Embed Size (px)

Citation preview

[1]

A GLOBAL/COUNTRY STUDY AND REPORT

ON

SRILANKA (TEA SECTOR)

Submitted to:

GUJARAT TECHNOLOGICAL UNIVERSITY

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

Masters of Business Administration

UNDER THE GUIDANCE OF

Ms. Shyma Gokul

Assistant Professor

Submitted by:

Shri H.D. Gardi MBA College,

Nyara, Rajkot.

College Code: 780

Affiliated to Gujarat Technological University Ahmedabad

May, 2012

[2]

Chapter-I

Introduction

[3]

Country Selection

Sri Lanka is a neighbor country of India. Sri Lankan culture is match with Indian culture.

Because of major population of Sri Lanka are Indian people. The environment of Sri Lanka is

match with Indian environment. The official name of Sri Lanka is a Democratic Socialist

Republic of Sri Lanka.

GEOGRAPHY OF SRI LANKA

[4]

Area 65,610 sq. km. (25,332 sq. me.).

Population 21.30 million of the Sri Lanka.

Annual population growth rate 0.9% of the Sri Lanka.

Cities: Capital- Colombo population 1.30 million, Sri Jaywardenepur Kotte is the officially

designed capital and is the site of the parliament. Other major cities are Kandy with 1,50,000

population, Galle with 1,10,000, and Jaffna with 1,00,000. Terrain is a coastal plains in the

northern side of the Sri Lanka. Hills and Mountains in southern & central Sri Lanka. It is high at

2,133 meters (7,000 ft.)

Climate of Sri Lanka:

Tropical, Rainy seasons light in northeast, fall and winter, with average rain fall of 50 inch.

Heavy rains fall in south-west Sri Lanka i.e. average 200 inch.

Religion wise division of people in Sri Lanka:

Sinhalese 74% of the total population.

Tamils 18% of the total population.

Muslims 7% of the total population.

Other 1% of the total population.

Languages speak in Sri Lanka:

Sinhala and Tamil (official), English.

Educational details of the Sri Lanka:

There is compulsory education up to 14 years children’s. The primary school attendance is

96.50%. In Sri Lanka, Their literacy ratio is very high i.e. 91% literacy rate in Sri Lanka.

Health of the Sri Lankan people:

[5]

The infant mortality rate of the Sri Lankan people is 18.57 per 1000. The life expectancy of men

in Sri Lanka is 73 years. The life expectancy of women is 77 years.

ECONOMY OF SRI LANKA

Sri Lanka has mostly had strong growth rates in previous years. Sri lanka economy has worth $

59 billion, and per capita GDP of about $7000 (PPP). In GDP per capita terms, it is ahead of

other countries in the South Asian region.

Tea export, Apparel, textile, Rice production and other Agricultural products, Tourism are the

country’s main economic factor.

After 2004 the government has concentrated on mass production of goods for domestic

consumption such as rice, grain and other Agricultural products.

Economic growth suffered in the following years as the economy faced many global and

domestic economic and political challenges. Overall, average annual GDP growth was 5.2% over

1991-2000.

In 2001, however, GDP growth was negative 1.4%--the first negative growth since

independence. The economy was badly affected by a series of global and domestic economic

problems and affected by terrorist attacks in Sri Lanka and the United States.

The crisis bare the fundamental policy failures and structural imbalances in the economy and the

need for reforms. Parliamentary elections were held in December, a pro-capitalist party was

elected to Parliament, while the socialism oriented Sri Lanka Freedom Party retained the

Presidency.

[6]

The government of Ranil Wickremasinghe of the United National Party has indicated a strong

commitment to economic and social sector reforms, deregulation, and private sector

development.

In 2002, the economy experienced a slow recovery. Early signs of a peace dividend were visible

throughout the economy—Sri Lanka has been able to reduce defense expenditures and had

started to focus on getting its large, public sector debt under control.

Also, the economy has benefited from lower interest rates, a recovery in domestic demand,

increased tourist arrivals, a revival of the stock exchange, and increased FDI.

In 2002, economic growth reached 4%, helped largely by strong service sector growth. The

agricultural sector of the economy staged a partial recovery. Total FDI inflows during 2002 were

about $246 million.

[7]

Chapter-II

Factors Affecting Selection of

the country

[8]

PESTLE ANALYSIS

PESTLE is an analytical tool which considers external factors and helps to think about their

impacts.

Is a useful tool for understanding the “big picture” of the environment in which we are operating

By understanding our environment, we can take advantage of the opportunities and minimize

the threats.

This provides the context within which more detailed planning can take place to take full

advantage of the opportunities that present themselves.

THE FACTOR IN PESTLE ANALYSIS

P – Political

(The current and potential influences from political pressures)

Government type and stability

Freedom of the press, rule of law and levels of bureaucracy and corruption

Regulation and de-regulation trends

Social and employment legislation

Tax policy, and trade and tariff controls

Environmental and consumer-protection legislation

Likely changes in the political environment

E – Economic

(The local, national and world economic impact)

[9]

Stage of a business cycle

Current and projected economic growth, inflation and interest rates

Unemployment and supply of labor

Labor costs

Levels of disposable income and income distribution

Impact of globalization

S - Sociological

(The ways in which changes in society affect the project)

Cultural aspects, health consciousness, population growth rate, age distribution,

Organizational culture, attitudes to work, management style, staff attitudes

Education, occupations, earning capacity, living standards

Ethical issues, diversity, immigration/emigration, ethnic/religious factors

Media views, law changes affecting social factors, trends, advertisements, publicity

Demographics: age, gender, race, family size

T - Technological

(How new and emerging technology affects our project / organization)

Maturity of technology, competing technological developments, research funding, technology

legislation, new discoveries

Information technology, internet, global and local communications

Technology access, licensing, patents, potential innovation, replacement technology/solutions,

inventions, research, intellectual property issues, advances in manufacturing

[10]

Transportation, energy uses/sources/fuels, associated/dependent technologies, rates of

obsolescence, waste removal/recycling

L - Legal

(How local, national and global legislation affects the project)

Current home market legislation, future legislation

European/international legislation

Regulatory bodies and processes

Environmental regulations, employment law, consumer protection

Industry-specific regulations, competitive regulations

E - Environmental

(Local, national and global environmental issues)

Ecological, environmental issues, environmental regulations

Customer values, market values, stakeholder/ investor values

Management style, staff attitudes, organizational culture, staff engagement

[11]

SWOT ANALYSIS of Sri Lanka

Strengths:

• Low operational costs

• Presence of established distribution networks in both urban and rural areas

• Presence of well-known brands in sector

Weaknesses:

• Lower scope of investing in technology and achieving economies of scale, especially in

small sectors

• Low exports levels

•"Me-too products, which illegally mimic the labels of the established brands. These products

narrow the scope of products in rural and semi-urban market.

Opportunities:

• Untapped rural market

• Rising income levels, i.e. increase in purchasing power of consumers

• Large domestic market- a population of over one billion.

• Export potential

• High consumer goods spending

Threats:

• Removal of import restrictions resulting in replacing of domestic brands

• Slowdown in rural demand

[12]

• Tax and regulatory structure

DEMOGRAPHIC PROFILE OF SRILANKA

Geography

Sri Lanka is an island in the Indian Ocean off the southeast tip of India. Most of the land is flat

and rolling; mountains in the south-central region rise to over 8,000 ft.

Government

Republic.

[13]

History

Indo-Aryan emigration from India in the 5th century B.C. came to form the largest ethnic group

on Sri Lanka today, the Sinhalese. Tamils, the second-largest ethnic group on the island, were

originally from Tamil region and emigrated between the 3rd century B.C. and A.D. 1200. Until

colonial powers controlled Ceylon, Sinhalese and Tamil rulers fought for dominance over the

island. The Tamils, mostly Hindus, claimed the northern section of the island and the Sinhalese,

who are predominantly Buddhist, controlled the south. In 1505 the Portuguese took possession of

Ceylon until the Dutch India Company took control (1658–1796). The British took over in 1796,

and Ceylon became an English colony in 1802. The British developed coffee, tea, and rubber

plantations. On Feb. 4, 1948, after pressure from Ceylonese nationalist leaders, Ceylon became a

self-governing dominion of the Commonwealth of Nations.

S.W.R.D. Bandaranaike became prime minister in 1956 and championed Sinhalese nationalism,

making Sinhala the country's only official language and including state support of Buddhism,

further marginalizing the Tamil minority. He was assassinated in 1959 by a Buddhist monk. His

widow, Sirimavo Bandaranaike, became the world's first female prime minister in 1960. The

name Ceylon was changed to Sri Lanka on May 22, 1972.

The Tamil minority's resentment toward the Sinhalese majority's monopoly on political and

economic power, made worse by cultural and religious differences, erupted in bloody violence in

1983. Tamil rebel groups, the strongest of which were the Liberation Tigers of Tamil Eelam,

began a civil war to fight for separate nation.

President Premadasa was assassinated at a May Day political rally in 1993, when a Tamil rebel

detonated explosives strapped to him. Tamil tigers have frequently resorted to terrorist attacks

against civilians. The next president, Chandrika Kumaratunga was herself wounded in a terrorist

attack in Dec 1999. By early 2000, 18 years of war had claimed the lives of more than 64,000,

mostly civilians.

[14]

After Dec. 2001 elections, Ranil Wickremesinghe, a longtime bitter rival of President

Kumaratunga, was sworn in as prime minister. Wickremesinghe's victory precipitated a formal

cease-fire with the Tamil rebels, signed in Feb. 2002. In September talks, the government lifted

its ban on the group, and the Tigers dropped their demand for an independent Tamil state.

Another significant breakthrough came in December when the Tigers and the government struck

a power-sharing deal that would give the rebels regional autonomy. But negotiations in 2003

achieved little.

Intense political rivalry threatened the peace process. In Nov. 2003, President Kumaratunga,

convinced that Prime Minister Wickremesinghe was too soft in his negotiations with the Tigers,

wrested away some of his powers. In Feb. 2004, the president dissolved parliament and called for

elections in the hope of further eroding the power of the prime minister. The gamble paid off for

Kumaratunga—her United People's Freedom Alliance won April's parliamentary elections, and

Wickremesinghe was replaced by a new prime minister, MahindaRajapaksa, a high-ranking

member of Kumaratunga's party.

On Dec. 26, 2004, a tremendously powerful tsunami ravaged 12 Asian countries. About 38,000

people were reported killed in Sri Lanka. President Kumaratunga and the Tamil Tigers reached a

deal in June 2005 to share about $4.5 billion in international aid to rebuild the country. But

intensifying violence in the eastern part of the country threatened the cease-fire and jeopardized

the aid package. In Aug. 2005, Foreign Minister Lakshman Kadirgamar was assassinated and the

government declared a state of emergency.

Prime Minister Mahinda Rajapaksa won November's presidential elections, taking 50% of the

vote to former prime ministerRanilWickremesinghe's 48%. Rajapaksa is expected to take a hard

line with the Tamil Tigers. Rajapaksa appointed RatnasiriWickremanayaka as prime minister.

In 2006, repeated violations of the 2002 cease-fire on both sides turned into outright war. Since

April 2006, about 1,000 soldiers and civilians have been killed, and 135,000, mostly Tamils,

[15]

have been displaced. Efforts by Norway, which brokered the 2002 cease-fire, to bring both sides

to the negotiating table were unsuccessful throughout the summer.

Fighting between the rebels and government troops continued into 2007. After a weeks of deadly

battles, the military took control of rebel-held regions of eastern Sri Lanka in March, leaving tens

of thousands more civilians displaced. In April, the Tamil Tigers launched their first air raid,

using small airplanes to bomb an air force base near Colombo. An attack by the Sri Lankan air

force in November killed the leader of the Tigers' political wing, S. P. Tamilselvan. Amid

continued fighting, the government abrogated the cease-fire in January 2008.

Sri Lanka was rocked by a series of suicide bombs on the eve of and during the country's

celebration of its 60th anniversary of independence in February. Nearly 40 people died in the

attacks. April was a particularly bloody month in Sri Lanka. Indeed, highways minister

JeyarajFernandopulle was killed in a bombing attributed to Tamil Tiger rebels. Later in the

month, more than 40 soldiers and 100 Tamil Tiger rebels died in a battle in the Jaffna peninsula.

TAMIL TIGERS DEFEATED BY GOVERNMENT TROOPS

The Sri Lankan government tasted success in the fall of 2008, when the military launched an

airstrike on Tamil headquarters in early October in Kilinochi. Plus, ground troops were closing in

on the rebels. In January 2009, the Sri Lankan government captured the northern town of

Kilinochchi, which for ten years had been the administrative headquarters of the Tamil Tigers.

Under the leadership of defense chief Gotabhaya Rajapaksa, the brother of the president, the

army continued to practise the Tigers relentlessly in early 2009. By April, the Tigers were

cornered on a small spread out of coastline in the north-east of the country. Civilian Tamils left

the area and moved into refugee camps that struggled to provide food and medical attention,

while the Tiger fighting force was reduced to 1,000 members.

In May 2009, a UN spokesperson called the situation a "bloodbath." International human rights

organizations claimed that the Sri Lankan army killed at least 500 Tamil civilians in the early

[16]

days of May 2009 alone. That brought the Tamil civilian death toll to at least 8,000 since the

beginning of the year, according to the UN. The Sri Lankan army lost at least 3,800 soldiers by

the period 18-months.

Conflict ended when Velupillai Prabhakaran, the leader of the Tamil Tigers, was killed in

fighting in which government troops took the last bit of reassurance territory. Early elections

were held in January 2010. President Rajapaksa won the election by a huge margin, defeating

former army Chief Gen. SarathFonseka. Fonseka presided over final battle that dense the Tamil

Tigers. He was arrested in March on charges of plotting to conquer the government. Rajapaksa

dissolved Parliament in March.

In April 2010's parliamentary elections, Rajapaksa coalition won another victory. In September,

Parliament endorsed a proposal to rewrite Sri Lanka's constitution to allow Rajapaksa to run for a

third term.

Nearly a year after his successful reelection bid in Jan. 2010, President Rajapaksa, was

inaugurated in a coronation-like ceremony. Slightly damaging his new administration was a UN-

sponsored report concerning the final days of Sri Lanka's civil war. A panel advising the UN

secretary-general found “credible evidence” those war crimes was committed by both sides in

2009, and that the Sri Lankan army killed tens of thousands of civilians.

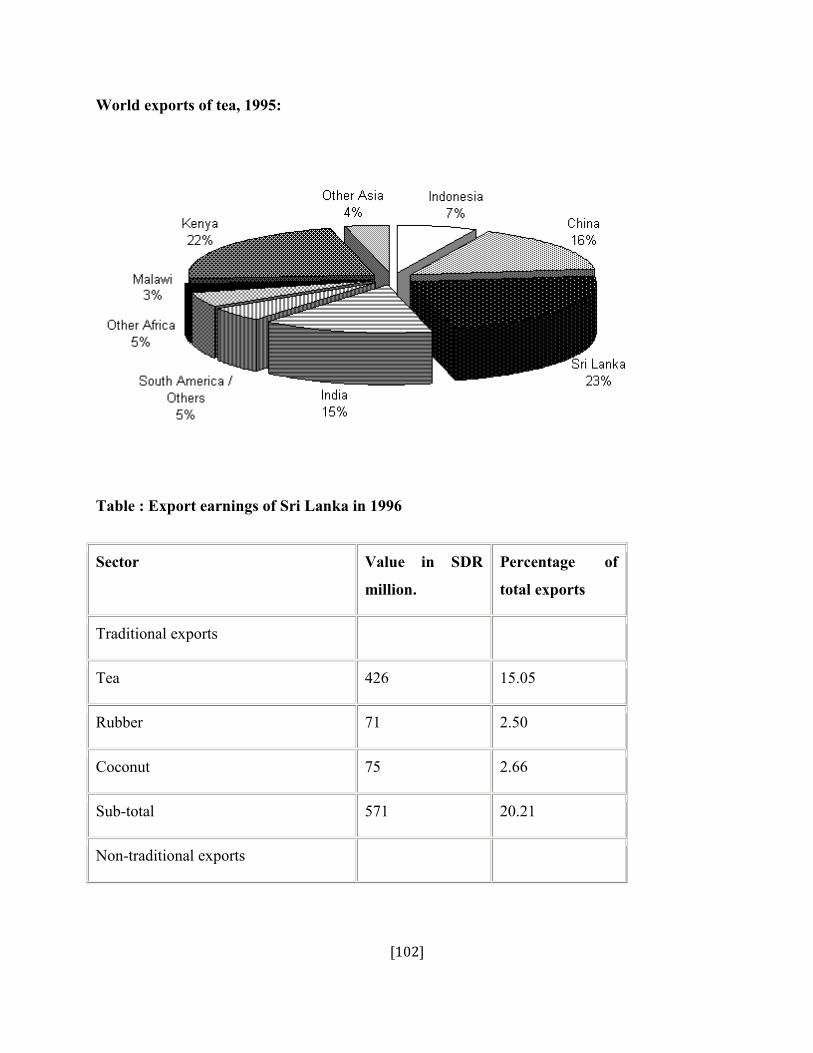

Tea production in Sri Lanka

Tea production in Sri Lanka is of high importance to the Sri Lankan economy and the world

market. Srilanka is the world's third largest producer of tea and the industry is one of the

country's main sources of foreign exchange and generating significant employment. Tea accounts

for 15% of the GDP, and it generates roughly $700 million annually. In 1995, Sri Lanka was the

world's leading exporter of tea, with 23% of the total world export. The tea sector employs,

directly or indirectly over 1 million people in Sri Lanka and in 1995 directly employed 215,338

on tea plantations and estates. The climate of the country favours the production of high quality

[17]

tea. The industry was introduced to the country in 1867 by James Taylor, the British planter who

arrived in 1852.

Foundation of tea plantations

James Taylor in Kandy, Sri Lanka in 1860s.

In 1824 a tea plant was brought to the land by the British from China and was planted in the

Royal Botanical Gardens in Peradeniya for non-commercial purposes. Further experimental tea

plants were brought from Assam and Calcutta in India to Peradeniya in 1839 through the East

India Company and over the years that followed. In 1839 the Ceylon Chamber of Commerce was

also established followed by the Planters' Association of Ceylon in 1854. In 1867, James Taylor

marked the birth of the tea industry in Ceylon by starting a tea plantation in Loolecondera estate

in Kandy in 1867. He began the tea plantation on an estate of just 19 acres. In 1872 he started a

fully equipped tea factory in the same Loolecondera estate and that year the first sale of

Loolecondra tea was made in Kandy. In 1873, the first shipment of Ceylon tea, a consignment of

some 10 kg, arrived in London.

Soon enough plantations surrounding Loolecondera such as Hope, Rookwood and Mooloya

located to the east and Le Vallon and Stellenberg to the south began changing into tea plantations

and were amongst the first tea estates to be established on the island.

[18]

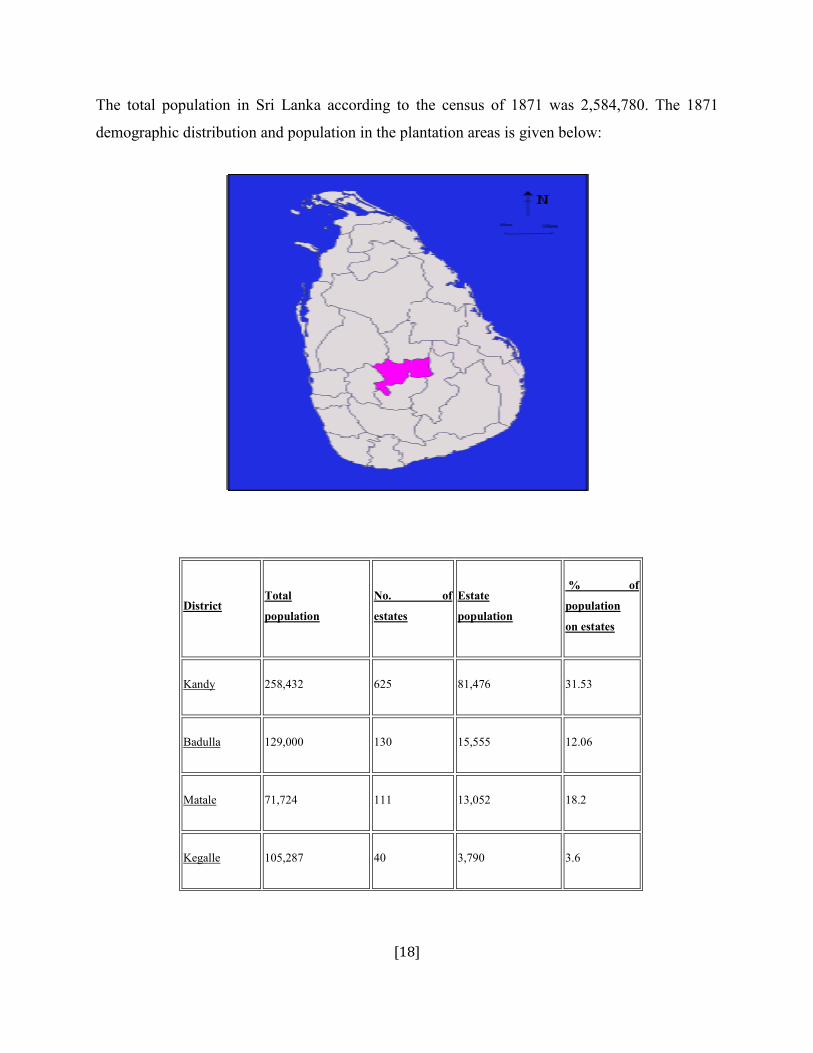

The total population in Sri Lanka according to the census of 1871 was 2,584,780. The 1871

demographic distribution and population in the plantation areas is given below:

District Total

population

No. of

estates

Estate

population

% of

population

on estates

Kandy 258,432 625 81,476 31.53

Badulla 129,000 130 15,555 12.06

Matale 71,724 111 13,052 18.2

Kegalle 105,287 40 3,790 3.6

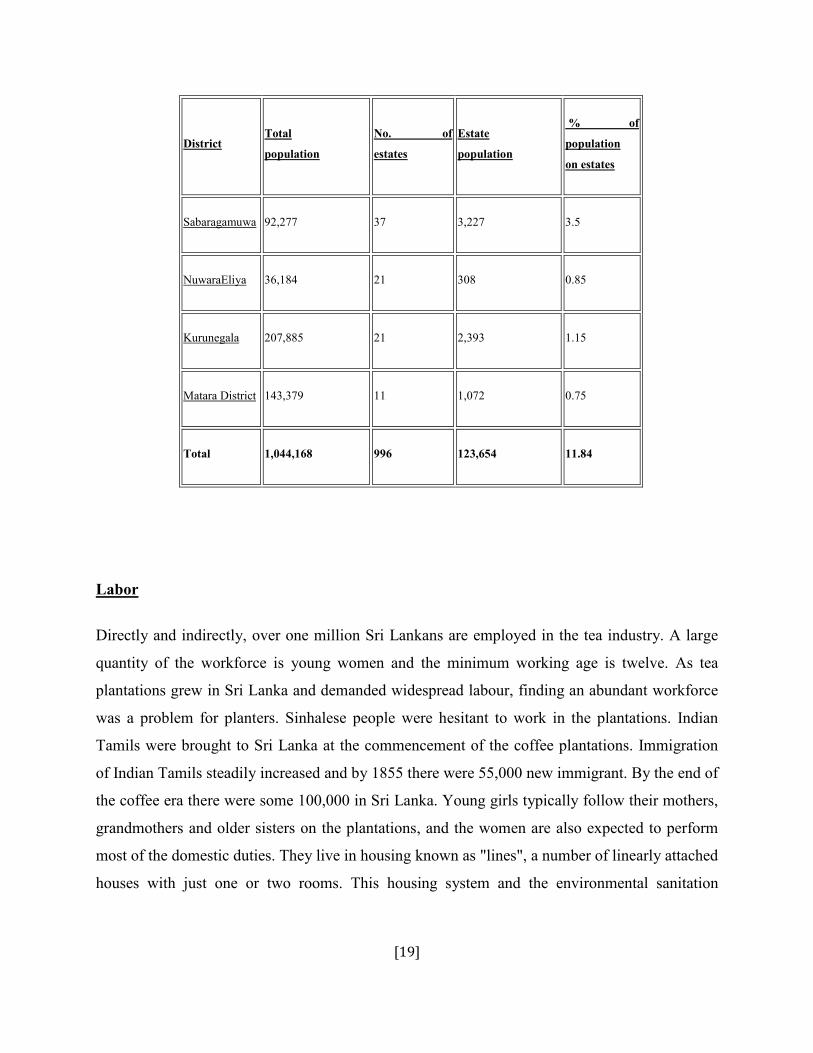

[19]

District Total

population

No. of

estates

Estate

population

% of

population

on estates

Sabaragamuwa 92,277 37 3,227 3.5

NuwaraEliya 36,184 21 308 0.85

Kurunegala 207,885 21 2,393 1.15

Matara District 143,379 11 1,072 0.75

Total 1,044,168 996 123,654 11.84

Labor

Directly and indirectly, over one million Sri Lankans are employed in the tea industry. A large

quantity of the workforce is young women and the minimum working age is twelve. As tea

plantations grew in Sri Lanka and demanded widespread labour, finding an abundant workforce

was a problem for planters. Sinhalese people were hesitant to work in the plantations. Indian

Tamils were brought to Sri Lanka at the commencement of the coffee plantations. Immigration

of Indian Tamils steadily increased and by 1855 there were 55,000 new immigrant. By the end of

the coffee era there were some 100,000 in Sri Lanka. Young girls typically follow their mothers,

grandmothers and older sisters on the plantations, and the women are also expected to perform

most of the domestic duties. They live in housing known as "lines", a number of linearly attached

houses with just one or two rooms. This housing system and the environmental sanitation

[20]

conditions are generally poor for laborers in the plantation sector. There are typically 6 to 12 or

24 line rooms in one line barrack. Often rooms for laborers are without windows and there is

little or no ventilation and as many as 6 to 11 members may often live in one room together. In

the housing system for plantation workers in Sri Lanka, women and girls have no privacy from

the male workers, which places them at a higher risk for sexual harassment. In June 2007, a

study conducted in the NuwaraEliya tea growing area revealed that the serious lack of privacy

has led several women to commit suicide, especially newly wedded women. According to

studies by Christian Aid, the female Indian Tamil plantation workers are particularly at risk from

discrimination and victimization. Some concern towards women's rights have been made in

regards to the female plantation workers in Sri Lanka, resulting in some 85 neighborhood

women's groups being formed across the country, educating them in gender, leadership and

preventing violence against women.

The tea plantation is prearranged in a social chain of command and the women,they consist of

75%-85% of the work force in the tea industry, are at the lowest social strata and are powerless.

This is not unusual as the sub regulation of women under men is present domestically and in the

social community in many parts of Sri Lanka. Wages are typically chiefly low. In NuwaraEliya,

women were once paid as little as 7 rupees per kilogram, the equivalent of 4 pence, or 7 cents,

and many must complete 16 kilograms a day. Given the social stratification in Sri Lanka's past,

the pay had to be collected by a husband or father. The men who work on the tea plantations

typically cut down trees or operate machinery and are better paid at 155 rupees (82p) a day and

finish the day hours earlier. Due to the severely low wages, industrial action took place in 2006.

Wages in the tea sector were enlarged with the average daily wage earned in the sector now

significantly higher at 378 rupees for men and 261 for women in some places.Studies show that

poverty is still a major problem and despite the tea industry employing a large number of poor

people, employment has failed to improve poverty since workers are often highly uneducated

and unskilled. Poverty levels on plantations have consistently been higher than the national

average and although overall poverty in Sri Lanka has declined in the last thirty years, it is now

significantly concentrated in rural areas. Poverty in the estate sector has been reported to be

increasing with roughly one in three suffering from poverty, rising from 30 percent in 2002 to 32

[21]

percent in 2006/07. NuwaraEliya showed a significant increase in poverty among workers from

2002 to 2007 from 22.6 percent in 2002 to 33.8 percent in 2006/07. But by no means is

employment secure in the tea sector in Sri Lanka. Like other industries, job security in the tea

industry has been threatened by the current financial crisis. Sri Lanka over 50,000 private sector

employees are expected to lose their jobs in 2009 due to the current slump.

BRIEF INTRODUCTION ABOUT SRI LANKA

Population growth rate

0.934% (2011 est.)

Birth rate

17.42 births/1,000 population (2011 est.)

Death rate

5.92 deaths/1,000 population (July 2011 est.)

Net migration rate

-2.16 migrant(s)/1,000 population (2011 est.)

Urbanization

Ø Urban population: 14% of total population (2010)

Ø Rate of urbanization: 1.1% annual rate of change (2010-15 est.)

Sex ratio

Ø At birth: 1.04 male(s)/female

Ø Under 15 years: 1.04 male(s)/female

Ø 15-64 years: 0.96 male(s)/female

[22]

Ø 65 years and over: 0.86 male(s)/female

Ø Total population: 0.97 male(s)/female (2011 est.)

Infant mortality rate

Ø Total: 9.7 deaths/1,000 live births

Ø Male: 10.68 deaths/1,000 live births

Ø Female: 8.68 deaths/1,000 live births (2011 est.)

Life expectancy at birth

Ø Total population: 75.73 years

Ø Male: 72.21 years

Ø Female: 79.38 years (2011 est.)

Total fertility rate

2.2 children born/woman (2011 est.)

Major infectious diseases

Ø Degree of risk: high

Ø food or waterborne diseases: Bacterial diarrhea and hepatitis A

Ø vector borne disease: Dengue fever and Chikungunya

Ø water contact disease: Leptospirosis

Ø animal contact disease: rabies (2009)

Nationality

Noun: Sri Lankan(s)

Adjective: Sri Lankan

Ethnic groups

[23]

Sinhalese 73.8%, Sri Lankan Moors 7.2%, Indian Tamil 4.6%, Sri Lankan Tamil 3.9%, other

0.5%, unspecified 10%.

Religions

Buddhist 69.1%, Muslim 7.6%, Hindu 7.1%, Christian 6.2%, unspecified 10%.

Languages

Sinhala 74%, Tamil 18%, other 8%

Note: English is commonly used in government and is spoken fluently by about 10% of the

population

Literacy

Total population: 90.7%

Male: 92.3%

Female: 89.1% (2001 census)

School life expectancy (primary to tertiary education)

Total: 13 years

Male: 12 years

Female: 13 years (2004)

Maternal mortality rate

39 deaths/100,000 live births (2008)

Children under the age of 5 years underweight

21.1% (2007)

Health expenditures

[24]

4% of GDP (2009)

Physicians’ density

0.492 physicians/1,000 population (2006)

Hospital bed density

3.1 beds/1,000 population (2004)

OVERVIEW OF THE SECTOR

•••• Tea is the agricultural product of the leaves, leaf buds, and internodes of the Camellia saneness plant , prepared and cured by various methods.

•••• "Tea" also refers to the aromatic beverage prepared from the cured leaves

by combination with hot or boiling water, and is the common name for the

Camellia saneness plant itself

•••• After water, tea is the most widely-consumed beverage in the world. It has

a cooling, sl ightly bitter, astringent flavor which many enjoy

•••• Tea is the most popular drink in the world in terms of consumption. Its

consumption equals all other manufactured drinks in the world

•••• Including coffee, chocolate, soft drinks, and alcohol put together. Most

tea consumed outside East Asia is produced on large plantations in India

or Sri Lanka, and is destined to be sold to large businesses.

[25]

•••• Opposite this large-scale industrial production there are many small

"gardens", sometimes minuscule plantations that produce highly sought-

after teas prized by gourmets

•••• The last two decades have witnessed a virtual explosion in the number of

free trade agreements , some of them involving several countries

•••• Many of them bilateral. The proliferation of free trade agreements has led

to fierce debate about the merits of these agreements.

Per Capital Income

CURRENT STATUS AND FUTURE RESEARCH FOCUS OF TEA IN SRI

LANKA

Sri Lankan tea ranks the best among world teas and over the 138 year of tea

industry in Sri Lanka, it faced many challenges and the Tea Research Insti tute

(TRI) played pivotal role in developing new technologies to stand against the

competing forces

Both within and outside the country. This paper makes an attempt to assemble

the available information on the current situation of the industry and the

research trends and developments in the resent time and its focus for the

futur

[26]

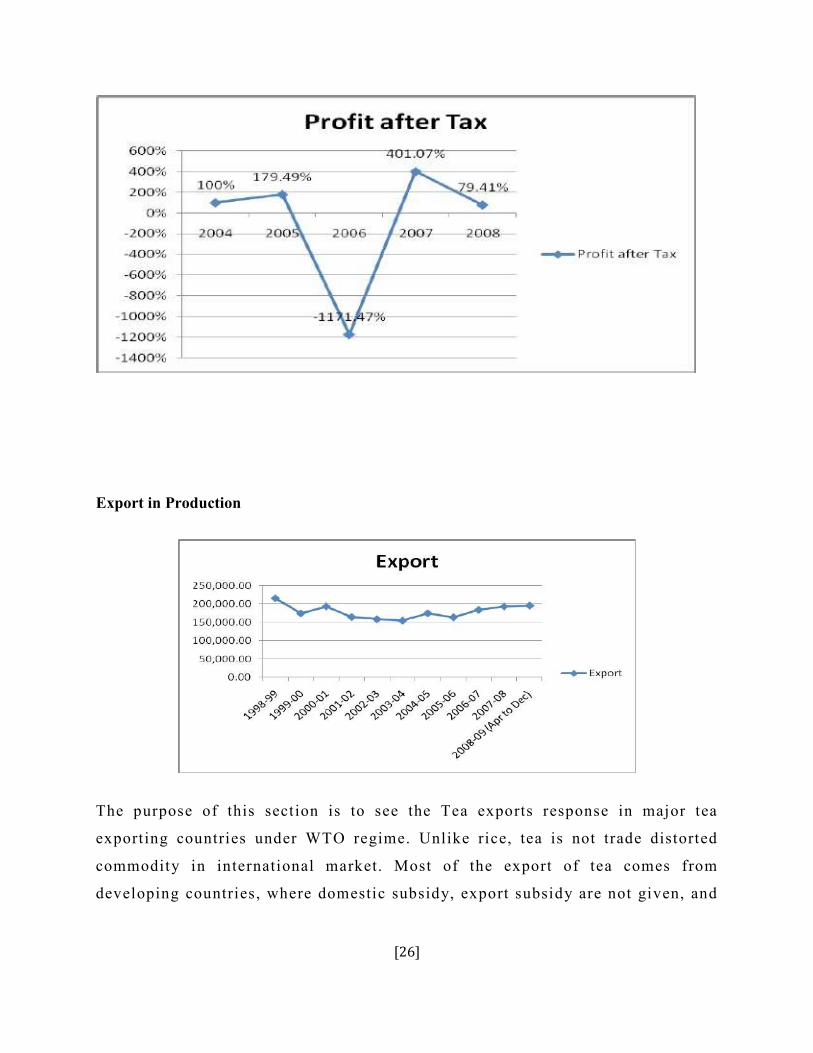

Export in Production

The purpose of this section is to see the Tea exports response in major tea

exporting countries under WTO regime. Unlike rice, tea is not trade distorted

commodity in international market. Most of the export of tea comes from

developing countries, where domestic subsidy, export subsidy are not given, and

[27]

it is believed that in these countries tea export is taxed for the purpose of

revenue tote government

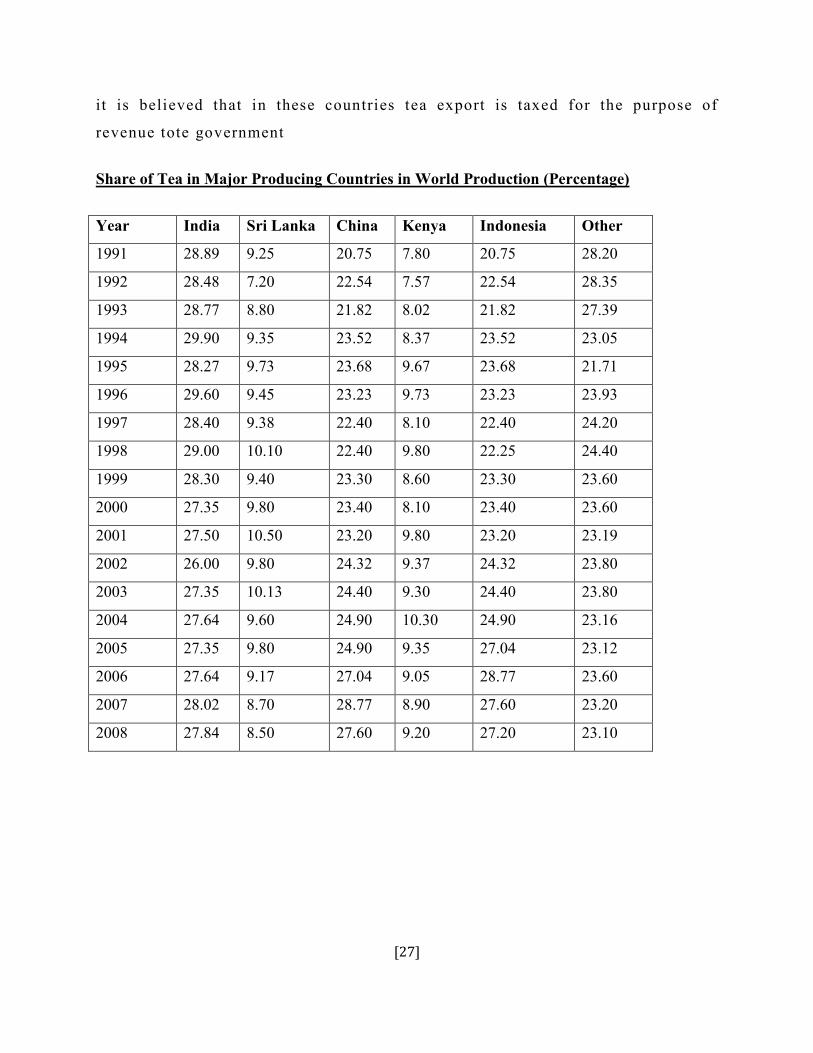

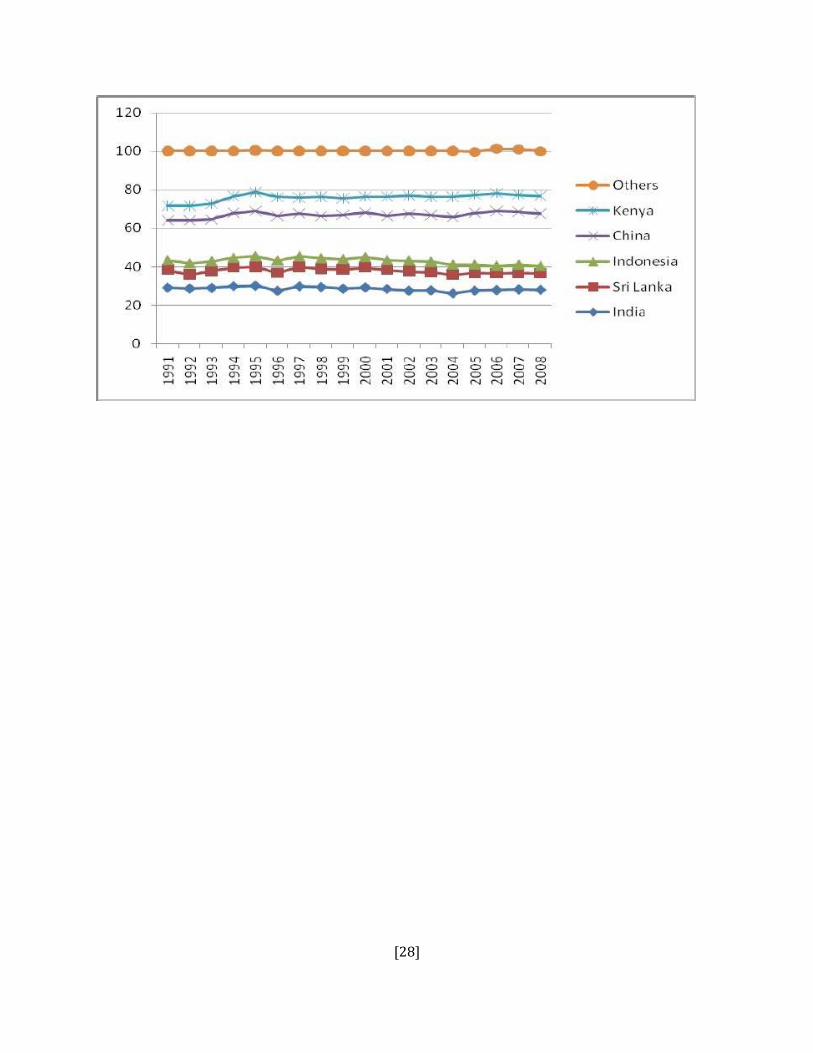

Share of Tea in Major Producing Countries in World Production (Percentage)

Year India Sri Lanka China Kenya Indonesia Other

1991 28.89 9.25 20.75 7.80 20.75 28.20

1992 28.48 7.20 22.54 7.57 22.54 28.35

1993 28.77 8.80 21.82 8.02 21.82 27.39

1994 29.90 9.35 23.52 8.37 23.52 23.05

1995 28.27 9.73 23.68 9.67 23.68 21.71

1996 29.60 9.45 23.23 9.73 23.23 23.93

1997 28.40 9.38 22.40 8.10 22.40 24.20

1998 29.00 10.10 22.40 9.80 22.25 24.40

1999 28.30 9.40 23.30 8.60 23.30 23.60

2000 27.35 9.80 23.40 8.10 23.40 23.60

2001 27.50 10.50 23.20 9.80 23.20 23.19

2002 26.00 9.80 24.32 9.37 24.32 23.80

2003 27.35 10.13 24.40 9.30 24.40 23.80

2004 27.64 9.60 24.90 10.30 24.90 23.16

2005 27.35 9.80 24.90 9.35 27.04 23.12

2006 27.64 9.17 27.04 9.05 28.77 23.60

2007 28.02 8.70 28.77 8.90 27.60 23.20

2008 27.84 8.50 27.60 9.20 27.20 23.10

[28]

[29]

Chapter-III

Operations Management of

Tea Sector

[30]

Market Basics

The Economics of Tea

The price of tea has been in long-term turn down while production costs have risen, putting

downward pressure on farmers’ incomes and laborers’ working conditions.

Since 1980, the real price of tea has fallen by 1 5%. As the chart below shows, another problem

has been price instability. In the last two decades, the annual average price has fluctuated

between a high of 333 kgs to a low of 142 kgs in 1980 terms, and the instability index has

averaged 13, which means that the price deviated from the exponential trend by 13% in any

given year.

Price decline:

The decline in prices has been primarily due to the strong growth in supply in the face of

sluggish demand. Unlike with cocoa and coffee, the ratio of stocks to demand play only a minor

role in determining the price level because the quantity of tea stocks held is relatively low.

Instead stocks function more as a transitory ‘pipeline’ stage in the supply chain.Competition

between producer countries for a share of the world market is concentrated for a number of

reasons, all of which contribute to low prices:

• A large number of countries produce tea and many of them are big enough to prevent the

Establishment of a clear monopolistic leader, which allows for fierce competition.

• Demand is rising slowly and so the only way to increase significantly the amount of tea

exported is at the expense of competitors.

• As tea deteriorate fairly quickly it is frequently necessary to cut prices in order to clear

stocks.

• Tea supply is greater than demand from manufacturers.

[31]

• Producing countries stay in the market despite its scant rewards because they have

invested a great deal in tea production and lack alternatives.

Low prices for tea are passed on to the poorest segments of a country in the form of low wages

on plantations. Given that it is easier to cut costs than raise prices , producing countries have to

remain competitive by lowering wages – which partially accounts for the rut in which plantation

wages are caught.

e prices in the long term. The present decline in prices was on the back of a 0.6% annual increase

in production between 1984 and 1994 – annual increase between 1994 and 2005 is estimated at

2.8%. For 2005, the projected surplus of export availabilities over import requirements stands at

about 24 000 tones, a surplus of 2%.

Price stability:

One area in which tea differs from coffee and cocoa is that the world tea market used not to be

particularly prone to price volatility. In fact until the 1980s world tea prices seemed relatively

stable when compared to other commodities. This can be accounted for in several ways:

• Tea production is less prone than coffee and cocoa to peaks and troughs due to weather

and disease. Also world production is fairly diversified and not concentrated in particular

areas as is the case with coffee (Brazil) and cocoa (West Africa).

• The tea market is not undermined by the destabilizing effects of speculation.

• Vertical integration and companies in monopolistic competition in consumer countries

also stabilize prices (if at low levels).

Price volatility is a necessary precondition for viable futures markets as it is only when price

fluctuates that producers, traders and processors find that they need to hedge against price

fluctuations. One analyst takes a rather interesting view on this, arguing that in the coffee and

cocoa markets the existence of futures trading makes price determination very organized,

[32]

centralized and transparent. By contrast the tea markets are not held around one international

price but according to different auction prices in producing countries. The entire market is th

The relative stability of the tea market was true until fairly recently – there was a noticeable

increase in the volatility of the markets in the 1990s. This volatility first began in the mid-1970s

when prices became twice as unstable as they had been the decade before. There began to be a.

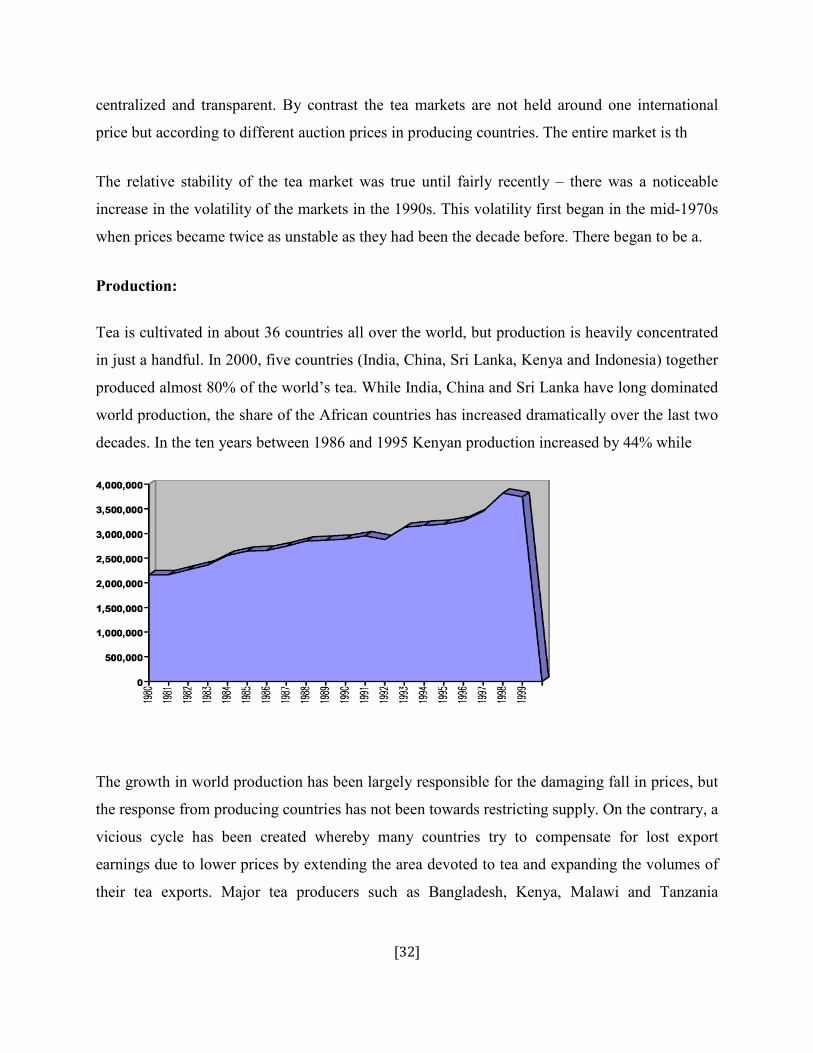

Production:

Tea is cultivated in about 36 countries all over the world, but production is heavily concentrated

in just a handful. In 2000, five countries (India, China, Sri Lanka, Kenya and Indonesia) together

produced almost 80% of the world’s tea. While India, China and Sri Lanka have long dominated

world production, the share of the African countries has increased dramatically over the last two

decades. In the ten years between 1986 and 1995 Kenyan production increased by 44% while

The growth in world production has been largely responsible for the damaging fall in prices, but

the response from producing countries has not been towards restricting supply. On the contrary, a

vicious cycle has been created whereby many countries try to compensate for lost export

earnings due to lower prices by extending the area devoted to tea and expanding the volumes of

their tea exports. Major tea producers such as Bangladesh, Kenya, Malawi and Tanzania

[33]

expanded their tea production area by more than 130,000 hectares in the first half of the 1990s.

Prices have been forced down further by strong competition from the ‘new’ African producers

who emerged onto the tea market relatively late.

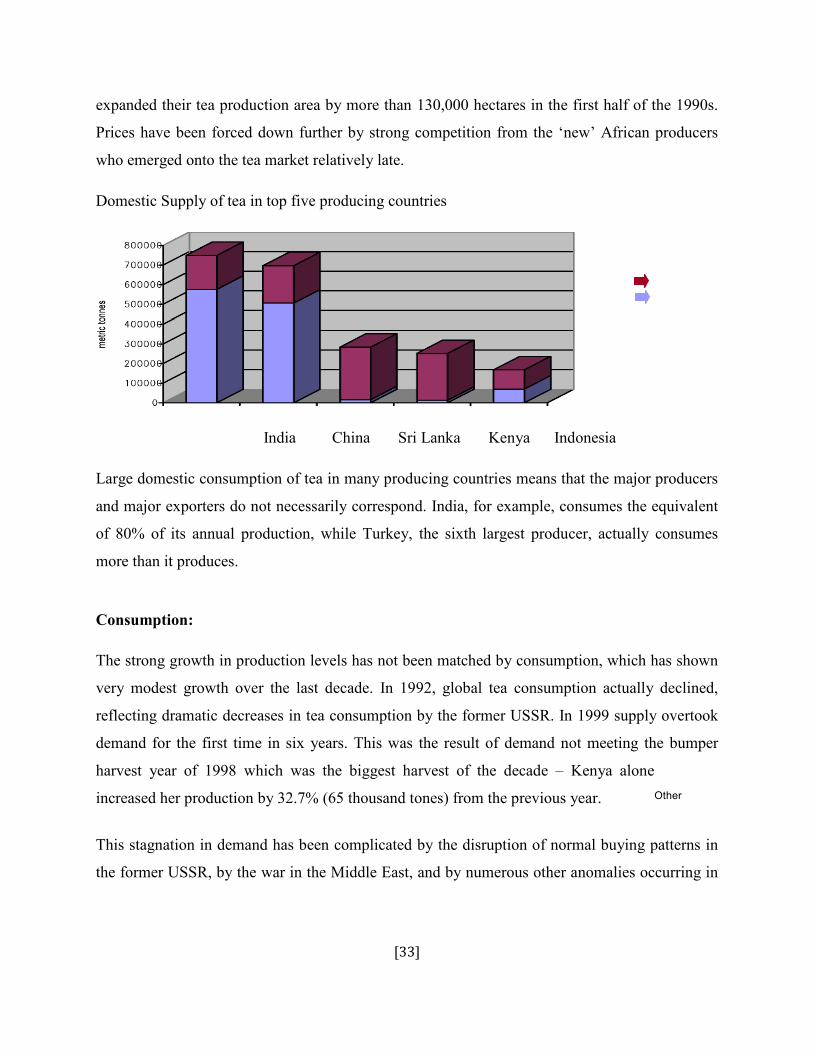

Domestic Supply of tea in top five producing countries

India China Sri Lanka Kenya Indonesia

Large domestic consumption of tea in many producing countries means that the major producers

and major exporters do not necessarily correspond. India, for example, consumes the equivalent

of 80% of its annual production, while Turkey, the sixth largest producer, actually co sumes

more than it produces.

Consumption:

The strong growth in production levels has not been matched by consumption, which has shown

very modest growth over the last decade. In 1992, global tea consumption actually declined,

reflecting dramatic decreases in tea consumption by the former USSR. In 1999 supply overtook

demand for the first time in six years. This was the result of demand not meeting the bumper

harvest year of 1998 which was the biggest harvest of the decade – Kenya alone

increased her production by 32.7% (65 thousand tones) from the previous year.

This stagnation in demand has been complicated by the disruption of normal buying patterns in

the former USSR, by the war in the Middle East, and by numerous other anomalies occurring in

Other

n

[34]

tea, has been flat. In an effort to make tea more convenient to prepare, the tea industry has gone

as far as to introduce a ‘tea tablet’, which was recently invented in Japan.

The paradox of the growth in tea in more convenient forms is that, while demand for tea products

may increase, less tea leaf is required to satisfy that demand. For example, CTC tea, which is

used in tea bags, yields twice the cup page per given weight of tea. A shift in tea-drinking

behavior towards the increasing use of tea bags and soluble instant tea effectively reduces the

quantity of tea needed per cup and also raises the demand for plain cheaper tea at the expense of

those of high quality.

A large proportion of the world’s tea (more than half) is consumed in producing countries

(unlike coffee and cocoa). India is both the world’s largest producer of tea and the world’s

thirstiest consumer. Although India produces almost 30% of the world’s tea it exports less than

20% of the world’s supply. Given that tea is the national drink for two thirds of the world’s

population and that much of the consumption is in the South where population is growing, there .

The promotion of ready-to-drink tea is also being explored as it can better compete with soft

drinks.

As the graph below on major importers of tea shows, the export trade must cater to very different

markets. Major buyers of tea in the Middle East want a very different product from what is in

demand in Europe. The United Arab Emirates buys low grows Sri Lankan tea which is not at all

in demand in the UK.

Germany and Japan buy First Flush Darjeeling at more than $30 per kg, while the UK would

only reluctantly pay $2.50 for a top quality Kenyan. Consumer tastes differ not only with regard

to quality and origin: continental Europe buys leafy orthodox teas, while the UK prefers CTC’s

(tea further processed by Crush, Tear and Curl) more suitable for tea bags. A tea producer,

therefore, will typically produce 5 main grades and 2 or 3 secondary grades, and must find a

market for each.

Profitability: Rising cost vs. rising productivity:

[35]

While market prices for tea have been falling, the costs of production have been on the rise,

putting downward pressure on profitability. The rise in costs has been partially outweighed by

increases in yields and productivity, but the extent of this varies across regions and according to

whether it is a smallholding or a plantation.

Governments frequently worsen the problem of high production costs in tea manufacture by

levying excise tax, which is disconnected to the sale price and thus punishes factories for the

production process itself13. Moreover, the final manufactured product is routinely under-utilized

because whatever is left at the final point in the manufacturing cycle gets dubbed ‘tea residue’,

which cannot legally be sold, impeding further use of the leaf by-product.

The world averages for tea yields in 1999 were 1077.1 kg/hectare, but average yields vary

enormously from country to country. At the top end, Kenya produced 2123.4 kg of tea per

hectare in 1999, while Nepal has one of the lowest productivities in the world at 200 kg per

hectare.

A major determinant of yield and cost of production in each country is lab our productivity.

Labor costs account for around half of the unit cost of production and approximately 75% of that

labor cost is on plucking. This explains the high cost of production in Sri Lanka, where even

high-yielding plantations have excess labor, except during heavy cropping months when they are

faced instead with a worker shortage. Another factor influencing yield is the quality of seedlings

and the land. Again, Sri Lanka tends to retain old low-yielding seedling tea and the land is

degraded. Availability of chemical inputs can also be a factor.

Kenyan smallholders have access to fertilizers on credit from the Kenya Tea Development

Agency, which may explain their relatively high yields.

Differences in yields, cost of production and prices have made the profitability of tea vary widely

across different countries. Among the various countries the highest profitability has been

obtained by Kenya , followed by India with the lowest being Sri Lanka.

[36]

With rising input costs and falling prices, there is pressure to limit labor costs, which constitute

around 55-60% of the total cost of production for tea. This has damaging implications for

workers on tea estates, who figure as a cost to be minimized by plantation companies despite the

desperate need for an improvement in their working and living conditions.

Forecast:

There is a danger that prices will drop yet further due to ambitious plans for increased tea

production in several countries, against a backdrop of sluggish demand.

The Vietnam Tea Association in 2000 agreed on concrete measures to increase production from

around 60,000 tons to 214,000 tons by 2010, with exports rising almost threefold. Similarly,

Nepal’s policy is to boost production to more than 46,000 tones by quality end of the market in

Russia, the Middle East and other developing countries. These are also the countries where

consumption is projected to grow at the fastest rate over the next five years. Oversupply in any

part of the market, however, is undesirable and potentially harmful for the whole market as lower

prices in the low-quality sector may drag down prices in other sectors.

To avoid further decline in prices, there must be an adequate amount of growth in consumption.

The FAO predicts, however, that the annual growth rate for both production and consumption

will be 2.8% until 2005.given the starting point of production being greater than consumption;

this will effectively mean a widening gap between supply and demand and therefore lower

prices.

The prospect is brighter for green tea, which is enjoying growing popularity in the west.

The Politics of Tea:

Developing countries’ dependence on tea:

Several countries are heavily dependent on tea for their export earnings, and have suffered

acutely due to low and volatile prices. In 1994 Rwanda was exceptionally dependent on tea and

coffee – earning more than 90% of its foreign exchange through the sale of those two

[37]

commodities. Kenya in 1998 earned almost 30% of its total exports value from the sale of tea.

Tea accounts for more than 20% of the value of exports from Sri Lanka.

This reliance on tea means that these countries are particularly badly hit by unfavorable price

trends in the tea market. When the price for tea declines, their terms of trade suffer as they have

less foreign currency to buy imports, which are generally increasing in price. The decline of tea

prices between 1980 and 1993 resulted in a loss of $580m in the terms of trade of developing

countries.

The intervention of politics in the tea trade:

As was shown by the Boston Tea Party, tea makes a good pawn in international affairs and the

politicization of tea is further compounded by the prevalence of consumption by the South,

unlike with coffee or cocoa.

omestic politics also plays an important part in tea production. The activities of the Tamil Tigers

in the tea-growing regions of Sri Lanka have been described as the greatest cost to the Sri

Lankan tea industry; while in India over 450 armed separatist extremist organizations disrupt the

operating environment.

The organization with jurisdiction over tea as an export commodity is the World Trade

Organization, which would ultimately have authority in mediating any dispute. For example, the

WTO has been pressuring the EU to abolish tea tariff ‘preference’ to Kenya, which bestows a

major price advantage to that nation. The WTO, however, has traditionally kept out of regulating

commodities markets, including tea, except in tariff issues. The Tea Working Group of the Food

and Agriculture Organization (FAO) of the UN, therefore, are more relevant as the international

body for the tea industry. On a regional level, organizations gaining in prestige and legal clout

include SAARC in South Asia and the Common Market for East and South Africa (COMESA)

in Africa.

A difficult issue that needs to be addressed in the international tea trade is re-exports, and this is

further discussed in the box below.

[38]

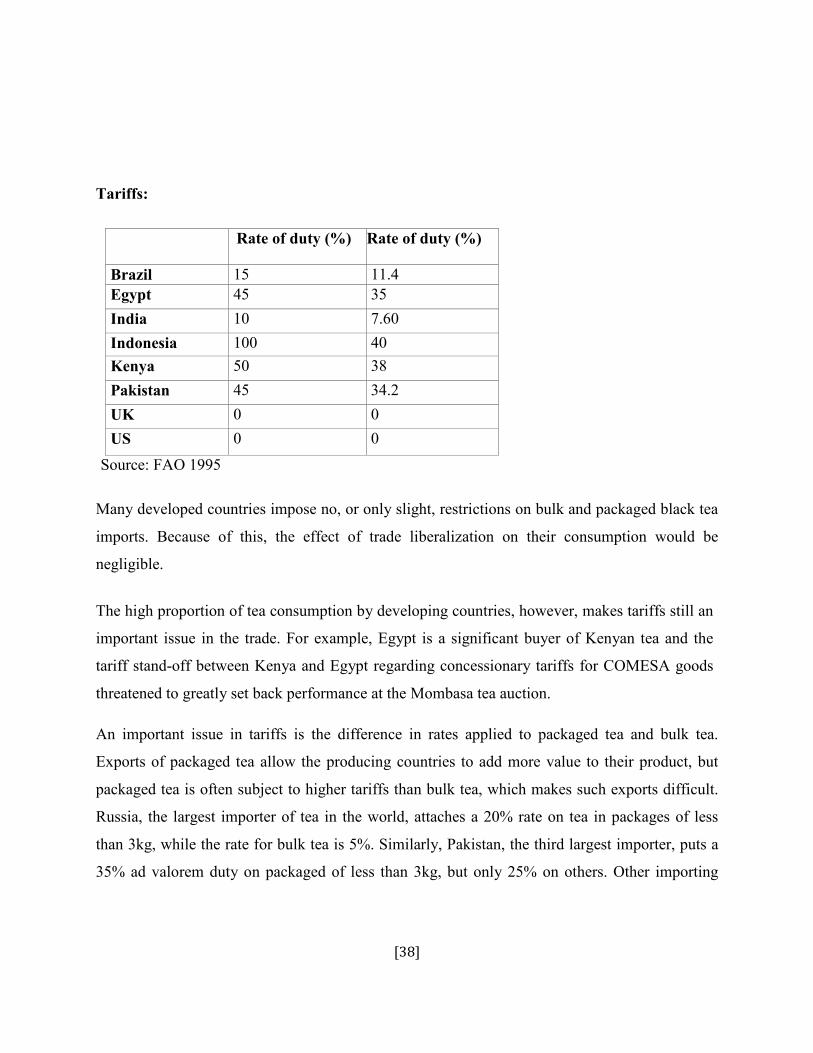

Tariffs:

Rate of duty (%) Rate of duty (%)

Brazil 15 11.4 Egypt 45 35

India 10 7.60

Indonesia 100 40 Kenya 50 38

Pakistan 45 34.2

UK 0 0

US 0 0

Source: FAO 1995

Many developed countries impose no, or only slight, restrictions on bulk and packaged black tea

imports. Because of this, the effect of trade liberalization on their consumption would be

negligible.

The high proportion of tea consumption by developing countries, however, makes tariffs still an

important issue in the trade. For example, Egypt is a significant buyer of Kenyan tea and the

tariff stand-off between Kenya and Egypt regarding concessionary tariffs for COMESA goods

threatened to greatly set back performance at the Mombasa tea auction.

An important issue in tariffs is the difference in rates applied to packaged tea and bulk tea.

Exports of packaged tea allow the producing countries to add more value to their product, but

packaged tea is often subject to higher tariffs than bulk tea, which makes such exports difficult.

Russia, the largest importer of tea in the world, attaches a 20% rate on tea in packages of less

than 3kg, while the rate for bulk tea is 5%. Similarly, Pakistan, the third largest importer, puts a

35% ad valorem duty on packaged of less than 3kg, but only 25% on others. Other importing

[39]

countries charging differentiated rates include Belarus, Kazakhstan, Ukraine, Saudi Arabia,

Jordan, Ethiopia and Morocco.

North America and the EU do not charge tariffs on either bulk or packaged black tea, but most

EU countries do charge 3.1% on green on packaged green tea, which discourages green tea

producers from adding more value to their tea. Spain and Portugal also charge around 12% on

soluble tea from outside the EC , against discouraging imports of value-added tea from

developing nations.

CAPTURING VALUE ALONG THE SUPPLY CHAIN

Further up the supply chain:

The role of the auction houses:

Unlike for coffee and cocoa there is no single indicator price for tea. Rather pricing is dominated

by the auction system, whereby the price of tea from each estate is determined on a day-to-day

basis, according to the quality and supply and demand on the day. This is because tea quality will

India, and one each in Sri Lanka (Colombo), Indonesia (Jakarta), Malawi (Limbe), eastern Africa

(Mombasa) and Bangladesh (Chittagong). Chinese tea is sold at commodity fairs in Guangzhou.

At auction, buyers bid for one particular grade from a particular tea garden at a time, after tasting

the tea and judging its value. The auctioneer plays an important role in the tea market. Apart

from personally tasting and evaluating each and every invoice, he has to use his knowledge of

the world demand and marketing skill in judging the marketability of the tea. He has final

jurisdiction and his judgment determines the selling price of the tea, to a certain extent.

Pros and Cons:

[40]

More than 70% of Kenya’s total tea sales are through auctions, while the figure for Sri Lanka is

almost 90%. There are several advantages of the dominance of the auction system for the tea

industry:

• The auction system is praised for allowing the highest price possible to be paid for the tea

in a way that equilibrates market demand and supply.

• The cost of going through the system is also fairly low. In India, auctioning costs less

than 2% of the merchandise including free sampling to prospective buyers, while in

Kenya the commission to the broker is 1% from the producer and 0.5% from the buyer.

• It is a transparent trading forum.

• Because buyers must buy the tea in its physical form rather than just on paper, it is

protected from destabilizing speculators.

Although the auction system would on the surface seem to approximate a perfectly fair market

where prices are determined solely by the interplay of supply and demand, a more detailed

picture is less attractive:

• In the 1970s, a Commission of Enquiry into the tea auction system set up by the Sri

Lanka government concluded that it appears that there is ‘a high degree of collusion that

prevails in buy and wide scope for collusion between brokers and buyers’. Such

collusion, if it occurred, would tend to reduce the price at which producers could sell tea

at the auctions, and would also affect prices of direct sales.

• Auction houses are usually seen as ‘middlemen’ that soak up cost.

• It is alleged that, when the situation is to their advantage, they increase price uncertainty,

delay and speculation.

There is some possibility that auction houses will become redundant with technological

advances. At the moment, almost all tea fields are located in regions where land phone lines

[41]

intermittently fail or simply do not exist. With the development of the internet through mobile

phones, however, and given that many plantations are financed by large companies, it is not

inconceivable that tea estates in the future will be able to post real-time data daily on the internet,

enabling a viable futures market. The global process for bringing buyers and sellers more

directly together, termed ‘disintermediation’, is already taking place with catalogue sales of

premium tea. This trend, combined with advanced internet systems, could potentially support a

price-stabilizing tea futures market, assuming that the market is financially transparent, reliably

instituted and justly enforced.

Recently more and more tea has been sold through forward contracts and private sales. The

benefit of this to producers is often considerable; they get payment faster, have less uncertainty

about sales and price, and can avoid the charges associated with auctioning tea (brokers fees,

warehousing).

The global tea brokers:

A few firms dominate the sales in each auction centre. J. Thomas & Co. Pvt. Ltd., the largest tea

broker in the world, handles over 155 million kg of tea a year, i.e. one-third of all tea auctioned

in India. Carritt Moran and Co. Ltd., the world’s second largest tea broker, handles 24% of

auctioned teas in India.

Brokers must be registered with the appropriate tea board in order to operate, which limits the

number of auction houses where tea can be sold. 11 brokers are registered with the Tea Board of

Kenya, while there are 4 registered brokers at Calcutta (J. Thomas & Co., Carritt Moran & Co.,

Contemporary Target and Paramount Tea Marketing) who together sell the majority of

Darjeeling tea.

The concentration of buyers at auction:

[42]

The concentration of buyers in most auction centers has traditionally been very high. New buyers

are inherently discriminated against for a number of reasons. Firstly, brokers generally do not

most of which are owned by the other companies competing with them in the same auction.

Blending:

Tea is generally exported with minimal processing to consumer countries, where it is blended

and packaged by the tea companies. Whilst many producers try to export pre-processed tea the

export of ‘ready-for-use’ tea is often hindered by the absence of money for expensive, glitzy

marketing strategies.

The consumer markets are dominated by the popular blended brands (over 70% of the UK

market). These are blends than can contain up to 35 different types of tea, necessitating blending

in the consuming country. They are designed to keep their taste constant despite the loss of one

or other source due to adverse weather or high prices.

By exporting tea in bulk, developing countries are missing the opportunity for significantly

increased export earnings. The producing countries currently sell tea most often as a generic

without branding and packaging, despite the fact that branded tea fetches prices which are six

times higher than bulk exports. Sri Lanka is an exception, and has succeeded in capturing more

value in the supply chain through value-added production.

Retail:

With the growth of the supermarket in Europe and North America the character of tea buying

changed quite dramatically in the 1990s. There has been a centralization of tea buying, increased

buying by individual companies and the bypassing of wholesalers with direct links between the

tea buyers and tea packers. The leading companies spend a great deal on promoting their

products. In Japan the advertising expenditure was 8%, compared to 4% in the US and 2.5% in

the UK. They also spend a great deal on offering trade seem to add small margins on the tea but

make their money from these promotional margin allowances from the packers.

[43]

The Ministry of Finance & Planning and the Treasury of Sri Lanka is a ministry of

the Government of Sri Lanka responsible for developing and executing the government's public

finance policy, economic policy and long term planning. The Treasury is housed at the General

Treasury Building in Colombo fort.

Sri lanka applaying very good financial policies which become the helpful for the got the strong

shri lanka with financial strong.

Although the officer of the treasurer of the British Government of Ceylon dates back to the early

nineteenth century the Ministry of Finance was established in 1947 prior to the independence of

Ceylon as the Ministry of Finance and the Treasury of Ceylon with young J.R Jayawardena as

the first Minister of Finance. Over time the Ministry took over the policy planning which it

currently undertakes.

The Financial Services Authority (FSA) is a quasi-judicial body responsible for the regulation

of the financial services industry in the Shri lanka. Its board is appointed by the Treasury,

although it operates independently of government. It is structured as a company limited by

guarantee and is funded entirely by fees charged to the financial services industry.Its main office

is based in Canary Wharf, London, with another office in Edinburgh. The FSA's Chairman and

CEO are currently Lord Turner of Ecchins well and Hector Sants, although on 16 March 2012

announced his resignation, effective from the end of June that year.

Foreign Investment in Sri Lanka

The Central Bank of Sri Lanka has introduced a new Direction for the investments by eligible

investors in Government securities and equity capital of companies, incorporated in Sri Lanka

and units of unit trusts in Sri Lanka.

Hence, Share Investment External Rupee Accounts (SIERA), Treasury bond Investment External

Rupee Accounts (TIERA), Treasury bill Investment External Rupee Account (TIERA 2) and

Treasury bonds/bills Investment External Rupee Accounts- Deshabhimani (TIERA-D) is now

amalgamated to one single account named as Securities Investment Accounts (SIA).

[44]

Account Features

• Sri Lankan Diaspora, migrant workforce and Citizens of foreign states now have the

ability to invest in Sri Lanka Government Securities, Equity capital of companies

incorporated in Sri Lanka and Units of unit trusts in Sri Lanka

• Remittances to the SIA would automatically be converted at the prevailing exchange rate

to Sri Lankan Rupees (local currency) and can be invested in the above

• Original investment and any income realized, can be repatriated in any designated foreign

currency to an account specified by the investor

• Transfer of funds between SIA of the same account holder is permitted

• SIA maybe held jointly by eligible investors

• Further, eligible investors who invest in T-bonds/T-bills are permitted to enter into

repurchase and reverse repurchase transactions using T-bonds/T-bills purchased under

this scheme as collateral

Eligible Investors

• Foreign institutional investors such as country funds regional funds or mutual funds

• Corporate bodies incorporated outside Sri Lanka

• Citizens of foreign states whether resident in Sri Lanka or outside Sri Lanka

• Non- resident Sri Lankans

• Sri Lankan Professionals living in Sri Lanka who receive inward remittances

• Dual citizens who receive inward remittances

Permitted Credits

• Inward remittances received from aboard through banking systems

• Transfer of funds from NRFC/FCBU/RNNFC accounts of the same account holder

• Sale proceeds realized out of sale or transfer or maturity of T-bonds/T-bills or any

income realized by way of capital gain thereof

[45]

• Sale proceeds of shares supported by documentary evidence (Broker’s Contract Notes

and evidence of payments of tax etc.) and dividends

• Dividend income and units of unit trusts net of tax supported by documentary evidence

• Proceeds on redemption of units net of tax supported by documentary evidence

• Commissions relating to share transactions with supporting evidence

• Liquidation proceeds of companies

• Interest received on T-bonds

The Government has launched an agenda for vigorous growth titled Regaining Sri Lanka. There

the private sector is given a central role in driving the nation's economic recovery. The prospect

of internal peace provides a springboard to undertake the improvements necessary for Sri Lanka

to compete effectively with the best investment and growth performers in Asia.

This report considers the improvements and reforms needed for private investment to accelerate

and foreign direct investment (FDI) inflows to expand markedly.

Sri Lanka’s performance in generating private investment. Economic growth and private

investment, including FDI, have been low by the standards of the best performers in Asia. Poor

policies inhibited private investment from independence in 1948 until 1977. A fitful easing of

restrictive business-related policies began in the late 1970s. Notable events were the creation of

the Board of Investment, or BOI (as it is now known), the formation of economic zones and the

successful 1990s privatization programme. FDI increased sharply in the 1990s, but it is still

narrowly based and reliant on one-off privatization opportunities. Moreover, it remains below the

levels achieved in the more dynamic regional countries. As a consequence of these trends, Sri

Lanka's economic structure has shifted little towards higher value-adding manufacturing and

services, although there are notable success stories such as the emergence of a competitive

textiles and garments industry. Yet a capable established business sector is poised to increase

investment and could provide a good platform for joint ventures with dynamic foreign investors.

The country's good educational system is a sound base for providing skilled managers and

professionals and trainable labour. But shortcomings in physical infrastructure have to be

[46]

overcome to capitalize on the human resources that Sri Lanka offers. With suitable

improvements and policy reforms, FDI inflows could at least double from recent levels.

The investment framework, outlining reforms that can lead to a more attractive investment

climate. The legacy of past restrictive policies is still reflected in some legislation – for example,

in land regulation – but administrative practice is often better. The Government has already

reformed important areas of business regulation, including competition law and protection of

intellectual property rights. This builds on sound sector regulatory regimes developed earlier

(e.g. in mining and telecommunications). The major extant weaknesses are the restrictions on

labour severance and a business taxation system that requires case-by-case grant of incentives

and is biased against smaller investors. A package of balanced labour measures is proposed.

Taxation should be reformed to provide an accessible and competitive fiscal regime for all

investors. Easing of FDI entry restrictions should continue. Moves underway to abolish foreign

exchange controls are endorsed, and current good business immigration practices can be

formalized and promoted. An important theme is that the haven of good regulation and

administrative practice afforded to larger investors under the BOI's extensive powers should

become the norm throughout the economy. All these changes would facilitate Sri Lanka's goal of

becoming an international business hub.

PRIVATE INVESTMENT: TRENDS AND IMPACT

Until 1965, Sri Lanka's economic performance surpassed that in several of today's dynamic

economies of East Asia. It subsequently lagged behind, while the East Asian economies

accelerated, fuelled mainly by high growth in private domestic investment and FDI. With

Government policy now emphasizing private-sector-led growth, Sri Lanka could yet witness

dynamism similar to that in East Asia.

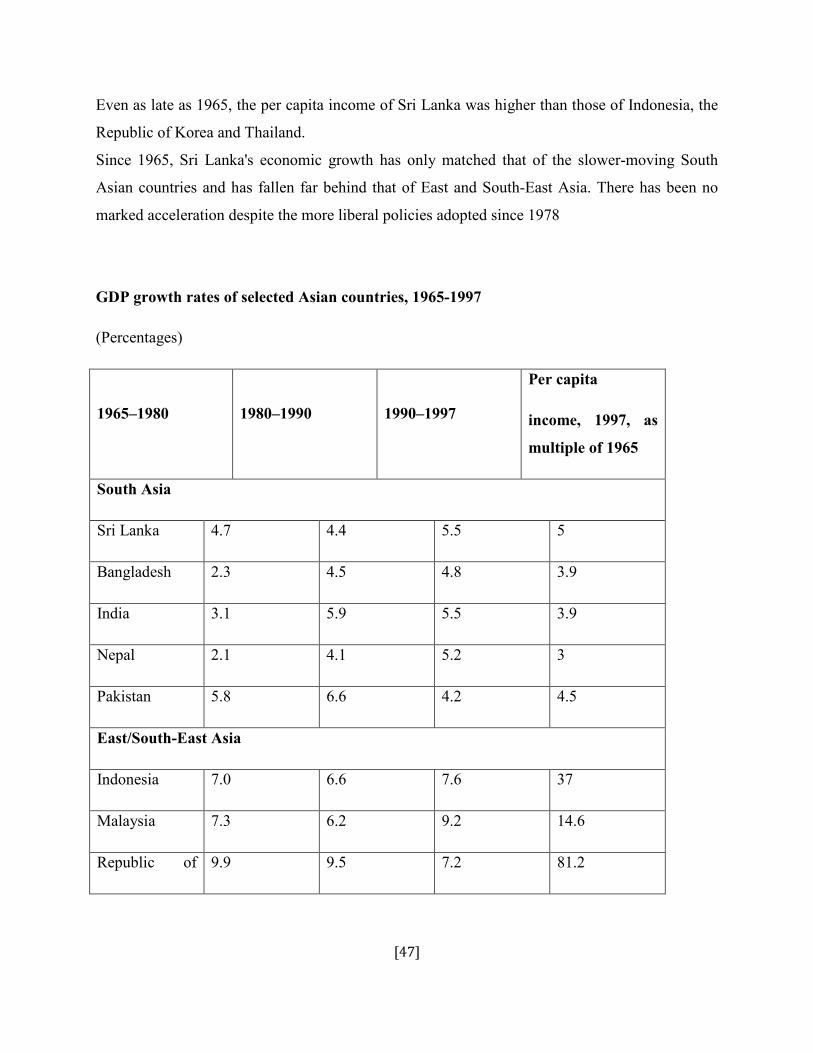

COMPARATIVE PERSPECTIVE

At the time of independence in 1948, Sri Lanka’s development indicators compared favourably

with those of other South Asian countries and most of the East and South-East Asian countries.

[47]

Even as late as 1965, the per capita income of Sri Lanka was higher than those of Indonesia, the

Republic of Korea and Thailand.

Since 1965, Sri Lanka's economic growth has only matched that of the slower-moving South

Asian countries and has fallen far behind that of East and South-East Asia. There has been no

marked acceleration despite the more liberal policies adopted since 1978

GDP growth rates of selected Asian countries, 1965-1997

(Percentages)

1965–1980 1980–1990 1990–1997

Per capita

income, 1997, as

multiple of 1965

South Asia

Sri Lanka 4.7 4.4 5.5 5

Bangladesh 2.3 4.5 4.8 3.9

India 3.1 5.9 5.5 3.9

Nepal 2.1 4.1 5.2 3

Pakistan 5.8 6.6 4.2 4.5

East/South-East Asia

Indonesia 7.0 6.6 7.6 37

Malaysia 7.3 6.2 9.2 14.6

Republic of 9.9 9.5 7.2 81.2

[48]

Korea

Singapore 10.4 7.7 7.3 62.1

Thailand 7.7 7.6 7.4 21.5

Viet Nam .. 2.5 8.0 ..

PHASES OF SRILANKA’S PRIVATE INVESTMENT

In the period since independence, two distinct phases of Government policy towards private

investment can be detected. These explain much of the slow growth and low structural change.

They are still important background to explaining much of today's regulations and institutions

dealing with private investment.

In the first phase (from 1948 to 1977), the public sector absorbed or controlled an increasing

share of the country's resources. Government intervention in the economy became pervasive.

Investment approvals and licensing and associated red tape were common. Employment

decisions were heavily regulated, controls on land ownership were imposed, access by the

private sector to finance was restricted, andtrade incentives were biased against exports. The

resulting business climate was inimical to private investment in general and FDI in particular. By

one estimate, as much as 70 per cent of the national economy was in the public domain in 1973

(World Bank 1995b: 4). In 1978, gross domestic investment was a low 19 per cent of GDP, of

which the private sector contributed less than half (45 per cent).

During this phase, mixed policies were pursued, and they are instructive in showing that private

investment in Sri Lanka reacts to changed regulatory conditions. For example, during the second

half of the 1960s there was a partial liberalization that generated better conditions for the private

sector. This had a beneficial impact on GDP growth, which averaged 5.3 per cent during the

[49]

period 1966–1970. The period 1971–1977 saw a reversal of intensified government intervention

and several policy measures that were adverse for private-sector investment. As a result, GDP

growth sharply decelerated to an annual average of 2.9 per cent during 1971–1977.

The second phase of Government policy was marked by liberalization. The poor economic

performance of 1971–1977 prompted a policy reorientation in 1977 to the pursuit of private-

sector-led, export-oriented development, including a greater role for FDI. Initially some of the

most severe controls were removed for all investors. These included dismantling of trade and

payment barriers, unification of the exchange rate, restructuring of agricultural and export taxes,

adjustment of administered prices, liberalization of interest rates and reduced restrictions on

pricing and investment by the private sector (IMF Institute 1996 and World Bank 1995b).

Later policies (including the issuance of the Industrialization Policy Statement in 1989)

introduced reforms to the tariff system (to lower tariff rates and reduce dispersion) and the tax

system (to reduce exemptions and lower rates).

However, comprehensive reforms of the regulations, taxes and administrative machinery

weighing down private investment were not tackled at the start. Instead the Greater Colombo

Economic Commission (which was reconstituted as the Board of Investment (BOI) in 1992) was

created in 1978 with wide powers of tax relief and administrative discretion for larger or priority

investors. No doubt this partial approach to liberalization was judged to be the only feasible

approach at the time.

Forms of FDI

FDI into the country has been mainly through 100 per cent foreign ownership rather than joint

ventures. Between 1979 and 2000, wholly foreign owned enterprises accounted for about 60 per

cent of estimated FDI by value and 45 per cent by number of projects.

However, the important feature of this statistic is that national investor participation in joint

ventures is unusually high given Sri Lanka's comparatively low per capita income. To some

extent this might reflect the preference for joint ventures in foreign investment policy and in

[50]

some privatizations. But it also suggests that Sri Lanka has a local private sector with the

technical and financial capability to provide strong partnerships with foreign investors.

Privatization has been an important channel of FDI into Sri Lanka. The 11 largest privatization

transactions between 1990 and 2000 accounted for $609 million of the $1,791 million in FDI

during the period. Cumulative data for the period February 1990–June 2001 shows that a little

more than two-thirds of privatization proceeds was raised from these foreign investors.

Since independence in 1948, conditions have never permitted national or foreign private

investment to flourish for sustained periods in Sri Lanka. The statistics show that Sri Lanka is

still a very low-income country with an economic structure not far removed from that of the

colonial era. Fortunately, the local skills base in both general education and business disciplines

is much better than would be expected in a country with a per capita income of only $800. There

is a well-established national private sector. There are good grounds for believing that private

investment will respond well to the prospects of greater stability and to reforms in the investment

framework. Sri Lanka's ambition to be an international business hub is realizable if regulatory,

tax and institutional reforms are made and Sri Lanka's strong points are developed and promoted

well. Preferential trade access to India and possibly to the United States presents enormous

opportunities.

Sri Lanka should aim high. There will be a substantial payoff in the size and quality of private

investment to the first South Asian country to implement a vision of becoming the first-choice

base for regional business operations. To be the first choice, Sri Lanka, a relatively small

country, must deliver a superb investment climate and highly effective investment generation.

The immediate areas to tackle in implementing such a vision are the weak points in the

regulatory and tax environment for private investment:

(i) Over-regulation and unpredictable administration of labour severance. This is by far the

most serious negative factor. A package of reforms is recommended. If fundamental

reforms are not made, any ambition to be the first-choice regional business hub will

have fallen at the first hurdle.

[51]

(ii) A business taxation system that is not competitive for all investors and is insufficiently

developed to cater to highly tax-sensitive activities. An overhaul of business taxation is

recommended to correct this.

(iii) Weaknesses in pro-competition policies, as manifested in sectoral and other legislation,

and a protectionist (but liberalizing) stance in FDI policy. The new Consumer Affairs

Authority should be tasked to investigate. All FDI entry restrictions should be re-

examined.

(iv) A continuing legacy of intrusive State powers in commercial matters (e.g. in land

powers).

(v) Provision of high-quality regulatory services through the BOI only for larger investors, in

contrast to services available to small- and medium-scale investors from the line

agencies.

HUMAN RESOURCE POLICIES OF SRI LANKA

According to the policy, the tea industry is operating by the Ministry of Public Estate

Management and Development and it is one of the important industries in Sri Lanka. It became

the world's leading exporter in 1995 with a 23% share of global tea export, higher

than Kenya's 22% share. The industry was introduced in the country in 1867 by James Taylor, a

British planter who arrived in 1852.

Now, Sri Lanka has become one of the countries exporting fair trade tea to the UK and other

many countries.

Tea which was one of the Sri Lanka's largest export commodities has crises over the past three

decades. According to statistics, in 1966 the value of the tea sector as a percentage of the gross

domestic product was only 2.2 per cent. But the contribution made by the tea sector to GDP in

1995 compared with other sectors of the economy is 1.9 per cent.

[52]

In 1996 the tea sector contributed 15 per cent of total export value. Export earnings from tea

sector in 1996 as compared to the other sectors are 15.05 per cent.

Recently, the tea industry is a major export producer, and particular tea sector as its net foreign

exchange earnings are very high. In 1991, Sri Lankan leading emerged the largest exporter of tea

to the world market. In international markets the share of Sri Lankan tea in 1995 was 23 per cent

compare to the Kenya was reported to have overtaken Sri Lanka in 1996 as the largest tea

exporter. Nowadays, in the international market tea export in bulk form, Sri Lanka has now

developed country and enters into the largest producer of retail consumer packets and bags to

other country.

The tea sector provides directly or indirectly employment to over 1 million people in Sri Lanka.

After the liberalization of economic policies, the development process for the sustainable use of

the natural resources and the government has also recognized the need to integrate environmental

concerns, in order to address national as well as international environmental concerns.

After the privatization of State plantations, the focus on environmental issues on tea plantation

sector becomes complicated and challenging. Tea sector appears that those issues are not solve

through contracts with the private sector at the time of privatization,

For example, land-use issues related to environmental degradation. Therefore, those issues may

need to be more addressed through normal laws and regulations of Sri lankan tea industries,

while at the same developmental needs time taking into account. In that level, balance measures

with awareness and training through assistance programmers appears to be a big challenge for

the authorities.

LABOUR STANDARDS OF TEA SECTOR IN SRI LANKA

Policy statement given by the board of investment of Sri lanka. Their support the Global

Compact addressed to the business community and proposed by the secretary-general of the

[53]

United Nations, which is incorporates the core labor standards of the international labor

organization.

The board of investment is also committed the related international labor standards by the

employers in the board of investment enterprises, and promoting to the application of the

principles underlying the Global Compact and both within and outside the export processing

Zones of Sri lanka.

EMPLOYMENT

1. Classification on the basis of Workers

Trainees workers:

Those are undergoing training for a period of not less than 6 months or 156 working days are

classified as trainees’ workers.

Semi-skilled workers:

Those are successfully completion of a training period of 6 month that worker called as a semi-

skilled workers.

Un-skilled workers:

Those works which does not related any training is called as un-skilled work.

Skilled workers:

Workers which have good skills for the job related is called as a skilled worker.

2. Recruitment and Retirement of workers:

- Minimum age for recruitment shall be 18 years

- Normal age of retirement is 55 years.

[54]

Persons who have attained the age of 16 years but below the age of 18 years can be employed,

subject to the following conditions:-

a) Persons under the age of 18 years cannot be employed for more than 50 hours of overtime

during any month.

b) Persons under the age of 18 years cannot be employed after 10.00 p.m. and before 6.00

a.m.

3. Prohibition on Child Labor:

Not employer should use any child labor through any contractor or sub-contractors with directly

or indirectly.

4. Contract of Employment:

a contract of employment is written with terms and conditions of service including the

designation or category of the employee, training period, probationary period, leave period,

holidays and others benefits, normal hours of work, rate of payment, has to be issued to every

worker including trainees and job obtained by the employer.

5. Equal Status

All male and female workers shall be paid equal remuneration for work and gives opportunity in

employment and occupation is also equal.

HOURS OF WORK

1. Normal Working Day:

One-Shift Operation:

Monday to Friday

A working day of 9 hours per day including of an interval of one hour for a meal or rest.

Saturday

[55]

A short working day of 6, 6 ½ or 7 hours including of an interval of one hour for a meal or rest.

Two/ Three-Shift Operation:

Monday to Friday

A working day of 8 hours per day including of an interval of half an hour for a meal or rest.

Saturday

A short working day of 5 ½ hours including of an interval of half an hour for a meal or rest.

2. Night Work:

There is no restriction on employment of male workers on night shift.

Employments of female workers on night work from 10.00 p.m. to 6.00 a.m. on the following

day will be allowed as a third shift, subject to the following conditions:-

a) Written consent of the worker to be available.

b) The employer to obtain approval from the department of labor for night work. The industrial

relations department of the board of investment will provide assistance depend upon request.

c) Payment of 1 ½ times the daily rate of wages for the normal night shift.

d) Maximum of 10 days night work per female worker in any one month.

e) A worker employed between 6.00 a.m. and 6.00 p.m. not to be employed on night shift on

same day.

f) A worker employed on night work to be allowed an adequate period for rest after such work.

[56]