Embed Size (px)

Citation preview

1

Sources of Inflation Dynamics in Japan: AS-AD and Monetary Policy Effectiveness

Seiji Komine, University of Wisconsin-Madison

Department of Economics

Abstract

Using a simple macroeconomic model, this paper inspects the driving factors of deflation long

observed in Japan, and accordingly, it assesses the effectiveness of monetary policy, including the

very recent policy instruments the BOJ has employed, such as Quantitative Easing (QE), Yield-Curve-

Control, and negative interest rates.

More specifically, I decompose the historical inflation dynamics into four components by sources,

using identified structural residuals from a SVAR model of AS-AD framework with two monetary

policy benchmarks: Taylor rule and Fisher’s equation of exchange. Then, I discuss lessons for

monetary policy, looking at the coordination of the impulse responses and structural shocks folded

inside the historical decomposition.

The empirical results suggest the following inferences. 1) Long-run inflation dynamics is pushed by

AS shocks, while short-run fluctuations are motivated by other structural deviations. 2) QE is now

possibly getting excessive and losing its efficiency, while monetary easing by interest rates performs

relatively well. This claim is reasoned from those observations: 2-a) It is likely there exist effective

channels (significant impulse responses), respectively for both of the policy instruments. When

sizes of impulses in each type of policy are sufficient to stimulate the system or enough large

according to the market surroundings, the inflation rates response significantly; 2-b) However, that

does not necessarily mean all the recent BOJ’s trials are effective. The variances in structural money

supply shocks are decreasing in these years, reflecting that the BOJ is losing control on money

supply in the saturated monetary environment.

* This paper is written for the semester work for Econ706, Fall 2017 at UW-Madison.

I would like to thank Professor Bruce Hansen at UW-Madison for helpful comments.

All analysis is made with the software EViews 10.

2

1. Introduction

1.1. Background story

“Japanese economy is kind of mystery.”

Deflation, for a long time beyond the last couple of decades (“Lost Decades”), Japanese economy

has experienced. I do not know how many discussions on this topic were made by outstanding

economists in and outside the country. Still it does not seem that we have achieved consensus on

several related questions.

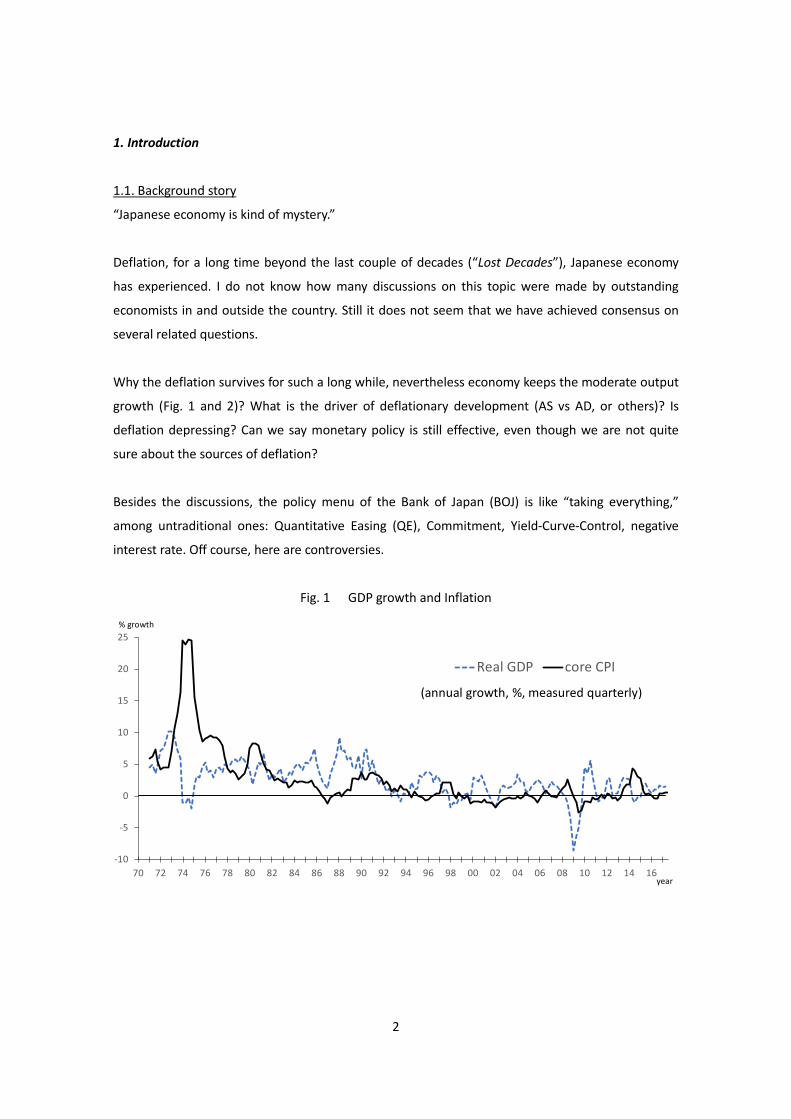

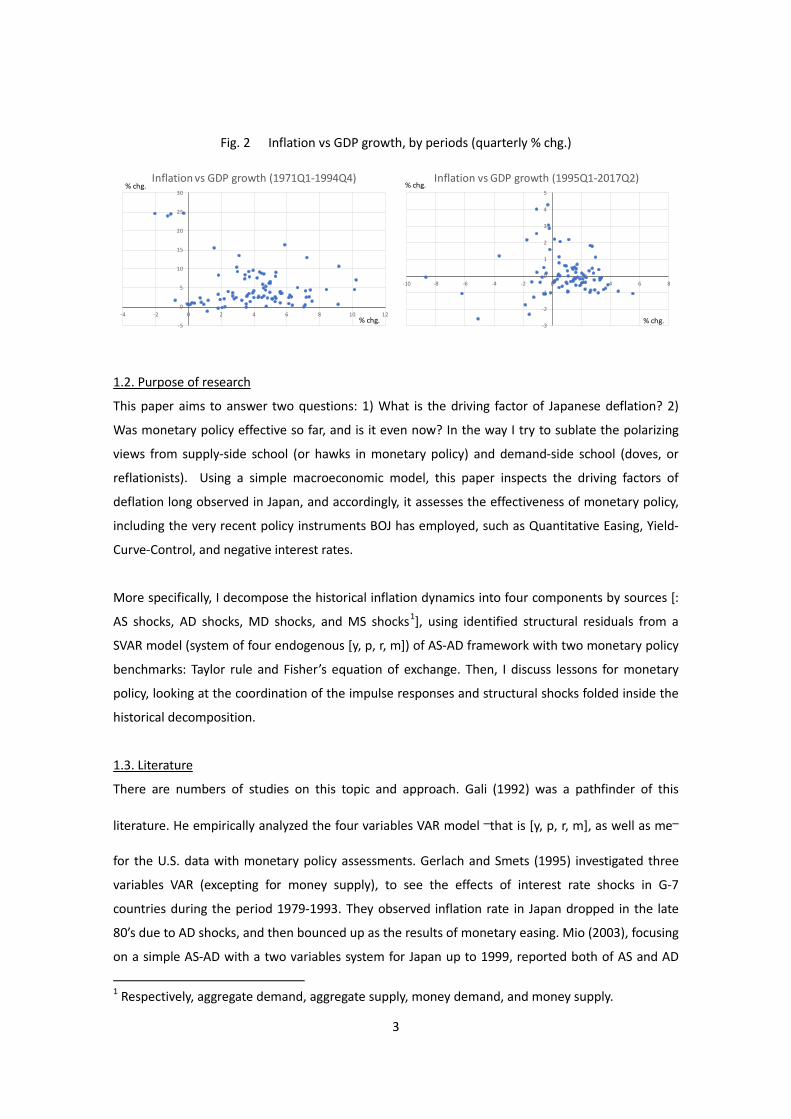

Why the deflation survives for such a long while, nevertheless economy keeps the moderate output

growth (Fig. 1 and 2)? What is the driver of deflationary development (AS vs AD, or others)? Is

deflation depressing? Can we say monetary policy is still effective, even though we are not quite

sure about the sources of deflation?

Besides the discussions, the policy menu of the Bank of Japan (BOJ) is like “taking everything,”

among untraditional ones: Quantitative Easing (QE), Commitment, Yield-Curve-Control, negative

interest rate. Off course, here are controversies.

Fig. 1 GDP growth and Inflation

-10

-5

0

5

10

15

20

25

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Real GDP core CPI

(annual growth, %, measured quarterly)

year

% growth

3

Fig. 2 Inflation vs GDP growth, by periods (quarterly % chg.)

1.2. Purpose of research

This paper aims to answer two questions: 1) What is the driving factor of Japanese deflation? 2)

Was monetary policy effective so far, and is it even now? In the way I try to sublate the polarizing

views from supply-side school (or hawks in monetary policy) and demand-side school (doves, or

reflationists). Using a simple macroeconomic model, this paper inspects the driving factors of

deflation long observed in Japan, and accordingly, it assesses the effectiveness of monetary policy,

including the very recent policy instruments BOJ has employed, such as Quantitative Easing, Yield-

Curve-Control, and negative interest rates.

More specifically, I decompose the historical inflation dynamics into four components by sources [:

AS shocks, AD shocks, MD shocks, and MS shocks1], using identified structural residuals from a

SVAR model (system of four endogenous [y, p, r, m]) of AS-AD framework with two monetary policy

benchmarks: Taylor rule and Fisher’s equation of exchange. Then, I discuss lessons for monetary

policy, looking at the coordination of the impulse responses and structural shocks folded inside the

historical decomposition.

1.3. Literature

There are numbers of studies on this topic and approach. Gali (1992) was a pathfinder of this

literature. He empirically analyzed the four variables VAR model ―that is [y, p, r, m], as well as me―

for the U.S. data with monetary policy assessments. Gerlach and Smets (1995) investigated three

variables VAR (excepting for money supply), to see the effects of interest rate shocks in G-7

countries during the period 1979-1993. They observed inflation rate in Japan dropped in the late

80’s due to AD shocks, and then bounced up as the results of monetary easing. Mio (2003), focusing

on a simple AS-AD with a two variables system for Japan up to 1999, reported both of AS and AD

1 Respectively, aggregate demand, aggregate supply, money demand, and money supply.

-5

0

5

10

15

20

25

30

-4 -2 0 2 4 6 8 10 12

Inflation vs GDP growth (1971Q1-1994Q4)% chg.

% chg.-3

-2

-1

0

1

2

3

4

5

-10 -8 -6 -4 -2 0 2 4 6 8

Inflation vs GDP growth (1995Q1-2017Q2)% chg.

% chg.

4

disturbances played non-negligible roles on disinflation in the 90’s. Monetary policy was not

assessed there.

1.4. Merits of this paper

A virtue of the approach in this series of studies is that we can have a single analytical platform

which synthesizes causal inductions of inflation dynamics and assessments of policy effects.

In addition, let me point out, compared with those predecessors, my research has the following

advantages:

1) Analyze both of two types of monetary policy: interest rate and quantity.

2) Use of long-term interest rate to capture the current policy trials on yield curves (The papers

above used short-term interbank rates).

3) Including recent data, the periods of unconventional policy.

4) Also, rather older data. In many studies with standard 10-year JGB yields for Japan, the sample

starts from the late 80’s, due to data availability2. I pick 9-year JGB as interest rate which is

obtained from 1973. For my historical decomposition analysis, it is essential to big have episodes

such as oil-shock and financial bubble during the 70-80’s.

2 I mean here that 10-year compound index obtained from Bloomberg starts from the mid 80’s.

5

2. Date

I am estimating a system of vectors with four endogenous variables: 𝑥𝑥 ≡ [∆𝑦𝑦,∆p,∆r,∆m]′, where

each of the ingredients noted as below is seasonally adjusted and in logarithm term (so differences

represent growth rates of levels),

y: real GDP,

p: CPI core index,

r: (expectational) real interest rate,

m: relative real balance against nominal GDP.

For (expectational) real interest rate r, I assume adaptive expectations. So that r is nominal interest

rate subtracted by moving average (with four lags) of inflation rates. Relative real balance m equals

to (M2+CD) over (GDP∙CPI) ratio. Note that m is adverse of the velocity in Fisher’s equation of

exchange. Those two variables r and m reflect degrees of monetary easing/tightening, according to

the economic environment, or to the model benchmark. More about statistical properties and

model selection are discussed in chapter 4.

The sample period is 1974:1-2017:2. Data are obtained from Cabinet Office of Government of

Japan, Bank of Japan, and Bloomberg.

3. Underlying Economic Model

For the empirical analysis after this section, I suppose the following theoretical model, behind the

SVAR. That is a macroeconomic system with four equations, composed with textbook forms of AS

curve, AD curve, MD curve (or Taylor rule), and MS curve (or Fisher’s equation of exchange).

Another important assumption is that endogenous move in reactions to four underlying

disturbances mutually orthogonal, 𝜀𝜀 ≡ [𝜀𝜀𝐴𝐴𝐴𝐴, 𝜀𝜀𝐴𝐴𝐴𝐴 , 𝜀𝜀𝑀𝑀𝐴𝐴 , 𝜀𝜀𝑀𝑀𝐴𝐴]′ . In addition, to identify those

structural shocks, we need a priori conditions on the model’s dynamic features. I will discuss this

point in chapter 4.

<Textbook forms:>

(AS; Philips curve): 𝑦𝑦 = 𝛽𝛽𝛽𝛽𝑝𝑝−1 + 𝜃𝜃(𝑦𝑦 − 𝑦𝑦∗) + 𝑢𝑢𝑎𝑎𝑎𝑎

(AD; AD curve): 𝑦𝑦 = 𝛼𝛼 − 𝜎𝜎(𝑖𝑖 − 𝐸𝐸𝛽𝛽𝑝𝑝+1) + 𝑢𝑢𝑎𝑎𝑎𝑎

(MD; Taylor rule): 𝑟𝑟 = 𝜙𝜙𝑦𝑦 + 𝜆𝜆𝑝𝑝 + 𝑢𝑢𝑚𝑚𝑎𝑎

(MS; Fisher’s exchange): 𝑚𝑚− 𝜇𝜇 = 𝑝𝑝 + 𝑦𝑦 + 𝑢𝑢𝑚𝑚𝑎𝑎

6

4. Empirical Method

Before estimating a system, to certify I have a covariance stationary vector process, I investigate the

time-series properties of each variables. As a result, I will take first differential formation

𝑥𝑥 ≡ [∆𝑦𝑦,∆p,∆r,∆m]′ in the SVAR estimation.

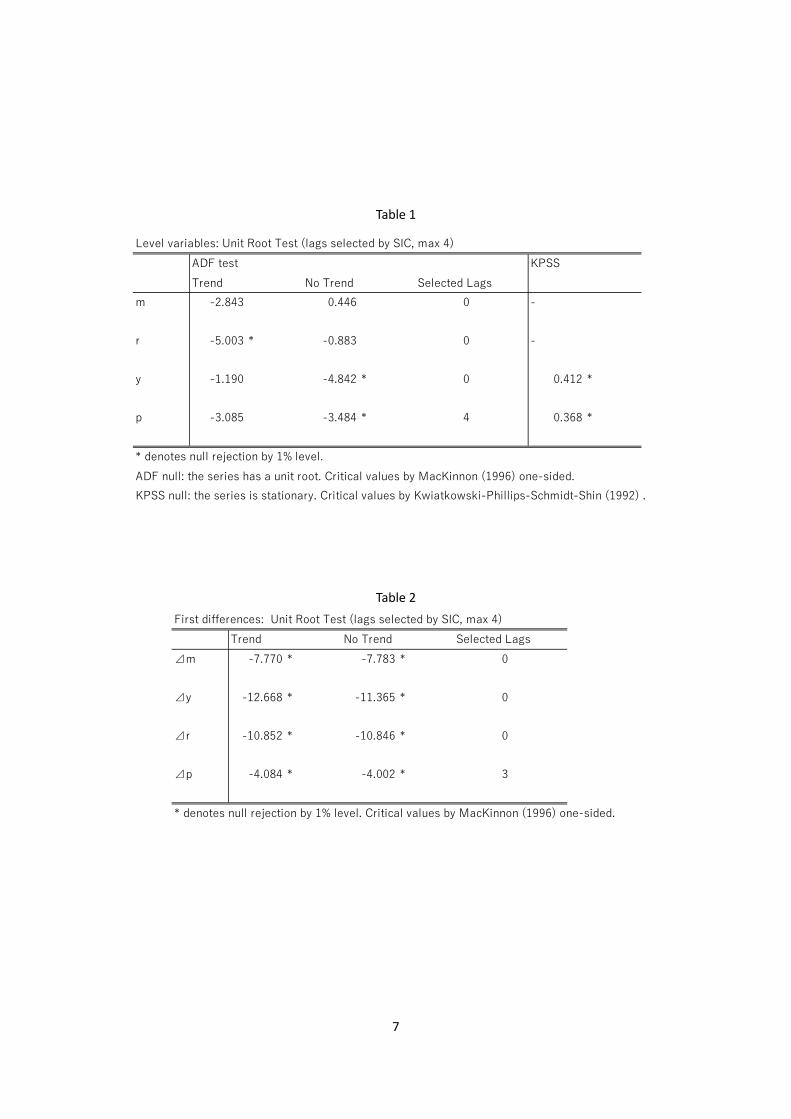

4.1. Unit root and cointegration tests

Table 1 summarizes the outcomes of unit root tests for level variables. At first, I examine unit root

of each level variable by Augmented Dickey-Fuller test (1979). In the table, there are shown both

results from tests with trend and without trend. Shortly, we can say m is nonstationary. On the

other hand, hypothesis of r’s unit root is rejected when a time trend is included. I interpret r is

trend-stationary process (TSP), supported by that the coefficient on the trend term was significant.

Anyway, I use Δr in SVAR analysis to eliminate the linear trend. Series y and p need an additional

step. ADF tests with trend did not reject unit roots, while those with trend did, suggesting

possibilities of non-stationarity. The powers of those tests, however, are presumably low, because

estimators on lagged terms were very close to 1 (0.99 for y, 0.96 for p). Thereat, I employ

Kwiatkowski-Phillips-Schmidt-Shin (1992) (KPSS) tests for y and p in a supplemental way, resulting in

rejections null hypothesis that they are stationary3. Thus, a plausible view is that the two series are

family of random walk. Also, it is confirmed there are no unit roots in first differences of all variables

by ADF tests (Table 2).

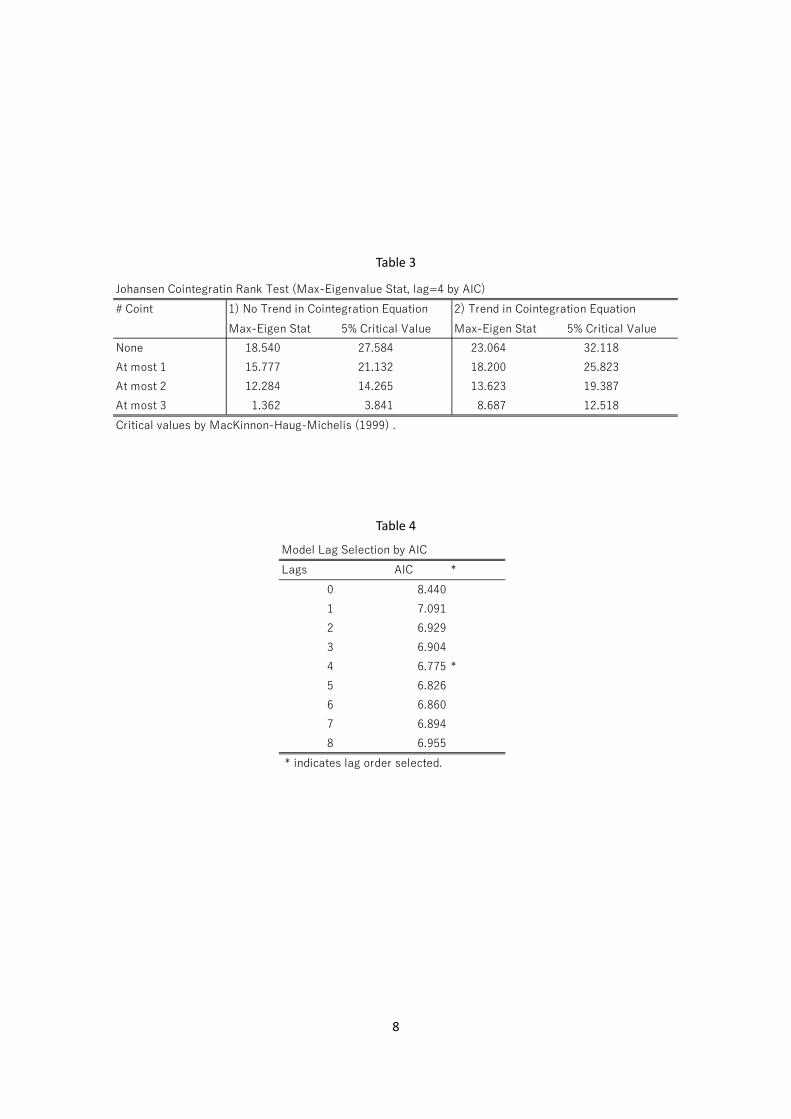

After checking unit roots, possibilities of cointegrations are tested, with Johansen and Juselius’s

(1990) maximum eigenvalue statistics. As reported in Table 3, the system is not likely a cointegrated

process. In this test, four lags are chosen by AIC, also in the forthcoming SVAR estimation (Table 4).

So, again, the system to estimate below is of 𝑥𝑥 ≡ [∆𝑦𝑦,∆p,∆r,∆m]′ with four lags.

3 Note that the design of null and counter hypothesis in KPSS test is reversed to Dickey-Fuller.

7

Table 1

Table 2

Level variables: Unit Root Test (lags selected by SIC, max 4)ADF test KPSSTrend No Trend Selected Lags

m -2.843 0.446 0 -

r -5.003 * -0.883 0 -

y -1.190 -4.842 * 0 0.412 *

p -3.085 -3.484 * 4 0.368 *

* denotes null rejection by 1% level.ADF null: the series has a unit root. Critical values by MacKinnon (1996) one-sided.KPSS null: the series is stationary. Critical values by Kwiatkowski-Phillips-Schmidt-Shin (1992) .

First differences: Unit Root Test (lags selected by SIC, max 4)Trend No Trend Selected Lags

⊿m -7.770 * -7.783 * 0

⊿y -12.668 * -11.365 * 0

⊿r -10.852 * -10.846 * 0

⊿p -4.084 * -4.002 * 3

* denotes null rejection by 1% level. Critical values by MacKinnon (1996) one-sided.

8

Table 3

Table 4

Johansen Cointegratin Rank Test (Max-Eigenvalue Stat, lag=4 by AIC)# Coint 1) No Trend in Cointegration Equation 2) Trend in Cointegration Equation

Max-Eigen Stat 5% Critical Value Max-Eigen Stat 5% Critical ValueNone 18.540 27.584 23.064 32.118At most 1 15.777 21.132 18.200 25.823At most 2 12.284 14.265 13.623 19.387At most 3 1.362 3.841 8.687 12.518Critical values by MacKinnon-Haug-Michelis (1999) .

Model Lag Selection by AICLags AIC *

0 8.4401 7.0912 6.9293 6.9044 6.775 *5 6.8266 6.8607 6.8948 6.955

* indicates lag order selected.

9

4.2. Identification

The very key part of SVAR method is identification strategy. Basically, I follow Gali (1992), whose

approach captures well the nature of AS-AD mechanism4, i.e., I combine the long-run and the short-

run restrictions, as summarized in Table 5.

For the system of four variables, I am estimating 4×4 coefficients matrices (conditionally on a

matrix of normalized orthogonal shocks), thus there are six arbitrary constraints, or six linear

independences, required to just-identify the structure.

Table 5

The long-run restrictions R1-R3 are what distinguish AS variances, associated with the theoretical

guidepost, a vertical long-run Philips curve.

For three additional constraints, I employ the short-run restrictions R4-R6. They are reasoned with

lags for monetary policy to affect other parts of economy. Blown by changes in interest rate or

money supply, GDP within the quarter hardly responses, since there would be idle time before

recognitions, judgements and adjustments of production schedules and investment plans. As well,

price stickiness is almost a stylized fact. I pick MS shock rather than MD shock on p’s slowness, since

velocity is supposed to be much flexible and to absorb by itself the short-run fluctuations on

Fisher’s exchange.

Off course, from the technical viewpoint, there are other possible combinations of restrictions.

4 Blanchard and Quah (1989) are ones of originators of AS-AD identification in VAR with the long-run restrictions. Besides Lippi and Reichlin (1993) made a criticism for this approach, Faust and Leeper (1997) summarized the conditions where it may/may-not be plausible. Stock and Watson (2001) noted their general appetite to VAR inferences. In this paper, I take the first differences of endogenous, which enables to avoid some criticisms. And I believe the prior that technology is the anchoring factor of the long-run production is the common among many economists.

Identifying RestrictionsLong-run restrictionsR1: no long-run effects of AD shocks on y.R2: no long-run effects of MD shocks on y.R3: no long-run effects of MS shocks on y.Short-run restrictionsR4: no contemporaneous effects of MD shocks on y.R5: no contemporaneous effects of MS shocks on y.R6: no contemporaneous effects of MS shocks on p.

10

However, from qualitative priors, it is not so plausible to have constraints on reactions of r and m,

since the financial market adapts very quickly to surprises.

4.3. Econometrical expressions

The VAR system has several formularizations. As noted, our system is of 𝑥𝑥 ≡ [∆𝑦𝑦,∆p,∆r,∆m]′,

whose dynamics are driven by structural disturbances 𝜀𝜀 ≡ [𝜀𝜀𝐴𝐴𝐴𝐴, 𝜀𝜀𝐴𝐴𝐴𝐴, 𝜀𝜀𝑀𝑀𝐴𝐴, 𝜀𝜀𝑀𝑀𝐴𝐴]′, which are mutually

orthogonal.

The MA representation of the structural form is,

𝑥𝑥 = 𝐶𝐶(𝐿𝐿)𝜀𝜀,

where 𝐶𝐶(𝐿𝐿) ≡ �𝐶𝐶(𝐿𝐿)𝑖𝑖𝑖𝑖�,𝑓𝑓𝑓𝑓𝑟𝑟 𝑖𝑖, 𝑗𝑗 = 1, 2, 3, 4.

We can also write Wold MA reduced form,

𝑥𝑥 = 𝐸𝐸(𝐿𝐿)𝑣𝑣,

where 𝐸𝐸(𝐿𝐿) ≡ �𝐸𝐸(𝐿𝐿)𝑖𝑖𝑖𝑖�,𝑓𝑓𝑓𝑓𝑟𝑟 𝑖𝑖, 𝑗𝑗 = 1, 2, 3, 4, 𝐸𝐸(0) = 𝐼𝐼, 𝑎𝑎𝑎𝑎𝑎𝑎 𝐸𝐸(𝐿𝐿) 𝑖𝑖𝑖𝑖 𝑖𝑖𝑎𝑎𝑣𝑣𝑖𝑖𝑟𝑟𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖. Innovations are

defined by 𝑣𝑣 ≡ 𝑥𝑥 − 𝑃𝑃[𝑥𝑥|𝑥𝑥(−1),𝑥𝑥(−2), … ], where P is the orthogonal projection operator, with the

variance-covariance matrix Σ ≡ 𝐸𝐸𝑣𝑣𝑣𝑣′.

Then we have an AR expression of the reduced form,

𝐵𝐵(𝐿𝐿) 𝑥𝑥 = 𝑣𝑣,

where 𝐵𝐵(𝐿𝐿) ≡ �𝐵𝐵(𝐿𝐿)𝑖𝑖𝑖𝑖�,𝑓𝑓𝑓𝑓𝑟𝑟 𝑖𝑖, 𝑗𝑗 = 1, 2, 3, 4,𝐸𝐸(0) = 𝐼𝐼,𝑎𝑎𝑎𝑎𝑎𝑎 𝐵𝐵(𝐿𝐿) = 𝐸𝐸(𝐿𝐿)−1.

By finding a 4×4 matrix S such that 𝑣𝑣 = 𝑆𝑆𝜀𝜀 and thus 𝑃𝑃[𝜀𝜀|𝑥𝑥(−1),𝑥𝑥(−2), … ] = 0, 𝑗𝑗 ≥ 1, and

𝐶𝐶(𝐿𝐿) = 𝐸𝐸(𝐿𝐿)𝑆𝑆, we acquire AR form of the structure,

𝐴𝐴(𝐿𝐿) 𝑥𝑥 = 𝜀𝜀,

where 𝐴𝐴(𝐿𝐿) ≡ �𝐴𝐴(𝐿𝐿)𝑖𝑖𝑖𝑖�,𝑓𝑓𝑓𝑓𝑟𝑟 𝑖𝑖, 𝑗𝑗 = 1, 2, 3, 4,𝑎𝑎𝑎𝑎𝑎𝑎 𝐴𝐴(0) ≡ 𝑆𝑆−1.

In a normalized version of shocks, 𝐸𝐸𝜀𝜀𝜀𝜀′ = I, so SS′ = Σ, accompanied by ten conditions.

To just-identify the structure, my six restrictions are imposed in the following ways.

The long-run constraints R1, R2 and R3 correspond to:

𝐶𝐶12(1) = 𝐶𝐶13(1) = 𝐶𝐶14(1) = 0.

Or equivalently,

𝐸𝐸11(1)𝑆𝑆12 + 𝐸𝐸12(1)𝑆𝑆22 + 𝐸𝐸13(1)𝑆𝑆32 + 𝐸𝐸14(1)𝑆𝑆42 = 0,

𝐸𝐸11(1)𝑆𝑆13 + 𝐸𝐸12(1)𝑆𝑆23 + 𝐸𝐸13(1)𝑆𝑆33 + 𝐸𝐸14(1)𝑆𝑆43 = 0,

𝐸𝐸11(1)𝑆𝑆14 + 𝐸𝐸12(1)𝑆𝑆24 + 𝐸𝐸13(1)𝑆𝑆34 + 𝐸𝐸14(1)𝑆𝑆44 = 0.

11

Also, the short-run restrictions R4-R6 require:

𝑆𝑆13 = 𝑆𝑆14 = 𝑆𝑆24 = 0.

5. Results

5.1. Guideline of chapter 5

In this chapter, I introduce the results of empirical analysis, along the following outline. Section 5.2

focuses on identified structural shocks. I check they are reasonably decomposed into economic

factors, as well as I brief how they have moved according to the history. Impulse responses are

inspected in the following section 5.3, depicting the way Japanese economy behaves in reactions to

the certain variances, on average within the sample periods. Then, section 5.4 is about the results

of historical decompositions, which reveals how the shocks were propagated thorough the impulse

responses into chronological developments of macro variables. Robustness of the results are

checked in Appendix.

Going through the stroke, a set of possible answers will be suggested for the questions I set in the

beginning. Again, those are questions of: 1) the driving factor of Japanese deflation; 2) monetary

policy effectiveness (in the past and current).

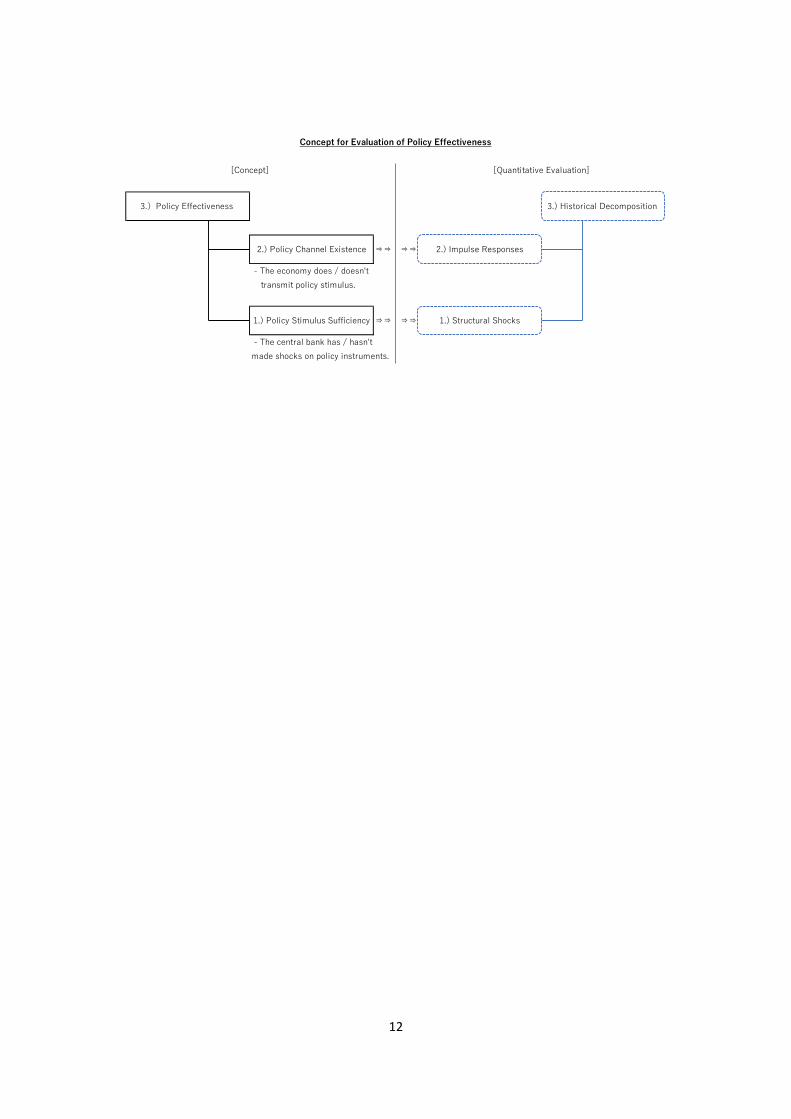

I believe it is helpful for further discussions to notice here this paper’s strategy of assessment on

policy effectiveness. That can be evaluated by three stages, as Fig. 3 illustrates. 1) At first, we should

examine if enough stimulus―sufficient according to the economic environment― were made on

policy instruments. This point includes the authority’s ability to control policy tools as intended. 2)

Second, we need to know there exist channels which transmit the policy effects into the system. 3)

Finally, both information is folded in one place, the total effectiveness. In the empirics, those three

stages correspond respectively to 1) structural deviations, 2) impulse responses, and 3) historical

decompositions.

Fig. 3

12

- The economy does / doesn't transmit policy stimulus.

- The central bank has / hasn't made shocks on policy instruments.

Concept for Evaluation of Policy Effectiveness

[Concept] [Quantitative Evaluation]

⇒⇒ ⇒⇒

3.) Historical Decomposition 3.)Policy Effectiveness

2.) Policy Channel Existence

1.) Policy Stimulus Sufficiency

2.) Impulse Responses

1.) Structural Shocks

⇒⇒ ⇒⇒

13

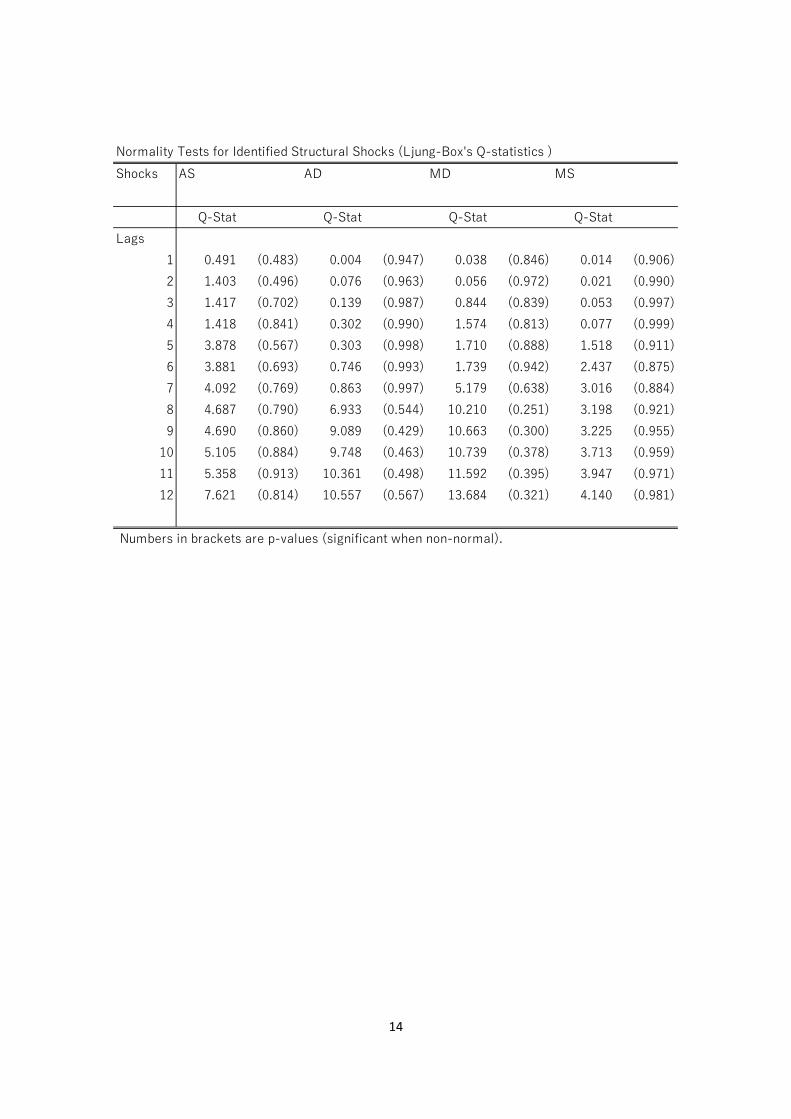

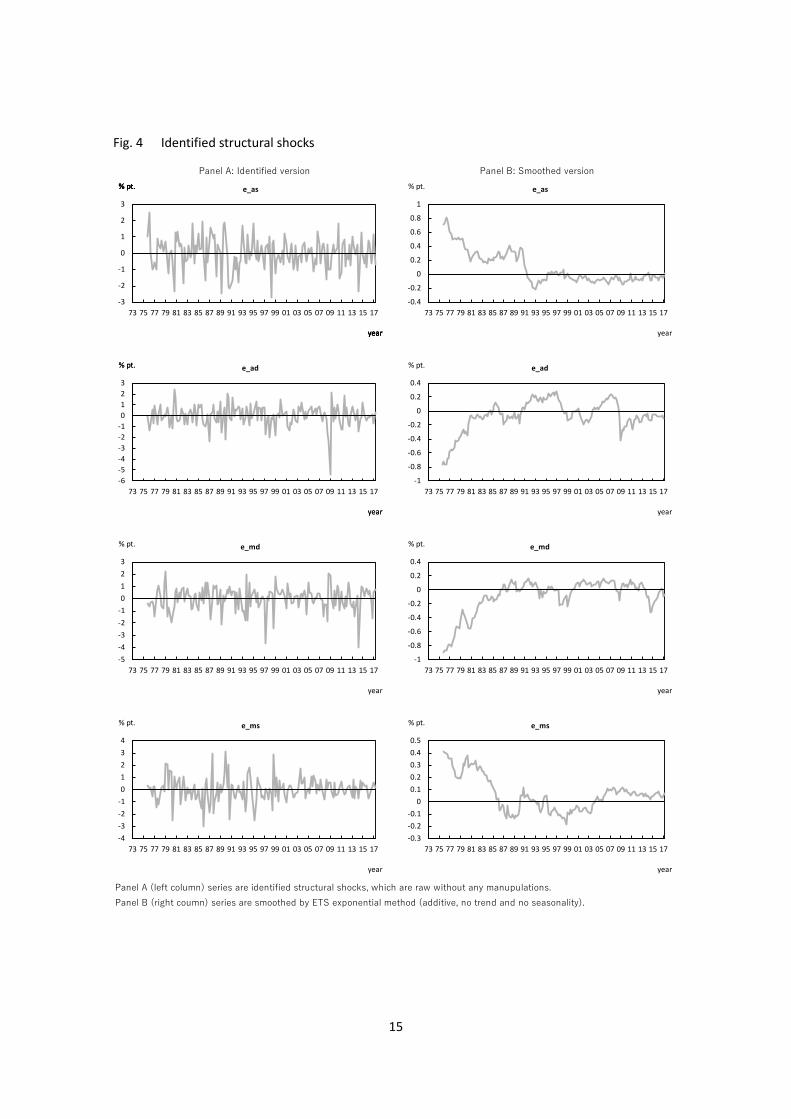

5.2. Identified structural shocks

The SVAR with the noted specifications reports the structural shocks as in Fig. 4-Panel A (left

column). It is seen that this stochastics is zero-mean, stable variance process, as tested by Ljung-

Box’s Q-stats as in Table 6. Fig. 4-Panel B (right column) plots the smoothed version by ETS

exponential smoothing (Hyndman, et al., 2002)5, which is for a supplemental reference to grab their

historical characteristics (Note that their appearances are relying upon transitions of the mid-term

mean, so just focus the big picture of momentum6). AS deviation dropped sharply at two oil-shocks

in the 70’s and the credit crisis in 1991-1993. AD shock grew rapidly in the 70’s, but it slowed down

in the late 80’s, corresponding to the end of the financial boom, and stagnated during the Lost

Decades. We can also find the collapses in 2001 and 2009. MS showed similar movement as AD, but

it became flatter after declining by the 90’s credit crunch. Meanwhile, MS behaved somehow

oppositely to MS, losing its initial height through the bubble economy.

Table 6

5 Spec: additive, no trend and no seasonality. 6 It is understandable if it is thought the appearances of Panel B invokes they would have a sort of

mid-term trends. Technologically speaking, however, it does not necessarily imply that (by the nature of ETS smoothing method). Even if it does, the normality of residuals holds at least in the long horizon, as tested in Table 6. Anyhow, I use this here for a brief characterization, as mentioned.

14

Normality Tests for Identified Structural Shocks (Ljung-Box's Q-statistics )Shocks AS AD MD MS

Q-Stat Q-Stat Q-Stat Q-StatLags

1 0.491 (0.483) 0.004 (0.947) 0.038 (0.846) 0.014 (0.906)2 1.403 (0.496) 0.076 (0.963) 0.056 (0.972) 0.021 (0.990)3 1.417 (0.702) 0.139 (0.987) 0.844 (0.839) 0.053 (0.997)4 1.418 (0.841) 0.302 (0.990) 1.574 (0.813) 0.077 (0.999)5 3.878 (0.567) 0.303 (0.998) 1.710 (0.888) 1.518 (0.911)6 3.881 (0.693) 0.746 (0.993) 1.739 (0.942) 2.437 (0.875)7 4.092 (0.769) 0.863 (0.997) 5.179 (0.638) 3.016 (0.884)8 4.687 (0.790) 6.933 (0.544) 10.210 (0.251) 3.198 (0.921)9 4.690 (0.860) 9.089 (0.429) 10.663 (0.300) 3.225 (0.955)

10 5.105 (0.884) 9.748 (0.463) 10.739 (0.378) 3.713 (0.959)11 5.358 (0.913) 10.361 (0.498) 11.592 (0.395) 3.947 (0.971)12 7.621 (0.814) 10.557 (0.567) 13.684 (0.321) 4.140 (0.981)

Numbers in brackets are p-values (significant when non-normal).

15

Fig. 4 Identified structural shocks

Panel A: Identified version Panel B: Smoothed version

Panel A (left column) series are identified structural shocks, which are raw without any manupulations. Panel B (right coumn) series are smoothed by ETS exponential method (additive, no trend and no seasonality).

-3

-2

-1

0

1

2

3

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_as% pt.

year

% pt.

year

% pt.

year

% pt.

year

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_md% pt.

year

-0.3-0.2-0.1

00.10.20.30.40.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_ms% pt.

year

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_ad% pt.

year

-6-5-4-3-2-10123

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_ad% pt.

year

% pt.

year

-5-4-3-2-10123

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_md% pt.

year

-4-3-2-101234

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_ms% pt.

year

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

e_as% pt.

year

16

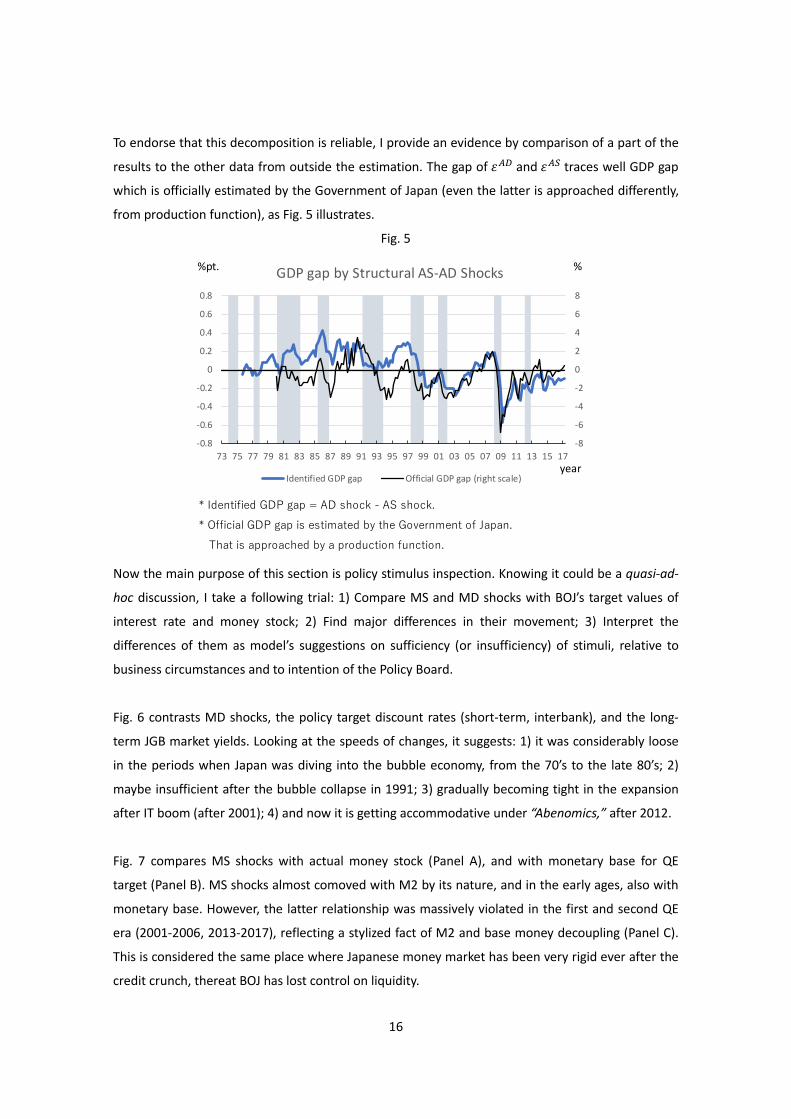

To endorse that this decomposition is reliable, I provide an evidence by comparison of a part of the

results to the other data from outside the estimation. The gap of 𝜀𝜀𝐴𝐴𝐴𝐴 and 𝜀𝜀𝐴𝐴𝐴𝐴 traces well GDP gap

which is officially estimated by the Government of Japan (even the latter is approached differently,

from production function), as Fig. 5 illustrates.

Fig. 5

Now the main purpose of this section is policy stimulus inspection. Knowing it could be a quasi-ad-

hoc discussion, I take a following trial: 1) Compare MS and MD shocks with BOJ’s target values of

interest rate and money stock; 2) Find major differences in their movement; 3) Interpret the

differences of them as model’s suggestions on sufficiency (or insufficiency) of stimuli, relative to

business circumstances and to intention of the Policy Board.

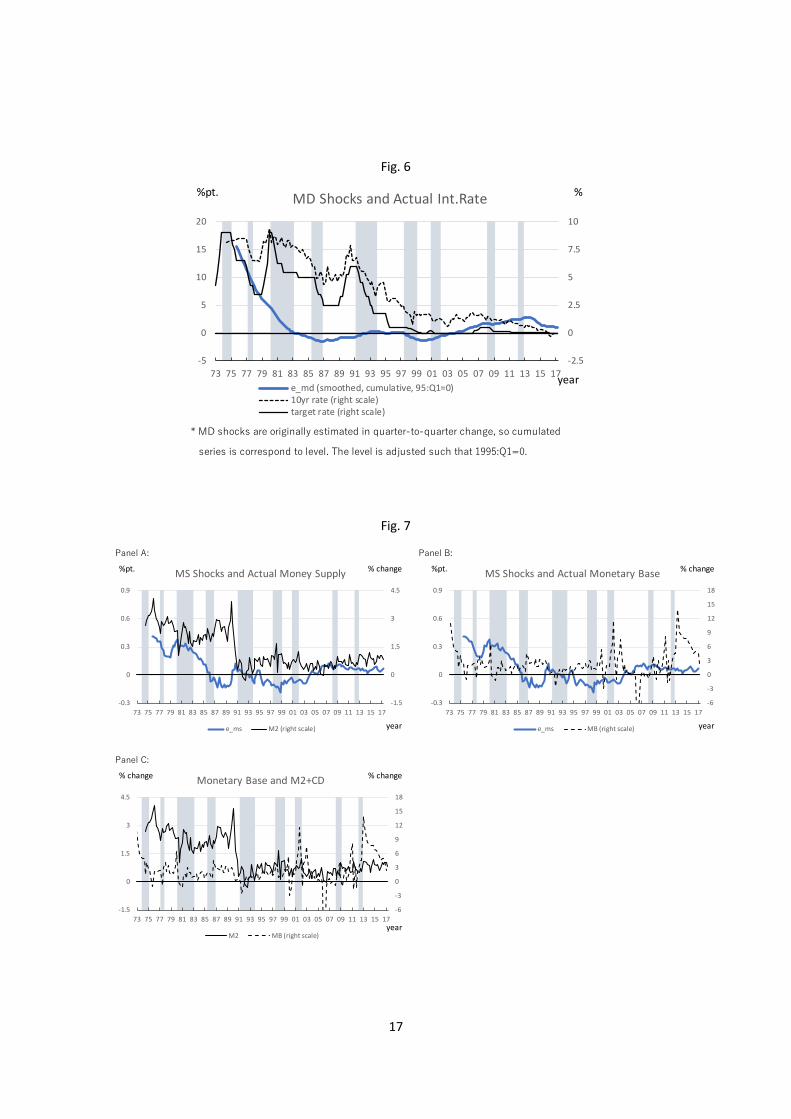

Fig. 6 contrasts MD shocks, the policy target discount rates (short-term, interbank), and the long-

term JGB market yields. Looking at the speeds of changes, it suggests: 1) it was considerably loose

in the periods when Japan was diving into the bubble economy, from the 70’s to the late 80’s; 2)

maybe insufficient after the bubble collapse in 1991; 3) gradually becoming tight in the expansion

after IT boom (after 2001); 4) and now it is getting accommodative under “Abenomics,” after 2012.

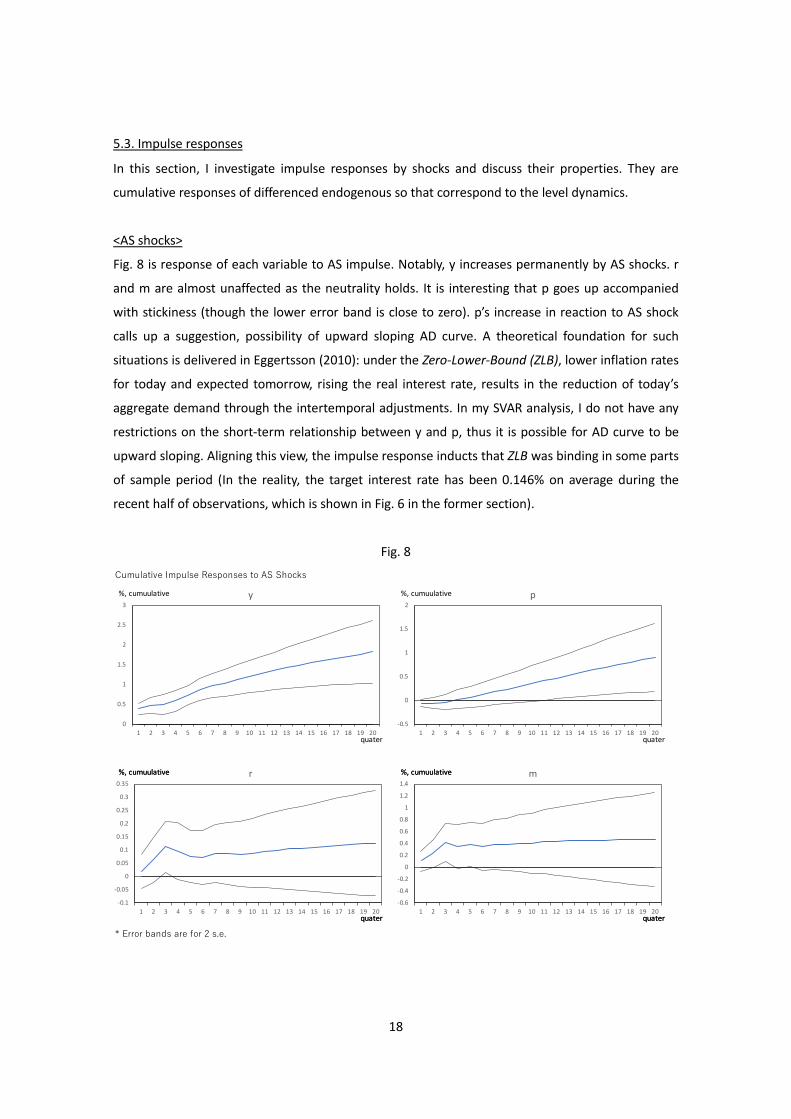

Fig. 7 compares MS shocks with actual money stock (Panel A), and with monetary base for QE

target (Panel B). MS shocks almost comoved with M2 by its nature, and in the early ages, also with

monetary base. However, the latter relationship was massively violated in the first and second QE

era (2001-2006, 2013-2017), reflecting a stylized fact of M2 and base money decoupling (Panel C).

This is considered the same place where Japanese money market has been very rigid ever after the

credit crunch, thereat BOJ has lost control on liquidity.

* Identified GDP gap = AD shock - AS shock. * Official GDP gap is estimated by the Government of Japan. That is approached by a production function.

-8

-6

-4

-2

0

2

4

6

8

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

GDP gap by Structural AS-AD Shocks

Identified GDP gap Official GDP gap (right scale)

%pt. %

year

17

Fig. 6

Fig. 7

* MD shocks are originally estimated in quarter-to-quarter change, so cumulated

series is correspond to level. The level is adjusted such that 1995:Q1=0.

-2.5

0

2.5

5

7.5

10

-5

0

5

10

15

20

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

MD Shocks and Actual Int.Rate

e_md (smoothed, cumulative, 95:Q1=0)10yr rate (right scale)target rate (right scale)

%pt. %

year

Panel A: Panel B:

Panel C:

-6

-3

0

3

6

9

12

15

18

-1.5

0

1.5

3

4.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

Monetary Base and M2+CD

M2 MB (right scale)

% change % change

year

-6

-3

0

3

6

9

12

15

18

-0.3

0

0.3

0.6

0.9

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

MS Shocks and Actual Monetary Base

e_ms MB (right scale)

%pt. % change

year

-1.5

0

1.5

3

4.5

-0.3

0

0.3

0.6

0.9

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

MS Shocks and Actual Money Supply

e_ms M2 (right scale)

%pt. % change

year

18

5.3. Impulse responses

In this section, I investigate impulse responses by shocks and discuss their properties. They are

cumulative responses of differenced endogenous so that correspond to the level dynamics.

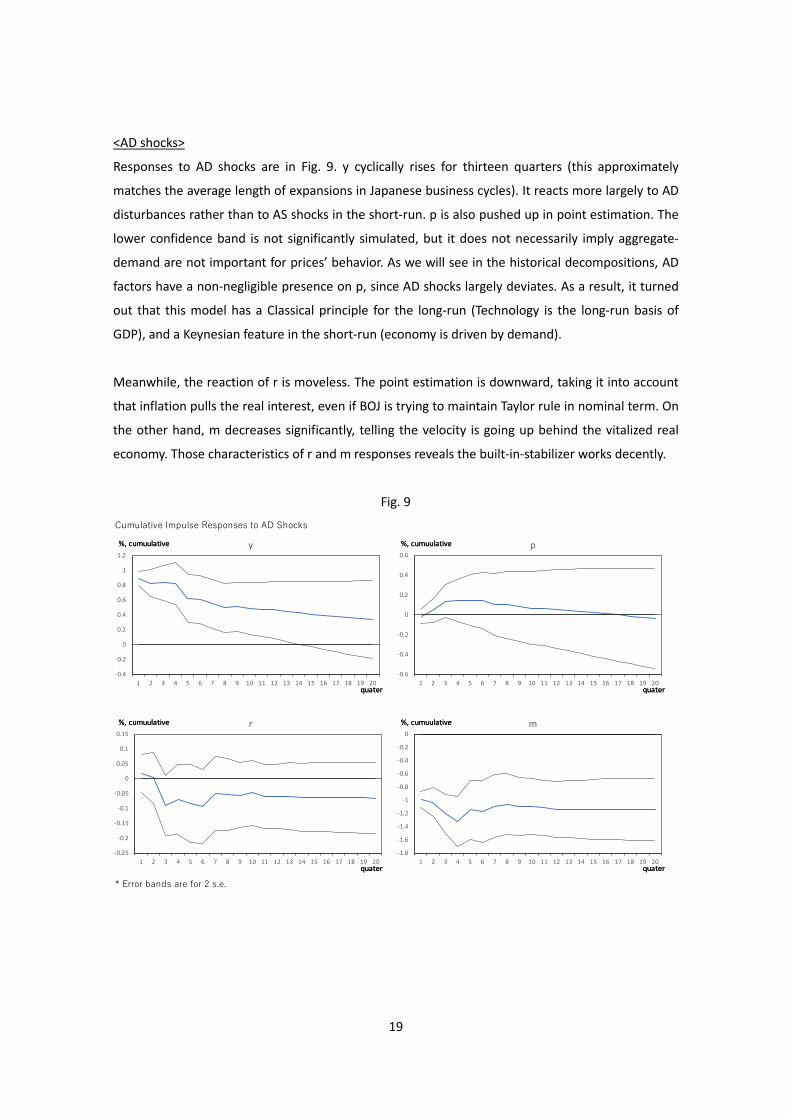

<AS shocks>

Fig. 8 is response of each variable to AS impulse. Notably, y increases permanently by AS shocks. r

and m are almost unaffected as the neutrality holds. It is interesting that p goes up accompanied

with stickiness (though the lower error band is close to zero). p’s increase in reaction to AS shock

calls up a suggestion, possibility of upward sloping AD curve. A theoretical foundation for such

situations is delivered in Eggertsson (2010): under the Zero-Lower-Bound (ZLB), lower inflation rates

for today and expected tomorrow, rising the real interest rate, results in the reduction of today’s

aggregate demand through the intertemporal adjustments. In my SVAR analysis, I do not have any

restrictions on the short-term relationship between y and p, thus it is possible for AD curve to be

upward sloping. Aligning this view, the impulse response inducts that ZLB was binding in some parts

of sample period (In the reality, the target interest rate has been 0.146% on average during the

recent half of observations, which is shown in Fig. 6 in the former section).

Fig. 8

Cumulative Impulse Responses to AS Shocks

* Error bands are for 2 s.e.

0

0.5

1

1.5

2

2.5

3

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

y%, cumuulative

quater

-0.5

0

0.5

1

1.5

2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

p%, cumuulative

quater

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

r%, cumuulative

quater

%, cumuulative

quater

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

m%, cumuulative

quater

%, cumuulative

quater

19

<AD shocks>

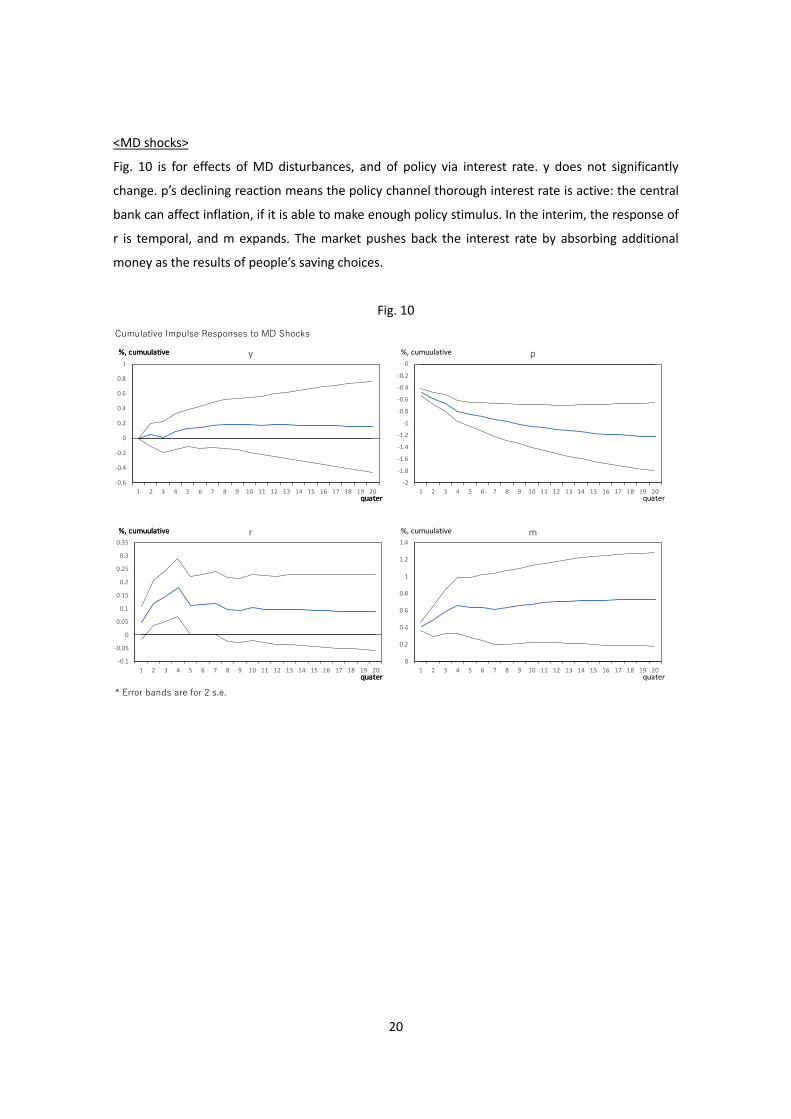

Responses to AD shocks are in Fig. 9. y cyclically rises for thirteen quarters (this approximately

matches the average length of expansions in Japanese business cycles). It reacts more largely to AD

disturbances rather than to AS shocks in the short-run. p is also pushed up in point estimation. The

lower confidence band is not significantly simulated, but it does not necessarily imply aggregate-

demand are not important for prices’ behavior. As we will see in the historical decompositions, AD

factors have a non-negligible presence on p, since AD shocks largely deviates. As a result, it turned

out that this model has a Classical principle for the long-run (Technology is the long-run basis of

GDP), and a Keynesian feature in the short-run (economy is driven by demand).

Meanwhile, the reaction of r is moveless. The point estimation is downward, taking it into account

that inflation pulls the real interest, even if BOJ is trying to maintain Taylor rule in nominal term. On

the other hand, m decreases significantly, telling the velocity is going up behind the vitalized real

economy. Those characteristics of r and m responses reveals the built-in-stabilizer works decently.

Fig. 9

Cumulative Impulse Responses to AD Shocks

* Error bands are for 2 s.e.

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

y%, cumuulative

quater

%, cumuulative

quater

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

p%, cumuulative

quater

%, cumuulative

quater

-0.25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

r%, cumuulative

quater

%, cumuulative

quater

-1.8

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

m%, cumuulative

quater

%, cumuulative

quater

20

<MD shocks>

Fig. 10 is for effects of MD disturbances, and of policy via interest rate. y does not significantly

change. p’s declining reaction means the policy channel thorough interest rate is active: the central

bank can affect inflation, if it is able to make enough policy stimulus. In the interim, the response of

r is temporal, and m expands. The market pushes back the interest rate by absorbing additional

money as the results of people’s saving choices.

Fig. 10

Cumulative Impulse Responses to MD Shocks

* Error bands are for 2 s.e.

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

y%, cumuulative

quater

%, cumuulative

quater

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

r%, cumuulative

quater

%, cumuulative

quater

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

m%, cumuulative

quater

-2

-1.8

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

p%, cumuulative

quater

21

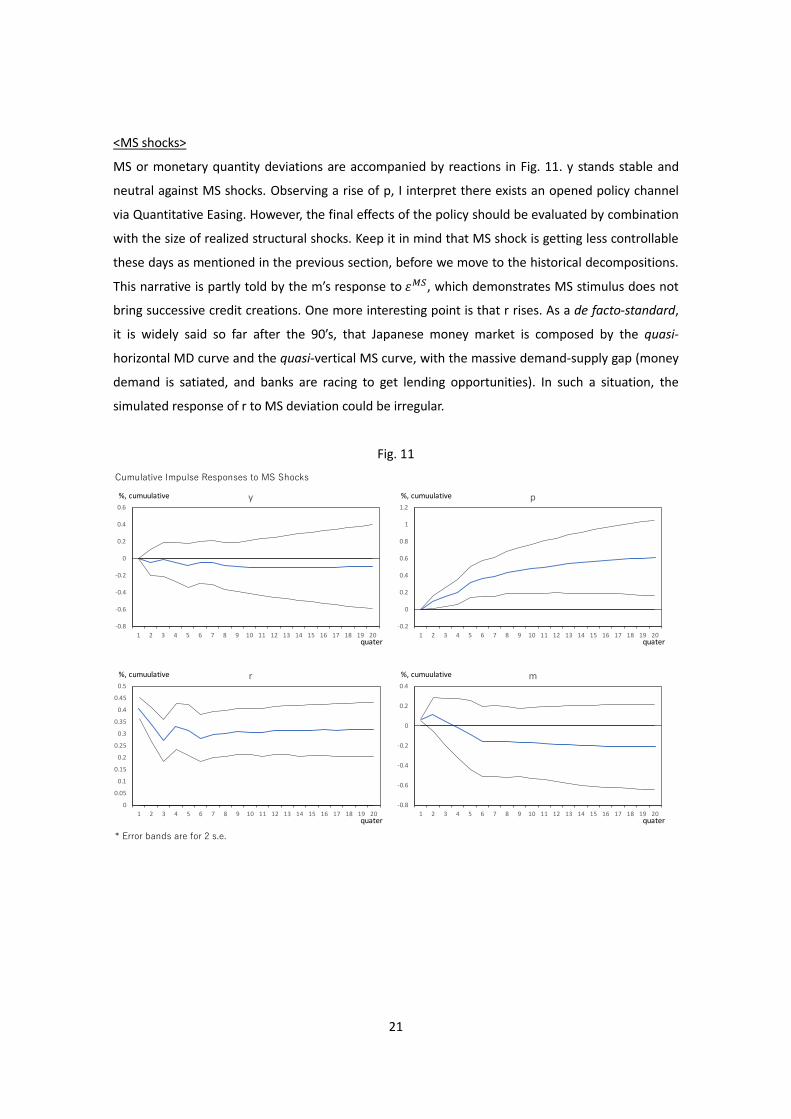

<MS shocks>

MS or monetary quantity deviations are accompanied by reactions in Fig. 11. y stands stable and

neutral against MS shocks. Observing a rise of p, I interpret there exists an opened policy channel

via Quantitative Easing. However, the final effects of the policy should be evaluated by combination

with the size of realized structural shocks. Keep it in mind that MS shock is getting less controllable

these days as mentioned in the previous section, before we move to the historical decompositions.

This narrative is partly told by the m’s response to 𝜀𝜀𝑀𝑀𝐴𝐴, which demonstrates MS stimulus does not

bring successive credit creations. One more interesting point is that r rises. As a de facto-standard,

it is widely said so far after the 90’s, that Japanese money market is composed by the quasi-

horizontal MD curve and the quasi-vertical MS curve, with the massive demand-supply gap (money

demand is satiated, and banks are racing to get lending opportunities). In such a situation, the

simulated response of r to MS deviation could be irregular.

Fig. 11

Cumulative Impulse Responses to MS Shocks

* Error bands are for 2 s.e.

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

y%, cumuulative

quater

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

r%, cumuulative

quater

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

m%, cumuulative

quater

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

p%, cumuulative

quater

22

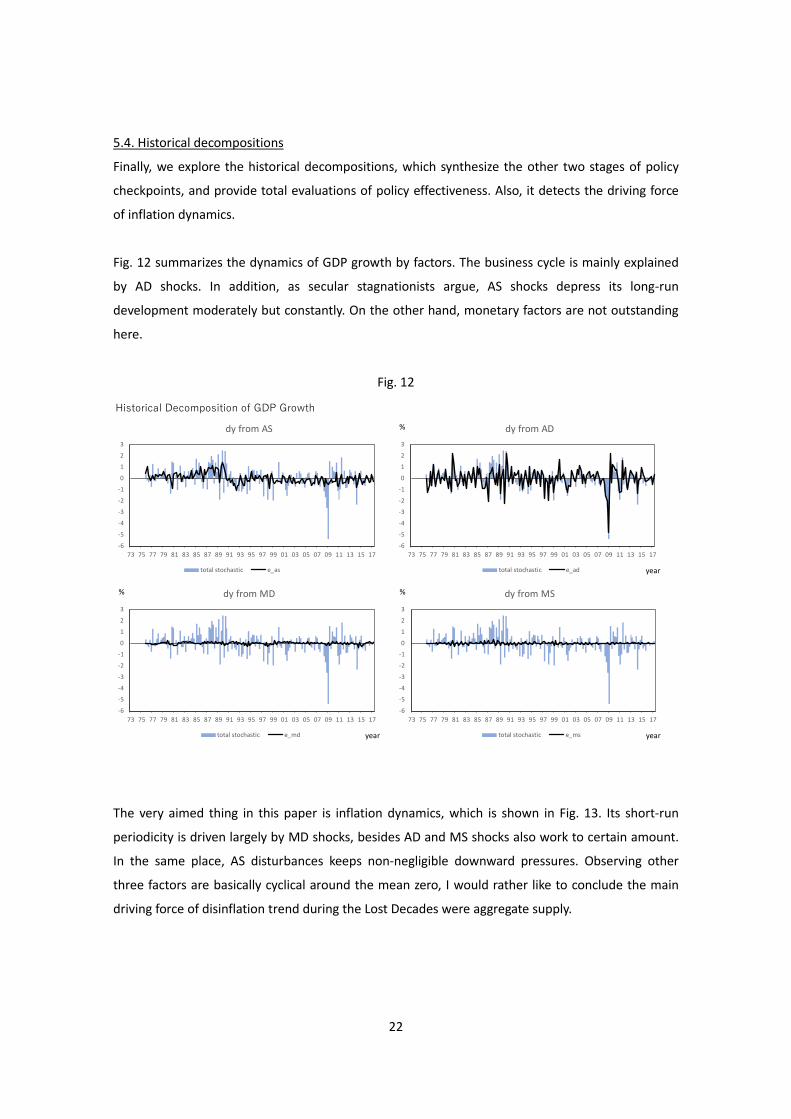

5.4. Historical decompositions

Finally, we explore the historical decompositions, which synthesize the other two stages of policy

checkpoints, and provide total evaluations of policy effectiveness. Also, it detects the driving force

of inflation dynamics.

Fig. 12 summarizes the dynamics of GDP growth by factors. The business cycle is mainly explained

by AD shocks. In addition, as secular stagnationists argue, AS shocks depress its long-run

development moderately but constantly. On the other hand, monetary factors are not outstanding

here.

Fig. 12

The very aimed thing in this paper is inflation dynamics, which is shown in Fig. 13. Its short-run

periodicity is driven largely by MD shocks, besides AD and MS shocks also work to certain amount.

In the same place, AS disturbances keeps non-negligible downward pressures. Observing other

three factors are basically cyclical around the mean zero, I would rather like to conclude the main

driving force of disinflation trend during the Lost Decades were aggregate supply.

Historical Decomposition of GDP Growth

-6

-5

-4

-3

-2

-1

0

1

2

3

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dy from AS

total stochastic e_as zero

-6

-5

-4

-3

-2

-1

0

1

2

3

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dy from AD

total stochastic e_ad

%

year

-6

-5

-4

-3

-2

-1

0

1

2

3

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dy from MD

total stochastic e_md

%

year

-6

-5

-4

-3

-2

-1

0

1

2

3

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dy from MS

total stochastic e_ms

%

year

23

Since AS stagnation is usually untouchable for the central bank, there would be a limit for monetary

policy to overwhelm deflation. However, I do not mean by this that monetary policy is not totally

helpless. As we saw, the MD component in the decomposition is large. Noticing that the MD

component includes both of policy effects and market behaviors7, anyway, I am not hesitating to

say that monetary policy via interest rate could be effective. Nevertheless, the quantitative easing is

not a big deal. As mentioned before, there would be an active channel for QE, but structural

deviations are getting smaller these days, because BOJ is losing control of market liquidity.

Therefore, MS factor is not playing an important role these days in the historical decomposition,

despite the immense expansion of recent monetary base.

Fig. 13

7 MD shocks are composed not only by arbitrary policy disturbances, but also by structural deviations from the MD curve, made by any economic agents (The SVAR does not eliminate them, by its nature). Thus, not all of the movements with MD factor in the historical decomposition derives from monetary policy.

Historical Decomposition of Inflation

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AS

total stochastic e_as

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AD

total stochastic e_ad

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MD

total stochastic e_md

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MS

total stochastic e_ms

%

year

24

6. Concluding Remark

In conclusion, to answer the two initial questions, 1) Japanese long-run deflation is mainly driven by

AS factor, and 2) Quantitative Easing is losing its effectiveness, whereas BOJ could still fight against

through via interest rate.

Note that the results above are from the mean estimation with long sample, so it should be

discounted that they are not specific results to the recent situations. Then, future effectiveness of

interest rate policy depends on conditions such as how strongly the ZLB will be bounding the

market. In addition, there would be side effects with today’s aggressive policy (for instance,

excessive low interest rate would distort the market functions), which I am not taking in the scope

here. Anyhow, after taking these into account, it would be better to reconsider the explosive

Quantitative Easing.

25

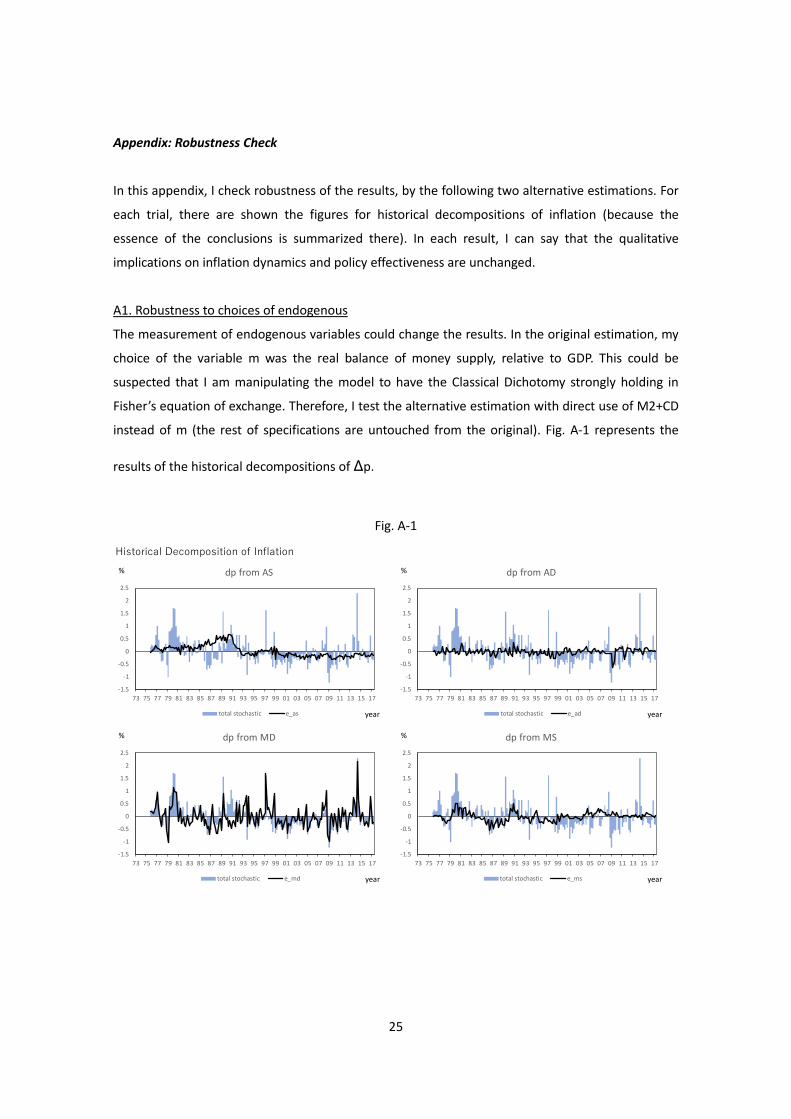

Appendix: Robustness Check

In this appendix, I check robustness of the results, by the following two alternative estimations. For

each trial, there are shown the figures for historical decompositions of inflation (because the

essence of the conclusions is summarized there). In each result, I can say that the qualitative

implications on inflation dynamics and policy effectiveness are unchanged.

A1. Robustness to choices of endogenous

The measurement of endogenous variables could change the results. In the original estimation, my

choice of the variable m was the real balance of money supply, relative to GDP. This could be

suspected that I am manipulating the model to have the Classical Dichotomy strongly holding in

Fisher’s equation of exchange. Therefore, I test the alternative estimation with direct use of M2+CD

instead of m (the rest of specifications are untouched from the original). Fig. A-1 represents the

results of the historical decompositions of Δp.

Fig. A-1

Historical Decomposition of Inflation

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AS

total stochastic e_as

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AD

total stochastic e_ad

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MD

total stochastic e_md

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MS

total stochastic e_ms

%

year

26

A2. Robustness to choices of lags

Also, lags selection can be a factor to alter. AIC was the criteria in the main estimation, and lags are

chosen as four periods (which sounds comfortable for quarterly data). To check the robustness, I

obey SIC and take two periods of lags here (everything else are the same as the original). Fig. A-2

displays the results.

Fig. A-2

Historical Decomposition of Inflation

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AS

total stochastic e_as

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from AD

total stochastic e_ad

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MD

total stochastic e_md

%

year

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

dp from MS

total stochastic e_ms

%

year

27

References

Blanchard, O. J. and D. Quah (1989), “The dynamic effects of aggregate demand and supply

disturbances”, The American Economic Review, 82(4), 901-921.

―――― (1993), “The Dynamic effects of aggregate demand and supply disturbances: Reply”, The

American Economic Review, 83(3), 653-658.

Dickey, D. A. and W. A. Fuller (1979), “Distribution of the estimators for autoregressive time series

with a unit root”, Journal of the American Statistical Association, 74, 427-431.

Eggertsson, G. B. (2010), “What fiscal policy is effective at zero interest rates?”, NBER

Macroeconomics Annual, University of Chicago Press, 25, 59-112.

Faust, J. and M. Leeper (1997), “When do long-run identification restrictions give reliable results?”,

Journal of Business & Economic Statistics, 15(3), 345-353.

Gali, J. (1992), “How well does the IS-LM model fit postwar U.S. data?”, Quarterly Journal of

Economics, May., 709-738.

Gerlach, S. and F. Smets (1995), “The monetary transmission mechanism: Evidence from the G-7

countries”, BIS working paper, No. 26.

Hyndman, R. J., A. B. Koehler, R. D. Snyder, and S. Grose (2002), “A state space framework for

automatic forecasting using exponential smoothing methods,” International Journal of Forecasting,

18, 439-454.

Johansen, S. and K. Juselius (1990), “Maximum likelihood estimation and inferences on

cointegration —with applications to the demand for money”, Oxford Bulletin of Economics and

Statistics, 52, 169-210.

Kwiatkowski, D., P. C. B. Phillips, P. Schmidt and Y. Shin (1992), “Testing the null hypothesis of

stationary against the alternative of a unit root”, Journal of Econometrics, 54, 159-178.

Lippi, M., and L. Reichlin (1993), “The dynamic effects of aggregate demand and supply

28

disturbances: Comment”, The American Economic Review, 83(3), 644-652.

Ljung, G. M. and G. E. P. Box (1978), "On a measure of a lack of fit in time series models",

Biometrika, 65(2), 297-303.

MacKinnon, J. G. (1996), “Numerical distribution functions for unit root and cointegration tests”,

Journal of Applied Econometrics, 11, 601-618.

MacKinnon, J. G., A. A. Haug, and L. Michelis (1999), “Numerical distribution functions of likelihood

ratio tests for cointegration”, Journal of Applied Econometrics, 14, 563-577.

Mio, H. (2002), “Identifying aggregate demand and aggregate supply components of inflation rate:

A structural vector autoregression analysis for Japan”, Monetary and Economic Studies, 20(1), 33-

56.

Schenkelberg, H. and S. Watzka (2013), “Real effects of quantitative easing at the zero lower bound:

Structural VAR-based evidence from Japan”, Journal of International Money and Finance, 33, 327-

357.

Shapiro, M. D., and M. W. Watson (1988), “Sources of business cycle fluctuations”, NBER

Macroeconomic Annual, MIT Press, 3, 111-156.

Stock, J. H., and M. W. Watson (2001), “Vector autoregressions”, The Journal of Economic

Perspectives, 15(4), 101-115.