Embed Size (px)

Citation preview

SOUTH AUSTRALIA

CREDIT UNIONS REGULATIONS, 1990

REGULATIONS UNDER THE CREDIT UNIONS ACT, 1989

Credit Unions Regulations, 1990

being

No. 46 of 1990: Gaz. 5 April 1990, p. 9721

as varied by

No. 151 of 1991: Gaz. 27 June 1991, p. 22682

1 Came into operation 12 April 1990: reg. 3.2 Came into operation 1 July 1991: reg. 2.

2.

PART I

PRELIMINARY

Citation1. These regulations may be cited as the Credit Unions Regulations, 1990.

Revocation2. All regulations made under the Credit Unions Act, 1976, are revoked.

Commencement3. These regulations will come into operation on 12 April, 1990.

Interpretation4. In these regulations—

"the Act" means the Credit Unions Act, 1989.

Note: For definition of divisional penalties see Appendix 2.

Forms5. (1) The forms set out in schedule 1 must—

(a) be used for the purposes specified in the schedule;

and

(b) be completed in accordance with the instructions contained in the forms.

(2) The name of a person signing a form set out in schedule 1 must be written legibly underor alongside the signature of that person.

(3) Where the space provided in a form is insufficient to contain all the requiredinformation—

(a) the information must be set out in an annexure to the form;

(b) the annexure must have an distinguishing mark such as a letter or numeral;

and

(c) the space in the form must contain the statement "See Annexure" together with thedistinguishing mark for the annexure, or words to similar effect.

Fees6. The fees set out in schedule 2 are payable as specified in the schedule.

Application of Securities Industry (South Australia) Code7. Pursuant to section 4(2) of the Act, the provisions of the Securities Industry (South

Australia) Code apply in relation to credit unions and associations subject to the modification thatthey do not apply in relation to any dealing by a credit union or association in its own securities.

3.

Application of Companies (South Australia) Code provisions relating to registration ofcharges

8. Pursuant to section 4(2) of the Act, the provisions of the Companies (South Australia)Code relating to the registration of charges (Division 9 of Part IV and Schedule 5) apply inrelation to credit unions and associations subject to the following modifications:

(a) a reference to a company is to be read as including a reference to a credit union orassociation;

(b) a reference to the Register of Company Charges or the Register is to be read asincluding a reference to—

(i) a Register of Credit Union Charges;

and

(ii) a Register of Credit Union Association Charges,

and section 203 of the Code is to be read as if the section included a requirement thateach Register is to be maintained separately by the Commission with entries relatingto companies, credit unions or associations being made by the Commission only in theRegister kept in relation to bodies of that kind;

(c) a reference to an official manager is to be read as including a reference to anadministrator appointed pursuant to section 121 of the Act;

and

(d) section 215A of the Code is not to apply in relation to a credit union or association.

Contents of rules of credit unions9. For the purposes of section 15 of the Act, the following provisions must be contained in

the rules of a credit union:

(a) the name of the credit union and the location of its first office;

(b) the objects of the credit union;

(c) the powers of the credit union;

(d) the mode and conditions of admission to membership and the shares to be acquiredbefore the exercise of rights of membership;

(e) the circumstances under which membership will cease and the manner in which amember may be expelled;

(f) the manner in which the funds of the credit union are to be raised;

(g) the manner in which the funds of the credit union are to be managed including themode of drawing and signing cheques, drafts, bills of exchange, promissory notes andother negotiable instruments;

4.

(h) the conditions relating to shares and deposits and the withdrawal of shares anddeposits;

(i) the manner in which any non-withdrawable shares may be transferred;

(j) the application and investment of funds;

(k) the conditions relating to loans and the security for loans, including the conditions onwhich a borrower may redeem the amount due prior to the expiration of the period ofthe loan;

(l) the manner in which any surplus arising out of the operations of the credit union is tobe distributed;

(m) the number of directors, the qualifications as to shareholding of directors, the mannerof the election, remuneration and removal of directors and the filling of vacancies inthe office of director;

(n) the powers and duties of the board of directors and the manner of calling meetings,the quorum for meetings and the procedure at meetings of the board of directors;

(o) the manner of calling general and special meetings of members and the requisitenotices of meetings and the quorum for meetings of the credit union;

(p) the procedure at meetings of the credit union, including the voting rights of members,the manner of voting and the majority necessary for carrying resolutions;

(q) the frequency with which the accounts of the credit union are to be audited;

(r) the manner of appointing, remunerating and removing auditors, the powers and dutiesof auditors and, in particular, the powers and duties of auditors with respect to theinspection of securities held by the credit union;

(s) the manner of settling disputes between the credit union and its officers or members,or any person claiming through any member or under the rules;

(t) the security to be given by any officer or employee of the credit union having thereceipt or charge of any money belonging to the credit union;

(u) the manner of altering, adding to or rescinding these rules;

(v) the custody and use of the seal of the credit union;

and

(w) the manner in which the credit union may be wound up.

5.

Auditor’s report for amalgamation application10. For the purposes of section 32(6)(c) of the Act, the report prepared by the auditor of a

credit union concerned in a proposed amalgamation must state—

(a) whether the accounts of the credit union for the financial year up to the date referredto in section 32(6)(c) are, in the opinion of the auditor, properly prepared—

(i) in accordance with applicable approved accounting standards;

and

(ii) in accordance with section 32(6) and the other provisions of the Act;

(b) any defect or irregularity in the accounts and any matter not set out in the accountswithout regard to which a true and fair view of the results for the period and state ofaffairs of the credit union, as at the date, would not be obtained;

and

(c) if he or she is not satisfied as to any matter referred to in paragraph (a), the reasonsfor not being so satisfied.

Disclosure statements11. (1) For the purposes of section 39(1) of the Act, a disclosure statement must—

(a) be printed in type of a size not less than the type known as eight point Times unlessthe Commission, before the issuing of the disclosure statement, approves the type andsize of print as being legible and satisfactory;

(b) state that a copy of the disclosure statement has been lodged with the Commission andalso state, immediately after that statement, that the Commission takes noresponsibility as to the contents of the disclosure statement;

(c) state that no securities will be issued on the basis of the disclosure statement later thansix months after the date of execution of the disclosure statement;

(d) if the disclosure statement includes any statement that is made by an expert or iscontained in what purports to be a copy of, or extract from, a report, memorandum orvaluation of an expert—state the date on which the statement, report, memorandum orvaluation was made and whether or not it was prepared by the expert for incorporationin the disclosure statement;

(e) state the dates of, the parties to, and the general nature of, every material contract;

(f) contain the information set out in schedule 3;

and

(g) not more that 14 days before the date on which the statement is issued to members ofthe credit union, be signed and dated by each director of the credit union or by a dulyauthorized agent of the director.

6.

(2) The credit union must, not less than six weeks before the date of execution of thedisclosure statement, lodge with the Commission—

(a) a copy of the disclosure statement;

and

(b) copies, verified by statements in writing, of all consents required by section 39(4) ofthe Act to the issue of the disclosure statement and of all material contracts referred toin the disclosure statement or, in the case of such a contract not reduced to writing, ormemorandum giving full particulars of the contract, verified by statement in writing.

Penalty: Division 7 fine.

(3) For the purposes of this regulation, a reference to a material contract does not include—

(a) a contract entered into in the ordinary course of the business of the credit union orany body on behalf of which the securities are to be issued;

or

(b) a contract entered into more than two years before the date of issue of the disclosurestatement.

(4) For the purposes of this regulation and schedule 3, the date of execution of a disclosurestatement is the date of signing of the statement by the director or the director’s agent last signingthe statement.

Commercial loans12. For the purposes of section 45(4) of the Act, courses in commercial or business lending

conducted by the Credit Union Association of S.A. are courses of instruction of a prescribed kind.

Liquidity13. (1) For the purposes of section 47(1) of the Act, the average amount of liquid funds held

by a credit union over a month must be computed by calculating the total amount of liquid fundsof the credit union at the end of each day during the month and, as soon as practicable after theend of the month, calculating the sum of those amounts and dividing the sum by the number ofdays in the month.

(2) For the purposes of the definition of "liquid funds" in section 47(2) of the Act—

(a) the following are prescribed associations:

(i) the Credit Union Association of S.A.;

and

(ii) the Credit Union Services Co-operative of S.A.;

and

7.

(b) the following are investments of a prescribed class:

(i) deposits with a company or other body corporate of a kind with which atrustee is authorized by law to invest trust funds on deposit;

(ii) securities issued or guaranteed by the Treasurer or Government of the State,the Commonwealth or another State or a Territory of the Commonwealth;

and

(iii) bills of exchange that have been endorsed or accepted by a bank.

Future losses account14. (1) For the purposes of section 49(1)(a)(ii) of the Act, the amount to be determined is

the aggregate for the time being of the amounts determined in accordance with the followingformula in relation to all loans made by the credit union—

(a) that are secured by registered first mortgages over real property;

and

(b) under which an amount is for the time being due and unpaid to the credit union thatequals or exceeds three months’ payments:

A = B × C100

Where—

A is the amount to be determined in relation to each such loan:

B is—

(i) where the amount due and unpaid under the loan equals orexceeds three months’ payments but is less than 6 months’payments—10;

(ii) where the amount due and unpaid under the loan equals orexceeds 6 months’ payments but is less than 9 months’payments—20;

(iii) where the amount due and unpaid under the loan equals orexceeds 9 months’ payments but is less that 12 months’payments—25;

(iv) where the amount due and unpaid under the loan equals orexceeds 12 months’ payments—30.

C is the total amount for the time being due and unpaid to the creditunion under the loan.

8.

(2) For the purposes of section 49(1)(b)(ii) the amount to be determined is the aggregate forthe time being of the amounts determined in accordance with the following formula in relation toall loans made by the credit union—

(a) that are not secured as referred to in subregulation (1);

and

(b) under which an amount is for the time being due and unpaid to the credit union thatequals or exceeds three months’ payments:

A = B × C100

Where—

A is the amount to be determined in relation to each such loan:

B is—

(i) where the amount due and unpaid under the loan equals orexceeds 3 months’ payments but is less than 6 months’payments—40;

(ii) where the amount due and unpaid under the loan equals orexceeds 6 months’ payments but is less than 9 months’payments—60;

(iii) where the amount due and unpaid under the loan equals orexceeds 9 months’ payments but is less than 12 months’payments—80;

(iv) where the amount due and unpaid under the loan equals orexceeds 12 months’ payments—100:

C is the total amount for the time being due and unpaid to the creditunion under the loan.

(3) A reference in this regulation to a number of months’ payments in relation to a loan is areference to the total amount required to be paid to the credit union according to the terms of theloan contract in respect of the immediately preceding period of that number of months.

Provisions governing investment15. (1) For the purposes of section 51(1)(d) of the Act, the following are investments of a

prescribed class:

(a) securities issued by the Treasurer or Government of a State other than this State orissued or guaranteed by the Treasurer or Government of a Territory of theCommonwealth;

9.

(b) securities issued or guaranteed by an instrumentality of the Crown in right of a Stateother than this State or of a Territory of the Commonwealth;

(c) securities issued by a bank, or securities issued by any other body corporate where theobligations of the body under the securities are guaranteed, or secured by a letter ofcredit issued or confirmed, by a bank;

(d) withdrawable shares in an association of which the credit union is a member;

(e) shares in, or deposits with—

(i) Data Action Pty. Ltd.;

or

(ii) Members Mortgage Fund Pty. Ltd.;

(f) units in Members Mortgage Loan Trust Fund.

(2) The investments referred to in subregulation (1)(e) and (f) are prescribed for the purposesof section 51(3) of the Act.

Application of Act to associations16. Pursuant to section 61 of the Act, the following provisions of the Act do not apply to or

in relation to associations:

(a) section 123(3)(a);

(b) section 137.

Registers17. (1) For the purposes of section 76 of the Act, but subject to this regulation, registers

must be kept by each credit union in writing as set out in schedule 4.

(2) Notwithstanding subregulation (1), a register to be kept by a credit union may be kept byrecording or storing the matters concerned by means of a mechanical, electronic or other deviceprovided that—

(a) the matters recorded or stored are capable, at any time, of being reproduced in awritten form, or a reproduction of those matters is kept in a written form, approved bythe Commission;

(b) all reasonable precautions are taken by the credit union for guarding against damageto, destruction of or falsification of or in, and for discovery of falsification of or in,the register;

and

10.

(c) when the register is required to be made available for inspection, or a copy of thewhole or part of its contents is required, pursuant to the Act, the register is madeavailable in written form or the whole or part of its contents is reproduced in writing,as the case may be.

Inspection of registers18. (1) For the purposes of section 77(2) of the Act, the matters in respect of which

particulars are recorded in the Register of Members and Shares kept by the credit union pursuantto the Act and these regulations are prescribed matters.

(2) A credit union must keep the Register of Prescribed Interests and Holders of PrescribedInterests kept by the credit union pursuant to the Act and these regulations open for inspection atits registered office without fee by the holders of such interests.

Requirements for preparation of accounts19. For the purposes of section 81(6) of the Act, the prescribed requirements are—

(a) the requirements set out in schedule 5;

and

(b) a requirement that the accounts or group accounts, as the case may be, include astatement of sources and applications of funds prepared so as to comply with theapproved accounting standard ASRB 1007: Financial Reporting of Sources andApplications of Funds.

Rounding off of amounts in accounts or reports20. (1) Pursuant to section 83(1) of the Act but subject to this regulation, a credit union may

insert in any accounts or report under the Act, in substitution for an amount that the credit unionwould otherwise be required or permitted to set out in the accounts or report, that amount to thenearest thousand dollars, or if the amount is $500 or less, zero.

(2) Where an amount is adjusted to the nearest thousand dollars, the fact that such anadjustment has been made must be clearly indicated on each page on which the adjusted amountappears.

(3) Where an amount is adjusted to zero, the original amount must be shown in full by wayof a note to the accounts or report.

(4) Where an amount is adjusted in accordance with this regulation, any correspondingamount for a previous period that is recorded in the accounts or report must be similarly adjusted.

(5) Where an amount is adjusted in accordance with this regulation in a report undersection 82(1) or (2) of the Act, the report must state that the credit union is a credit union to whichthis regulation applies and that the amount has been adjusted in accordance with this regulation.

(6) This regulation applies only in relation to—

(a) a credit union with total assets in excess of $10 000 000;

or

11.

(b) a holding credit union where the total assets of the group for which it is the holdingcredit union are in excess of $10 000 000.

Final audit on amalgamation21. For the purposes of section 94(1) of the Act, the following are prescribed statements to

be made by the auditor in a report under that section:

(a) a statement whether the accounts are, in the opinion of the auditor, properlyprepared—

(i) so as to give a true and fair view of the profit or loss of the credit union forthe financial year up to the date of dissolution of the credit union, and so asto give a true and fair view of the state of affairs of the credit union as atthat date;

(ii) in accordance with the provisions of the Act;

and

(iii) in accordance with applicable approved accounting standards;

(b) a statement of any defect or irregularity in the accounts and any matter not set out inthe accounts without regard to which a true and fair view of the results for the periodand state of affairs of the credit union as at that date would not be obtained;

and

(c) if he or she is not satisfied as to any matter referred to in paragraph (a), a statementof the reasons for not being so satisfied.

Credit Union Deposit Insurance Fund22. (1) For the purposes of section 110(2) of the Act, the prescribed percentage is—

(a) in relation to a credit union with reserves less than 3 per cent of its total assets—2 percent;

(b) in relation to a credit union with reserves equal to or greater than 3 per cent but lessthat 3.5 per cent of its total assets—1.8 per cent;

(c) in relation to a credit union with reserves equal to or greater than 3.5 per cent but lessthan 4 per cent of its total assets—1.6 per cent;

(d) in relation to a credit union with reserves equal to or greater than 4 per cent but lessthan 4.5 per cent of its total assets—1.4 per cent;

(e) in relation to a credit union with reserves equal to or greater than 4.5 per cent but lessthan 5 per cent of its total assets—1.2 per cent;

(f) in relation to a credit union with reserves equal to or greater than 5 per cent of itstotal assets—1 per cent.

12.

(2) In this regulation—

"reserves" means the amount comprising reserves of the credit union pursuant to section 48of the Act as at the preceding 30 June:

"total assets" means the amount recorded in the accounts of the credit union as the amountof its total assets as at the preceding 30 June.

Rate of interest payable to Board on amounts outstanding23. For the purposes of section 110(10) and 111(7) of the Act, the prescribed rate of interest

is 20 per cent per annum.

Winding up24. (1) For the purposes of section 123(2) of the Act, the application of Part XII of the

Companies (South Australia) Code is subject to the following modifications:

(a) notwithstanding the provisions of that Part, on the winding up of a credit union, nopresent or past member of the credit union will be liable to contribute to the propertyof the credit union by reason only of his or her membership of the credit union;

and

(b) the persons on whose application under section 363 of the Code a credit union may bewound up under an order of the Court include any member of the credit union.

(2) For the purposes of section 123(7) of the Act, a winding up on the certificate of theCommission must be carried by the Court, on application by the Commission and lodgement of acopy of the certificate, in accordance with the provisions of Part XII of the Companies (SouthAustralia) Code as applied by section 123 of the Act as if the credit union had by specialresolution resolved that it be wound up by the Court.

Application for registration as foreign credit union25. For the purposes of section 127(2)(c) of the Act, each document or copy of a document

must be verified by an officer of the foreign credit union, by statutory declaration, as truly statingthe matters set out in the document, or as constituting a true copy, as at a date not earlier thanthree months before lodgment of the document or copy with the Commission.

Notification to Commission of changes relating to foreign credit union26. For the purposes of section 130 of the Act, notice of any change to the name under

which the foreign credit union carries on business in the place of its origin must, if the changeresults in the issue of a new or amended certificate of incorporation or registration by theappropriate authority in the State or Territory of its origin, be accompanied by a copy of the newor amended certificate certified by that authority.

Copy of court orders for Commission27. A credit union must, within seven days after the entering of any order made by the

Court pursuant to the Act in relation to the credit union, lodge an office copy of the order with theCommission.

Penalty: Division 7 fine.

13.

SCHEDULE 1

Forms

(Regulation 5)

Form 1: Application for registration as a credit union.

Form 2: Declaration to accompany application for registration as a credit union.

Form 3: Certificate of incorporation of credit union.

Form 4: Application by credit union/association for registration of alteration of rules.

Form 5: Certificate of incorporation of credit union/association (following change of name).

Form 6: Notice of change of registered office.

Form 7: Application for registration of amalgamation of credit unions or associations.

Form 8: Certificate of incorporation on amalgamation—new local credit union/association.

Form 9: Certificate of amalgamation—new local credit union/association.

Form 10: Certificate of registration—new foreign credit union.

Form 11: Certificate of amalgamation—new foreign credit union.

Form 12: Certificate of amalgamation—local merger of credit unions/associations.

Form 13: Certificate of amalgamation—foreign merger.

Form 14: Report of a credit union to the Credit Union Deposit Insurance Board—prescribed loans madefor the month of ...........

Form 15: Application for registration of an association.

Form 16: Certificate of incorporation of an association.

Form 17: Application for registration of special resolution.

Form 18: Application for consent to resignation as auditor.

Form 19: Notice of resignation, retirement, withdrawal or removal of auditor.

Form 20: Return of a credit union or association for financial year ended on ............

Form 21: Application for registration of a foreign credit union.

Form 22: Certificate of registration of a foreign credit union.

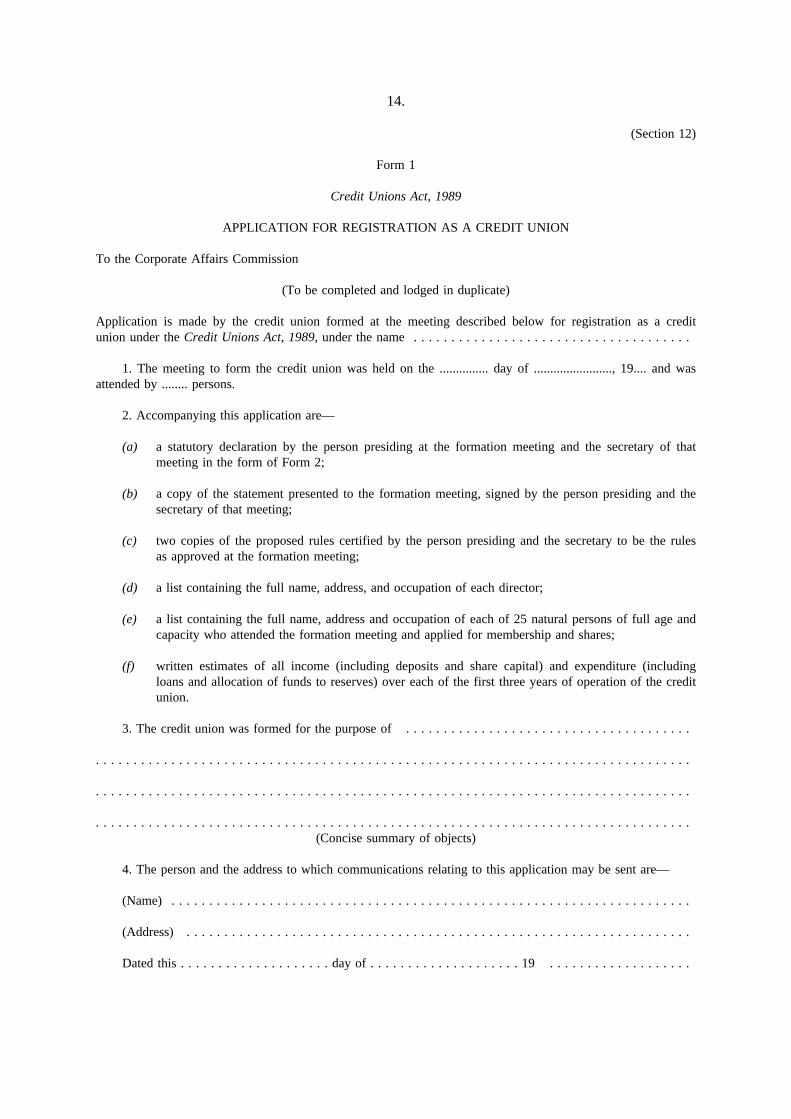

14.

(Section 12)

Form 1

Credit Unions Act, 1989

APPLICATION FOR REGISTRATION AS A CREDIT UNION

To the Corporate Affairs Commission

(To be completed and lodged in duplicate)

Application is made by the credit union formed at the meeting described below for registration as a creditunion under the Credit Unions Act, 1989, under the name . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. The meeting to form the credit union was held on the ............... day of ........................, 19.... and wasattended by ........ persons.

2. Accompanying this application are—

(a) a statutory declaration by the person presiding at the formation meeting and the secretary of thatmeeting in the form of Form 2;

(b) a copy of the statement presented to the formation meeting, signed by the person presiding and thesecretary of that meeting;

(c) two copies of the proposed rules certified by the person presiding and the secretary to be the rulesas approved at the formation meeting;

(d) a list containing the full name, address, and occupation of each director;

(e) a list containing the full name, address and occupation of each of 25 natural persons of full age andcapacity who attended the formation meeting and applied for membership and shares;

(f) written estimates of all income (including deposits and share capital) and expenditure (includingloans and allocation of funds to reserves) over each of the first three years of operation of the creditunion.

3. The credit union was formed for the purpose of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Concise summary of objects)

4. The person and the address to which communications relating to this application may be sent are—

(Name) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Address) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dated this . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . 19 . . . . . . . . . . . . . . . . . . .

15.

Signatures of all directors of applicant credit union:

Director . . . . . . . . . . . . . . . . . . . . . . . . . Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

16.

(Section 12)

Form 2

Credit Unions Act, 1989

DECLARATION TO ACCOMPANY APPLICATION FORREGISTRATION AS A CREDIT UNION

Name of Applicant Credit Union . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

We, . . . . . . . . . . . . . . . . . . . of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

and . . . . . . . . . . . . . . . . . . . of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Full Name) (Residential Address)

being the person presiding and the secretary of the meeting held at ............................. on the ............ day of....................., 19.... for the purpose of forming the abovementioned credit union do solemnly and sincerelydeclare that—

(a) there were presented to the meeting—

(i) a written statement showing the objects of the credit union and the reasons for believingthat an application for registration of the credit union should be granted and that, ifregistered, it would be able to carry out its objects successfully;

and

(ii) a copy of the rules tendered for registration;

(b) there were 25 or more natural persons of full age and capacity qualified to be members of the creditunion present at the meeting and they approved of the rules now being tendered for registration;

and

(c) the requirements of Part III of the Act as to formation have been complied with.

And we make this solemn declaration conscientiously believing the same to be true and by virtue of theprovisions of the Oaths Act, 1936.

.........................................................................Signature of person presiding at meeting

...................................................................Signature of secretary of the meeting

Declared before me at . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .this . . . . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . .,19 . . . . . . . . . . . . . . . . . . . . . .

...............................................................Justice of the Peace, Notary Public

or Commissioner for Affidavits

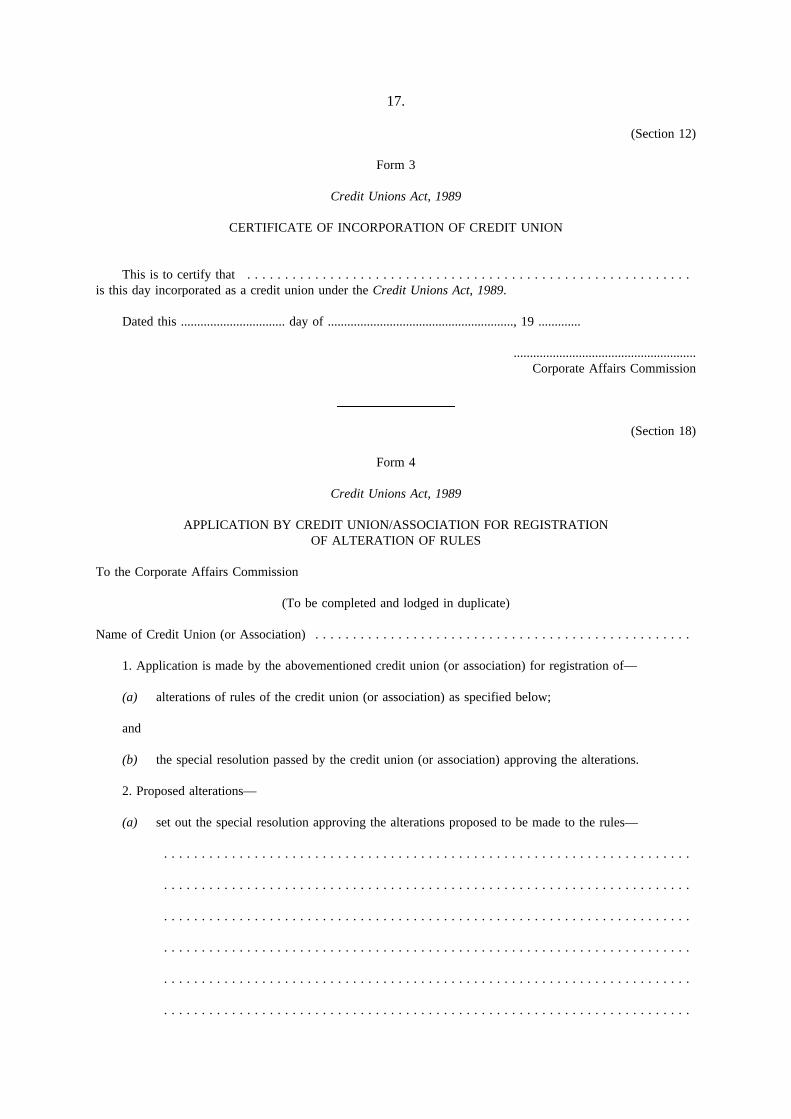

17.

(Section 12)

Form 3

Credit Unions Act, 1989

CERTIFICATE OF INCORPORATION OF CREDIT UNION

This is to certify that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .is this day incorporated as a credit union under the Credit Unions Act, 1989.

Dated this ................................ day of ........................................................., 19 .............

........................................................Corporate Affairs Commission

(Section 18)

Form 4

Credit Unions Act, 1989

APPLICATION BY CREDIT UNION/ASSOCIATION FOR REGISTRATIONOF ALTERATION OF RULES

To the Corporate Affairs Commission

(To be completed and lodged in duplicate)

Name of Credit Union (or Association) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Application is made by the abovementioned credit union (or association) for registration of—

(a) alterations of rules of the credit union (or association) as specified below;

and

(b) the special resolution passed by the credit union (or association) approving the alterations.

2. Proposed alterations—

(a) set out the special resolution approving the alterations proposed to be made to the rules—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

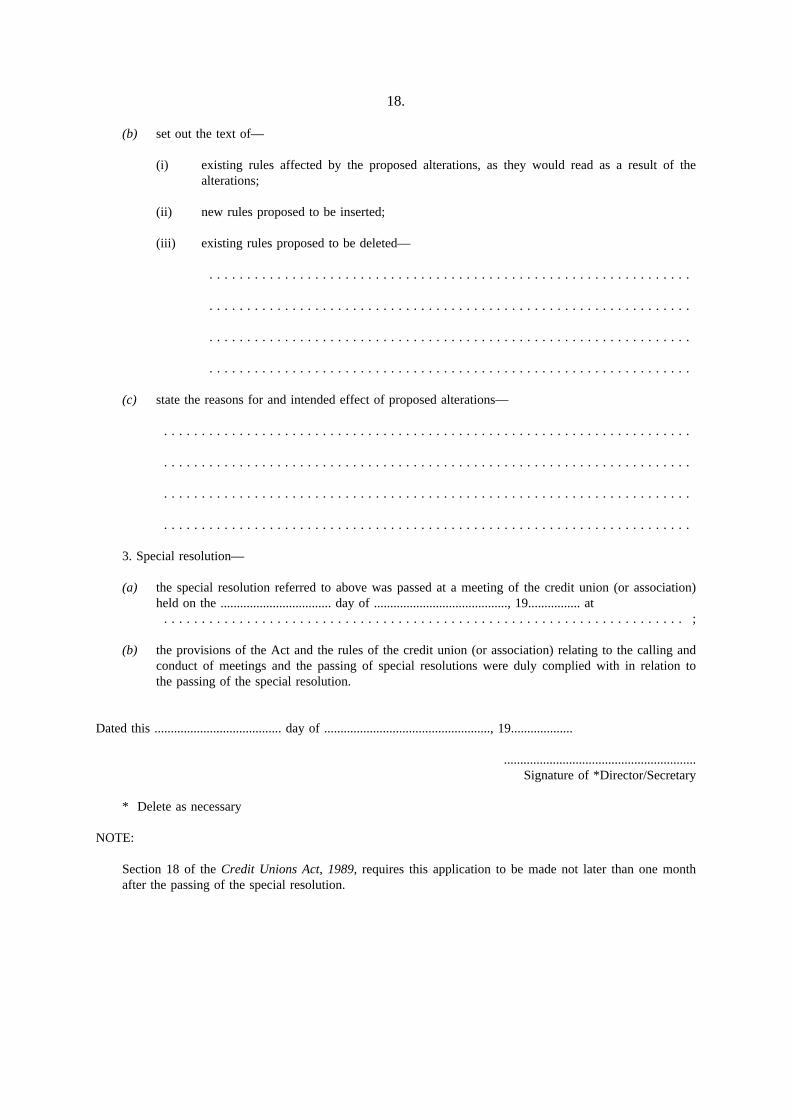

18.

(b) set out the text of—

(i) existing rules affected by the proposed alterations, as they would read as a result of thealterations;

(ii) new rules proposed to be inserted;

(iii) existing rules proposed to be deleted—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(c) state the reasons for and intended effect of proposed alterations—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. Special resolution—

(a) the special resolution referred to above was passed at a meeting of the credit union (or association)held on the .................................. day of ........................................., 19................ at

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ;

(b) the provisions of the Act and the rules of the credit union (or association) relating to the calling andconduct of meetings and the passing of special resolutions were duly complied with in relation tothe passing of the special resolution.

Dated this ....................................... day of ..................................................., 19...................

...........................................................Signature of *Director/Secretary

* Delete as necessary

NOTE:

Section 18 of the Credit Unions Act, 1989, requires this application to be made not later than one monthafter the passing of the special resolution.

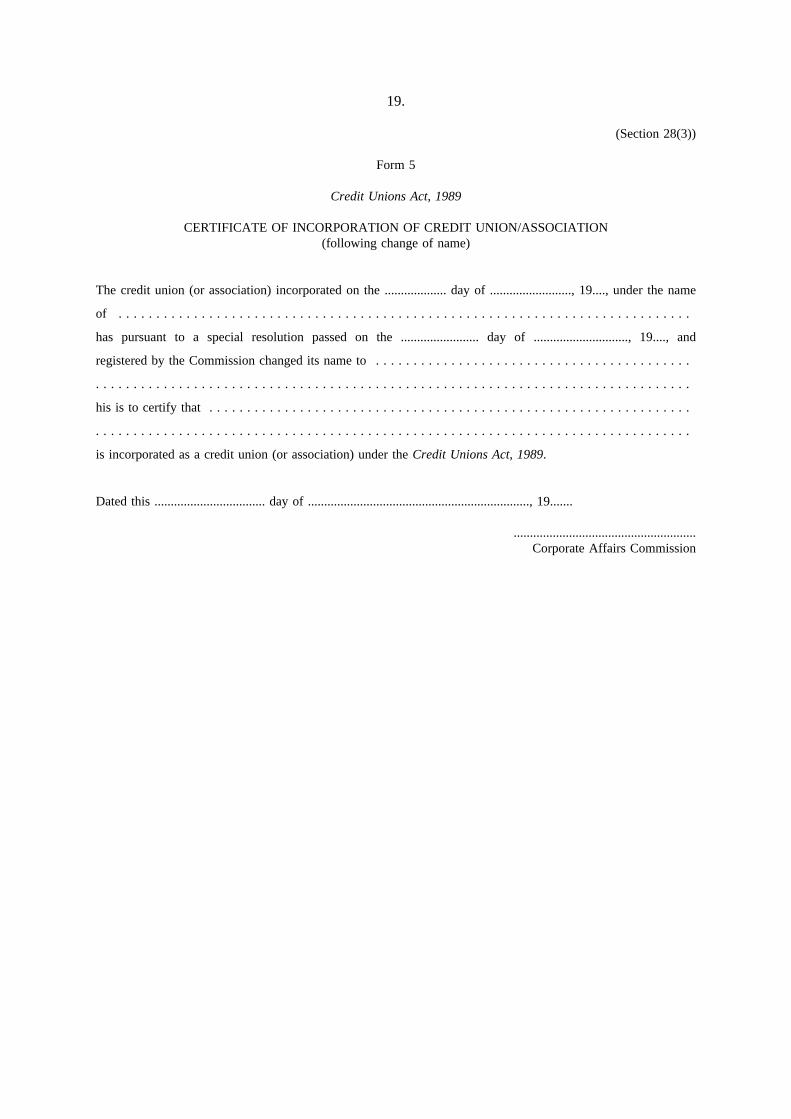

19.

(Section 28(3))

Form 5

Credit Unions Act, 1989

CERTIFICATE OF INCORPORATION OF CREDIT UNION/ASSOCIATION(following change of name)

The credit union (or association) incorporated on the ................... day of ........................., 19...., under the name

of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

has pursuant to a special resolution passed on the ........................ day of ............................., 19...., and

registered by the Commission changed its name to . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

his is to certify that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

is incorporated as a credit union (or association) under the Credit Unions Act, 1989.

Dated this .................................. day of ...................................................................., 19.......

........................................................Corporate Affairs Commission

20.

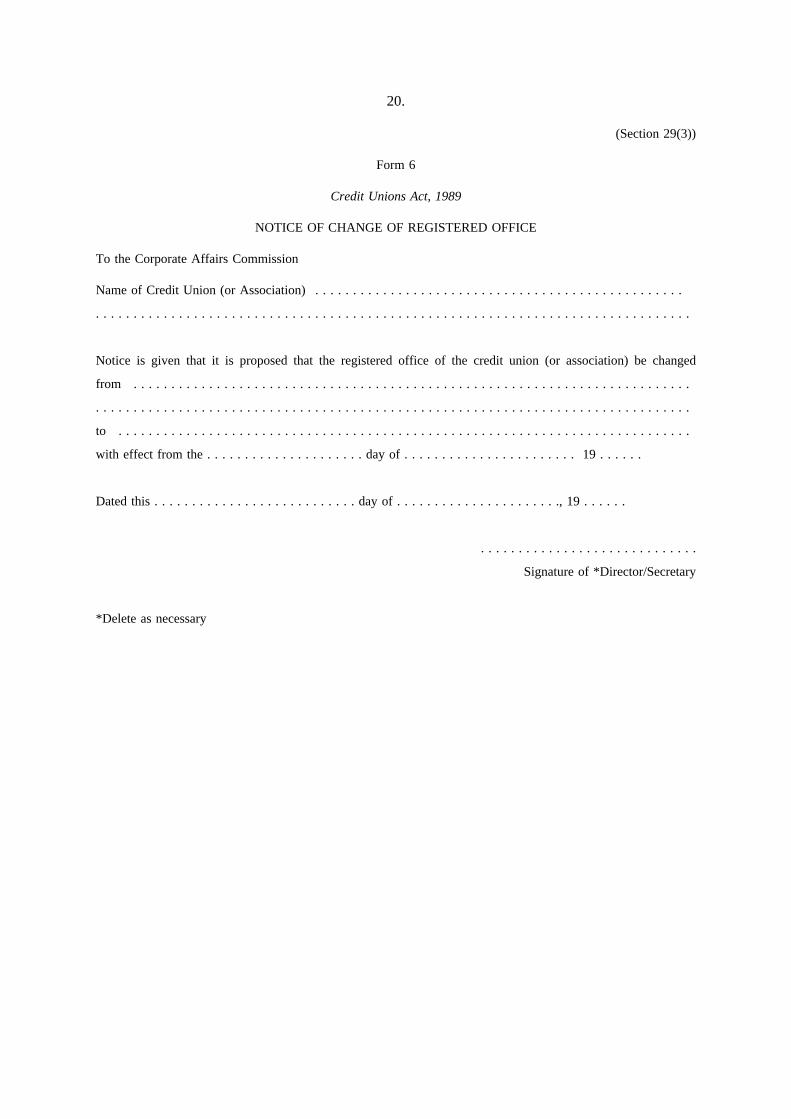

(Section 29(3))

Form 6

Credit Unions Act, 1989

NOTICE OF CHANGE OF REGISTERED OFFICE

To the Corporate Affairs Commission

Name of Credit Union (or Association) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Notice is given that it is proposed that the registered office of the credit union (or association) be changed

from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

to . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

with effect from the . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . . . . 19 . . . . . .

Dated this . . . . . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . . ., 19 . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Signature of *Director/Secretary

*Delete as necessary

21.

(Section 32)Form 7

Credit Unions Act, 1989

APPLICATION FOR REGISTRATION OF AMALGAMATION OF CREDITUNIONS OR ASSOCIATIONS

To the Corporate Affairs Commission

(To be completed and lodged in duplicate)

Name of Proposed Amalgamated Credit Union (or Association) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Application is made by the undermentioned credit unions (or associations) for registration under the namestated above of a credit union/association to be formed by amalgamation of the applicants—

(i) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(ii) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(iii) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(set out names of applicant credit unions/associations)

1. Attached are—

(a) a certified copy of the special resolution passed by each of the applicant credit unions/associationsapproving of the terms of amalgamation;

(b) two copies of the proposed rules or constitution of the amalgamated credit union/association signedby a director and secretary thereof;

(c) the certificates of incorporation of the applicant credit unions/associations.

2. Each local credit union/association concerned in the amalgamation has complied with the requirementsof section 32(5), (6) and (7) of the Credit Unions Act, 1989.

3. The registered office of the amalgamated credit union/association is to be at. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dated this . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . . . . . . . ., 19 . . . . . .

Signatures of a director and the secretary of each applicant:

Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Credit Union/Association . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Credit Union/Association . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Credit Union/Association . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

NOTE: If any of all of the certificates of incorporation cannot be produced, statutory declarations as to theloss must accompany this application.

(Section 33(1)(d))

22.

Form 8

Credit Unions Act, 1989

CERTIFICATE OF INCORPORATION ON AMALGAMATION—NEW LOCAL CREDITUNION/ASSOCIATION

This is to certify that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

is this day incorporated as a credit union (or association) under the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . . . . . ., 19 . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

(Section 33(1)(d))

Form 9

Credit Unions Act, 1989

CERTIFICATE OF AMALGAMATION—NEW LOCAL CREDIT UNION/ASSOCIATION

This is to certify that the credit union (or association) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

was formed by the amalgamation of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

and . . . . . . . . . . . . . . . . on this day under the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

23.

(Section 33(2)(d))Form 10

Credit Unions Act, 1989

CERTIFICATE OF REGISTRATION—NEW FOREIGN CREDIT UNION

This is to certify that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

was this day registered as a foreign credit union under Part III of the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . ., 19 . . . . . .

. . . . . . . . . . . . . . . . . . . . .Corporate Affairs Commission

(Section 33(2)(d))

Form 11

Credit Unions Act, 1989

CERTIFICATE OF AMALGAMATION—NEW FOREIGN CREDIT UNION

This is to certify that the foreign credit union . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

was formed by the amalgamation of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

and . . . . . . . . . . . . . . . . on this day under Part III of the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . ., 19 . . . . . . .

. . . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

24.

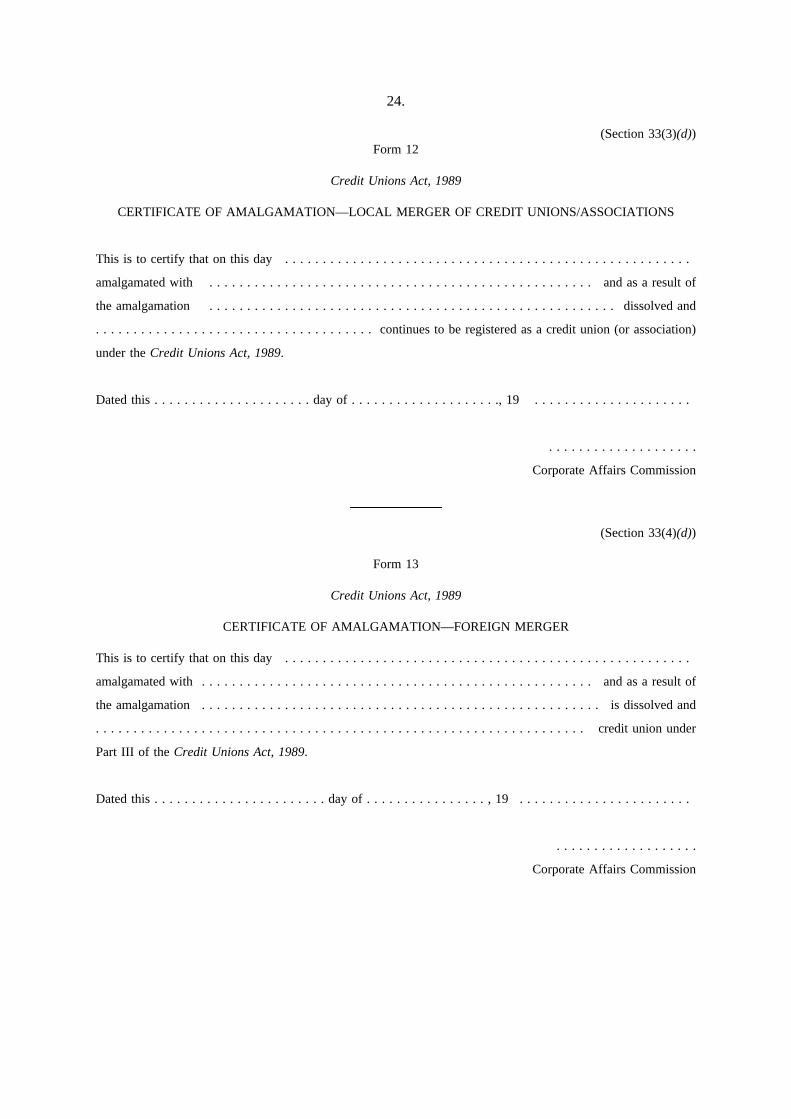

(Section 33(3)(d))Form 12

Credit Unions Act, 1989

CERTIFICATE OF AMALGAMATION—LOCAL MERGER OF CREDIT UNIONS/ASSOCIATIONS

This is to certify that on this day . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

amalgamated with . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . and as a result of

the amalgamation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . dissolved and

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . continues to be registered as a credit union (or association)

under the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

(Section 33(4)(d))

Form 13

Credit Unions Act, 1989

CERTIFICATE OF AMALGAMATION—FOREIGN MERGER

This is to certify that on this day . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

amalgamated with . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . and as a result of

the amalgamation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . is dissolved and

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . credit union under

Part III of the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

25.

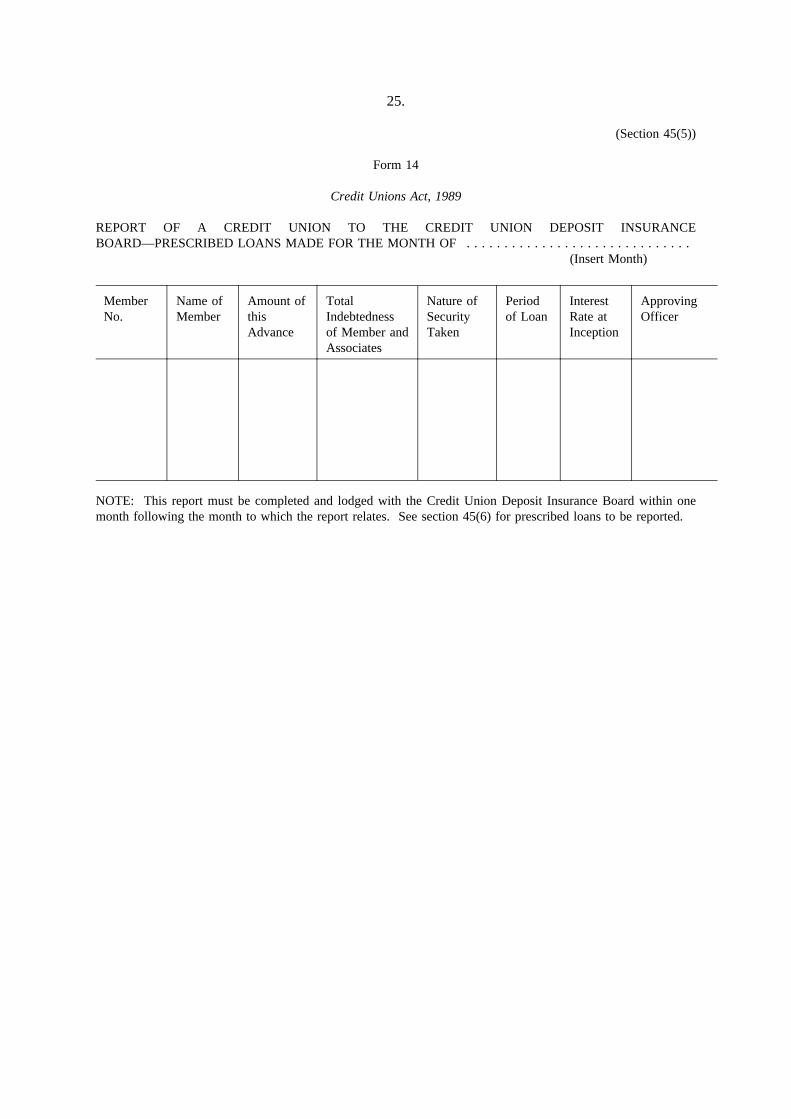

(Section 45(5))

Form 14

Credit Unions Act, 1989

REPORT OF A CREDIT UNION TO THE CREDIT UNION DEPOSIT INSURANCEBOARD—PRESCRIBED LOANS MADE FOR THE MONTH OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Insert Month)

MemberNo.

Name ofMember

Amount ofthisAdvance

TotalIndebtednessof Member andAssociates

Nature ofSecurityTaken

Periodof Loan

InterestRate atInception

ApprovingOfficer

NOTE: This report must be completed and lodged with the Credit Union Deposit Insurance Board within onemonth following the month to which the report relates. See section 45(6) for prescribed loans to be reported.

26.

(Section 56(1))

Form 15

Credit Unions Act, 1989

APPLICATION FOR REGISTRATION OF AN ASSOCIATION

To the Corporate Affairs Commission

(To be completed and lodged in duplicate)

Application is made by the credit unions whose common seals are affixed below for registration of anassociation under the name . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Accompanying this application are two copies of the rules proposed for the association signed on behalfof each applicant credit union by a director of the credit union.

2. The meeting to form the association was held on the ............. day of ......................... , 19....., and wasattended by ..... persons.

3. Not less than two representatives of each of the applicant credit unions were present at the formationmeeting and approved of the rules now being tendered for registration.

4. The association is to be formed for the following purposes:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Concise summary of objects).

5. The following persons were elected as directors of the association at the formation meeting:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Set out the full name, address and occupation of each such person and the name of the credit union ofwhich he or she is a member or officer.)

27.

6. Set out details of the share capital proposed for the association and the numbers of shares applied forby each applicant credit union—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. The person and the address to which communications relating to this application may be sent are—

(Name) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Address) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dated this . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . .

Common seals of applicant credit unions:

28.

(Section 56(2))

Form 16

Credit Unions Act, 1989

CERTIFICATE OF INCORPORATION OF AN ASSOCIATION

This is to certify that . . . . . . . . . . . . . . . . . is . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

this day incorporated as an association under the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .

Corporate Affairs Commission

(Section 74(5))

Form 17

Credit Unions Act, 1989

APPLICATION FOR REGISTRATION OF SPECIAL RESOLUTION(other than a special resolution altering the rules of a credit union or association)

To the Corporate Affairs Commission

Name of Credit Union (or Association) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Application is made by the abovementioned credit union (or association) for registration of a specialresolution as specified below.

2. Special Resolution—

(a) set out the special resolution—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(b) State the reasons for and intended effect of the special resolution—

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(c) The special resolution was passed at a meeting of the credit union (or association) held on the . . . .

. . . . . . . . . . . . . day of . . . . . . . . . . ., 19. . . . . . , at . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

29.

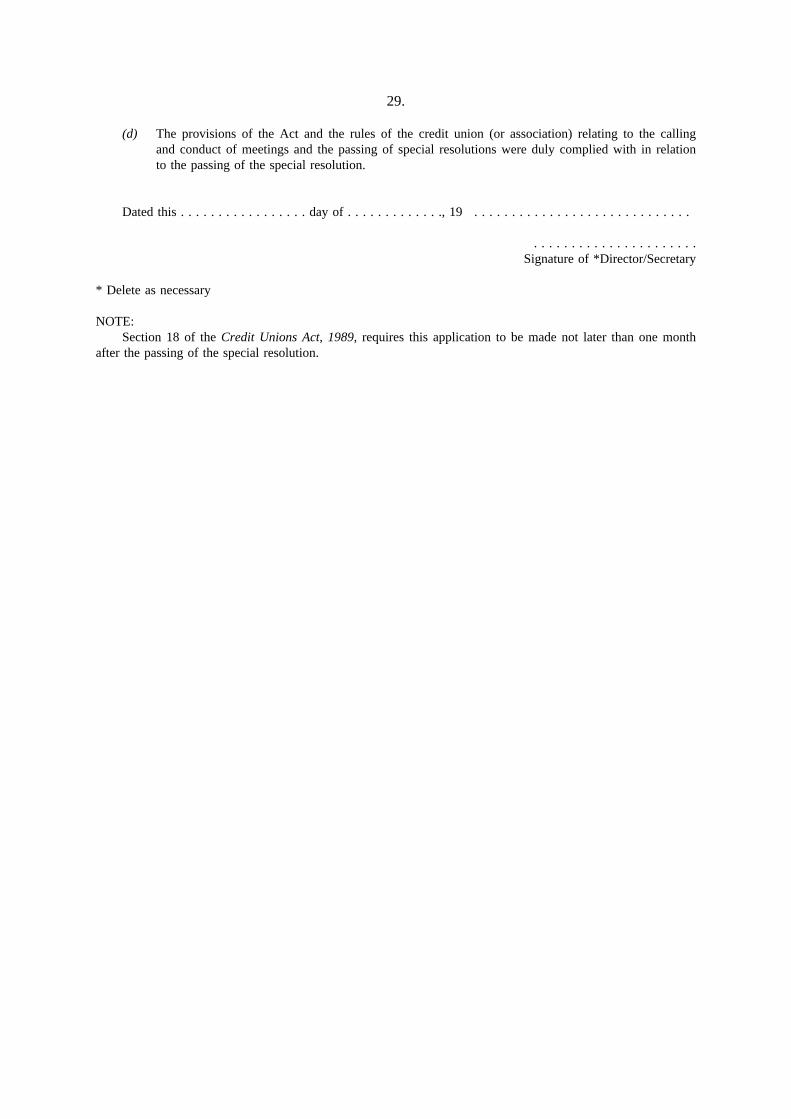

(d) The provisions of the Act and the rules of the credit union (or association) relating to the callingand conduct of meetings and the passing of special resolutions were duly complied with in relationto the passing of the special resolution.

Dated this . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .Signature of *Director/Secretary

* Delete as necessary

NOTE:Section 18 of the Credit Unions Act, 1989, requires this application to be made not later than one month

after the passing of the special resolution.

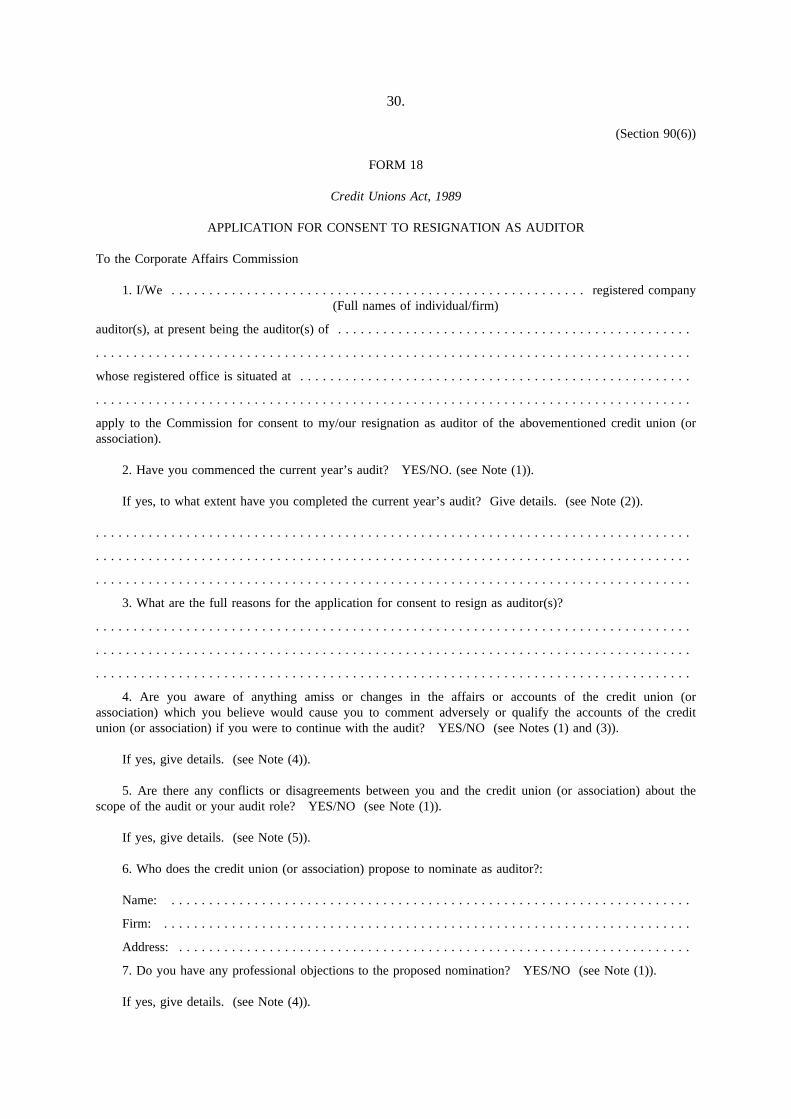

30.

(Section 90(6))

FORM 18

Credit Unions Act, 1989

APPLICATION FOR CONSENT TO RESIGNATION AS AUDITOR

To the Corporate Affairs Commission

1. I/We . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . registered company(Full names of individual/firm)

auditor(s), at present being the auditor(s) of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

whose registered office is situated at . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

apply to the Commission for consent to my/our resignation as auditor of the abovementioned credit union (orassociation).

2. Have you commenced the current year’s audit? YES/NO. (see Note (1)).

If yes, to what extent have you completed the current year’s audit? Give details. (see Note (2)).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. What are the full reasons for the application for consent to resign as auditor(s)?

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Are you aware of anything amiss or changes in the affairs or accounts of the credit union (orassociation) which you believe would cause you to comment adversely or qualify the accounts of the creditunion (or association) if you were to continue with the audit? YES/NO (see Notes (1) and (3)).

If yes, give details. (see Note (4)).

5. Are there any conflicts or disagreements between you and the credit union (or association) about thescope of the audit or your audit role? YES/NO (see Note (1)).

If yes, give details. (see Note (5)).

6. Who does the credit union (or association) propose to nominate as auditor?:

Name: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Firm: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Address: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. Do you have any professional objections to the proposed nomination? YES/NO (see Note (1)).

If yes, give details. (see Note (4)).

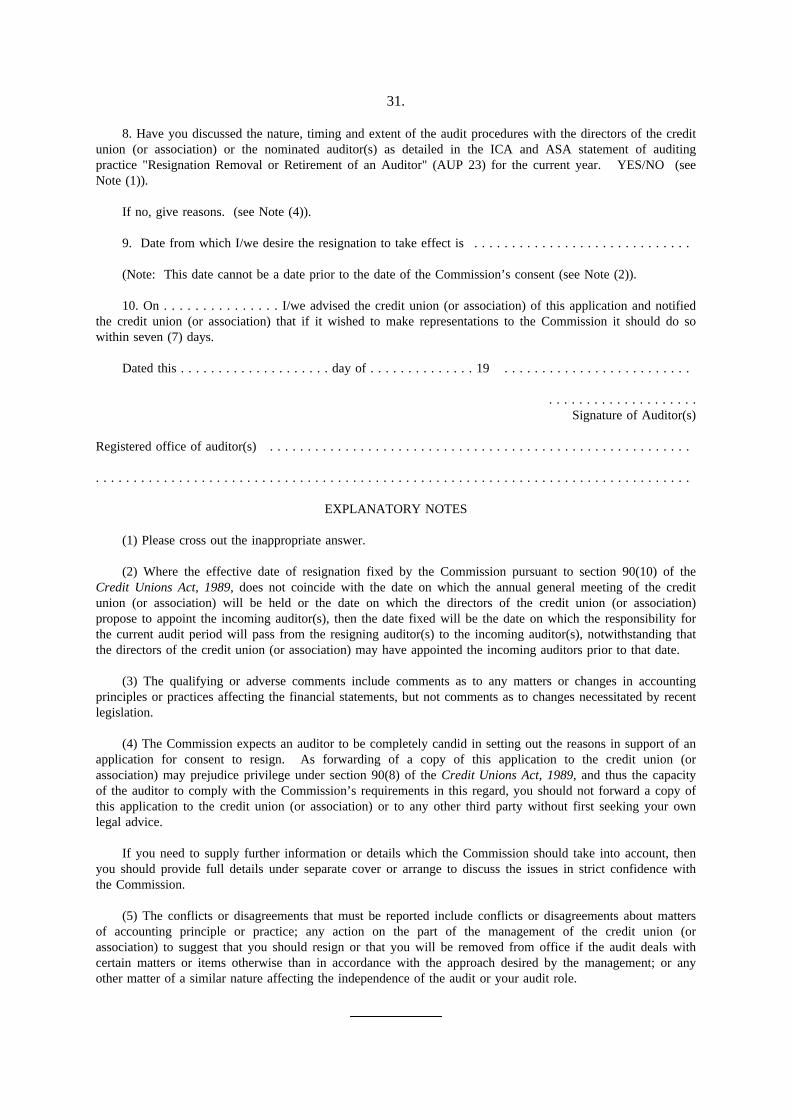

31.

8. Have you discussed the nature, timing and extent of the audit procedures with the directors of the creditunion (or association) or the nominated auditor(s) as detailed in the ICA and ASA statement of auditingpractice "Resignation Removal or Retirement of an Auditor" (AUP 23) for the current year. YES/NO (seeNote (1)).

If no, give reasons. (see Note (4)).

9. Date from which I/we desire the resignation to take effect is . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Note: This date cannot be a date prior to the date of the Commission’s consent (see Note (2)).

10. On . . . . . . . . . . . . . . . I/we advised the credit union (or association) of this application and notifiedthe credit union (or association) that if it wished to make representations to the Commission it should do sowithin seven (7) days.

Dated this . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . 19 . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .Signature of Auditor(s)

Registered office of auditor(s) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

EXPLANATORY NOTES

(1) Please cross out the inappropriate answer.

(2) Where the effective date of resignation fixed by the Commission pursuant to section 90(10) of theCredit Unions Act, 1989, does not coincide with the date on which the annual general meeting of the creditunion (or association) will be held or the date on which the directors of the credit union (or association)propose to appoint the incoming auditor(s), then the date fixed will be the date on which the responsibility forthe current audit period will pass from the resigning auditor(s) to the incoming auditor(s), notwithstanding thatthe directors of the credit union (or association) may have appointed the incoming auditors prior to that date.

(3) The qualifying or adverse comments include comments as to any matters or changes in accountingprinciples or practices affecting the financial statements, but not comments as to changes necessitated by recentlegislation.

(4) The Commission expects an auditor to be completely candid in setting out the reasons in support of anapplication for consent to resign. As forwarding of a copy of this application to the credit union (orassociation) may prejudice privilege under section 90(8) of the Credit Unions Act, 1989, and thus the capacityof the auditor to comply with the Commission’s requirements in this regard, you should not forward a copy ofthis application to the credit union (or association) or to any other third party without first seeking your ownlegal advice.

If you need to supply further information or details which the Commission should take into account, thenyou should provide full details under separate cover or arrange to discuss the issues in strict confidence withthe Commission.

(5) The conflicts or disagreements that must be reported include conflicts or disagreements about mattersof accounting principle or practice; any action on the part of the management of the credit union (orassociation) to suggest that you should resign or that you will be removed from office if the audit deals withcertain matters or items otherwise than in accordance with the approach desired by the management; or anyother matter of a similar nature affecting the independence of the audit or your audit role.

32.

(Section 90(12))

FORM 19

Credit Unions Act, 1989

NOTICE OF RESIGNATION, RETIREMENT, WITHDRAWAL OR REMOVAL OF AUDITOR

To the Corporate Affairs Commission

Re: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Name of credit union or association)

Notice is given that—

*On the . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . . . . . .

notice was received of the resignation of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Name of auditor or audit firm)

as auditor of this credit union/association. The Commission consented to the resignation on

the . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

*On the . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . . . . . . . .

notice was received of the *retirement/withdrawal of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Name of auditor or audit firm)

as auditor of this credit union/association.

*On the . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Name of auditor or audit firm)

was removed as auditor of this credit union/association.

Dated this . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .Signature of *Director/Secretary

* Delete as necessary

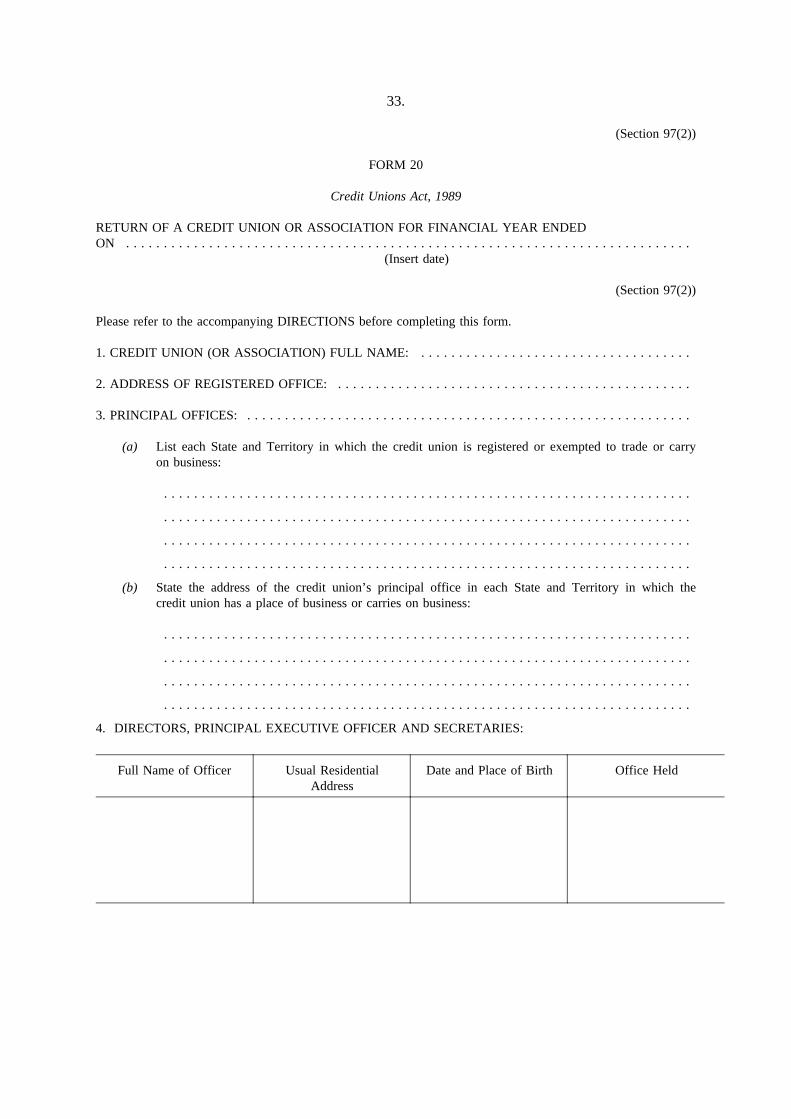

33.

(Section 97(2))

FORM 20

Credit Unions Act, 1989

RETURN OF A CREDIT UNION OR ASSOCIATION FOR FINANCIAL YEAR ENDEDON . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Insert date)

(Section 97(2))

Please refer to the accompanying DIRECTIONS before completing this form.

1. CREDIT UNION (OR ASSOCIATION) FULL NAME: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. ADDRESS OF REGISTERED OFFICE: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. PRINCIPAL OFFICES: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(a) List each State and Territory in which the credit union is registered or exempted to trade or carryon business:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(b) State the address of the credit union’s principal office in each State and Territory in which thecredit union has a place of business or carries on business:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. DIRECTORS, PRINCIPAL EXECUTIVE OFFICER AND SECRETARIES:

Full Name of Officer Usual ResidentialAddress

Date and Place of Birth Office Held

34.

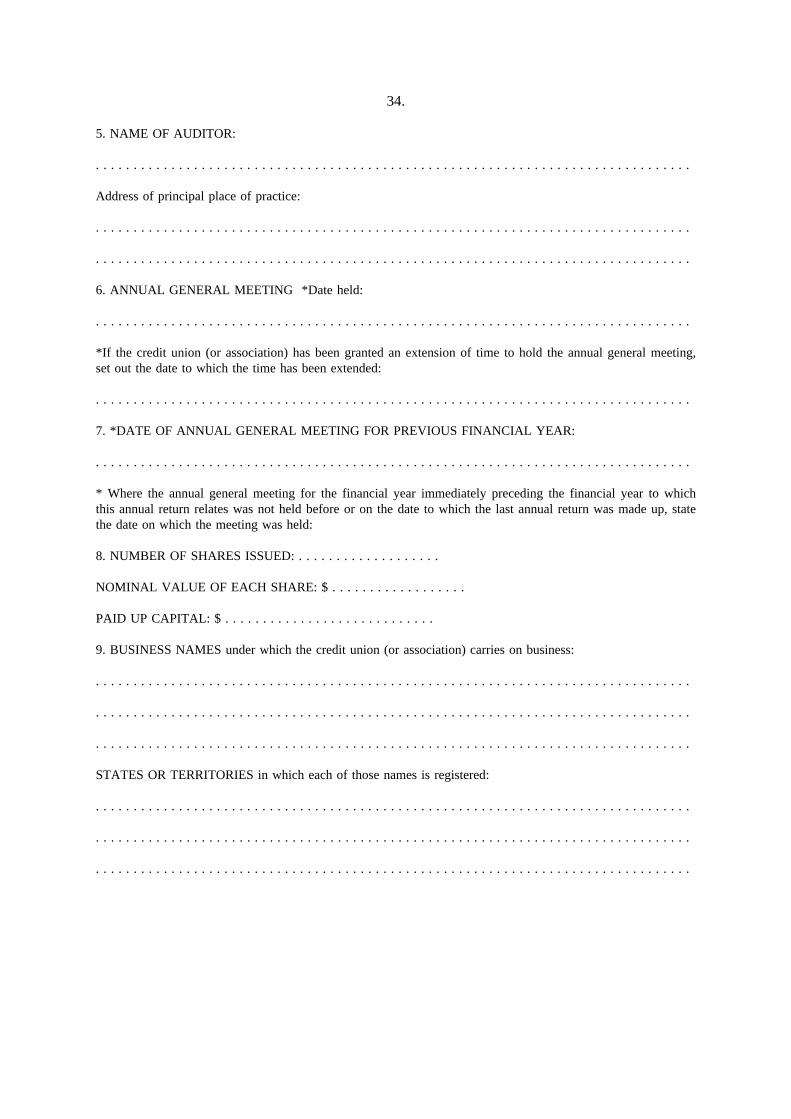

5. NAME OF AUDITOR:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Address of principal place of practice:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. ANNUAL GENERAL MEETING *Date held:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

*If the credit union (or association) has been granted an extension of time to hold the annual general meeting,set out the date to which the time has been extended:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. *DATE OF ANNUAL GENERAL MEETING FOR PREVIOUS FINANCIAL YEAR:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

* Where the annual general meeting for the financial year immediately preceding the financial year to whichthis annual return relates was not held before or on the date to which the last annual return was made up, statethe date on which the meeting was held:

8. NUMBER OF SHARES ISSUED: . . . . . . . . . . . . . . . . . . .

NOMINAL VALUE OF EACH SHARE: $ . . . . . . . . . . . . . . . . . .

PAID UP CAPITAL: $ . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9. BUSINESS NAMES under which the credit union (or association) carries on business:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

STATES OR TERRITORIES in which each of those names is registered:

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

35.

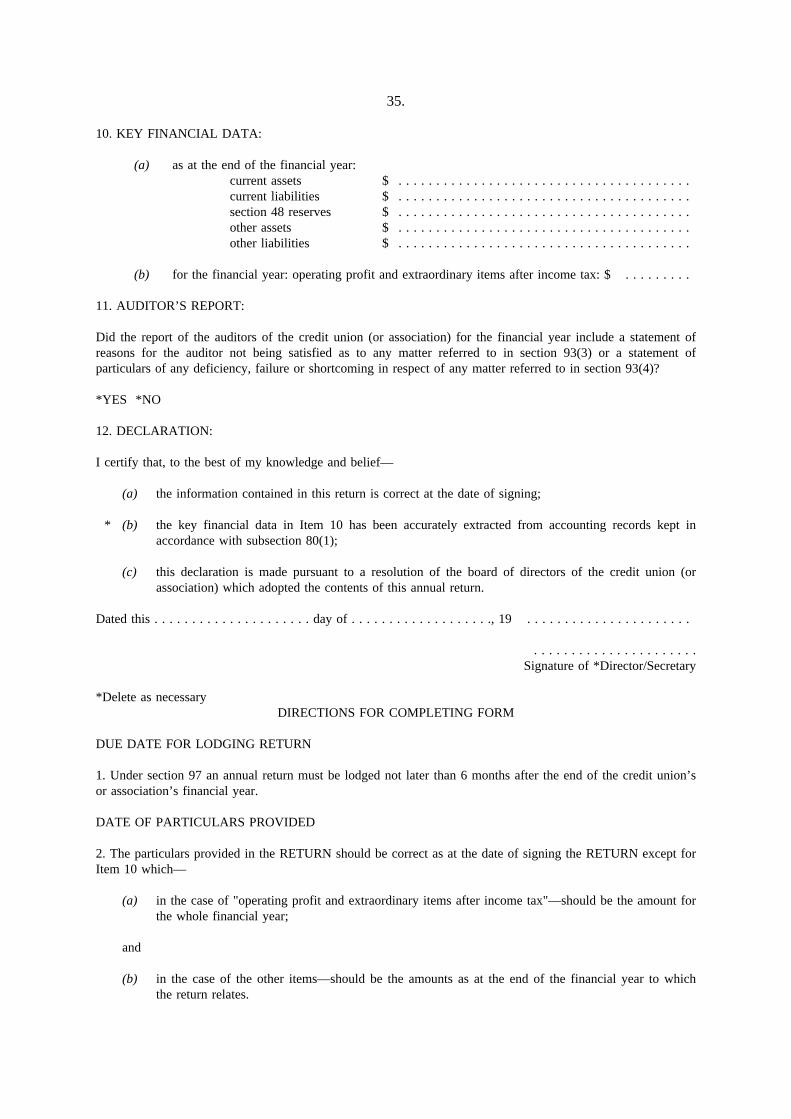

10. KEY FINANCIAL DATA:

(a) as at the end of the financial year:current assets $ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .current liabilities $ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .section 48 reserves $ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .other assets $ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .other liabilities $ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(b) for the financial year: operating profit and extraordinary items after income tax: $ . . . . . . . . .

11. AUDITOR’S REPORT:

Did the report of the auditors of the credit union (or association) for the financial year include a statement ofreasons for the auditor not being satisfied as to any matter referred to in section 93(3) or a statement ofparticulars of any deficiency, failure or shortcoming in respect of any matter referred to in section 93(4)?

*YES *NO

12. DECLARATION:

I certify that, to the best of my knowledge and belief—

(a) the information contained in this return is correct at the date of signing;

* (b) the key financial data in Item 10 has been accurately extracted from accounting records kept inaccordance with subsection 80(1);

(c) this declaration is made pursuant to a resolution of the board of directors of the credit union (orassociation) which adopted the contents of this annual return.

Dated this . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .Signature of *Director/Secretary

*Delete as necessaryDIRECTIONS FOR COMPLETING FORM

DUE DATE FOR LODGING RETURN

1. Under section 97 an annual return must be lodged not later than 6 months after the end of the credit union’sor association’s financial year.

DATE OF PARTICULARS PROVIDED

2. The particulars provided in the RETURN should be correct as at the date of signing the RETURN except forItem 10 which—

(a) in the case of "operating profit and extraordinary items after income tax"—should be the amount forthe whole financial year;

and

(b) in the case of the other items—should be the amounts as at the end of the financial year to whichthe return relates.

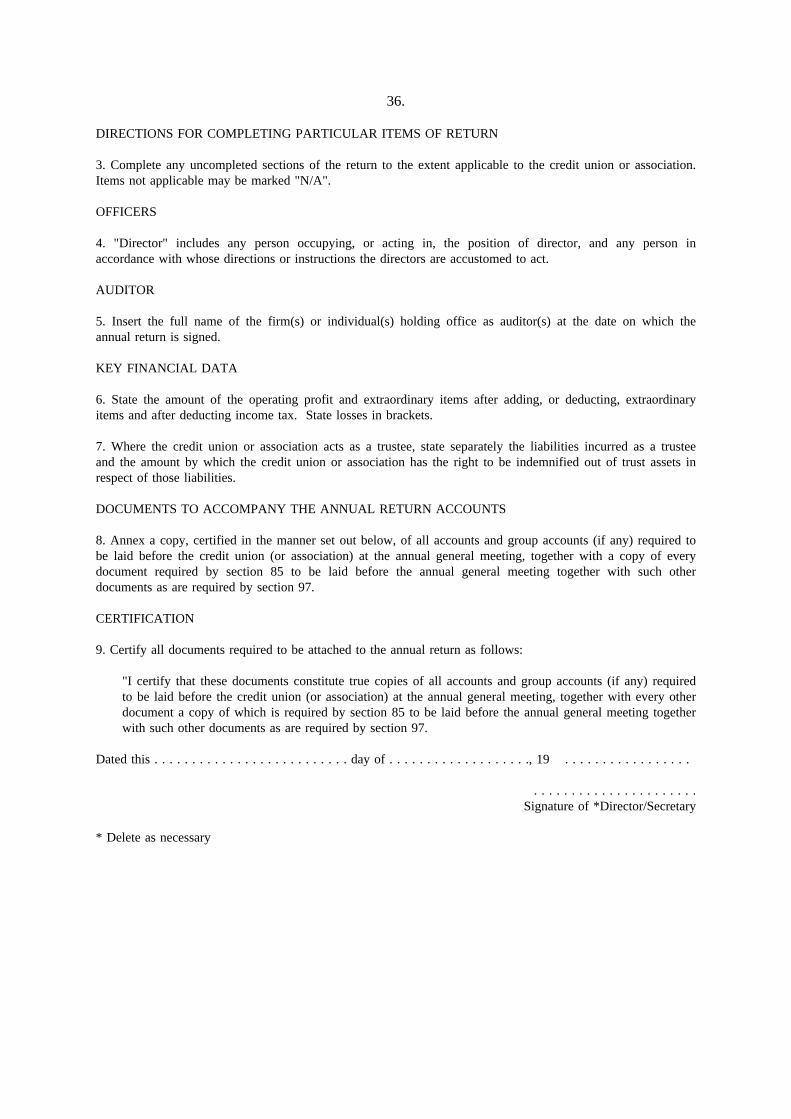

36.

DIRECTIONS FOR COMPLETING PARTICULAR ITEMS OF RETURN

3. Complete any uncompleted sections of the return to the extent applicable to the credit union or association.Items not applicable may be marked "N/A".

OFFICERS

4. "Director" includes any person occupying, or acting in, the position of director, and any person inaccordance with whose directions or instructions the directors are accustomed to act.

AUDITOR

5. Insert the full name of the firm(s) or individual(s) holding office as auditor(s) at the date on which theannual return is signed.

KEY FINANCIAL DATA

6. State the amount of the operating profit and extraordinary items after adding, or deducting, extraordinaryitems and after deducting income tax. State losses in brackets.

7. Where the credit union or association acts as a trustee, state separately the liabilities incurred as a trusteeand the amount by which the credit union or association has the right to be indemnified out of trust assets inrespect of those liabilities.

DOCUMENTS TO ACCOMPANY THE ANNUAL RETURN ACCOUNTS

8. Annex a copy, certified in the manner set out below, of all accounts and group accounts (if any) required tobe laid before the credit union (or association) at the annual general meeting, together with a copy of everydocument required by section 85 to be laid before the annual general meeting together with such otherdocuments as are required by section 97.

CERTIFICATION

9. Certify all documents required to be attached to the annual return as follows:

"I certify that these documents constitute true copies of all accounts and group accounts (if any) requiredto be laid before the credit union (or association) at the annual general meeting, together with every otherdocument a copy of which is required by section 85 to be laid before the annual general meeting togetherwith such other documents as are required by section 97.

Dated this . . . . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . ., 19 . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .Signature of *Director/Secretary

* Delete as necessary

37.

(Section 127(1))

FORM 21

Credit Unions Act, 1989

APPLICATION FOR REGISTRATION OF A FOREIGN CREDIT UNION

To the Corporate Affairs Commission

(To be completed and lodged in duplicate)

Application is made by . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Insert name of foreign credit union)

for registration as a foreign credit union under the name

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Accompanying this application are—

(a) a copy of the certificate of incorporation or registration issued in respect of the credit union by theappropriate authority in the State or Territory of the credit union’s origin, certified by that authority;

(b) a copy of the rules or constitution of the credit union and a copy of the last audited balance sheet ofthe credit union, in each case certified by at least two of the directors of the credit union;

(c) the following, verified in the manner prescribed in regulation 25:

(i) the full name, address and occupation of each director of the credit union;

(ii) the full name and address of each person who will act as an agent of the credit union inthis State;

(iii) the address of the proposed registered office of the credit union in this State;

and

(iv) a copy of an instrument appointing a person resident in this State (not being a bodycorporate incorporated outside this State) as a person on whom all notices or legal processmay be served on behalf of the credit union.

2. The person to whom and the address to which communications relating to this application may be sentare—

(Name) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Address) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dated this . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .Signature of Director/Secretary

* Delete as necessary(Section 127(3))

38.

FORM 22

Credit Unions Act, 1989

CERTIFICATE OF REGISTRATION OF FOREIGN CREDIT UNION

This is to certify that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .is this day registered as a foreign credit union under Part IX of the Credit Unions Act, 1989.

Dated this . . . . . . . . . . . . . . . . . . . . . . . day of . . . . . . . . . . . . . . . . , 19 . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .Corporate Affairs Commission

39.

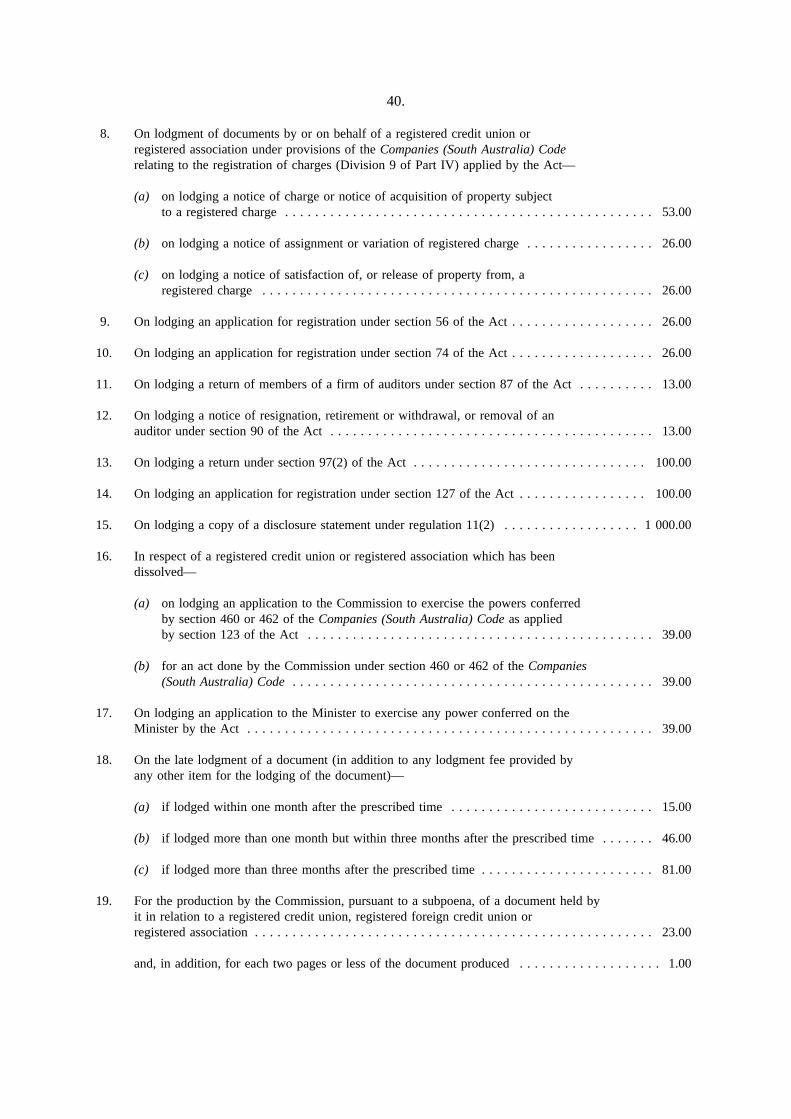

SCHEDULE 2

Regulation 6

FEES

Item Matter Amount$

PART A

To be paid to the Commission—

1. For inspection under section 6(2) of the Act of documents lodged by or inrelation to a registered credit union, registered foreign credit union orregistered association (other than an inspection by or on behalf of theAustralian Broadcasting Corporation, the Australian Bureau of Statistics,the holder of a licence for a commercial broadcasting or television station,or the proprietor or publisher of a newspaper generally available to thepublic otherwise than only on subscription) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.00

2. For the supply of an uncertified copy or extract of a document lodged byor on behalf of a registered credit union, registered foreign credit unionor registered association, in addition to the fee payable under item 1 . . . . . . . . . . . . . . . . . . . . . 3.00

3. For the supply of a certified copy of, or the supply of a certified copyof an extract from, a document held by the Commission in relation to aregistered credit union, registered foreign credit union or registeredassociation—

for one page . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.00for each additional page . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50