Embed Size (px)

Citation preview

Southern Company’s Investigation of BioPower

Southern CompanySouthern Company’’s s Investigation of Investigation of BioPowerBioPower

BioPro Conference

March, 2011

BioPro Conference

March, 2011

CC

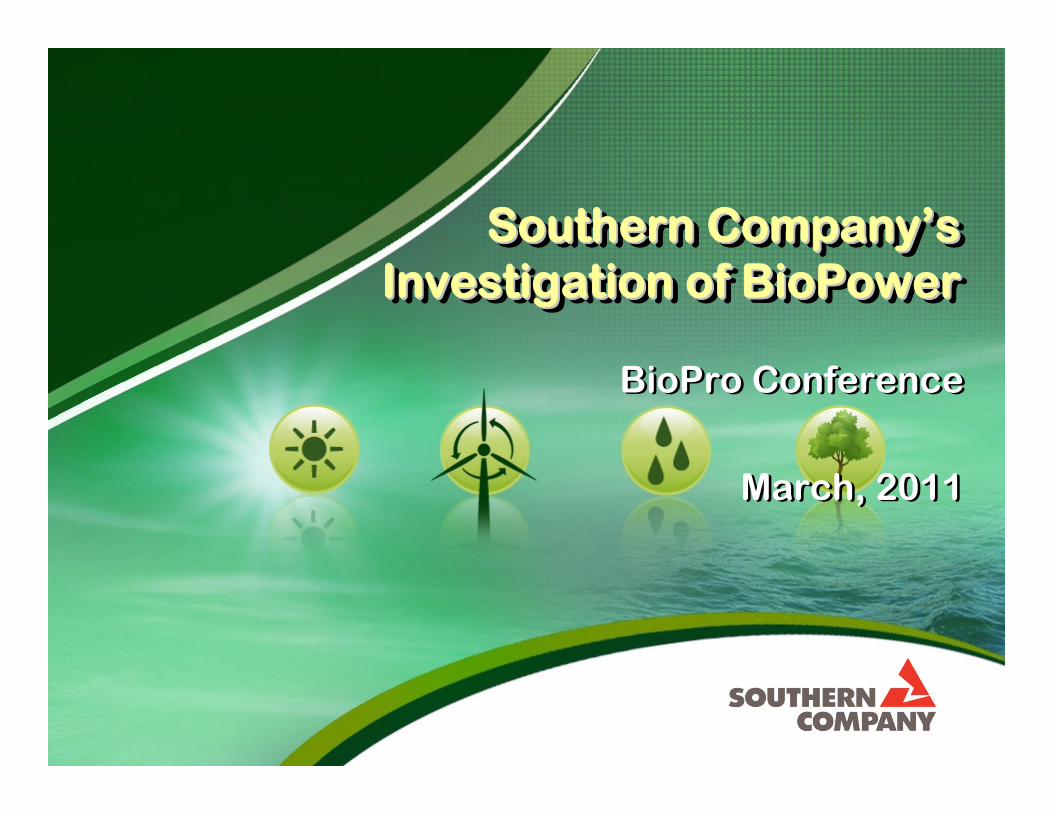

OPCO Plant Type

GPC

APC

GULF

MPC

SPC

H Weiss Dam

Total 42, 514 MW Total 42, 514 MW

Southern Company GenerationSouthern Company Generation

N

S

Combined Cycle (8,359 MW)

H

CT

PA

Nuclear (3,759 MW)

Steam (21,587 MW)

Combustion Turbine (3,992 MW)

Hydro (2,815 MW)

Power Purchase Agreements (2,002 MW)

HLay Dam

HMitchell Dam

H Martin DamH Yates Dam

H Thurlow Dam

HSinclair Dam

H Logan Martin Dam

HHolt Dam

HNeely Henry Dam

HHolt Dam

HJordan Dam

HBankhead Dam

HBouldin Dam

H Riverview Dam

H Smith Dam

H Harris Dam

HRocky Mountain

HMorgan Falls Dam

H Langdale DamH Bartletts Ferry Dam

H Goat Rock Dam

H Oliver Dam

H North Highlands Dam

H Flint River Dam

H Lloyd Shoals Dam

SPlant McManus

H Wallace Dam

H Barnett Shoals Dam

H Estatoah DamH Burton Dam

H Terrora Dam

H Yonah Dam

HNacoochee Dam

HTugalo Dam

HTallulah DamSPlant Gorgas

N Plant Vogtle

S Plant Miller

SPlant Greene County

S Plant Gadsden

SPlant Bowen

SPlant Gaston

SPlant Barry

SPlant Scholz

S Plant Mitchell

SPlant Wansley

S Plant YatesS Plant McDonough

SPlant Scherer

S Plant Hammond

SPlant McIntosh

SPlant Kraft

SPlant Smith

SPlant Watson

SPlant Daniel

SPlant Sweatt

S Plant Eaton

S Plant Crist

N Plant FarleyN Plant Hatch

S Plant Branch

CCStanton Generating Facility

CC Washington County

CC

CC CC Plant Theodore

CC

CCPlant HarrisCCPlant Franklin

CC

CC

CTDeSoto County Energy Complex

CT Chevron Cogen

CT

CT

CTPlant Wilson

CT Plant Dahlberg

CT Plant RobinsCT

CTPlant Oleander

PA Murray

PA Calhoun

PA Mid-GA Cogen

PA West Georgia

CCRowan County Energy ComplexCT

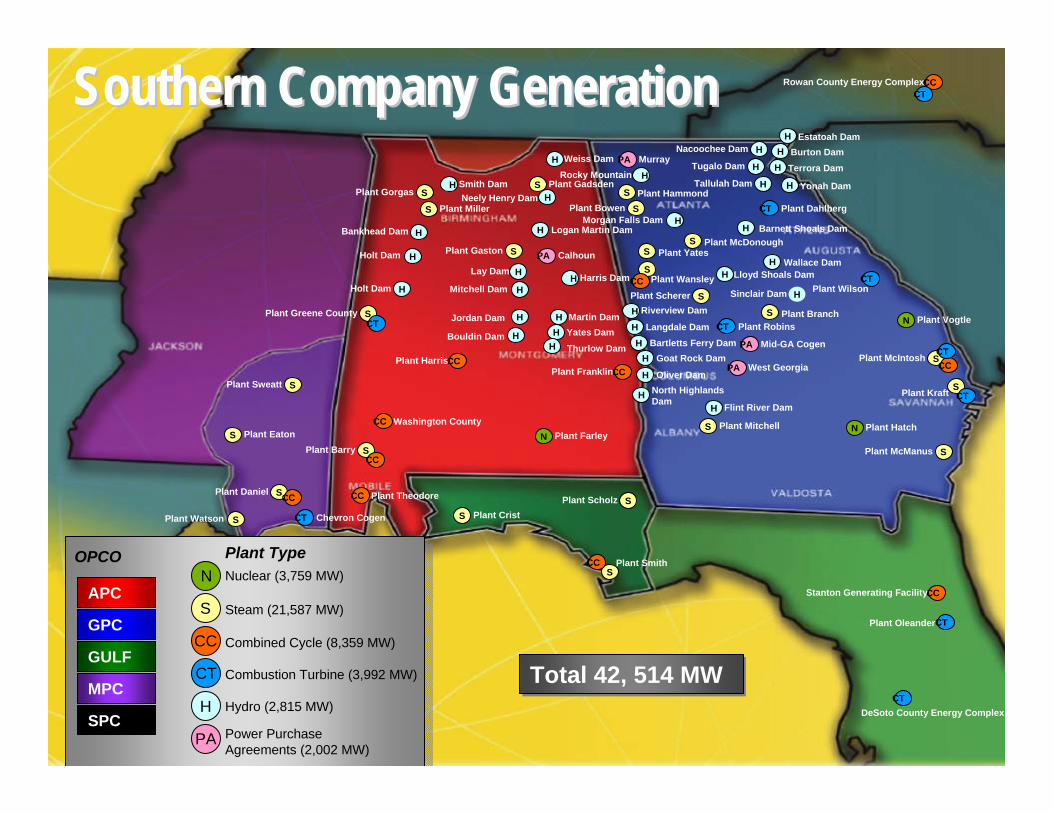

RPS Policies

Renewable portfolio standard

Renewable portfolio goal

www.dsireusa.org / November 2010

Solar water heating eligible *† Extra credit for solar or customer-sited renewables

Includes non-renewable alternative resources

WA: 15% x 2020*

CA: 33% x 2020

NV: 25% x 2025*

AZ: 15% x 2025

NM: 20% x 2020 (IOUs)10% x 2020 (co-ops)

HI: 40% x 2030

Minimum solar or customer-sited requirement

TX: 5,880 MW x 2015

UT: 20% by 2025*

CO: 30% by 2020 (IOUs)10% by 2020 (co-ops & large munis)*

MT: 15% x 2015

ND: 10% x 2015

SD: 10% x 2015

IA: 105 MW

MN: 25% x 2025(Xcel: 30% x 2020)

MO: 15% x 2021

WI: Varies by utility; 10% x 2015 statewide

MI: 10% + 1,100 MW x 2015*

OH: 25% x 2025†

ME: 30% x 2000New RE: 10% x 2017

NH: 23.8% x 2025

MA: 22.1% x 2020 New RE: 15% x 2020

(+1% annually thereafter)

RI: 16% x 2020

CT: 23% x 2020

NY: 29% x 2015

NJ: 22.5% x 2021

PA: ~18% x 2021†

MD: 20% x 2022

DE: 25% x 2026*

DC: 20% x 2020

VA: 15% x 2025*

NC: 12.5% x 2021 (IOUs)10% x 2018 (co-ops & munis)

VT: (1) RE meets any increase in retail sales x 2012;

(2) 20% RE & CHP x 2017

KS: 20% x 2020

OR: 25% x 2025 (large utilities)*5% - 10% x 2025 (smaller utilities)

IL: 25% x 2025 WV: 25% x 2025*†

29 states + DC and PR have

an RPS(7 states have goals)

29 states + DC and PR have

an RPS(7 states have goals)

DCOK: 15% x 2015

PR: 20% x 2035

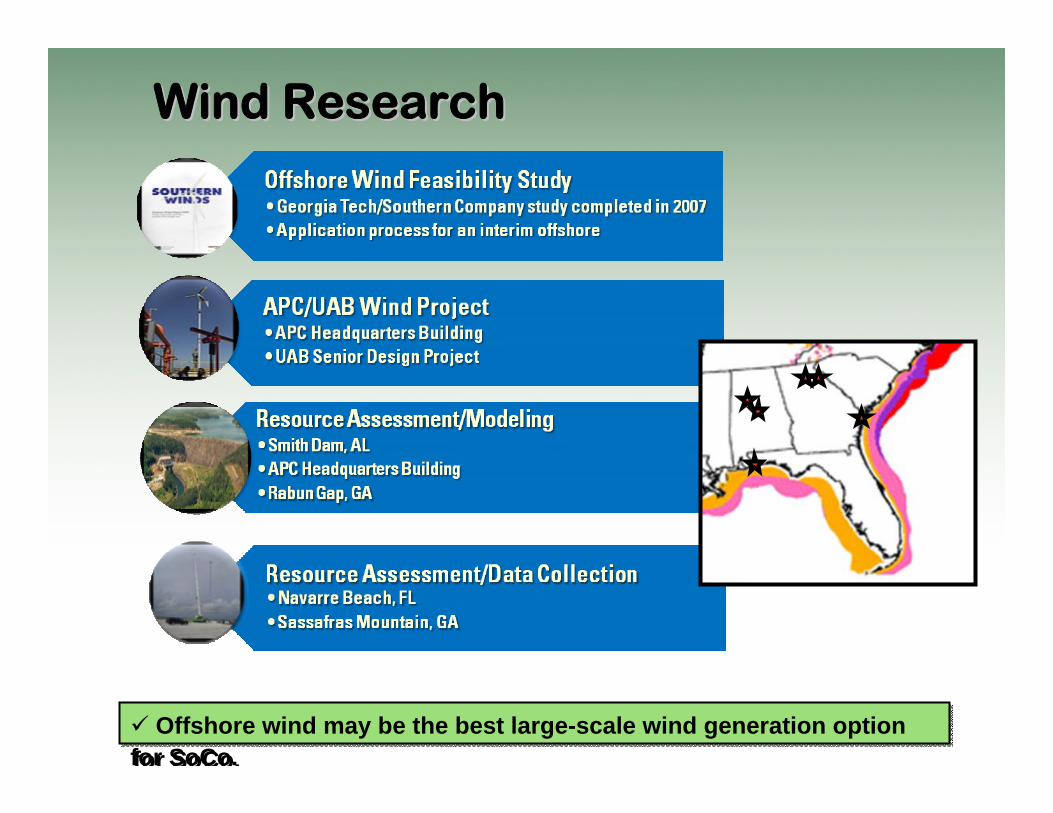

Wind ResearchWind Research

Offshore wind may be the best large-scale wind generation option for SoCo.

Offshore wind may be the best large-scale wind generation option for SoCo.

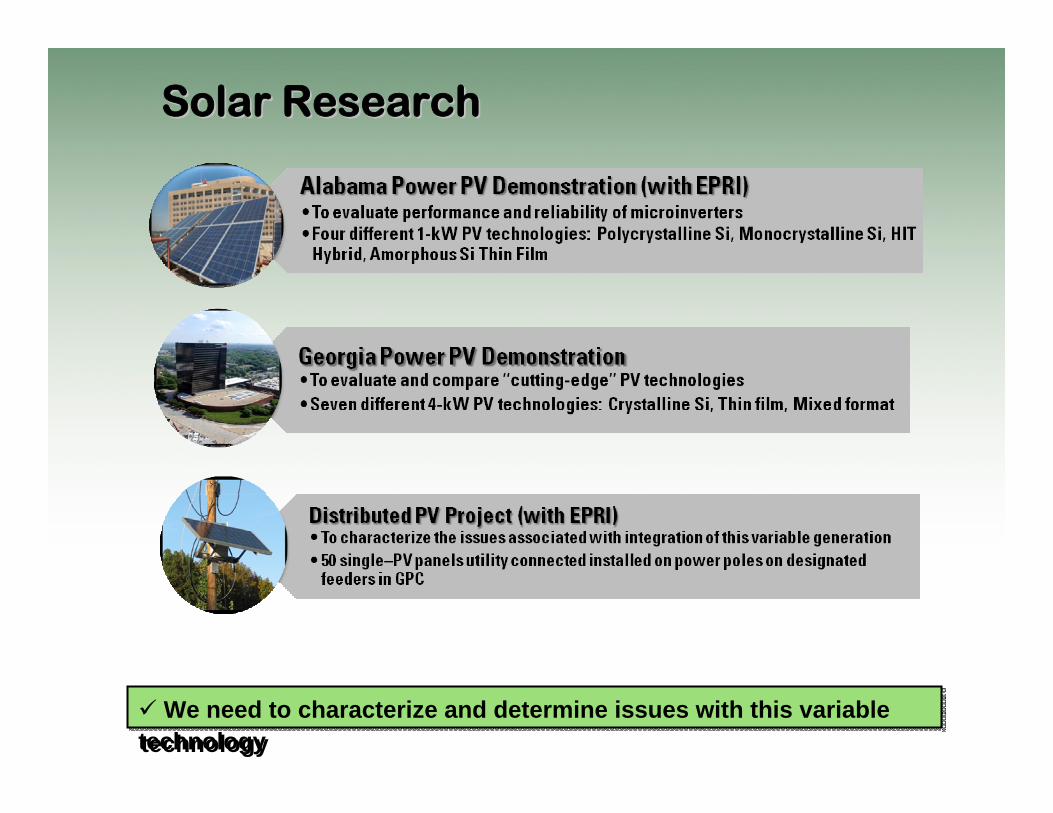

Solar ResearchSolar Research

We need to characterize and determine issues with this variabletechnology

We need to characterize and determine issues with this variabletechnology

Mississippi PowerMississippi Power

Georgia PowerGeorgia Power

BarryBarry

Gadsden Gadsden

MitchellMitchell

Auburn Auburn

Gulf PowerGulf Power

Alabama PowerAlabama Power

Biomass-to-Power Demonstrations

Hammond Hammond

Gaston Gaston

Gorgas Gorgas

Greene County Greene County

Watson Watson Plant MitchellBiomass Conversion

Auburn UniversityBiomass Gasification Project

Plant GadsdenSwitchgrass Co-Firing

Biomass Co-milling tests

SweattSweatt

ScholzScholz

Plants Barry, Scholz, & Sweatt Biomass Conversion Studies

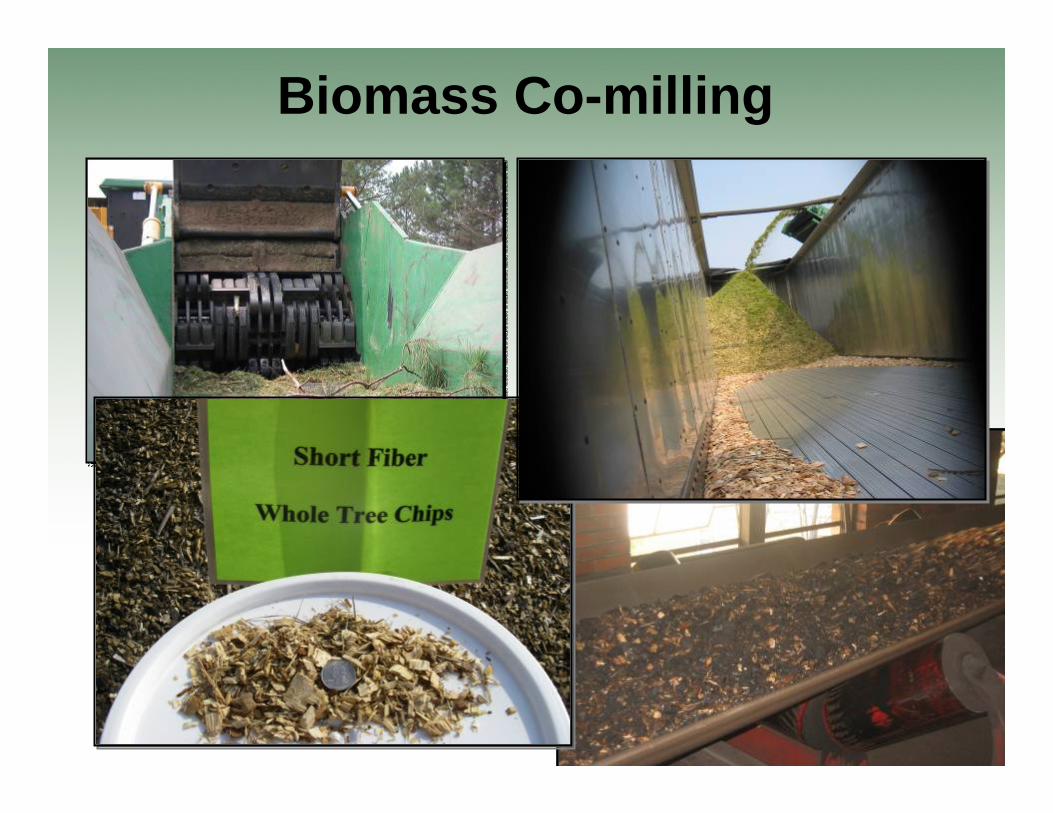

Biomass Co-milling• Biomass co-milling involves

creation of a fuel mix of biomass with coal and sending this mix to the existing fuel handling system

• Advantages• Little or no capital investment• Quick implementation• Low cost fuel

• Disadvantages• Low co-firing %• Fuel handling• Extra pulverizer O&M?• Ash sales

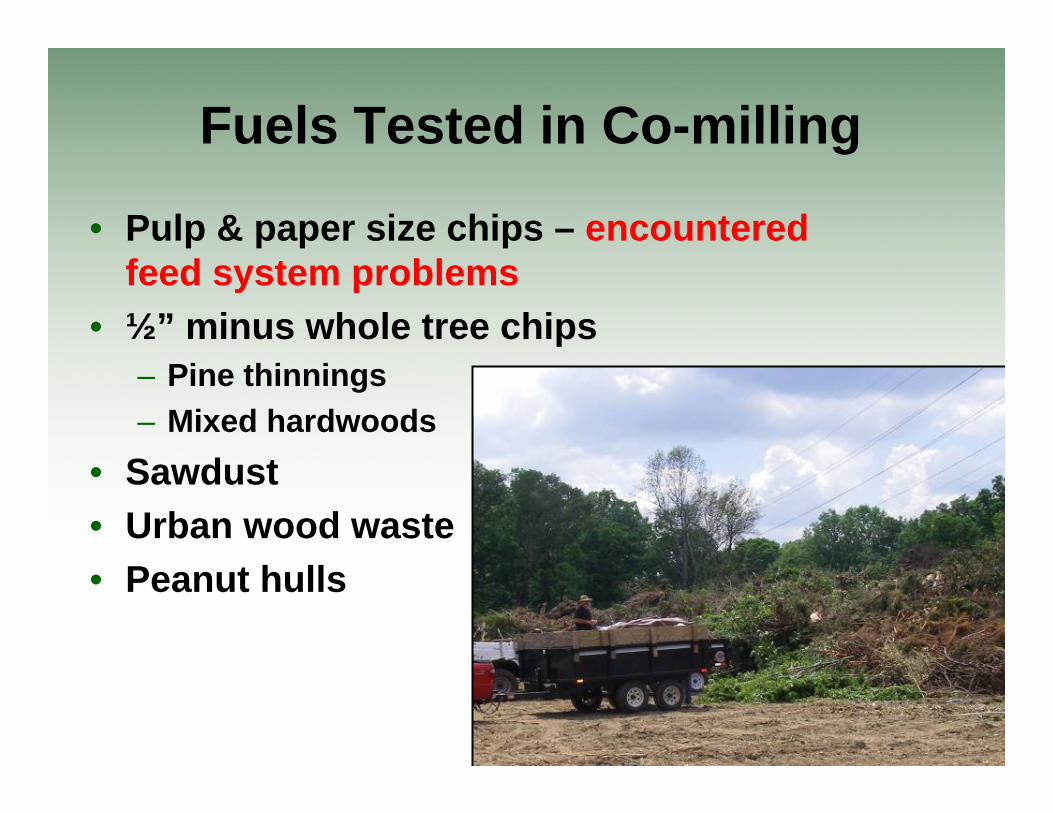

Fuels Tested in Co-milling

• Pulp & paper size chips – encountered feed system problems

• ½” minus whole tree chips– Pine thinnings– Mixed hardwoods

• Sawdust• Urban wood waste• Peanut hulls

Various Fuels Used in Co-milling

Biomass Co-milling

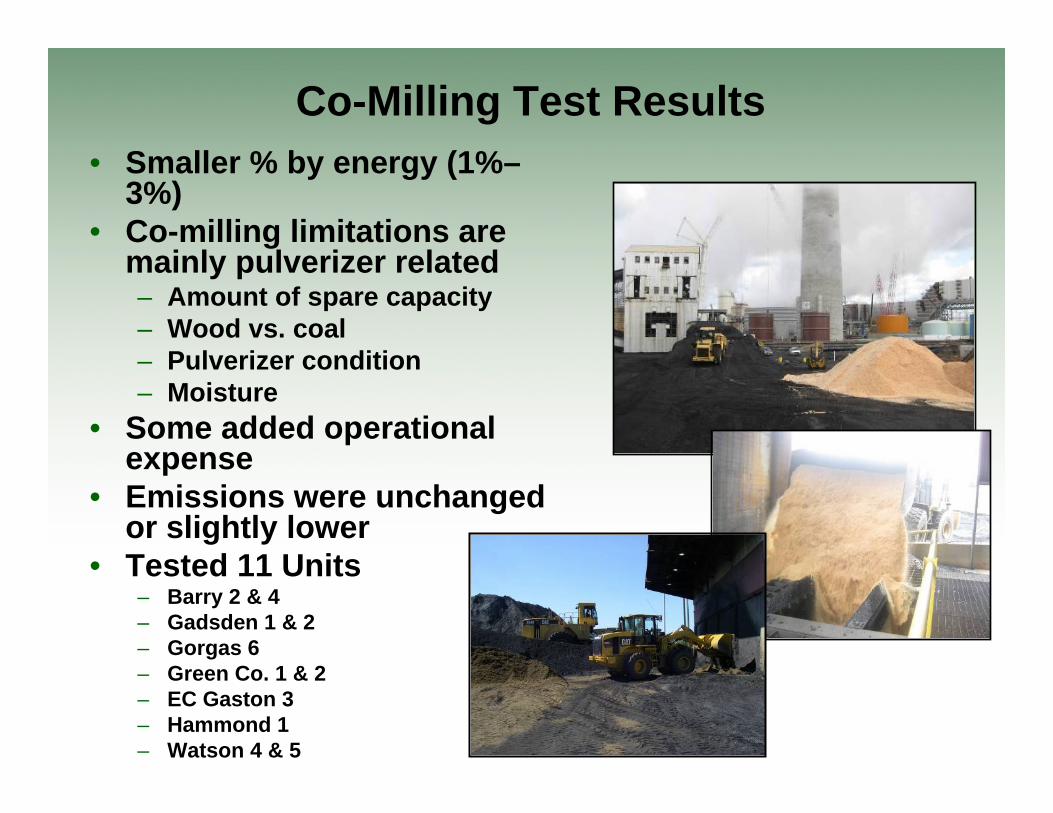

Co-Milling Test Results• Smaller % by energy (1%–

3%)• Co-milling limitations are

mainly pulverizer related– Amount of spare capacity– Wood vs. coal– Pulverizer condition– Moisture

• Some added operational expense

• Emissions were unchanged or slightly lower

• Tested 11 Units– Barry 2 & 4– Gadsden 1 & 2– Gorgas 6– Green Co. 1 & 2– EC Gaston 3– Hammond 1– Watson 4 & 5

Barry 4 Wood Pellet Co-MillingResults• Achieved 7.2% by energy

co-milling at near full load (350 MW)

• New record for Southern Company renewable energy generation at 25 MW

Pellet Disadvantages• Price $10 – 12/MMBtu• Must keep dry• Added capital would be

required for material handling and storage

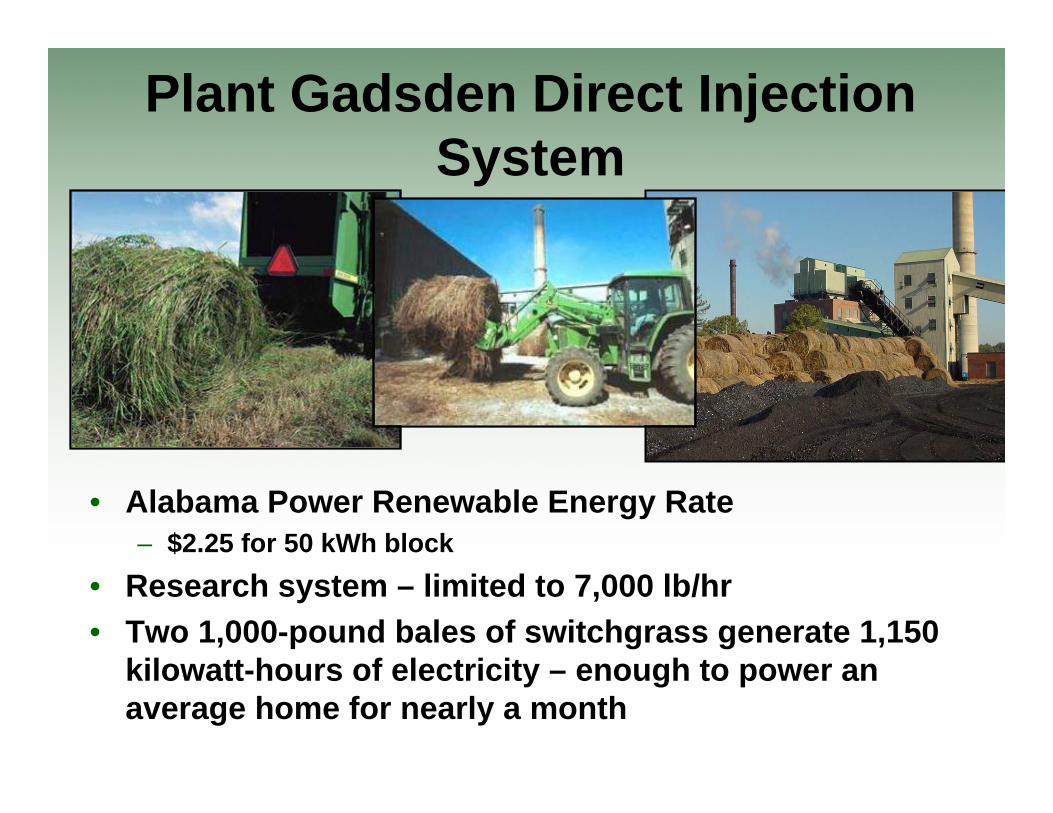

Plant Gadsden Direct Injection System

• Alabama Power Renewable Energy Rate– $2.25 for 50 kWh block

• Research system – limited to 7,000 lb/hr• Two 1,000-pound bales of switchgrass generate 1,150

kilowatt-hours of electricity – enough to power an average home for nearly a month

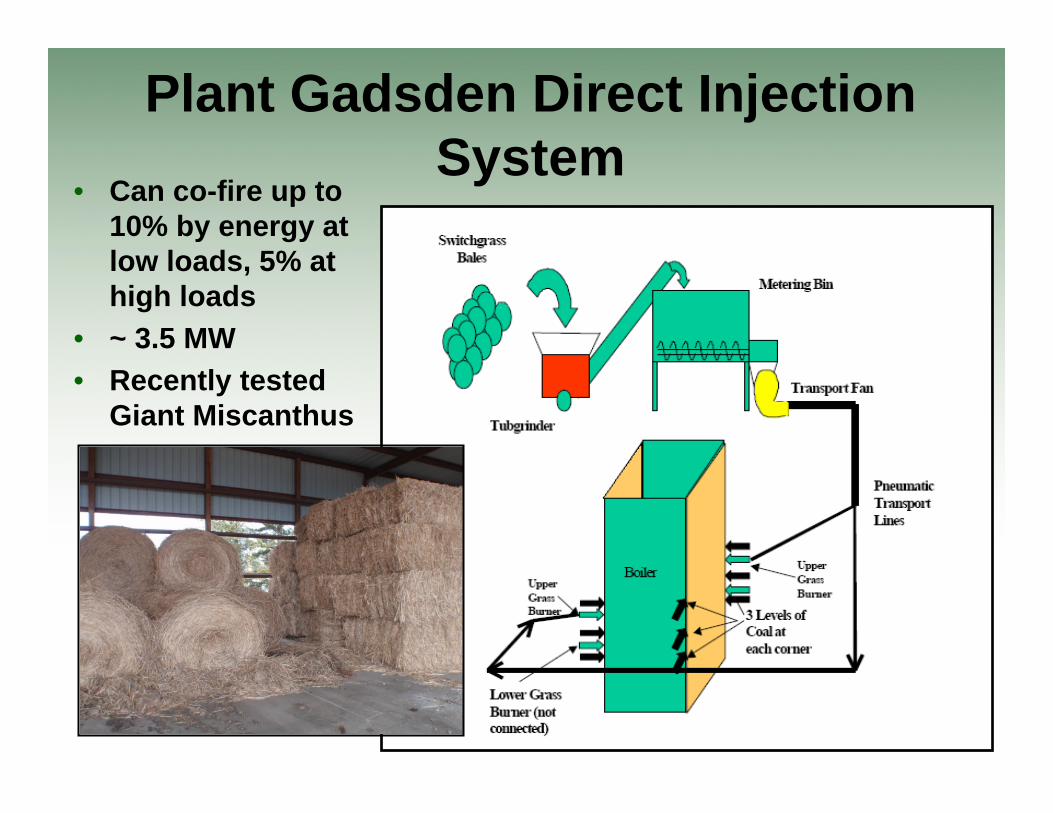

Plant Gadsden Direct Injection System

• Can co-fire up to 10% by energy at low loads, 5% at high loads

• ~ 3.5 MW• Recently tested

Giant Miscanthus

Direct Injection• Proposed direct injection system

– Multiple system designs at different cost points– Will pursue DOE funding in 2011 and beyond

• Only systems in the U.S. located in the Northeast– 2010 trip to visit direct injection sites in New York

• Extensive European experience– Several sites in Europe co-fire Biomass– European sites utilize a wide range of feedstocks

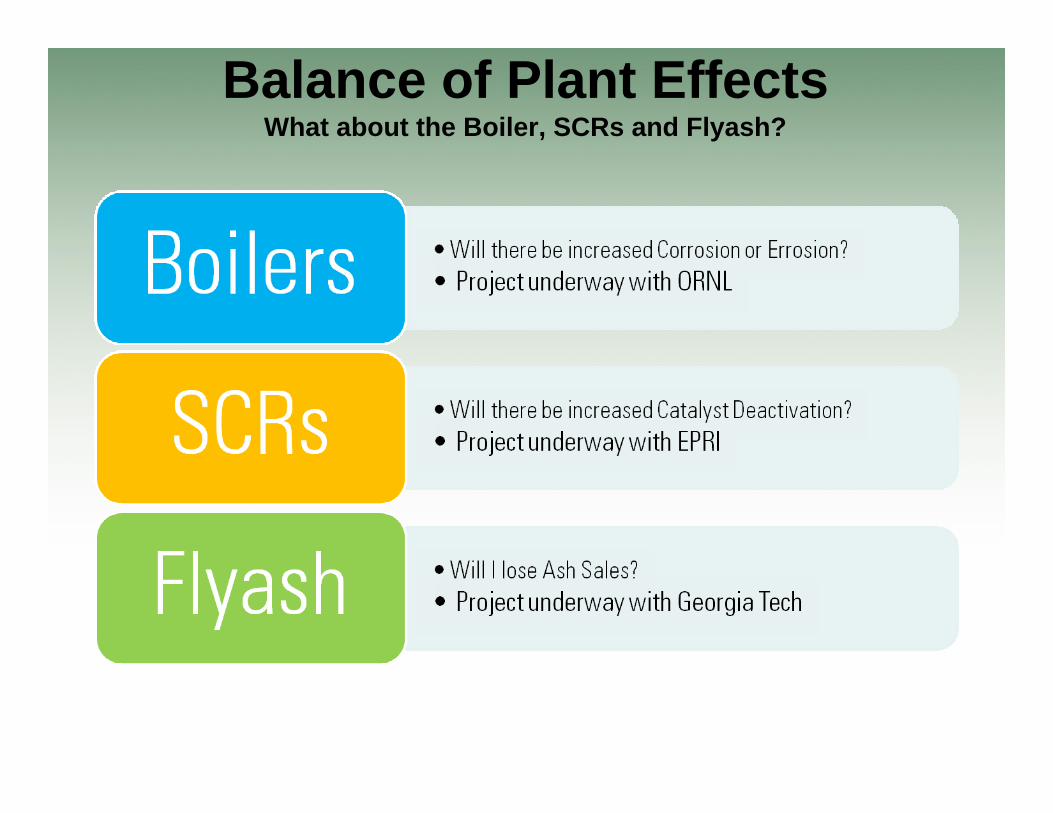

Balance of Plant EffectsWhat about the Boiler, SCRs and Flyash?

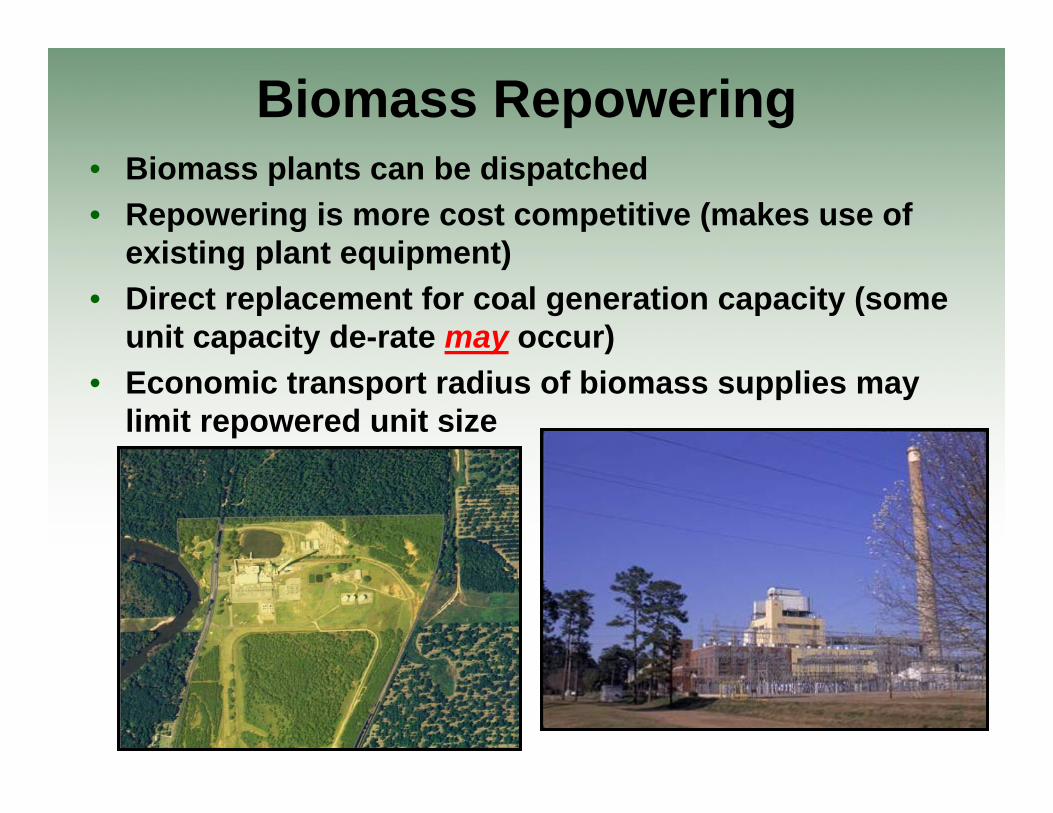

Biomass Repowering• Biomass plants can be dispatched• Repowering is more cost competitive (makes use of

existing plant equipment)• Direct replacement for coal generation capacity (some

unit capacity de-rate may occur)• Economic transport radius of biomass supplies may

limit repowered unit size

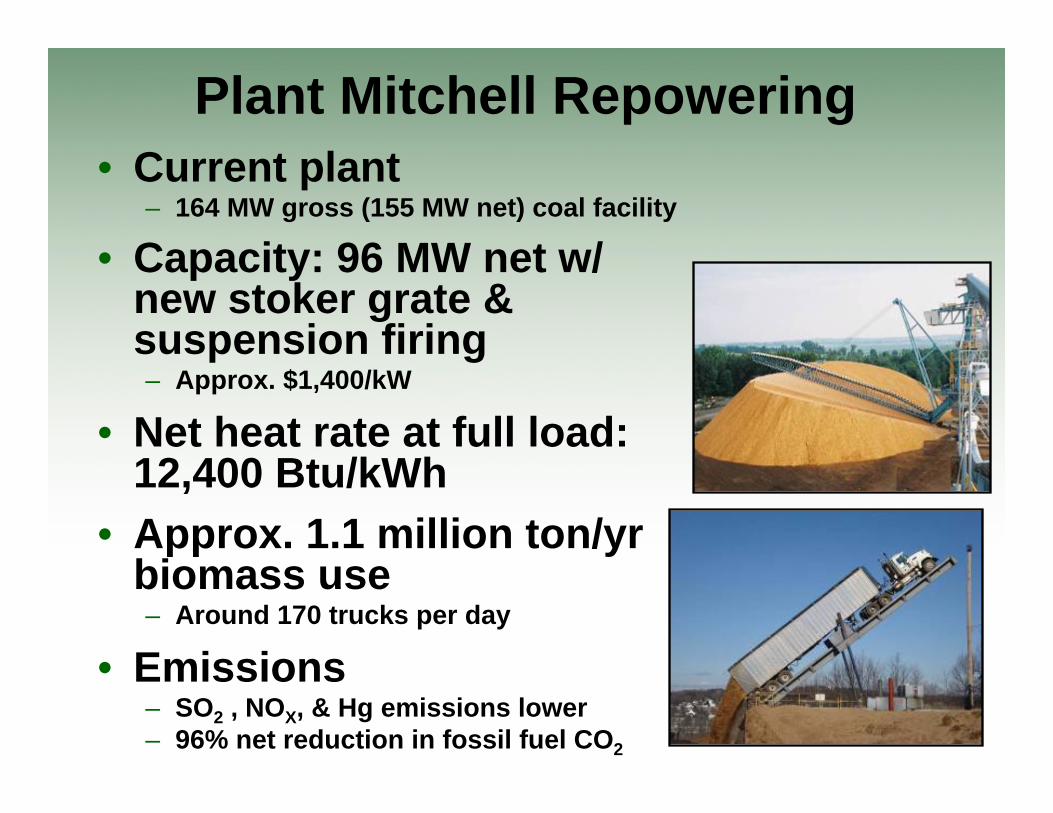

Plant Mitchell Repowering• Current plant

– 164 MW gross (155 MW net) coal facility

• Capacity: 96 MW net w/ new stoker grate & suspension firing– Approx. $1,400/kW

• Net heat rate at full load: 12,400 Btu/kWh

• Approx. 1.1 million ton/yr biomass use– Around 170 trucks per day

• Emissions– SO2 , NOX, & Hg emissions lower– 96% net reduction in fossil fuel CO2

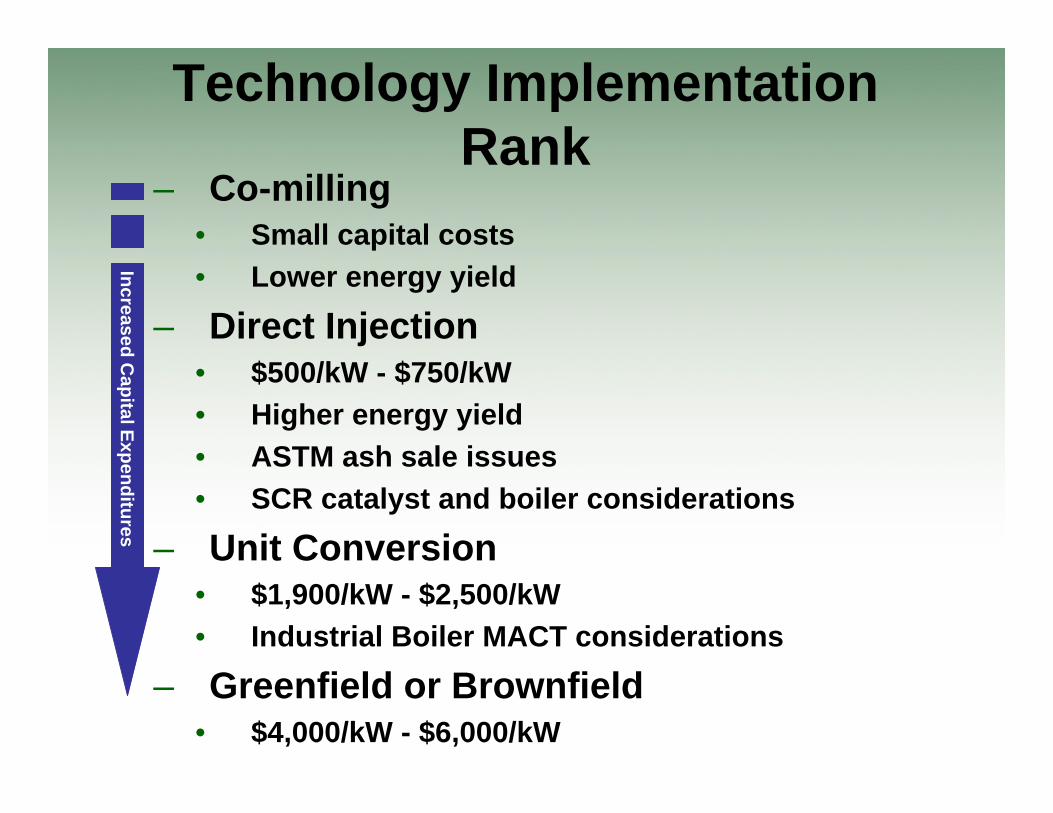

Technology Implementation Rank

– Co-milling• Small capital costs• Lower energy yield

– Direct Injection• $500/kW - $750/kW• Higher energy yield• ASTM ash sale issues• SCR catalyst and boiler considerations

– Unit Conversion• $1,900/kW - $2,500/kW• Industrial Boiler MACT considerations

– Greenfield or Brownfield• $4,000/kW - $6,000/kW

Increased Capital Expenditures

Mitchell Feedstock Plot

• 150 Acres near Plant Mitchell

• Both Herbaceous and Woody Species

• Study of Growth Rates, Maintenance Requirements, and Yields

• Start Date in 2012

Torrefied Wood Research

• Project underway with CEATI to investigate the Torrefactionmarket

• Work is underway to purchase 500 tons of torrefied wood for a test burn at Plant Gadsden.

• Lab and combustor scale testing of material will help understand handling needs and risks

Algae

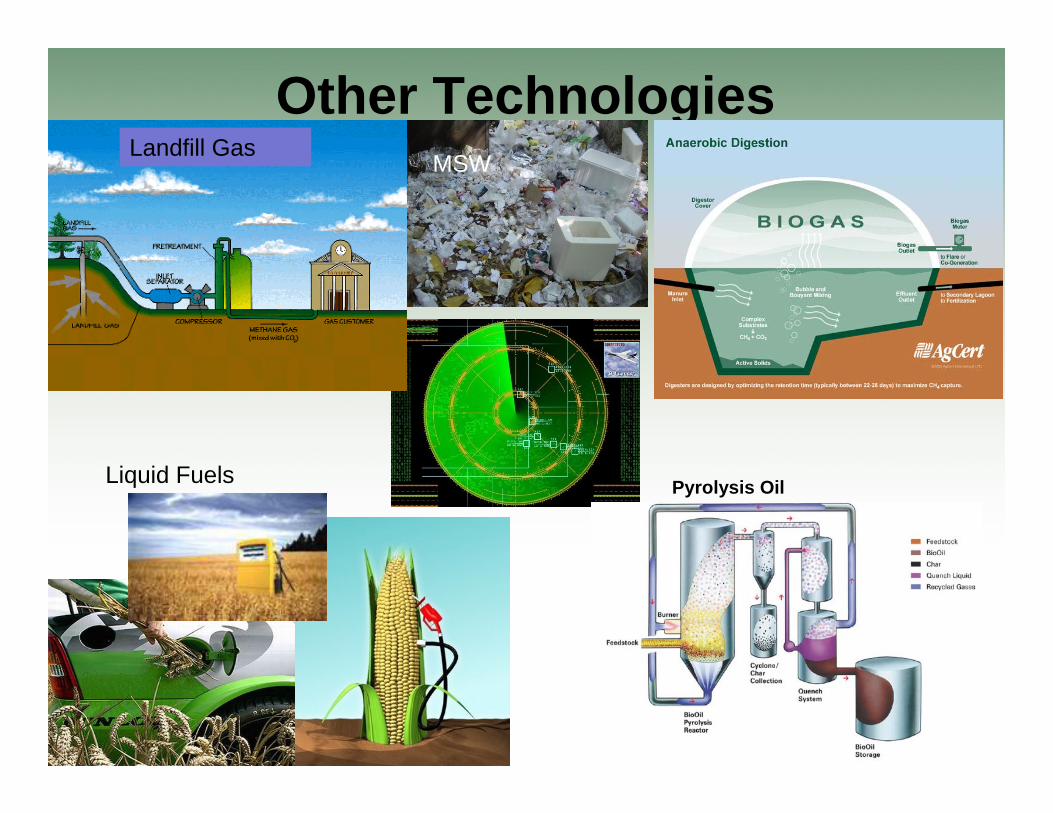

Other Technologies

Pyrolysis Oil

Landfill GasMSW

Liquid Fuels

• Auburn small scale gasifiers– 25 kW distributed gasification trailer– Pressurized (150 psi) gasification bench

scale unit (based on GTI technology)

• UND EERC gasification– Collaboration with EPRI– Transport Reactor Development Unit

(pressurized)

• PSDF pilot plant Transport Reactor research in pressurized biomass gasification– Tested wood pellet feeding 1Q 2009– Gasification test of 20% by energy in 4Q

2009

Biomass Gasification

Neutrality and Sustainability

• Work has begun with NREL on a nationwide sustainability study considering both the RFS 2 and a possible future federal RPS

• Work has begun with Duke and NC State to look at an ideal fuel mix for carbon neutrality.

END