Embed Size (px)

Citation preview

Triple S Scheme August 2013

Super

insight

TS_midyrs

gDannielle, Teacher, DeCD

in thiS iSSueGet Super inFormed!

When it comes to planning for retirement you don’t need to be a financial whiz.When it comes to managing super, Susan is the first to admit that she’s not a financial whiz and looks to Super SA for information and assistance.

“I’m not very financially minded so I attempt to take an interest so I am not blind-sided by anything. I look for information that can guide me through. “

“I tend to use the online services but I appreciate that I can also get someone at the other end of the phone. I find both options very convenient. I’ve had a fair bit of contact with Super SA lately.”

So what strategies has Susan adopted to help boost her savings? Apart from making regular after-tax contributions of 4.5% from her take home pay, Susan’s combined all her super into her Triple S account.

She did her homework and learned that consolidating her super into one account would save her money and could add thousands to her final retirement balance.1Not to mention cutting down on time and trees.

Now Susan only needs to worry about one account, one set of fees and one lot of paperwork. everything she needs to know about her super is summarised on the annual statement she receives each year for her Triple S account.

One of Susan’s passions is travelling and she’s looking forward to doing more of it in retirement. She’s conscious of having enough money to retire on so that she doesn’t have to struggle in retirement. She also realises the importance of supplementing the compulsory super her employer puts in.

“I like to travel as often as I can. I probably worry about old age. So my retirement and my super is on my mind to get me through old age.”

As far as knowing your options when it comes to super, Susan’s advice to others is “take advantage of all of the expertise around you!”

> Get super informed!

> Changes in super

> Super update

> Super smart strategy

> early access to super (eATS)

> Top ratings for Super SA products

> Going on extended leave?

> Super SA member tools

> Market update

5 things you can do now to help with your super planning:

5 Consolidate your super

5 Choose your investment option

5 Make extra contributions

5 Come to a Super SA seminar

5 Speak to a financial adviser

1 Before you make any decisions, you should check whether your other super fund/s charge exit fees. Also, consider if your other super fund provides you with insurance cover.

“Take advantage of all the expertise

around you”This newsletter is printed on paper that is farmed from sustainable resources.

g SuSAn, Administration officer, dpC

Super INSIGHTTriple S > August 2013

www.supersa.sa.gov.au 2 | Super Insight | August 2013

Super updAte

recently Super SA has directed considerable effort to working with Funds SA and global professional services company, Towers Watson, to better understand our members’ investment risk tolerance and the importance of choosing the right investment option.

Most super is affected by the normal volatility or ‘ups and downs’ of investment markets. However, research shows that as members approach retirement, they have less ability to recover from the effects of major market events such as the negative returns seen during the Global Financial Crisis. The ability to recover from events like these and achieve your desired level of income in retirement depends on your investment option and age.

If you don’t need to access your super for another 20 years, you may want to take on some investment risk to build your retirement balance. You will still have a good chance of withstanding the effects of any major market events that may happen in the future.

But if you’re close to retirement and your super is invested in a Moderate to High Growth option, you are more exposed to negative investment returns and may end up with less retirement income than you were expecting.

SG increase

The Superannuation Guarantee (SG) rate increased to 9.25% on 1 July 2013 and will eventually rise to 12%.

The SG age limit of 70 has also been removed from 1 July 2013.

Government Co-contribution

The Commonwealth Government’s Co-contribution scheme has reduced entitlements ($500 down from $1000) and the higher threshold ($46,920 down from $61,920) for personal contributions made from 1 July 2012.

reduced higher tax concessions

The Government has made a minor amendment to reduce the amount of concession for those with higher incomes above $300,000.

Further information about the impact of this change will be published on our website as soon as it becomes available.

Super SA Select established

Our new fund, Super SA Select, has been up and running since 1 January 2013.

For those who earn $37,000 or less per year this may be a good option as it may attract a Low Income Super Contribution (LISC) of up to $500 per year.

For more information visit www.supersa.sa.gov.au.

“A lower risk, lower return strategy may be better su ited to

someone retiring soon.”

more information is available on the Super SA website:

• use the “What kind of investor am I?” calculator. • read the “Investment” Fact Sheet for more detailed

information about investment options. • Calculate what your final entitlement could be using the

“Benefit projector”.

ChAnGeS in Super

neW produCt

Is your investment option appropriate to your financial needs and objectives at this time in your life?

One of the issues that has been concerning me recently is whether members have a clear idea about the sort of lifestyle they want in retirement and whether they’re on track to achieve their financial goals.

STepHeN rOWe, General Manager, Super SA

So it’s important to review your selected investment option, ensuring it’s appropriate given your age, the amount of investment risk you’re prepared to take and your desired level of retirement income. This will help you to achieve your financial goals in retirement.

investment options

In Triple S you have a choice of investment options ranging from Cash to High Growth, each with a different level of risk and expected return.

A higher risk, higher return strategy may be suitable if you’re trying to build your super and retirement is still a long way off. In contrast, a lower risk, lower return strategy may be better suited to someone retiring soon. You can also have your super in two options to diversify your investments.

To make sure you’re on track with your super you’ll need to work out what sort of retirement lifestyle you want and therefore the retirement benefit you’ll need. A good place to start is the ASFA retirement Standard on www.superguru.com.au.

Then you can use the “Benefit projector” on www.supersa.sa.gov.au to check whether you’re on track.

www.supersa.sa.gov.au 3 | Super Insight | August 2013

Super updAte Super SmArt StrAteGy

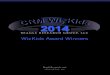

Salary sacrificing to your super is a great financial strategy say financial planners paul Cameron and Andrew Hiscock.

name Age Salary Starting super balance2

extra amount contributed

per year

Super balance age 653 – without extra contributions

Super balance age 653

– with extra contributions

Tracey 35 $50,000 $46,000 3% ($1,500) $439,613 $517,584

Travis 40 $50,000 $53,000 8% ($4,000) $356,887 $512,561

Tran 45 $50,000 $63,000 15% ($7,500) $291,463 $503,121

Teresa 50 $50,000 $77,000 28% ($14,000) $240,532 $507,774

Tom 55 $50,000 $103,000 51% ($25,500) $211,488 $505,339

Tina 60 $50,000 $145,000 87% (43,500) $233,466 $498,031

1 Westpac ASFA Retirement Standard benchmarks (March Quarter 2013).2 Starting balance – average Triple S account balance for the quoted age at 30/6/12. 3 Projection: In today’s dollars, $1.35 per week administration fee, $1.50 per week Death and TPD insurance premium, 0.2% of salary IP insurance premium, 7% investment rate, 3% inflation, 3% salary growth, 9.25% SG for after-tax contributions that are less than 4.5% and 10% employer contribution for members contributing after-tax equal to or greater than 4.5%. SG increases incrementally by 0.5% pa from 9.5% to 12% between July 2014 and July 2019.

the eArlier you StArt ContributinG the lonGer your Super hAS to GroW...

They also say that salary sacrifice is “a simple, tax-free way of saving money.” And they should know, after all as financial planners with Industry Fund Services (IFS) they have over twenty-five years of experience between them.

Salary sacrifice means contributing to your super from your before-tax, or gross salary. This can reduce your taxable income, so you pay less tax and more goes into your super.

Why consider salary sacrifice

paul admits that salary sacrifice doesn’t seem as exciting as some other money-making schemes – but therein lies its appeal.

“It might be considered a boring option…there’s a lot of fanciful ways of making money that people are being presented with, but this is such a simple way to save money.”

He says that when making the case for salary sacrifice, it pays to let the numbers do the talking.

“Most people are visual…what they want to see is how their money grows and what the benefit is.”

projecting where a client’s super will be in five and ten years is a technique Andrew uses to demonstrate the impact of salary sacrifice.

“The numbers speak for themselves with salary sacrifice, it is quite amazing how much you can boost your super.”

no caps in triple S

No annual concessional caps in Triple S also means that members can put more into their super than is the case with other super funds. In paul’s view this is “an enormous advantage” as members don’t have to worry about paying extra tax if they exceed the caps.

Commission-free and fixed upfront cost

IFS offers single issue and comprehensive commission-free advice but paul has some completely free advice for those still years away from retirement.

“The fact that people don’t salary sacrifice is because they’re just not aware of the advantages. When you’re in your thirties and forties retirement still seems a long way away…but all the people we see at retirement say, ‘Gee, it went quick.’”

Salary sacrifice facts:

5 Complete one form and pay a payroll fee of $44.

iFS facts:

5 Commission-free service is available in the city. Triple S members can have the cost deducted from their Triple S Account. To make an appointment call 1300 138 848.

Situation: Jo is 442 and earns $50,000 pa

Scenario3: how much super will Jo have at 65 if she salary sacrifices 5%, 10% or 15%?

5% salary sacrifice=$50,000 super!

Summary: each extra 5% in salary sacrifice gives Jo an extra $50,000 when she retires!

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

15%10%5%0%

Super INSIGHTTriple S > August 2013

www.supersa.sa.gov.au 4 | Super Insight | August 2013

GoinG on extended leAVe?

You may need to talk to us first.Whether it’s an overseas holiday, a job secondment, or just to extend your recreation leave, it’s comforting to know that Leave Without pay (LWOp) is an option if you need it.

Before you go on leave though, there are a few things you need to know.

insurance

– You’re not covered for Income protection while on LWOp.

– Your Death and Total and permanent Disablement (TpD) insurance cover will continue during your LWOp.

– You can suspend your Death and TpD insurance cover while on LWOp.1

– If you choose to suspend your cover, no Death and TpD will be paid within one year of your arranging to reinstate your insurance cover unless your death or disablement is caused by an accident.

Contributions

– You can choose to make after-tax member contributions into your super during LWOp.

– Your employer is not required to make contributions into your super during this time.

eArly ACCeSS to Super (eAtS)

member Story

retirement’s still a long way off, but it’s good to have a plan.Did you know that when you reach your preservation age (currently age 55) you can access your super via regular income payments from an income stream to build your retirement wealth or ease into retirement?

Wealth creation

A way to build your super is to salary sacrifice into your Triple S account and supplement your reduced income with an income stream. Why? You’ll reduce the tax you’ll pay so you can put what you save into your super to build it more quickly.

easing into retirement

If you only want to work three days per week you’d only get three-fifths of your salary. You could top this up with an income stream. The down side? You’ll end up with less super in retirement.

Starting up an income stream

You’ll need at least $30,000 from a superannuation source such as Triple S to roll into an income stream, like the Super SA Income Stream. While you’re still working your Triple S account remains open and continues to receive contributions. So even though you’re drawing down your super it’s still growing!

tax benefits

When you turn 60 your regular income payments from an income stream are tax free. If you’re under 60 your payments are added to your assessable income but you’ll get a 15% super rebate and a portion of your payments may be tax free.

WAnt to knoW more? Download the “early Access to Super” fact sheet from the Super SA website, or attend the early Access to Super seminar.

Get more info!

– Download the “Leave Without pay” fact sheet from the Super SA website

– Contact us at [email protected]

– Call 1300 369 315

1 If you’re on LWOP for 12 months or more, you will not be covered for any pre-existing medical condition that was known to you on the day you returned to work for a period of two years from that date.

Super SA Income Stream, Flexible rollover product, Triple S and Super SA Select have been awarded ‘platinum’ ratings by independent researcher Super ratings.

Triple S has been platinum rated for five years.

In addition, the Triple S Scheme and Income Stream have received the 5 Apples rating from Chant West.

These ratings are the highest possible ratings from two of the industry’s leading independent researchers.

here’s how we rate in 2013:triple S Scheme

– 5 years platinum and 5 Apples

Super SA income Stream – platinum and 5 Apples

Flexible rollover product – platinum

Super SA Select – platinum

top rAtinGS For Super SA produCtS > 1

IN THIS FACT SHEET

> Facts about LWOP

> What to do when you take

LWOP

> Paying for member

contributions while on

LWOP

Last updated February 2013

To find out more call 1300 369 315 or visit www.supersa.sa.gov.au

TSFS07

The information in this document forms part of the Triple S Product Disclosure Statement dated June 2013

You must let Super SA know that you are taking Leave Without Pay

regardless of whether or not you choose to maintain member

contributions during your period of LWOP.

There are a number of reasons that SA public sector

employees take Leave Without Pay (LWOP). These

may include:

– parenting leave

– extended study leave

– overseas holidays

– secondment to another employer

– overseas aid programs.

If you are taking LWOP you need to contact Super SA

to discuss your options.

Facts about LWOP

– You are able to make after-tax member

contributions into your super for the period of

LWOP granted by your employer. During a period

of LWOP you are not entitled to any employer

contributions.

– If you have Income Protection Insurance you will

have immediate cover for Income Protection

Insurance when you return to work. However, if

you are on LWOP for 12 months or more, you will

not be covered for any pre-existing medical

condition that was known to you on the day you

returned to work for a period of two years from

that date. You cannot claim for Income Protection

Insurance while on LWOP even if you continue to

contribute.

– Your Triple S Death and Total and Permanent

Disablement (TPD) insurance cover will continue

during your LWOP. The cost of your insurance will

be deducted from your Employer Account. If

there are insufficient funds in your Employer

Account, your insurance will be suspended.

– You can choose to suspend your Death and TPD

insurance cover while on LWOP. If you do this,

you will not be covered by insurance and you will

not be charged a fee. You should contact Super

SA to suspend your insurance cover.

– No Death and TPD insurance will be paid within

one year of your arranging to reinstate your

insurance cover unless your death or disablement

is caused by an accident.

What to do when you take LWOP

You must let Super SA know that you are taking

LWOP regardless of whether or not you choose to

maintain member contributions during your period of

LWOP.

Visit the Super SA website and download the “Leave

Without Pay” form or contact Super SA to have one

posted to you. This form should be completed and

returned to Super SA before you commence your

leave.

Paying for member contributions while on

LWOP

If you have elected to maintain your personal

contributions during your LWOP you can pay by:

– making a lump sum payment following

notification of the amount from Super SA, or

– direct debit.

If you choose direct debit as your payment method

you need to complete the “Member Direct Debit

Request (DDR)” form included with the “Leave

Without Pay“ form.

Please note that if you choose to make a lump sum

payment, in the interests of the security of our

If you are taking LWOP

you need to contact

Super SA to discuss

your options.

LEAVE WITHOUT PAYFact Sheet > Triple S

Super INSIGHTTriple S > August 2013

www.supersa.sa.gov.au 5 | Super Insight | August 2013

Free seminars, online calculators, user-friendly guides, worksite visits...it’s easy to get your super on track.

Super SA WebSite Super SA CAlCulAtorS

Seminar, guide, or both? There’s Grow Your Super the guide, Sort-Grow-Know – the seminar or guide... simply go online to book into a regional or city-based seminar or to download a guide.

Worksite visitsWhy not have a super workshop at your workplace? Our Member education Officers are more than happy to come to you! email [email protected] to register your interest.

Get “Super SAvvy” with seminars, guides and worksite visits

SUPER SATRIPLE S – GROW YOUR SUPERSeven simple steps to grow your super

Date of issue: 1 August 2011

It’s all about time...

Nowadays there’s much more to super

than just putting money away for your

life after work.

Triple S members have access to

insurance, investment choice and

government incentives. Triple S is also an

untaxed, or tax deferred scheme, which

means your earnings are fully reinvested

and you don’t pay any tax until you claim

your super from Triple S.

There’s a lot to consider! That’s why

we’ve arranged this guide in 3 easy steps

to help you get on top of your super and

make the most of Triple S.

Triple S members enjoy:

– Low administration fees.

– Competitive investment returns.

– An extra 1% employer

contribution to your super if you

contribute 4.5% or more of your

salary after tax.

– The option to salary sacrifice

to your super.

– A choice of investment options

to best suit your needs.

– A choice in the level of your

Death and Total and Permanent

Disablement Insurance.

– Access to

Income Protection Insurance.

– The option to create an account

for your partner.

Triple S is the super scheme for SA public sector

employees. We’re a member-based scheme which

means we’re here solely for the benefit of our

members. You!

In this guide...

This newsletter is printed

on paper farmed from

sustainable resources.

sort – grow – know 3 easy st

eps to help you

make

the most of your supe

r...

Triple S Guide >

Step 1 – sort your super

> Rolling In

> Investment Choice

> Insurance

> Spouse Accounts

Step 2 – grow your super

> Why super?

> After-tax Contributions

> Salary Sacrifice

> Government Co-contribution

> Contribution Caps

Step 3 – know your super

> Super SA website

> Seminars

> Member Enquiries

> Member Solutions

> Financial Planning

Super the SmArt WAy

Super updatese-news sign up

Financial advice info

Seminars

Worksite Visits

Secure member Area

balance

Super SA member toolS

Take the guesswork out of super with Super SA’s calculators. They’re fast, fun and let you factor in your circumstances so you can really put your choices to the test.

use your smartphone to transform your super!

Head online to www.supersa.sa.gov.au:

– Book a seminar – email forms to your inbox – Calculate your balance – Lost super info – Get your details

No cost, no app! Access the site on any mobile device using our web address.

We’re here to help If you require further information please contact Super SA:

Website www.supersa.sa.gov.au

email [email protected]

member Service Centre Ground Floor 151 pirie St (enter from pulteney Street) Adelaide SA 5000

postal address GpO Box 48, Adelaide SA 5001

telephone (08) 8207 2094 (for calls within the State Government network), or 1300 369 315

Facsimile (08) 8226 0593

Triple S is an exempt public sector superannuation scheme and is not regulated by the Australian Securities and Investments Commission (ASIC) or the Australian Prudential Regulation Authority (APRA). Super SA is not required to hold an Australian Financial Services Licence to provide general advice about Triple S. The information in this document is of a general nature only and has been prepared without taking into account your objectives, financial situation or needs. Super SA recommends that before making any decisions about Triple S, you consider the appropriateness of this information in the context of your own objectives, financial situation and needs, read the Product Disclosure Statement (PDS) and seek financial advice from a licensed financial adviser in relation to your financial position and requirements. Super SA and the State Government disclaim all liability for all claims, losses, damages, costs or expenses whatsoever (including consequential or incidental loss or damage), which arise as a result of or in connection with any use of, or reliance upon, any information in this document.The Chant West ratings logo is a trademark of Chant West Pty Limited and used under licence.

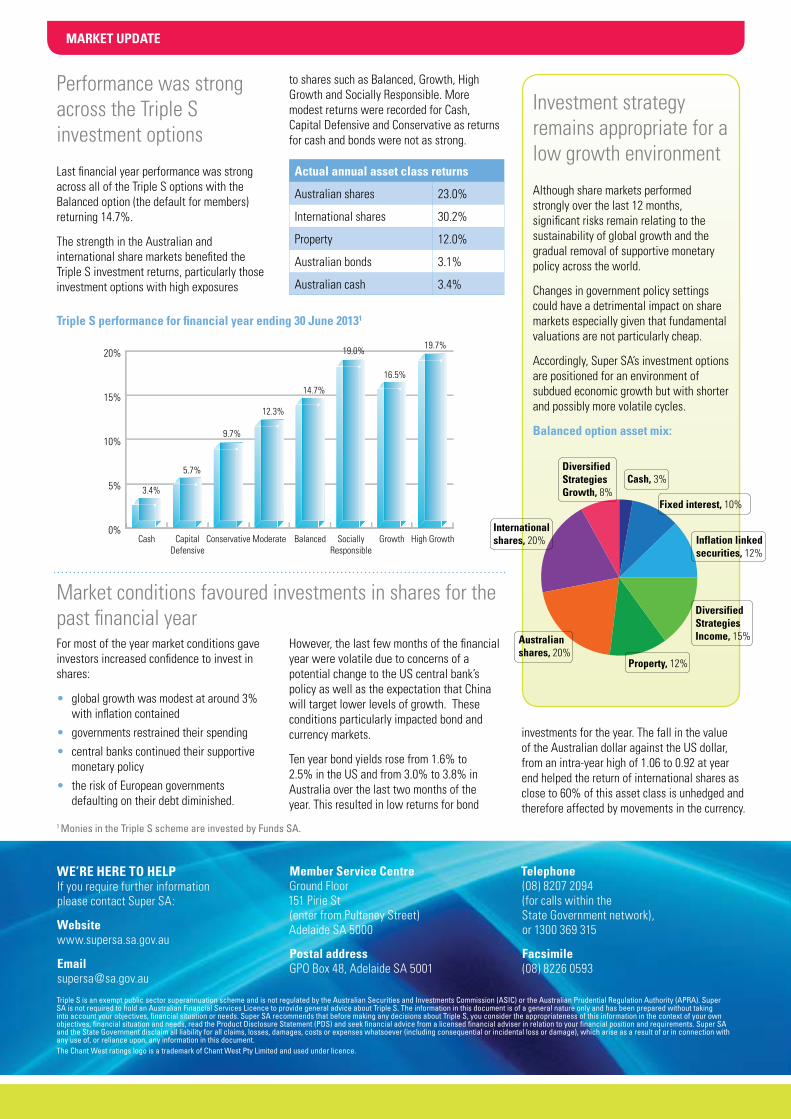

mArket updAte

performance was strong across the Triple S investment options

Last financial year performance was strong across all of the Triple S options with the Balanced option (the default for members) returning 14.7%.

The strength in the Australian and international share markets benefited the Triple S investment returns, particularly those investment options with high exposures

to shares such as Balanced, Growth, High Growth and Socially responsible. More modest returns were recorded for Cash, Capital Defensive and Conservative as returns for cash and bonds were not as strong.

Actual annual asset class returns

Australian shares 23.0%

International shares 30.2%

property 12.0%

Australian bonds 3.1%

Australian cash 3.4%

DiversifiedStrategiesGrowth, 8%

Internationalshares, 20%

Australianshares, 20%

Property, 12%

DiversifiedStrategiesIncome, 15%

Inflation linkedsecurities, 12%

Fixed interest, 10%

Cash, 3%

Investment strategy remains appropriate for a low growth environment

Although share markets performed strongly over the last 12 months, significant risks remain relating to the sustainability of global growth and the gradual removal of supportive monetary policy across the world.

Changes in government policy settings could have a detrimental impact on share markets especially given that fundamental valuations are not particularly cheap.

Accordingly, Super SA’s investment options are positioned for an environment of subdued economic growth but with shorter and possibly more volatile cycles.

balanced option asset mix:

triple S performance for financial year ending 30 June 20131

3.4%

5.7%

9.7%

12.3%

14.7%

16.5%

19.7%

0%

5%

10%

15%

20%

High GrowthGrowthSociallyResponsible

BalancedModerateConservativeCapitalDefensive

Cash

19.0%

Market conditions favoured investments in shares for the past financial yearFor most of the year market conditions gave investors increased confidence to invest in shares:

• global growth was modest at around 3%with inflation contained

• governments restrained their spending• central banks continued their supportive

monetary policy• the risk of european governments

defaulting on their debt diminished.

However, the last few months of the financial year were volatile due to concerns of a potential change to the uS central bank’s policy as well as the expectation that China will target lower levels of growth. These conditions particularly impacted bond and currency markets.

Ten year bond yields rose from 1.6% to 2.5% in the uS and from 3.0% to 3.8% in Australia over the last two months of the year. This resulted in low returns for bond

investments for the year. The fall in the value of the Australian dollar against the uS dollar, from an intra-year high of 1.06 to 0.92 at year end helped the return of international shares as close to 60% of this asset class is unhedged and therefore affected by movements in the currency.

1 Monies in the Triple S scheme are invested by Funds SA.