Embed Size (px)

Citation preview

EXECUTIVE PROGRAMME

MODULE 1, PAPER 2

PRACTICE MANUAL

Cost and Management Accounting

APRIL 2016

Price : Rs. 300/-

© THE INSTITUTE OF COMPANY SECRETARIES OF INDIA

No part of this Publication may be translated or copied in any form or by any means without the prior written permission of The Institute of Company Secretaries of India.

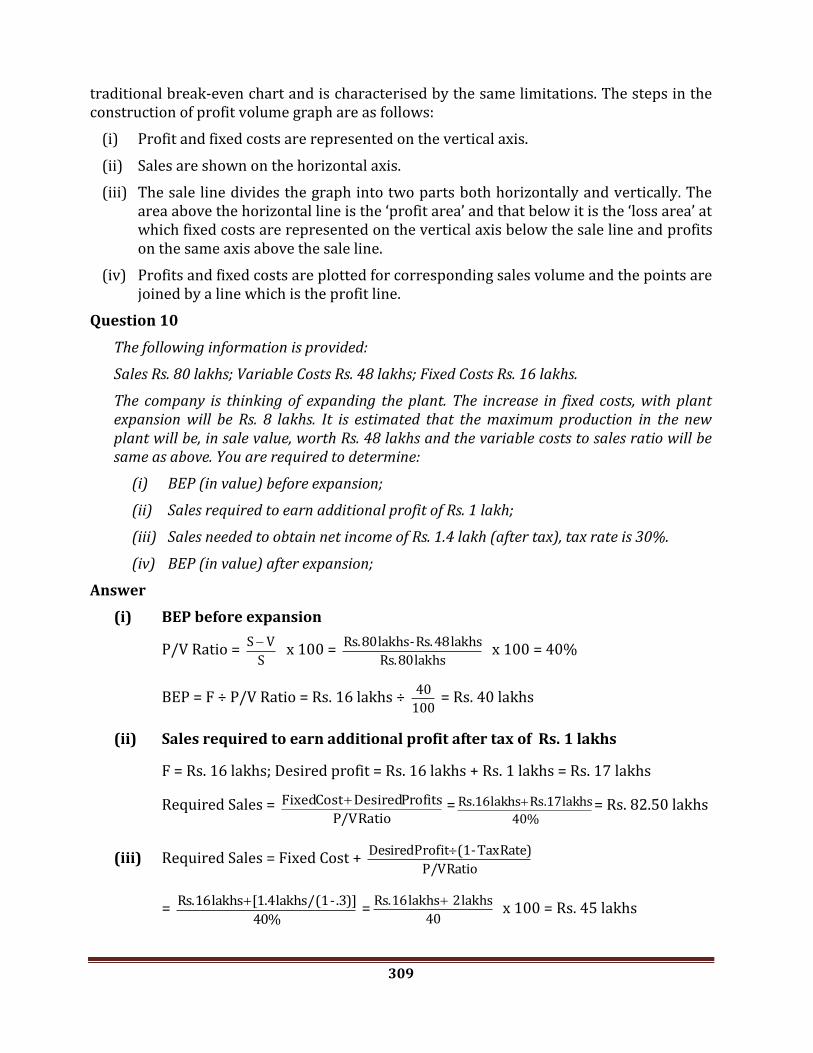

The PRACTICE MANUAL has been prepared by competent persons and the Institute hopes that it will facilitate the students in preparing for the Institute's examinations. It is, however, to be noted that the answers are to be treated as model answers and not as exhaustive and there can be alternative solutions available for a questions provided in this practice manual. The Institute is not in any way responsible for the correctness or otherwise of the answers.

The Practice Manual contains the information based on the Laws/Rules applicable at the time of preparation. Students are expected to be well versed with the amendments in the Laws/Rules made upto six months prior to the date of examination.

Please note that the paper of Cost and Management Accounting is in Optical Mark Recognition (OMR) format, but to give an insight into the problem solving technique, this practice manual is prepared to build competency in practical aspects by providing the students with a pool of solved practical problems.

ISBN No. : 978-93-82207-70-2

Printed at : Chandu Press/1,000/April 2016

(ii)

PREFACE

“Knowledge is a treasure, but practice is the key to it” -Lao Tzu

In the contemporary era, the global business is exemplified under the intense competition from

domestic as well as transnational players. Competitive advantages of the inclusive economy can

be achieved by placing right strategy in right direction. The successful achievement of the goals

requires constant update and brushing up of one’s specializations and skills. It is observed time

and again that the updating of knowledge is fundamental to development of changing times. In

line with the dynamic nature of the economy, the students must be equipped and thorough in

their analytical abilities to work in the dynamic environment. This demands the development of

basic theoretical concepts as well as practical aspects of this growing and competitive

specialization.

In lines with updating the information, the Institute in the past brought Practice Manual on

Financial Treasury and Forex Management (Professional Programme) and Company Accounts

and Auditing Practices (Executive Programme). Now, we are presenting the Practice Manual

prepared specifically for the subject “Cost and Management Accounting” to the students of

Executive Programme. This Practice Manual is a learning instrument which serves as a refresher.

Though the pattern of the paper will be in OMR format, but to give an insight into the problem

solving technique, this Practice Manual is prepared to build competency in practical aspects by

providing the students with a pool of solved practical problems.

This Practice Manual is not intended to replace the study material but to supplement the same.

Therefore, the students are expected to make a holistic study of both the study material and

Practice Manual to gain maximum benefit and acquire in-depth knowledge of the subject.

I acknowledge with thanks all those experts, authors and institutions whose material has been

consulted and referred in preparation of this Practice Manual. I place on record my sincere

appreciation to Ms. Akansha Rawat, Executive (Academics) in the Academic Team at the Institute

headed by Ms. Sonia Baijal, Director for this initiative.

I have great pleasure in introducing this practice manual to the students. I am sure, this manual

will prove to be useful and beneficial to the students. Therefore, I advise all the students to take

maximum benefit out of it by meticulously practicing the questions given therein. As the saying

goes “Practice makes a man perfect”, practicing more will develop clear knowledge of

fundamental concepts to solve practical questions correctly and give a stronger hold in the

subject.

My best wishes to you all!

New Delhi CS Mamta Binani

25th April, 2016 President, ICSI

(iii)

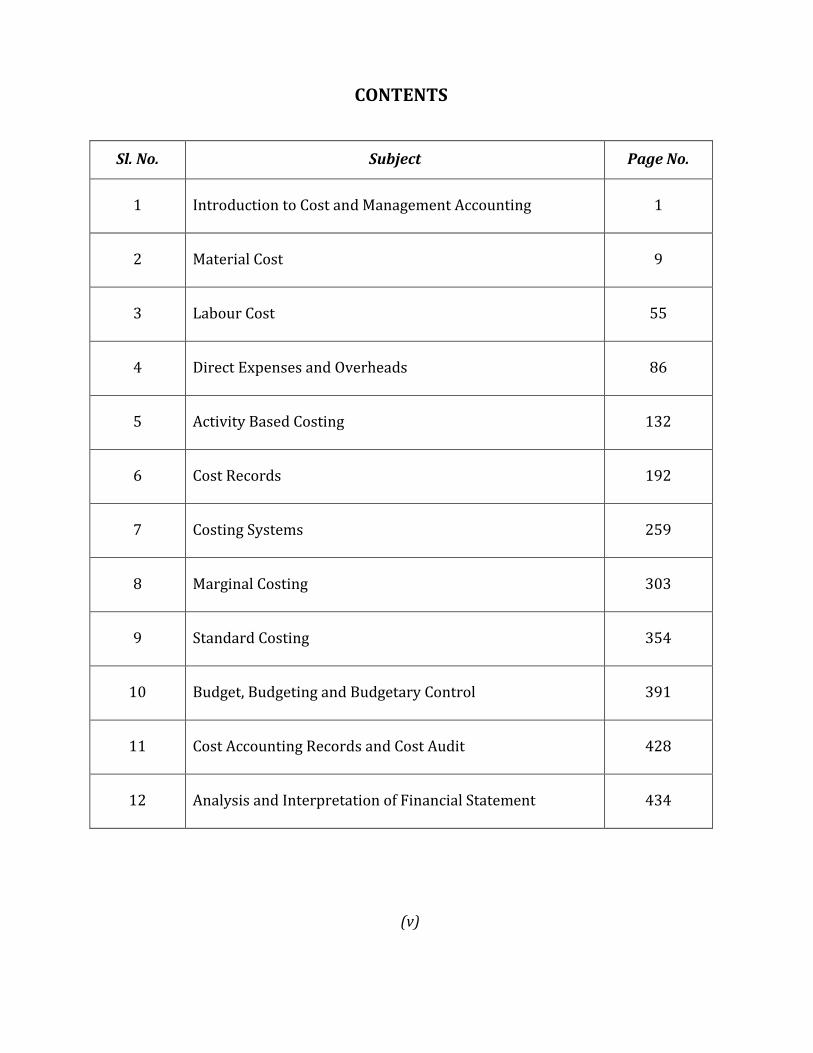

CONTENTS

Sl. No. Subject Page No.

1 Introduction to Cost and Management Accounting 1

2 Material Cost 9

3 Labour Cost 55

4 Direct Expenses and Overheads 86

5 Activity Based Costing 132

6 Cost Records 192

7 Costing Systems 259

8 Marginal Costing 303

9 Standard Costing 354

10 Budget, Budgeting and Budgetary Control 391

11 Cost Accounting Records and Cost Audit 428

12 Analysis and Interpretation of Financial Statement 434

(v)

1

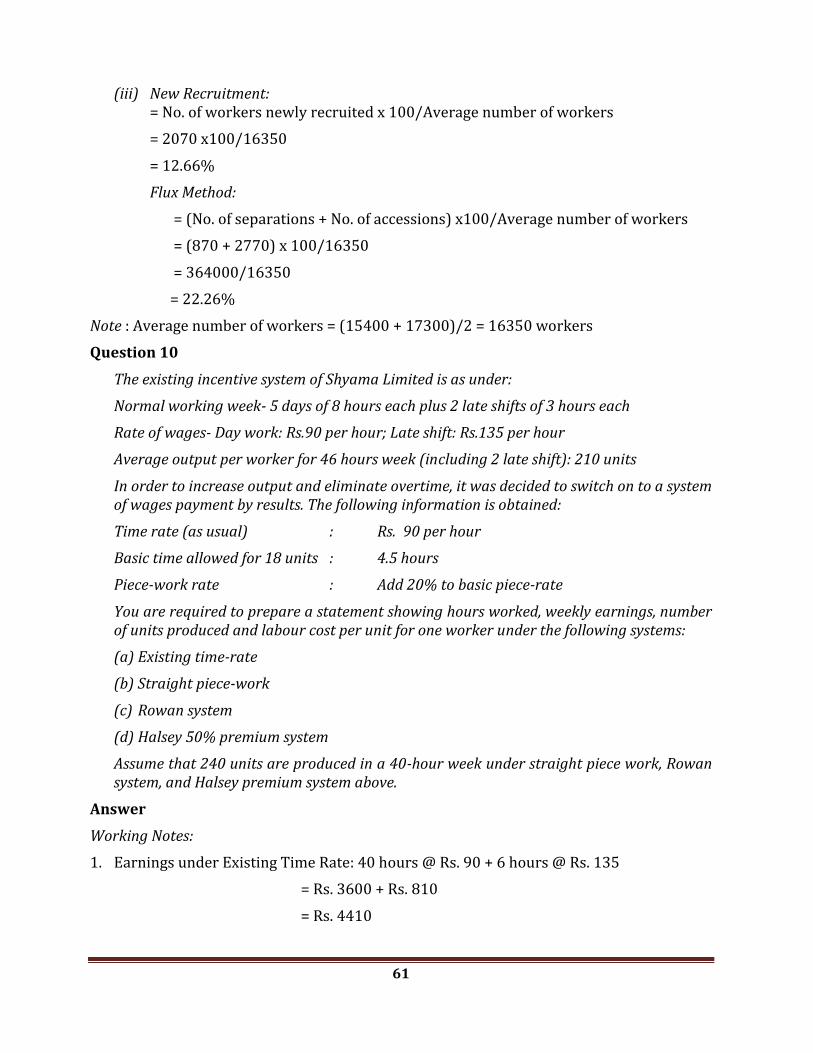

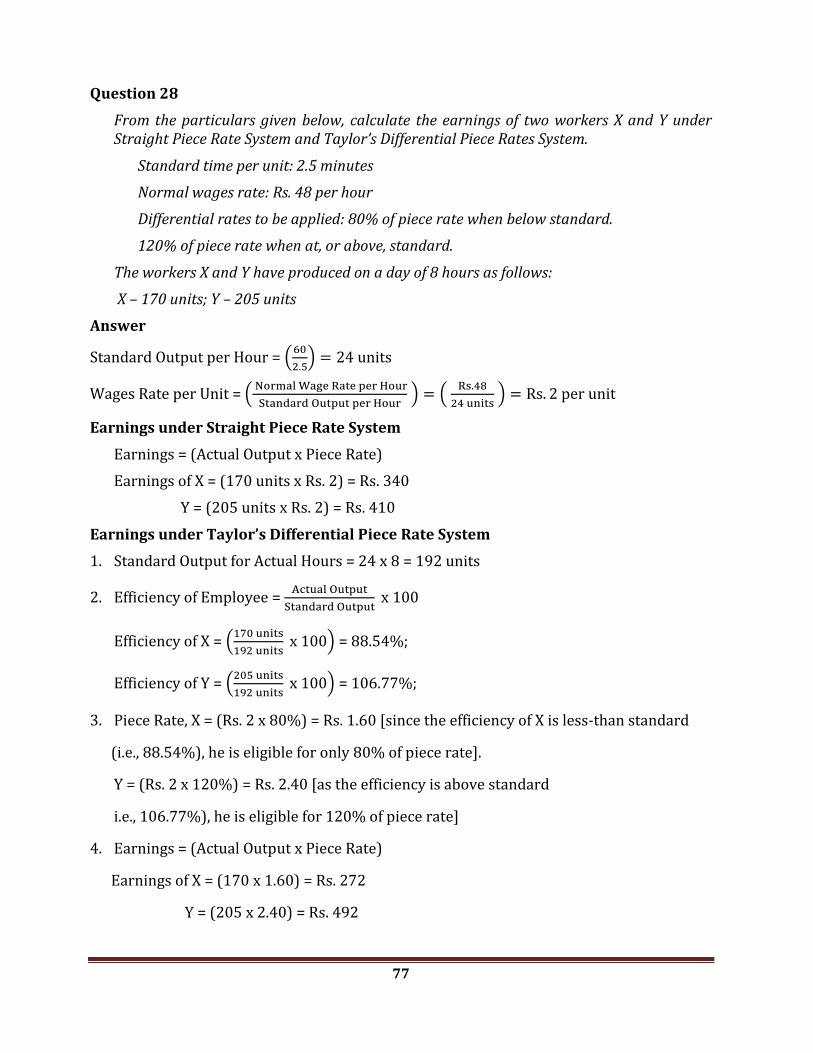

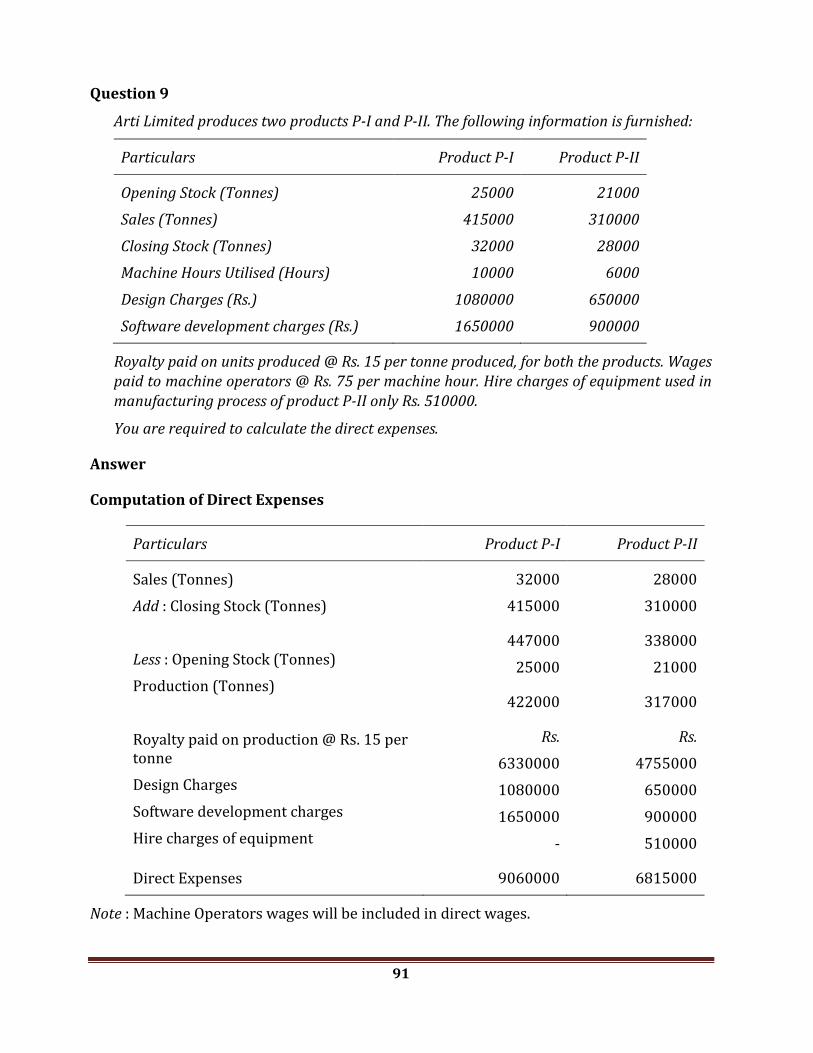

Question 1

Question 1

Define costing and discuss its objectives.

Answer

Costing is defined as the technique and process of ascertaining costs. The technique refers to principles, which are applied for ascertaining cost of products, jobs, processes and services. Costing involves the classifying, recording, and appropriate allocation of expenditure for the determination of costs of products or services; the relation of these costs to sales values and the ascertainment of profitability.

In practice, the terms costing, cost accounting and cost accountancy are most often used interchangeably although they are defined differently. The main objectives of costing may be summarised as follows:

(i) To analyse and classify all expenditures with reference to the cost of products and operations.

(ii) To arrive at the cost of production of every unit, job, operation, process, department or service and to develop cost standard.

(iii) To indicate to the management any inefficiencies and the extent of various forms of waste, whether of materials, time, expenses or in the use of machinery, equipment and tools. Analysis of the causes of unsatisfactory results may indicate remedial measures.

(iv) To provide data for periodical profit and loss accounts and balance sheets and also, to explain in detail the exact reasons for profit or loss revealed in total in the profit and loss account.

(v) To reveal sources of economies in production having regard to methods, types of equipment, design, output and layout.

(vi) To provide actual figures of cost for comparison with estimates and to serve as guide for future estimates or quotations and to assist the management in their price fixing policy.

(vii) To analyse the variance between budgeted and actuals so that corrective action may be taken.

(viii) To present comparative cost data for different periods and various volumes of output.

1

Introduction to Cost and

Management Accounting

2

(ix) To record the relative production results of each unit of plant and machinery in use as a basis for examining its efficiency.

(x) To provide information to enable management to make short-term decisions of various types.

Question 2

The scope of Cost accounting is very wide. Discuss

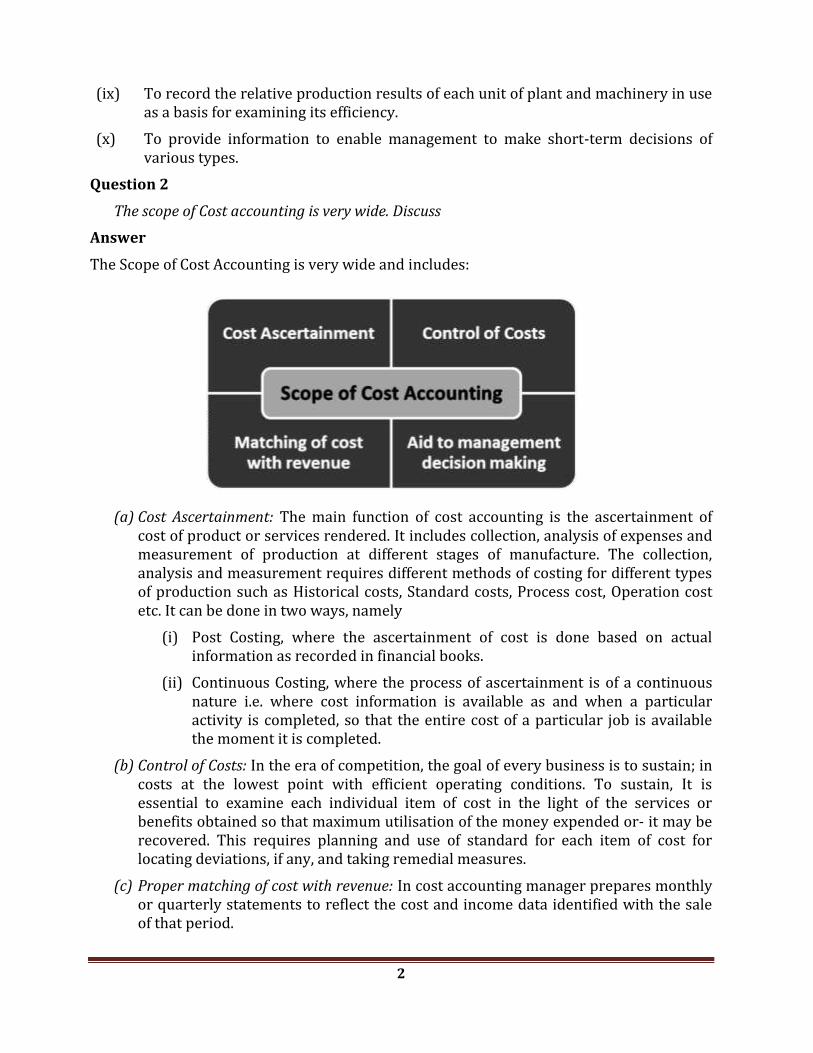

Answer

The Scope of Cost Accounting is very wide and includes:

(a) Cost Ascertainment: The main function of cost accounting is the ascertainment of cost of product or services rendered. It includes collection, analysis of expenses and measurement of production at different stages of manufacture. The collection, analysis and measurement requires different methods of costing for different types of production such as Historical costs, Standard costs, Process cost, Operation cost etc. It can be done in two ways, namely

(i) Post Costing, where the ascertainment of cost is done based on actual information as recorded in financial books.

(ii) Continuous Costing, where the process of ascertainment is of a continuous nature i.e. where cost information is available as and when a particular activity is completed, so that the entire cost of a particular job is available the moment it is completed.

(b) Control of Costs: In the era of competition, the goal of every business is to sustain; in costs at the lowest point with efficient operating conditions. To sustain, It is essential to examine each individual item of cost in the light of the services or benefits obtained so that maximum utilisation of the money expended or- it may be recovered. This requires planning and use of standard for each item of cost for locating deviations, if any, and taking remedial measures.

(c) Proper matching of cost with revenue: In cost accounting manager prepares monthly or quarterly statements to reflect the cost and income data identified with the sale of that period.

3

(d) Aids to Management Decision-making: Decision-making is a process of choosing between two or more alternatives, based on the resultant outcome of the various alternatives. A Cost Benefit Analysis also needs to be done. All this can be achieved through a good cost accounting system

Question 3

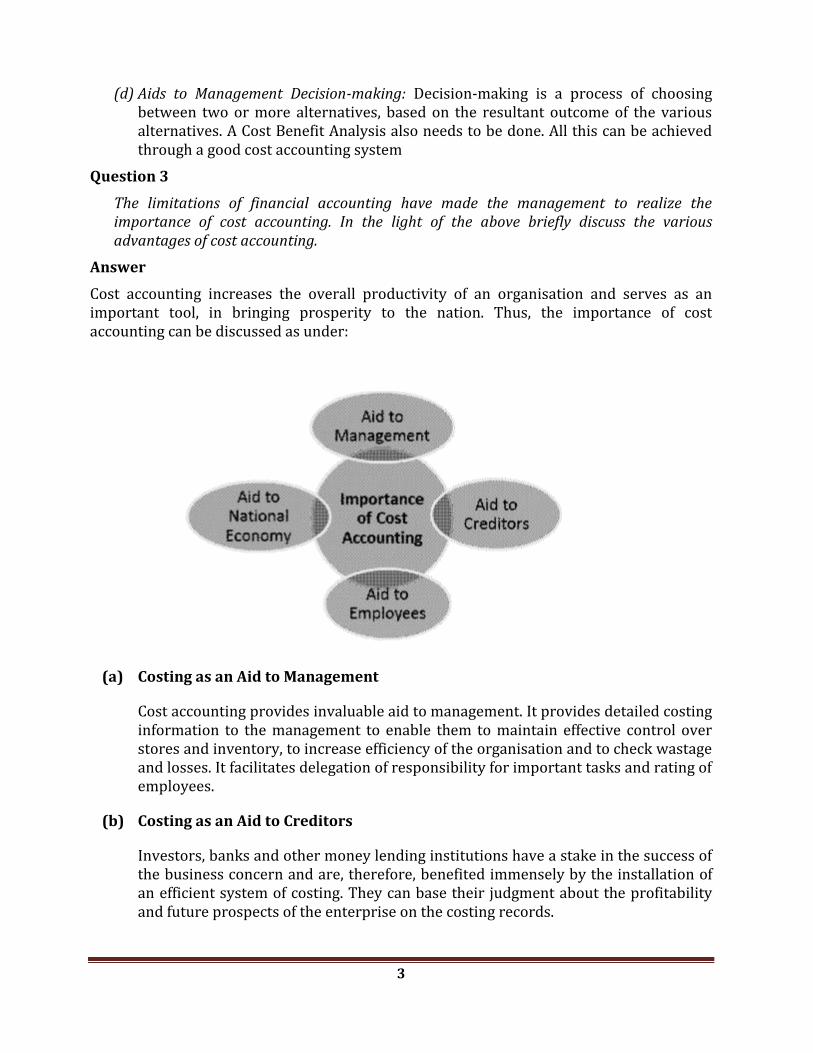

The limitations of financial accounting have made the management to realize the importance of cost accounting. In the light of the above briefly discuss the various advantages of cost accounting.

Answer

Cost accounting increases the overall productivity of an organisation and serves as an important tool, in bringing prosperity to the nation. Thus, the importance of cost accounting can be discussed as under:

(a) Costing as an Aid to Management

Cost accounting provides invaluable aid to management. It provides detailed costing information to the management to enable them to maintain effective control over stores and inventory, to increase efficiency of the organisation and to check wastage and losses. It facilitates delegation of responsibility for important tasks and rating of employees.

(b) Costing as an Aid to Creditors

Investors, banks and other money lending institutions have a stake in the success of the business concern and are, therefore, benefited immensely by the installation of an efficient system of costing. They can base their judgment about the profitability and future prospects of the enterprise on the costing records.

4

(c) Costing as an Aid to Employees

Employees have a vital interest in their employer’s enterprise in which they are employed. They are benefited by a number of ways by the installation of an efficient system of costing. They are benefited, through continuous employment and higher remuneration by way of incentives, bonus plans, etc.

(d) Costing as an Aid to National Economy

An efficient system of costing brings prosperity to the business enterprise which in turn results in stepping up of the government revenue. The overall economic development of a country takes place as a consequence increase in efficiency of production.

Question 4

Define and explain the term (a) cost centre and (b) cost unit.

Answer

(a) Cost centre

According to the Chartered Institute of Management Accountants, London, cost centre means, “a production or service location, function, activity or item of equipment whose costs may be attributed to cost units”. Cost centre is the smallest organisational sub-unit for which separate cost collection is attempted. Thus cost centre refers to one of the convenient unit into which the whole factory organisation has been appropriately divided for costing purposes.

Cost centres may be classified as follows:

(i) Productive, Unproductive and Mixed Cost Centres

(ii) Personal and Impersonal Cost Centre

(iii) Operation and Process Cost Centre

(b) Cost unit

The Chartered Institute of Management Accountants, London, defines a unit of cost as “a unit of product or service in relation to which costs are ascertained”. A cost unit is a devise for the purpose of breaking up or separating costs into smaller sub-divisions. These smaller sub-divisions are attributed to products or services to determine product cost or service cost or cost of time spent for a particular job etc. For example:

Industry/Product Cost unit

Automobile Number

Brick works 1000 bricks

Cement Tonne

Transport Tonne - Kilometre

Passenger - Kilometre

5

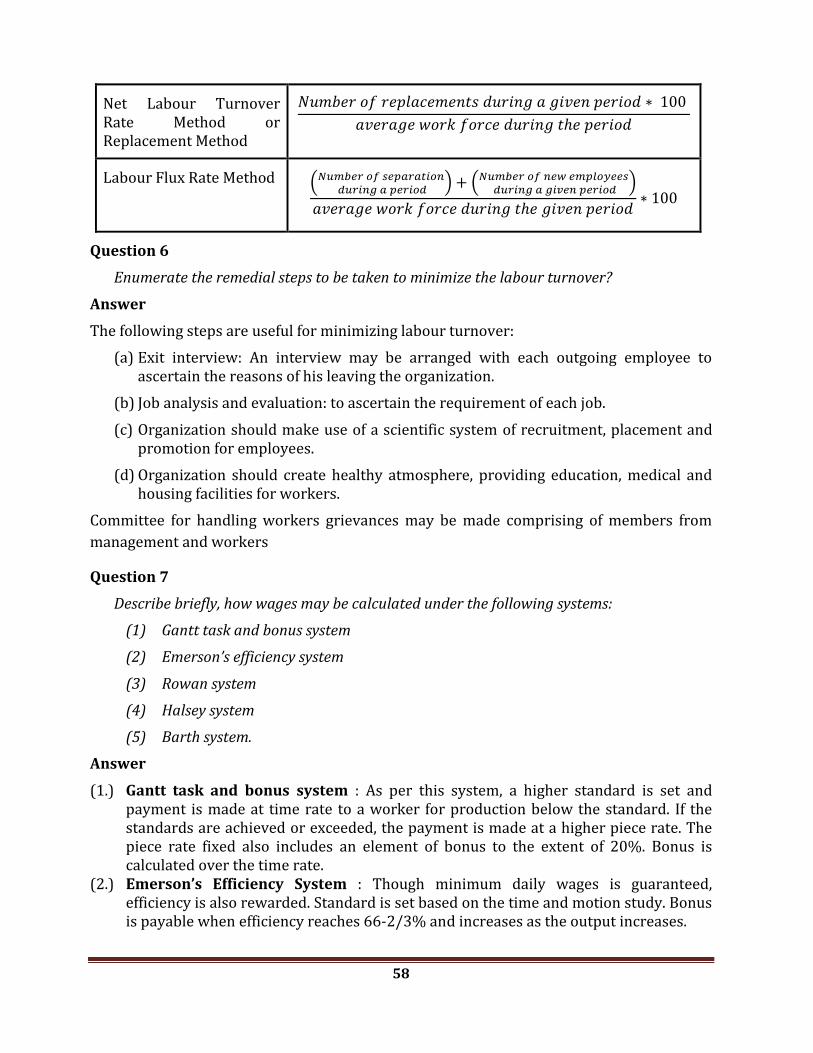

Question 5

Distinguish between:

(a) Cost accounting and management accounting

(b) Imputed Costs and Common Costs

Answer

(a) Cost accounting and management accounting

Cost Accounting Management Accounting

1. Cost accounting is concerned with the ascertainment, allocation, distribution and accounting aspects of costs.

Management accounting is concerned with impact and effect aspect of costs.

2. Cost accounting data generally serves as a base to which the tools and techniques of management accounting can be applied to make it more purposeful and management oriented.

The management accounting data is derived both, from the cost accounts and financial accounts.

3. A cost accountant collects and presents costing data.

Management accountant analyses and decides specific business problems on the basis of data available.

4. The cost accountant is generally placed at a lower level of hierarchy.

The management accountant generally is placed at a higher level of hierarchy.

5. The approach of the cost accountant is much narrower

The approach of management accountant is wider as it includes interpretation of economic and statistical data along with the costing data.

6. Tools and techniques like variable costing, break-even analysis, standard costing, etc., are used.

Management accounting, in addition to the techniques of cost accounting, uses other techniques like cash flow, ratio analysis, etc.

7. Cost accounting does not include financial accounting and has nothing to do with tax accounting.

Management accounting includes both financial accounting as well as tax accounting. It also embraces tax planning and tax accounting.

8. Cost accounting is more Management accounting is concerned

6

concerned with short-term planning.

equally with short-term and long-term planning

9. Cost accounting is mostly historical in its approach and it projects the past.

Management accounting is futuristic in its approach.

10. Cost accounting system can be installed without management accounting.

Management accounting cannot be installed without a proper cost accounting system.

(b) Imputed Costs and Common Costs

Imputed costs are the costs that are not incurred but are useful while taking decision pertaining to a particular situation. These costs are known as imputed or notional costs and they do not appear in financial records. These costs are notional in nature and do not involve any cash outlay. It is the value of a benefit where no actual cost is incurred. Interest on internally generated funds, rental value of company owned property and salaries of owners of a single proprietorship or partnership are some examples of imputed costs. When alternate capital investment projects are being evaluated it is necessary to consider the imputed interest on capital before a decision is arrived as to which is the most profitable project.

Common costs are costs, which are incurred for more than one product, job, territory or any other specific costing object. It is the cost of services employed in the creation of two or more outputs which is not allocated to those outputs on a clearly justified basis. They are not easily related with individual products and hence are generally apportioned. Common costs are not only common to products, but they may be common to process, functions, responsibilities, customs, sales territories, periods of time and similar costing units. In general, management decisions influence the occurrence of common costs e.g., rent of the factory in a common cost to all departments located in a factory.

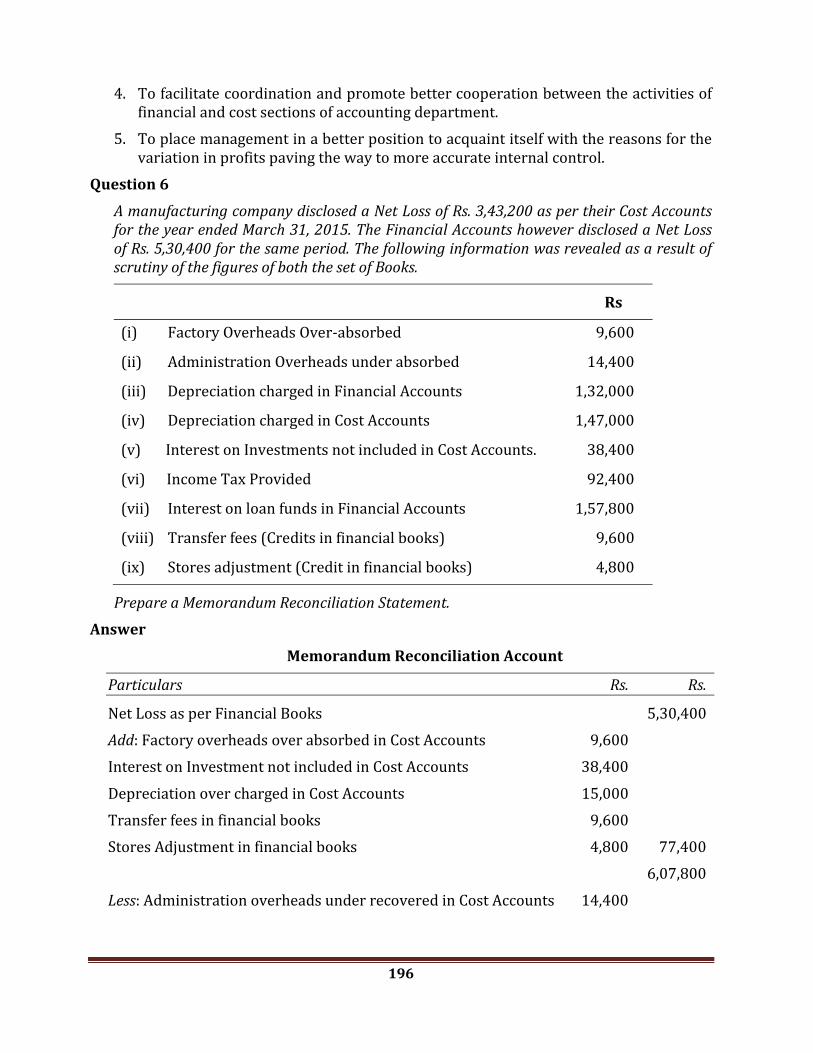

Question 6

Explain the significance of decision-making costs. Briefly explain the various type of costs used by the management in decision-making.

Answer

There are certain costs which are specially used for decision making by the management. Such decision making costs may be relevant costs or irrelevant costs.

Various types of costs used by management in decision making are briefly described below:

• Opportunity costs : Opportunity cost is the cost of selecting one course of action and the losing of other opportunities to carry out that course of action. It is the amount that can be received if the asset is utilized in its next best alternative.

• Differential cost : Differential cost has been defined as “the difference in total cost between alternatives, calculated to assist decision making”. It helps management

7

to know the additional profit that would be earned if idle capacity is used or when additional investments are made.

• Imputed costs : Some costs are not incurred and are useful while taking decision pertaining to a particular situation. Examples: Interest on internally generated funds, salaries of owners of proprietorship or partnership, notional rent etc.

• Out-of-pocket costs : Out-of-pocket costs signify such outlay required for an activity. The management would like to know that the income from a particular project will at least cover the expenditure for the project. Acceptance of a special order requires to be considered as additional costs need not be incurred if the special order is not accepted. Hence the importance of out-of-pocket costs.

• Marginal costs : It is the aggregate of variable costs, i.e., prime cost plus variable overheads. Thus, costs are classified as fixed and variable.

• Replacement costs : This is the cost of replacing an asset at current market values e.g. when the cost of replacing an asset is considered, it means the cost of purchasing the asset at the current market price is important and not the cost at which it was purchased.

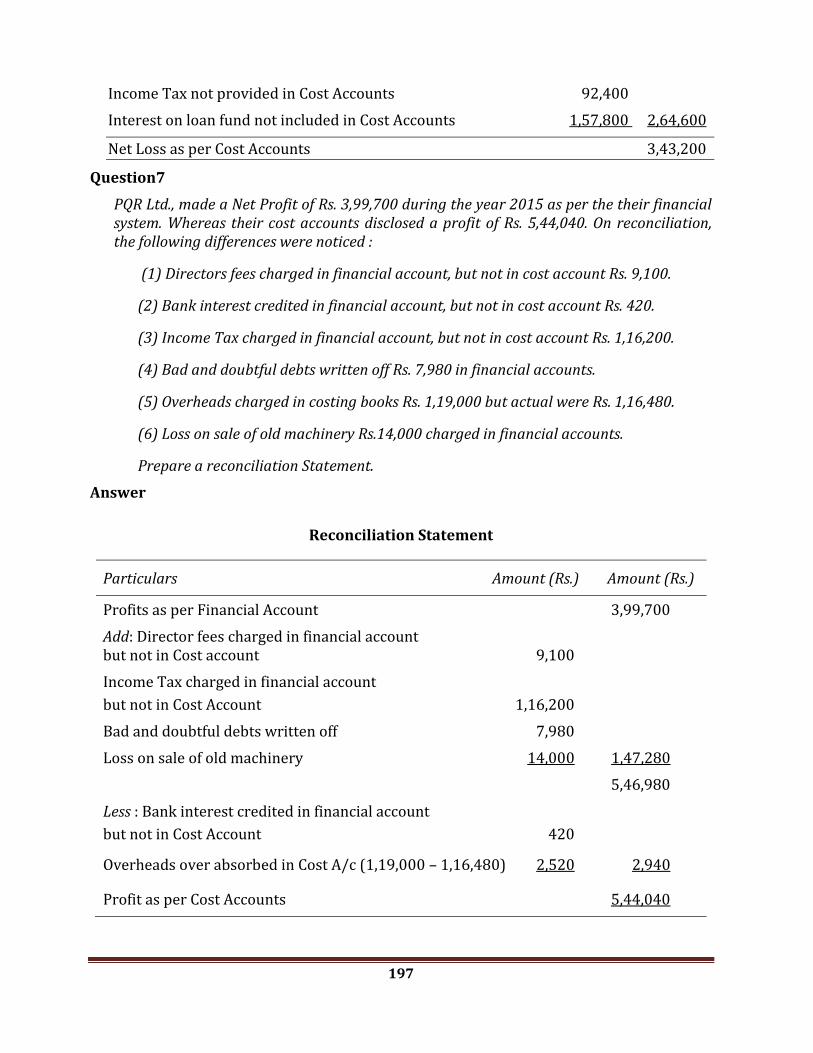

Question 7

“Management accounting is concerned with accounting information which is useful to management”. Comment.

Answer

According to CIMA, London : “Management accounting is an integral part of management concerned with identifying, presenting and interpreting information used for: (a) formulating strategy; (b) planning and controlling activities; (c) decision taking; (d) optimising the use of resources; (e) disclosure to shareholders and others external to the entity; (f) disclosure to employees; (g) safeguarding assets.

The fundamental objective of management accounting is to assist the management in carrying out its duties efficiently so that maximize profits or minimize losses of management.

The main objectives of management accounting are as follows:

1. To formulate Planning and policy

Planning involves forecasting on the basis of available information, setting goals; framing polices determining the alternative courses of action and deciding on the program of activities. It facilitate the preparation of statements in the light of past results and gives estimation for the future.

2. To interpretation of financial documents

Management accounting is to present financial information to the management. Financial information must be presented in such away that it is easily understood. It presents accounting information with the help of statistical devices like charts, diagrams, graphs, etc.

8

3. To assist in Decision-making process

Management accounting makes decision-making process more scientific with the help of various modern techniques. Information/figure relating to cost, price, profit and savings for each of the available alternatives are collected and analyzed accordingly which will provide a base for taking sound decisions.

4. To help in control

Management accounting is a helpful for managerial control. Management accounting tools e.g. standard costing and budgetary control are helpful in controlling performance. Cost control is affected through the use of standard costing and departmental control is made possible through the use of budgets. Performance of each and every individual is controlled with the help of management accounting.

5. To provide report

Management accounting keeps the management fully informed about the latest position of the concern through reporting. It helps management to take proper and quick decisions. It informs the performance of various departments regularly to the top management.

6. To Facilitate Coordination of Operations

Management accounting provides tools for overall control and coordination of business operations. Budgets are important means of coordination.

***

9

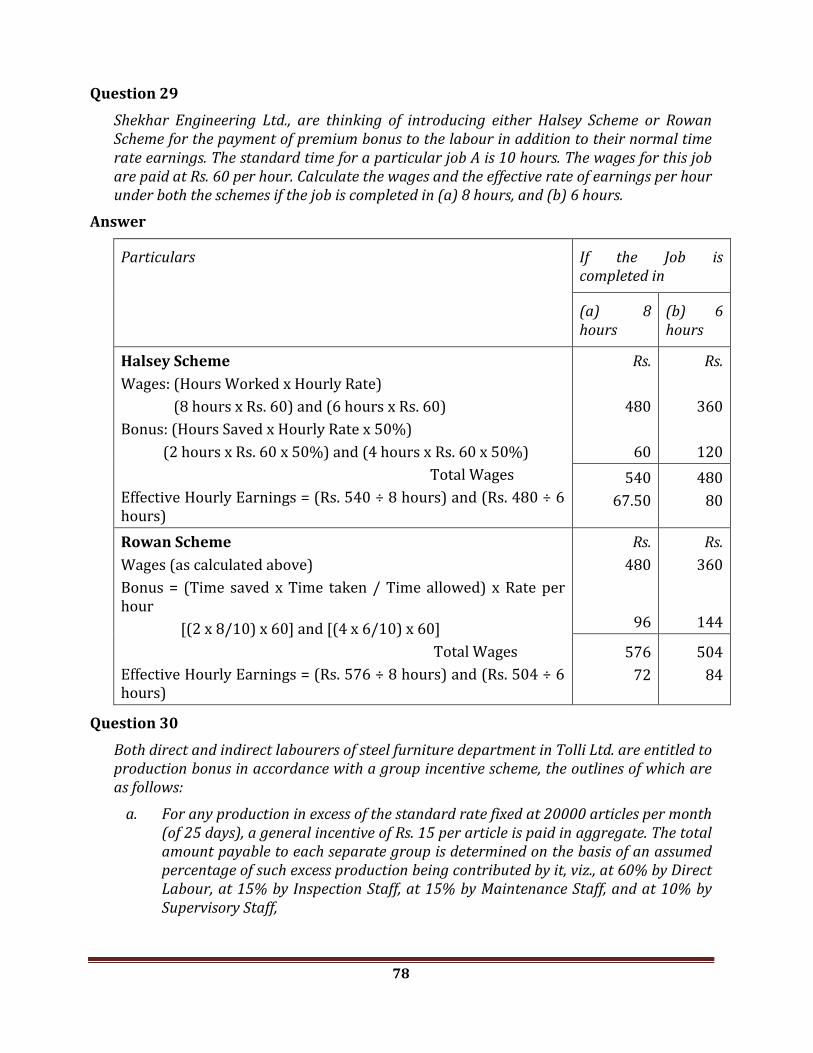

Question 1

Question 1

What are the different techniques of inventory control?

Answer

The following are the common techniques of inventory control:

(i) Min-max Plan

(ii) The two-bin System

(iii) Order Cycling System

(iv) ABC Analysis

(v) Fixation of various levels

(vi) Use of Perpetual Inventory System and Continuous Verifications

(vii) Use of Control Ratios

(viii) Review of Slow and Non-moving Items.

Question 2

Explain the concept of ’ABC Analysis’ as a technique of inventory control.

Answer

ABC Analysis is a system of selective inventory control whereby the measure of control

over an item of inventory varies with its usage value. It exercises discriminatory control

over different items of stores grouped on the basis of the investment involved. Usually the

items of material are grouped into three categories viz; A,B and C according to their use

value during a period. In other words, the high use value items are controlled more closely

than the items of low use value.

(i) ‘A’ Category of items consists of only a small percentage i. e., about 10% of the

total items of material handled by the stores but require heavy investment i. e.,

about 70% of inventory value, because of their high prices and heavy requirement.

(ii) ‘B’ Category of items comprises of about 20% of the total items of material

handled by stores. The percentage of investment required is about 20% of the

total investment in inventories.

2

Material Cost

10

(iii) ‘C’ Category of items does not require much investment. It may be about 10% of

total inventory value but they are nearly 70% of the total items handled by stores.

‘A’ Category of items can be controlled effectively by using a regular system ,which ensures

neither over-stocking nor shortage of materials for production. Such a system plans its

total material requirements by making budgets. The stocks of materials are controlled by

fixing certain levels like maximum level, minimum level and re-order level. A reduction in

inventory management costs is achieved by determining economic order quantities after

taking into account ordering cost and carrying cost. To avoid shortages and to minimize

heavy investment of funds in inventories, the techniques of value analysis, variety

reduction, standardization etc. are used along with aforesaid techniques.

In the case of ‘B’ category of items, as the sum involved is moderate, therefore, the same

degree of control as applied in ‘A’ category of items is not warranted. The order for the

items, belonging to this category may be placed after reviewing their situation periodically.

This category of items can be control by routine control measures.

For ‘C’ category of items, there is no need of exercising constant control. Orders for items in

this group may be placed either after six months or once in a year, after ascertaining

consumption requirements.

Question 3

Distinguish between Bin Card and Stores Ledger.

Answer

Difference between Bin Card and Stores Ledger

Bin Card Stores Ledger

It is a quantity record

It is kept inside the stores

It is maintained by the store-keeper

The postings are done before the transactions take place

Each transaction is individually posted

It is a record of quantity and value

It is kept outside the stores

It is maintained by the accounts department

The postings are done after the transactions take place

Transactions may be posted periodically and in total

Question 4

How will you treat the normal and abnormal losses of material arising during storage, in

cost accounting?

11

Answer

The difference between book balance and actual physical stock, which may either be gain

or loss, should be transferred to Inventory Adjustment Account pending scrutiny to

ascertain the reason for the difference.

If on scrutiny, the difference arrived at is considered as normal, then such a difference

should be transferred to overhead control account and if abnormal, it should be debited to

Costing Profit and Loss Account.

In case of normal losses, an alternative method may be used. Under this method the price of

the material issued to production may be inflated so as to cover the normal loss.

Question 5

What do you mean by scrap? How will you treat it in cost accounting?

Answer

Scrap

Scrap represents the unusable loss which can be sold. It is a residue which is measurable

and has a Minor value. It may result from the processing of materials, obsolete stock or

defective parts.The sale value is credited to the concerned department which produced it. If

the vale is negligible, it is credited to the Costing Profit and Loss Account.

Scrap may arise in the form of turnings, boring’s, filings etc. from metal; sawdust in timber

industry, off-cuts and cut pieces in leather industry.

Accounting Treatment

(i) Where the scrap has negligible value, it is charged to good units. Income is credited

to other income.

(ii) The sale value can be reduced from the material cost.

(iii) If the scrap is of very little value, then only a quantity record need be kept.

(iv) The cost is calculated by reducing the sale price by the selling cost and this sum is

taken as a credit to the production overhead account.

(v) Scrap arising in one job may be used in another. Such transfers should be properly

recorded on material transfer notes.

Question 6

What are defectives? Discuss the accounting treatment of defectives in cost accounting.

12

Answer

Defectives refers to those units or portion of production, which do not meet the prescribed

specifications. Such units can be reworked or re-conditioned by the use of additional

material, labour and/or processing and brought to the point of either standard or sub-

standard units.

The possible way of treating defectives in cost accounting are as follows:

(a) When defectives are normal and it is not beneficial to identity them job-wise, then

the following methods may be used—

1. Charged to good products: The cost of rectification of normal defectives is

charged to good units. This method is used when defectives rectified are

normal.

2. Charged to general overheads: If the department responsible for defectives

cannot be identified, the rework costs are charged to general overheads.

3. Charged to departmental overheads: If the department responsible for

defectives can be correctly identified, the rectification costs should be charged

to the department.

(b) When normal defectives are easily identifiable with specific job the rework costs

are debited to the identified job.

(c) When defectives are abnormal and due to uncontrollable factors,, the rework cost

should be charged to the Costing Profit and Loss Account.

Question 7

Explain why the Last in First out (LIFO) has an edge over First in First out (FIFO) or any

other method of pricing material issues.

Answer

LIFO has following advantages:

(a) The cost of the material issued will be reflecting the current market price.

(b) The use of the method during the period of rising prices does not reflect undue high

profit in the income statement.

(c) In the case of falling price, profit tend to rise due to lower material cost, yet the

finished goods appear to be more competitive and are at market price.

(d) During the period of inflation, LIFO will tend to show the correct profit.

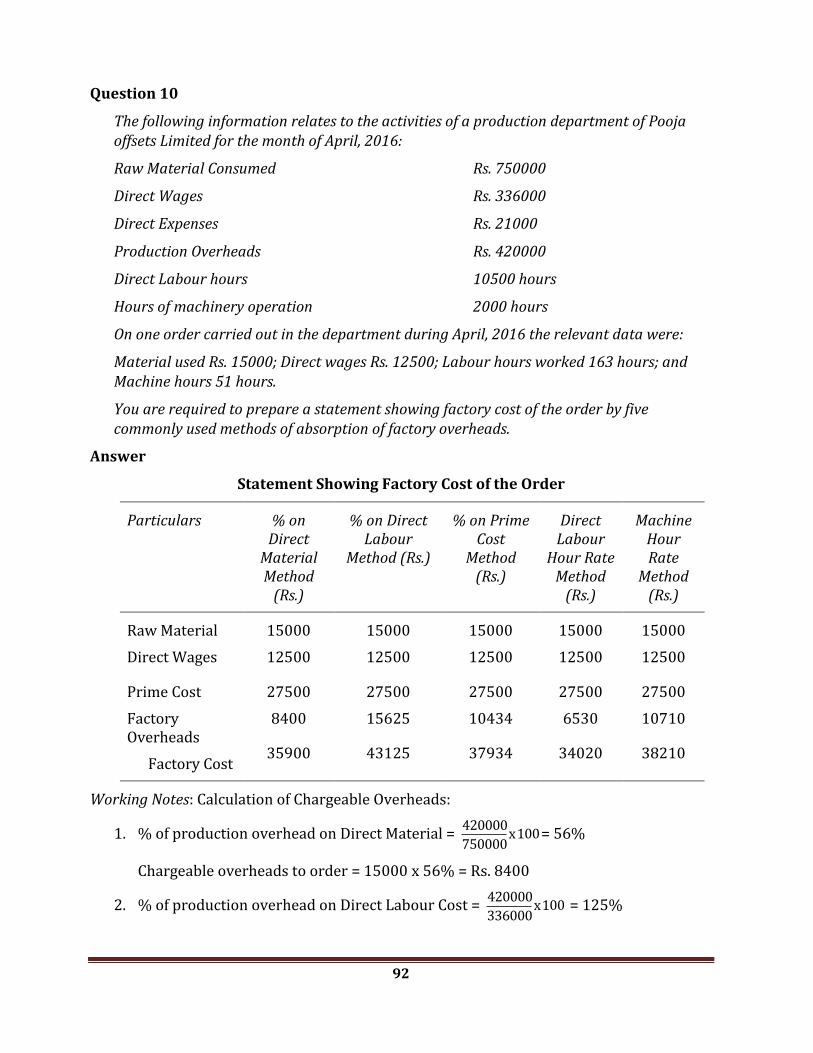

Question 8

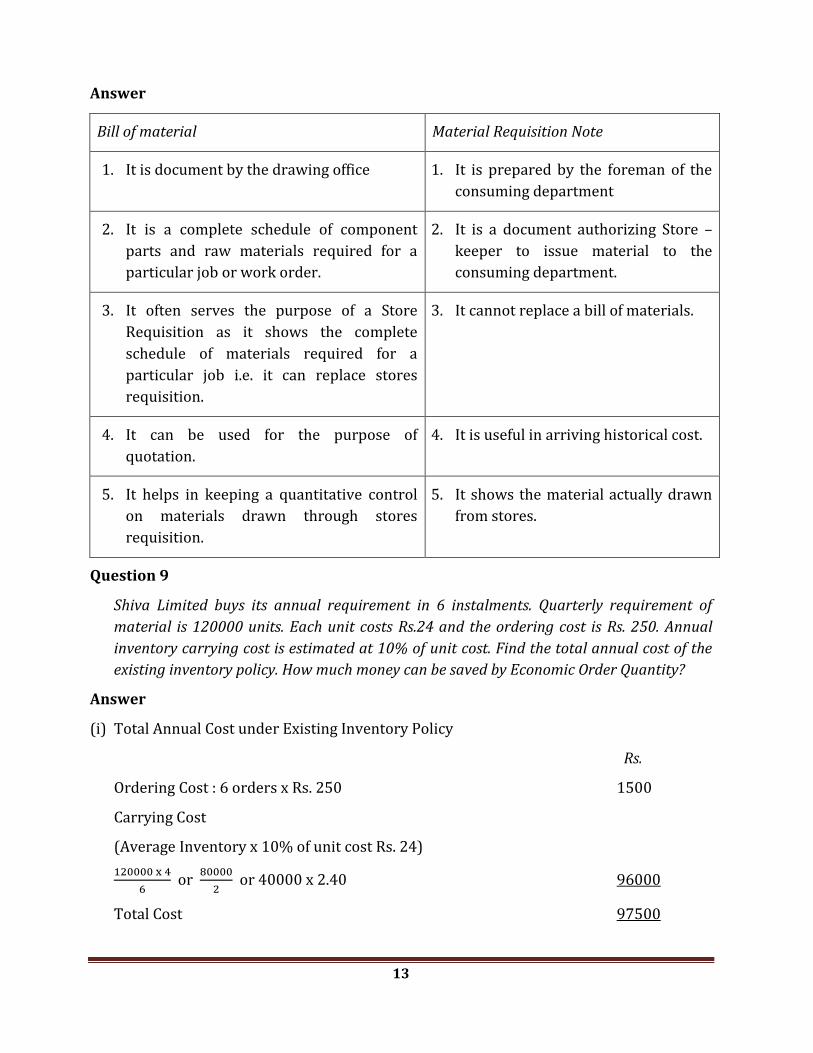

Distinguish between bill of material and material requisition note.

13

Answer

Bill of material Material Requisition Note

1. It is document by the drawing office 1. It is prepared by the foreman of the

consuming department

2. It is a complete schedule of component

parts and raw materials required for a

particular job or work order.

2. It is a document authorizing Store –

keeper to issue material to the

consuming department.

3. It often serves the purpose of a Store

Requisition as it shows the complete

schedule of materials required for a

particular job i.e. it can replace stores

requisition.

3. It cannot replace a bill of materials.

4. It can be used for the purpose of

quotation.

4. It is useful in arriving historical cost.

5. It helps in keeping a quantitative control

on materials drawn through stores

requisition.

5. It shows the material actually drawn

from stores.

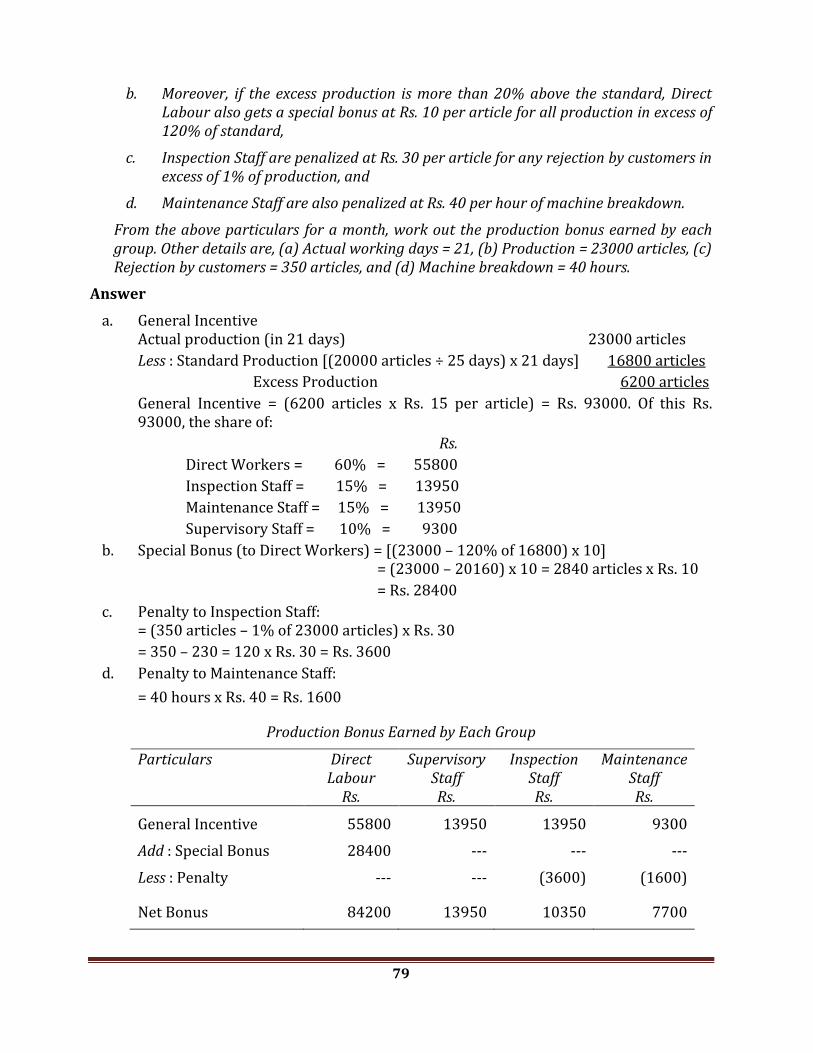

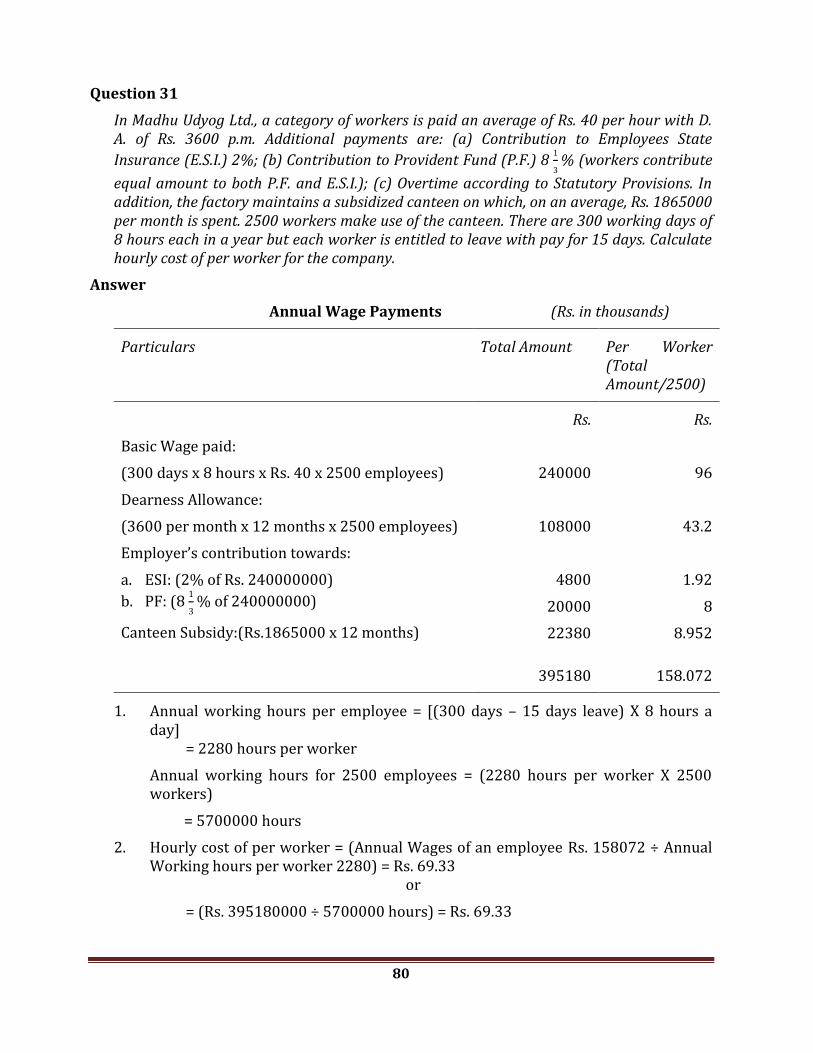

Question 9

Shiva Limited buys its annual requirement in 6 instalments. Quarterly requirement of

material is 120000 units. Each unit costs Rs.24 and the ordering cost is Rs. 250. Annual

inventory carrying cost is estimated at 10% of unit cost. Find the total annual cost of the

existing inventory policy. How much money can be saved by Economic Order Quantity?

Answer

(i) Total Annual Cost under Existing Inventory Policy

Rs.

Ordering Cost : 6 orders x Rs. 250 1500

Carrying Cost

(Average Inventory x 10% of unit cost Rs. 24)

or

or 40000 x 2.40 96000

Total Cost 97500

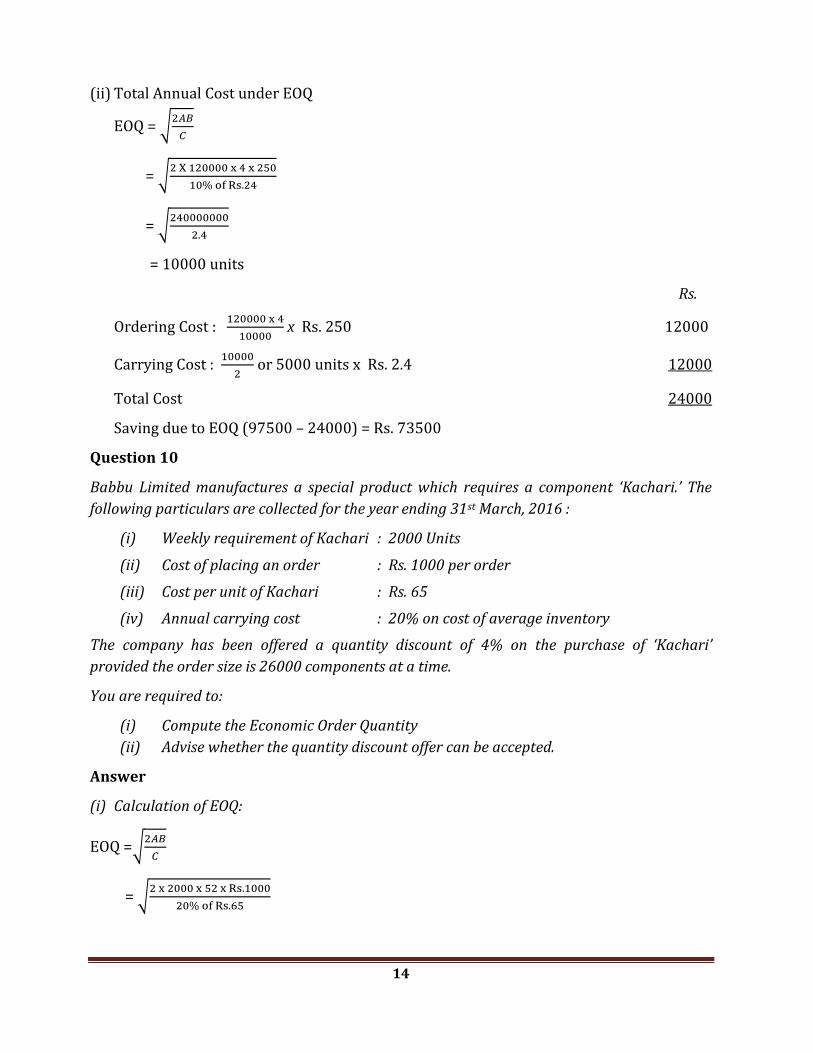

14

(ii) Total Annual Cost under EOQ

EOQ = √

= √

= √

= 10000 units

Rs.

Ordering Cost :

x Rs. 250 12000

Carrying Cost :

or 5000 units x Rs. 2.4 12000

Total Cost 24000

Saving due to EOQ (97500 – 24000) = Rs. 73500

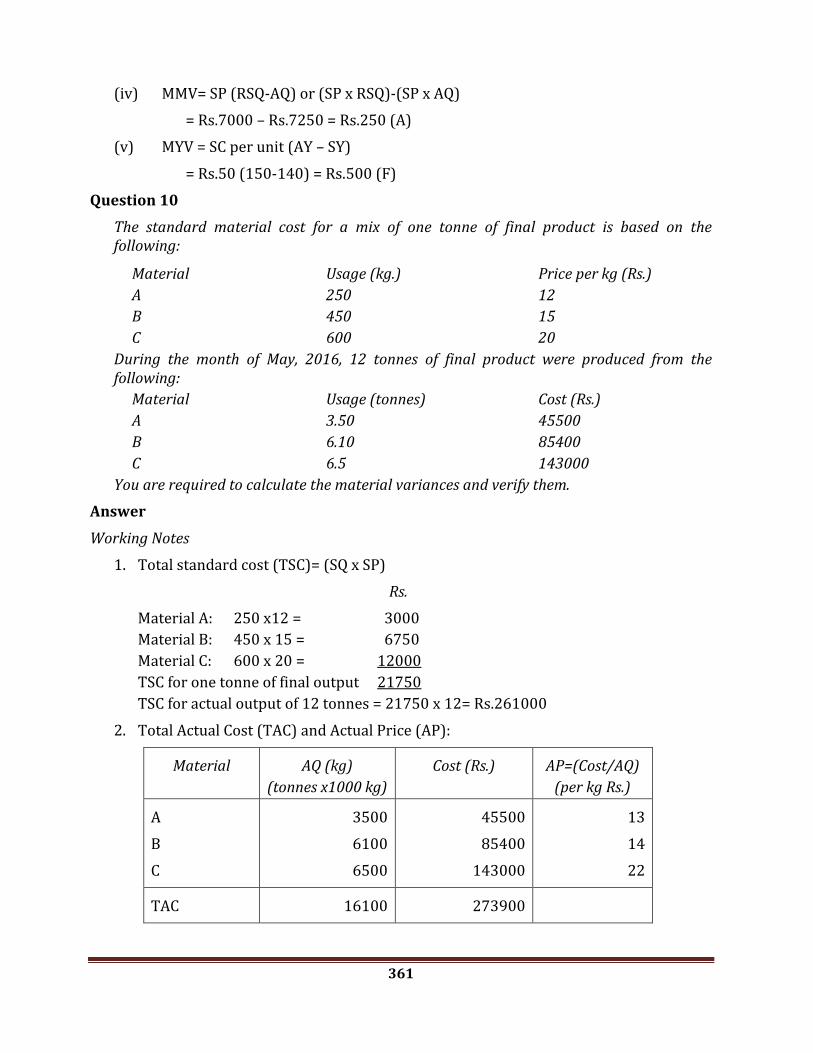

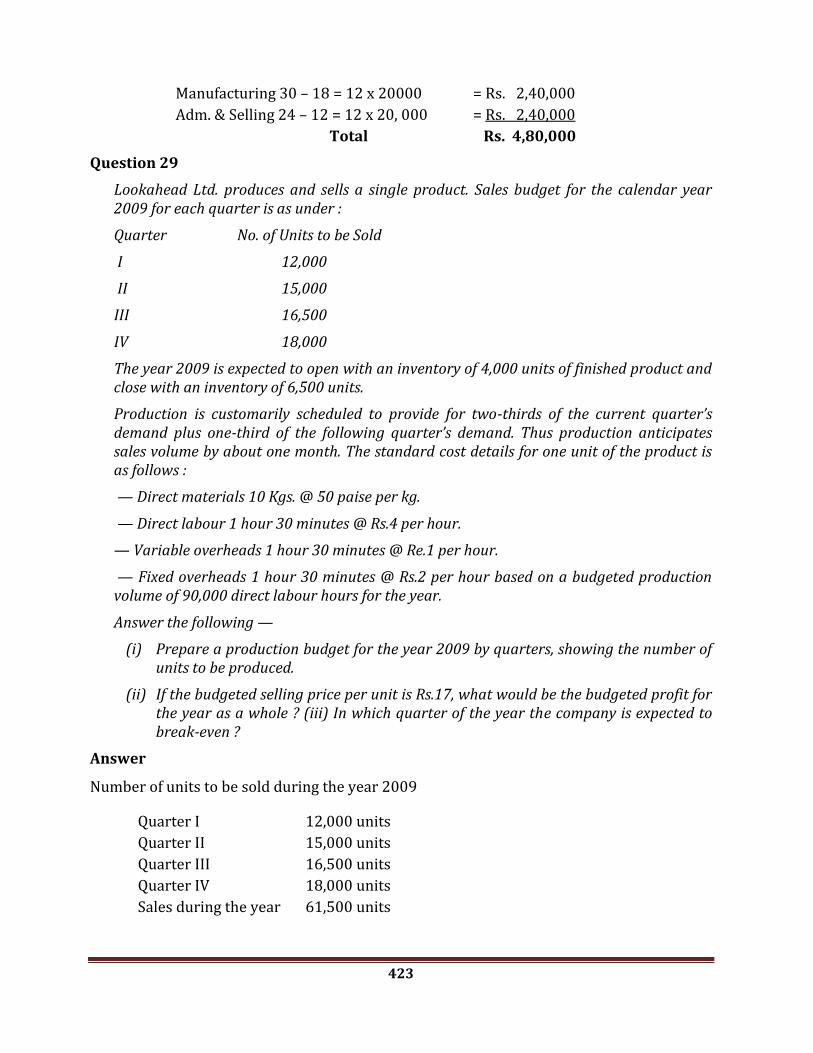

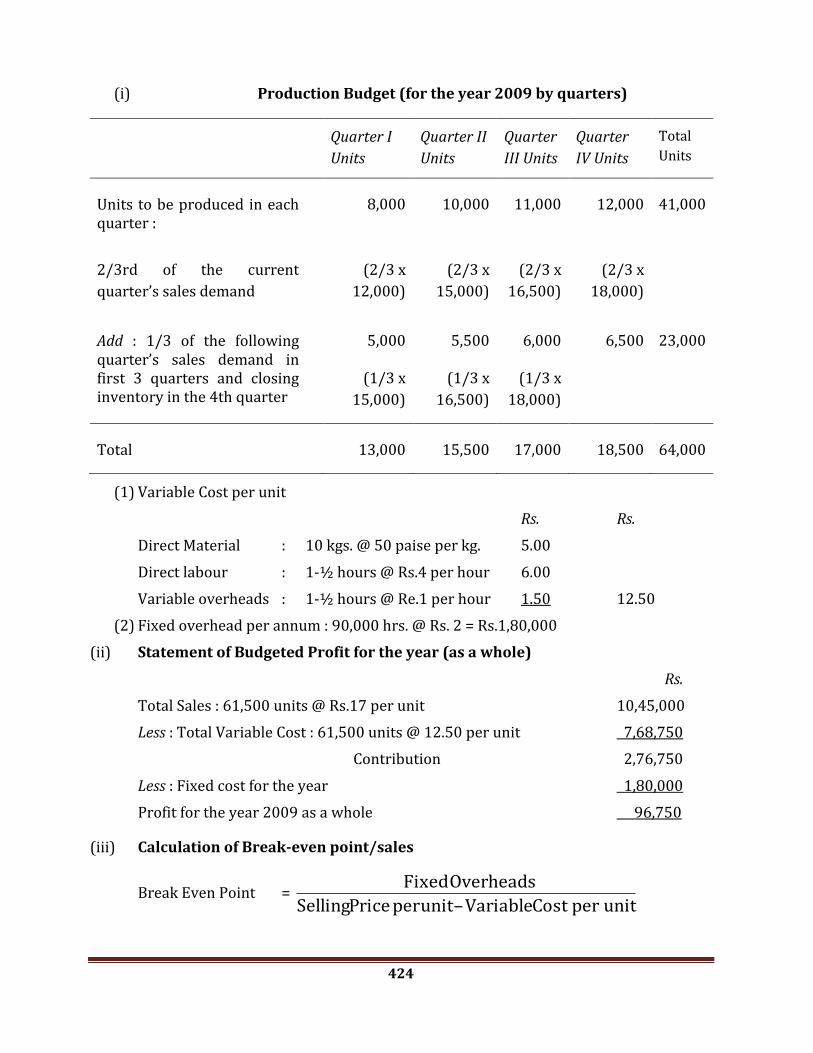

Question 10

Babbu Limited manufactures a special product which requires a component ‘Kachari.’ The

following particulars are collected for the year ending 31st March, 2016 :

(i) Weekly requirement of Kachari : 2000 Units

(ii) Cost of placing an order : Rs. 1000 per order

(iii) Cost per unit of Kachari : Rs. 65

(iv) Annual carrying cost : 20% on cost of average inventory

The company has been offered a quantity discount of 4% on the purchase of ‘Kachari’

provided the order size is 26000 components at a time.

You are required to:

(i) Compute the Economic Order Quantity

(ii) Advise whether the quantity discount offer can be accepted.

Answer

(i) Calculation of EOQ:

EOQ =√

= √

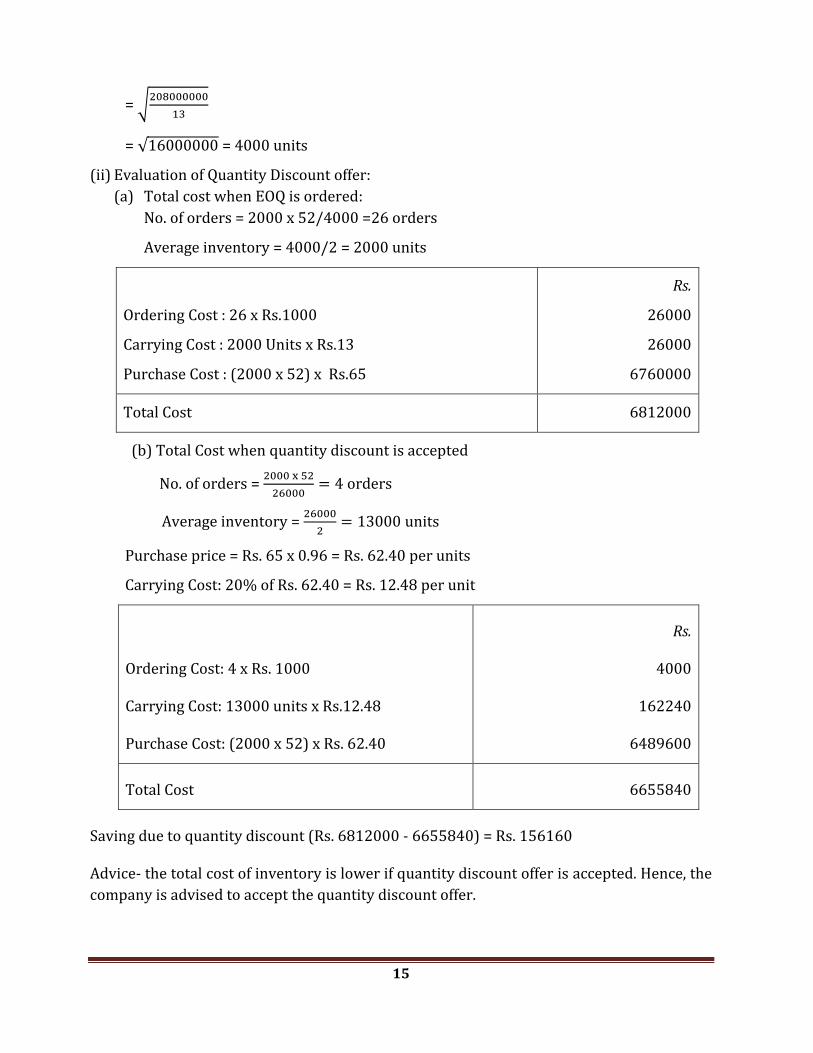

15

= √

= √ = 4000 units

(ii) Evaluation of Quantity Discount offer:

(a) Total cost when EOQ is ordered:

No. of orders = 2000 x 52/4000 =26 orders

Average inventory = 4000/2 = 2000 units

Ordering Cost : 26 x Rs.1000

Carrying Cost : 2000 Units x Rs.13

Purchase Cost : (2000 x 52) x Rs.65

Rs.

26000

26000

6760000

Total Cost 6812000

(b) Total Cost when quantity discount is accepted

No. of orders =

Average inventory =

Purchase price = Rs. 65 x 0.96 = Rs. 62.40 per units

Carrying Cost: 20% of Rs. 62.40 = Rs. 12.48 per unit

Ordering Cost: 4 x Rs. 1000

Carrying Cost: 13000 units x Rs.12.48

Purchase Cost: (2000 x 52) x Rs. 62.40

Rs.

4000

162240

6489600

Total Cost 6655840

Saving due to quantity discount (Rs. 6812000 - 6655840) = Rs. 156160

Advice- the total cost of inventory is lower if quantity discount offer is accepted. Hence, the

company is advised to accept the quantity discount offer.

16

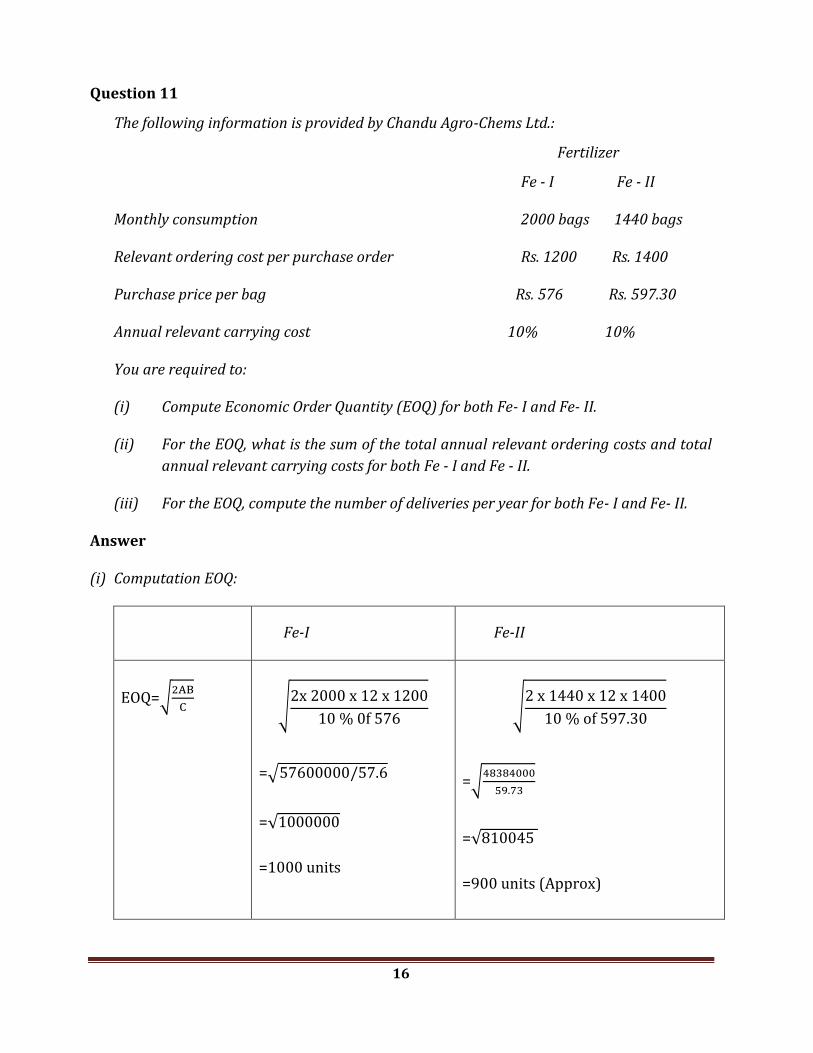

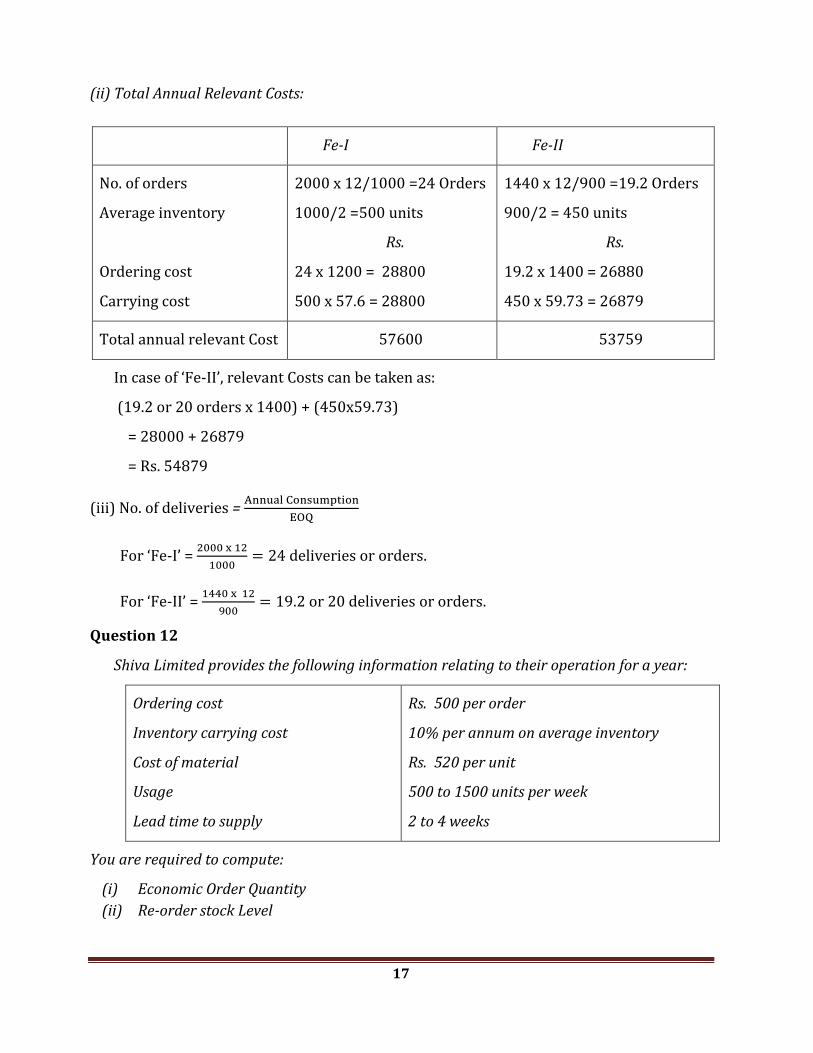

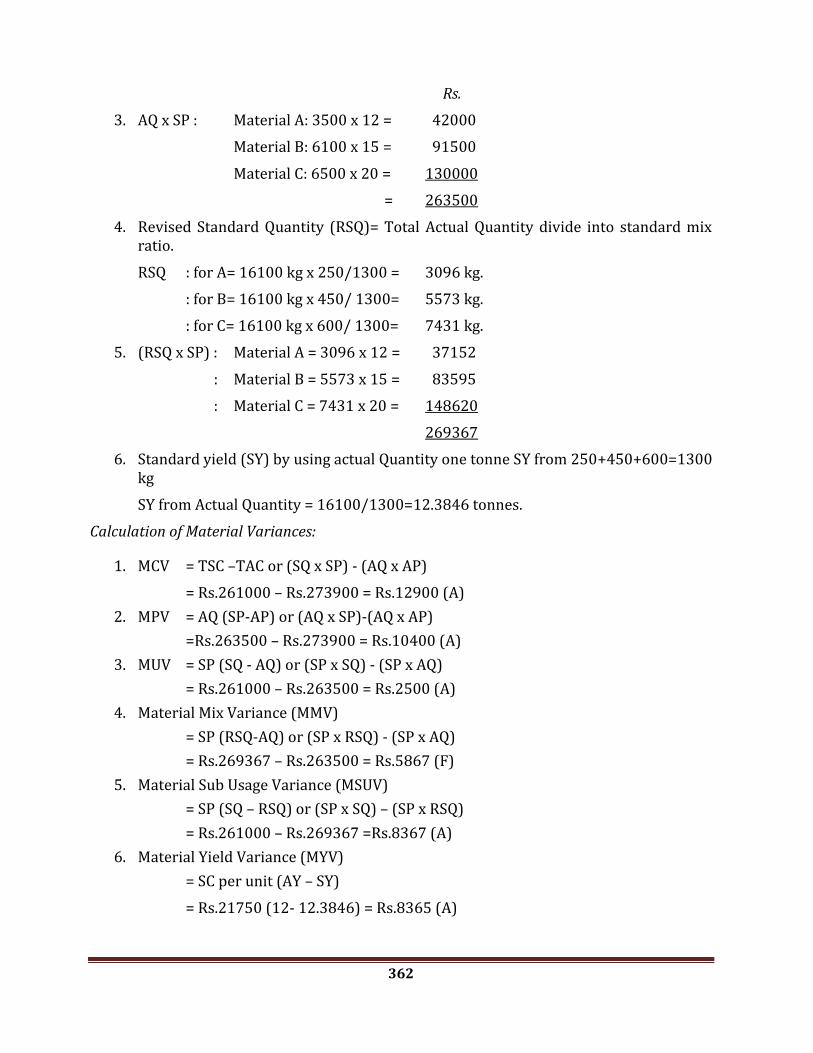

Question 11

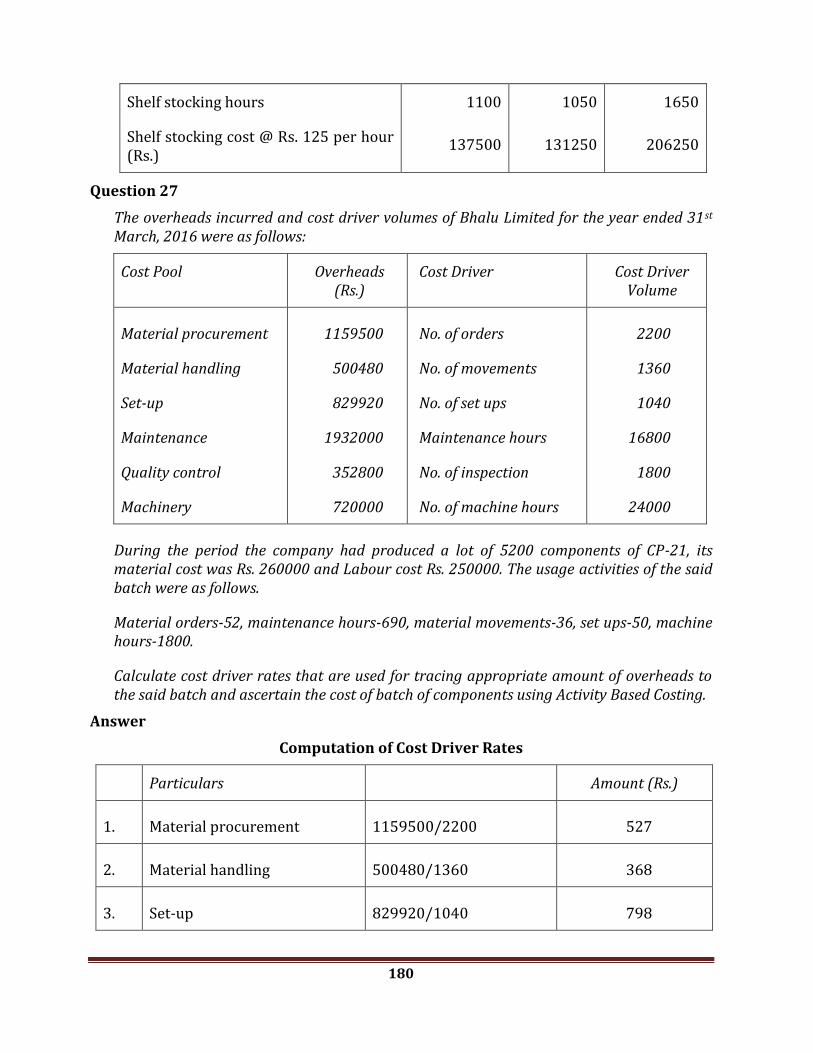

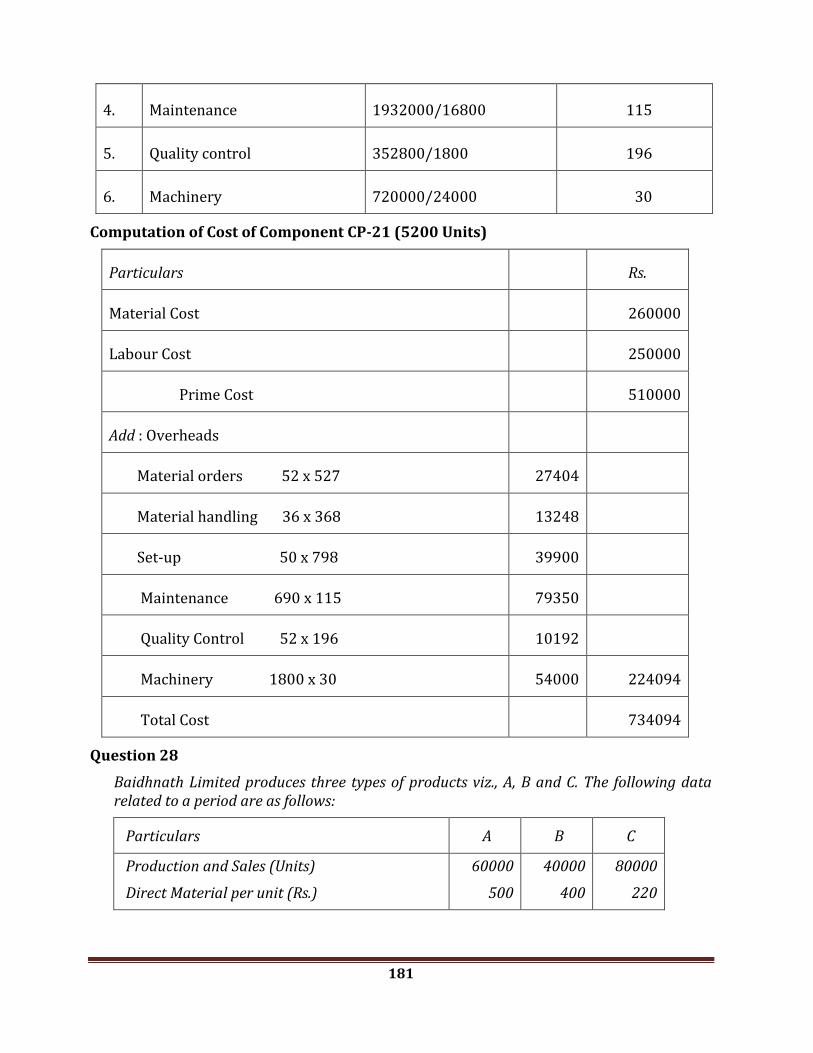

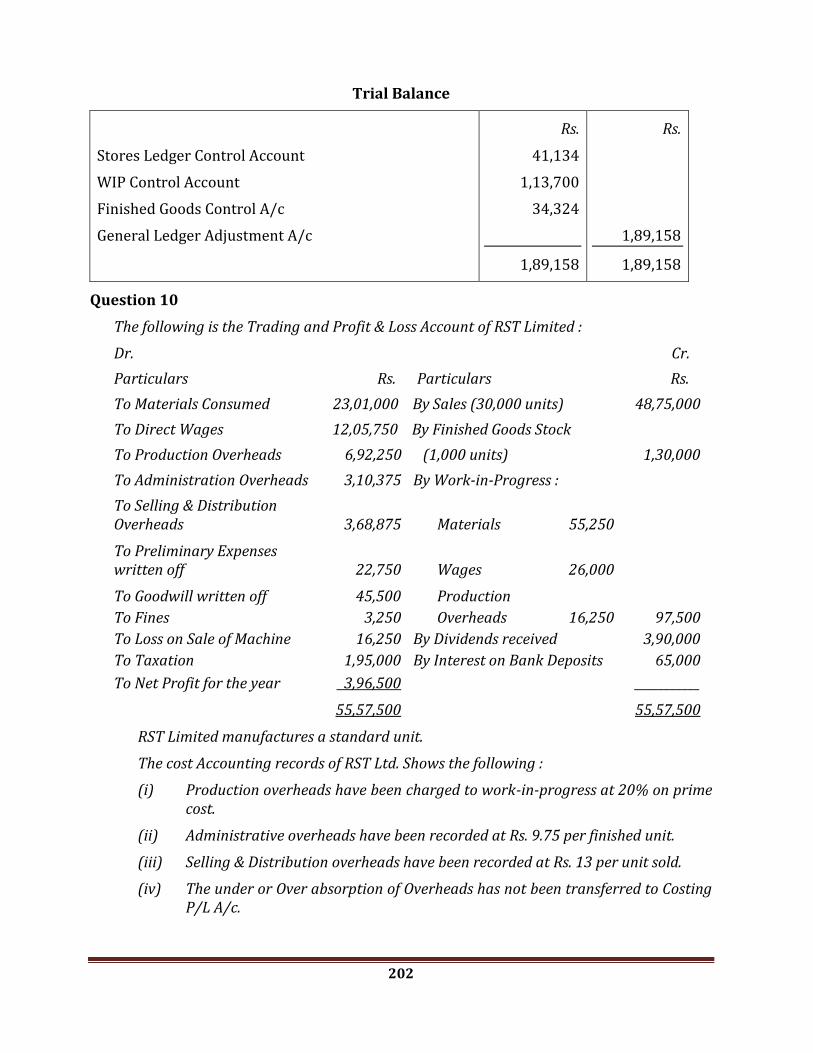

The following information is provided by Chandu Agro-Chems Ltd.:

Fertilizer

Fe - I Fe - II

Monthly consumption 2000 bags 1440 bags

Relevant ordering cost per purchase order Rs. 1200 Rs. 1400

Purchase price per bag Rs. 576 Rs. 597.30

Annual relevant carrying cost 10% 10%

You are required to:

(i) Compute Economic Order Quantity (EOQ) for both Fe- I and Fe- II.

(ii) For the EOQ, what is the sum of the total annual relevant ordering costs and total

annual relevant carrying costs for both Fe - I and Fe - II.

(iii) For the EOQ, compute the number of deliveries per year for both Fe- I and Fe- II.

Answer

(i) Computation EOQ:

Fe-I Fe-II

EOQ=√

√

=√

=√

=1000 units

√

=√

=√

=900 units (Approx)

17

(ii) Total Annual Relevant Costs:

Fe-I Fe-II

No. of orders

Average inventory

Ordering cost

Carrying cost

2000 x 12/1000 =24 Orders

1000/2 =500 units

Rs.

24 x 1200 = 28800

500 x 57.6 = 28800

1440 x 12/900 =19.2 Orders

900/2 = 450 units

Rs.

19.2 x 1400 = 26880

450 x 59.73 = 26879

Total annual relevant Cost 57600 53759

In case of ‘Fe-II’, relevant Costs can be taken as:

(19.2 or 20 orders x 1400) + (450x59.73)

= 28000 + 26879

= Rs. 54879

(iii) No. of deliveries =

For ‘Fe-I’ =

For ‘Fe-II’ =

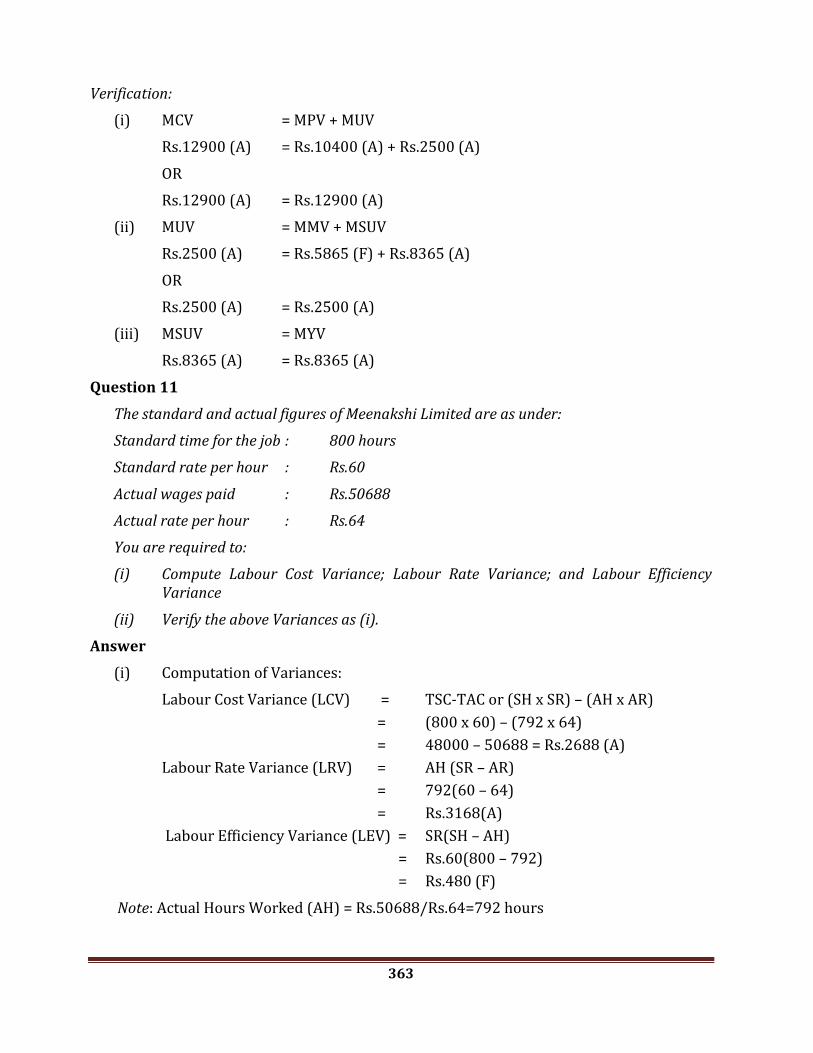

Question 12

Shiva Limited provides the following information relating to their operation for a year:

Ordering cost

Inventory carrying cost

Cost of material

Usage

Lead time to supply

Rs. 500 per order

10% per annum on average inventory

Rs. 520 per unit

500 to 1500 units per week

2 to 4 weeks

You are required to compute:

(i) Economic Order Quantity

(ii) Re-order stock Level

18

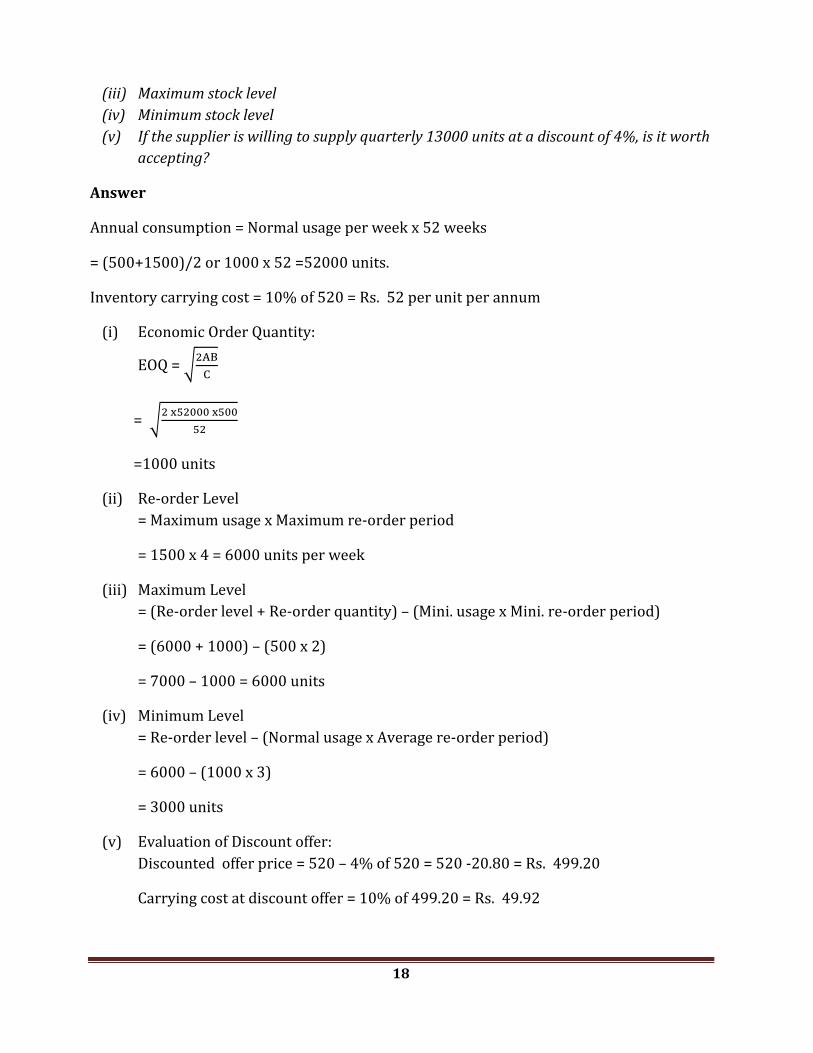

(iii) Maximum stock level

(iv) Minimum stock level

(v) If the supplier is willing to supply quarterly 13000 units at a discount of 4%, is it worth

accepting?

Answer

Annual consumption = Normal usage per week x 52 weeks

= (500+1500)/2 or 1000 x 52 =52000 units.

Inventory carrying cost = 10% of 520 = Rs. 52 per unit per annum

(i) Economic Order Quantity:

EOQ = √

= √

=1000 units

(ii) Re-order Level

= Maximum usage x Maximum re-order period

= 1500 x 4 = 6000 units per week

(iii) Maximum Level

= (Re-order level + Re-order quantity) – (Mini. usage x Mini. re-order period)

= (6000 + 1000) – (500 x 2)

= 7000 – 1000 = 6000 units

(iv) Minimum Level

= Re-order level – (Normal usage x Average re-order period)

= 6000 – (1000 x 3)

= 3000 units

(v) Evaluation of Discount offer:

Discounted offer price = 520 – 4% of 520 = 520 -20.80 = Rs. 499.20

Carrying cost at discount offer = 10% of 499.20 = Rs. 49.92

19

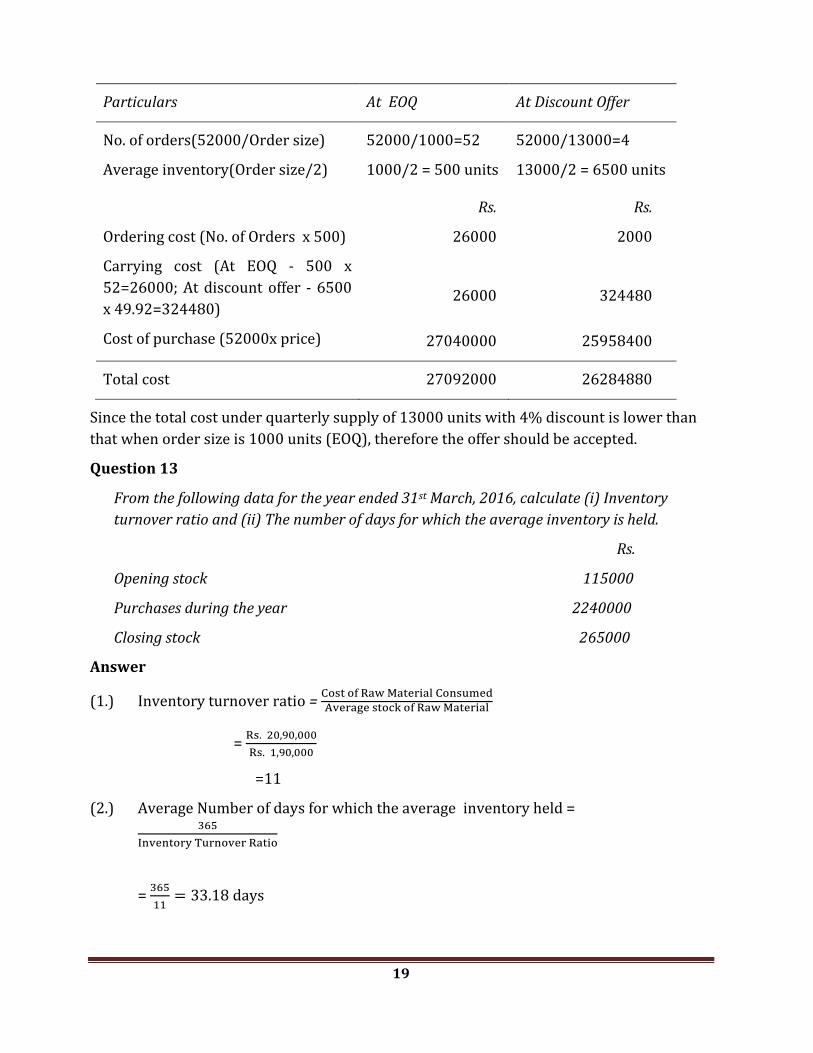

Particulars At EOQ At Discount Offer

No. of orders(52000/Order size)

Average inventory(Order size/2)

52000/1000=52

1000/2 = 500 units

52000/13000=4

13000/2 = 6500 units

Ordering cost (No. of Orders x 500)

Carrying cost (At EOQ - 500 x

52=26000; At discount offer - 6500

x 49.92=324480)

Cost of purchase (52000x price)

Rs.

26000

26000

27040000

Rs.

2000

324480

25958400

Total cost 27092000 26284880

Since the total cost under quarterly supply of 13000 units with 4% discount is lower than

that when order size is 1000 units (EOQ), therefore the offer should be accepted.

Question 13

From the following data for the year ended 31st March, 2016, calculate (i) Inventory

turnover ratio and (ii) The number of days for which the average inventory is held.

Rs.

Opening stock 115000

Purchases during the year 2240000

Closing stock 265000

Answer

(1.) Inventory turnover ratio =

=

=11

(2.) Average Number of days for which the average inventory held =

=

20

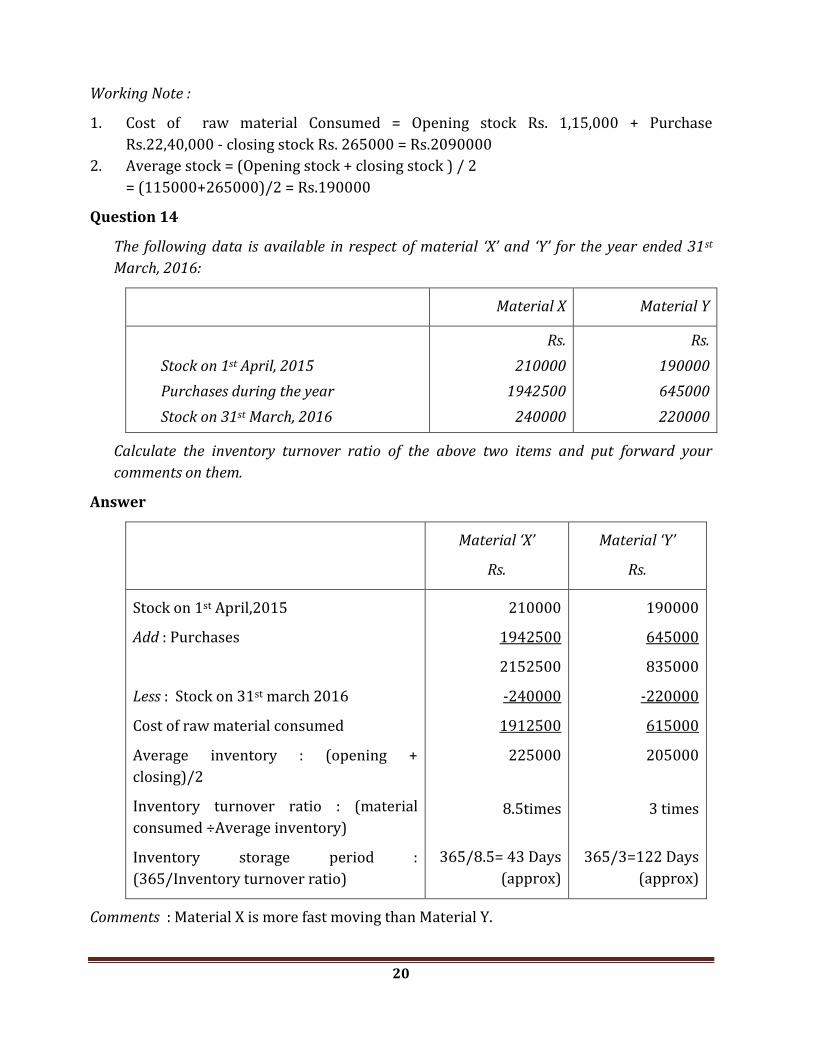

Working Note :

1. Cost of raw material Consumed = Opening stock Rs. 1,15,000 + Purchase

Rs.22,40,000 - closing stock Rs. 265000 = Rs.2090000

2. Average stock = (Opening stock + closing stock ) / 2

= (115000+265000)/2 = Rs.190000

Question 14

The following data is available in respect of material ‘X’ and ‘Y’ for the year ended 31st

March, 2016:

Material X Material Y

Stock on 1st April, 2015

Purchases during the year

Stock on 31st March, 2016

Rs.

210000

1942500

240000

Rs.

190000

645000

220000

Calculate the inventory turnover ratio of the above two items and put forward your

comments on them.

Answer

Material ‘X’

Rs.

Material ‘Y’

Rs.

Stock on 1st April,2015

Add : Purchases

Less : Stock on 31st march 2016

Cost of raw material consumed

Average inventory : (opening +

closing)/2

Inventory turnover ratio : (material

consumed ÷Average inventory)

Inventory storage period :

(365/Inventory turnover ratio)

210000

1942500

2152500

-240000

1912500

225000

8.5times

365/8.5= 43 Days

(approx)

190000

645000

835000

-220000

615000

205000

3 times

365/3=122 Days

(approx)

Comments : Material X is more fast moving than Material Y.

21

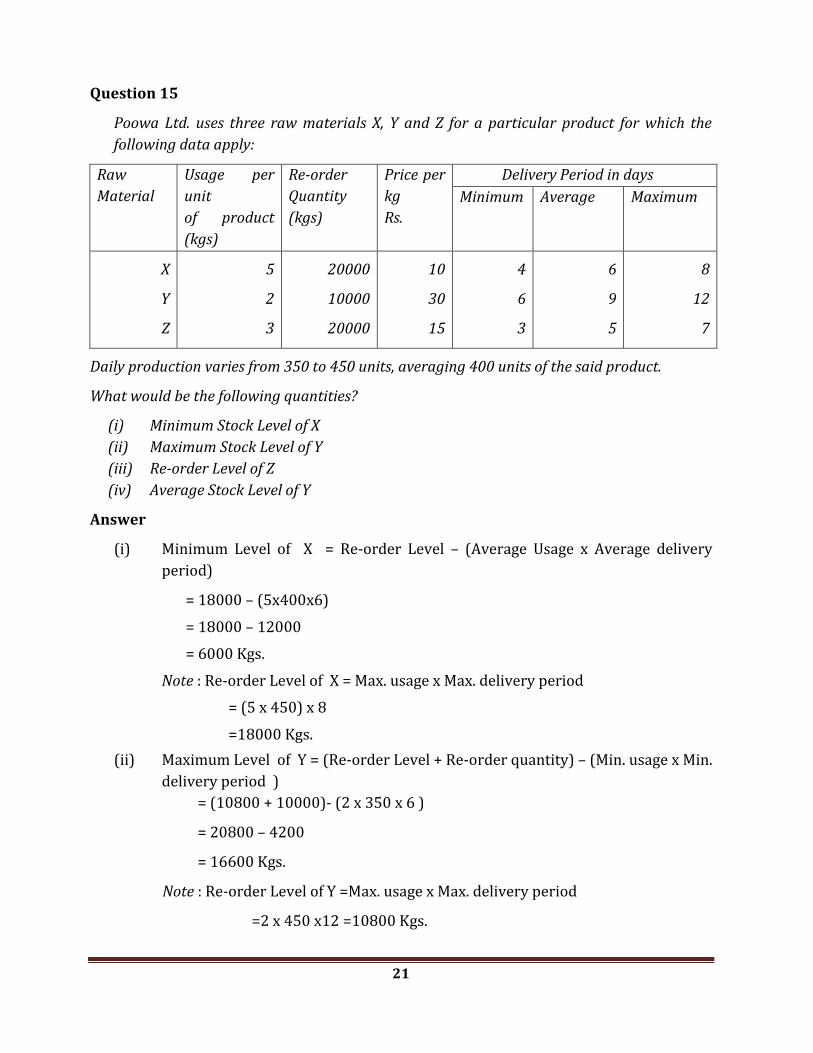

Question 15

Poowa Ltd. uses three raw materials X, Y and Z for a particular product for which the

following data apply:

Raw

Material

Usage per

unit

of product

(kgs)

Re-order

Quantity

(kgs)

Price per

kg

Rs.

Delivery Period in days

Minimum Average Maximum

X

Y

Z

5

2

3

20000

10000

20000

10

30

15

4

6

3

6

9

5

8

12

7

Daily production varies from 350 to 450 units, averaging 400 units of the said product.

What would be the following quantities?

(i) Minimum Stock Level of X

(ii) Maximum Stock Level of Y

(iii) Re-order Level of Z

(iv) Average Stock Level of Y

Answer

(i) Minimum Level of X = Re-order Level – (Average Usage x Average delivery

period)

= 18000 – (5x400x6)

= 18000 – 12000

= 6000 Kgs.

Note : Re-order Level of X = Max. usage x Max. delivery period

= (5 x 450) x 8

=18000 Kgs.

(ii) Maximum Level of Y = (Re-order Level + Re-order quantity) – (Min. usage x Min.

delivery period )

= (10800 + 10000)- (2 x 350 x 6 )

= 20800 – 4200

= 16600 Kgs.

Note : Re-order Level of Y =Max. usage x Max. delivery period

=2 x 450 x12 =10800 Kgs.

22

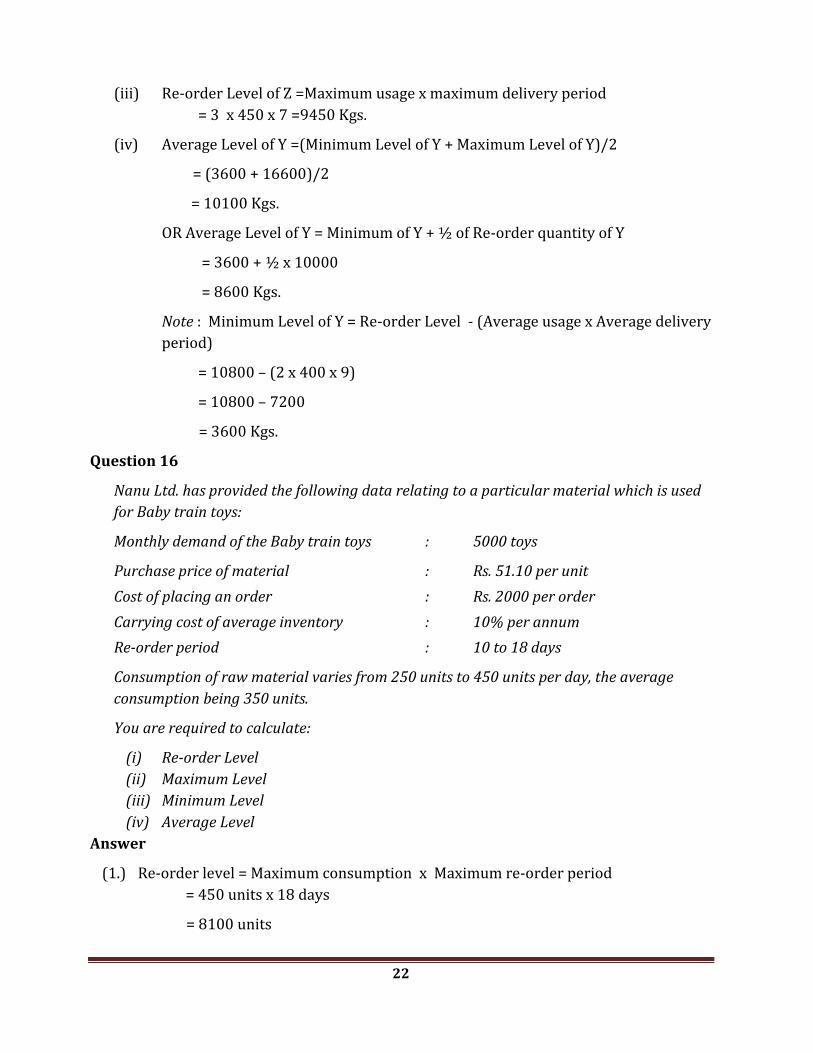

(iii) Re-order Level of Z =Maximum usage x maximum delivery period

= 3 x 450 x 7 =9450 Kgs.

(iv) Average Level of Y =(Minimum Level of Y + Maximum Level of Y)/2

= (3600 + 16600)/2

= 10100 Kgs.

OR Average Level of Y = Minimum of Y + ½ of Re-order quantity of Y

= 3600 + ½ x 10000

= 8600 Kgs.

Note : Minimum Level of Y = Re-order Level - (Average usage x Average delivery

period)

= 10800 – (2 x 400 x 9)

= 10800 – 7200

= 3600 Kgs.

Question 16

Nanu Ltd. has provided the following data relating to a particular material which is used

for Baby train toys:

Monthly demand of the Baby train toys : 5000 toys

Purchase price of material : Rs. 51.10 per unit

Cost of placing an order : Rs. 2000 per order

Carrying cost of average inventory : 10% per annum

Re-order period : 10 to 18 days

Consumption of raw material varies from 250 units to 450 units per day, the average

consumption being 350 units.

You are required to calculate:

(i) Re-order Level

(ii) Maximum Level

(iii) Minimum Level

(iv) Average Level

Answer

(1.) Re-order level = Maximum consumption x Maximum re-order period

= 450 units x 18 days

= 8100 units

23

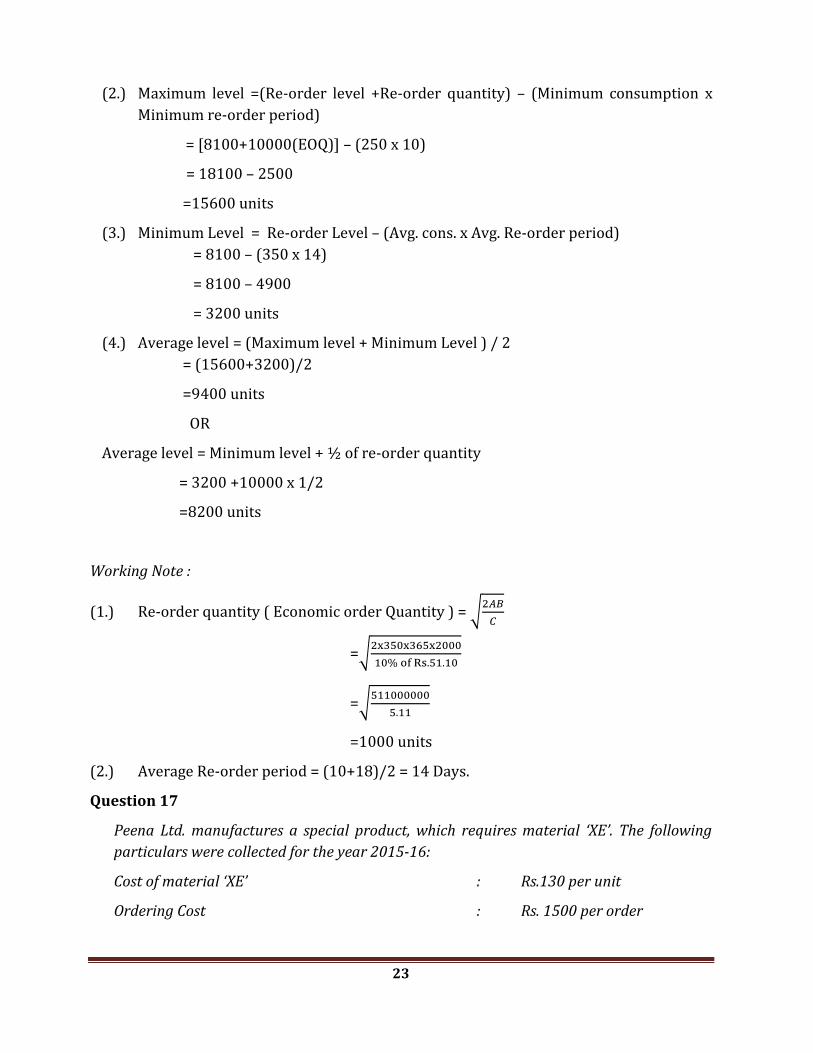

(2.) Maximum level =(Re-order level +Re-order quantity) – (Minimum consumption x

Minimum re-order period)

= [8100+10000(EOQ)] – (250 x 10)

= 18100 – 2500

=15600 units

(3.) Minimum Level = Re-order Level – (Avg. cons. x Avg. Re-order period)

= 8100 – (350 x 14)

= 8100 – 4900

= 3200 units

(4.) Average level = (Maximum level + Minimum Level ) / 2

= (15600+3200)/2

=9400 units

OR

Average level = Minimum level + ½ of re-order quantity

= 3200 +10000 x 1/2

=8200 units

Working Note :

(1.) Re-order quantity ( Economic order Quantity ) = √

=√

=√

=1000 units

(2.) Average Re-order period = (10+18)/2 = 14 Days.

Question 17

Peena Ltd. manufactures a special product, which requires material ‘XE’. The following

particulars were collected for the year 2015-16:

Cost of material ‘XE’ : Rs.130 per unit

Ordering Cost : Rs. 1500 per order

24

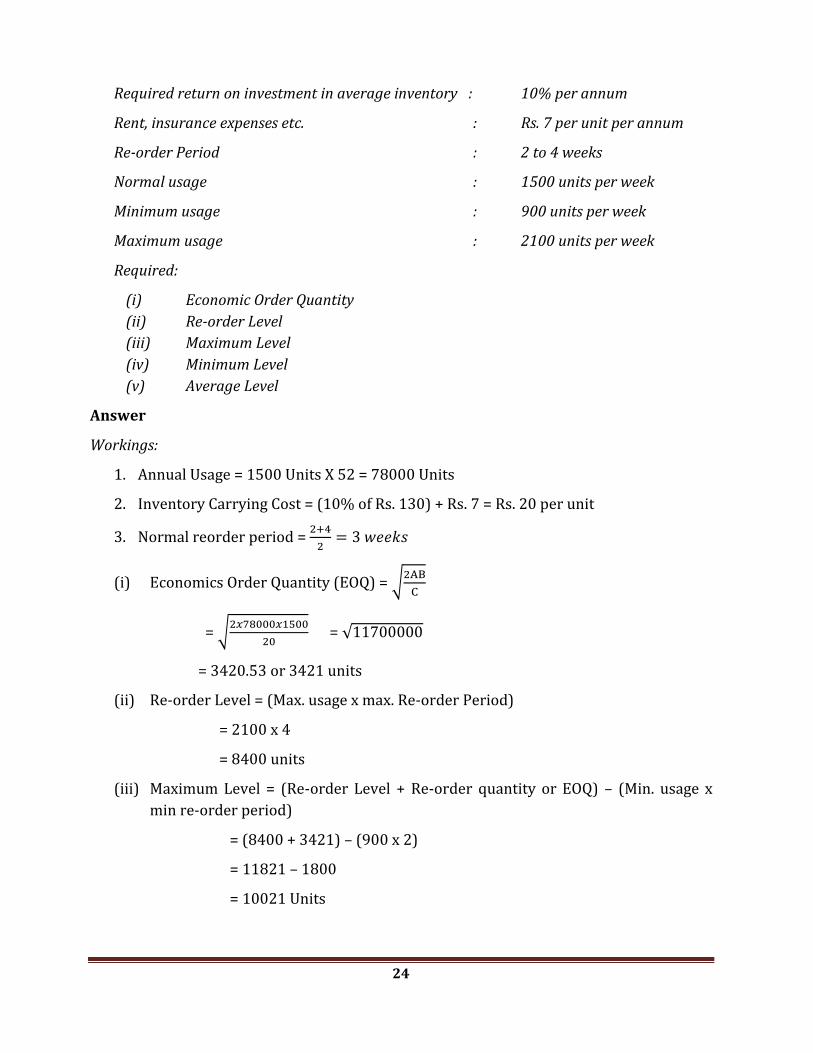

Required return on investment in average inventory : 10% per annum

Rent, insurance expenses etc. : Rs. 7 per unit per annum

Re-order Period : 2 to 4 weeks

Normal usage : 1500 units per week

Minimum usage : 900 units per week

Maximum usage : 2100 units per week

Required:

(i) Economic Order Quantity

(ii) Re-order Level

(iii) Maximum Level

(iv) Minimum Level

(v) Average Level

Answer

Workings:

1. Annual Usage = 1500 Units X 52 = 78000 Units

2. Inventory Carrying Cost = (10% of Rs. 130) + Rs. 7 = Rs. 20 per unit

3. Normal reorder period =

(i) Economics Order Quantity (EOQ) = √

= √

= √

= 3420.53 or 3421 units

(ii) Re-order Level = (Max. usage x max. Re-order Period)

= 2100 x 4

= 8400 units

(iii) Maximum Level = (Re-order Level + Re-order quantity or EOQ) – (Min. usage x

min re-order period)

= (8400 + 3421) – (900 x 2)

= 11821 – 1800

= 10021 Units

25

(iv) Minimum level = Re-order level – (Normal usage x Normal re-order period)

= 8400 – (1500 x 3)

= 8400 – 4500

= 3900 Units

Average level = (Minimum level + maximum level) /2

= (3900 + 10021) / 2

= 6960.5 or 6961 Units

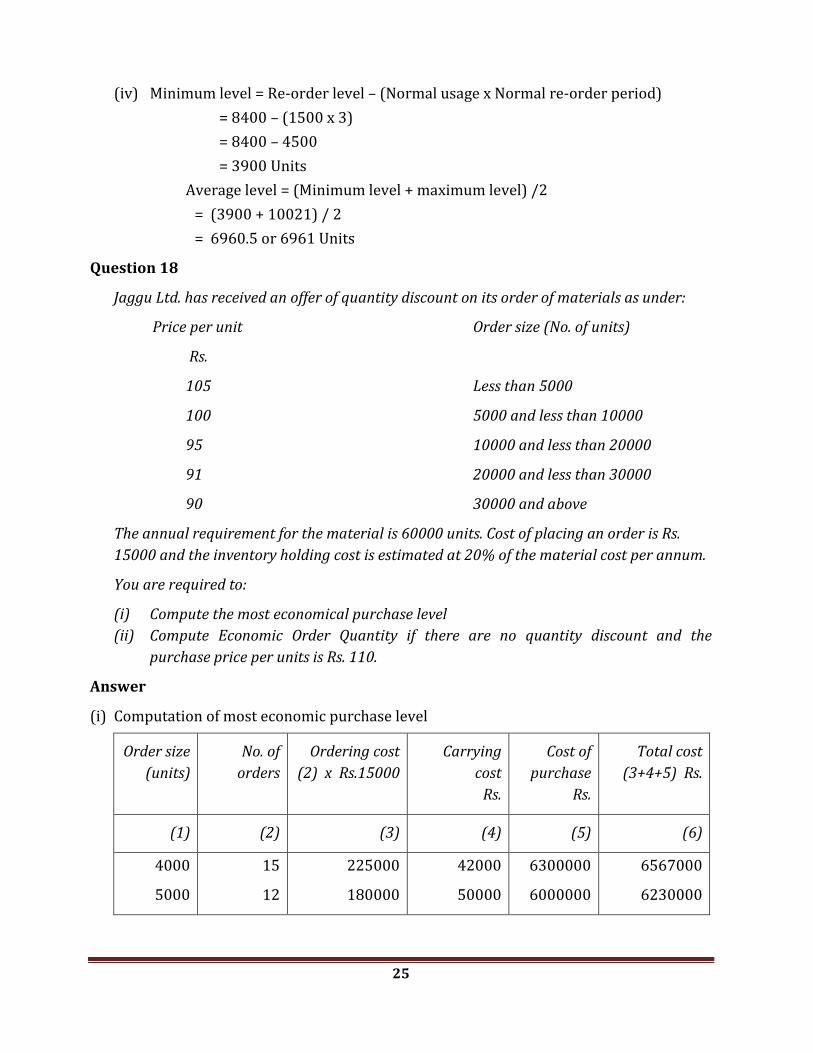

Question 18

Jaggu Ltd. has received an offer of quantity discount on its order of materials as under:

Price per unit Order size (No. of units)

Rs.

105 Less than 5000

100 5000 and less than 10000

95 10000 and less than 20000

91 20000 and less than 30000

90 30000 and above

The annual requirement for the material is 60000 units. Cost of placing an order is Rs.

15000 and the inventory holding cost is estimated at 20% of the material cost per annum.

You are required to:

(i) Compute the most economical purchase level

(ii) Compute Economic Order Quantity if there are no quantity discount and the

purchase price per units is Rs. 110.

Answer

(i) Computation of most economic purchase level

Order size

(units)

No. of

orders

Ordering cost

(2) x Rs.15000

Carrying

cost

Rs.

Cost of

purchase

Rs.

Total cost

(3+4+5) Rs.

(1) (2) (3) (4) (5) (6)

4000

5000

15

12

225000

180000

42000

50000

6300000

6000000

6567000

6230000

26

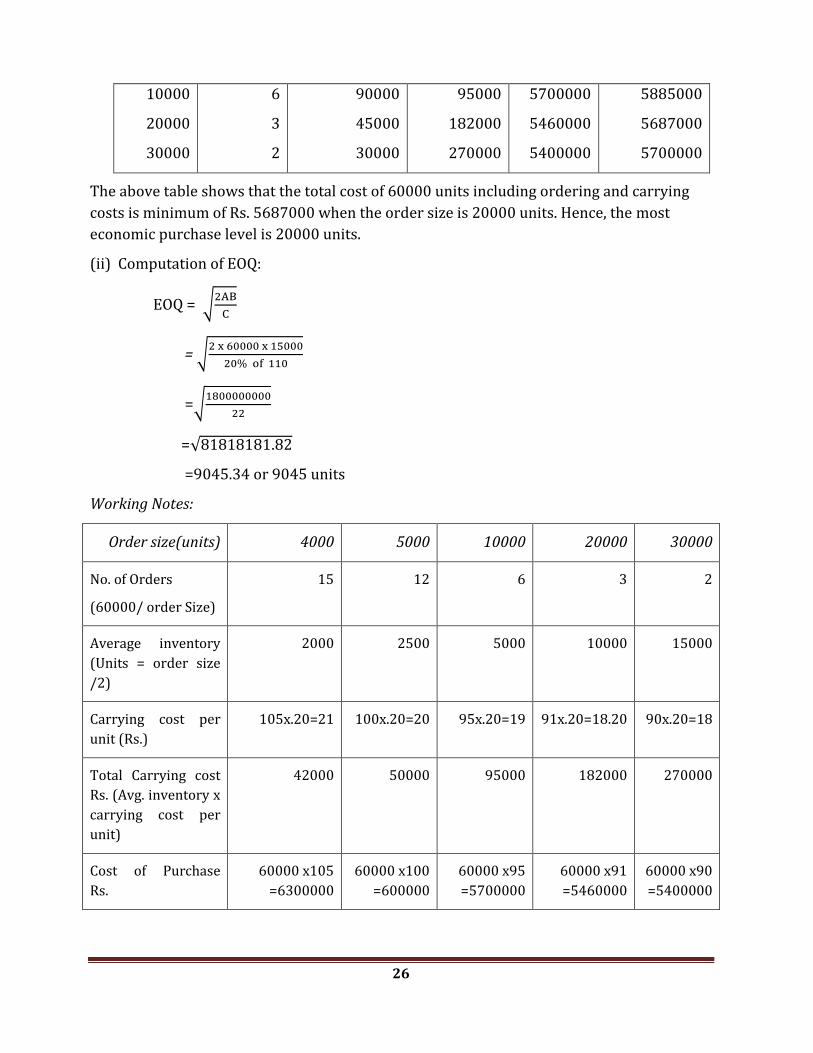

10000

20000

30000

6

3

2

90000

45000

30000

95000

182000

270000

5700000

5460000

5400000

5885000

5687000

5700000

The above table shows that the total cost of 60000 units including ordering and carrying

costs is minimum of Rs. 5687000 when the order size is 20000 units. Hence, the most

economic purchase level is 20000 units.

(ii) Computation of EOQ:

EOQ = √

= √

=√

=√

=9045.34 or 9045 units

Working Notes:

Order size(units) 4000 5000 10000 20000 30000

No. of Orders

(60000/ order Size)

15 12 6 3 2

Average inventory

(Units = order size

/2)

2000 2500 5000 10000 15000

Carrying cost per

unit (Rs.)

105x.20=21 100x.20=20 95x.20=19 91x.20=18.20 90x.20=18

Total Carrying cost

Rs. (Avg. inventory x

carrying cost per

unit)

42000 50000 95000 182000 270000

Cost of Purchase

Rs.

60000 x105

=6300000

60000 x100

=600000

60000 x95

=5700000

60000 x91

=5460000

60000 x90

=5400000

27

Question 19

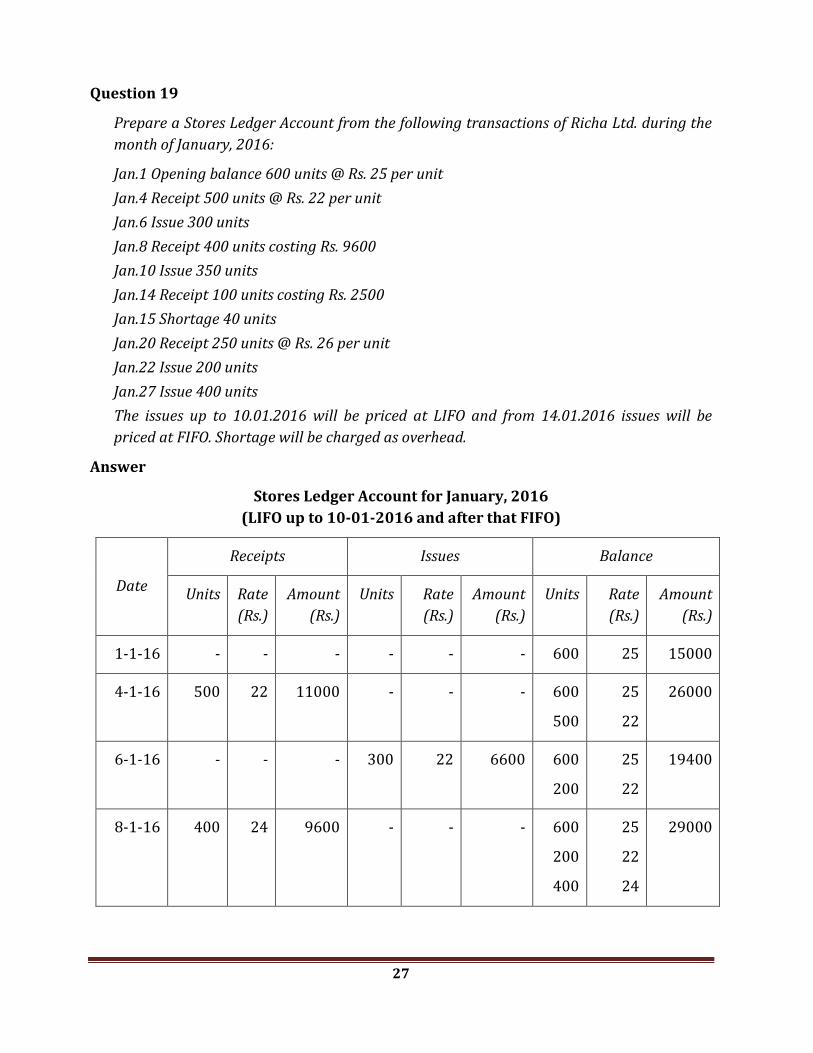

Prepare a Stores Ledger Account from the following transactions of Richa Ltd. during the

month of January, 2016:

Jan.1 Opening balance 600 units @ Rs. 25 per unit

Jan.4 Receipt 500 units @ Rs. 22 per unit

Jan.6 Issue 300 units

Jan.8 Receipt 400 units costing Rs. 9600

Jan.10 Issue 350 units

Jan.14 Receipt 100 units costing Rs. 2500

Jan.15 Shortage 40 units

Jan.20 Receipt 250 units @ Rs. 26 per unit

Jan.22 Issue 200 units

Jan.27 Issue 400 units

The issues up to 10.01.2016 will be priced at LIFO and from 14.01.2016 issues will be

priced at FIFO. Shortage will be charged as overhead.

Answer

Stores Ledger Account for January, 2016

(LIFO up to 10-01-2016 and after that FIFO)

Date

Receipts Issues Balance

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Amount

(Rs.)

1-1-16 - - - - - - 600 25 15000

4-1-16 500 22 11000 - - - 600

500

25

22

26000

6-1-16 - - - 300 22 6600 600

200

25

22

19400

8-1-16 400 24 9600 - - - 600

200

400

25

22

24

29000

28

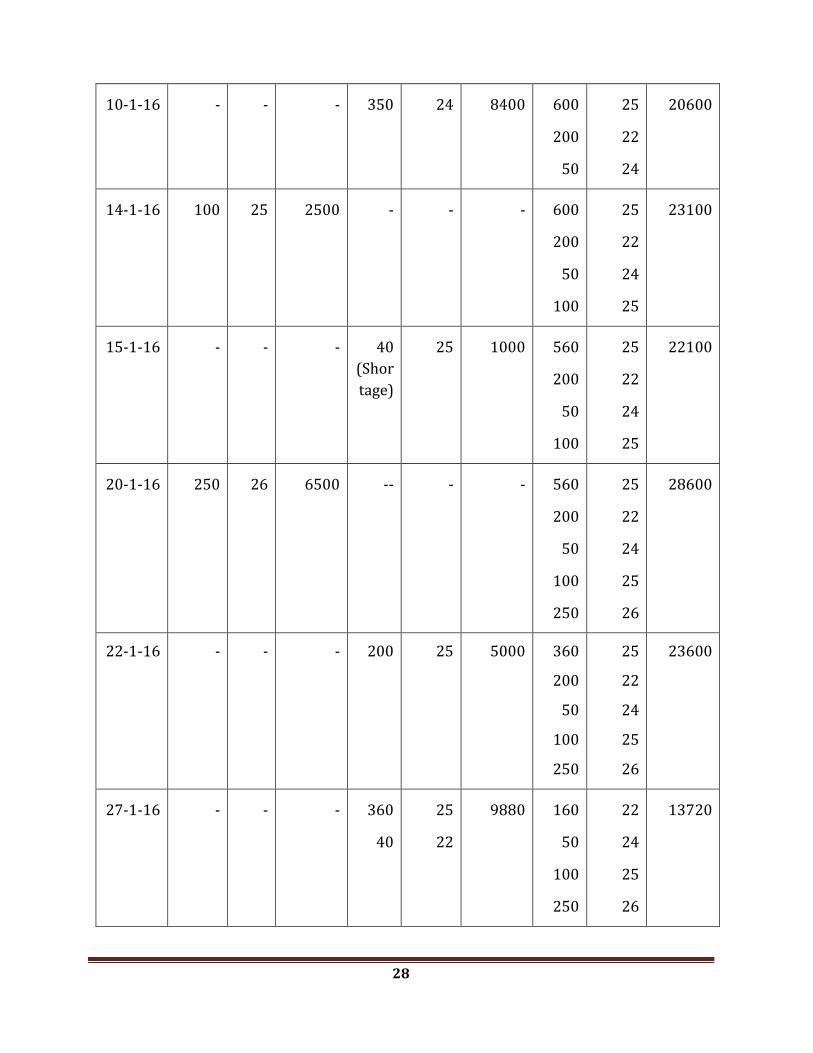

10-1-16 - - - 350 24 8400 600

200

50

25

22

24

20600

14-1-16 100 25 2500 - - - 600

200

50

100

25

22

24

25

23100

15-1-16 - - - 40

(Shor

tage)

25 1000 560

200

50

100

25

22

24

25

22100

20-1-16 250 26 6500 -- - - 560

200

50

100

250

25

22

24

25

26

28600

22-1-16 - - - 200 25 5000 360

200

50

100

250

25

22

24

25

26

23600

27-1-16 - - - 360

40

25

22

9880 160

50

100

250

22

24

25

26

13720

29

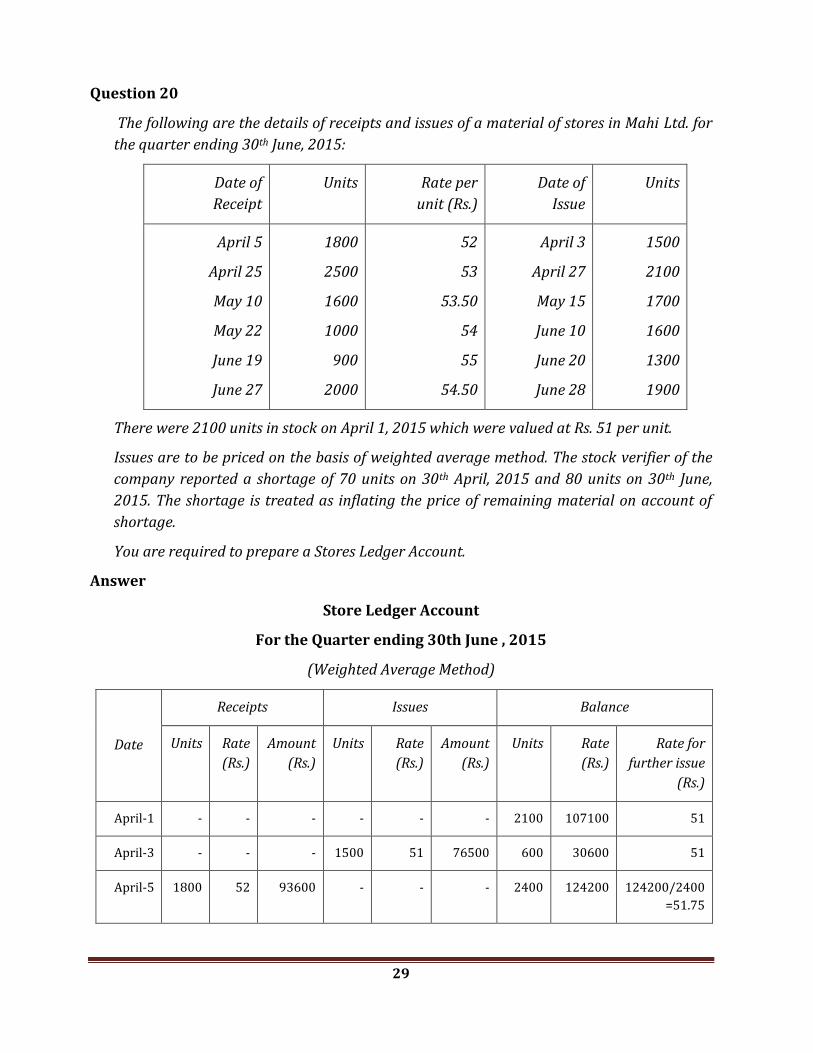

Question 20

The following are the details of receipts and issues of a material of stores in Mahi Ltd. for

the quarter ending 30th June, 2015:

Date of

Receipt

Units Rate per

unit (Rs.)

Date of

Issue

Units

April 5

April 25

May 10

May 22

June 19

June 27

1800

2500

1600

1000

900

2000

52

53

53.50

54

55

54.50

April 3

April 27

May 15

June 10

June 20

June 28

1500

2100

1700

1600

1300

1900

There were 2100 units in stock on April 1, 2015 which were valued at Rs. 51 per unit.

Issues are to be priced on the basis of weighted average method. The stock verifier of the

company reported a shortage of 70 units on 30th April, 2015 and 80 units on 30th June,

2015. The shortage is treated as inflating the price of remaining material on account of

shortage.

You are required to prepare a Stores Ledger Account.

Answer

Store Ledger Account

For the Quarter ending 30th June , 2015

(Weighted Average Method)

Date

Receipts Issues Balance

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Rate for

further issue

(Rs.)

April-1 - - - - - - 2100 107100 51

April-3 - - - 1500 51 76500 600 30600 51

April-5 1800 52 93600 - - - 2400 124200 124200/2400

=51.75

30

April-25 2500 53 132500 - - - 4900 256700 256700/4900

=52.39

April- 27 - - - 2100 52.39 110019 2800 146681 52.39

April- 30 - - - 70

Short

.

- - 2730 146681 146681/2730

=53.73

May-10 1600 53.50 85600 - - - 4330 232281 232281/4330

=53.64

May-15 - - - 1700 53.64 91188 2630 141093 53.64

May-22 1000 54 54000 -- - - 3630 195093 195093/3630

=53.74

June-10 - - - 1600 53.74 85984 2030 109109 53.74

June-19 900 55 49500 - - - 2930 158609 158609/2930

=54.13

June-20 - - - 1300 54.13 70369 1630 88240 54.13

June-27 2000 54.5 109000 - - - 3630 197240 197240/3630

=54.34

June-28 - - - 1900 54.34 103246 1730 93994 54.34

June -30 - - - 80

Short

- - 1650 93994 93944/1650=

56.93

Question 21

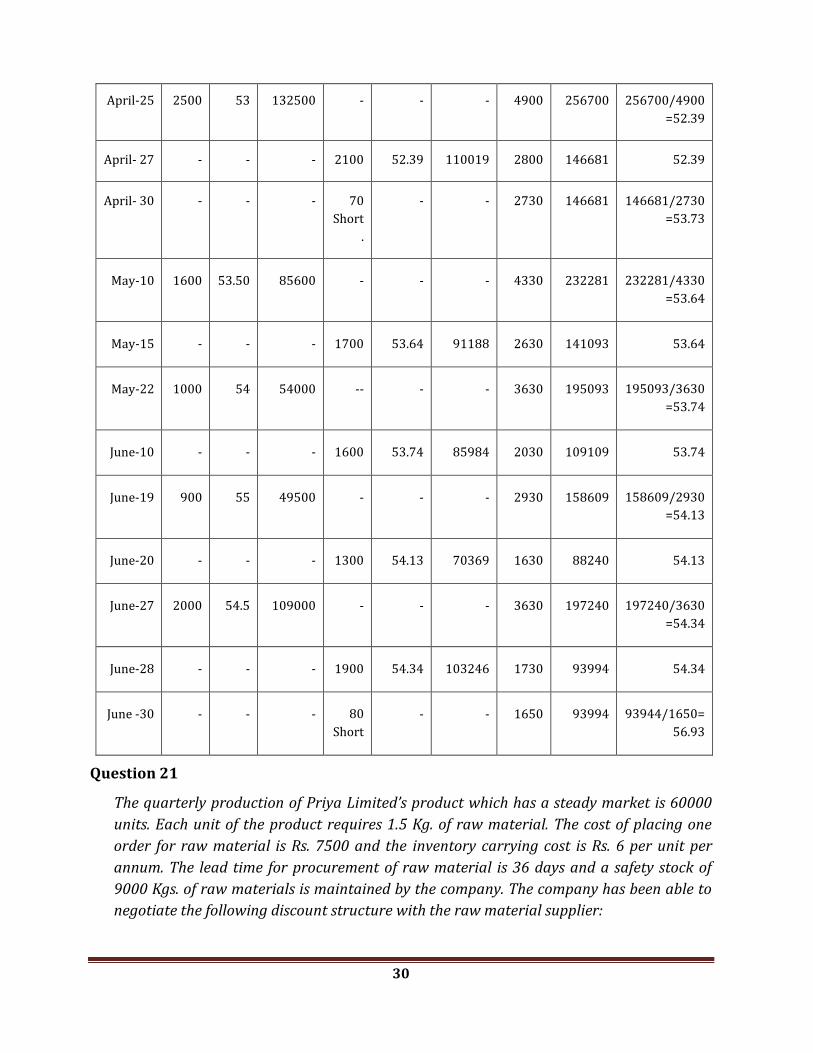

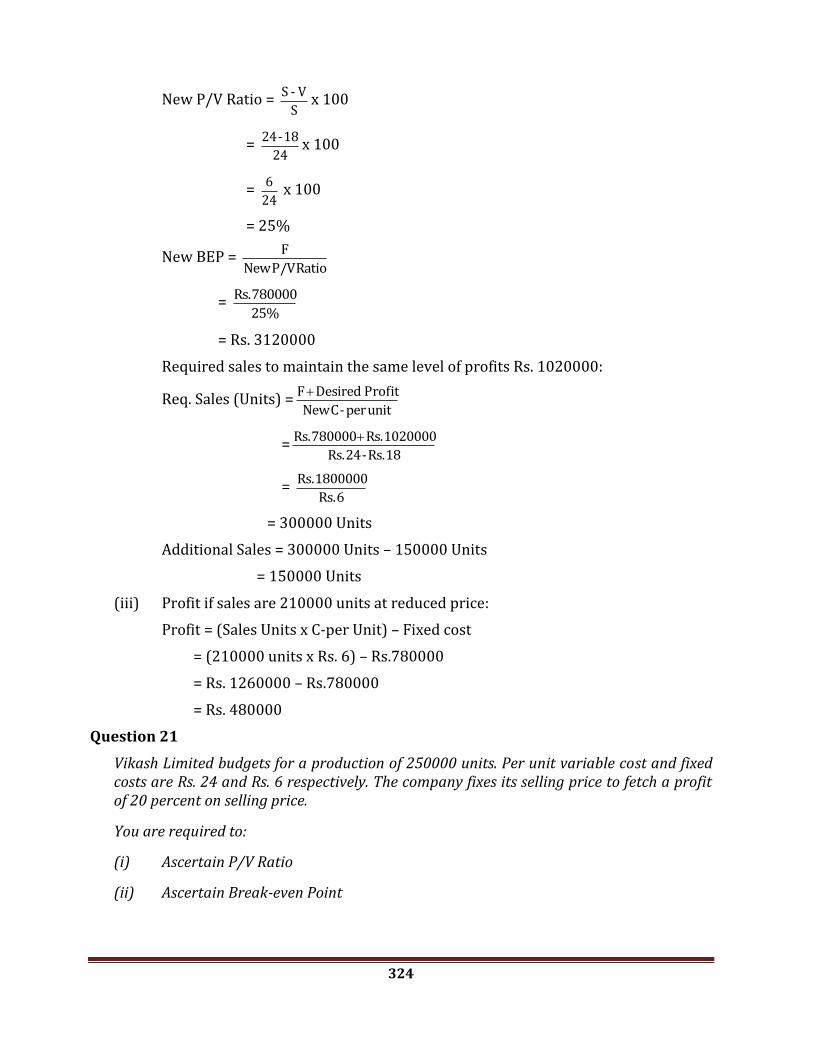

The quarterly production of Priya Limited’s product which has a steady market is 60000

units. Each unit of the product requires 1.5 Kg. of raw material. The cost of placing one

order for raw material is Rs. 7500 and the inventory carrying cost is Rs. 6 per unit per

annum. The lead time for procurement of raw material is 36 days and a safety stock of

9000 Kgs. of raw materials is maintained by the company. The company has been able to

negotiate the following discount structure with the raw material supplier:

31

Order Quantity (Kgs.) Discount (Rs.)

Less than 60000

60000-80000

80000-100000

100000-150000

150000-300000

300000-400000

Nil

25000

50000

120000

150000

200000

You are required to:

(i) Calculate the re-order point taking 30 days in a month.

(ii) Prepare a statement showing the total cost of procurement and storage of raw

material after considering the discount of the company elects to place one, two,

three, four, or six orders in the year.

(iii) State the number of orders which the company should place to minimize the cost

after taking EOQ also into consideration.

Answer

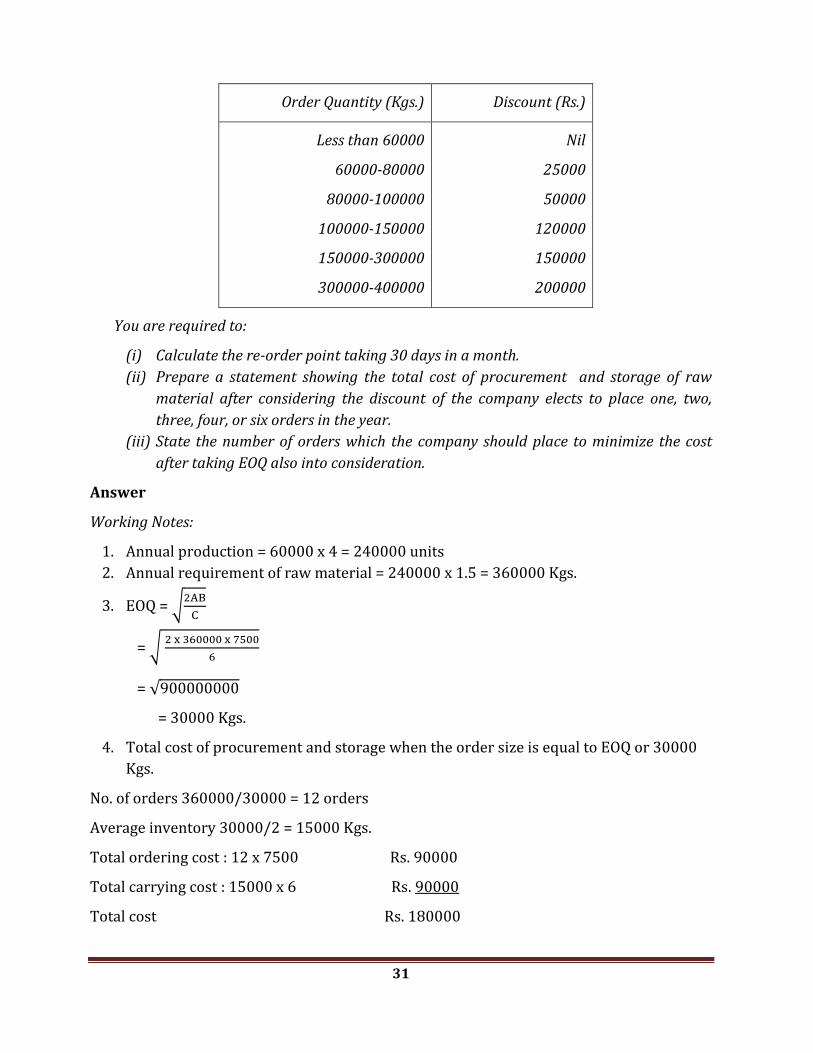

Working Notes:

1. Annual production = 60000 x 4 = 240000 units

2. Annual requirement of raw material = 240000 x 1.5 = 360000 Kgs.

3. EOQ = √

= √

= √

= 30000 Kgs.

4. Total cost of procurement and storage when the order size is equal to EOQ or 30000

Kgs.

No. of orders 360000/30000 = 12 orders

Average inventory 30000/2 = 15000 Kgs.

Total ordering cost : 12 x 7500 Rs. 90000

Total carrying cost : 15000 x 6 Rs. 90000

Total cost Rs. 180000

32

(i) Re-order point =Lead time consumption + Safety stock

= (360000/360) x 36 + 9000 Kgs.

= 36000+9000

= 45000 Kgs.

(ii) Statement showing the total cost of procurement and storage of raw material (after

considering the discount)

Order

size

(kgs)

No. of

Orders

Total of

Procurement

Rs.

Average

Stock

(kgs)

Total cost of

Storage of

raw materials

(Rs.)

Discount

(Rs.)

Total cost

(Rs.)

(1) (2) (3)=(2)x Rs.7500 (4)=(1)/2 (5)=(4) x Rs.6 (6) (7)=3+5+6

60000

90000

120000

180000

360000

6

4

3

2

1

45000

30000

22500

15000

7500

30000

45000

60000

90000

180000

180000

270000

360000

540000

1080000

25000

50000

120000

150000

200000

200000

250000

262500

405000

887500

(iii) Number of orders which the company should place to minimize the costs after taking

EOQ also into consideration is 12 orders each of size 30000 kgs. The total cost of

procurement and storage in this case comes to Rs. 180000, which is minimum.

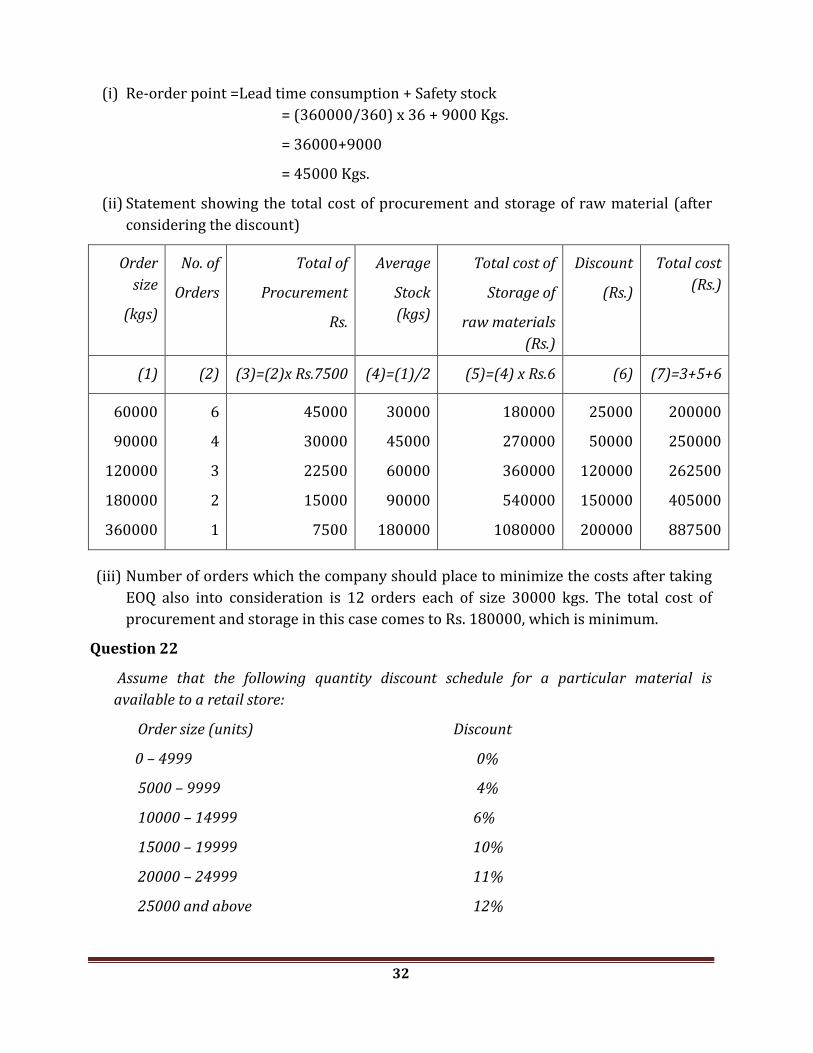

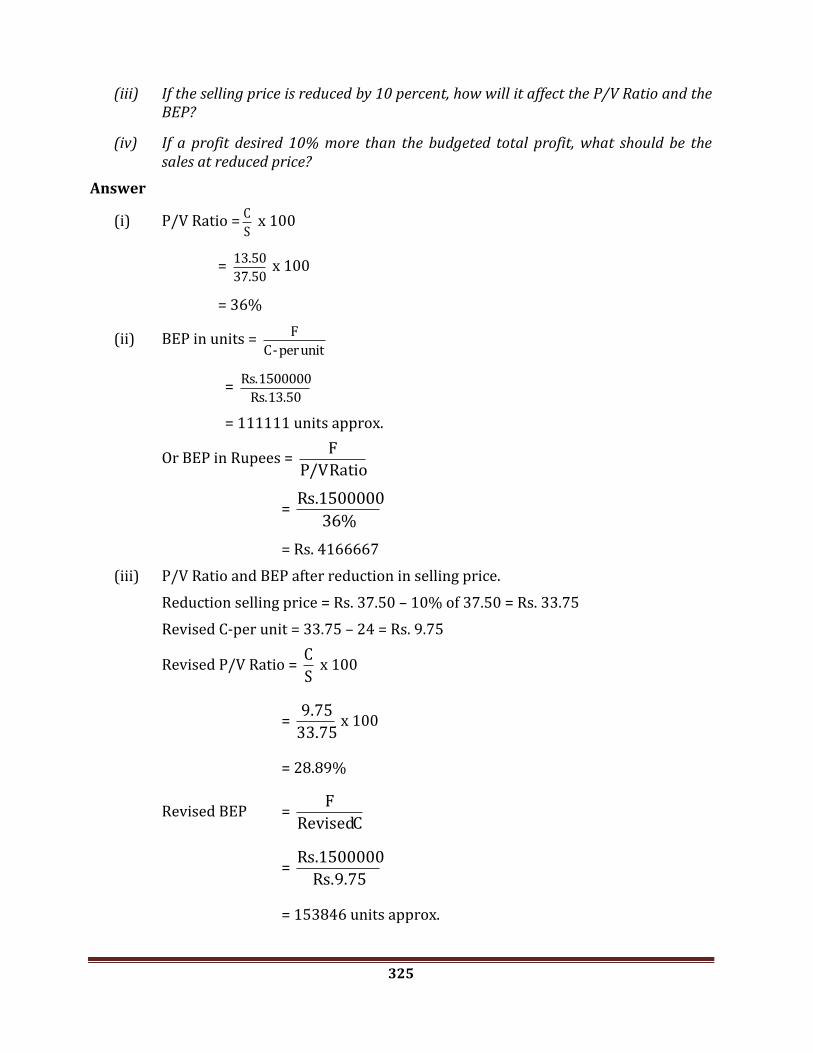

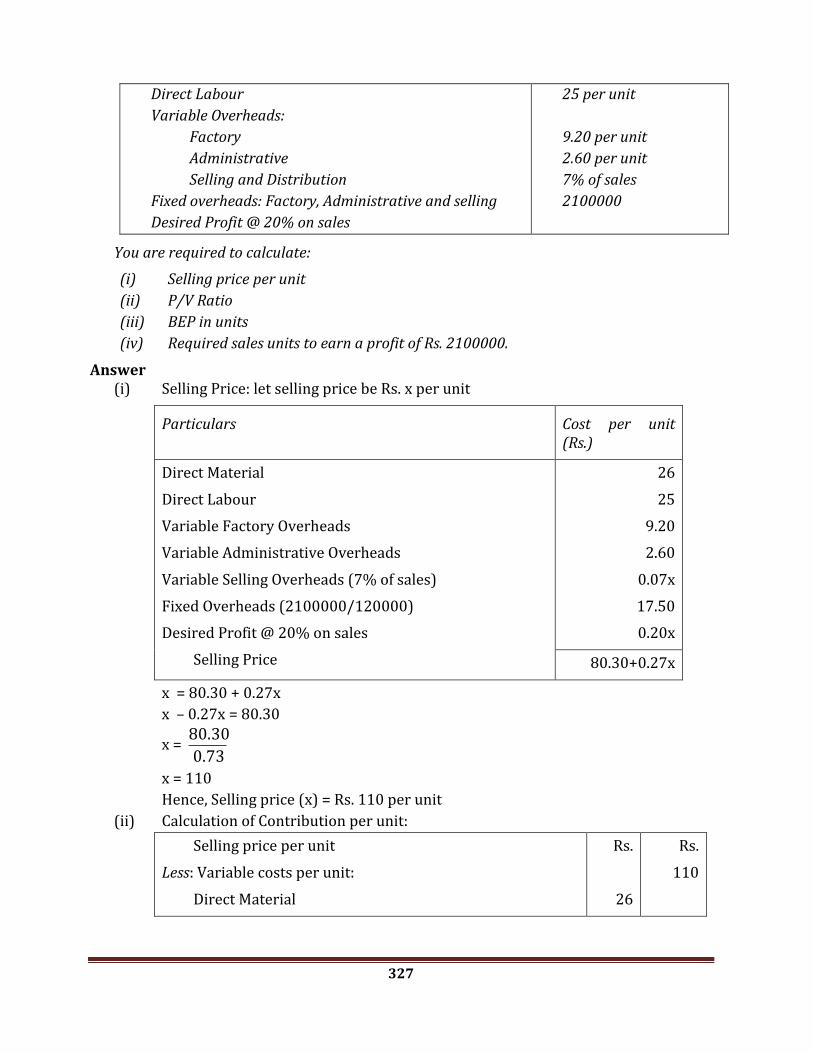

Question 22

Assume that the following quantity discount schedule for a particular material is

available to a retail store:

Order size (units) Discount

0 – 4999 0%

5000 – 9999 4%

10000 – 14999 6%

15000 – 19999 10%

20000 – 24999 11%

25000 and above 12%

33

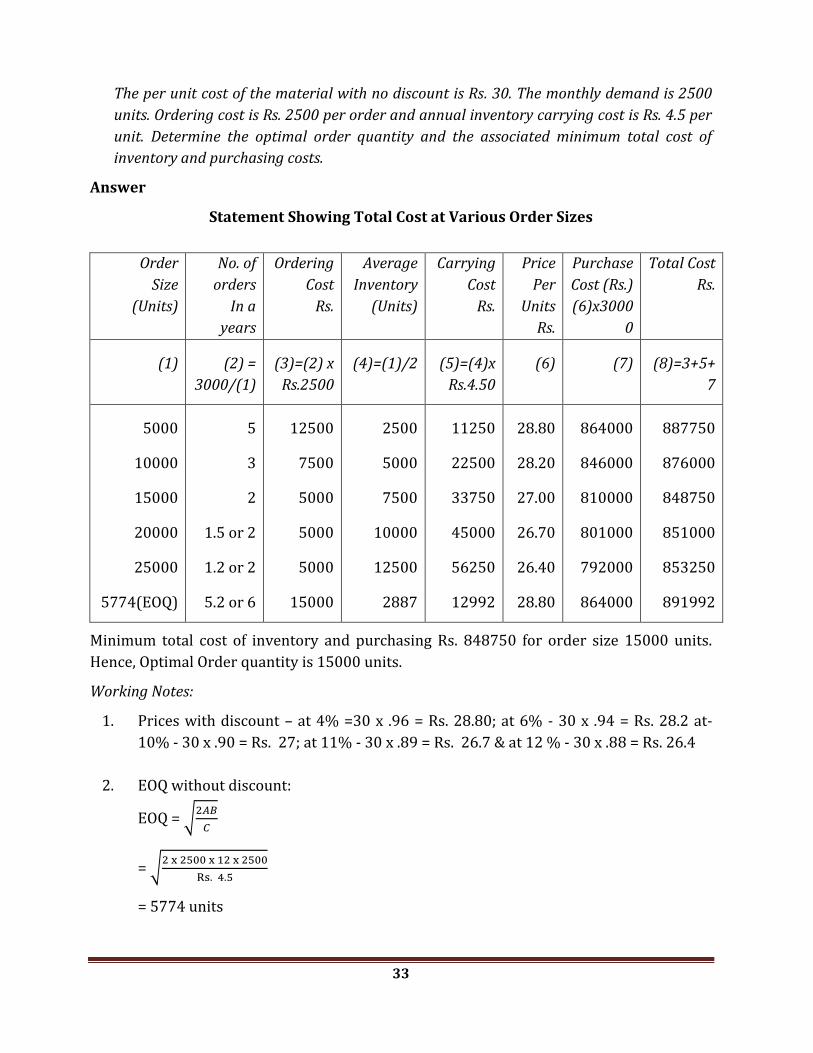

The per unit cost of the material with no discount is Rs. 30. The monthly demand is 2500

units. Ordering cost is Rs. 2500 per order and annual inventory carrying cost is Rs. 4.5 per

unit. Determine the optimal order quantity and the associated minimum total cost of

inventory and purchasing costs.

Answer

Statement Showing Total Cost at Various Order Sizes

Order

Size

(Units)

No. of

orders

In a

years

Ordering

Cost

Rs.

Average

Inventory

(Units)

Carrying

Cost

Rs.

Price

Per

Units

Rs.

Purchase

Cost (Rs.)

(6)x3000

0

Total Cost

Rs.

(1) (2) =

3000/(1)

(3)=(2) x

Rs.2500

(4)=(1)/2 (5)=(4)x

Rs.4.50

(6) (7) (8)=3+5+

7

5000

10000

15000

20000

25000

5774(EOQ)

5

3

2

1.5 or 2

1.2 or 2

5.2 or 6

12500

7500

5000

5000

5000

15000

2500

5000

7500

10000

12500

2887

11250

22500

33750

45000

56250

12992

28.80

28.20

27.00

26.70

26.40

28.80

864000

846000

810000

801000

792000

864000

887750

876000

848750

851000

853250

891992

Minimum total cost of inventory and purchasing Rs. 848750 for order size 15000 units.

Hence, Optimal Order quantity is 15000 units.

Working Notes:

1. Prices with discount – at 4% =30 x .96 = Rs. 28.80; at 6% - 30 x .94 = Rs. 28.2 at-

10% - 30 x .90 = Rs. 27; at 11% - 30 x .89 = Rs. 26.7 & at 12 % - 30 x .88 = Rs. 26.4

2. EOQ without discount:

EOQ = √

= √

= 5774 units

34

Question 23

Prepare Bin Card from the following information:

Material Received Material Issued

Date G. R. No. Units Date Req. No. Units

2.3.16

14.3.16

20.3.16

27.3.16

101

112

209

304

2500

1900

3200

1100

8.3.16

15.3.16

18.3.16

24.3.16

28.3.16

222

283

338

436

572

1100

800

1300

600

1900

On 31st March, 2016 stock was verified and it revealed a shortage of 35 units in stock.

Answer

Bin Card

Description ...................................... Bin...............................................

Store Ledger Folio ............................ Code No. ...................................

Maximum Level.....................

Minimum Level......................

Re-Order Level........................

Date

March,

2016

Receipts Issues Balance

Quantity

(units)

Remarks G.R. No. or

M.R. No-

Quantity

(Units)

Requisition

No.

Quantity

(Units)

2-3-16 101 2500 - - 2500

Verified

By

8-3-16 - - 222 1100 1400

14-3-16 112 1900 - - 3300

15-3-16 - - 283 800 2500

35

18-3-16 - - 338 1300 1200

20-3-16 209 3200 - - 4400

24-3-16 - - 436 600 3800

27-3-16 304 1100 - - 4900

28-3-16 - - 572 1900 3000

31-3-16 - - Shortage 35 2965

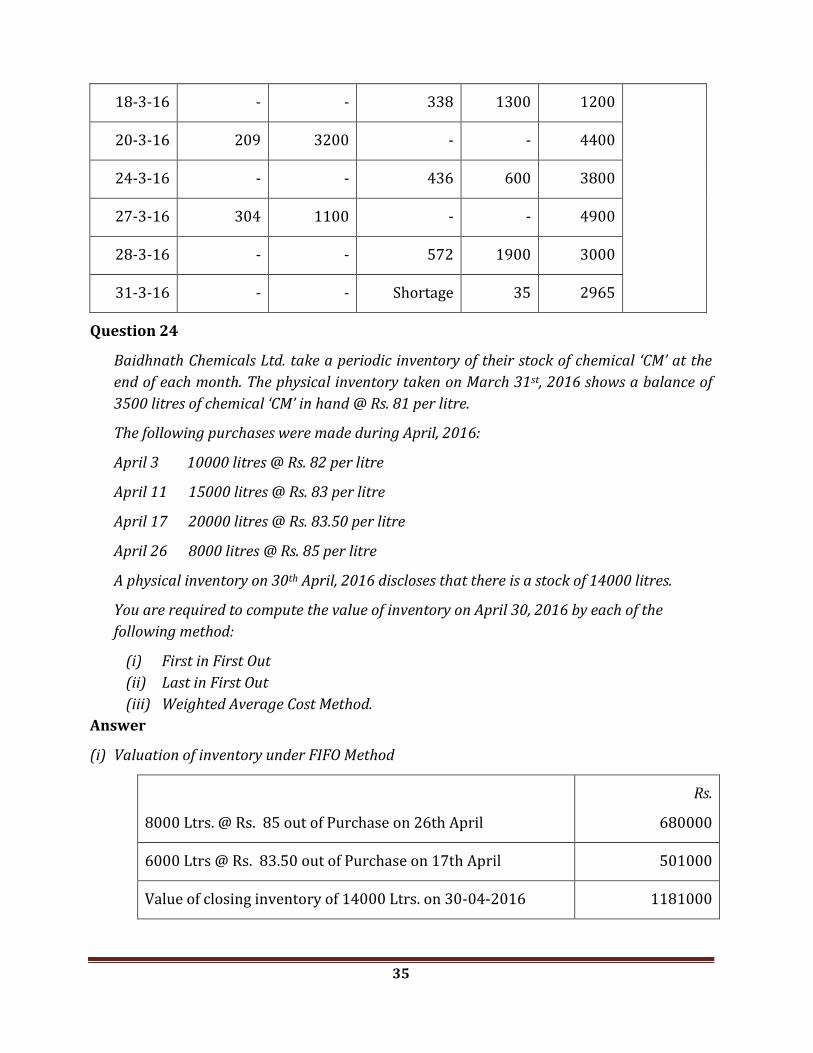

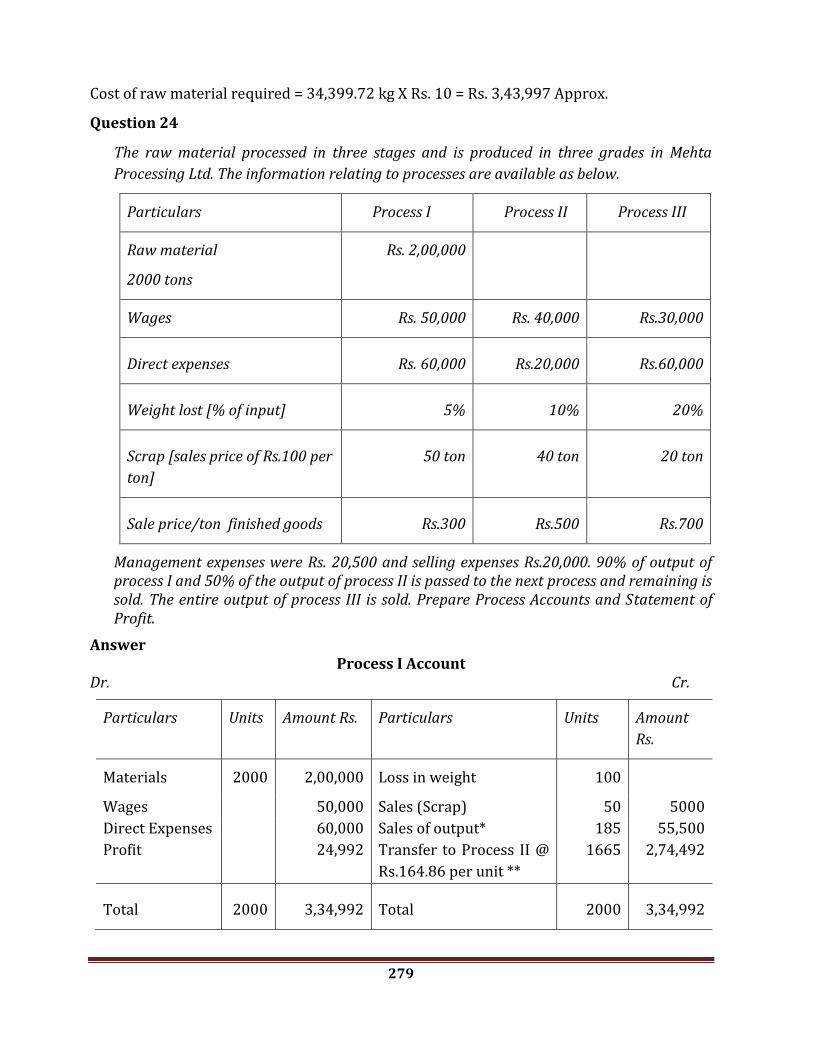

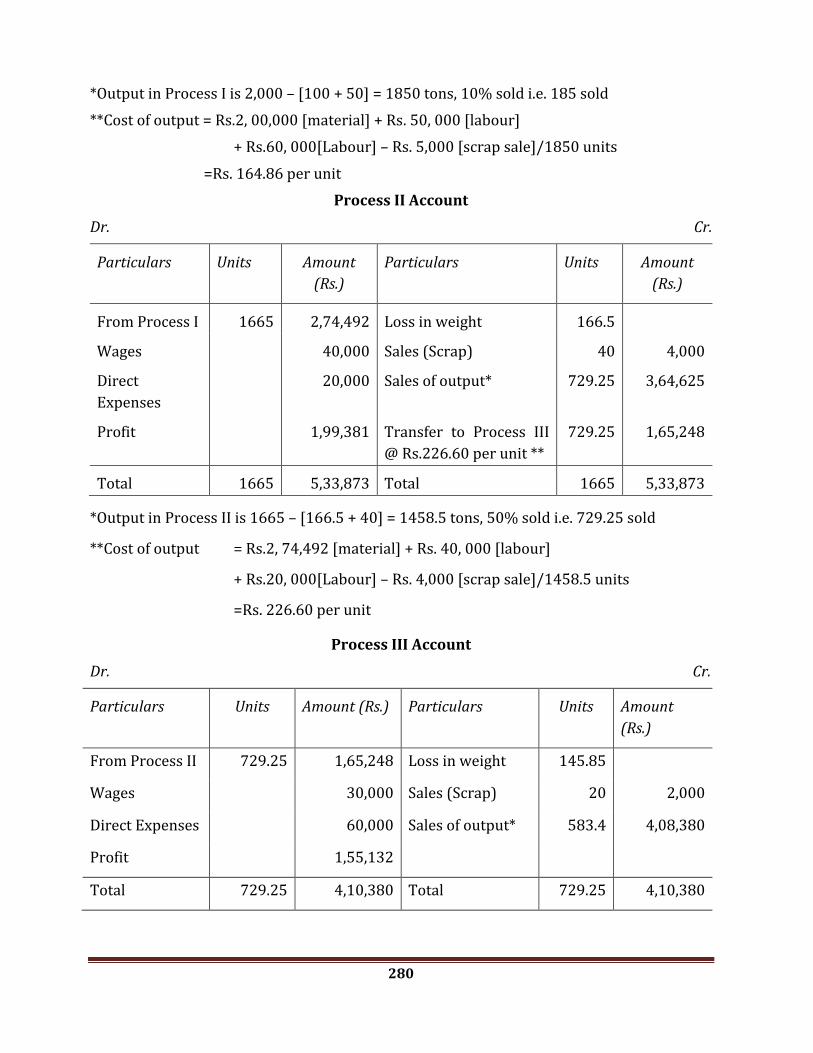

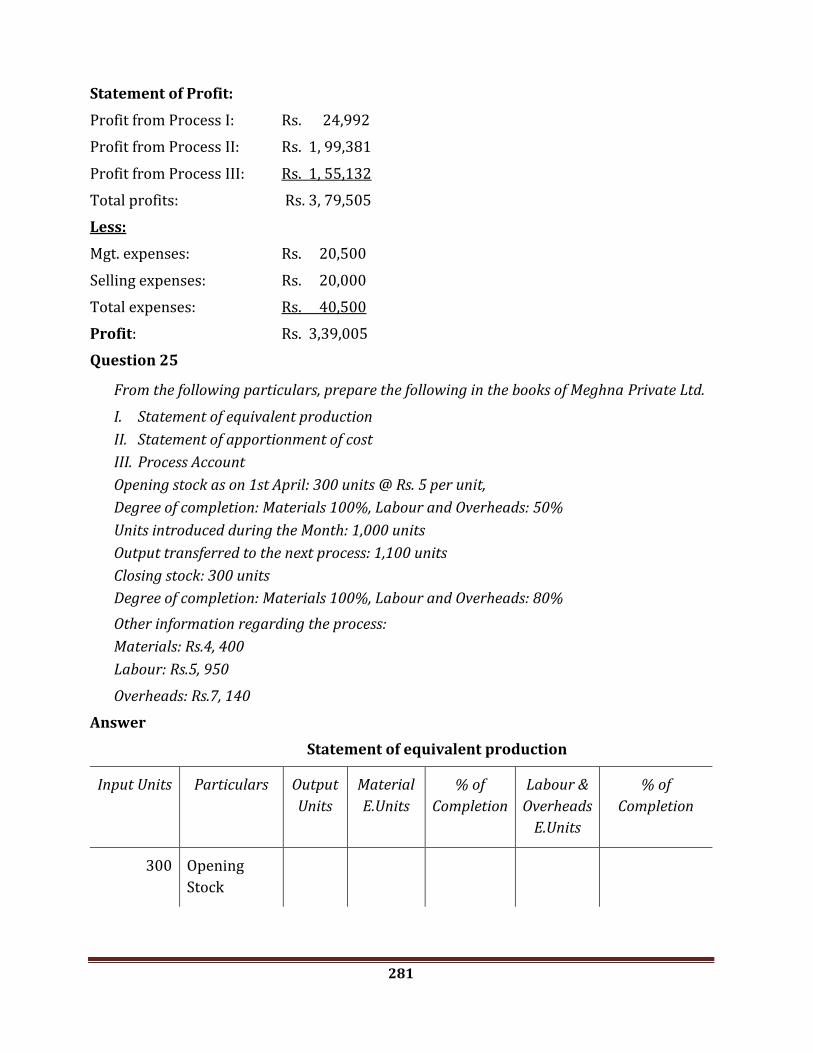

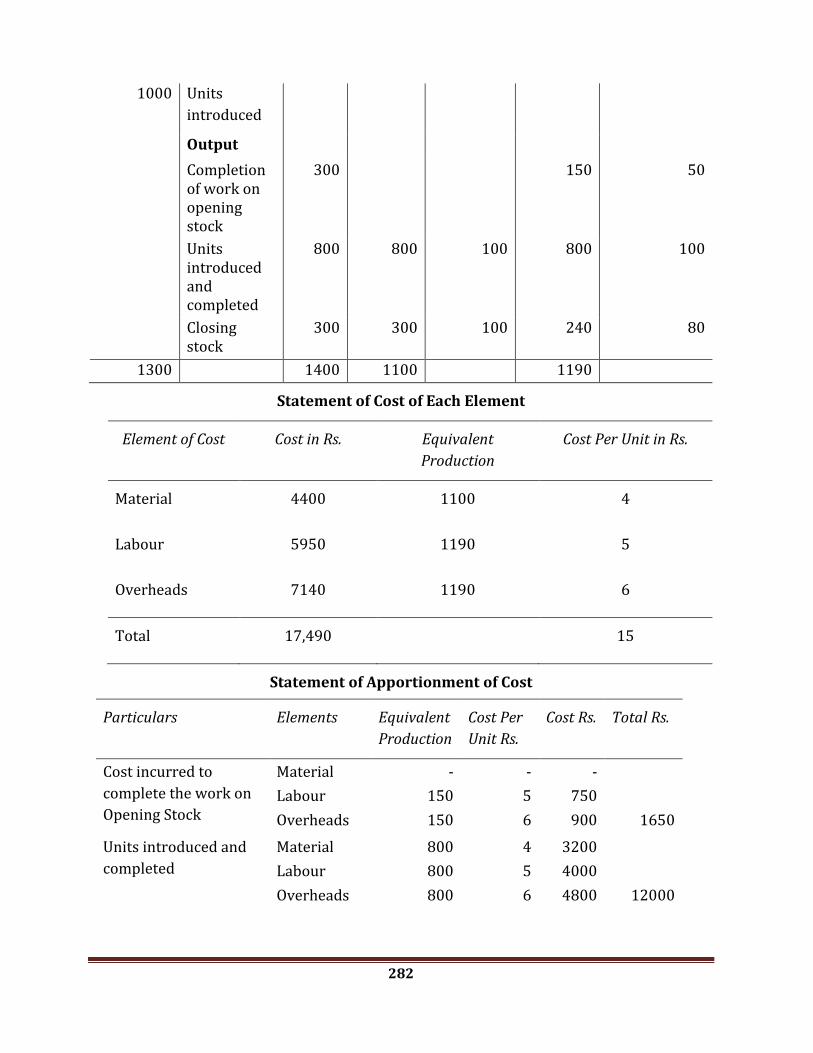

Question 24

Baidhnath Chemicals Ltd. take a periodic inventory of their stock of chemical ‘CM’ at the

end of each month. The physical inventory taken on March 31st, 2016 shows a balance of

3500 litres of chemical ‘CM’ in hand @ Rs. 81 per litre.

The following purchases were made during April, 2016:

April 3 10000 litres @ Rs. 82 per litre

April 11 15000 litres @ Rs. 83 per litre

April 17 20000 litres @ Rs. 83.50 per litre

April 26 8000 litres @ Rs. 85 per litre

A physical inventory on 30th April, 2016 discloses that there is a stock of 14000 litres.

You are required to compute the value of inventory on April 30, 2016 by each of the

following method:

(i) First in First Out

(ii) Last in First Out

(iii) Weighted Average Cost Method.

Answer

(i) Valuation of inventory under FIFO Method

8000 Ltrs. @ Rs. 85 out of Purchase on 26th April

Rs.

680000

6000 Ltrs @ Rs. 83.50 out of Purchase on 17th April 501000

Value of closing inventory of 14000 Ltrs. on 30-04-2016 1181000

36

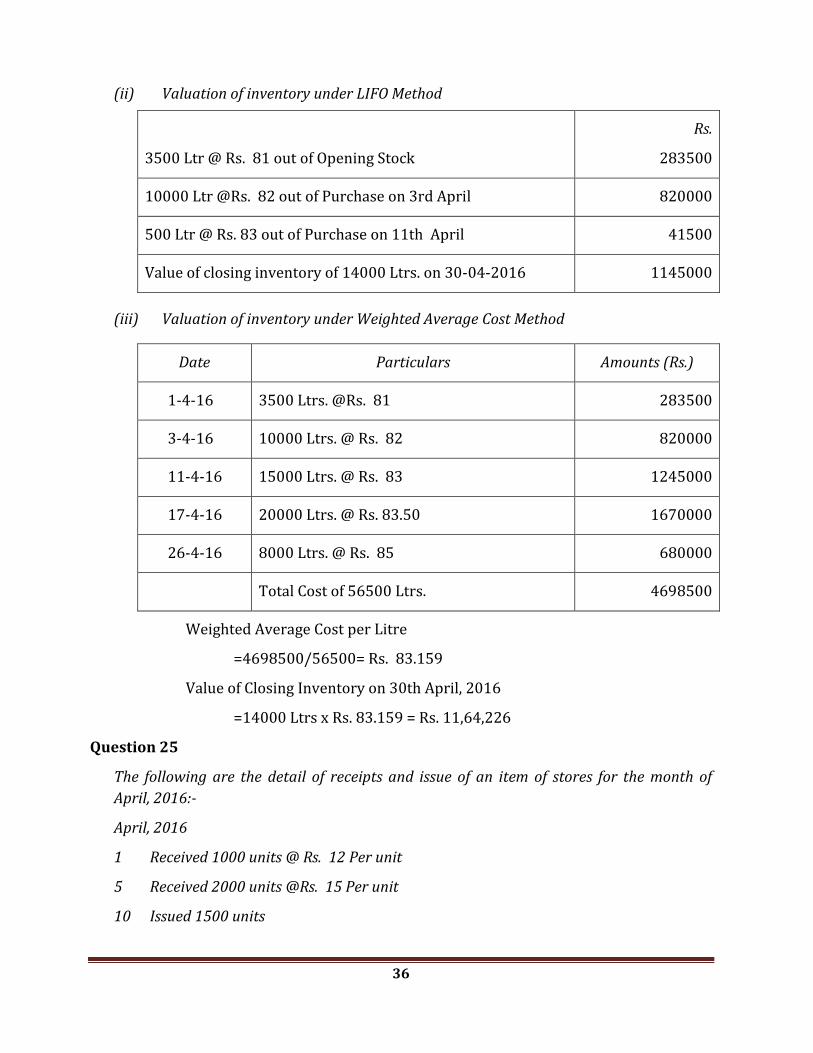

(ii) Valuation of inventory under LIFO Method

3500 Ltr @ Rs. 81 out of Opening Stock

Rs.

283500

10000 Ltr @Rs. 82 out of Purchase on 3rd April 820000

500 Ltr @ Rs. 83 out of Purchase on 11th April 41500

Value of closing inventory of 14000 Ltrs. on 30-04-2016 1145000

(iii) Valuation of inventory under Weighted Average Cost Method

Date Particulars Amounts (Rs.)

1-4-16 3500 Ltrs. @Rs. 81 283500

3-4-16 10000 Ltrs. @ Rs. 82 820000

11-4-16 15000 Ltrs. @ Rs. 83 1245000

17-4-16 20000 Ltrs. @ Rs. 83.50 1670000

26-4-16 8000 Ltrs. @ Rs. 85 680000

Total Cost of 56500 Ltrs. 4698500

Weighted Average Cost per Litre

=4698500/56500= Rs. 83.159

Value of Closing Inventory on 30th April, 2016

=14000 Ltrs x Rs. 83.159 = Rs. 11,64,226

Question 25

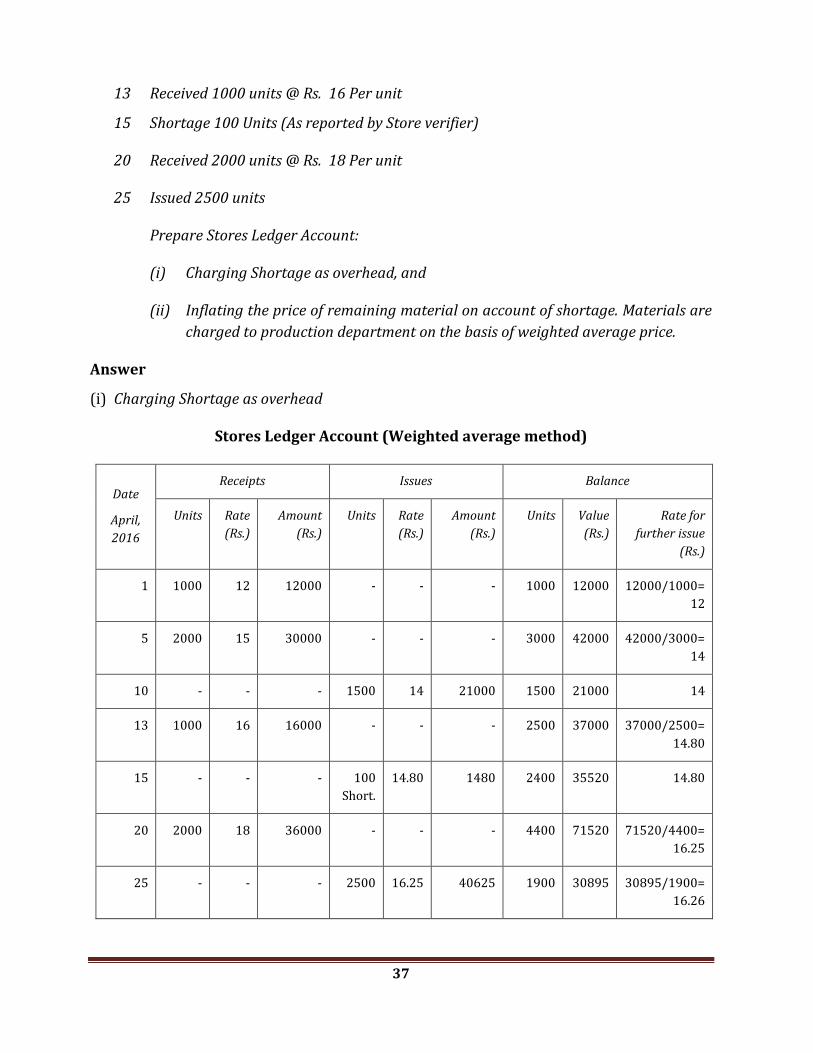

The following are the detail of receipts and issue of an item of stores for the month of

April, 2016:-

April, 2016

1 Received 1000 units @ Rs. 12 Per unit

5 Received 2000 units @Rs. 15 Per unit

10 Issued 1500 units

37

13 Received 1000 units @ Rs. 16 Per unit

15 Shortage 100 Units (As reported by Store verifier)

20 Received 2000 units @ Rs. 18 Per unit

25 Issued 2500 units

Prepare Stores Ledger Account:

(i) Charging Shortage as overhead, and

(ii) Inflating the price of remaining material on account of shortage. Materials are

charged to production department on the basis of weighted average price.

Answer

(i) Charging Shortage as overhead

Stores Ledger Account (Weighted average method)

Date

April,

2016

Receipts Issues Balance

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Amount

(Rs.)

Units Value

(Rs.)

Rate for

further issue

(Rs.)

1 1000 12 12000 - - - 1000 12000 12000/1000=

12

5 2000 15 30000 - - - 3000 42000 42000/3000=

14

10 - - - 1500 14 21000 1500 21000 14

13 1000 16 16000 - - - 2500 37000 37000/2500=

14.80

15 - - - 100

Short.

14.80 1480 2400 35520 14.80

20 2000 18 36000 - - - 4400 71520 71520/4400=

16.25

25 - - - 2500 16.25 40625 1900 30895 30895/1900=

16.26

38

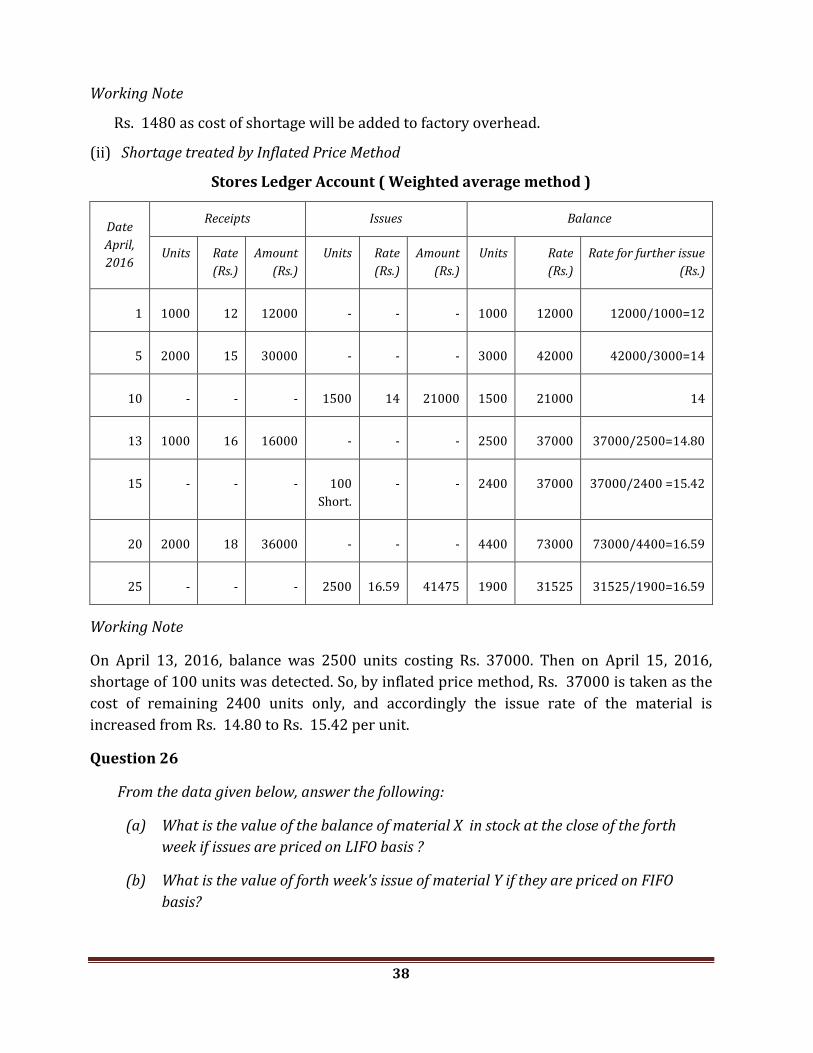

Working Note

Rs. 1480 as cost of shortage will be added to factory overhead.

(ii) Shortage treated by Inflated Price Method

Stores Ledger Account ( Weighted average method )

Date

April,

2016

Receipts Issues Balance

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Amount

(Rs.)

Units Rate

(Rs.)

Rate for further issue

(Rs.)

1 1000 12 12000 - - - 1000 12000 12000/1000=12

5 2000 15 30000 - - - 3000 42000 42000/3000=14

10 - - - 1500 14 21000 1500 21000 14

13 1000 16 16000 - - - 2500 37000 37000/2500=14.80

15 - - - 100

Short.

- - 2400 37000 37000/2400 =15.42

20 2000 18 36000 - - - 4400 73000 73000/4400=16.59

25 - - - 2500 16.59 41475 1900 31525 31525/1900=16.59

Working Note

On April 13, 2016, balance was 2500 units costing Rs. 37000. Then on April 15, 2016,

shortage of 100 units was detected. So, by inflated price method, Rs. 37000 is taken as the

cost of remaining 2400 units only, and accordingly the issue rate of the material is

increased from Rs. 14.80 to Rs. 15.42 per unit.

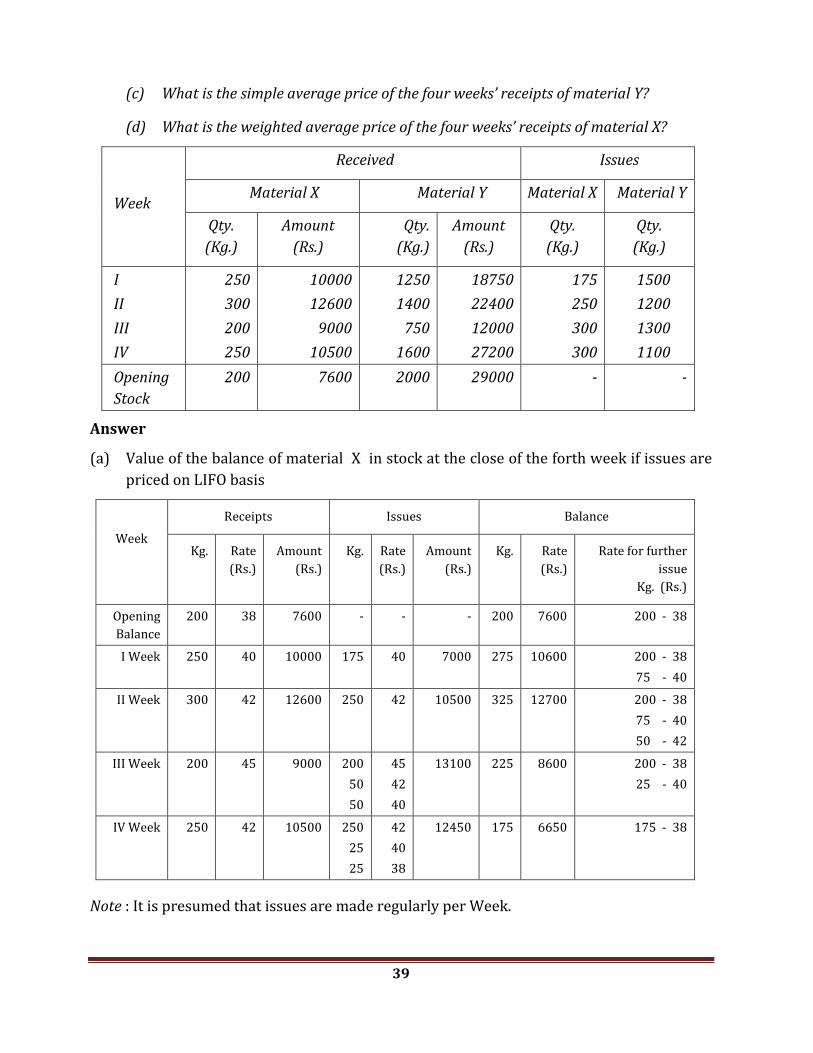

Question 26

From the data given below, answer the following:

(a) What is the value of the balance of material X in stock at the close of the forth

week if issues are priced on LIFO basis ?

(b) What is the value of forth week's issue of material Y if they are priced on FIFO

basis?

39

(c) What is the simple average price of the four weeks’ receipts of material Y?

(d) What is the weighted average price of the four weeks’ receipts of material X?

Week

Received Issues

Material X Material Y Material X Material Y

Qty.

(Kg.)

Amount

(Rs.)

Qty.

(Kg.)

Amount

(Rs.)

Qty.

(Kg.)

Qty.

(Kg.)

I

II

III

IV

250

300

200

250

10000

12600

9000

10500

1250

1400

750

1600

18750

22400

12000

27200

175

250

300

300

1500

1200

1300

1100

Opening

Stock

200 7600 2000 29000 - -

Answer

(a) Value of the balance of material X in stock at the close of the forth week if issues are

priced on LIFO basis

Week

Receipts Issues Balance

Kg. Rate

(Rs.)

Amount

(Rs.)

Kg. Rate

(Rs.)

Amount

(Rs.)

Kg. Rate

(Rs.)

Rate for further

issue

Kg. (Rs.)

Opening

Balance

200 38 7600 - - - 200 7600 200 - 38

I Week 250 40 10000 175 40 7000 275 10600 200 - 38

75 - 40

II Week 300 42 12600 250 42 10500 325 12700 200 - 38

75 - 40

50 - 42

III Week 200 45 9000 200

50

50

45

42

40

13100 225 8600 200 - 38

25 - 40

IV Week 250 42 10500 250

25

25

42

40

38

12450 175 6650 175 - 38

Note : It is presumed that issues are made regularly per Week.

40

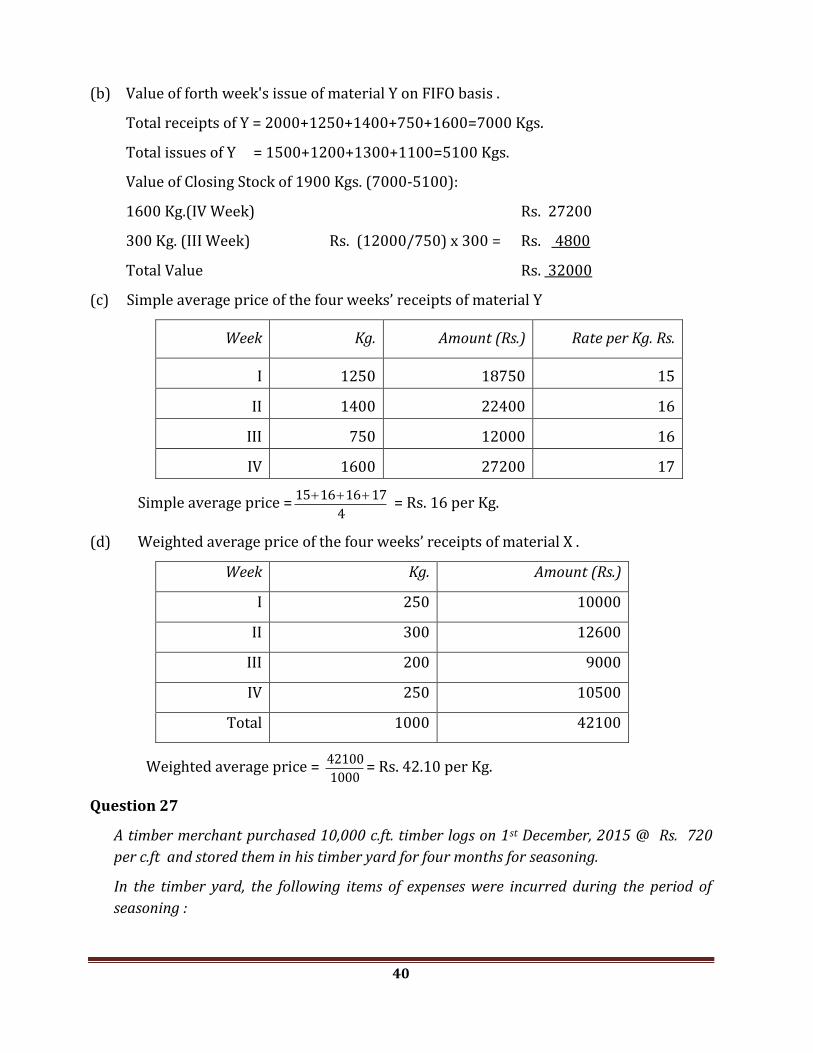

(b) Value of forth week's issue of material Y on FIFO basis .

Total receipts of Y = 2000+1250+1400+750+1600=7000 Kgs.

Total issues of Y = 1500+1200+1300+1100=5100 Kgs.

Value of Closing Stock of 1900 Kgs. (7000-5100):

1600 Kg.(IV Week) Rs. 27200

300 Kg. (III Week) Rs. (12000/750) x 300 = Rs. 4800

Total Value Rs. 32000

(c) Simple average price of the four weeks’ receipts of material Y

Week Kg. Amount (Rs.) Rate per Kg. Rs.

I 1250 18750 15

II 1400 22400 16

III 750 12000 16

IV 1600 27200 17

Simple average price =4

17 16 16 15 = Rs. 16 per Kg.

(d) Weighted average price of the four weeks’ receipts of material X .

Week Kg. Amount (Rs.)

I 250 10000

II 300 12600

III 200 9000

IV 250 10500

Total 1000 42100

Weighted average price = 1000

42100= Rs. 42.10 per Kg.

Question 27

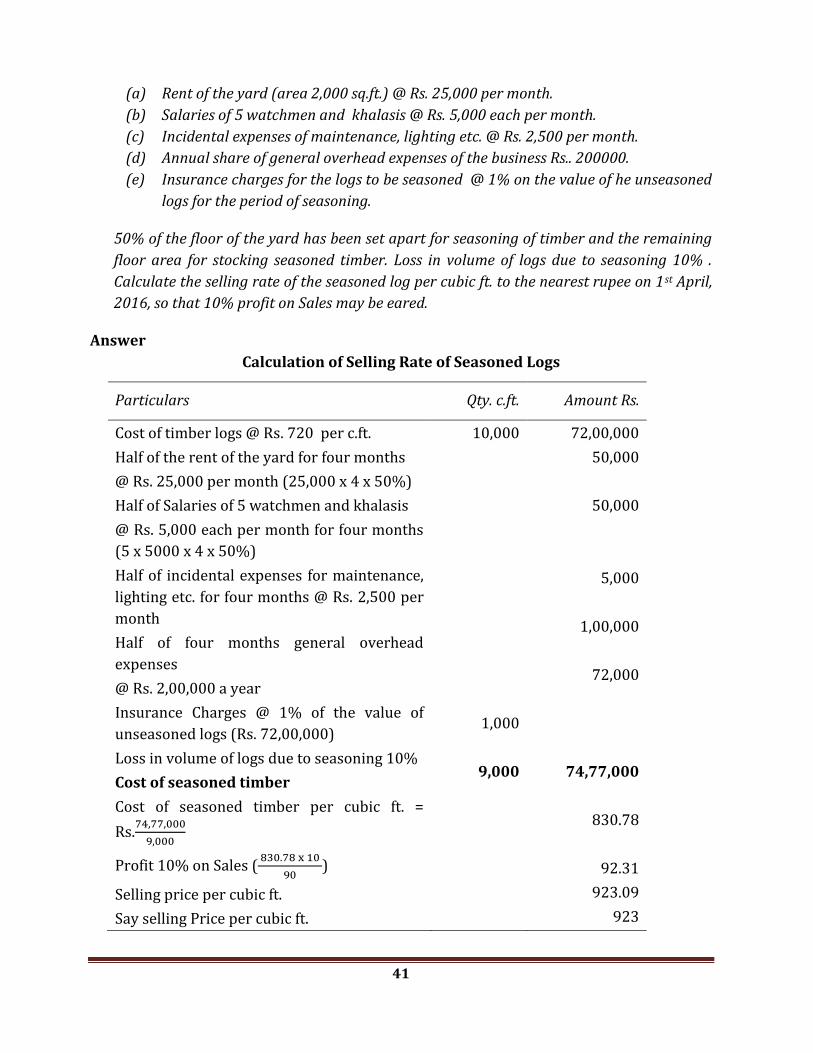

A timber merchant purchased 10,000 c.ft. timber logs on 1st December, 2015 @ Rs. 720

per c.ft and stored them in his timber yard for four months for seasoning.

In the timber yard, the following items of expenses were incurred during the period of

seasoning :

41

(a) Rent of the yard (area 2,000 sq.ft.) @ Rs. 25,000 per month.

(b) Salaries of 5 watchmen and khalasis @ Rs. 5,000 each per month.

(c) Incidental expenses of maintenance, lighting etc. @ Rs. 2,500 per month.

(d) Annual share of general overhead expenses of the business Rs.. 200000.

(e) Insurance charges for the logs to be seasoned @ 1% on the value of he unseasoned

logs for the period of seasoning.

50% of the floor of the yard has been set apart for seasoning of timber and the remaining

floor area for stocking seasoned timber. Loss in volume of logs due to seasoning 10% .

Calculate the selling rate of the seasoned log per cubic ft. to the nearest rupee on 1st April,

2016, so that 10% profit on Sales may be eared.

Answer

Calculation of Selling Rate of Seasoned Logs

Particulars Qty. c.ft. Amount Rs.

Cost of timber logs @ Rs. 720 per c.ft.

Half of the rent of the yard for four months

@ Rs. 25,000 per month (25,000 x 4 x 50%)

Half of Salaries of 5 watchmen and khalasis

@ Rs. 5,000 each per month for four months

(5 x 5000 x 4 x 50%)

Half of incidental expenses for maintenance,

lighting etc. for four months @ Rs. 2,500 per

month

Half of four months general overhead

expenses

@ Rs. 2,00,000 a year

Insurance Charges @ 1% of the value of

unseasoned logs (Rs. 72,00,000)

Loss in volume of logs due to seasoning 10%

Cost of seasoned timber

Cost of seasoned timber per cubic ft. =

Rs.

Profit 10% on Sales (

)

Selling price per cubic ft.

Say selling Price per cubic ft.

10,000

1,000

9,000

72,00,000

50,000

50,000

5,000

1,00,000

72,000

74,77,000

830.78

92.31

923.09

923

42

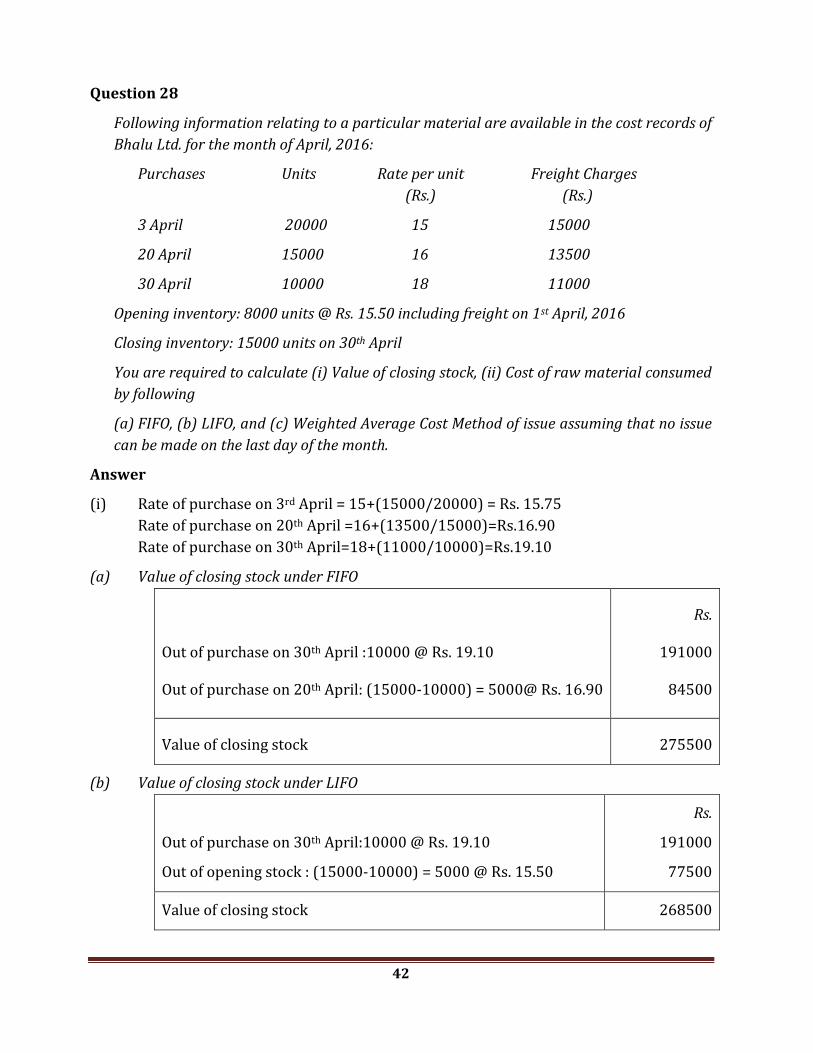

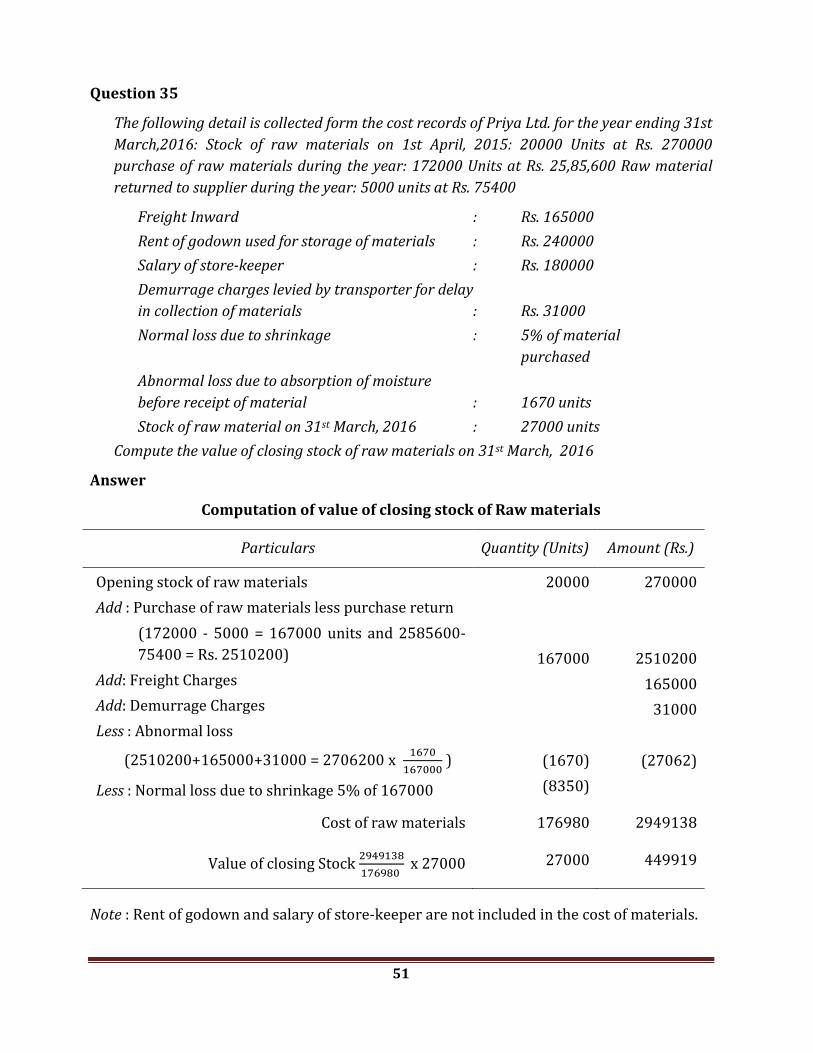

Question 28

Following information relating to a particular material are available in the cost records of

Bhalu Ltd. for the month of April, 2016:

Purchases Units Rate per unit Freight Charges

(Rs.) (Rs.)

3 April 20000 15 15000

20 April 15000 16 13500

30 April 10000 18 11000

Opening inventory: 8000 units @ Rs. 15.50 including freight on 1st April, 2016

Closing inventory: 15000 units on 30th April

You are required to calculate (i) Value of closing stock, (ii) Cost of raw material consumed

by following

(a) FIFO, (b) LIFO, and (c) Weighted Average Cost Method of issue assuming that no issue

can be made on the last day of the month.

Answer

(i) Rate of purchase on 3rd April = 15+(15000/20000) = Rs. 15.75

Rate of purchase on 20th April =16+(13500/15000)=Rs.16.90

Rate of purchase on 30th April=18+(11000/10000)=Rs.19.10

(a) Value of closing stock under FIFO

Out of purchase on 30th April :10000 @ Rs. 19.10

Out of purchase on 20th April: (15000-10000) = 5000@ Rs. 16.90

Rs.

191000

84500

Value of closing stock 275500

(b) Value of closing stock under LIFO

Out of purchase on 30th April:10000 @ Rs. 19.10

Out of opening stock : (15000-10000) = 5000 @ Rs. 15.50

Rs.

191000

77500

Value of closing stock 268500

43

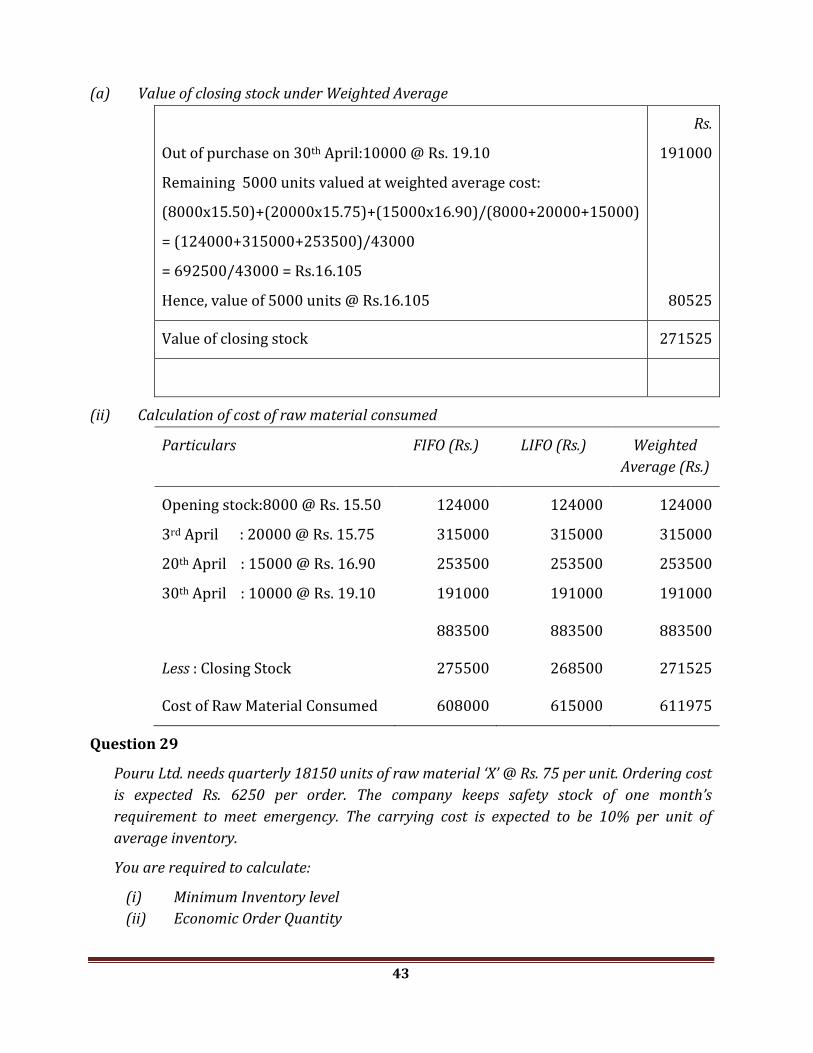

(a) Value of closing stock under Weighted Average

Out of purchase on 30th April:10000 @ Rs. 19.10

Remaining 5000 units valued at weighted average cost:

(8000x15.50)+(20000x15.75)+(15000x16.90)/(8000+20000+15000)

= (124000+315000+253500)/43000

= 692500/43000 = Rs.16.105

Hence, value of 5000 units @ Rs.16.105

Rs.

191000

80525

Value of closing stock 271525

(ii) Calculation of cost of raw material consumed

Particulars FIFO (Rs.) LIFO (Rs.) Weighted

Average (Rs.)

Opening stock:8000 @ Rs. 15.50

3rd April : 20000 @ Rs. 15.75

20th April : 15000 @ Rs. 16.90

30th April : 10000 @ Rs. 19.10

124000

315000

253500

191000

124000

315000

253500

191000

124000

315000

253500

191000

883500 883500 883500

Less : Closing Stock 275500 268500 271525

Cost of Raw Material Consumed 608000 615000 611975

Question 29

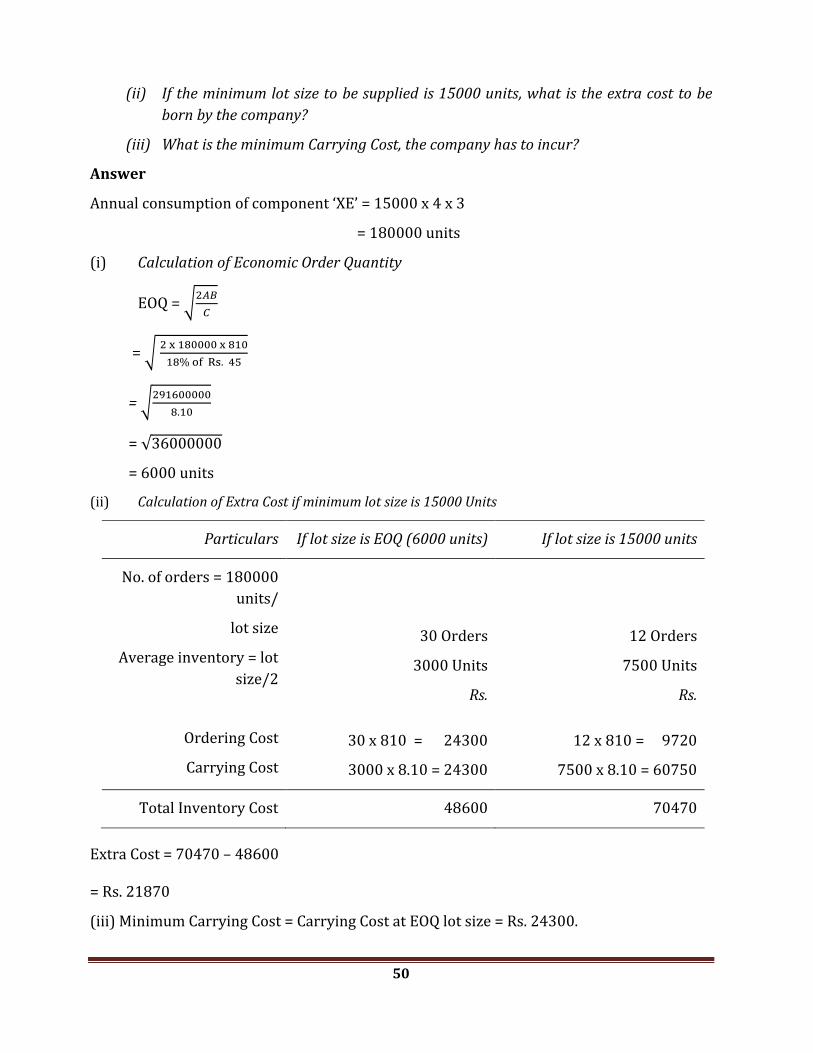

Pouru Ltd. needs quarterly 18150 units of raw material ‘X’ @ Rs. 75 per unit. Ordering cost

is expected Rs. 6250 per order. The company keeps safety stock of one month’s

requirement to meet emergency. The carrying cost is expected to be 10% per unit of

average inventory.

You are required to calculate:

(i) Minimum Inventory level

(ii) Economic Order Quantity

44

(iii) Maximum Inventory level

(iv) Average Inventory level

(v) Total Annual Ordering Cost

(vi) Total Annual Carrying Cost

(vii) Total Inventory Cost excluding purchase cost

Answer

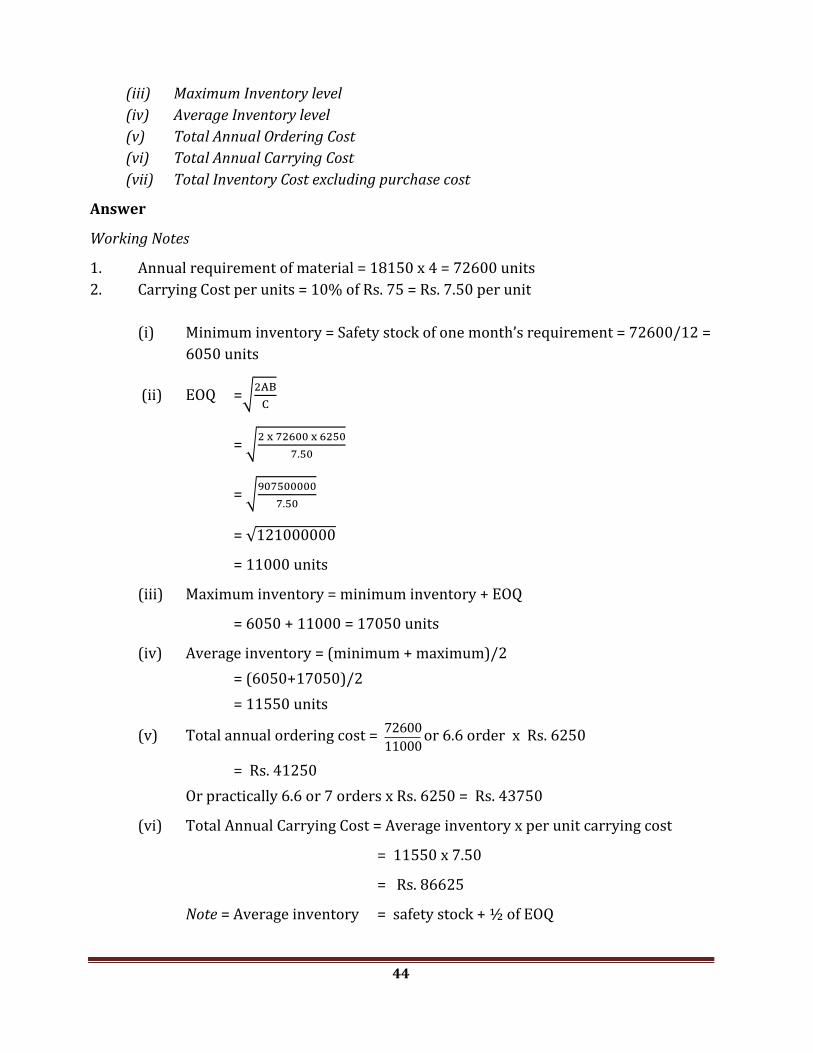

Working Notes

1. Annual requirement of material = 18150 x 4 = 72600 units

2. Carrying Cost per units = 10% of Rs. 75 = Rs. 7.50 per unit

(i) Minimum inventory = Safety stock of one month’s requirement = 72600/12 =

6050 units

(ii) EOQ =√

= √

= √

= √

= 11000 units

(iii) Maximum inventory = minimum inventory + EOQ

= 6050 + 11000 = 17050 units

(iv) Average inventory = (minimum + maximum)/2

= (6050+17050)/2

= 11550 units

(v) Total annual ordering cost = 11000

72600or 6.6 order x Rs. 6250

= Rs. 41250

Or practically 6.6 or 7 orders x Rs. 6250 = Rs. 43750

(vi) Total Annual Carrying Cost = Average inventory x per unit carrying cost

= 11550 x 7.50

= Rs. 86625

Note = Average inventory = safety stock + ½ of EOQ

45

= 6050 + 11000 x ½

= 6050 + 5500 = 11550 units

(vii) Total inventory cost = 41250 + 86625 = Rs.127875

Or 43750 + 86625 = Rs. 130375

Question 30

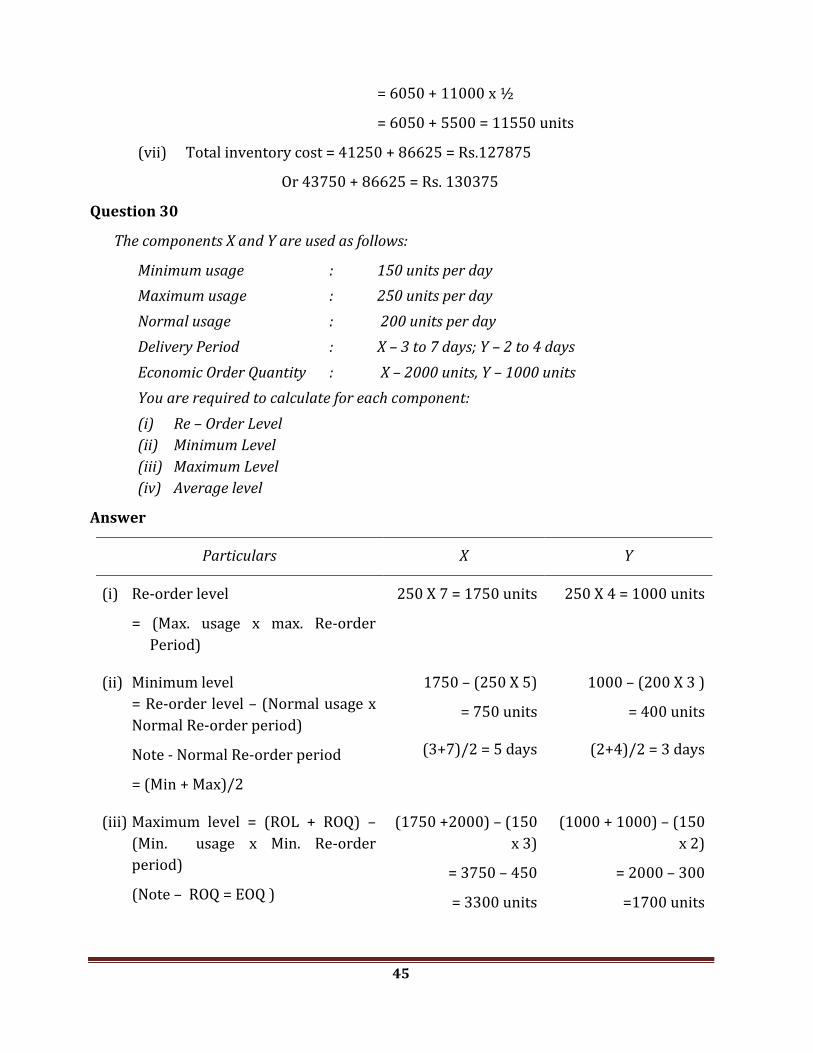

The components X and Y are used as follows:

Minimum usage : 150 units per day

Maximum usage : 250 units per day

Normal usage : 200 units per day

Delivery Period : X – 3 to 7 days; Y – 2 to 4 days

Economic Order Quantity : X – 2000 units, Y – 1000 units

You are required to calculate for each component:

(i) Re – Order Level

(ii) Minimum Level

(iii) Maximum Level

(iv) Average level

Answer

Particulars X Y

(i) Re-order level

= (Max. usage x max. Re-order

Period)

250 X 7 = 1750 units 250 X 4 = 1000 units

(ii) Minimum level

= Re-order level – (Normal usage x

Normal Re-order period)

Note - Normal Re-order period

= (Min + Max)/2

1750 – (250 X 5)

= 750 units

(3+7)/2 = 5 days

1000 – (200 X 3 )

= 400 units

(2+4)/2 = 3 days

(iii) Maximum level = (ROL + ROQ) –

(Min. usage x Min. Re-order

period)

(Note – ROQ = EOQ )

(1750 +2000) – (150

x 3)

= 3750 – 450

= 3300 units

(1000 + 1000) – (150

x 2)

= 2000 – 300

=1700 units

46

(iv) Average level = (Min. level + Max.

level)/2 (or)

Min. level + ½ of ROQ

(750 + 3300 )/2 =

2025 units

(or)

750 +2000 X ½

= 1750 units

(400 + 1700)/2 =

1050 units

(or)

400 + 1000 X ½

= 900 units

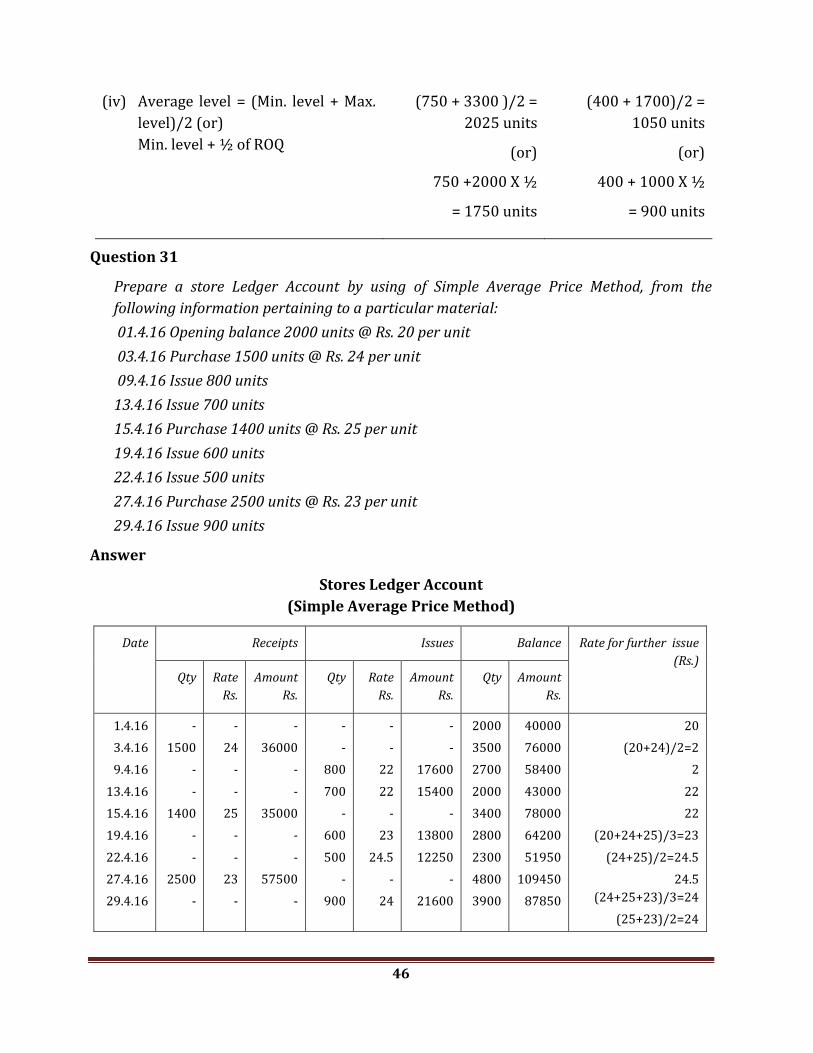

Question 31

Prepare a store Ledger Account by using of Simple Average Price Method, from the

following information pertaining to a particular material:

01.4.16 Opening balance 2000 units @ Rs. 20 per unit

03.4.16 Purchase 1500 units @ Rs. 24 per unit

09.4.16 Issue 800 units

13.4.16 Issue 700 units

15.4.16 Purchase 1400 units @ Rs. 25 per unit

19.4.16 Issue 600 units

22.4.16 Issue 500 units

27.4.16 Purchase 2500 units @ Rs. 23 per unit

29.4.16 Issue 900 units

Answer

Stores Ledger Account

(Simple Average Price Method)

Date Receipts Issues Balance Rate for further issue

(Rs.)

Qty Rate

Rs.

Amount

Rs.

Qty Rate

Rs.

Amount

Rs.

Qty Amount

Rs.

1.4.16

3.4.16

9.4.16

13.4.16

15.4.16

19.4.16

22.4.16

27.4.16

29.4.16

-

1500

-

-

1400

-

-

2500

-

-

24

-

-

25

-

-

23

-

-

36000

-

-

35000

-

-

57500

-

-

-

800

700

-

600

500

-

900

-

-

22

22

-

23

24.5

-

24

-

-

17600

15400

-

13800

12250

-

21600

2000

3500

2700

2000

3400

2800

2300

4800

3900

40000

76000

58400

43000

78000

64200

51950

109450

87850

20

(20+24)/2=2

2

22

22

(20+24+25)/3=23

(24+25)/2=24.5

24.5

(24+25+23)/3=24

(25+23)/2=24

47

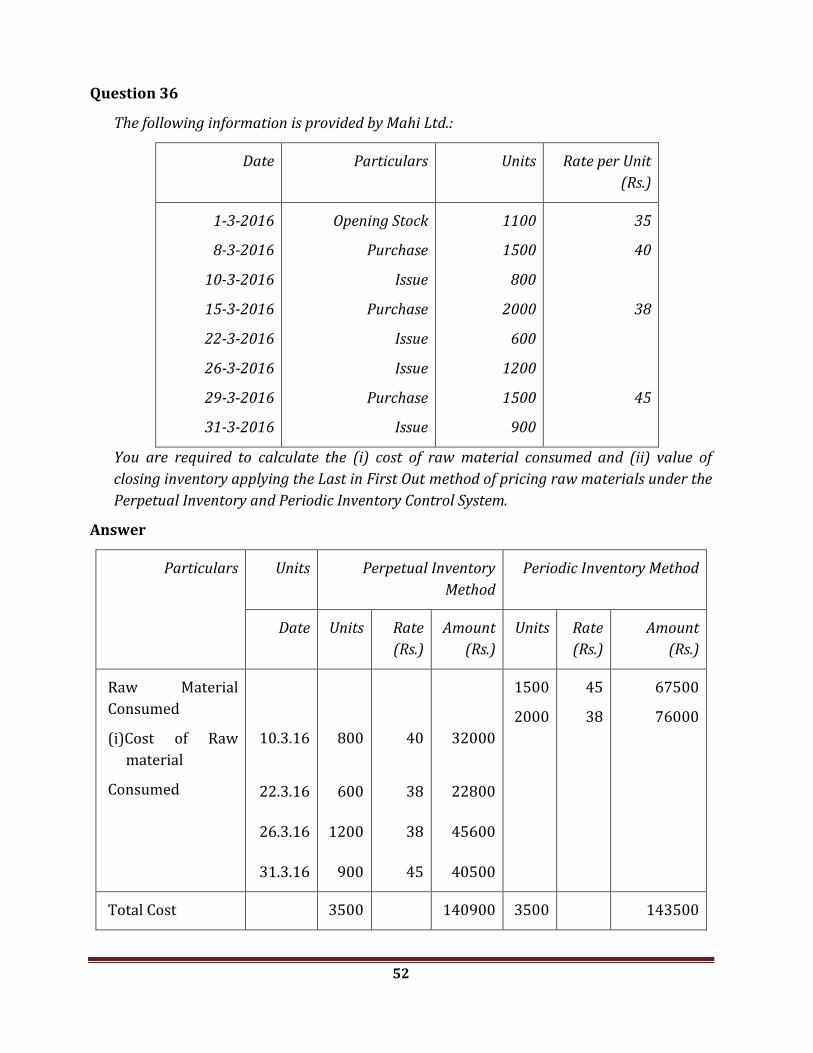

Question 32

The following receipts and issues were recorded in the books of Mogari Udyog Ltd.:

01.1.2016 Opening stock 1500 units @ Rs. 40 per unit

03.1.2016 Purchase 1000 units @ Rs. 45 per unit

06.1.2016 Issue 800 units

09.1.2016 Issue 500 units

13.1.2016 Purchase 1200 units @ Rs. 47 per unit

15.1.2015 Return from production department 50 units @ Rs. 40 per unit

17.1.2016 Issue 700 units

20.1.2016 Purchase 1000 units @ Rs. 48 per unit

22.1.2016 Issue 400 units

27.1.2016 Issue 600 units

You are required to (i) prepare a Stores Ledger Account showing how the values of issues

would be. Calculate under Weighted Average Cost Method if Base Stock of 500 units is

maintained. (ii) Find out value of closing stock on 31st January, 2016.

Answer

(i) Stores Ledger Account

(Base stock of 500 units under weighted Average cost method)

Date Receipts Issues Balance Rate for further issue

(Rs.)

Qty Rate

Rs.

Amount

Rs.

Qty Rate

Rs.

Amount

Rs.

Qty Amount

Rs.

1.1.16

3.1.16

6.1.16

-

1000

-

-

45

-

-

45000

-

-

-

800

-

-

42.5

-

-

34000

500

1000

500

2000

500

20000

40000

20000

85000

20000

Base stock 500-40

40000/1000=40

85000/2000=42.50

51000/1200=42.50

48

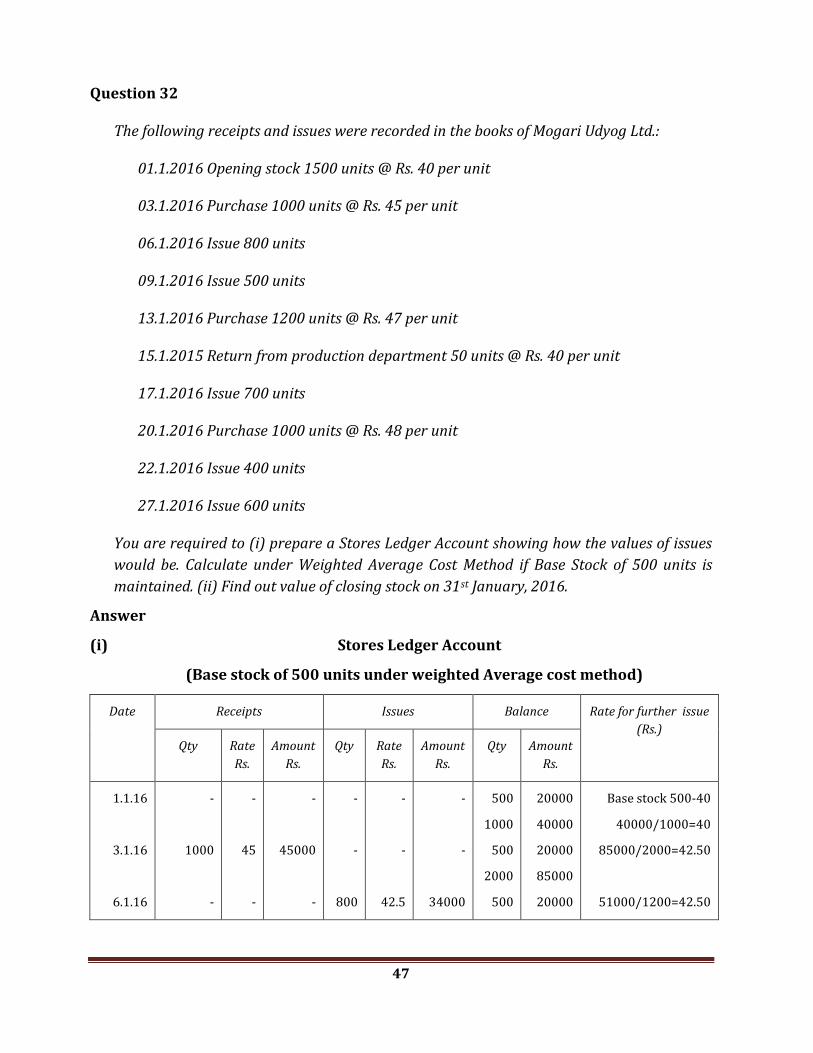

9.1.16

13.1.16

15.1.16

17.1.16

20.1.16

22.1.16

27.1.16

-

1200

50

(Return)

-

1000

-

-

-

47

40

-

48

-

-

-

56400

2000

-

48000

-

-

500

-

-

700

-

400

600

42.5

-

-

45.21

-

46.45

46.45

21250

-

-

31647

-

18580

27870

1200

500

700

500

1900

500

1950

500

1250

500

2250

500

1850

500

1250

51000

20000

29750

20000

86150

20000

88150

20000

56503

20000

104503

20000

85923

20000

58053

29750/700=42.50

86150/1900=45.34

88150/1950=45.21

56503/1250=45.20

104503/2250=46.45

85923/1850=46.45

58053/1250=46.44

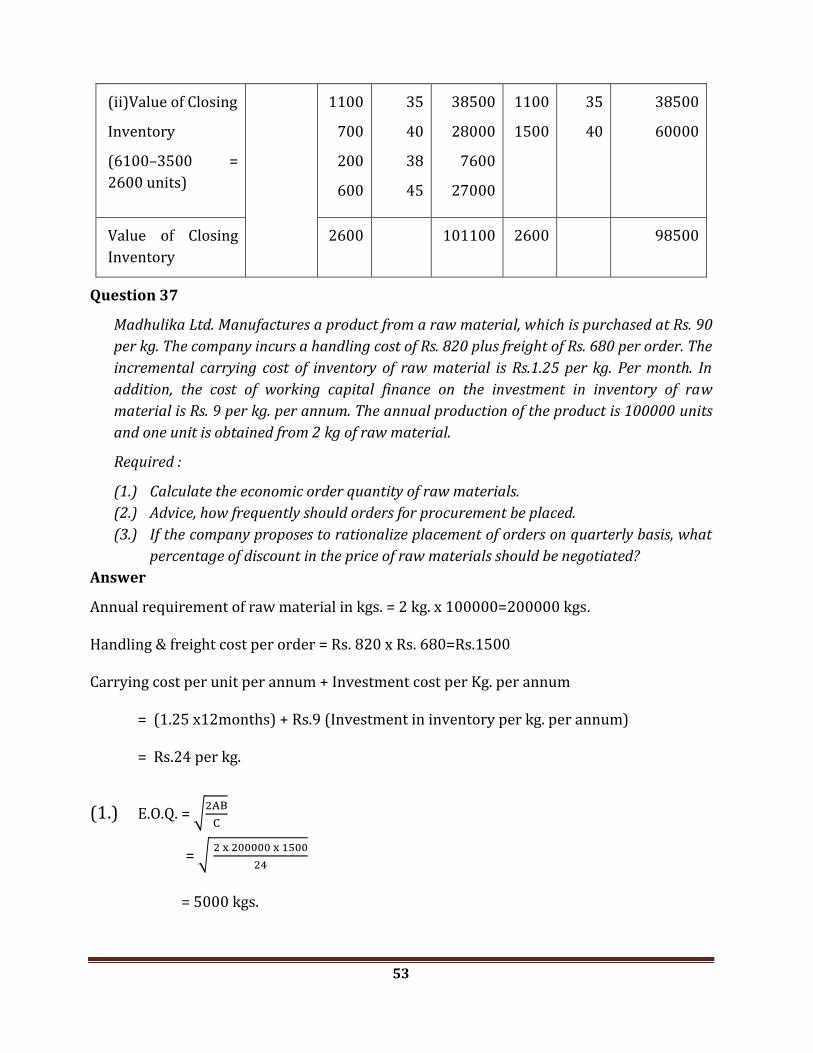

(ii) Value of closing stock on 31st January, 2016; 500+1250=1750 units

At Rs. 78053 (20000 + 58053) .

Question 33

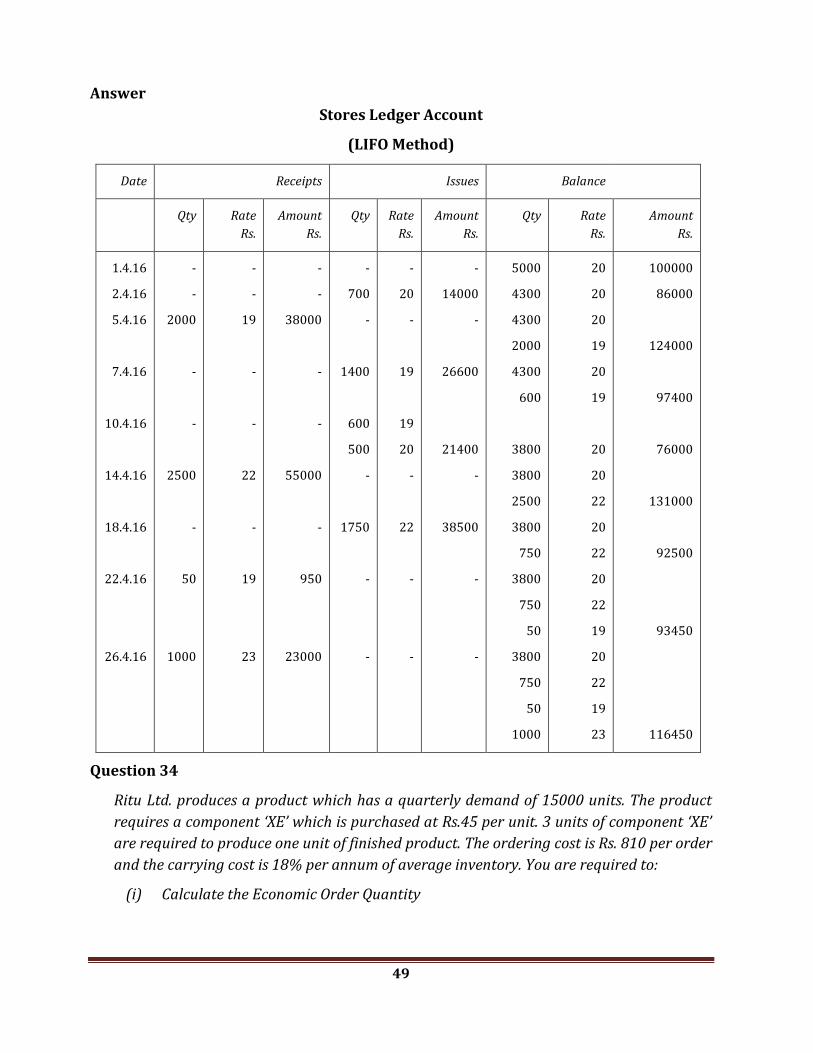

Prepare a Stores Ledger Account from the following information adopting LIFO method of

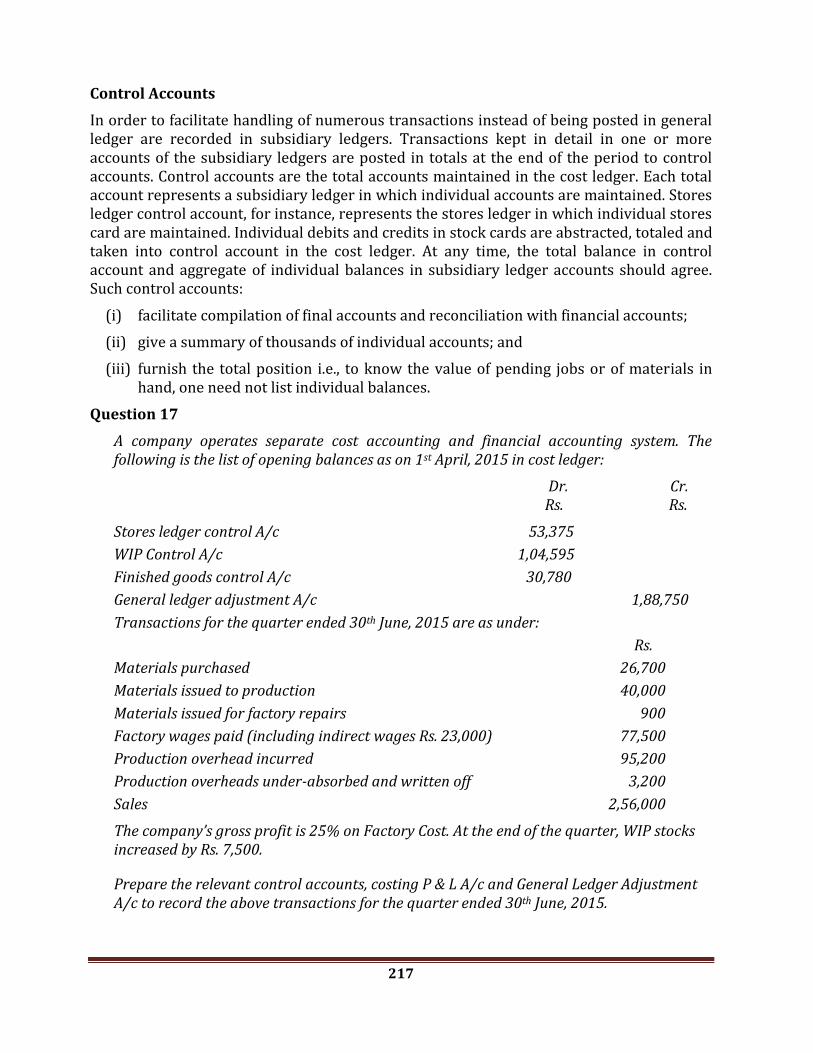

pricing of issues of materials:

01.4.2016 Opening balance 5000 kgs @ Rs. 20 per kg.

02.4.2016 Issued to Department A - 700 kgs

05.4.2016 Received from suppliers - 2000 kgs @ Rs. 19 per kg.

07.4.2016 Issued to Department B - 1400 kgs

10.4.2016 Issued to Department C - 1100 kgs

14.4.2016 Received from suppliers - 2500 kgs @ Rs. 22 per kg.

18.4.2016 Issued to Department D - 1750 kgs.

22.4.2016 Returned from department B (out of issue on 7.4.2016) - 50 kgs.

26.4.2016 Received from suppliers - 1000 kgs @ Rs. 23 per kg.

49

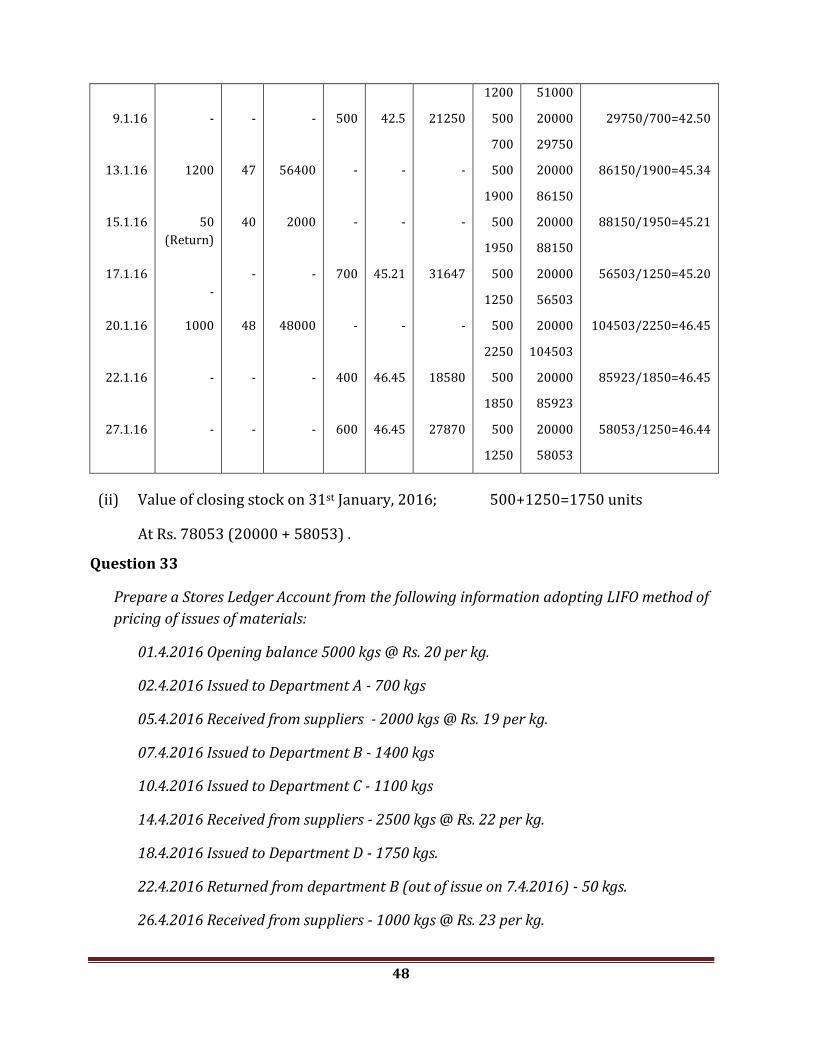

Answer

Stores Ledger Account

(LIFO Method)

Date Receipts Issues Balance

Qty Rate

Rs.

Amount

Rs.

Qty Rate

Rs.

Amount

Rs.

Qty Rate

Rs.

Amount

Rs.

1.4.16

2.4.16

5.4.16

7.4.16

10.4.16

14.4.16

18.4.16

22.4.16

26.4.16

-

-

2000

-

-

2500

-

50

1000

-

-

19

-

-

22

-

19

23

-

-

38000

-

-

55000

-

950

23000

-

700

-

1400

600

500

-

1750

-

-

-

20

-

19

19

20

-

22

-

-

-

14000

-

26600

21400

-

38500

-

-

5000

4300

4300

2000

4300

600

3800

3800

2500

3800

750

3800

750

50

3800

750

50

1000

20

20

20

19

20

19

20

20

22

20

22

20