Embed Size (px)

Citation preview

Spraberry Investor PresentationSeptember 2008

2

Forward-Looking StatementsExcept for historical information contained herein, the statements, charts and graphs in this presentation are forward-looking statements that are made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements and the business prospects of Pioneer are subject to a number of risks and uncertainties that may cause Pioneer's actual results in future periods to differ materially from the forward-looking statements. These risks and uncertainties include, among other things, volatility of commodity prices, product supply and demand, competition, the ability to obtain environmental and other permits and the timing thereof, other government regulation or action, the ability to obtain approvals from third parties and negotiate agreements with third parties on acceptable terms, international operations and associated international political and economic instability, litigation, the costs and results of drilling and operations, access to and availability of drilling equipment and transportation, processing and refining facilities, Pioneer's ability to replace reserves, implement its business plans or complete its development activities as scheduled, access to and cost of capital, uncertainties about estimates of reserves and resource potential and the ability to add proved reserves in the future, the assumptions underlying production forecasts, quality of technical data, environmental and weather risks, and acts of war or terrorism. These and other risks are described in Pioneer's 10-K and 10-Q Reports and other filings with the Securities and Exchange Commission. In addition, Pioneer may be subject to currently unforeseen risks that may have a materially adverse impact on it. Pioneer undertakes no duty to publicly update these statements except as required by law.

Please see the appendix slides included in this presentation for other important information.

3

SPRABERRY OVERVIEW

4

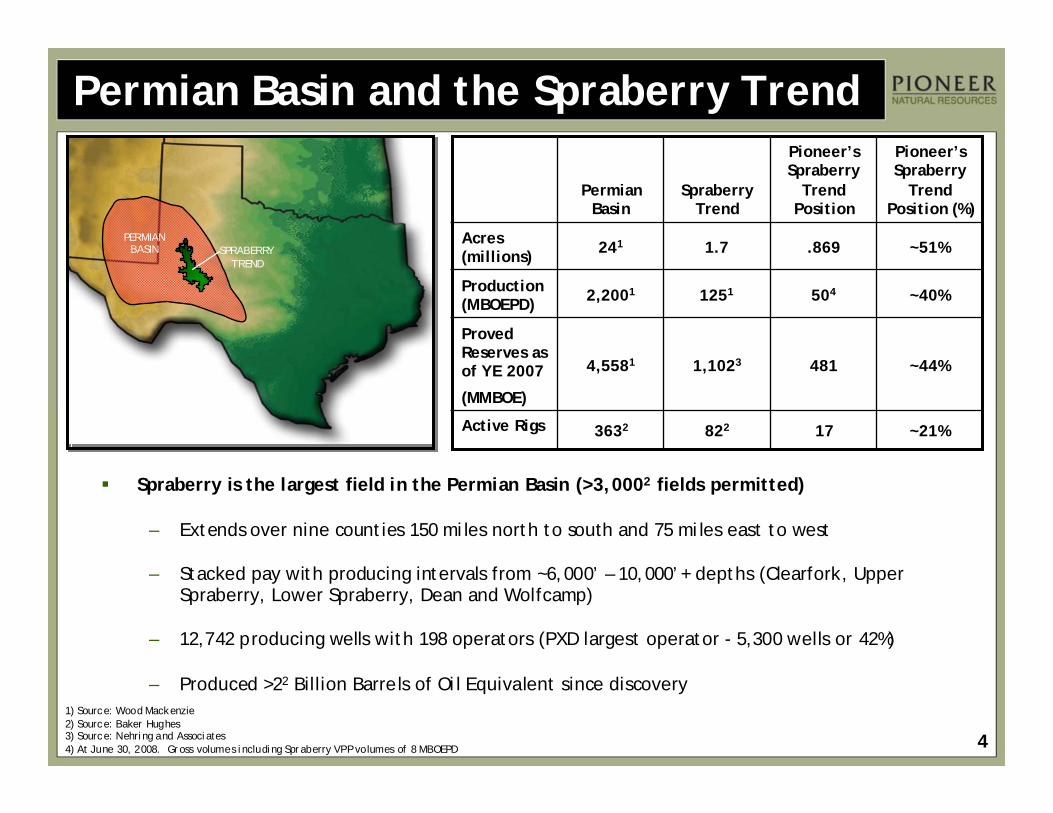

Permian Basin and the Spraberry Trend

~21%178223632Active Rigs

~44%

~40%

~51%

Pioneer’s Spraberry

Trend Position (%)

481

504

.869

Pioneer’s Spraberry

Trend Position

1,10234,5581

Proved Reserves as of YE 2007

(MMBOE)

12512,2001Production (MBOEPD)

1.7241Acres (millions)

Spraberry Trend

Permian Basin

Spraberry is the largest field in the Permian Basin (>3,0002 fields permitted)

– Extends over nine counties 150 miles north to south and 75 miles east to west

– Stacked pay with producing intervals from ~6,000’ – 10,000’+ depths (Clearfork, Upper Spraberry, Lower Spraberry, Dean and Wolfcamp)

– 12,742 producing wells with 198 operators (PXD largest operator - 5,300 wells or 42%)

– Produced >22 Billion Barrels of Oil Equivalent since discovery1) Source: Wood Mackenzie2) Source: Baker Hughes3) Source: Nehring and Associates 4) At June 30, 2008. Gross volumes including Spraberry VPP volumes of 8 MBOEPD

PERMIAN BASIN SPRABERRY

TREND

5

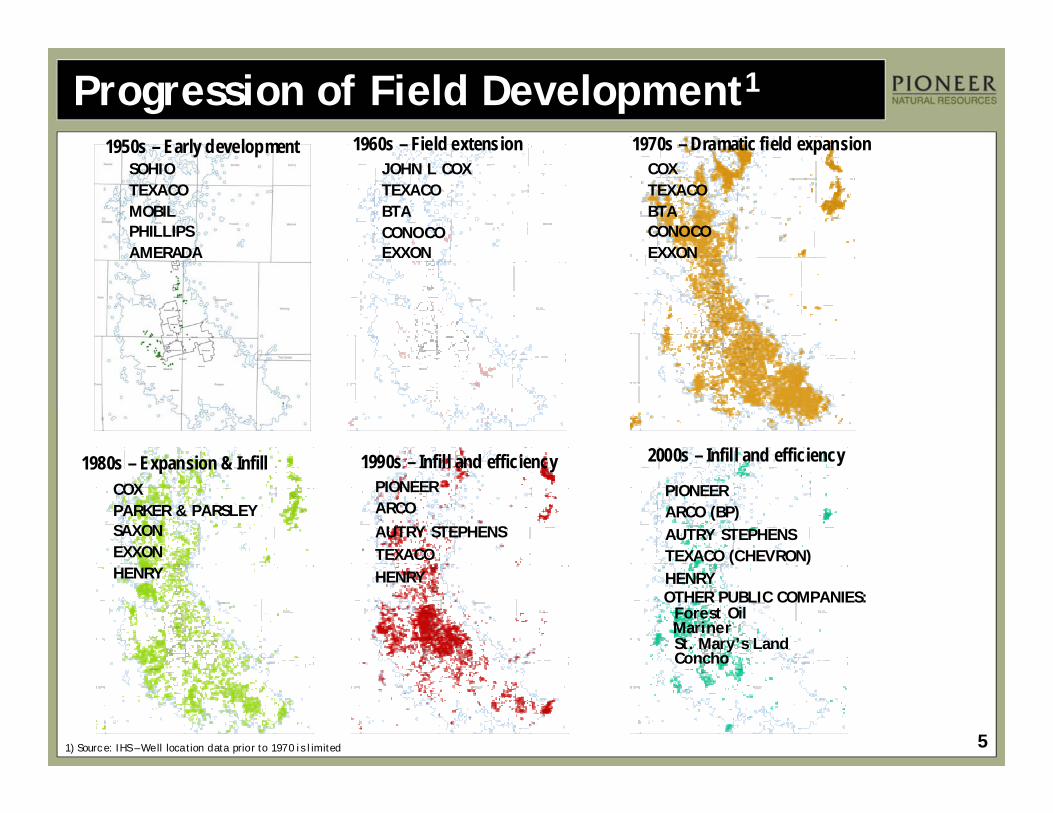

1950s – Early developmentSOHIOTEXACOMOBILPHILLIPSAMERADA

1960s – Field extensionJOHN L COXTEXACOBTACONOCOEXXON

1970s – Dramatic field expansionCOXTEXACOBTACONOCOEXXON

1980s – Expansion & InfillCOXPARKER & PARSLEYSAXONEXXONHENRY

1990s – Infill and efficiencyPIONEERARCOAUTRY STEPHENSTEXACOHENRY

2000s – Infill and efficiency

PIONEERARCO (BP)AUTRY STEPHENSTEXACO (CHEVRON)HENRY

Progression of Field Development1

OTHER PUBLIC COMPANIES:Forest OilMarinerSt. Mary’s LandConcho

1) Source: IHS – Well location data prior to 1970 is limited

6

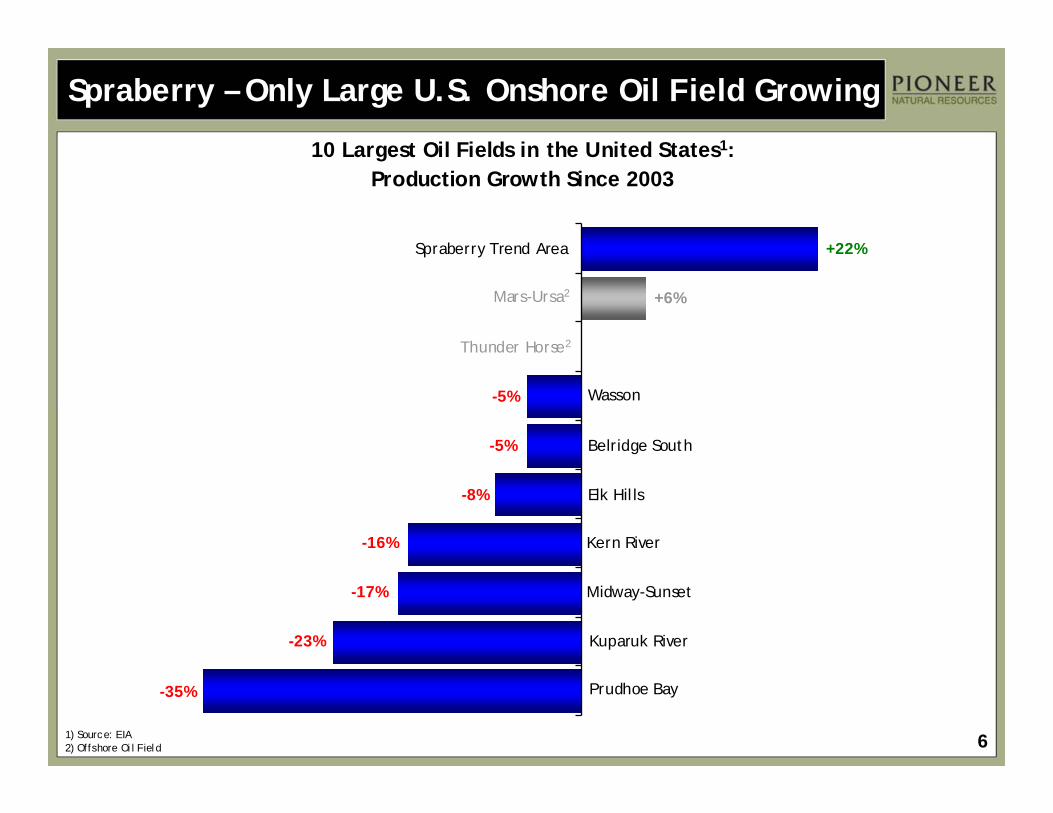

Spraberry – Only Large U.S. Onshore Oil Field Growing

10 Largest Oil Fields in the United States1:Production Growth Since 2003

Spraberry Trend Area

Mars-Ursa2

Thunder Horse2

Wasson

Belridge South

Elk Hills

Kern River

Midway-Sunset

Kuparuk River

Prudhoe Bay

+22%

+6%

-5%

-8%

-16%

-17%

-23%

-35%

1) Source: EIA2) Offshore Oil Field

-5%

7

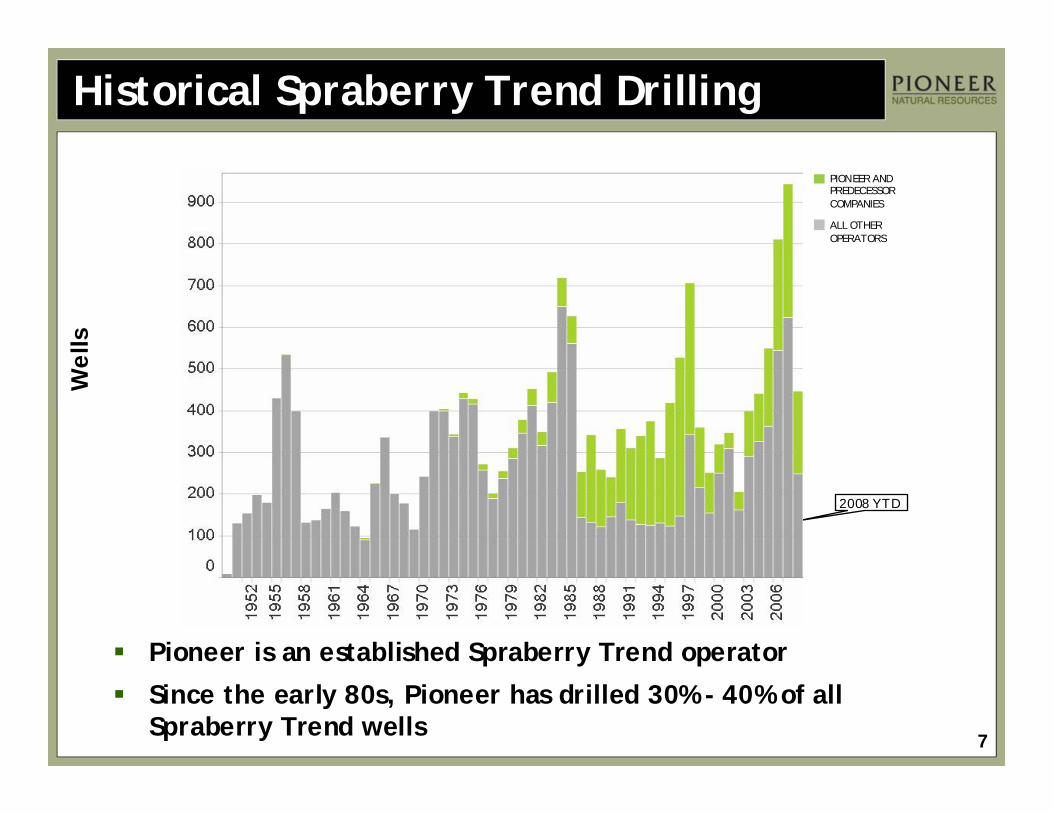

Historical Spraberry Trend Drilling

Pioneer is an established Spraberry Trend operator

Since the early 80s, Pioneer has drilled 30% - 40% of all Spraberry Trend wells

Wel

ls

2008 YTD

PIONEER AND PREDECESSOR COMPANIES

ALL OTHER OPERATORS

8

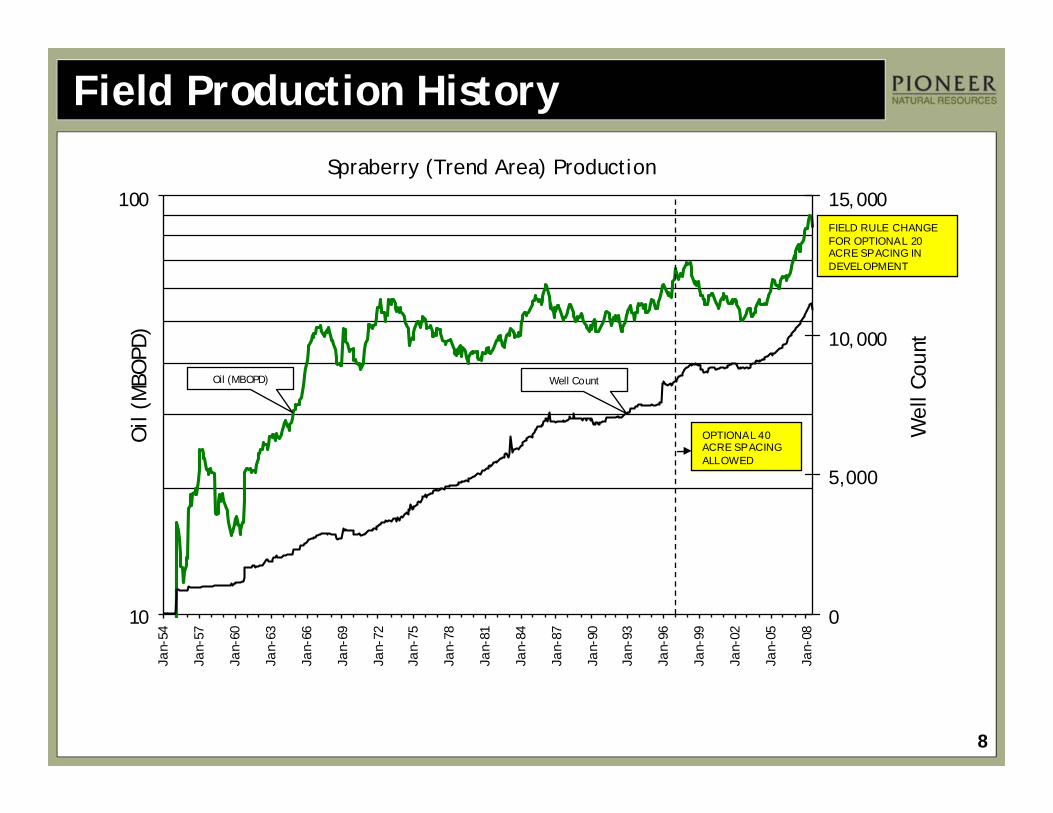

Field Production History

10

100

Jan-

54

Jan-

57

Jan-

60

Jan-

63

Jan-

66

Jan-

69

Jan-

72

Jan-

75

Jan-

78

Jan-

81

Jan-

84

Jan-

87

Jan-

90

Jan-

93

Jan-

96

Jan-

99

Jan-

02

Jan-

05

Jan-

08

0

5,000

10,000

15,000

Spraberry (Trend Area) ProductionO

il (M

BOPD

)

Wel

l Cou

nt

Oil (MBOPD) Well Count

OPTIONAL 40 ACRE SPACING ALLOWED

FIELD RULE CHANGE FOR OPTIONAL 20 ACRE SPACING IN DEVELOPMENT

9

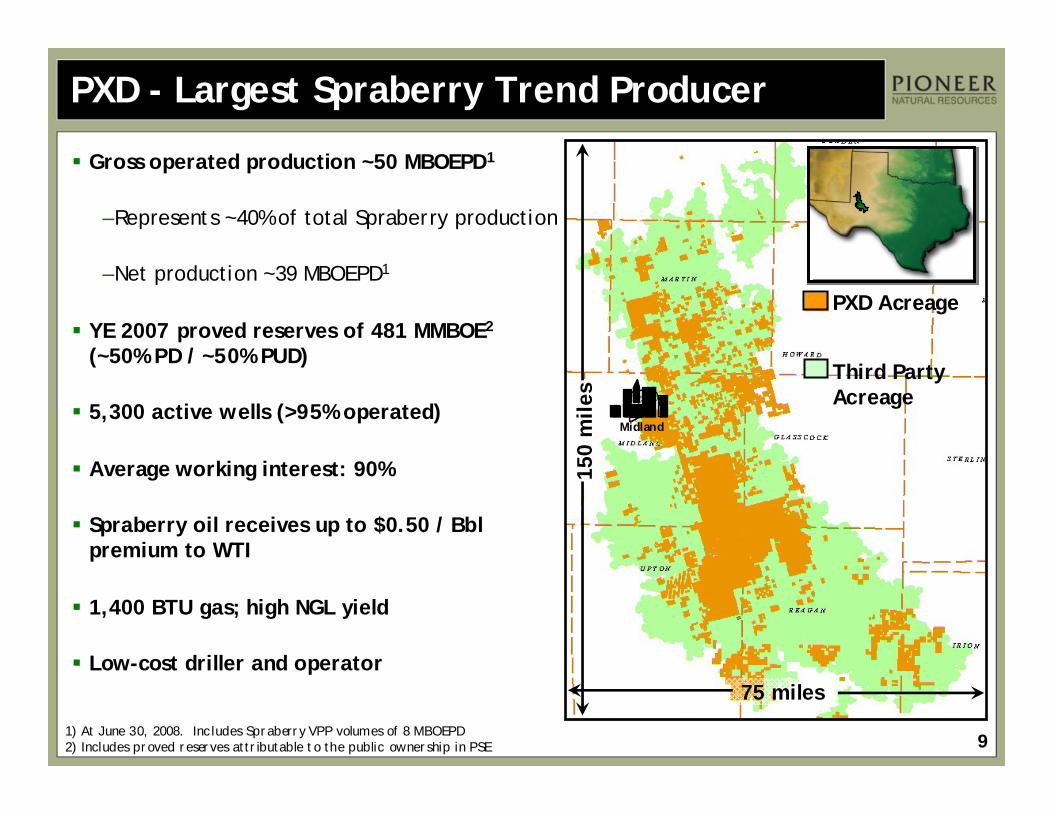

PXD - Largest Spraberry Trend Producer

Gross operated production ~50 MBOEPD1

–Represents ~40% of total Spraberry production

–Net production ~39 MBOEPD1

YE 2007 proved reserves of 481 MMBOE2

(~50% PD / ~50% PUD)

5,300 active wells (>95% operated)

Average working interest: 90%

Spraberry oil receives up to $0.50 / Bbl premium to WTI

1,400 BTU gas; high NGL yield

Low-cost driller and operator

1) At June 30, 2008. Includes Spraberry VPP volumes of 8 MBOEPD2) Includes proved reserves attr ibutable to the public ownership in PSE

Midland

(869,000 gross acres)

PXD Acreage

150

mile

s

75 miles

Third Party Acreage

Midland

10

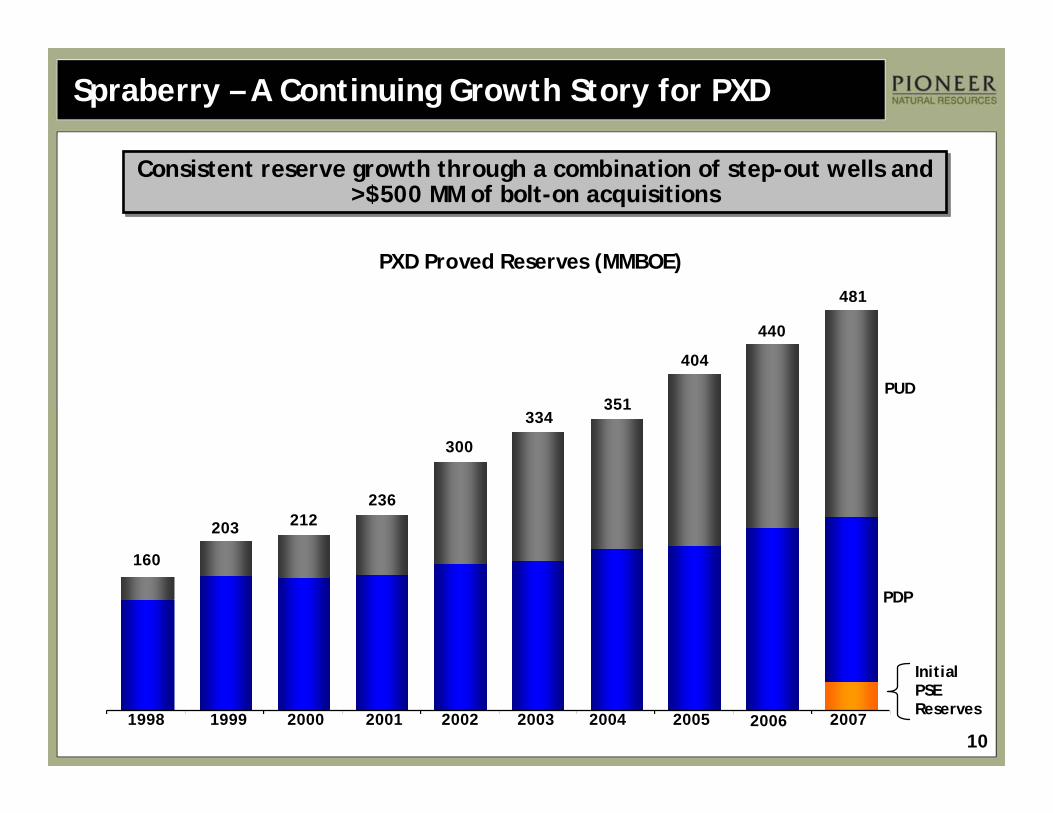

Spraberry – A Continuing Growth Story for PXD

PXD Proved Reserves (MMBOE)

Consistent reserve growth through a combination of step-out wells and >$500 MM of bolt-on acquisitions

Consistent reserve growth through a combination of step-out wells and >$500 MM of bolt-on acquisitions

Initial PSE Reserves

PDP

PUD

20072005200420032001 2002200019991998

440

404

351334

236

300

212203

160

2006

481

11

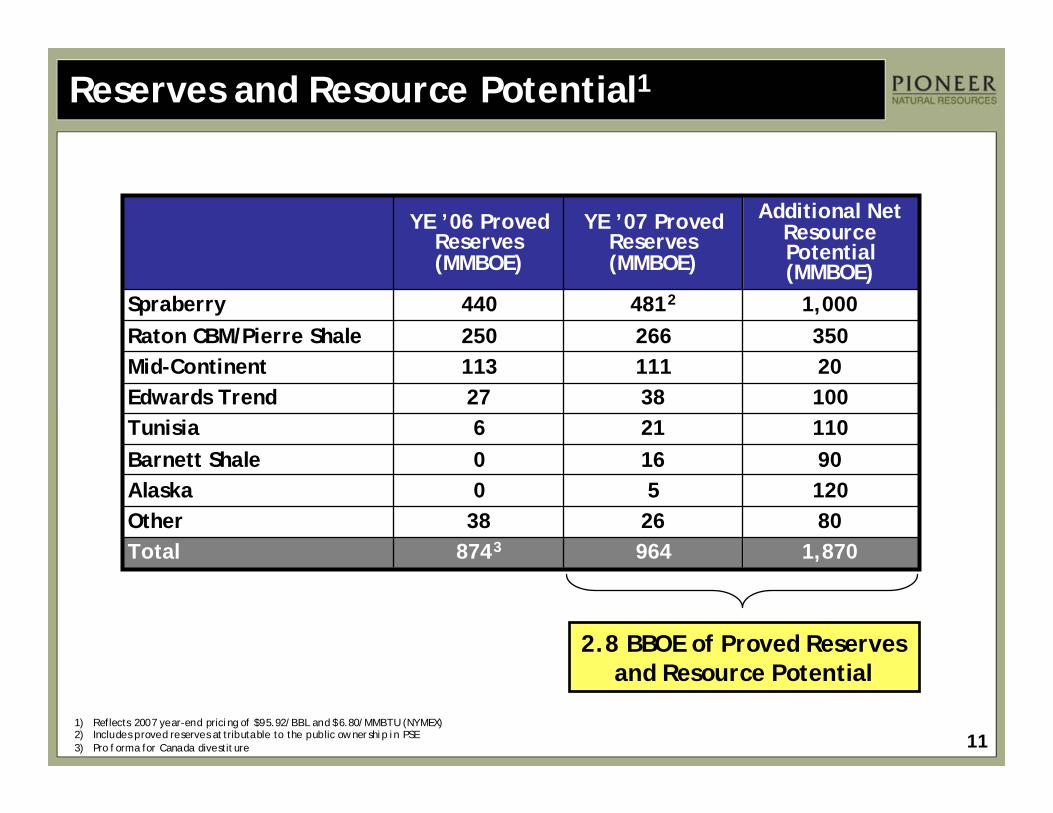

Reserves and Resource Potential1

8743

38006

27113250440

YE ’06 Proved Reserves (MMBOE)

1205Alaska8026Other

964

1621381112664812

YE ’07 Proved Reserves(MMBOE)

1,870Total

Additional Net Resource Potential(MMBOE)

20Mid-Continent

90110100

3501,000

Barnett ShaleTunisiaEdwards Trend

Raton CBM/Pierre ShaleSpraberry

1) Reflects 2007 year-end pricing of $95.92/BBL and $6.80/MMBTU (NYMEX)2) Includes proved reserves attributable to the public ownership in PSE3) Pro forma for Canada divestiture

2.8 BBOE of Proved Reserves and Resource Potential

12

Spraberry – Progressing Resource Initiatives

Ongoing 40-acre field development (additional net resource potential: 200 MMBOE)

– ~70 unbooked well locations drilled YTD including deeper Wolfcamp

– Excludes YE 2007 proved undeveloped reserves of 248 MMBOE (~210 wells drilled YTD)

20-acre spacing (additional net resource potential: 500 MMBOE)

– Commenced drilling remainder of 25-well program with dedicated rig

– >120 days of production from first 3 wells continues to support at least 75% - 80% of 40-acre EUR recovery assumption

– Planning to drill a minimum of 40 wells in 2009

– Applying for field rule changes with Texas Railroad Commission in Q3 to allow fieldwide down-spacing

Waterflood (additional net resource potential: 300 MMBOE)

– Identified ~12,000-acre area under two existing units for large scale project in 2009

– Planning to drill 20 – 35 water injection wells and construct facilities during 1H 2009

– Water injection expected to begin Q3 2009 with initial response anticipated 6 – 9 months thereafter

Actively progressing initiatives to capture additional 1 BBOE net resource potentialActively progressing initiatives to capture additional 1 BBOE net resource potential

13

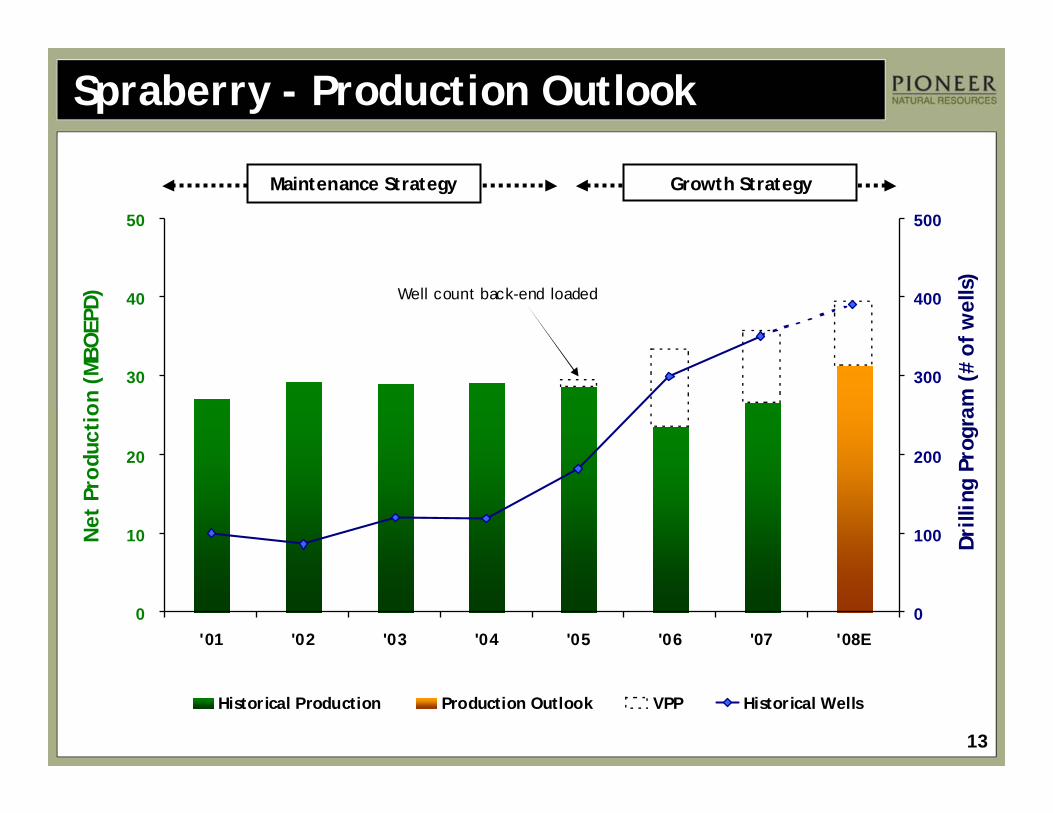

Spraberry - Production Outlook

0

10

20

30

40

50

'01 '02 '03 '04 '05 '06 '07 '08E0

100

200

300

400

500

Historical Production Production Outlook VPP Historical Wells

Net

Pro

duct

ion

(MBO

EPD)

Dri

lling

Pro

gram

(#

of

wel

ls)

Maintenance Strategy

Well count back-end loaded

Growth Strategy

14

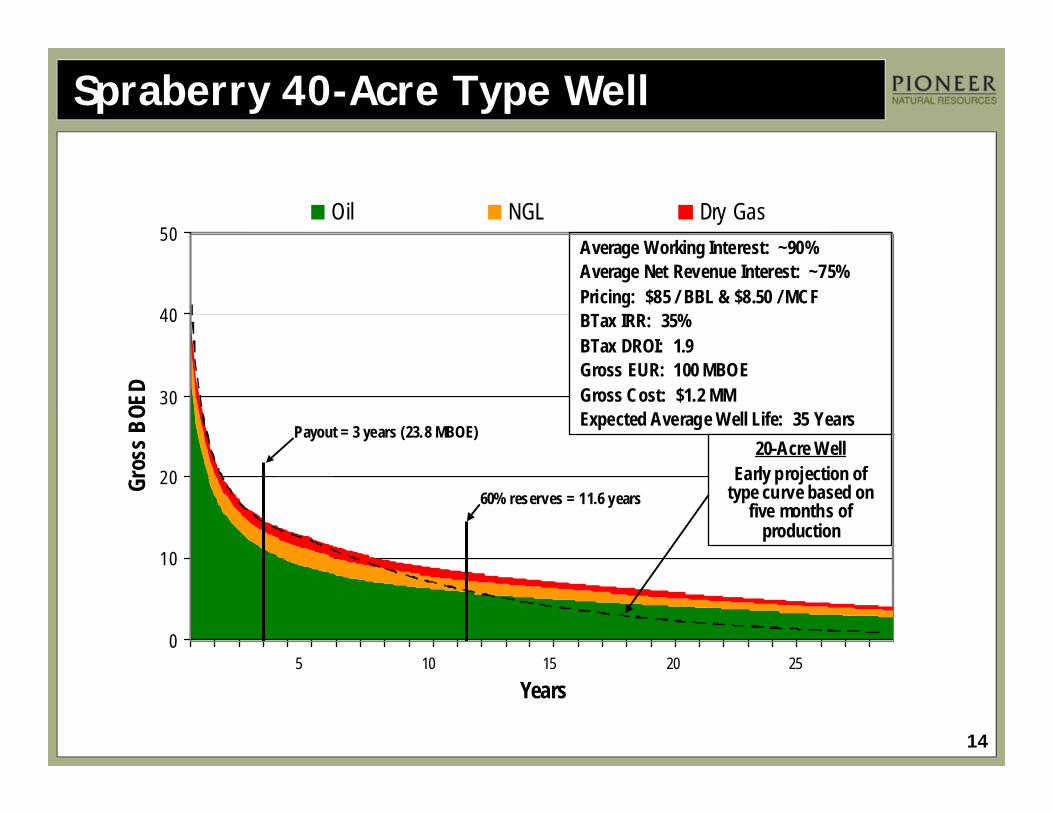

Spraberry 40-Acre Type Well

0

10

20

30

40

50

Years

Gros

s BOE

D

Oil NGL Dry Gas

Payout = 3 years (23.8 MBOE)

5 10 15 20 25

Average Working Interest: ~90%Average Net Revenue Interest: ~75% Pricing: $85 / BBL & $8.50 / MCFBTax IRR: 35%BTax DROI: 1.9Gross EUR: 100 MBOEGross Cost: $1.2 MMExpected Average Well Life: 35 Years

60% reserves = 11.6 years

20-Acre WellEarly projection of

type curve based on five months of

production

15

SPRABERRY GEOLOGY

16

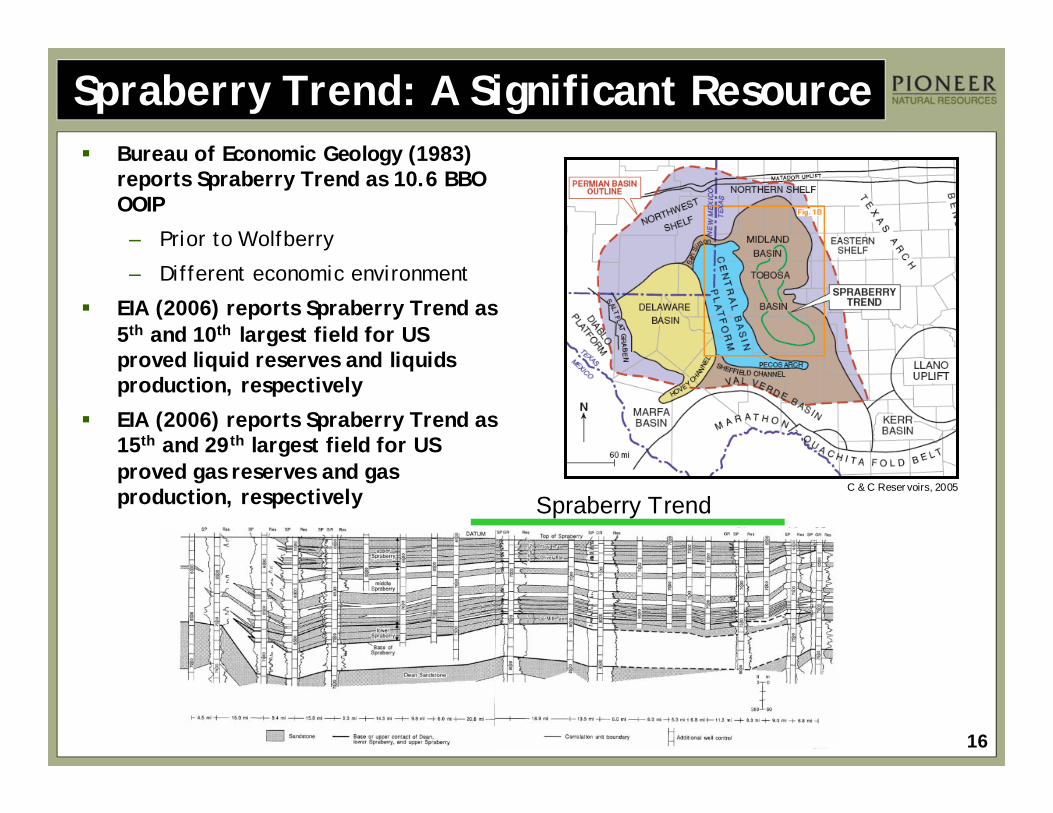

Spraberry Trend: A Significant ResourceBureau of Economic Geology (1983) reports Spraberry Trend as 10.6 BBO OOIP

– Prior to Wolfberry

– Different economic environment

EIA (2006) reports Spraberry Trend as 5th and 10th largest field for US proved liquid reserves and liquids production, respectively

EIA (2006) reports Spraberry Trend as 15th and 29th largest field for US proved gas reserves and gas production, respectively C & C Reser voirs, 2005

Spraberry Trend

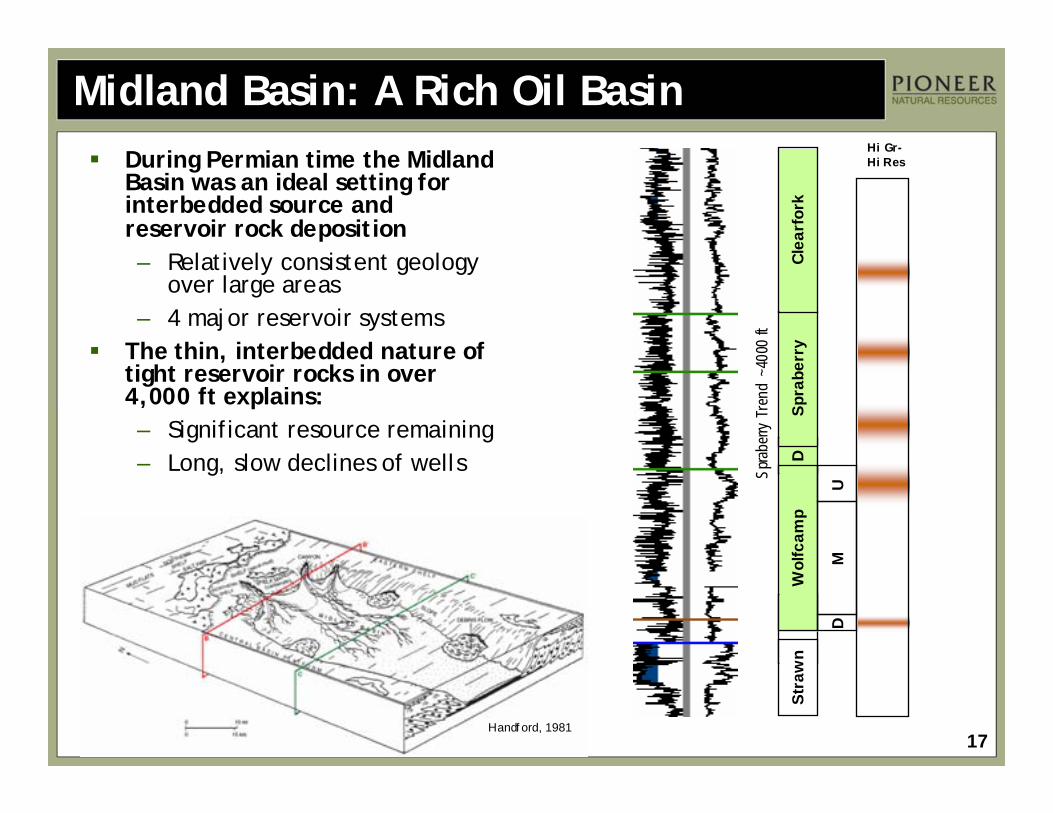

17

Midland Basin: A Rich Oil BasinDuring Permian time the Midland Basin was an ideal setting for interbedded source and reservoir rock deposition– Relatively consistent geology

over large areas– 4 major reservoir systems

The thin, interbedded nature of tight reservoir rocks in over 4,000 ft explains: – Significant resource remaining– Long, slow declines of wells D

Stra

wn

Wol

fcam

pSp

rabe

rry

Clea

rfor

k

UM

D

Hi Gr-Hi Res

Sprab

erry

Tren

d ~4

000

ft

Handf ord, 1981

18

2008 PXD Acreage

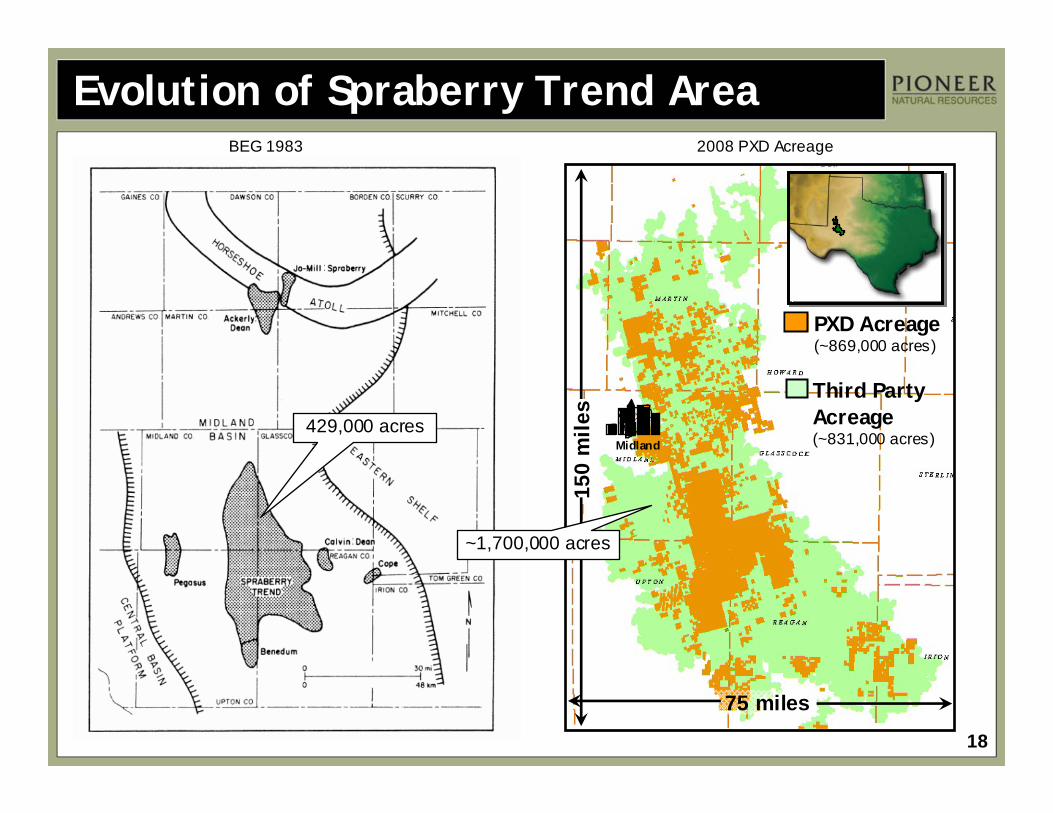

Evolution of Spraberry Trend AreaBEG 1983

429,000 acres

PXD Acreage

150

mile

s

75 miles

Third Party Acreage

Midland

(~869,000 acres)

(~831,000 acres)

~1,700,000 acres

19

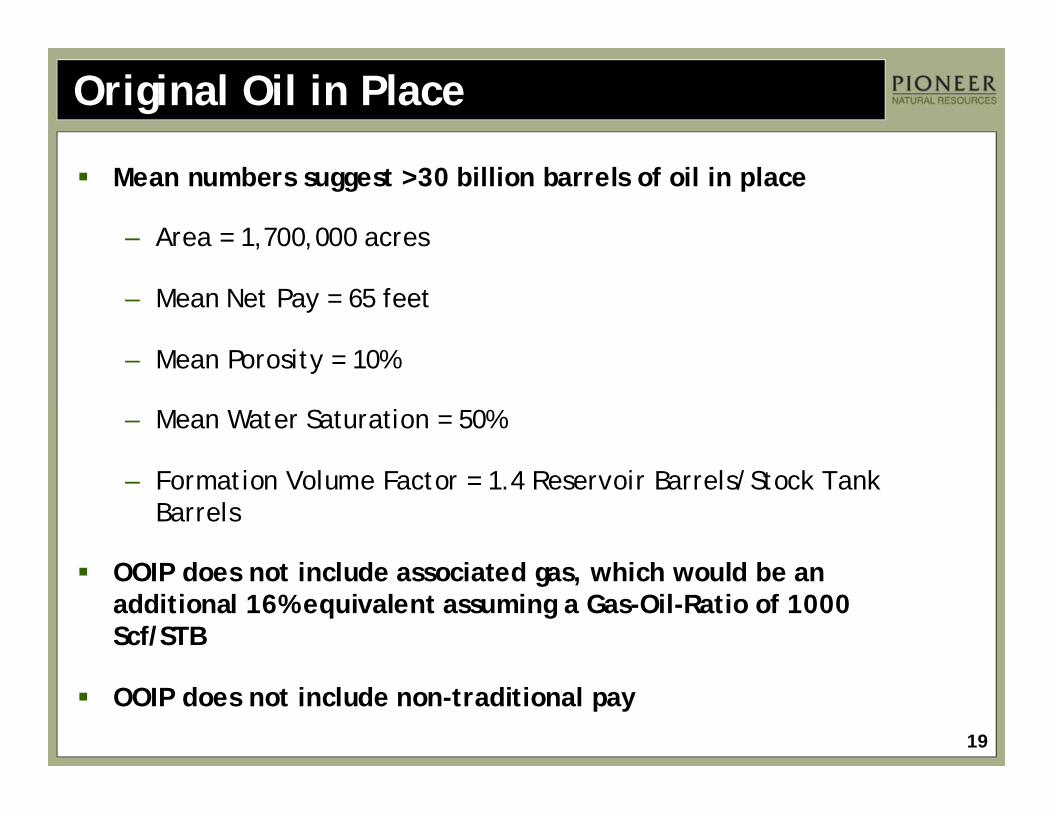

Original Oil in Place

Mean numbers suggest >30 billion barrels of oil in place

– Area = 1,700,000 acres

– Mean Net Pay = 65 feet

– Mean Porosity = 10%

– Mean Water Saturation = 50%

– Formation Volume Factor = 1.4 Reservoir Barrels/Stock Tank Barrels

OOIP does not include associated gas, which would be an additional 16% equivalent assuming a Gas-Oil-Ratio of 1000 Scf/STB

OOIP does not include non-traditional pay

20

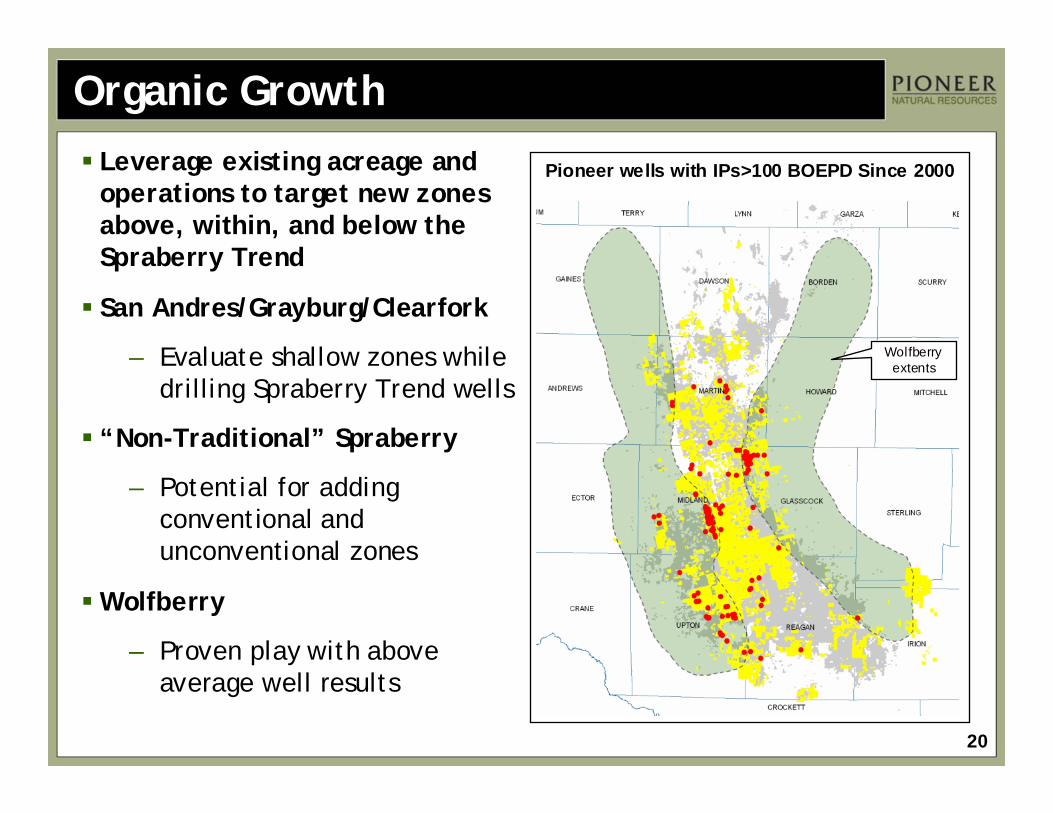

Organic GrowthLeverage existing acreage and operations to target new zones above, within, and below the Spraberry Trend

San Andres/Grayburg/Clearfork

– Evaluate shallow zones while drilling Spraberry Trend wells

“Non-Traditional” Spraberry

– Potential for adding conventional and unconventional zones

Wolfberry

– Proven play with above average well results

Wolfberry extents

Pioneer wells with IPs>100 BOEPD Since 2000

21

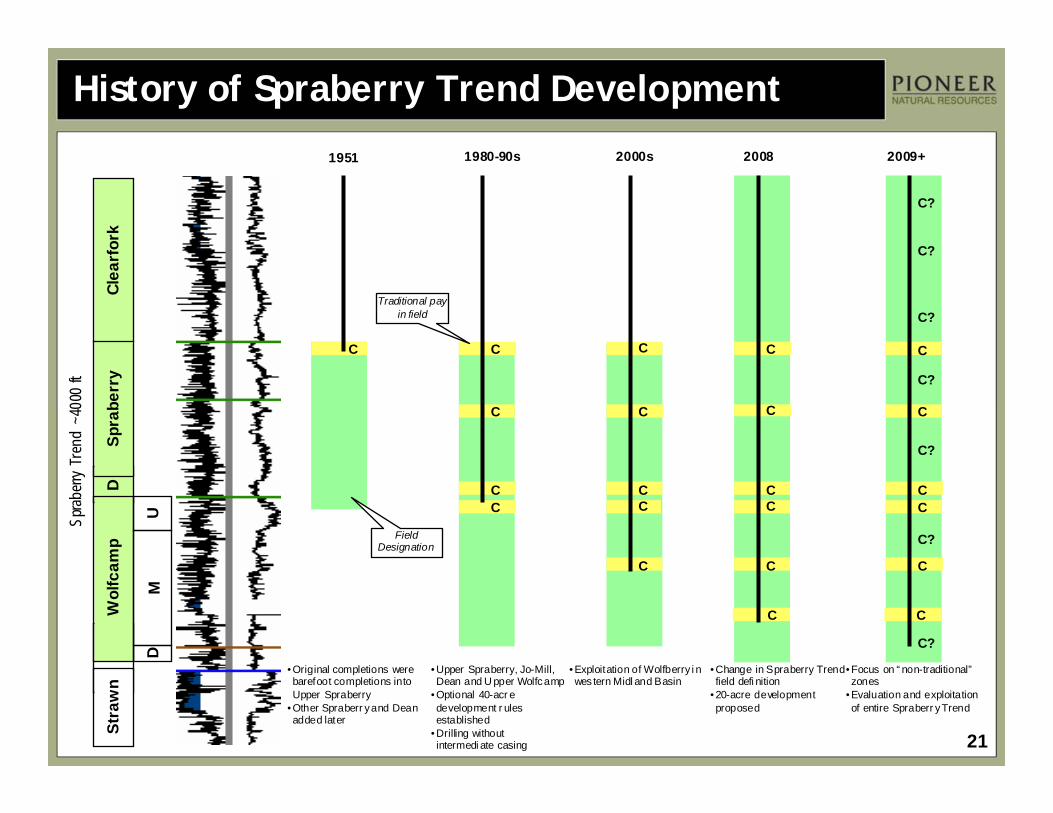

History of Spraberry Trend DevelopmentD

Stra

wn

Wol

fcam

pSp

rabe

rry

Clea

rfor

k

UM

D

Sprab

erry

Tren

d ~4

000

ft

C

1951

C

1980-90s

C

CC

C

C

CC

2000s

• Exploitation of Wolfberry i n wes tern Midl and Basin

C

2008

• Change in Spraberry Trend field defi nition

• 20-acre development proposed

2009+

• Upper Spraberry, Jo-Mill, Dean and U pper Wolfcamp

• Optional 40-acr e development r ules established

• Drilling without intermedi ate casing

• Focus on “ non-traditional”zones

• Evaluation and exploitation of entire Spraberr y Trend

• Original completions were barefoot completions into Upper Spraberry

• Other Spraberr y and Dean added later

C

C

CC

C

C

C

C

CC

C

C

C?

C?

C?

C?

C?

C?

Traditional pay in field

Field Designation

C?

22

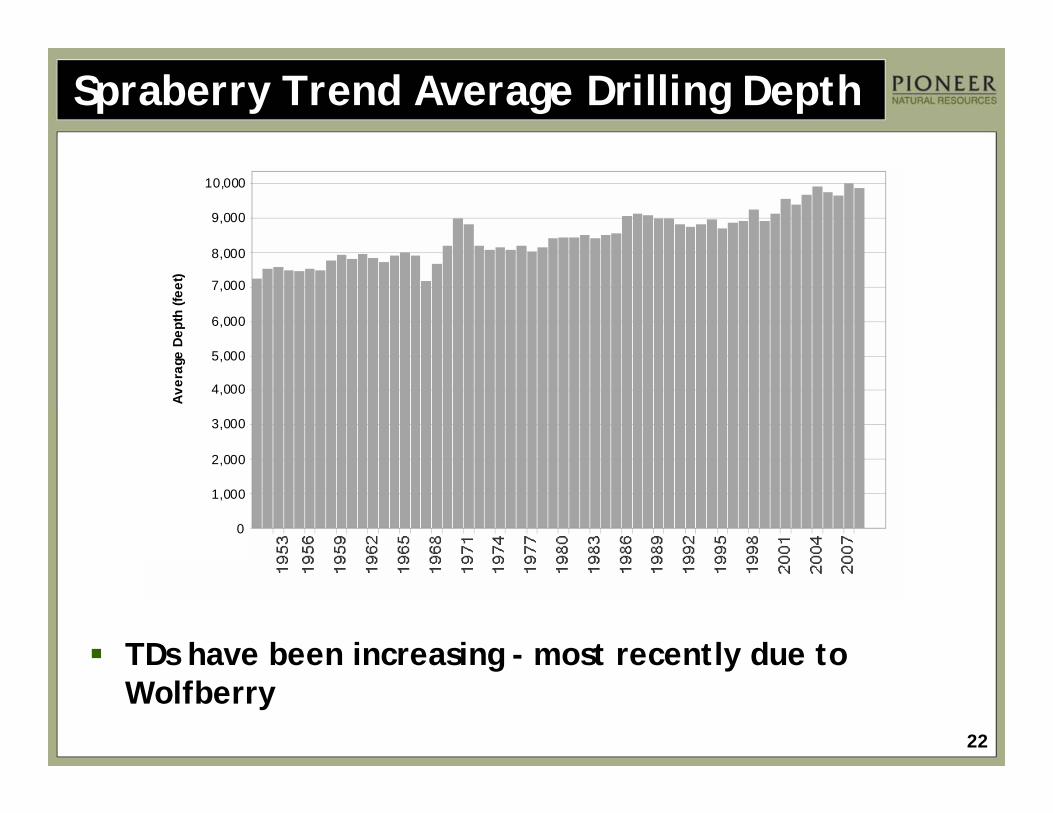

Spraberry Trend Average Drilling Depth

TDs have been increasing - most recently due to Wolfberry

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000A

vera

ge D

epth

(fee

t)

23

Spraberry Trend

Limestone

Sandstone

Non‐Organic Shale

Organic Rich Shale

~700

ft

~1,500

ft

Clearfork

Dean

Upp

er

Sprabe

rry

Wolfcam

p

~300

ft

~1,500

ft

~4,000’

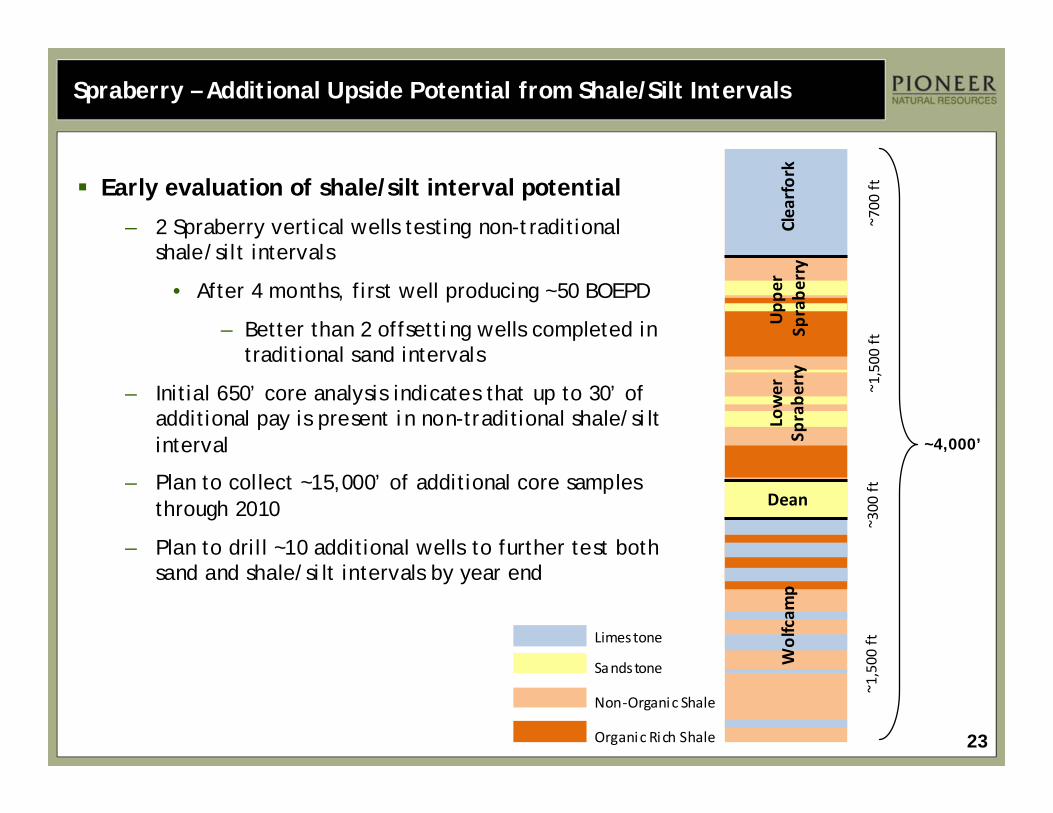

Early evaluation of shale/silt interval potential

– 2 Spraberry vertical wells testing non-traditional shale/silt intervals

• After 4 months, first well producing ~50 BOEPD

– Better than 2 offsetting wells completed in traditional sand intervals

– Initial 650’ core analysis indicates that up to 30’ of additional pay is present in non-traditional shale/silt interval

– Plan to collect ~15,000’ of additional core samples through 2010

– Plan to drill ~10 additional wells to further test both sand and shale/silt intervals by year end

Spraberry – Additional Upside Potential from Shale/Silt Intervals

Lower

Sprabe

rry

24

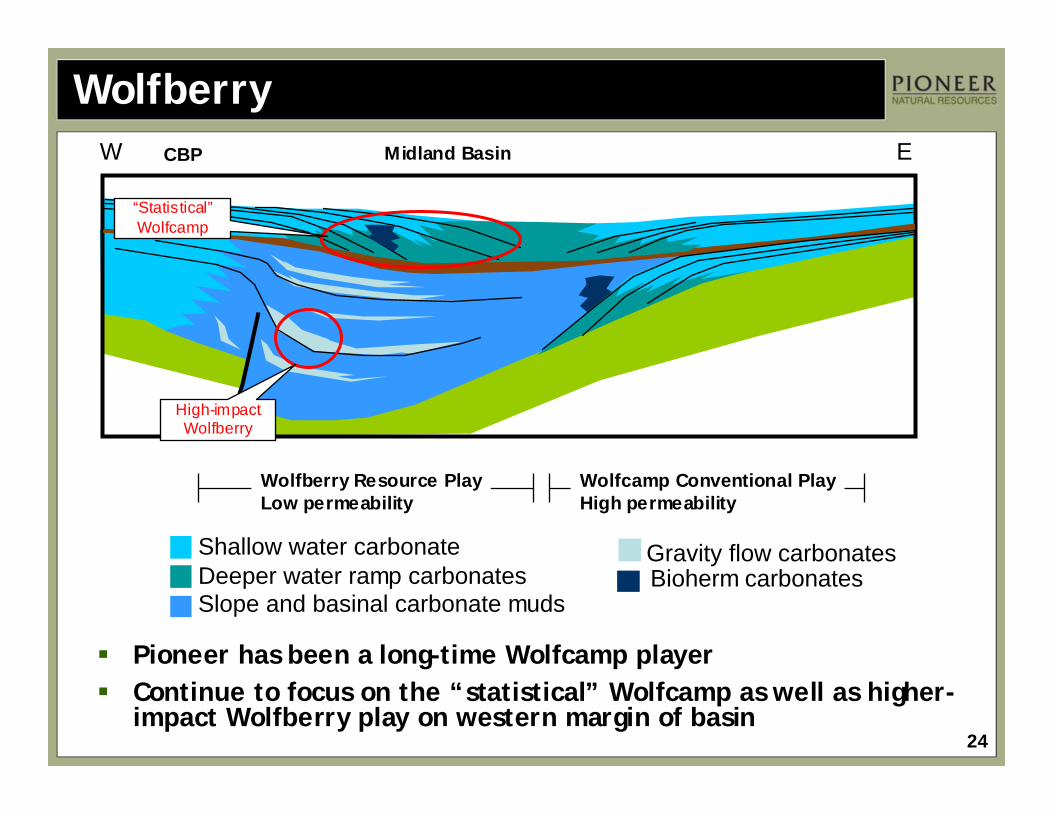

Shallow water carbonate

Slope and basinal carbonate mudsDeeper water ramp carbonates Bioherm carbonates

WolfberryW EMidland BasinCBP

Wolfberry Resource PlayLow permeability

Wolfcamp Conventional PlayHigh permeability

High-impact Wolfberry

“Statistical”Wolfcamp

Gravity flow carbonates

Pioneer has been a long-time Wolfcamp playerContinue to focus on the “statistical” Wolfcamp as well as higher-impact Wolfberry play on western margin of basin

25

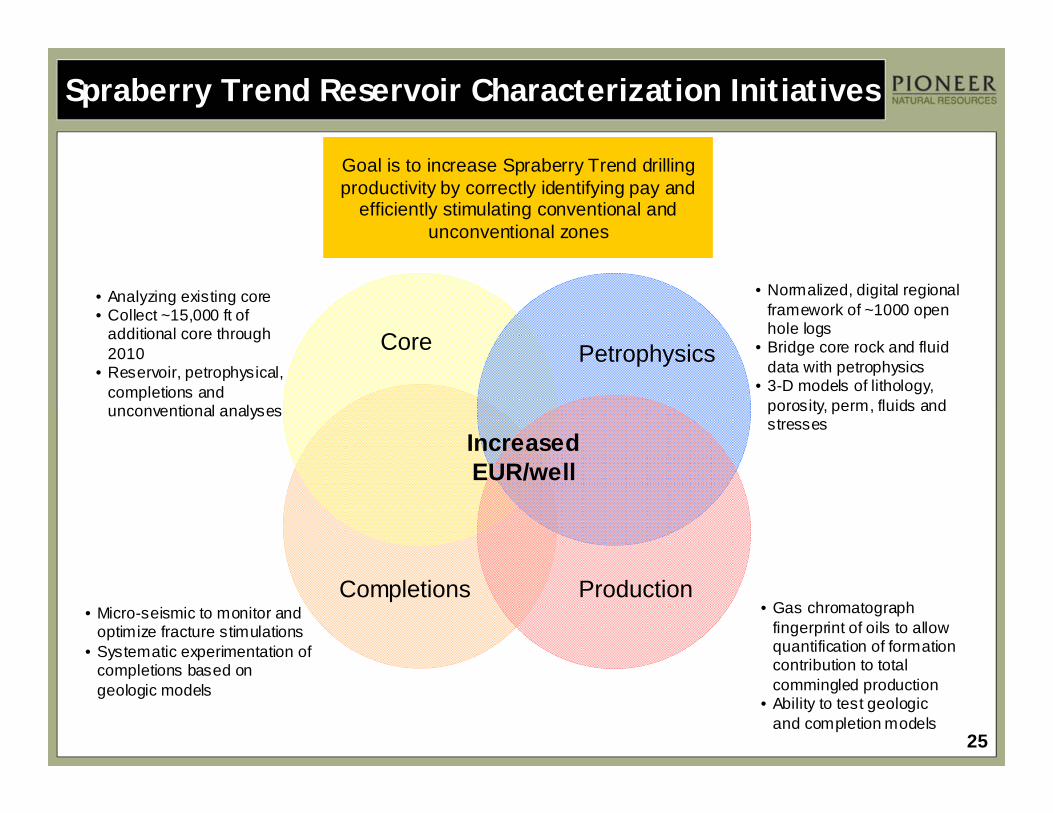

Spraberry Trend Reservoir Characterization Initiatives

IncreasedEUR/well

Core Petrophysics

ProductionCompletions

• Analyzing existing core• Collect ~15,000 ft of

additional core through 2010

• Reservoir, petrophysical, completions and unconventional analyses

• Normalized, digital regional framework of ~1000 open hole logs

• Bridge core rock and fluid data with petrophysics

• 3-D models of lithology, porosity, perm, fluids and stresses

• Gas chromatograph fingerprint of oils to allow quantification of formation contribution to total commingled production

• Ability to test geologic and completion models

• Micro-seismic to monitor and optimize fracture stimulations

• Systematic experimentation of completions based on geologic models

Goal is to increase Spraberry Trend drilling productivity by correctly identifying pay and

efficiently stimulating conventional and unconventional zones

26

SPRABERRY OPERATIONS

27

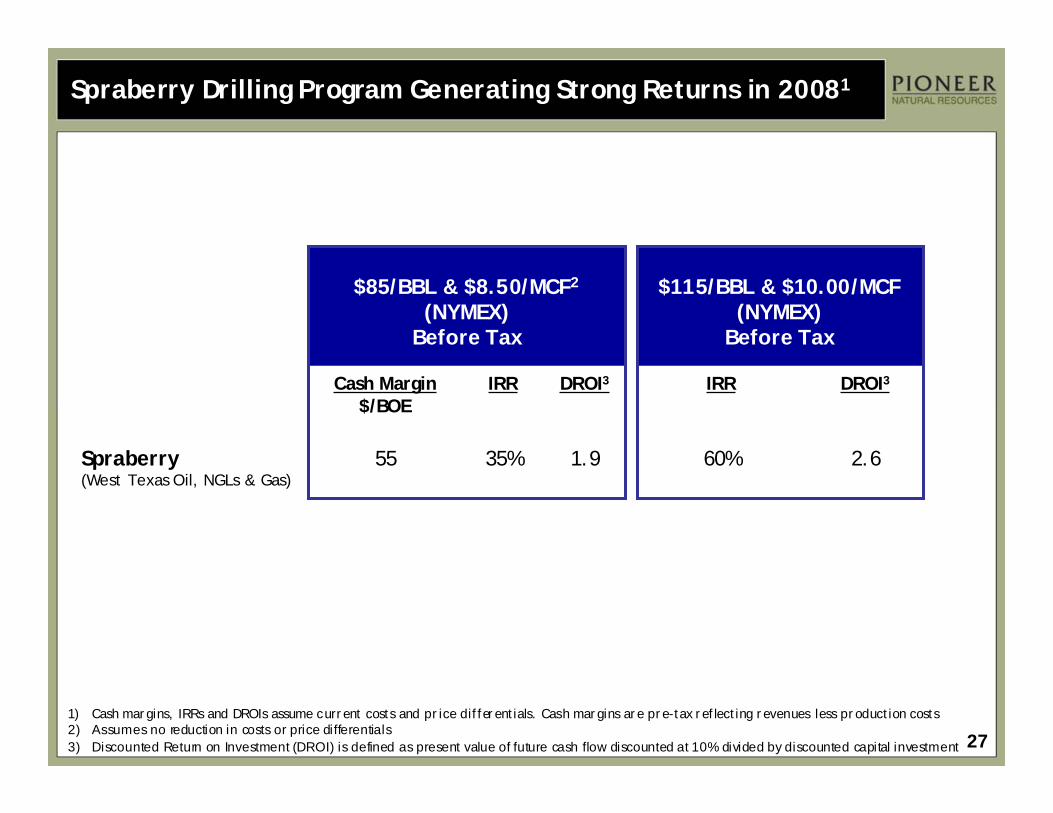

Spraberry Drilling Program Generating Strong Returns in 20081

60%

IRR

$115/BBL & $10.00/MCF (NYMEX)

Before Tax

2.6

DROI3

55

Cash Margin$/BOE

$85/BBL & $8.50/MCF2

(NYMEX)Before Tax

35%

IRR

1.9

DROI3

Spraberry (West Texas Oil, NGLs & Gas)

1) Cash margins, IRRs and DROIs assume current costs and pr ice differentials. Cash margins are pre-tax reflecting revenues less production costs2) Assumes no reduction in costs or price differentials3) Discounted Return on Investment (DROI) is defined as present value of future cash flow discounted at 10% divided by discounted capital investment

28

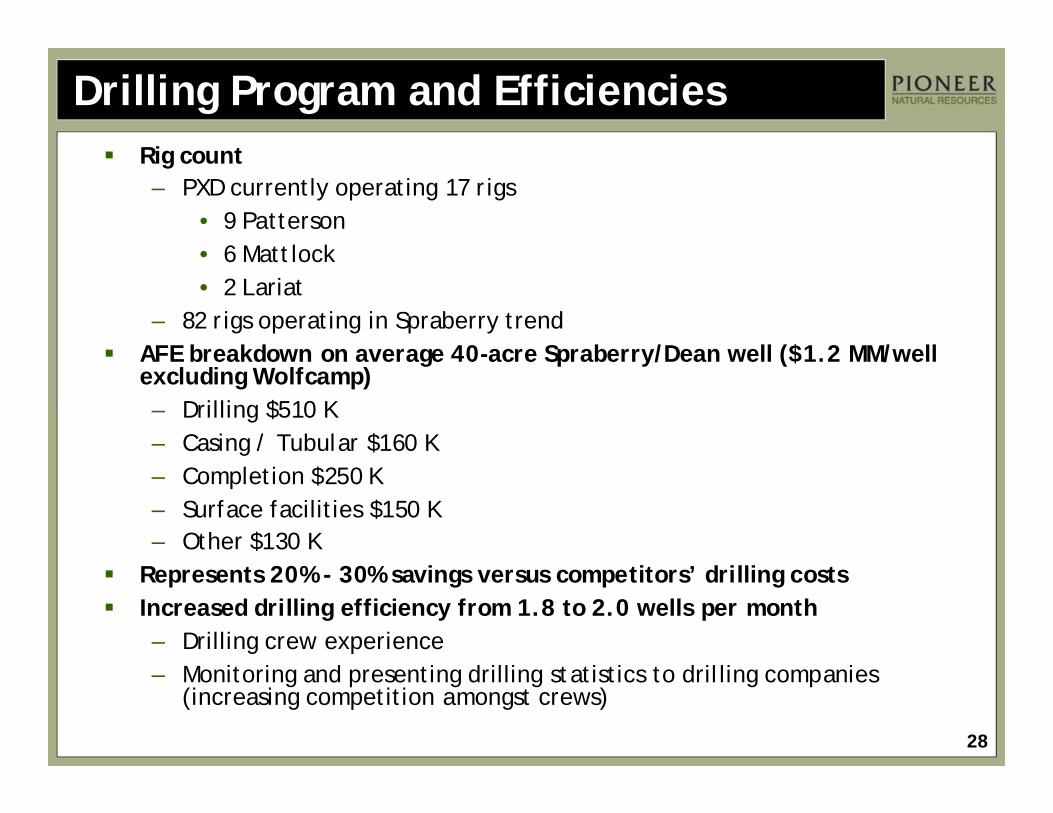

Drilling Program and EfficienciesRig count– PXD currently operating 17 rigs

• 9 Patterson• 6 Mattlock• 2 Lariat

– 82 rigs operating in Spraberry trendAFE breakdown on average 40-acre Spraberry/Dean well ($1.2 MM/well excluding Wolfcamp)– Drilling $510 K– Casing / Tubular $160 K– Completion $250 K– Surface facilities $150 K– Other $130 K

Represents 20% - 30% savings versus competitors’ drilling costsIncreased drilling efficiency from 1.8 to 2.0 wells per month– Drilling crew experience – Monitoring and presenting drilling statistics to drilling companies

(increasing competition amongst crews)

29

Continuing Focus on Field Optimization

Automation

Route Optimization

Rig Scheduling

Training

API Crude Oil Measurement

Thermography Gas Leak Detection

30

Integrated Services and Operating Cost Reduction Initiatives

Currently operating 15 pulling units– ~40% cost savings compared to current market rates

– <2 year payout and >100% IRR

– Utilizing 20 pulling units for well maintenance

• Plan to add additional pulling units in 2009

• Focus on owning enough pulling units to maintain current well inventory

Fishing tools– Operating two reverse rigs

– Small inventory of fishing tools

Currently Operating 250 Frac Tanks– Reduced tank requirements from

350 to 250 due to operational

efficiencies

– Plan to add additional tanks in 2009

due to increased drilling

31

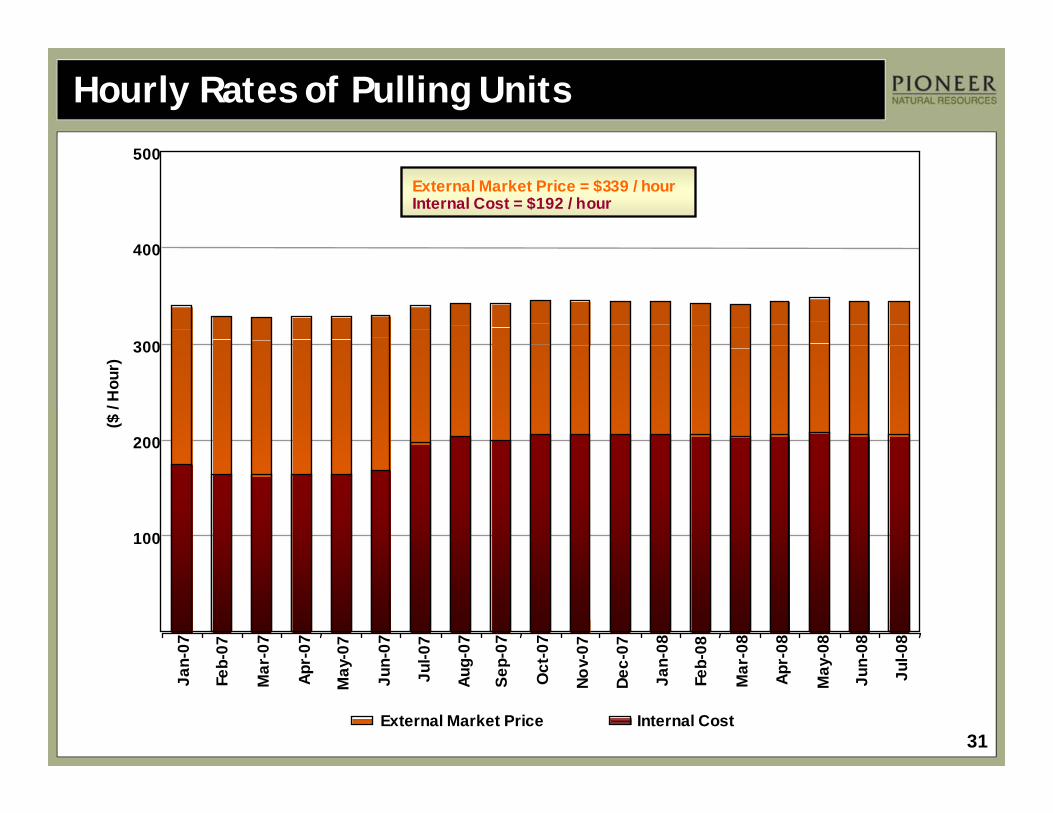

Hourly Rates of Pulling Units($

/ H

our)

100

200

300

400

500

Jan-

07

Feb-

07

Mar

-07

Apr-

07

May

-07

Jun-

07

Jul-0

7

Aug-

07

Sep-

07

Oct

-07

Nov-

07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

External Market Price Internal Cost

External Market Price = $339 / hourInternal Cost = $192 / hour

32

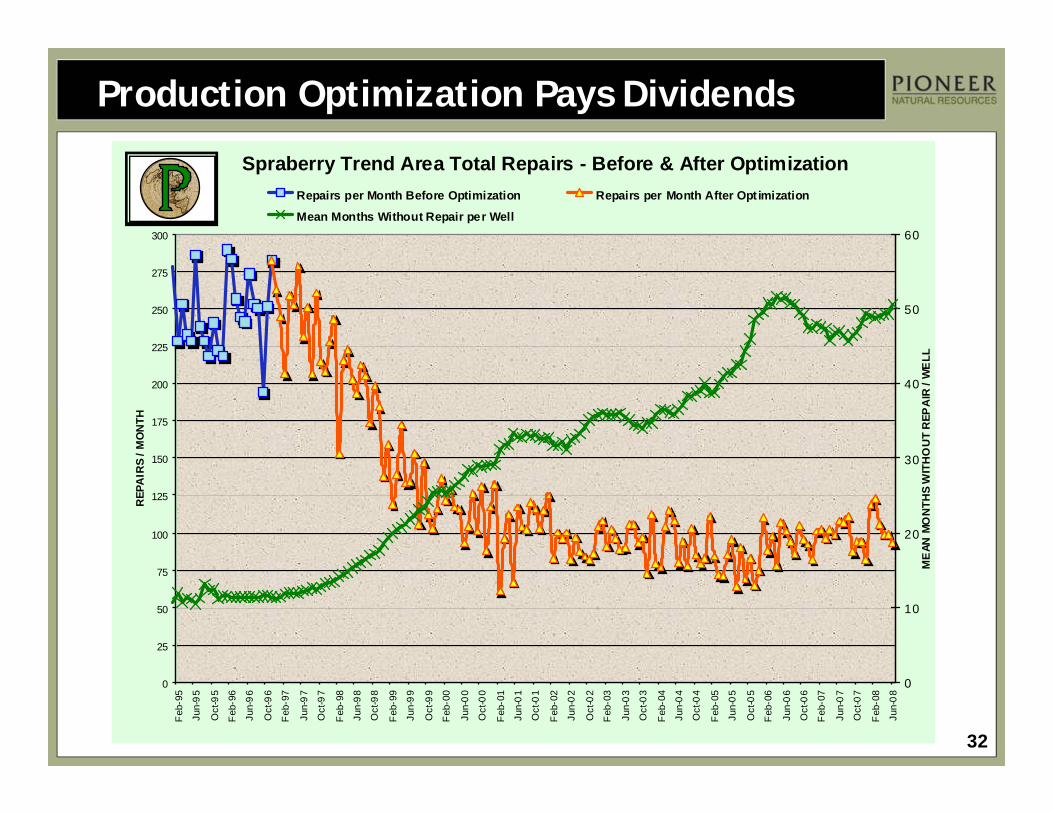

Production Optimization Pays Dividends

Spraberry Trend Area Total Repairs - Before & After Optimization

0

25

50

75

100

125

150

175

200

225

250

275

300

Feb

-95

Jun-

95

Oct

-95

Feb

-96

Jun-

96

Oct

-96

Feb

-97

Jun-

97

Oct

-97

Feb

-98

Jun-

98

Oct

-98

Feb

-99

Jun-

99

Oct

-99

Feb

-00

Jun-

00

Oct

-00

Feb

-01

Jun-

01

Oct

-01

Feb

-02

Jun-

02

Oct

-02

Feb

-03

Jun-

03

Oct

-03

Feb

-04

Jun-

04

Oct

-04

Feb

-05

Jun-

05

Oct

-05

Feb

-06

Jun-

06

Oct

-06

Feb

-07

Jun-

07

Oct

-07

Feb

-08

Jun-

08

REP

AIR

S / M

ON

TH

0

10

20

30

40

50

60

ME

AN M

ON

THS

WIT

HO

UT

REP

AIR

/ W

ELL

Repairs per Month Before Optimization Repairs per Month After Optimization

Mean Months Without Repair per Well

33

SPRABERRY OUTLOOK

34

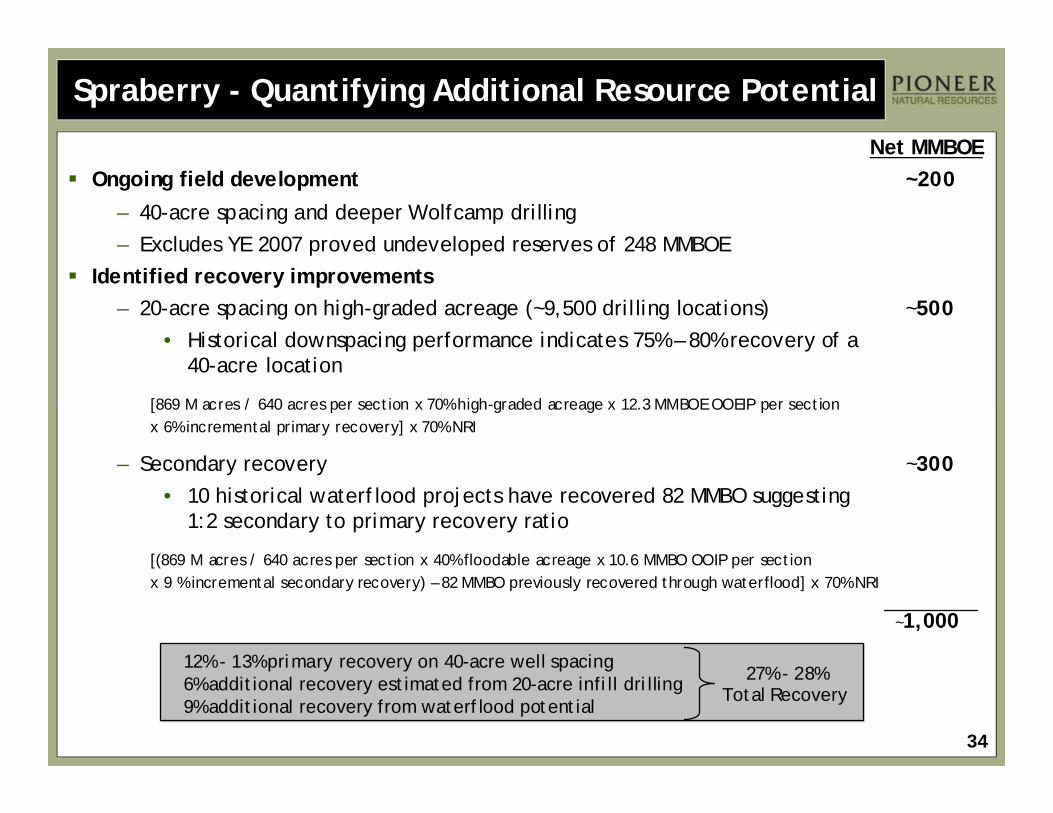

Spraberry - Quantifying Additional Resource Potential

Net MMBOEOngoing field development ~200

– 40-acre spacing and deeper Wolfcamp drilling – Excludes YE 2007 proved undeveloped reserves of 248 MMBOE

Identified recovery improvements– 20-acre spacing on high-graded acreage (~9,500 drilling locations) ~500

• Historical downspacing performance indicates 75% – 80% recovery of a 40-acre location

[869 M acres / 640 acres per section x 70% high-graded acreage x 12.3 MMBOE OOEIP per section x 6% incremental primary recovery] x 70% NRI

– Secondary recovery ~300• 10 historical waterflood projects have recovered 82 MMBO suggesting

1:2 secondary to primary recovery ratio

[(869 M acres / 640 acres per section x 40% floodable acreage x 10.6 MMBO OOIP per section x 9 % incremental secondary recovery) – 82 MMBO previously recovered through waterflood] x 70% NRI

~1,000

12% - 13% primary recovery on 40-acre well spacing6% additional recovery estimated from 20-acre infill drilling9% additional recovery from waterflood potential

27% - 28%Total Recovery

35

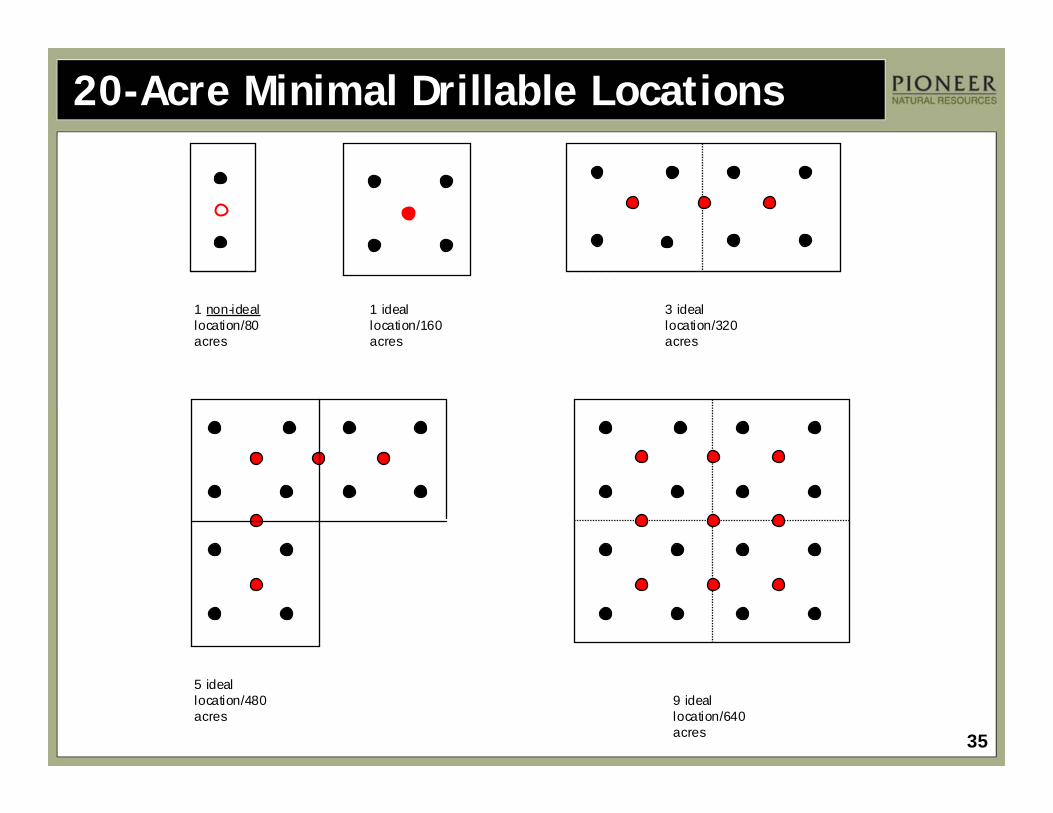

1 non-ideallocation/80 acres

1 ideal location/160 acres

3 ideal location/320acres

5 ideal location/480acres

9 ideal location/640acres

20-Acre Minimal Drillable Locations

36

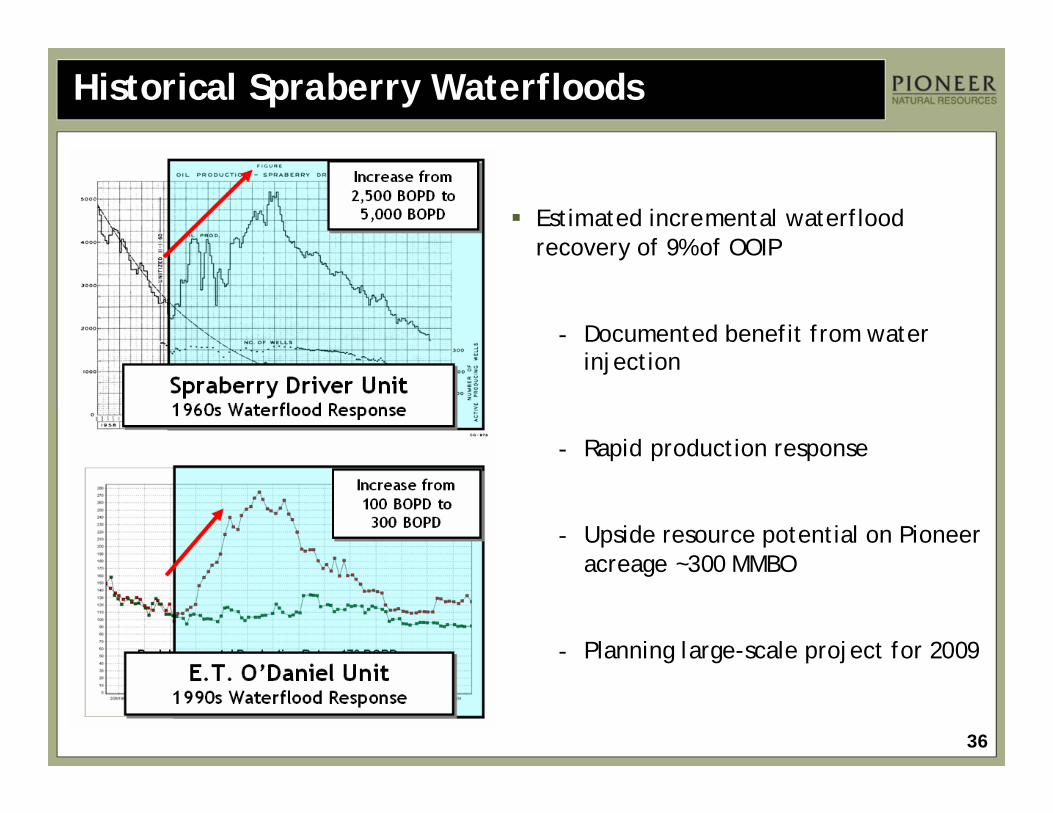

Historical Spraberry Waterfloods

Estimated incremental waterflood recovery of 9% of OOIP

- Documented benefit from water injection

- Rapid production response

- Upside resource potential on Pioneer acreage ~300 MMBO

- Planning large-scale project for 2009

37

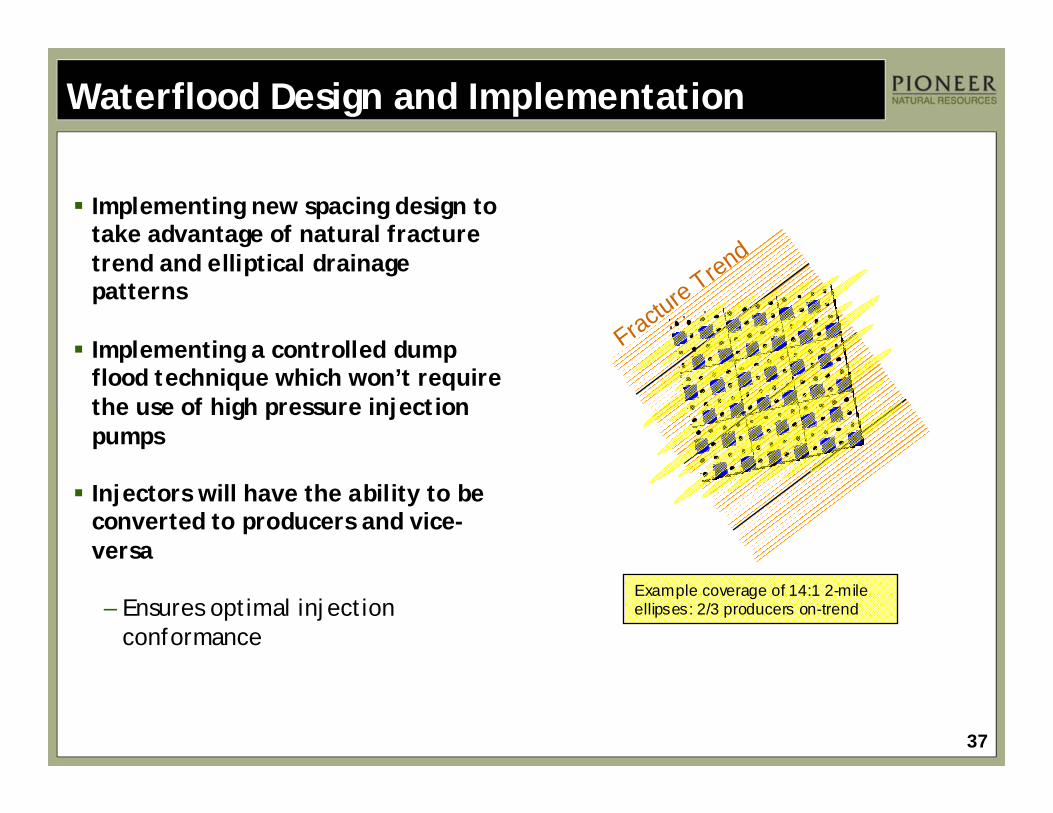

Waterflood Design and Implementation

Fracture Trend

Example coverage of 14:1 2-mile ellipses: 2/3 producers on-trend

Implementing new spacing design to take advantage of natural fracture trend and elliptical drainage patterns

Implementing a controlled dump flood technique which won’t require the use of high pressure injection pumps

Injectors will have the ability to be converted to producers and vice-versa

– Ensures optimal injection conformance

38

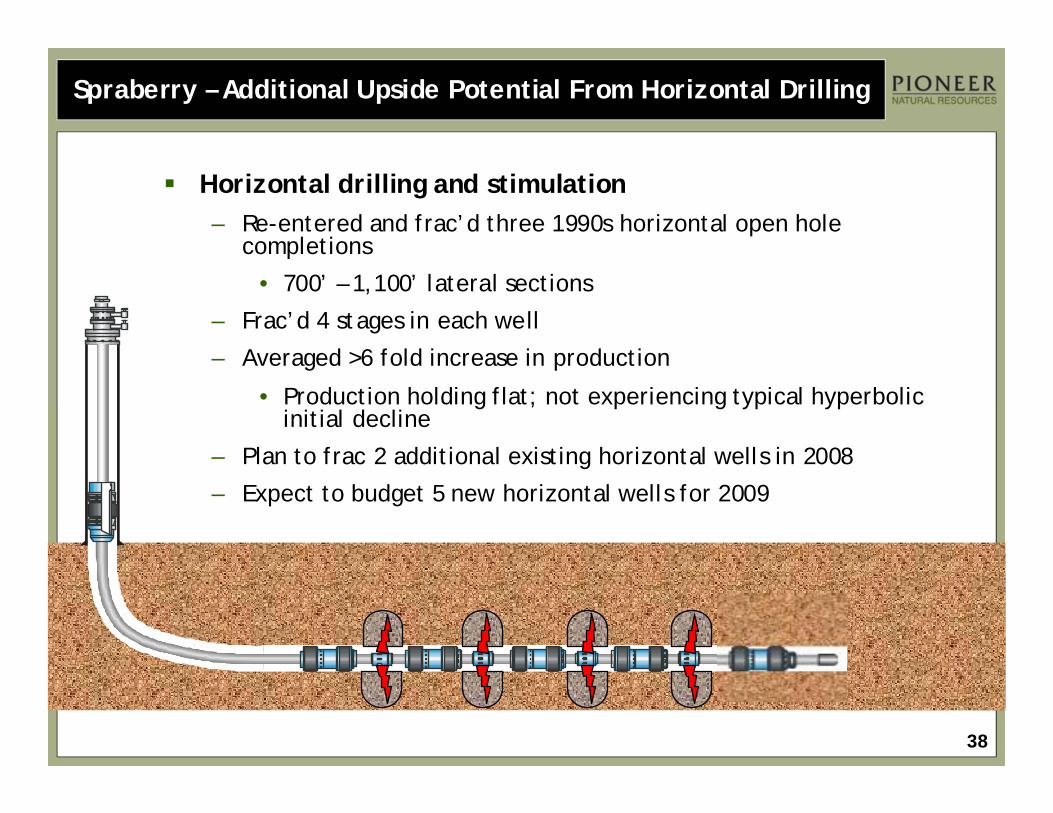

Spraberry – Additional Upside Potential From Horizontal Drilling

Horizontal drilling and stimulation– Re-entered and frac’d three 1990s horizontal open hole

completions

• 700’ – 1,100’ lateral sections

– Frac’d 4 stages in each well

– Averaged >6 fold increase in production

• Production holding flat; not experiencing typical hyperbolic initial decline

– Plan to frac 2 additional existing horizontal wells in 2008

– Expect to budget 5 new horizontal wells for 2009

39

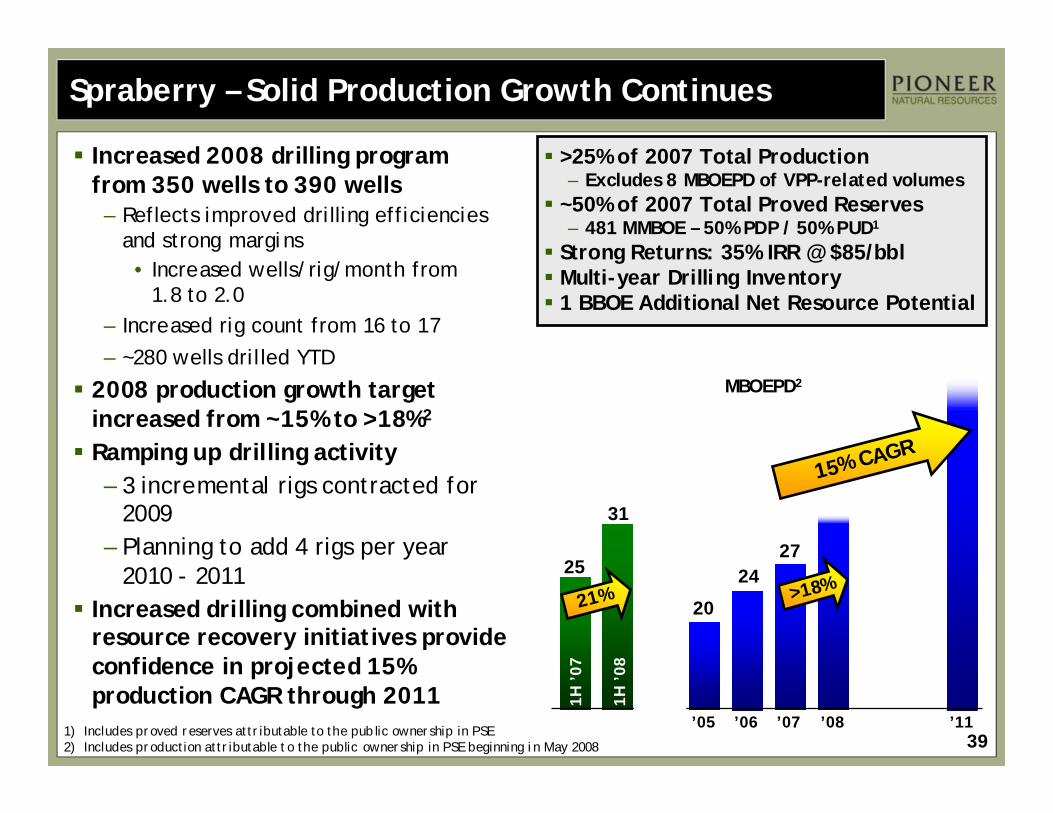

Spraberry – Solid Production Growth Continues

Increased 2008 drilling program from 350 wells to 390 wells

– Reflects improved drilling efficiencies and strong margins

• Increased wells/rig/month from 1.8 to 2.0

– Increased rig count from 16 to 17 – ~280 wells drilled YTD

2008 production growth target increased from ~15% to >18%2

Ramping up drilling activity– 3 incremental rigs contracted for

2009 – Planning to add 4 rigs per year

2010 - 2011Increased drilling combined with resource recovery initiatives provide confidence in projected 15% production CAGR through 2011

>25% of 2007 Total Production – Excludes 8 MBOEPD of VPP-related volumes

~50% of 2007 Total Proved Reserves– 481 MMBOE – 50% PDP / 50% PUD1

Strong Returns: 35% IRR @ $85/bblMulti-year Drilling Inventory1 BBOE Additional Net Resource Potential

1) Includes proved reserves attr ibutable to the pub lic ownership in PSE2) Includes production attr ibutable to the public ownership in PSE beginning in May 2008

’11

MBOEPD2

2427

’06 ’07 ’08

20

’05

15% CAGR

>18%1H

’07

31

25

1H ’

08

21%

40

Certain Reserve Information

Cautionary Note to U.S. Investors -- The U.S. Securities and Exchange Commission (the “SEC”) permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. Pioneer uses certain terms in this presentation, such as “resource potential,” “net resource potential,” “EUR,” “original oil in place” or other descriptions of volumes of reserves that the SEC’s guidelines strictly prohibit Pioneer from including in filings with the SEC. These estimates are by their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of being recovered by Pioneer. U.S. investors are urged to consider closely the disclosure in our most recent Form 10-K, file No. 1-13245, available from us at Investor Relations, 5205 N. O’Connor Blvd., Suite 200, Irving, Texas 75039. You can also obtain this form from SEC by calling 1-800-SEC-0330.