Embed Size (px)

Citation preview

42 renewable energy focus May/June 2010

Feature article

The solar photovoltaic (PV) industry suff ered a major blow last year when the

Spanish market collapsed, but despite this loss the market performed much

better than expected. Shipments to the fi rst point of sale, including installers,

system integrators, distributors and other technology manufacturers, grew by

44% to 7.9 GW. This was a signifi cant rise from 5.5 GW in 2008.

The year began with practically non-existent sales from manufacturers

as the industry worked off more than 1.2 GW of demand-side inventory.

By the middle of the second quarter, however, the inventory had

been completed and demand in Germany, France, Italy and the Czech

Republic took off .

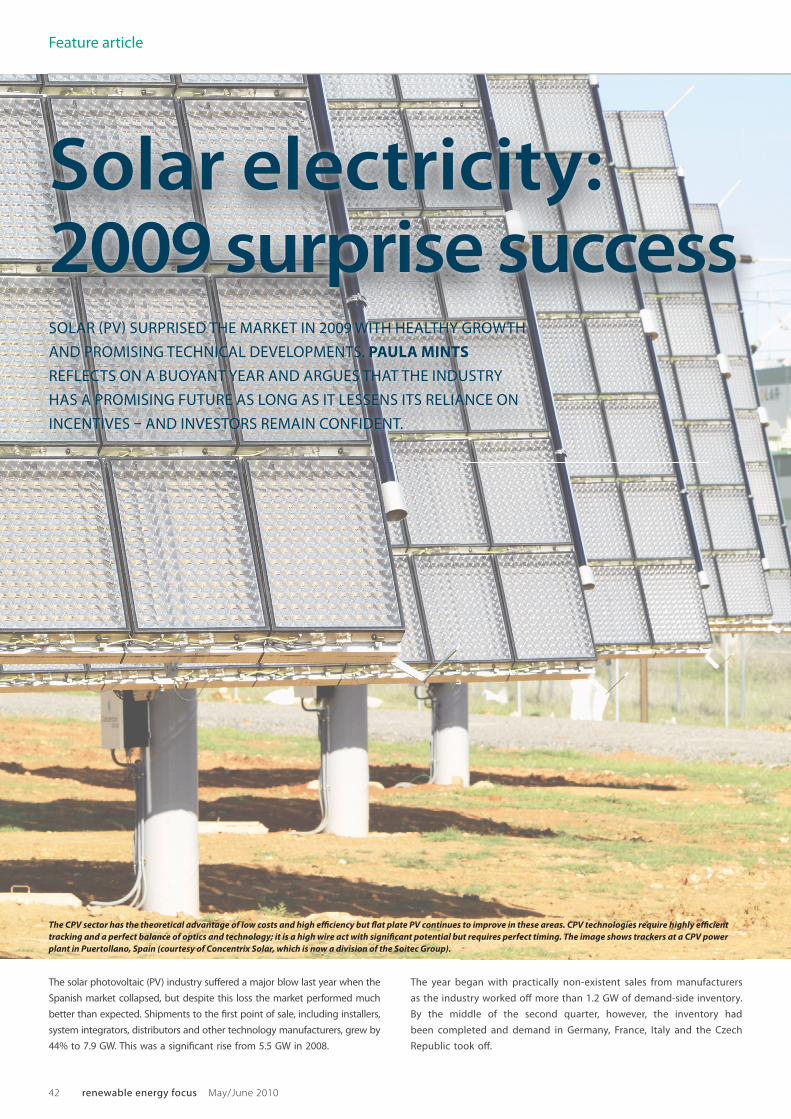

The CPV sector has the theoretical advantage of low costs and high effi ciency but fl at plate PV continues to improve in these areas. CPV technologies require highly effi cient

tracking and a perfect balance of optics and technology; it is a high wire act with signifi cant potential but requires perfect timing. The image shows trackers at a CPV power

plant in Puertollano, Spain (courtesy of Concentrix Solar, which is now a division of the Soitec Group).

Solar electricity: 2009 surprise successSOLAR PV SURPRISED THE MARKET IN 2009 WITH HEALTHY GROWTH

AND PROMISING TECHNICAL DEVELOPMENTS. PAULA MINTS

REFLECTS ON A BUOYANT YEAR AND ARGUES THAT THE INDUSTRY

HAS A PROMISING FUTURE AS LONG AS IT LESSENS ITS RELIANCE ON

INCENTIVES AND INVESTORS REMAIN CONFIDENT.

renewable energy focus May/June 2010 43

Solar electricity/market

25000

20000

15000

10000

5000

02008 2009 2009 2009 2009 2009 200920202020202020 22222200000000009090909 2202020202009999090909 99999992020202009090909090909 0909090909090920202020202020

02000202020202020000000008080808080808 22022020202020200000000222222222 202020202020200009090900909090909092008 2009 2009 2009 2009 2009 2009 2009

Dem

and side

inventory into 2009Shipm

ents

Production

Announced productionInstallations

(ind 2008 inventory)Com

mercial capacity

Announced capacity D

emand side

inventory (or, extra

product) into 2009

MWp

Figure 1: 2009 PV Industry Metrics.

8000

6000

5000

4000

3000

2000

1000

0

7000

2004 2005 2006 2007 2008 2009

MWp

Figure 2: PV Industry Growth, 2004 – 2009.

Shipments do not equate exactly to installations but last year’s

installation fi gures are impressive: Germany totalled around 3.8 GW, Italy

around 1 GW and the Czech Republic close to 500 MW. When Japan’s

new feed-In tariff (FiT) began in November, demand in that country

grew close to 500 MWp. As a result, the 2009 market for PV technologies

came as an overall relief to the global PV industry.

Looking back at 2009, there are many diff erent numbers to analyse and

just as many categories to put them in. Figure 1 shows these categories,

including inventory, shipments, production, capacity and installation for

the year.

PV industry growth over the past fi ve years has been impressive by any

standard, with two caveats; the industry remains entirely incentive driven

for grid connected application and grid connected application represents

95% of industry demand. Until the industry can function without incen-

tives and subsidies it will always be a risky market to invest in or to enter

as a manufacturer or installer. (Of course, all energy technologies are

subsidised, including conventional energy).

Figure 2 shows PV industry growth from 2004 through 2009. During this

period the industry grew by a compound annual rate of 50%.

Shipments grew by an impressive 44% compared to 2008, which was

particularly surprising in a year when they had been forecasted to

decrease. Unsurprisingly, given the low prices from manufacturers

in the region, 47% of 2009 shipments came from China and Taiwan.

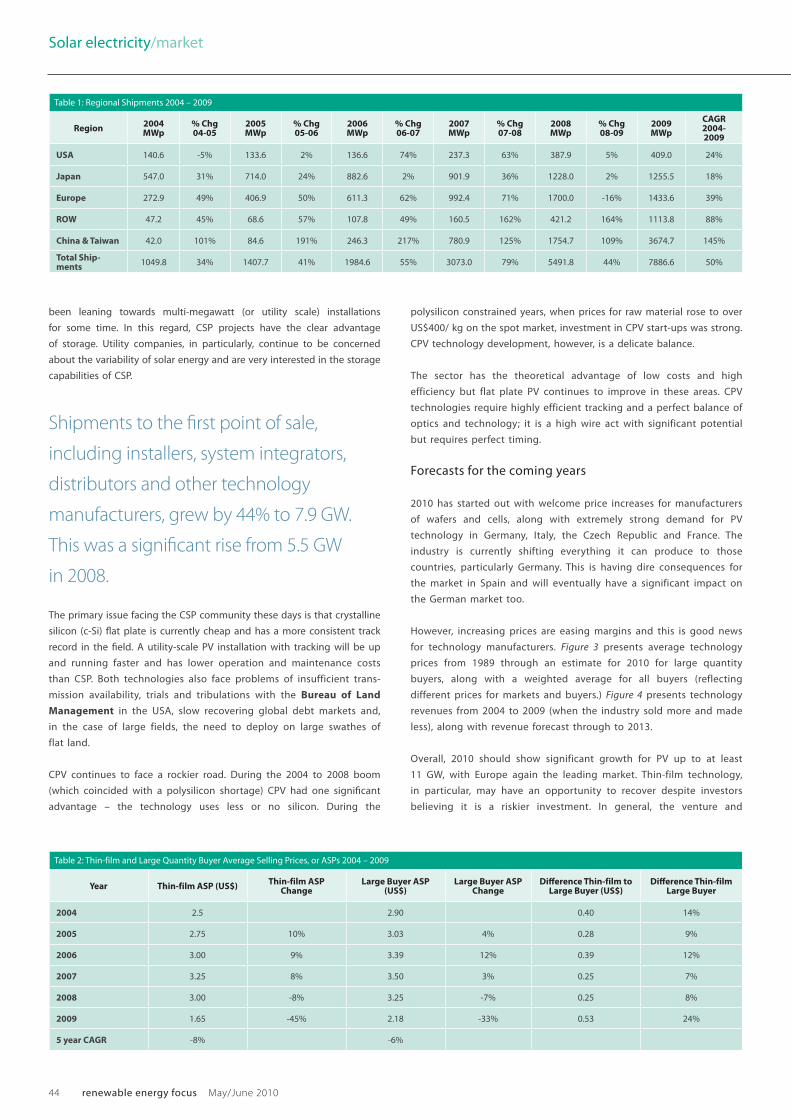

Table 1 presents shipment information from 2004 to 2009.

During this period, shipments from China and Taiwan grew at a compound

annual rate of 145%. The ROW region includes manufacturers from India,

Malaysia and the Philippines.

Last year, strong demand coincided with aggressive pricing from

manufacturers in China and Taiwan. In mid-2009 it was cheaper in many

cases to outsource cells and modules from China or Taiwan than it was to

manufacture them in-house. Outsourcing and tolling (for manufacturers

with wafer capacity) became commonplace, while prices dropped

signifi cantly. It was a good time for companies buying technology but

not so good for technology manufacturers. Thin-fi lm faced a particularly

diffi cult competitive position with low-priced crystalline driving margins

to uncomfortable levels.

Average selling prices – 2009 from 2008

■ Thin-fi lm fell 45% from US$3.00/Wp to US$1.65/Wp;

■ Cell fell 60% from US$3.20/Wp to US$1.26/Wp;

■ Module for large quantity buyers (typically 50 MWp to over 100 MWp

a year) fell 33% from US$3.25/Wp to US$2.18/Wp;

■ Module for mid-level buyers (typically 10 MWp to over 25 MWp per

year) fell 23% from US$3.65/Wp to US$2.82/Wp;

■ Module for small quantity buyers fell 27% from US$5.02/Wp to

US$3.68/Wp.

Table 2 presents average selling prices (ASPs) over time for thin-fi lm tech-

nologies and large quantity buyers of all technologies. The large quantity

buyer category is representative of crystalline technologies. PV technolo-

gies with lower conversion effi ciency have an area penalty (this includes

higher balance of system and installation costs) that requires a lower

price/Wp. Typically this price must be lower than the lowest available

price for crystalline technology.

CSP versus CPV

2009 began as a year of dire predictions and low expectations, and ended

with strong demand, bargain basement prices and stressed margins for

the PV industry. So what did it mean for concentrated solar power (CSP)

and concentrated photovoltaics (CPV)?

Size is crucial in the case of CSP. Installation needs to be in the megawatt

range to make economic sense, while fl at plate PV can be installed on

roofs and in smaller kilowatt confi gurations. The solar world has, however,

An industry that relies on incentives...and

suff ers criticism for this reliance, is always

risky to enter or invest in.

44 renewable energy focus May/June 2010

Solar electricity/market

been leaning towards multi-megawatt (or utility scale) installations

for some time. In this regard, CSP projects have the clear advantage

of storage. Utility companies, in particularly, continue to be concerned

about the variability of solar energy and are very interested in the storage

capabilities of CSP.

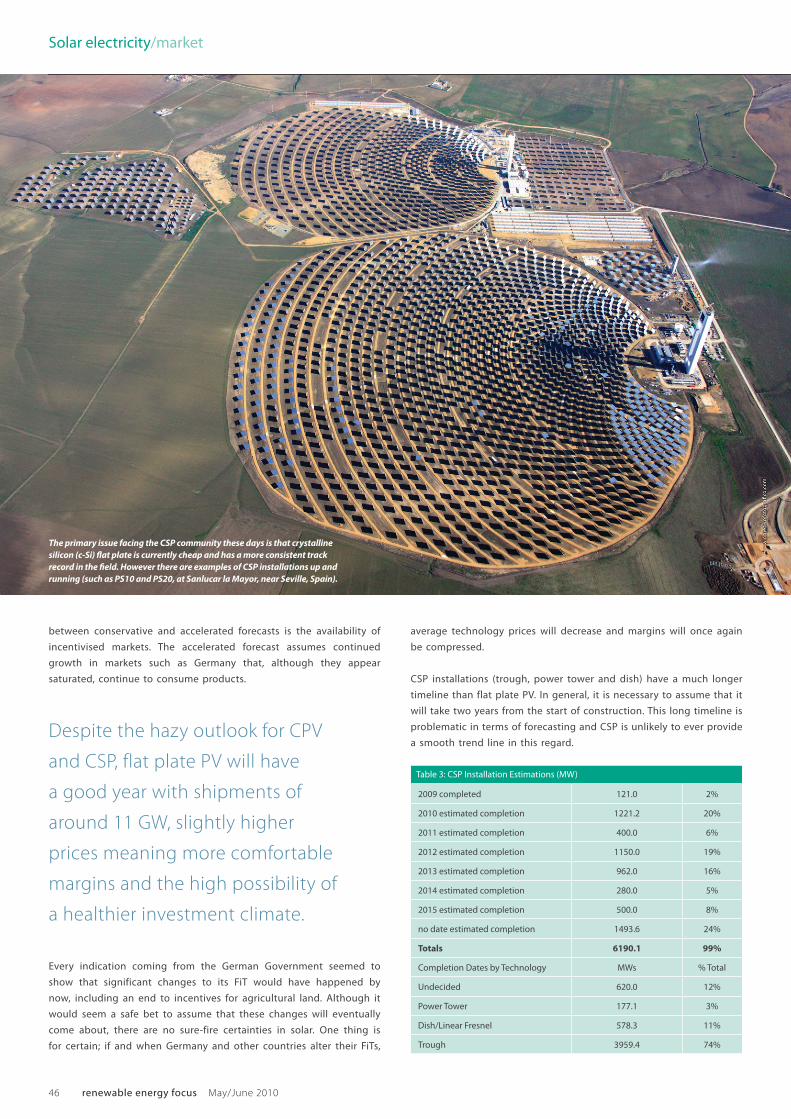

The primary issue facing the CSP community these days is that crystalline

silicon (c-Si) flat plate is currently cheap and has a more consistent track

record in the field. A utility-scale PV installation with tracking will be up

and running faster and has lower operation and maintenance costs

than CSP. Both technologies also face problems of insufficient trans-

mission availability, trials and tribulations with the Bureau of Land

Management in the USA, slow recovering global debt markets and,

in the case of large fields, the need to deploy on large swathes of

flat land.

CPV continues to face a rockier road. During the 2004 to 2008 boom

(which coincided with a polysilicon shortage) CPV had one significant

advantage – the technology uses less or no silicon. During the

polysilicon constrained years, when prices for raw material rose to over

US$400/ kg on the spot market, investment in CPV start-ups was strong.

CPV technology development, however, is a delicate balance.

The sector has the theoretical advantage of low costs and high

efficiency but flat plate PV continues to improve in these areas. CPV

technologies require highly efficient tracking and a perfect balance of

optics and technology; it is a high wire act with significant potential

but requires perfect timing.

Forecasts for the coming years

2010 has started out with welcome price increases for manufacturers

of wafers and cells, along with extremely strong demand for PV

technology in Germany, Italy, the Czech Republic and France. The

industry is currently shifting everything it can produce to those

countries, particularly Germany. This is having dire consequences for

the market in Spain and will eventually have a significant impact on

the German market too.

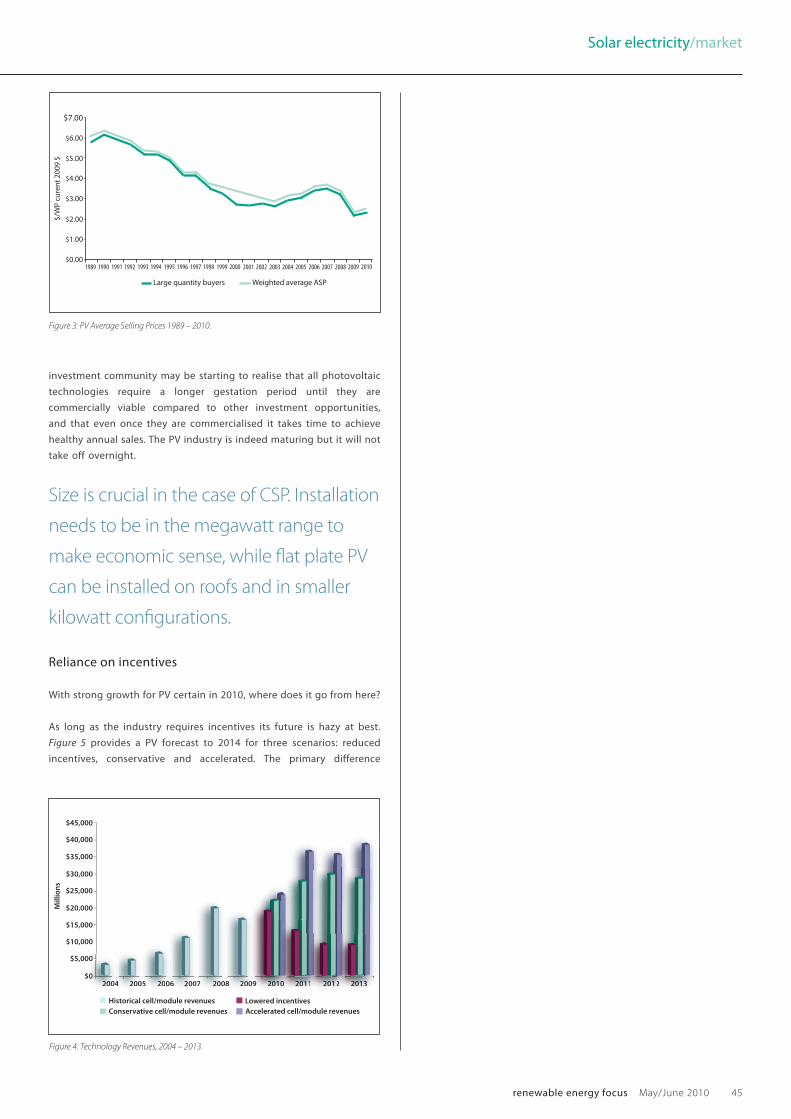

However, increasing prices are easing margins and this is good news

for technology manufacturers. Figure 3 presents average technology

prices from 1989 through an estimate for 2010 for large quantity

buyers, along with a weighted average for all buyers (reflecting

different prices for markets and buyers.) Figure 4 presents technology

revenues from 2004 to 2009 (when the industry sold more and made

less), along with revenue forecast through to 2013.

Overall, 2010 should show significant growth for PV up to at least

11 GW, with Europe again the leading market. Thin-film technology,

in particular, may have an opportunity to recover despite investors

believing it is a riskier investment. In general, the venture and

Table 1: Regional Shipments 2004 – 2009

Region2004 MWp

% Chg 04-05

2005 MWp

% Chg 05-06

2006 MWp

% Chg 06-07

2007 MWp

% Chg 07-08

2008 MWp

% Chg 08-09

2009 MWp

CAGR 2004-2009

USA 140.6 -5% 133.6 2% 136.6 74% 237.3 63% 387.9 5% 409.0 24%

Japan 547.0 31% 714.0 24% 882.6 2% 901.9 36% 1228.0 2% 1255.5 18%

Europe 272.9 49% 406.9 50% 611.3 62% 992.4 71% 1700.0 -16% 1433.6 39%

ROW 47.2 45% 68.6 57% 107.8 49% 160.5 162% 421.2 164% 1113.8 88%

China & Taiwan 42.0 101% 84.6 191% 246.3 217% 780.9 125% 1754.7 109% 3674.7 145%

Total Ship-ments

1049.8 34% 1407.7 41% 1984.6 55% 3073.0 79% 5491.8 44% 7886.6 50%

Table 2: Thin-film and Large Quantity Buyer Average Selling Prices, or ASPs 2004 – 2009

Year Thin-film ASP (US$)Thin-film ASP

ChangeLarge Buyer ASP

(US$)Large Buyer ASP

ChangeDifference Thin-film to

Large Buyer (US$)Difference Thin-film

Large Buyer

2004 2.5 2.90 0.40 14%

2005 2.75 10% 3.03 4% 0.28 9%

2006 3.00 9% 3.39 12% 0.39 12%

2007 3.25 8% 3.50 3% 0.25 7%

2008 3.00 -8% 3.25 -7% 0.25 8%

2009 1.65 -45% 2.18 -33% 0.53 24%

5 year CAGR -8% -6%

Shipments to the first point of sale,

including installers, system integrators,

distributors and other technology

manufacturers, grew by 44% to 7.9 GW.

This was a significant rise from 5.5 GW

in 2008.

renewable energy focus May/June 2010 45

Solar electricity/market

investment community may be starting to realise that all photovoltaic

technologies require a longer gestation period until they are

commercially viable compared to other investment opportunities,

and that even once they are commercialised it takes time to achieve

healthy annual sales. The PV industry is indeed maturing but it will not

take off overnight.

Reliance on incentives

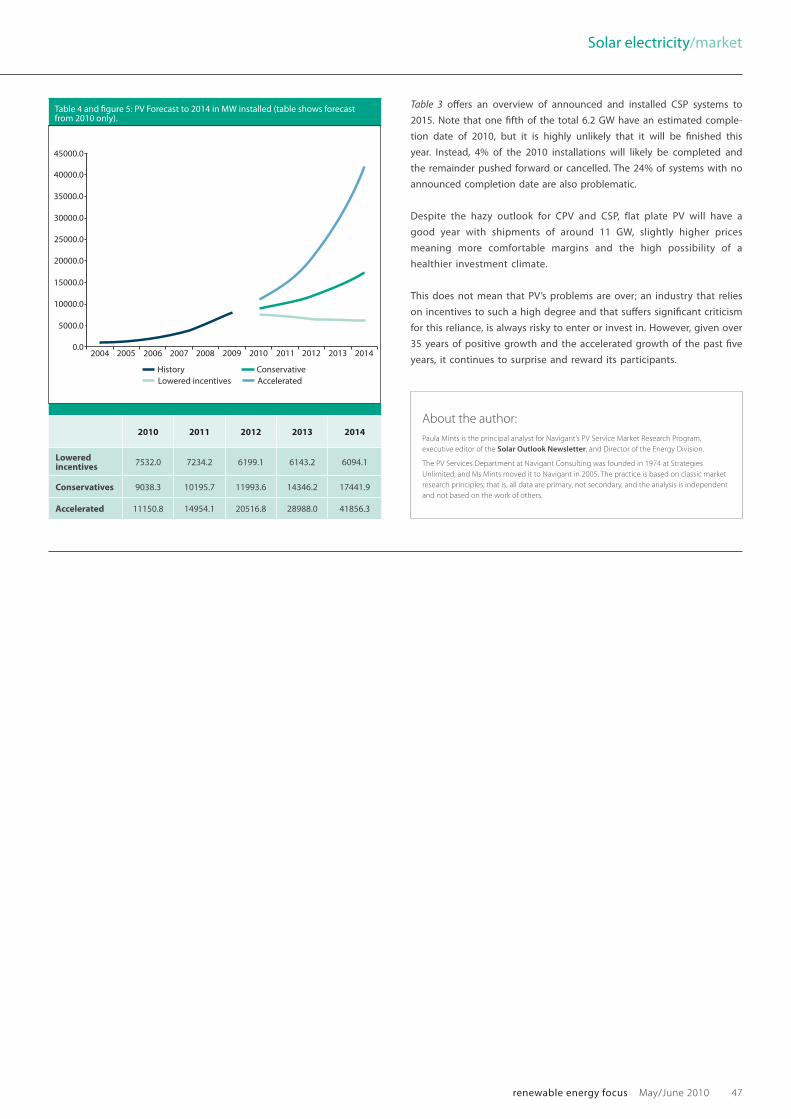

With strong growth for PV certain in 2010, where does it go from here?

As long as the industry requires incentives its future is hazy at best.

Figure 5 provides a PV forecast to 2014 for three scenarios: reduced

incentives, conservative and accelerated. The primary difference

$45,000

$40,000

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$0

Historical cell/module revenuesConservative cell/module revenues Accelerated cell/module revenues

Lowered incentives

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

00

$022004 220004 5 22005 6 20006 7 220007 8 22008 33300999 2202202022200020220220 0000 2220222022002202022000000000011010110 111 2220200222002022020201111111 22020222202020202022011331131132222221121212

Mill

ion

s

Figure 4: Technology Revenues, 2004 – 2013.

$7.00

$6.00

$5.00

$4.00

$3.00

$2.00

$1.00

$0.001989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Weighted average ASPLarge quantity buyers

$/W

P cu

rent

200

9 $

Figure 3: PV Average Selling Prices 1989 – 2010.

Size is crucial in the case of CSP. Installation

needs to be in the megawatt range to

make economic sense, while flat plate PV

can be installed on roofs and in smaller

kilowatt configurations.

46 renewable energy focus May/June 2010

Solar electricity/market

between conservative and accelerated forecasts is the availability of

incentivised markets. The accelerated forecast assumes continued

growth in markets such as Germany that, although they appear

saturated, continue to consume products.

Every indication coming from the German Government seemed to

show that significant changes to its FiT would have happened by

now, including an end to incentives for agricultural land. Although it

would seem a safe bet to assume that these changes will eventually

come about, there are no sure-fire certainties in solar. One thing is

for certain; if and when Germany and other countries alter their FiTs,

average technology prices will decrease and margins will once again

be compressed.

CSP installations (trough, power tower and dish) have a much longer

timeline than flat plate PV. In general, it is necessary to assume that it

will take two years from the start of construction. This long timeline is

problematic in terms of forecasting and CSP is unlikely to ever provide

a smooth trend line in this regard. Despite the hazy outlook for CPV

and CSP, flat plate PV will have

a good year with shipments of

around 11 GW, slightly higher

prices meaning more comfortable

margins and the high possibility of

a healthier investment climate.

Table 3: CSP Installation Estimations (MW)

2009 completed 121.0 2%

2010 estimated completion 1221.2 20%

2011 estimated completion 400.0 6%

2012 estimated completion 1150.0 19%

2013 estimated completion 962.0 16%

2014 estimated completion 280.0 5%

2015 estimated completion 500.0 8%

no date estimated completion 1493.6 24%

Totals 6190.1 99%

Completion Dates by Technology MWs % Total

Undecided 620.0 12%

Power Tower 177.1 3%

Dish/Linear Fresnel 578.3 11%

Trough 3959.4 74%

The primary issue facing the CSP community these days is that crystalline

silicon (c-Si) flat plate is currently cheap and has a more consistent track

record in the field. However there are examples of CSP installations up and

running (such as PS10 and PS20, at Sanlucar la Mayor, near Seville, Spain).

renewable energy focus May/June 2010 47

Solar electricity/market

Table 3 offers an overview of announced and installed CSP systems to

2015. Note that one fifth of the total 6.2 GW have an estimated comple-

tion date of 2010, but it is highly unlikely that it will be finished this

year. Instead, 4% of the 2010 installations will likely be completed and

the remainder pushed forward or cancelled. The 24% of systems with no

announced completion date are also problematic.

Despite the hazy outlook for CPV and CSP, flat plate PV will have a

good year with shipments of around 11 GW, slightly higher prices

meaning more comfortable margins and the high possibility of a

healthier investment climate.

This does not mean that PV’s problems are over; an industry that relies

on incentives to such a high degree and that suffers significant criticism

for this reliance, is always risky to enter or invest in. However, given over

35 years of positive growth and the accelerated growth of the past five

years, it continues to surprise and reward its participants.

About the author:

Paula Mints is the principal analyst for Navigant’s PV Service Market Research Program,

executive editor of the Solar Outlook Newsletter, and Director of the Energy Division.

The PV Services Department at Navigant Consulting was founded in 1974 at Strategies

Unlimited, and Ms Mints moved it to Navigant in 2005. The practice is based on classic market

research principles; that is, all data are primary, not secondary, and the analysis is independent

and not based on the work of others.

Table 4 and figure 5: PV Forecast to 2014 in MW installed (table shows forecast from 2010 only).

2010 2011 2012 2013 2014

Lowered incentives

7532.0 7234.2 6199.1 6143.2 6094.1

Conservatives 9038.3 10195.7 11993.6 14346.2 17441.9

Accelerated 11150.8 14954.1 20516.8 28988.0 41856.3

45000.0

40000.0

35000.0

30000.0

25000.0

20000.0

15000.0

10000.0

5000.0

0.02004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

History ConservativeAcceleratedLowered incentives