Embed Size (px)

Citation preview

SOUTH AFRICA CONNECT:FUNDING MODELS

Presented at the South African Department of Communications Broadband Workshop

Pretoria, November 11, 2013

Bronwyn Howell, General Manager

CORPORATE MEMBERS

Contact Energy

Fonterra Co-Operative Dairy

Group

Meridian Energy

Powerco

Telecom Corporation of New

Zealand Ltd

Victoria University of Wellington

Westpac Institutional Bank

OVERVIEW

South Africa Connect – a good starting point– awareness of the importance of both supply and demand– some clear, achievable objectives

What can be learned from other countries?– funding models must take account of sector complexity,

dynamism and interaction – Government has a powerful influence on sector performance

• regulator, customer, infrastructure owner/investor

– strong, independent policy and regulatory institutions required, regardless of the specific funding models deployed

• activities of all must be aligned with overarching policy objectives• long-term nature of investments necessitates confidence in consistency

of policy and its implementation/enforcement

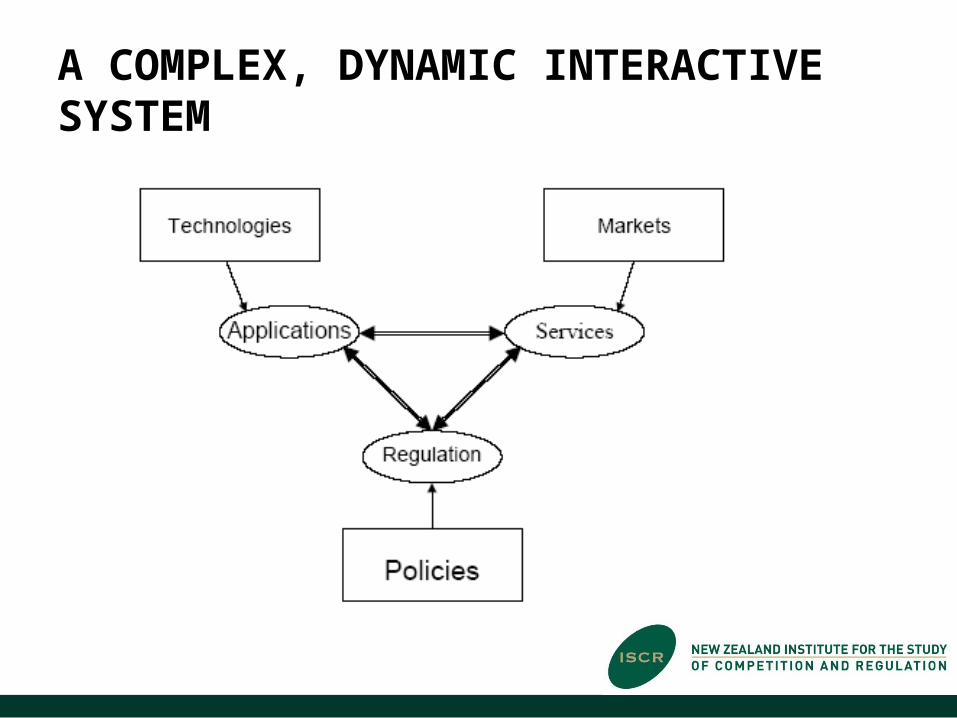

A COMPLEX, DYNAMIC INTERACTIVE SYSTEM

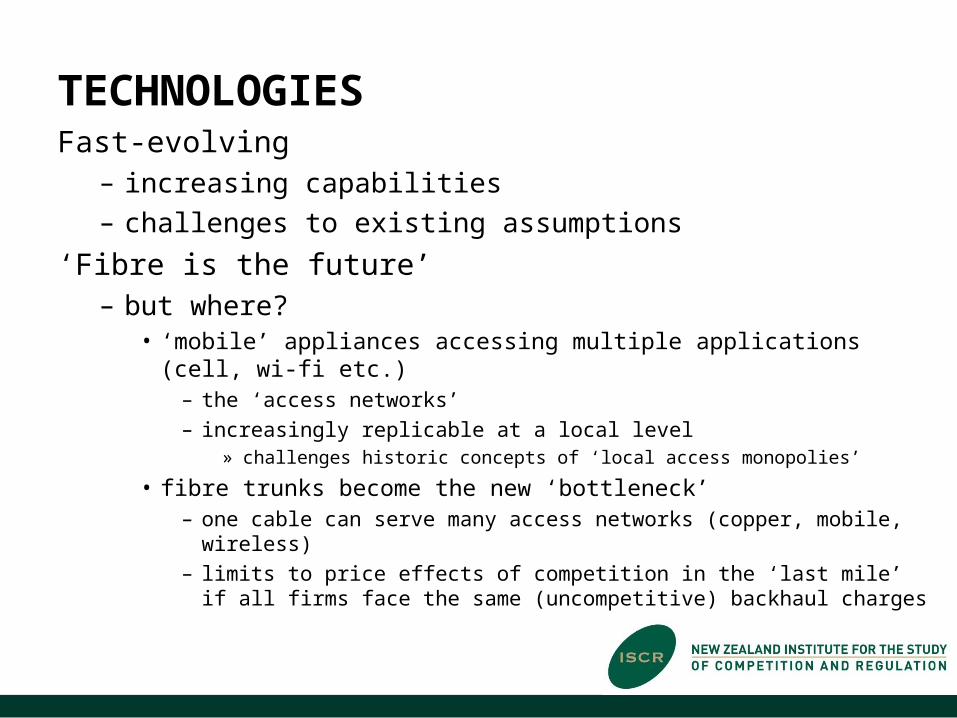

TECHNOLOGIESFast-evolving

– increasing capabilities– challenges to existing assumptions

‘Fibre is the future’– but where?

• ‘mobile’ appliances accessing multiple applications (cell, wi-fi etc.)– the ‘access networks’– increasingly replicable at a local level

» challenges historic concepts of ‘local access monopolies’

• fibre trunks become the new ‘bottleneck’ – one cable can serve many access networks (copper, mobile, wireless)– limits to price effects of competition in the ‘last mile’ if all firms face the

same (uncompetitive) backhaul charges

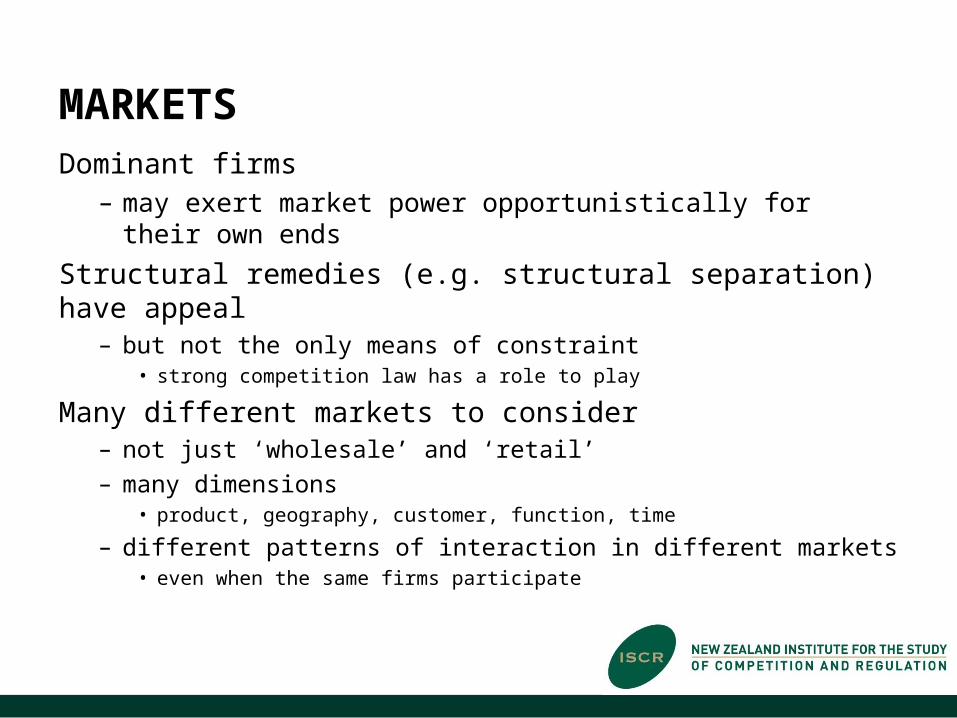

MARKETSDominant firms

– may exert market power opportunistically for their own ends

Structural remedies (e.g. structural separation) have appeal– but not the only means of constraint

• strong competition law has a role to play

Many different markets to consider– not just ‘wholesale’ and ‘retail’– many dimensions

• product, geography, customer, function, time

– different patterns of interaction in different markets• even when the same firms participate

POLICY

Regulation– rules that govern interactions across the entire system

• not just confined to market management

Effective regulation– oversees interactions in a manner that delivers policy objectives– requires

• clear, transparent purpose, independent of political considerations• empowering legislative framework • comprehensive mandate across all elements of system• consistent, cohesive instruments aligned to delivering objectives• resourcing (human capital as well as financial funding)

ALIGNING POLICY AND REGULATORY INSTRUMENTS TO FUNDING MECHANISMS

Lessons from other jurisdictions– Australia– New Zealand

Key issues:– structural separation– government funding

STRUCTURAL SEPARATIONAn appealing means of constraining a dominant vertically-integrated incumbent (most stringent form of access regulation)But a remedy of last resort, not first recourse

– assumes no improvement of existing regulatory framework possible – necessarily higher costs, as forfeits many benefits of vertical integration– targets a firm, not markets; assumes enduring, intractable dominance

• problematic when potential and actual infrastructure competition varies widely across different markets

It increases (rather than reduces) policy, regulatory responsibilities – high potential for co-ordination gaps

• Australia => disconnection between deployment and retail effort – delaying rather than accelerating fibre take-up

• New Zealand => no-one taking responsibility for sector strategic development – confused objectives, inconsistent and contradictory actions by firms (incl. government) and regulator(s)

GOVERNMENT FUNDING

Unless there is no infrastructure present, then inevitably impinges on existing competitive interaction

– decision to invest must be based upon• a full project cost-benefit assessment• a detailed competitive analysis

– with dynamic counterfactual (the status quo is not static)

– again, necessitates strong, independent, well-resourced and capable regulatory and policy institutions

• economic and competitive implications of politically-motivated funding interventions must be tested

– did not occur in Australia, New Zealand• EU State Aid provisions provide an effective set of checks • increased regulatory responsibility

PUBLIC-PRIVATE PARTNERSHIPSSeem an appealing way to proceed when government cannot fully fund a project

– roads, prisons, schools, etc.

BUT important considerations about form of partnership– private sector builds, operates for government

• ‘private’ networks operated for schools, medical facilities etc• long term bespoke contractual agreements

– government underwrites construction, utilisation risk

– government pays for network transferred to private sector• ‘public’ access networks; associated regulatory provisions apply• government underwrites demand risk• but private partner exposed to regulatory, political risk

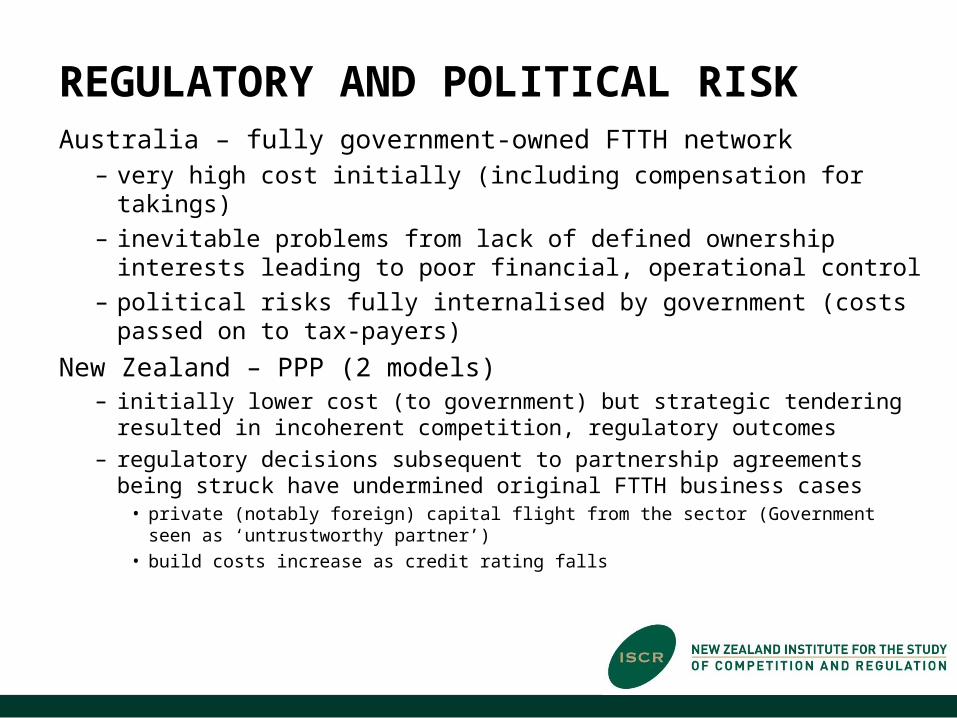

REGULATORY AND POLITICAL RISK Australia – fully government-owned FTTH network

– very high cost initially (including compensation for takings)– inevitable problems from lack of defined ownership interests leading to

poor financial, operational control– political risks fully internalised by government (costs passed on to tax-

payers)

New Zealand – PPP (2 models)– initially lower cost (to government) but strategic tendering resulted in

incoherent competition, regulatory outcomes – regulatory decisions subsequent to partnership agreements being struck have

undermined original FTTH business cases• private (notably foreign) capital flight from the sector (Government seen as ‘untrustworthy

partner’)• build costs increase as credit rating falls

IMPLICATIONS FOR SOUTH AFRICAPolicy delivery requires strong, independent, effective policy and regulatory institutions

– changes to industry structure, funding models cannot make up for the consequences of weak or ineffective policy and regulatory institutions

Not clear that of all avenues available under existing regulatory provisions have been exhausted

– structural changes are very difficult to reverse; institutional ones are more malleable

– a good starting point would be to strengthen existing regulatory and policy institutions

– can then proceed further with greater confidence that the full ramifications of proposed policy tools have been independently and effectively assessed and understood