Embed Size (px)

Citation preview

TRANSITIONING TO A CONSUMER-LED ECONOMY

Louise Keely Hong Kong September 10, 2015

SOLD IN CHINA

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

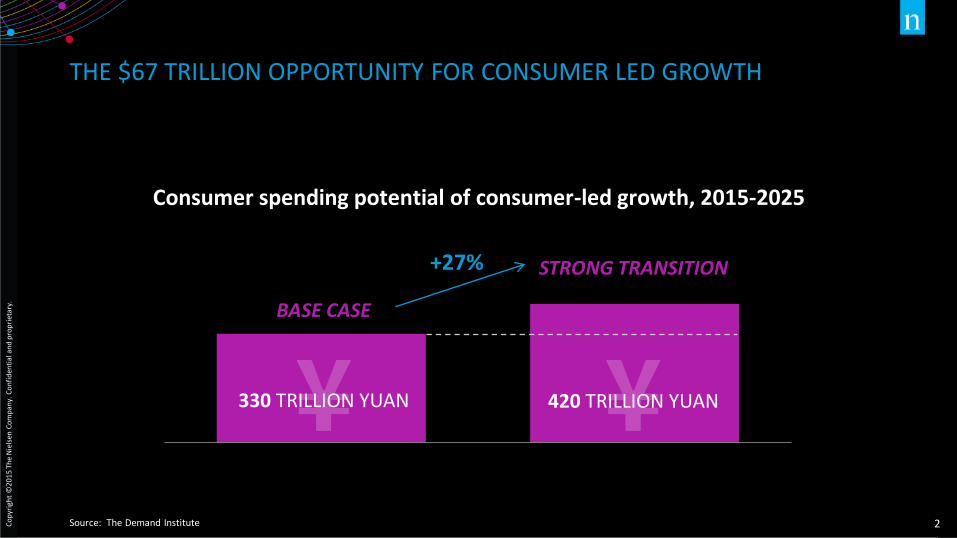

THE $67 TRILLION OPPORTUNITY FOR CONSUMER LED GROWTH

Source: The Demand Institute

Consumer spending potential of consumer-led growth, 2015-2025

BASE CASE

STRONG TRANSITION

420 TRILLION YUAN 330 TRILLION YUAN

+27%

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

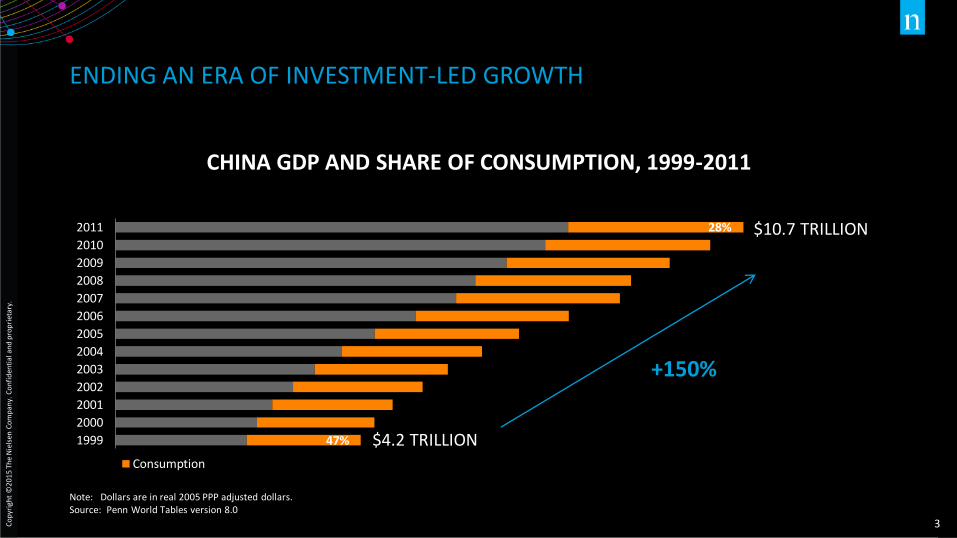

ENDING AN ERA OF INVESTMENT-LED GROWTH

CHINA GDP AND SHARE OF CONSUMPTION, 1999-2011

Note: Dollars are in real 2005 PPP adjusted dollars. Source: Penn World Tables version 8.0

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Consumption

$10.7 TRILLION 28%

47% $4.2 TRILLION

+150%

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

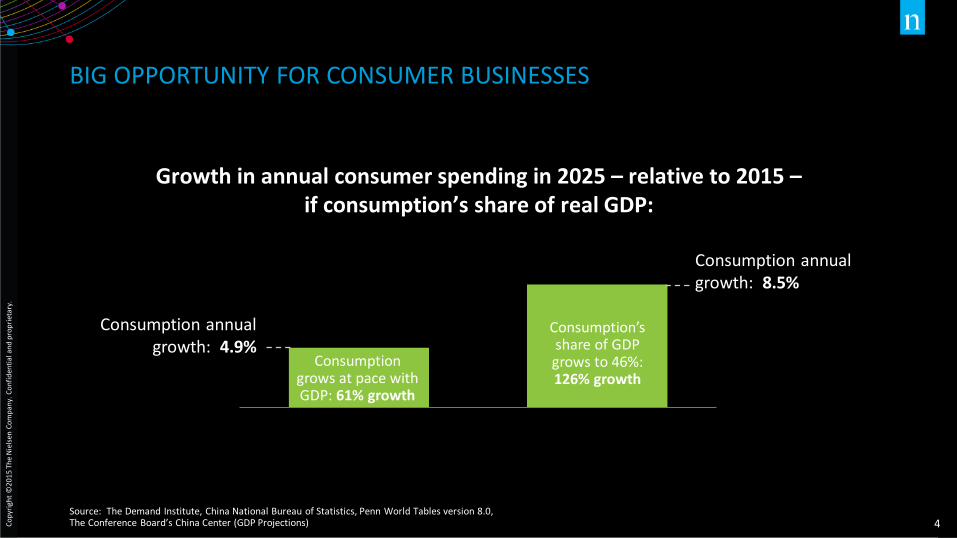

BIG OPPORTUNITY FOR CONSUMER BUSINESSES

Source: The Demand Institute, China National Bureau of Statistics, Penn World Tables version 8.0, The Conference Board’s China Center (GDP Projections)

Growth in annual consumer spending in 2025 – relative to 2015 – if consumption’s share of real GDP:

Consumption annual growth: 8.5%

Consumption annual growth: 4.9%

Consumption grows at pace with GDP: 61% growth

Consumption’s share of GDP grows to 46%: 126% growth

WHAT CAN BUSINESS LEADERS DO?

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

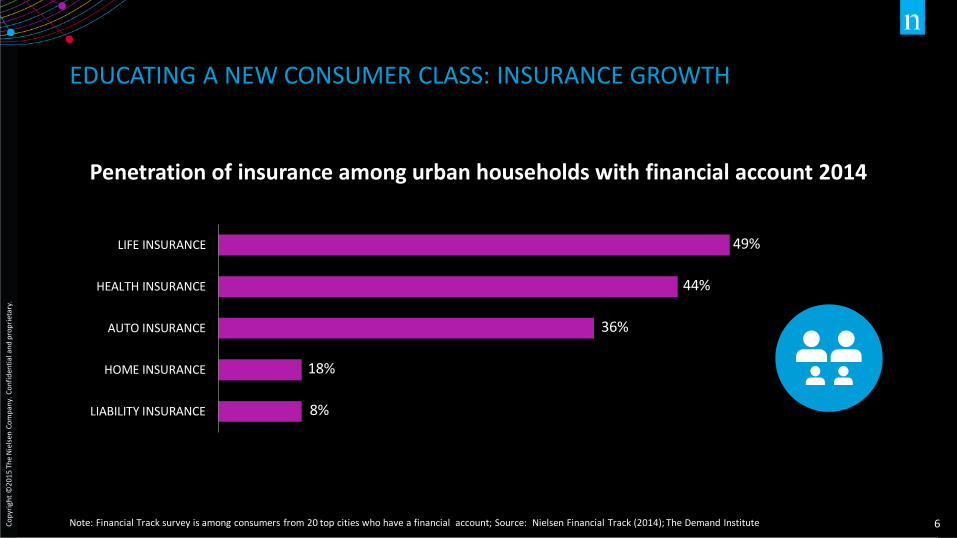

EDUCATING A NEW CONSUMER CLASS: INSURANCE GROWTH

Note: Financial Track survey is among consumers from 20 top cities who have a financial account; Source: Nielsen Financial Track (2014); The Demand Institute

Penetration of insurance among urban households with financial account 2014

LIABILITY INSURANCE

HOME INSURANCE

AUTO INSURANCE

HEALTH INSURANCE

LIFE INSURANCE 49%

44%

36%

18%

8%

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

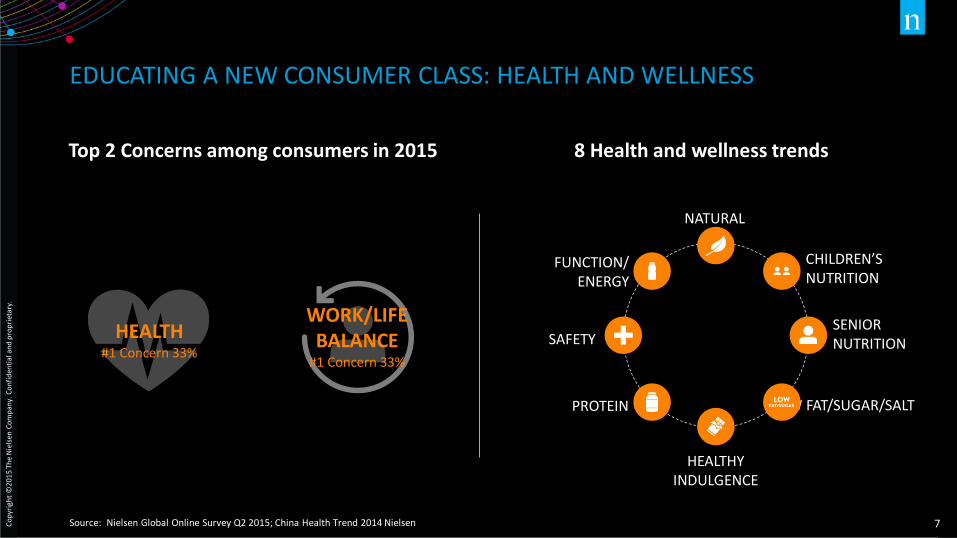

EDUCATING A NEW CONSUMER CLASS: HEALTH AND WELLNESS

Source: Nielsen Global Online Survey Q2 2015; China Health Trend 2014 Nielsen

FUNCTION/ ENERGY

8 Health and wellness trends

PROTEIN LOW FAT/SUGAR/SALT

SENIOR NUTRITION

CHILDREN’S NUTRITION

HEALTHY INDULGENCE

NATURAL

SAFETY

Top 2 Concerns among consumers in 2015

HEALTH #1 Concern 33%

WORK/LIFE BALANCE

#1 Concern 33%

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

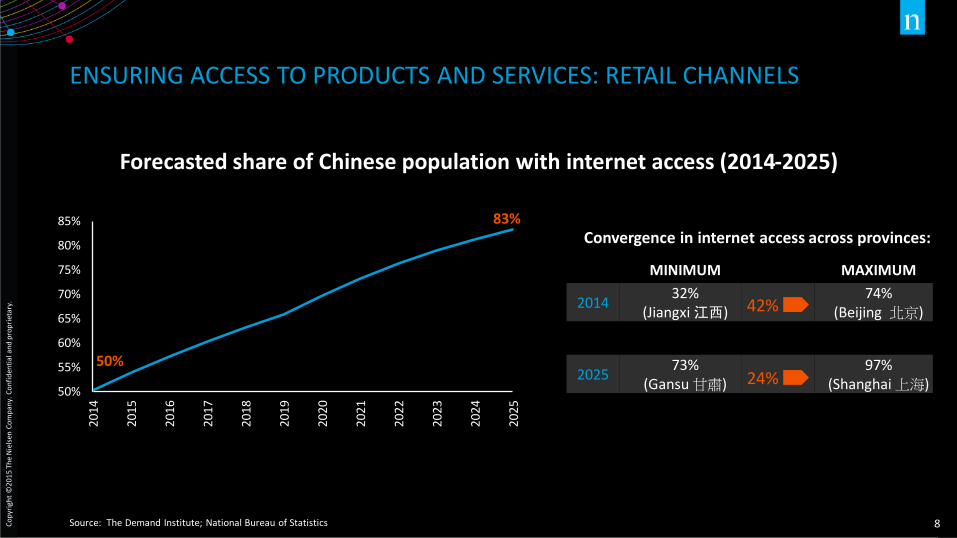

ENSURING ACCESS TO PRODUCTS AND SERVICES: RETAIL CHANNELS

Source: The Demand Institute; National Bureau of Statistics

Forecasted share of Chinese population with internet access (2014-2025)

50%

55%

60%

65%

70%

75%

80%

85%

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Convergence in internet access across provinces:

MINIMUM MAXIMUM

2014 32%

(Jiangxi 江西) 74%

(Beijing 北京)

2025 73%

(Gansu 甘肅) 97%

(Shanghai 上海)

42%

24% 50%

83%

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

ENSURING ACCESS: LOGISTICS TO NEW REGIONS

Note: Data are for 2013 except as noted; Source: CEIC; The Demand Institute

XINYANG |信陽 Henan province |河南省

Population: 8.6M

GUANGZHOU |廣州 Guandong province |廣東省

Population: 12.9M

WUHAN |武漢 Hubei province |湖北省 Population:10.2M

ZANGZHOU |漳州 Fukian province |福建省 Population: 4.9M

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

PRODUCTS TO SERVE VARIED DEMAND: CATEGORY OPTIONS

Source: The Demand Institute

PERSONAL TRANSPORT

SMARTPHONES SPORTSWEAR

Audi 添加奥迪、Geoby 徽标 Apple 添加、Xiaomi 小米徽标 Nike 添加耐克、Alta 徽标

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

PRODUCTS TO SERVE VARIED DEMAND: TRADE UP ACROSS REGIONS

Source: The Demand Institute

Relative growth across cities of consumer products through 2025

MORE AFFLUENT CITIES “ADVANCED” TRADE UP

LESS AFFLUENT CITIES “BASIC” TRADE UP

PERSONAL CARE

MILK PRODUCTS

CONFECTIONS

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

CONNECTED SPENDERS AS LEADING EDGE CONSUMERS

Focus on “middle class” consumers based on middle income not as relevant for luxury, financial

services sectors in China, and an income-based definition does not indicate willingness to spend

Connected Spender framework addresses, via willingness to spend spare cash once basic

essentials are covered, and by access to the internet.

We identify who they are, where they are found, how many there are today and project how many there will be in the future, and how they spend their money today and are likely to do so in the future.

Within this group, luxury and financial services sectors can identify their highest potential

Connected Spenders, based on metrics such as income and wealth

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

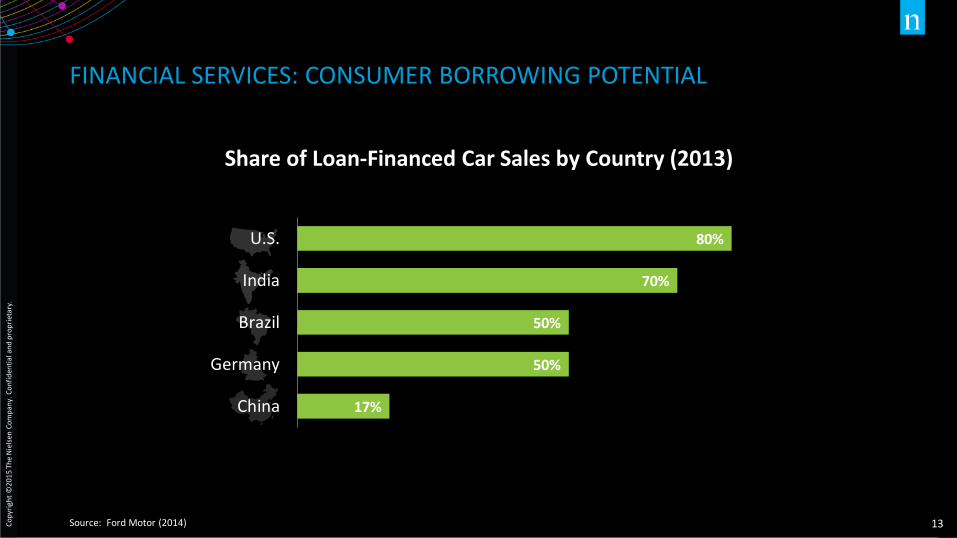

FINANCIAL SERVICES: CONSUMER BORROWING POTENTIAL

Source: Ford Motor (2014)

17%

50%

50%

70%

80%

China

Germany

Brazil

India

U.S.

Share of Loan-Financed Car Sales by Country (2013)

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

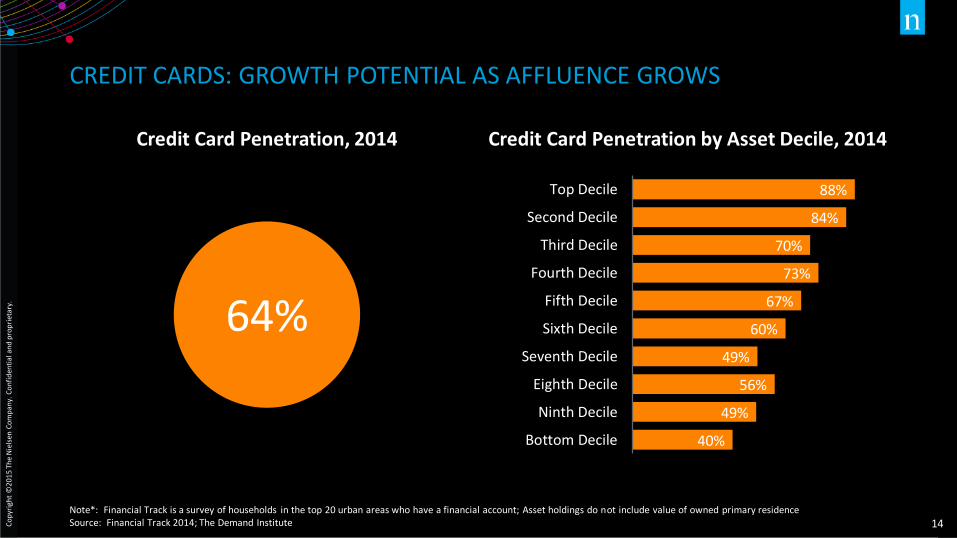

CREDIT CARDS: GROWTH POTENTIAL AS AFFLUENCE GROWS

88%

84%

70%

73%

67%

60%

49%

56%

49%

40%

Top Decile

Second Decile

Third Decile

Fourth Decile

Fifth Decile

Sixth Decile

Seventh Decile

Eighth Decile

Ninth Decile

Bottom Decile

Note*: Financial Track is a survey of households in the top 20 urban areas who have a financial account; Asset holdings do not include value of owned primary residence Source: Financial Track 2014; The Demand Institute

Credit Card Penetration by Asset Decile, 2014

64%

Credit Card Penetration, 2014

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

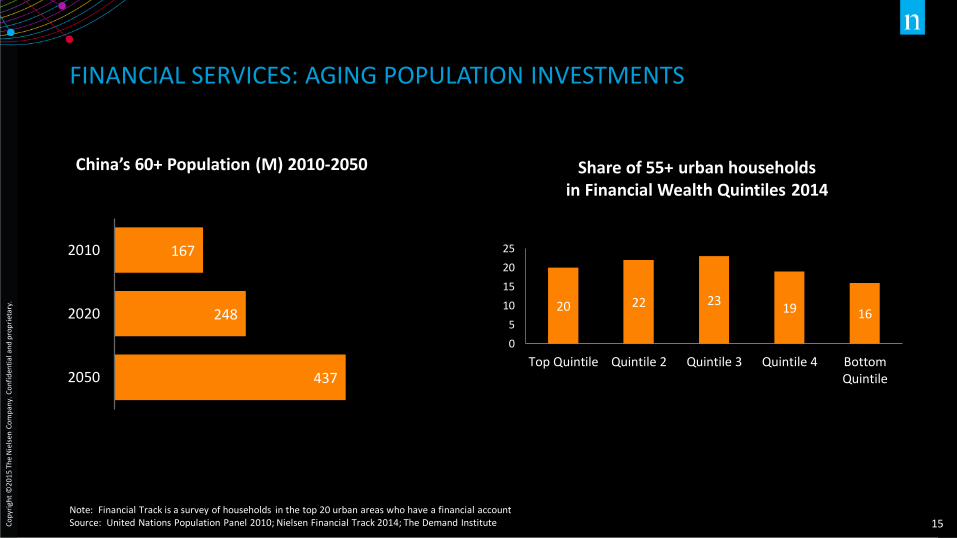

FINANCIAL SERVICES: AGING POPULATION INVESTMENTS

Note: Financial Track is a survey of households in the top 20 urban areas who have a financial account Source: United Nations Population Panel 2010; Nielsen Financial Track 2014; The Demand Institute

China’s 60+ Population (M) 2010-2050

167

248

437

2010

2020

2050

Share of 55+ urban households in Financial Wealth Quintiles 2014

20 22 23 19 16

0

5

10

15

20

25

Top Quintile Quintile 2 Quintile 3 Quintile 4 BottomQuintile

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

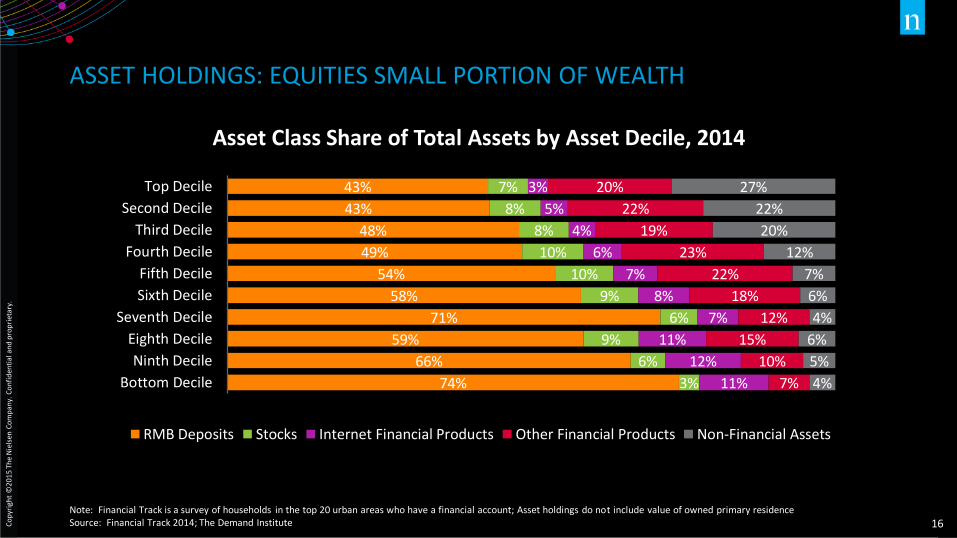

ASSET HOLDINGS: EQUITIES SMALL PORTION OF WEALTH

43%

43%

48%

49%

54%

58%

71%

59%

66%

74%

7%

8%

8%

10%

10%

9%

6%

9%

6%

3%

3%

5%

4%

6%

7%

8%

7%

11%

12%

11%

20%

22%

19%

23%

22%

18%

12%

15%

10%

7%

27%

22%

20%

12%

7%

6%

4%

6%

5%

4%

Top Decile

Second Decile

Third Decile

Fourth Decile

Fifth Decile

Sixth Decile

Seventh Decile

Eighth Decile

Ninth Decile

Bottom Decile

RMB Deposits Stocks Internet Financial Products Other Financial Products Non-Financial Assets

Note: Financial Track is a survey of households in the top 20 urban areas who have a financial account; Asset holdings do not include value of owned primary residence Source: Financial Track 2014; The Demand Institute

Asset Class Share of Total Assets by Asset Decile, 2014

Co

pyr

igh

t ©

20

15

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

CALL TO ACTION FOR BUSINESS

Cultivating a consumer culture

Activating consumer access to goods and services

Products and services to serve varied demand

Financial services offering to support consumer spending

To capture a 420 trillion yuan opportunity

FINANCIAL SERVICES OPPORTUNITIES?

LUXURY MARKET OPPORTUNITIES?