Embed Size (px)

Citation preview

Solvency II Risk Management

for Infrastructure Investments

February 22, 2018

Assetklasse “Flugzeugfinanzierungen”

2

17

26

Infrastructure as a Solvency II Asset Class

Infrastructure & Risk Management

Asset: “Infrastruktur Equity”

Ökonomisches RM (quantitativ)

Agenda

2

13 Anhang29

42 Kontakt & Vorstellung

17 Ökonomisches RM (qualitativ)

10

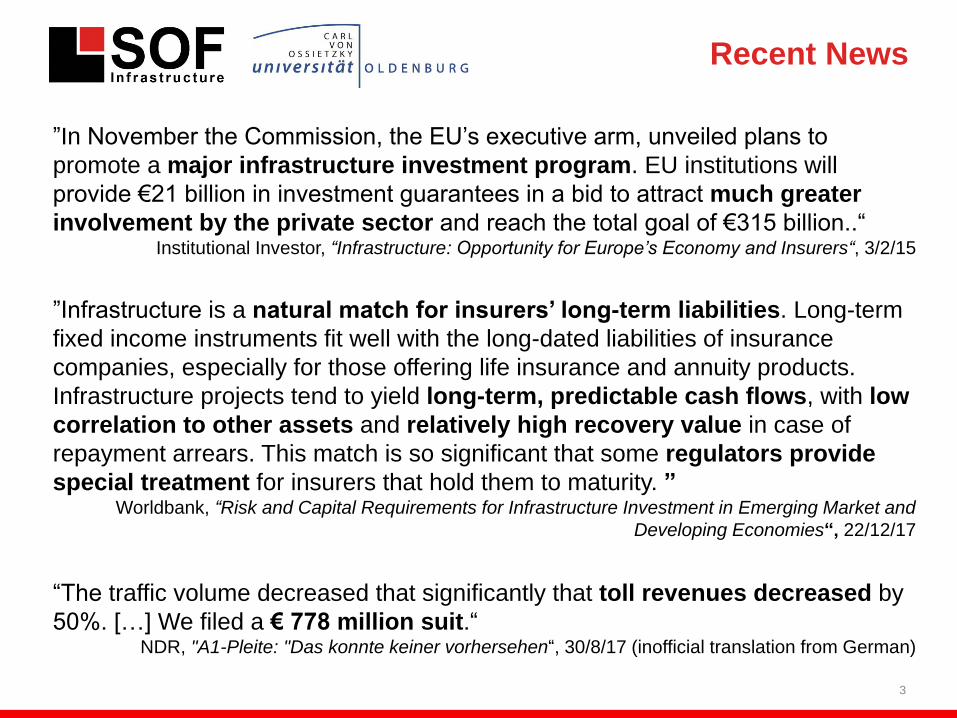

”Infrastructure is a natural match for insurers’ long-term liabilities. Long-term

fixed income instruments fit well with the long-dated liabilities of insurance

companies, especially for those offering life insurance and annuity products.

Infrastructure projects tend to yield long-term, predictable cash flows, with low

correlation to other assets and relatively high recovery value in case of

repayment arrears. This match is so significant that some regulators provide

special treatment for insurers that hold them to maturity. ”Worldbank, “Risk and Capital Requirements for Infrastructure Investment in Emerging Market and

Developing Economies“, 22/12/17

“The traffic volume decreased that significantly that toll revenues decreased by

50%. […] We filed a € 778 million suit.“NDR, "A1-Pleite: "Das konnte keiner vorhersehen“, 30/8/17 (inofficial translation from German)

”In November the Commission, the EU’s executive arm, unveiled plans to

promote a major infrastructure investment program. EU institutions will

provide €21 billion in investment guarantees in a bid to attract much greater

involvement by the private sector and reach the total goal of €315 billion..“Institutional Investor, “Infrastructure: Opportunity for Europe’s Economy and Insurers“, 3/2/15

Recent News

3

Investment Case:

Value Drivers & Risks

4

Tokarevich, Düsterlho (2018) in Insurance Asset Risk. „FAQ: investing in infrastructure under Solvency II”

Investment Case:

Example

5

Infrastructure Loan Government Bond

Market value EUR 100,000,000

(at par)

EUR 93,000,000

(below par)

Purpose of financing Operating management of a tunnel in

UK & France

Government activities of

Italy

Currency EUR EUR

Residual maturity in years 33 30

Listing / External rating No / No (internal rating CQS 3) Yes / CQS 3 (e.g. BBB)

Mod. duration in years 17.6 19.5

Coupon 3.75%, semi-annual 2.7% (of EUR 100,000,000), semi-annual

Return / IRR / Yield to Maturity 3.63% 3.05%

Z spread 1.9% Ca. 1.5%

Solvency II pillar 1 spread risk EUR 18,500,000

(qualifying infrastructure investment)

EUR 0

(government bond)

Economic spread risk EUR 27,600,000

(approximated by the pillar 1 spread

shock for a CQS 3 bond)

EUR 29,500,000

(approximated by the pillar 1 spread

shock for a CQS 3 bond)

Reduction of the economic market risk

through diversification

EUR 20,670,000

(Correlation = 0.25)

EUR 7,360,000

(Correlation = 0.75)

Reduction of the Solvency II interest

rate risk (interest rate down)

EUR 1,200,000 EUR 3,500,000

Operational requirements Higher Lower

Regulatory risk Higher Lower

Investment Case:

Possible Conclusion

6

Lower contribution to the economic market risk (spread) on the portfolio level due

to the stronger diversification benefit

(EUR 6.9m (infrastructure) vs. EUR 22.1m (government bond))

-> Infrastruktur kann sich als Beimischung zu liquiden Portfolios eignen, da

hier der Diversifikationseffekt am höchsten ist

• Higher infrastructure spread compared to the government bond due to the

illiqudity premium and the complexity premium amongst others

• Higher operational requirements and regulatory risks for the infrastructure

loan compared to the government bond

-> Infrastructure could be a suitable complement to liquid Solvency II

portfolios due to the diversification benefit

-> Effective and standardised investment processes could reduce the operational

expenses and thus increase the net spread

-> Ineffecient or ineffective investment processes could reduce the net spread

Please note: Further factors such as regulatory capital requirements or interest rate

risks could play an important role based on the specific requirements of an

individual insurance investor

▪ Wirtschaftliche Definitionen nach Sektoren /

Risikoprofil

• Economic(e.g. transport, energy, IT, environment,...)

• Social(e.g. education, health, sports,…)

• Institutional(e.g. administration, defense,…)

Example

Wind park

selling electricity to

a car manufacturer

for its own usage

Economic: yes

Solvency II: no

Definitions

Economic definition based on sectors / risk profiles*

Wirtschaftliche Definitionen nach Sektoren /

Risikoprofil

• physical assets, structures, facilities, systems, networks

• provide or support

• essential public services

Solvency II definition based on the intended use**

**see Article 55a DR 2015/35 and EIOPA papers such as EIOPA-16-490

*e.g. see Trunzer (1980), “Infrastrukturinvestitionen und Wirtschaftswachstum“

7

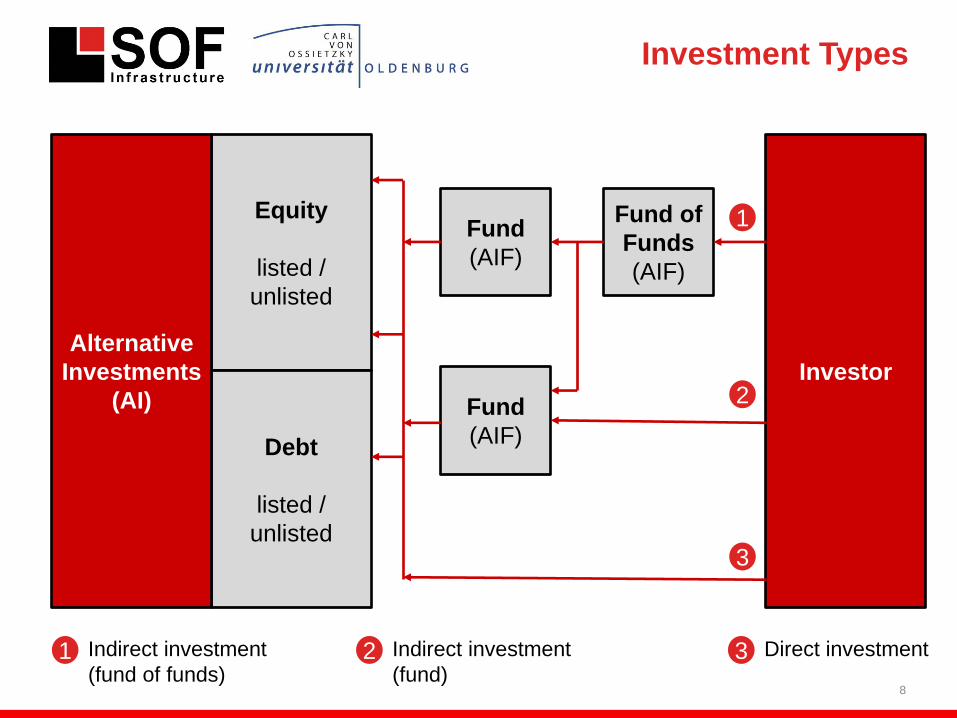

Investment Types

8

Equity

listed /

unlisted

Debt

listed /

unlisted

Alternative

Investments

(AI) Fund

(AIF)

Investor

Fund of

Funds

(AIF)

Fund

(AIF)

3

1

2

1 Indirect investment

(fund of funds)2 Indirect investment

(fund)3 Direct investment

Solvency II Requirements

9

Solvency II Requirements for Infrastructure Investments

Pillar 1 Pillar 3Pillar 2

Valuation according to

the Fair Value

Hierarchy• Market prices

• Peer group

• Valuation model

Capital requirement

(SCR)*• Equity risk

(Type 1 / Type 2 / QI / QIC)**

• Spread risk(Loan/ Securitisation / QI / QIC)**

• Interest rate risk

• FX risk

• For funds: Look-through

Prudent Person

Principle (PPP)• Security, quality, liquidity,

and profitability of the

portfolio

• Risk management

requirements for

• Non-routine investments

• Illiquid investments

*Only material SCR modules are in scope of this presentation

** QI = qualifying infrastructure investment; QIC = qualifying infrastructure corporate investment

Further process

requirements• ORSA including own risk

assessments, stress tests &

look-through

• Outsourcing

Reporting to the

supervisor (RSR +

QRT) / Disclosure

(SFCR)

• Quantitative Reporting

Templates (QRTs) for

• Infrastructure investments

• Fair Value (model)

valuation

• SCR

• For Fonds: Look-through

• Description of the risk profile

• Description of processes

including risk management

Assetklasse “Flugzeugfinanzierungen”

2

17

26

Infrastructure as a Solvency II Asset Class

Infrastructure & Risk Management

Asset: “Infrastruktur Equity”

Ökonomisches RM (quantitativ)

Agenda

10

13 Anhang29

42 Kontakt & Vorstellung

17 Ökonomisches RM (qualitativ)

10

Characteristics & Risks

11

Typical Characteristics

• Key importance for the real economy

-> collaboration with the public

sector is often required

• Usually (de facto) monopolies,

especially with regard to revenues

• Long-term regular cash flows

• Relatively high barriers to entry

• Relatively high investment volumes

Typical Risks

• Construction risk (greenfield)

• Revenue risk

• Operational risk

• Financial risk

• Sponsor risk

• Project risk & other risks

• Corporate risks

Historical Default Rates

12

Quelle: S&P. Lessons Learned From 20 Years Of Rating Global Project Finance Debt. 2014.

=> The occurance of the construction risk and the revenue risk historically

led to the most frequent defaults

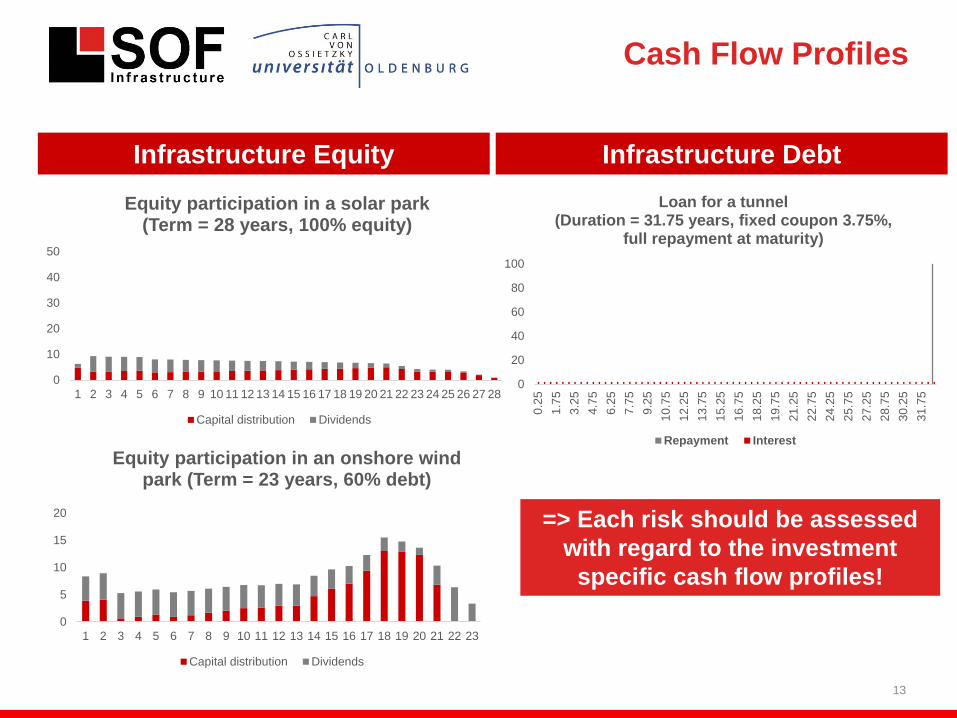

Cash Flow Profiles

13

Infrastructure Equity Infrastructure Debt

0

10

20

30

40

50

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28

Equity participation in a solar park(Term = 28 years, 100% equity)

Capital distribution Dividends

0

20

40

60

80

100

0.2

5

1.7

5

3.2

5

4.7

5

6.2

5

7.7

5

9.2

5

10.7

5

12.2

5

13.7

5

15.2

5

16.7

5

18.2

5

19.7

5

21.2

5

22.7

5

24.2

5

25.7

5

27.2

5

28.7

5

30.2

5

31.7

5

Loan for a tunnel(Duration = 31.75 years, fixed coupon 3.75%,

full repayment at maturity)

Repayment Interest

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Equity participation in an onshore wind park (Term = 23 years, 60% debt)

Capital distribution Dividends

=> Each risk should be assessed

with regard to the investment

specific cash flow profiles!

SCR – Infrastructure Equity

Assumption: Symmetric Adjustment = 2.4% (30/9/17)

QI

• Up to 37% or

19 percentage points less than

for type 2 equities

• Up to 22% or

9 percentage points less than for

type 1 equities

QIC

• Up to 25% or

13 percentage points less

than for type 2 equities

• Up to 7% or 3 percentage points

less than for type 1 equities

31%

37%40%

50%

0%

10%

20%

30%

40%

50%

60%

QI QIC Unqualifying(Type 1 AIF)

Unqualifying(Type 2 AIF)

SCR Equity Risk for Infrastructure Equity

Equity Risk

14

SCR – Infrastructure Debt

8%

13%

17%

20%

9%

15%

19%

23%

15%

24%

30%

36%

0%

5%

10%

15%

20%

25%

30%

35%

40%

5 10 15 20

SCR Spread Risk for Unrated Debt withDifferent Modified Durations

QI QIC Unqualifying

Rating (CQS) BB

(4)

Unrated BBB (3)

Loan 44% 30% 25%

QI 44% 17% 17%

QIC 44% 19% 19%

Securitisation 100% 100% 45%-

100%

Example for modified duration = 15 years

QI• Up to 44% or

16 percentage points less than

for an unrated unqualifying loan

• Up to 32% or

8 percentage points less than for

an unqualifying BBB rated loan

QIC• Up to 36% or

13 percentage points less than

for an unrated unqualifying loan

• Up to 24% or

6 percentage points less than for

an unqualifying BBB rated loan

General• Unrated QI / QIC =

BBB rated QI / QIC

Spread Risk

15

16

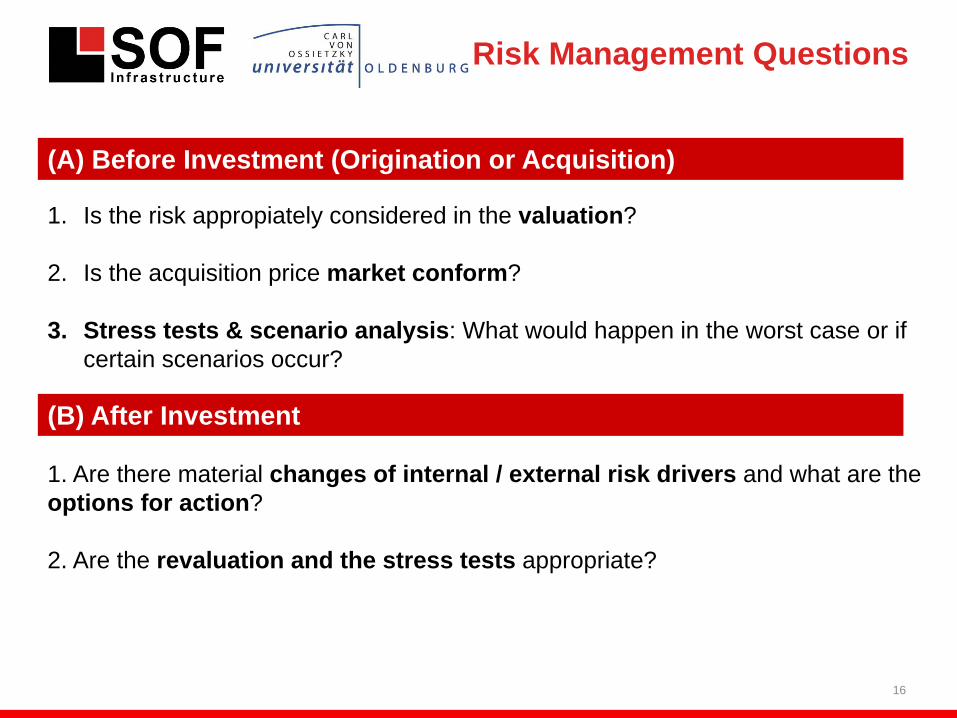

(A) Vor Investition (Gewährung oder Erwerb)

1. Is the risk appropiately considered in the valuation?

2. Is the acquisition price market conform?

3. Stress tests & scenario analysis: What would happen in the worst case or if

certain scenarios occur?

(B) Nach Investition

1. Are there material changes of internal / external risk drivers and what are the

options for action?

2. Are the revaluation and the stress tests appropriate?

Risk Management Questions

(A) Before Investment (Origination or Acquisition)

(B) After Investment

17

(A.1) Valuation Methods

Fair Value Valuation

Market Approach Income Approach Replacement Cost

• Price of recent

investment

• Multiples

• Industry Valuation

Benchmarks

• (Available Market Prices)

• DCF methods* • Net Assets

See e.g. IPEV. International Private Equity and Venture Capital Valuation Guidelines. December 2015.

*Industry Best Practice

18

(A.1) Valuation Risks

Commercial Due Diligence (DD)

• Future revenues & market forecasts

• Business model

Financial & Tax DD

• Tax & financial risks from the internal

structure and the external environment

Legal DD

• Legal risks from agreements &

regulations

Other DD (e.g. technical)

• e.g. technical condition of the assets

Financial

Model

Assumptions

Calculations

Theoretical

Value

Cash

Flows

Other

indicators

Investment

Risks

Model

Risks

Assumptions

Assumptions

Assumptions

(A.1) Valuation Risks:

Examples

NCHRP. Estimating Toll Road Demand and Revenue. 2008.

Significant deviations of

material input parameters

such as toll road revenue

forecasts possible

20

(A.1) Valuation Risks:

Mitigants

Managing Valuation Risks

Model Process

• Identification and usage of other

independent data (e.g. through

further DD)

• Definition of further assumptions

as a case may be

• Validation of the implementation

of DD assumptions in the model

• Stress tests & sensitivity analysis

• Governance &

separation of functions

• Transparent &

comprehensive process

• Effective controls

• Documented valuation

guidelines

• Validation with other

models (e.g. multiples)

• Model audit

(e.g. recalculation)

• Stress tests &

Sensitivity analysis

Inputs

See e.g. Art. 67-74 Delegated Regulation (EU) 231/2013.

21

(A.2) Market Conformity

(1) Transaction parameters (2) Market parameters

• Model value & transaction price

• Financial / operational indicators

(e.g. IRR, rating, feed-in tariff)

• Market prices (e.g. latest transaction price)

• Comparable transactions / asset prices

• Financial / operational indicators

(e.g. IRR, rating, feed-in tariff)

• Choose the method for the market-conformity assessment

• Define the benchmark / comparative market, eliminate outliers

• Determine the market-conformity interval (e.g. IRR 7%-8%)

• Ensure the comparability between (1) and (2) through adjustments (e.g. leverage), compare (1) &

(2) and assess the market conformity

“Fund transactions that are not market-conform are generally prohibited. Exceptions are admitted for

transactions that benefit the investor (e.g. transactions at beneficial prices […]). For special AIF

(„Spezial-AIF“) exceptions are admitted for transactions that are not market-conform where the transaction

is approved by all investors, is objectively reasonable and documented.“

BaFin. Zf. 4.6.10. BaFin-Rundschreiben 01/2017 (WA).10.01.2017. (inofficial translation from German)

22

(A.3) Stress tests &

scenario analysis (1)

IAA. Stress Testing and Scenario Analysis. Juli 2013.

23

(A.3) Stress tests &

scenario analysis (2)

Valuation / Base Case

(= expected risk)

• Cash Flows

• Cost of Capital

• Other parameters

Worst Case (= unexpected risk)

• Stress tests

• Reverse stress tests

• Scenario analysis

• (Back testing)

Assumptions

(1) “How much“ risk is already contained in the

base case?

-> starting point for the definition of stress cases

(2) Calibration & application

(2.1) Data

• Historical (e.g. market data)

• Forecasts (e.g. worst case in DD)

• Expert judgement

(2.2) Methods

• Point of time vs. period of time

• Qualitative vs. quantitative

• Historical vs. hypothetical

• Deterministic vs. stochastic

(3) Impact analysis

• Target variable

(Net Present Value, returns, cash flows, DSCR)

• Analysis, discussion and decisions

24

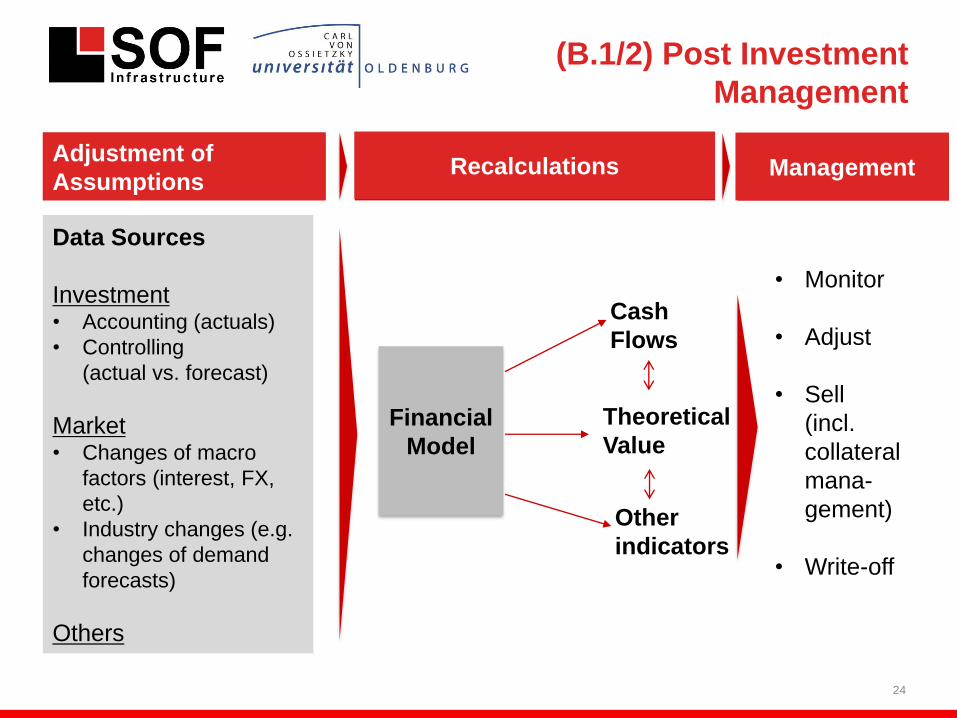

(B.1/2) Post Investment

Management

Data Sources

Investment• Accounting (actuals)

• Controlling

(actual vs. forecast)

Market• Changes of macro

factors (interest, FX,

etc.)

• Industry changes (e.g.

changes of demand

forecasts)

Others

Financial

Model

Adjustment of

Assumptions

• Monitor

• Adjust

• Sell

(incl.

collateral

mana-

gement)

• Write-off

Recalculations ManagementAdjustment of

AssumptionsRecalculations Management

Theoretical

Value

Cash

Flows

Other

indicators

25

Case Study “Eurotunnel”

Folie 25

Text and image source: Vilanova. Financial distress, lender

passivity and project finance: the case of Eurotunnel. Juni 2005.

*See also: Moody‘s. Moody's assigns Baa2 ratings to Notes to

be issued by Channel Link Enterprises Finance; stable outlook.

9.5.17.

1987 Financing via IPO (ca. 700.000 equity investors) und 220 banks (junior debt)

for ca. GBP 6 bn

1987 - 1994 Construction phase with significant budget overruns (GBP 4 bn) and time overruns

1994 Construction completed

1995 Suspension of an interest payment to junior debtholders

1995 - 1998 Financial restructuring

Until 2004 Significant deviations of the actual revenues from the budget

2007 Restructuring and debt relief

2017 Equity: 5y performance: > 80%

Senior Bonds Rating: Baa2 (CQS = 3)*

26

Indirect Investments

Alternative

Investment

Fund (AIF)

Solvency II

Balance Sheet

(Assets)

Target Investment 1

Target Investment n

…

SII-Investor• Portfolio manager

• Risk manager

AIFM*• Portfolio manager

• Risk manager

Fund shares Participations,

loans,

fund shares

Manages fund

assets (e.g. in

accordance with AIFMD)

Manages

own assets

according to Solvency II

(1) Object of the investment and risk management activities

• Fund share (no look-through):

• Assessment of the fund share as a whole

(e.g. investment guidelines before the investment, benchmarking with other funds)

• Assessment of the AIFM (Manager Due Diligence)

• Target investments (look-through):

• Separate assessment of each individual target investment; sometimes veto / approval rights

(2) Division of responsibilities between the SII Investor and the AIFM

• Acceptance of the AIFM data without controls vs. additional own assessments

• Outsourcing requirements vs. double work

*AIFM = Alternative Investment Fund Manager

27

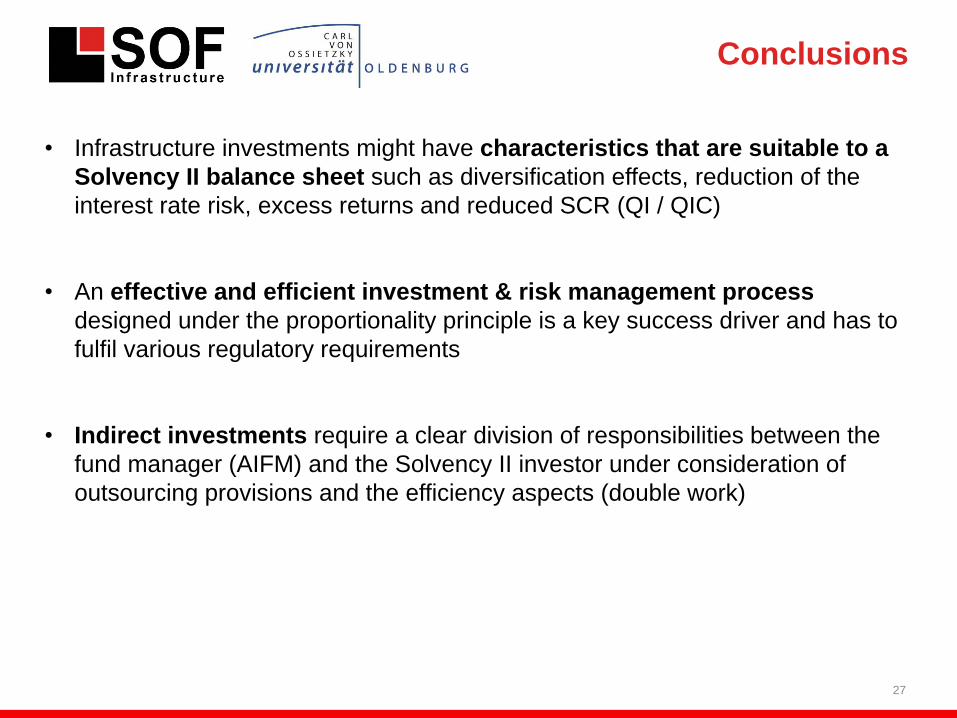

Conclusions

• Infrastructure investments might have characteristics that are suitable to a

Solvency II balance sheet such as diversification effects, reduction of the

interest rate risk, excess returns and reduced SCR (QI / QIC)

• An effective and efficient investment & risk management process

designed under the proportionality principle is a key success driver and has to

fulfil various regulatory requirements

• Indirect investments require a clear division of responsibilities between the

fund manager (AIFM) and the Solvency II investor under consideration of

outsourcing provisions and the efficiency aspects (double work)

Contact

Get in touch!

28

Jegor Tokarevich

Partner (SOF / SOFI)

DE: + 49 (0) 174 497 857 3

UK: + 44 (0) 748 208 226 1

www.sof-ltd.com

Disclaimer

The information contained in this presentation is confidential and must not be disclosed to any other party. The Recipient should conduct its own independent

investigation and assessment as to the validity of the information contained in this presentation, and the economic, financial, regulatory, legal, taxation, stamp duty

and accounting implications of that information. The Recipient confirms that it is not relying on any recommendation or statement of SOF Infrastructure Ltd.. Except

as required by law, SOF Infrastructure Ltd. and its respective directors, officers, employees, agents and consultants make no representation or warranty as to the

accuracy or completeness of the information contained in this presentation, and take no responsibility under any circumstances for any loss or damage suffered as a

result of any omission, inadequacy, or inaccuracy in this presentation. This presentation may contain certain forward-looking statements, forecasts, estimates,

projections and opinions ("Forward Statements"). No representation is made or will be made that any Forward Statements will be achieved or will prove to be correct.

Actual future results and operations could vary materially from the Forward Statements. Similarly no representation is given that the assumptions disclosed in this

presentation upon which Forward Statements may be based are reasonable. The Recipient acknowledges that circumstances may change and the contents of this

presentation may become outdated as a result. The Recipient acknowledges that neither it nor SOF Infrastructure Ltd. intends that SOF Infrastructure Ltd. act or be

responsible as a fiduciary to the Recipient, its management, stockholders, creditors or any other person. Source: SOF Infrastructure Ltd.

SOF Infrastructure Ltd (SOFI) is an appointed representative of Aldgate Advisors Ltd which is authorised and regulated by the Financial Conduct Authority. SOFI may

provide certain regulated investment services concerning infrastructure investments and is registered with the FCA. Further information is provided on the website of

FCA: https://register.fca.org.uk/.

![Infrastruktur TI [Compatibility Mode]](https://img.pdfslide.us/doc/110x75/546a9f97b4af9fe5268b4898/infrastruktur-ti-compatibility-mode.jpg)