Embed Size (px)

Citation preview

Southeast Association of Rail Shippers Intermodal Perspective

Don Ingersoll Vice President of Transportation

XPO Today: A Top Ten Global Leader

XPO provides cutting-edge supply chain solutions to the most successful companies in the world

! #2 contract logistics provider worldwide by square footage

! #2 freight brokerage firm worldwide by net revenue

! #1 last mile logistics provider for heavy goods in North America

! #1 manager of expedited shipments in North America

! #3 provider of intermodal in North America

! Largest owned fleet in Europe

! Largest platform for outsourced e-fulfillment in Europe

! Growing presence in global freight forwarding

2 | Intermodal Perspective

Source: Industry publications and company filings

3 | Intermodal Perspective

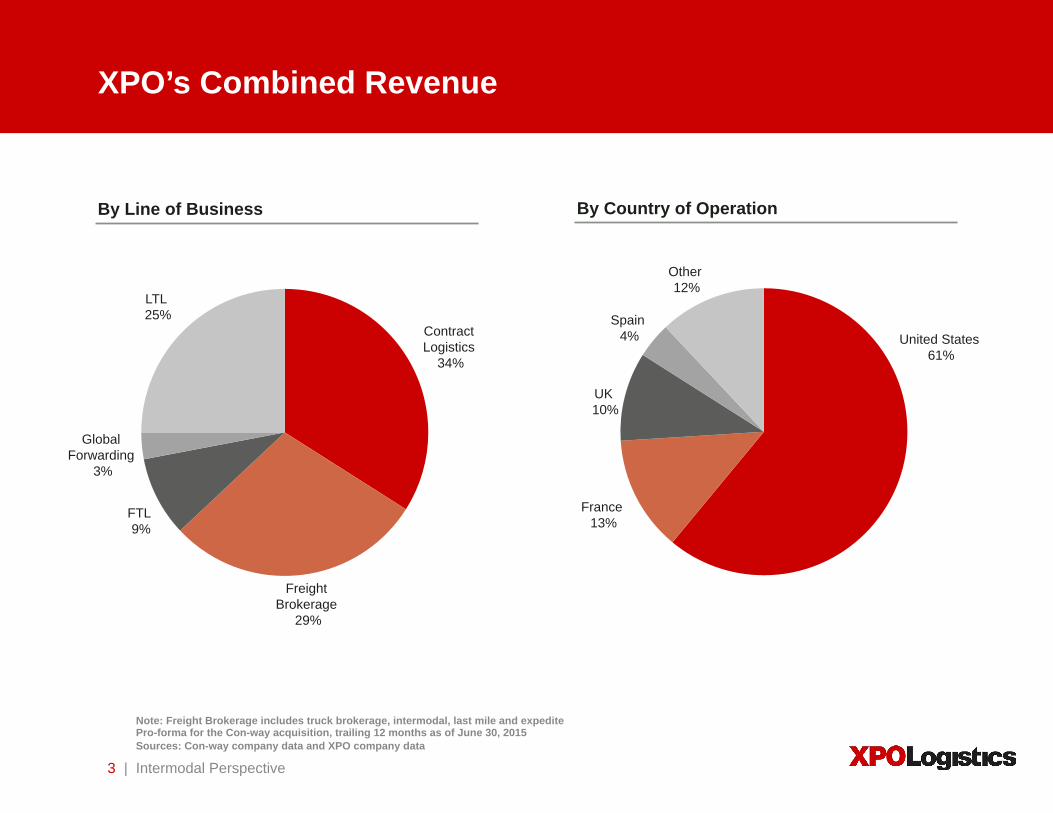

XPO’s Combined Revenue

Note: Freight Brokerage includes truck brokerage, intermodal, last mile and expedite Pro-forma for the Con-way acquisition, trailing 12 months as of June 30, 2015 Sources: Con-way company data and XPO company data

By Line of Business

Contract Logistics

34%

Freight Brokerage

29%

FTL 9%

Global Forwarding

3%

LTL 25%

By Country of Operation

United States 61%

France 13%

UK 10%

Spain 4%

Other 12%

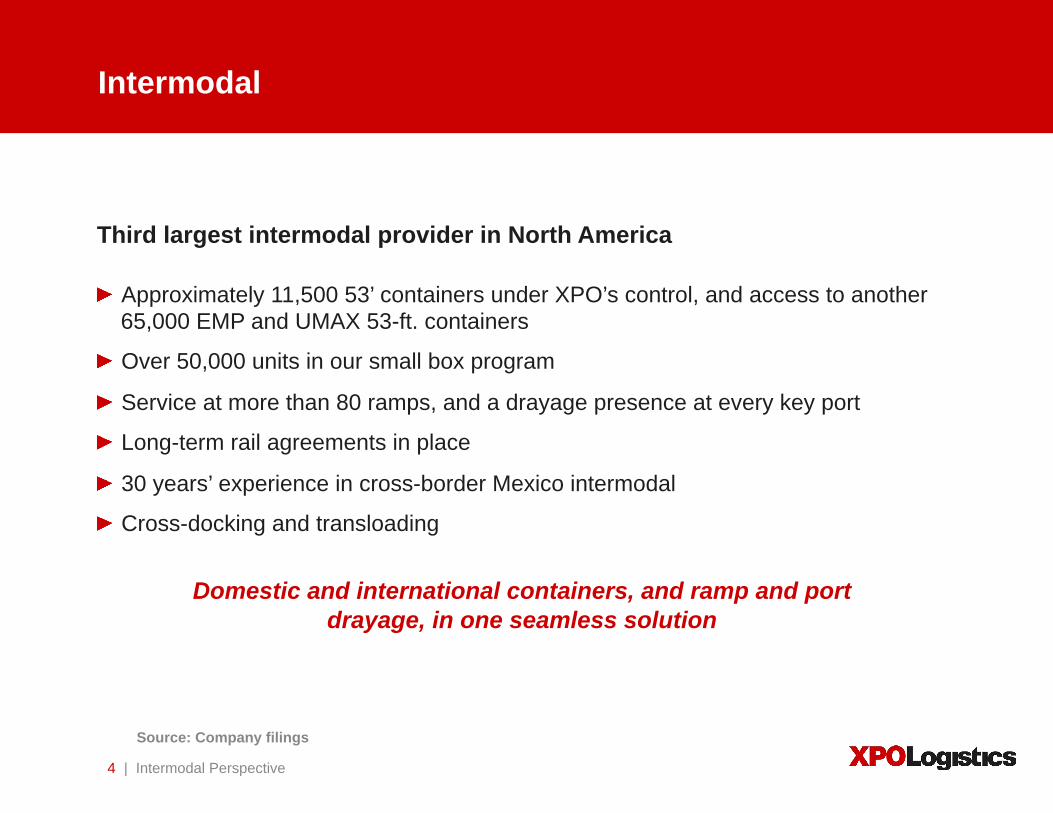

Intermodal

4 | Intermodal Perspective

! Approximately 11,500 53’ containers under XPO’s control, and access to another 65,000 EMP and UMAX 53-ft. containers

! Over 50,000 units in our small box program

! Service at more than 80 ramps, and a drayage presence at every key port

! Long-term rail agreements in place

! 30 years’ experience in cross-border Mexico intermodal

! Cross-docking and transloading

Domestic and international containers, and ramp and port drayage, in one seamless solution

Source: Company filings

Third largest intermodal provider in North America

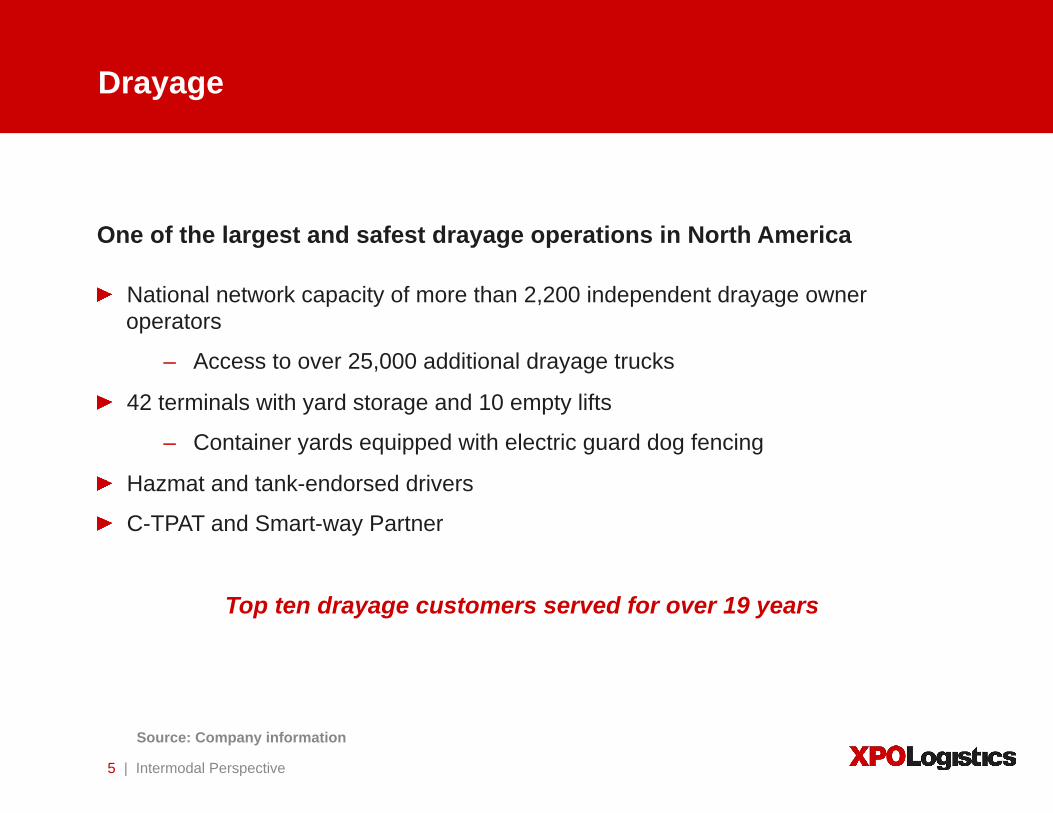

Drayage

5 | Intermodal Perspective

! National network capacity of more than 2,200 independent drayage owner operators

– Access to over 25,000 additional drayage trucks

! 42 terminals with yard storage and 10 empty lifts

– Container yards equipped with electric guard dog fencing

! Hazmat and tank-endorsed drivers

! C-TPAT and Smart-way Partner

Top ten drayage customers served for over 19 years

Source: Company information

One of the largest and safest drayage operations in North America

6 | Intermodal Perspective

Intermodal Locations

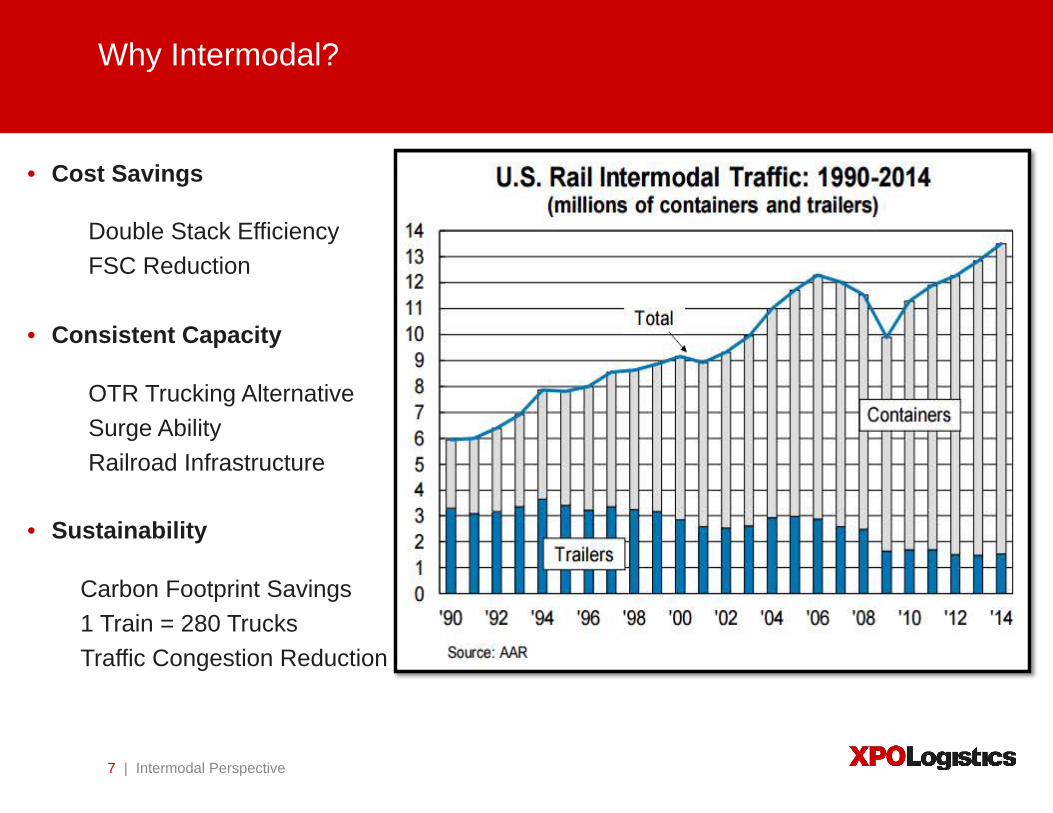

Why Intermodal?

• Cost Savings

Double Stack Efficiency FSC Reduction

• Consistent Capacity

OTR Trucking Alternative Surge Ability Railroad Infrastructure

• Sustainability

Carbon Footprint Savings 1 Train = 280 Trucks Traffic Congestion Reduction

| Intermodal Perspective 7

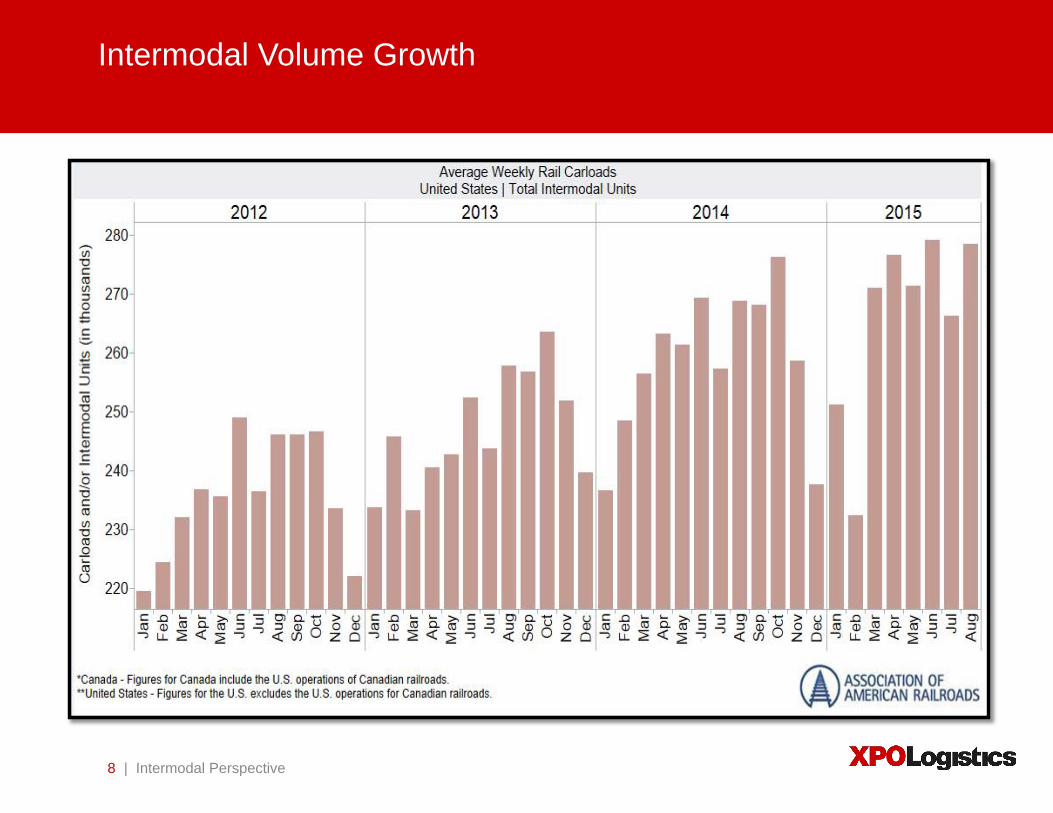

Intermodal Volume Growth

| Intermodal Perspective 8

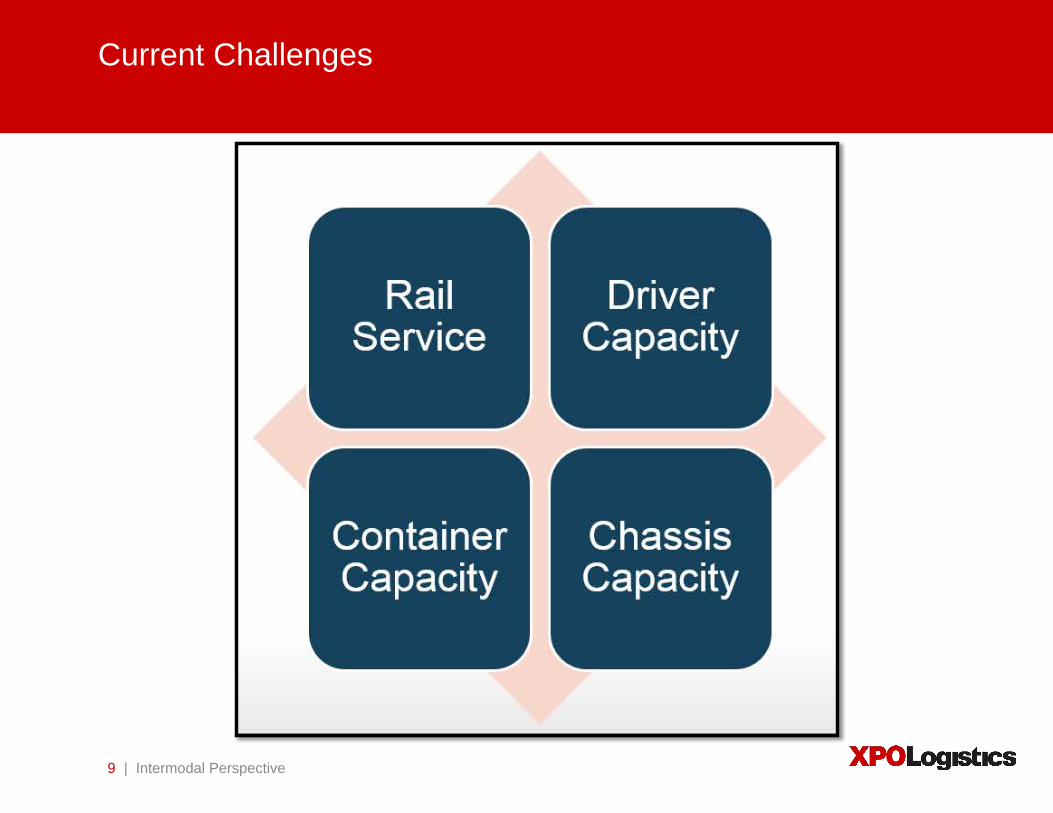

Current Challenges

| Intermodal Perspective 9

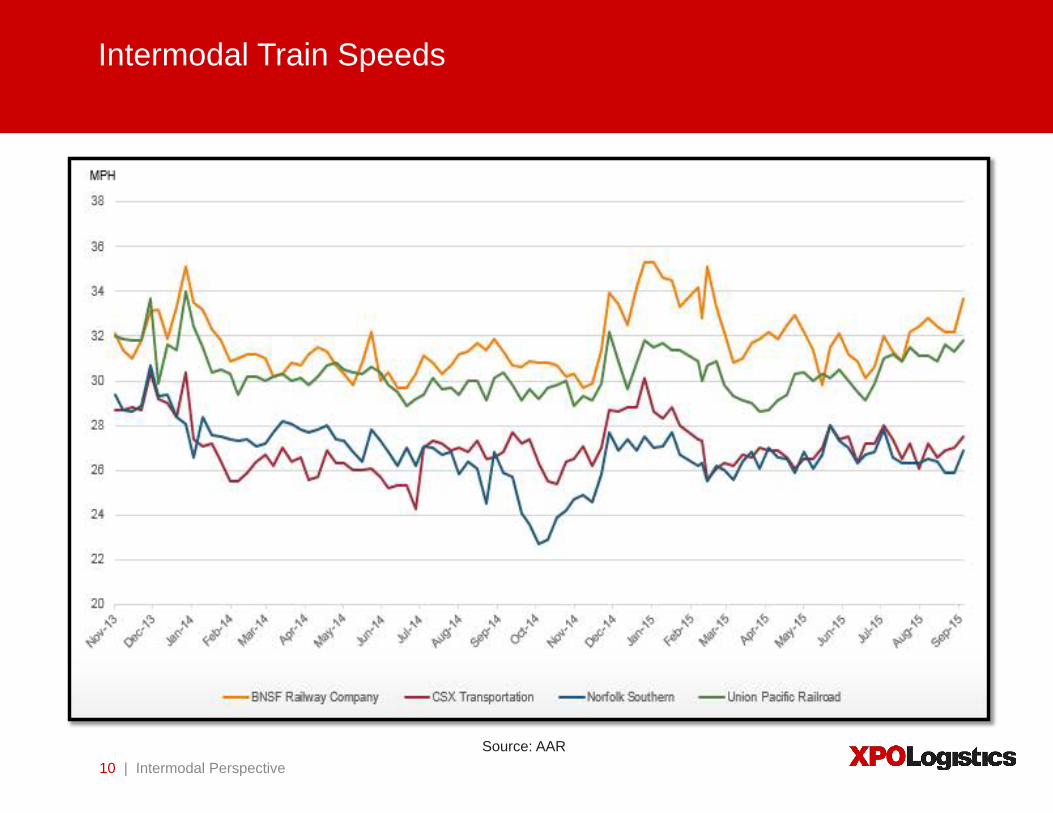

Intermodal Train Speeds

| Intermodal Perspective 10 Source: AAR

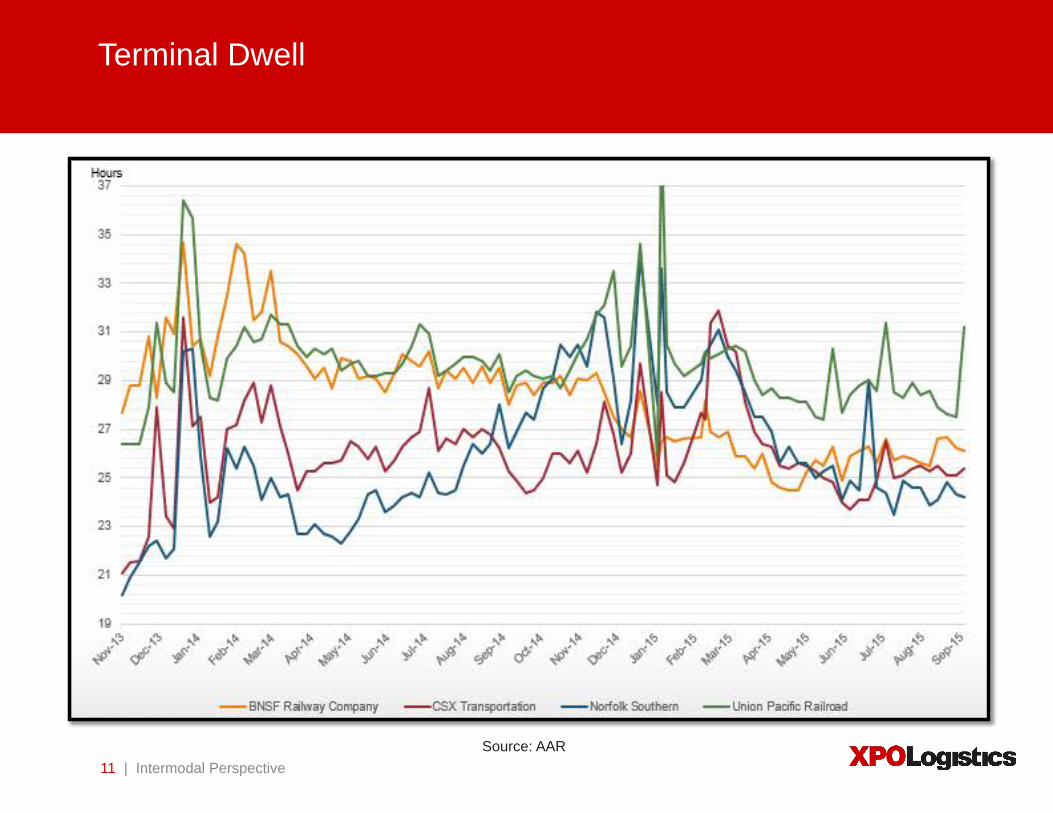

Terminal Dwell

| Intermodal Perspective 11 Source: AAR

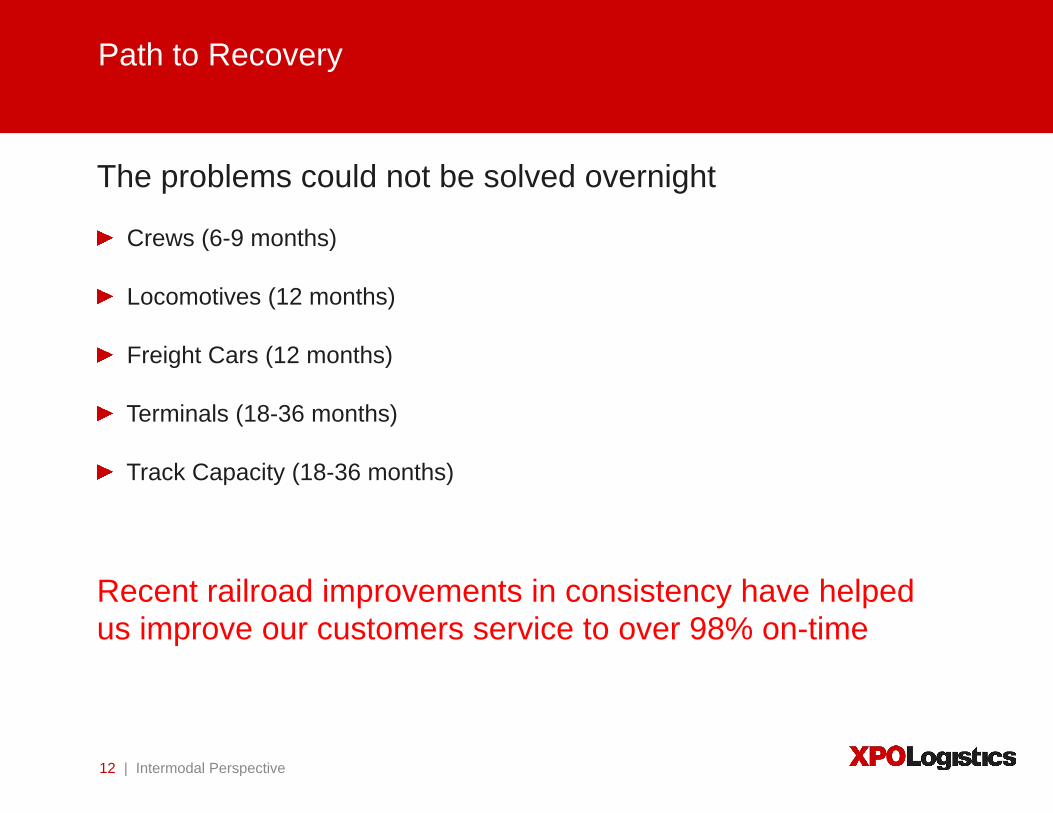

Path to Recovery

The problems could not be solved overnight

! Crews (6-9 months)

! Locomotives (12 months)

! Freight Cars (12 months)

! Terminals (18-36 months)

! Track Capacity (18-36 months)

Recent railroad improvements in consistency have helped us improve our customers service to over 98% on-time

| Intermodal Perspective 12

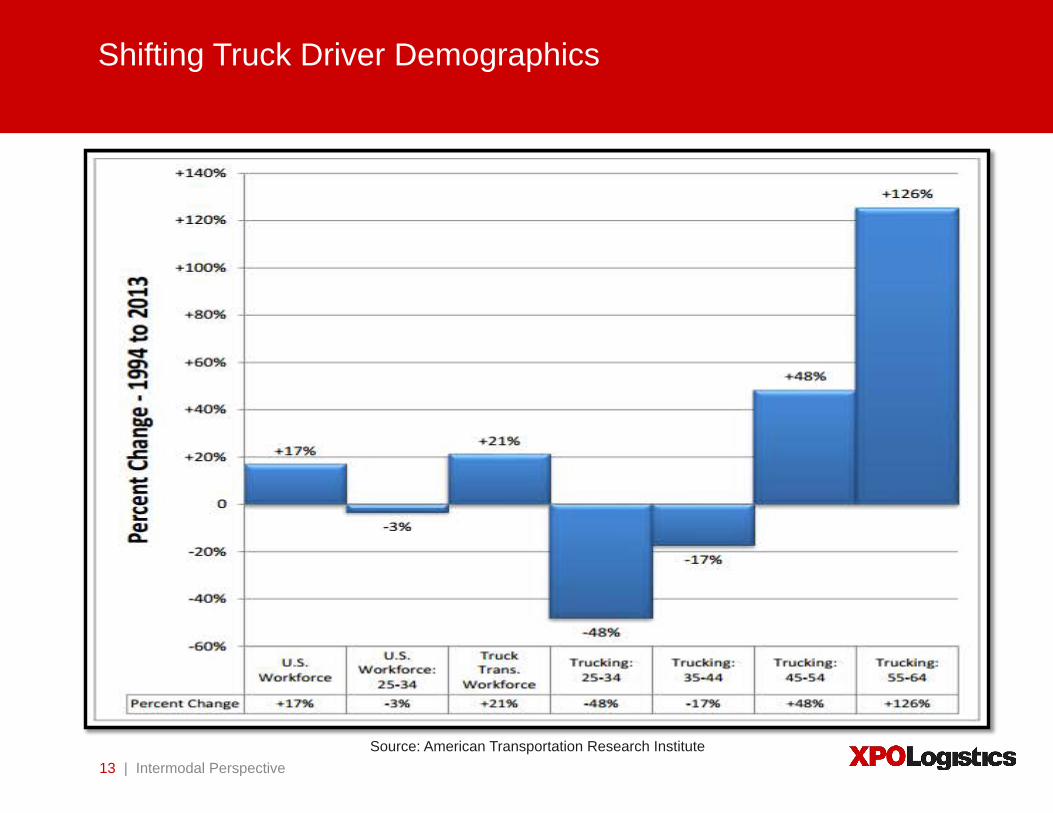

Shifting Truck Driver Demographics

| Intermodal Perspective 13 Source: American Transportation Research Institute

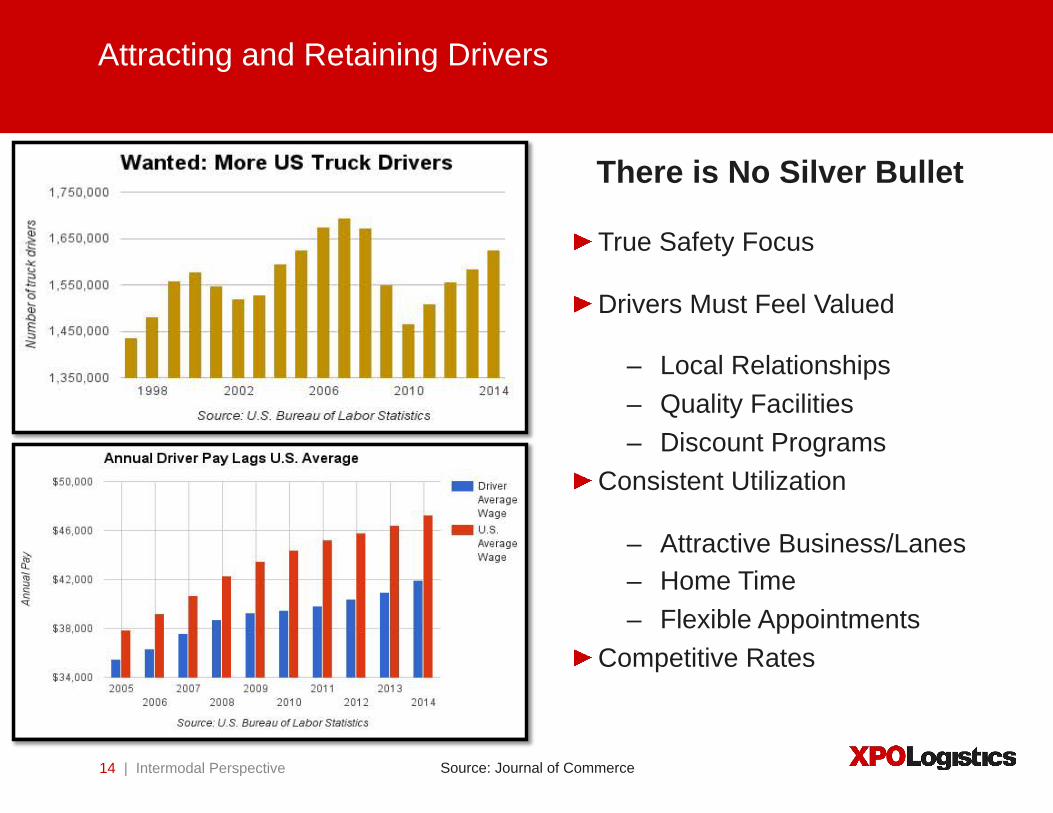

Attracting and Retaining Drivers

! True Safety Focus

! Drivers Must Feel Valued

– Local Relationships – Quality Facilities – Discount Programs

! Consistent Utilization

– Attractive Business/Lanes – Home Time – Flexible Appointments

! Competitive Rates

There is No Silver Bullet

| Intermodal Perspective 14 Source: Journal of Commerce

Container and Chassis Capacity

Container

• Variability in rail service has resulted longer terminal dwell

• Longer rail transits and slow turn times result in need for more containers

• Overall volume increases consuming more capacity

• Disruptions in network flows making it more difficult to provide planned capacity

Chassis

• Increase in terminal dwell causing more wheeled units to sit longer

• Misalignment of chassis demand and supply

• Steamship lines leaving chassis ownership

• Challenges with pool chassis maintenance

• More interest from shippers to develop a long-term dedicated chassis program

| Intermodal Perspective 15

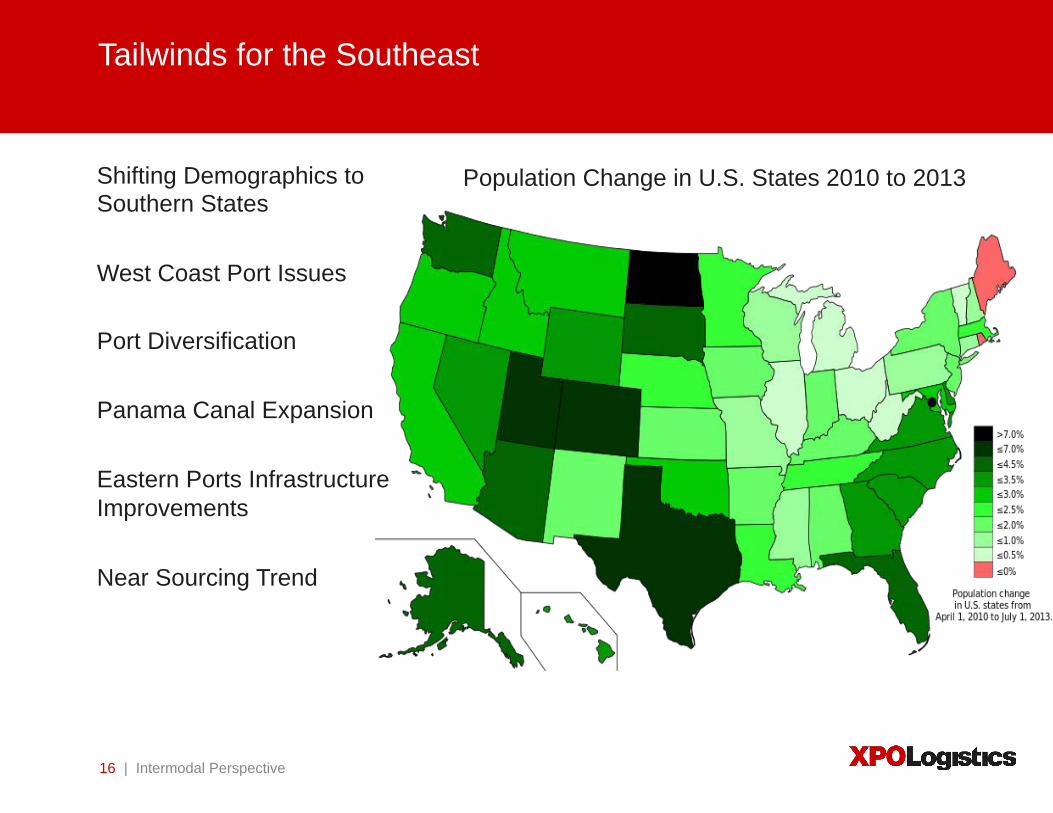

Tailwinds for the Southeast

Shifting Demographics to Southern States West Coast Port Issues Port Diversification Panama Canal Expansion Eastern Ports Infrastructure Improvements Near Sourcing Trend

| Intermodal Perspective 16

Population Change in U.S. States 2010 to 2013

Thank You

| Intermodal Perspective 17