Embed Size (px)

Citation preview

SOULCYCLE BRAZIL

MIND + BODY + CARDIO = SOULCYCLE

Take your journey. Change your body. Find your soul.

SOULCYCLE has done more than revolutionize indoor cycling and become the most popular cycling fitness trend to date. Each SOULCYCLE ride delivers a FULL-BODY workout that is fun, energized atmospherically and mentally inspiring as well. Riders using the SOULCYCLE Method work their core and lift hand weights to tone their upper body. While in select studios, SoulBands are offered in their revolutionary class that challenges the whole body through the use of resistance training where bands hang above the bikes. So that each rider gets a full 60 minutes of toning key upper body muscles while minting fat-burning cardio intervals. SOULCYCLE combines a killer card and anaerobic workout fused with a transcendental atmosphere, motivational music and inspirational coaching.

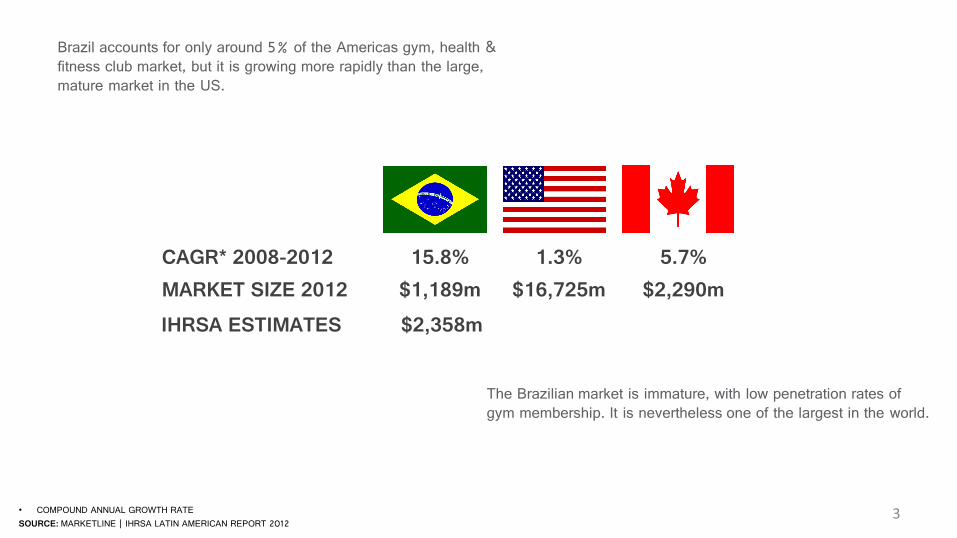

Brazil accounts for only around 5% of the Americas gym, health & fitness club market, but it is growing more rapidly than the large, mature market in the US.

CAGR* 2008-2012 15.8% 1.3% 5.7% MARKET SIZE 2012 $1,189m $16,725m $2,290m

The Brazilian market is immature, with low penetration rates of gym membership. It is nevertheless one of the largest in the world.

• COMPOUND ANNUAL GROWTH RATE SOURCE: MARKETLINE | IHRSA LATIN AMERICAN REPORT 2012 3

IHRSA ESTIMATES $2,358m

4

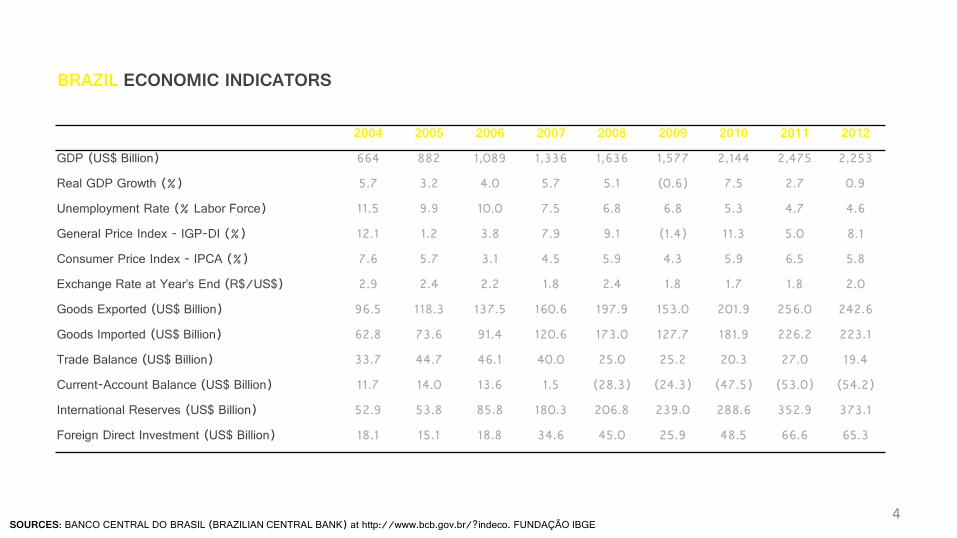

2004 2005 2006 2007 2008 2009 2010 2011 2012 GDP (US$ Billion) 664 882 1,089 1,336 1,636 1,577 2,144 2,475 2,253 Real GDP Growth (%) 5.7 3.2 4.0 5.7 5.1 (0.6) 7.5 2.7 0.9 Unemployment Rate (% Labor Force) 11.5 9.9 10.0 7.5 6.8 6.8 5.3 4.7 4.6 General Price Index - IGP-DI (%) 12.1 1.2 3.8 7.9 9.1 (1.4) 11.3 5.0 8.1 Consumer Price Index - IPCA (%) 7.6 5.7 3.1 4.5 5.9 4.3 5.9 6.5 5.8 Exchange Rate at Year’s End (R$/US$) 2.9 2.4 2.2 1.8 2.4 1.8 1.7 1.8 2.0 Goods Exported (US$ Billion) 96.5 118.3 137.5 160.6 197.9 153.0 201.9 256.0 242.6 Goods Imported (US$ Billion) 62.8 73.6 91.4 120.6 173.0 127.7 181.9 226.2 223.1 Trade Balance (US$ Billion) 33.7 44.7 46.1 40.0 25.0 25.2 20.3 27.0 19.4 Current-Account Balance (US$ Billion) 11.7 14.0 13.6 1.5 (28.3) (24.3) (47.5) (53.0) (54.2) International Reserves (US$ Billion) 52.9 53.8 85.8 180.3 206.8 239.0 288.6 352.9 373.1 Foreign Direct Investment (US$ Billion) 18.1 15.1 18.8 34.6 45.0 25.9 48.5 66.6 65.3

SOURCES: BANCO CENTRAL DO BRASIL (BRAZILIAN CENTRAL BANK) at http://www.bcb.gov.br/?indeco. FUNDAÇÃO IBGE

BRAZIL ECONOMIC INDICATORS

5

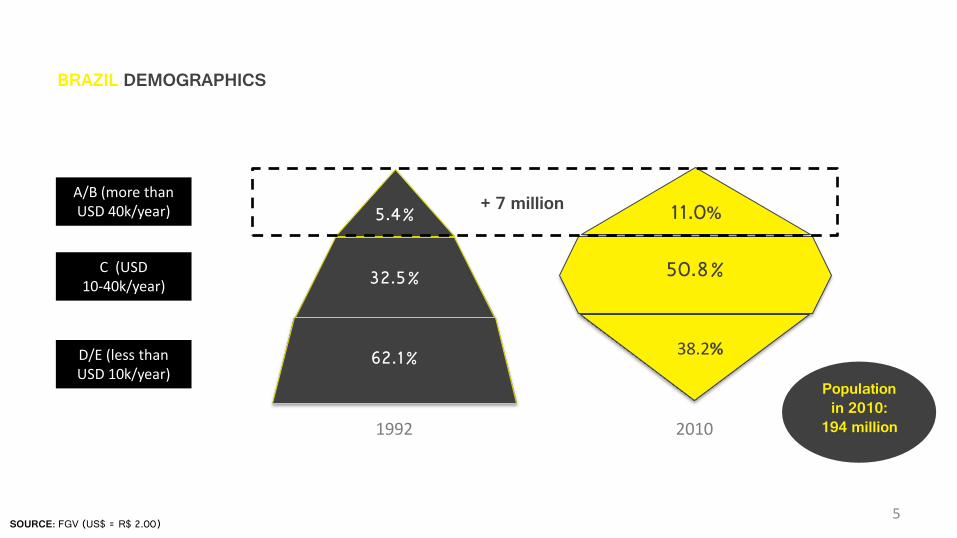

32.5%

62.1%

1992

11.0%

50.8%

38.2%

2010

A/B (more than USD 40k/year)

C (USD 10-40k/year)

D/E (less than USD 10k/year)

5.4%

Population in 2010:

194 million

SOURCE: FGV (US$ = R$ 2.00)

+ 7 million

BRAZIL DEMOGRAPHICS

6 SOURCE: IBGE

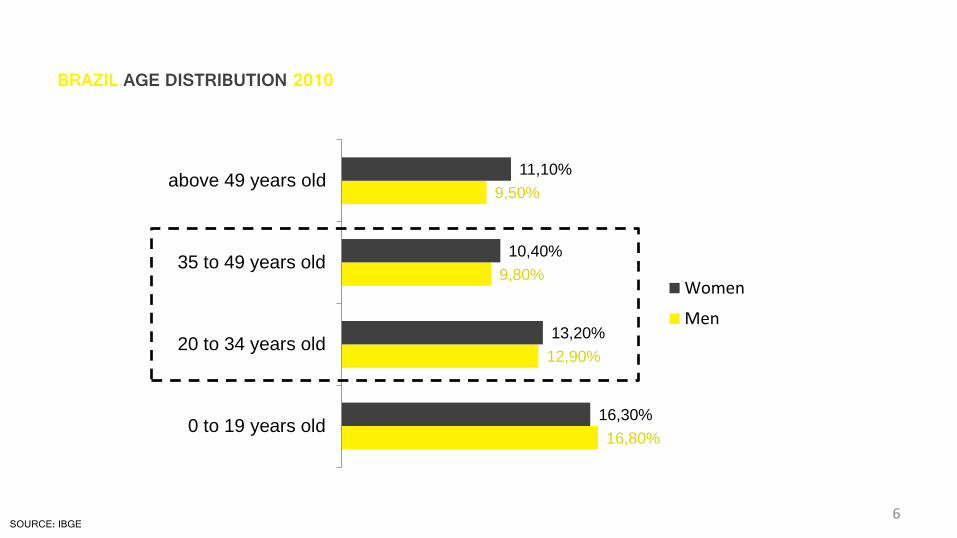

16,80%

12,90%

9,80%

9,50%

16,30%

13,20%

10,40%

11,10%

0 to 19 years old

20 to 34 years old

35 to 49 years old

above 49 years old

Women

Men

BRAZIL AGE DISTRIBUTION 2010

7

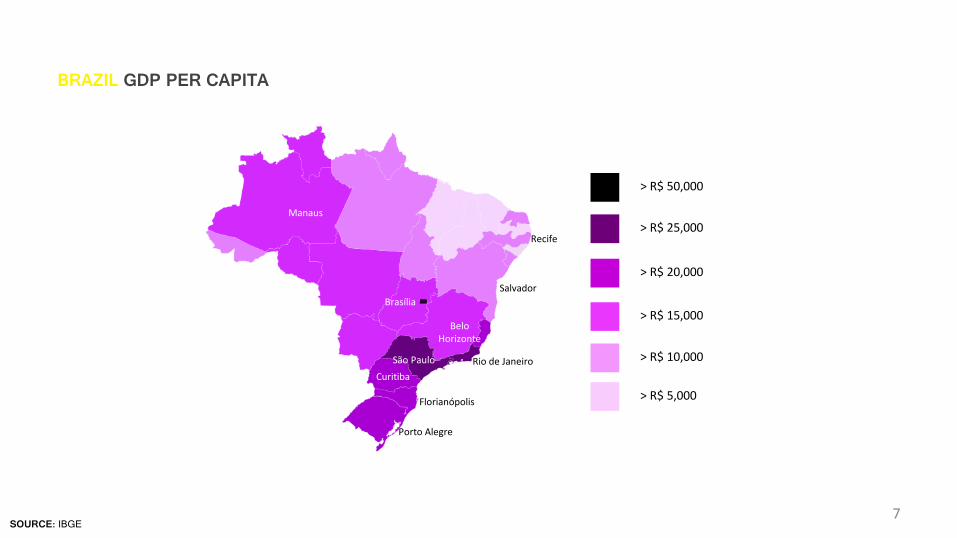

> R$ 50,000

> R$ 25,000

> R$ 20,000

> R$ 15,000

> R$ 5,000

> R$ 10,000 São Paulo Rio de Janeiro

Brasília

Florianópolis

Curitiba

Manaus

Recife

Salvador

Belo Horizonte

SOURCE: IBGE

Porto Alegre

BRAZIL GDP PER CAPITA

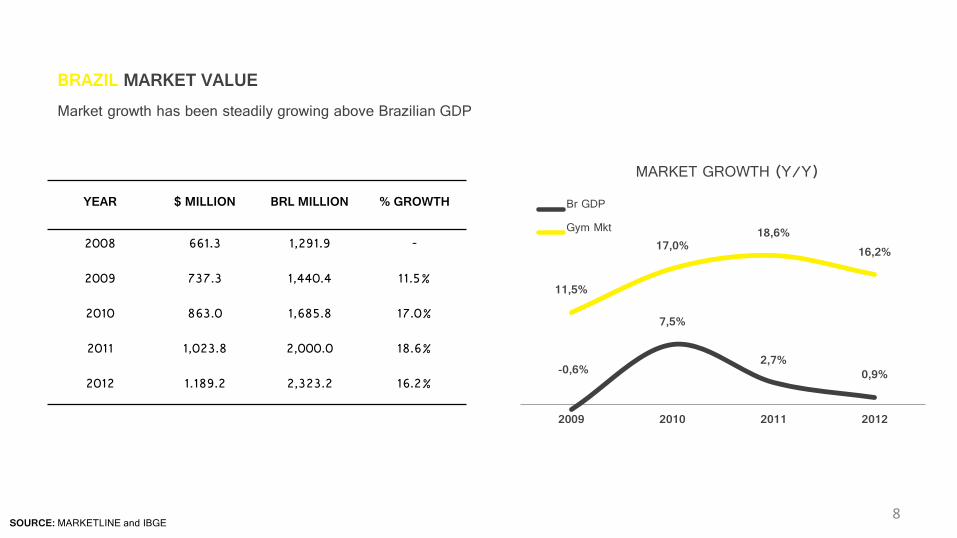

BRAZIL MARKET VALUE

YEAR $ MILLION BRL MILLION % GROWTH

2008 661.3 1,291.9 -

2009 737.3 1,440.4 11.5%

2010 863.0 1,685.8 17.0%

2011 1,023.8 2,000.0 18.6%

2012 1.189.2 2,323.2 16.2%

SOURCE: MARKETLINE and IBGE 8

Market growth has been steadily growing above Brazilian GDP

-0,6%

7,5%

2,7% 0,9%

11,5%

17,0% 18,6%

16,2%

2009 2010 2011 2012

MARKET GROWTH (Y/Y) Br GDPGym Mkt

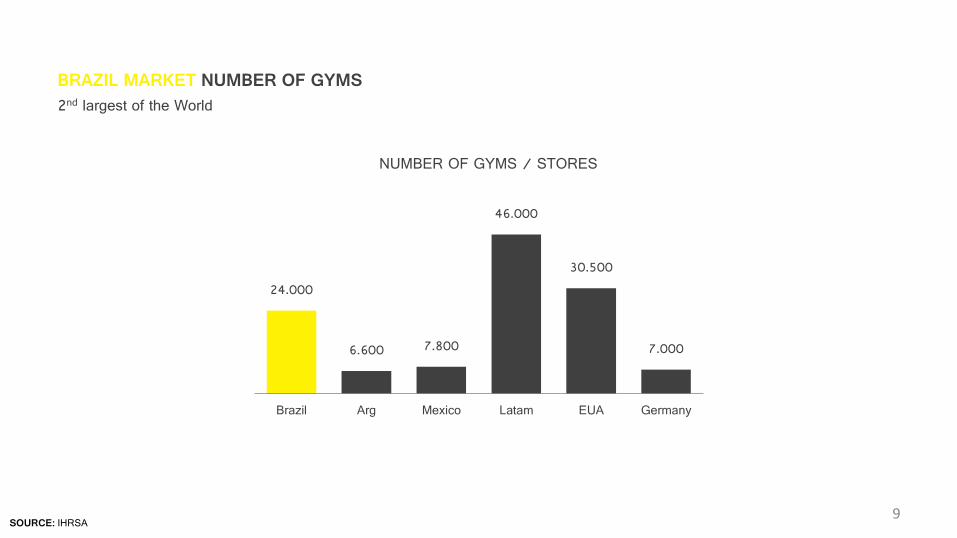

BRAZIL MARKET NUMBER OF GYMS 2nd largest of the World

SOURCE: IHRSA 9

24.000

6.600 7.800

46.000

30.500

7.000

Brazil Arg Mexico Latam EUA Germany

NUMBER OF GYMS / STORES

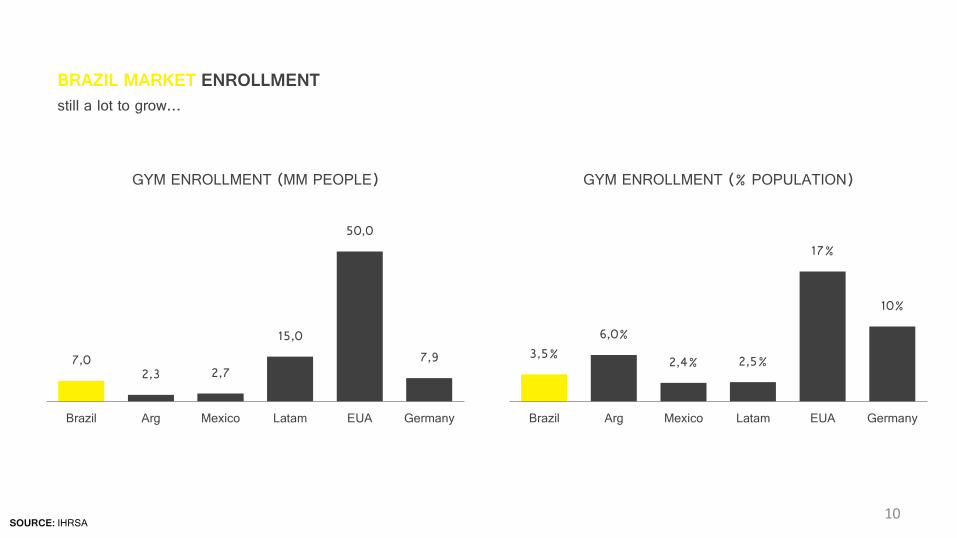

BRAZIL MARKET ENROLLMENT still a lot to grow…

SOURCE: IHRSA 10

7,0 2,3 2,7

15,0

50,0

7,9

Brazil Arg Mexico Latam EUA Germany

GYM ENROLLMENT (MM PEOPLE)

3,5% 6,0%

2,4% 2,5%

17%

10%

Brazil Arg Mexico Latam EUA Germany

GYM ENROLLMENT (% POPULATION)

11 SOURCE: MARKETLINE

MARKET HIGHLIGHTS

The market is highly fragmented. There are more than 23,000 gyms and fitness clubs in Brazil, but even leading players such as BodyTech have fewer than 100 locations, equating to a market share by volume of less than 0.5%. The Brazilian market is expanding rapidly in value, which means that it is quite possible for one player to increase revenue without encroaching on its rivals’ market share. This weakens rivalry. Also, exit costs are low, which should tend to ease rivalry as companies (or franchise locations) that are unprofitable can leave the market rather than struggle in an unprofitable business. However, players tend to be highly focused on their core business, with little diversification of revenue streams, which tends to boost rivalry.

12 SOURCE: VEJASP

MARKET HIGHLIGHTS

90%

10%

GYM SIZE IN BRAZIL

Small (500sqm) Big (500sqm +)

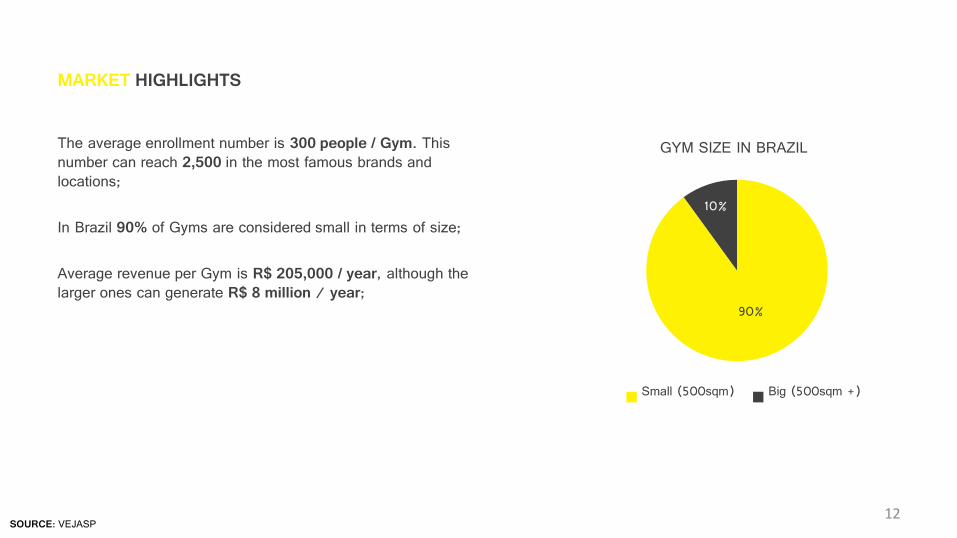

The average enrollment number is 300 people / Gym. This number can reach 2,500 in the most famous brands and locations; In Brazil 90% of Gyms are considered small in terms of size; Average revenue per Gym is R$ 205,000 / year, although the larger ones can generate R$ 8 million / year;

13 SOURCE: IHRSA

MARKET HIGHLIGHTS

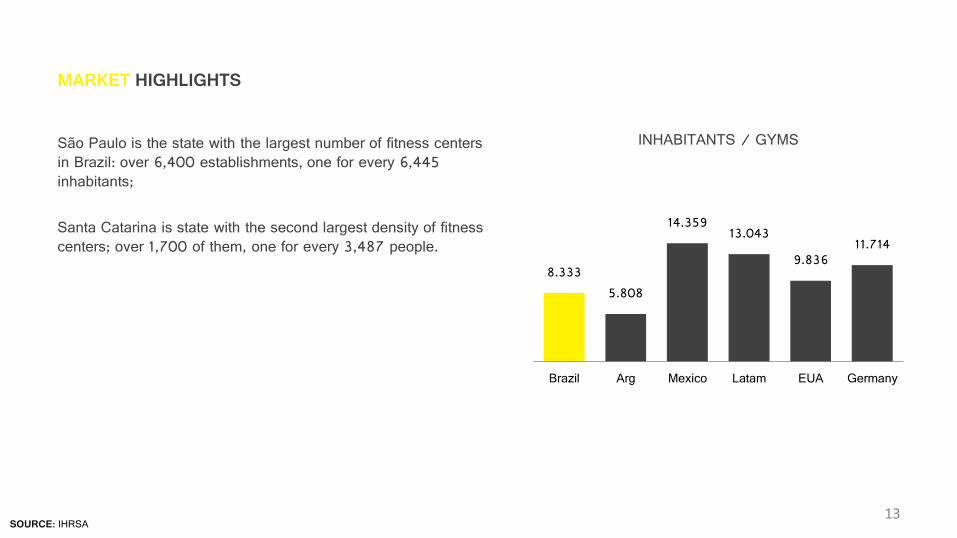

São Paulo is the state with the largest number of fitness centers in Brazil: over 6,400 establishments, one for every 6,445 inhabitants; Santa Catarina is state with the second largest density of fitness centers; over 1,700 of them, one for every 3,487 people.

8.333 5.808

14.359 13.043 9.836

11.714

Brazil Arg Mexico Latam EUA Germany

INHABITANTS / GYMS

14 SOURCE: IBGE

BRAZIL NEW ENTRANTS

The Brazilian fitness market is expanding rapidly, which will attract new players, including foreign companies wishing to expand beyond their domestic markets. Capital barriers to market entry are low. It is common for fitness centers to expand by franchising, and the investment required is within the reach of many individuals with some savings available. Furthermore, factors such as regulation and intellectual property have little impact on the ease of entrance. Fitness centers operate as self-contained units, and there are limited opportunities for scale economies in this market, beyond perhaps some back-office functions in the larger chains.

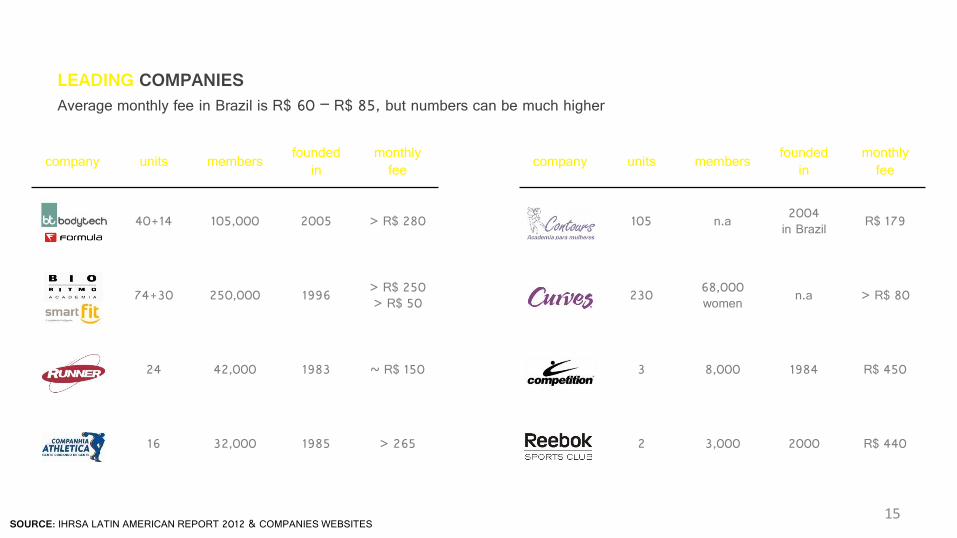

company units members founded in

monthly fee company units members founded

in monthly

fee

40+14 105,000 2005 > R$ 280 105 n.a 2004 in Brazil R$ 179

74+30 250,000 1996 > R$ 250 > R$ 50 230 68,000

women n.a > R$ 80

24 42,000 1983 ~ R$ 150 3 8,000 1984 R$ 450

16 32,000 1985 > 265 2 3,000 2000 R$ 440

15 SOURCE: IHRSA LATIN AMERICAN REPORT 2012 & COMPANIES WEBSITES

LEADING COMPANIES Average monthly fee in Brazil is R$ 60 – R$ 85, but numbers can be much higher

company initial capex area monthly fees

R$ 890,000 ~ 1,100,000 500 m2 Royalties: 6% of GR

Advert.: 2% of GR

R$ 550,000 ~ 1,500,000 800 m2 Royalties: up to 10%

Advert.: 4.5% of GR

R$ 260,000 ~ 280,000 250 m2 Royalties: R$28

Advert.: R$790

R$ 140,000 n.i n.i

R$ 210,000 ~ 310,000 120 m2 Advert.: 2% of GR

16 SOURCE: www.franquiaagora.com.br

GYM FRANCHISES

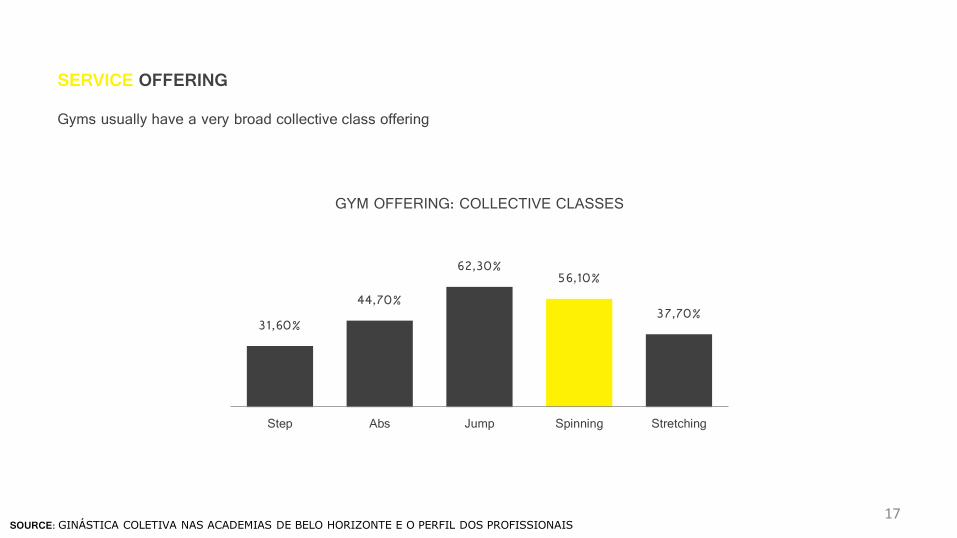

17 SOURCE: GINÁSTICA COLETIVA NAS ACADEMIAS DE BELO HORIZONTE E O PERFIL DOS PROFISSIONAIS

SERVICE OFFERING Gyms usually have a very broad collective class offering

31,60% 44,70%

62,30% 56,10%

37,70%

Step Abs Jump Spinning Stretching

GYM OFFERING: COLLECTIVE CLASSES

18 SOURCE: VEJASP

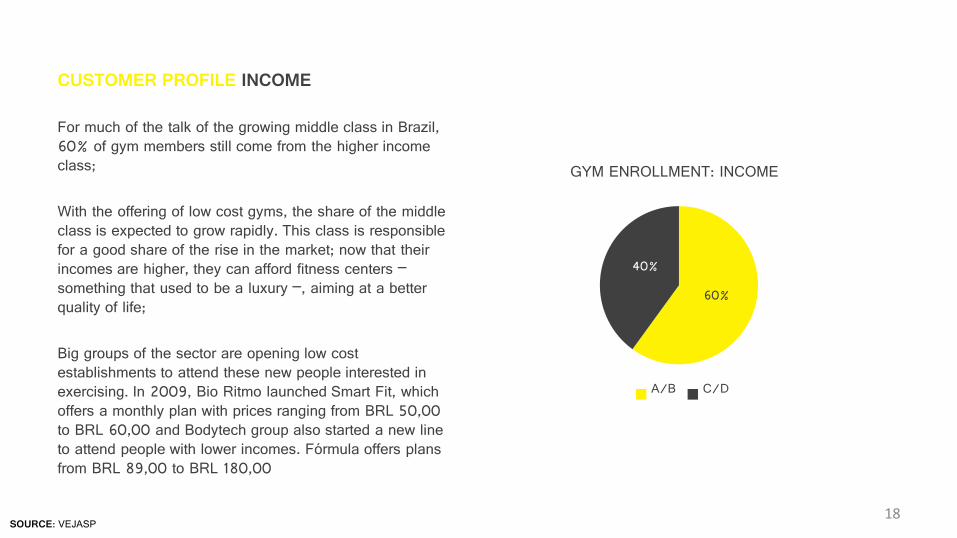

CUSTOMER PROFILE INCOME

For much of the talk of the growing middle class in Brazil, 60% of gym members still come from the higher income class; With the offering of low cost gyms, the share of the middle class is expected to grow rapidly. This class is responsible for a good share of the rise in the market; now that their incomes are higher, they can afford fitness centers – something that used to be a luxury –, aiming at a better quality of life; Big groups of the sector are opening low cost establishments to attend these new people interested in exercising. In 2009, Bio Ritmo launched Smart Fit, which offers a monthly plan with prices ranging from BRL 50,00 to BRL 60,00 and Bodytech group also started a new line to attend people with lower incomes. Fórmula offers plans from BRL 89,00 to BRL 180,00

60%

40%

GYM ENROLLMENT: INCOME

A/B C/D

19 SOURCE: MOTIVAÇÃO PARA A PRÁTICA DE MUSCULAÇÃO DE ADERENTES E DESISTENTES DE ACADEMIAS - FLORIANOPOLIS2011

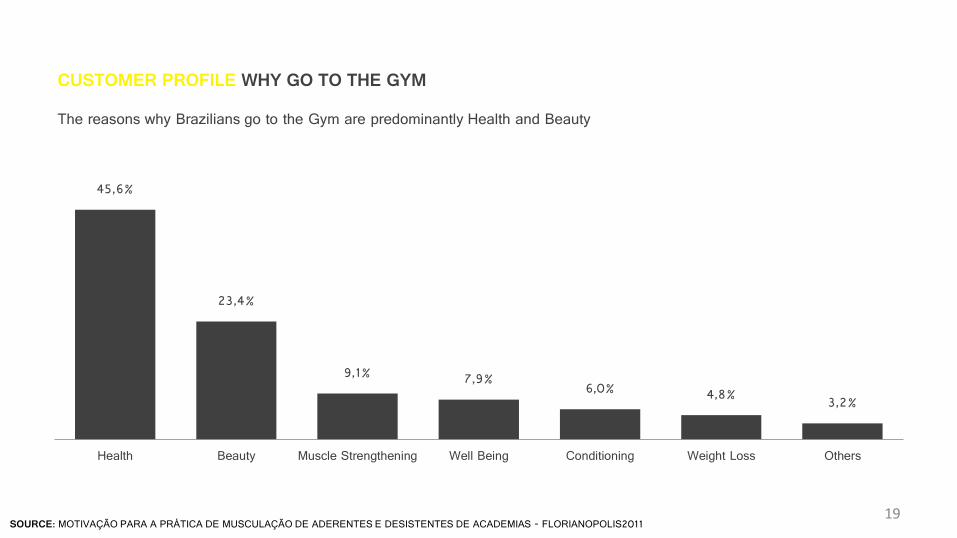

CUSTOMER PROFILE WHY GO TO THE GYM The reasons why Brazilians go to the Gym are predominantly Health and Beauty

45,6%

23,4%

9,1% 7,9% 6,0% 4,8% 3,2%

Health Beauty Muscle Strengthening Well Being Conditioning Weight Loss Others

20 SOURCE: VEJA SÃO PAULO

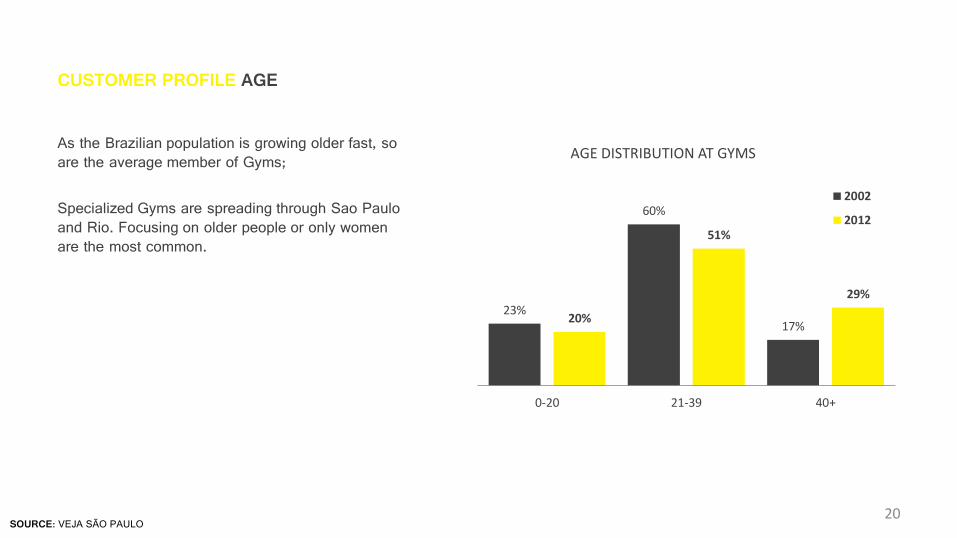

CUSTOMER PROFILE AGE

As the Brazilian population is growing older fast, so are the average member of Gyms; Specialized Gyms are spreading through Sao Paulo and Rio. Focusing on older people or only women are the most common.

23%

60%

17% 20%

51%

29%

0-20 21-39 40+

AGE DISTRIBUTION AT GYMS

2002

2012

21 SOURCE: DELLOITE

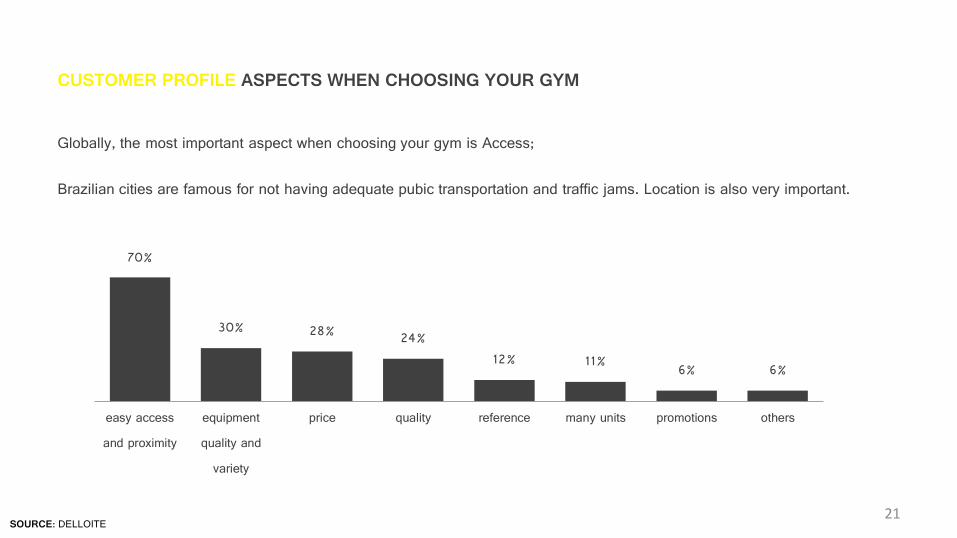

CUSTOMER PROFILE ASPECTS WHEN CHOOSING YOUR GYM

Globally, the most important aspect when choosing your gym is Access; Brazilian cities are famous for not having adequate pubic transportation and traffic jams. Location is also very important.

70%

30% 28% 24% 12% 11% 6% 6%

easy accessand proximity

equipmentquality and

variety

price quality reference many units promotions others

22 SOURCE: DELLOITE

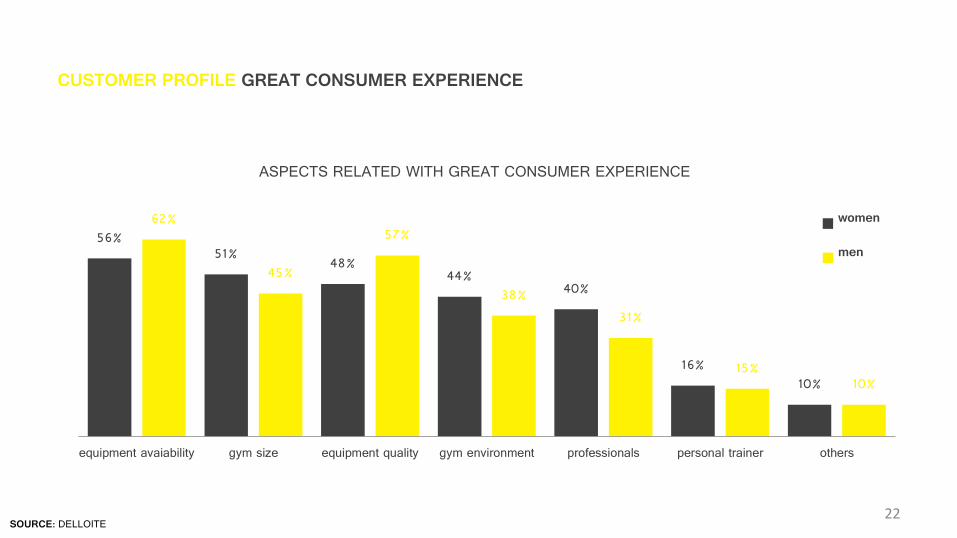

CUSTOMER PROFILE GREAT CONSUMER EXPERIENCE

56% 51% 48%

44% 40%

16% 10%

62%

45%

57%

38% 31%

15% 10%

equipment avaiability gym size equipment quality gym environment professionals personal trainer others

ASPECTS RELATED WITH GREAT CONSUMER EXPERIENCE

women

men

23 SOURCE: PERFIL DOS USUÁRIOS DE MUSCULAÇÃO DA UNISC: UM OLHAR SOBRE A FREQUÊNCIA E PERMANÊNCIA NA ACADEMIA

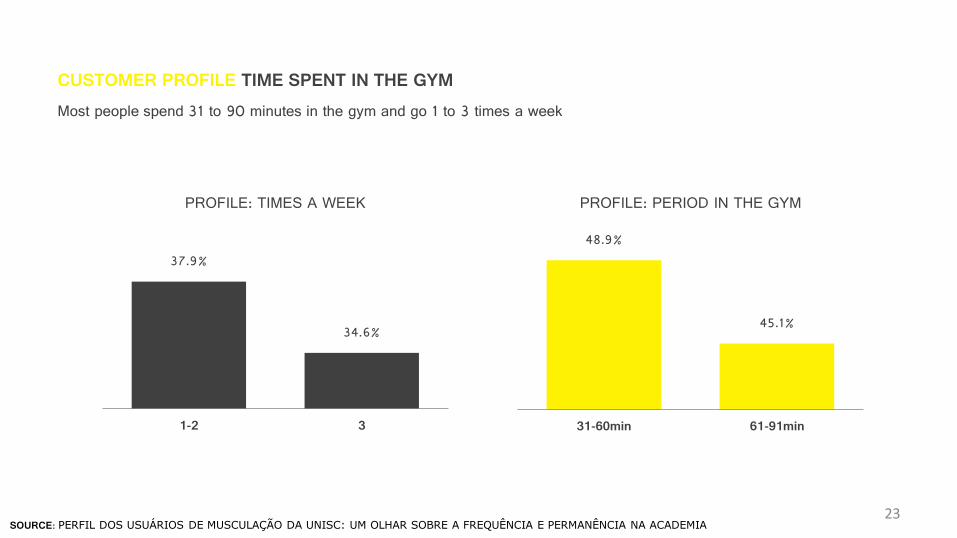

CUSTOMER PROFILE TIME SPENT IN THE GYM Most people spend 31 to 90 minutes in the gym and go 1 to 3 times a week

37.9%

34.6%

1-2 3

PROFILE: TIMES A WEEK

48.9%

45.1%

31-60min 61-91min

PROFILE: PERIOD IN THE GYM

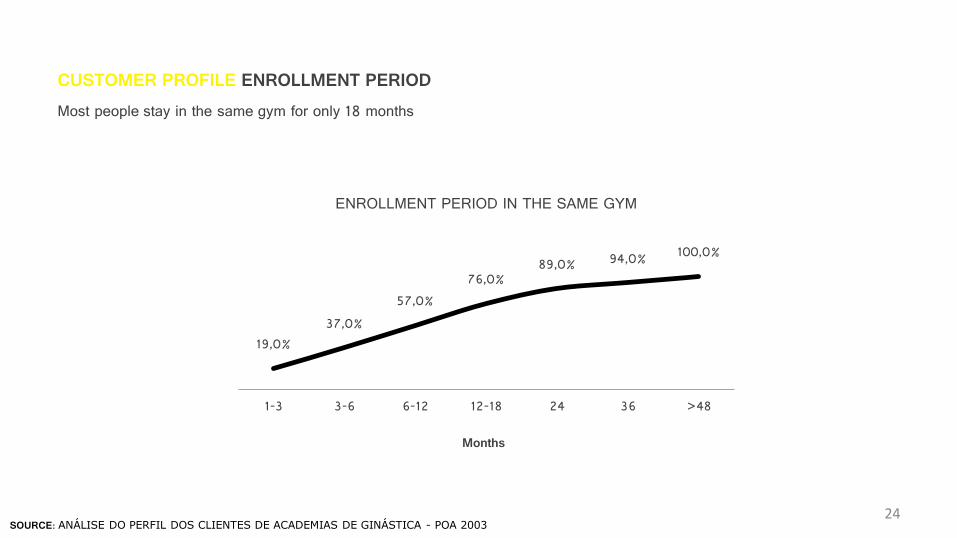

24 SOURCE: ANÁLISE DO PERFIL DOS CLIENTES DE ACADEMIAS DE GINÁSTICA - POA 2003

CUSTOMER PROFILE ENROLLMENT PERIOD Most people stay in the same gym for only 18 months

19,0% 37,0%

57,0% 76,0%

89,0% 94,0% 100,0%

1-3 3-6 6-12 12-18 24 36 >48

Months

ENROLLMENT PERIOD IN THE SAME GYM

25 SOURCE: ADERÊNCIA AOS PROGRAMAS DE EXERCÍCIOS FÍSICOS EM ACADEMIAS DE GINÁSTICA NA CIDADE DE CURITIBA – PR

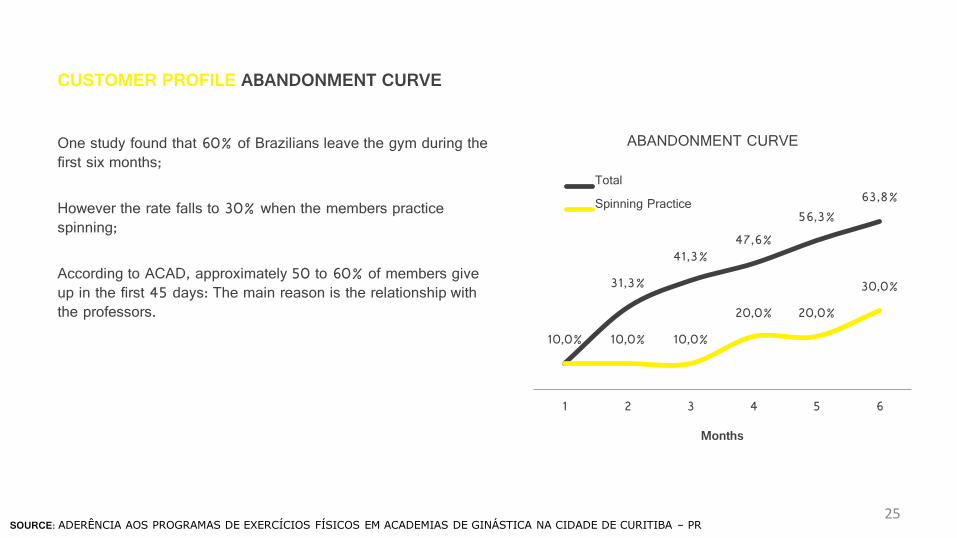

CUSTOMER PROFILE ABANDONMENT CURVE

One study found that 60% of Brazilians leave the gym during the first six months; However the rate falls to 30% when the members practice spinning; According to ACAD, approximately 50 to 60% of members give up in the first 45 days: The main reason is the relationship with the professors.

10,0%

31,3% 41,3%

47,6% 56,3%

63,8%

10,0% 10,0% 20,0% 20,0%

30,0%

1 2 3 4 5 6

Months

ABANDONMENT CURVE

TotalSpinning Practice

26 SOURCE: HEALTH MINISTRY

BRAZIL OBESITY SNAPSHOT

51% are overweight (more than 100 million people) 17% are obese (around 34m people). In 2006, it was 11.6% 33.5% exercises regularly (39.6% men and 22.4% women) 10% uses some sort of medicine to loose weight (among the highest rates of the world) Porto Alegre is the city with higher percentage of overweight people

27 SOURCE: IHRSA

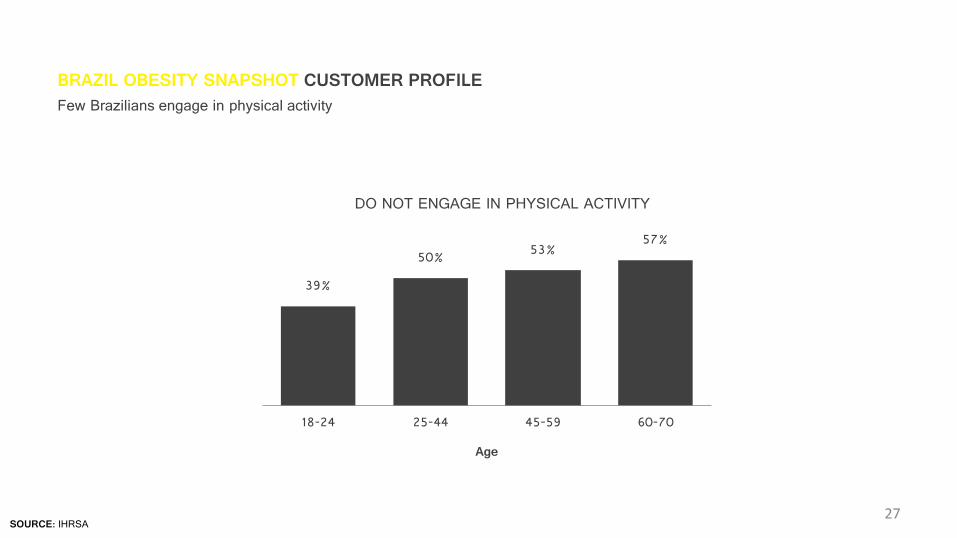

BRAZIL OBESITY SNAPSHOT CUSTOMER PROFILE Few Brazilians engage in physical activity

39% 50% 53% 57%

18-24 25-44 45-59 60-70

Age

DO NOT ENGAGE IN PHYSICAL ACTIVITY

28 SOURCE: IHRSA and IG GUIA DE PROFISSÕES

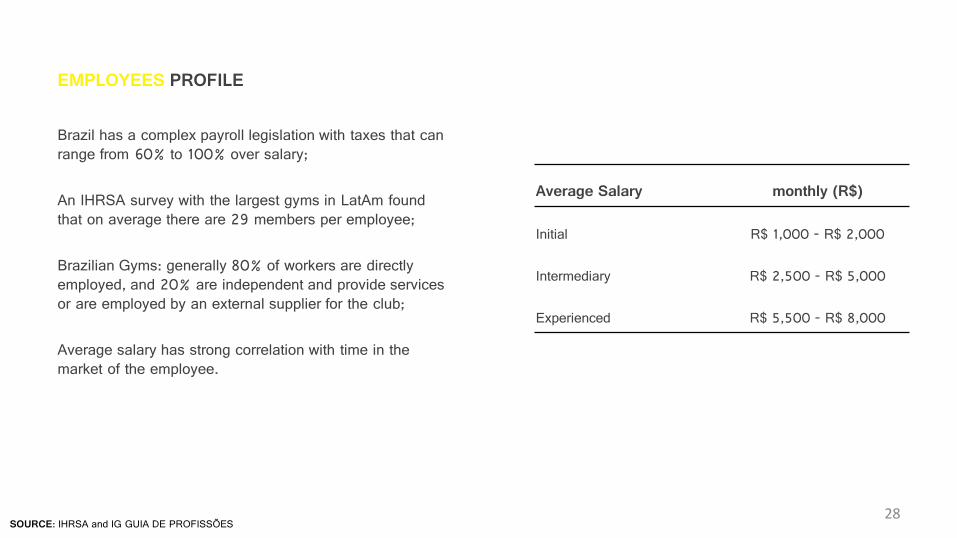

EMPLOYEES PROFILE

Brazil has a complex payroll legislation with taxes that can range from 60% to 100% over salary; An IHRSA survey with the largest gyms in LatAm found that on average there are 29 members per employee; Brazilian Gyms: generally 80% of workers are directly employed, and 20% are independent and provide services or are employed by an external supplier for the club; Average salary has strong correlation with time in the market of the employee.

Average Salary monthly (R$)

Initial R$ 1,000 - R$ 2,000

Intermediary R$ 2,500 - R$ 5,000

Experienced R$ 5,500 - R$ 8,000