prices over the next three months.

• The slope of the curve also contains information on the volatility of the market

Forward Bunker Contracts

12

©A. Alizadeh Shipping Risk Management Slide 23

Rotterdam Bunker Forward Curves at Different Points in Time

96

98

100

102

104

106

108

110

Rotterdam 1m FWD Rotterdam 2m FWD Rotterdam 3m FWD

% o

f Spo

t pric

e

Sep-97 Sep-98 Sep-99 Sep-00 Sep-01

Forward Bunker Curves

©A. Alizadeh Shipping Risk Management Slide 24

Asian Bunker Forward Curves at Different Points in Time

98

99

100

101

102

103

104

105

106

Asia 1m FWD Asia 2m FWD Asia 3m FWD

% o

f Spo

t pric

e

Sep-97 Sep-98 Sep-99 Sep-00 Sep-01

Forward Bunker Curves

13

©A. Alizadeh Shipping Risk Management Slide 25

Bunker Swaps

©A. Alizadeh Shipping Risk Management Slide 26

• Swaps are perhaps the most popular instruments for bunker price

risk management and many banks and commodity trading houses

now offer bunker swap contracts as a part of their derivative

products.

• Swaps are OTC arrangements, which involve no transfer of

physical commodity, and are settled in cash at the maturity date(s).

• Swap contracts are normally done through a third party known as

swap facilitator or broker. • The role of the swap facilitator is to help the two counterparties identify

each other and help them to settle swap contract transaction. Therefore,

swap facilitators, act as intermediaries.

Bunker Swap Contracts

14

©A. Alizadeh Shipping Risk Management Slide 27

Bunker Swaps: The Benefits

• Bunker swaps can protect the buyer (shipowner) from the

impact of adverse movements in bunker prices on the profits.

• From a bunker supplier point of view entering into a bunker

swap contract can stabilise the selling price of his bunker

stock and consequently his revenue.

• Swaps are a customised product that can be tailored to the

needs of the principal, be he the shipowner or bunker

supplier.

©A. Alizadeh Shipping Risk Management Slide 28

• Swap providers are normally market makers who take differentpositions at any point in time

• This means that they exposed to risk each time they enter a swaparrangement.

• However, for every position, they try to take an offsetting positionwith another counterparty.

• Their gain is the difference in prices of the two offsetting contracts(i.e. the premium) which cover the costs of taking risk and subsequenthedging

• The premium also reflects the credit risk of the customer

• Market makers provide liquidity

Bunker Swaps: Role of the Market Maker

15

©A. Alizadeh Shipping Risk Management Slide 29

• In this example AAA Shipping swaps a fixed for floating bunker payment

with XXX refinery through the swap facilitator.

• AAA swaps a flat price of 325 $/mt for a floating price

• XXX swaps a floating price for a flat price of 315 $/mt

Shipowner

AAA Shipping

Swap

Counter-party

XXX refinery

Flat Price 325$/mt

Floating Price

Swap

Facilitator

YYY Capital

Flat Price 315$/mt

Floating Price

• A net profit of 10$/mt for the facilitator

• Security of cost and revenue for shipowner and bunker seller

• The swap facilitator may add premium to flat or floating prices to

compensate for the credit risk involved for each contract

Bunker Swaps: The Mechanics

©A. Alizadeh Shipping Risk Management Slide 30

Bunker Swap Contracts; Pricing

In a Plain Vanilla swap contract: • when the spot bunker price is greater than the swap rate (e.g. 325$/t), then the

shipowner is compensated by the swap seller for the increased bunker price over the swap rate,

• whereas when the spot bunker prices is less than the swap rate (e.g. 325$/t), the shipowner has to compensate the seller with the difference between the market price and the swap rate.

100.00

200.00

300.00

400.00

500.00

Janu

ary

Feb

ruar

y

Mar

ch

Apr

il

May

June

July

Aug

ust

Sep

tem

ber

Oct

ober

Nov

embe

r

Dec

embe

r

Us

$/m

t

Floating Price $/mt Sw ap Price $/mt

16

©A. Alizadeh Shipping Risk Management Slide 31

Pricing a swap contract

Price of a swap contract can be determined using prices of forward

contract for the same amount of the underlying variable for the

same expiry time as the swap contract.

For example, the swap contract mentioned in the previous example

is equivalent to a 12-month forward contract staring from January

for every month thereafter. The price of each forward contract

therefore set to 325$/mt.

Pricing Bunker Swap Contracts

©A. Alizadeh Shipping Risk Management Slide 32

]),()[,(1

)(1

m

k

kk KstFstPm

tSP

• Plain Vanilla Bunker Swaps can be priced directly from forward

bunker curves since the appropriate portfolio of forward contracts

is a hedge for the swap contract

• This is because the price of each reset date is the same as the price

for a forward for that date

• Therefore, if F(t,sk) is the floating price, K is fixed price and

P(t,sk) is discount factor from period sk to today, we can write the

value of a swap as

Pricing Bunker Swap Contracts

17

©A. Alizadeh Shipping Risk Management Slide 33

As an example consider that in December 2006, forward bunker prices for

January, February and March 2007 are, $230, $250 and 262$/mt, (e.g.

1000 mt) respectively, while 1, 2 and 3 month interest rates are all 5%,

4.75% and 4.25% per annum, respectively.

Using the above formula, a fair value for the fixed price of the swap contract for the following 3 months has to be 247.30$/mt to set the value of the swap to zero in December 2006.

The reason is that if there is any differences between the prices, agents will arbitrage any riskless profits

30 Dec 2006 Jan 2007 Feb 2007 Mar 2007

Forward Price 230 250 262

Fixed Price ? ? ?

Interest rates 5% 4.75% 4.5%

Pricing Bunker Swap Contracts

©A. Alizadeh Shipping Risk Management Slide 34

However, the swap provider may ask for a higher fixed price to

initiate the swap contract. This is a protective measure against the risk

that he is exposed to by taking a position

This might be spot market risk as well as credit risk

Using Excel spreadsheet and solver or goal-seek function, it is not

difficult to do this simple calculation

Pricing Bunker Swap Contracts

22-Dec-06 Jan-07 Feb-07 Mar-07

Forward Price 230 250 262

Fixed Price 247.30 247.30 247.30

Interest rates 5% 4.75% 4.50%

swap duration 3

swap value 9.18E-14

18

©A. Alizadeh Shipping Risk Management Slide 35

A Differential Swap is a simple swap contract in which

counterparties exchange the difference between two floating

prices (the differential) for a fixed price differential.

For example, the difference between bunker prices in Singapore

and Rotterdam is exchanged for a fixed price (fixed price diff)

Pricing Bunker Swap Contracts

22-Dec-06 Jan-07 Feb-07 Mar-07

Singapore 230 250 262

Rotterdam 215 238 248

Fix Diff ? ? ?

Actual Diff 15 12 14

Interest rates 5% 4.75% 4.50%

©A. Alizadeh Shipping Risk Management Slide 36

The question is how to price this differential!

We use the same principle as we did for Plain Vanilla swap; that is,

we set the DPV of differences between forwards equal to the

average DPV of fixed differential as follows

where F1(t,sk) and F2(t,sk) are forward prices, K is the fixed

differential and P(t,sk) is discount factor as usual.

It is not difficult to calculate this in excel to get the fixed

differential

m

k

kkk KstFstFstPm

tSP1

21 )],(),([),(1

)(diff_

Pricing Bunker Swap Contracts

19

©A. Alizadeh Shipping Risk Management Slide 37

Therefore, the fixed differential is

Pricing Bunker Swap Contracts

12/312/212/1 )12/045.01(

)248262(

)12/0475.01(

)238250(

)12/05.01(

)215230(

3

1)(diff_

KKKtSP

22-Dec-06 Jan-07 Feb-07 Mar-07

Singapore 230 250 262

Rotterdam 215 238 248

Fix Diff ? ? ?

Actual Diff 15 12 14

Interest rates 5% 4.75% 4.50%

Swap Duration 3

Swap Value 0

©A. Alizadeh Shipping Risk Management Slide 38

So far we discussed the properties of simple swap contracts

But, swap contracts can also be more complex and difficult in structure

designed and offered by financial institutions and commodity trading

houses in order to fulfil the hedging performance and risk management

requirements of the shipowners.

Among these are; • Variable volume swap or swing,

• Participation swap,

• Double up swap,

• Extendable swap, etc.

Each contract has certain specifications, structure and payoff, which

makes it more relevant in to counterparties involved.

• More detail on payoffs and pricing of these types of swap contracts can

be found in Clewlow and Strickland [2000] and Hull [2000].

Different Types of Swap Contracts

20

©A. Alizadeh Shipping Risk Management Slide 39

Bunker Options

©A. Alizadeh Shipping Risk Management Slide 40

Option Contracts on Bunker Prices

Options give the holder the flexibility (right but not the obligation) of

buying or selling the asset at certain pre-specified price during or at certain

period.

The most popular option contracts in the commodity markets, especially

the bunker market are the Asian option contracts.

• An Asian option is similar to an European option in that it can be onlyexercised at the maturity, but it differs from an European option in that eitherexercise price or the spot price at the expiry is calculated as the average ofspot prices over certain period.

• This property of the Asian option is important as sharp fluctuations andexcess volatility in the commodity markets, especially oil markets, increaseboth premium and payoffs of other (Eu or Am) options.

• Therefore, by smoothing the strike prices in Asian options, they become

cheaper instruments for risk management in commodity markets.

21

©A. Alizadeh Shipping Risk Management Slide 41

Bunker Options

When the average spot price over certain period prior to maturity is used

as spot price, then the option is called average price option, whereas

when the average market price over some period prior to maturity is used

as strike price, the option is called average strike option.

It is not difficult to extend these results to Asian call and put options.

• The payoff of a an average price Asian call is

• The payoff of an average price Asian put is

)0,1

max(1

KSm

m

k

k

)0,1

max(1

m

k

kSm

K

©A. Alizadeh Shipping Risk Management Slide 42

Caps and Floors on Bunker Prices

• A caplet is defined as a hedging position, which is the result of a

long call option on an underlying asset.

– Usually the hedger has a short physical position on the same asset.

• A caplet gives its holder the opportunity to limit any possible

future losses due to the increase in the price of the asset.

• Purchase of the call option compensates the owner in the case of

a price rise and provides an upper bound on the price that the

owner has to pay for bunker at expiry.

• A cap is a portfolio of two or more caplets with the same

exercise price but different maturity dates.

22

©A. Alizadeh Shipping Risk Management Slide 43

• A floorlet, on the other hand, is defined as a hedging position,

which consists of a long put option on the underlying asset

– Usually the hedger has a long physical position on the same asset.

• A floorlet gives its holder the opportunity to limit any possible

future losses due to a price drop.

• Purchase of the put option compensates the bunker supplier in

the case a price fall and provides a lower bound on the selling

price that the supplier receives for bunker in two months time.

• A floor is a portfolio of two or more floorlets with the same

exercise price but different maturities.

Caps and Floors on Bunker Prices

©A. Alizadeh Shipping Risk Management Slide 44

Hedging Bunker Prices Using a Cap

• The following example shows how a combination of long call option and

short physical can be used by a shipowner to create a cap for hedging

against adverse bunker price fluctuations

• On 20 December 2006 a tanker owner fixes a voyage for January 2007

and expects the vessel to take bunker towards the end of January. The

owner can leave his bunker cost unhedged, or he can use a call option to

get rid of the risk of market moving against him

• date 20 December 2006

• current bunker price = $302/mt

• bunker is required in 1 months time; i.e. expiry is 1 month - Jan

• amount of bunker required is 10,000 mt, so the option should be

written for 10,000 mt of fuel oil

• detail of the option available for January 2007

• Call with strike price $310/mt and $10/mt premium, Fujairah

23

©A. Alizadeh Shipping Risk Management Slide 45

Hedging Bunker Prices Using a Cap

Caplet hedge for January 2007

Physical Market Options Market

20 December 2006

Bunker price in Fujairah : $302/mt Option Details: January 2007 Call with a strike

Bunker cost: $3,020,000 (=10,000*302) Price of $310/mt, Premium= $10/mt

Shipowner buys January 2007 call at a total cost of $100,000 (=10*10,000)

31 January 2007 – First Scenario

Falling Bunker Market

Bunker price in Fujairah: $280/mt Strike Price ($310) > Settlement Price ($280)

Actual Bunker Cost : $2,800,000 Therefore Option is not exercised

Notional Gain in the Physical Market Payoff from the Option Transaction

3,020,000 – 2,800,000 = - $220,000 $ -100,000

Total Bunker Cost (including option premium) = 2,800,000 + 100,000 = $2,900,000

31 January 2007 – Alternative Scenario

Rising Bunker Market

Bunker price in Fujairah: $350/tonne Strike Price ($310) > Settlement Price ($350)

Actual Bunker Cost : $3,500,000 Therefore Option is exercised

Notional Loss in the Physical Market Payoff from the Options Transaction

3,020,000 – 3,500,000 = - $480,000 (350 – 310) *10,000 –100,000 = $300,000

Total Bunker Cost (including option premium) = $ 3,500,000 - 300,000 = 3,200,000

©A. Alizadeh Shipping Risk Management Slide 46

Profit and loss of the hedged position for the tanker owner10000 mt to buy in January 2007

Hedging Bunker Prices Using a Cap

-600

-400

-200

0

200

400

600

250 270 290 310 330 350 370

Prevailing Bunker Price at the Maturity ($/tonne)

Pro

ffit

& lo

ss fro

m the h

edged P

ort

folio

000$

Long call

Physical M arket Position

Overall Position

24

©A. Alizadeh Shipping Risk Management Slide 47

• The Cap ensures that shipowner pays maximum $113/mt for fuel whatever happens to bunker prices at maturity.

• This means that the risk of losing profits in case of rising bunker prices is protected, while the owner can benefit from falling bunker prices.

Hedging Bunker Prices Using a Cap

250

260

270

280

290

300

310

320

330

340

350

360

370

250 270 290 310 330 350 370

Prevailing Bunker Price at the Maturity ($/tonne)

Price P

aid

by the s

hip

ow

ner

($/tonne)

©A. Alizadeh Shipping Risk Management Slide 48

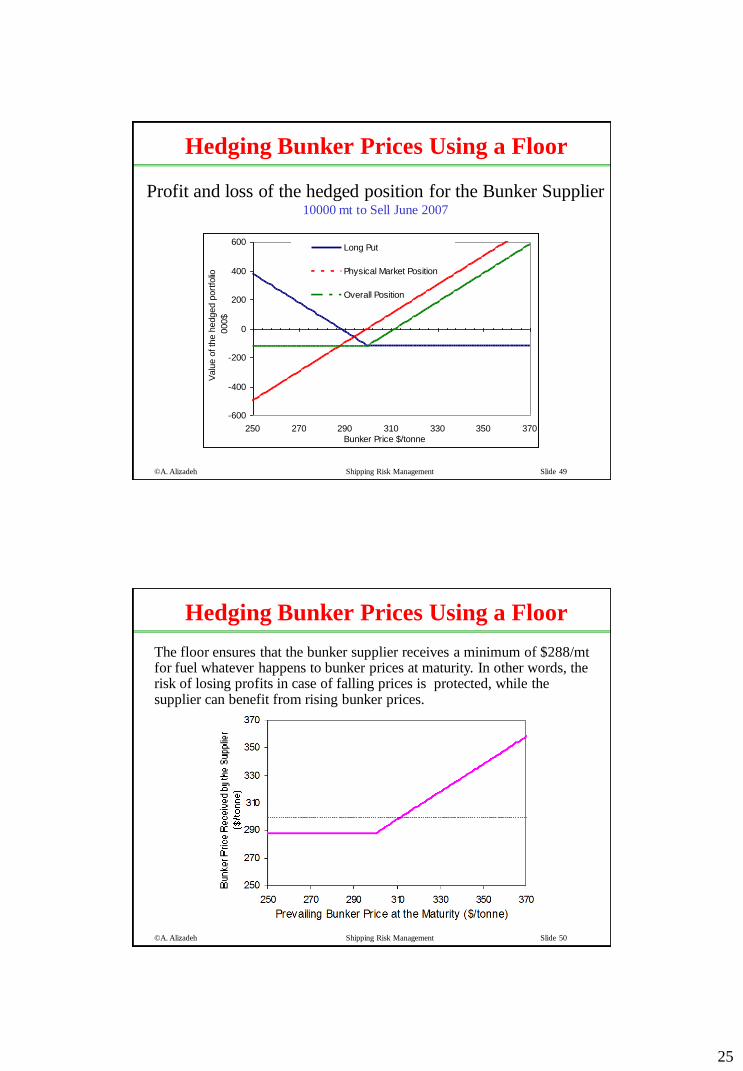

Hedging Bunker Prices Using a Floor

• The following example shows how a bunker supplier can use

combination of long put option and long physical to create a floor for

hedging against adverse bunker price fluctuations

• On 20 March 2007, a bunker supplier expects delivery and sale of

10,000 mt of fuel oil in June. However, he is not sure about the market

condition in June, therefore, he decides to buy put option to protect his

revenue (profit) in June 2007.

• date 20 March 2007

• current bunker price = $305/mt

• bunker will be sold in 3 months time; i.e. expiry is June 2007

• Total bunker is 10,000 mt,

• detail of the option available for June 2007

• Asian average price put option with strike price $300/mt and

$12/mt premium

25

©A. Alizadeh Shipping Risk Management Slide 49

Hedging Bunker Prices Using a Floor

-600

-400

-200

0

200

400

600

250 270 290 310 330 350 370

Bunker Price $/tonne

Valu

e o

f th

e h

edged p

ort

folio

000$

Long Put

Physical Market Position

Overall Position

Profit and loss of the hedged position for the Bunker Supplier10000 mt to Sell June 2007

©A. Alizadeh Shipping Risk Management Slide 50

Hedging Bunker Prices Using a Floor

The floor ensures that the bunker supplier receives a minimum of $288/mt for fuel whatever happens to bunker prices at maturity. In other words, the risk of losing profits in case of falling prices is protected, while the supplier can benefit from rising bunker prices.

26

©A. Alizadeh Shipping Risk Management Slide 51

• Sometimes shipowners (or bunker suppliers) may decide to hedge if

the costs involved is low or even zero.

• It is possible to construct a hedged position through a portfolio of

options (put and call) to have minimum or zero cost

• This type of options are known as zero cost, collar or cylinder options

• The idea is to hedge the bunker fluctuations through selling the upside

risk position and buying downside risk protection

• Therefore, a zero cost collar for a shipowner who has a short physical

position can be constructed by selling a put and using the proceeds to

buy a call option for the same maturity. However, strike prices may

vary and define the protection limits.

Zero Cost Collar for Ship-operator

©A. Alizadeh Shipping Risk Management Slide 52

• As an example consider a shipowner who needs to purchase 10,000

mt of bunker in 3 months time (T=3month) and the current bunker

price is $300/mt.

• The market seems to be very unstable and there are news about

severe volatility in the oil (bunker) market.

• The following options are currently available to him

– Put option, 3m to maturity, strike $290/mt, 10,000 mt volume, $8/mt

– Call option, 3m to maturity, strike $310/mt, 10,000 mt volume, $8/mt

• In order to secure a reasonable bunkering cost and avoid any

uncertainty, as well as paying a large some for such protection, he

decides to use “zero cost collar”

• This is done as follows:

Zero Cost Collar for Ship-operator

27

©A. Alizadeh Shipping Risk Management Slide 53

Zero Cost Collar for Ship-operator

The over all position of the shipowner, a zero cost collarShort physical + short put + long call

-600

-400

-200

0

200

400

600

250 260 270 280 290 300 310 320 330 340 350 360

Prevailing Bunker Price at the Maturity ($/tonne)

Payoff o

f th

e z

ero

-cost C

olla

r

(000$)

Long call (X=310$/t, pr=8$/t, T=3M )

Short put (X=290$/t, pr=8$/t, T=3M )

Physical M arket

Shipowner's Overall Payoff

©A. Alizadeh Shipping Risk Management Slide 54

Zero Cost Collar for Ship-operator

Expected bunker cost for a shipowner using a zero cost collar

260

270

280

290

300

310

320

330

340

350

250 260 270 280 290 300 310 320 330 340 350 360

Prevailing Bunker Price at the Maturity ($/tonne)

Bunker

Price P

aid

by the S

hip

ow

ner

($/tonne)

28

©A. Alizadeh Shipping Risk Management Slide 55

Bunker Risk Management Summary

• The methods and instruments available to shipowners and

bunker supplier to hedge their costs and revenue are by no

means limited

• Here we learned how to asses the risk involved in ship

operation and bunkering activities

• We also learned how to use derivative instruments to hedge

bunker price fluctuations both from the point of view of

shipowner and bunker supplier

• We also learned how to price some of these derivatives

©A. Alizadeh Shipping Risk Management Slide 56

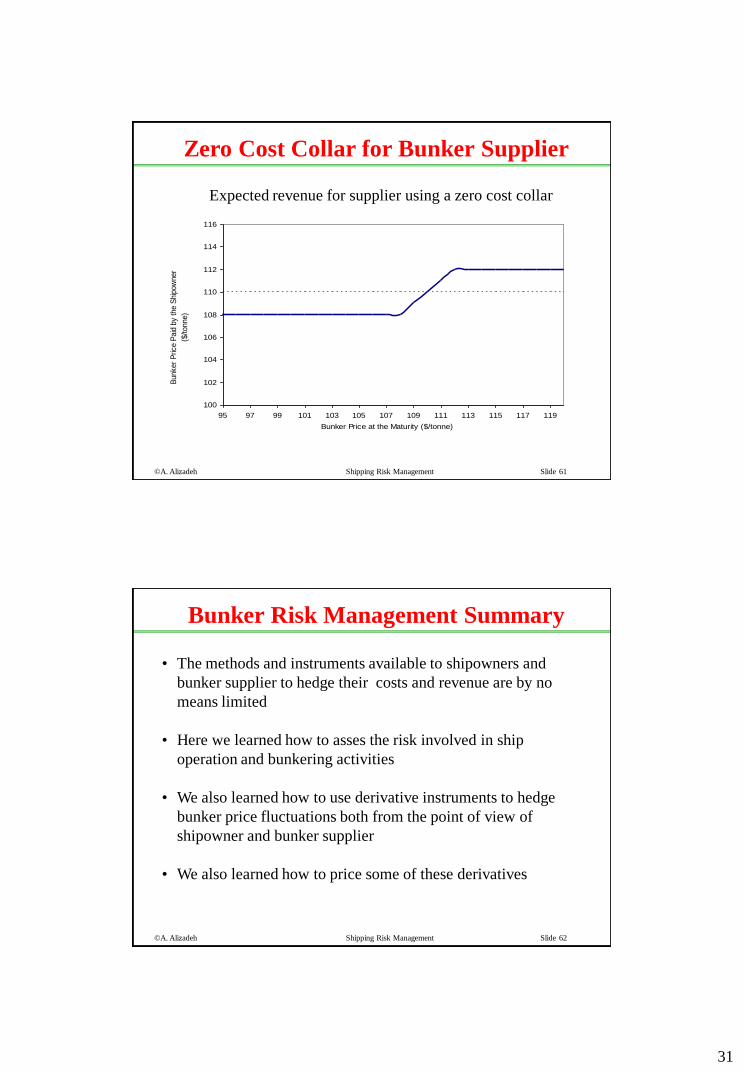

• A zero cost collar for a bunker supplier who has a long physical

position can be constructed by selling a call and using the proceeds

to buy a put option for the same maturity.

• This will give the opportunity to the bunker supplier to secure the

selling price (revenue) of his/her bunker within a range at no cost

• For example consider the supplier has a long physical bunker

position in 3 months and the following options are currently traded

in the market– Put option, 3m to maturity, strike $112/t, 10,000t volume, $2/t premium

– Call option, 3m to maturity, strike $110/t, 10,000t volume, $3/t premium

• A hedged portfolio at zero cost can be constructed by selling call

option and buying put simultaneously in the following form

Zero Cost Collar for Bunker Supplier

29

©A. Alizadeh Shipping Risk Management Slide 57

Zero Cost Collar for Bunker Supplier

The short position of the supplier in the physical market

Assuming an expected price of $110/t

-8

-6

-4

-2

0

2

4

6

8

10

12

102 104 106 108 110 112 114 116 118 120

Bunker Price at the Maturity ($/tonne)

Payoff o

f th

e z

ero

-cost C

olla

r

($/tonne)

Physical Market Position

©A. Alizadeh Shipping Risk Management Slide 58

Zero Cost Collar for Bunker Supplier

The short position of the supplier in the physical market plus a short call ($3/t)

-8

-6

-4

-2

0

2

4

6

8

10

12

102 104 106 108 110 112 114 116 118 120

Bunker Price at the Maturity ($/tonne)

Payoff o

f th

e z

ero

-cost C

olla

r

($/tonne)

Short call (X=110$/t, pr=3$/t, T=3M)

Physical Market Position

30

©A. Alizadeh Shipping Risk Management Slide 59

Zero Cost Collar for Bunker Supplier

The short position of the supplier in the physical market plus a short call ($3/t) and long put ($3/t)

-8

-6

-4

-2

0

2

4

6

8

10

12

102 104 106 108 110 112 114 116 118 120

Bunker Price at the Maturity ($/tonne)

Payoff o

f th

e z

ero

-cost C

olla

r

($/tonne)

Short call (X=110$/t, pr=3$/t, T=3M)

Long put (X=112$/t, pr=3$/t, T=3M)

Physical Market Position

©A. Alizadeh Shipping Risk Management Slide 60

Zero Cost Collar for Bunker Supplier

The short position of the supplier using a zero cost collarLong physical + short cal + long put

-8

-6

-4

-2

0

2

4

6

8

10

12

102 104 106 108 110 112 114 116 118 120

Bunker Price at the Maturity ($/tonne)

Pa

yoff

of t

he

ze

ro-c

ost

Co

llar

($/to

nn

e)

Short call (X=110$/t, pr=3$/t, T=3M)

Long put (X=112$/t, pr=3$/t, T=3M)

Physical Market Position

Supplier's overall position

31

©A. Alizadeh Shipping Risk Management Slide 61

Zero Cost Collar for Bunker Supplier

Expected revenue for supplier using a zero cost collar

100

102

104

106

108

110

112

114

116

95 97 99 101 103 105 107 109 111 113 115 117 119

Bunker Price at the Maturity ($/tonne)

Bunker

Price P

aid

by the S

hip

ow

ner

($/tonne)

©A. Alizadeh Shipping Risk Management Slide 62

Bunker Risk Management Summary

• The methods and instruments available to shipowners and

bunker supplier to hedge their costs and revenue are by no

means limited

• Here we learned how to asses the risk involved in ship

operation and bunkering activities

• We also learned how to use derivative instruments to hedge

bunker price fluctuations both from the point of view of

shipowner and bunker supplier

• We also learned how to price some of these derivatives

32

©A. Alizadeh Shipping Risk Management Slide 63

End of Slides