Embed Size (px)

Citation preview

OFFICES INDUSTRIAL

RETAIL LEISURE

INVESTMENTRESIDENTIAL

DEVELOPMENT LAND

5YEARS OF ANALYSIS

DEMANDSUPPLYHEADLINE RENTPRIME YIELDS

SOUTH WEST OF ENGLAND & SOUTH WALES

Market Monitor

Contents

2 Welcome

3 Acrosstheregion

5 Bath

7 Bristol

9 Cardiff

11 Exeter

13 Gloucester

15 Newport

17 Plymouth

19 Swansea

21 Swindon

23 Taunton

25 Truro

27 Yeovil

29 Aserviceoverview

AlderKingMarketMonitor20141

Welcome to the 2014 edition of Market Monitor.

This report provides a review of the commercial property market in the South West of England and Wales over the past 12 months, with data, trends and market analysis on 12 key regional centres.

After a year of steady GDP growth and improved confidence, particularly in the manufacturing, construction and service sectors, prospects for the region’s occupier market are at their most optimistic since the downturn began in 2008.

As forecast in last year’s Market Monitor, stronger office and industrial take up combined with a greater shortage of new well-specified space led to a return of speculative development in 2013, the first for over four years. Two high profile office schemes are now underway in Bristol city centre, both of which could push rental levels over the £27.50 per sq ft mark. There are also speculative industrial schemes underway in Bristol, Gloucester, Wellington, Bridgwater and Newquay.

The region’s retail sector benefits from continued investment, with new retail schemes either in the pipeline or recently completed in Swindon, Gloucester, Exeter, Plymouth, Newport, Swansea, Taunton and Yeovil.

Together with a resurgent residential land market and strengthening investor confidence in the regions, we expect to see improving occupier demand and an increasing level of development and investment activity in 2014.

Simon Price, Head of Agency at Alder King

100 Temple Street, Bristol.

2www.alderking.com

Industrial

Offices

Across the region

(sqm)sqft

occupational summary

• Takeupin2013decreasedonthepreviousyearinallbutCardiff,Gloucester,Taunton,YeovilandTruro,withalackofgoodqualitysupplybeingaconstrainttoactivityintheothercentres.

• Supplycontinuedtofallacrosstheregion,withtheexceptionofGloucesterwheretherewasanincreaseasaresultofSuperGroup’srelocation.

• SupplyinBristolisnowatitslowestlevelfor10years.

• Demandisincreasinglyfocusedonbetterspecifiedspace,withnewbuildactivitycurrentlyunderwayinBristol,Gloucester,Wellington,BridgwaterandNewquay.

• Withanimprovingnumberofmediumsizedrequirements,occupiersareincreasinglyonlyabletosatisfytheirneedsviathedesignandbuildroute.

• Withthelackofsupplyandrisinglevelsoftakeup,particularlyinthedemandtriangleofBristol,Gloucester,SwindonandTaunton,weanticipatefurtherspeculativeactivity.

• Theoverallreductioninsupplyisalreadyresultinginreducedincentivelevelsinsomelocationsandtheprospectsforrentalgrowthareimproving.

officeheadlinerent£psf

industrialheadlinerent£psf

0

10

8

6

4

2

rent

occupational summary

• 2013sawincreasedofficetakeupinBristol,Exeter,Gloucester,SwindonandYeovil.

• Aspredictedlastyear,2013alsosawthereturnofspeculativeofficedevelopmentincentralBristolwithbothSkanskaandSalmonHarvestercommencingmajornewdevelopments.

• TheintroductionofPermittedDevelopmentRightshasalreadyresultedinasignificantlevelofproposalsforconversionofsecondaryofficebuildingstoresidentialuse.

• ThepositiveimpactofthesePDRproposalsislikelytobetwo-fold:reducingthesupplyofpoorerquality,secondhandspaceandpushingmoreoccupiersintothemarket.

• Theoverallreductioninsupplyisalreadyresultinginreducedincentivelevelsinsomelocationsandtheprospectsforrentalgrowthareimproving.

Simon Price T 0117 317 1084 E [email protected]

Andrew Ridler T 0117 317 1071 E [email protected]

(16

1)15

(18

8)

17.5

Swin

don

0

30

25

20

15

10

5

intown outoftown

Glouc

este

r

(124

)11

.5 (18

8)

17.5

Bath

(226

)21

Bristo

l

(29

6)

27.5

(231

)21

.5

Newpo

rt

(172

)16

(129

)12

Cardi

ff

(237

)22

(129

)12

Swan

sea

(15

6)

14.5

(116

)10

.75

Taun

ton

(18

3)

17(1

78)

16.5

Yeov

il

(14

0)

13(1

40

)14

Trur

o

(118

)11

(9

1)8

.5

Exete

r

(178

)16

.5(1

88

)17

.5

Plymou

th

(12

)15

(16

7)

15.5

Swin

don

(73

)6

.75

Glouc

este

r

(65

)6

Exete

r

(75

)7

Bath

(81)

7.5

Bristo

l

(81)

7.5

Newpo

rt

(43

)4

Cardi

ff

(54

)5

Swan

sea

(45

)4

.2

Taun

ton

(75

)7

Yeov

il

(70

)6

.5

Trur

o

(75

)7

Plymou

th

(64

)5

.95

AlderKingMarketMonitor20143

Retail Market Summary Residential Development Land

zoneAheadlinerent£psf

0

100

50

300

250

200

150

outoftownrent£psf

0

20

10

50

40

30

Swin

don

(30

1)2

8

Bath

(377

)30

Bristo

l

(377

)30

Cardi

ff(3

23)

30

Swan

sea

(377

)35

Taun

ton

(20

5)

19

Yeov

il

(24

8)

23

Newpo

rt

(26

9)

25

Exete

r

(30

1)2

8Glo

uces

ter

(26

9)

25

Plymou

th

(?)

20.5

Trur

o

(215

)20

• FollowingaperiodofimprovingGDPgrowthandanincreaseinconsumerspending,thelatterpartof2013sawacautiouslevelofconfidencereturntotheretailsector.

• Primerentallevelshavegenerallystabilisedacrosstheregionandtherearereasonableprospectsforgrowthinsomecentresduringthecourseof2014.Goodlevelsofdemandremainforprimelocationsinlargertownandcities.Selectivedemandhasreturnedtogoodsecondarylocations.

• Followingseveralyearsofnodevelopment,2013sawthecompletionofanewleisuredevelopmentatStStephen’sPlace,Trowbridge.In2014,themixedretailandleisureRegentCircusdevelopmentinSwindonwillopenandproposalsforthedeliveryoftheFriarsWalkShoppingCentreinNewportin2015areprogressing.

• Thefood-storesectorremainsveryactivebothinandoutofcentre.Thebigfiveoperatorscontinuetodriveexpansionthroughtheirconvenienceformatsandsizerequirementsforlargerformatstoreshavegenerallyreduced.

• Inmostlocations,discounterscontinuetodominatedemandforboththefoodandnon-food,withAldi,Lidl,B&M,Poundlandand99pStoresactivethroughouttheregion.

• TheleisuresectorcontinuestothrivebothinandoutofcentreandA3operatorsareprovingawelcomeadditiontothetenantmixinmanyestablishedshoppingcentresandretailparks.2013hasalsowitnessedconsiderablegrowthindemandfromthebudgetgymoperators.

Development land market summary

• 2013wasthemostactiveresidentialdevelopmentlandmarketinrecentyears.Housebuildingwasatitshighestlevelforadecade,withhousepriceshittingarecordhigh,fuellingdeveloperdemandfornewopportunities.ThispositivechangeinsentimentwasstimulatedbyGovernmentinitiativesmakingavailableupto95%LTVmortgages.

• Asanticipatedinlastyear’sMarketMonitor,demandforwell-locatedqualityresidentialdevelopmentlandisoutstrippingsupplywithconsequentupwardpressureonlandvalues.Consented,fullyservicedsitesingoodlocationsarenowregularlyexceeding£1millionpernetdevelopableacre.

• Thereismuchactivityongreenfieldlandontheperipheryofcities,townsandvillages.Sitesrangingfromfiveto200acresareinshortsupplyandourResidentialDevelopmentteamhasbeenverybusyadvisinglandowneranddeveloperclientsonConditionalContracts,Options,PlanningPromotionAgreementsandJointVentures.

• Housebuildersarere-enteringthehighdensitycitycentremarketandweanticipatemoresmallandmediumsizedapartmentschemesin2014.Wehavealsoreceivedinstitutional-backed,deliverableproposalsoncitycentresitesforhigh-densityPrivateRentalSchemes(PRS)whichareprogressing.

• TherehasbeenaverypositivereactiontotheGovernment’srelaxationofPermittedDevelopmentRights,enablingchangeofusefromofficestoresidential.InBristolalone,circa0.5millionsqftofdevelopmentisinthepipeline.

• Withahugeamountofconstructioncapacitylostsince2007,coupledwithanupturninconstructionactivity,materialandlabourcostsarebeginningtorise.Anydifferentialbetweenconstructioncostsandhousepriceswillimpactdirectlyonlandvalue.Currently,theequationisinequilibrium.

• Demandremainsstrongintheretirement,careandstudentmarkets.

Charles Russell-Smith T 0117 317 1043 E [email protected]

Chris HaworthT 0117 317 1042E [email protected]

Investment

investment market summary

• Increasedconfidenceinasustainedeconomicrecoveryandrenewedactivityintheoccupierleasingmarkethasledtotheregionalcommercialinvestmentmarketgaininginstrengththroughout2013,mostnotablyinthefinalquarter.

• Strongestdemandhasbeenforprimeorindex-linkedincomestreamsbut,withsupplyconstrained,thishasledtoimprovementsforsecondaryassets,asinvestorsbecomemorewillingtoacceptincreasedriskintheirhuntforimprovedreturns.

• InvestmentintheSouthWestandSouthWalesisdominatedbyUKinvestorsbutthereisoverseasinterestinprimetrophyassets.Allassettypeshavebenefitedwiththestrongestdemandforregionaloffices,industrialandalternativesectorsincludinghotels,studentaccommodationandhealth.EarlyinterestinthePrivateResidentialSectorisalsogainingmomentum.

• RelaxationofPermittedDevelopmentRightshasseenstrongdemandforsecondaryofficeswithpotentialforalternativeresidentialorstudentuseandthistrendwillcontinueinto2014.

• Barringunforeseeneconomicshocks,weexpecttoseethesetrendscontinueinto2014,withstrongdemandacrossallassettypesforprimeandsecondaryproperties.Yieldswillcontinuetohardenasdemanddeepensandevidenceofrentalgrowthisconfirmed.

valueofinvestmenttransactions£ms

John Benson T 0117 317 1100 E [email protected]

Bath

Bristo

l

Cardi

ff

Exete

r

Glouc

este

r

Newpo

rt

Plymou

th

Swan

sea

Swin

don

Taun

ton

Trur

o

Yeov

il

0

350

300

250

200

100

50

150

41.6

16.6

349

.64

21.4

5

123.

98

131.

33

52

.85

67.

18

319

9.6

3

8.8

7 42

.75

(1,6

15)

150

Swin

don

(1,0

76)

100

Glouc

este

r

(2,15

3)

200

Bath

(2,15

3)

200

Bristo

l

(Cab

ot C

ircus

)

(59

2)

55

Newpo

rt

(2,4

22)

225

Cardi

ff

(1,0

76)

100

Swan

sea

(59

2)

55

Yeov

il

(2,15

3)

200

Exete

r

(1,6

15)

150

Plymou

th

(1,18

4)

110

Trur

o

Taun

ton

(96

8)

90

4www.alderking.com

Bath

Industrial

Offices

(sqm)sqft

Simon Price T 0117 317 1084 E [email protected]

Andrew Ridler T 0117 317 1071 E [email protected]

demand

• Theupturninoccupierdemandwitnessedin2012continuedinto2013withanotherstrongyearoftakeup.Atthebeginningof2014,anumberoflargeenquiriesareactivelyseekingspaceinthecitycentre.

• Thelargestdealsoftheyearincludedtheacquisitionof14,000sqft(1,300sqm)byBritishMaritimeTechnologyatPlymouthHousetogetherwiththesaleofLawrenceHouse,LowerBristolRoadcomprising16,577sqft(1,540sqm).

• Onceagainmostactivityinthemarketcamefromtheservicesandprofessionalservicessectors.TheTMTsectoralsocontinuestogrow.

supply

• TotalavailabilitywithinBathreducedfurtherduring2013to240,000sqft(22,296sqm).

• WithnonewGradeAspacecurrentlyunderconstructioninthecity,themajorityoftheavailablespaceisofaperiodcellularnatureandnotcapableofmeetingoccupierdemandforflexibleopenplanaccommodation.

• Thesupplypictureissettotightenfurtherduring2014asanumberoftheavailablebuildingsarecurrentlythesubjectofproposalsforalternativeuses,mostcommonlyforhotel,studentandprivateresidentialuses.

headline rent

• Thebestheadlinerentachievedduring2013matchedthelevelsetin2012at£21.00psf(£226psm).

• AnyfurtherrentalgrowthatthetopendofthemarketislikelytobehamperedintheshorttermbythelackofavailableGradeAspaceinthemarket.

• Thegeneralreductioninavailabilityinthemarketisalreadyresultinginareductioninincentivelevelsbeingofferedtosecureoccupiers.

demand

• Goodfreeholdowneroccupierdemandremainsalbeitwithlimitedopportunities.

• Thelackofgoodqualitymodernspaceisholdingbacktakeup.

• Thereisincreasedinterestinthecityfromtradeandroadsideusesbutagainfewsuitableopportunities.

supply

• Nospeculativeindustrial/distributiondevelopmenthastakenplaceinBath.

• Thereisanegligibleamountofgoodqualitystockandtheshortageofmodernspaceissettocontinue.

headline rent

• Asaconsequenceofthelackofsupply,headlinerentallevelshaveincreasedto£7.50psf(£80.73psm).

Alder King Market Monitor 20145

demand000ssqft

50

0

100

125

150

2010 2011 2012 2013

75

25

2009

65(6)

65(6)

92(8.5)

82(8)68

(6)

supply000ssqft

200

0

400

500

600

2010

2011 2012 2013

2011 2012 2013

300

100

255(24)

350(33)

360(33) 305

(28)240(22)

2009

headlinerent£psf

15

0

20

2010 2011 2012 2013

2011 2012 2013

10

2009

5

(215

.27

)20

(215

.27

)20

(19

9.13

)18

.5

(226

)21

(226

)21

demand000ssqft

10

0

20

25

30

15

5

headlinerent£psf

4

0

8

10

6

2

2009 2010

(69

.96

)6

.5

(64

.58

)6

(67.

28)

6.2

5

(75

.34

)7

(81)

7.5supply000ssqft

20

0

40

50

70

30

10

2009 2010

60 65(6)

50(5)

30(3)

30(3)

20(2)

citycentre

20(2)

20(2)

25(2.3)

7.5(0.7)

15(1)

2009 2010 2011 2012 2013

1. Little SouthGate, Bath. Courtesy of SouthGate Limited Partnership.

2. CGI of Saw Close, Bath. Courtesy of Deeley Freed/Aaron Evans.

Investment

Retail & Leisure Charles Russell-Smith T 0117 317 1043 E [email protected]

John Benson T 0117 317 1100 E [email protected]

1 2

zone A headline rent

• Duringthecourseof2013,TKMaxxopenedanewstoreinHighStreetandCotswoldOutdooropenedinAbbeygate.

• BHSannouncedthatitwillcloseinJanuary2014.ItisunderstoodthatPrimarkwillopenanewstoreinthepremisesfrommid-2014.

• AnthropologieisbelievedtohaveagreedtermstooccupytheformerHabitatstoreinNewBondStreet.

• InthepopularsuburbofTwerton,MorrisonshasopeneditsfirstLocalstore.

out of town rent

• OnLowerBristolRoad,LidlhasconfirmedthatitwillshortlysubmitanewplanningapplicationonbehalfoftheformerHermanMillersite.Acornfieldhasannouncedthatitwillcommenceconstructionoftworetailunitsontheremainderofthesiteinearly2014.

• TheSecretaryofStatehasrefusedTesco’sappealformixedusedevelopmentontheformerBathPresssite.

• Sainsbury’shaswithdrawnitsapplicationforanewfoodstoreonthecurrentHomebasesiteatWesternRiverside.

leisure headline rent

• TheformerBeauNashpubonMilsomStreetistoreopenasaMiller&Cartersteakhouse.

• Elsewhereinthecity,PrezzohasopenedintheVaultsandtheStableinGeorgeStreet.Bill’shasopenedinCheapStreet.

• DeeleyFreedhassubmittedaplanningapplicationforthedevelopmentofacasino,148bedhotelandtworestaurantsatSawClose.Thedevelopmentisanticipatedtoopenin2016.

• TheCouncilhasannouncedproposalstotransformGrandParadeandtheUndercroftintoanexclusivediningquarter,includinguptothreenewupmarketrestaurants.

value of investment transactions

• ThetotalvalueofinvestmenttransactionsinBathin2013was£123.98m,asignificantincreasefromthepreviousyearandthehighestlevelinthelastsixyears.Aconsiderableproportionofthistotalwasfromonetransaction-thesaleofaninterestintheSouthGateretailcentre.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7%

- Office 7%

- Retailhighstreet 5.5%

- Retailoutoftown 6%

investment by sector

• ThelargesttransactioninthecitywasMultiSouthGate(LP)’ssaleofits50%shareintheSouthGateretailcentretoBritishLandfor£101m.Thecentrehas55retailunits,14leisureunits,acarparkand25,000sqftofficespace.

• TherewerelimitedindustrialinvestmenttransactionsinBath.Onenotabledealwasthesaleofthemulti-letWansdykeBusinessCentrefor£1.2m(NIY10.24%).

• AnothersignificantinvestmentdealwasthesaleoftheTravelodgeonRossiterRoadfor£11.2m(NIY9%)toLaSalleInvestmentManagement.

2

6www.alderking.com

50

100

125

150

175

75

25

zoneAheadlinerent£psf

150

0

250

300

2011 2012 20132010

200

100

2009

50

(2,5

29.4

2)

235

(2,6

90

.88

)25

0

(2,4

21.9

0)

225

(2,4

21.9

0)

225

(2,15

3)

200

outoftownrent£psf

20

0

40

60

2010 2011 2012 2013

30

10

2009

50

(430

.54

)4

0

(430

.54

)4

0

(430

.54

)4

0

(376

.72

)35

(323

)30

leisureheadlinerent£psf

0

5

10

15

30

2010 2011 2012 20132009

cinema health&fitness A3/A4

25

20

(139

.93

)13

(10

7.6

4)

10(2

69

.09

)25

(139

.93

)13

(96

.87

)9

(322

.91)

30

(139

.93

)13

(15

0.6

9)

14

(15

1)14

(96

.87

)9

(96

.87

)9

(118

)11

(33

4.4

5)

32

(376

.72

)35

(377

)35

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

27.8 25 22.5

37.57

123.98

5

3

7

8

6

4

investmentbysector

2009 2010 2011 2012 2013

primeyields%

industrial

office

retailhighstreet

retailoutoftown

1%

industrial

retailhighstreet

other90%

9%

Bristol 1

Industrial

Offices

(sqm)sqft

Simon Price T 0117 317 1084 E [email protected]

Andrew Ridler T 0117 317 1071 E [email protected]

demand

• 2013sawoccupierdemandreboundstronglyfollowingapooryearin2012.Inparticularthecitycentreperformedwellwithdemandbeatingthefiveyearaverage.

• MajordealsduringtheyearincludedBristolCityCouncil’sacquisitionof130,000sqft(12,077sqm)at100TempleStreetandImperialTobacco’sdevelopmentofanew85,000sqft(7,897sqm)HQatWinterstokeRoad.

• Severallargepre-letenquiriesarenowactiveinthemarket,particularlyfromthefinancialservicesandprofessionalservicessectors.

supply

• Inthecitycentre,lessthan260,000sqft(24,154sqm)ofnewGradeAspaceisnowimmediatelyavailable,withlessthan30,000sqft(2,787sqm)availableinnorthBristol.

• TwonewspeculativeGradeAdevelopmentsarenowunderconstructioninthecitycentrewithSkanskaonsitewith61,000sqft(5,667sqm)at66QueenSquareandSalmonHarvester/NFUMwith98,500sqft(9,151sqm)at2GlassWharf,TempleQuayCentral.

• ThechangesinPermittedDevelopmentRightsarealreadyresultinginproposalstoconvertasignificantamountofpoorersecondhandofficespacetoresidentialuse.

headline rent

• ThebestheadlinerentsagreedonnewGradeAaccommodationinboththecitycentreandnorthBristolmarketsremainedsteadyatthesamelevelsachievedin2012.

• IncentivelevelsforthebestremainingnewGradeAspacearelikelytoreduceduring2014assupplytightens.

• TheprospectsforincreasesinGradeAheadlinerentallevels,especiallyinthecitycentre,areimproving.

demand

• Thereisarealshortageofgoodqualitystock,particularlymodernspace,whichimpactedontakeupinthesecondhalfof2013andisholdingbackactivity.

• Therehasbeenareturnofmid-rangerequirementsinthe25,000–75,000sqft(2,323–6,968sqm)sizerangewithlimitedavailability.

• SignificantdealsincludeCulina’sleaseholdacquisitionof211,000sqft(19,603sqm)oftheCrossflow550BuildingandArla’s115,000sqft(10,684sqm)atDC115,bothonCabotPark,Avonmouth.

supply

• Supplyisata10yearlowandlargelycomprisespoorqualitysecondhandspace.

• WebelievethereisrealpotentialfordesignandbuildactivityasevidencedbyWBC’sacquisitionof20,000sqft(1,858sqm)inWarmley.

• Thecity’sfirstspeculativeindustrial/distributiondevelopmentcomprisingfiveunitstotalling15,000sqft(1,394sqm)isduetostartatCaxtonBusinessPark,Warmley.

• Owneroccupierscontinuetoseekgoodfreeholdopportunitiesbuthavealimitedchoice.

headline rent

• Thereisnonewspaceimmediatelyavailable,andweanticipatethatrentalsofcirca£7.75psf(£83.40psm)couldbeachievedforaccommodationbelow10,000sqft(929sqm).

• Rentsformodernandmid-rangebuildingsremainat£6.50psf(£70psm).Goodqualitysecondhandbuildingsarecommandingrentsofaround£4.75-£5.50(£51.11-£59.18psm).

• Withthereducedlevelsofgoodqualityavailablestock,rentalincentivesforprimespacearebeginningtoreduceandleasedurationsareextending.

Alder King Market Monitor 20147

2010 2011 2012 2013

demand000ssqft

400

0

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013

600

200

2009

594(55)

860(80) 700

(65)658(61)

735(68)

supply000ssqft

1,000

0

2,000

2,500

3,000

3,500

4,000

1,500

500

2009

1,900(177)

2,350(218)

2,650(246)

2,550(237) 2,380

(221)

headlinerent£psf

15

0

25

30

2010 2011 2012 2013

20

5

2009

10

(29

0.6

1)2

7

(29

6)

27.5

(29

6)

27.5

(29

6)

27.5

(29

6)

27.5

(215

.27

)20

(226

.03

)21

(226

.03

)21

(231

)21

.5

(231

)21

.5

citycentre outoftown

demand000ssqft

1,000

0

2,000

2,500

3,000

3,500

2010 2011 2012 2013

1,500

500

2009

2,100(195)

2,400(223)

2,400(223)

2,325(216)

2,200(204)

supply000ssqft

2,000

0

3,000

4,000

5,000

7,000

2010 2011 2012 2013

1,000

2009

6,000

headlinerent£psf

3

0

5

8

2010 2011 2012 2013

4

2

2009

1

6

7

(80

.73

)7.

5

(80

.73

)7.

5

(80

.73

)7.

5

(81)

7.5

(83.

42

)7.

75

5,500(511)

4,500(418)

4,500(418)

3,750(348)

2,750(255)

1. 2 Glass Wharf, Bristol. Courtesy of Salmon Harvester Properties/NFUM.

2. 66 Queen Square, Bristol. Courtesy of Skanska Property Development.

3. The Mall at Cribbs Causeway, Bristol.32

Investment

Retail & Leisure Charles Russell-Smith T 0117 317 1043 E [email protected]

John Benson T 0117 317 1100 E [email protected]

zone A headline rent

• CabotCircuscontinuestoattractnewretailerstothecitycentre.VansopenedinthesummerandPull&Bearopeneda48,000sqftstore,itsfifthintheUK,inDecember.

• TheMallatCribbsCausewayhasre-shapeditsretailofferthroughanumberofrelocations.NewlettingsincludeSuperdry,JackWills,Lakeland,BoseandLinksofLondon.

out of town rent

• RedevelopmentoftheformerBigW&TJHughesstoreatAbbeyWoodShoppingParkisnearingcompletion.NewtenantswillincludeAsda,B&M,Frankie&Benny’s,Nando’sandCosta.

• AtthenearbyShieldRetailCentre,HomeBargainshaspre-let14,300sqft(1,328sqm).

• ThegrantofplanningconsenttoSainsbury’sattheMemorialStadiumisnowsubjecttoJudicialReview.

• Foodstoreactivityremainsstrong.Sainsbury’sisshortlytocommenceworksonanewstoreinPortishead.AnewWaitroseatChippingSodburyisnowtrading.

leisure headline rent

• CabotCircushasaddedtoitsexistingfoodandbeverageofferthroughtheintroductionofTGIFriday’sandWagamama.

• WhiteladiesRoadcontinuestoseegoodlevelsofactivity.TheformerRanchhasbeenlettoBe.InGroupandthepopularCowshedhasextendedintotheformerPictureHouse.

• FurtherafieldDominionCorporateTrust,theownersofYateShoppingCentre,isfinalisingproposalsforanewleisuredevelopmentcomprisingasixscreencinemaandsixrestaurants.

value of investment transactions

• ThetotalvalueofinvestmenttransactionsinBristolin2013was£319m.Thisissignificantlyhigherthanthe2012totalof£155m.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 6.75%

- Office 6.75%

- Retailhighstreet 6.75%

- Retailoutoftown 6%

investment by sector

• OneofthelargestindustrialtransactionsinBristolwasthesaleofadistributionwarehouseonWesternApproachlettoDSGRetailLtduntil2031.M&GPropertyacquiredthepropertyfor£23m(NIY7.13%).

• Therewasahighlevelofofficeinvestmentactivityinbothoutoftownandcitycentrelocations.ThesaleofPortwallPlacewasthelargestofficetransactionoftheyear.Termsofthedealwereconfidentialalthoughweunderstandthepropertyachievedclosetoitsaskingpriceof£53m(NIY6.9%).

• Asignificantretailandmixeduseinvestmenttransactionwasthesaleof15-33UnionStreetfor£8.6m(NIY9%).

8www.alderking.com

200

400

500

600

700

300

100

28%

4%

65%

zoneAheadlinerent£psf

0

50

150

250

350

2010 2011 2012 20132009

Broadmead TheMall CabotCircus

100

200

300

(2,0

45

.07

)19

0

(1,9

91.2

5)

185

(1,8

83.

70)

180

(1,8

83.

70)

175

(1,8

84

)17

4

(3,3

36.6

9)

310

(3,3

36.6

9)

310

(2,4

21.7

9)

225

(2,15

2.7

0)

200

(3,2

29.2

0)

300

(3,2

29.2

0)

300

(3,2

29)

300

outoftownrent£psf

20

0

40

50

2010 2011 2012 2013

30

10

2009

(430

.54

)4

0

(430

.54

)4

0

(376

.72

)35

(323

)30

(48

4.3

6)

45

leisureheadlinerent£psf

0

10

20

30

50

2010 2011 2012 20132009

cinema health&fitness A3/A4

40

(16

1.45

)15

(139

.93

)13

(26

9.0

9)

25

(16

1.45

)15

(139

.93

)13

(322

.91)

30

(16

1.45

)15

(139

.93

)13

(322

.91)

30

(16

1.45

)15

(16

1)15

(129

.16)

12

(129

)12

(322

.91)

30

(323

)30

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

262

349

49

2

155

.19

319

primeyields%

5

3

7

8

2012 20132011

6

4

20102009

investmentbysector

industrial

office

retailhighstreet

other industrial

office

retailhighstreet

retailoutoftown

(2,15

2.7

0)

200

(2,15

3)

200

(2,15

2.7

0)

200

3%

Cardiff 1

Industrial

Offices Owen Young T 029 2038 1996 E [email protected]

Owen Young T 029 2038 1996 E [email protected]

demand

• 2013sawa30+%reductioninoccupierdemandcomparedtothefiveyearaverageof443,000sqft(41,156sqm).Currentactivedemandexceeds350,000sqft(32,516sqm)

• Over80%ofdealswerelessthan5,000sqft(464.5sqm).50%wereout-of-town.

• NotabledealsincludedSouthWalesUniversitytaking21,958sqft(2,039sqm)atAtlanticHouseandHughJamesSolicitorstaking19,383sqft(1,800sqm)atHodgeHouse.

supply

• Supplydecreasedslightlyandcomprisesmainlysecondarystock.ItisarguablewhetheranyGradeAstockremainswithinthecitycentre.

• PotentialnewGradeAwilloccuratCapitalQuarter,CallaghanSquareandCentralStationwithmanyoftheopportunitiesinpublicsectorownership.

• Itispredictedthatover300,000sqft(27,871sqm)ofnewdevelopmentwillbecompletedbymid-2015.

headline rent

• Headlinerentwasmaintainedinthecitycentrewithlettingsat3AssemblySquaretoWelshLifeSciencesHub,WelshMinistersandITV.Futuredevelopmentschemeswilltestheadlinerents.

• LettingsatCardiffGatetoFosterCareAssociatesandJDHullmaintainedoutoftownheadlinerents.

• Reduceddemandhasnotaffectedincentivesbutweexpectthemtotightenin2014.

demand

• Afteraslowstarttothefirsthalfof2013,occupierdemandstrengthenedtorecordaslightincreasecomparedtothefiveyearaverage.

• Over90%ofdealswerelessthan10,000sqft(929sqm).

• Notabledealsincludedthelettingof38,000sqft(3,530.3sqm)atTridentParctoGSSand27,000sqft(2,508sqm)atParcTyGlastoRampworldCardiff.

supply

• Supplyremainedrelativelystaticwheresecondhandbuildingscomingtomarkethaveoffsetdemand.

• Stockprovidinglessthan10,000sqft(929sqm)accountsforapproximately76%oftotalavailability.

• 177,000sqft(16,444sqm)hasbecomeavailableatWentloogAvenue,formerlyoccupiedbyG24i.

headline rent

• £5psf(£53.82sqm)hasprevailedsince2011andisnotexpectedtoincreaseoverthenext12months.

• Ashortageofgoodqualitystockandaslightincreaseindemandshouldreflectinheadlinerentsincreasingforqualitystock.

• Otherinfluences,suchasthedelayintheratingrevaluation,willundoubtedlynothelpmorefragilesecondarylocations.

(sqm)sqft

Alder King Market Monitor 20149

demand000ssqft

0

200

300

400

500

600

700

2010 2011 2012 2013

100

2009

379(35)

437(41)

639(59)

380(35)

300(28)

supply000ssqft

400

0

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013

600

200

2009

1,214(113)

1,200(111)

1,200(111) 1,100

(102) 1,000(93)

headlinerent£psf

0

5

10

15

20

25

2010 2011 2012 20132009

citycentre outoftown

(226

.03

)21

(226

.03

)21

(215

.27

)20

(236

.81)

22

(237

)22

(16

1.45

)15

(15

0.6

9)

14

(139

.93

)13

(139

.93

)13

(129

)12

demand000ssqft

0

200

300

400

500

600

700

2010 2011 2012 2013

100

515(48)

516(48)

518(48)

572(53)

631(59)

2009

supply000ssqft

0

500

1,000

1,500

2,000

2010 2011 2012 20132009

2,043(190) 1,894

(176)

1,467(136) 1,368

(127)

1,986(184)

headlinerent£psf

0

2

3

4

5

6

7

2010 2011 2012 2013

1

2009

5.5(59.20)

5.5(59.20) 5

(53.82)5

(53.82)5

(54)

1. Alder King offices at 18 Park Place, Cardiff.

2. 380 Newport Road, Cardiff.

3. The Levels Industrial Park, Cardiff.2 3

Investment

Retail & Leisure Owen Young T 029 2038 1996 E [email protected]

John Benson T 0117 317 1100 E [email protected] Owen Young T 029 2038 1996 E [email protected]

zone A headline rent

• StDavid’sShoppingCentrecontinuestodominatecitycentretradingespeciallywithfashionretailers.DespitetheclosureofGillyHicks,mostofthe1.4msqft(130,064.2sqm)Centreisnowoccupied.

• QueenStreetremainspopularasaretailandleisurelocation,asevidencedbytherecentrelocationofSpecsaversandthenewdevelopmentofPrimarkattheformerBHSpremises.

out of town rent

• CardiffGateandLeckwithRetailParksarefullyoccupiedattopachievablerents.

• NewportRoadcontainsthelargestmassofretailstoresinthecitybuthasbecomemoresecondaryevenwithanewMorrisonssuperstore.Notabletransactionsin2013includedB&MBargainstakingtheformerKwikSaveandHomeBargainsoccupyingthelastunitsatAvenueRetailPark.

leisure headline rent

• Mitchells&ButlerswillbetakingthegroundflooroftheformerHabitatbuildinglocatedinTheHayes,reinforcingtheleisureofferadjoiningStDavid’sCentre.

• BudgetgymscontinuetothriveasevidencedbythelettingoftheformerPorcelanosaunitonNewportRoadtoTheGymGroup.

value of investment transactions

• ThetotalvolumeofinvestmenttransactionsinCardiffincreasedby67%onthe2012figures,risingfrom£78.43mto£131.33m.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7.25%

- Office 7%

- Retailhighstreet 5.5%

- Retailoutoftown 6%

investment by sector

• ThelargestretailinvestmenttransactioninCardiffwasablockonQueenStreetwhichwasboughtbyNFUMutualfor£45.5m(NIY4.7%).TenantsincludeZara,TopshopandRiverIsland.

• AnothersignificanttransactionwasthesaleofHelmontHousefor£23.15m(NIY8%).Thepropertycomprisesa60,000sqftmulti-letofficeanda200bedPremierInnhotel.

• AleisurecomplexonMaryAnnStreetwithtenantsincludingCineworldandGalaCasinosoldfor£18.96m(NIY6.9%).

10www.alderking.com

1%

15%

60

120

150

180

210

90

30

zoneAheadlinerent£psf

0

200

300

400

500

600

2010 2011 2012 20132009

100

outoftownrent£psf

25

0

35

40

2010 2011 2012 2013

30

20

2009

15

10

5

(376

.72

)35

(322

.91)

30

(322

.91)

30

(322

.91)

30

(323

)30

leisureheadlinerent£psf

0

10

20

30

60

2010 2011 2012 20132009

cinema health&fitness A3/A4

40

50

(16

1.45

)15

(139

.93

)13

(322

.91)

30

(139

.93

)13

(139

.93

)13

(10

7.6

4)

12

(10

7.6

4)

12

(322

.91)

30

(322

.91)

30

(139

.93

)13

(322

.91)

30

(14

0)

13(1

18)

11

(431

)4

0

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

174.4

129.6

204.36

78.43

131.33

primeyields%

5

3

7

8

2012 2013

6

4

201120102009

investmentbysector

industrial

office

retailhighstreet

retailoutoftown

47%

36%

(3,

013

.78

)28

0

(2,

475

)23

0

(2,

422

)22

5

(2,

422

)22

5

(2,

69

0.8

8)

250

industrial

office

retailhighstreet

other

(118

.40

)11

Exeter

Industrial

Offices

(sqm)sqft

Noel Stevens T 01392 353093 E [email protected] Collison T 01392 353091 E [email protected]

Noel Stevens T 01392 353093 E [email protected] Collison T 01392 353091 E [email protected]

1

demand

• Therewassteadytakeupbothinandoutoftown.

• Therearethefirstsignsofoccupiersseekingbespokequalityspace.

• Manyoccupiershavere-negotiatedtheirexistingleaseterms.

supply

• Therehavebeennonewbuildstartsforthreeyears.

• Weexpectsupplylevelstohavepeaked.Theincreasesfrom2013aremadeupofsmallerstockratherthanlargebuildingsbecomingvacant.

• SeveralofficebuildingsarebeingconvertedtoresidentialunderPermittedDevelopmentRights.

headline rent

• ThelettingofEagleHousetoBlurGroupoffanaskingpriceof£17.50psfisalandmarkdealdemonstratingpotentialforviablenewbuild.

• Rentalsforsecondhandspacearestartingtoriseandincentivesreduced.

demand

• Inabsolutetermsdemandhalvedcomparedto2012.Howeverthe2012figurewasinflatedduetoa500,000sqft(46,452sqm)requirementfromasupermarket.Inrealtermsdemandisupon2012.

• TheAmbulanceSpecialOperationsCentreagreedtermsona22,000sqft(2,044sqm)buildingatSkyPark.

• AtMatfordGreen,VWagreedterms(subjecttoplanning)toleaseanew35,000sqft(3,252sqm)dealership.

• GeoPostisfinalisingtermsona60,000sqft(5,574sqm)leaseholdfacility.

supply

• Supplyremainsbroadlyinlinewithpreviousyears.

• ThereisagoodsupplyofservicedlandreadyfordevelopmentinprimelocationsaroundExeter.

• InfrastructureworkssuchastheClystHonitonBypasswhichopenedinOctober2013ishelpingtoimprovetransportlinksacrosstheregion.

• Wepredictspeculativedevelopmentwillreturntothemarketin2014.

headline rent

• Headlinerentswillmoveupto£7.00psf(£75.34psm)fornewbuildstockintheearlypartof2014.Thisisdrivenbydemandfornewstockandtheincreasingcostsofdeliveringqualitybuildings.

• Weexpecttoseeareductioninincentivesonexistingbuildingsin2014asthemarketimprovesandthedevelopmentpipelinelagsbehind.

Alder King Market Monitor 201411

demand000ssqft

50

0

100

125

150

175

200

2010 2011 2012 2013

75

25

2009

185(17)

150(14)

140(13)

100(9)

135(12)

supply000ssqft

100

0

200

250

300

400

450

2010 2011 2012 2013

150

50

2009

350

200(19)

215(20)

310(28.8)

350(33)

410(38)

headlinerent£psf

6

0

10

12

14

16

18

2010 2011 2012 2013

8

2

2009

4

citycentre outoftown

(177

.60

)16

.5

(177

.60

)16

.5

(177

.60

)16

.5

(177

.60

)16

.5

(177

.60

)16

.5

(178

)16

.5

(177

.60

)16

.5

(177

.60

)16

.5

(177

.60

)16

.5

(18

8)

17.5

demand000ssqft

200

0

400

500

600

700

800

2010 2011 2012 2013

300

100

2009

190(18)

200(19)

310(29)

600(56)

310(29)

supply000ssqft

200

0

400

500

2010 2011 2012 2013

300

100

2009

250(23)

390(36)

305(28)

300(28)

300(28)

headlinerent£psf

3

0

5

8

2010 2011 2012 2013

4

2

2009

1

6

7

(72

.65

)6

.75

(67.

27)

6.2

5

(64

.58

)6

(64

.58

)6

(75

.34

)7

Investment

Retail & Leisure Lee Southan T 01392 353090 E [email protected]

John Benson T 0117 317 1100 E [email protected] Scott Rossiter T 01392 353089 E [email protected]

3

1. Ambulance Special Operations Centre, SkyPark, Exeter. Courtesy of St Modwen.

2. CGI of Volkswagen Showroom, Matford Green, Exeter. Courtesy of Eagle One.

3. Exeter College Technology Centre, Exeter. Courtesy of Stride Treglown.2

zone A headline rent

• Exeter’sretailsectorremainsstrong,withlimitedvoidsfillingquickly.

• DemandagainbuckedtheregionaltrendinthecitycentrewithnewoccupiersincludingTheWhiteCompany,Saltrock,CoralandTwo-Seasonsaswellasahighnumberofnewindependentoperators.

• Rentsremainedstablewithincentivepackagesreducingassupplydiminishes.

out of town rent

• InOctober2013Ikeaannouncedplanstoopena£60mstoreontheoutskirtsofthecity.Ithassubmittedplanningpermissionandislookingtoopenin2015.

• Thecompletionofthe23,000sqft(2,137sqm)AlphingtonRetailParkprovedpopular,withthreeoutoffourunitscompletedorunderoffertonationalcovenants.

• SecondaryretailofferingsprovedstrongwithvoidsintheStThomasNeighbourhoodCentretransactingabovetheaskingrents.

• Discountretailer99pStorescontinueditsexpansion,completingontheD&BsiteatExeBridgeRetailPark.

leisure headline rent

• ThefoodandbeveragesceneinExetercontinuestotradewell.Newentrantsin2013includedCoteBrasserie,Bill’s,Lloyd’sKitchen,Brody’sBreakfastBistroandUrbanBurger.

• Demandfromgymoperatorscontinuedthroughout2013;findingsuitablestocktoaccommodatethemprovedproblematic.

• Planstoredevelopthecitycentrebusstationintoaleisureandretailschemearemovingeverclosertobeingfinalised.

value of investment transactions

• Thetotalvolumeofinvestmentactivityin2013was£52.85m.Thisisafallfromthelevelrecordedin2012,althoughthiswasimpactedbyasinglelargeretailwarehousetransaction.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7%

- Office 7.5%

- Retailhighstreet 6%

- Retailoutoftown 6%

investment by sector

• ThelargestofficetransactionwasthesaleofPeninsulaHousefor£17m(NIY6.75%).TheofficeislettoSouthWestWaterfor17years.

• AsignificantretailtransactionwasthesaleoftheHouseofFraserstoreinthecitycentrefor£7.15m(NIY6.5%).ThepropertyislettoHouseofFraseruntil2038andwaspurchasedbyCordeaSavills.

• TheAlphingtonRoadRetailParkwassoldfor£13.8m(NIY7.5%).ThethreepurposebuiltretailwarehouseunitsarelettoB&Q,IcelandandAldiwithanAWULTof9.75years.

12www.alderking.com

50

100

125

150

175

75

25

leisureheadlinerent£psf

0

10

20

30

50

2010 2011 2012 20132009

40

(18

2.9

9)

17

(18

3)

17

(86

.11)

8

(86

)8

(18

2.9

9)

17

(430

.54

)4

0

(431

)4

0

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

158.74

63.36

40.4252.85

82.03

primeyields%

5

3

7

8

2012 2013

6

4

201120102009

outoftownrent£psf

10

0

20

30

2010 2011 2012 2013

15

5

2009

25

(26

9.0

9)

25

(26

9.0

9)

25

(26

9.0

9)

25

(24

7.5

6)

23

(30

1)2

8

zoneAheadlinerent£psf

150

0

250

2010 2011 2012 2013

200

100

2009

50

(2,3

67.

97

)22

0

(2,15

2.7

0)

200

(2,15

2.7

0)

200

(2,15

2.7

0)

200

(2,15

3)

200

HighSt.

investmentbysector

industrial

office

retailhighstreet

retailoutoftown

cinema health&fitness A3/A4

(29

6)

27.5

(118

.40

)11

(86

.11)

8

(118

.40

)12

(86

.11)

8

(29

6)

27.5

(118

.40

)11

(86

.11)

8

industrial

office

retailhighstreet

retailoutoftown

other

9%

40%

22%

26%

2%

Gloucester 1

Industrial

Offices

(sqm)sqft

Adrian Rowley T 01452 627133 E [email protected]

Adrian Rowley T 01452 627133 E [email protected]

demand

• Overalltakeupwasuponthepreviousyear’sfigure.

• Significanttransactionsin2013includedthesaleofthe25,000sqft(2,323sqm)Building4CarterCourtatWaterwellsBusinessParkandthelettingofthe7,000sqft(650sqm)Building1250LansdowneCourtonGloucesterBusinessPark.

• Asinrecentyears,themajorityofactivityoccurredoutoftown.Howeveractivityinthecitycentrehasnowincreased.

supply

• Generallytheavailabilityofstockremainslow,particularlyforGradeAofficespace.

• Partlyasaresultoftheabove,itisanticipatedthattherewillberenewedactivityindesignandbuildopportunities.

headline rent

• Headlinerentsremainedconstantat£17.50psf(£188.36psm).

• Theshortageofstockcontinuestoapplyadownwardpressureonincentives.

demand

• Overalltakeupishigherthanthepreviousyear’sfigure.

• OfkeyimportanceisthenewbuilddevelopmentatQuedgeleyWestwheresome75,000sqft(6,968sqm)intwobuildingsisbeingbuiltforListerPetterandGardnerBros.

• Itisanticipatedthattherewillbefurtherdesignandbuildactivitycontinuingthrough2014inresponsetotheshortageofGradeAspace.

supply

• Generallytheavailabilityofstockremainslowinmostsectorsoftheindustrialmarket.

• Thetotalsupplyincreasedonlastyear’sfigureprimarilyduetothenewavailabilityoftwolargewarehousebuildingswhicharebeingvacatedbySuperGroup.

• Glenmorecommittedtotheregion’sfirstspeculativeindustrialdevelopmentforfiveyearswiththeconstructionofPhoenixHouseatWaterwellsBusinessPark.This21,900sqft(2,035sqm)developmentisdueforcompletioninJanuary2014.

headline rent

• Headlinerentsremainedconstantat£6.00psf(£64.59psm).

• Thereiscontinuedpressureonincentivesasmarketconditionsharden.

Alder King Market Monitor 201413

demand000ssqft

50

0

100

125

150

175

200

225

2011 2012 20132010

75

25

130(12)

200(19)

100(9)

95(9)

120(11)

2009

supply000ssqft

100

0

200

250

300

350

400

2010 2011 2012 2013

150

50

170(16) 150

(14)

250(23)

200(19)

120(11)

2009

headlinerent£psf

6

0

10

12

14

16

18

2010 2011 2012 2013

8

2

2009

4

(123

.78

)11

.5

(18

8.3

6)

17.5

(123

.78

)11

.5

(18

8.3

6)

17.5

(123

.78

)11

.5

(123

.78

)11

.5

(124

)11

.5

(18

8.3

6)

17.5

(18

8.3

6)

17.5

(18

8)

17.5

citycentre outoftown

demand000ssqft

200

0

400

500

600

700

2010 2011 2012 2013

300

100

2009

600(56)

400(37)

300(28) 275

(26)

300(28)

headlinerent£psf

2

0

4

5

6

7

2010 2011 2012 2013

3

1

2009

(64

.58

)6

(64

.58

)6

(64

.58

)6

(64

.58

)6

(65

)6

supply000ssqft

400

0

800

1,000

1,200

2010 2011 2012 2013

600

200

2009

400(37)

450(42) 350

(33) 275(26)

625(30)

1. 4 Carter Court, Waterwells Business Park, Gloucester.

2. Morrisons supermarket, Triangle Park, Gloucester. Courtesy of Gloucester Citizen.

3. CGI of Lister Petter’s new unit at Quedgeley West. Courtesy of St Modwen.2 3

Retail & Leisure John Hawkins T 01452 627135 E [email protected]

Investment John Benson T 0117 317 1100 E [email protected] Adrian Rowley T 01452 627133 E [email protected]

zone A headline rent

• TheopeningofthenewM&SonEastgateStreethasincreasedfootfalltothecitycentre.

• TheimminentarrivalofTKMaxxtothecoveredEastgateShoppingMallwillfurtherrejuvenatethecitycentre.

• TheCityCouncilhassignedanexclusivityagreementwithStanhopeonproposalsfortheKingsQuarterredevelopmentandadjacentbusstation.

out of town rent

• SignificantprogresshasbeenmadeatTriangleParkwherethenewMorrisonsstoreandpetrolstationisnowopenandtrading.Pre-lettermshavealsobeenagreedwithCostaCoffee.

• AtWhittleSquare,Barnardosisfittingoutanew2,000sqft(186sqm)storeleavingjusttwovacantunits.

• AtSt.OswaldsPark,WrenKitchenshasleasedhalfoftheformerCometstore,andplanningconsenthasbeengrantedforanewMcDonaldsrestaurantanddrive-through.

leisure headline rent

• AtGloucesterQuays,thenewCineworld10screencinemahasopened.

• ThenewcinemahasprovidedthecatalystforthearrivalofnewrestaurantsincludingChimichanga,Zizzi’sandEd’sEasyDiner.

• JDWetherspoonisalsoopeningintheDockshavingacquiredtheformerCootscaféoffLlanthonyWay.

• Withinthehealthandfitnesssector,demandremainsstrongfrombudgetgymoperatorswhocontinuetosearchfortherightopportunities.

value of investment transactions

• ThevolumeofinvestmentsalesinCheltenhamandGloucesterincreasedslightlyto£41.6m.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7%

- Office 7.5%

- Retailhighstreet 7%

- Retailoutoftown 6.25%

investment by sector

• Oneofthelargestindustrialtransactionsintheregionin2013wasthesaleofBamfurlongIndustrialEstateinCheltenham.Thepropertysoldfor£3.37m(NIY6.5%).Theyieldreflectedthegroundleasenatureoftheincome.

• TwyerHouse,Gloucesterwasboughtfor£9.65m(NIY7%)byGreenridgeCorporation.The1960sofficebuildingislettoHMLandRegistryuntil2067.

• ThemostsignificantretailwarehousetransactionwasthesaleofTheRangeunit,TewkesburyRoad,Cheltenhamfor£6.03m(NIY8%).ThepropertyislettoCDSsuperstoresInternationalLtduntilJune2020.

14www.alderking.com

zoneAheadlinerent£psf

75

0

125

150

175

2011 2012 20132010

100

25

2009

50

15

25

30

35

20

5

10

EastgateSt. KingsWalk

(1,4

53.

07

)13

5

(1,2

91.6

2)

120

(1,4

53.

07

)13

5

(1,2

91.6

2)

120

(1,0

76.4

0)

100

(1,0

76.4

0)

100

(1,0

76)

100

(1,0

76.4

0)

100

(1,0

76.4

0)

100

(1,0

76)

100

outoftownrent£psf

10

0

20

25

2010 2011 2012 2013

15

5

2009

(26

9.0

9)

25

(26

9.0

9)

25

(26

9.0

9)

25

(26

9)

25

(236

.80

)22

leisureheadlinerent£psf

0

2010 2011 2012 20132009

cinema health&fitness A3/A4

(129

.16)

12

(129

.16)

12

(129

.16)

12

(129

)12

(16

1.45

)15

(34

4.4

5)

32

(34

4.4

5)

32

(34

4)

32

valueofinvestmenttransactions£ms

30

0

60

75

90

105

2010 2011 2012 2013

45

15

2009

91.9

57.2

62.98

40.29 41.6

primeyields%

5

3

7

8

2012 2013

6

4

201120102009

investmentbysector

industrial

office

retailhighstreet

retailoutoftown

(118

.40

)11

(86

.11)

8

(16

1.45

)15

industrial

office

retailhighstreet

retailoutoftown

other

(10

7.6

4)

10

(96

.88

)9

(96

.88

)9

(97

)9

1%

50%

17%12%

20%

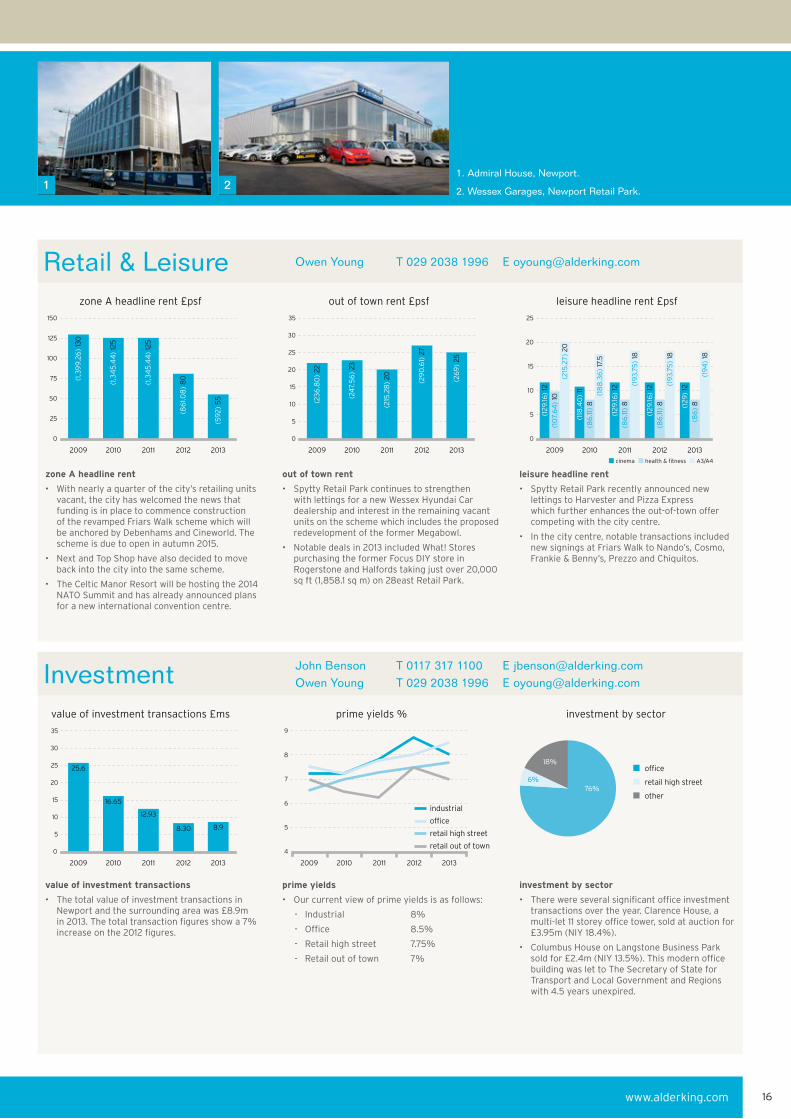

Newport

Industrial

Offices

(sqm)sqft

Owen Young T 029 2038 1996 E [email protected]

Owen Young T 029 2038 1996 E [email protected]

demand

• 2013takeupwashalfthatof2012and20%downonthefiveyearaverage.

• ThetrendisturningmoretowardsthecitycentreandawayfromfringelocationssuchasCelticSprings.Admiral’snewbuildingisnearingcompletionandshouldstimulatesomemuchneededactivityinthearea.

• OneofthelargesttransactionswasthesaleofShireHall,aresidentialconversioncomprising17,894sqft(1,662.4sqm).

supply

• Theamountofvacantspacereducedasaresultoflackofdevelopmentandcontinuedtakeupofsecondarystock.

• SimilartoCardiff,thereisarealshortageofGradeAstockinthecitycentre.

• Thenumberofresidentialconversionsisexpectedtoincreasereducingavailabilitystillfurtherin2014.

headline rent

• HeadlinerentwasmaintainedinthecitycentrewiththelettingtothePassportOfficeatNexusHouse.Thetransactionrepresentedthelargestlettingfortheyearat23,868sqft(2,217sqm).

• Outoftownrentshavesufferedwithamplequalityspaceavailableinseverallocations.

demand

• 2013sawareductioninoccupierdemandcomparedtothefiveyearaverageof575,000sqft(53,419sqm).

• Over90%ofdealswerelessthan10,000sqft(929sqm)withagrowingnumberoffreeholdsalesandrequirements.

• NotabledealsincludedthesaleoftheformerSPTSsiteatImperialParkcomprising89,500sqft(8,315sqft)toG24i.ReeveslandIndustrialEstatecontinuedtobeactivewiththelettingof52,000sqft(4,831sqm)toBisley.

supply

• Supplyfellby35%whencomparedtothefiveyearaverageandisdirectlyattributedtotakeupandalackofnewdevelopment.

• 76%ofstockcomprisesunitsoflessthan10,000sqft.Unitsofthissizeareprovingattractivetoowneroccupiers.

• Thereisalimitedsupplyofmodernqualityunitswherethetenantdemandremains.

headline rent

• Rentsremainedstaticin2013.

• Assupplydecreases,weexpectupwardspressureonrentallevelsonbetterqualitystock.

Alder King Market Monitor 201415

demand000ssqft

100

0

200

250

2010 2011 2012 2013

150

50

2009

43(4)

80(7)

172(16)

78(7)

99(9)

supply000ssqft

200

0

400

500

2010 2011 2012 2013

300

100

2009

340(32)

446(41)

460(43)

386(36) 345

(32)

headlinerent£psf

0

5

10

15

20

2010 2011 2012 20132009

citycentre outoftown

(172

.22

)16

(172

.22

)16

(16

1.45

)15

(172

.22

)16

(172

)16

(16

1.45

)15

(16

1.45

)15

(139

.93

)13

(139

.93

)13

(129

)12

demand000ssqft

200

0

400

500

600

700

800

900

2010 2011 2012 2013

300

100

2009

417(39)

407(38)

404(38)

652(61)

385(36)

supply000ssqft

0

500

750

1,000

1,250

1,500

1,750

2010 2011 2012 2013

250

2009

789(73)

1,080(100)

1,192(111)

1,104(103)

720(67)

headlinerent£psf

0

2

3

4

5

6

7

2010 2011 2012 2013

1

2009

4.5(48.44)

4.5(48.44) 4

(43.05)4

(43.05)4

(43)

1. Admiral House, Newport.

2. Wessex Garages, Newport Retail Park.

Investment

Retail & Leisure Owen Young T 029 2038 1996 E [email protected]

John Benson T 0117 317 1100 E [email protected] Owen Young T 029 2038 1996 E [email protected]

1 2

value of investment transactions

• ThetotalvalueofinvestmenttransactionsinNewportandthesurroundingareawas£8.9min2013.Thetotaltransactionfiguresshowa7%increaseonthe2012figures.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 8%

- Office 8.5%

- Retailhighstreet 7.75%

- Retailoutoftown 7%

investment by sector

• Therewereseveralsignificantofficeinvestmenttransactionsovertheyear.ClarenceHouse,amulti-let11storeyofficetower,soldatauctionfor£3.95m(NIY18.4%).

• ColumbusHouseonLangstoneBusinessParksoldfor£2.4m(NIY13.5%).ThismodernofficebuildingwaslettoTheSecretaryofStateforTransportandLocalGovernmentandRegionswith4.5yearsunexpired.

zone A headline rent

• Withnearlyaquarterofthecity’sretailingunitsvacant,thecityhaswelcomedthenewsthatfundingisinplacetocommenceconstructionoftherevampedFriarsWalkschemewhichwillbeanchoredbyDebenhamsandCineworld.Theschemeisduetoopeninautumn2015.

• NextandTopShophavealsodecidedtomovebackintothecityintothesamescheme.

• TheCelticManorResortwillbehostingthe2014NATOSummitandhasalreadyannouncedplansforanewinternationalconventioncentre.

out of town rent

• SpyttyRetailParkcontinuestostrengthenwithlettingsforanewWessexHyundaiCardealershipandinterestintheremainingvacantunitsontheschemewhichincludestheproposedredevelopmentoftheformerMegabowl.

• Notabledealsin2013includedWhat!StorespurchasingtheformerFocusDIYstoreinRogerstoneandHalfordstakingjustover20,000sqft(1,858.1sqm)on28eastRetailPark.

leisure headline rent

• SpyttyRetailParkrecentlyannouncednewlettingstoHarvesterandPizzaExpresswhichfurtherenhancestheout-of-townoffercompetingwiththecitycentre.

• Inthecitycentre,notabletransactionsincludednewsigningsatFriarsWalktoNando’s,Cosmo,Frankie&Benny’s,PrezzoandChiquitos.

2009

16www.alderking.com

10

20

25

30

35

15

5

76%6%

18%

zoneAheadlinerent£psf

75

0

125

150

2010 2011 2012 2013

100

50

2009

25

(1,3

99

.26

)13

0

(1,3

45

.44

)12

5

(1,3

45

.44

)12

5

(86

1.08

)8

0

(59

2)

55

outoftownrent£psf

10

0

25

35

2010 2011 2012 2013

15

5

2009

30

20

(236

.80

)22

(24

7.5

6)

23

(215

.28

)20 (29

0.6

1)2

7

(26

9)

25

leisureheadlinerent£psf

0

5

10

15

25

2010 2011 2012 20132009

cinema health&fitness A3/A4

20

(129

.16)

12

(129

.16)

12

(129

)12

(86

.11)

8

(86

.11)

8

(86

)8

(19

3.75

)18

(19

3.75

)18

(19

4)

18

(129

.16)

12(1

07.

64

)10

(215

.27

)20

(118

.40

)11

(86

.11)

8

(18

8.3

6)

17.5

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

12.93

8.30 8.9

25.6

16.65

primeyields%

6

4

8

9

20132012

7

5

20112010

investmentbysector

industrial

office

retailhighstreet

retailoutoftown

office

retailhighstreet

other

1

Industrial

Offices

(sqm)sqft

Noel Stevens T 01392 353093 E [email protected]

Noel Stevens T 01392 353093 E [email protected]

demand

• Therewerefewsubstantialrequirementsin2013.

• Theserviceandpublicsectorspredictlittlenewdemand.

• ConversionofspacetoresidentialunderPermittedDevelopmentRightscouldsparkreneweddemand.

supply

• TherecontinuestobealackofGradeAspace.

• Supplyoverallfaroutstripsdemand.

• Therearenomajorschemesplannedduetotheweakmarketandlackofrentalgrowth.

headline rent

• Secondhandstockdominatesthemarketandrentallevelshaveremainedconsistentwith2012.

• Therearethefirstsignsofareductioninincentives.

demand

• Takeupreturnedtomorenormallevelsin2013followingthe385,000sqft(35,768sqm)saleanddemolitionoftheToshibapremisesin2012.Theunderlyingtrendshowspositivesignsforthemarket.

• PlymouthEnterpriseParkhasseengooddemandsinceitsinceptionwithlettingstoViSpring,WestCountryStorageSolutions,PlymouthKartingandFulcrumPowerGeneration.

• DXMailagreedtermstoleasea22,000sqft(2,044sqm)buildingatLangageScienceParkformaildistribution.

supply

• Thesupplypictureremainssimilartothatof2012but,importantly,isdownonthepeakfigureof2010.

• Supplyisheavilyweightedtowardsthesmallerendofthemarket.Only10%ofavailablebuildingsareinexcessof10,000sqft(929sqm)insize.

• Asin2013,thelargestsinglefacilityonthemarketistheformerStIvesPrintFactoryatLangage.

headline rent

• Headlinerentsremainedstaticat£5.95psf(£64.04psm).

• Incentiveswillcontinuetobestrongfortenantswithgoodcovenantsseeking3+yearleases.

Plymouth

Alder King Market Monitor 201417

demand000ssqft

100

0

200

250

2011 2012 20132010

150

50

2009

105(10) 90

(8)

95(9)

145(13)

95(9)

supply000ssqft

200

0

400

500

2010 2011 2012 2013

300

100

2009

275(26)

325(30)

330(31)

360(33) 310

(29)

headlinerent£psf

15

0

20

2010 2011 2012 2013

5

2009

10

(16

6.8

3)

15.5

(16

6.8

3)

15.5

(16

6.8

3)

15.5

(16

6.8

3)

15.5

(16

7)

15.5

citycentre outoftown

(172

.22

)16

(172

.22

)16

(172

.22

)16

(16

2)

15

(16

2)

15

demand000ssqft

200

0

400

500

2010 2011 2012 2013

300

100

2009

160(15)

200(19)

250(23)

500(46)

290(27)

supply000ssqft

1,000

0

2,000

2,500

3,000

2010 2011 2012 2013

1,500

500

2009

800(74)

1,000(93) 715

(66)720(67)

1,400(130)

headlinerent£psf

2

0

4

7

2010 2011 2012 2013

3

1

2009

5

6

(64

.04

)5

.95

(64

.04

)5

.95

(64

.04

)5

.95

(64

.04

)5

.95

(64

)5

.95

1. Drake Circus, Plymouth.

2. Sutton Harbour, Plymouth.

3. Tamar Bridge, Plymouth.2 3

Investment

Retail & Leisure

John Benson T 0117 317 1100 E [email protected] Rossiter T 01392 353089 E [email protected]

zone A headline rent

• RetailtrendsinPlymouthcontinuedmuchastheydidin2012.TakeupoutsideDrakeCircusisslow,withsupplystilloutstrippingdemandandmanyretailunitsremainvacantforlongperiodsoftime.

• Discountretailingprovidedthemostactivity,withPoundlandopeningitssecondstoreinthecityand99pStoreslookingforitssecond.Charityoccupiersandindependentdiscountclothingretailersalsoprovedacquisitivein2013.

out of town rent

• Constructionofthenew£800,000retailschemeatWoolwellwascompleted,withpre-letsagreedtoCompanionCareveterinarypractice,Barnardo’sandaDomino’sPizzaoutlet.

• HomeSupplyRetailtook5,000sqft(464sqm)ofgroundfloorretailspaceatGdyniaWayandEvansCyclestook7,500sqft(697sqm)atCharlesCross.

• SecondaryretailinginMutleyPlainprovedpopularwithmanymajorbrandsalreadyrepresentedandnewsupermarketentrantstakingpremisesoverthelast12months.

leisure headline rent

• HigherHomePark,AkkeronGroup’s£50mretailandleisureschemesurroundingPlymouthArgyleFootballClub,hasbeengrantedplanningconsent.The492,216sqft(45,729sqm)developmentwillincludeahotel,cinema,icerinkandcomplimentaryretailandfoodofferings.

• GaryRhodesopenedhisrestaurantRhodesatTheDomeonPlymouth’squayside.Ithasprovedapopularvenueprovidingrestaurantandbarfacilities.

value of investment transactions

• TherewasaconsiderablefallinthevolumeofinvestmentactivityinPlymouthin2013.Thetotalvolumeofinvestmenttransactionswas£9.6mcomparedto£26.3min2012.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7.25%

- Office 8%

- Retailhighstreet 7.25%

- Retailoutoftown 6.5%

investment by sector

• TherewereanumberofsmallofficeinvestmenttransactionsinPlymouthin2013.HydeParkHouse,amulti-letmixeduseretailandofficeblockonMutleyPlain,wassoldfor£660,000(NIY16.5%).

• ThereweretwolargeretailwarehousetransactionsinPlymouth.AtLairaBridgeRetailPark,twounitslettoCarpetrightandGoOutdoorssoldfor£6.6m(NIY7.88%).SugarMillRetailPark,multi-letandanchoredbyTheRange,soldfor£4.7m(NIY9.19%).

Lee Southan T 01392 353090 E [email protected]

18www.alderking.com

100

200

250

300

350

150

50

zoneAheadlinerent£psf

150

0

250

2010 2011 2012 2013

200

100

2009

50

(1,9

37.4

3)

180

(1,8

83.

61)

175

(1,8

83.

61)

175

(1,6

14.6

0)

150

(1,6

15)

150

outoftownrent£psf

10

0

20

30

2011 2012 2013

15

5

20102009

25

(24

2.18

)22

.5

(24

2.18

)22

.5

(24

2.18

)22

.5

(24

2.18

)22

.5

(?)

20.5

leisureheadlinerent£psf

0

5

10

15

20

20102009

cinema health&fitness A3/A4

(16

1.45

)15

(13

4.5

4)

12.5

(19

3.74

)18

(139

.93

)13

(10

7.6

4)

10

(19

3.74

)18

2011

(139

.93

)13

(86

.10)

8

(16

1.46

)15

2012

(139

.93

)13

(86

.10)

8

(16

1.46

)15

2013

(14

0)

13(8

6)

8

(16

1)15

valueofinvestmenttransactions£ms

0

2010 2011 2012 20132009

86.43

278.2

9.6313.62

primeyields%

6

4

8

9

2011 20132012

7

5

20102009

investmentbysector

industrial

office

retailhighstreet

retailoutoftown26.33

29%

10%

49%

9% industrial

office

retailhighstreet

retailoutoftown

other

3%

Swansea 1

Industrial

Offices

(sqm)sqft

Owen Young T 029 2038 1996 E [email protected]

Owen Young T 029 2038 1996 E [email protected]

demand

• Takeupreducedto60%ofthefiveyearaveragewithlessthan35occupiertransactions.Onlyoneoccupationexceeded5,000sqft(464.6sqm).

• 95%comprisedoutoftownorcitycentrefringetransactions,manyinandaroundSwanseaEnterprisePark.

• Notabledealsin2013includedFieldbayLtdacquiring5,300sqft(492.4sqm)atChestnutHouseandtheBritishRedCrossSocietyacquiringKidwellyHouse,bothontheEnterprisePark.

supply

• AvailabilitydecreasedslightlyduetoalackofnewdevelopmentandthedemolitionofOldwayHouseinthecitycentre.

• SimilartoCardiffandNewport,thereisashortageofGradeAstockwithlittlenowavailableontheSA1waterfront.

• Over80,000sqft(7,432sqm)stillremainsatCruciblePark,SwanseaVale,sincefirstbecomingavailablein2008.

headline rent

• Therewasnogrowthinheadlinerentsduring2013.

• WithlittlemodernaccommodationavailableinSA1andthecitycentre,headlinefiguresshouldbemaintainedinto2014.

• Outoftownrentsandincentivesshouldcontinueatthesamelevelthrough2014.

demand

• 2013sawasubstantialdecreaseintake-upagainstabackdropofpositiveagentsentiment.

• Theabsenceofanyparticular‘bigshed’transactionswithinthecountyboundaryhasbeenoffsetwithsomelargertransactionsalongFabianWayandintoNeathandPortTalbot.Theseneighbouringdealshaveaccountedforover600,000sqft(55,741.8sqm).

supply

• Supplyfellin2013,accountedforbythedemolitionofobsoletebuildingsandgeographicalre-categorisationofpropertyalongpartsofFabianWay.

• Stockprovidinglessthan10,000sqft(929sqm)accountsforapproximately73%ofallavailablestock.

headline rent

• Overthepastthreeyearsrentallevelshaveremainedunchanged.

• Thehighproportionofexistingsecondarystockandthelimitedamountofnewstockbeingbroughttothemarkethavehinderedanyrentalgrowth.

Alder King Market Monitor 201419

demand000ssqft

0

100

150

200

250

2010 2011 2012 2013

50

2009

163(15)

108(10)

68(6)

108(10)

54(5)

supply000ssqft

0

100

200

300

400

600

2010 2011 2012 20132009

500 540(50)

566(53)

490(46)

473(44)

521(48)

headlinerent£psf

15

0

20

2010 2011 2012 2013

5

2009

10

citycentre outoftown

(15

6.0

7)

14.5

(15

6.0

7)

14.5

(14

8)

13.7

5

(15

6.0

7)

14.5

(15

6)

14.5

(123

.78

)11

.5

(123

.78

)11

.5

(115

.71)

10

.75

(115

.71)

10

.75

(116

)10

.75

demand000ssqft

0

200

400

600

800

1,200

2010 2011 2012 20132009

1,000

459(43)

472(44)

461(43)

795(74)

180(17)

supply000ssqft

1,000

0

2,000

2,500

3,000

3,500

2010 2011 2012 2013

1,500

500

2009

2,938(273) 2,755

(256)2,755(258)

2,315(215)

1,724(160)

headlinerent£psf

2

0

4

5

6

7

2010 2011 2012 2013

3

1

2009

4.20(45.21)

4.20(45.21)

4.20(45.21)

4.20(45)

4.35(46.82)

1. Ethos House, Swansea.

2. Harbourside, Port Talbot.

3. CGI of Swansea University’s Bay Campus. Courtesy of St Modwen.2 3

Investment

Retail & Leisure Owen Young T 029 2038 1996 E [email protected]

John Benson T 0117 317 1100 E [email protected] Owen Young T 029 2038 1996 E [email protected]

value of investment transactions

• ThetotalvolumeofinvestmenttransactionsinSwanseawas£49.64m.Thisisasignificantincreaseonthe2012figuresandislargelyattributabletoonesingletransaction.

prime yields

• Ourcurrentviewofprimeyieldsisasfollows:

- Industrial 7.75%

- Office 7.75%

- Retailhighstreet 7.25%

- Retailoutoftown 6.5%

investment by sector

• OneofthemostsignificantinvestmenttransactionsinSwanseawasM&G’scommitmenttoprovide£32mofdevelopmentfinanceforstudentaccommodationatSwanseaUniversity.M&Gacquiredalongleaseholdinterestwhichwillprovidea45yearrentalincomelinkedtoinflation.

• AlargeretailinvestmentsalewasaparadeonPrincessWaywhichismulti-letwithanAWULTofsixyearsandsoldfor£5.3m(NIY12.6%).

• InnearbyBridgend,the300acreBridgendIndustrialEstatesoldfor£20m(NIY9%).

zone A headline rent

• UncertaintysurroundsthefutureregenerationofthetowncentrewiththewithdrawalofHammerson,theCouncil’slatestdevelopmentpartner.Togetherwithotherregionaleconomicfactors,thishasnaturallyhadanegativeimpactondemand.

• Onthepositiveside,Hammersonisplanningtorevampits240,000sqft(22,296sqm)ParcTaweschemewithanewanchortenant.

out of town rent

• Therewasnogrowthinout-of-townrentsin2013.

• NotabledealsincludeOakFurnitureLandtakingtheformerEddershawspropertyonPhoenixWayandOneStopsettingupstoresonbothNeathRoadandPentregethinRoad.

• Secondaryandtertiarypropertiescontinuetotradeatrealisticprices,manythroughauctionhouses.

leisure headline rent

• A3rentshaveonceagainimprovedwiththelettingoftheformerLaTascapremisesonSalubriousPlacetoSmokeHaus.

• SwanseaUniversity’s£450msecondcampusoffFabianWayshouldprovideashotinthearmtothecitycentrewiththefirst£150mphaseexpectedtobecompletedbythesummerof2015.

20www.alderking.com

3%

(1,4

53.

07

)13

5

(1,2

37.8

0)

115

(1,18

4)

110

(1,18

4)

110

(1,0

76)

100

zoneAheadlinerent£psf

150

0

250

300

2010 2011 2012 2013

200

100

2009

50

outoftownrent£psf

20

0

40

70

2010 2011 2012 2013

30

10

2009

60

50

(430

.54

)4

0

(376

.72

)35

(376

.74

)35

(376

.74

)35

(377

)35

leisureheadlinerent£psf

0

5

10

15

25

2010 2011 2012 20132009

cinema health&fitness A3

20

(13

4.5

4)

12.5

(118

.40

)11

(215

.27

)20

(118

.40

)11

(129

.17)

12

(129

.17)

12

(129

)12

(10

7.6

4)

10

(10

7.6

4)

10

(96

.88

)9

(97

)9(16

1.45

)15

(18

2.9

9)

17

(18

2.9

9)

17

(215

)20

valueofinvestmenttransactions£ms

40

0

80

100

120

140

2010 2011 2012 2013

60

20

2009

47.7

17.9

113.9

8.65

49.64

primeyields%

5

3

7

8

2012 2013

6

4

201120102009

investmentbysector

industrial

office

retailhighstreet

retailoutoftown

3%

75%

19% industrial

office

retailhighstreet

other

Swindon

Industrial

Offices

(sqm)sqft

James Gregory T 01793 428106 E [email protected]

James Gregory T 01793 428106 E [email protected]

1

demand

• Therewasanoverallimprovementintakeup,withsignificantlettingsatWashingtonHouse,LydiardFieldstoOpenwork,WakefieldHouse,AspectParktoNationwideandStationSquareinthetowncentretoPrePayTechnologies.

• Themajorityofactivitytookplaceoutoftownwithlessthan25%ofalltransactionsbeinginthetowncentreorOldTown.

• Thenumberoftransactionswassimilarto2012buttheaveragesizeoftransactionwassignificantlylarger.

• Mosttransactionswereofaleaseholdnatureratherthanfreehold.

supply

• TheoverallsupplyremainedrelativelystableaslargesecondhandofficesatUKLifeCentreandDeltaOfficeParkhavecometothemarket.

• Therewasagradualreductioningoodqualityaccommodationwithnobrandnewofficespacecurrentlyavailableoutoftown.

• Therewasnospeculativedevelopment.

• Occupiersareincreasinglyseekingbetterqualitystock.

headline rent

• Theheadlinerentforoutoftownofficesincreased,reflectingthelackofgoodqualitystock.

• Towncentrerentscontinuedtostrugglebutthereweresomesignificantlettingsin2013.

• Rentfreeperiodscontinuetobegrantedinfavourofthetenant.

demand

• TakeuphasreachedthelongtermaveragelevelwithsignificanttransactionsattheOxfordBuilding,EuropatoKBRandGroundwellDistributionCentre,GroundwelltoNetworkRail.

• Thekeydrivertosecuringoccupierscontinuestobeensuringpropertiesareingoodconditionandcapableofimmediateoccupationtosatisfycontract-ledrequirements.

• 2013sawamarkedincreaseinfreeholdrequirementsandtherearestillanumberofunsatisfiedones.

supply

• Thereisnowarealshortageoflargebuildingsavailableforimmediateoccupationwiththeneedtobringforwarddeliverabledevelopmentbecomingurgent.

• Thereareveryfewgoodqualityopportunitiesforthemid-rangeoccupier.

• Thesupplyofallsizeshassteadilybeeneroded.

headline rent

• Rentsforsecondhandaccommodationhaveriseninsomecaseswherecompetitivesituationshavearisen.

• Occupiersunderstandtheneedtopayforearlybreakclauses.

• Rentalincentiveshavestabilisedandinsomecasesmovedinfavouroflandlords.

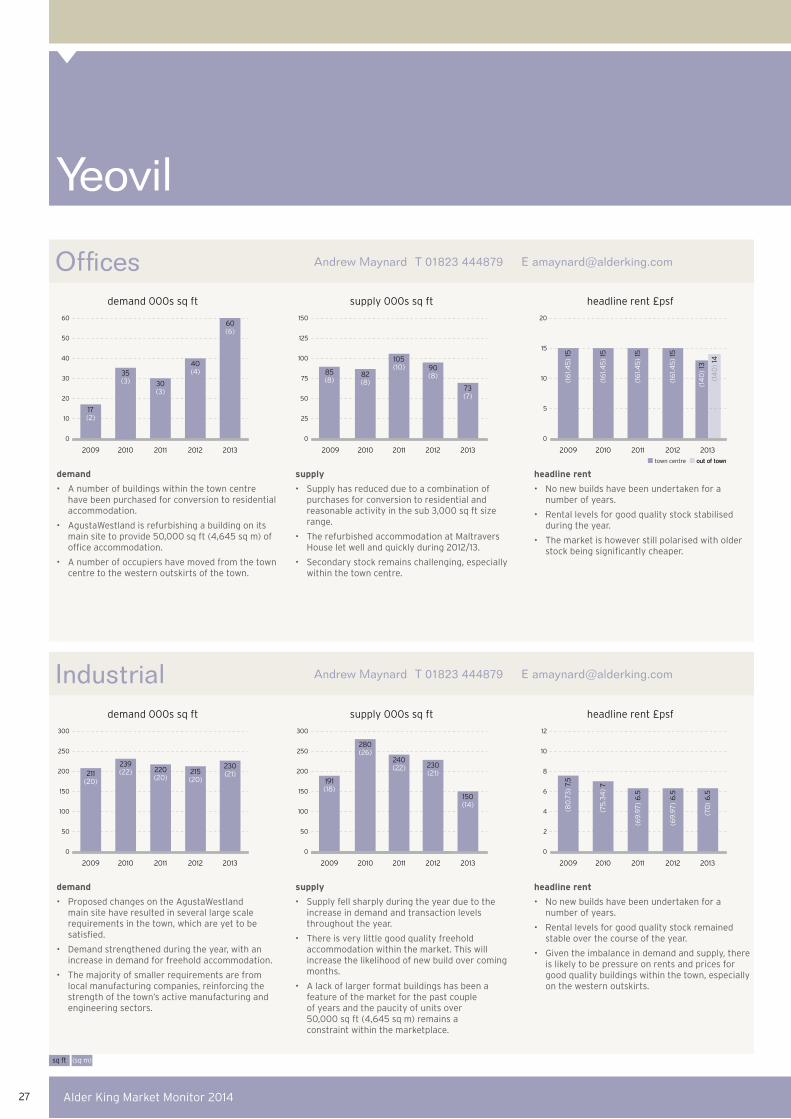

Alder King Market Monitor 201421

demand000ssqft

100

0

200

250

300

350

400

2011 2012 20132010

150

50

2009

205(19)

85(8)

170(16)

199(18)

131(12)

400

0

800

1,000

1,200

1,400

1,600

2011 2012 20132010

600

200

2009

1,270(118)

1,306(121)

1,320(123)

1,150(107) 1,020

(95)

supply000ssqft headlinerent£psf

0

5

10

15

20

2011 2012 201320102009

towncentre outoftown

(19

9.12

)18

.5

(19

9.12

)18

.5

(172

.22

)16

(172

.22

)16

(18

8)

17.5

(16

9.5

3)