Embed Size (px)

Citation preview

Inc. Langdon Seah | Hyder Consulting | EC Harris

“Establishing Port PPPs

in Emerging Maritime

Nations”

Sri Lanka Maritime Week, Colombo International Maritime Conference

Dr Jonathan Beard

23rd September Colombo

Source: Vesseltracker.com

© Arcadis 2015

• Private party to ‘typical’ port PPP is specific project company formed for that purpose - Special

Purpose Vehicle (SPV). SPV raises finance via combination of equity (provided by project company’s

shareholders) and debt provided by banks, or through bonds or other financial instruments.

• Finance structure = the combination of equity and debt, and contractual relationships between the

equity holders and lenders.

28 September 2016 2

Private Sector Involvement in the Port Sector ‘PPP’ now used to describe a range of models, many not strictly PPPs

Port Models: Public-Private

Roles

Source: World Bank

Public Service

Port

Tool Port

Landlord Port

Private Port

Private Sector Risk

Pu

bli

c se

cto

r ri

sk

Low High

Low

High

Works & Services

Contract

Operations &

Maintenance

Contract

Concession

Agreement

Full

PrivatizationPrivate Sector Participation

UKAustralia

Hong Kong

© Arcadis 2015

Is private capital available - who would want to invest in supply chain infrastructure?

“Developing Asia needs to spend US$40 trillion

on infrastructure between now and 2030.”

Danny Alexander, AIIB

A major portion of this must go to transport

& logistics infrastructure

Where will the money come from?

Asia is a major exporter of capital. Better

question might be: where are the bankable

projects?

Too many “Hambantota airports” (Sri Lanka),

”YuanMo expressways” (Yunnan) & Cai Mep

Ports (Vietnam)

Of 95 PRC road & rail projects with ADB & WB

financing, only a third were economically productive

(traffic volumes on two thirds were below forecast,

cost over-runs, etc)*

Focus on better project preparation….especially

under conditions of slower demand

28 September 2016 3Source: *A Ansar (2016) Oxford University

© Arcadis 2015

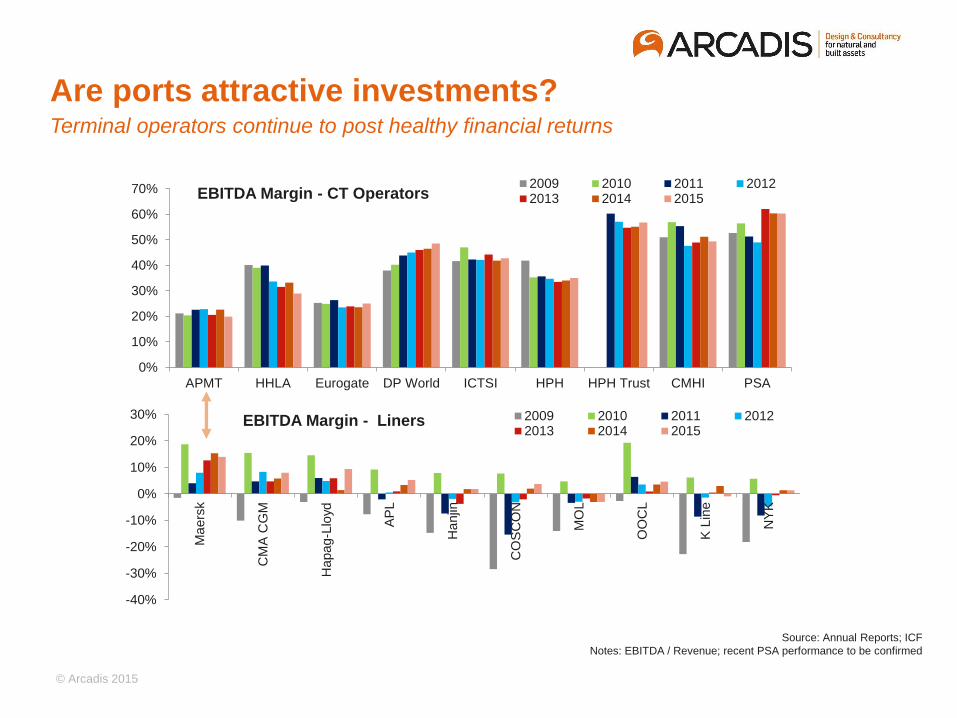

Are ports attractive investments?Terminal operators continue to post healthy financial returns

0%

10%

20%

30%

40%

50%

60%

70%

APMT HHLA Eurogate DP World ICTSI HPH HPH Trust CMHI PSA

EBITDA Margin - CT Operators2009 2010 2011 20122013 2014 2015

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Ma

ers

k

CM

A C

GM

Hapag‐L

loyd

AP

L

Ha

njin

CO

SC

ON

MO

L

OO

CL

K L

ine

NY

K

EBITDA Margin - Liners 2009 2010 2011 20122013 2014 2015

Source: Annual Reports; ICF

Notes: EBITDA / Revenue; recent PSA performance to be confirmed

© Arcadis 2015

Port PPPs – Some Key Issues & ChallengesWe only have time to cover a few in this session

Healthy demand growth is beneficial, but does not guarantee success:

see for example, South Vietnam

Key issues for public and private sectors:

– Supply side response, barriers to entry and Greenfield versus brownfield - the

resilience of older, inner city terminals

– Ensuring competition without unnecessary fragmentation: phasing up for

economies of scale

– Government ability to deliver supporting infrastructure: especially critical for

gateway ports

– Cargo mix and revenue type

– ‘Freedom to price’, revenue risk and cost risk

– Tender process and evaluation criteria - bidding re-runs & programme delay

– Environmental risks, including climate change

© Arcadis 2015

e.g. Vietnam – Why has Healthy Demand not

Guaranteed Successful PPPs?

Source: ICF

© Arcadis 2015

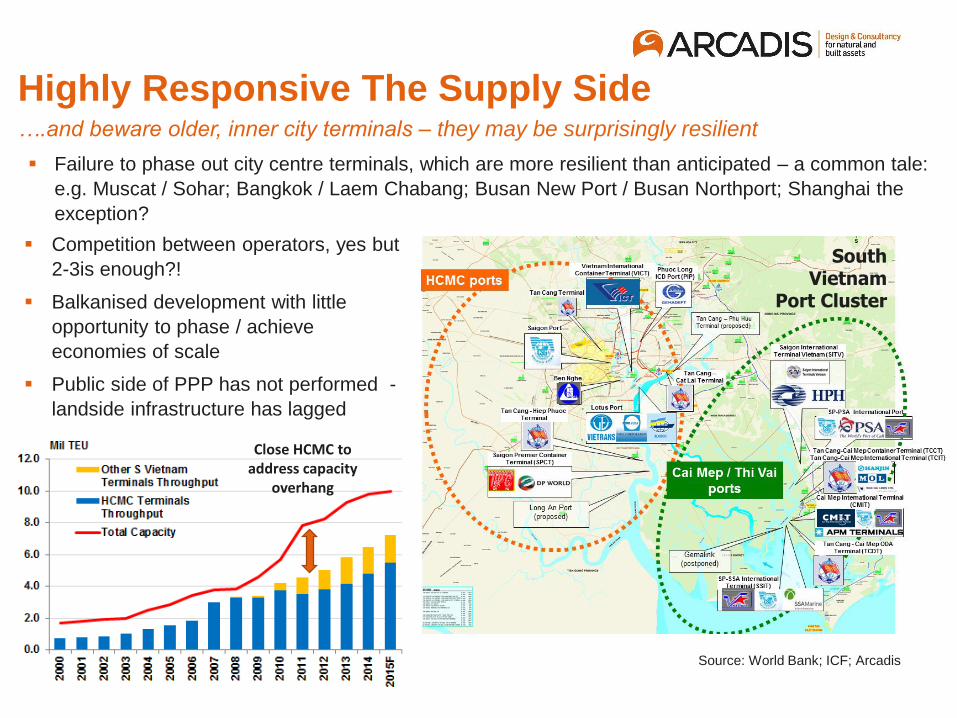

Highly Responsive The Supply Side….and beware older, inner city terminals – they may be surprisingly resilient

Failure to phase out city centre terminals, which are more resilient than anticipated – a common tale:

e.g. Muscat / Sohar; Bangkok / Laem Chabang; Busan New Port / Busan Northport; Shanghai the

exception?

Source: World Bank; ICF; Arcadis

Close HCMC to address capacity

overhang

Competition between operators, yes but

2-3is enough?!

Balkanised development with little

opportunity to phase / achieve

economies of scale

Public side of PPP has not performed -

landside infrastructure has lagged

South Vietnam

Port Cluster

© Arcadis 2015

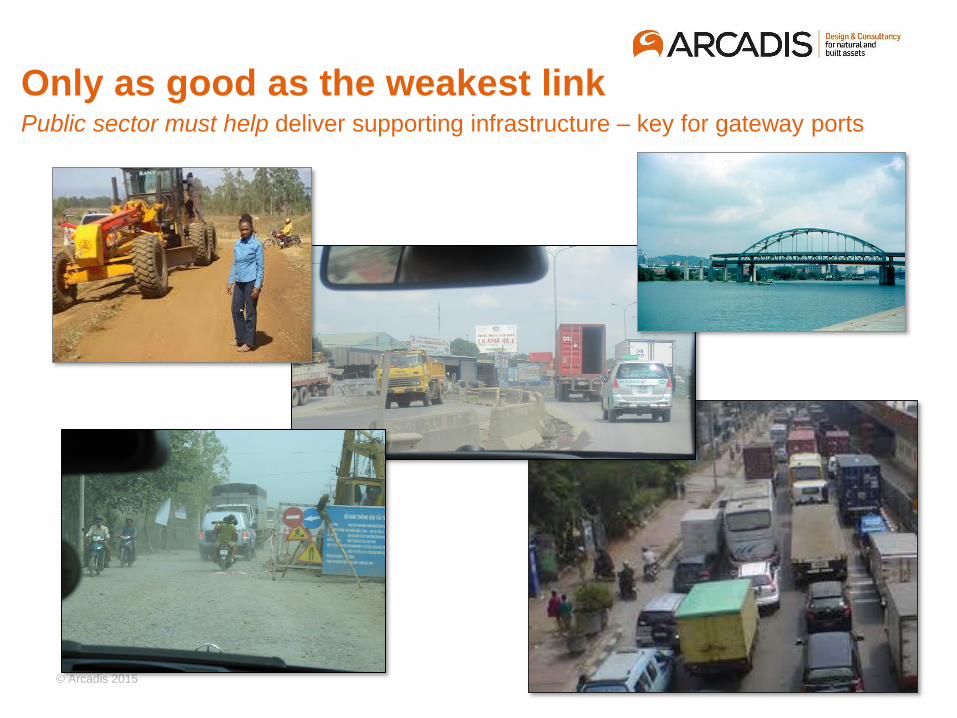

Only as good as the weakest linkPublic sector must help deliver supporting infrastructure – key for gateway ports

© Arcadis 2015

Revenue Risk: Tariff Control or Freedom to Price?And regulation of major cost items – rent, lease, etc.

Freedom to price preferred by private sector, but surplus capacity will push down tariffs:

– Removal of price controls in S. Vietnam originally favoured by private operators, but

rates fell to < USD 40 / 20’ container before the floor of USD 46 was introduced in

August 2013

Tariff control poses additional regulatory risk, but transparent system with clear scope

for adjustment mitigates some of this:

– Indonesia / Priok: regulated, but some transparency with upward (and downward

adjustment)

As contrasted with:

– Thailand / Laem Chabang: regulated, but limited transparency and no increase >20yrs

Cost control: reviews of rateable value, rents, etc.

– e.g. Melbourne and increase for DPW concession, once new bidder (ICTSI) indicated a

possible higher “market value” (although Port Authority subsequently backed down)

Competitive concession bid – revenue share / upfront payment is seductive for port

authority / government, but private bidders often over-commit (e.g. Mumbai) and then try

to pull out, further delaying projects, or incumbents bid high to keep out competition…

© Arcadis 2015

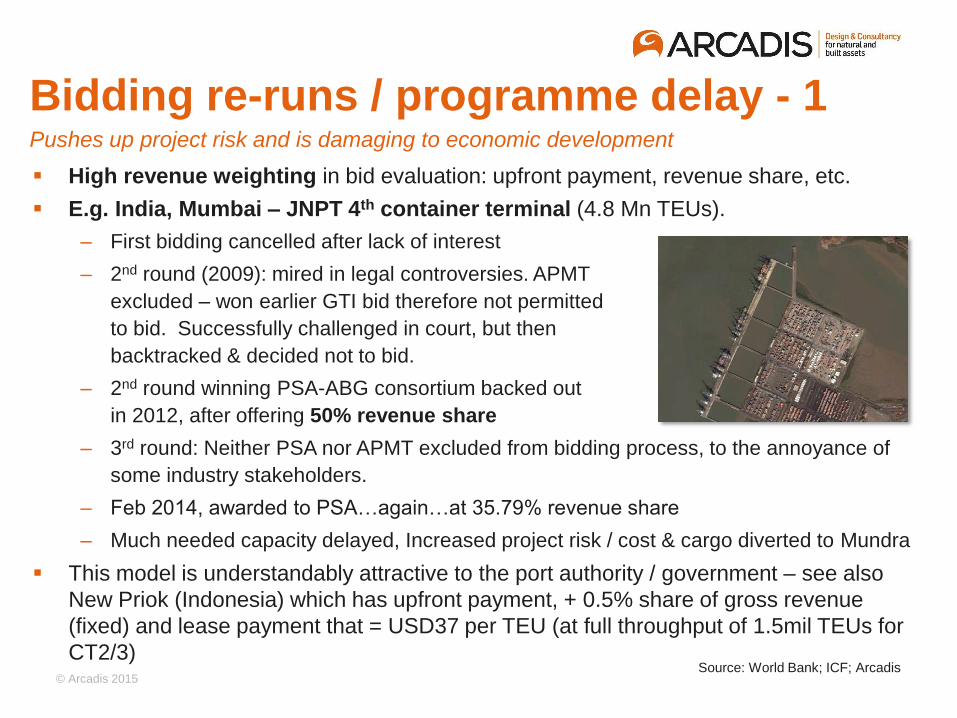

Bidding re-runs / programme delay - 1Pushes up project risk and is damaging to economic development

High revenue weighting in bid evaluation: upfront payment, revenue share, etc.

E.g. India, Mumbai – JNPT 4th container terminal (4.8 Mn TEUs).

– First bidding cancelled after lack of interest

– 2nd round (2009): mired in legal controversies. APMT

excluded – won earlier GTI bid therefore not permitted

to bid. Successfully challenged in court, but then

backtracked & decided not to bid.

– 2nd round winning PSA-ABG consortium backed out

in 2012, after offering 50% revenue share

– 3rd round: Neither PSA nor APMT excluded from bidding process, to the annoyance of

some industry stakeholders.

– Feb 2014, awarded to PSA…again…at 35.79% revenue share

– Much needed capacity delayed, Increased project risk / cost & cargo diverted to Mundra

This model is understandably attractive to the port authority / government – see also

New Priok (Indonesia) which has upfront payment, + 0.5% share of gross revenue

(fixed) and lease payment that = USD37 per TEU (at full throughput of 1.5mil TEUs for

CT2/3) Source: World Bank; ICF; Arcadis

© Arcadis 2015

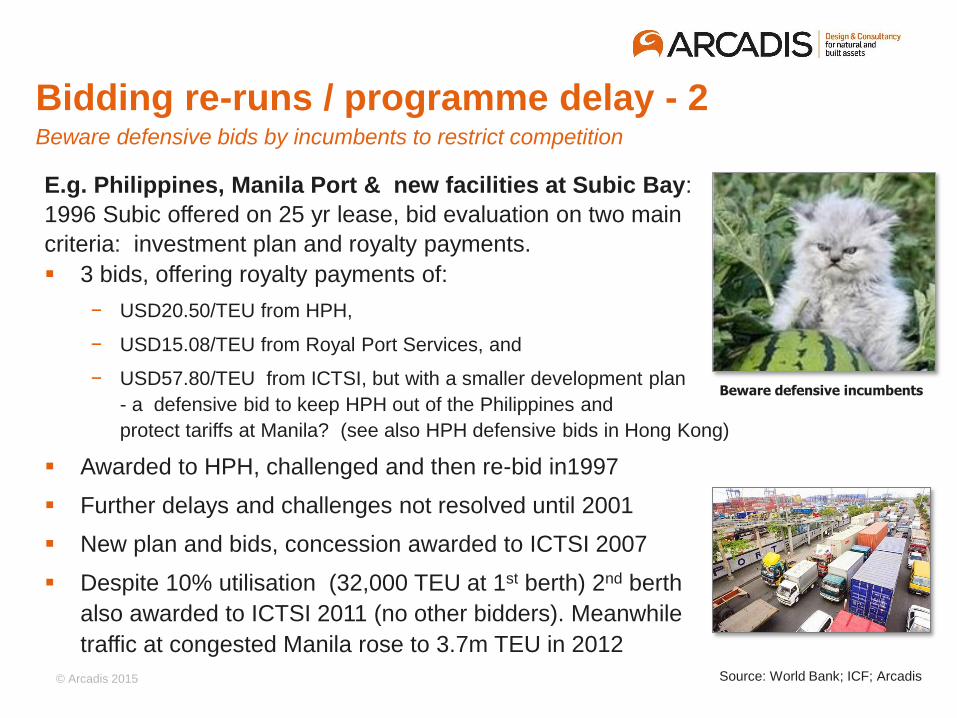

Bidding re-runs / programme delay - 2Beware defensive bids by incumbents to restrict competition

E.g. Philippines, Manila Port & new facilities at Subic Bay:

1996 Subic offered on 25 yr lease, bid evaluation on two main

criteria: investment plan and royalty payments.

3 bids, offering royalty payments of:

− USD20.50/TEU from HPH,

− USD15.08/TEU from Royal Port Services, and

− USD57.80/TEU from ICTSI, but with a smaller development plan

- a defensive bid to keep HPH out of the Philippines and

protect tariffs at Manila? (see also HPH defensive bids in Hong Kong)

Awarded to HPH, challenged and then re-bid in1997

Further delays and challenges not resolved until 2001

New plan and bids, concession awarded to ICTSI 2007

Despite 10% utilisation (32,000 TEU at 1st berth) 2nd berth

also awarded to ICTSI 2011 (no other bidders). Meanwhile

traffic at congested Manila rose to 3.7m TEU in 2012

Beware defensive incumbents

Source: World Bank; ICF; Arcadis

© Arcadis 2015

Wrap - Port PPPs & BeyondIn an ideal world public sector would establish...

Transparent (and simple) selection procedure

Clear and committed timelines for phase in (and out)

of new capacity…including option to develop adequate

economies of scale where possible (note impact of

mega vessels / alliances at major ports)

Deliver supporting infrastructure

Regulation via competition is preferred, but may not be possible in early

stages where only one operator is feasible

Plan long-term – opportunities to phase, expand and secure scale economies

Be wary of defensive bids by incumbents

Fair and clear allocation of risk and reward between both ‘Ps’ ...and be clear

on policy objectives

Establish a track record in successful delivery of PPPs – create a virtuous

circle

IFIs (ADB, AIIB, etc.) can play a key role, especially on technical assistance

Thank you

Any questions?

28-9-2016 13

T +852 2263 7300

M +852 6095 8434

Arcadis 38/F AIA Kowloon TowerLandmark East100 How Ming StreetKwun Tong, KowloonHong Kong

DR JONATHAN BEARDHead of Transportation & Logistics, Asia

IVAN KEOGHCountry Director IndiaArcadis 2nd Floor, Esquire CenterNo.9 M.G RoadBangalore560 001, IndiaT +91 80 4123 9141 F +91 80 4123 8922 M +91 77 6045 2763E [email protected]

© Arcadis 2015 28-9-2016 14

Our Clients

![July 29 August 2, 2013 - UF/IFAS OCI · ARCADIS US, Inc. [BOOTH #36] WEBSITE: REPRESENTATIVE: Robert Daoust (robert.daoust@arcadis-us.com) ARCADIS is an international company providing](https://img.pdfslide.us/doc/110x75/5f18cf45d3ebda26806f2458/july-29-august-2-2013-ufifas-oci-arcadis-us-inc-booth-36-website-representative.jpg)