Embed Size (px)

Citation preview

Special Estate Planning & Post-Special Estate Planning & Post-Death Trust AdministrationDeath Trust Administration

Ryan W. LockhartRyan W. LockhartAssociateAssociate

Phone: (925) 944-9700Phone: (925) 944-9700Fax: (925) 944-9701Fax: (925) 944-9701

Email:[email protected]:[email protected]

Ryan Lockhart graduated with Honors from Ryan Lockhart graduated with Honors from University of Phoenix (B.S. 2007), and then University of Phoenix (B.S. 2007), and then attended Golden Gate University School of Law attended Golden Gate University School of Law (J.D. 2010, L.L.M. in Taxation 2014). At Golden (J.D. 2010, L.L.M. in Taxation 2014). At Golden Gate, Ryan was member of Jesse Carter Society Gate, Ryan was member of Jesse Carter Society for Academic Excellence, and was on the Deanfor Academic Excellence, and was on the Dean’’s s List from Spring 2007 through Spring 2010. List from Spring 2007 through Spring 2010. Ryan was admitted to the California State Bar in Ryan was admitted to the California State Bar in 2010. His practice focuses on estate planning, 2010. His practice focuses on estate planning, wealth transfer planning, estate and gift tax wealth transfer planning, estate and gift tax planning, tax controversy, trust administration planning, tax controversy, trust administration and probateand probate.

Mr. Lockhart is an estate and tax planning Mr. Lockhart is an estate and tax planning attorney whose practice includes:attorney whose practice includes:

• • Trust, estate and probate administrationTrust, estate and probate administration

Membership:Membership:

• • American Bar AssociationAmerican Bar Association• • State Bar of CaliforniaState Bar of California• • Contra Costa County Bar AssociationContra Costa County Bar Association• • Bay Area Young Tax LawyerBay Area Young Tax Lawyer

Education:Education:

• • Golden Gate University School of LawGolden Gate University School of Law• • University of PhoenixUniversity of Phoenix

Practice Areas:Practice Areas:• • Asset ProtectionAsset Protection• • Charitable GivingCharitable Giving• • ConservatorshipsConservatorships• • Health Care DirectivesHealth Care Directives• • Powers of AttorneyPowers of Attorney• • ProbateProbate• • Special Needs TrustsSpecial Needs Trusts• • Succession PlanningSuccession Planning• • Tax PlanningTax Planning• • Trust AdministrationTrust Administration• • Will Contests and Trust DisputesWill Contests and Trust Disputes• • Wills and TrustsWills and Trusts

Jenifer K. LeeceJenifer K. LeecePartnerPartner

Phone: (925) 944-9700Phone: (925) 944-9700Fax: (925) 944-9701Fax: (925) 944-9701

Email:[email protected]:[email protected]

Jenifer Leece's practice focuses on estate planning, Jenifer Leece's practice focuses on estate planning, trust and estate administration and estate related trust and estate administration and estate related litigation. Ms. Leece has extensive litigation and litigation. Ms. Leece has extensive litigation and mediation experience of trust and probate related mediation experience of trust and probate related matters representing trustees, executors, matters representing trustees, executors, beneficiaries and conservators.beneficiaries and conservators.

Ms. Leece graduated from University of California, Davis in Ms. Leece graduated from University of California, Davis in 1990 with a B.A.in International Relations and 1990 with a B.A.in International Relations and Spanish. She received her Juris Doctor from the Spanish. She received her Juris Doctor from the University of San Francisco School of Law in 1994 and University of San Francisco School of Law in 1994 and was admitted to practice in California and federal was admitted to practice in California and federal courts in 1994.courts in 1994.

While at the University of California, Davis and the While at the University of California, Davis and the University of San Francisco School of Law, Ms. Leece University of San Francisco School of Law, Ms. Leece interned at the District Attorney's Office in interned at the District Attorney's Office in Sacramento and San Francisco where she worked as a Sacramento and San Francisco where she worked as a victim advocate with victims of domestic violence and victim advocate with victims of domestic violence and as a certified legal intern in both the felony domestic as a certified legal intern in both the felony domestic violence and narcotics units.violence and narcotics units.

Ms. Leece is an estate planning attorney whose Ms. Leece is an estate planning attorney whose practice includes:practice includes:

• • Estate PlanningEstate Planning• • Trust, estate and probate administrationTrust, estate and probate administration• • LitigationLitigation

Membership:Membership:

• • State Bar of CaliforniaState Bar of California• • Contra Costa County Bar AssociationContra Costa County Bar Association

Education:Education:

• • University of San Francisco School of LawUniversity of San Francisco School of Law• • University of California, DavisUniversity of California, Davis• • University of Salamanca, SpainUniversity of Salamanca, Spain

Practice Areas:Practice Areas:

• • Wills and TrustsWills and Trusts• • Trust AdministrationTrust Administration• • Succession PlanningSuccession Planning• • Will Contests and Trust DisputesWill Contests and Trust Disputes• • ProbateProbate• • Powers of AttorneyPowers of Attorney• • Health Care DirectivesHealth Care Directives• • Special Needs TrustsSpecial Needs Trusts• • ConservatorshipsConservatorships• • Tax PlanningTax Planning• • Asset ProtectionAsset Protection• • Ownership of Real PropertyOwnership of Real Property

NEW TAX ACT REVIEWNEW TAX ACT REVIEW

UNIFIED CREDIT (GIFT/ESTATE TAX UNIFIED CREDIT (GIFT/ESTATE TAX

EXLCLUSION)EXLCLUSION)

PORTABILITYPORTABILITY

ESTATE TAX PLANNING v. INCOME TAX ESTATE TAX PLANNING v. INCOME TAX PLANNINGPLANNING

NEW TAX ACT NEW TAX ACT PLANNING OPPORTUNITIESPLANNING OPPORTUNITIES

Irrevocable PlanningIrrevocable Planning BUSINESSESBUSINESSES

REAL ESTATEREAL ESTATE

LIFE INSURANCELIFE INSURANCE

FINANCIAL ACCOUNTSFINANCIAL ACCOUNTS

IRREVOCABLE PLANNINGIRREVOCABLE PLANNING

EXCLUDED FROM GROSS ESTATEEXCLUDED FROM GROSS ESTATE

GENERALLY LESS CONTROL OVER ASSETSGENERALLY LESS CONTROL OVER ASSETS

ESTATE TAX PLANNINGESTATE TAX PLANNING

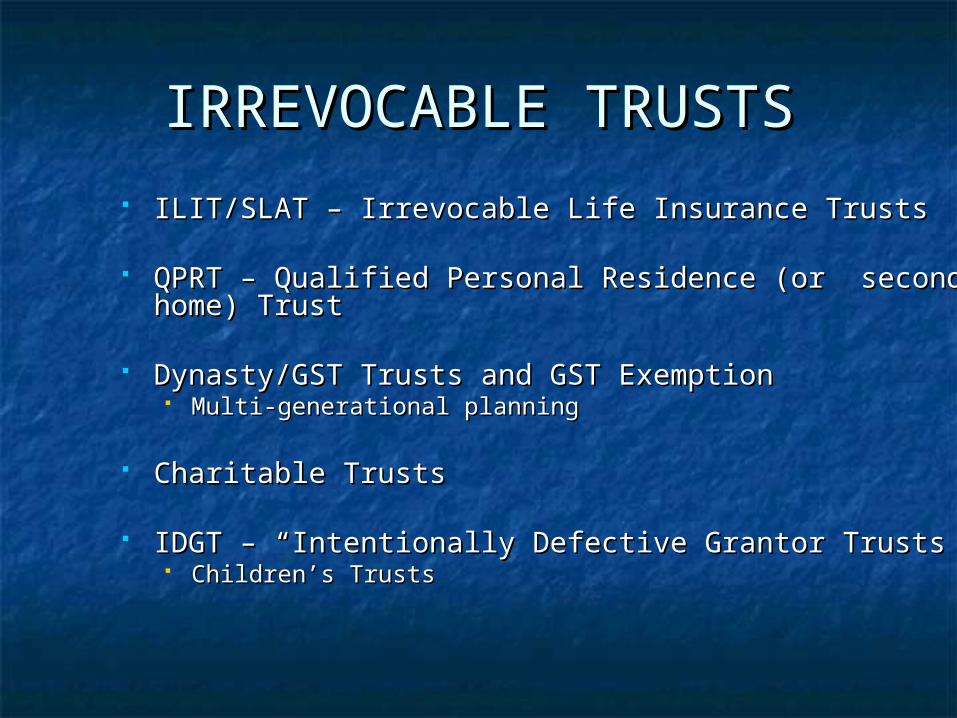

IRREVOCABLE TRUSTSIRREVOCABLE TRUSTS

ILIT/SLAT – Irrevocable Life Insurance TrustsILIT/SLAT – Irrevocable Life Insurance Trusts

QPRT – Qualified Personal Residence (or QPRT – Qualified Personal Residence (or second home) Trustsecond home) Trust

Dynasty/GST Trusts and GST ExemptionDynasty/GST Trusts and GST Exemption Multi-generational planningMulti-generational planning

Charitable TrustsCharitable Trusts

IDGT – “Intentionally Defective Grantor Trusts”IDGT – “Intentionally Defective Grantor Trusts” Children’s TrustsChildren’s Trusts

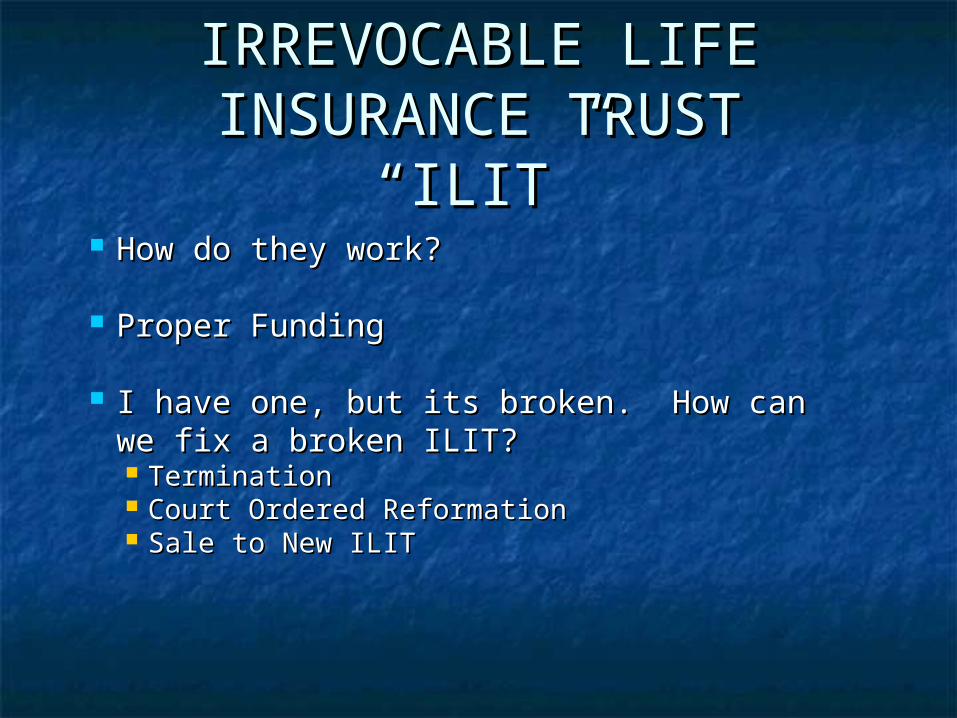

IRREVOCABLE LIFE IRREVOCABLE LIFE INSURANCE TRUSTINSURANCE TRUST

““ILITILIT”” How do they work?How do they work?

Proper FundingProper Funding

I have one, but its broken. How can we fix I have one, but its broken. How can we fix a broken ILIT?a broken ILIT? TerminationTermination Court Ordered ReformationCourt Ordered Reformation Sale to New ILITSale to New ILIT

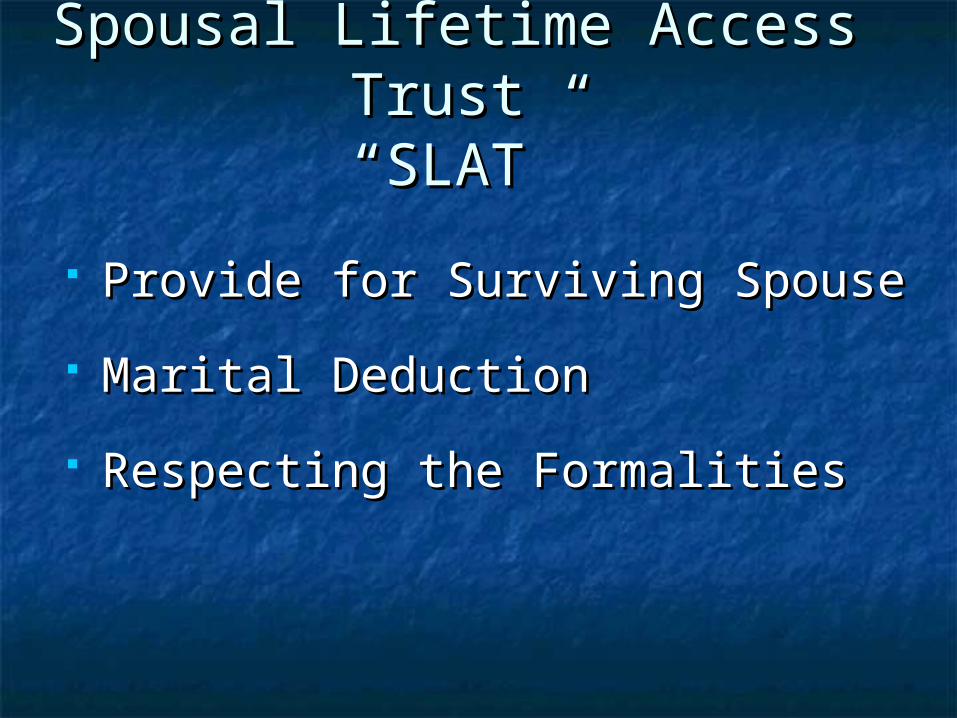

Spousal Lifetime Access Spousal Lifetime Access Trust Trust ““SLATSLAT””

Provide for Surviving SpouseProvide for Surviving Spouse

Marital DeductionMarital Deduction

Respecting the FormalitiesRespecting the Formalities

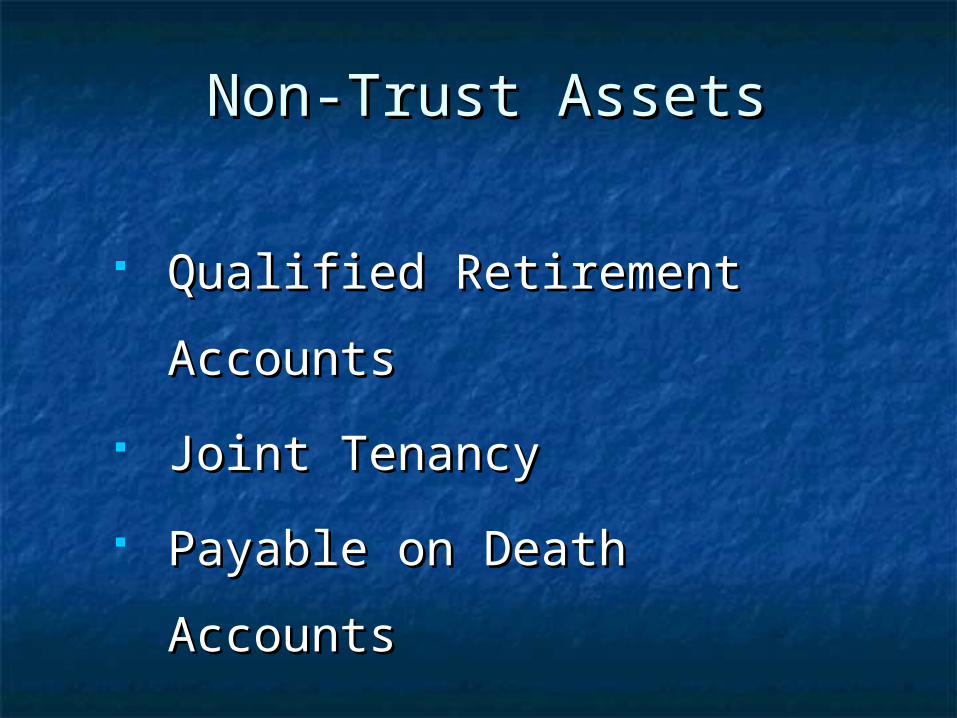

Non-Trust AssetsNon-Trust Assets

Qualified Retirement Qualified Retirement

AccountsAccounts

Joint TenancyJoint Tenancy

Payable on Death AccountsPayable on Death Accounts

Qualified Retirement PlansQualified Retirement Plans

Individual Retirement Individual Retirement

Account (“IRA”)Account (“IRA”)

Spousal RolloverSpousal Rollover

Required Minimum Required Minimum

Distributions & Stretch-Out Distributions & Stretch-Out

OptimizationOptimization

INCOME TAX LAWINCOME TAX LAW

Step-up in tax basis on Step-up in tax basis on ““ownedowned”” assets at deathassets at death ““OwnedOwned”” assets are those that are assets are those that are

includible in a decedentincludible in a decedent’’s gross estate s gross estate for tax purposesfor tax purposes

Joint-TenancyJoint-Tenancy

Death of First Joint TenantDeath of First Joint Tenant

Non-Step Up of Basis for Non-Step Up of Basis for

Surviving OwnerSurviving Owner

Tax ImplicationsTax Implications

Payable on Death Payable on Death AccountsAccounts

Death of First OwnerDeath of First Owner

Step-up of basisStep-up of basis

Tax ImplicationsTax Implications

Trust Trust Administration Administration

101101

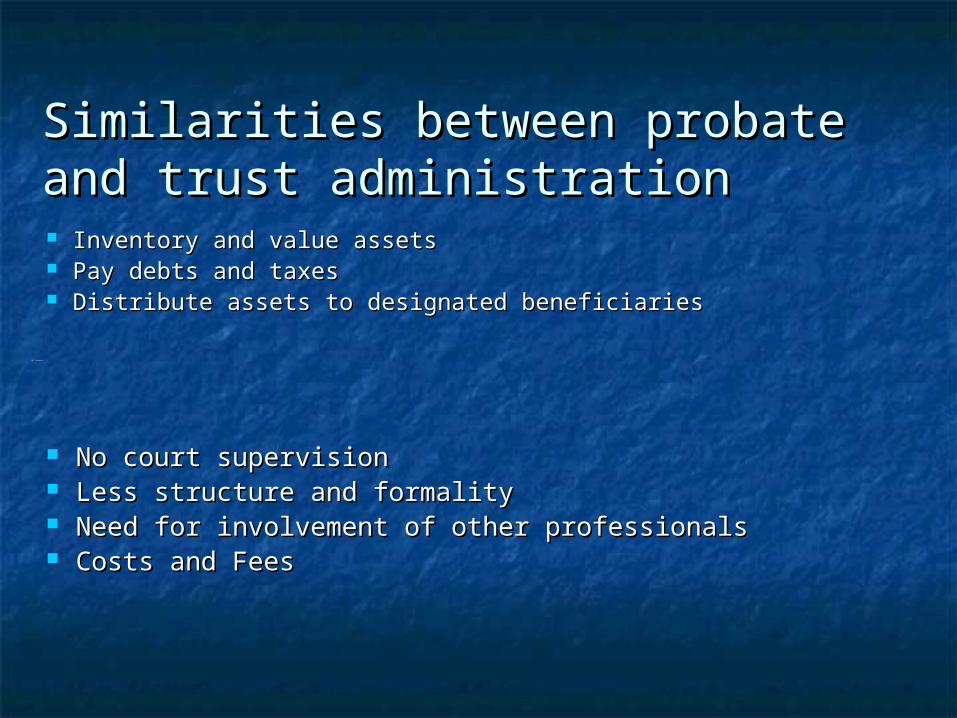

Similarities between probate and Similarities between probate and trust administrationtrust administration Inventory and value assetsInventory and value assets Pay debts and taxesPay debts and taxes Distribute assets to designated beneficiariesDistribute assets to designated beneficiaries

Differences:Differences:

No court supervisionNo court supervision Less structure and formalityLess structure and formality Need for involvement of other professionalsNeed for involvement of other professionals Costs and FeesCosts and Fees

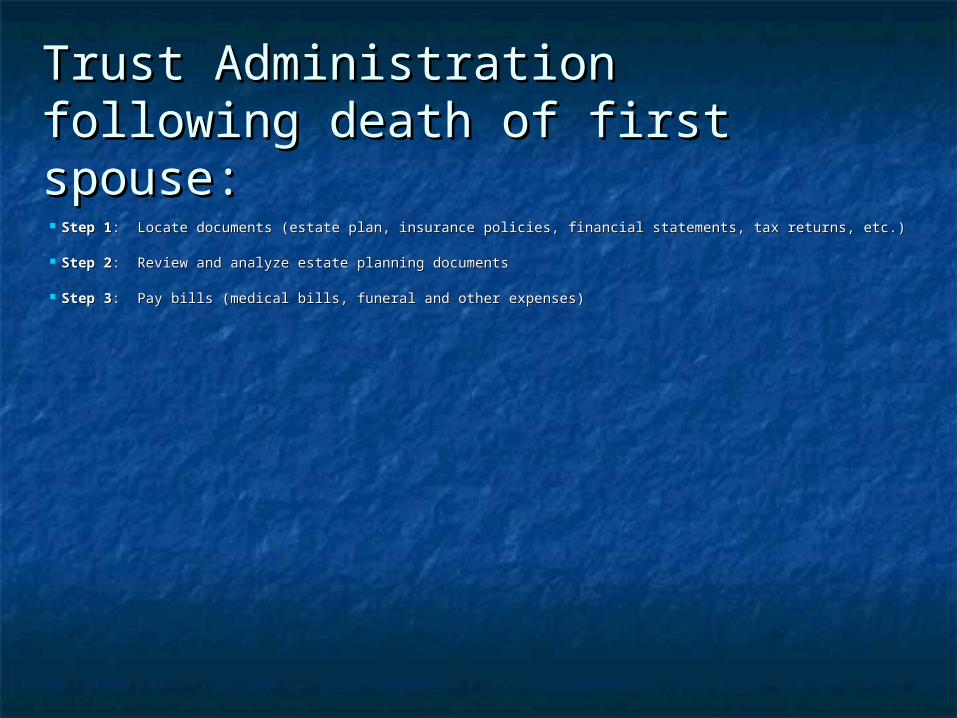

Trust Administration following Trust Administration following death of first spouse:death of first spouse: Step 1Step 1: Locate documents (estate plan, insurance policies, financial statements, tax returns, etc.): Locate documents (estate plan, insurance policies, financial statements, tax returns, etc.)

Step 2Step 2: Review and analyze estate planning documents: Review and analyze estate planning documents

Step 3Step 3: Pay bills (medical bills, funeral and other expenses): Pay bills (medical bills, funeral and other expenses)

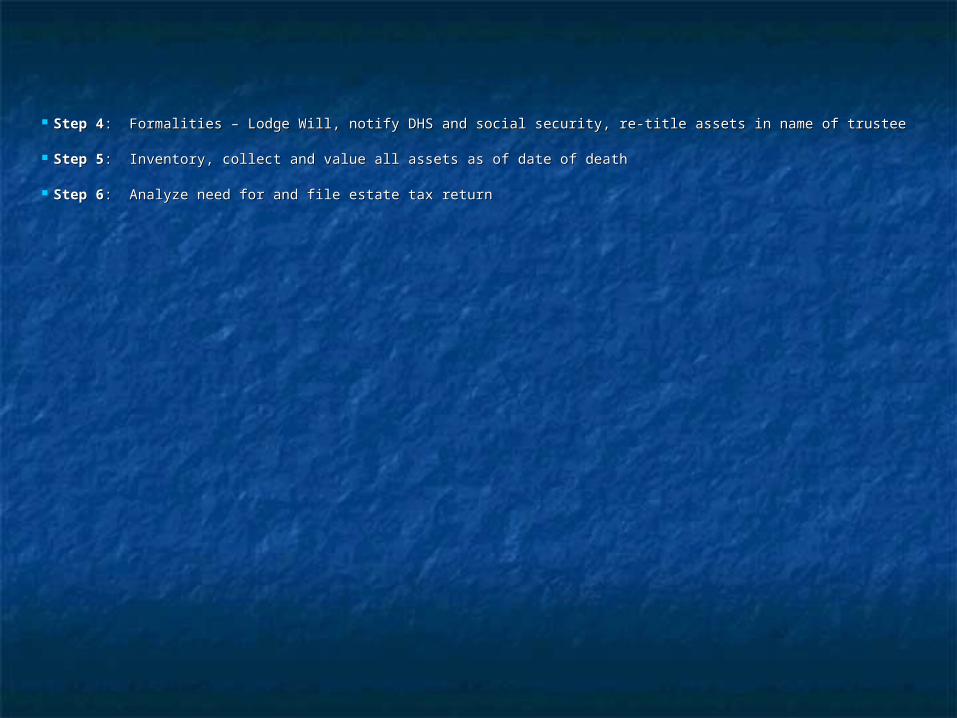

Step 4Step 4: Formalities – Lodge Will, notify DHS and social security, re-title assets in name of trustee: Formalities – Lodge Will, notify DHS and social security, re-title assets in name of trustee

Step 5Step 5: Inventory, collect and value all assets as of date of death: Inventory, collect and value all assets as of date of death

Step 6Step 6: Analyze need for and file estate tax return: Analyze need for and file estate tax return

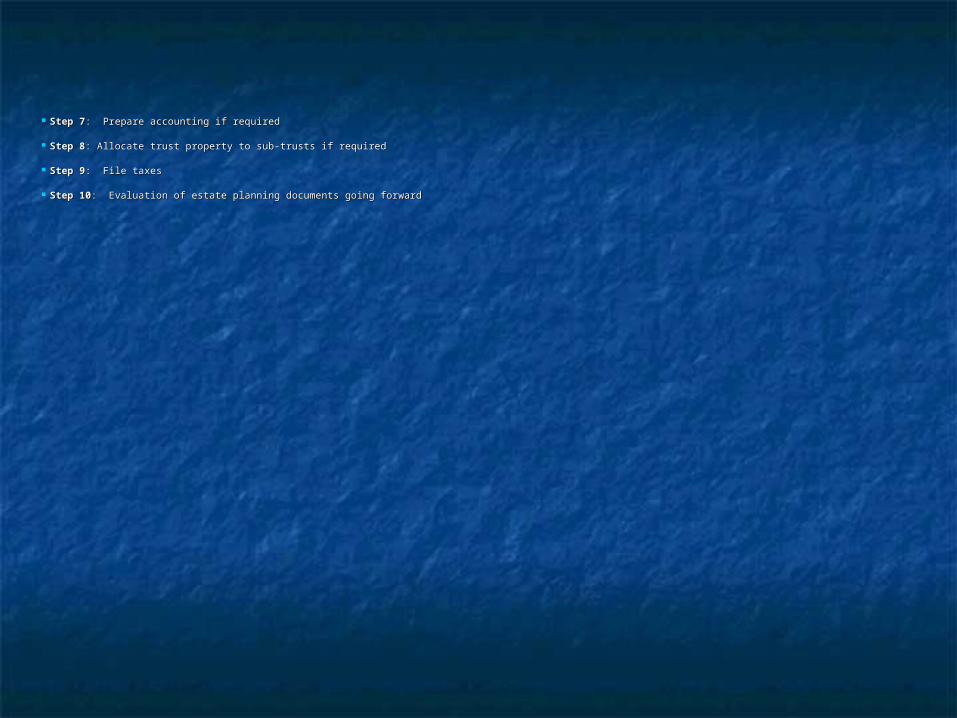

Step 7Step 7: Prepare accounting if required: Prepare accounting if required

Step 8Step 8: Allocate trust property to sub-trusts if required : Allocate trust property to sub-trusts if required

Step 9Step 9: File taxes: File taxes

Step 10Step 10: Evaluation of estate planning documents going forward: Evaluation of estate planning documents going forward

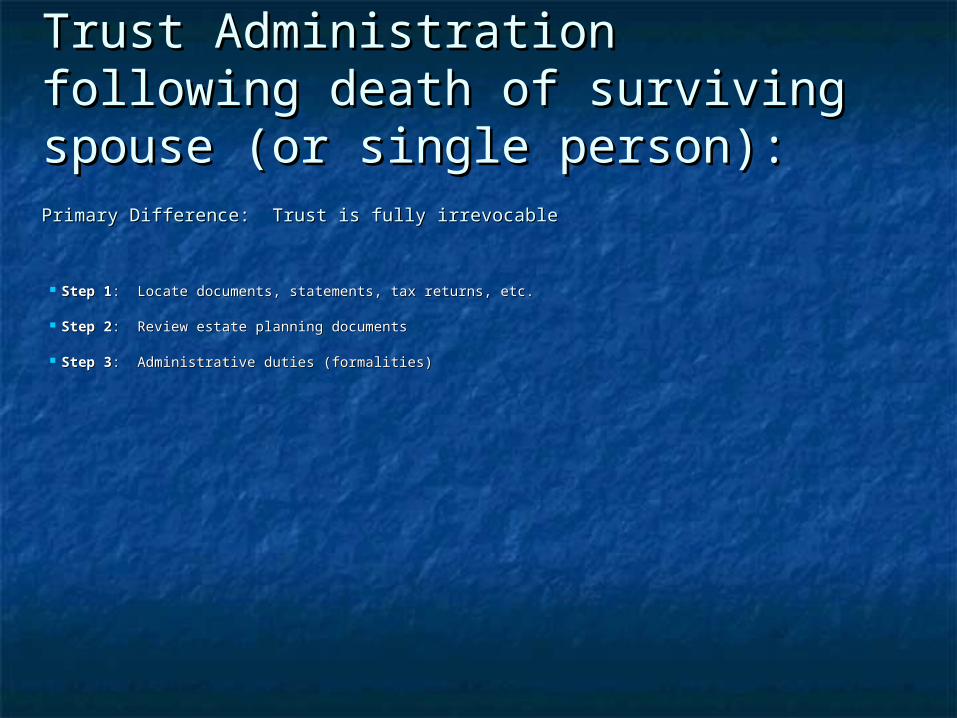

Trust Administration following Trust Administration following death of surviving spouse (or death of surviving spouse (or single person):single person):

Step 1Step 1: Locate documents, statements, tax returns, etc.: Locate documents, statements, tax returns, etc.

Step 2Step 2: Review estate planning documents: Review estate planning documents

Step 3Step 3: Administrative duties (formalities): Administrative duties (formalities)

Primary Difference: Trust is fully irrevocablePrimary Difference: Trust is fully irrevocable

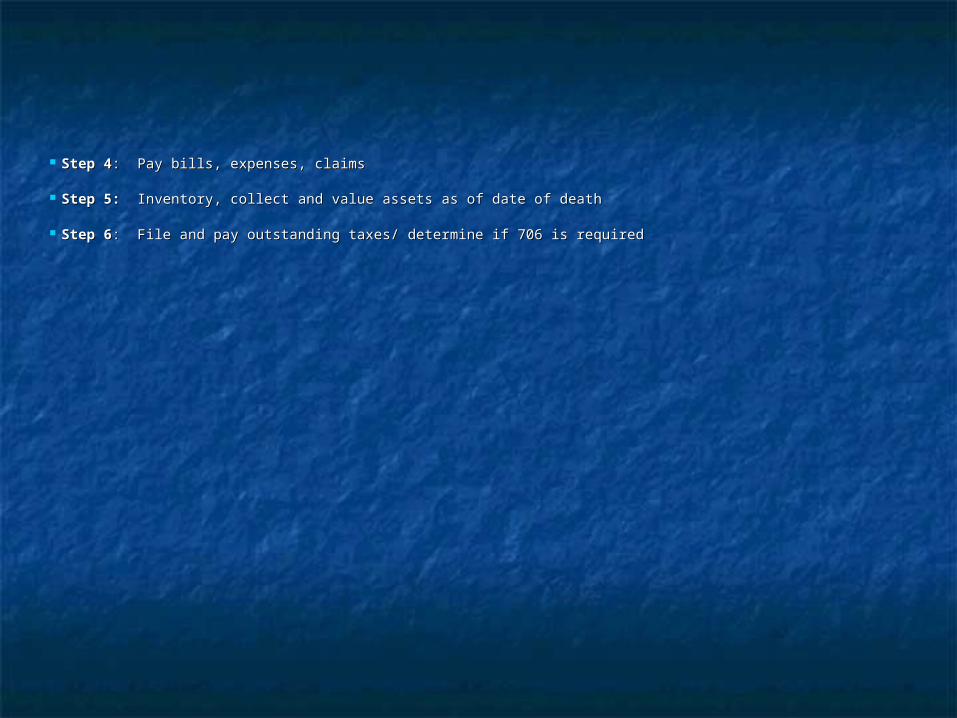

Step 4Step 4: Pay bills, expenses, claims: Pay bills, expenses, claims

Step 5: Step 5: Inventory, collect and value assets as of date of deathInventory, collect and value assets as of date of death

Step 6Step 6: File and pay outstanding taxes/ determine if 706 is required: File and pay outstanding taxes/ determine if 706 is required

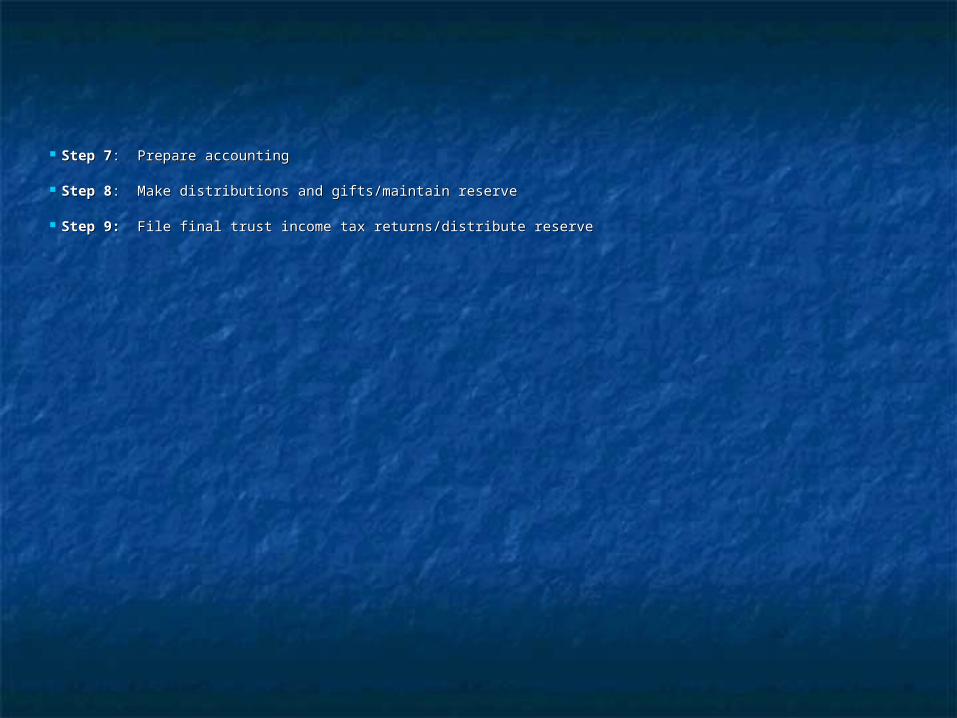

Step 7Step 7: Prepare accounting: Prepare accounting

Step 8Step 8: Make distributions and gifts/maintain reserve: Make distributions and gifts/maintain reserve

Step 9: Step 9: File final trust income tax returns/distribute reserveFile final trust income tax returns/distribute reserve

OUR CLIENTSOUR CLIENTS

Business OwnersBusiness Owners

Real Estate InvestorsReal Estate Investors

High Net Worth IndividualsHigh Net Worth Individuals

Life Insurance PortfoliosLife Insurance Portfolios

ProfessionalsProfessionals

Clients Requiring General Estate PlansClients Requiring General Estate Plans

PRACTICE AREASPRACTICE AREAS BusinessBusiness

Real EstateReal Estate

Wealth Succession and EstateWealth Succession and Estate

TaxTax

EmploymentEmployment

Business, Real Estate, Estate and Business, Real Estate, Estate and

Commercial LitigationCommercial Litigation