Embed Size (px)

DESCRIPTION

BBM Project

Citation preview

in SBI

CHAPTER I

INTRODUCTION

HISTORY OF BANKING

A banker or bank is a financial institution that acts as a payment agent for customers, and

borrows and lends money. In some countries such as Germany and Japan banks are the

primary owners of industrial corporations while in other countries such as the United States

Banks are prohibited from owning non financial companies.

Banks act as payment agents by conducting current accounts for customers paying cheques

drawn by customers on the bank, and collection cheques deposited to customer’s current

accounts for customer payment via other payment methods such as telegraphic transfer.

Banks borrow money by accepting funds deposited on current account, accepting term

deposit and by issuing debt securities such as banknotes and bonds. Banks lend money by

making advances to customers on current account, by making installment loans, and by

investing in marketable debt securities and forms of lending.

Banks provide almost all payment services, and a bank account is considered indispensable

by most businesses, individuals and governments. Non-banks that provide payment services

such as remittance companies are not normally considered an adequate substitute for having a

bank account.

Banks borrow most funds borrowed from households and non-financial businesses, and lend

most funds lent to households and non-financial businesses, but non-bank lenders provide a

significant and in many cases adequate substitute for bank loans, and money market funds,

cash management trusts and other non-bank financial institution in many cases provide an

adequate substitute to banks for lending saving to.

Seshadripuram academy of business studies. Page 1

in SBI

GROWTH OF BANKING IN INDIA:

Banking in India back to 1786 where the first bank that was established in India. Then the

nationalization of banks in 1969 liberalisation in 1991.In India, Banking sector is segregated

as public sector banks, private sector banks and co-operative banks.

Banks can be categorized into non-scheduled banks and scheduled banks. Scheduled banks

constitute of commercial banks and co-operative banks. There are about 67,000 branches of

scheduled banks spread across India. During the first phase of financial reforms, there was a

nationalization of 14 major banks in 1969. This crucial step led to a shift from Class banking

to Mass banking. Since then the growth of the banking industry in India has been a

continuous process.

As far as the present scenario is concerned the banking industry is in a transition phase. The

Public Sector Banks (PSBs), which are the foundation of the Indian Banking System account

for more than 78 percent of total banking industry assets. On the other hand the Private

Sector Banks in India is witnessing immense progress. They are leaders in Internet banking,

mobile banking, phone banking, ATMs. On the other hand the Public Sector Banks are still

facing the problem of unhappy employees. There has been a decrease of 20 percent in the

employee strength of the private sector in the wake of the Voluntary Retirement Schemes

(VRS). As far as foreign banks are concerned they are likely to succeed in India.

Indus land Bank was the first private bank to be set up in India. IDBI, ING Vysya Bank, SBI

Commercial and International Bank Ltd., Dhanalakshmi Bank Ltd., Karur Vysya Bank Ltd.,

Bank of Rajasthan Ltd etc are some Private Sector Banks. Banks from the Public Sector

include Punjab National Bank, Vijaya Bank, UCO Bank, Oriental Bank, Allahabad Bank.

Banking industry has revolutionized the transactions and financial services system

worldwide. Through the development in technology, banking services has been availed to

customers at all times, even after the normal banking hours. Banking industry services is

nothing but the access of most of banking related services (Verification of account details,

going with transaction, etc.).

Seshadripuram academy of business studies. Page 2

in SBI

DEFINITION OF BANKING:

Sec(1)(b) defines banking as accepting for the purpose of lending or investments of deposits

of money from the public repayable on demand or otherwise and withdrawal by cheque ,

draft, order, or otherwise.

IMPORTANCE OF BANKING IN INDIA:

Banking plays a very important role in economic development of a country. They touch every

aspect of the modern banking. Some of the important roles played by banking for the

developments of Indian economy are as follows.

Banking mobilizes the small, scattered and ideal saving of the people and

make available for the productive purpose i.e. they help in the process of

capital formation.

By offering interest banks attracts depositors and promote the habit of thrift

and saving among people.

Bank is a convient and economic means payment and transfer of funds i.e.

cheques, DD, bank drafts.

Bank helps the movement of funds from region where they are not very useful

to regions where they can be more usefully employed.

Though the supply of money (bank money and credit money) bank exert a

powerful influence on the interest rates in the money market.

Banks helps trade and commerce. Industry and agriculture by meeting their

financial needs.

Bank directs flow of funds into productive channels. While lending money

they discriminate in favor of essential activities and against non-essential

activities.

In the modern economy people who save people who undertakes investment

are different hence there is a need for financial intermediaries like banks that

should help the flow of funds from savers to investors.

Seshadripuram academy of business studies. Page 3

in SBI

INDIAN BANKING SYSTEM

The Indian banking system can be broadly classified into nationalized, private banks and

specialized banking institution, the RESERVE BANK OF INDIA acts as a centralized body

monitoring any discrepancies and shortcoming in the system. Since the nationalization of

bank in 1969 the public sector banks like THE SBI BANK have acquired a place of

prominence and has since then seen tremendous progress.

The need to become highly CUSTOMER FOCUSSED has forced the slow moving

public sector banks to adopt a fast track approach, the varieties of products and services

through e-banking has increased the scope of our banking system.

The conservative banking practices allowed Indian. Banks to be insulted partially from the

Asian currency crisis. Indian banks are now quoting all higher valuation when compared to

banks in other Asian countries (Via, Hong Kong, Singapore, Philippines etc.) that have major

problems linked to huge Non-performing assets (NPA’s) and payments defaults. The SBI are

growing its revenue through the efficient branch networks mainly focused on the retail

segments like car finance, housing loans, track finance etc.

The Indian banking has finally worked up to face the competitive dynamics of the new Indian

market and is addressing the relevant issues to take on the multifarious challenges of

globalization. Banks that employ INFORMATION TECHNOLOGY SOLUTION are

perceived to be FUTURISTICS and PROACTIVE players capable of meeting the

multifarious requirement of the large customers ‘base.

Now the private banks have been fast on the uptake and are reorienting their strategies using

E-BANKING as a medium, the E-BANKING has emerged as the new a challenging frontier

of marketing with the conventional physical world being just as applicable like in any other

marketing medium.

The Indian banking has come from a long way from being a sleepy business institution to

a highly proactive and dynamics entity. This transformation has been largely brought about

by the large close of liberalization and economic reforms that allowed banks to expose new

business opportunities rather than generating revenues from conventional streams (i.e.

Seshadripuram academy of business studies. Page 4

in SBI

borrowing and lending). The banking in India is highly fragmented with 30 banking units

contributing to almost 50% of deposits and 60% of advance.

Indian nationalized banks (i.e. Government owned) continue to be the major lenders

in the economy due to their sheer size and penetrative networks which assures them high

deposit mobilization.

ESSENTIAL CHARACTERISTICS OF BANK:

The essential characteristics of a bank are:

Acceptance of deposits from the public on fixed, current or savings bank account

Allowing of withdrawal of such deposits by cheques, drafts, orders or otherwise.

Utilization of deposits in hand for the purpose of lending or investments.

FUNCTIONS OF BANKING

The most important functions of banking may be classified as follows:

To assemble capital and make it effective.

To receive deposits and make collections.

To check out and transfer funds.

To discount or lend.

To exercise fiduciary or trust powers.

To issue circulating notes.

Every bank which expects to succeed must first of all prove its value to the community. The

services which a bank performs are so generally taken for granted that the public is unaware

of the real extent of the facilities offered. Banks are equipped to utilize funds, for either a

short or long period of time, safely, and with some profit.

CLASSIFICATION OF BANKS

Banks are classified into several types based on the function they perform. Generally the

banks are classified:

Seshadripuram academy of business studies. Page 5

in SBI

Commercial banks

Investment or industrial banks

Exchange banks

Co-operative banks

Land Mortgage banks

Saving banks

Central banks

Commercial banks.

1. Commercial banks:

Commercial banks perform all types of business transactions and accept three

types of deposits fixed deposits, saving bank deposits and current deposits. They accept these

deposits which are repayable on demand or on short notice. They provide funds only for short

term needs.

2. Investment bank /industrial banks:

Investment bank is those banks, which provide funds on long term for

industries. The investment banks are specialized in providing long term loans to industries

with a view to buy plant and machinery. The investment banks obtain funds through share

capital, debentures and long term deposits from the public.

3. Exchange banks:

Exchange banks are known as foreign banks or foreign exchange banks,

which provide foreign exchange for import trade. Their main function is to make

international payments through the purchase and sale of exchange bills. They convert home

currency into foreign currency and foreign currency into home currency.

4. Co-operative banks:

Co-operative banks are promoted to meet the banking requirements of

consumer not only in urban areas and rural areas. They are formed on the co-operative banks

principle and as such they are more service oriented than profit oriented.

Seshadripuram academy of business studies. Page 6

in SBI

5. Central banks:

Central banks are an apex bank in the country, which brings the entire banking

system unified, controlled and regulated. In our country the central bank is the Reserve Bank

of India (RBI).

6. Land Mortgage banks:

Land Mortgage bank provides long term loans on the security of the land to

initiate permanent improvements on the land to buy agriculture machineries.

BANKER AND A CUSTOMER

BANKER

A banker is a person or company carrying on the business of receiving money and

collecting drafts, for customers subject to the obligation of honoring cheques drawn upon

them time to time by the extent of the available in their ‘current accounts’.

CUSTOMER

A person becomes a customer of a bank, when he makes a regular transaction with

the bank and has maintained his accounts regularly with the banker, the moment his cheques

is accepted for collection and there must be some recognizable course of habit of dealing

between the person and the bank.

FINANCE

A branch of economics concerned with resource allocation as well as resource

management, acquisition and investment. Simply finance deals with matters related to money

and the market. The term “Finance” may thus incorporate any of the following:

The study of money and other assets;

The management and control of those assets;

Profiling and managing project risks;

The science of managing money;

Seshadripuram academy of business studies. Page 7

in SBI

Finance is defined as the provision of money at the time when it is required. Every

Enterprise, whether big, medium or small, needs finance to carry on its operation achieve its

targets finances is some indispensable today that it is rightly said that it is the life blood of an

enterprise.

DEFINITION OF FINANCE:

According to OXFORD DICTIONARY finance may be defined as:

The management of money.

Monetary support for an organization.

As a verb, “to finance” is to provide funds for business or for an individual’s

large purchase (car, home, etc)

The activity of finance is the application of a set of technique that individual

and organizations (entities) use to manage their money, particularly the differences between

income and expenditure and the risks of their investments.

Finance is used by individuals (personal finance) by governments (public

finance), by business (corporate finance), as well as by a wide variety of organization

including schools and non –profit organization.

In general, the goals of each of the above activities are achieved through the

use of appropriate financial instruments, with consideration to their institutional setting.

Finance is one of the most important aspects of business management without

proper financial planning a new enterprise is unlikely to be successful. Managing money (a

liquid asset) is essential to ensure a secure future, both for the individual and an organization.

OBJECTIVES OF FINANCE

Profit maximization.

Wealth maximization.

Maintaining balanced asset structure.

Long-term Liquidity.

Seshadripuram academy of business studies. Page 8

in SBI

Judicious planning of funds.

Innovation and efficiently.

Financial discipline like capital budgeting, fund flow and cash flow analysis and

performance budgeting.

FEATURES OF FINANCE

Finance or Financing is an essential business activity.

Finance may be short-term finance, medium-term finance or long-term finance,

depending upon the nature of the activities to be financed.

Business Finance includes owned funds or owned capital and ploughed back

profits, and borrowed funds or borrowed capital like Debentures issued, public

deposits accepted, loans from financial institutions accepted and banks.

Finance estimates the financial requirements of the undertakings, profitable use of

the funds.

TPYES OF FINANCE

Depending upon the nature of nature of activities to be finance, the financial requirements

or needs of a business enterprise may be classified into three types of finance:

1. Short-term finance.

2. Medium-term finance.

3. Long-term finance.

Short-Term Finance:

Short-term finance refers to the financial required by a firm for a period of one year or

less. It is a finance required for the purchase of raw materials, payment of wages and salaries

and for meeting the other day-to-day expenditure like manufacturing, administrative,

marketing and other expenses of a firm.

Seshadripuram academy of business studies. Page 9

in SBI

Short- term finance is also known as working capital finance, as it is required for

investment in working capital or current assets like cash and bank balances, inventories and

accounts receivables and marketable securities.

Medium-Term Finance:

Medium-Term Finance refers to finance required for period of one year to five

years. It is the finance required for permanent or regular working capital, replacement of

worn-out machines, heavy repairs to buildings, heavy advertising campaign, small expansion

and modernization and also for meeting long-term needs for which long-term finance cannot

be quickly arranged.

Long-Term Finance:

Long-term finance refers to the finance required for a period exceeding five years,

usually for five to twenty years. It is required for financing the fixed capital, like, for

procurement of fixed assets required for the establishment of a new undertaking and for

major expansion and modernization of an existing undertaking.

FUNCTIONS OF FINANCE

The functions of finance includes:-

Benchmarking of Finance processes and practices to identify performance gaps and

issues;

Visioning of the overall Finance Function, considering organization, process, people

and technology;

Developing Finance policies and control frameworks, factoring in all relevant

business, regulatory, governance and internal control requirements;

Designing best of breed Finance organizations, including mapping of roles and

responsibilities of corporate, business unit and shared services Finance groups;

Identifying opportunities for shared services and outsourcing/co-sourcing delivery

models

Seshadripuram academy of business studies. Page 10

in SBI

Designing detailed Finance transaction processing and reporting processes including

business intelligence; and

Delivering programs for large-scale, multi-work stream transformational initiatives.

Meaning of Financial Management

The term “Financial Management” has a number of meanings including the administration

and maintenance of financial assets. The process of financial management may also include

identifying and trying to work around the various risks to which a particular project may be

exposed.

Definition of Financial Management

According to Prof. Bradley, "Financial management is the area of business management,

devoted to a judicious use of capital and a careful selection of sources of capital, in order to

enable a spending unit to move in the direction of reaching its goals."

According to Phillip hates: “FM is concerned with the managerial decisions that results in

acquisition and finance of long term and credit for the firm as such it deals with solution that

require selection of specific assets selection of liabilities as well as problems of size and

growth of enterprise. The analysis of these decisions is based on the expected inflow and

outflow of funds and their effect upon management function”.

Financial management is that part of management which is concerned mainly with raising

funds in the most economic and suitable manner, using these funds as profitable as possible,

planning future operations and controlling current performance and future development

through financial accountancy , cost accountancy , budgeting ,statistics and other means.

Financial Management provides the best guide for the future resources allocation of firm. It

provides relatively uniform yardstick for judging most of the enterprises operations and

projects.

In short Financial Management is the operational activity of a business that is responsible for

obtaining and effectively utilizing of funds

Seshadripuram academy of business studies. Page 11

in SBI

OBJECTIVES OF FINANCIAL MANAGEMENT

Profit maximization:

Profit earnings the main aim of every economic activity. A business being an

economic institution must earn profit to cover its cost and provide funds for

growth. No business can survive without earning profit. Profit is a measure of

efficiency of a business enterprise .Profit also serves as a protection against risk

which cannot be ensured. Thus, profit maximization is considered as the main

objective of the business.

Wealth maximization:

Wealth maximization is the appropriate objective of an enterprise.

Financial theory asserts that wealth maximization is a single substitute for a

stockholder’s utility. When the firm maximizes the stockholder’s wealth, the individual

stockholder’s can use this wealth to maximize his individual utility. It means that by

maximizing stockholder’s wealth the firm is operating consistently towards maximizing

stockholder’s utility.

1. Financial management is a distinct area of business management - i.e. financial

manager has a key role in overall business management.

2. To select the prudent or rational use of capital resources.

3. To make proper allocation and utilization of funds.

4. To have a careful selection of the source of capital.

5. To determining the debt equity ratio and designing a proper capital structure for the

corporate goal achievement.

6. To ensuring the achievement of business objectives viz. wealth or profit

Maximization.

7. To make fair returns to the investors.

8. Capital Budgeting.

Seshadripuram academy of business studies. Page 12

in SBI

IMPORTANCE OF FINANCIAL MANAGEMENT:

It is necessary for the smooth running of an Enterprise.

Financial management provides complete coordination between various functional

areas such as purchase, stores, production, marketing, etc.

Financial management helps the top management to evaluate the profitability of

operational activities of the organization.

Financial management is important to all level of management for decisions.

Financial management helps to determine the financial soundness of a firm.

Methods of financial analysis:

1. Comparative analysis.2. Common- size statement.3. Trend analysis.4. Ratio analysis.5. Fund flow analysis.6. Cash flow analysis.7. Cost volume profit analysis

1. Comparative Financial Statement:

The preparation of the comparative financial statement is based on the premise that a statement covering a period of number of years is more meaningful and significant than for a single year only and that the financial statement for one period represent only one phase of the long and continuous history of the firm. The comparative financial analyst in horizontal analysis of the firm seeks in establishing operations and conditional trend of the firm.

2. Common –size statement:

The common size statement represent the relationship of different items of financial statement with some common item by expressing each item as a percentage of the common items, in common size statement balance sheet and income statement are shown in analyzed percentage.

3. Trend analysis:

The financial statement may be analyzed by computing trend of series of information. This method evaluates the direction of upwards or down ward trend and involves the computation of the percentage relationship that each statement item bears to

Seshadripuram academy of business studies. Page 13

in SBI

the same item in base year. The information out of a number of years is taken up for one year. Generally the first year is considered as base year.

4. Fund Flow Analysis: This is a statement which show2s the movement of funds and is a report of financial operative of the business under taking. It indicates various means by which funds were obtained during a particular period and the ways in which those funds were employed.

5. Cash Flow Analysis: Cash flow analysis is a statement which describes the inflow and out flow of cash and cash equivalents in an enterprise during a specified period of time. Such a statement shows net effect of the various business transactions on cash and taken into account as receipts and disbursements of cash.

6. Cost-volume profit analysis: Cost volume profit analysis is a technique for studying the relationships, between cost, volume and profit. Profits of an undertaking depend upon a large number of factors.

7. Ratio analysis: This is an important mean of expressing the relationships between two elements. A ratio must be represented as a meaningful relationship, but use of ratio cannot take the place of studying the underlying data.

Limitations of financial statement analysis:

Financial Statement analysis is a powerful mechanism of determining financial strengths and weakness of a firm, but the analysis is based on the information available in the financial statement.

The financial statement analyses have few limitations which are shown here under:

1. Financial Statement Analysis is only a statement of interim reports.2. Financial statement Analysis is based only on monetary factors and non monetary

factors are ignored.3. Changes in accounting procedure by a firm may often make financial statement

analysis misleading.

TYPES OF RATIOS:

1. Liquidity ratios2. Leverage ratios3. Activity ratios

Seshadripuram academy of business studies. Page 14

in SBI

4. Profitability ratios

1. Liquidity ratios: These are the ratios which are calculated for the purpose of measuring the short term solvencies or liquidity of an organization. Liquidity refers to ability of an organization to meet its short term obligation out of its short term resources or assets. These ratios also indicate whether a firm has sufficient working capital to carry on its day today activities.

A. Current Ratio: This ratio is called by different names such as 2:1 ratio, working capital ratio, and solvency ratio. This ratio emerged out of the experience of the bankers who wanted compare the current assets to current liabilities before lending money to the commercial and corporate enterprises. This ratio helps to know the solvency and liquidity of the firm. The ratio is connected with the working capital and hence it is called “working capital ratio”

Current ratio is symbolically expressed as follows: Current AssetsCurrent Ratio= Current liabilities

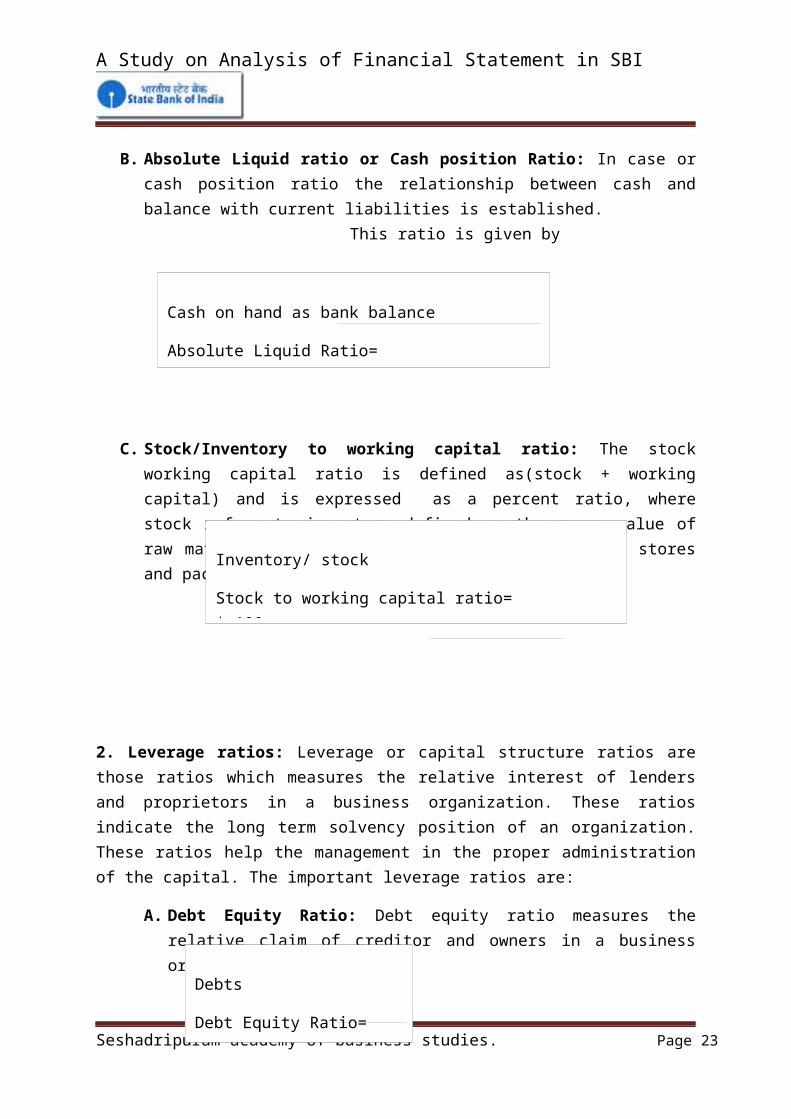

B. Absolute Liquid ratio or Cash position Ratio: In case or cash position ratio the relationship between cash and balance with current liabilities is established.

This ratio is given by

Absolute Liquidity Ratio

C. Stock/Inventory to working capital ratio: The stock working capital ratio is defined as(stock + working capital) and is expressed as a percent ratio, where stock refers to inventory defined as the rupee value of raw materials, work-in –progress, finished goods, stores and packing materials.

Seshadripuram academy of business studies. Page 15

Current Assets

Current Ratio=

Current Liabilities

Cash on hand as bank balance

Absolute Liquid Ratio=

Current liabilities

Inventory/ stock

Stock to working capital ratio= * 100

Working capital

in SBI

2. Leverage ratios: Leverage or capital structure ratios are those ratios which measures the relative interest of lenders and proprietors in a business organization. These ratios indicate the long term solvency position of an organization. These ratios help the management in the proper administration of the capital. The important leverage ratios are:

A. Debt Equity Ratio: Debt equity ratio measures the relative claim of creditor and owners in a business organization.

B. Proprietary Ratio: The proprietary ratio, also known as ‘owner fund ratio’ shareholder’s equity ratio, the relationship between the contributions of owners and the contributions of owners plus outsiders. The formula for this ratio may be written as follows

C. Fixed assets to net worth ratio: This ratio signifies the relationship between fixed assets and net worth.

4. Activity Ratios: These ratios are adopted to assess the effectiveness of the resources employed in the business activity. The company would like to have control over the fund employed in the business and these ratios tell the extent of control the firm has over the funds employed. If any gap is noticed by adopting these ratios, it can be immediately rectified. These ratios also analyze the use of resources and the utility of

Seshadripuram academy of business studies. Page 16

Debts

Debt Equity Ratio=

Equity

Net worth

Proprietary ratio=

Total assets

Fixed assets

Fixed assets to net worth=

Net worth

in SBI

each component of total assets. The profitability of the firm can be determined by activity ratios coupled with the degree of leverage.

A. Stock turnover ratio: This ratio shows the efficiency of the organization in managing its invention or stock. Inventory turnover ratio indicates the number of times the stock is turned over.

B. Debtor turnover ratios: this ratio is also known as ‘Receivables’. Turnover ratio is inter-statement ratio. The ratio is expressed as follows:

4. Profitability Ratios: Profitability of business organization shows how successfully the business is carried out during a period. These ratios measure the profitability of the business. These ratios are very important from the point of view of different set of people who are interested in the business organization likes owners, creditors, employee’s supplier’s government. Organization etc.

A. Gross profit ratio: The gross profit ratio is the relationship of gross profit on sales to net sales.

Seshadripuram academy of business studies. Page 17

Cost of goods sold

Stock turnover ratio=

Average stock of inventory.

Net credit sales

Debtor turnover ratios=

Net Debtors

Gross profit

Gross profit ratio= *100

Net sales

in SBI

B. Earnings per share: This is computed by dividing the net profit after tax and dividend to preference share holders. This avoids confusion and indicates the profit available to the ordinary shareholders on a “per share basis”. This computed as follows;

Seshadripuram academy of business studies. Page 18

Net profit after tax

Earnings per share=

Number of Equity shares

in SBI

ADVANTAGES OF RATIO ANLYSIS:

1. Useful in analysis of financial statement: It helps in analyzing the financial statement i.e. P and L account and balance sheet which is useful for all the stakeholders of the company.

2. Improving future performance: It identifies the weakness of the business and helps the management to overcome these weaknesses.

3. Judging the efficiency of the business: It evaluates the liquidity, solvency, and profitability position if the firm which helps in judging the overall efficiency of the firm.

4. Inter firm comparision: It helps in comparing the performance of one firm with that of another in the same industry.

5. Simplifies accounting figures: Complex accounting data presented in P and L account and balance sheet is simplified, summarized and systamised with the help of ratio analysis.

LIMITATIONS OF RATIO ANALYSIS:

1. Ratio computation is based on the financial statement of an organization. So, the ratios may not reflect the true and fair financial position if there are manipulation or window dressing in the basic data itself.

2. Ratio deals with quantitative aspects, hence does not reflect the qualitative aspects in its report.

3. Ratios are not decisions; it is the information to make effective decision.

4. Ratios are understandable by professional knowledge only; hence common people cannot use it.

5. Ratios are based on many assumptions and may mislead the decision maker’s.

5.

Seshadripuram academy of business studies. Page 19

in SBI

.

CHAPTER-2

RESEARCH DESIGN

Title of the study: A Study on Analysis of financial statement.

STATEMENT OF THE PROBLEM:

Financial statement reflects the financial position of any business. The primary aim of preparing financial statement is to make wise decision of the business. The financial efficiency managerial efficiency and probability can be justified with the help analysis of statement.

The focus of financial analysis on key figures in the financial statement and significant relationship that exist between them. The analysis of the financial statement is the process of evaluating the relationship between component part of financial statement to obtain a better understanding of the firms’ position and performance. In brief, financial analysis is the process of selection, relation evaluation.

Evaluated statement can be used as a tool to judge financial position operational efficiency profitability and managerial qualitative decision making power. The current study aims at ascertaining and analyzing the status of banks ability to meet its financial obligation performance.

OBJECTIVES:

1. To know overall operating efficiency and performance of bank.2. To analyses the financial statement of bank through past year.3. To determine the financial conditions and financial performance of the

bank.4. To know the process of utilization of funds.5. To through light on the areas where bank has to be more caution.

SCOPE OF THE STUDY: A detailed study on analysis of financial statement is highly the adequacy and optimum level of financial statement of bank.

1. Study on analysis of financial statement at STATE BANK OF INDIA is limited to a Raja Rajeshwari nagar only.

2. This study will be a source of information for further practical application of the bank.

Seshadripuram academy of business studies. Page 20

in SBI

3. The scope of the study comprises of various information from balance sheet and profit and loss account of bank for the 5 consecutive years.

LIMITATIONS:

1. A study is based on data provided by bank, truthfulness cannot be completely believed.2. Confidential data of bank are not revealed.3. Study is restricted only to past 5 years.

Nature of study:

The study is based on description and analytical study.

Tools:

Though there are many devices to analyze the financial statement ratio analysis, comparative financial statement analysis, common size statement and trend analysis are used.

Research instrument used:

Interpretation of the analyzed data computed using different statement is graphically represent through

Graphs. Tables.

Research Methodology:

Sources of Data: Primary source: The information is as it gathered from the personal interactions with the bank manager and accounting staffs of the bank.

Secondary sources: The study also done by using the following resources.

SBI Web site SBI Records Published articles Text books

Seshadripuram academy of business studies. Page 21

A Study on Analysis of Financial Statement

CHAPTER -3

COMPANY PROFILE

YEAR OF ESTABLISHMENT OF BRANCH: Bank has established in

30.7.1992 at Raja Rajeshwari nagar.

STATE BANK OF INDIA BRANCHES:

State bank of India branches span the country with a vast network to reach out to as many

customers as possible making full contribution to the status of India’s largest bank for SBI.

Each SBI branch is provided an identification code that is unique to each branch. The SBI

bank branches are categorized according to the banking services they provide.

These include SBI:

Core banking branch

Domestic Forex branch

Internet banking and

Personal banking (Real Time Gross Settlement) Branches.

State Bank of India being the largest bank provides specialized banking services in accordance

with the special requirement of a particular community or area. The SBI branch type there by

depends on the special banking services it aims to provide. These include:

Agricultural business and development branches

Commercial retail branches

Corporate accounts and mid corporate group branches

Main branches

Industrial finance branches

NRI banking branch

Seshadripuram academy of business studies. Page 22

A Study on Analysis of Financial Statement

Overseas branches

Personal banking branch

Rehabilitation and recovery branch

SSI and SIB branch

Services branches

VISION STATEMENT:

Premier India financial services group with global perspective, world class standing of

the efficiency and profession and core institution values

Retain its position in the country as a pioneer in developing countries.

Maximize shareholder value through high sustained earnings per share.

An institution with a culture of mutual care and commitment a satisfying and exciting.

Work environment and continuous learning opportunity.

MISSION STATEMENT:

To retain the banks position as the premise India financial services

Group with world class standards and significant global business commitment to

excellence in customer, shareholder and employee satisfaction and to play a leading role in the

expanding and diversifying financial services sector while continuing emphasis on its

development banking role.

VALUES:

Excellence in customer service

Profit orientation.

Belonging and commitment to the bank.

Seshadripuram academy of business studies. Page 23

A Study on Analysis of Financial Statement

Fairness in all dealing and relation.

Risk taking and innovation.

New business undertaking by SBI:

Due to completion from the private banks and in order to serve the customer’s needs as well

for the development of the economy state Banks of India has been entered into the new

market.

Recently SBI has started two new services providing area they are:

1. SBI LIFE INSURANCE

2. SBI MUTUAL FUNDS

3. SBI MEDICAL INSURANCE.

GOAL AND OBJECTIVES:

State Banks of India (SBI) is government-owned and is the largest banks in India it has its

own goal and objectives:

It traces its ancestry bank to the banks to Calcutta, which was established in 1806; this

makes SBI the oldest commercial banks in the Indian subcontinent.

SBI aims at providing regular services to its customer.

It aims at managing the nation’s largest ATM network.

SBI aims at providing various domestic, international and NRI products and services,

through its vast network in India and overseas for the sake of customer satisfaction.

In recent years the banks has focused on three priorities:

1. Reducing its huge staff through Golden handshake schemes know as the voluntary

Retirement scheme, which saw many of its best and brightest defect to the private sector.

2. Computerizing its operations.

Seshadripuram academy of business studies. Page 24

A Study on Analysis of Financial Statement

3. Trying to change the attitude of its largely rude staff through a program aptly named

‘parivartan’ or ‘change’.

SBI BRANCHES:

State Bank of India has 131 foreign offices in 32 countries across the globe.

SBI has about 21,000 ATMs; and SBI group (including associate banks) has about

45,000 ATMs.

SBI has 26,500 branches, including branches that belong to its associate banks.

SBI includes 99345 officers in our country.

SYMBOL AND SLOGAN:

The symbol of the State Bank of India is a circle and not key hole and a small man at

centre of the circle. A circle depicts perfection and the common man being the centre of the

bank’s business.

SLOGANS:

o With you all the way

o Pure banking nothing else

o The banker to every Indian

Trustees

SBI Mutual Fund Trustee Company Private Limited (the “Trustee”), through its Board of

Directors discharge its obligations as Trustee of the SBI Mutual Fund. The Board of Directors

of SBI Mutual Fund Trustee Company Private Limited are as under:

o Shri T.L. Palani Kumar

Independent

o Shri C.M. Dixit

Independent

Seshadripuram academy of business studies. Page 25

A Study on Analysis of Financial Statement

o Ms. Sandra Martyres

Associate

o Ms. Bharati Rao

Associate

Current Board of Directors

After the end of O. P. Bhatt's reign as SBI Chairman on 31st March, 2011, the post was taken

over by Pratip Chaudhuri, who is the former Deputy Managing Director of the International

Division of SBI. As on 4th August, 2011, there are twelve members in the SBI Board of

Directors, including Subir Gokarn, who is also one of the four Deputy Governors of the

Reserve Bank of India. The complete lists of the Board members are:

1. Pratip Chaudhuri (Chairman)

2. Hemant G. Contractor (Managing Director)

3. Diwakar Gupta (Managing Director)

4. A Krishna Kumar (Managing Director)

5. Dileep C Choksi (Director)

6. S. Venkatachalam (Director)

7. D. Sundaram (Director)

8. Parthasarathy Iyengar (Director)

9. G. D. Nadaf (Officer Employee Director)

10. Rashpal Malhotra (Director)

11. D. K. Mittal (Director)

12. Subir V. Gokarn (Director)

Associate banks:

Seshadripuram academy of business studies. Page 26

A Study on Analysis of Financial Statement

There are seven other associate banks that fall under SBI. They all use the and quote;

State Bank of India and quote; name followed by the regional headquarters name.

State Bank of Bikaner and Jaipur

State Bank of Hyderabad

State Bank of Indore

State banks of Mysore

State Bank of Patiala

State bank of Travancore

Seshadripuram academy of business studies. Page 27

A Study on Analysis of Financial Statement

The Main branch of SBI at Mumbai

Foreign offices:

State Banks of India is present in 32 countries, where it has 84 offices serving the

international needs of the bank’s foreign customers, and in some cases conducts retail

operations. The focus of these offices is India-related business.

SBI has branches in these countries:

Australia

Bahrain

Bangladesh

Belgium

Canada

Dubai

Seshadripuram academy of business studies. Page 28

A Study on Analysis of Financial Statement

France

Germany

Hong Kong

Japan

Israel

The Israeli branch of the State Bank of India located in Ramat Gan.

PRODUCTS:

Private Banking

Asset management

Pension

Mortgages

Credit Cards

State Bank of India- Financial and Strategic analysis review:

Summary:

Seshadripuram academy of business studies. Page 29

A Study on Analysis of Financial Statement

State bank of India (SBI) is a large financial services group operating in the banking industry.

The bank is engaged in providing trading services, international banking and traditional

banking and treasury operations. The Reserve bank of India holds more than half of SBI’s

equity capital. SBI has a network of over 10,000 branches. In addition, the seven associate

banks of SBI have more than 4900 branches. SBI along with its subsidiaries is engaged in

providing a wide range of financial services including Life Insurance, Merchant banking,

Mutual funds, credit card and factoring, security trading and primary dealership in the money

market.

Global Markets Direct, the leading business information provider, presents an in-depth

business, strategic and financial analysis of State Bank of India. The report provides a

comprehensive insight into the company, including business structure and operations,

executive biographies and key competitors. The hallmark of the report is the detailed strategic

analysis and Global Markets Directs views on the company

Scope:

-The company’s strengths and weaknesses and areas of development or decline are analyzed.

Financial, strategic and operation factors are considered.

-The opportunities open to the company are considered and its growth potential assessed

competitive or technological threats are highlighted.

-The report contains critical company information-business structure and operations, the

company history, major products and services, key competitors, key employees and executive

biographies, different locations and important subsidiaries.

-It provides detailed financial ratios for the past five years as well as interim ratios for the last

four quarters.

-Financial ratios include profitability, margins and returns, liquidity and leverage, financial

position and efficiency ratios.

PRODUCTS AND SERVICES:

Seshadripuram academy of business studies. Page 30

A Study on Analysis of Financial Statement

1. PERSONAL BANKING:

SBI Term deposits SBI loan for pensioners

SBI Recurring Deposits Loan Against Mortgage of Property

SBI Housing loan, Loan Against Share and Debentures

SBI Car Loan Rent Plus Scheme

SBI Educational loan Medi -Plus Scheme

2. NRI services

3. Agriculture/ Rural Banking

4. International Banking

5. Corporate Banking

6. Domestic Treasury

7. Services

8. Interest Rates

9. Safe Deposit Lockers

10. Other services:

ATM Services

Demat services

Internet Banking

Mobile banking

SME

RBIEFT

E-Pay

Seshadripuram academy of business studies. Page 31

A Study on Analysis of Financial Statement

E- Rail

SBI Vishwa yatra foreign Travel Card

Broking Services

Gift Cheques

New products and services:

Apart from restructuring, SBI launched several innovation, value-added products and

services to project a customer friendly image. It launched a special service for corporate

customers called ‘tele banking and remote login’ to support transactional requests.

SCHEMES:

Now new schemes introduced by State Bank of India are:

Equity Scheme

Debt Scheme

Balanced Scheme

Exchange Traded Scheme.

WORK FORCE STRENGTH:

Main Branch strength:

SBI through the central Reserve Bank of India-also operates the world’s largest network, with

more than 13,500 branch offices throughout India, staffed by nearly 2,20,000 employees.

Principal Competitors:

ICICI Bank

Vijaya bank

Seshadripuram academy of business studies. Page 32

A Study on Analysis of Financial Statement

Bank of Baroda

Canara Bank

Punjab National Bank

Bank of India

Union Bank of India

Central Bank of India

HDFC Bank

Oriental Bank of Commerce

SOCIAL RESPONSIBILITY:

SBI branch:

1. SBI provides loan to weaker sections.

2. It provides Home Loan, vehicle Loan, personal Loan, and Educational Loan.

State Bank of India: SBI has taken an initiative to encourage commercial workers to save their

earning. This project was implemented in sonagachi, one of Asia’s largest red light areas,

where residents were encouraged to open a saving bank (SBI) account. While this can be

called a social service, it also reflects a sharp business sense.

Awards

Seshadripuram academy of business studies. Page 33

A Study on Analysis of Financial Statement

At SBI Funds Management, we devote considerable resources to gain, maintain and sustain

our profitable insights into market movements. The trust reposed on us by millions of

investors is a genuine tribute to our expertise in Fund Management and dedication to our

singular focus. And this has resulted in various awards and accolades for us from the fund

industry, motivating us to do better. Some of the awards won by us are listed below.

2011

Readers Digest Awards 2011 for Trusted Brand in Fund Management Category

ICRA Mutual Fund Awards 2011 for Magnum Income Fund - Floating Rate Plan - Long Term

Plan

2010

ICRA Mutual Fund Awards 2010 for Magnum Global Fund

2009

ICRA Mutual Funds Awards 2009 for Magnum Tax Gain Scheme 1993

The Lipper India Fund Awards 2009 for Various Schemes

2008

Outlook Money NDTV Profit Awards 2008

The Lipper India Fund Awards 2008 for Magnum Balanced Fund – Dividend

ICRA Mutual Fund Awards 2008 for Various Schemes

2007

Seshadripuram academy of business studies. Page 34

A Study on Analysis of Financial Statement

Outlook Money NDTV Profit Awards 2007

CNBC Awaaz Consumer Awards 2007

The Lipper India Fund Awards 2007 for Various Schemes

ICRA Mutual Funds Awards 2007 for Various Schemes

CNBC TV18 - CRISIL Mutual Fund of the Year Award 2007 for Various Schemes

CHAPTER -4

Data Analysis and Interpretation

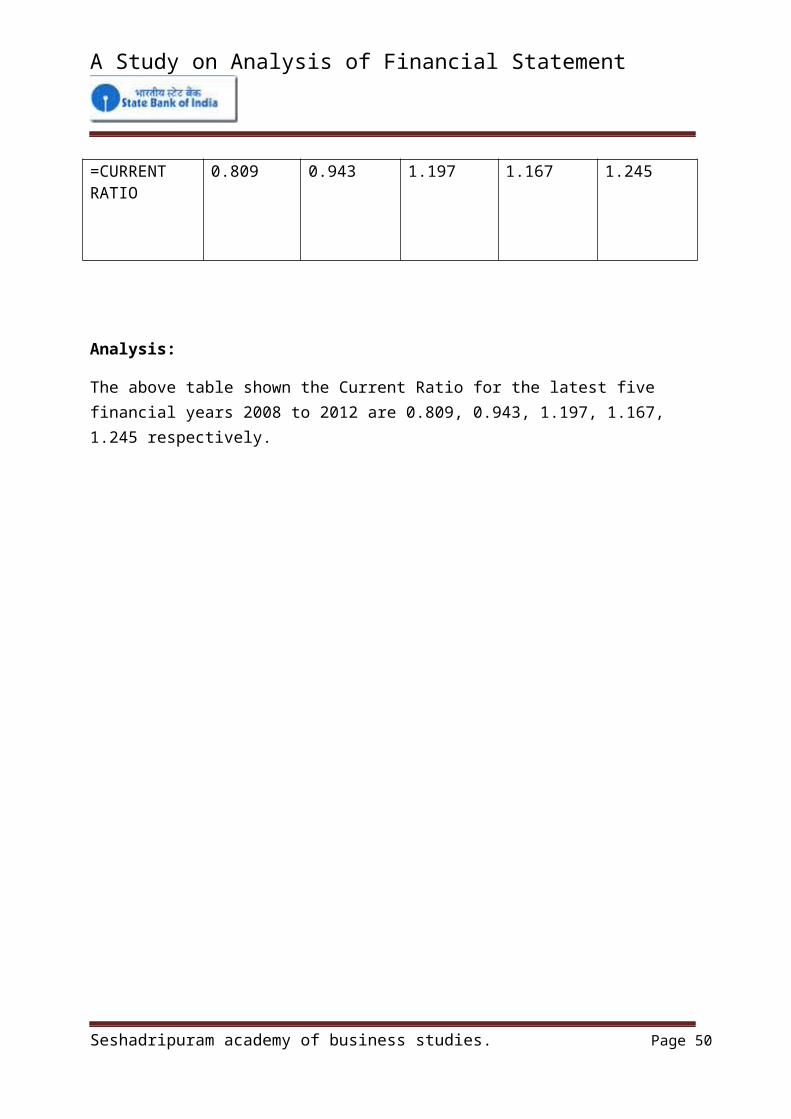

Table no: 4.1 CURRENT RATIO=CURRENT ASSETS/CURRENT LIABILITIES

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

CURRENT ASSETS

67466.34 104403.80 96183.11 122874.15 143365.10

/CURRENT LIABILITIES

83362.30 110697.57 80336.70 105248.39 115083.80

=CURRENT RATIO

0.809 0.943 1.197 1.167 1.245

Seshadripuram academy of business studies. Page 35

A Study on Analysis of Financial Statement

Analysis:

The above table shown the Current Ratio for the latest five financial years 2008 to 2012 are 0.809, 0.943, 1.197, 1.167, 1.245 respectively.

2007-2008 2008-2009 2009-2010 2010-2011 2011-20120

0.2

0.4

0.6

0.8

1

1.2

1.4

GRAPH 4.1 SHOWING THE CURRENT RATIO

CURRENT RATIO

years

in cro

res

Interpretation: From the above graph we can interpret that, in 2008 to 2010 slightly increases in the position of current ratio of the bank, where as in 2011 and 2012 fluctuate.

Seshadripuram academy of business studies. Page 36

A Study on Analysis of Financial Statement

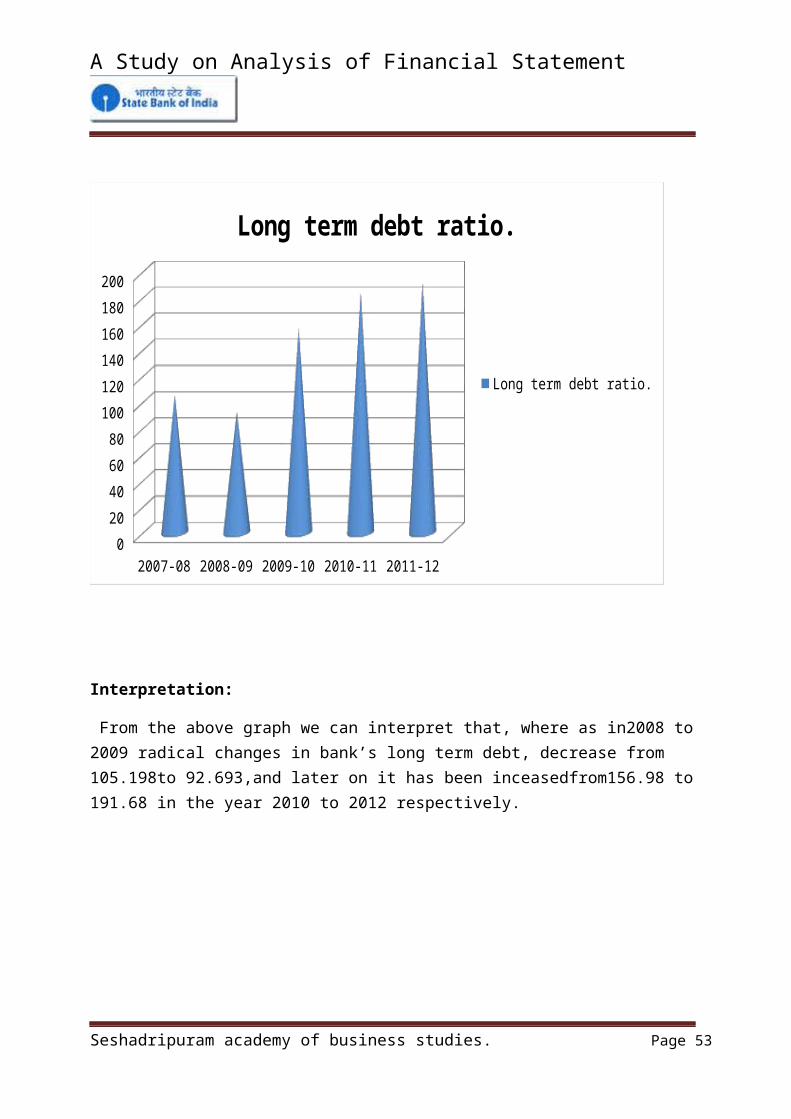

Table no:4.2 RATIO OF LONG TERM DEBTS=FUND DEBT (LONG TERM LIABILITIES)*100/TOTAL CAPITATION

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

FUNDED DEBTS

51727.41 53713.68 103011.60 119568.96 126607.61

/TOTAL CAPITATION

49032.66 57947.70 65949.20 64986.04 66048.30

=LONG TERM DEBT RATIO

105.49 92.69 156.19 183.99 191.68

Analysis: The above table shown that the long term debt ratio is 105.49, 92.69, 156.19, 183.99and191.68 respectively.

Seshadripuram academy of business studies. Page 37

A Study on Analysis of Financial Statement

2007-08 2008-09 2009-10 2010-11 2011-120

20

40

60

80

100

120

140

160

180

200

Long term debt ratio.

Long term debt ratio.

Interpretation:

From the above graph we can interpret that, where as in2008 to 2009 radical changes in bank’s long term debt, decrease from 105.198to 92.693,and later on it has been inceasedfrom156.98 to 191.68 in the year 2010 to 2012 respectively.

Seshadripuram academy of business studies. Page 38

A Study on Analysis of Financial Statement

Table no 4.3 RATIO OF CURRENT ASSETS=CURRENT ASSETS/PROPREITORY FUNDS

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010

2010-2011 2011-2012

CURRENT ASSETS

67466.34 104403.80 96183.85 122874.15 132508.50

PROPREITORY FUND

631.47 634.88 634.88 635.00 671.04

=RATIO OF CURRENT ASSETS

106.840 164.446 151.499 193.502 197.467

Analysis:

The above table shown the ratio of Current Asset for the last five financial years 2008to 2012 are 106.840, 164.446, 151.499, 193.502, 197.467.respectively.

Seshadripuram academy of business studies. Page 39

A Study on Analysis of Financial Statement

2007-2008

2008-2009

2009-2010

201 0-2011

2011-2012

0

50

100

150

200

250

4.3 GRAPH SHOWING RATIO OF CURRENT ASSETS

RATIO OF CURRENT ASSETS

years

in cr

ores

Interpretation:

From the above analysis we observe that the ratio of Current Assets has been increased in the year 2008 to 2009,106.840 to164.446 , it again decreased in 2010,here it has decreased to 151.499.againit has increased in 2011to 2012, from 193.502 to 197.467 respectively.

Seshadripuram academy of business studies. Page 40

A Study on Analysis of Financial Statement

Table no: 4.4 EQUITY OR PROPREITORY RATIO=SHARE HOLDER’S FUND/TOTAL ASSETS

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

SHARE HOLDER’S FUND

631.47 634.88 634.88 635.00 671.04

/TOTAL ASSETS

721526.32 964432.08 1053413.74 1223736.20 1335519.22

=EQUITY RATIO

0.0008 0.0006 0.0006 0.0005 0.0005

Analysis:

The above table shown the equity ratio for the latest five financial year 2008 to 2012 are 0.0008, 0.0006, 0.0006, 0.0005, 0.0005 respectively.

Seshadripuram academy of business studies. Page 41

A Study on Analysis of Financial Statement

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

0

0.0001

0.0002

0.0003

0.0004

0.0005

0.0006

0.0007

0.0008

0.0009

4.4 GRAPH SHOWING OF EQUITY RATIO

EQUITY RATIO

years

in cr

ores

Interpretation:

The efficiency of equity ratio decreased in 2008 to 2010, but in the year 2010 to 2012 it is 0.0005, in the same ratio position.

Seshadripuram academy of business studies. Page 42

A Study on Analysis of Financial Statement

4.5 SOLVENCY RATIO=TOTAL LIABILITIES-SHARE HOLDERS FUND/TOTAL ASSET

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

TOTAL LIABILITIES

721526.31 964432.08 1053413.73 1223736.20 1335519.22

-SHARE HOLDER’SFUND

631.47 634.88 634.88 635.00 671.04

/TOTAL ASSET 721526.32 964432.08 1053413.74 1223736.20 1335519.24

=SOLVENCY RATIO

0.9991 0.9993 0.9993 0.9994 0.9994

Analysis: The above table shown the Solvency Ratio is 0.9991, 0.9993, 0.9993, 0.9994, 0.9994 in the year 2008 to 2012 respectively.

Seshadripuram academy of business studies. Page 43

A Study on Analysis of Financial Statement

2007-2008 2008-2009 2009-2010 2010-2011 2011-20120.99895

0.999

0.99905

0.9991

0.99915

0.9992

0.99925

0.9993

0.99935

0.9994

4.5 GRAPH SHOWING THE SOLVENCY RATIO

SOLVENCY RATIO

years

in cr

ores

Interpretation: From the above graph we can identify that the bank has experienced the increased trend in solvency ratio from 2008 to 2012. Solvency ratio in the year 2009 is continued till the year 2010 as 0.9993.

Seshadripuram academy of business studies. Page 44

A Study on Analysis of Financial Statement

4.6 CURRENT ASSET TO TOTAL ASSET=CURRENT ASSET/TOTAL ASSET

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

CURRENT ASSET/

67466.34 104403.80 96183.11 122874.15 132508.50

TOTAL ASSET 721526.32 964432.8 1053413.74 12237620 1335519.24

=CURRENT ASSET TO TOTAL ASSET

0.0935 0.108 0.0913 0.0100 0.0992

Analysis: The above table shows the current asset to total asset is increase to year to year, but in 2011-2012 slitely decrease. It shows as follows 0.0935, 0.108, 0.0913, 0.0100, and 0.0992 respectively.

Seshadripuram academy of business studies. Page 45

A Study on Analysis of Financial Statement

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

0.08

0.085

0.09

0.095

0.1

0.105

0.11

4.6 GRAPH SHOWING CURRENT ASSET TO TOTAL ASSET

CURRENT ASSET TO TOTAL ASSET

years

in cro

res

Interpretation: the above graph shows current asset to total asset, it is fluctuating in compare to 2009- 2010 and fluctuates year to year.

Seshadripuram academy of business studies. Page 46

A Study on Analysis of Financial Statement

4.7 PRICE EARNING RATIO=RESERVES AND SURPLUS+EQUITY SHARE HOLDER/PREFERANCE SHARE

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

RESERVES AND SURPLUS+

48401.19 57312.82 65314.32 64351.04 83951.20

EQUITY SHARE HOLDER/

631.47 634.88 634.88 635 671.04

PREFERANCE SHARE

51727.41 53713.68 103011.60 119568.96 120840.68

=PRICE EARNING RATIO

0.947 1.078 0.640 0.543 0.700

Analysis: the price earnings ratio is 0.947, 1.078, 0.640, 0.543, and 0.700 for the year 2008 to 2012 respectively.

Seshadripuram academy of business studies. Page 47

A Study on Analysis of Financial Statement

2007-2008 2008-2009 2009-2010 2010-2011 2011-20120

0.2

0.4

0.6

0.8

1

1.2

4.7 GRAPH SHOWING OF PRICE EARNING RATIO(In crores)

PRICE EARNING RATIO

years

in cr

ores

Interpretation: The above graph shown in the year 2008 price earnings ratio has been increased from ,0.947 to1.078 but in the year 2010to 2012 suddenly it was decreased.

Seshadripuram academy of business studies. Page 48

A Study on Analysis of Financial Statement

4.8 EARNING PER SHARE=NET PROFIT AFTER TAX+PREFERANCE DIVIDEND/NUMBER OF EQUITY SHARE. In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

NET PROFIT AFTER TAX+

6729.12 9121.23 9166.05 7370.35 11686.01

PREFERANCE DIVIDEND/

00 00 00 00 00

NUMBER OF EQUITY SHARE

631.47 634.88 634.88 635 671.04

=EARNING PER SHARE(in crores)

10.656 14.366 14.437 11.606 17.414

Analysis: The price earnings ratio is10.656, 14.366, 14.437, 11.606, 17.414 for the year 2008 to 2012 respectively.

Seshadripuram academy of business studies. Page 49

A Study on Analysis of Financial Statement

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

02468

1012141618

4.8 GRAPH SHOWING EARNING SHARE

EARNING PER SHARE(In crores)

years

in cr

ores

Interpretation: The above graph indicates the increased trend in earnings per share ratio year to year, but in the year 2011there is slightly decreased in earning per share ratio.

Seshadripuram academy of business studies. Page 50

A Study on Analysis of Financial Statement

4.9 DEBT EQUITY RATIO=OUT SIDER’S FUND (BORROWING)/SHARE HOLDER FUND

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

OUT SIDER’S FUND(BORROWING)

537403.94 742073.13 804116.26 933932.81 1043647.36

/SHARE HOLDERS FUND

631.47 634.88 634.88 635 671.04

=DEBT EQUITY RATIO

851.036 1168.839 1266.56 1470.760 1555.268

Analysis: The above table shows the debt equity ratio, it is increase year to year, likes 851.036, 1168.839, 1266.56, 1470.760, and 1555.268, respectively.

Seshadripuram academy of business studies. Page 51

A Study on Analysis of Financial Statement

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

0

200

400

600

800

1000

1200

1400

1600

4.9 GRAPH SHOWING DEBT EQUITY RATIO

4.9 GRAPH SHOWING DEBT EQUITY RATIO(In crores)

years

In cro

res

Interpretation: This graph shows the debt equity ratio, it is shown that it is increase year to year. The bank has good position in debt equity ratio.

Seshadripuram academy of business studies. Page 52

A Study on Analysis of Financial Statement

4.10 CURRENT LIABILITIES TO NET WORTH RATIO=CURRENT LIABILITIES/NET WORTH.

In crores

PARTICULAR 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012

CURRENT LIABILITIES

83362.30 110697.57 80336.70 105248.39 115083.80

/NET WORTH 83951.20 64986.04 65949.20 57947.70 49032.66

=CURRENT LIABILITIES TO NET WORTH RATIO

0.992 1.703 1.218 1.816 2.347

Analysis: The above table shows that current liabilities to net worth ratio, it is slightly increase year to year, but in 2009 decrease. It shows as 0.992, 1.703, 1.218, 1.816, and 2.347 respectively.

Seshadripuram academy of business studies. Page 53

A Study on Analysis of Financial Statement

2007-2008 2008-2009 2009-2010 2010-2011 2011-20120

0.5

1

1.5

2

2.5

4.10 GRAPH SHOWING CURRENT LIABILITIES TO NET WORTH RATIO

years

in cro

res

Interpretation: The above graph shows the current liabilities to net worth ratio it fluctuate year to year.

Seshadripuram academy of business studies. Page 54

A Study on Analysis of Financial Statement

Table 4.11 shows TREND ANALYSIS OF 2008-2009.

PARTICULAR 2007-2008 (base year)

2008-2009 (current year)

Changes in percentage.% (Base year)

Changes in percentage. %(current year)

Assets1. Cash and balance with RBI.

51534.62 55546.17 100% 107.7%

2. Balance with banks, money at call.

15931.72 48857.63 100% 306.6%

3.Advances 416768.20 542503.20 100% 130.1%4.Investment 189501.27 275953.96 100% 145.6%5.Net block 3139.22 3574.41 100% 113.8%6.Capital working progress

234.26 263.44 100% 112.4%

7.Other assets 44417.03 37733.27 100% 84.9%8. Total assets 721526.32 964432.08 100% 133.6%CapitalandLiabilities1.Equity share capital

631.47 634.88 100% 100.5%

2.Reserves 48401.19 57312.82 100% 118.4%3.Net worth 49032.66 57947.70 100% 118.1%Long term Liabilities1.Deposits 537403.94 742073.13 100% 138.08%2.Borrowings 51727.41 53713.68 100% 103.85%3.Total debts 589131.35 795786.81 100% 135.0%4.Other Liabilities and provision

83362.30 110697.57 100% 132.7%

5.Total liabilities 721526.31 964432.08 100% 133.6%

Analysis:

Seshadripuram academy of business studies. Page 55

A Study on Analysis of Financial Statement

The cash and balance with RBI have been increased by 107.7%in the year 2009.

The money at call has been increased by 306.6% in the current year compare to base year.

The advances have been increased by 130.1% in year of 2009.

The investments of the bank have been increased by145.6% in the year 2009.

The net block balance of the bond has been slightly increased by 113.8% in the year 2009.

Capital work in progress has radically increased by112.4% in the year 2009.

Other assets have been decrease by 84.9% in the current year compare to base year.

The reserves have been increased by 118.4%in the year 2009.

The deposits have been increased by 138.08% in the year of 2009.

The borrowings of the bank have been increased by 103.85% in the year 2009.

The net block has been increased by 113.8% in the current year.

Equity shares have been increased by 100.5% in the current year.

Net worth has been increased by 118.1% in the year 2009.

Seshadripuram academy of business studies. Page 56

A Study on Analysis of Financial Statement

Cash and balance w

ith RBI

Balance w

ith banks, money a

t call

AdvancesNet b

lock

Capital workin

g progressInvest

ment

Other asset

s

Total asset

s

Equity share

capitalReserves

Net worth

Deposits

Borrowings

Total debts

Other liabilities

Total liabilitis

0

100

200

300

4.11 GRAPH SHOWING TREND ANALYSIS 2008 TO 2009.

4.11 GRAPH SHOWING TREND ANALYSIS 2008 TO 2009.

Seshadripuram academy of business studies. Page 57

A Study on Analysis of Financial Statement

Interpretation:

The Trend analysis of the financial statement made between the year 2008 and 2009, where 2008 has taken as base year.

The trend analysis financial statement analyzed clearly shows that the position of the statement in the year 2009.

The total assets have been increased in the year 2009, by 133.6%

The net worth has been increased by 118.1% in the current year compare to base year.

The total debts have been increased by 135% in the year 2009.

The other liabilities of the bank has been increased by 132.7%

The total liability of the bank has also been increased by 133.6% in the year 2009 as compare to that of 2008 as base year.

Seshadripuram academy of business studies. Page 58

A Study on Analysis of Financial Statement

Table 4.12 shows TREND ANALYSIS OF 2009-2010

PARTICULAR 2007-2008 (base year)

2009-2010 (current year)

Changes in percentage.% (Base year)

Changes in percentage% (current year)

Assets1. Cash and balance with RBI.

51534.62 61290.87 100% 118.9%

2. Balance with banks, money at call.

15931.72 34892.98 100% 219%

3.Advances 416768.20 631914.15 100% 151.6%4.Investment 189501.27 285790.07 100% 150.8%5.Net block 3139.22 4117.73 100% 131.1%6.Capital working progress

234.26 295.18 100% 126%

7.Other assets 44417.03 35112.76 100% 79.05%8. Total assets 721526.32 1053413.74 100% 145.9%Capital and Liabilities1.Equity share capital

631.47 634.88 100% 100.5%

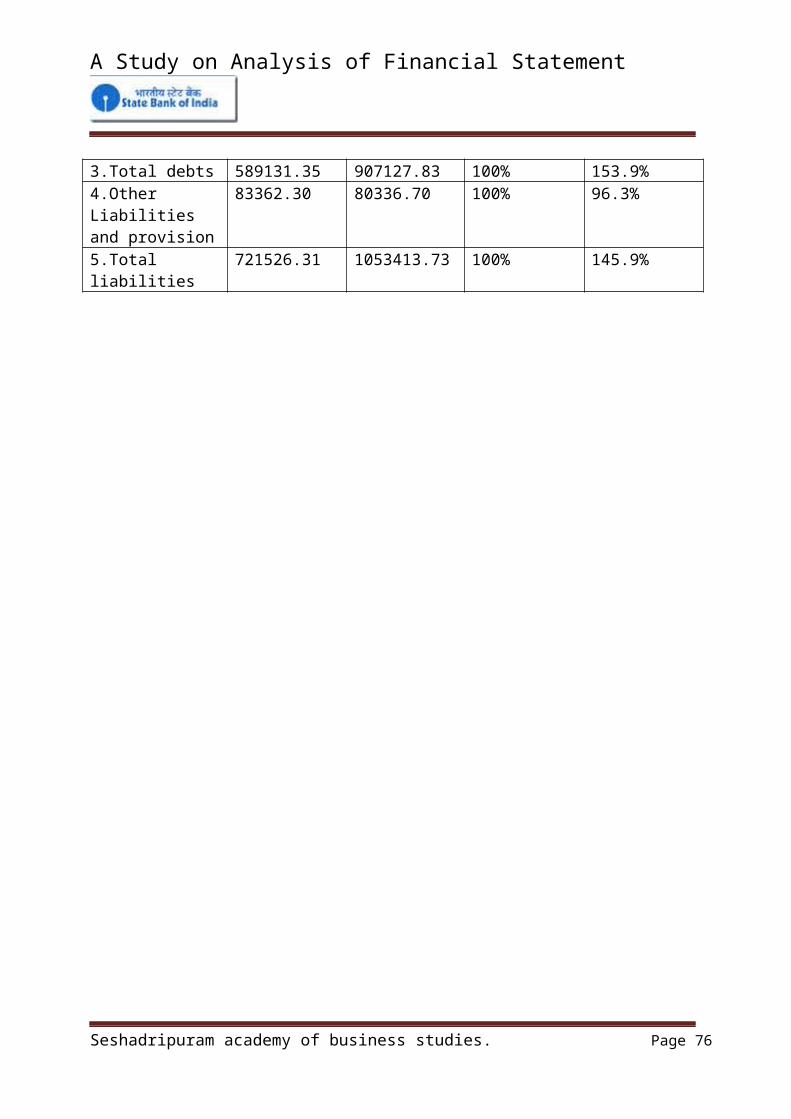

2.Reserves 48401.19 65314.32 100% 134.9%3.Net worth 49032.66 65949.20 100% 134.5%Long term Liabilities1.Deposits 537403.94 804116.23 100% 149.6%2.Borrowings 51727.41 103011.60 100% 199.1%3.Total debts 589131.35 907127.83 100% 153.9%4.Other Liabilities and provision

83362.30 80336.70 100% 96.3%

5.Total liabilities 721526.31 1053413.73 100% 145.9%

Seshadripuram academy of business studies. Page 59

A Study on Analysis of Financial Statement

Analysis:

The cash and balance with RBI have been increased by 118.9%in the year 2010.

The money at call has been increased by 219% in the current year compare to base year.

The advances have been increased by 151.1% in year of 2010.

The investments of the bank have been increased by150.8% in the year 2010.

The net block balance of the bond has been slightly increased by 131.1% in the year 2010.

Capital work in progress has radically increased by126% in the year 2010.

Other assets have been decrease by 79.05% in the current year compare to base year.

The reserves have been increased by 134.9%in the year 2010.

The deposits have been increased by 149.6% in the year of 2010.

The borrowings of the bank have been increased by 199.1% in the year 2010.

The net block has been increased by 134.4% in the current year.

Equity shares have been increased by 100.5% in the current year.

Net worth has been increased by 118.9% in the year 2010.

Seshadripuram academy of business studies. Page 60

A Study on Analysis of Financial Statement

Cash and balance w

ith RBI

Balance w

ith banks, money at

call

Advances

Investments

Capital work in

progressOther as

setsTotal a

ssets

Equity share c

apitalReser

ves

Net worth

Deposits

BorrowingsTotal d

ebts

Other Liabilities

Total liabilitiesNet block

0

50

100

150

200

250

4.12 GRAPH SHOWS TREND ANALYSIS OF 2009-2010

Seshadripuram academy of business studies. Page 61

A Study on Analysis of Financial Statement

Interpretation:

The Trend analysis of the financial statement made between the year 2008 and 2010, where 2008 has taken as base year.

The trend analysis financial statement analyzed clearly shows that the position of the statement in the year 2010.

The total assets have been increased in the year 2010, by 145.5%

The net worth has been increased by 134.5% in the current year compare to base year.

The total debts have been increased by 153.9% in the year 2010.

The other liabilities of the bank has been increased by 196.3%

The total liability of the bank has also been increased by 145.9% in the year 2010 as compare to that of 2008 as base year.

Seshadripuram academy of business studies. Page 62

A Study on Analysis of Financial Statement

4.13 TABLE SHOWS TREND ANALYSIS OF 2010-2011

PARTICULAR 2007-2008 (Base year)

2010-2011 (Current year)

Changes in percentage.% (Base year)

Changes in percentage%(current year)

Assets1. Cash and balance with RBI.

51534.62 94395.5 100% 183.1%

2. Balance with banks, money at call.

15931.72 28478.65 100% 178.7%

3.Advances 416768.20 756719.45 100% 181.1%

4.Investment 189501.27 295600.57 100% 155.9%

5.Net block 3139.22 4413.95 100% 140.6%6.Capital working progress

234.26 332.23 100% 141.8%

7.Other assets 44417.03 43777.85 100% 98.5%

8. Total assets 721526.32 1223736.20 100% 169.6%

Capital and Liabilities

1.Equity share capital 631.47 635 100% 100.5%

2.Reserves 48401.19 64351.04 100% 132.9%

3.Net worth 49032.66 64986.04 100% 132.5%

Long term Liabilities1.Deposits 537403.94 933932.81 100% 173.7%

2.Borrowings 51727.41 119568.96 100% 231.1

3.Total debts 589131.35 1053501.77 100% 178.8%

4.Other Liabilities and provision

83362.30 105248.39 100% 126.6%

5.Total liabilities 721526.31 1223736.20 100% 169.6%

Seshadripuram academy of business studies. Page 63

A Study on Analysis of Financial Statement

Analysis:

The cash and balance with RBI have been increased by 183.1%in the year 2011.

The money at call has been increased by 178.7% in the current year compare to base year.

The advances have been increased by 181.1% in year of 2011.

The investments of the bank have been increased by155.5% in the year 2011.

The net block balance of the bond has been slightly increased by 140.6% in the year 2011.

Capital work in progress has radically increased by141.8% in the year 2011.

Other assets have been decrease by 98.5% in the current year compare to base year.

The reserves have been increased by 132.9%in the year 2011.

The deposits have been increased by 173.7% in the year of 2011.

The borrowings of the bank have been increased by 231.1% in the year 2011.

The net block has been increased by 140.6% in the current year.

Equity shares have been increased by 100.5% in the current year.

Net worth has been increased by 132.5% in the year 2011.

Seshadripuram academy of business studies. Page 64

A Study on Analysis of Financial Statement

Cash and balance w

ith RBI

Balance w

ith banks, money a

t callAdvances

Invest ment

Net block

Capital work in

progressOther a

ssets

Total asset

s

Equity share

capitalReserves

Net worth

Deposits

Borrowings

Total debts

Other Liabilities a

nd provisionTotal li

abilities

0

50

100

150

200

250

4.13 GRAPH SHOWS TREND ANALYSIS OF 2010-2011

Seshadripuram academy of business studies. Page 65

A Study on Analysis of Financial Statement

Interpretation:

The Trend analysis of the financial statement made between the year 2008 and 2011, where 2008 has taken as base year.

The trend analysis financial statement analyzed clearly shows that the position of the statement in the year 2011.

The total assets have been increased in the year 2011, by 169.6%

The net worth has been increased by 132.5% in the current year compare to base year.

The total debts have been increased by 178.8% in the year 2011.

The other liabilities of the bank has been increased by 126.6%

The total liability of the bank has also been increased by 169.6% in the year 2011 as compare to that of 2008 as base year.

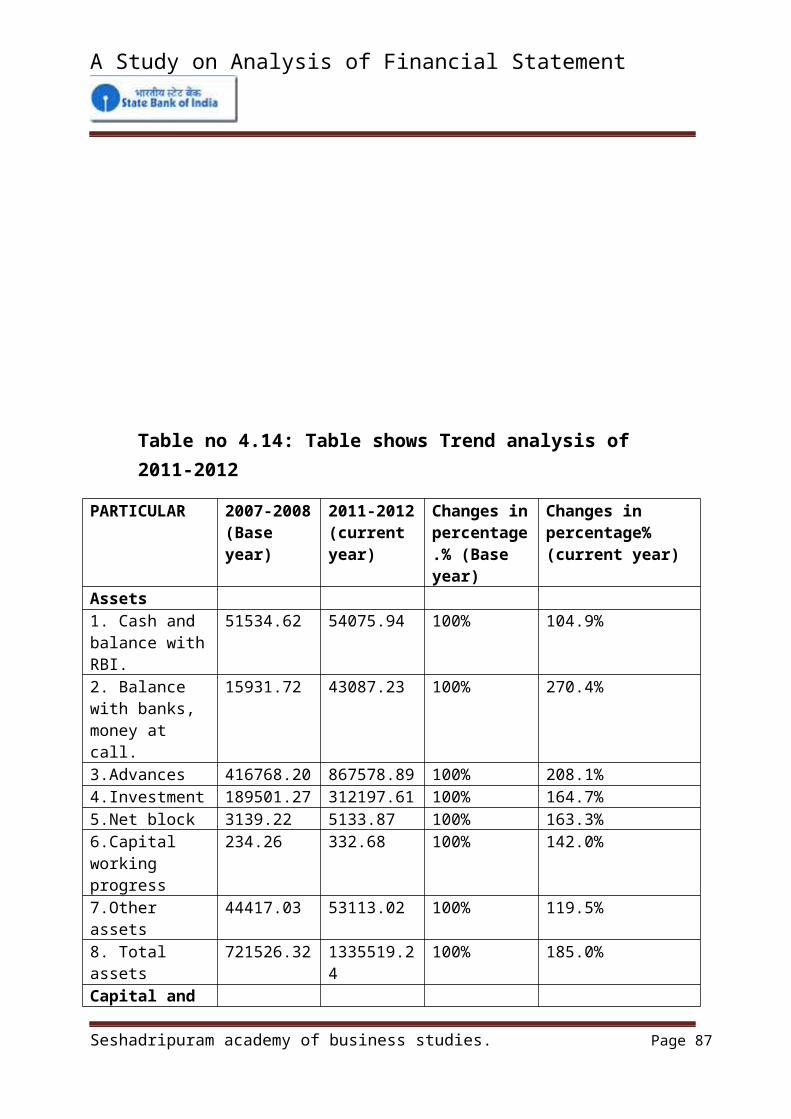

Table no 4.14: Table shows Trend analysis of 2011-2012

Seshadripuram academy of business studies. Page 66

A Study on Analysis of Financial Statement

PARTICULAR 2007-2008 (Base year)

2011-2012 (current year)

Changes in percentage.% (Base year)

Changes in percentage%(current year)

Assets1. Cash and balance with RBI.

51534.62 54075.94 100% 104.9%

2. Balance with banks, money at call.

15931.72 43087.23 100% 270.4%

3.Advances 416768.20 867578.89 100% 208.1%4.Investment 189501.27 312197.61 100% 164.7%5.Net block 3139.22 5133.87 100% 163.3%6.Capital working progress

234.26 332.68 100% 142.0%

7.Other assets 44417.03 53113.02 100% 119.5%8. Total assets 721526.32 1335519.24 100% 185.0%

Capital and Liabilities1.Equity share capital

631.47 671.04 100% 106.2%

2.Reserves 48401.19 83280.16 100% 172.0%

3.Net worth 49032.66 83951.20 100% 171.2%

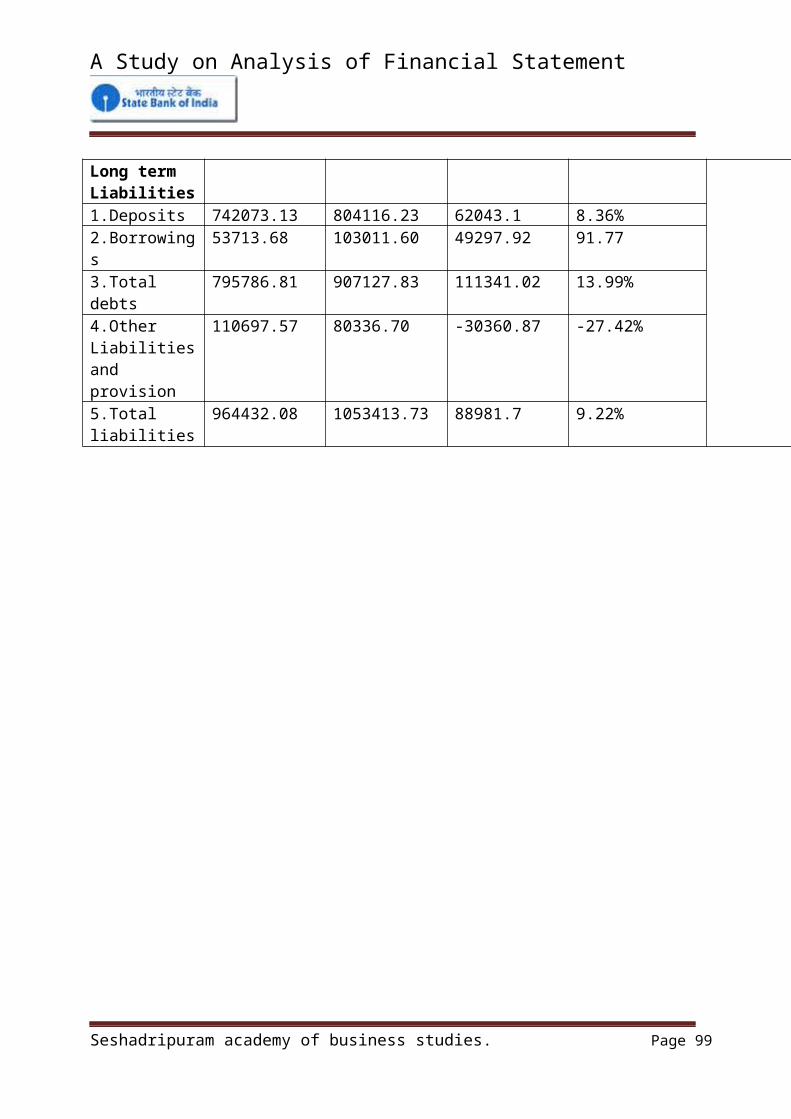

Long term Liabilities1.Deposits 537403.94 1043647.36 100% 194.2%

2.Borrowings 51727.41 127005.57 100% 245.5%

3.Total debts 589131.35 1170652.93 100% 198.7%

4.Other Liabilities and provision

83362.30 80915.09 100% 97.0%

5.Total liabilities 721526.31 1335519.22 100% 185.0%

Seshadripuram academy of business studies. Page 67

A Study on Analysis of Financial Statement

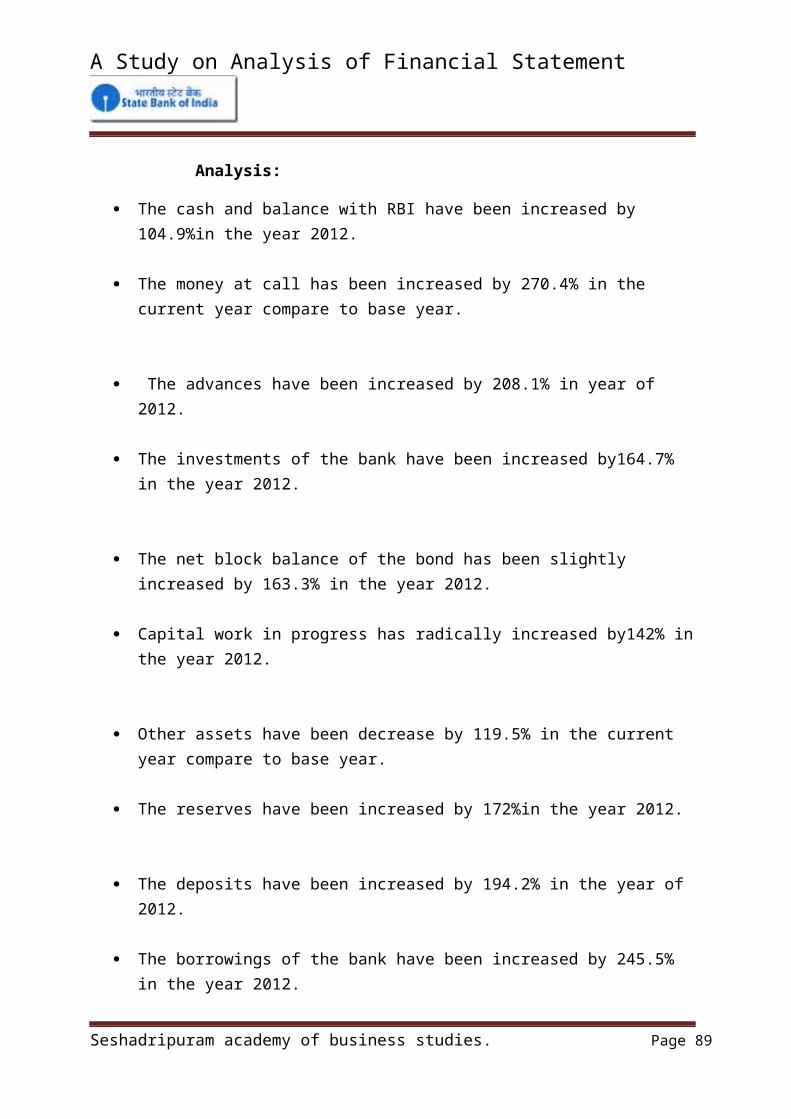

Analysis:

The cash and balance with RBI have been increased by 104.9%in the year 2012.

The money at call has been increased by 270.4% in the current year compare to base year.

The advances have been increased by 208.1% in year of 2012.

The investments of the bank have been increased by164.7% in the year 2012.

The net block balance of the bond has been slightly increased by 163.3% in the year 2012.

Capital work in progress has radically increased by142% in the year 2012.

Other assets have been decrease by 119.5% in the current year compare to base year.

The reserves have been increased by 172%in the year 2012.

The deposits have been increased by 194.2% in the year of 2012.

The borrowings of the bank have been increased by 245.5% in the year 2012.

The net block has been increased by 163.3% in the current year.

Equity shares have been increased by 106.2% in the current year.

Net worth has been increased by 171.2% in the year 2012.

Seshadripuram academy of business studies. Page 68

A Study on Analysis of Financial Statement

Cash and balance w

ith RBI

Balance w

ith banks, money a

t call

Advances

Investment

Net block

Capital work in

progressOther a

ssets

Total asset

s

Equity share

capitalReserves

Net worth

Deposits

Borrowings

Total debts

Other Liabilities a

nd provisionTotal li

abilities

0.00%50.00%

100.00%150.00%200.00%250.00%300.00%

4.14 GRAPH SHOWS TREND ANALYSIS OF 2011-2012

Seshadripuram academy of business studies. Page 69

A Study on Analysis of Financial Statement

Interpretation:

The Trend analysis of the financial statement made between the year 2008 and 2012, where 2008 has taken as base year.

The trend analysis financial statement analyzed clearly shows that the position of the statement in the year 2012.

The total assets have been increased in the year 2012, by 185%

The net worth has been increased by 171.2% in the current year compare to base year.

The total debts have been increased by 198.7% in the year 2012.

The other liabilities of the bank has been increased by 97.00%

The total liability of the bank has also been increased by 185% in the year 2012 as compare to that of 2008 as base year.

Seshadripuram academy of business studies. Page 70

A Study on Analysis of Financial Statement

4.15 Table shows: COMPARATIVE FINANCIAL STATEMENT ANALYSIS.

Particular 2008 2009 Increase/decrease in (rs)

Increase/decrease in(%)

Assets1. Cash and balance with RBI.

51534.62 55546.17 4011.55 7.78%

2. Balance with banks, money at call.

15931.72 48857.63 32926.06 206.66%

3.Advances 416768.20 542503.20 12735 30.16%4.Investment 189501.27 275953.96 86452.69 45.62%5.Net block 3139.22 3574.41 435.19 13.86%6.Capital work in progress

234.26 263.44 29.18 12.45%

7.Other assets 44417.03 37733.27 -6684.03 -15.04%8. Total assets 721526.32 964432.08 242905.76 33.66%Capital and Liabilities1.Equity share capital

631.47 634.88 3.41 0.54%

2.Reserves 48401.19 57312.82 8911.63 18.41%3.Net worth 49032.66 57947.70 8915.04 18.18%Long term Liabilities1.Deposits 537403.94 742073.13 204669.19 38.08%2.Borrowings 51727.41 53713.68 1986.27 3.83%3.Total debts 589131.35 795786.81 206655.46 35.07%4.Other Liabilities and provision

83362.30 110697.57 27335.27 32.79%

5.Total liabilities

721526.31 964432.08 242905.77 33.66%

Seshadripuram academy of business studies. Page 71

A Study on Analysis of Financial Statement

Analysis:

The cash and balance with RBI have been increased 7.78% in the year 2008 The money at call have been increased by 206.6% in the year 2009 The advances have been increased by 30.16 %in the year 2009 The investment of the bank have been increased by 45.62% in the year 2009 Capital work in progress has radically increased by 12.45% when compared to

past year Other assets have also been decreased -15.04% The equity share capital have been increased by 054% in the year 2008 and

2009 The reserves have been increased by 18.41% in the year 2009 The net block balance of the bank has been slightly increased by 38.08% in the

year 2009 The borrowings of the bank has also been increased by 3.83 % in the year 2009

as compared with that of 2008

Interpretation: