Embed Size (px)

Citation preview

SPECIFIED DOMESTIC TRANSACTION –

SECTION 40a(2)

-Nihar Jambusaria

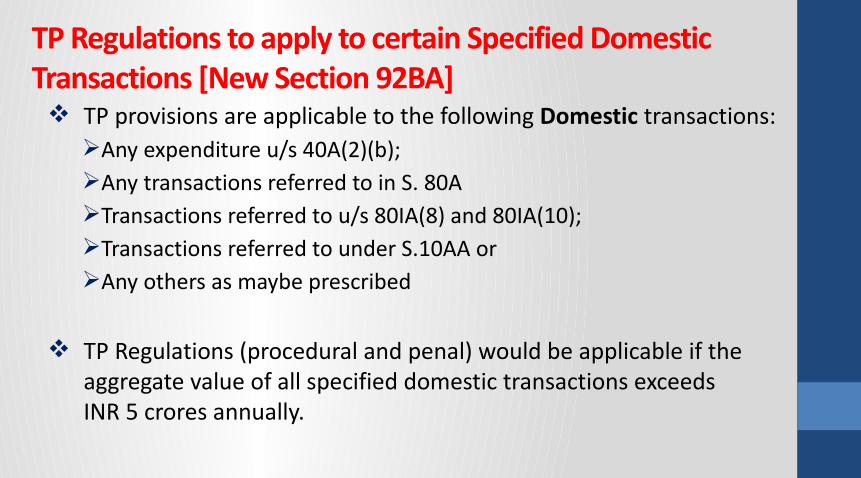

TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic transactions:

Any expenditure u/s 40A(2)(b); Any transactions referred to in S. 80ATransactions referred to u/s 80IA(8) and 80IA(10);Transactions referred to under S.10AA orAny others as maybe prescribed

TP Regulations (procedural and penal) would be applicable if the aggregate value of all specified domestic transactions exceeds INR 5 crores annually.

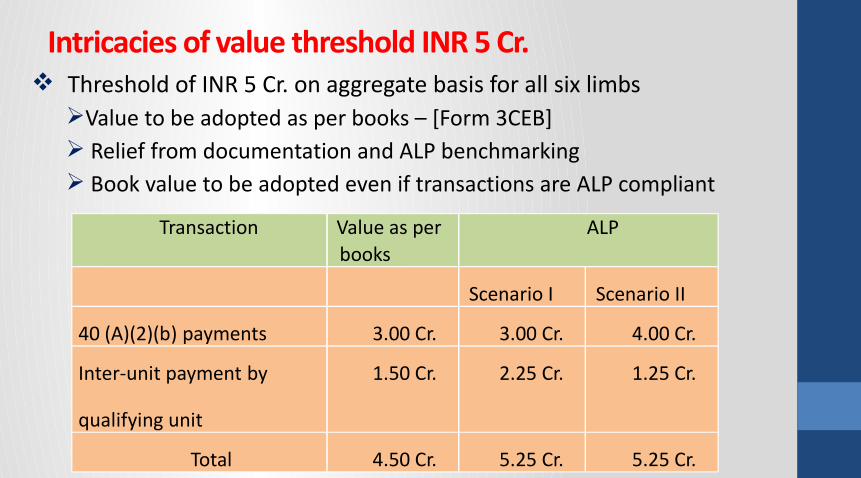

Intricacies of value threshold INR 5 Cr. Threshold of INR 5 Cr. on aggregate basis for all six limbs

Value to be adopted as per books – [Form 3CEB] Relief from documentation and ALP benchmarking Book value to be adopted even if transactions are ALP compliant

Transaction Value as per books

ALP

Scenario I

Scenario II

40 (A)(2)(b) payments

3.00 Cr.

3.00 Cr.

4.00 Cr.

Inter-unit payment by

qualifying unit

1.50 Cr.

2.25 Cr.

1.25 Cr.

Total

4.50 Cr.

5.25 Cr.

5.25 Cr.

Concept of ALP applicable for determining taxable income arising from international transaction introduced in 2001, extended to SDTs from A.Y. 2013-14

ALP defined to mean a price which is applied or proposed to be applied in a transaction between persons other than AEs, in uncontrolled conditions

Comparability and FAR fundamental to the concept of ALP

Comparison of conditions in a controlled transactions with conditions in transactions between uncontrolled enterprises

Compensation usually reflects functions performed (taking into account assets used and risks assumed)

ALP concept usually relevant for transactions between “separate enterprises”; may need to be applied by analogy to SDT involving inter-unit transfer of goods/ services

Concept of arm’s length price (alp)

Domestic TP not restricted to transactions with residents S. 92BA excludes International Transaction from within its scope

Trigger for AE relationship different for International and Domestic TP

In terms of s. 92BA certain transactions are regarded as SDT if they are not Int. Tr and are covered by one of the specified clauses of s. 92B

SDT does not mean that transaction should not be cross border neither does it mean that both parties to the transaction need to be resident.

There could be a SDT which may be cross border and either or both parties to the transaction could be non-resident.

Domestic TP not restricted to transaction with residents Illustrative examples where transactions with non-resident may be

covered under Domestic TP

Remuneration paid by an Indian company to a non-resident director

Remuneration paid by a FC having PE to non resident director

Payment by Indian Co to Foreign Co. where Foreign Co. holds 20% to < 26% in Indian Co.

Section 40A(2)(b)

Any Transactions with the following persons will be covered within the purview of Domestic Transfer Pricing:

A Company, firm, AOP or HUF holding substantial interest in the business or profession of the Assessee or any other company in which the first mentioned company has substantial interest;

Any Company in which Assessee has substantial interest in the business or profession of such company;

Individual holding substantial interest in the business or profession of the assessee or any relative of such individual; and

Any Director of the company or partner of the firm or member of HUF or any of their relative holding substantial interest in the business or profession of the assessee.

‘Substantial Interest’ is defined as: in case of company, any person who is the beneficial owner of

shares carrying not less than 20% of the voting power; and In other case, any person who is beneficially entitled to not less

than 20% of profits of such business or profession.

The term beneficial owner of shares is no where defined in the Act.

Black’s Law dictionary: A beneficial owner is “one recognized in equity as the owner of something because use and title belong to that person, even though legal title belongs to someone else.”

Also, in respect of section 79 of the Act, typically, position is adopted when there is a change in more than 51% of ‘beneficial holding’ in a closely held company. Change in shareholding should be seen at immediate holding company level. Section 79 is not invoked where there is change in shareholding at the ultimate holding company level.

Further, as per S. 92A(2), the term associated entities is clearly defined to include an enterprise holding directly or indirectly shares carrying not less than 26% of the voting power in the other enterprise.

However, under section 40 A(2)(b) of the Act, only substantial interest has been used, which is specifically defined to include that shareholder who is the beneficial owner of shares. There is no mention about the words direct or indirect holding of shares.

9

Under normal circumstances, immediate holder of shares is regarded as beneficial owner and applicability of S.40A(2)(b) is restricted to that immediate holder of shares. The fact that immediate holder is beneficial owner of share and its rights is not constrained in any manner needs to be demonstrated by facts.

10

Key Features As per the provisions of section 92(2A) introduced by the

Finance Act, 2012 - Any allowance for an expenditure or interest or allocation of any

cost or expense or any income in relation to the specified domestic transaction shall be computed having regard to the arm's length price

However, the provisions of section 92BA specifically include only -

any expenditure in respect of which payment has been made or is to be made to a person referred to in clause (b) of sub-section (2) of section 40A

Accordingly, in the case of transactions as specified in S.40A(2)(b), only the entity making payment for expenditure shall be covered. The entity receiving income shall not be covered.

Only the entity incurring expenses will need to complete the prescribed compliances.

There is no provision regarding indirect holding of shares. Therefore a view can be taken that any transactions between Holding Company and its step down subsidiaries are not covered.

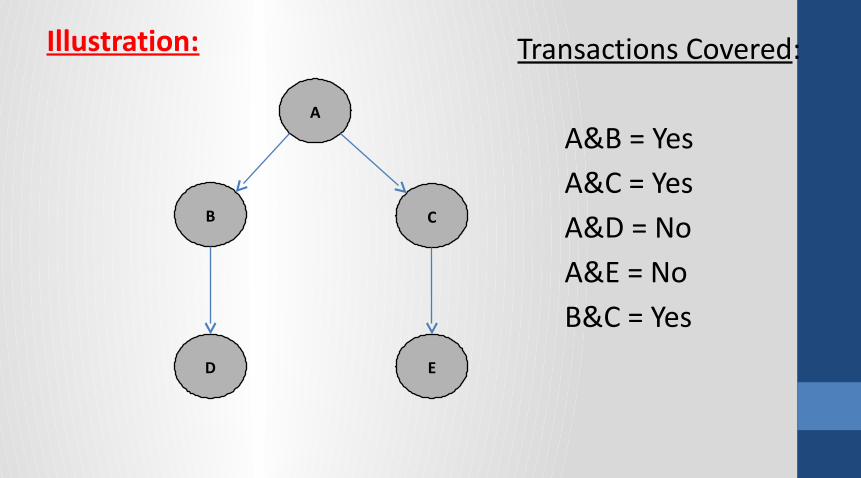

Illustration:

A

B C

ED

Transactions Covered:

A&B = YesA&C = YesA&D = NoA&E = NoB&C = Yes

Transactions covered (illustrative):

Expenditure on buying goods or procurement of services; or

Expenditure on salary, training services, marketing expenses, interest payments.

Expenditure on purchase of tangible and intangible property, Group charges Reimbursements, Guarantee fees etc.

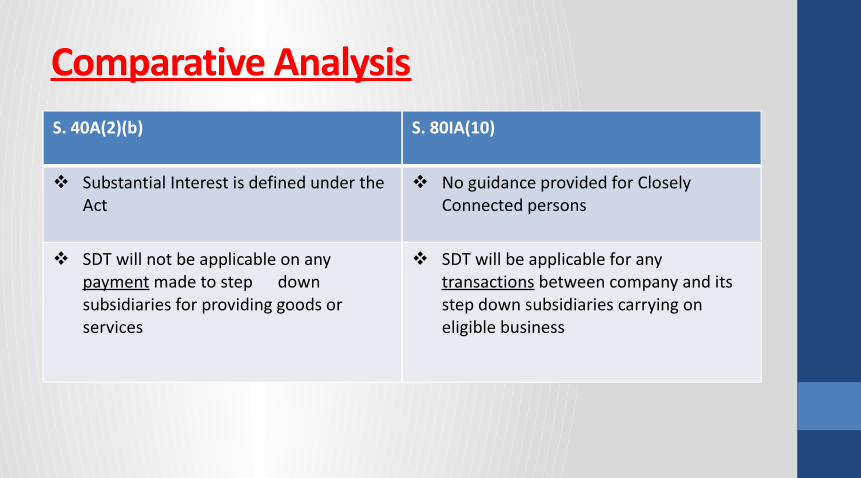

Comparative AnalysisS. 40A(2)(b) S. 80IA(10)

Substantial Interest is defined under the Act

No guidance provided for Closely Connected persons

SDT will not be applicable on any payment made to step down subsidiaries for providing goods or services

SDT will be applicable for any transactions between company and its step down subsidiaries carrying on eligible business

Case Study

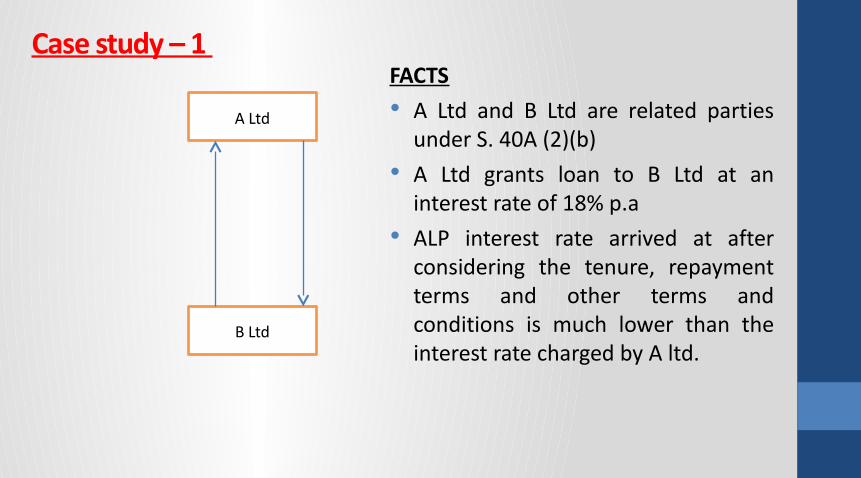

Case study – 1 FACTS A Ltd and B Ltd are related parties

under S. 40A (2)(b) A Ltd grants loan to B Ltd at an

interest rate of 18% p.a ALP interest rate arrived at after

considering the tenure, repayment terms and other terms and conditions is much lower than the interest rate charged by A ltd.

A Ltd

B Ltd

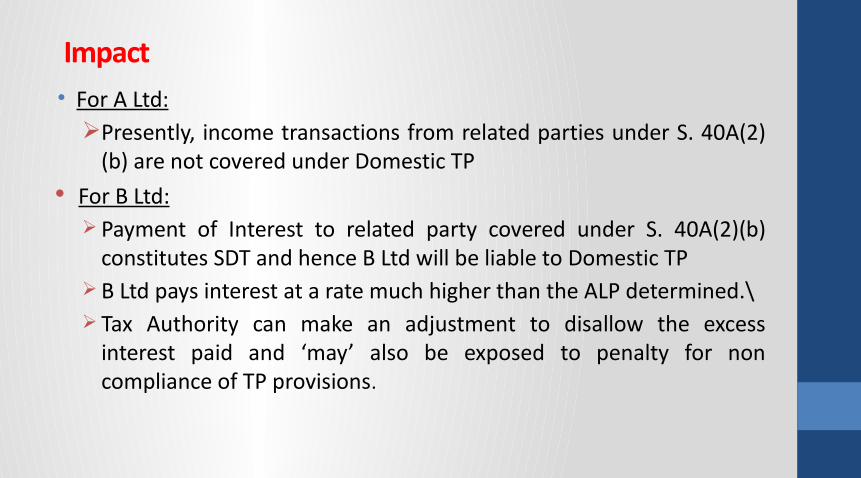

Impact• For A Ltd:

Presently, income transactions from related parties under S. 40A(2)(b) are not covered under Domestic TP

For B Ltd: Payment of Interest to related party covered under S. 40A(2)(b)

constitutes SDT and hence B Ltd will be liable to Domestic TP B Ltd pays interest at a rate much higher than the ALP determined.\ Tax Authority can make an adjustment to disallow the excess

interest paid and ‘may’ also be exposed to penalty for non compliance of TP provisions.

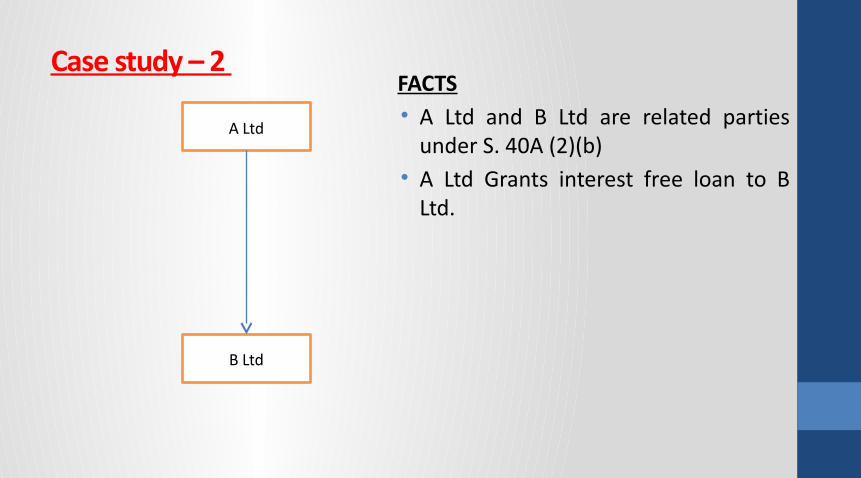

Case study – 2 FACTS• A Ltd and B Ltd are related parties

under S. 40A (2)(b)• A Ltd Grants interest free loan to B

Ltd.

A Ltd

B Ltd

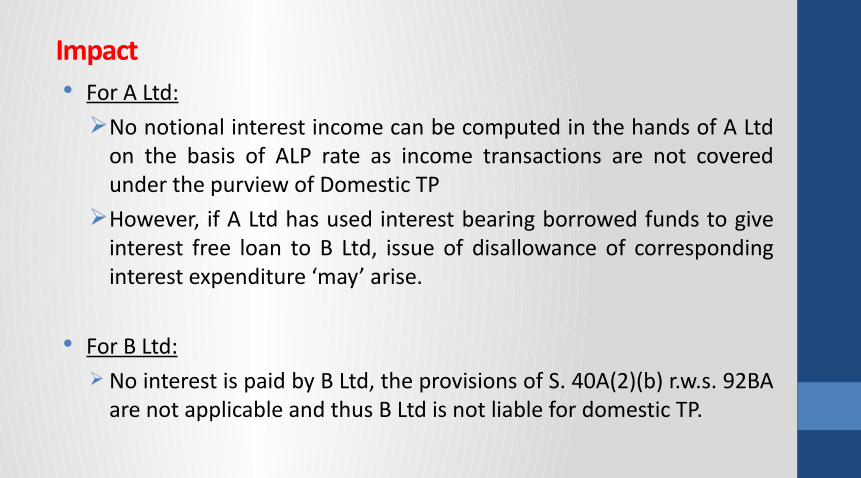

Impact For A Ltd:

No notional interest income can be computed in the hands of A Ltd on the basis of ALP rate as income transactions are not covered under the purview of Domestic TP

However, if A Ltd has used interest bearing borrowed funds to give interest free loan to B Ltd, issue of disallowance of corresponding interest expenditure ‘may’ arise.

For B Ltd:

No interest is paid by B Ltd, the provisions of S. 40A(2)(b) r.w.s. 92BA are not applicable and thus B Ltd is not liable for domestic TP.

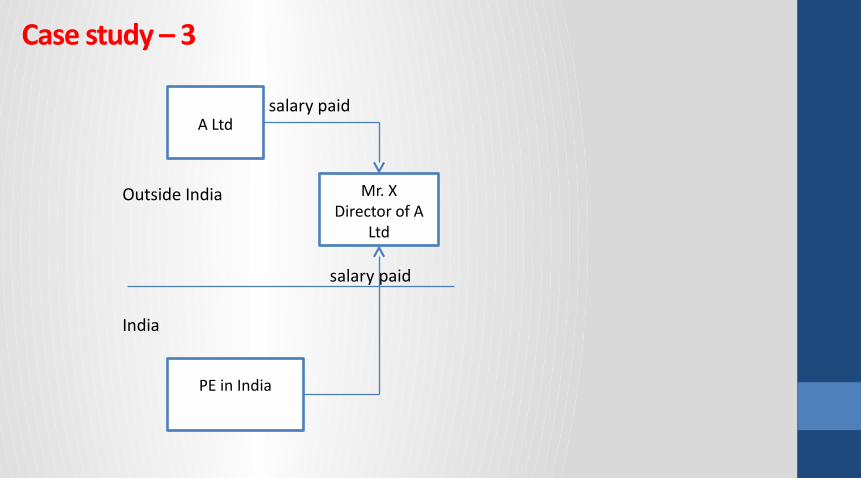

Case study – 3

salary paid

Outside India

salary paid India

A Ltd

PE in India

Mr. XDirector of A

Ltd

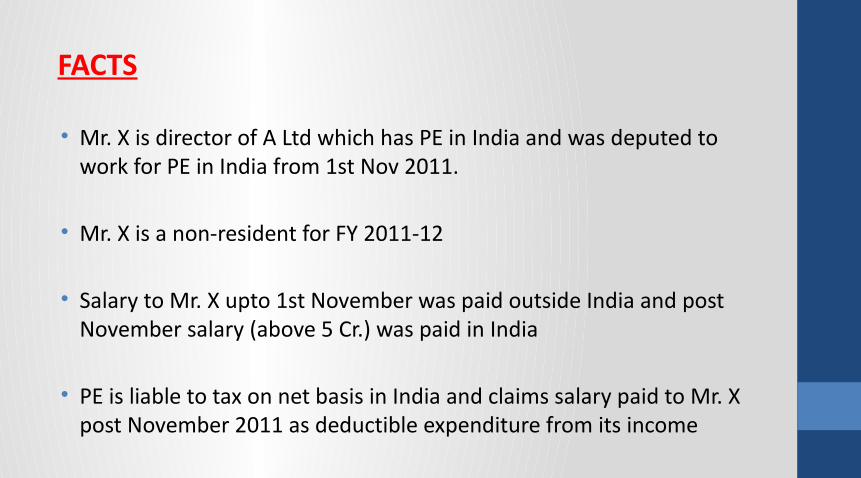

FACTS

• Mr. X is director of A Ltd which has PE in India and was deputed to work for PE in India from 1st Nov 2011.

• Mr. X is a non-resident for FY 2011-12

• Salary to Mr. X upto 1st November was paid outside India and post November salary (above 5 Cr.) was paid in India

• PE is liable to tax on net basis in India and claims salary paid to Mr. X post November 2011 as deductible expenditure from its income

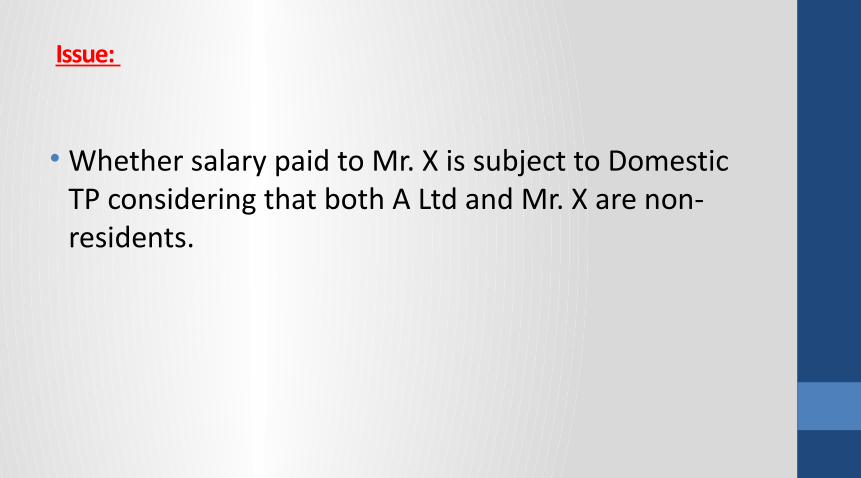

Issue:

• Whether salary paid to Mr. X is subject to Domestic TP considering that both A Ltd and Mr. X are non-residents.

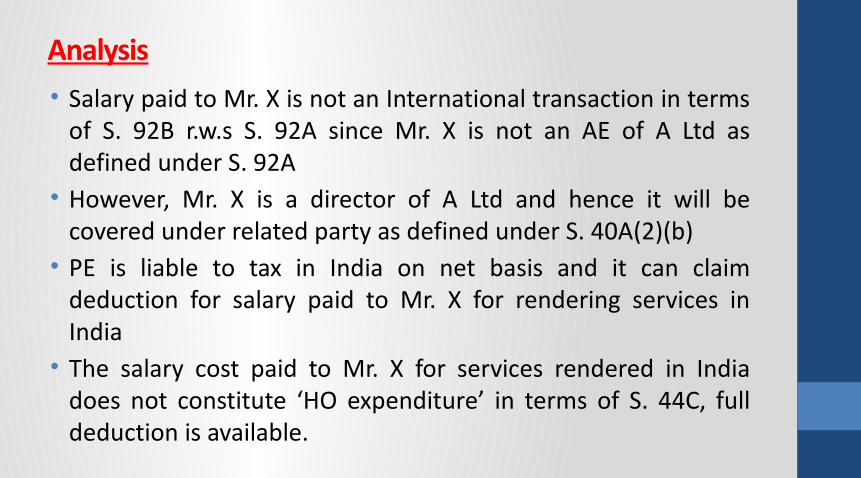

Analysis• Salary paid to Mr. X is not an International transaction in terms

of S. 92B r.w.s S. 92A since Mr. X is not an AE of A Ltd as defined under S. 92A• However, Mr. X is a director of A Ltd and hence it will be

covered under related party as defined under S. 40A(2)(b)• PE is liable to tax in India on net basis and it can claim

deduction for salary paid to Mr. X for rendering services in India• The salary cost paid to Mr. X for services rendered in India

does not constitute ‘HO expenditure’ in terms of S. 44C, full deduction is available.

• The payment made by PE to Mr. X will be covered under the purview of Domestic TP as payment is made to related party covered under S. 40A(2)(b)• PE will be required to benchmark the payment made to Mr. X

to ALP and required to comply with all the provisions of Domestic TP.• The fact that both A Ltd and Mr. X are non-residents is not

relevant. • SDT can be applicable to transactions with / between non-

residents.

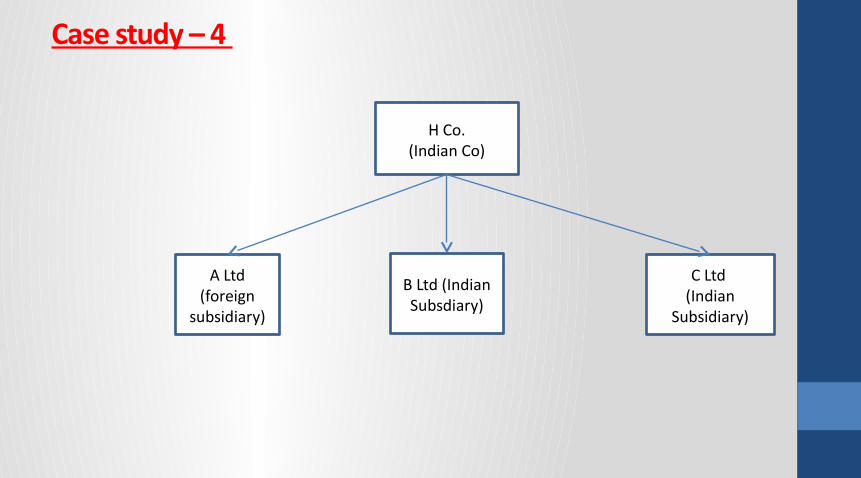

Case study – 4

H Co.(Indian Co)

A Ltd (foreign

subsidiary)

B Ltd (Indian Subsdiary)

C Ltd (Indian

Subsidiary)

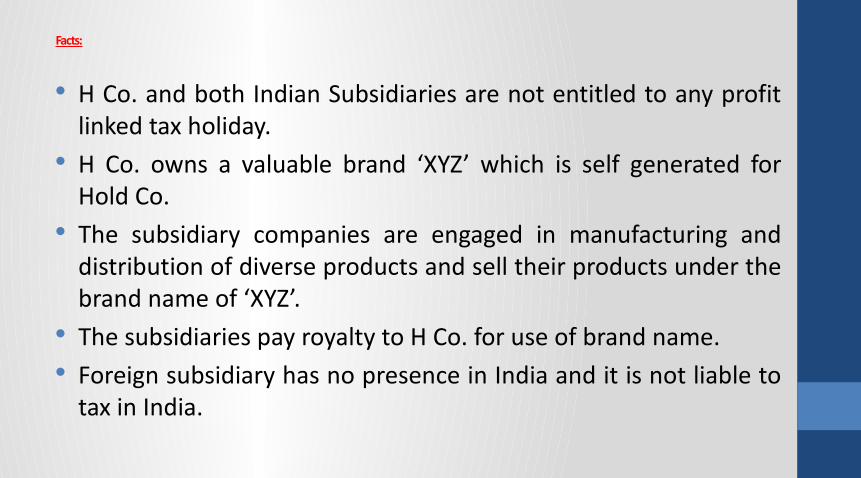

Facts:

H Co. and both Indian Subsidiaries are not entitled to any profit linked tax holiday.

H Co. owns a valuable brand ‘XYZ’ which is self generated for Hold Co.

The subsidiary companies are engaged in manufacturing and distribution of diverse products and sell their products under the brand name of ‘XYZ’.

The subsidiaries pay royalty to H Co. for use of brand name. Foreign subsidiary has no presence in India and it is not liable to

tax in India.

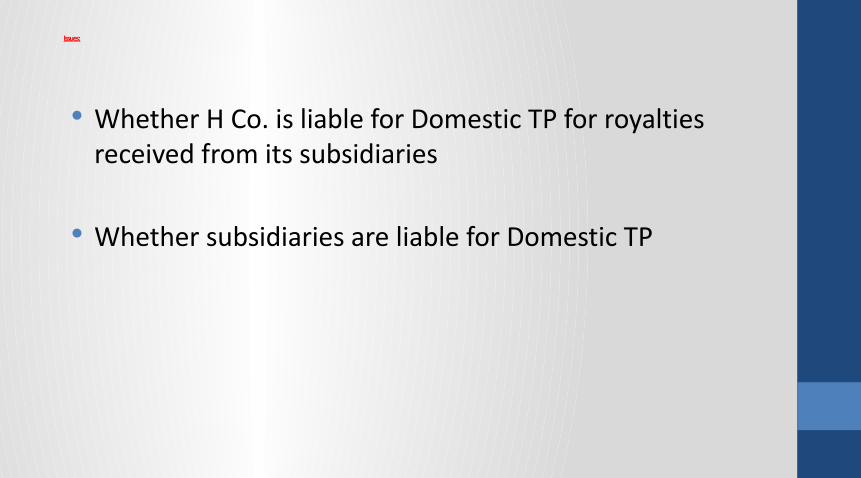

Issues:

Whether H Co. is liable for Domestic TP for royalties received from its subsidiaries

Whether subsidiaries are liable for Domestic TP

Analysis:

Applicability of Domestic TP for H. Co

Even though B Ltd and C Ltd (domestic subsidiaries)are related parties covered under 40A(2)(b), the royalty income received from subsidiaries is not covered by the provisions of domestic TP as it covers only the payments made to related parties and not income transactions.

However, A ltd (foreign subsidiary) is an AE for H Co. Royalty Income received from A Ltd will constitutes Intl. transaction for H Co. and it is required to benchmark royalty income received

Applicability of Domestic TP to A Ltd

A Ltd has no presence in India and not liable to tax in India hence S. 40A(2)(b) and Domestic TP provisions are not applicable.

Applicability of Domestic TP to B Ltd & C Ltd

B Ltd and C Ltd (domestic subsidiaries)are related parties covered under 40A(2)(b), the provisions of Domestic TP will be applicable.

Royalty fees paid by B Ltd and C Ltd will be required to be benchmarked with ALP.

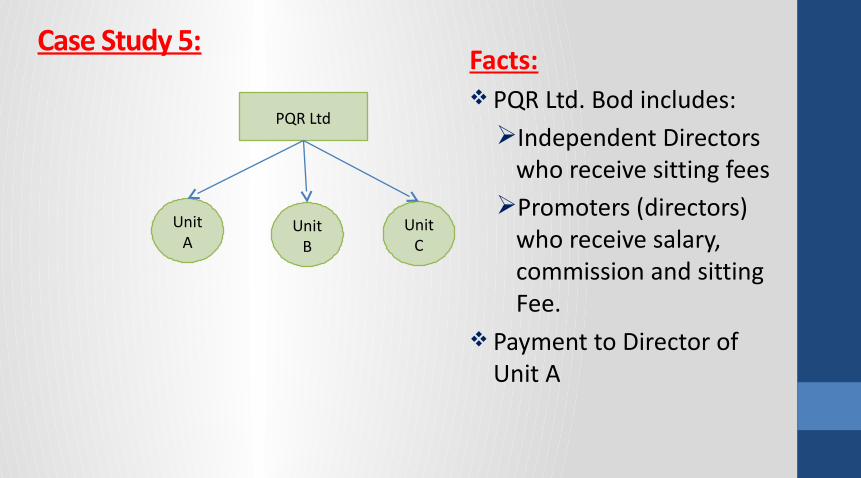

Case Study 5:

PQR Ltd

Unit A

Unit B

Unit C

Facts: PQR Ltd. Bod includes:

Independent Directors who receive sitting fees

Promoters (directors) who receive salary, commission and sitting Fee.

Payment to Director of Unit A

Issues

Are the payments made to Directors covered under Specified Domestic Transactions?

Methods to determine the Arm’s length Price?

Benchmarking Of Directors Remuneration

It can be benchmarked based on their work experience and qualification.

Further the remuneration paid to them is as per the limit of Companies Act 1956.

However there is no streamlined process to benchmark the transaction.

33

FACTS A and B are related parties under S.

40A (2)(b) A pays interest to B which is

assessable under the head “Income from Other Sources”.

Case study – 7A

“A”

“B”

Whether the provisions of Domestic Transfer Pricing would apply to A for the payment of interest to B (related party) and which is claimed as a deduction while computing income under the head “Income from Other Sources” (IFOS)? In other words can the provisions of Domestic TP apply to the computation of Income under the head IFOS as they apply to business income?

Issue

Section 58(2) of the Act states that: “The provisions of section 40A shall, so far as may be, apply in computing the income chargeable under the head "Income from other sources" as they apply in computing the income chargeable under the head "Profits and gains of business or profession.

In view of the specific reference to section 40A in section 58(2), it is clear that the disallowance can be made in respect of excessive payments made to related parties and claimed as deduction while computing IFOS.

The reference to section 40A(2)(b) made in section 92BA(i) is merely to qualify the persons (related parties) to whom the payments are made and are covered under the provisions of Domestic TP.

Analysis

Also, section 92(2A) does not state that any allowance of an expenditure should be in respect of such income which are assessable under Business Income.

Further, the provisions of section 40A(2) and section 58(2) were introduced simultaneously in Finance Act, 1968 and the Memorandum to Finance Act, 1968 clarifies that the provisions of section 40A will also apply for the purpose of computation of IFOS.

Thus, the provisions of Domestic TP would apply for the transactions with related parties even in the case where the income is charged under IFOS

Analysis

FACTS A and B are related parties under S. 40A

(2)(b) A paid brokerage to B for sale of Capital

Asset and claimed such expenditure as deduction while computing Capital Gains.

Case study – 7B

“A”

“B”

Whether the provisions of Domestic Transfer Pricing would apply to A on such brokerage payments on the fact that there is no specific provision similar to section 58(2) which extends the scope of section 40A(2) to computation of income under the head “Capital Gains” (CG)

Issue

Section 92BA(i) refers to any expenditure in respect of which payment has been made or is to be made to a person referred to in 40A(2)(b).

The provision does not state that it applies only to expenditure which is claimed as deduction under Business Income. It covers all payments to related parties covered within the scope of s. 40A(2)(b) irrespective of the head of income under which such payments are claimed as deduction.

Analysis

Also, section 92(2A) does not state that any allowance of an expenditure should be in respect of such income which are assessable under Business Income.

Thus, it is possible to argue that the provisions of Domestic TP would apply for the transactions with related parties even in the case where the income is charged under the head “Capital Gains”.

Both the views are equally strong and arguable.

Analysis

FACTS A Ltd and B Ltd are related parties under S.

40A (2)(b) A Ltd. and B Ltd. are paying tax under the

normal provision of Income tax.

Case study – 8

“A LTD”

“B LTD”

Whether the provisions of Domestic Transfer Pricing would apply even if the transactions are revenue neutral?

Issue

The Supreme Court in the case of Glaxo Smithkline Asia (P) Ltd. (2010) 195 Taxman 35 (SC) held that there was a need to extend TP regulations (as applicable to Int. Tr) to domestic transactions and suggested that Ministry of Finance should consider appropriate provisions in law to make TP regulations applicable to such related party domestic transactions.

The Finance Act 2012 has inserted the provisions of Domestic TP for the transactions with the related parties.

Analysis

The provisions of Domestic TP would apply to all the transactions with the related parties even if the transactions are tax neutral.

Various representations were made stating that the excess income is already being taxed at the same rate by the person receiving such income and thus, the provisions of Domestic TP should not apply to such transactions between related parties where the taxes are paid at the same rate.

Analysis

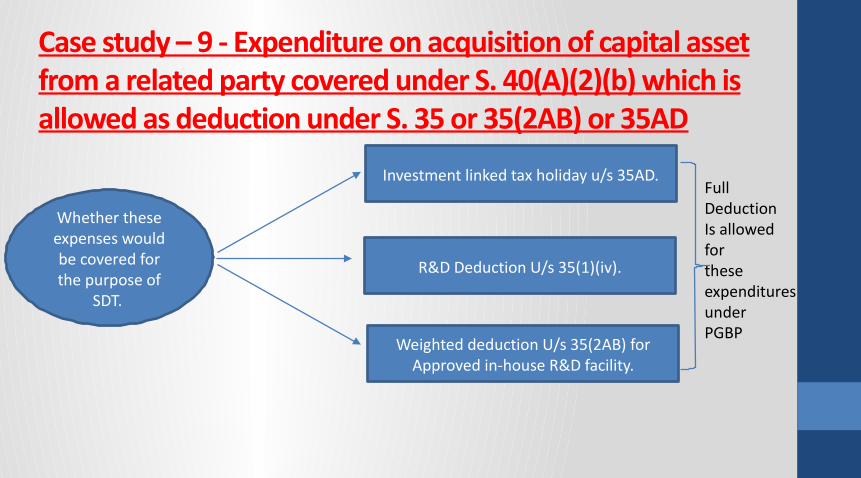

Case study – 9 - Expenditure on acquisition of capital asset from a related party covered under S. 40(A)(2)(b) which is allowed as deduction under S. 35 or 35(2AB) or 35AD

Investment linked tax holiday u/s 35AD.

Whether these expenses would be covered for the purpose of

SDT.

R&D Deduction U/s 35(1)(iv).

Weighted deduction U/s 35(2AB) for Approved in-house R&D facility.

FullDeduction Is allowed for these expenditures under PGBP

Analysis

S. 92BA(i) refers to any expenditure in respect of which payment has been made or is to be made to a person referred to in S.40A(2)(b).

There are no restrictions or limitations in either S. 92BA(i) or S. 92(2A) that these provisions are restricted in their application to revenue expenditure

Reference to S. 40A(2)(b) in S. 92BA(i) merely governs the relationship specified in that section and not the nature of expenditure i.e Capital or revenue

Analysis

Guidance note of ICAI defines expenditure as “Incurring a liability, disbursement of cash or transfer of property for the purpose of obtaining assets, goods or services”.

From above it is clear that the term expenditure will include both revenue and capital. Wherever legislature intended to exclude capital expenditure from the scope of expenditure it has specifically provided.

There is also a possibility that any excessive payments towards capital asset may result in artificially reducing the taxable income of the taxpayer. Hence application of ALP may be considered to determine correct profits.

Case study – 10 - Interplay between 40(A)(2)(a) and 92BA

ISSUE:

If the payment exceeds ALP as determined under S. 92C will disallowance under 40(A)(2)(a) be attracted?

Analysis: Section 40A of the Act empowers the AO to disallow unreasonable expenditure

incurred between related parties. However there is no specific method provided under these sections.

SC in case of Glaxo Smith Kline Asia (P) Ltd suggested that ministry of finance should consider appropriate provisions in law to make TP regulations applicable to such domestic related party transactions which would provide objectivity in determination of income from such parties and determination of reasonableness of expenditure between related domestic parties.

Analysis: S. 40(A)(2) is a disallowance provision, while allowance may be governed by S.

92(2A) as per ALP norm, If an expenditure is considered as excessive having regard to FMV or having regard to legitimate needs or having regard to benefit received, the disallowance can still be attracted as per the main provision of S. 40A(2).

Proviso which has been added to S. 40A(2)(a) upon introduction of TP can be considered as further caveat to the main provision. The proviso can be attracted when principal provision is attracted in different contingencies on ground of considered as excessive having regard to FMV.

Nihar Jambusaria

THANK YOU

![BELIZE: POLICE (AMENDMENT) ACT, 2018 ARRANGEMENT OF … · 2018-04-17 · 13. Amendment of section 28. 14. Amendment of section 29. 15 ... Insertion of new section 40A. No. 7] Police](https://img.pdfslide.us/doc/110x75/5f52bb531286655617619e77/belize-police-amendment-act-2018-arrangement-of-2018-04-17-13-amendment-of.jpg)