Embed Size (px)

Citation preview

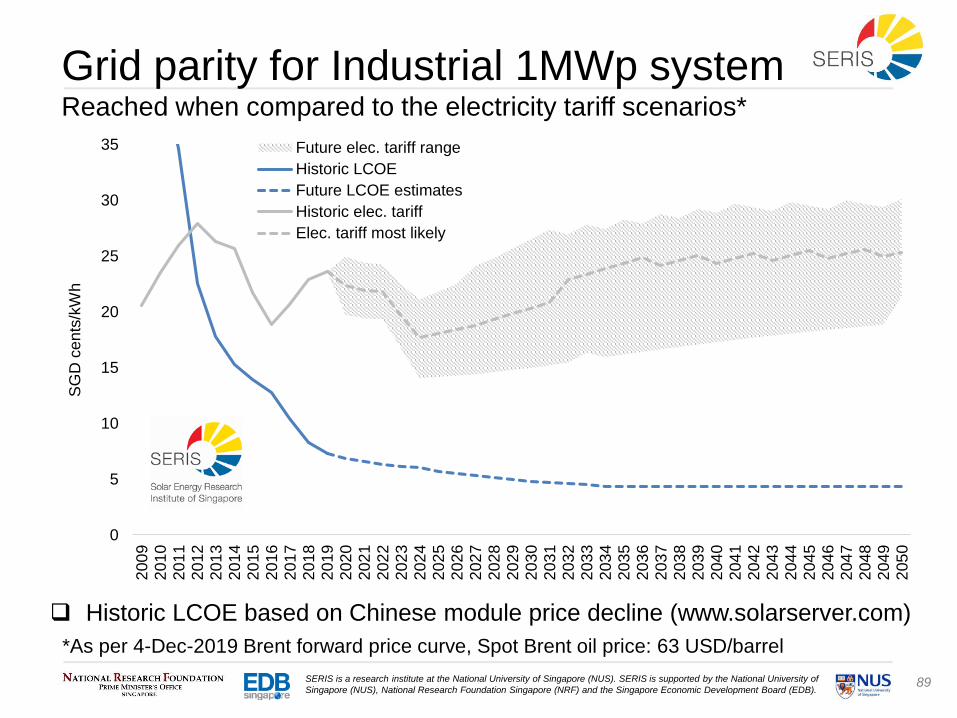

1SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Solar Economics Handbook of Singapore

Celine PATON, Congyi TAN, Dr. Thomas REINDL

Solar Energy Research Institute of Singapore (SERIS)

Singapore, 19 December 2019

2SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Disclaimer

Disclaimer, limitation of liability

This report represents the personal opinions of the members of the

evaluation team. The evaluation team members, the Solar Energy

Research Institute of Singapore (SERIS) and the National University

of Singapore (NUS), exclude any legal liability for any statement

made in the report. In no event shall the evaluation team members,

SERIS, and NUS of any tier be liable in contract, tort, strict liability,

warranty or otherwise, for any special, incidental or consequential

damages, such as, but not limited to, delay, disruption, loss of

product, loss of anticipated profits or revenue, loss of use of the

equipment or system, non-operation or increased expense of

operation of other equipment or systems, cost of capital, or cost of

purchase or replacement equipment systems or power.

3SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Overview

1. Global PV market

2. Singapore PV market

3. Singapore electricity market

a) Structure

b) Generation

c) Demand

d) Prices

4. PV adoption in Singapore

5. Future electricity price scenarios

6. Grid parity and economic viability analysis

4SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

1. Global PV market

5SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

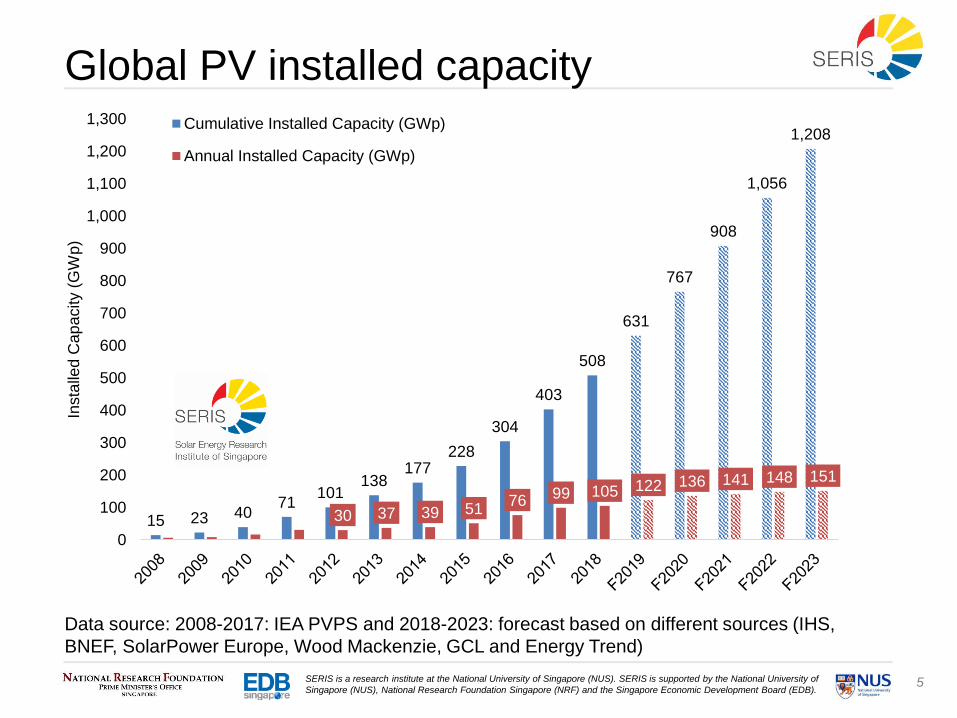

15 23 4071

101138

177228

304

403

508

631

767

908

1,056

1,208

30 37 39 5176 99 105 122 136 141 148 151

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

Insta

lled

Cap

acity (

GW

p)

Cumulative Installed Capacity (GWp)

Annual Installed Capacity (GWp)

Global PV installed capacity

Data source: 2008-2017: IEA PVPS and 2018-2023: forecast based on different sources (IHS,

BNEF, SolarPower Europe, Wood Mackenzie, GCL and Energy Trend)

6SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

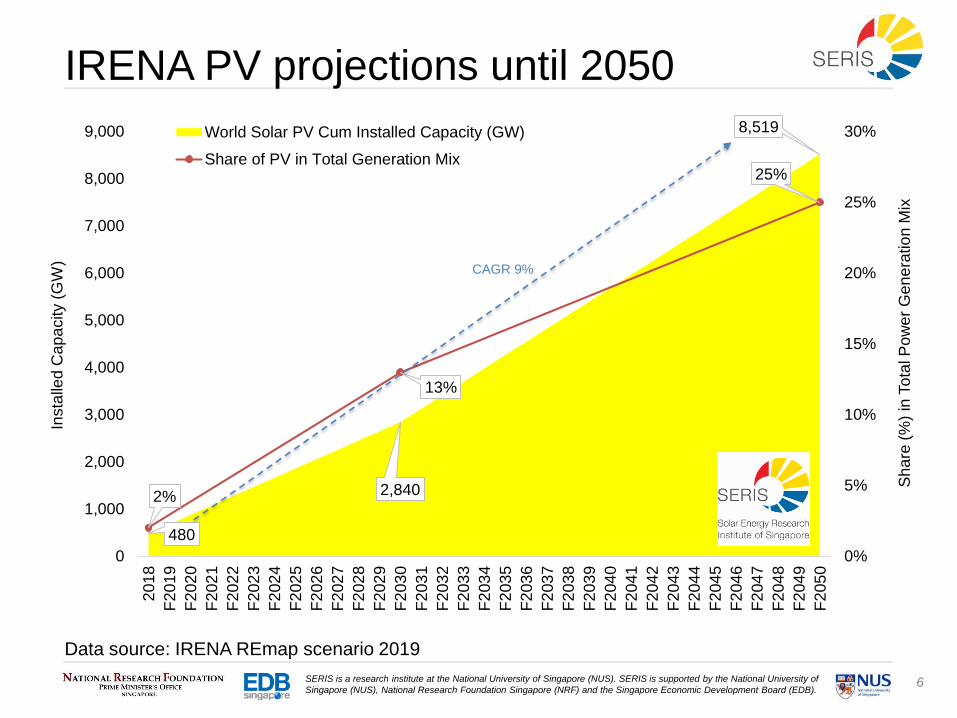

480

2,840

8,519

2%

13%

25%

0%

5%

10%

15%

20%

25%

30%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,0002

01

8

F2

01

9

F2

02

0

F2

02

1

F2

02

2

F2

02

3

F2

02

4

F2

02

5

F2

02

6

F2

02

7

F2

02

8

F2

02

9

F2

03

0

F2

03

1

F2

03

2

F2

03

3

F2

03

4

F2

03

5

F2

03

6

F2

03

7

F2

03

8

F2

03

9

F2

04

0

F2

04

1

F2

04

2

F2

04

3

F2

04

4

F2

04

5

F2

04

6

F2

04

7

F2

04

8

F2

04

9

F2

05

0

Sh

are

(%

) in

To

tal P

ow

er

Ge

ne

ratio

n M

ix

Insta

lled

Cap

acity (

GW

)

World Solar PV Cum Installed Capacity (GW)

Share of PV in Total Generation Mix

IRENA PV projections until 2050

Data source: IRENA REmap scenario 2019

CAGR 9%

7SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

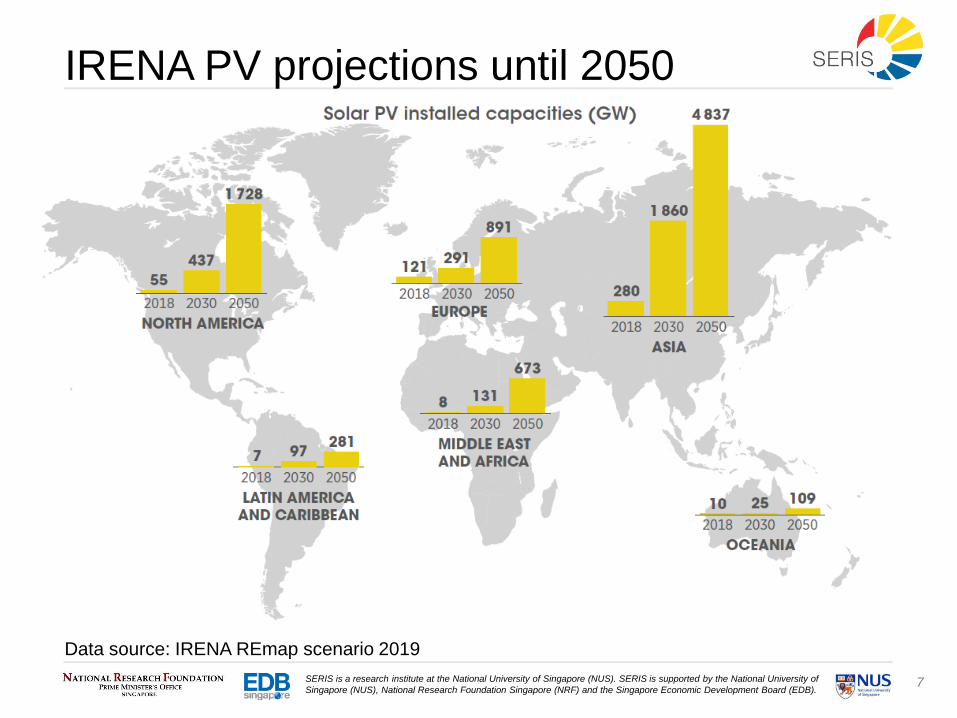

IRENA PV projections until 2050

Data source: IRENA REmap scenario 2019

8SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Data source: SERIS market research, ITRPV 10th edition (October 2019)

Historic global PV module pricesReducing trend of module prices with increasing installed capacity

0

100

200

300

400

500

600

0

2

4

6

8

10

12

14

16

18

20

198

01

98

11

98

21

98

31

98

41

98

51

98

61

98

71

98

81

98

91

99

01

99

11

99

21

99

31

99

41

99

51

99

61

99

71

99

81

99

92

00

02

00

12

00

22

00

32

00

42

00

52

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8

Cu

m insta

lled

ca

pa

city (

GW

)

Mo

du

le p

rice

(U

SD

/Wp

)

Module price (22% learning rate)

Module price (ITRPV)

Cumulative installed capacity (GW)

9SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

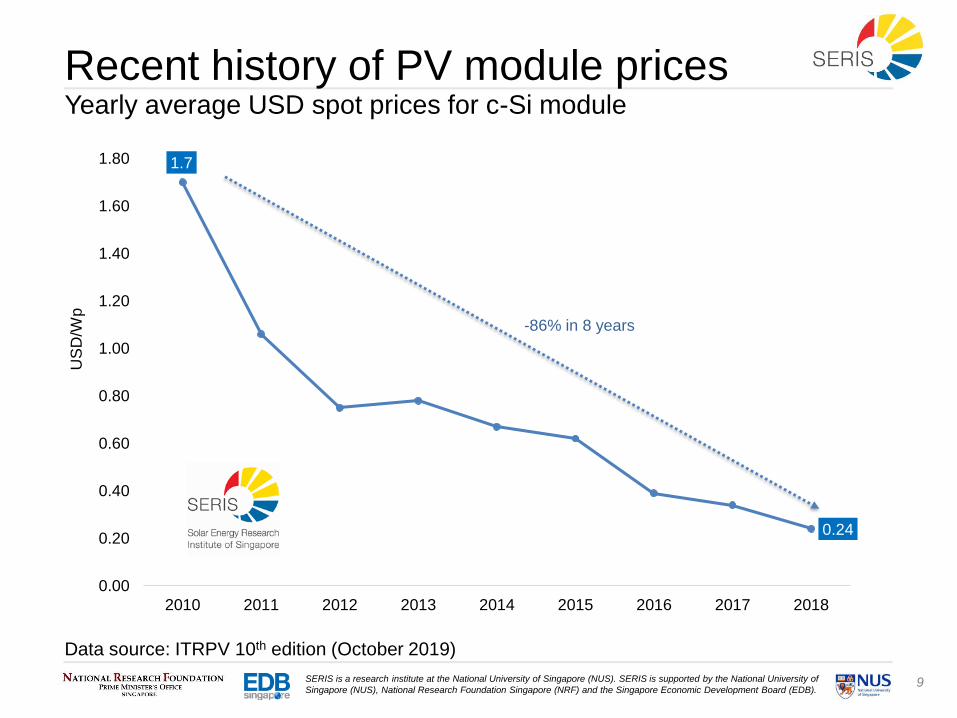

1.7

0.24

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2010 2011 2012 2013 2014 2015 2016 2017 2018

US

D/W

pRecent history of PV module pricesYearly average USD spot prices for c-Si module

Data source: ITRPV 10th edition (October 2019)

-86% in 8 years

10SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

4/1

/20

17

4/2

/20

17

4/3

/20

17

4/4

/20

17

4/5

/20

17

4/6

/20

17

4/7

/20

17

4/8

/20

17

4/9

/20

17

4/1

0/2

017

4/1

1/2

017

4/1

2/2

017

4/1

/20

18

4/2

/20

18

4/3

/20

18

4/4

/20

18

4/5

/20

18

4/6

/20

18

4/7

/20

18

4/8

/20

18

4/9

/20

18

4/1

0/2

018

4/1

1/2

018

4/1

2/2

018

4/1

/20

19

4/2

/20

19

4/3

/20

19

4/4

/20

19

4/5

/20

19

4/6

/20

19

4/7

/20

19

4/8

/20

19

4/9

/20

19

4/1

0/2

019

4/1

1/2

019

4/1

2/2

019

US

D/W

p

PVI Multi-Si

PVI Multi-Si High Eff / PERC

PVI Mono High Eff / PERC

PVI Thin-Film

ET 270-75W Multi-Si

ET 280-85W Multi-Si

ET 290-95W Mono-Si

ET 300-10W Mono-Si

ET 310W+ Mono-Si

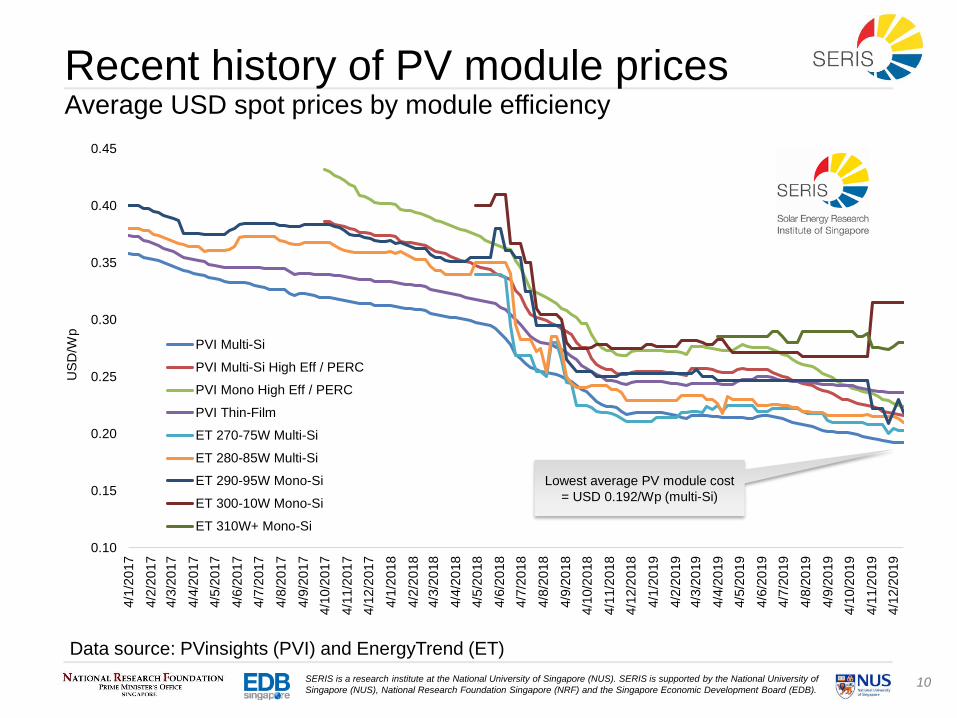

Recent history of PV module pricesAverage USD spot prices by module efficiency

Data source: PVinsights (PVI) and EnergyTrend (ET)

Lowest average PV module cost

= USD 0.192/Wp (multi-Si)

11SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

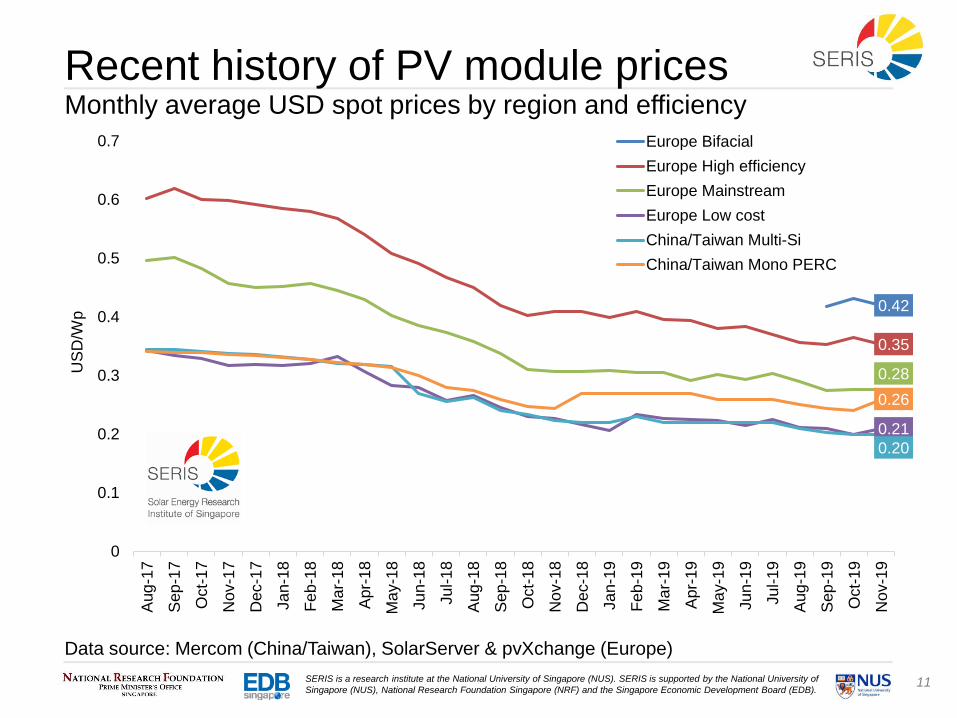

Recent history of PV module pricesMonthly average USD spot prices by region and efficiency

Data source: Mercom (China/Taiwan), SolarServer & pvXchange (Europe)

0.42

0.35

0.28

0.21

0.20

0.26

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7A

ug

-17

Sep

-17

Oct-

17

Nov-1

7

Dec-1

7

Ja

n-1

8

Fe

b-1

8

Ma

r-18

Apr-

18

Ma

y-1

8

Ju

n-1

8

Ju

l-1

8

Aug

-18

Sep

-18

Oct-

18

Nov-1

8

Dec-1

8

Ja

n-1

9

Fe

b-1

9

Ma

r-19

Apr-

19

Ma

y-1

9

Ju

n-1

9

Ju

l-1

9

Aug

-19

Sep

-19

Oct-

19

Nov-1

9

US

D/W

p

Europe Bifacial

Europe High efficiency

Europe Mainstream

Europe Low cost

China/Taiwan Multi-Si

China/Taiwan Mono PERC

12SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

2. Singapore PV market

13SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

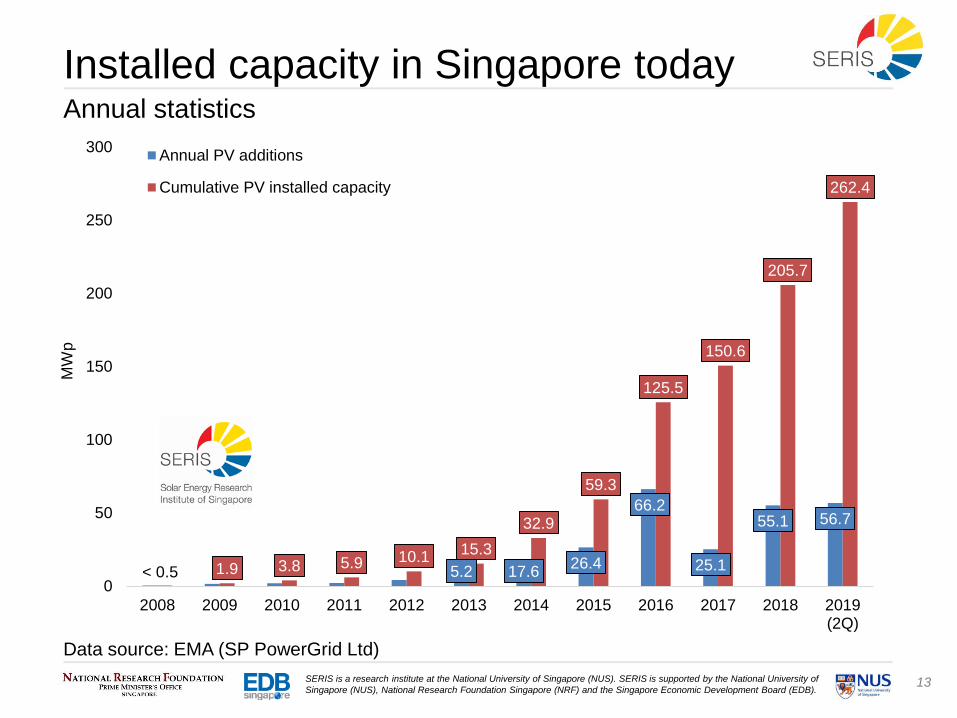

5.2 17.626.4

66.2

25.1

55.1 56.7

1.9 3.8 5.9 10.115.3

32.9

59.3

125.5

150.6

205.7

262.4

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019(2Q)

MW

p

Annual PV additions

Cumulative PV installed capacity

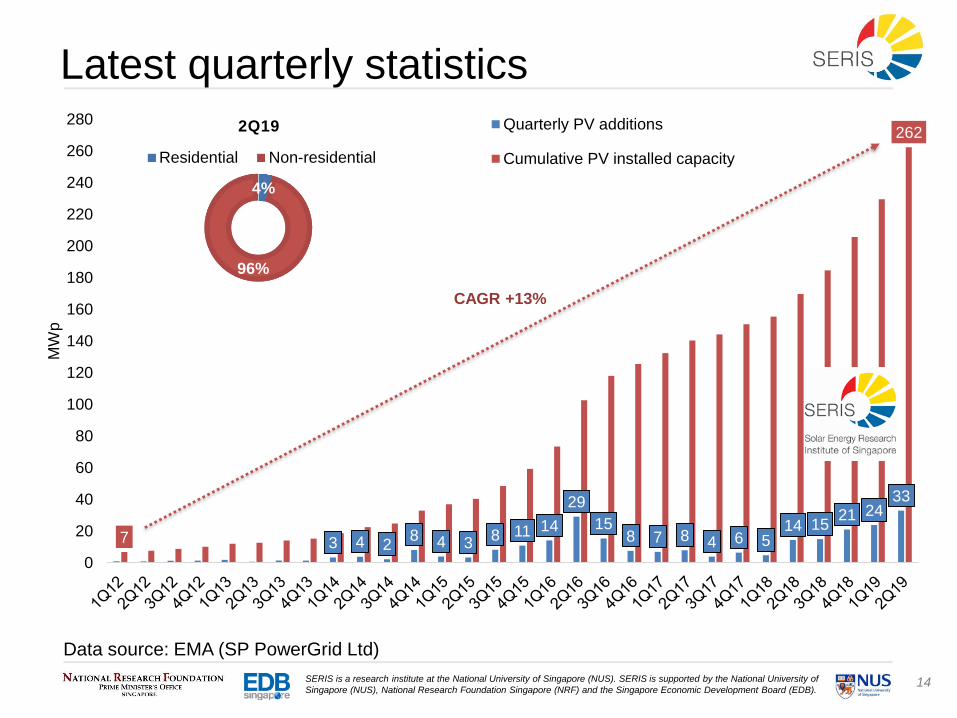

Installed capacity in Singapore todayAnnual statistics

Data source: EMA (SP PowerGrid Ltd)

< 0.5

14SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

3 4 28 4 3

8 11 14

29

158 7 8 4 6 5

14 1521 24

33

7

262

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

MW

p

Quarterly PV additions

Cumulative PV installed capacity

Latest quarterly statistics

Data source: EMA (SP PowerGrid Ltd)

CAGR +13%

4%

96%

2Q19

Residential Non-residential

15SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

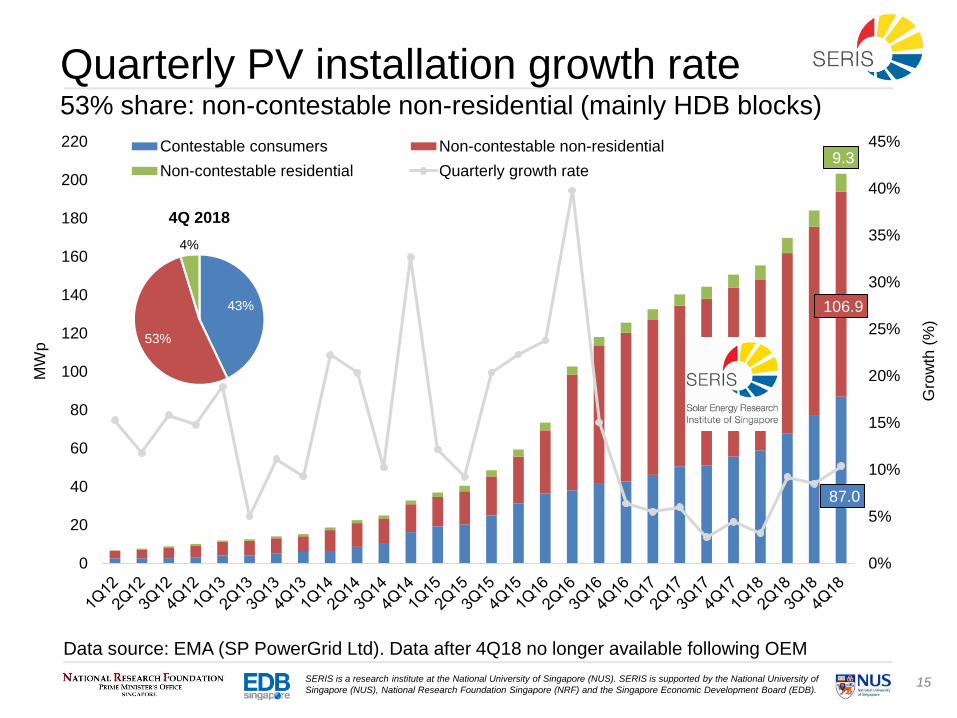

87.0

106.9

9.3

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

20

40

60

80

100

120

140

160

180

200

220

Gro

wth

(%

)

MW

p

Contestable consumers Non-contestable non-residential

Non-contestable residential Quarterly growth rate

Quarterly PV installation growth rate53% share: non-contestable non-residential (mainly HDB blocks)

Data source: EMA (SP PowerGrid Ltd). Data after 4Q18 no longer available following OEM

43%

53%

4%

4Q 2018

16SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

20

40

60

80

100

120

140

160

180

200

220

240

260

2801

Q1

2

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

MW

p

Public service agencies

Town councils & grassroots units

Private sector

Residential

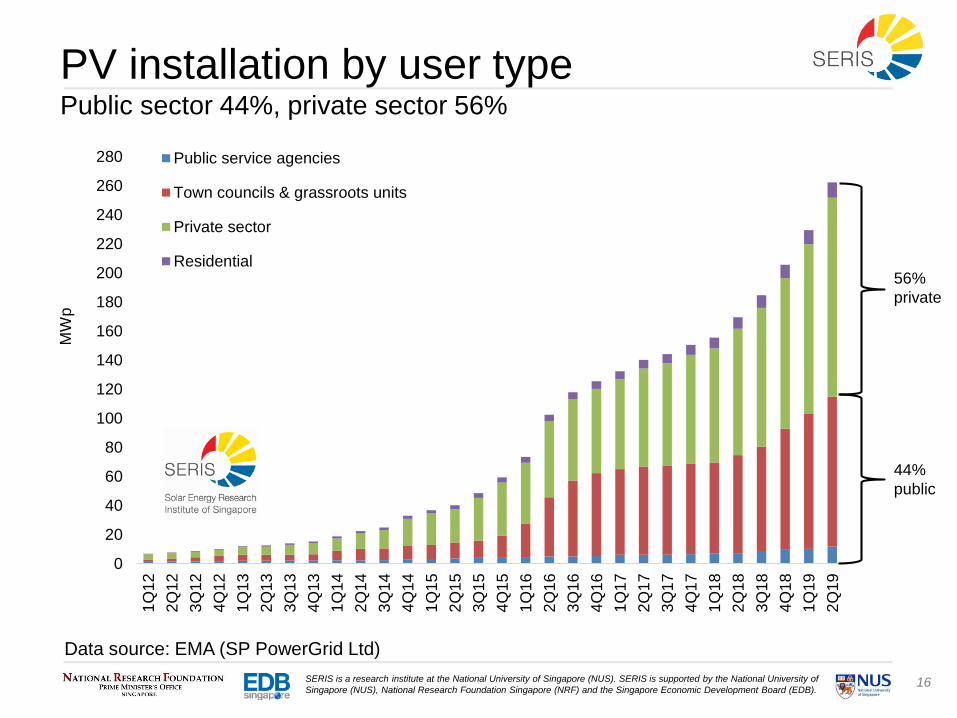

PV installation by user typePublic sector 44%, private sector 56%

44%

public

56%

private

Data source: EMA (SP PowerGrid Ltd)

17SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Regional split within Singapore [MWac]

30.1 MWac

501 Systems

Residential: 1%

31.8 MWac

477 Systems

Residential: 5%

Data source: EMA & SPPG, 2Q2019

24.5 MWac

645 Systems

Residential: 15%

26.2 MWac

857 Systems

Residential: 8%

Total installed: 202 MWac

Total systems: 3,173

89.4 MWac

693 Systems

Residential: <1%

18SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

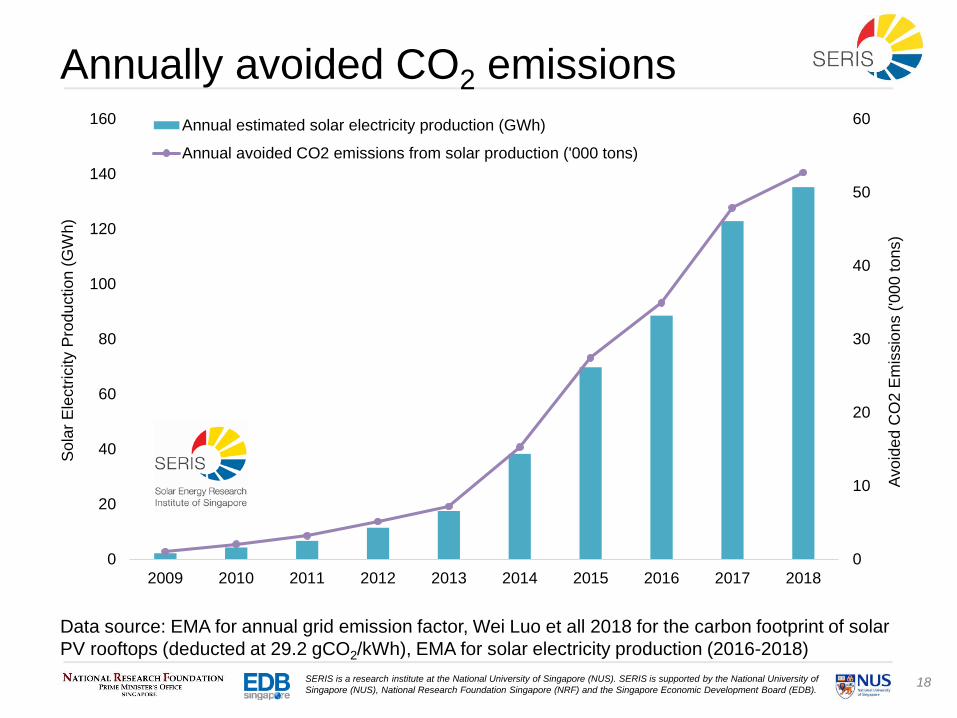

Annually avoided CO2 emissions

Data source: EMA, 1Q2015Data source: EMA for annual grid emission factor, Wei Luo et all 2018 for the carbon footprint of solar

PV rooftops (deducted at 29.2 gCO2/kWh), EMA for solar electricity production (2016-2018)

0

10

20

30

40

50

60

0

20

40

60

80

100

120

140

160

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Avo

ide

d C

O2

Em

issio

ns (

'00

0 to

ns)

So

lar

Ele

ctr

icity P

rod

uctio

n (

GW

h)

Annual estimated solar electricity production (GWh)

Annual avoided CO2 emissions from solar production ('000 tons)

19SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

1

2

3

4

5

6

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

203

8

203

9

204

0

204

1

204

2

204

3

204

4

204

5

204

6

204

7

204

8

204

9

205

0

In %

ele

ctr

icity d

em

an

d

Insta

lled

ca

pa

city (

GW

p)

BAS Scenario (GWp)

ACC Scenario (GWp)

Actual capacity (GWp)

BAS Scenario (GWp)

ACC Scenario (GWp)

BAS Scenario (%)

ACC Scenario (%)

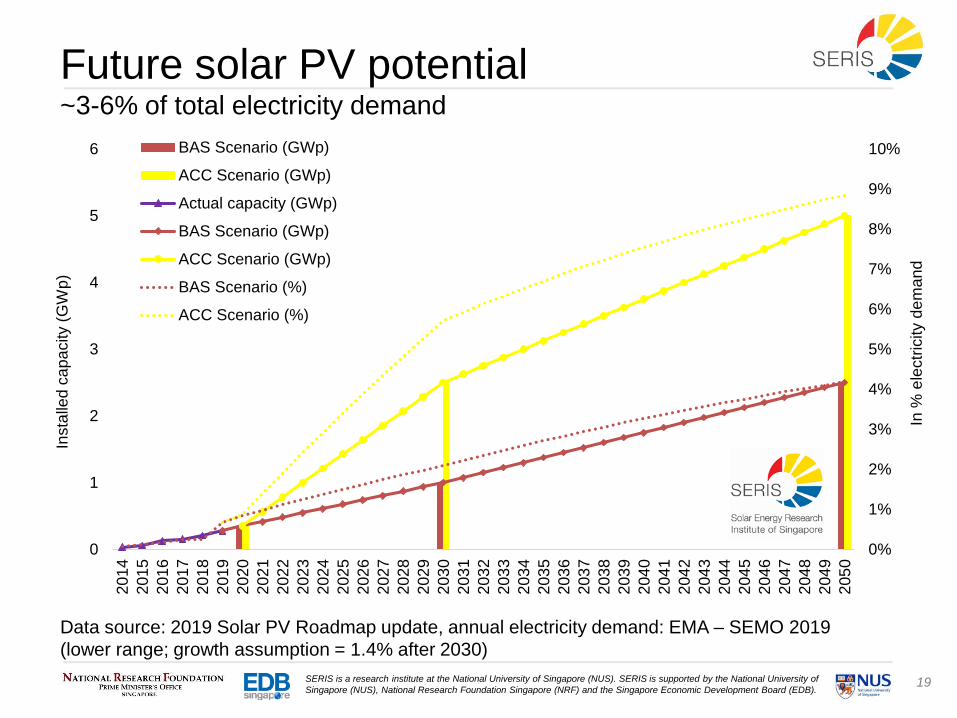

Future solar PV potential~3-6% of total electricity demand

Data source:Q2015Data source: 2019 Solar PV Roadmap update, annual electricity demand: EMA – SEMO 2019

(lower range; growth assumption = 1.4% after 2030)

20SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

203

8

203

9

204

0

204

1

204

2

204

3

204

4

204

5

204

6

204

7

204

8

204

9

205

0

In %

of to

tal a

nn

ua

l C

O2

em

issio

ns

An

nu

ally

avo

ide

d C

O2

em

issio

ns (

mill

ion

to

nn

es)

BAS Scenarios (MT)

ACC Scenarios (MT)

BAS Scenario (MT)

ACC Scenario (MT)

BAS Scenario (%)

ACC Scenario (%)

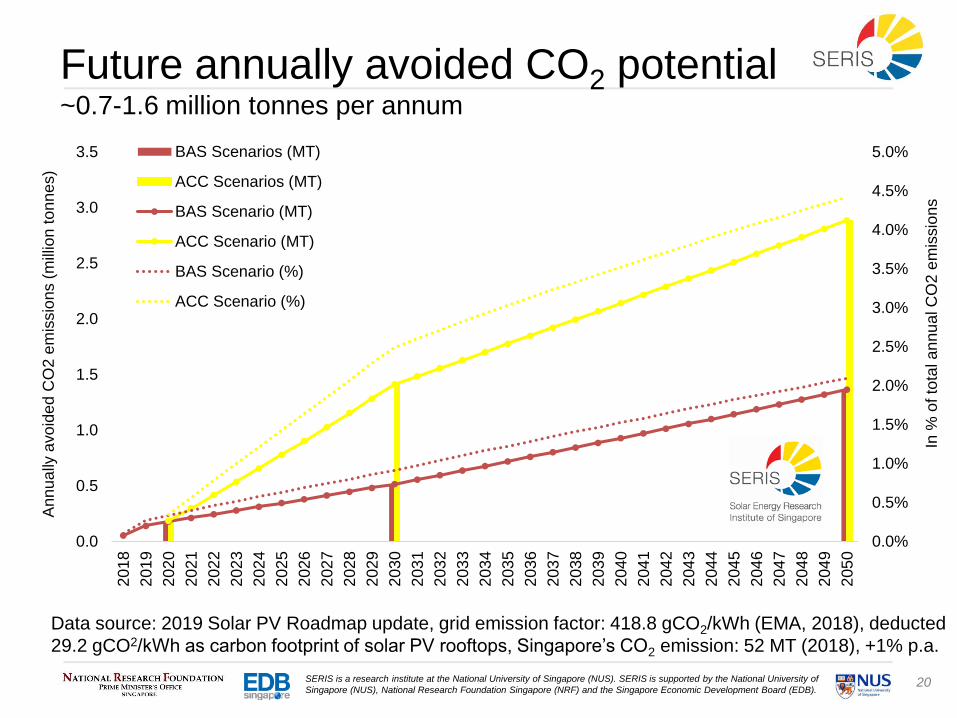

Future annually avoided CO2 potential~0.7-1.6 million tonnes per annum

Data source:Q2015Data source: 2019 Solar PV Roadmap update, grid emission factor: 418.8 gCO2/kWh (EMA, 2018), deducted

29.2 gCO2/kWh as carbon footprint of solar PV rooftops, Singapore’s CO2 emission: 52 MT (2018), +1% p.a.

21SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

3a) Singapore electricity market: Structure

22SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

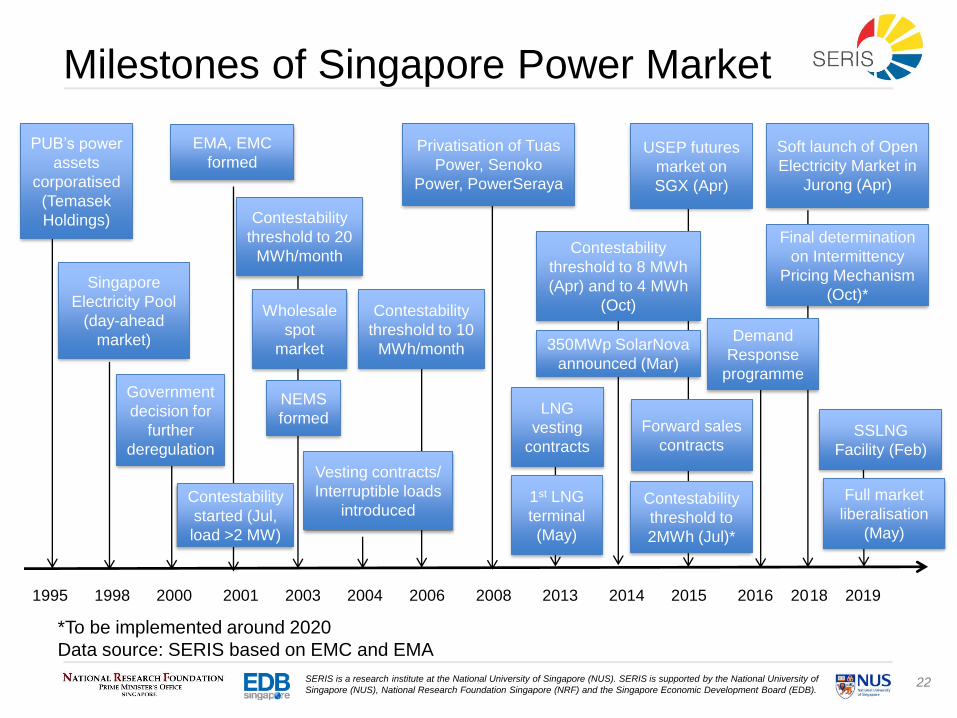

Milestones of Singapore Power Market

*To be implemented around 2020

Data source: SERIS based on EMC and EMA

PUB’s power

assets

corporatised

(Temasek

Holdings)

1995 1998 2000 2001 2003 2004 2006 2008 2013 2014 2015 2016 2018 2019

Singapore

Electricity Pool

(day-ahead

market)

Government

decision for

further

deregulation

Wholesale

spot

market

Vesting contracts/

Interruptible loads

introduced1st LNG

terminal

(May)

Privatisation of Tuas

Power, Senoko

Power, PowerSeraya

Contestability

threshold to

2MWh (Jul)*

USEP futures

market on

SGX (Apr)

EMA, EMC

formed

Contestability

started (Jul,

load >2 MW)

NEMS

formed

Contestability

threshold to 20

MWh/monthContestability

threshold to 8 MWh

(Apr) and to 4 MWh

(Oct)Contestability

threshold to 10

MWh/month 350MWp SolarNova

announced (Mar)

Forward sales

contracts

LNG

vesting

contracts

Full market

liberalisation

(May)

Soft launch of Open

Electricity Market in

Jurong (Apr)

SSLNG

Facility (Feb)

Final determination

on Intermittency

Pricing Mechanism

(Oct)*

Demand

Response

programme

23SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

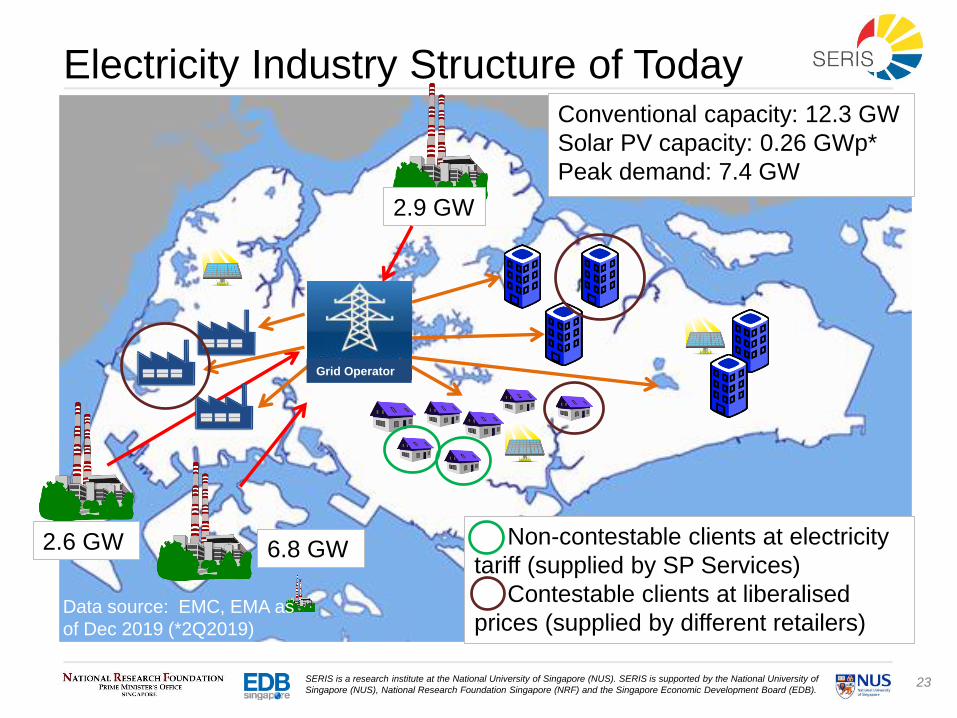

Electricity Industry Structure of Today

2.9 GW

2.6 GW 6.8 GW

Conventional capacity: 12.3 GW

Solar PV capacity: 0.26 GWp*

Peak demand: 7.4 GW

Grid Operator

Data source: EMC, EMA as

of Dec 2019 (*2Q2019)

Non-contestable clients at electricity

tariff (supplied by SP Services)

Contestable clients at liberalised

prices (supplied by different retailers)

24SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

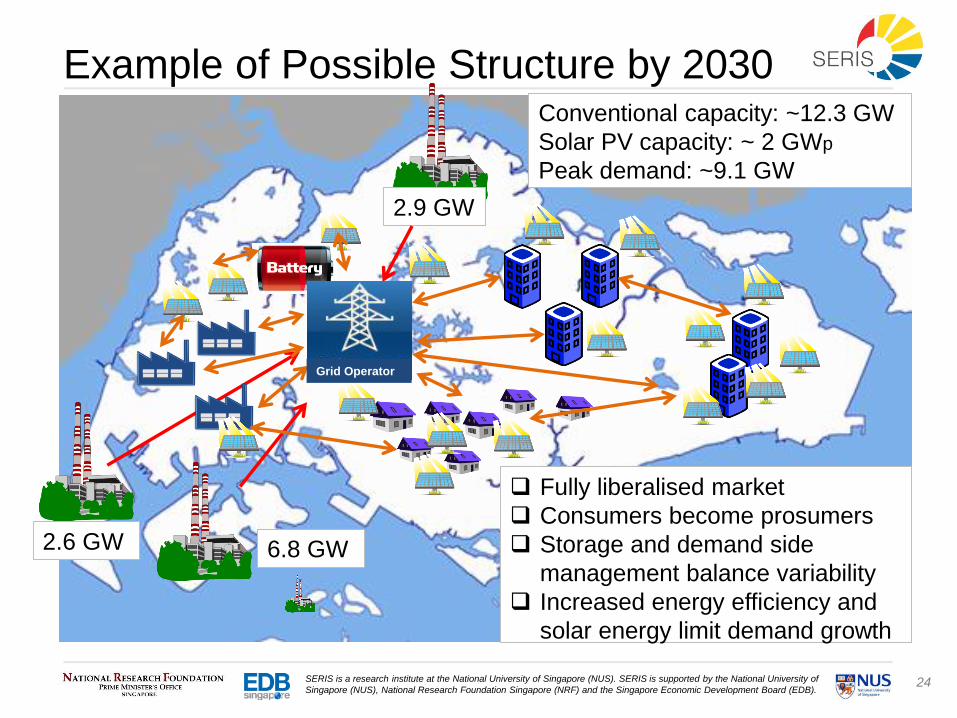

Example of Possible Structure by 2030

2.9 GW

2.6 GW 6.8 GW

Fully liberalised market

Consumers become prosumers

Storage and demand side

management balance variability

Increased energy efficiency and

solar energy limit demand growth

Conventional capacity: ~12.3 GW

Solar PV capacity: ~ 2 GWp

Peak demand: ~9.1 GW

Grid Operator

25SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

3b) Singapore electricity market: Generation

26SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

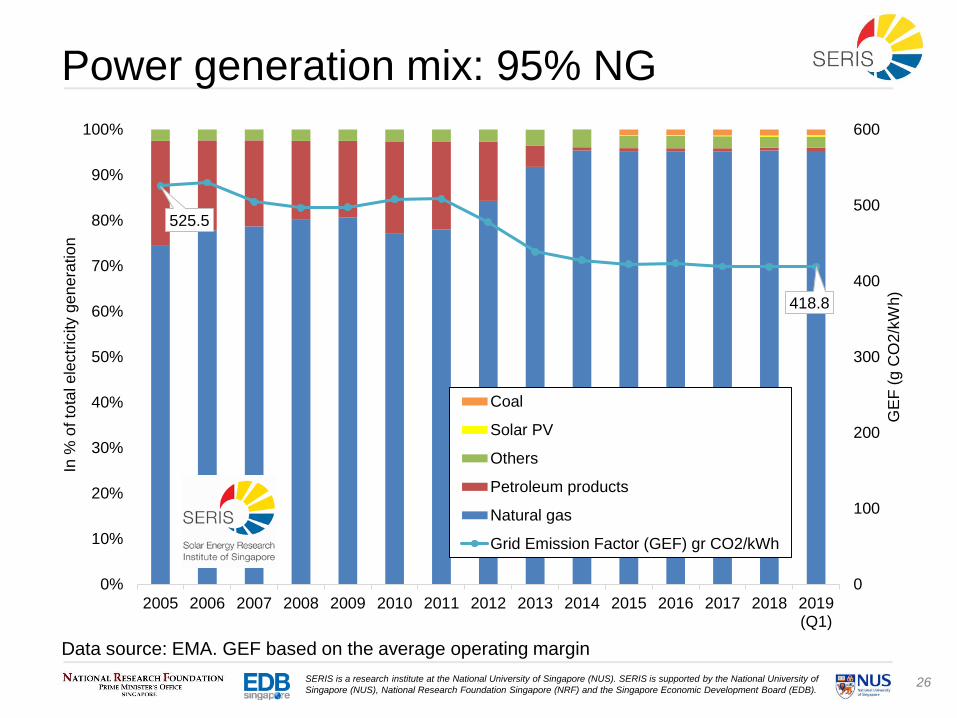

525.5

418.8

0

100

200

300

400

500

600

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019(Q1)

GE

F (

g C

O2

/kW

h)

In %

of to

tal e

lectr

icity g

en

era

tio

n

Coal

Solar PV

Others

Petroleum products

Natural gas

Grid Emission Factor (GEF) gr CO2/kWh

Power generation mix: 95% NG

Data source: EMA. GEF based on the average operating margin

27SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

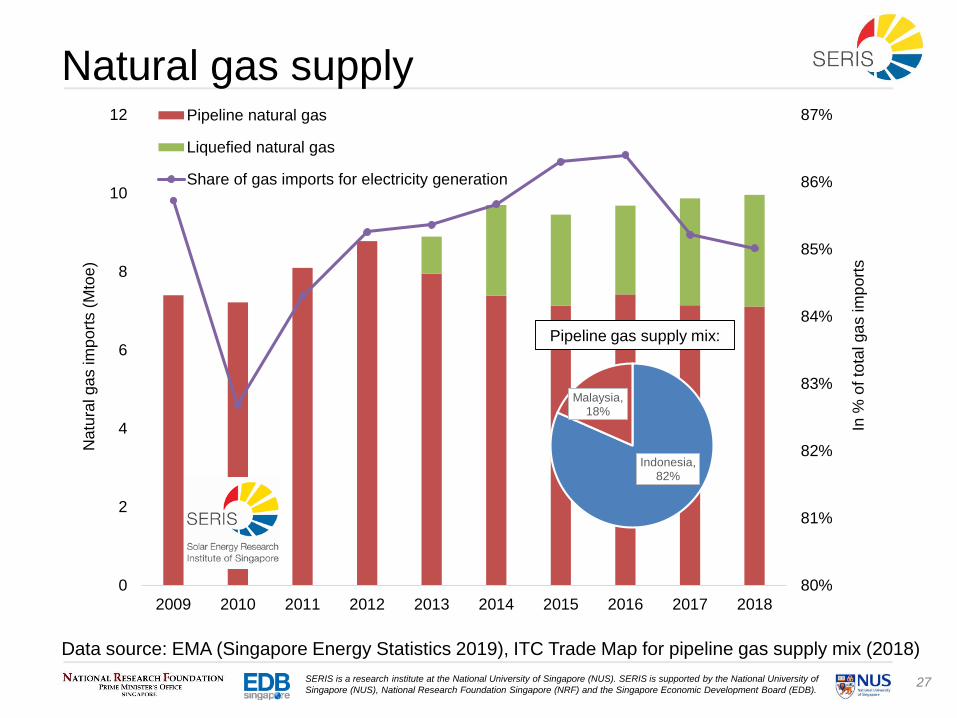

80%

81%

82%

83%

84%

85%

86%

87%

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

In %

of to

tal ga

s im

po

rts

Natu

ral ga

s im

po

rts (

Mto

e)

Pipeline natural gas

Liquefied natural gas

Share of gas imports for electricity generation

Natural gas supply

Data source: EMA (Singapore Energy Statistics 2019), ITC Trade Map for pipeline gas supply mix (2018)

Pipeline gas supply mix:

Indonesia, 82%

Malaysia, 18%

28SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ma

rket sh

are

(%

)

Ma

rket sh

are

(%

)

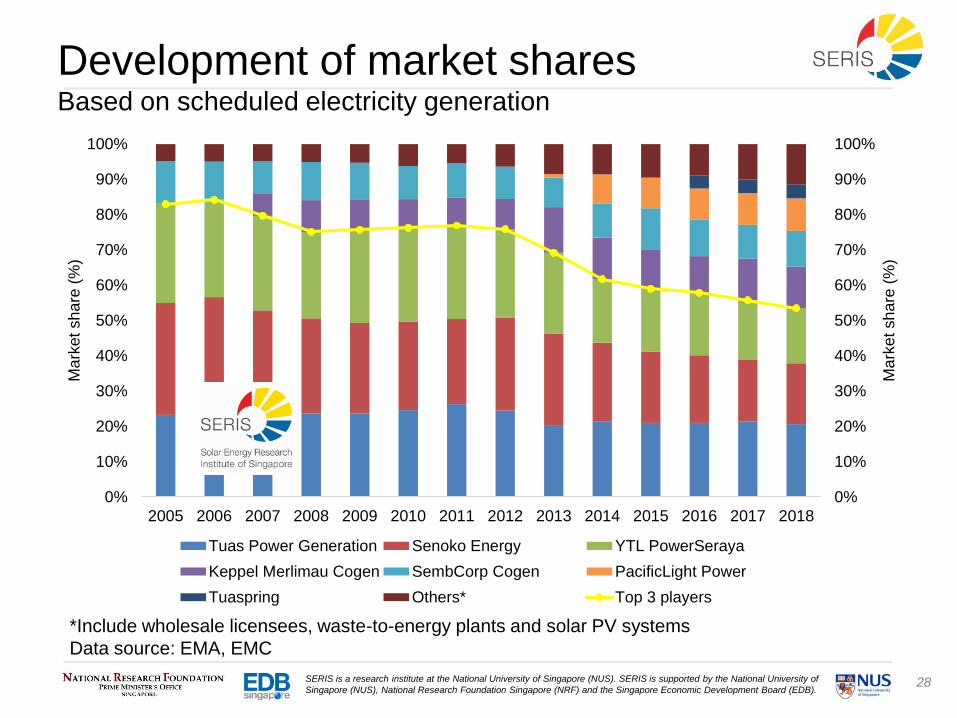

Tuas Power Generation Senoko Energy YTL PowerSeraya

Keppel Merlimau Cogen SembCorp Cogen PacificLight Power

Tuaspring Others* Top 3 players

Development of market sharesBased on scheduled electricity generation

*Include wholesale licensees, waste-to-energy plants and solar PV systems

Data source: EMA, EMC

29SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Market share of generation capacity

*SP Services and IGS owners are registering PV systems who chose EMC registration. As of 12 December

2019, registered IGS systems = 127 MWac. IGS = Intermittent Generation Sources

Data source: EMC. Total registered capacity of 12,440 MW as of 12 December 2019

22.6%

20.5%

19.3%

10.5%

9.6%

6.4%3.2%

4.8%

2.1%

1.0%

0.1%

Senoko Energy

Tuas Power Generation

YTL PowerSeraya

Keppel Merlimau Cogen

Sembcorp Cogen

PacificLight Power

Tuaspring

Embedded generators

Waste incineration

SP Services/IGS*

30SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

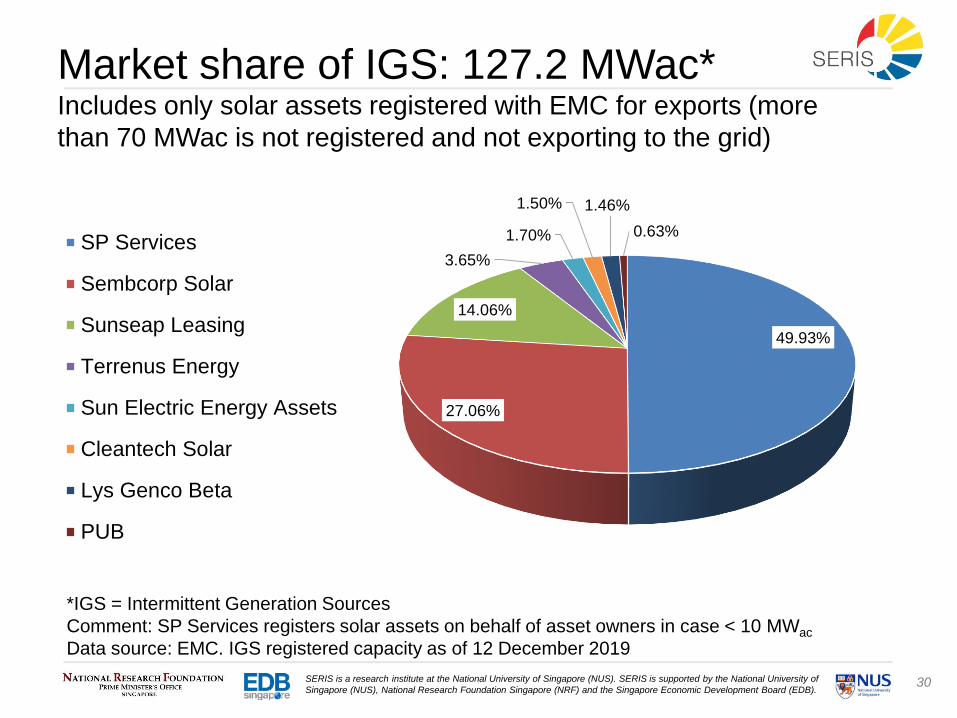

Market share of IGS: 127.2 MWac*Includes only solar assets registered with EMC for exports (more

than 70 MWac is not registered and not exporting to the grid)

*IGS = Intermittent Generation Sources

Comment: SP Services registers solar assets on behalf of asset owners in case < 10 MWac

Data source: EMC. IGS registered capacity as of 12 December 2019

49.93%

27.06%

14.06%

3.65%

1.70%

1.50% 1.46%

0.63%SP Services

Sembcorp Solar

Sunseap Leasing

Terrenus Energy

Sun Electric Energy Assets

Cleantech Solar

Lys Genco Beta

PUB

31SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

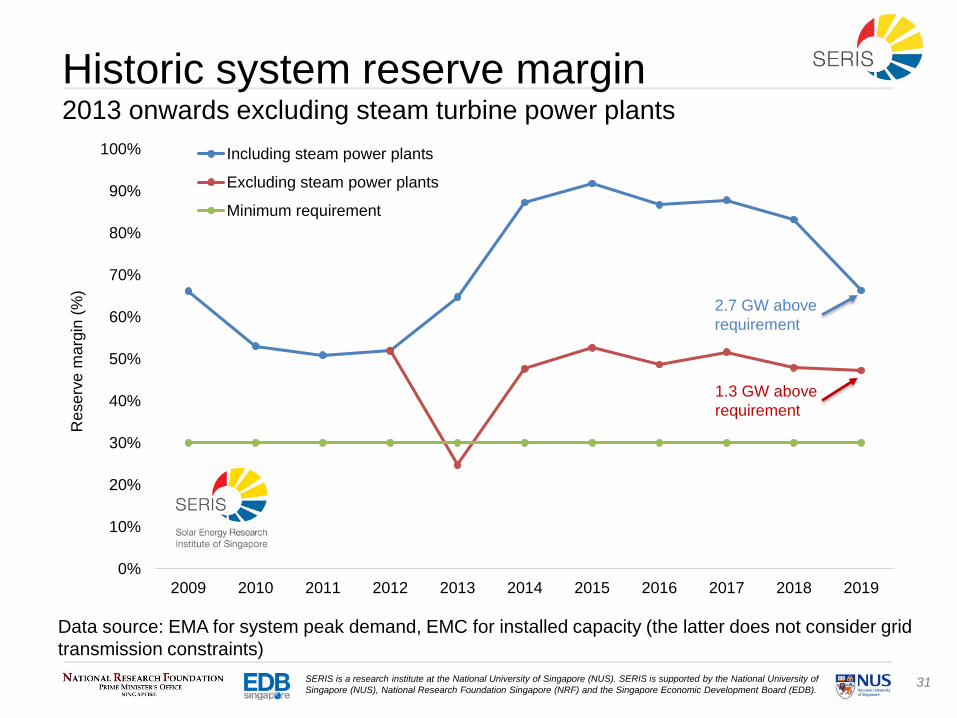

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Rese

rve

ma

rgin

(%

)

Including steam power plants

Excluding steam power plants

Minimum requirement

Historic system reserve margin2013 onwards excluding steam turbine power plants

Data source: EMA for system peak demand, EMC for installed capacity (the latter does not consider grid

transmission constraints)

2.7 GW above

requirement

1.3 GW above

requirement

32SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

In %

of to

tal ca

pa

city

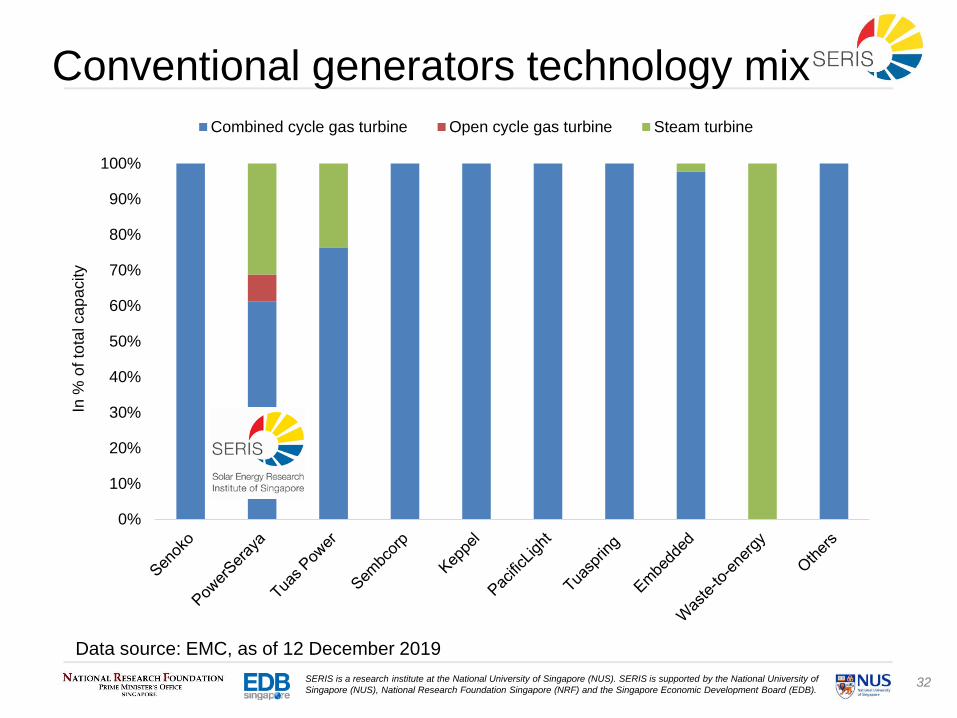

Combined cycle gas turbine Open cycle gas turbine Steam turbine

Conventional generators technology mix

Data source: EMC, as of 12 December 2019

33SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Cap

acity u

tilis

atio

n (

%)

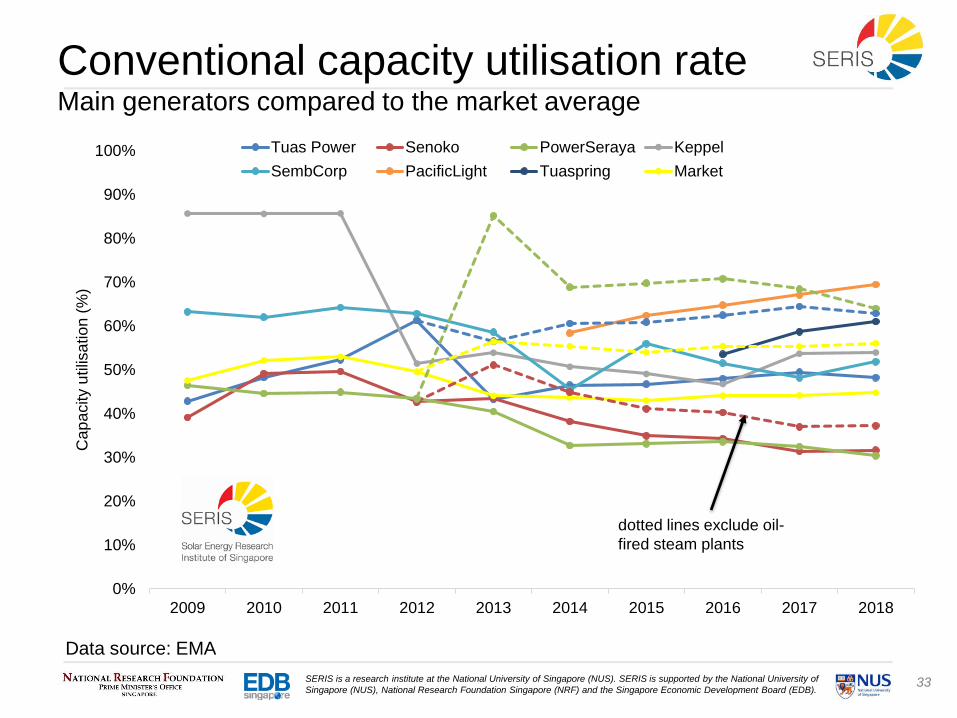

Tuas Power Senoko PowerSeraya Keppel

SembCorp PacificLight Tuaspring Market

Conventional capacity utilisation rateMain generators compared to the market average

Data source: EMA

dotted lines exclude oil-

fired steam plants

34SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

3c) Singapore electricity market: Demand

35SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

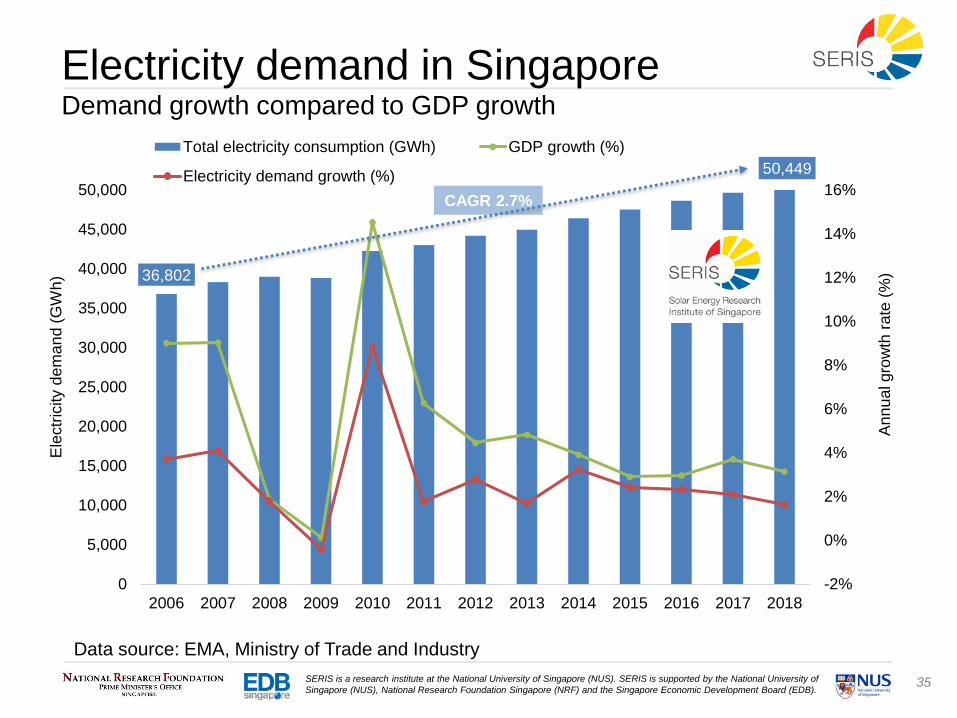

36,802

50,449

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

An

nu

al gro

wth

rate

(%

)

Ele

ctr

icity d

em

an

d (

GW

h)

Total electricity consumption (GWh) GDP growth (%)

Electricity demand growth (%)

Electricity demand in SingaporeDemand growth compared to GDP growth

Data source: EMA, Ministry of Trade and Industry

CAGR 2.7%

36SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

7,200

7,400

7,600

7,800

8,000

8,200

8,400

8,600

8,800

9,000

9,200

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Pe

r ca

pita

(kW

h/y

ea

r)

Ele

ctr

icity d

em

an

d (

GW

h)

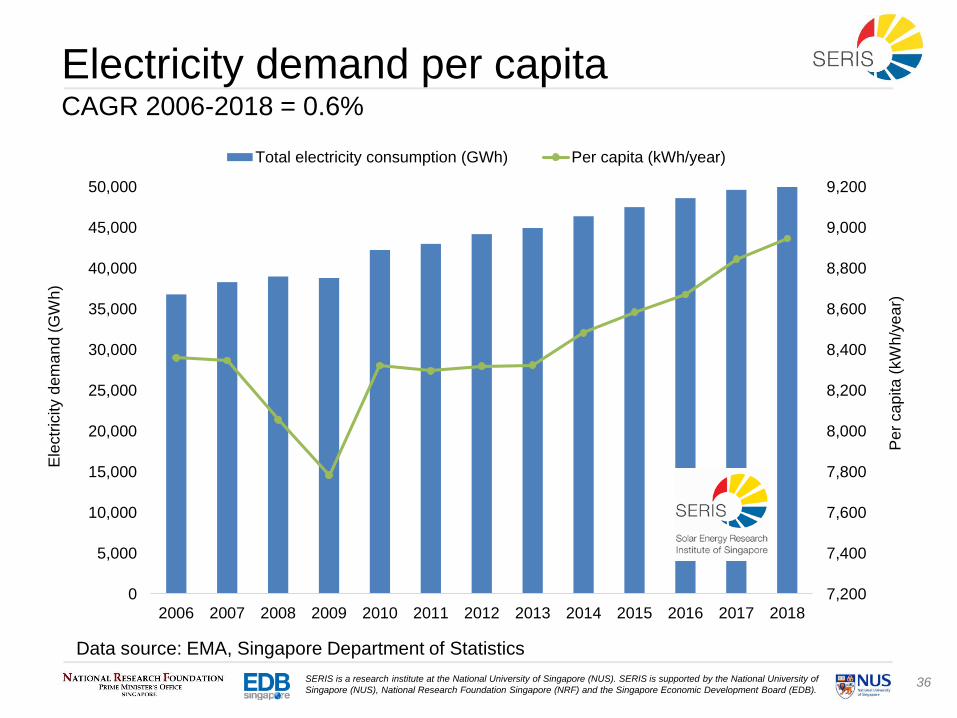

Total electricity consumption (GWh) Per capita (kWh/year)

Electricity demand per capitaCAGR 2006-2018 = 0.6%

Data source: EMA, Singapore Department of Statistics

37SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

10,000

20,000

30,000

40,000

50,000

60,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ele

ctr

icity c

on

su

mp

tio

n (

GW

h)

Industry

Commerce and Services

Transport-related

Households

Others

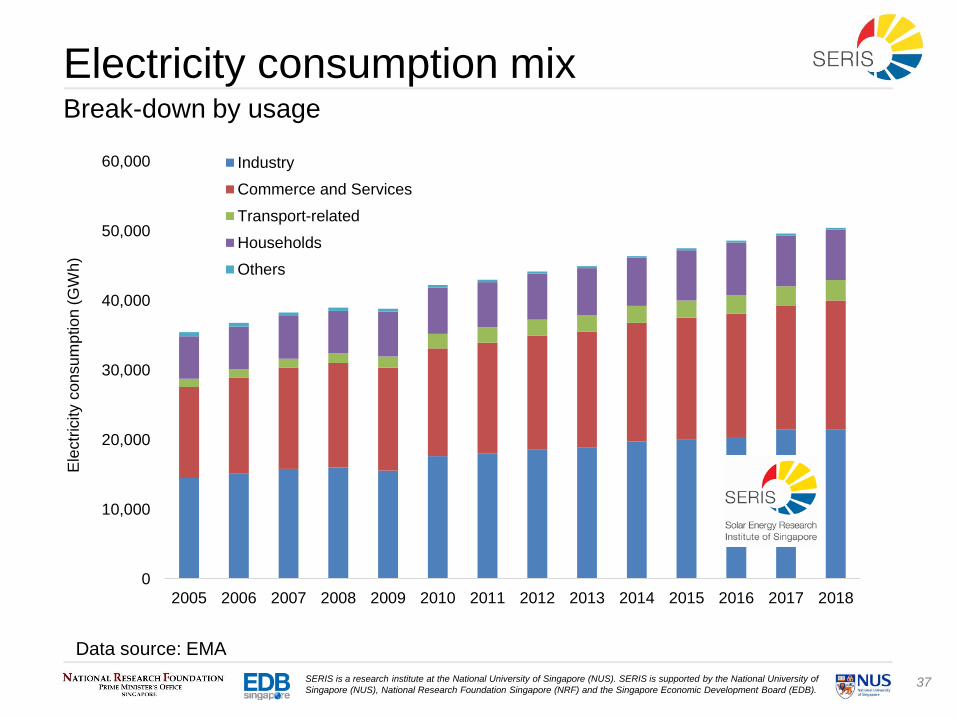

Electricity consumption mixBreak-down by usage

Data source: EMA

38SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

An

nu

al gro

wth

rate

(%

)

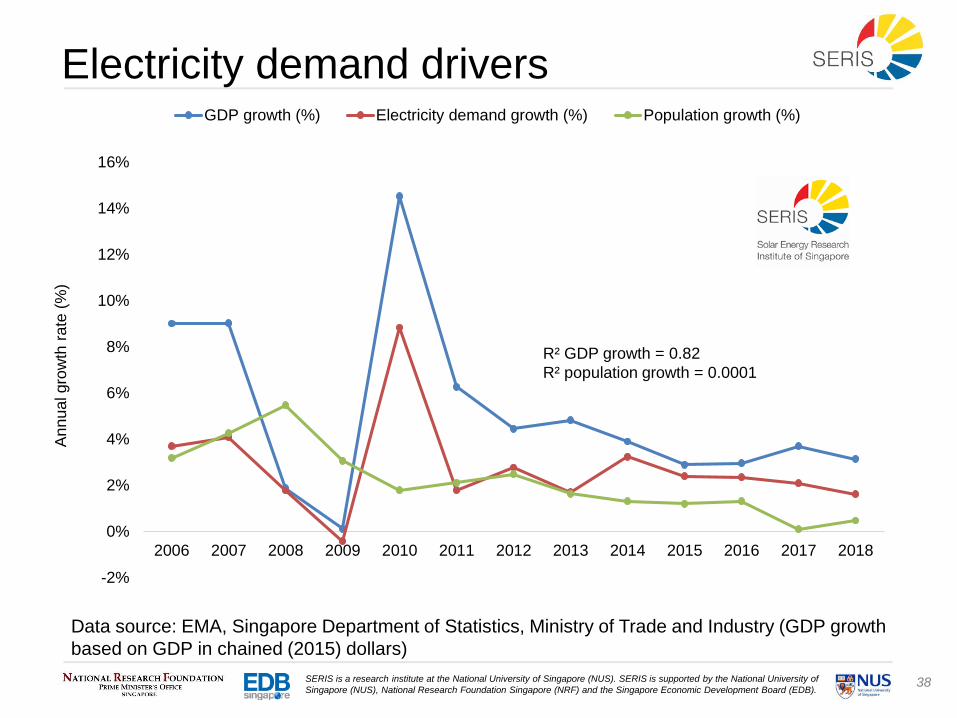

GDP growth (%) Electricity demand growth (%) Population growth (%)

Electricity demand drivers

Data source: EMA, Singapore Department of Statistics, Ministry of Trade and Industry (GDP growth

based on GDP in chained (2015) dollars)

R² GDP growth = 0.82

R² population growth = 0.0001

39SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

4,500

5,000

5,500

6,000

6,500

7,000

7,500

Syste

m d

em

an

d (

MW

)

Mon

Tue

Wed

Thu

Fri

Sat

Sun

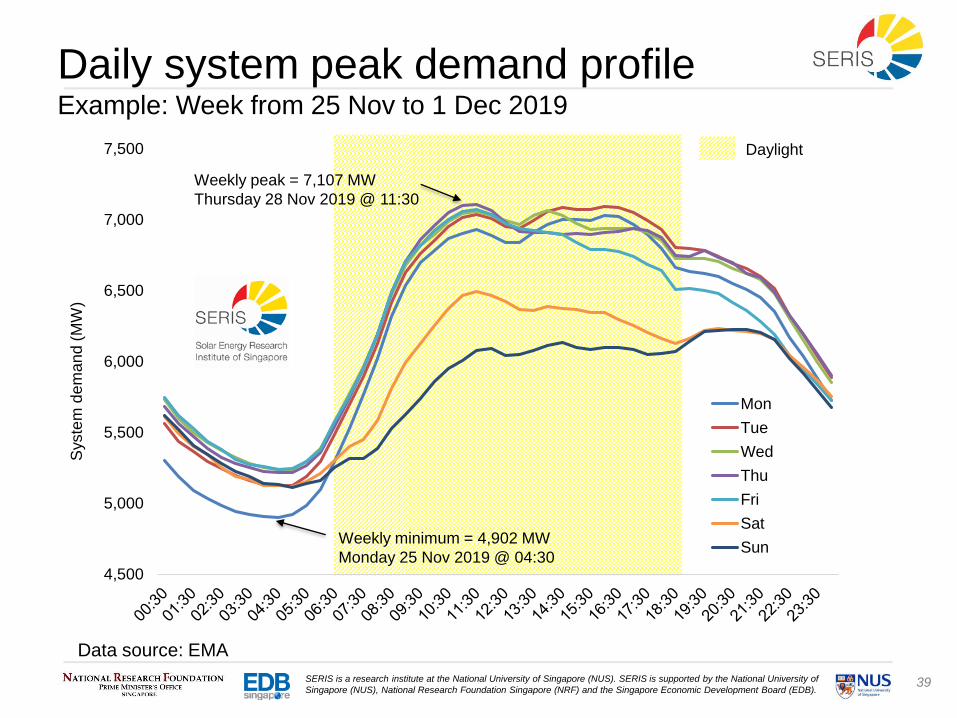

Daily system peak demand profileExample: Week from 25 Nov to 1 Dec 2019

Data source: EMA

Daylight

Weekly peak = 7,107 MW

Thursday 28 Nov 2019 @ 11:30

Weekly minimum = 4,902 MW

Monday 25 Nov 2019 @ 04:30

40SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Historic system peak demand profileNo significant change of daily demand pattern over past eight years

Data source: EMA. Average daily profile for the month of June, excludes weekends/public holidays, the

annual peak happened in different months for 2012 (May), 2016 (August) and 2019 (May)

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

Syste

m p

ea

k d

em

an

d (

MW

)

June 2012

June 2013

June 2014

June 2015

June 2016

June 2017

June 2018

June 2019

Daylight

41SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Pe

ak s

yste

m d

em

an

d (

MW

)

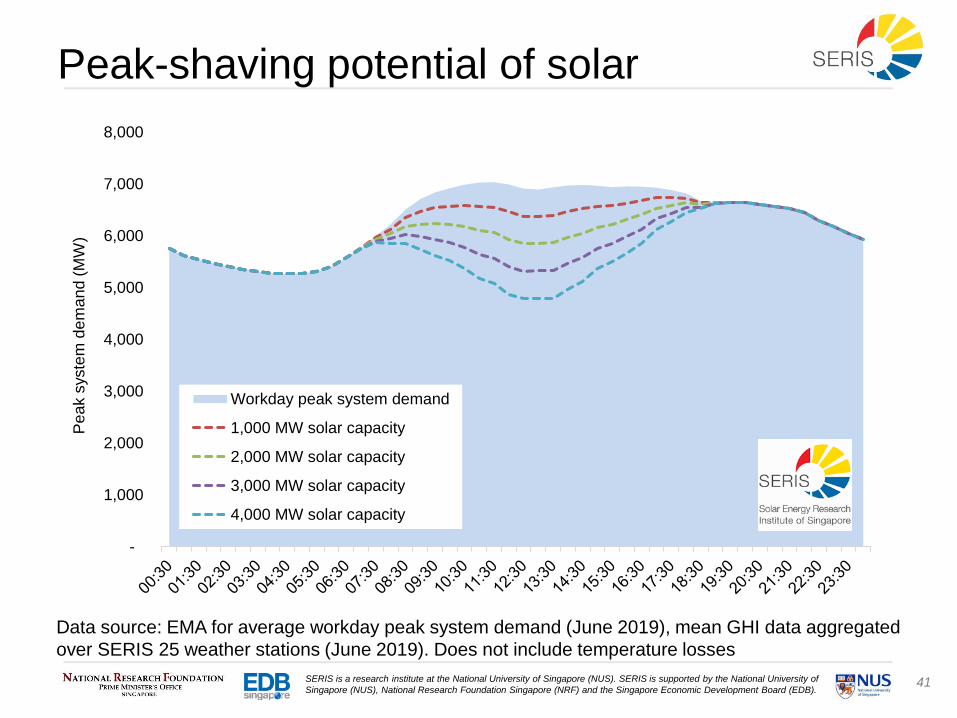

Workday peak system demand

1,000 MW solar capacity

2,000 MW solar capacity

3,000 MW solar capacity

4,000 MW solar capacity

Peak-shaving potential of solar

Data source: EMA for average workday peak system demand (June 2019), mean GHI data aggregated

over SERIS 25 weather stations (June 2019). Does not include temperature losses

42SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

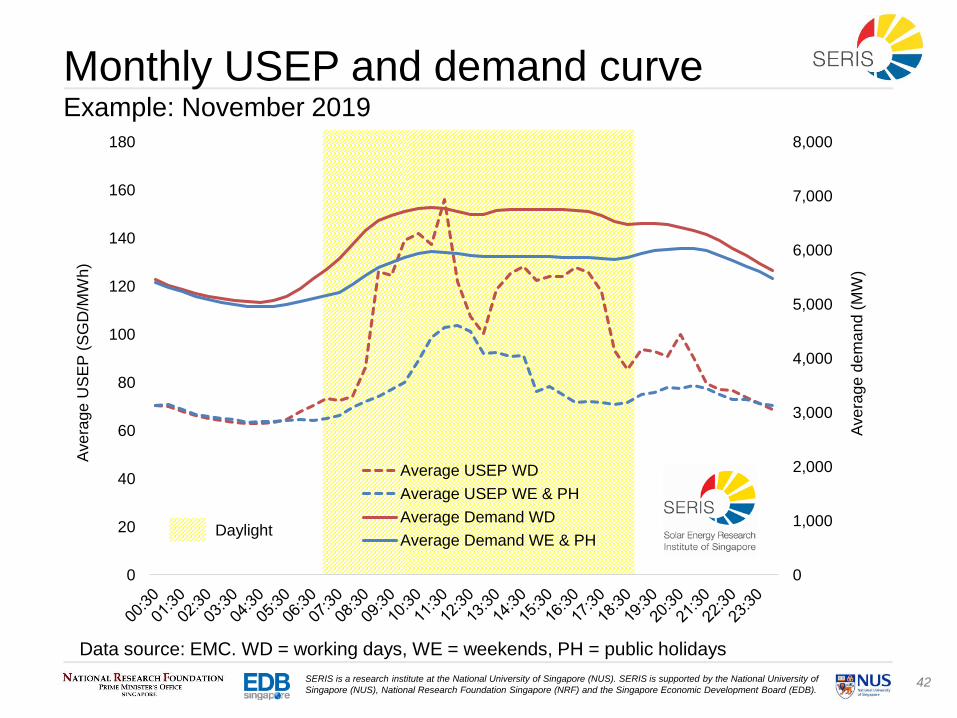

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

20

40

60

80

100

120

140

160

180

Ave

rage

de

ma

nd

(M

W)

Ave

rage

US

EP

(S

GD

/MW

h)

Average USEP WD

Average USEP WE & PH

Average Demand WD

Average Demand WE & PH

Monthly USEP and demand curveExample: November 2019

Data source: EMC. WD = working days, WE = weekends, PH = public holidays

Daylight

43SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

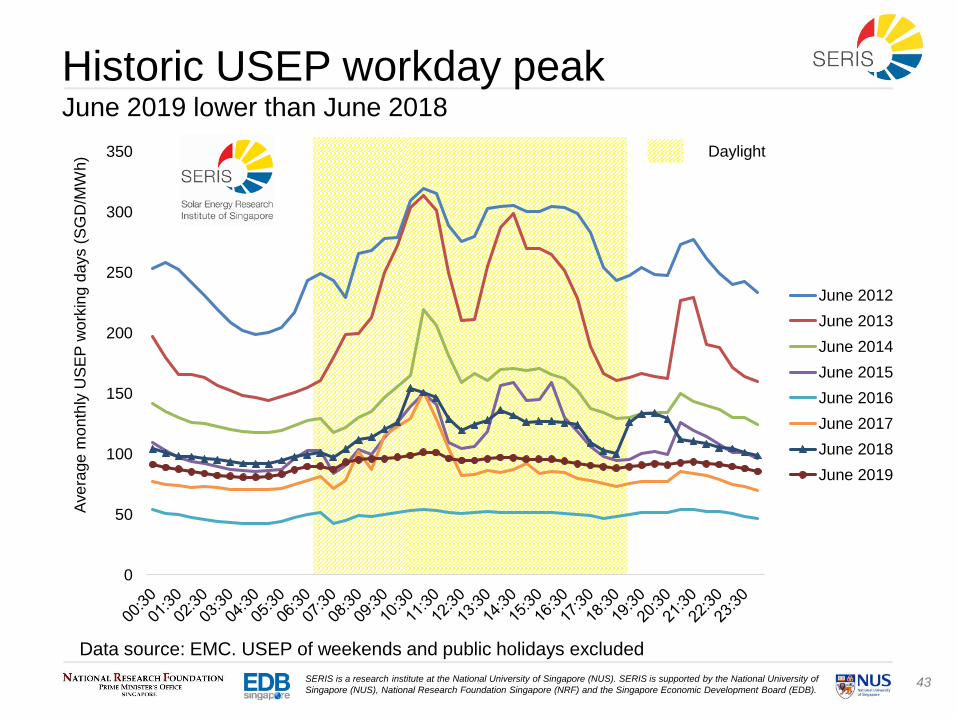

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

50

100

150

200

250

300

350

Ave

rage

mo

nth

ly U

SE

P w

ork

ing d

ays (

SG

D/M

Wh)

June 2012

June 2013

June 2014

June 2015

June 2016

June 2017

June 2018

June 2019

Historic USEP workday peakJune 2019 lower than June 2018

Data source: EMC. USEP of weekends and public holidays excluded

Daylight

44SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

-2%

0%

2%

4%

6%

8%

10%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019*

An

nu

al gro

wth

(%

)

Pe

ak s

yste

m d

em

an

d (

MW

)

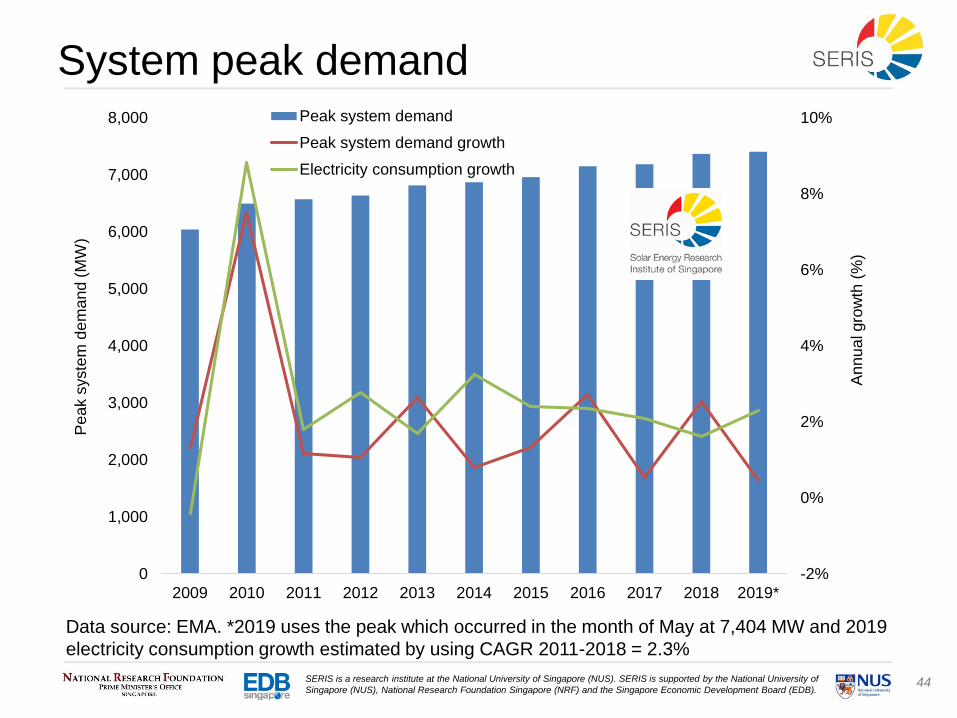

Peak system demand

Peak system demand growth

Electricity consumption growth

System peak demand

Data source: EMA. *2019 uses the peak which occurred in the month of May at 7,404 MW and 2019

electricity consumption growth estimated by using CAGR 2011-2018 = 2.3%

45SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

80%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ma

rke

t sh

are

of

top

3 d

om

ina

nt re

taile

rs (

%)

Ind

ivid

ua

l m

ark

et sh

are

(%

)

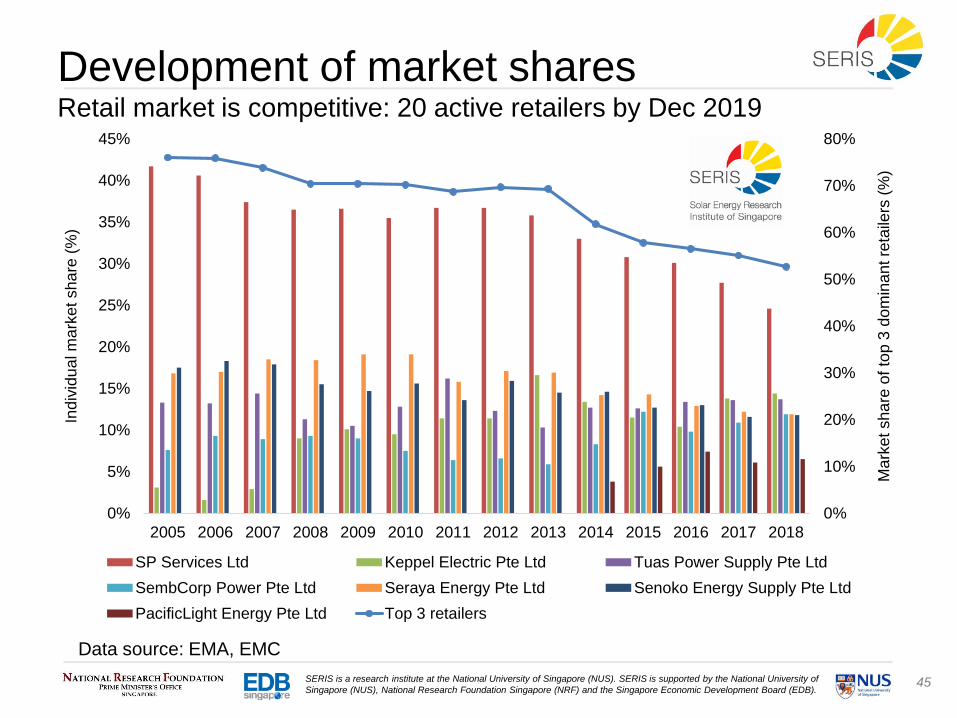

SP Services Ltd Keppel Electric Pte Ltd Tuas Power Supply Pte Ltd

SembCorp Power Pte Ltd Seraya Energy Pte Ltd Senoko Energy Supply Pte Ltd

PacificLight Energy Pte Ltd Top 3 retailers

Development of market sharesRetail market is competitive: 20 active retailers by Dec 2019

Data source: EMA, EMC

46SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

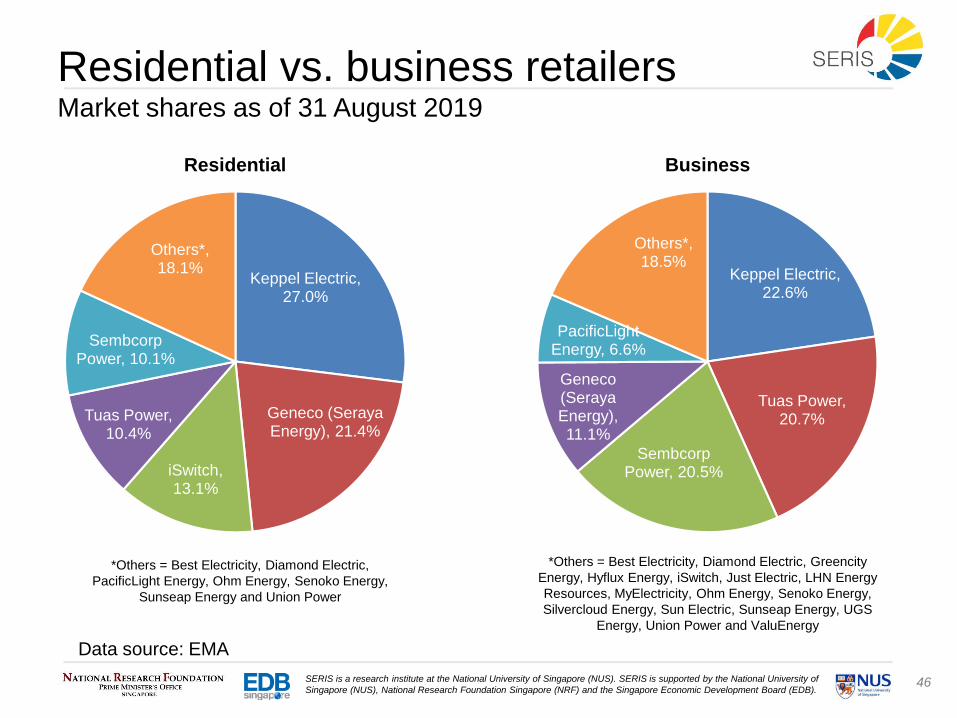

Residential vs. business retailersMarket shares as of 31 August 2019

Data source: EMA

Keppel Electric, 27.0%

Geneco (Seraya Energy), 21.4%

iSwitch, 13.1%

Tuas Power, 10.4%

Sembcorp Power, 10.1%

Others*, 18.1%

Residential

Keppel Electric, 22.6%

Tuas Power, 20.7%

Sembcorp Power, 20.5%

Geneco (Seraya Energy), 11.1%

PacificLight Energy, 6.6%

Others*, 18.5%

Business

*Others = Best Electricity, Diamond Electric,

PacificLight Energy, Ohm Energy, Senoko Energy,

Sunseap Energy and Union Power

*Others = Best Electricity, Diamond Electric, Greencity

Energy, Hyflux Energy, iSwitch, Just Electric, LHN Energy

Resources, MyElectricity, Ohm Energy, Senoko Energy,

Silvercloud Energy, Sun Electric, Sunseap Energy, UGS

Energy, Union Power and ValuEnergy

47SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

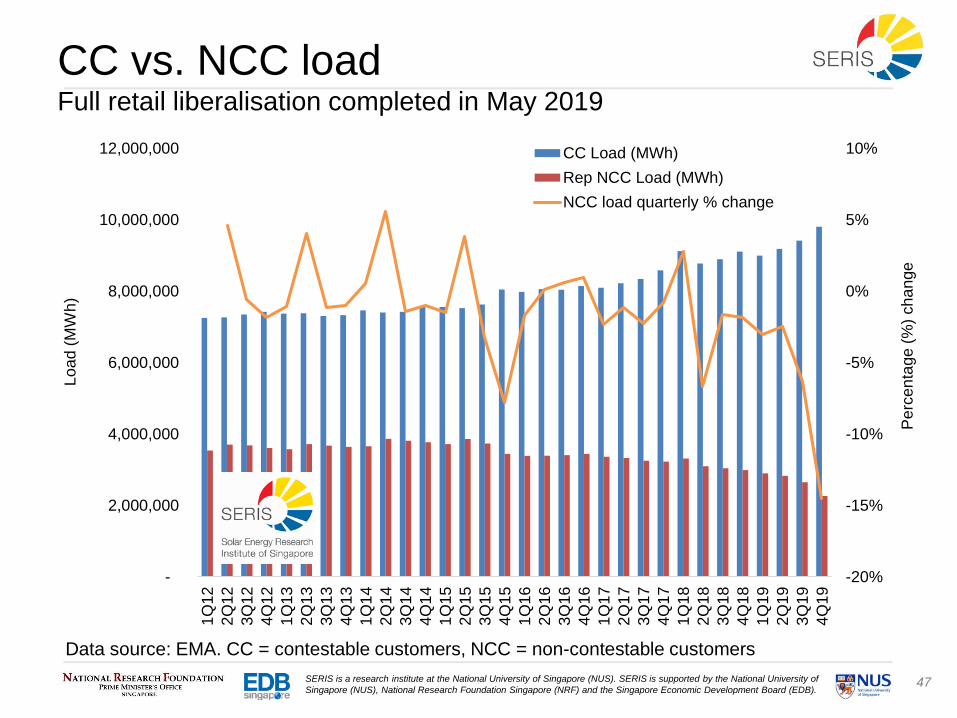

CC vs. NCC loadFull retail liberalisation completed in May 2019

Data source: EMA. CC = contestable customers, NCC = non-contestable customers

-20%

-15%

-10%

-5%

0%

5%

10%

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

Pe

rcen

tage

(%

) ch

an

ge

Lo

ad

(M

Wh

)

CC Load (MWh)

Rep NCC Load (MWh)

NCC load quarterly % change

48SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

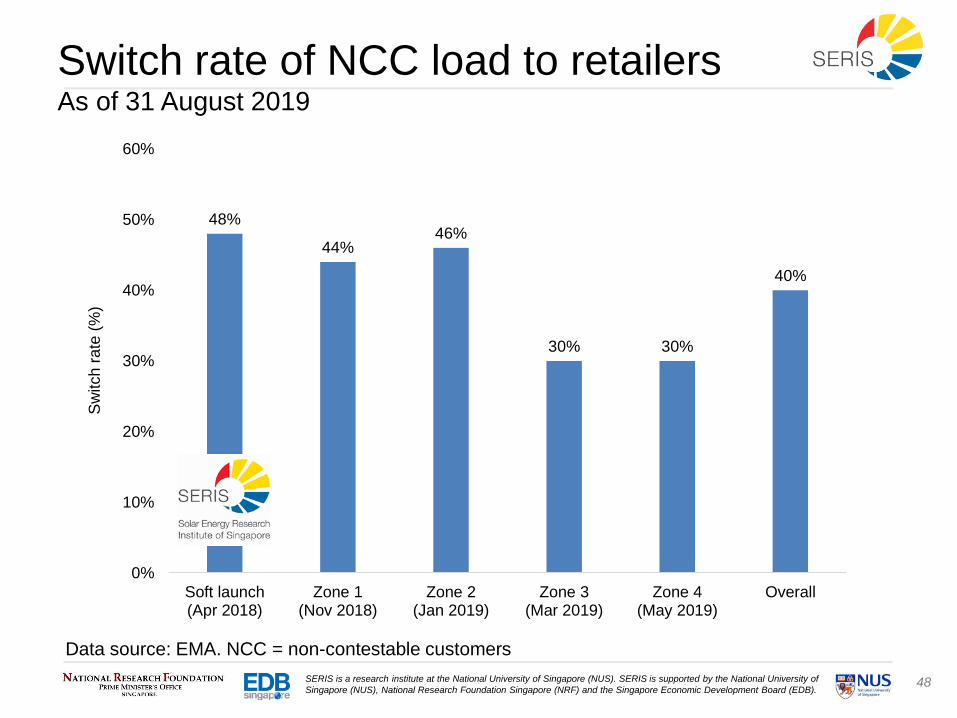

48%

44%46%

30% 30%

40%

0%

10%

20%

30%

40%

50%

60%

Soft launch(Apr 2018)

Zone 1(Nov 2018)

Zone 2(Jan 2019)

Zone 3(Mar 2019)

Zone 4(May 2019)

Overall

Sw

itch

ra

te (

%)

Switch rate of NCC load to retailersAs of 31 August 2019

Data source: EMA. NCC = non-contestable customers

49SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

3d) Singapore electricity market: Prices

50SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

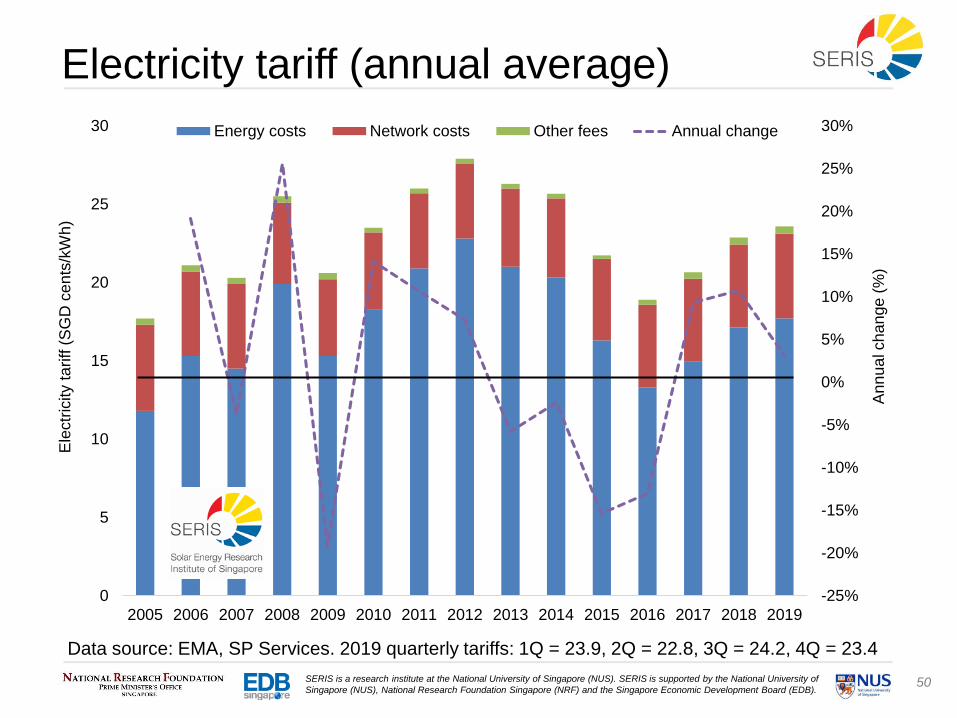

Electricity tariff (annual average)

Data source: EMA, SP Services. 2019 quarterly tariffs: 1Q = 23.9, 2Q = 22.8, 3Q = 24.2, 4Q = 23.4

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

An

nu

al ch

an

ge

(%

)

Ele

ctr

icity t

ariff

(S

GD

ce

nts

/kW

h)

Energy costs Network costs Other fees Annual change

51SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

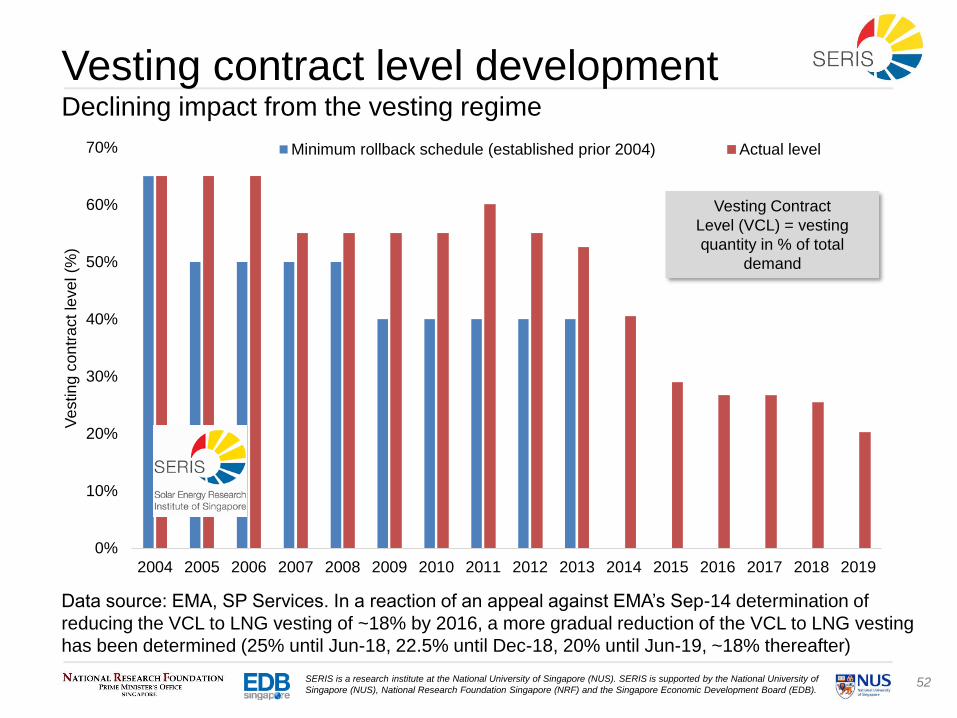

Vesting contractsA unique feature of the Singaporean power market

Implemented in Jan-2004 as a regulatory instrument to mitigate

market power by the generation companies (gencos)*

Commits gencos to sell a specified quantity (i.e. the Vesting Contract

Level, VCL) for a specified price (i.e. the Vesting Price, VP)

A 10-year LNG vesting scheme was introduced in May-13 to

encourage the uptake of regasified LNG whereas eligible gencos

receive the LNG vesting price for a specified LNG vesting quantity

Vesting prices (one for piped gas and one for regasified LNG gas)

are based on a regulatory review done every 24 months and are

updated quarterly based on fuel cost and cost inflation changes

Vesting prices mirror the long run marginal cost (LRMC, i.e. variable

and fixed operating cost including reasonable return to investors) of

the most efficiency power plant in Singapore (currently combined

cycle gas turbines, CCGTs)

*Mandatory for Senoko Energy, PowerSeraya, Tuas Power, SembCorp, Keppel and PacificLight

Data source: EMA

52SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0%

10%

20%

30%

40%

50%

60%

70%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Ve

stin

g c

on

tra

ct le

ve

l (%

)

Minimum rollback schedule (established prior 2004) Actual level

Vesting contract level developmentDeclining impact from the vesting regime

Data source: EMA, SP Services. In a reaction of an appeal against EMA’s Sep-14 determination of

reducing the VCL to LNG vesting of ~18% by 2016, a more gradual reduction of the VCL to LNG vesting

has been determined (25% until Jun-18, 22.5% until Dec-18, 20% until Jun-19, ~18% thereafter)

Vesting Contract

Level (VCL) = vesting

quantity in % of total

demand

53SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

20

40

60

80

100

120

140

160

180

0

2

4

6

8

10

12

14

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

Ve

stin

g c

on

tra

ct le

ve

l (%

)

Ve

stin

g q

ua

ntity

, d

em

an

d (

TW

h)

Balance VQ (TWh) LNG VQ (TWh)CC Load (TWh) Non-CC Load (TWh)VQ in % of total demand VQ in % of NCC demand

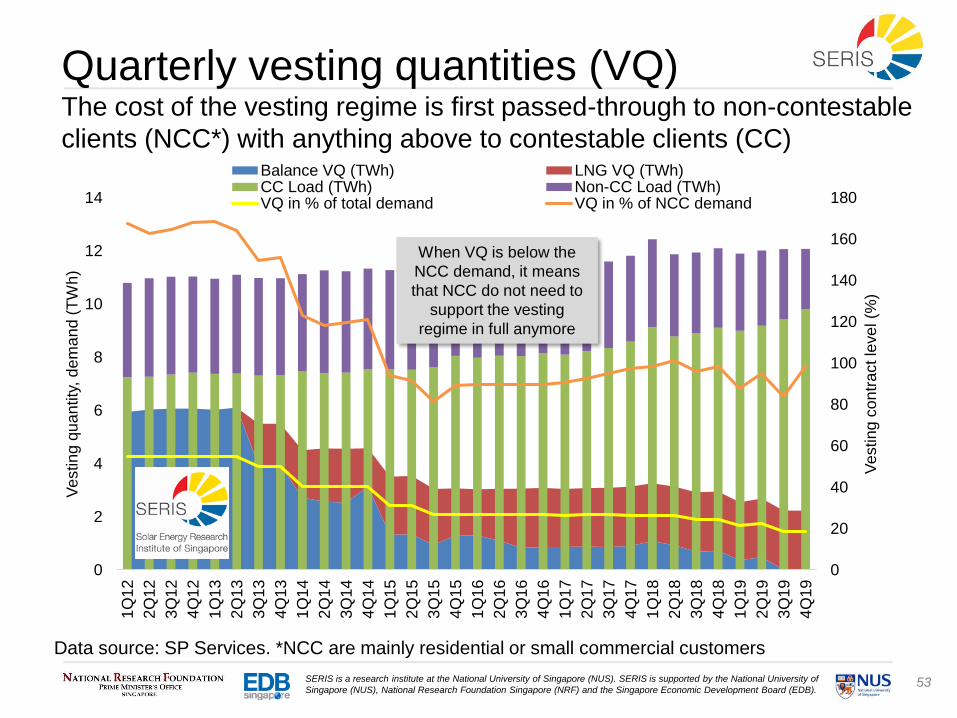

Quarterly vesting quantities (VQ)The cost of the vesting regime is first passed-through to non-contestable

clients (NCC*) with anything above to contestable clients (CC)

Data source: SP Services. *NCC are mainly residential or small commercial customers

When VQ is below the

NCC demand, it means

that NCC do not need to

support the vesting

regime in full anymore

54SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

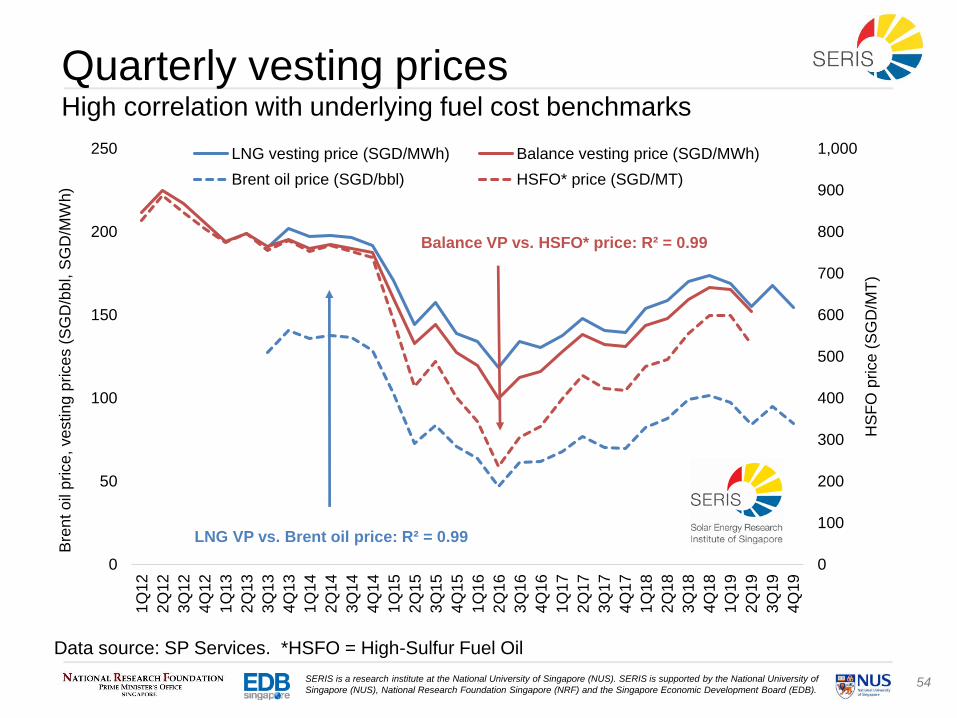

Quarterly vesting pricesHigh correlation with underlying fuel cost benchmarks

Data source: SP Services. *HSFO = High-Sulfur Fuel Oil

0

100

200

300

400

500

600

700

800

900

1,000

0

50

100

150

200

2501

Q1

2

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

HS

FO

price

(S

GD

/MT

)

Bre

nt o

il p

rice

, ve

stin

g p

rice

s (

SG

D/b

bl, S

GD

/MW

h)

LNG vesting price (SGD/MWh) Balance vesting price (SGD/MWh)

Brent oil price (SGD/bbl) HSFO* price (SGD/MT)

Balance VP vs. HSFO* price: R² = 0.99

LNG VP vs. Brent oil price: R² = 0.99

55SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

20

40

60

80

100

120

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019*

Bre

nt o

il p

rice

(U

SD

/bb

l)

Ele

ctr

icity p

rice

s (

SG

D c

en

ts/k

Wh

)

Electricity tariff

Contestable client average price

USEP

Brent oil price

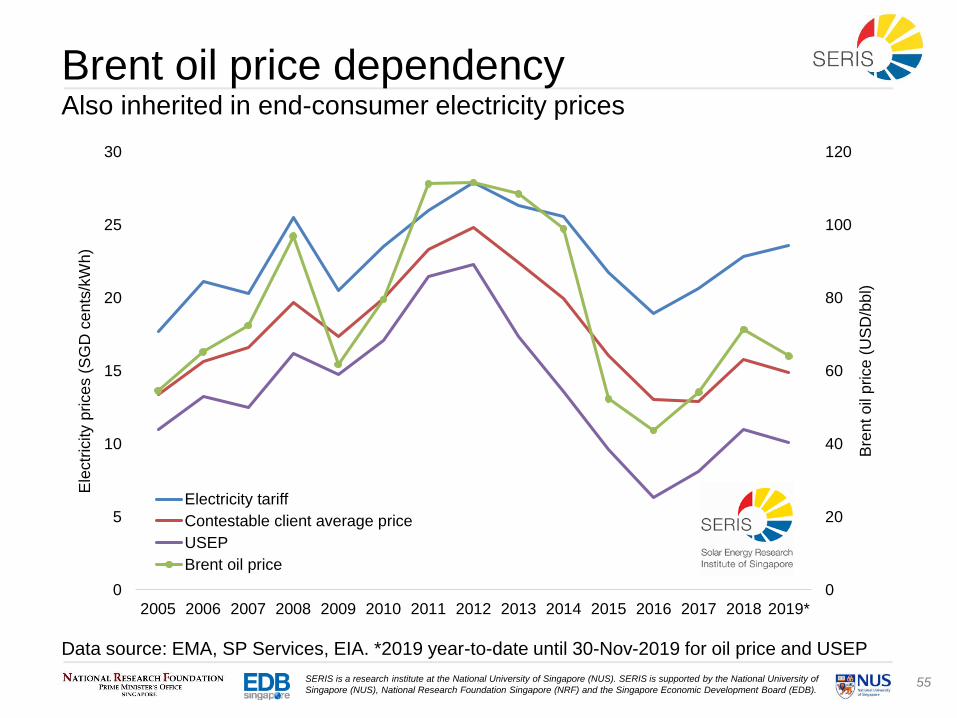

Brent oil price dependency Also inherited in end-consumer electricity prices

Data source: EMA, SP Services, EIA. *2019 year-to-date until 30-Nov-2019 for oil price and USEP

56SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

100

200

300

400

500

600

700

800

0

5

10

15

20

25

30

35

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

Fu

el o

il p

rice

s (

US

D/M

T)

Ele

ctr

icity p

rice

s (

SG

D c

en

ts/k

Wh

)

Wholesale Price (USEP) Contestable Average Rate

Electricity Tariff (residential)* Vesting Price (piped gas)

Vesting Price (LNG) Forward Fuel Oil Price

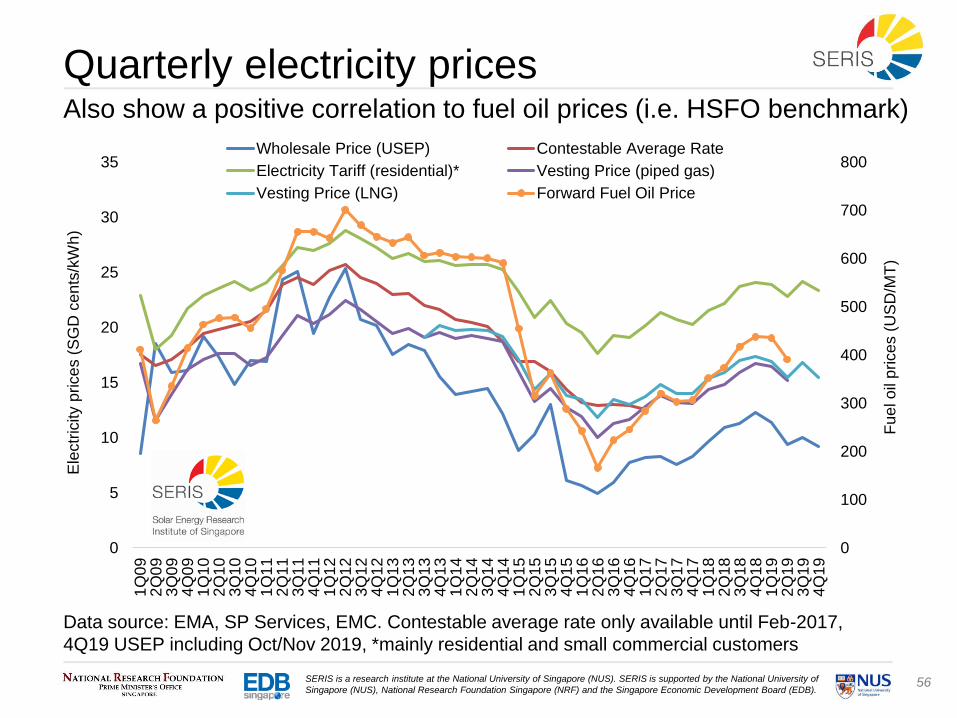

Quarterly electricity pricesAlso show a positive correlation to fuel oil prices (i.e. HSFO benchmark)

Data source: EMA, SP Services, EMC. Contestable average rate only available until Feb-2017,

4Q19 USEP including Oct/Nov 2019, *mainly residential and small commercial customers

57SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

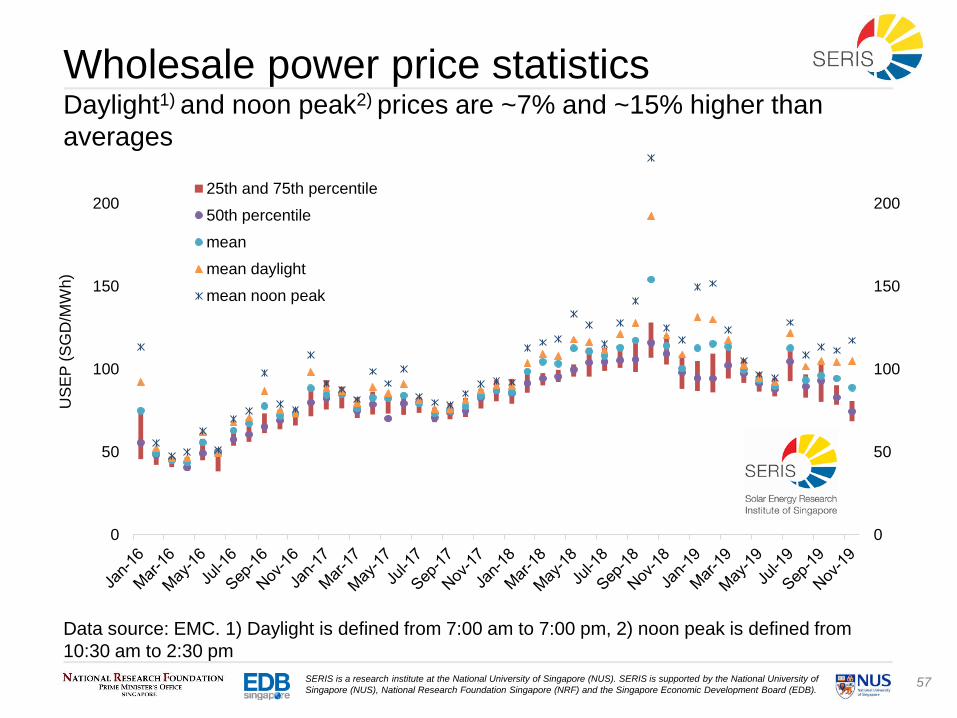

Wholesale power price statisticsDaylight1) and noon peak2) prices are ~7% and ~15% higher than

averages

Data source: EMC. 1) Daylight is defined from 7:00 am to 7:00 pm, 2) noon peak is defined from

10:30 am to 2:30 pm

0

50

100

150

200

0

50

100

150

200

US

EP

(S

GD

/MW

h)

25th and 75th percentile

50th percentile

mean

mean daylight

mean noon peak

58SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

4. PV adoption in Singapore

59SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

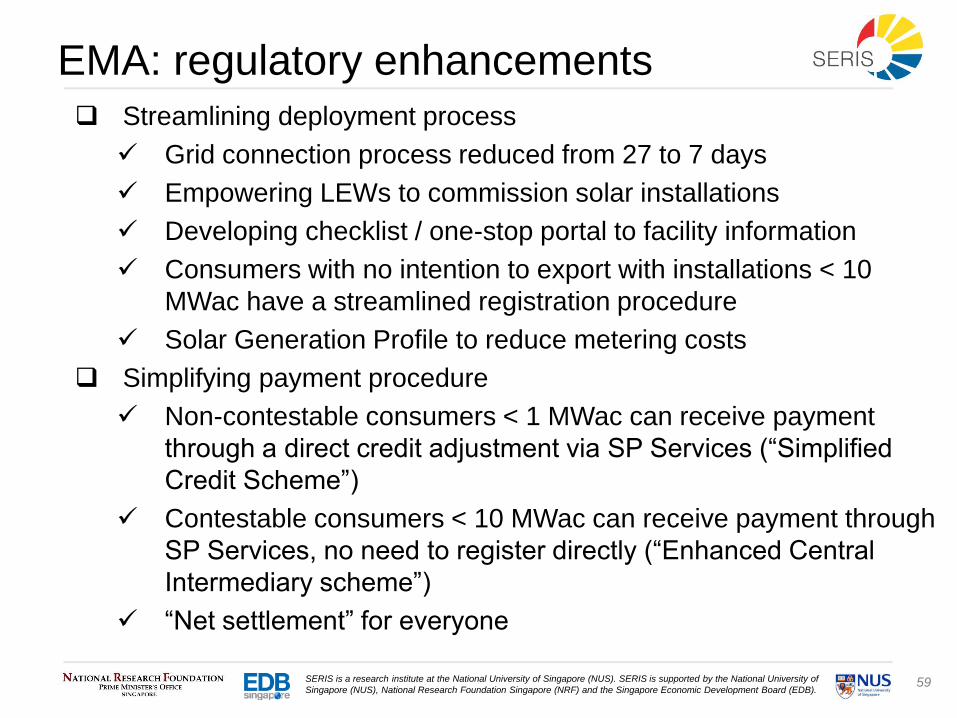

EMA: regulatory enhancements

Streamlining deployment process

Grid connection process reduced from 27 to 7 days

Empowering LEWs to commission solar installations

Developing checklist / one-stop portal to facility information

Consumers with no intention to export with installations < 10

MWac have a streamlined registration procedure

Solar Generation Profile to reduce metering costs

Simplifying payment procedure

Non-contestable consumers < 1 MWac can receive payment

through a direct credit adjustment via SP Services (“Simplified

Credit Scheme”)

Contestable consumers < 10 MWac can receive payment through

SP Services, no need to register directly (“Enhanced Central

Intermediary scheme”)

“Net settlement” for everyone

60SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

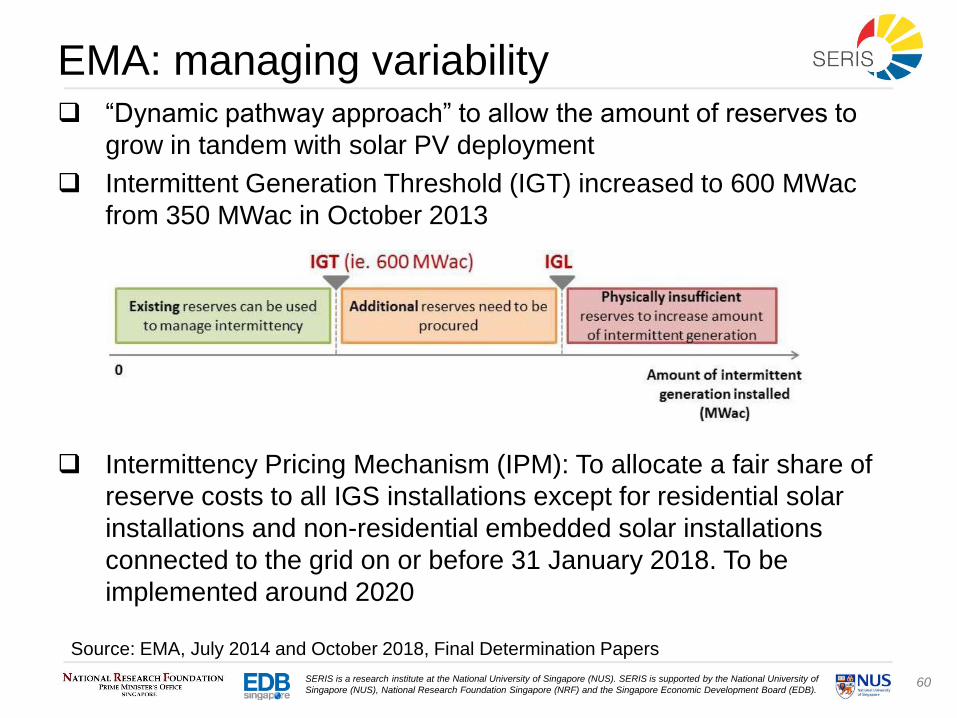

EMA: managing variability “Dynamic pathway approach” to allow the amount of reserves to

grow in tandem with solar PV deployment

Intermittent Generation Threshold (IGT) increased to 600 MWac

from 350 MWac in October 2013

Intermittency Pricing Mechanism (IPM): To allocate a fair share of

reserve costs to all IGS installations except for residential solar

installations and non-residential embedded solar installations

connected to the grid on or before 31 January 2018. To be

implemented around 2020

Source: EMA, July 2014 and October 2018, Final Determination Papers

61SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

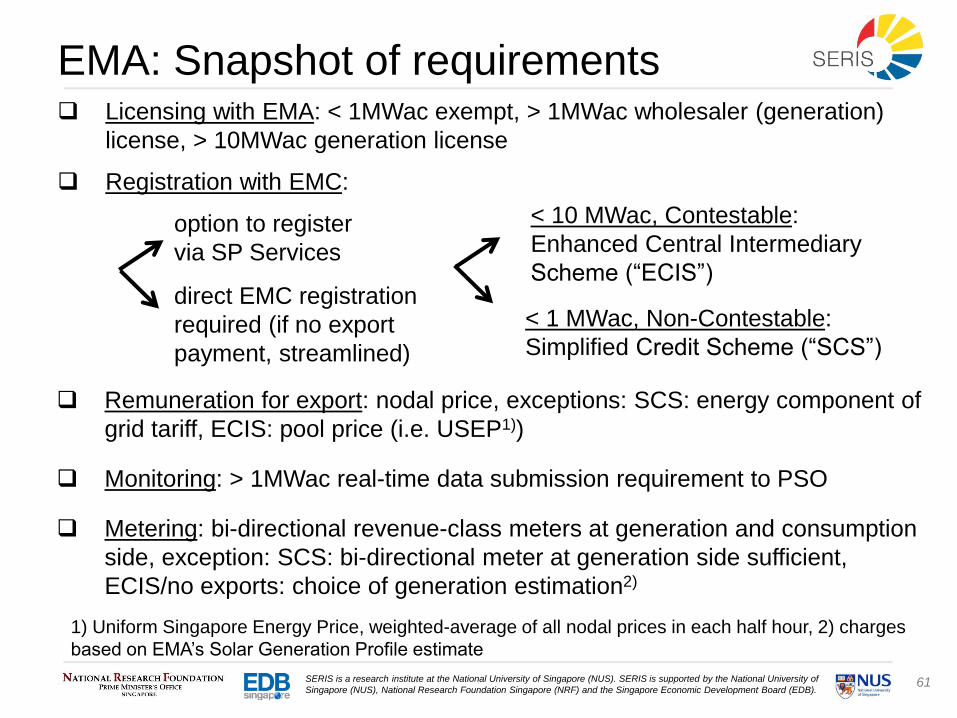

EMA: Snapshot of requirements Licensing with EMA: < 1MWac exempt, > 1MWac wholesaler (generation)

license, > 10MWac generation license

Registration with EMC:

option to register

via SP Services

direct EMC registration

required (if no export

payment, streamlined)

< 10 MWac, Contestable:

Enhanced Central Intermediary

Scheme (“ECIS”)

< 1 MWac, Non-Contestable:

Simplified Credit Scheme (“SCS”)

Remuneration for export: nodal price, exceptions: SCS: energy component of

grid tariff, ECIS: pool price (i.e. USEP1))

Monitoring: > 1MWac real-time data submission requirement to PSO

Metering: bi-directional revenue-class meters at generation and consumption

side, exception: SCS: bi-directional meter at generation side sufficient,

ECIS/no exports: choice of generation estimation2)

1) Uniform Singapore Energy Price, weighted-average of all nodal prices in each half hour, 2) charges

based on EMA’s Solar Generation Profile estimate

62SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

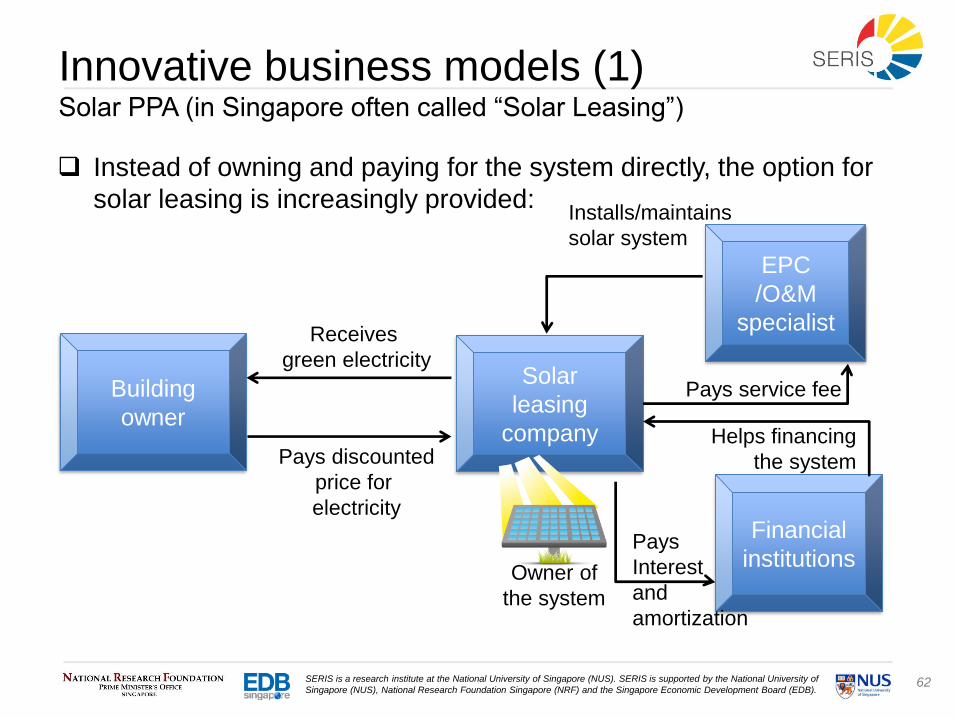

Innovative business models (1)Solar PPA (in Singapore often called “Solar Leasing”)

Instead of owning and paying for the system directly, the option for

solar leasing is increasingly provided:

Building

owner

Solar

leasing

company

EPC

/O&M

specialist

Financial

institutions

Receives

green electricity

Pays discounted

price for

electricity

Owner of

the system

Installs/maintains

solar system

Helps financing

the system

Pays

Interest

and

amortization

Pays service fee

63SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

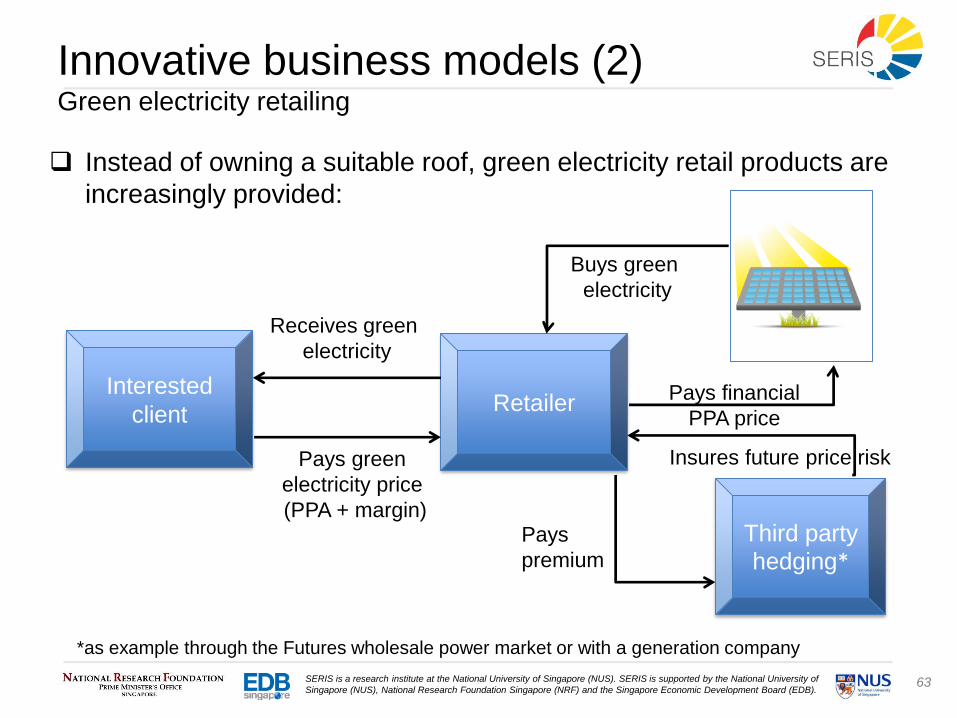

Innovative business models (2)Green electricity retailing

Instead of owning a suitable roof, green electricity retail products are

increasingly provided:

Interested

clientRetailer

Third party

hedging*

Receives green

electricity

Pays green

electricity price

(PPA + margin)

Buys green

electricity

Pays financial

PPA price

*as example through the Futures wholesale power market or with a generation company

Insures future price risk

Pays

premium

64SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

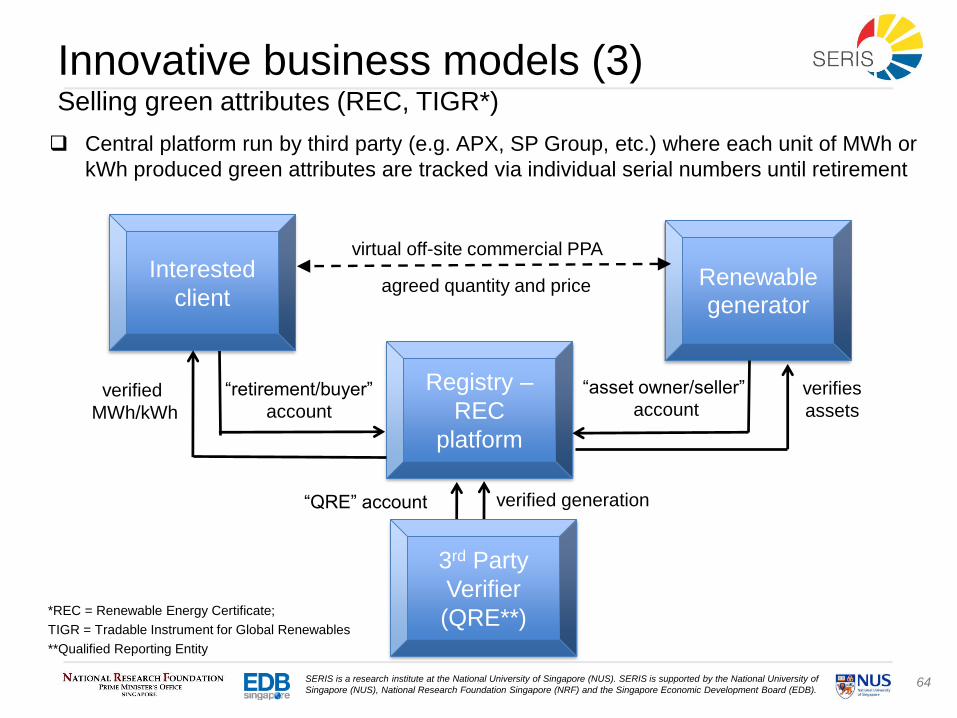

Innovative business models (3)Selling green attributes (REC, TIGR*)

Central platform run by third party (e.g. APX, SP Group, etc.) where each unit of MWh or

kWh produced green attributes are tracked via individual serial numbers until retirement

Interested

client

Registry –

REC

platform

Renewable

generator

virtual off-site commercial PPA

“retirement/buyer”

account

*REC = Renewable Energy Certificate;

TIGR = Tradable Instrument for Global Renewables

**Qualified Reporting Entity

agreed quantity and price

verifies

assets

3rd Party

Verifier

(QRE**)

“asset owner/seller”

accountverified

MWh/kWh

verified generation“QRE” account

65SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

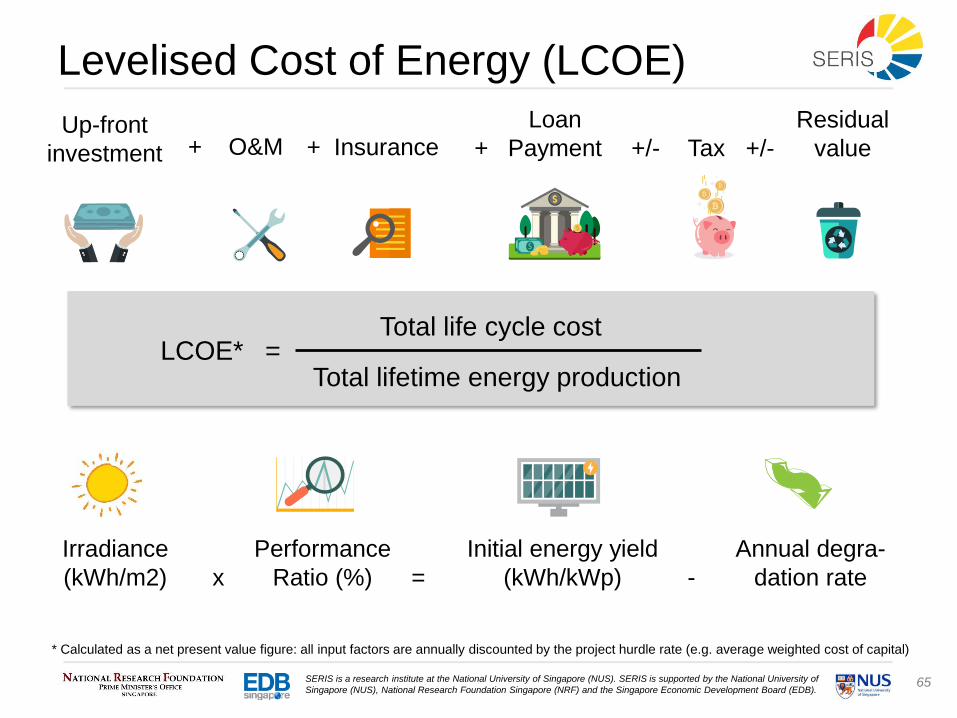

Levelised Cost of Energy (LCOE)

Total life cycle cost

Total lifetime energy productionLCOE* =

Up-front

investment

Irradiance

(kWh/m2) x

* Calculated as a net present value figure: all input factors are annually discounted by the project hurdle rate (e.g. average weighted cost of capital)

+ O&M +

Loan

Payment +/- Tax +/-

Residual

value+ Insurance

-

Annual degra-

dation rate

Initial energy yield

(kWh/kWp)

Performance

Ratio (%) =

66SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

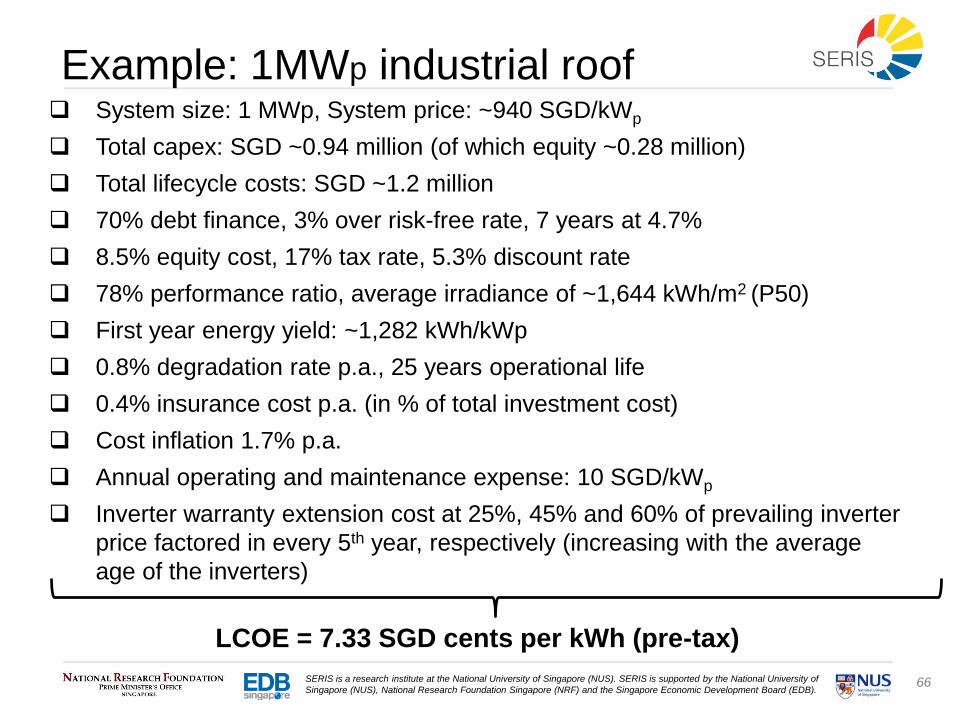

System size: 1 MWp, System price: ~940 SGD/kWp

Total capex: SGD ~0.94 million (of which equity ~0.28 million)

Total lifecycle costs: SGD ~1.2 million

70% debt finance, 3% over risk-free rate, 7 years at 4.7%

8.5% equity cost, 17% tax rate, 5.3% discount rate

78% performance ratio, average irradiance of ~1,644 kWh/m2 (P50)

First year energy yield: ~1,282 kWh/kWp

0.8% degradation rate p.a., 25 years operational life

0.4% insurance cost p.a. (in % of total investment cost)

Cost inflation 1.7% p.a.

Annual operating and maintenance expense: 10 SGD/kWp

Inverter warranty extension cost at 25%, 45% and 60% of prevailing inverter

price factored in every 5th year, respectively (increasing with the average

age of the inverters)

LCOE = 7.33 SGD cents per kWh (pre-tax)

Example: 1MWp industrial roof

67SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

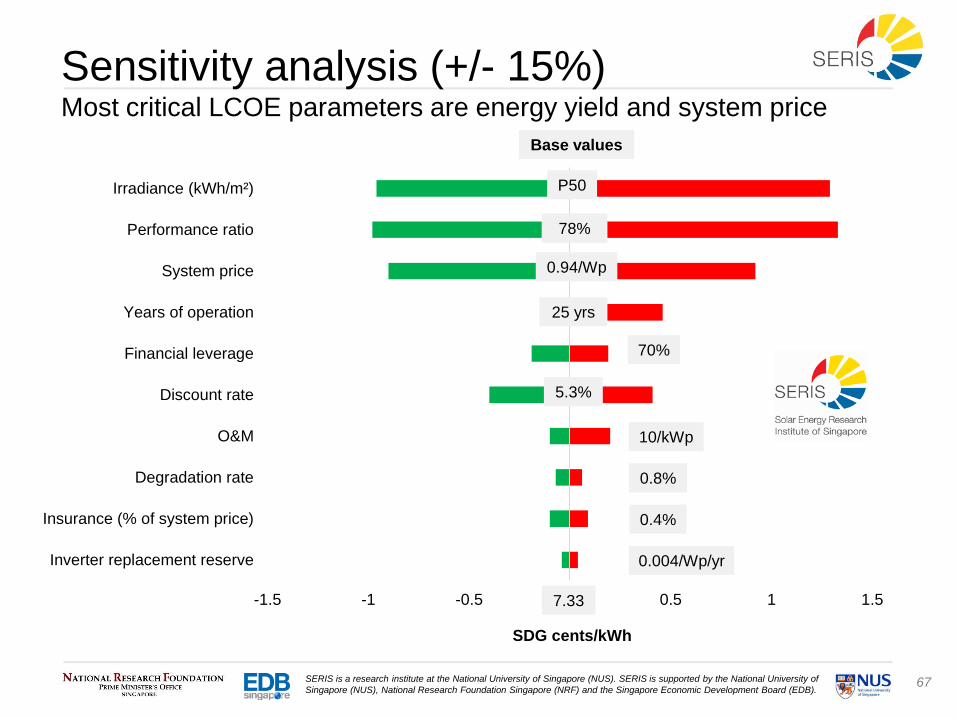

Sensitivity analysis (+/- 15%)Most critical LCOE parameters are energy yield and system price

-1.5 -1 -0.5 0 0.5 1 1.5

Irradiance (kWh/m²)

Performance ratio

System price

Years of operation

Financial leverage

Discount rate

O&M

Degradation rate

Insurance (% of system price)

Inverter replacement reserve

7.33

Base values

SDG cents/kWh

P50

78%

0.94/Wp

25 yrs

70%

5.3%

0.8%

0.4%

0.004/Wp/yr

10/kWp

68SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

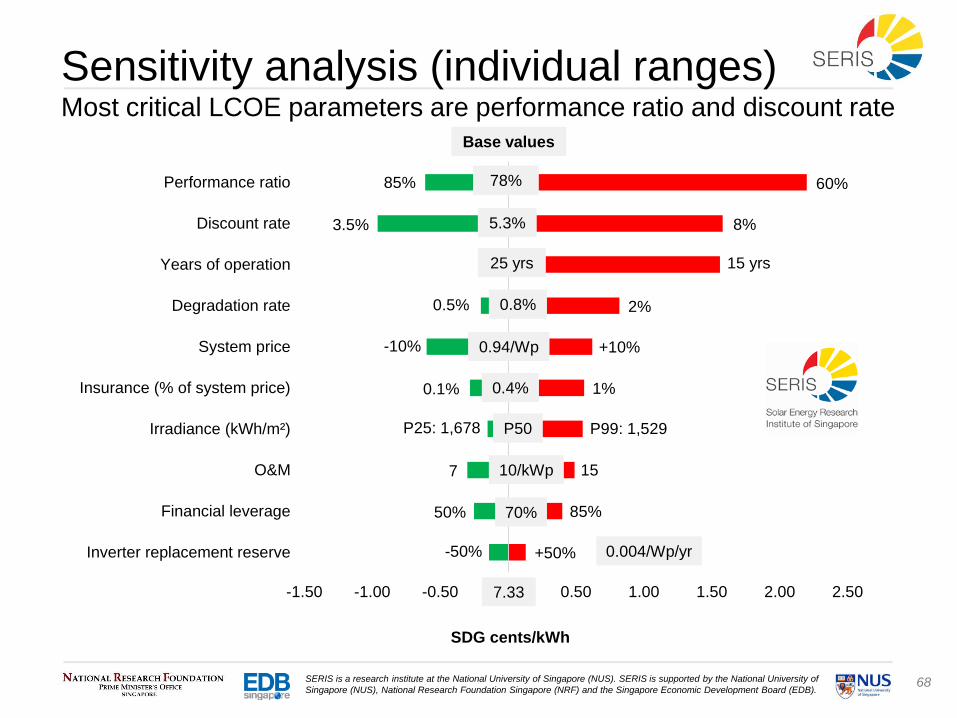

Sensitivity analysis (individual ranges)Most critical LCOE parameters are performance ratio and discount rate

-1.50 -1.00 -0.50 0.00 0.50 1.00 1.50 2.00 2.50

Performance ratio

Discount rate

Years of operation

Degradation rate

System price

Insurance (% of system price)

Irradiance (kWh/m²)

O&M

Financial leverage

Inverter replacement reserve

2%

SDG cents/kWh

Base values

7.33

P50

78%

0.94/Wp

25 yrs

70%

5.3%

0.8%

0.4%

0.004/Wp/yr

10/kWp

60%85%

3.5% 8%

-10%

0.5%

15 yrs

P25: 1,678

1%0.1%

+10%

157

P99: 1,529

85%

-50% +50%

50%

69SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

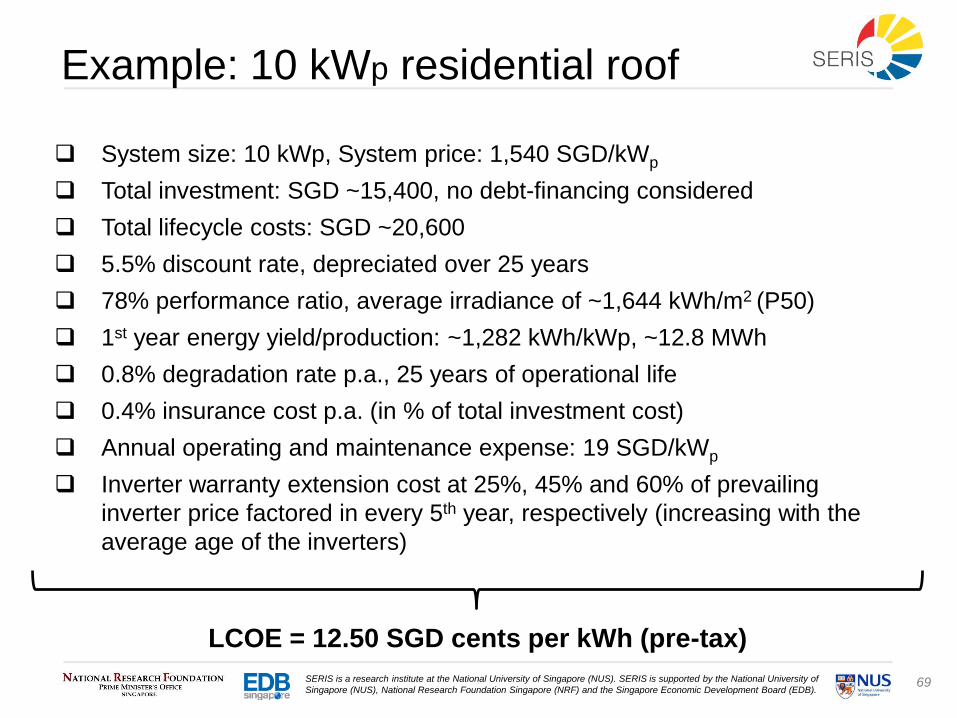

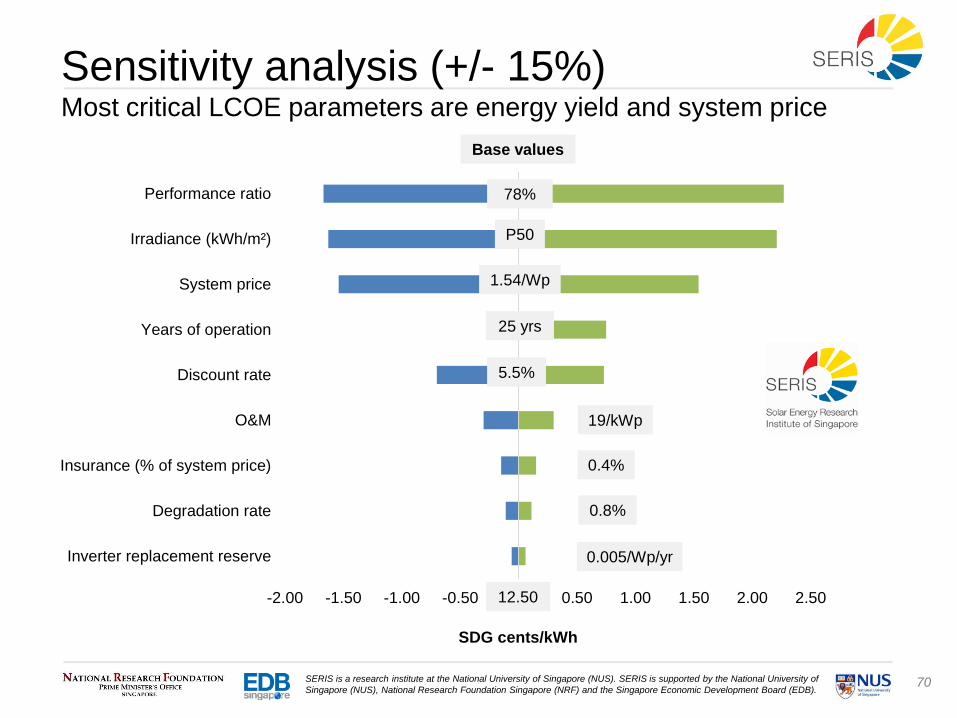

System size: 10 kWp, System price: 1,540 SGD/kWp

Total investment: SGD ~15,400, no debt-financing considered

Total lifecycle costs: SGD ~20,600

5.5% discount rate, depreciated over 25 years

78% performance ratio, average irradiance of ~1,644 kWh/m2 (P50)

1st year energy yield/production: ~1,282 kWh/kWp, ~12.8 MWh

0.8% degradation rate p.a., 25 years of operational life

0.4% insurance cost p.a. (in % of total investment cost)

Annual operating and maintenance expense: 19 SGD/kWp

Inverter warranty extension cost at 25%, 45% and 60% of prevailing

inverter price factored in every 5th year, respectively (increasing with the

average age of the inverters)

LCOE = 12.50 SGD cents per kWh (pre-tax)

Example: 10 kWp residential roof

70SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Sensitivity analysis (+/- 15%)Most critical LCOE parameters are energy yield and system price

-2.00 -1.50 -1.00 -0.50 0.00 0.50 1.00 1.50 2.00 2.50

Performance ratio

Irradiance (kWh/m²)

System price

Years of operation

Discount rate

O&M

Insurance (% of system price)

Degradation rate

Inverter replacement reserve

Base values

SDG cents/kWh

12.50

P50

78%

1.54/Wp

25 yrs

5.5%

0.8%

0.4%

0.005/Wp/yr

19/kWp

71SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Sensitivity analysis (individual ranges)Most critical LCOE parameters are performance ratio, durability and

discount rate

-2.00 -1.00 0.00 1.00 2.00 3.00 4.00

Performance ratio

Years of operation

Discount rate

Degradation rate

System price

Irradiance (kWh/m²)

Insurance (% of system price)

O&M

Inverter replacement reserve

Base values

SDG cents/kWh

12.50

P50

78%

1.54/Wp

25 yrs

5.5%

0.8%

0.4%

0.005/Wp/yr

19/kWp

60%85%

3.5% 8%

0.5%

15 yrs

-10%

P25: 1,678

1%0.1%

+10%

15 25

P99: 1,529

-50% +50%

2%

72SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

Irradiance resource in Singapore (1) Exceedance probability risk assessment is important

Data source: National Environment Agency (NEA), monthly data from 1991-2000, 2010-2018, Changi

Met. Station (S24), irradiance resource varies among different locations in Singapore and between

different sensor technologies and level of maintenance. P-values shown are empirical figures

Example:

A P90 value of

~1,573 kWh/m2

means that there is a

90% likelihood that

the annual irradiance

resource will be

greater than 1,573

kWh/m2.

1500 1550 1600 1650 1700 1750 1800-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1 Normal dist. CDF

P99: ~1,529 kWh/m2

P95: ~1,554 kWh/m2

P90: ~1,573 kWh/m2

P75: ~1,609 kWh/m2

Cum

ula

tive

dis

trib

utio

n f

un

ction

(CD

F)

Annual irradiance [kWh/m2]

P50: ~1,644 kWh/m2

Normal dist. P-values

NEA raw data

73SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

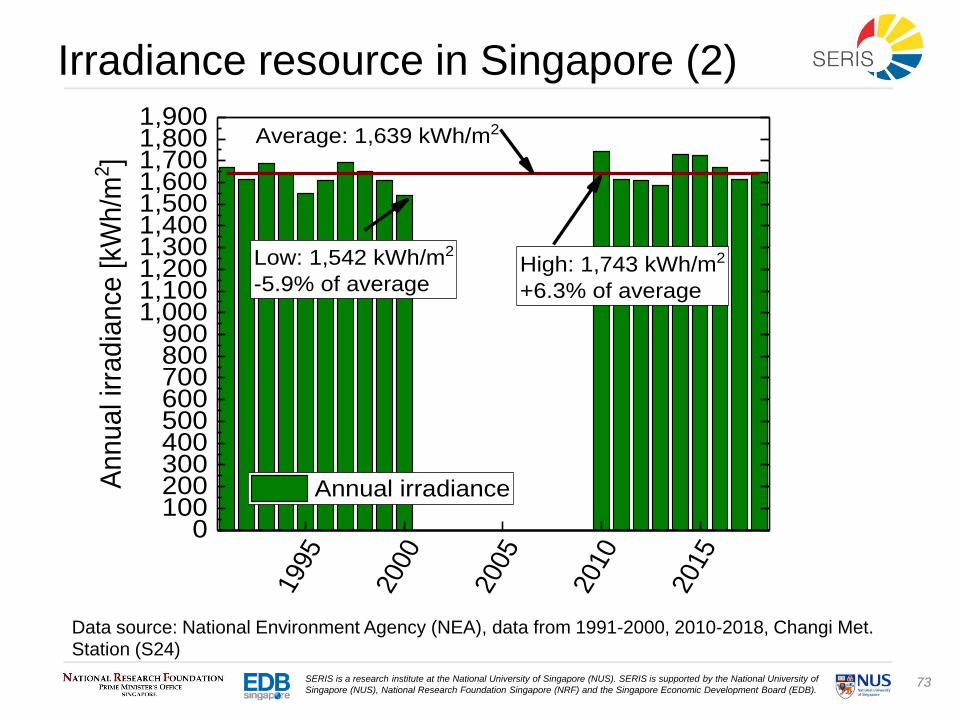

Irradiance resource in Singapore (2)

1995

2000

2005

2010

2015

0100200300400500600700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,8001,900

High: 1,743 kWh/m2

+6.3% of average

Low: 1,542 kWh/m2

-5.9% of average

An

nu

al i

rra

dia

nce

[kW

h/m

2]

Annual irradiance

Average: 1,639 kWh/m2

Data source: National Environment Agency (NEA), data from 1991-2000, 2010-2018, Changi Met. Station (S24)

74SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

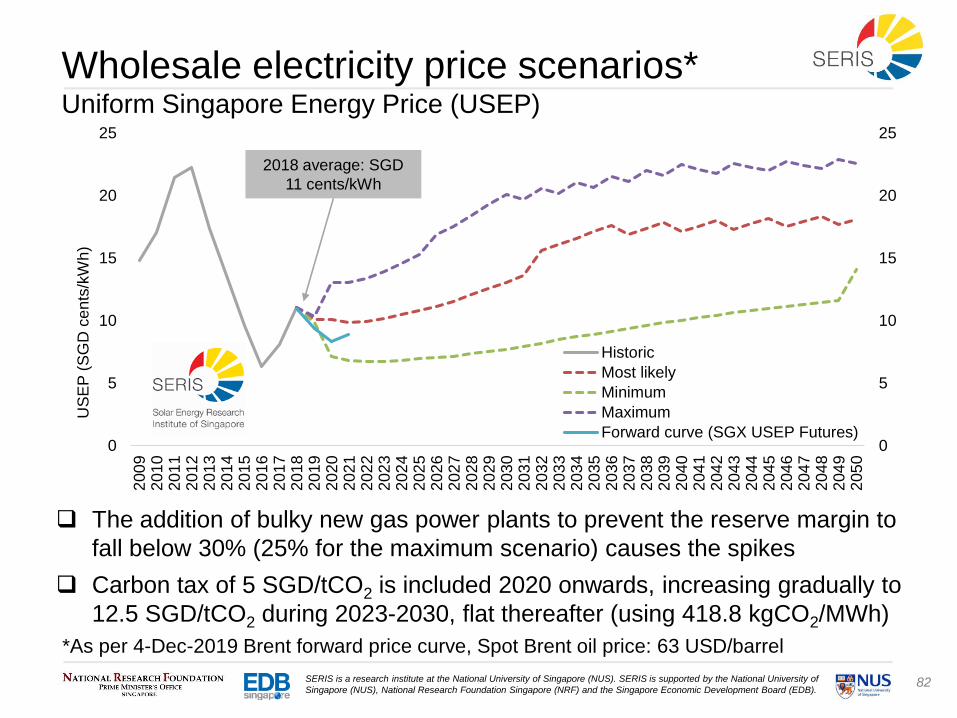

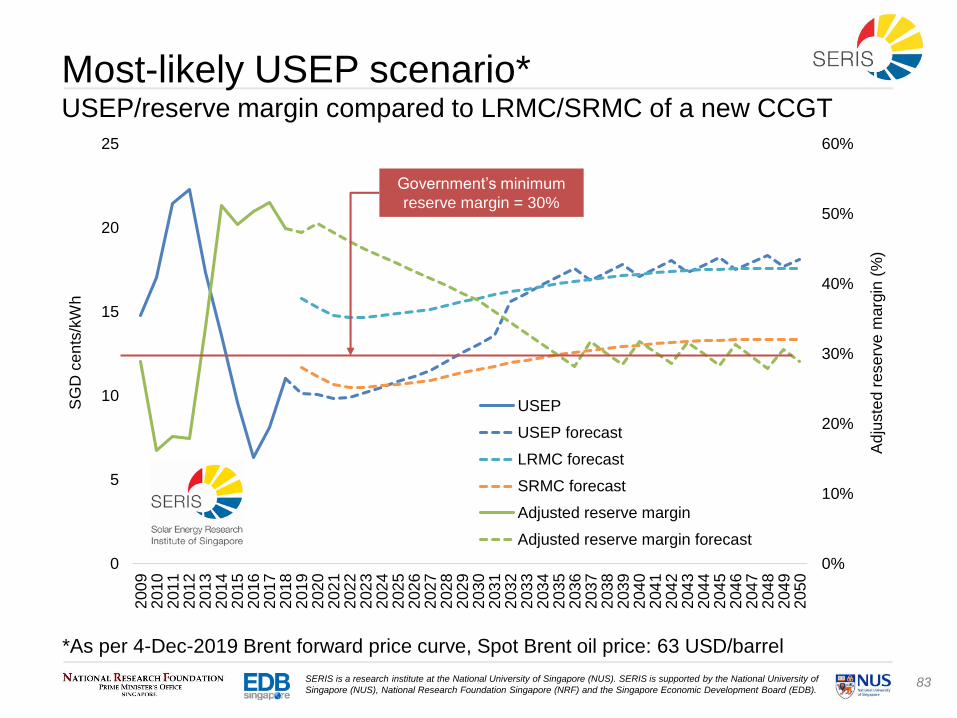

5. Future electricity price scenarios

75SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

5

10

15

20

25

30

35

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

SG

D c

en

ts/k

Wh

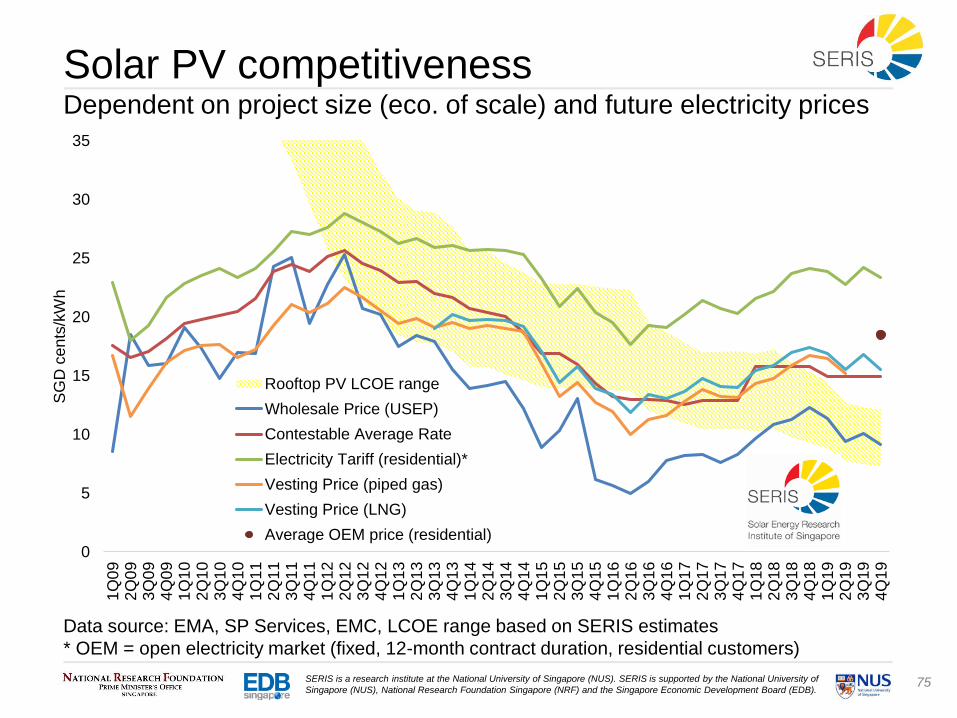

Rooftop PV LCOE range

Wholesale Price (USEP)

Contestable Average Rate

Electricity Tariff (residential)*

Vesting Price (piped gas)

Vesting Price (LNG)

Average OEM price (residential)

Solar PV competitivenessDependent on project size (eco. of scale) and future electricity prices

Data source: EMA, SP Services, EMC, LCOE range based on SERIS estimates

* OEM = open electricity market (fixed, 12-month contract duration, residential customers)

76SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

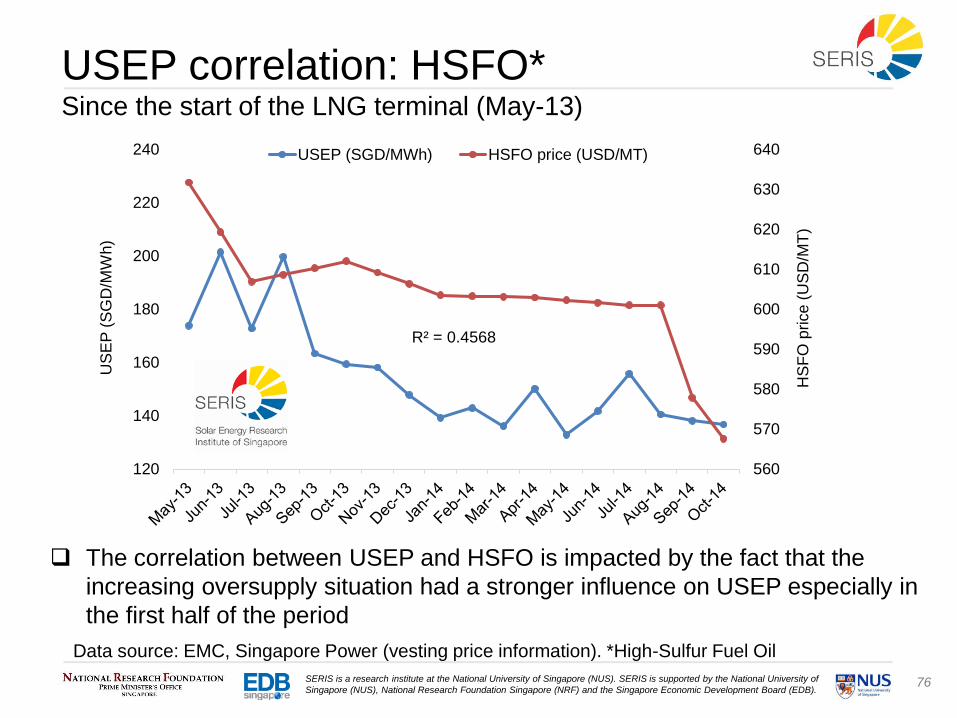

USEP correlation: HSFO*Since the start of the LNG terminal (May-13)

Data source: EMC, Singapore Power (vesting price information). *High-Sulfur Fuel Oil

The correlation between USEP and HSFO is impacted by the fact that the

increasing oversupply situation had a stronger influence on USEP especially in

the first half of the period

560

570

580

590

600

610

620

630

640

120

140

160

180

200

220

240

HS

FO

price

(U

SD

/MT

)

US

EP

(S

GD

/MW

h)

USEP (SGD/MWh) HSFO price (USD/MT)

R² = 0.4568

77SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

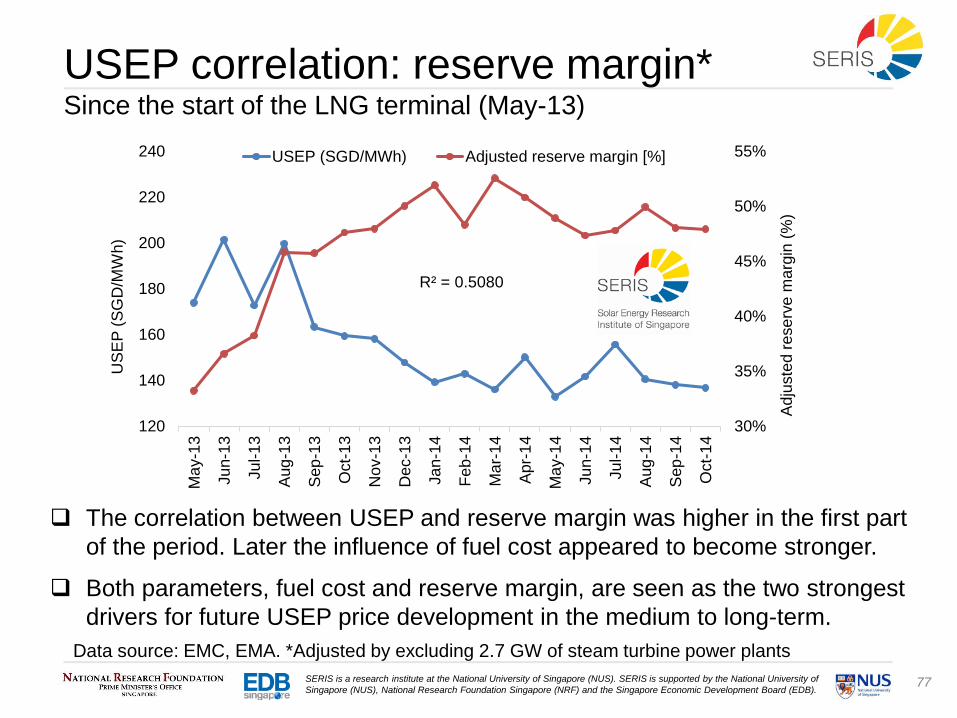

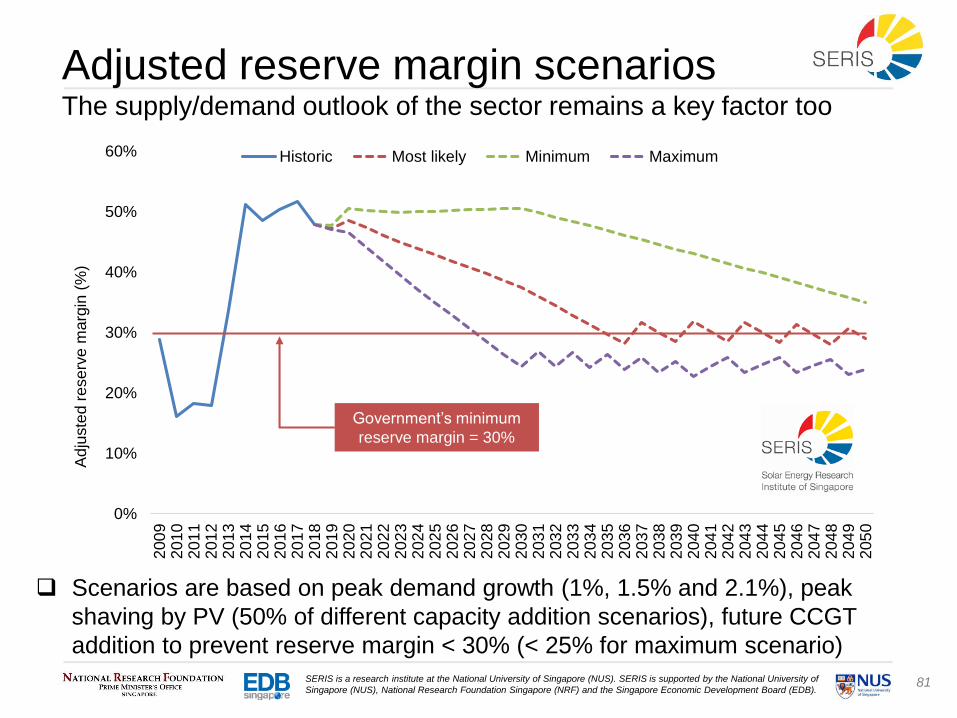

Data source: EMC, EMA. *Adjusted by excluding 2.7 GW of steam turbine power plants

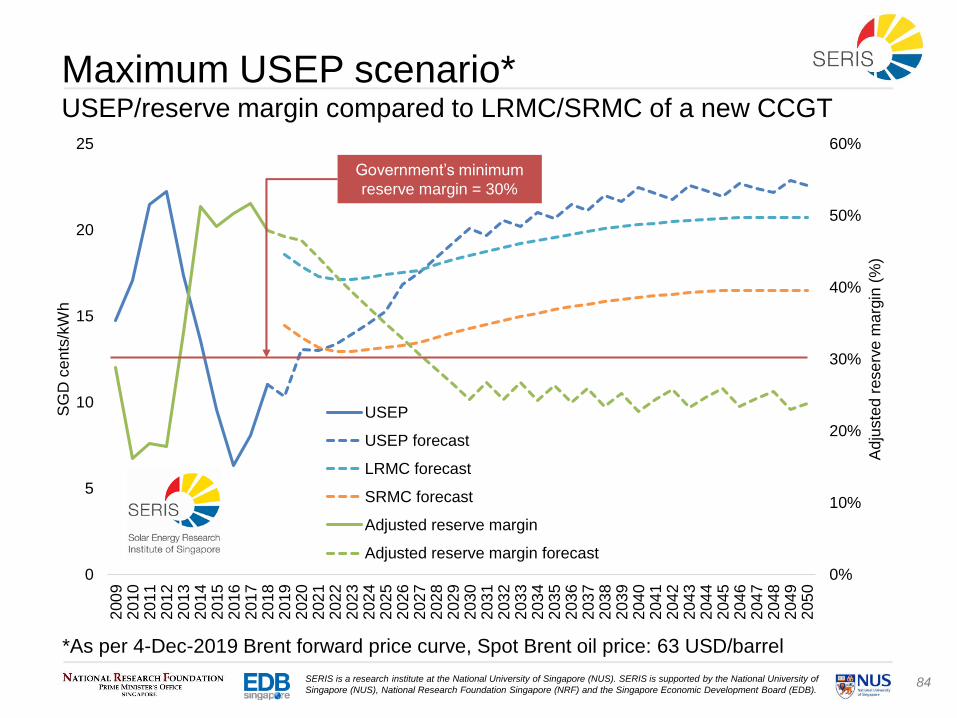

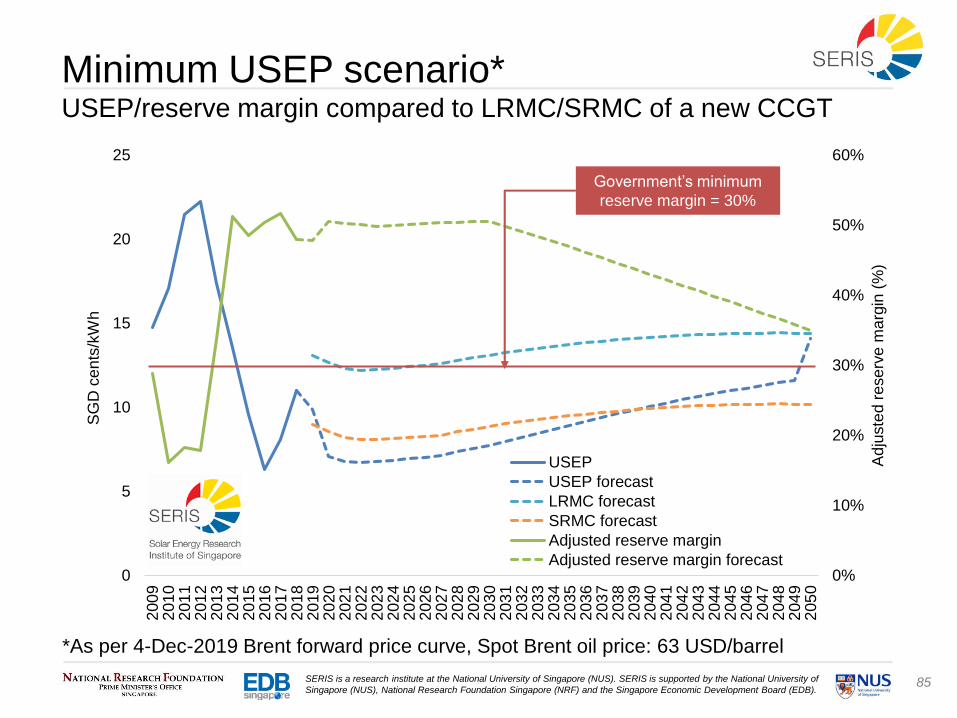

USEP correlation: reserve margin*Since the start of the LNG terminal (May-13)

The correlation between USEP and reserve margin was higher in the first part

of the period. Later the influence of fuel cost appeared to become stronger.

Both parameters, fuel cost and reserve margin, are seen as the two strongest

drivers for future USEP price development in the medium to long-term.

R² = 0.5080

30%

35%

40%

45%

50%

55%

120

140

160

180

200

220

240

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Aug

-13

Sep

-13

Oct-

13

Nov-1

3

Dec-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-14

Apr-

14

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Aug

-14

Sep

-14

Oct-

14

Ad

juste

d r

ese

rve

ma

rgin

(%

)

US

EP

(S

GD

/MW

h)

USEP (SGD/MWh) Adjusted reserve margin [%]

78SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

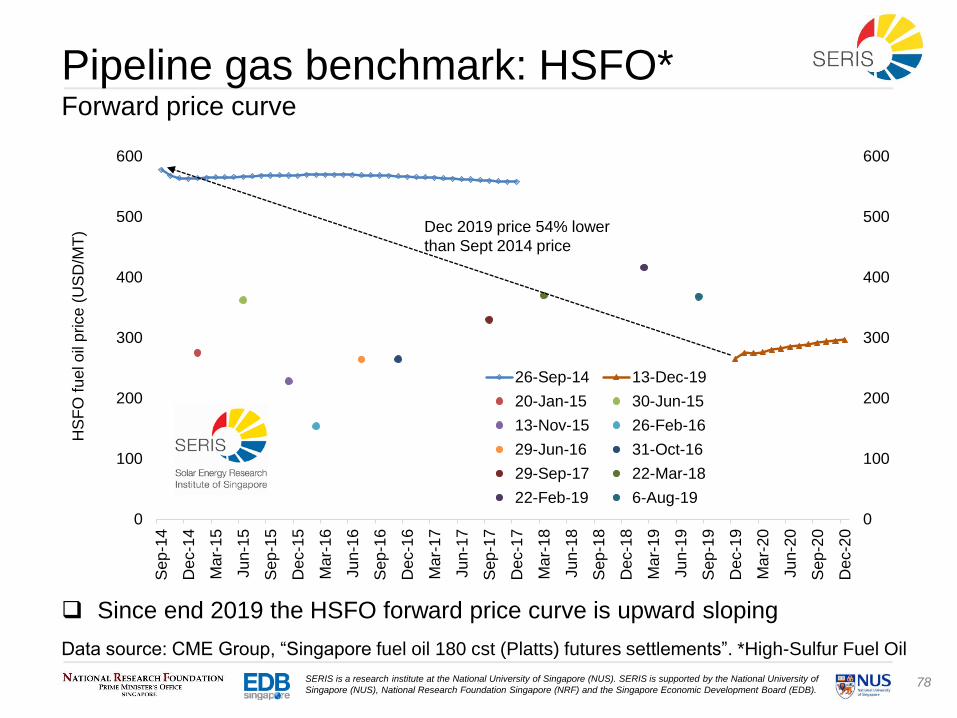

Pipeline gas benchmark: HSFO*Forward price curve

Data source: CME Group, “Singapore fuel oil 180 cst (Platts) futures settlements”. *High-Sulfur Fuel Oil

Since end 2019 the HSFO forward price curve is upward sloping

0

100

200

300

400

500

600

0

100

200

300

400

500

600S

ep

-14

Dec-1

4

Ma

r-15

Ju

n-1

5

Sep

-15

Dec-1

5

Ma

r-16

Ju

n-1

6

Sep

-16

Dec-1

6

Ma

r-17

Ju

n-1

7

Sep

-17

Dec-1

7

Ma

r-18

Ju

n-1

8

Sep

-18

Dec-1

8

Ma

r-19

Ju

n-1

9

Sep

-19

Dec-1

9

Ma

r-20

Ju

n-2

0

Sep

-20

Dec-2

0

HS

FO

fu

el o

il p

rice

(U

SD

/MT

)

26-Sep-14 13-Dec-19

20-Jan-15 30-Jun-15

13-Nov-15 26-Feb-16

29-Jun-16 31-Oct-16

29-Sep-17 22-Mar-18

22-Feb-19 6-Aug-19

Dec 2019 price 54% lower

than Sept 2014 price

79SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

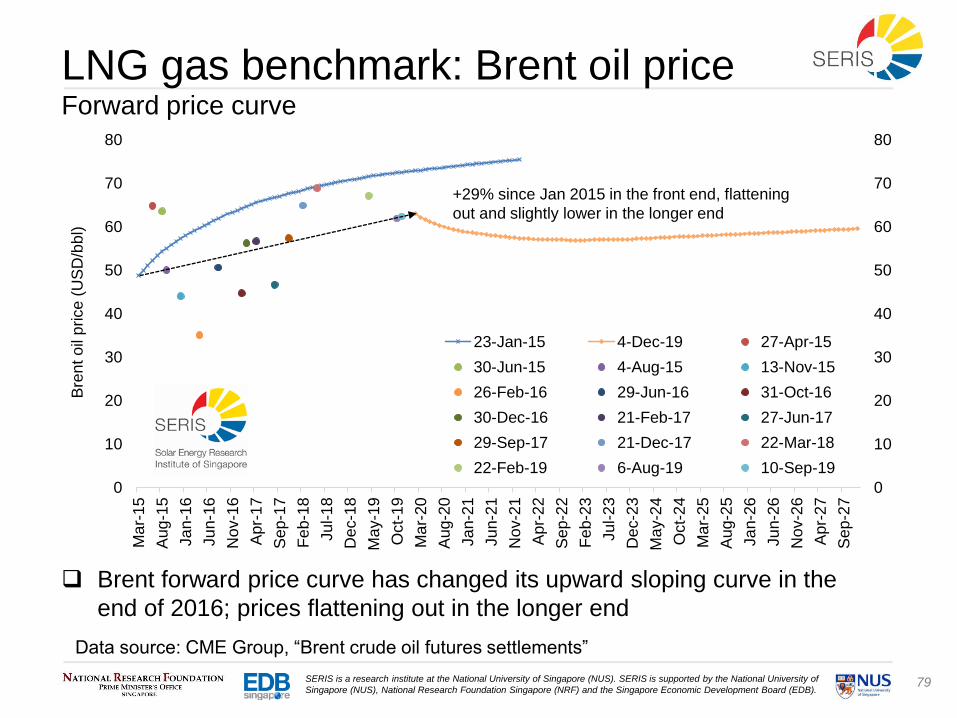

LNG gas benchmark: Brent oil priceForward price curve

Data source: CME Group, “Brent crude oil futures settlements”

Brent forward price curve has changed its upward sloping curve in the

end of 2016; prices flattening out in the longer end

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80M

ar-

15

Aug

-15

Ja

n-1

6

Ju

n-1

6

Nov-1

6

Apr-

17

Sep

-17

Fe

b-1

8

Ju

l-1

8

Dec-1

8

Ma

y-1

9

Oct-

19

Ma

r-20

Aug

-20

Ja

n-2

1

Ju

n-2

1

Nov-2

1

Apr-

22

Sep

-22

Fe

b-2

3

Ju

l-2

3

Dec-2

3

Ma

y-2

4

Oct-

24

Ma

r-25

Aug

-25

Ja

n-2

6

Ju

n-2

6

Nov-2

6

Apr-

27

Sep

-27

Bre

nt o

il p

rice

(U

SD

/bb

l)

23-Jan-15 4-Dec-19 27-Apr-15

30-Jun-15 4-Aug-15 13-Nov-15

26-Feb-16 29-Jun-16 31-Oct-16

30-Dec-16 21-Feb-17 27-Jun-17

29-Sep-17 21-Dec-17 22-Mar-18

22-Feb-19 6-Aug-19 10-Sep-19

+29% since Jan 2015 in the front end, flattening

out and slightly lower in the longer end

80SERIS is a research institute at the National University of Singapore (NUS). SERIS is supported by the National University of

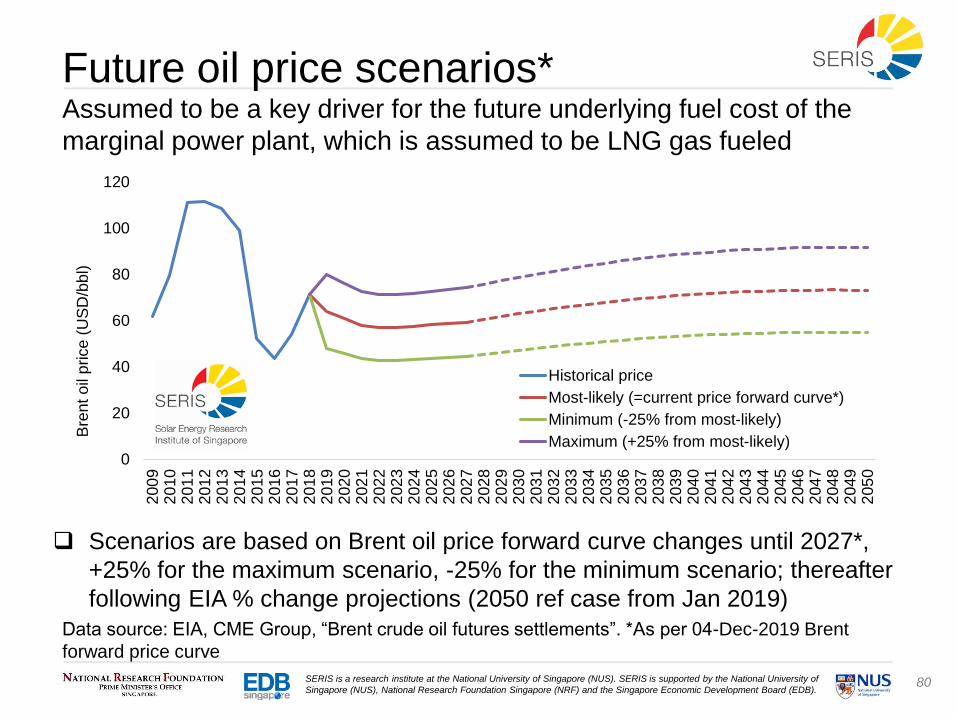

Singapore (NUS), National Research Foundation Singapore (NRF) and the Singapore Economic Development Board (EDB).

0

20

40

60

80

100

120

200

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

82

01

92

02

02

02

12

02

22

02

32

02

42

02

52

02

62

02

72

02

82

02

92

03

02

03

12

03

22

03

32

03

42

03

52

03

62

03

72

03

82

03

92

04

02

04

12

04

22

04

32

04

42

04

52

04

62

04

72

04

82

04

92

05

0

Bre

nt o

il p

rice

(U

SD

/bb

l)

Historical price