Embed Size (px)

Citation preview

1

Spread of Self Help Group (SHG) movement in Haryana (An Indian State):

Review of developments and way forward1

Abstract

The SHGs have proved to be very successful instrument of economic development,

women empowerment and social change in the southern states of India over the

last two and half decades. The SHG movement has connected millions of poor

people, especially women, to the financial and banking services and more

importantly created healthy financial habits like savings, inter-lending, loaning

besides unleashing entrepreneurial talent and livelihood activities. However, the

states in the Northern part of India, especially Haryana, seem to have remained

largely untouched with this movement. This paper shows that relatively lower

poverty in the state cannot be the main reason for the poor take-off of this

movement. Analyzing the survey results conducted in four select districts of

Haryana, the paper throws light on unique socio-economic dynamics prevailing in

the state which mostly restricts the SHG movement in the state. Based on the

survey findings, it is concluded that the SHG movement in the state is trapped in

vicious circle of traditional societal structure, poor execution of SHG programmes

by different agencies and lack of alternative economic enterprises and activities in

rural economy for disadvantaged group. These conditions lead to creating an

1 This paper has been written by Shri Naveen Kumar, Assistant Adviser while working in Chandigarh

Regional Office, Department of Economic and Policy Research (DEPR), Reserve Bank of India. Shri

Yogesh Jindal who was working as an Executive Intern in DEPR, Chandigarh Regional Office provided

enabling support during conduct of the primary survey. The author is grateful to all the SHG members

and other stakeholders whom he met during the primary survey and conduct of the study. The views

expressed in the paper are those of the authors and not of the institution to which they belong.

2

acute problem of non-scalability and spread of few successful SHGs across state.

Building on the accumulated experience and consultation with SHG members and

survey findings, the paper suggest way forward for the SHG movement in the state.

JEL Classification: I 138, G 21

Key words: poverty, micro finance institutions

3

Spread of Self Help Group (SHG) movement in Haryana (An Indian State):

Review of developments and way forward

I. Introduction

The progress of SHGs in last two decades has been remarkable, thus, becoming an

inseparable part of the developmental infrastructure, embodying massive social capital of

social mobilization and empowerment of women. With the rapid spread of SHGs over

time, the innovations associated with them have also flourished. Essentially, Self Help

Groups (SHGs), everywhere, act as tiny savings and loan cooperatives providing

economic means to poor people to engage in productive activities and inculcation of

saving habits. The success of SHGs has attracted widespread attention of policy makers

for attaining multiple objectives like poverty reduction, women empowerment, social

upliftment, financial inclusion, entrepreneurial development, reducing inequality, etc.

The SHG movement in India took shape in the 1980s as several NGOs experimented with

social mobilization and organization of the rural poor into groups for self-help. But, the

biggest thrust to the SHG movement in India was provided by National Bank for

Agriculture and Rural Development (NABARD) SHG-Bank Linkage Programme (SBLP)

under the aegis of Swarnajayanti Gram Swarojgar Yojana (SGSY) - a centrally

Sponsored Programme in 1990s . This programme over time has become the largest

programme in the world providing financial services to the poor people. The reason for

the success of this programme was the role of SHGs in financial inclusion/

mainstreaming of poor families as well as a development model with wider application.

It is interesting to look back at the SBLP in 1992-93 when only 255 SHGs were financed.

The major breakthrough happened in 2001 when this number crossed one lakh figure

showing scalability of the novel idea. It had recorded explosive average annual growth of

155 per cent till then (Chart 1). By then, the policy makers across board had recognized

the importance of SHGs as channel of development and emancipation from poverty.

4

0200400600800

100012001400

Th

ou

san

d

Year

Chart 1: Phase of growth of Bank financed SHG sector in India

No of SHGs financed by Banks

A. Low base but explosive

average annual growth of 155%

B. Mature stage growing at average annual

growth of 41 %

C. Stagnation/decline

Unfortunately, the success of this programme has been regionally skewed. In North India,

the SHG movement has failed to take-off. Haryana remained almost untouched with the

impact of mainstream microfinance movement. However, given the positive externalities

of SHG movement in emancipation of women and poor from the clutches of poverty and

bring empowerment, it becomes imperative to establish the movement in Haryana in the

right earnest. This would call for a probe into the reasons which have led to the failure of

the SHG movement in Haryana and also learn from few success SHGs. The present paper

attempts to analyze the ground realities through evidence collected during interactions

with SHG members and other stakeholders in a holistic manner.

5

Section II: Objective and Structure of the Study

Objective: The objective is to find reasons for the failure of the SHG movement in

Haryana through primary survey and confront the myth that lower poverty is the main

reason for failure of SHG movement in Haryana. In light of experience gained over years

of operation of SHGs in Haryana, the paper also suggest a way forward.

Structure: After brief Introduction and delineating study objective the paper is structured

into following sections. Methodology adopted for conduct of the study is discussed in

Section III. In the Section IV relevant literature is discussed. The Section V discusses

reason for failure of SHG movement in the State. Section VI discusses SHG movement

in Haryana through various programmes. In the Section VII Survey results are discussed.

Overall Assessment of SHG movement in Haryana is presented in Section VIII. Section

IX gives policy recommendations and way forward. Section X gives the conclusion.

6

Section III: Methodology

The paper has relied on conducting primary survey and interview methodology to gain

insight into the working of SHGs in Haryana, their reason for the failure, lessons from

successful ones and their views on ways to make the movement a success in future. For

this purpose, two districts each representing relatively both success and failure of SHGs

in Haryana, in terms of SHGs per population of district were chosen. Attempt was made

to visit different types of SHGs from diverse institutional support background like

National Rural Livelihoods Mission (NRLM), Swarnajayanti Gram Swarojgar Yojana

(SGSY), NABARD, etc. Altogether, author compiled response to questionnaire from 80

SHG members representing 29 SHGs from nineteen villages, with size ranging from 800

populations to ten thousand populations. The four districts surveyed were Ambala,

Faridabad, Mewat and Sonipat, with 20 SHGs members from each of them being

interviewed. Comments were also solicited from them regarding wide range of issues

ranging to rural economy, constraints to growth of SHGs and steps required for success

of SHG movement in Haryana. The survey was conducted during 2014-15.

7

Section IV: Literature Survey

There is vast literature existing conferring the virtues of Microfinance and the various

feasible models of operation and delivery. The literature also discusses the impacts of a

variety of microfinance interventions in different countries. Among different theories,

some follow the traditional narrative of modeling credit that enables entrepreneurship,

investment and growth. Ahlin and Jiang (2008) modeled Micro-credit as a pure

improvement in the credit market that opens up self-employment options to some agents

who otherwise could only work for wages or subsist. Recently, Greaney, Kaboski and

Leemput (2013) examined a cost-reducing innovation to the delivery of “Self-Help

Group” microfinance services and showed that membership fees could actually improve

performance without sacrificing membership, simply by mitigating an adverse selection

problem.

In this regard, comment “Many successful organizations working with the poorest of the

poor to try to get them to put aside some money as savings, no matter how little, before

giving them loans. Some of our self-help groups (SHGs) work on this principle (Rajan

2014)” summarizes the basic mechanics of SHGs in India. Not only does the savings

habit, once inculcated, allow the customer to handle the burden of repayment better, it

may also lead to better credit allocation. With the power of information technology,

perhaps the analysis of the savings and payment patterns of a client can indicate which

one of them is ready to use credit well. The groups in effect act as financial

intermediaries or ‘mini banks’ with the members both as owners and users (Ajay tankha,

2012).

Further, in the recent World Bank policy research paper titled ‘Localising Development:

Does Participation Work?’, Mansuri and Rao (2013) describes the virtues of

microfinance programme being that it mobilize groups of individuals to collectively

enforce the repayment schedule of every member, in an attempt to resolve coordination

8

problems and asymmetries in information on the creditworthiness of individuals, which

prevent banks and other large credit suppliers from servicing such communities.

Given, the fast growth of SHGs in recent time, the literature has taken cognizance with

many papers focusing specifically on SHGs. Self-help groups have also been mobilized

to help expand livelihood opportunities more generally—by providing training in

handicrafts and agricultural techniques, for example, and assisting in small-scale

entrepreneurial and other activities. The group provides peer education, technical and

moral support, using the power of networks to diffuse information and knowledge.

Unlike similar experiments in other developing countries, the SHG-BLP laid emphasis on

regular savings by the members with the savings corpus being used to lend among them-

selves and as needs arise, later by linking the groups with banks for availing credit

(NABARD, 2013).

The SHG movement in rural Haryana is at early stages and taking many shapes as

different agencies promote micro-finance with a variety of approaches and strategies

(Batra, 2012). At present there is no adequate and complete database on SHGs in the

State as the information is scattered around with different departments and institution.

Among all micro-finance programmes, SGSY is leading with highest numbers of SHGs

and loan amount and also it has special focus on BPL families. The results of the micro-

finance programme of Mewat Development Agency are also very encouraging. There are

smaller numbers of community-based organizations in the state and small NGOs are in

the field but with certain limitations. Given the positive impact of micro-finance on

women, as claimed worldwide, certain innovative practices should be adopted to

streamline the SHG movement in the state.

9

Section V: Does lower poverty explains the failure of SHG movement in Haryana?

The strongest argument put forward to explain the failure of SHG movement in Haryana

has been that lower incidence of poverty in the state does not necessitates any

requirement of SHGs in the state. It is argued that there is no need for SHGs in Haryana

as people are already well off. Thus, there is no scope for SHGs to grow in the state as

the developmental need of the most people have been taken care-off. However, when a

national comparison is made (Table 1) in terms of incidence of poverty, it is seen that

some of the states having lower incidence of poverty than Haryana have considerably

better penetration of SHGs. It is observed that the least poor state (among major states) is

having highest penetration of SHGs followed by states like AP and TN. Exceptions to

the trend are Northern states of Haryana, Punjab and J&K having low poverty co-existing

with low penetration of SHGs. It appears strange that while the southern states witnessed

poverty reduction along with strong SHG movement, similar phenomenon in Haryana,

Punjab and J&K is absent.

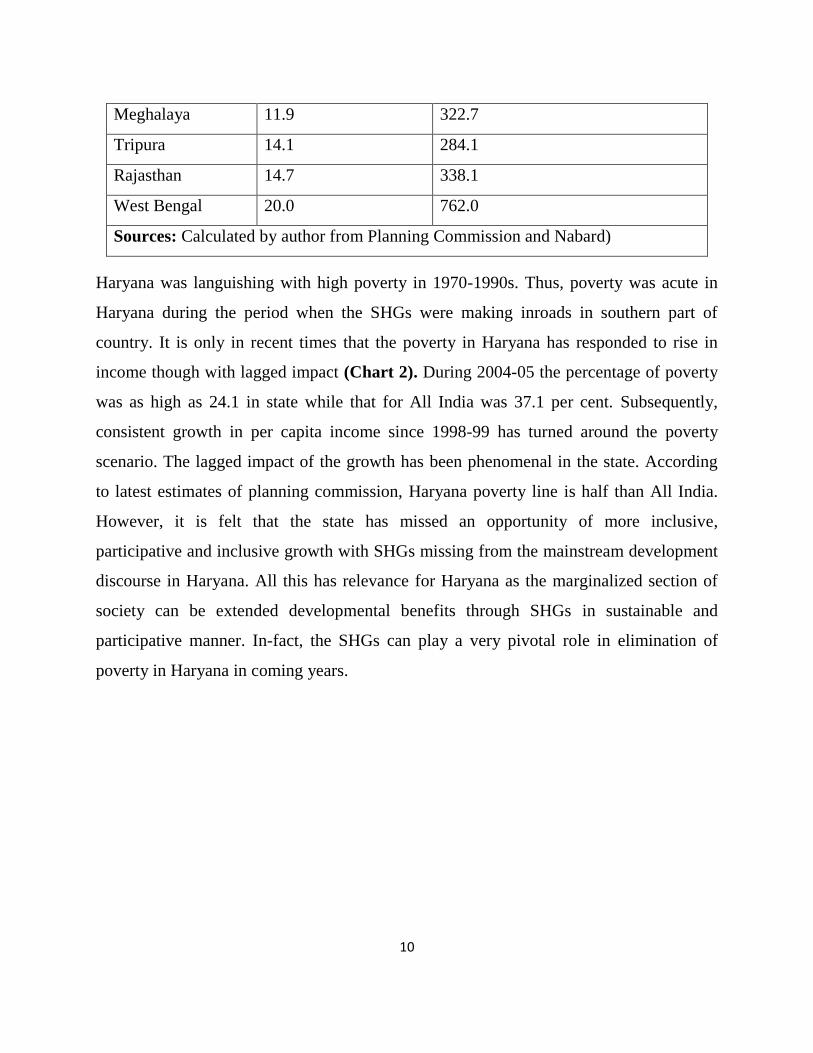

Table 1: SHGs penetration and Poverty

Poverty (%) 2011-12

No of SHGs per Lakh person

(March 2013)

Kerala 7.1 1740.2

Himachal Pradesh 8.1 775.6

Sikkim 8.2 578.0

Punjab 8.3 126.4

Andhra Pradesh 9.2 1684.1

Jammu & Kashmir 10.4 46.2

Haryana 11.2 168.0

Uttarakhand 11.3 399.7

Tamil Nadu 11.3 1210.0

10

Meghalaya 11.9 322.7

Tripura 14.1 284.1

Rajasthan 14.7 338.1

West Bengal 20.0 762.0

Sources: Calculated by author from Planning Commission and Nabard)

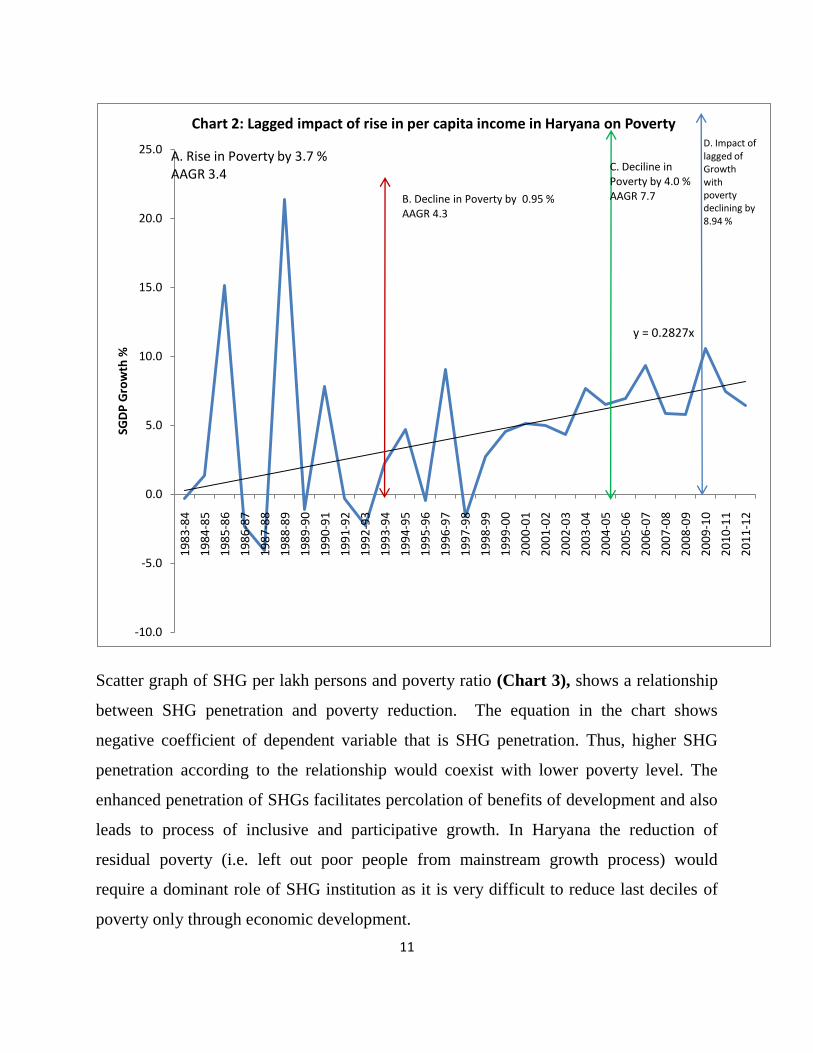

Haryana was languishing with high poverty in 1970-1990s. Thus, poverty was acute in

Haryana during the period when the SHGs were making inroads in southern part of

country. It is only in recent times that the poverty in Haryana has responded to rise in

income though with lagged impact (Chart 2). During 2004-05 the percentage of poverty

was as high as 24.1 in state while that for All India was 37.1 per cent. Subsequently,

consistent growth in per capita income since 1998-99 has turned around the poverty

scenario. The lagged impact of the growth has been phenomenal in the state. According

to latest estimates of planning commission, Haryana poverty line is half than All India.

However, it is felt that the state has missed an opportunity of more inclusive,

participative and inclusive growth with SHGs missing from the mainstream development

discourse in Haryana. All this has relevance for Haryana as the marginalized section of

society can be extended developmental benefits through SHGs in sustainable and

participative manner. In-fact, the SHGs can play a very pivotal role in elimination of

poverty in Haryana in coming years.

11

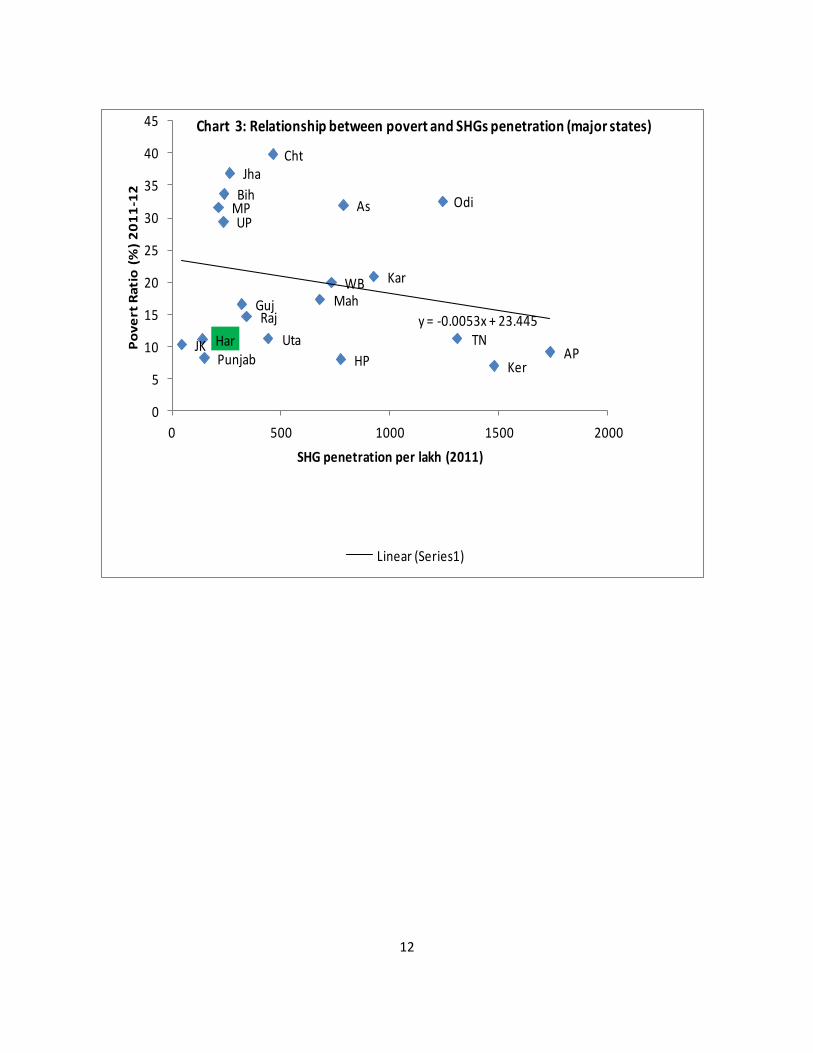

Scatter graph of SHG per lakh persons and poverty ratio (Chart 3), shows a relationship

between SHG penetration and poverty reduction. The equation in the chart shows

negative coefficient of dependent variable that is SHG penetration. Thus, higher SHG

penetration according to the relationship would coexist with lower poverty level. The

enhanced penetration of SHGs facilitates percolation of benefits of development and also

leads to process of inclusive and participative growth. In Haryana the reduction of

residual poverty (i.e. left out poor people from mainstream growth process) would

require a dominant role of SHG institution as it is very difficult to reduce last deciles of

poverty only through economic development.

y = 0.2827x

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

19

83

-84

19

84

-85

19

85

-86

19

86

-87

19

87

-88

19

88

-89

19

89

-90

19

90

-91

19

91

-92

19

92

-93

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

SGD

P G

row

th %

Chart 2: Lagged impact of rise in per capita income in Haryana on Poverty

A. Rise in Poverty by 3.7 % AAGR 3.4

B. Decline in Poverty by 0.95 % AAGR 4.3

C. Deciline in Poverty by 4.0 % AAGR 7.7

D. Impact of lagged of Growth with poverty declining by 8.94 %

12

WB

Uta

UP

TN

Raj

Punjab

OdiMP

Mah

Ker

Kar

Jha

JKHP

Har

Guj

Cht

BihAs

AP

y = -0.0053x + 23.445

0

5

10

15

20

25

30

35

40

45

0 500 1000 1500 2000

Po

ve

rt R

ati

o (

%)

20

11

-12

SHG penetration per lakh (2011)

Chart 3: Relationship between povert and SHGs penetration (major states)

Linear (Series1)

13

Section VI: SHG movement in Haryana

In Haryana, Self Help Groups has been promoted under different programme/projects by

various departments and agencies (Figure 1). The Women and Child Development

Department has promoted SHGs under the Programme for Advancement of Gender

Equity (PAGE) and Swayamsiddha. Women’s Awareness & Management Academy

(WAMA) has promoted the Swashakti project while the Forest Department has been

promoting SHGs under the Haryana Community Forest Project (HCFP) and Integrated

Natural Resource Management and Poverty Reduction. Banks are promoting SHGs under

NABARD’s SHGs-Bank linkage Programme; District Rural Development Agencies

(DRDA) is promoting SHGs under Swarnjayanti Gram Swarozgar Yojana (now NRLM)

and Mewat Development Agency (MDA) is promoting SHGs under the International

Fund for Agricultural Development (IFAD) programme in Mewat district. Besides

government departments, agencies and banks, some international, national and regional

NGOs are also involved in this work. The Ministry of Rural Development, GOI has

launched the National Rural Livelihood Mission (NRLM) as a flagship rural development

program. The objective of this Mission is to eliminate rural poverty through innovative

social mobilization, financial and economic inclusion strategies. The NRLM

implementation framework draws on the lessons from successful implementation of rural

livelihoods project in Andhra Pradesh, Bihar and Kerala.

The Government of Haryana has set up an autonomous society i.e. Haryana State Rural

Livelihood Society (HSRLM), under the aegis of Rural Development Department,

registered under the Societies Registration Act,1860 This Society is responsible for

implementing mission across the state. Though, the paper has focused on bank linked

SHGs, the importance and contribution of other channels of SHG movement on

development and empowerment of poor people cannot be ignored.

It may be noted that most dominant mode of SHGs in state has been through SGSY. The

NABARD has not been successful in galvanizing the movement in the desired manner.

14

Figure 1: SHG movement in Haryana

Source: Adapted from Vikas Batra (2012).

SHG

Movement

in Haryana

IWEDP-

July

1994

PAGE-

2003 SWAYAMS

IDDHA- 2001

SWA-

SHAKTI

Project

Project

Conversion

of Mahila

Mandals into SHGs

HARYANA COMMUNITY

FORESTRY PROJECT (HCFP)-

1999

MICRO-CREDIT

scheme of HWDC-

2008

NABARD/

SBLP

SGSY/ NRLM

Integrated Natural

Resource Management and Poverty Reduction-

2004

Mainstream SHGs

based Programme

State Level Initiatives and

Programmes based on

SHGs

15

Section VII: Analysis of survey results:

a. Benefits/Success of SHG movement in Haryana: Some evidence from survey

1. Favorable demographic attributes: It is found in the survey that approximately

90 per cent of the members were literate, though, mostly at primary level. Majority of

the members of SHGs were women (89 per cent). Most of the SHGs members were in

their thirties. Thus, it is revealed that the women members were mostly literate, could

understand the working of SHG’s operations and were relatively younger. This gives the

SHG movement in Haryana the required vigor, strength and hope for success in future,

provided the observed lacunas are appropriately addressed.

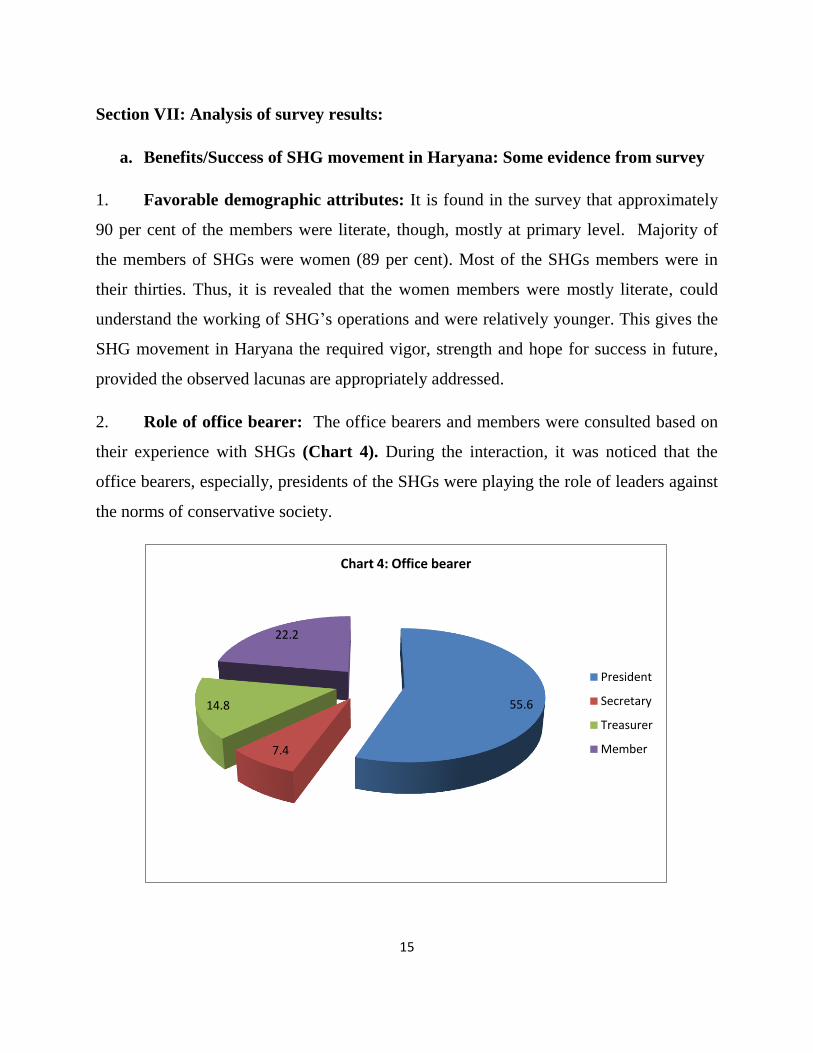

2. Role of office bearer: The office bearers and members were consulted based on

their experience with SHGs (Chart 4). During the interaction, it was noticed that the

office bearers, especially, presidents of the SHGs were playing the role of leaders against

the norms of conservative society.

55.6

7.4

14.8

22.2

Chart 4: Office bearer

President

Secretary

Treasurer

Member

16

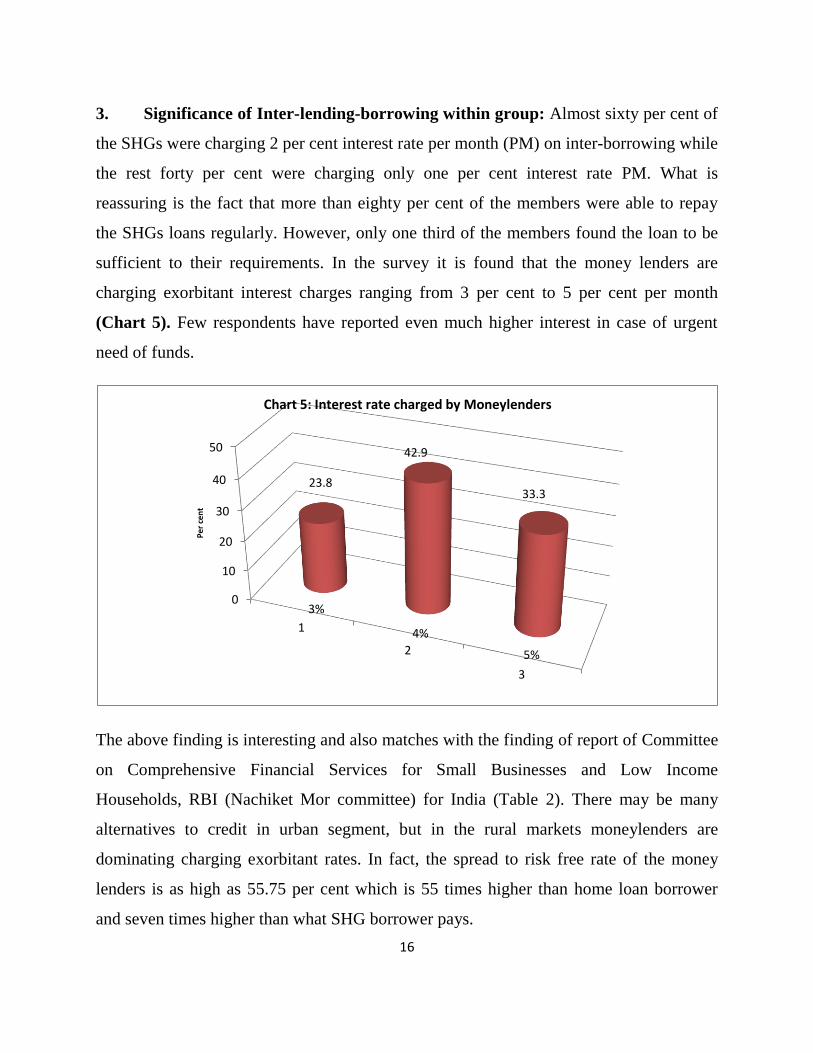

3. Significance of Inter-lending-borrowing within group: Almost sixty per cent of

the SHGs were charging 2 per cent interest rate per month (PM) on inter-borrowing while

the rest forty per cent were charging only one per cent interest rate PM. What is

reassuring is the fact that more than eighty per cent of the members were able to repay

the SHGs loans regularly. However, only one third of the members found the loan to be

sufficient to their requirements. In the survey it is found that the money lenders are

charging exorbitant interest charges ranging from 3 per cent to 5 per cent per month

(Chart 5). Few respondents have reported even much higher interest in case of urgent

need of funds.

The above finding is interesting and also matches with the finding of report of Committee

on Comprehensive Financial Services for Small Businesses and Low Income

Households, RBI (Nachiket Mor committee) for India (Table 2). There may be many

alternatives to credit in urban segment, but in the rural markets moneylenders are

dominating charging exorbitant rates. In fact, the spread to risk free rate of the money

lenders is as high as 55.75 per cent which is 55 times higher than home loan borrower

and seven times higher than what SHG borrower pays.

0

10

20

30

40

50

1

2

3

3%

4%

5%

23.8

42.9

33.3

Per

cen

t

Chart 5: Interest rate charged by Moneylenders

17

Table 2: Comparison of Alternative loan markets

Customer Class Expected Loss Rate*

Interest Rate (per annum)

Adjusted Interest Rate net of expected loss

Spread to Risk Free Rate**

Personal Loan Borrower 5.80% 18.00% 12.20% 3.35%

SHG Borrower 7.08% 24.00% 16.92% 8.07%

JLG Borrower 0.40% 26.00% 25.60% 16.75%

Money Lender Borrower 0.40% 65.00% 64.60% 55.75%

Home Loan Borrower 0.43% 10.30% 9.87% 1.02%

Note:* Observed default rate, ** Return on 365 day T-Bills, as on December 16, 2013 is 8.85%. Source: Committee on Comprehensive Financial Services for Small Businesses and Low Income Households, RBI.

The operations of SHGs provide competition in the rural credit market, but in a very

limited manner, benefitting mainly SHG members (Figure 2). It is seen that the open

credit market settles at very high interest rate of 5 per cent per month in rural economy of

Haryana. This is mainly on account of financial exclusion i.e. inadequate operation of

banks branches, lack of collaterals, lack of comptetion in rural credit market, financial

ignorance and inadequate and improper legislation related to money lending.

Credit

Figure 2: Working of Informal and SHG credit system

10-12 SHG members

are served

2%

5%

by

mon

elen

ders

SHG-Inter-

lending

Informal credit

market

Interest

Rate

18

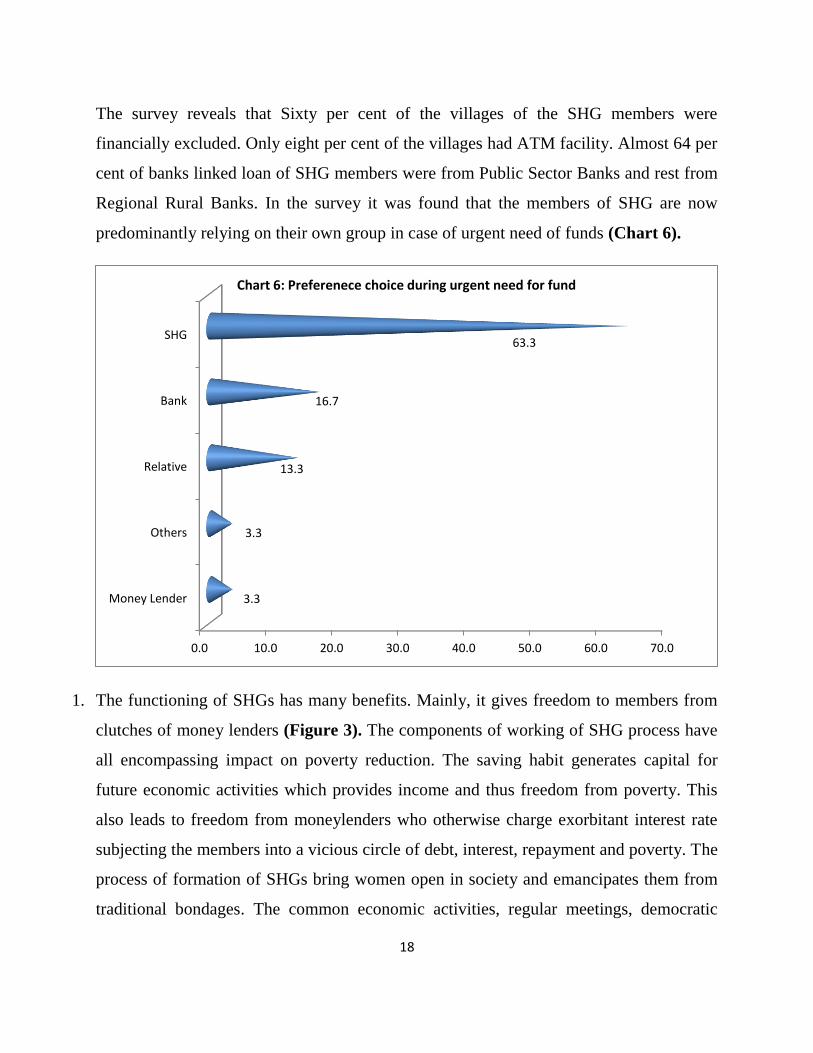

The survey reveals that Sixty per cent of the villages of the SHG members were

financially excluded. Only eight per cent of the villages had ATM facility. Almost 64 per

cent of banks linked loan of SHG members were from Public Sector Banks and rest from

Regional Rural Banks. In the survey it was found that the members of SHG are now

predominantly relying on their own group in case of urgent need of funds (Chart 6).

1. The functioning of SHGs has many benefits. Mainly, it gives freedom to members from

clutches of money lenders (Figure 3). The components of working of SHG process have

all encompassing impact on poverty reduction. The saving habit generates capital for

future economic activities which provides income and thus freedom from poverty. This

also leads to freedom from moneylenders who otherwise charge exorbitant interest rate

subjecting the members into a vicious circle of debt, interest, repayment and poverty. The

process of formation of SHGs bring women open in society and emancipates them from

traditional bondages. The common economic activities, regular meetings, democratic

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0

Money Lender

Others

Relative

Bank

SHG

3.3

3.3

13.3

16.7

63.3

Chart 6: Preferenece choice during urgent need for fund

19

decision of inter borrowings and exposure to banking services creates a virtuous cycle of

women empowerment, freedom from money-lenders and ultimately removal of poverty.

Financial inclusion of excluded segments through SHG has potential of deepening reach

of monetary policy signals more effectively to hitherto untouched segments and will get

further mainstreamed in due course.

Stages

Wom

en Empowerm

ent

Freedom from

money-lenders

Constraints

Patriarch

Society Inadequate Loaning

from banks

Attitude of bank

employees Lack of Financial

Awareness

Working/benefits of SHGs

Inculcation of saving habit

Inter-lending among SHGs

Access to banking services

Regular meeting with democratic

participation

Lack of Economic opportunities

Removal of Poverty

Figure 3: Working of SHGs in Haryana: Benefits and Constraints

In Haryana, the SHG movement, in a very limited manner, has created many positive

externalities in terms of women empowerment, freedom from money lenders, opening

entrepreneurship avenues to enterprising women, impacting poverty, financial awareness,

more access to banking facilities, awareness about democratic institution, group

bargaining power, increased self confidence and dignity of SHG members, social change,

etc. The success in terms of number of groups may be dismal but generation of right sprit

20

of successful partnership by few successful SHGs have generated the confidence that

with appropriate support structure and right incentive the movement can be scaled up

further.

b. Reasons for failure of the SHG movement: Some reflections on survey results

1. One of the indicators of the fact that the SHG movement is in the nascent stage of

development is reflected by the finding of the survey that the average age of SHGs were

around three years only, though, the sample was quite varied with SHGs ranging from

newly formed to as old as ten years.

2. During the interactions with various stakeholders of the SHG movement, among the

common reasons lack of social cohesion and individualistic tendencies were the main

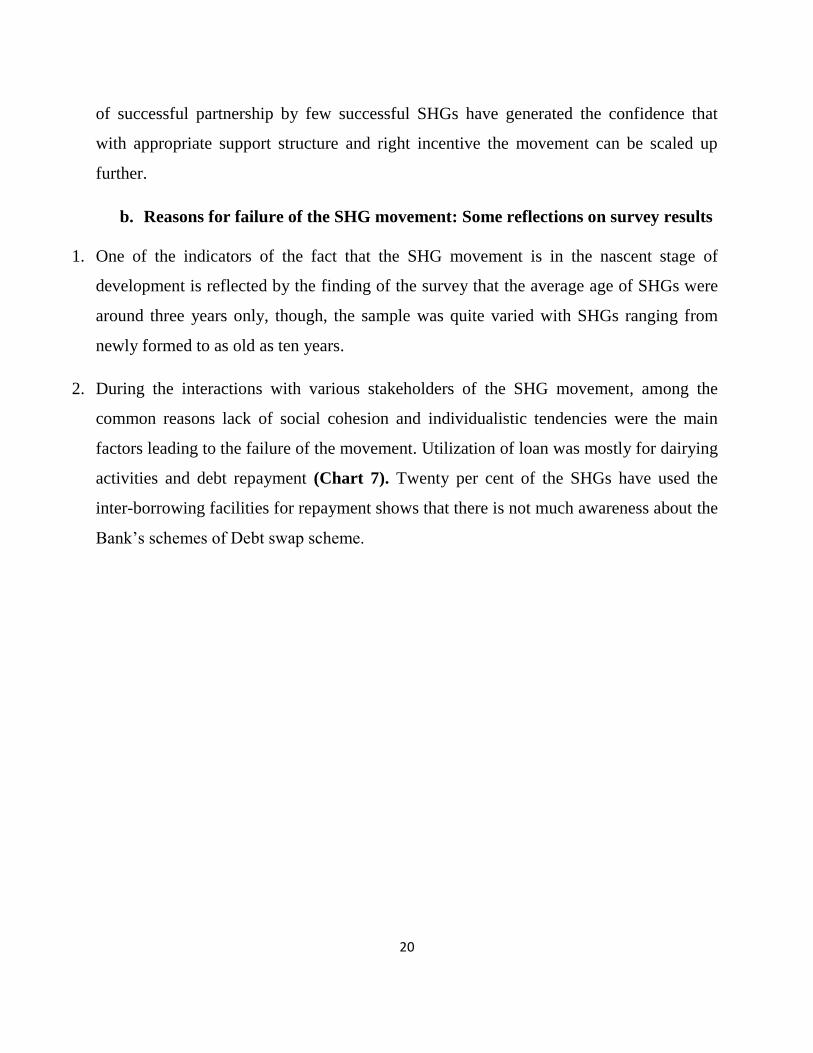

factors leading to the failure of the movement. Utilization of loan was mostly for dairying

activities and debt repayment (Chart 7). Twenty per cent of the SHGs have used the

inter-borrowing facilities for repayment shows that there is not much awareness about the

Bank’s schemes of Debt swap scheme.

21

The patriarchal nature of society is quite rigid and dominant in Haryana which is

significantly impacting the social behavior of women members, thus, creating limits to

the percolation and spread of SHG movement. Also, it need to be noted that women

members have the tendencies to be divided on the caste lines, thus making the group

dynamics prone to local political factors. There has been no progressive political

movement in Haryana which has taken the cause of SHGs. Almost everywhere it was

observed that people would prefer for individual enterprise rather than any group activity

as the non-cooperating psyche is well ingrained in their mind.

3. The role of social status in success of few SHGs: It is noticed that some of the women

SHGs belonging to middle/higher caste were able to organize economic ventures

successfully. One reason was that they are non-SGSY groups formed on the basis of

efficiency and not subsidy. However, they were not supported by their spouses at any

47.4

21.1

10.5 10.5

5.3 5.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Dairy Debt repayment Shops Consumption need

House construction

Other economi activity

Chart 7: Utilisation of loan

22

stage. This process of SHG running and common activities has led to women

empowerment. One case in particular can be recalled from village Baktua in Ambala

District. The Baktua Mahila Samiti is linked to forest department of Haryana. The group

is engaged in business of producing and selling bio-fertilizers. The group is doing this

job profitably apart from also engaging in making traditional handicraft items. They

want to scale up but is not supported by linked bank branch. The members counted

synergy and exchange of experience as most valuable strength in the group. The

constraints counted were marketing, raw material, non-display and lower margins. This

was the position of a relatively success story of an SHG belonging to better off section of

society. The main outcome of SHG was women empowerment, economic freedom and

social mobility. On the other hand, it is observed that most of the SHGs formed under

SGSY have failed (formed by SC population). All the SHG formed by DRDA pertains to

SGSY (Chart 8). Even gram sevikas are also active in forming SHGs under SGSY.

Women belonging to low social class in the state are generally very poor and lack assets.

However, the biggest asset that they lack is self confidence. This is required for

28.6

10.7

53.6

7.1

0.0

10.0

20.0

30.0

40.0

50.0

60.0

NGO Gram Savika DRDA Others

Chart 8: Agency wise formation of SHG

23

transcending the institutional and generational barriers. The society bias against women

restricts their movement. A SHG activity primarily tries to break these barriers. But

women generally ends up as failure as a lack of handholding and poor societal attitude.

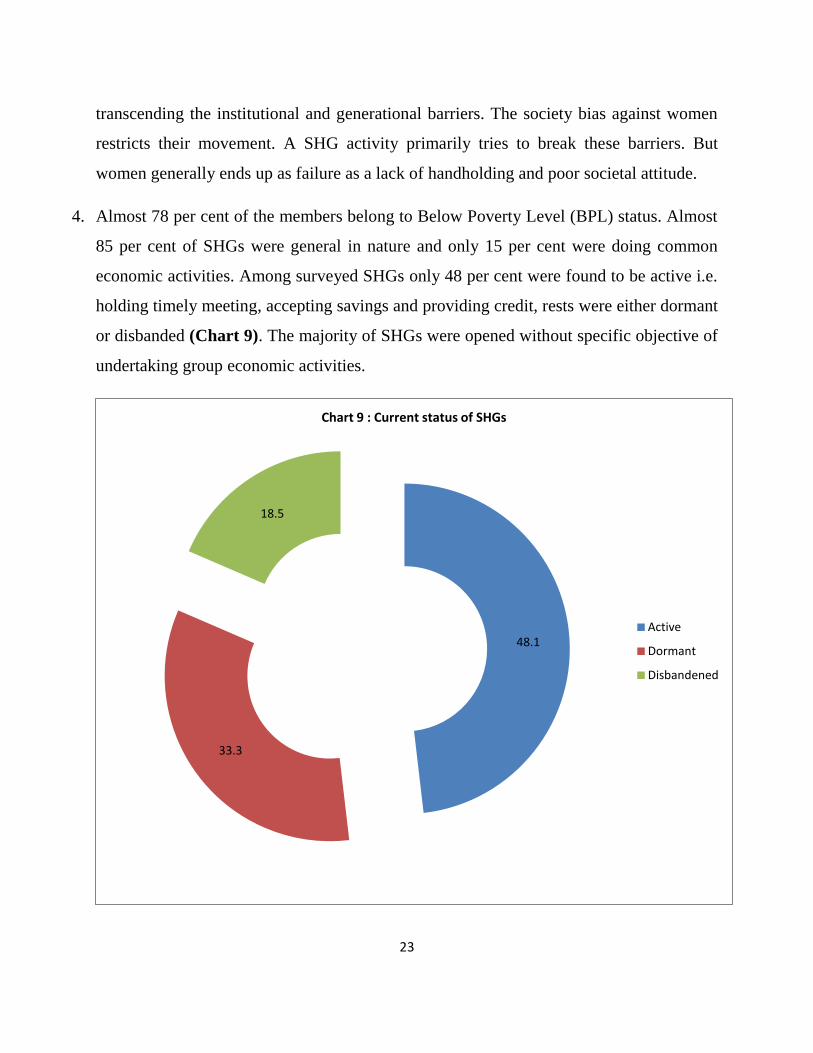

4. Almost 78 per cent of the members belong to Below Poverty Level (BPL) status. Almost

85 per cent of SHGs were general in nature and only 15 per cent were doing common

economic activities. Among surveyed SHGs only 48 per cent were found to be active i.e.

holding timely meeting, accepting savings and providing credit, rests were either dormant

or disbanded (Chart 9). The majority of SHGs were opened without specific objective of

undertaking group economic activities.

48.1

33.3

18.5

Chart 9 : Current status of SHGs

Active

Dormant

Disbandened

24

5. The survey reveals that only five percent of SHGs have received formal training related

to accounts, while 63 per cent of SHGs had received some kind of training for different

economic activities. The average days of training imparted was seven days. It is felt that

the training which is being imparted is inadequate, insufficient and not useful in most of

the cases. Another important requirement for the success of SHGs are frequent meetings

of the group. During the survey, it was found that almost sixty per cent of SHGs were

meeting at some intervals with fixed dates (Chart 10).

6. Saving mobilization: The survey reveals that Most of the SHGs members had started

with Rs 100 as saving amount per month and still continues with the same. However, as

seen in earlier section, per capita income in Haryana has increased rapidly and the state is

relatively prosperous. During our discussion with SHG members, we found that they

were continuing with the Rs 100 mobilization due to ignorance of the fact that they do

not require any permission to increase this amount. At all places they were explained the

benefits of higher mobilization of savings such as increased loans from banks, greater

availability of saving corpus for inter-lending and more importantly for taking higher

level of common economic activities. Almost all agreed that it can be increased easily by

3.6 10.7

39.3

42.9

3.6

Chart 10: Frequency of meeting

Weekly

Fortnightly

Monthly

Not meeting

No fixed frequency

25

50 per cent immediately and by 100 per cent in the next meeting itself. Many members

showed interest to raise the saving fund by even five times.

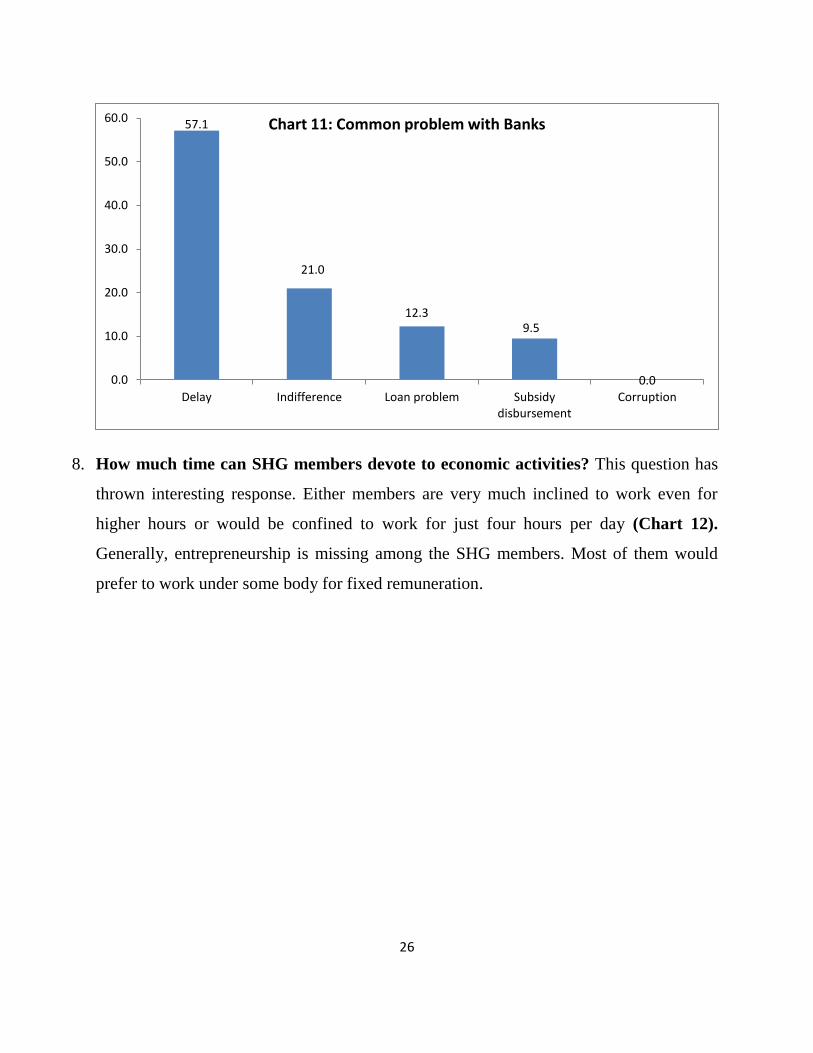

7. Problems with Banks: According to the survey results, delay in processing and

indifference shown by bankers were told as top two problems with banking sector (Chart

11). The SHG movement is not getting requisite support from the banking system. The

bankers are reluctant to even open accounts of SHG members. During the survey many

SHG members complained that even after meeting all the eligibility criteria, the bankers

were reluctant to open their saving bank account. When bankers opinion was sought,

many indicated the SHG members to be low valued customers, hardly bringing any

profitable business to them. The problem was widespread and the poorest of poor were

the main victims of banker’s apathy. The negative attitude of the bankers was

exemplified in one of the visit to bank branch in Mewat district. Even in the presence of

Lead District Manager (LDM) and the author, the manager ridiculed the whole policy of

financial inclusion and futility of opening bank accounts of poor SHG members. This is

reflective of the resistance that is being encountered at ground level by SHG movement.

This kind of attitude is both contagious and anemic for the success of SHG movement in

the state. While some bankers vocally express themselves, other’s act is reflected in their

non-committal attitude. At the next level, many instances were cited by SHG members

wherein the members were denied loans for years even after becoming eligible. It appears

that there is lack of effective redressal mechanism available for SHG members in case of

denial of banking services in rural part of the state. The role of bankers in nurturing the

SHGs was not found positive, except some RRB branches which were actively involved

with SHG members.

26

8. How much time can SHG members devote to economic activities? This question has

thrown interesting response. Either members are very much inclined to work even for

higher hours or would be confined to work for just four hours per day (Chart 12).

Generally, entrepreneurship is missing among the SHG members. Most of them would

prefer to work under some body for fixed remuneration.

57.1

21.0

12.3 9.5

0.0 0.0

10.0

20.0

30.0

40.0

50.0

60.0

Delay Indifference Loan problem Subsidy disbursement

Corruption

Chart 11: Common problem with Banks

27

9. SHG and Financial Awareness: No members were having ATM/Credit Card/Debit

card/Kisan card /GCC card. Fifty six per cent of the member showed willingness for

ATM cards. Only 46 per cent of the interviewed women could be categorized as

financially aware because of their restricted exposure and knowledge.

c. Summary of Survey results:

The survey reveals the multifarious reasons which explains the failure of SHG movement

in Haryana viz., lack of social cooperation, individualistic tendencies, concentration on

dairying at the cost of group activity, patriarchal nature of society, discrimination of

women reflected in adverse sex ratio, caste differences, faulty implementation of

programmes, lack of appropriate trainings, stagnant saving mobilization, non-cooperation

of banks, lack of financial knowledge, inadequate grievance redressal forums, lack of

entrepreneurial experience, lack of political initiative, etc., which have led to failure of

SHG movement in Haryana. On the positive side, the future of the movement looks

0

5

10

15

20

25

30

35

40

45

50

4 Hrs

6 Hrs

8 Hrs

10 Hrs

32.4

2.7

2.7

45.9 P

er

cen

t

Chart 12: Choice of working hours

28

bright as revealed from the favourable demographic indicators of SHG members. The

most significant impact of the extant SHGs has been the women empowerment, freedom

from money lenders and impact on poverty, though at limited scale.

29

Section VIII: Overall Assessment of SHG movement in Haryana

1. During the interactions with members of SHGs in four different districts, it was felt that

sensitive support structure in the state was missing. Even the active SHGs were not able

to get the required information and support services to scale up their activities. The

continuous nurturing support that a poor SHG member needs was mostly missing.

2. One of the factors responsible for the failure of SHG movement in Haryana was the ad-

hoc approach adopted by various agencies involved viz., NGOs, State Government,

banks, NABARD, etc. There was absence of backward/forward linkages and of

ownership as the Self Help Groups were left to fend for themselves once formed. There

were hardly any economic activities undertaken, most of the SHGs were not provided

bank loans, few could get meager amount. Even few of the successful SHGs faced

problems in marketing the produce. There was lack of guidance/help from any quarters.

The entire movement has suffered due to the bureaucratic approach of achieving targets

without any tangible, worthwhile outcome and the poor remain at the mercy of

moneylenders for financial need. Respective agencies need to assume the complete

ownership of the SHGs in their area of operation and address the problems listed above.

3. The progress of SHGs, especially in SGSY was being measured in terms of number of

group formed, number of people covered and amount of credit disbursed- not in terms of

income accruing from various activities. There was specific pressure put on the

administration to achieve group targets within a limited time frame. Over the years, the

emphasis on achievements of quantitative targets has resulted in wrong selection of the

projects, poor quality group formation without real assessment of entrepreneurial

potential, under-financing and instances of willful defaulting.

4. NABARD seems to have failed in giving the required push and direction to SHG

movement in state.

30

5. There was no trend of SHGs coming together and forming federation at village or block

level.

6. The programme-implementing agencies in the state especially, District Rural

Development Agency (DRDA) and Integrated Child Development Services (ICDS) were

facing problems in effective implementation due to being overburdened with other

responsibilities and inadequate manpower. These agencies also faced problems such as

lack of staff trained on income generation, financial literacy and other social issues.

7. Lack of handholding support has led to failure of some SHGs and sustenance of vicious

circle of poverty. An external dedicated, sensitive support structure was missing in most

of the cases with the members relying on mutual support. However, expanding capacities

and skills requires initial handholding at-least in formative stage.

31

Section IX: Policy Recommendations and Way Forward

It should be recognized that poor have innate capabilities and a strong desire to come out

of poverty for any meaningful intervention. They are entrepreneurial, an essential coping

mechanism to survive under conditions of poverty. The challenge is to unleash their

capabilities to generate meaningful livelihoods and enable them to come out of poverty.

The experience gained during the conduct of the survey has been used to suggest a way

out for SHG movement in Haryana. The primary building blocks of these

recommendations have been SHG member’s suggestions A cross section of the

stakeholders in SHG movement have also shared their experiences. It may be noted that

Haryanvi’s are very hard working people who just need right environment to show their

entrepreneurial potential. The SHG movement can channelize their latent energies. The

implementation of the following recommendation will provide a new direction to the

SHG movement in the state.

1. It would not be out of context to look into following aspects of shortcomings of NRLM

which is also being implemented in Haryana: (1) The NRLM design perhaps looks at the

rural economy as one whereas in reality, many segments exist within rural low income

people as well as across the broader rural economy spectrum. Therefore, it would become

crucial to ensure that a range of bundled services (as envisaged) are provided in

accordance with the needs of the different segments. (2) The whole concept of NRLM,

which is SHG focused, should in reality be driven by critical sub-sectors, associated

value chains and related livelihoods including MSMEs. In other words, it should use

these as focal points and address the practical challenges emanating from a detailed

analysis of the concerned sub-sectors/value chains/livelihoods to address the vulnerability

and risks faced by rural producers. (3) The strategy of NRLM is too broad and sweeping.

Rather than attempting to do a whole lot of things across the board, it may be better if the

NRLM learns from its past avataar's such as the Integrated Rural Development

Programme (IRDP) or Shahari Jan Sahabhagi Yojana (SJSY) previous mistakes and

32

focuses on areas that could impact livelihoods of large number of rural livelihoods so as

to generate quick wins for the program as well as get the initial thrust and momentum –

so critical for medium and long term success.

2. There is a need for micro-level planning to identify key livelihood activities. In order to

identify appropriate livelihood opportunities, a Task Force should be set up at the local

level by including all concerned, NGOs and the private sector. Village potential mapping

with a sub-sectoral analysis would play a substantial role in the development of income

generation activities. In order to have a knowledge base about the availability of

resources, panchayat-level surveys can also be conducted under the auspices of local

authorities. To make them operational, the cluster-based local development approaches

should be adopted.

3. All the procedures involving any government agency/banks/financial institutions with

SHGs should be simplified to extent possible and made hassle free.There is need to adopt

state specific approach for formation, grooming, nurturing, training and skill

development and handholding support system and infrastructure as the state has unique

socio-economic conditions. Blindly following the successful models of other states or

countries is not expected to give the desired results.

4. Initiating SHGs into economic activities: One of the major failures of the current SHGs

has been their inability to engage the group into common economic activities. It is felt

that some professional bodies may be engaged in initiating the SHGs into economic

activities by guiding SHGs appropriately from production to marketing and finally to

repayment of loans.

5. SHG federations: Although, the NRLM also talks about need for SHG federation, it is

felt that the scope of federation should be vast to cater the need of non-NRLM groups

also. The federation should not discriminate between SHGs and should include all types

of SHGs.

33

6. Marketing Solution: One of the common problems being faced by the SHGs is the

marketing of product to right segment at right price. Mostly, the intermediaries are

involved in final sale of product. The major chunk of the profit is pocketed by the

intermediaries. Thus, even though the product may be commanding high price in market,

lack of marketing avenues leads to lower realization of prices and lower profits and also

unsold inventories. Most of these products don’t have market in village itself and are

mostly tailored for urban market.

It is suggested that State level federation should brand the product of all SHGs under

common state brand name ensuring uniformity and quality of product across all SHGs.

Branding all the products through common hologram under common umbrella would

lead to credibility and acceptability of SHG products in the market. It is also suggested

that state level federation should launch Business to Consumer web site by tying up with

payment gateway. The state government can provide sale counter to SHG federation at

all tourist places in the state. The government can also provide space in shopping malls to

SHG federation at subsidized rates. The spaces in shopping malls are perfect place for

promoting SHG products. The federations at various levels can coordinate to operate the

sale counters under guidance of the Apex federation. The state level federation can even

hire marketing professional to cement tie up in the market and also building supply chain

integration with retailers and malls.

7. SHG leaders as Business correspondent: It is suggested that leaders from SHGs having

good track record in various steps in formation, nurturing and maturity of SHGs should

be preferred as Business correspondents in their villages. The proven leadership qualities

of the SHG leaders can be of great help in facilitating BC business across all section of

villagers.

8. Visits to successful SHGs: In order to encourage learning and sharing of experience

among SHGs, the visits of not so successful SHGs should be organized to relatively

34

successful SHG across state. This would facilitate practical learning and realistic

assessment of opportunities existing at the ground level. It will also help in spread of

positive impact of ‘demonstration impact’ of successful SHGs.

9. Identification of resource people and networking: During the visit to the different

SHGs, it became evident that many SHG members have acquired important skills and

experience required for successful operation of SHG. These members should be given

specialized assignment of guiding startup SHGs in nurturing and scaling up. Federation

should prepare a data base of such resource people and facilitate proper networking

across SHGs.

10. Agro-processing and SHGs: During the survey, it was observed that few SHGs were

involved in agro-processing though non-professional manner and at very local level. The

agro-processing industry has vast scope in the state given the fact that it has ready-made

market as thirty per cent of state fall in NCR region and have adequate supply of raw

material. The labour cost of SHG members is quite cheaper as compared to those

prevailing in the market. Thus, it is a win-win proposition for SHGs. However, major

breakthrough can be achieved only if right technological solution of packaging and

marketing is available at the door step of SHG members. In this regard, it is suggested

that the federation should take help of professionals in guiding the prospective and

existing entrepreneurs among SHGs.

11. Dairying in Haryana and SHGs: After agriculture, animal husbandry is an important

sector to supplement the income of rural masses in the State. It has been observed during

the survey that almost half of the loans taken by SHG members have been utilized for

dairying activities. However, no common dairy farm of any SHG group was observed

during the survey. This fact should compel policy makers to reprioritize and make

appropriate strategy according to unique socio-cultural ethos of the state. There is

pressing need for Milk federation in the states. The dairying activities supplements

35

income and some time is the only available employment opportunity. However, mostly

the dairying activities of the SHG members are done on unscientific and traditional

manner leading unproductive practices and waste of potential. It is suggested that

specialized SHGs should be formed taking dairying activities as common group

activities. There should be more incentives in terms of compulsory training in relevant

institute for learning scientific dairying and more loan amount from banks for such

activities. They should all be part of milk federation and also SHG federation for better

synergy.

12. Banking services to SHGs: The bankers need to be sensitized about the importance of

SHGs for overall development of society and role of banks in achievement of this

objective. They should also be sensitized about the good track record in terms of payment

of loan dues by SHGs and loaning to SHGs as good business decision. It was found in the

survey that SHG members were interested in ATM services. It was also desired by some

that cheque books should be issued to them. Therefore, the bankers should educate the

SHG members about operation of debit cards, cheques and encourage them to opt for the

same. In the long run ATM reach in rural areas will lead to reduction in cost for banks

provided most of the villagers have practices of using debit cards.

It should be mandated that bankers should take part in SHG meeting once every quarter

at least in the respective village under their jurisdiction. This would develop close

contacts of bank officials with SHG members and help in professionalizing the operation

of SHGs, appraisal of credit history, better liaison, dissemination of new bank loan

scheme and government programme, two way dialogue, grievance redressal, financial

literacy, accounts checkup, guidance, etc.

13. Adequate flow of Credit to SHGs: After interacting with the SHGs members it is felt

that the credit need of these poor women mostly remain unaddressed as the loan that is

offered does not take care of even essential demands. Those who have ventured in

36

economic activities could not break up due to lower scale of operations. For scalability

additional and more credit was required which was denied at the required time. It was

also found that the even the mandated credit under various programmes was not being

provided to them. Until and unless it is ensured that each and every SHGs would be

provided adequate credit both serving their individual demand and also demand of group

for economic activities, the success of SHGs in the states cannot be achieved.

14. Role of NGO: It has been observed that at many places the NGOs have played pivotal

role in formation and nurturing of SHGs. Generally SHGs and NGOs are in symbiotic

relationship. The NGOs should be adequately compensated for their consultancy services

and should be encouraged to bring entrepreneurship closer to SHG groups by placing

right incentives and enabling right connection and support structure. At some places it

was found that the NGO itself was playing the role of entrepreneur providing work to the

groups. In these types of cases there should be no discrimination in providing the

incentives and NGOs should be properly rewarded. However, bigger incentives should be

on passing on the entrepreneurial knowledge to SHG groups in long run. For imparting

training the capacity of NGOs should be properly utilized

15. Capacity Building: It is very important to have strong institutions at the community

level. To achieve this objective a structured learning and capacity building system should

exist in the state. The government with the active involvement of SHG federation should

tie up with relevant institutions like Industrial Training Institute, Rural Self Employment

Training Institutes (RSETI), etc, to impart knowledge, training and experience on

technological and financial know how for project planning, execution, appraisal,

marketing, etc for village and small scale industries. The SIDBI should open small

incubators for SHG member startups at district level. The certification should make SHG

members eligible for higher and faster loans.

37

16. Promise of Mobile Banking: It was found in the survey that the SHG members were

using mobile phones. Given the high growth of apps for smart phones and their declining

cost and also some acquaintances with them in rural part of the country in recent years, a

customized app may be developed for the use of all SHG members. This can bring

cheaper solution to many problems and integration of mobile banking and other solution

to communication and accounting and also work as seamless integration of knowledge,

technology, networking of traditional socio-economic landscape and skills. An innovative

use in future can lead to leveraging of SHG skills.

38

Section X: Conclusion

The SHG movement has connected millions of poor women to the banking services and

more importantly created healthy financial habits like savings, inter-lending, loaning and

poverty reduction. However, the states in the Northern part of India, especially Haryana,

seem to have remained untouched with this movement. The paper breaks the myth that

reason for the failure of SHG movement in Haryana is because of lower poverty and

recognizes the positive impact of per capita income which is a proxy of economic growth

on reduction in poverty.

The paper reveals the multifarious reasons which explains the failure of SHG movement

in Haryana viz., lack of social cooperation, individualistic tendencies, concentration on

dairying at the cost of group activity, patriarchal nature of society, discrimination of

women reflected in adverse sex ratio, caste differences, faulty implementation of

programmes, lack of appropriate trainings, stagnant saving mobilization, non-cooperation

of banks, lack of financial knowledge, inadequate grievance redressal forums, lack of

entrepreneurial experience, lack of political initiative, etc., which have led to failure of

SHG movement in Haryana.

In Haryana, the success in terms of number of groups may be dismal but generation of

right sprit of successful partnership by few successful SHGs have generated the

confidence that with appropriate support structure and right incentive the movement can

be scaled up further. Building on the experience gained over years and also suggestions

of stake holders including SHG members, a way forward is suggested emphasizing on the

role of sensitive support structure capable of handholding in critical stages, need for

capacity building, timely and adequate flow of credit and sensitizing banking staff to

specific need of SHGs, specialized agency for livelihood projects, innovative marketing

solutions, inter-learning from successful SHGs, etc. In the end it may be concluded that

the SHG movement has not acquired a scale where its tangible benefits could be

39

showcased. However, there is pressing need for successful movement in the state to

benefit the marginalized section of the state and bring more inclusive growth. The lessons

learn so far should be the starting point for bringing innovation in the designs and

implementation of existing and prospective SHG specific programme.

40

References

1. Ajay tankha (2012), “Banking on Self-help Groups Twenty Years On”, Sage

Publications.Annual Report (2013), Ministry of Rural Development, Government of

India.

2. Ahlin, Christian and Neville Jiang (2005), “Can Micro-credit bring development?”,

Working Paper No. 05-W19, Department of Economics, Vanderbilt University, Nshville,

July.

3. Annual Report (2013), Ministry of Rural Development, Government of India.

4. Greaney, Brian, Joseph P. Kaboski and Eva Van Leemput (2013), “Can Self-Help

Groups Really Be Self-Help?”, Working Paper Series, Research Division, Federal

Reserve Bank of St. Louis, April.

5. Financial Inclusion: Technology, Institutions and Policies (Keynote address delivered by

Dr. Raghuram Rajan, Governor, Reserve Bank of India, at the NASSCOM India

Leadership Forum in Mumbai on February 12, 2014)

6. Mansuri, Ghazala and Vijayendra Rao (2013), “Localizing development: Does

participation work?”, A World Bank Policy Research Report, The World Bank,

Washington.

7. Status of microfinance in India- 2012-13, NABARD (2013).

8. Vikas Batra (2012), “Self help group movement in rural Haryana: An analysis of trends,

patterns and schemes”, School of Management Science Varanasi, Vol. VIII, No. 2,

December.