Embed Size (px)

Citation preview

SOUTHERN AFRICAN INSTITUTE FOR BUSINESS ACCOUNTANTS

SAIBA

Recognition of Prior Learning Policy1

Reference number S-P-RPL-002 Accountable Manager

Membership

Policy Owner CEO

Responsible division Membership Status Final Draft

Innitial approval Membership Date of approval 07/2013

Final approval CEO

Date of approval Amendments

Date of Amendment Review Date 2013

Address of policy www.saiba.org.za

1 This policy has been prepared by the SAIBA Membership Department based on the following sources

http://www.saqa.org.za/show.asp?include=focus/rpl.htm

http://www.ifa.org.uk/members/new-members/routes-to-membership/

http://www.openawards.org.uk/scripts/jscripts/tiny_mce/jscripts/tiny_mce/plugins/filemanager/files/Documents/Recognition_of_Prior_Learning_updated.pdf

http://regqs.saqa.org.za/viewQualification.php?id=90913

http://regqs.saqa.org.za/viewQualification.php?id=20366

2

1. Introduction

Recognition of Prior Learning (RPL) is a process whereby potential SAIBA members’ prior learning can be

formally recognised in terms of obtaining the SAIBA designation, regardless of where and how the learning

was attained. RPL acknowledges that people never stop learning, whether it takes place formally at an

educational institution, or whether it happens informally.

The purpose of RPL is:

To redress the historical disadvantages like exclusion of many people from education and training

because of regulations used by institutions, exclusion from certain jobs of certain population

groups, etc.

To validate people's skills and knowledge

For broader development of individuals

To facilitate access to jobs and progression in career paths

For recognition in terms of grading and pay/salary

For planning through skills audits

To promote employment equity

The process of RPL is as follows:

Identifying what a person knows and can do

Matching the person’s knowledge, skills and experience to specific standards and the associated

assessment criteria for a SAIBA designation

Assessing the learning against those standards

Crediting the person for skills, knowledge and experience built up through formal,informal and non-

formal learning that occurred in the past

In practice what this means is that a learner or an employee’s non-traditional or non-formal experience

and learning can be recognised.

The RPL assessment is mostly summative in nature with formative assessment done only to an applicant

where further action is required. The assessment of RPL applicants is done against the same competency

outcomes and assessment criteria as for other SAIBA applicants. All applicants must demonstrate the same

competency outcomes.

The principles of RPL:

RPL is a valid method of enabling individuals to obtain a relevant SAIBA designation

RPL must comply with all regulatory requirements for assessments

RPL is a learner-centred voluntary process

The process of RPL is subject to the same standard of quality assurance and monitoring processes as

any other form of learning and assessment

Assessment methods for RPL must be of equal rigour as other assessment methods, must be fit for

purpose and relate to the evidence of leaning

3

2. Routes to obtaining a SAIBA designation

SAIBA recognises there are many ways of acquiring knowledge and proving competence which may be

proven in different ways. As a consequence SAIBA provides flexible RPL procedures to obtaining a

designation. All RPL routes are measured against the SAIBA competency outcomes and assessment criteria.

RPL by exemption, where recognition is given to relevant completed commerce qualifications that

contain relevant modules

RPL by association, where recognition is given to other relevant professional designations

RPL by credit, where recognition is given to workplace experience and/or part-qualifications/unit

standards/non accredited modules/courses

A SAIBA designation is only issued to SAIBA members. You first have to be approved as a SAIBA member

before you will be eligible for a SAIBA designation.

SAIBA issues the following designations:

Business Accountant

Business Accountant in Practice

2.1 Business Accountant

To obtain the designation Business Accountant an applicant has to:

a. Register as a SAIBA Member

b. Complete an application form to obtain the designation

c. Submit certified copies of a latest ID, CV, academic transcripts

d. Provide proof of

A completed commmerce qualification at NQF 6 or higher (e.g. National Diploma: Accounting, B

Comm: Accounting) that was obtained from an institute of higher learning registered with the

South African Department of Education or

A completed qualification in a related field at NQF 6 or higher that was obtained from an

institute of higher learning registered with the South African Department of Education or

A SAQA evaluation and alignment certificate indicating the comparitive equivilent South African

qualification if the qualification was obtained from a Non South African institute of higher

learning or

Relevent prior learning obtained in the form of part qualifications, modules, short courses our

similar courses completed and which SAIBA has recognised for membership purposes or

Membership of a professional body that ascribes to the membership criteria of the International

Federation of Accountants (IFAC) or a professional body with whom SAIBA has signed a

membership agreement, and whom SAIBA has recognised for membership purposes

e. Complete the workplace experience asessment and confirmation – Refer appendix 1 and 3

4

2.2 Business Accountant in Practice

To obtain the designation Business Accountant in Practice an applicant has to:

a. Register as a SAIBA Member

b. Complete an application form to obtain the designation

c. Submit certified copies of a latest ID, CV, academic transcripts

d. Provide proof of:

A completed commerce qualification at NQF 6 or higher (e.g. National Diploma: Accounting, B

Comm: Accounting) that was obtained from an institute of higher learning registered with the

South African Department of Education or

A SAQA evaluation and alignment certificate indicating the comparative equivalent South

African qualification if the qualification was obtained from a foreign institute of higher learning

(Commerce qualification at NQF 6 or higher) or

Practicing Membership Status of a professional body that ascribes to the membership criteria of

the International Federation of Accountants (IFAC) or a professional body with whom SAIBA has

signed a membership agreement, and whom SAIBA has recognised for membership purposes

e. Academic transcripts must indicate the following modules:

Accounting 1

Economics 1

Business Management 1

South African Commercial Law 1

Business Statistics 1

Accounting Information Systems 2

Management Accounting and Finance 2

Auditing 2

South African Taxation 2

Financial Accounting 2

Ethics 3

Management Accounting and Finance 3

Auditing 3

South African Taxation 3

Financial Accounting 3

f. If the academic transcripts does not include South African Commercial Law or Taxation as described

above then the applicant need to indicate how the competence outcomes was achieved

g. Complete the workplace experience asessment and confirmation – Refer appendix 1 and 3

3. RPL requirements

To obtain a SAIBA designation via RPL a applicant must produce valid and reliable evidence of learning to

support any claims based on experience.

5

3.1 In order to achieve recognition of achievement the learner should submit a portfolio of evidence

based on previous learning, skills and / or competence cross referenced to the SAIBA competnecy

outcomes and assessment criteria – Refer to appendix 1 and appendix 3

3.2 Under some circumstances there may be a limit to the type of designation that can be achieved by

RPL

3.3 The applicant must play an active role in the process as s/he must produce evidence and map it to

the competence outcomes and assessment criteria. Appropriately trained staff from SAIBA should

be available to give advice on this process. The applicant is also required to obtain the support of

their employer or other organisation (e.g. if they have worked as an unpaid volunteer) in order to

be able to confirm achievement of criteria for which there is no tangible evidence, e.g. practical

tasks.

4. Guidance for implementation

SAIBA will adhere to the following RPL operational procedures:

4.1 Awareness raising regarding RPL information, advice and guidance.

4.1.1 Once applicants have decided to consider their application for RPL purposes, they will need to

know about:

o How to claim credit via the RPL process

o Sources of professional support and guidance available to individuals and employers

o The administrative process for RPL applications

o Timelines, appeals processes, and any fees or subsidies

o Does the evidence relate to current learning

o Specific requirements and / or time limits for the currency of evidence, certification, or

demonstration of learning

4.2 Pre-assessment – gathering evidence and giving information

4.2.1 When an individual has decided to pursue an RPL route towards achievement it is vital that the

candidate is fully informed of the RPL process and has sufficient support to make a viable claim

and to make decisions about evidence collection and presentation for assessment.

4.2.2 During this stage the applicant will carry out the evidence collection. The evidence required for

the award of credit will depend on the purpose, learning outcomes and assessment criteria for

the relevant designation

4.2.3 Complete the RPL application form – Refer appendix 2

4.3 Assessment / documentation of evidence

4.3.1 Assessment as part of RPL is a structured process for gathering and reviewing evidence and

making judgements about a applicant’s prior leaning and experiencein relation to a designation.

6

4.3.2 Assessment must be valid and reliable to ensure the integrity RPL system as a whole. The

assessment process for RPL must be subject to the same quality assurance processes as any

other of the assessment process. An appicants’ work which contributes towards their claim for

credit via the RPL process should be internally and externally verified and all achievement

documented as for conventional applicant achievement, all RPL related achievement should be

marked as such in all documentation.

4.4 Awarding credit

4.4.1 SAIBA is responsible for awarding credit. The procedure is the same as for other forms of

assessment. The credit is recorded in the applicants’ record.

4.5 Feedback

4.5.1 After the assessment SAIBA will need to give feedback to the applicant, discussing the results

and giving support and guidance on the options available to the applicant, which may include,

for example, further leaning and development.

4.6 Appeal

4.6.1 If an applicant wish to appeal against a decision made about their claim for credit (via the RPL

process) they would need to follow the standard appeals process that exist within SAIBA.

5. Collating information on the use of RPL

In order to quantify the use of RPL processes, SAIBA will be required to identify the provision where RPL

has been applied. Collated information about the use of RPL and credit exemption will be made available as

part of the annual quality process.

7

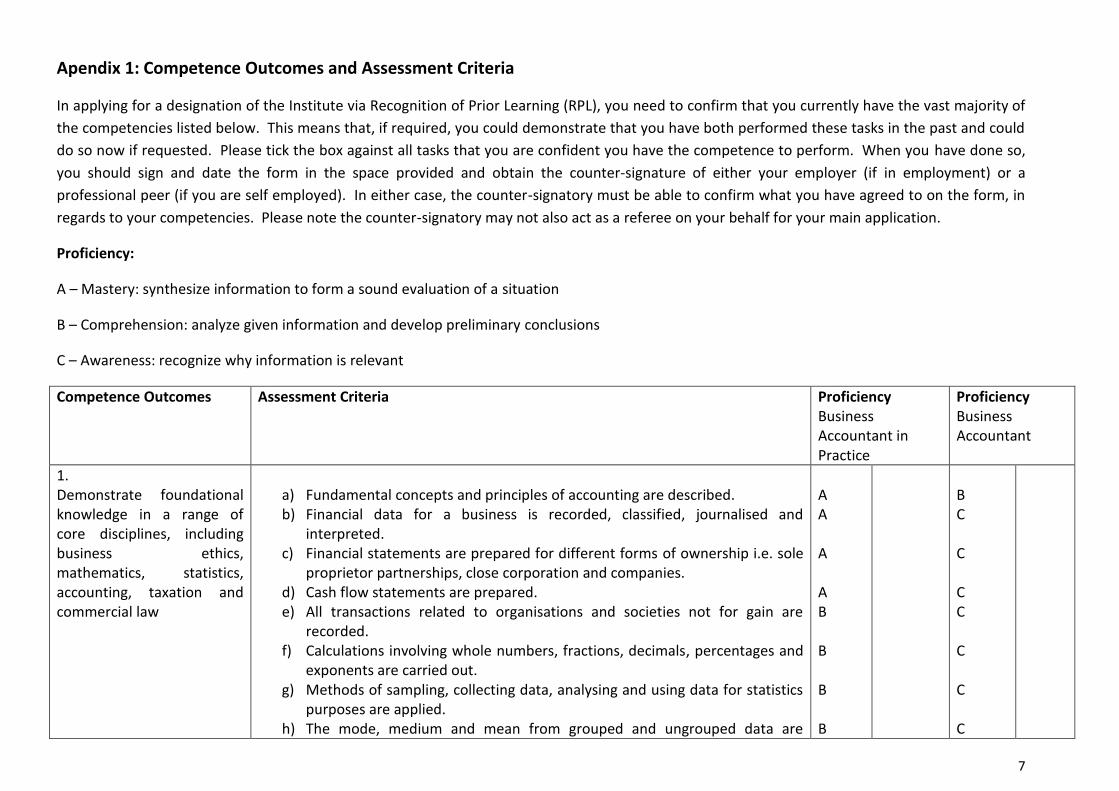

Apendix 1: Competence Outcomes and Assessment Criteria

In applying for a designation of the Institute via Recognition of Prior Learning (RPL), you need to confirm that you currently have the vast majority of

the competencies listed below. This means that, if required, you could demonstrate that you have both performed these tasks in the past and could

do so now if requested. Please tick the box against all tasks that you are confident you have the competence to perform. When you have done so,

you should sign and date the form in the space provided and obtain the counter-signature of either your employer (if in employment) or a

professional peer (if you are self employed). In either case, the counter-signatory must be able to confirm what you have agreed to on the form, in

regards to your competencies. Please note the counter-signatory may not also act as a referee on your behalf for your main application.

Proficiency:

A – Mastery: synthesize information to form a sound evaluation of a situation

B – Comprehension: analyze given information and develop preliminary conclusions

C – Awareness: recognize why information is relevant

Competence Outcomes Assessment Criteria Proficiency Business Accountant in Practice

Proficiency Business Accountant

1. Demonstrate foundational knowledge in a range of core disciplines, including business ethics, mathematics, statistics, accounting, taxation and commercial law

a) Fundamental concepts and principles of accounting are described. b) Financial data for a business is recorded, classified, journalised and

interpreted. c) Financial statements are prepared for different forms of ownership i.e. sole

proprietor partnerships, close corporation and companies. d) Cash flow statements are prepared. e) All transactions related to organisations and societies not for gain are

recorded. f) Calculations involving whole numbers, fractions, decimals, percentages and

exponents are carried out. g) Methods of sampling, collecting data, analysing and using data for statistics

purposes are applied. h) The mode, medium and mean from grouped and ungrouped data are

A A A A B B B B

B C C C C C C C

8

calculated and analysed. i) Common measures of dispersion from grouped and ungrouped data

including the range, inter-quartile range, quartile, mean deviation and standard deviation are examined.

j) The law of contract; the formation of a contract; principles and rules concerning valid and binding contracts; breach of contract, remedies on the ground of breach of contract are applied.

k) Knowledge of the provisions of the Basic Conditions of Employment Act is demonstrated.

l) Income tax, donations tax, capital gains and losses and value-added tax are calculated.

m) Tax payable by individuals, partners, sole traders and non-residents are calculated.

n) Tax Administration is effectivly applied o) The ethical decision-making process is discussed. p) Principles of macro-ethics are applied. q) The relationship between management and organisational ethics are

critically evaluated. r) The principles of corporate social responsibility are applied.

B B B A B B A B B B

C B B C C C A B B B

2. Demonstrate specialist forefront knowledge and expertise in information systems.

a) Gained knowledge and understanding of accounting information systems is

practiced. b) Knowledge of accounting information systems in the business environment

is applied. c) Accounting information skills are applied in order to participate and interact

on a practical level in a business environment.

B B A

C C B

3. Provide accurate financial information vital in the organisational structures to management for decision making

a) An understanding of the key concepts in cost accounting and various costing

systems is demonstrated. b) A cost-volume-profit relationship is evaluated and cost data are analysed for

decision making. c) The nature and purpose of budgeting and budgetary control are described. d) The activity-based model is implemented to measure the costs of activities. e) The nature and purpose of a number of recent developments in

management accounting practice are outlined.

A B B B B

B C C C C

9

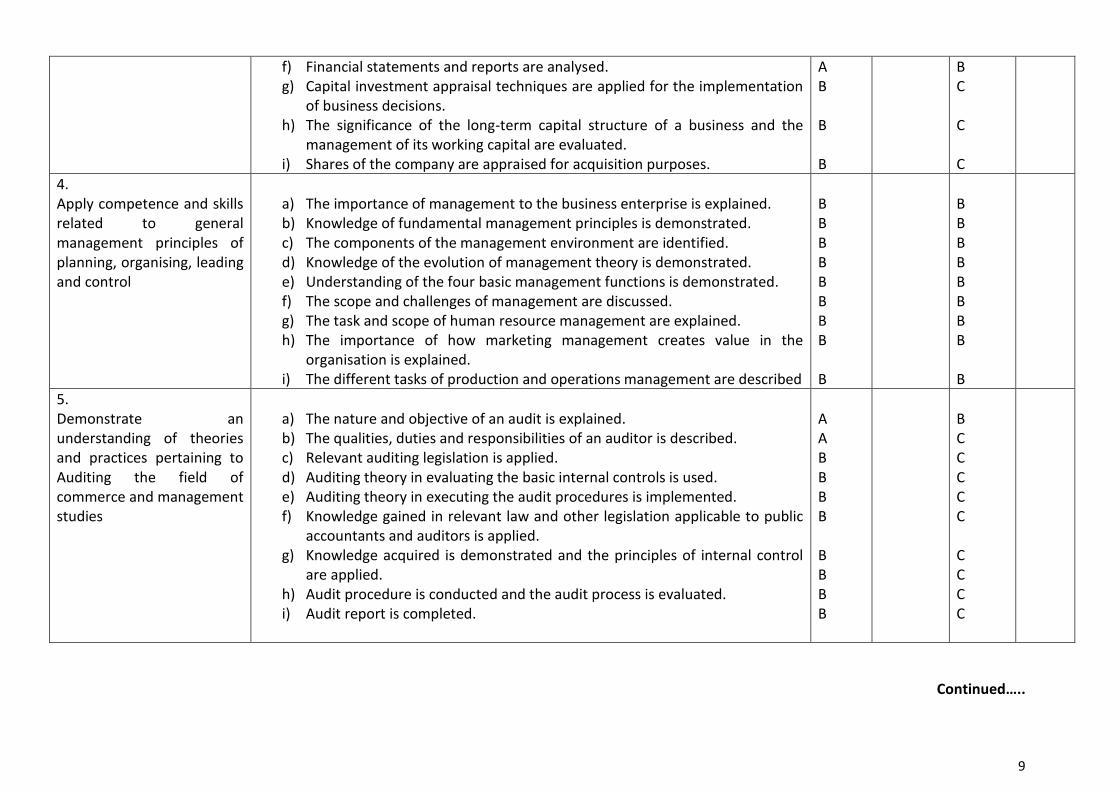

f) Financial statements and reports are analysed. g) Capital investment appraisal techniques are applied for the implementation

of business decisions. h) The significance of the long-term capital structure of a business and the

management of its working capital are evaluated. i) Shares of the company are appraised for acquisition purposes.

A B B B

B C C C

4. Apply competence and skills related to general management principles of planning, organising, leading and control

a) The importance of management to the business enterprise is explained. b) Knowledge of fundamental management principles is demonstrated. c) The components of the management environment are identified. d) Knowledge of the evolution of management theory is demonstrated. e) Understanding of the four basic management functions is demonstrated. f) The scope and challenges of management are discussed. g) The task and scope of human resource management are explained. h) The importance of how marketing management creates value in the

organisation is explained. i) The different tasks of production and operations management are described

B B B B B B B B B

B B B B B B B B B

5. Demonstrate an understanding of theories and practices pertaining to Auditing the field of commerce and management studies

a) The nature and objective of an audit is explained. b) The qualities, duties and responsibilities of an auditor is described. c) Relevant auditing legislation is applied. d) Auditing theory in evaluating the basic internal controls is used. e) Auditing theory in executing the audit procedures is implemented. f) Knowledge gained in relevant law and other legislation applicable to public

accountants and auditors is applied. g) Knowledge acquired is demonstrated and the principles of internal control

are applied. h) Audit procedure is conducted and the audit process is evaluated. i) Audit report is completed.

A A B B B B B B B B

B C C C C C C C C C

Continued…..

10

Confirmation of Assessment.

I confirm that the completed assessment is an honest & accurate self-appraisal of my competencies.

Signature of RPL Applicant .....................................................................

Name ..................................................................... Date.....................................................................

I confirm the accuracy of the applicant’s self assessment, based upon my own accurate knowledge of their competence.

Signature. .................................................... Professional qualification.........................................

Name .................................................................... Date.....................................................................

Job Title/Position Held. .....................................................................................................................

Name of Business Organisation ........................................................................................................

Address .............................................................................................................................................

Post Code ....................................................

Telephone Contact Number ..........................................................................................................

Relationship to the Applicant ..........................................................................................................

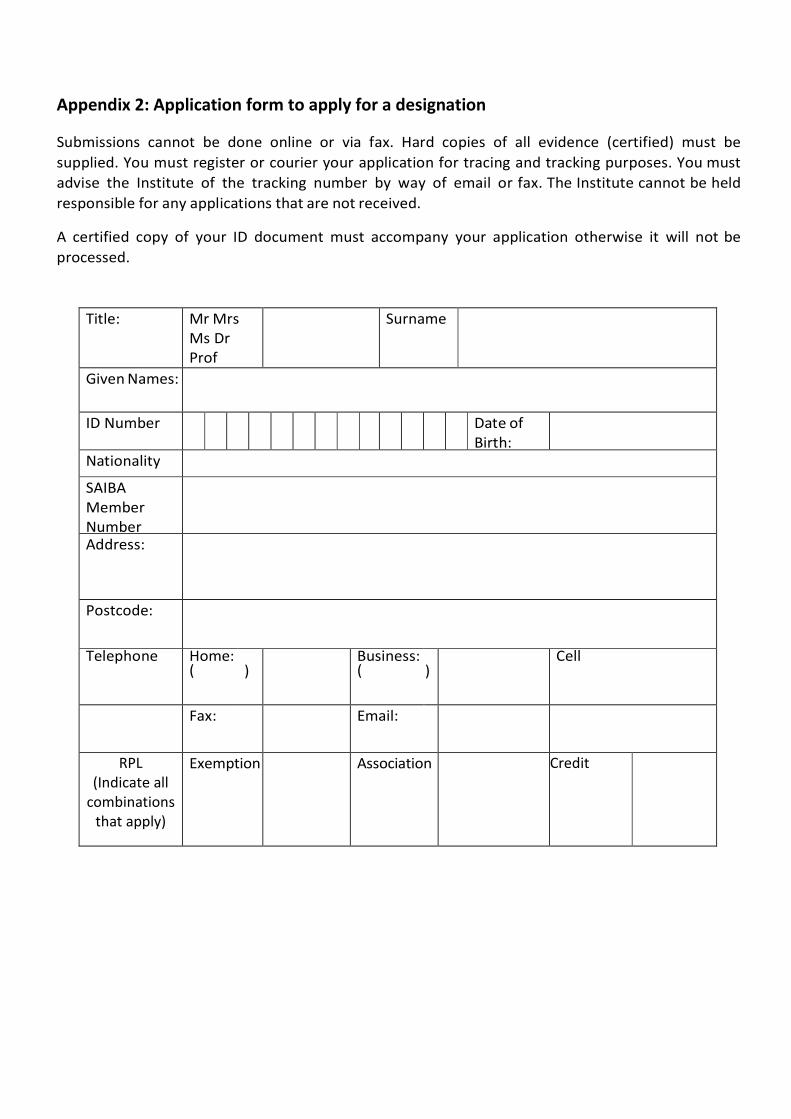

Appendix 2: Application form to apply for a designation

Submissions cannot be done online or via fax. Hard copies of all evidence (certified) must be

supplied. You must register or courier your application for tracing and tracking purposes. You must

advise the Institute of the tracking number by way of email or fax. The Institute cannot be held

responsible for any applications that are not received.

A certified copy of your ID document must accompany your application otherwise it will not be

processed.

Title: Mr Mrs Ms Dr Prof

Surname

Given Names:

ID Number Date of Birth:

Nationality

SAIBA Member Number

Address:

Postcode:

Telephone Home: (

)

Business: (

)

Cell

Fax: Email:

RPL (Indicate all

combinations that apply)

Exemption Association Credit

12

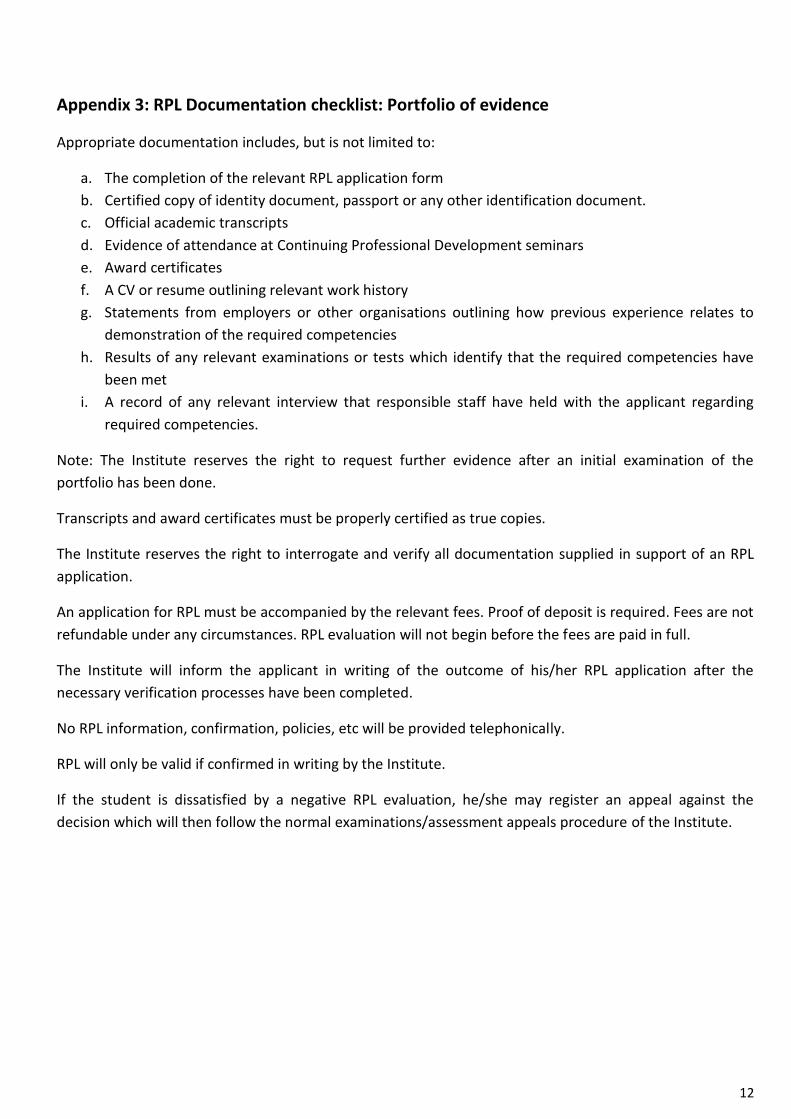

Appendix 3: RPL Documentation checklist: Portfolio of evidence

Appropriate documentation includes, but is not limited to:

a. The completion of the relevant RPL application form

b. Certified copy of identity document, passport or any other identification document.

c. Official academic transcripts

d. Evidence of attendance at Continuing Professional Development seminars

e. Award certificates

f. A CV or resume outlining relevant work history

g. Statements from employers or other organisations outlining how previous experience relates to

demonstration of the required competencies

h. Results of any relevant examinations or tests which identify that the required competencies have

been met

i. A record of any relevant interview that responsible staff have held with the applicant regarding

required competencies.

Note: The Institute reserves the right to request further evidence after an initial examination of the

portfolio has been done.

Transcripts and award certificates must be properly certified as true copies.

The Institute reserves the right to interrogate and verify all documentation supplied in support of an RPL

application.

An application for RPL must be accompanied by the relevant fees. Proof of deposit is required. Fees are not

refundable under any circumstances. RPL evaluation will not begin before the fees are paid in full.

The Institute will inform the applicant in writing of the outcome of his/her RPL application after the

necessary verification processes have been completed.

No RPL information, confirmation, policies, etc will be provided telephonically.

RPL will only be valid if confirmed in writing by the Institute.

If the student is dissatisfied by a negative RPL evaluation, he/she may register an appeal against the

decision which will then follow the normal examinations/assessment appeals procedure of the Institute.