Embed Size (px)

Citation preview

Special Committees

Dealing with the Difficult Situations

Al Hudec Blair Horn

Farris, Vaughan, Wills & Murphy LLP Fasken Martineau LLP

Mergers and Acquisitions 2011

The Continuing Legal Education Society of British Columbia

June 16, 2011

Dealing with the Difficult Situations

1. Transactions with a majority shareholder

2. Defending against a corporate raider

3. Dealing with conflicted advisors

4. Management buy-outs

Important New Cases

1. Magna International and The Stronach Trust – OSC Reasons for Decision published Jan 31, 2011 (and related decisions of the Superior Court and Divisional Court (Ontario))

2. Icahn Partners and Lions Gate Entertainment – BC Supreme Court, Nov 1, 2010

3. Del Monte Foods Shareholder Litigation – Delaware Chancery Court, Feb 14, 2011

4. J Crew Management Buy-Out Litigation Settlement –Jan 18, 2011

Transactions with a Majority Shareholder:

Magna: Background

• Shareholder approved, dual-class share structure with multiple voting shares and no “coat-tail” protection for subordinate voting shares

• Stronach Trust controlled Magna (66% of voting rights) with less than 1% of the equity

• Magna Class A shares traded at a discount to industry peers for many years

• Management proposed collapse of Magna’s dual class share structure in exchange for combination of consideration valued at approximately $860M

• Implied premium of 1800% on the value of the Class A Shares

Magna: Background (cont’d)

• Subordinate voting shareholders would experience substantial

dilution, but reduction or elimination of Magna’s trading

discount would mean shareholders would benefit from an

increase in the value of the Class A Shares

• Magna board established a special committee of independent

directors to review the proposal

• Proposal structured as plan of arrangement requiring approval

of “minority” Class A shareholders voting as a separate class

(exempt from MI 61-101 because value less than 25% of

market cap)

Magna: Background (cont’d)

• Financial advisor to the committee was not able to provide a

fairness opinion

• Special Committee was unable to recommend in favour or

against the proposal so the full board decided to put the deal

to the shareholders with no recommendation

• Proposal was announced on May 6, 2010, prior to Magna’s

AGM and the same day that Magna announced that its Q1

earnings for that year had exceeded targets

• Closing price of Magna’s Class A Shares on May 6

substantially higher than closing price of the Class A Shares

on May 5

Magna: Shareholder Challenge

• Proposal challenged by institutional shareholders and

proceedings brought before the OSC to cease-trade the

Proposal

• OSC found the transaction not abusive, but ordered Magna to

provide shareholders with enhanced disclosure given the

absence of both a fairness opinion and a recommendation

from the Special Committee or the Board

• At the special shareholders’ meeting, Magna’s Class A

Shareholders approved the arrangement by a three-to-one

margin

Magna: Shareholder Challenge (cont’d)

• At the contested fairness hearing on the arrangement, the

Ontario Superior Court of Justice approved the plan of

arrangement

Court found that arrangement resolved conflicting rights of Class

A and Class B shareholders in a “fair and balanced” way

Court need not make an objective determination or precise

calculation of its own regarding the financial costs and benefits

of a plan of arrangement

• While certain traditional indicia of fairness were not present,

the Court relied on shareholder vote, market reaction and

market liquidity

Magna: Shareholder Challenge (cont’d)

• On appeal, the Ontario Divisional Court unanimously upheld

the Superior Court decision

• Approval of arrangement is fact-specific

Class A shareholders given opportunity to acquire control

Class A shareholders had veto

Value of bargain, and underlying rationale, would fall to be

determined in the future by market forces

“Unprecedented” level of disclosure to shareholders

Sophistication of majority of Class A shareholders, 80% of which

were large institutional investors

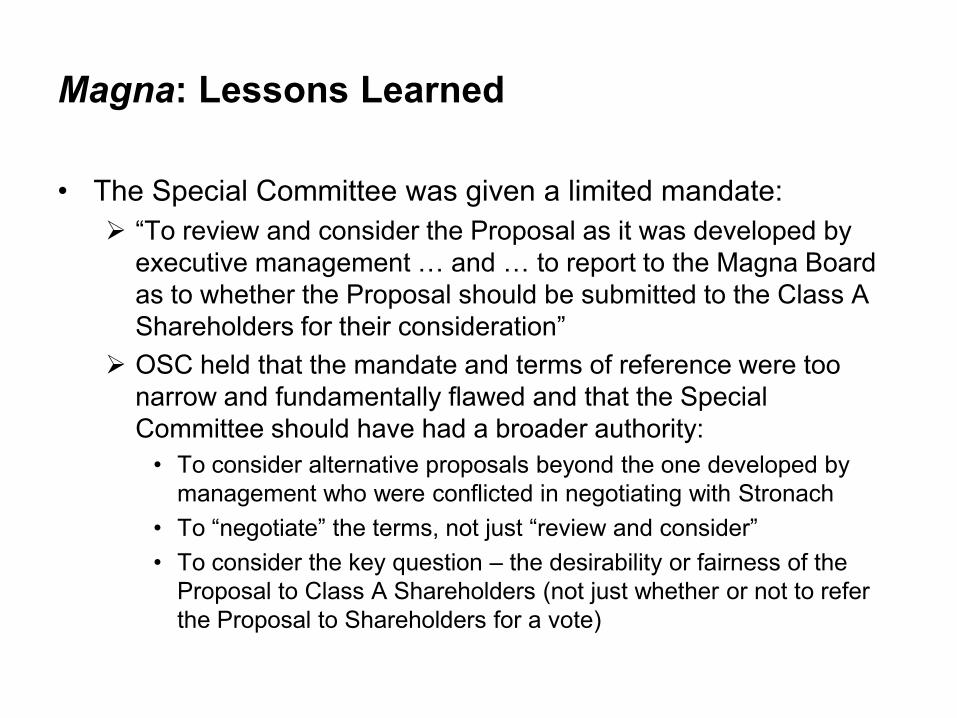

Magna: Lessons Learned

• The Special Committee was given a limited mandate:

“To review and consider the Proposal as it was developed by

executive management … and … to report to the Magna Board

as to whether the Proposal should be submitted to the Class A

Shareholders for their consideration”

OSC held that the mandate and terms of reference were too

narrow and fundamentally flawed and that the Special

Committee should have had a broader authority:

• To consider alternative proposals beyond the one developed by

management who were conflicted in negotiating with Stronach

• To “negotiate” the terms, not just “review and consider”

• To consider the key question – the desirability or fairness of the

Proposal to Class A Shareholders (not just whether or not to refer

the Proposal to Shareholders for a vote)

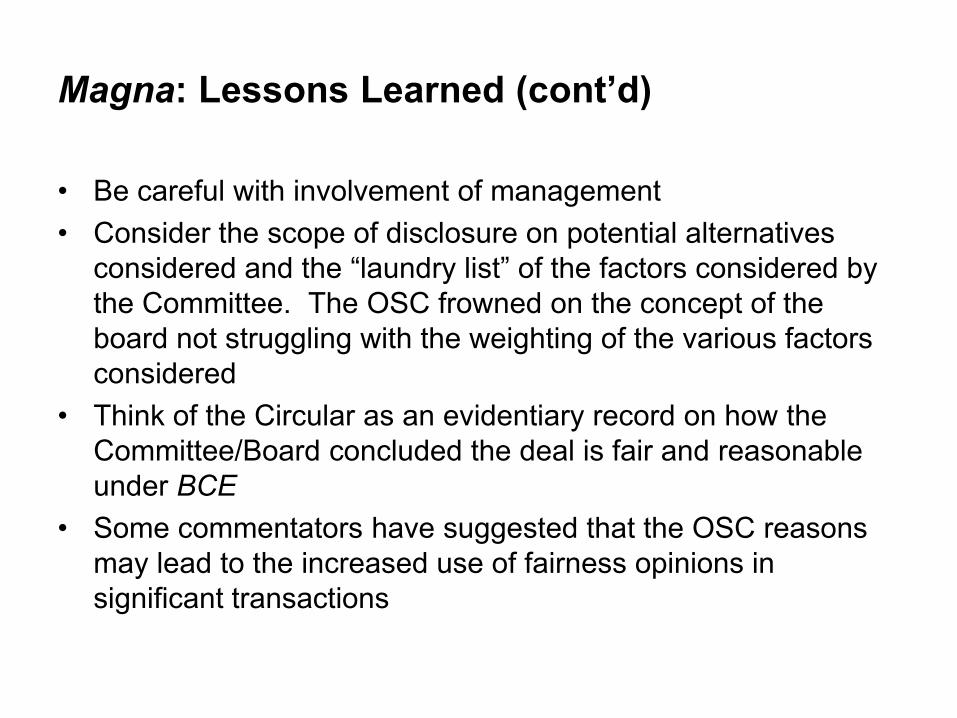

Magna: Lessons Learned (cont’d)

• Be careful with involvement of management

• Consider the scope of disclosure on potential alternatives

considered and the “laundry list” of the factors considered by

the Committee. The OSC frowned on the concept of the

board not struggling with the weighting of the various factors

considered

• Think of the Circular as an evidentiary record on how the

Committee/Board concluded the deal is fair and reasonable

under BCE

• Some commentators have suggested that the OSC reasons

may lead to the increased use of fairness opinions in

significant transactions

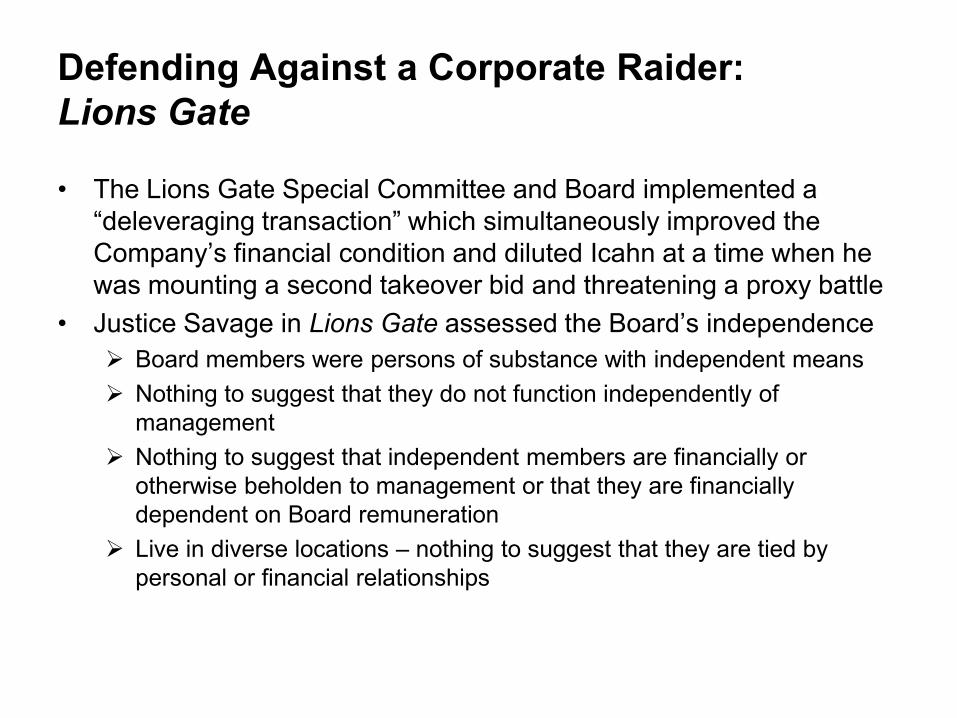

Defending Against a Corporate Raider:

Lions Gate

• The Lions Gate Special Committee and Board implemented a

“deleveraging transaction” which simultaneously improved the

Company’s financial condition and diluted Icahn at a time when he

was mounting a second takeover bid and threatening a proxy battle

• Justice Savage in Lions Gate assessed the Board’s independence

Board members were persons of substance with independent means

Nothing to suggest that they do not function independently of

management

Nothing to suggest that independent members are financially or

otherwise beholden to management or that they are financially

dependent on Board remuneration

Live in diverse locations – nothing to suggest that they are tied by

personal or financial relationships

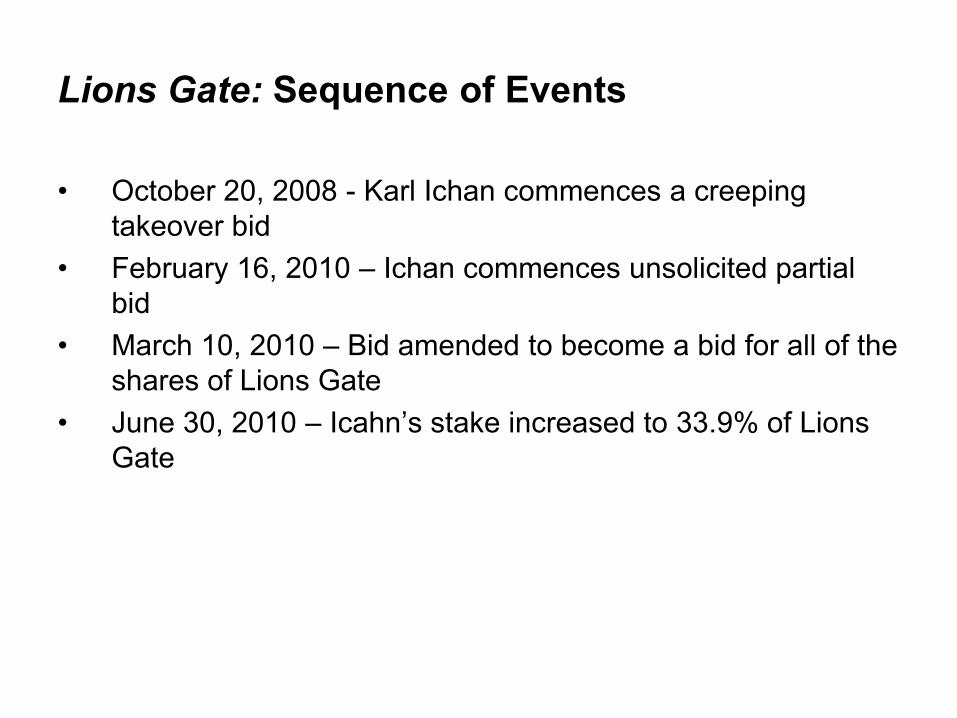

Lions Gate: Sequence of Events

• October 20, 2008 - Karl Ichan commences a creeping

takeover bid

• February 16, 2010 – Ichan commences unsolicited partial

bid

• March 10, 2010 – Bid amended to become a bid for all of the

shares of Lions Gate

• June 30, 2010 – Icahn’s stake increased to 33.9% of Lions

Gate

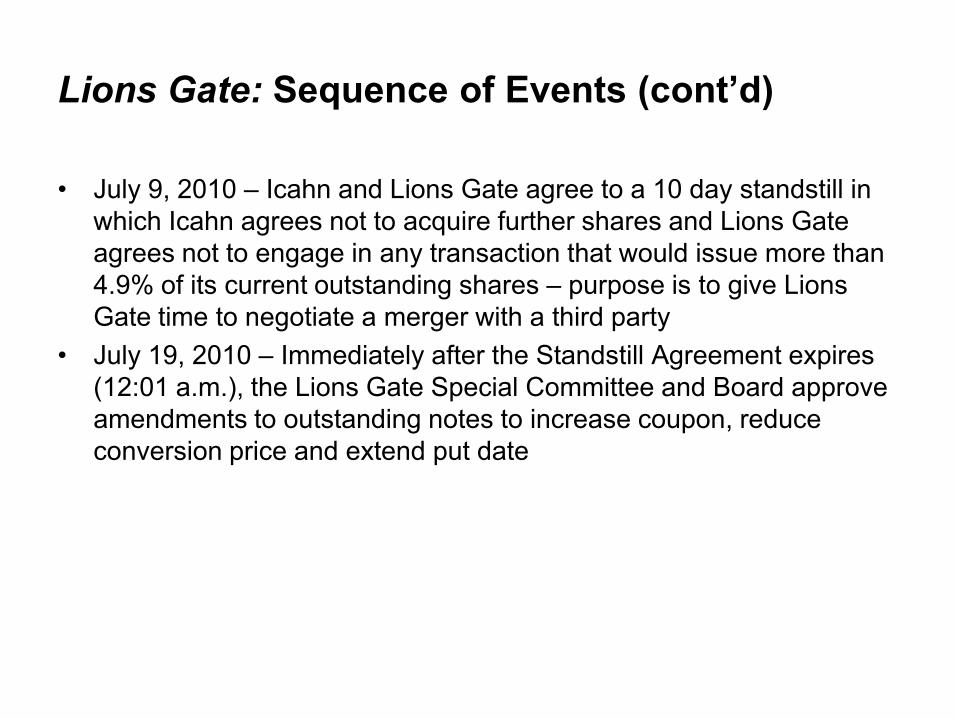

Lions Gate: Sequence of Events (cont’d)

• July 9, 2010 – Icahn and Lions Gate agree to a 10 day standstill in

which Icahn agrees not to acquire further shares and Lions Gate

agrees not to engage in any transaction that would issue more than

4.9% of its current outstanding shares – purpose is to give Lions

Gate time to negotiate a merger with a third party

• July 19, 2010 – Immediately after the Standstill Agreement expires

(12:01 a.m.), the Lions Gate Special Committee and Board approve

amendments to outstanding notes to increase coupon, reduce

conversion price and extend put date

Lions Gate: Legal Analysis

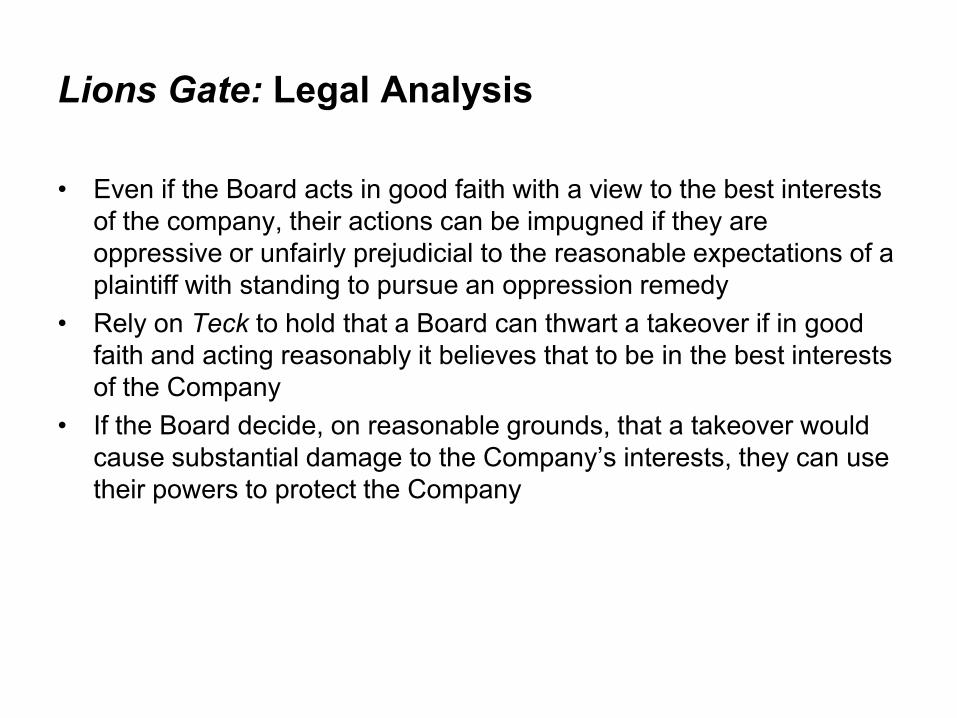

• Even if the Board acts in good faith with a view to the best interests

of the company, their actions can be impugned if they are

oppressive or unfairly prejudicial to the reasonable expectations of a

plaintiff with standing to pursue an oppression remedy

• Rely on Teck to hold that a Board can thwart a takeover if in good

faith and acting reasonably it believes that to be in the best interests

of the Company

• If the Board decide, on reasonable grounds, that a takeover would

cause substantial damage to the Company’s interests, they can use

their powers to protect the Company

Lions Gate: Oppression Analysis

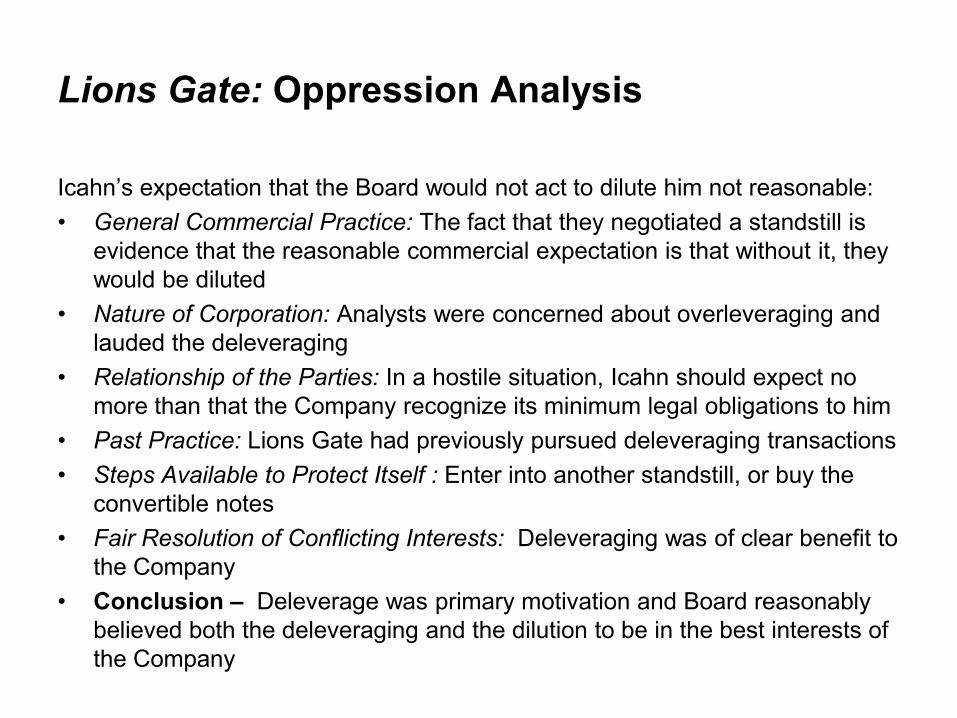

Icahn’s expectation that the Board would not act to dilute him not reasonable:

• General Commercial Practice: The fact that they negotiated a standstill is

evidence that the reasonable commercial expectation is that without it, they

would be diluted

• Nature of Corporation: Analysts were concerned about overleveraging and

lauded the deleveraging

• Relationship of the Parties: In a hostile situation, Icahn should expect no

more than that the Company recognize its minimum legal obligations to him

• Past Practice: Lions Gate had previously pursued deleveraging transactions

• Steps Available to Protect Itself : Enter into another standstill, or buy the

convertible notes

• Fair Resolution of Conflicting Interests: Deleveraging was of clear benefit to

the Company

• Conclusion – Deleverage was primary motivation and Board reasonably

believed both the deleveraging and the dilution to be in the best interests of

the Company

Dealing with Conflicted Advisors: Del Monte

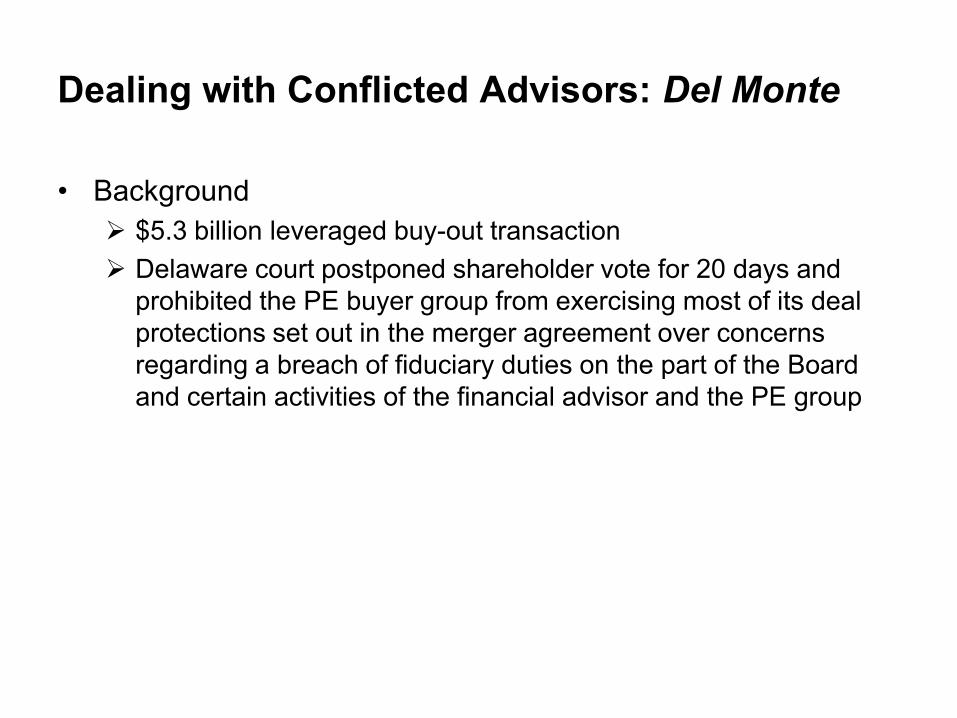

• Background

$5.3 billion leveraged buy-out transaction

Delaware court postponed shareholder vote for 20 days and

prohibited the PE buyer group from exercising most of its deal

protections set out in the merger agreement over concerns

regarding a breach of fiduciary duties on the part of the Board

and certain activities of the financial advisor and the PE group

Del Monte: Activities of the Financial Advisor

• Barclays orchestrated buy-side activities that put Del Monte

in play before they were retained by Del Monte and

continued after they were told by the Special Committee to

shut down the process

• Barclays hid the fact that they steered KKR and Vestar into a

“club deal” notwithstanding that such a deal was prohibited

by a “no teaming” clause in Del Monte’s confidentiality

agreements

• Pursued a buy-side financing mandate from the outset and

continued to negotiate the purchase price on behalf of Del

Monte even after they were representing the buyers with

respect to financing

Del Monte: The Board’s mistakes

• Allowed Vestar, the highest bidder in a previous effort to sell the company,

to team with KKR – the Special Committee did not seem to have

considered whether it would have been better to team Vestar with another

potential purchaser to induce some competitive tension in the process or

whether it could extract a price increase for waiver of the “no teaming”

covenant

• Permitting Barclays to provide buy-side financing to KKR – No evidence

that Barclay’s participation in the financing was necessary to get the deal

done or to maximize price; in fact the Special Committee had to spend

another $3 million to hire another independent fairness advisor

• No meaningful Board consideration or informed decision making;

unreasonable to sign off on conflicts without some reasonable justification

relating to shareholder interests

• Tainted “go shop” process since Barclays had the incentive to maintain

the existing deal

Del Monte: Practice points

• Special Committees must be careful to explore all possible

conflicts when retaining a financial advisor

• ABA has prepared draft language for financial advisor

engagement letters for representations and warranties,

covenants and indemnities dealing with past and future

relationships of the financial advisor that could create conflicts

• Boards should be careful about waiving “teaming” provisions

unless there appears to be a benefit to doing so (competition

among buyers is presumed to lead to a higher price)

• Consider financial advisor conflicts on buy-side financing

requirements

Management Buy-Outs: J Crew

• US $3 billion Buy-out of J Crew by TPG Capital and Leonard Green Partners

• Proxy circular published Dec, 2010 revealed a flawed process

• CEO, Millard Drexler discussed the sale with TPG for 7 weeks before informing the Board of discussions

• Special Committee never did take control of the process

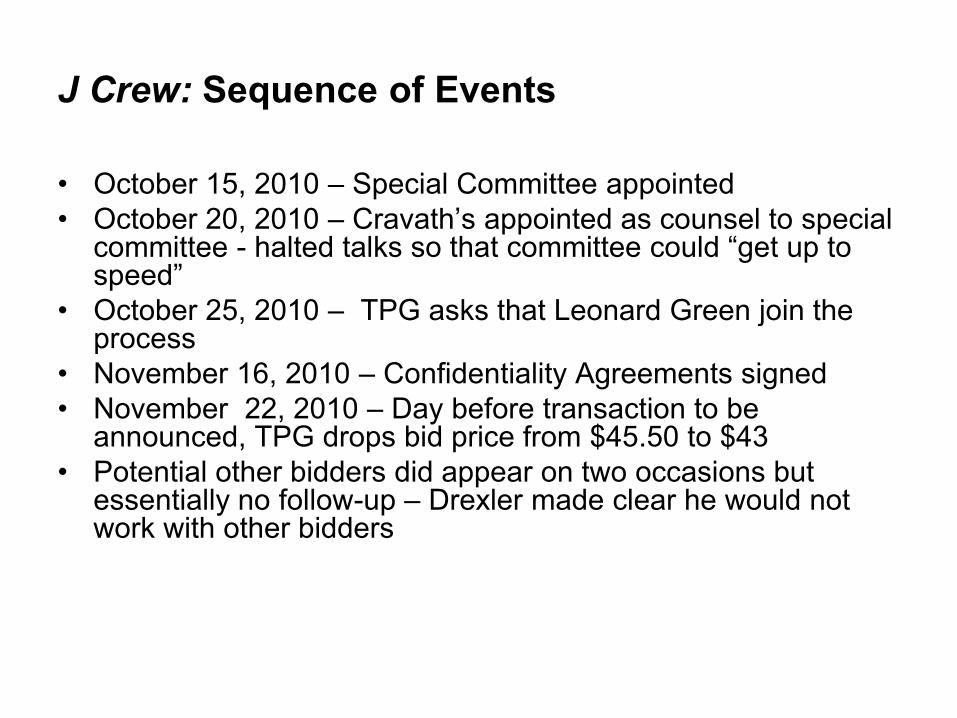

J Crew: Sequence of Events

• October 15, 2010 – Special Committee appointed

• October 20, 2010 – Cravath’s appointed as counsel to special committee - halted talks so that committee could “get up to speed”

• October 25, 2010 – TPG asks that Leonard Green join the process

• November 16, 2010 – Confidentiality Agreements signed

• November 22, 2010 – Day before transaction to be announced, TPG drops bid price from $45.50 to $43

• Potential other bidders did appear on two occasions but essentially no follow-up – Drexler made clear he would not work with other bidders

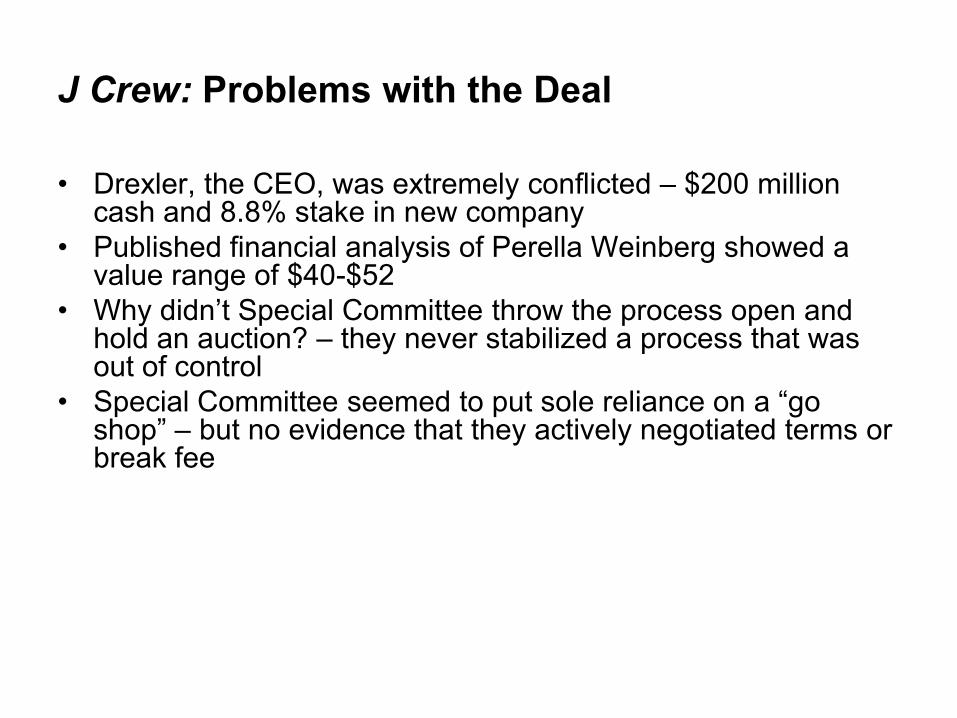

J Crew: Problems with the Deal

• Drexler, the CEO, was extremely conflicted – $200 million cash and 8.8% stake in new company

• Published financial analysis of Perella Weinberg showed a value range of $40-$52

• Why didn’t Special Committee throw the process open and hold an auction? – they never stabilized a process that was out of control

• Special Committee seemed to put sole reliance on a “go shop” – but no evidence that they actively negotiated terms or break fee

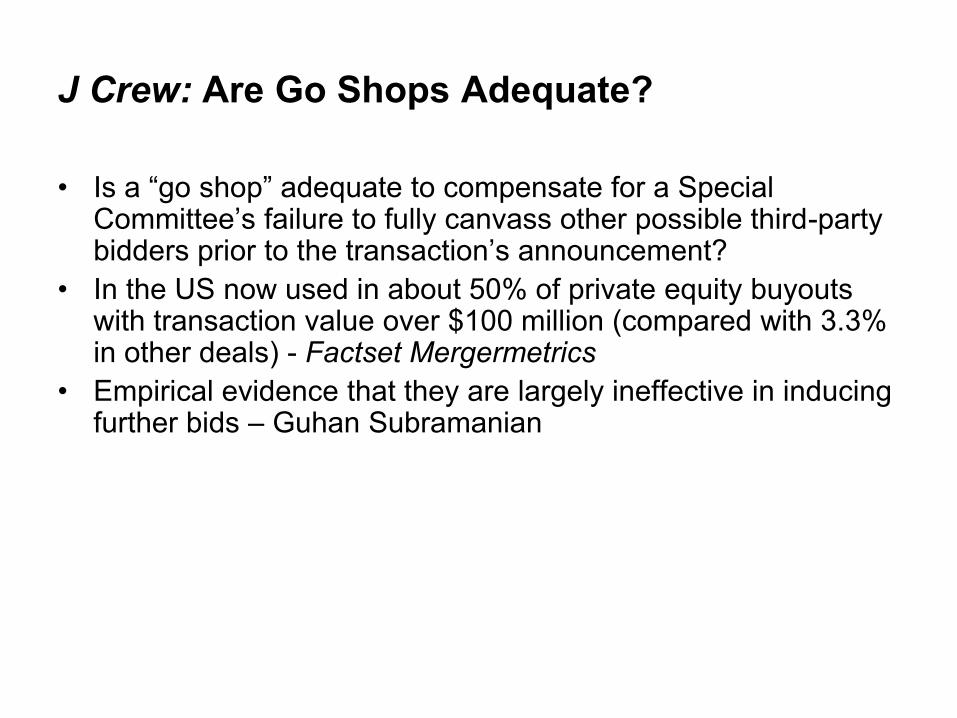

J Crew: Are Go Shops Adequate?

• Is a “go shop” adequate to compensate for a Special Committee’s failure to fully canvass other possible third-party bidders prior to the transaction’s announcement?

• In the US now used in about 50% of private equity buyouts with transaction value over $100 million (compared with 3.3% in other deals) - Factset Mergermetrics

• Empirical evidence that they are largely ineffective in inducing further bids – Guhan Subramanian

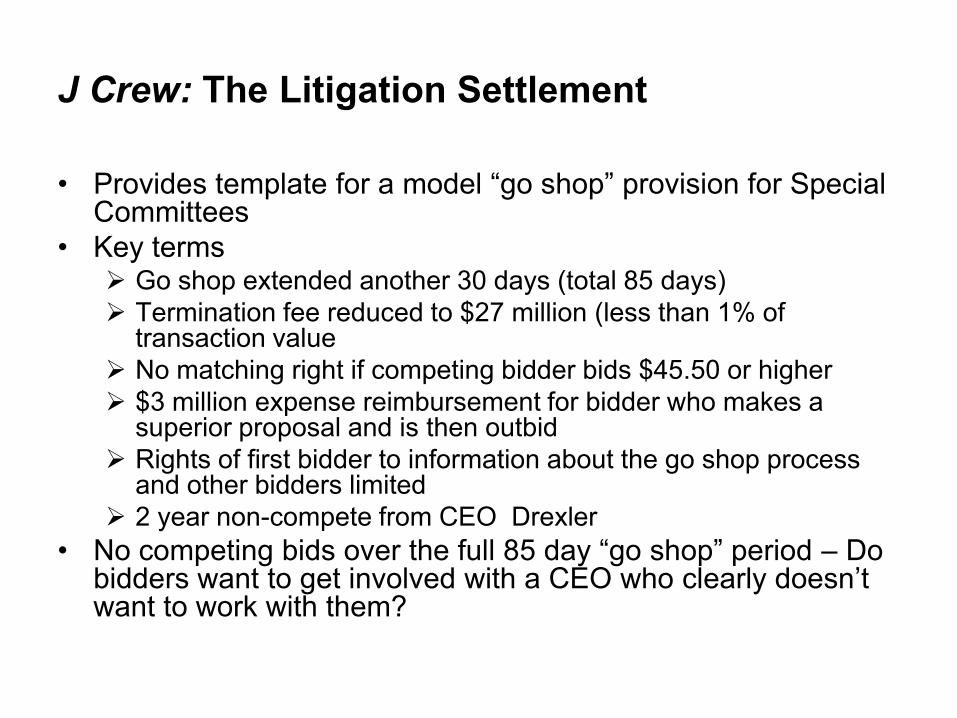

J Crew: The Litigation Settlement

• Provides template for a model “go shop” provision for Special Committees

• Key terms Go shop extended another 30 days (total 85 days)

Termination fee reduced to $27 million (less than 1% of transaction value

No matching right if competing bidder bids $45.50 or higher

$3 million expense reimbursement for bidder who makes a superior proposal and is then outbid

Rights of first bidder to information about the go shop process and other bidders limited

2 year non-compete from CEO Drexler

• No competing bids over the full 85 day “go shop” period – Do bidders want to get involved with a CEO who clearly doesn’t want to work with them?

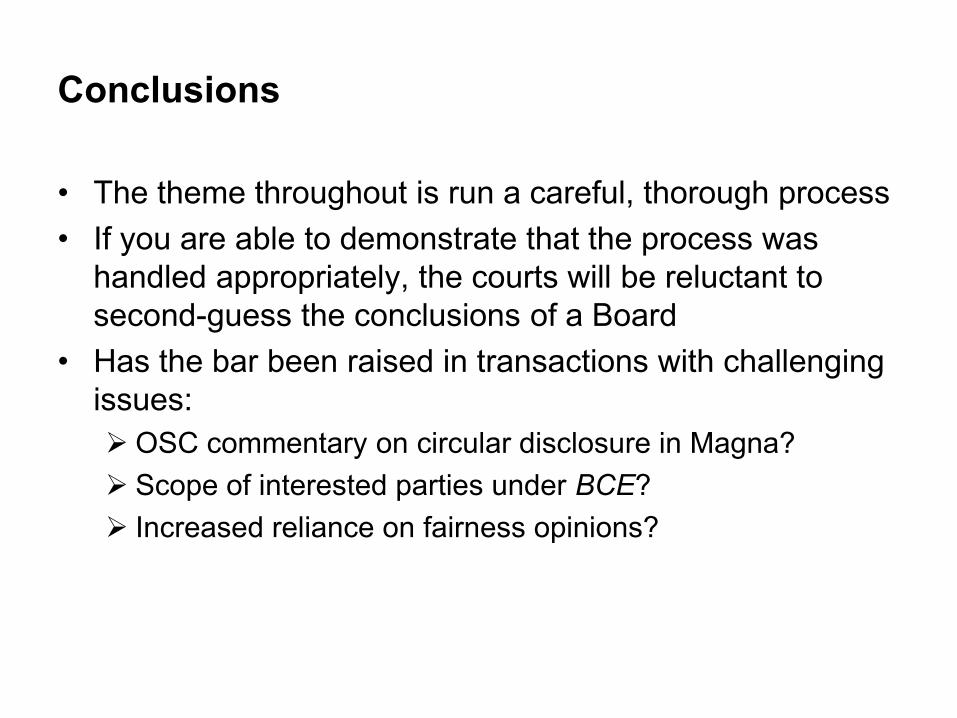

Conclusions

• The theme throughout is run a careful, thorough process

• If you are able to demonstrate that the process was

handled appropriately, the courts will be reluctant to

second-guess the conclusions of a Board

• Has the bar been raised in transactions with challenging

issues:

OSC commentary on circular disclosure in Magna?

Scope of interested parties under BCE?

Increased reliance on fairness opinions?

Special Committees

Dealing with the Difficult Situations

Al Hudec Blair HornFarris, Vaughan, Wills & Murphy LLP Fasken Martineau LLP(604) 661-9356 (604) 631-3172

[email protected] [email protected]

Mergers and Acquisitions 2011

The Continuing Legal Education Society of British Columbia

June 16, 2011