Embed Size (px)

Citation preview

Solutions to Improve Cash FlowWhat Business Owners Need to Know

Kimberly Bonzelaar Kimberly Bonzelaar Senior Vice President, Merchant ServicesSenior Vice President, Merchant Services

Nicole Epp, CTPNicole Epp, CTPSenior Vice President, Treasury Senior Vice President, Treasury

ManagementManagement

Hampton Roads Association for Finance Hampton Roads Association for Finance ProfessionalsProfessionals

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 2

• Are you taking advantage of the latest treasury management technology to save time and money?

• Are you at risk of losing money due to fraud?

Two Critical Questions to AnswerTwo Critical Questions to Answer

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 3

How Business Owners View LiquidityHow Business Owners View Liquidity

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 4

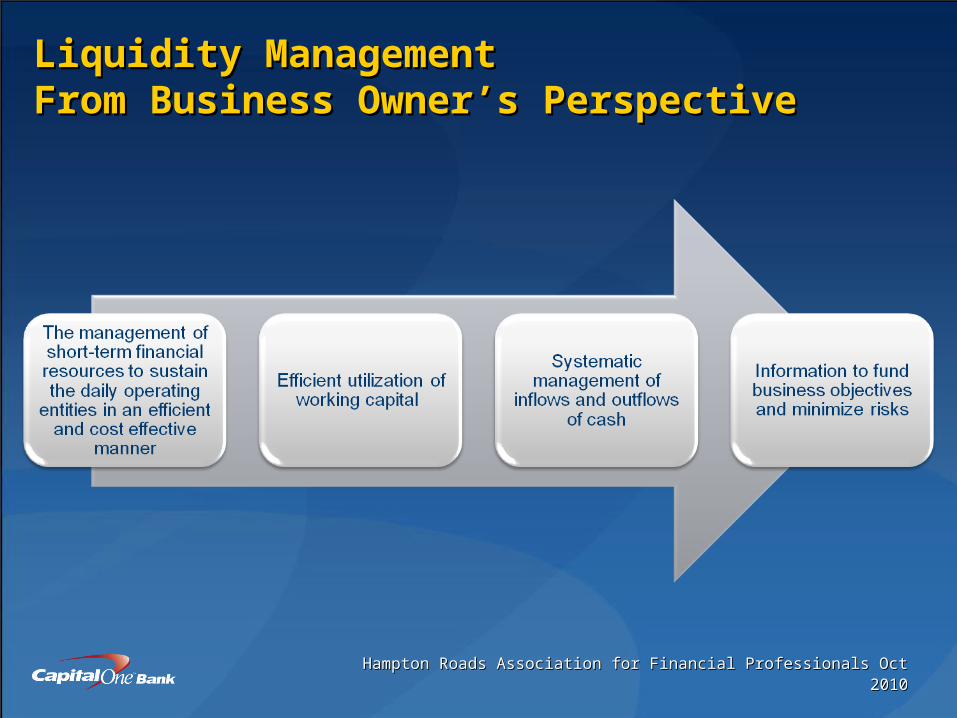

Liquidity Management Liquidity Management From Business Owner’s PerspectiveFrom Business Owner’s Perspective

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 5

Goal for Liquidity ManagementGoal for Liquidity Management

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 6

Operating CycleOperating Cycle

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 7

Payment ChannelsPayment Channels

Check

Cash

ACH

Bill Pay

Lockbox

Merchant Processing

Remote Deposit

Vault

Electronic Bill Payment

& Presentment

Remittance Processing

Card

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 8

Improve Payment Efficiencies and Improve Payment Efficiencies and Control Cash FlowControl Cash Flow

Cash Flow Timeline

• Control cash flow

• Gain efficiencies/capture data

• Prevent costly fraud

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 9

Cash Flow Gain Efficiencies Capture Data

Emerging Trends: Emerging Trends: Commercial Card AdaptationCommercial Card Adaptation

• Maximize float through grace periods

• Negotiate discounts with suppliers

• Capture rebates/ rewards

• Streamline A/P

• Eliminate paper related to paper purchase orders, invoices and checks, checks

• Online management

• A $7.5 Billion manufacturing company realized $300,000 in process savings by moving non Purchasing Order transactions under $1,500.00 to a Commercial Card program *

• Data feeds into accounting systems

• Reporting for tax

documents (1099) and

socioeconomic data for

vendors

• Improve controls around

spend categories and

amounts

* Source: 2008 Visa Global Procure to Pay and Commercial Card Best Practices Executive Summary

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 10

Here’s ProofHere’s Proof

Spend Categories for Purchasing Programs

21%

23%

24%

30%

41%

49%

56%

61%

61%

70%

73%

89%

55%

Utilities

Temporary Labor

Capital Purchases

Fleet Management

Transportation & Logistics

Hotels/Lodging/Rental Car

Telecommunications

Airline & Rail

Maintenance Services

MRO Supplies

Computers / Peripherals / Software

Advertising & Printing Services

Office Equipment

Aberdeen Research 2008

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 11

Cash Flow Management Innovative Cash Flow Management Innovative ThinkingThinking

Commercial Card30 Day Billing Cycle

25 Day Grace Period

CYCLE TIME GRACE PERIOD

Cycle Begins

Cycle Ends Grace Period EndsGrace Period Begins

Pay Vendor here on Discount date or day

60

Pay Commercial

Card balance at

end of grace

period for up to 55

days extra cash float!

2/10, net 60 - can deduct 2% of the net amount owed if invoice is paid within 10 days of invoice date. If not paid within the discount period of 10 days, the net purchase amount (without the discount) is due 60 days after the invoice date.

• Pay a vendor under their negotiated discount terms OR

• Forego the discount to delay payment and conserve cash (if invoice paid at day 60, beginning of billing cycle, full-payment period interest free up to 115 days)

$15,0002/10 net 60

INVOICE

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 12

With payment terms of 2/10 net 30, the effective cost of paying on day 30 instead of on day 10 is:

i = .02 x 365 .98 30 -10 = 37.24%

Source: NCCMA Essentials of Cash Management, 1986

Payment Terms

• 2/10 net 30

• 1/10 net 30

• 2/10 net 45

• 1/10 net 45

Effective Cost

• 37.24%

• 18.43%

• 21.28%

• 10.53%

ExampleExample

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 13

Best Practices to Improve Cash FlowBest Practices to Improve Cash Flow

• Do you regularly review your cash flow strategy with your bank?

• Are you taking advantage of emerging electronic payment channels:– Commercial Card Programs

– Electronic Bill Presentment and Payment (EBPP)

– Remote deposit with payment card processing

– Remote safe service

– Online shopping cart payments

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 14

Are you at risk of losing money due to Are you at risk of losing money due to fraud?fraud?

• Reprogramming scams - criminal may pose as employee of merchant company then reroute transactions to their own bank account

• Hacking wireless - fraudsters hack into wireless terminals. To prevent, use equipment that meets security standards for storing, processing, and transmitting card holder data

• Rigged upon delivery - recent fraud ring programmed terminals before deploying in U.S. for final shipment to merchant

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 15

External Fraud: Defending the External Fraud: Defending the BusinessBusiness

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 16

PCI DSS CompliancePCI DSS Compliance

• Payment Card Industry Data Security Standard

• Compliance with PCI DSS helps companies minimize the risk of a data security breach

• Visa® estimates that 85% of breaches occur at small businesses

Source: http://www.bbb.org/data-security/intro-to-small-businesses/

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 17

Why Comply with PCI DSS?Why Comply with PCI DSS?

• A breach can negatively impact a merchant’s brand image and customer loyalty

• Card associations mandate compliance:– Fine: $10,000 to $550,000– Increased transaction-processing fees– Suspension of credit card processing abilities

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 18

How To Become PCI CompliantHow To Become PCI Compliant

• Build and maintain a secure network

• Protect cardholder data

• Maintain a vulnerability management program

• Implement strong access control measures

• Regularly monitor and test networks

• Maintain an information security policy

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 19

What is Required for PCI Compliance?What is Required for PCI Compliance?

Visa® and MasterCard® requires that all merchants do the following:

– PCI DSS Self Assessment Questionnaire (SAQ). An approved list of questions from the card associations about the security controls on a merchant’s transaction network

– Network Vulnerability Scan. A remote scan of a merchant’s transaction network to detect weaknesses that could be exploited by hackers or unauthorized third-parties

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 20

Improve Cash Flow

Gain Efficiencies/Capture Data

Fraud Prevention

Best PracticesBest Practices

• Leverage commercial card programs

• Improve disbursement float by understanding grace periods

• Negotiate better vendor discounts through merchant synergies

• Improve receivables collection through electronic payment acceptance

• Leverage online reporting tools to eliminate paper-intensive processes

• Increase controls by limiting spend categories and amounts

• Automate reconciliation

• Protect against data security breaches that can be costly

• Online reporting tools

help prevent against

internal and external

fraud

Hampton Roads Association for Financial Professionals Oct 2010Hampton Roads Association for Financial Professionals Oct 2010

Slide 21

Questions

Kimberly BonzelaarKimberly BonzelaarSenior Vice President

Capital One Bank | Merchant Services936-524-7485

Nicole Epp, CTPNicole Epp, CTPSenior Senior Vice President

Capital One Bank | Treasury Management

240-497-7880

This presentation is for informational purposes only, does not constitute the rendering of legal, accounting or other professional services by Capital One, N. A. or any of its subsidiaries or affiliates, and is without any

warranty whatsoever.© 2010 Capital One. Member FDIC. All rights reserved.