Embed Size (px)

Citation preview

2

SOLVING TOO BIG TO FAIL BANKING RECOVERY, RESOLUTION AND STRUCTURAL REFORM26 June 2015, Dublin

2

Recovery and Resolution in Europe - Three pillars

▪ Set of harmonised tools for bank recovery and resolution.

▪ Avoids bail-out of banks by taxpayers and fragmentation of the single market.

Bank Recovery and Resolution Directive

▪ Eliminates tensions between single supervisor (ECB) and national resolution authorities

▪ Provides for strong central decision-making on resolution decisions

▪ Breaks the the link between sovereigns and banks

Single Resolution Mechanism

▪ Provides loans to Members States for recapitalisation of financial institutions.

European Stability Mechanism

3

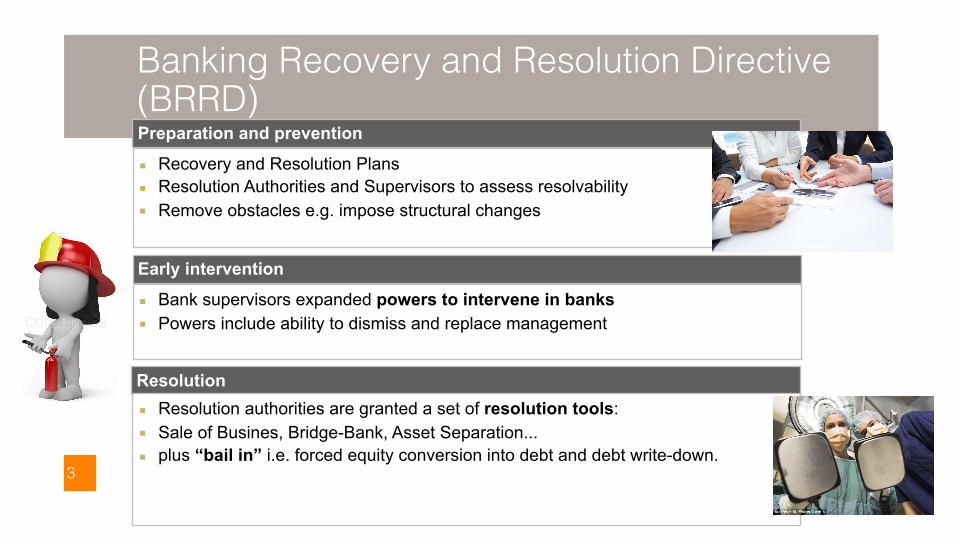

Banking Recovery and Resolution Directive (BRRD)

Page ▪ X

Early intervention

▪ Bank supervisors expanded powers to intervene in banks ▪ Powers include ability to dismiss and replace management

Resolution▪ Resolution authorities are granted a set of resolution tools: ▪ Sale of Busines, Bridge-Bank, Asset Separation... ▪ plus “bail in” i.e. forced equity conversion into debt and debt write-down.

Preparation and prevention

▪ Recovery and Resolution Plans ▪ Resolution Authorities and Supervisors to assess resolvability ▪ Remove obstacles e.g. impose structural changes

4

Bail-in tool in detail

Page ▪ X

▪ Any liability not backed by assets or collateral

▪ Exclusions: deposits protected by DGS; short-term interbank lending, claims of clearing houses and settlement systems, client assets.

▪ Exceptionally, other liabilities can be excluded on an ad hoc basis, to avoid market disruption.

▪ Requirement to maintain a minimum level of liabilities subject to bail-in (MREL)

Scope

▪ Same as ordinary allocation of losses and ranking in insolvency:

▪ Equity first and in full before any debt is written down, starting with subordinated debt and then senior debt.

▪ Depositors from SME and natural persons in excess of EU 100K are preferred over senior creditors.

Write-down hierarchy

▪ Exceptionally and where necessary for financial stability, bail-in can be discontinued upon reaching 8% of total liabilities, including capital.

▪ After this, banks-financed resolution funds can contribute to loss absorbtion or provide liquidity

Thresholds

5

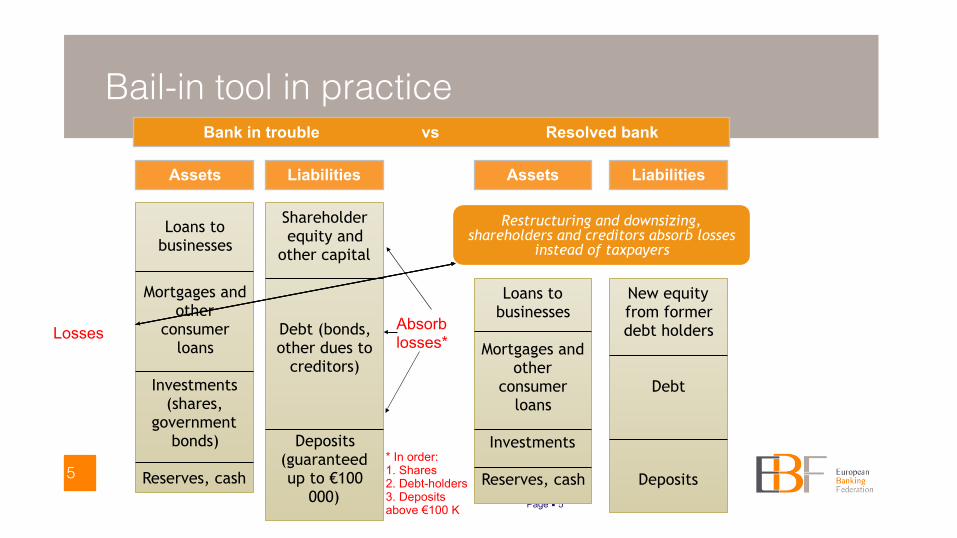

Bail-in tool in practice

Page ▪ 5

Loans to businesses

Mortgages and other

consumer loans

Investments (shares,

government bonds)

Reserves, cash

Shareholder equity and

other capital

Debt (bonds, other dues to

creditors)

Deposits (guaranteed up to €100

000)

Losses

Loans to businesses

Mortgages and other

consumer loans

Investments

Reserves, cash

New equity from former debt holders

Debt

Deposits

Absorb losses*

* In order: 1. Shares 2. Debt-holders 3. Deposits above €100 K

Restructuring and downsizing, shareholders and creditors absorb losses

instead of taxpayers

Bank in trouble vs Resolved bank

Assets Liabilities Assets Liabilities

6

Financing of bank resolutionFunding Application of Funds

▪ Member States to set up resolution funds (RFs) financedex ante by banks

▪ Bank contributions in proportion to liabilities and risk profile

▪ Banks to pay annually to reach 1% of covered deposit over a 10-year period

▪ Borrowing between national arrnagements is possible

▪ RFs to compensate costs derived from use of resolution tools e.g. providing loans to a bridge institution, guarantee certain asssets or liabilities, etc

▪ Once 8% of Total Liabilities is bailed in, RFs can exceptionally be used for recapitalisation

7

Single Resolution Mechanism Objectives

▪ European decision-making structure that is legally sound and effective in times of crisis – not a mere network

▪ Alignment of responsibility for supervision, resolution and funding at EU level

Centralised decision making on bank resolution▪ A Single Resolution Board adopts a resolution scheme, upon notification from the

ECB that a bank is failing or likely to fail

Scope

▪ Mirror SSM: Euro Area and other participating Member States ▪ All banks

8

Single Resolution Mechanism(cont.)

Decentralised execution

▪ National resolution authorities implement resolution decisions in line with national company and insolvency law

Centralised financing arrangements

▪ A Single Resolution Fund (SRF) under the control of the Board ▪ 1% of covered deposits in participating Member States over 8 years. ▪ The banking sector will contribute annually 12,5% of target amount i.e. around 6.8

billion ▪ Initially SRF composed of national compartments, but… ▪ National compartments will be mutualised gradually: 60% over the first two years

and 6.7% in each of the remaining six years.

EU endorsement

▪ Commission and, to a lesser extent, Council ensorse resolution scheme proposed by Board within 32 hours

9

Resolution procedure under the SRM

Page ▪ 9

Bank likely to fail

Board assesses situation and proposes resolution decision together with national resolution authorities based on resolution plans

COM decides to trigger resolution and instructs Board to execute the measures, checking consistency with EU State aid rules

ECB notifies Board, COM and relevant national authorities

National resolution authorities implement (e.g. bail-in, bridge bank)

10

Timeline

Legal framework

Single Resolution Fund

European Stability Mechanism

BBRD & SRM Full bail-in

SRF built up (within 8 years) able to borrow from markets

Possible ESM direct recap

Possible ESM direct recapitalisation and fiscal backstop, progressive decrease as fund and

bail-in develop

Autumn 2014 January 2015

January 2016

January 2024

11

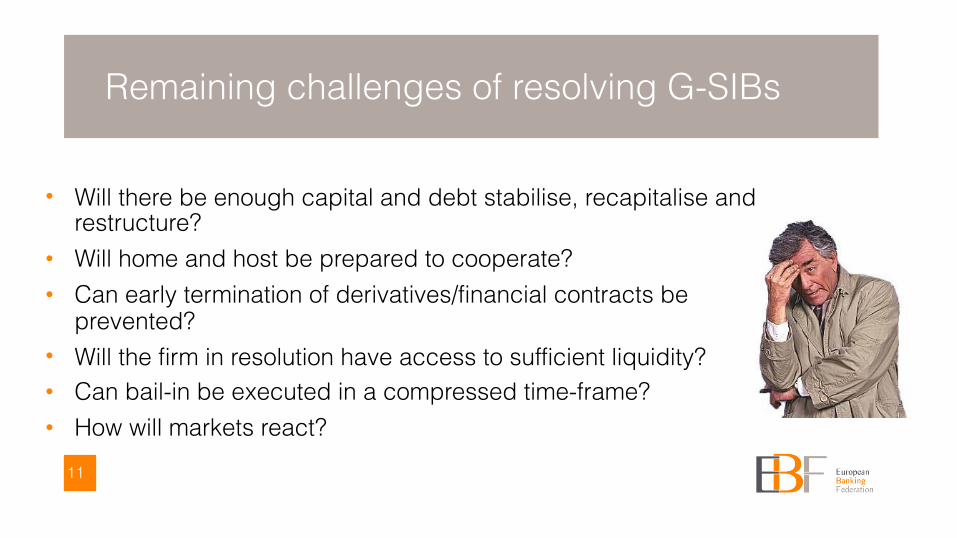

Remaining challenges of resolving G-SIBs

• Will there be enough capital and debt stabilise, recapitalise and restructure?

• Will home and host be prepared to cooperate? • Can early termination of derivatives/financial contracts be

prevented? • Will the firm in resolution have access to sufficient liquidity? • Can bail-in be executed in a compressed time-frame? • How will markets react?

12

TLAC: Total Loss Absorbing Capacity

• FSB Scope: intended only for G-SIBs • Calibration: Loss Absorbing and Recapitalisation Capacity:

• 16-20% RWAs or 2x Leverage Ratio plus Pillar 2; buffers “sit on top” • Composition:

• Capital + subordinated debt (expected to be 33%) • Prepositioning:

• 75%-90 within material subsidiaries • Start date:

• 1 January 2019

13

How TLAC fits in your capital structure

TLAC vs MRELTLAC MREL

Scope G-SIBs All banks

Composition Regulatory capital Subordinated debt 2.5 % of RWA in non subordinated debt accepted (difficult)

Regulatory capital Bail-inable debt No subordination requirement

Calibration 16-22% RWA; buffers “sit on top” Pillar 2 add on 2x Leverage Ratio = 6 % ?

Case-by-case approach based on each bank’s characteristics: resolvability assessment; complexity, risk profile, etc.

Prepositioning 75-90% internal TLAC No prepositioning in BRRD

Entry into force No earlier than 1 January 2019 2016 Phase-in period 4 years

15

TLAC discussion in Europe

▪ Will the EU apply the TLAC to G-SIBs only or wider (e.g. D-SIBs)? ▪ Cost of funding? ▪ Best solution for subordination? Strcutural, Operational or Statutory? ▪ Can the EU argue for more OpCo senior debt to be recognised in TLAC? ▪ Pro’s and cons of a common EU regime? ▪ Level playing field vs. flexibility? ▪ Will a breach of TLAC trigger resolution?

17

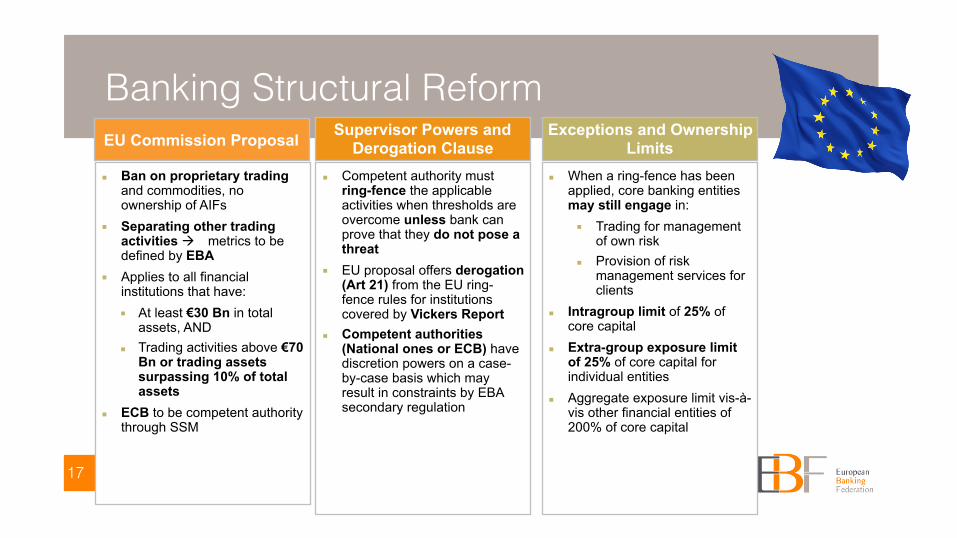

Banking Structural Reform

▪ Competent authority must ring-fence the applicable activities when thresholds are overcome unless bank can prove that they do not pose a threat

▪ EU proposal offers derogation (Art 21) from the EU ring-fence rules for institutions covered by Vickers Report

▪ Competent authorities (National ones or ECB) have discretion powers on a case-by-case basis which may result in constraints by EBA secondary regulation

Supervisor Powers and Derogation Clause

▪ When a ring-fence has been applied, core banking entities may still engage in: ▪ Trading for management

of own risk ▪ Provision of risk

management services for clients

▪ Intragroup limit of 25% of core capital

▪ Extra-group exposure limit of 25% of core capital for individual entities

▪ Aggregate exposure limit vis-à-vis other financial entities of 200% of core capital

Exceptions and Ownership Limits

▪ Ban on proprietary trading and commodities, no ownership of AIFs

▪ Separating other trading activities ! metrics to be defined by EBA

▪ Applies to all financial institutions that have: ▪ At least €30 Bn in total

assets, AND ▪ Trading activities above €70

Bn or trading assets surpassing 10% of total assets

▪ ECB to be competent authority through SSM

EU Commission Proposal

Is BSR still necessary in light of...

■ CRR and BRRD already deliver the tools ■ FSB TLAC to be agreed at G-20 Antalya (15 Nov) ■ Juncker's Jobs and Growth Agenda / CMU ■ Need for competitive Europe ■ Commission’s Better Regulation Package

Major devevlopment since...Council reaches agreement ahead of EP

■Vote on 26 May produced a smorgasbord text drawing from left and right (but not from the compromises) which ultimately was rejected (30 to 29)!

“We don’t know what we are voting for!” - Elisa Ferreira

“Setback is nowhere near big enough to consider a withdrawal of the file.” - according to Lord Hill’s cabinet

19

19

■ECOFIN in Luxembourg (19 June) delivers major political agreement…

Latvian Compromise - step in the right direction

■ The non-automaticity of the zoning approach wrt to separation■ The preservation of market making activities for liquidity, risk management

and clients■ The separation of proprietary trading rather than banning■ A risk based approach to identify excessive risk taking■ And a wider range of flexible solutions including capital add-ons to be

applied proportionally based on two zones 20

20

21

For more information

Tim Buenker [email protected]

European Banking Federation Avenue des Arts 56, B-1000 Brussels European Transparency Register ID number: 4722660838-23. +32 (0)2 508 37 11 | [email protected] | @EBF_FBE www.ebf-fbe.eu

Cover image: European Space Agency