Embed Size (px)

Citation preview

Special Risks in ETFs

Addressing Myths and Uncovering Real Concerns

Sponsored by:

Speakers:

Dave Nadig Director of Research IndexUniverse

Joel Dickson Senior Investment Analyst & Principal Vanguard

Matt Hougan President, ETF Analytics Global Head of Editorial IndexUniverse

Paul Britt ETF Analyst IndexUniverse

Special Risks?

ETFs’ Bad Name

Adverse Trends in Markets Critical Reports Unfavorable Press Regulatory Scrutiny

Today’s Agenda Do ETFs Deliver?

▪ Tracking Error

▪ Expectation Error: Leveraged Products

▪ Contango

▪ Transparency

Can ETFs Hurt You? ▪ Counterparty Risk

▪ Closure

▪ Tax Distributions

▪ Collapse

Are ETFs Bad For The Market? ▪ Correlations

▪ Volatility

▪ Systemic & Settlement Risk

▪ Capital Formation

Do ETFs Deliver?

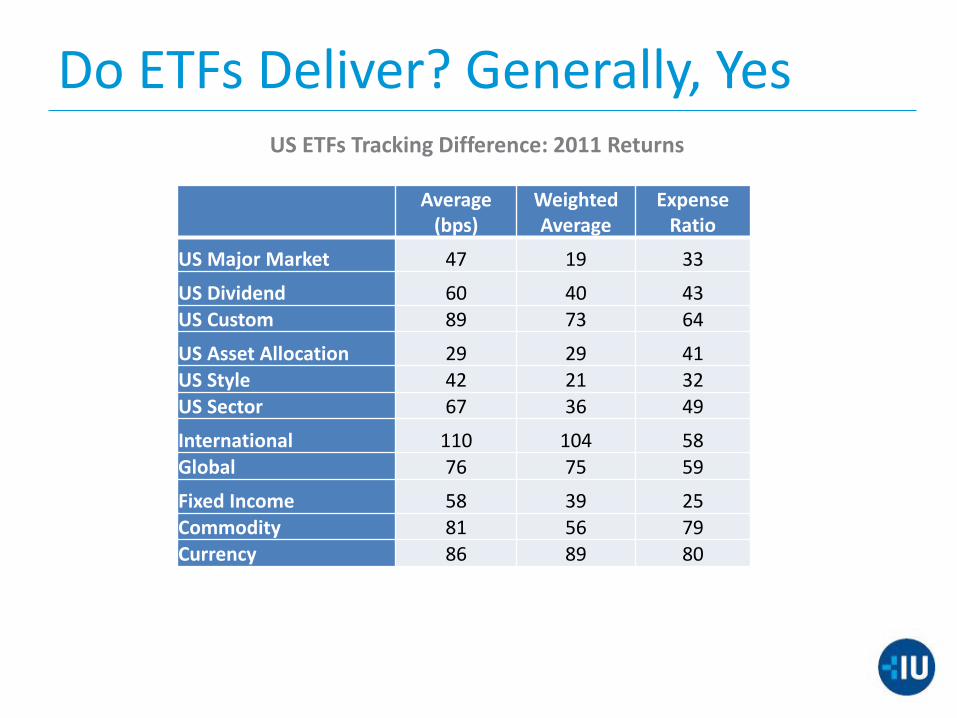

Do ETFs Deliver? Generally, Yes US ETFs Tracking Difference: 2011 Returns

Average

(bps) Weighted Average

Expense Ratio

US Major Market 47 19 33

US Dividend 60 40 43 US Custom 89 73 64

US Asset Allocation 29 29 41 US Style 42 21 32

US Sector 67 36 49

International 110 104 58

Global 76 75 59

Fixed Income 58 39 25

Commodity 81 56 79 Currency 86 89 80

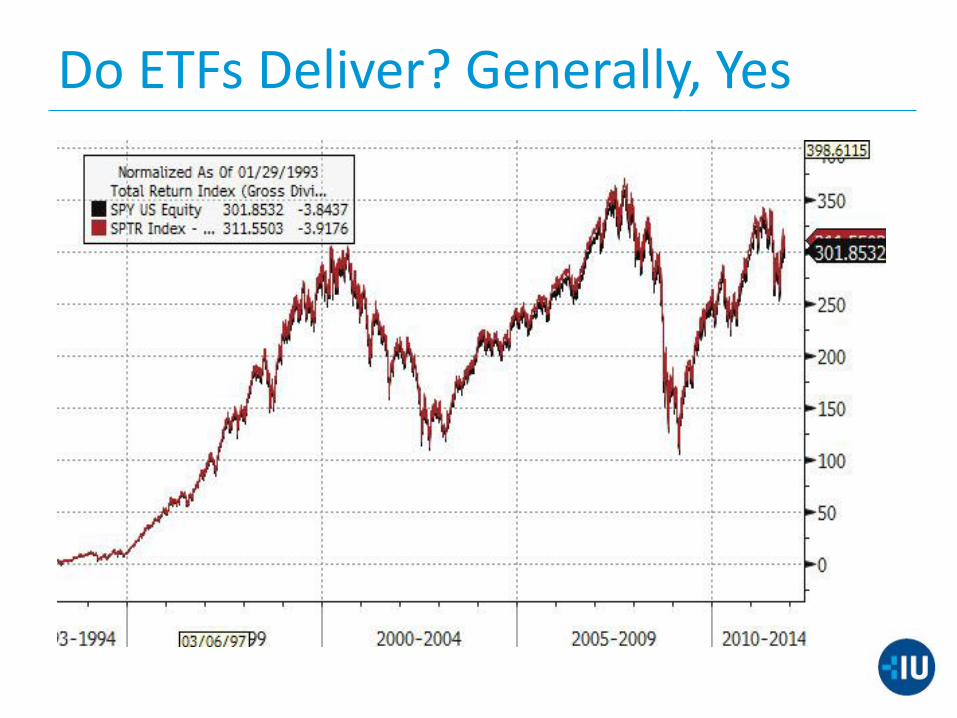

Do ETFs Deliver? Generally, Yes

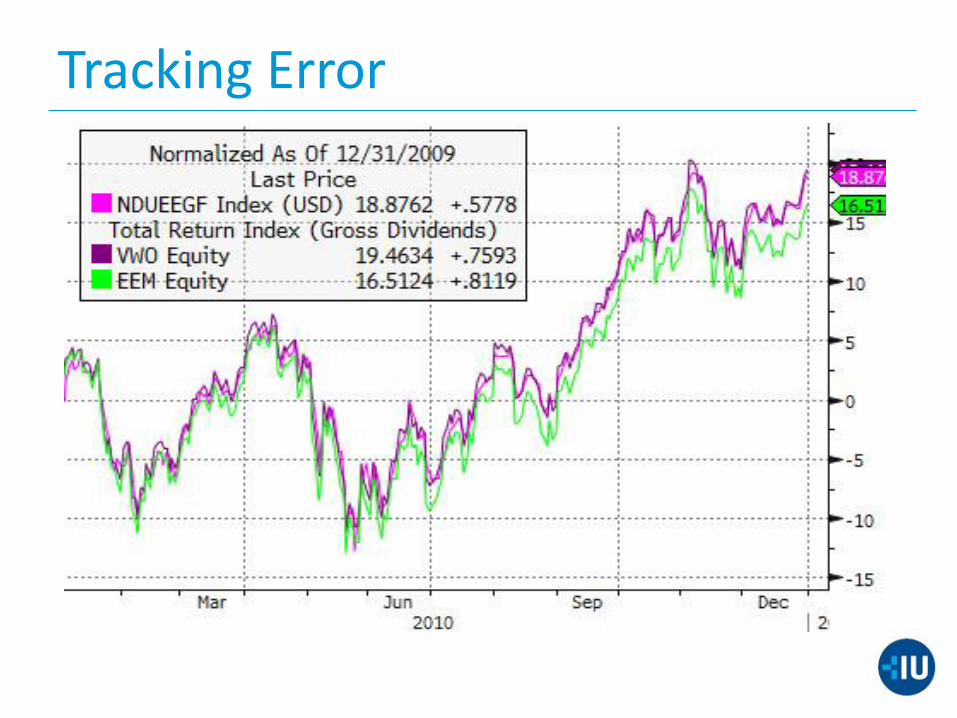

Tracking Error

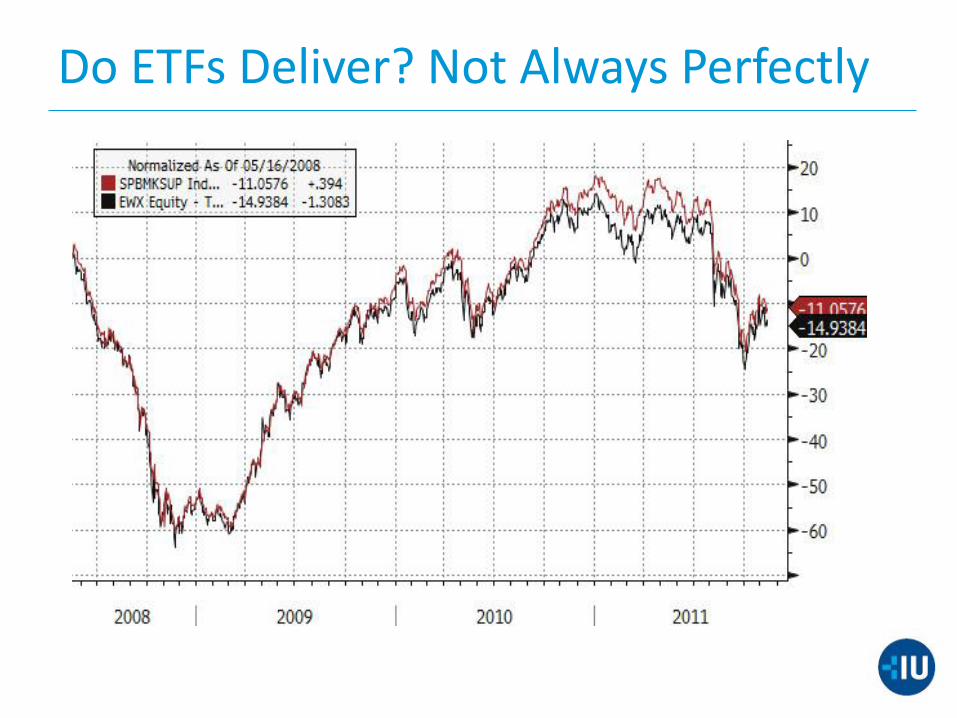

Do ETFs Deliver? Not Always Perfectly

Expectations Error

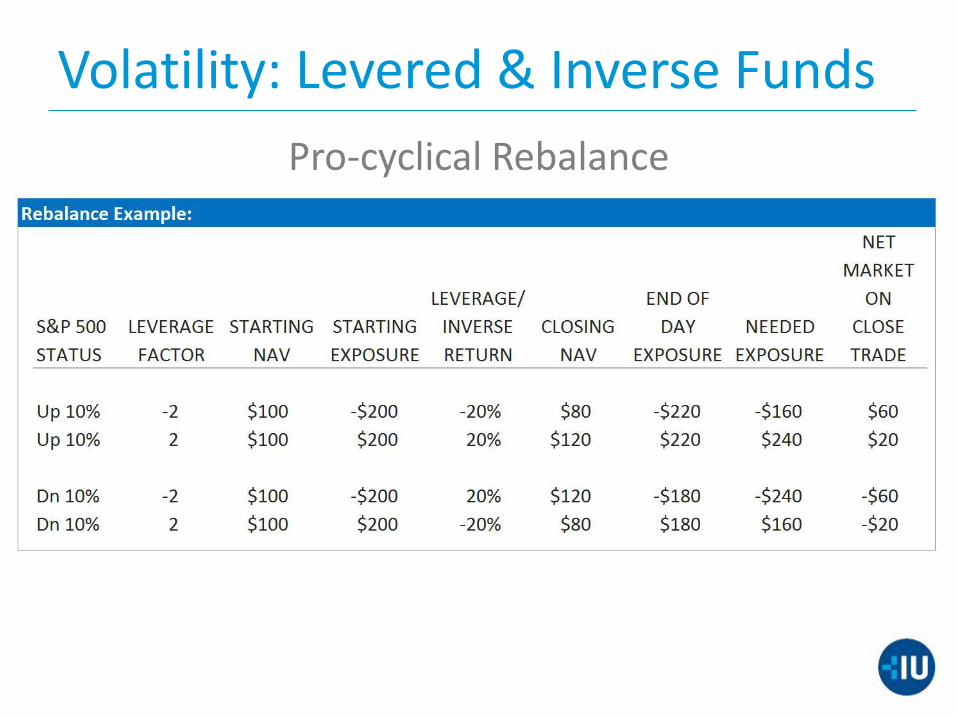

Daily Resetting: Leverage & Inverse

A Simple Promise: 1 Day’s Return

▪ Daily rebalance can ruin long term returns

▪ Is full disclosure adequate protection for retail investors?

▪ Minimal systemic risk impact

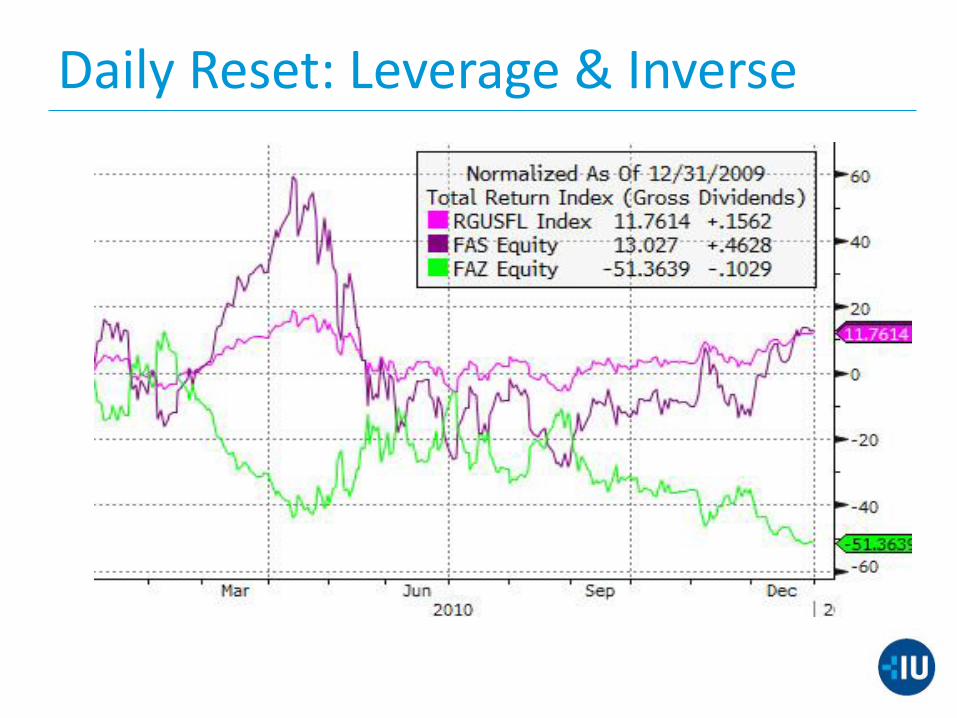

Daily Reset: Leverage & Inverse

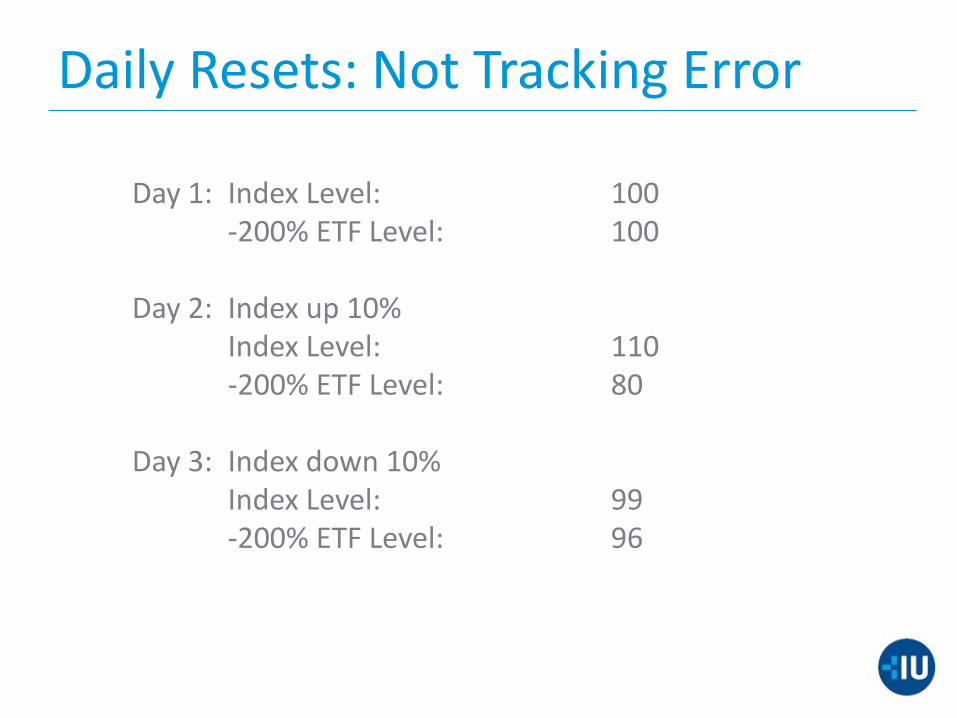

Daily Resets: Not Tracking Error

Day 1: Index Level: 100 -200% ETF Level: 100 Day 2: Index up 10% Index Level: 110 -200% ETF Level: 80 Day 3: Index down 10% Index Level: 99 -200% ETF Level: 96

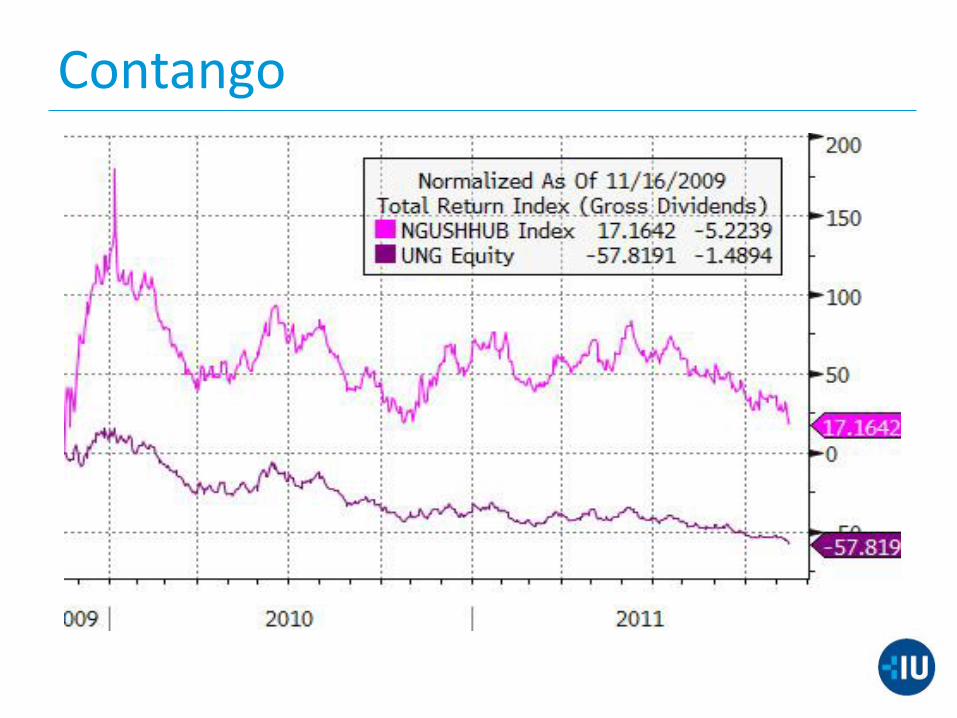

Contango

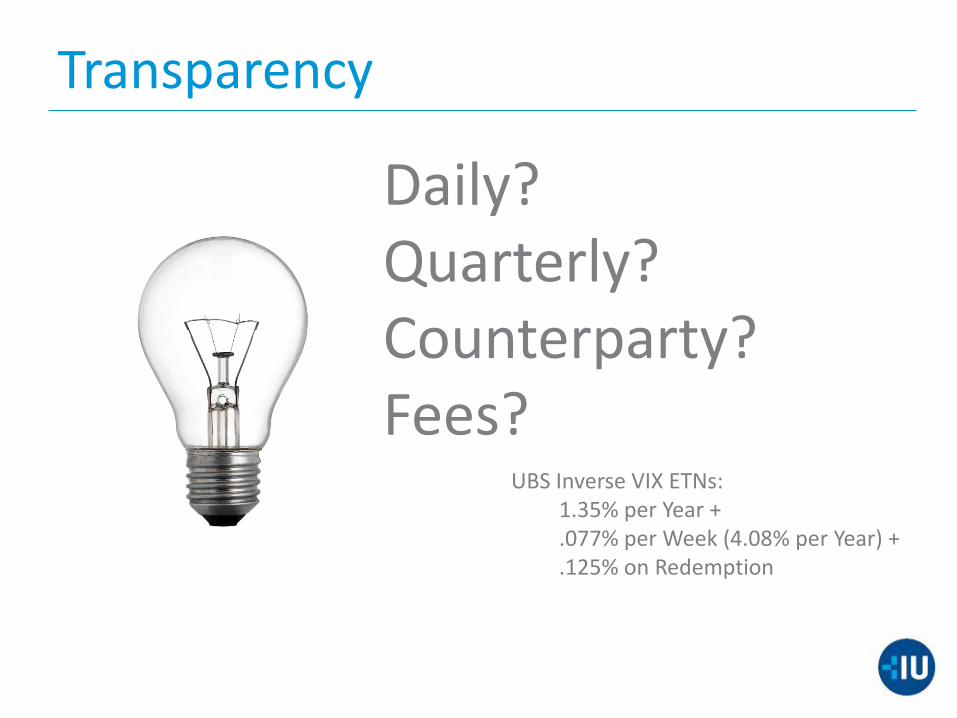

Transparency

Daily? Quarterly? Counterparty? Fees?

UBS Inverse VIX ETNs: 1.35% per Year + .077% per Week (4.08% per Year) + .125% on Redemption

Tax Efficiency

Are ETFs Tax-Efficient? Mostly Yes.

Until they’re not.

Biggest risk in REITs, MLPs, etc.

Understand K-1s.

Can ETFs Hurt You?

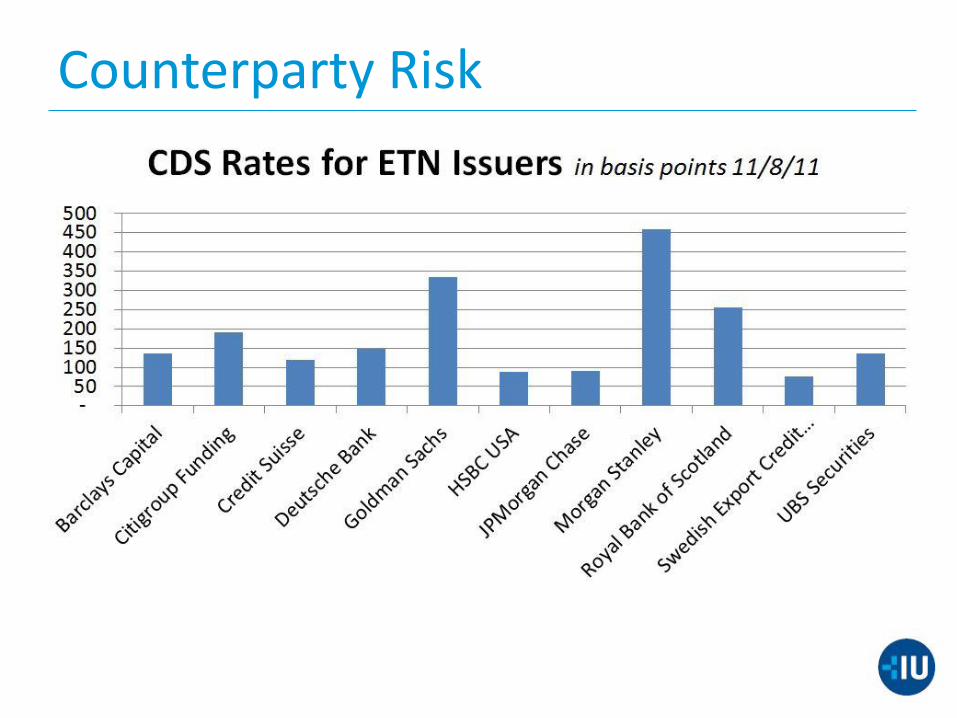

Counterparty Risk Counterparty Risk is Real, but threatens

Individuals more than Markets

▪ ETN

▪ Over the Counter Derivatives

▪ Listed Derivatives*

▪ Securities Lending

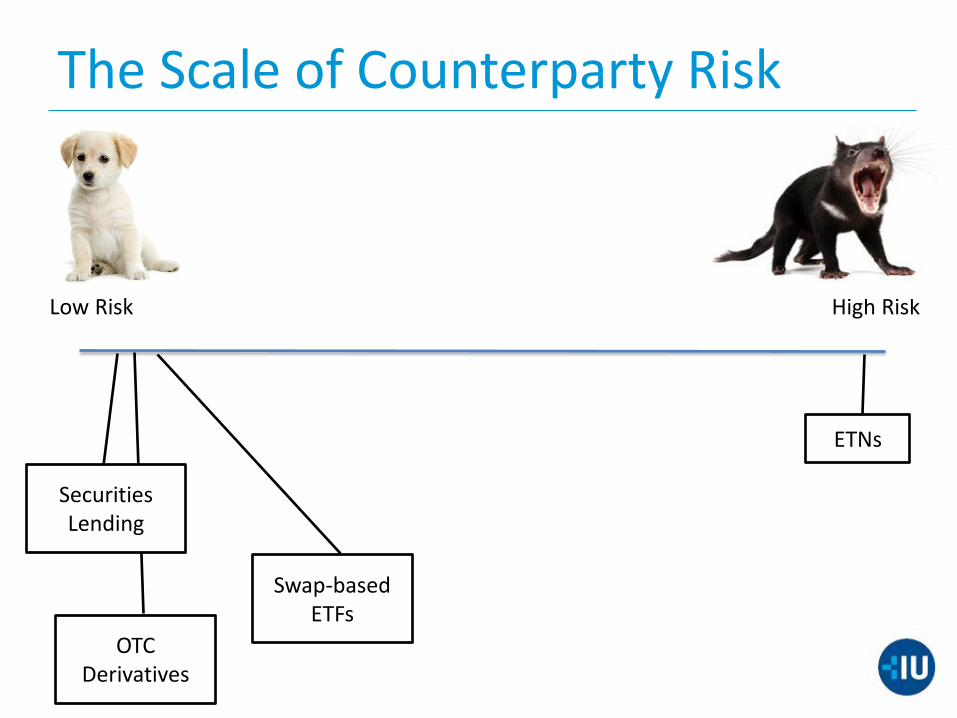

The Scale of Counterparty Risk

High Risk Low Risk

ETNs

Swap-based ETFs

OTC Derivatives

Securities Lending

Counterparty Risk

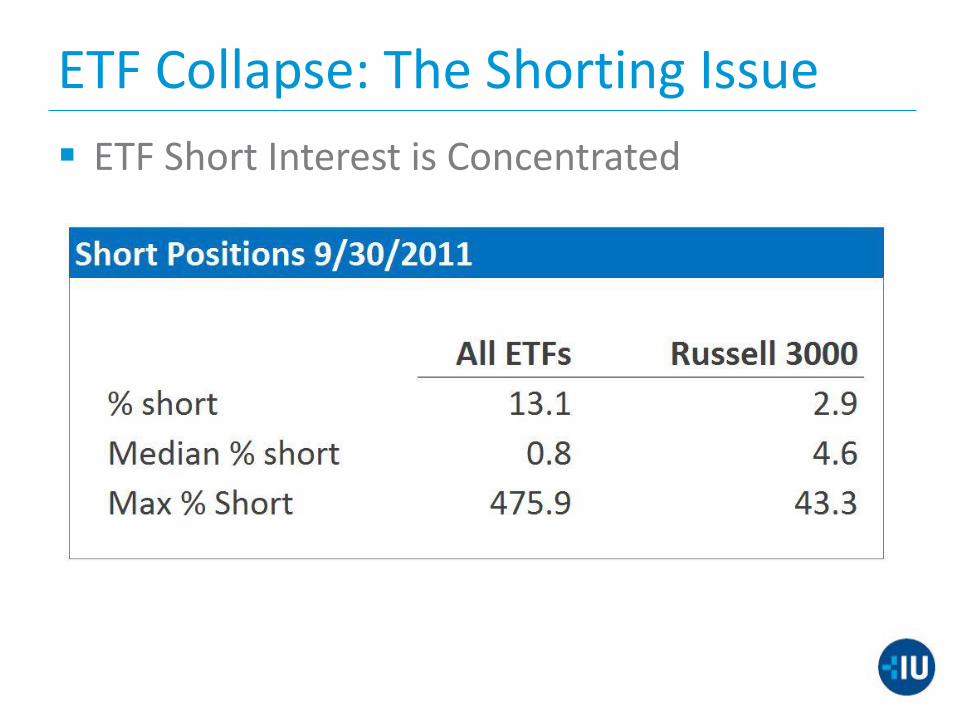

ETF Collapse: The Shorting Issue

ETF Short Interest is Concentrated

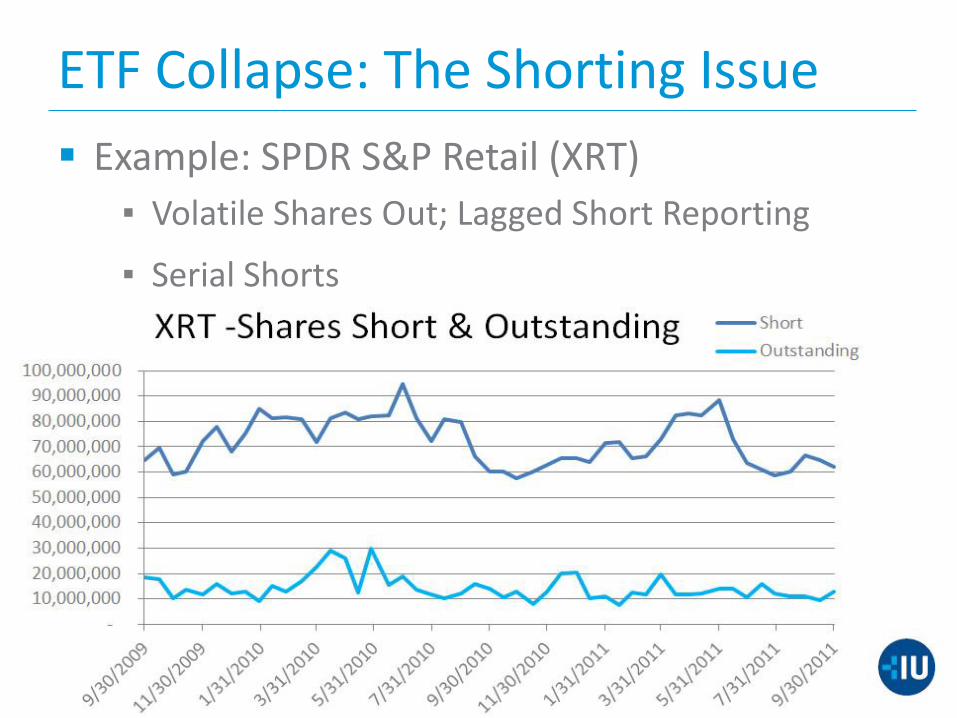

ETF Collapse: The Shorting Issue

Example: SPDR S&P Retail (XRT)

▪ Volatile Shares Out; Lagged Short Reporting

▪ Serial Shorts

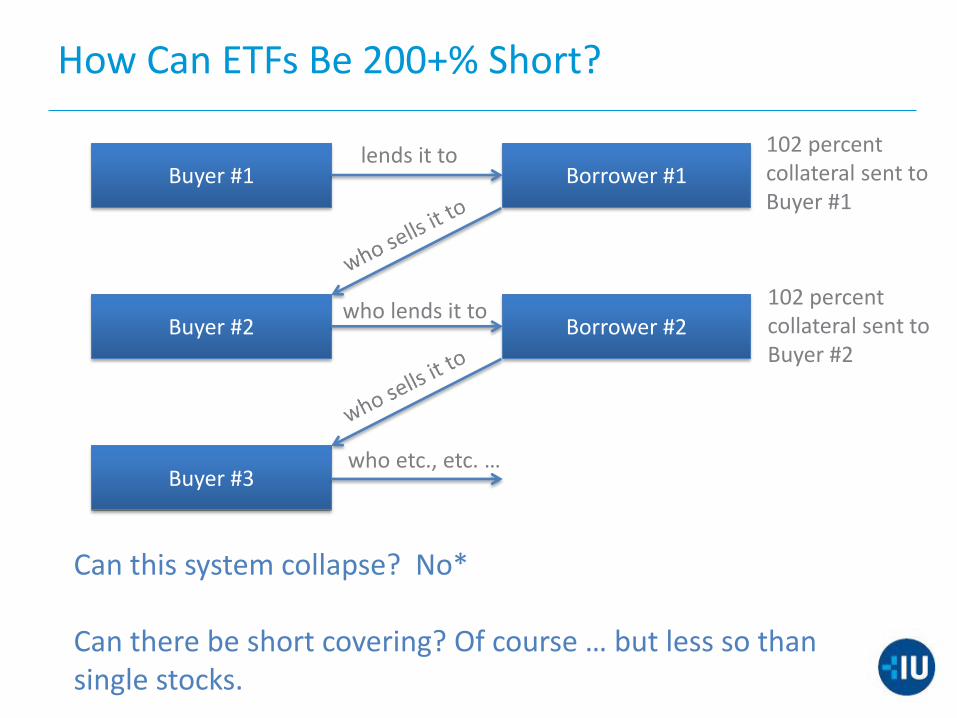

who lends it to

How Can ETFs Be 200+% Short?

Buyer #1 Borrower #1

Buyer #2

Buyer #3

lends it to 102 percent collateral sent to Buyer #1

102 percent collateral sent to Buyer #2

Can this system collapse? No* Can there be short covering? Of course … but less so than single stocks.

Borrower #2

who etc., etc. …

Are ETFs Bad for the Market?

Do ETFs break capital markets?

Are ETFs the tail that wags the dog?

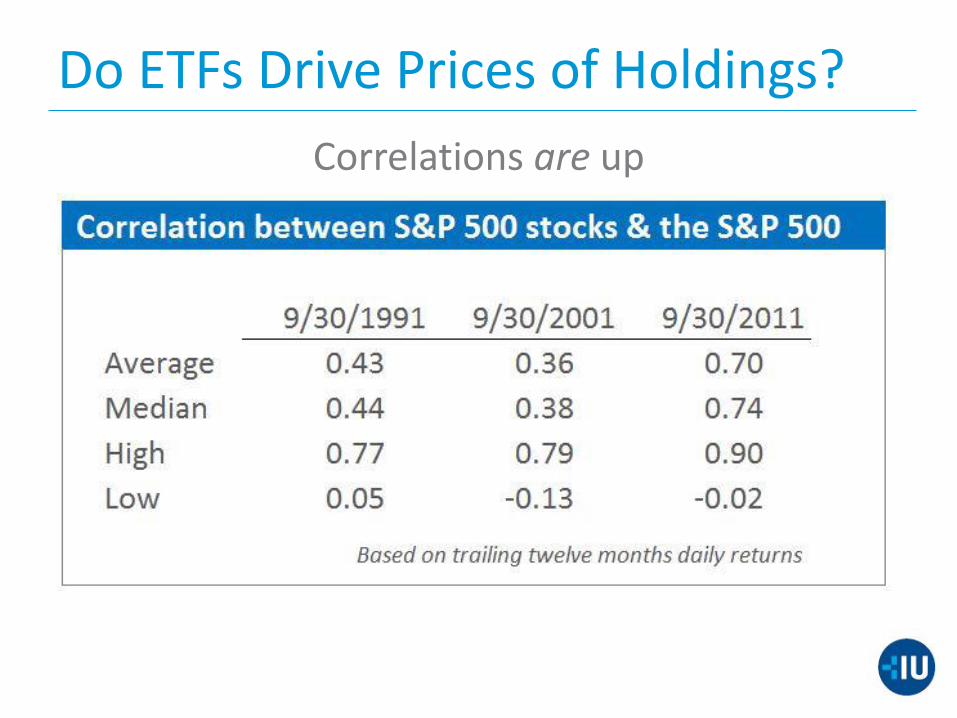

Do ETFs Drive Prices of Holdings?

Correlations are up

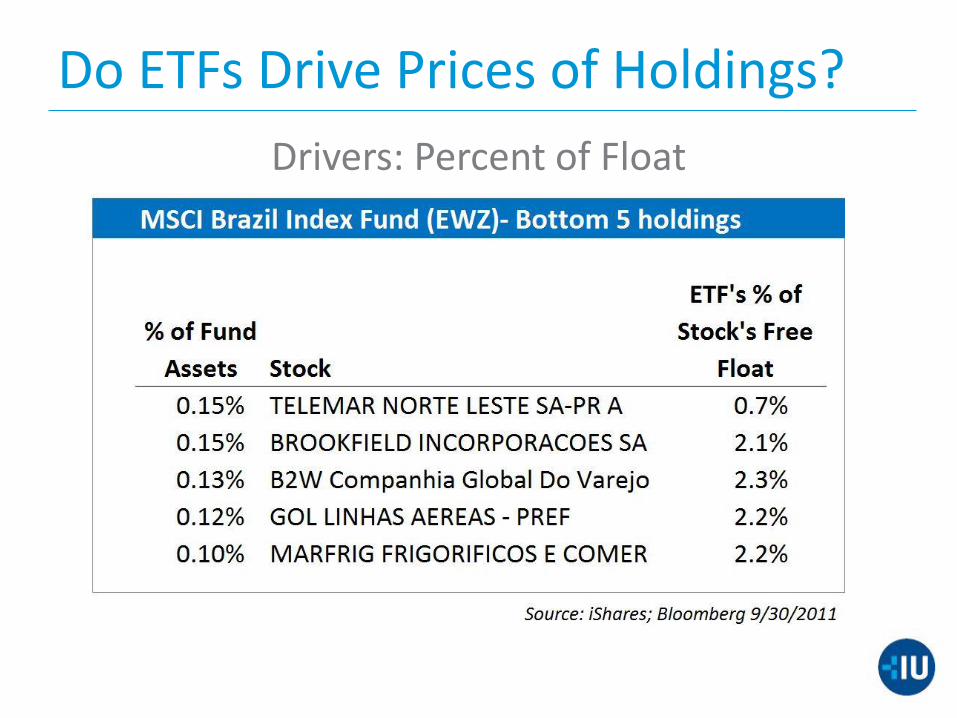

Do ETFs Drive Prices of Holdings?

Drivers: Percent of Float

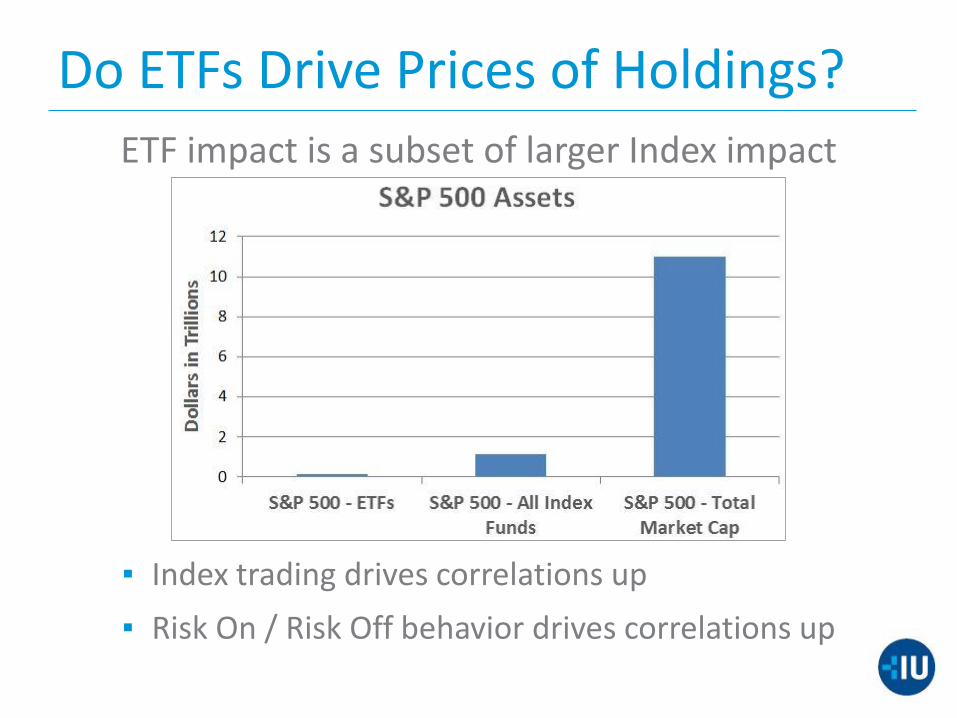

Do ETFs Drive Prices of Holdings?

ETF impact is a subset of larger Index impact

▪ Index trading drives correlations up

▪ Risk On / Risk Off behavior drives correlations up

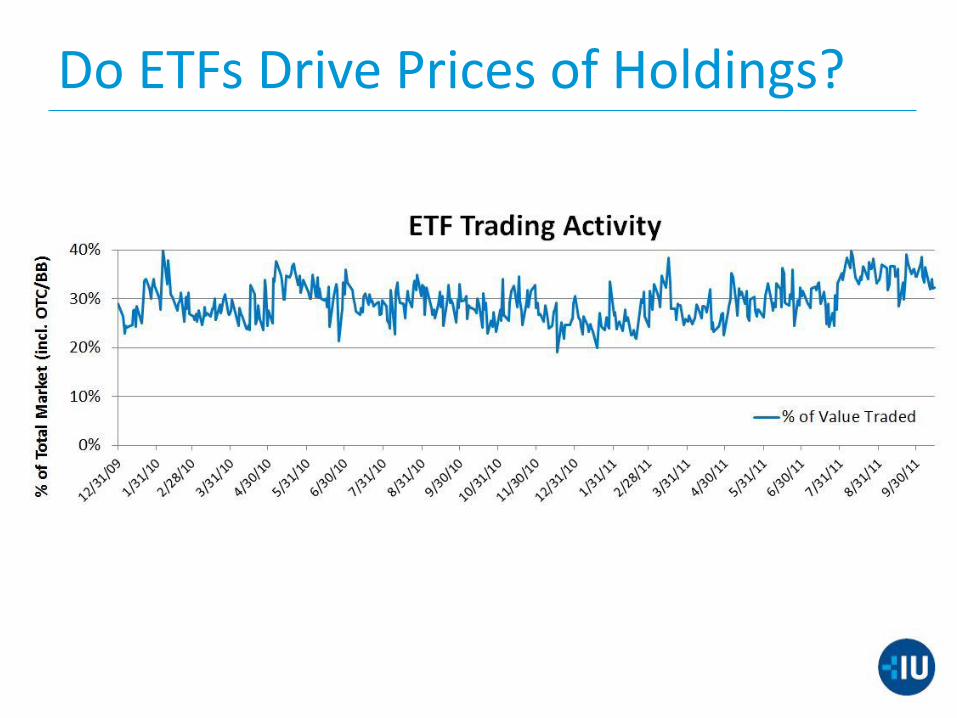

Do ETFs Drive Prices of Holdings?

Do ETFs Drive Prices of Holdings?

High Frequency Trading Increases Correlations

▪ Index Arbitrage

▪ Best Execution

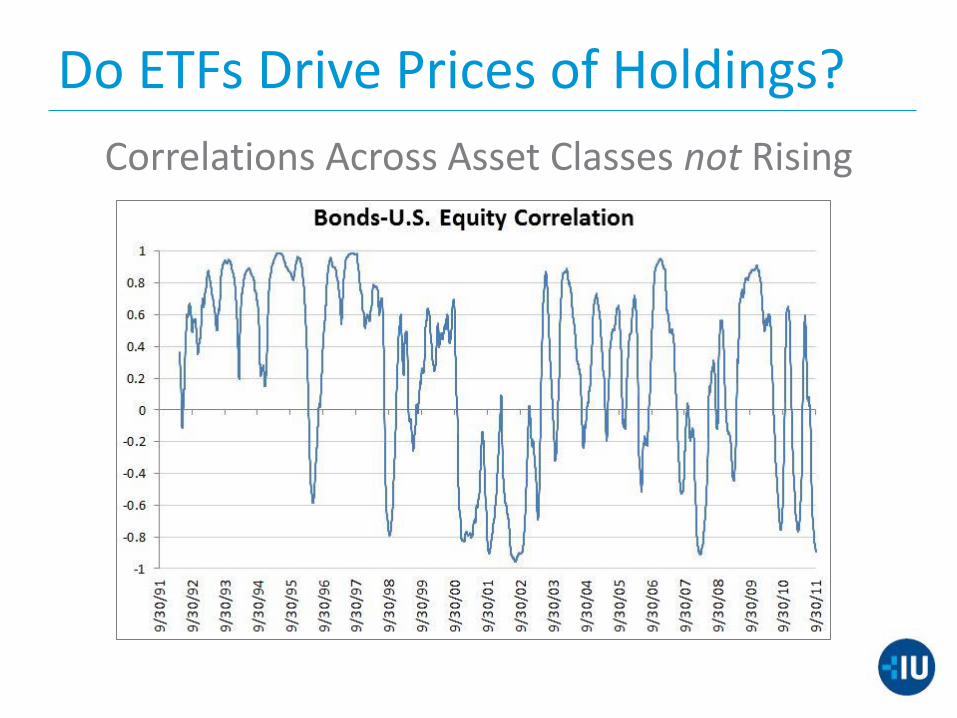

Do ETFs Drive Prices of Holdings?

Correlations Across Asset Classes not Rising

Volatility: Levered & Inverse Funds

ETFs blamed for End-of-Day Market Volatility

Facts don’t support the claim

▪ Tiny assets and net exposure

▪ Pro-cyclical Rebalance

▪ No evidence that L & I funds increase volatility

Volatility: Levered & Inverse Funds

Pro-cyclical Rebalance

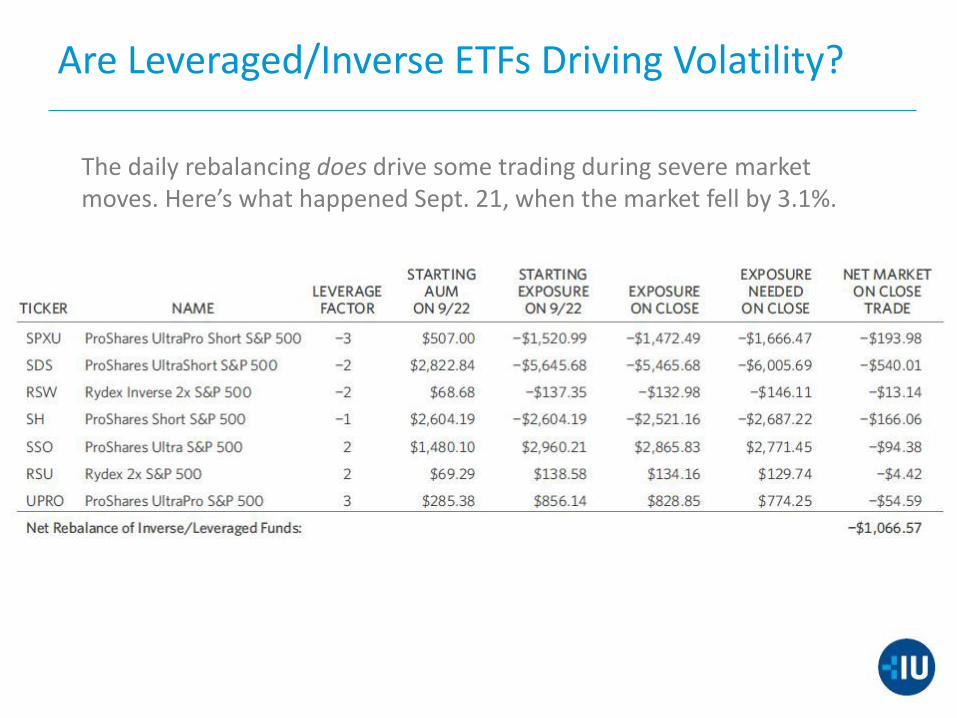

Are Leveraged/Inverse ETFs Driving Volatility?

The daily rebalancing does drive some trading during severe market moves. Here’s what happened Sept. 21, when the market fell by 3.1%.

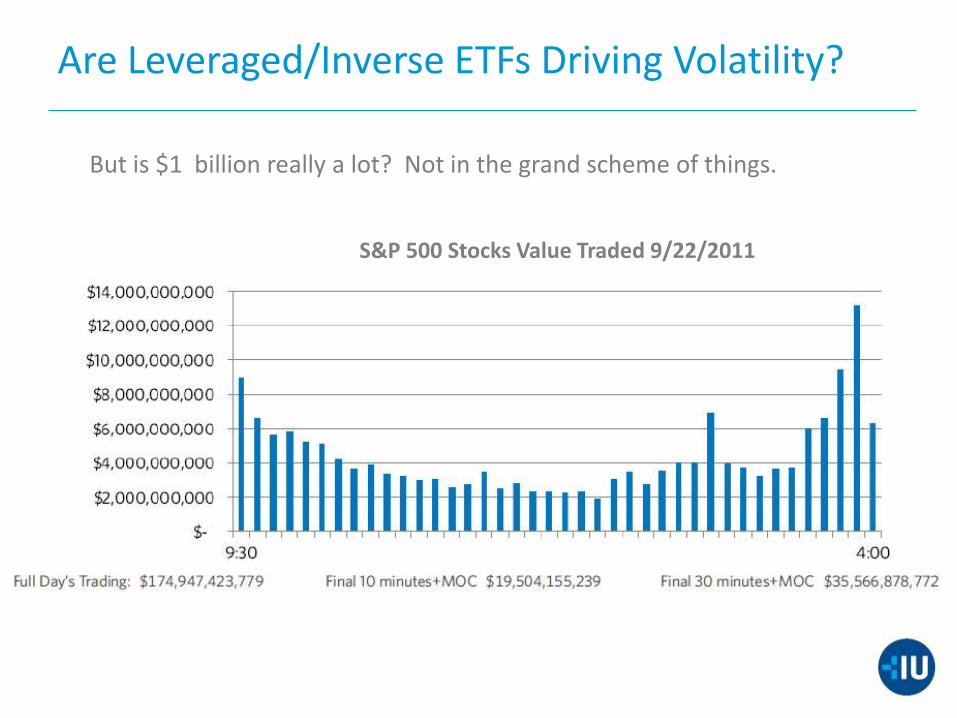

Are Leveraged/Inverse ETFs Driving Volatility?

But is $1 billion really a lot? Not in the grand scheme of things.

S&P 500 Stocks Value Traded 9/22/2011

Volatility: Levered & Inverse Funds

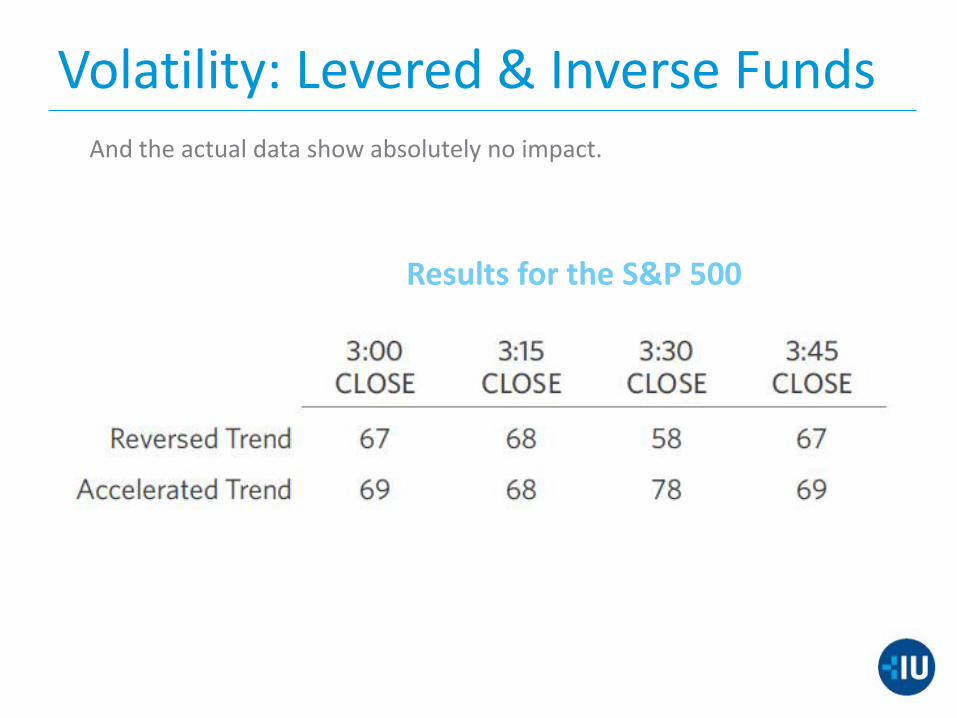

Results for the S&P 500

And the actual data show absolutely no impact.

Broken Trades

Fact #1: Nearly Every security on the SHO list is an ETF.

Fact #2: Virtually no ETF trades “fail.”

Broken Trades

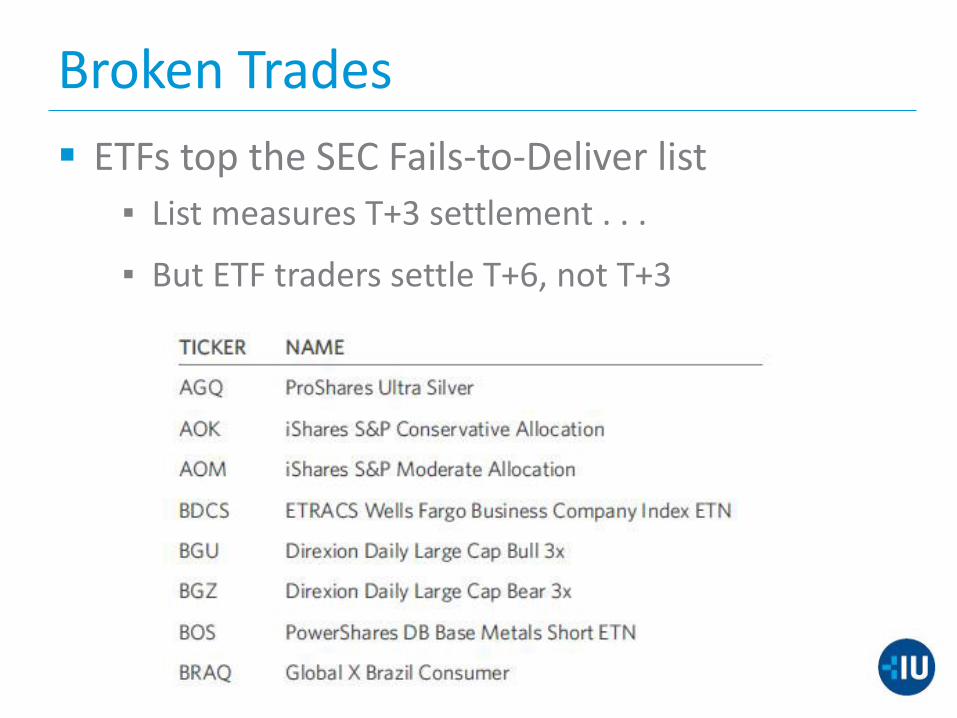

ETFs top the SEC Fails-to-Deliver list

▪ List measures T+3 settlement . . .

▪ But ETF traders settle T+6, not T+3

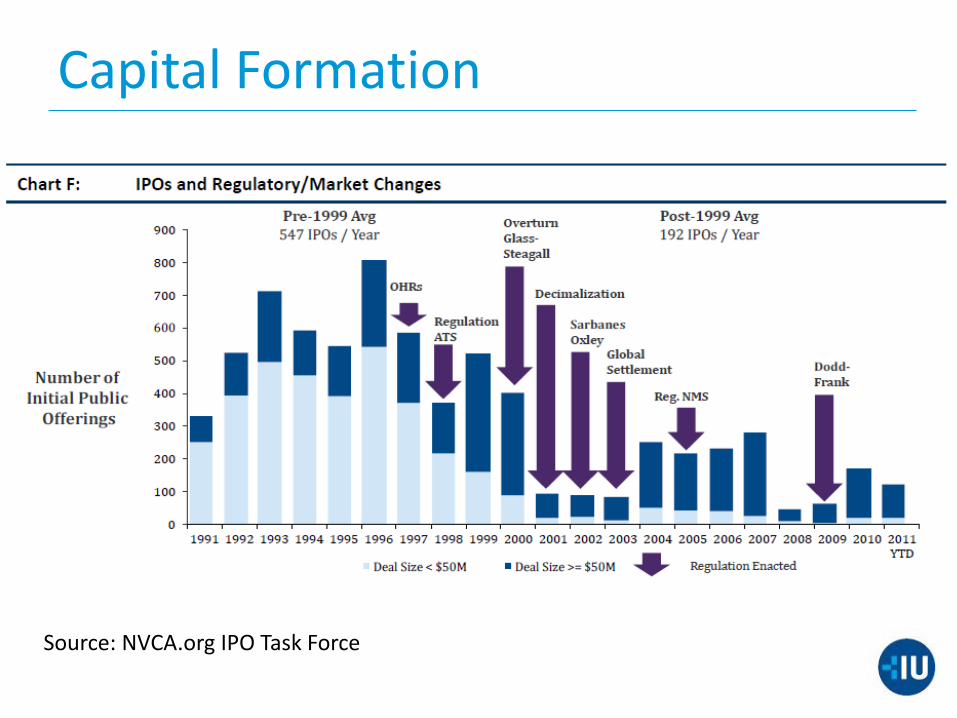

Capital Formation

Source: NVCA.org IPO Task Force

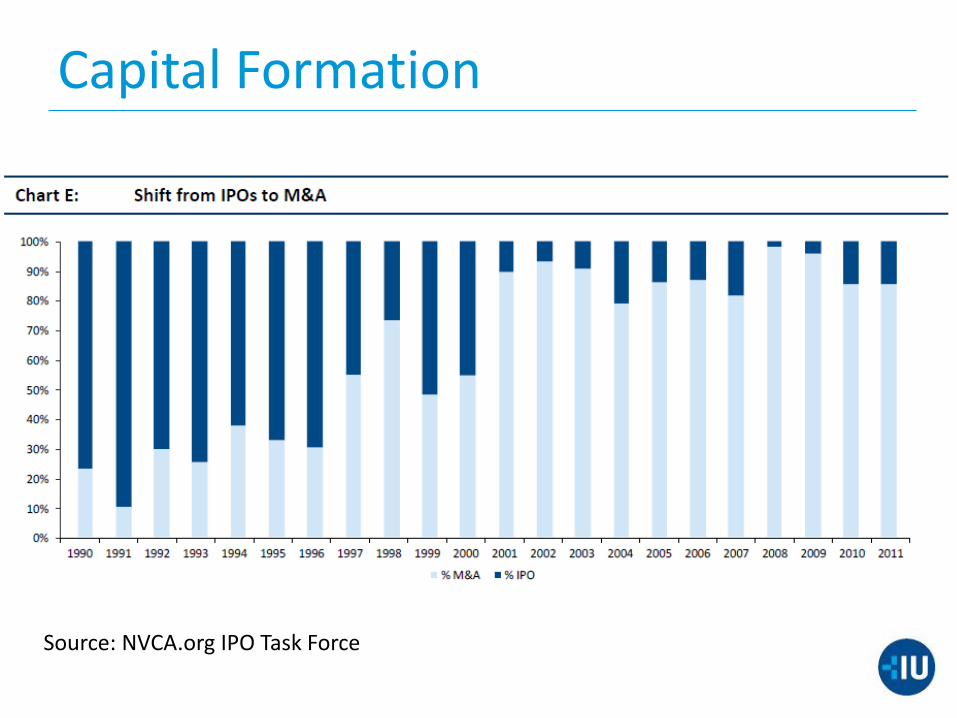

Capital Formation

Source: NVCA.org IPO Task Force

Outlook

Regulatory

▪ SEC March 2011 derivative review

▪ CFTC Oct 2011 new position limit guidelines

Labeling

▪ Name system floated by iShares

Access

▪ Raise the bar for geared funds, volatility products

Speakers:

Dave Nadig Director of Research IndexUniverse

Joel Dickson Senior Investment Analyst & Principal Vanguard

Matt Hougan President, ETF Analytics Global Head of Editorial IndexUniverse

Paul Britt ETF Analyst IndexUniverse

Thank you

For More Information: Indexuniverse.com

Vanguard.com