Embed Size (px)

Citation preview

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

SOCIETE GENERALE BANKA MONTENEGRO AD FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2013 AND INDEPENDENT AUDITORS’ REPORT

SOCIETE GENERALE MONTENEGRO AD, PODGORICA

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

CONTENTS Page Independent Auditors’ Report 1 Income Statement 2 Balance Sheet 3 Statement of Changes in Equity 4 Cash Flow Statement 5 Notes to Financial Statements 6 – 50

Deloitte d.o.o. Bulevar Svetog Petra Cetinjskog bb, Zgrada Maxim 81000 Podgorica Crna Gora Tel: +382 (0) 20 228-324 +382 (0) 20 228-096 Fax: +382 (0) 20 228-327 www.deloitte.com

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the Montenegrin s hall prevail.

INDEPENDENT AUDITORS’ REPORT

To the Shareholders Assembly of Societe Generale ba nk Montenegro AD, Podgorica

We have audited the accompanying financial statements (pages 2 to 50) of Societe Generale bank Montenegro AD, Podgorica (hereinafter: “the “Bank”), which comprise the balance sheet as of December 31, 2013 and the related income statement, statement of changes in equity and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with the Law on accounting and audit of Montenegro and the regulations of the Central Bank of Montenegro governing the financial reporting of banks, as well as for internal control which management consider to be relevant to the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing and the Law on Accounting and Auditing of Montenegro. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide solid basis for our audit opinion.

Opinion In our opinion, the financial stataments present fairly, in all material respects, the financial position of Societe Generale bank Montenegro AD, Podgorica as of December 31, 2013, as well as of its financial performance and cash flows for the year then ended in accordance with the accounting regulations of Montenegro and regulations of the Central Bank of Montenegro governing the financial reporting of banks. Other Matter The financial statements of the Bank for the year ended December 31, 2012 were audited by another auditor, who expressed an unmodified opinion on those statements as at March 7, 2013.

Deloitte d.o.o. Podgorica

March 17, 2014

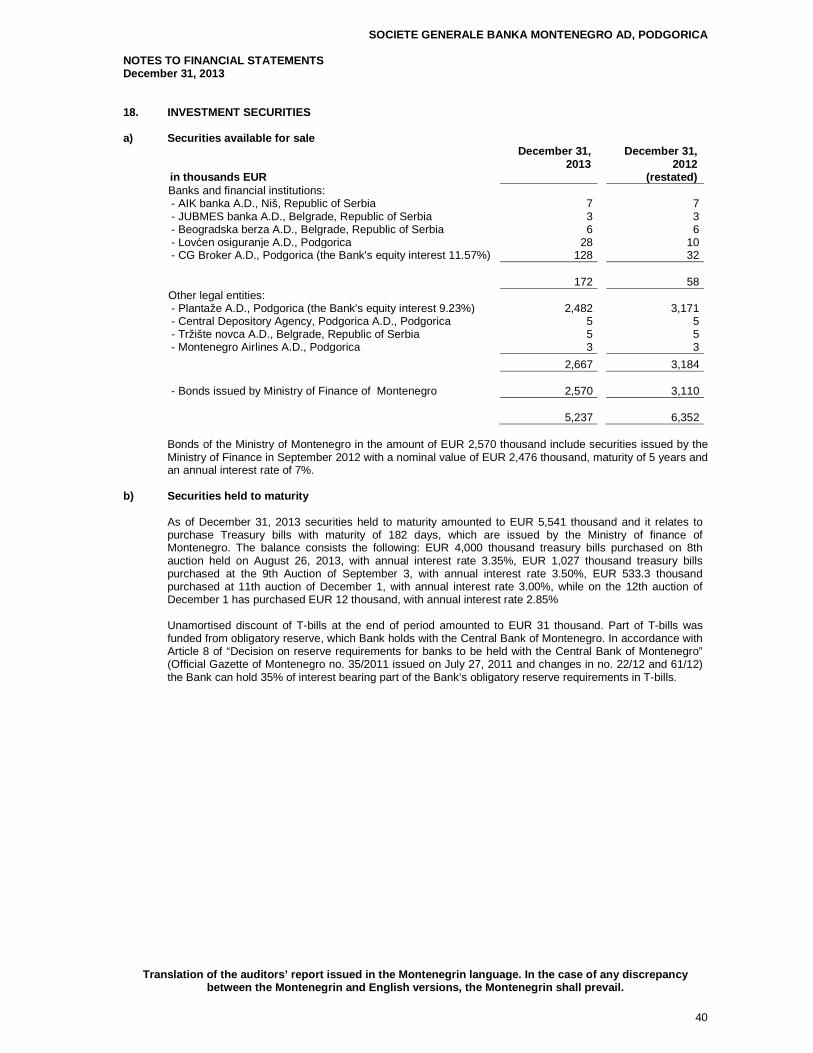

Žarko Mionić, Certified Auditor

(Licence No. 062, issued on March 10, 2011)

SOCIETE GENERALE MONTENEGRO BANKA AD, PODGORICA

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

2

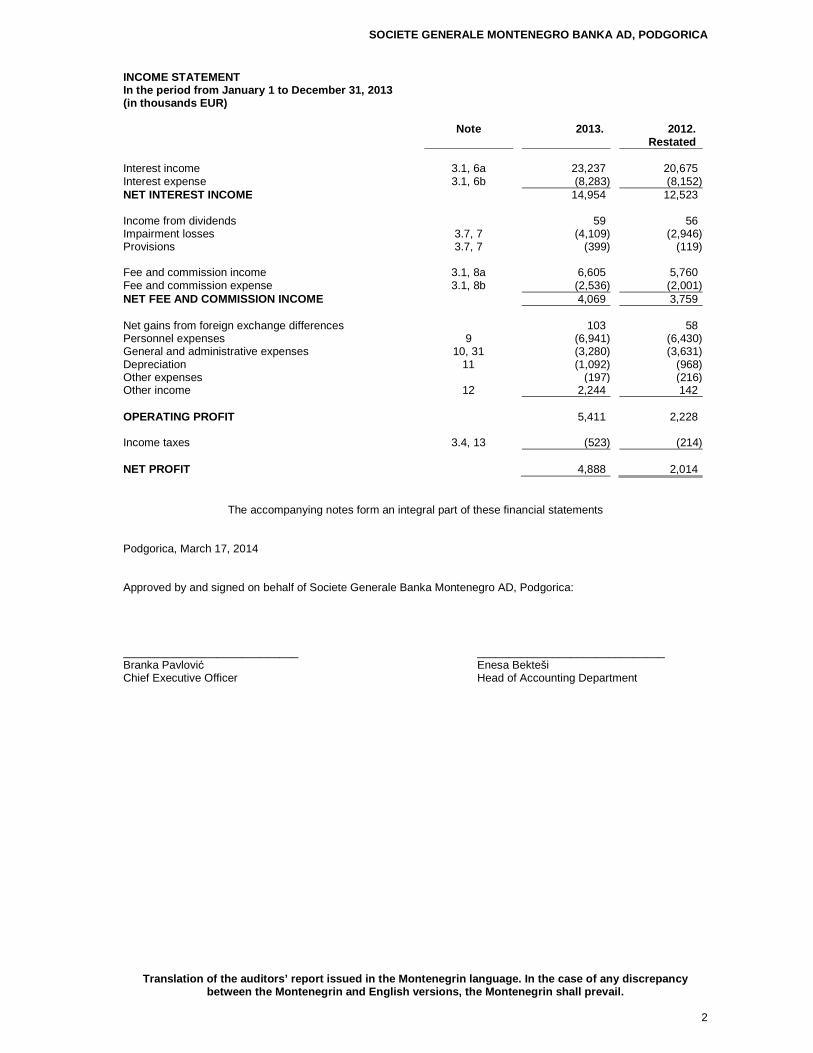

INCOME STATEMENT In the period from January 1 to December 31, 2013 (in thousands EUR)

Note

2013.

2012.

Restated Interest income 3.1, 6a 23,237 20,675 Interest expense 3.1, 6b (8,283) (8,152)NET INTEREST INCOME 14,954 12,523 Income from dividends 59 56 Impairment losses 3.7, 7 (4,109) (2,946)Provisions 3.7, 7 (399) (119) Fee and commission income 3.1, 8a 6,605 5,760 Fee and commission expense 3.1, 8b (2,536) (2,001)NET FEE AND COMMISSION INCOME 4,069 3,759 Net gains from foreign exchange differences 103 58 Personnel expenses 9 (6,941) (6,430)General and administrative expenses 10, 31 (3,280) (3,631)Depreciation 11 (1,092) (968)Other expenses (197) (216)Other income 12 2,244 142 OPERATING PROFIT 5,411 2,228 Income taxes 3.4, 13 (523) (214) NET PROFIT 4,888 2,014

The accompanying notes form an integral part of these financial statements

Podgorica, March 17, 2014 Approved by and signed on behalf of Societe Generale Banka Montenegro AD, Podgorica: ____________________________ ______________________________ Branka Pavlović Enesa Bekteši Chief Executive Officer Head of Accounting Department

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

3

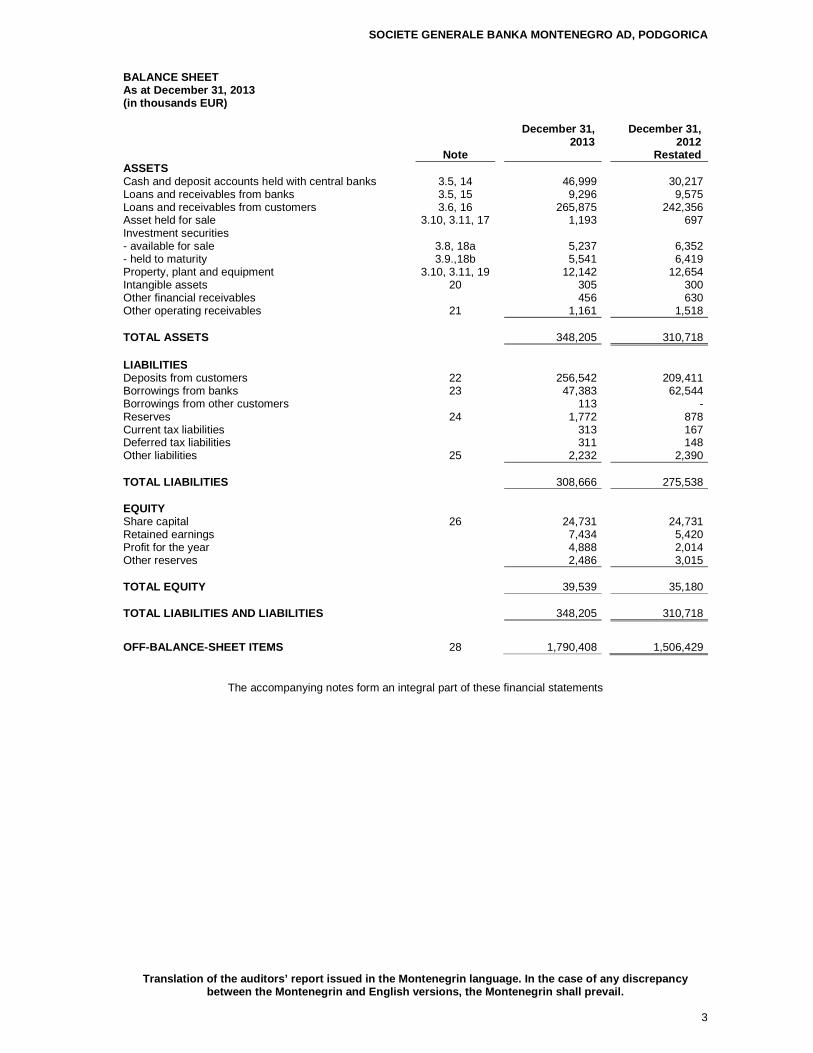

BALANCE SHEET As at December 31, 2013 (in thousands EUR)

Note

December 31, 2013

December 31, 2012

Restated ASSETS Cash and deposit accounts held with central banks 3.5, 14 46,999 30,217 Loans and receivables from banks 3.5, 15 9,296 9,575 Loans and receivables from customers 3.6, 16 265,875 242,356 Asset held for sale 3.10, 3.11, 17 1,193 697 Investment securities - available for sale 3.8, 18a 5,237 6,352 - held to maturity 3.9.,18b 5,541 6,419 Property, plant and equipment 3.10, 3.11, 19 12,142 12,654 Intangible assets 20 305 300 Other financial receivables 456 630 Other operating receivables 21 1,161 1,518 TOTAL AS SETS 348,205

310,718

LIABILITIES Deposits from customers 22 256,542 209,411 Borrowings from banks 23 47,383 62,544 Borrowings from other customers 113 - Reserves 24 1,772 878 Current tax liabilities 313 167 Deferred tax liabilities 311 148 Other liabilities 25 2,232 2,390 TOTAL LIABILITIES 308,666 275,538 EQUITY Share capital 26 24,731 24,731 Retained earnings 7,434 5,420 Profit for the year 4,888 2,014 Other reserves 2,486 3,015 TOTAL EQUITY 39,539 35,180 TOTAL LIABILITIES AND LIABILITIES 348,205 310,718

OFF-BALANCE-SHEET ITEMS 28 1,790,408 1,506,429

The accompanying notes form an integral part of these financial statements

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

4

STATEMENT OF CHANGES IN EQUITY In the period from January 1 to December 31, 2013 (in thousands EUR)

Share

capital Retained earnings

Profit for the year

Other reserves Total

Balance, as of January 1, 2012 24,731 1,142 4,278 2,756 32,907 Effects of fair value adjustment of securities available for sale

-

-

-

57

57

Actuarial gains in accordance with IAS 19 - - - 110 110 Deferred taxes on actuarial gains - - - (10) (10)Free shares to employees - - - 55 55 Transfer of profit from previous year - 4,278 (4,278) - - Profit for the year - - 2,014 - 2,014 Balance, as of December 31, 2012 24,731 5,420 2,014 2,968 35,133 The effects of the first application of the methodology for impairment of balance sheet assets in accordance with IAS 39 - - - 47 47 Restated balance, as of December 31, 2012 24,731 5,420 2,014 3,015 35,180 Effects of fair value adjustment of securities available for sale

-

-

- (552) (552)

Actuarial gains in accordance with IAS 19 - - - (28) (28)Deferred taxes on actuarial gains - - - 2 2 Free shares to employees - - - 49 49 Transfer of profit from previous year - 2,014 (2,014) - - Profit for the year - - 4,888 - 4,888 Balan ce, as of December 31, 201 3 24,731 7,434 4,888 2,486 39,539

The accompanying notes form an integral part of these financial statements

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

5

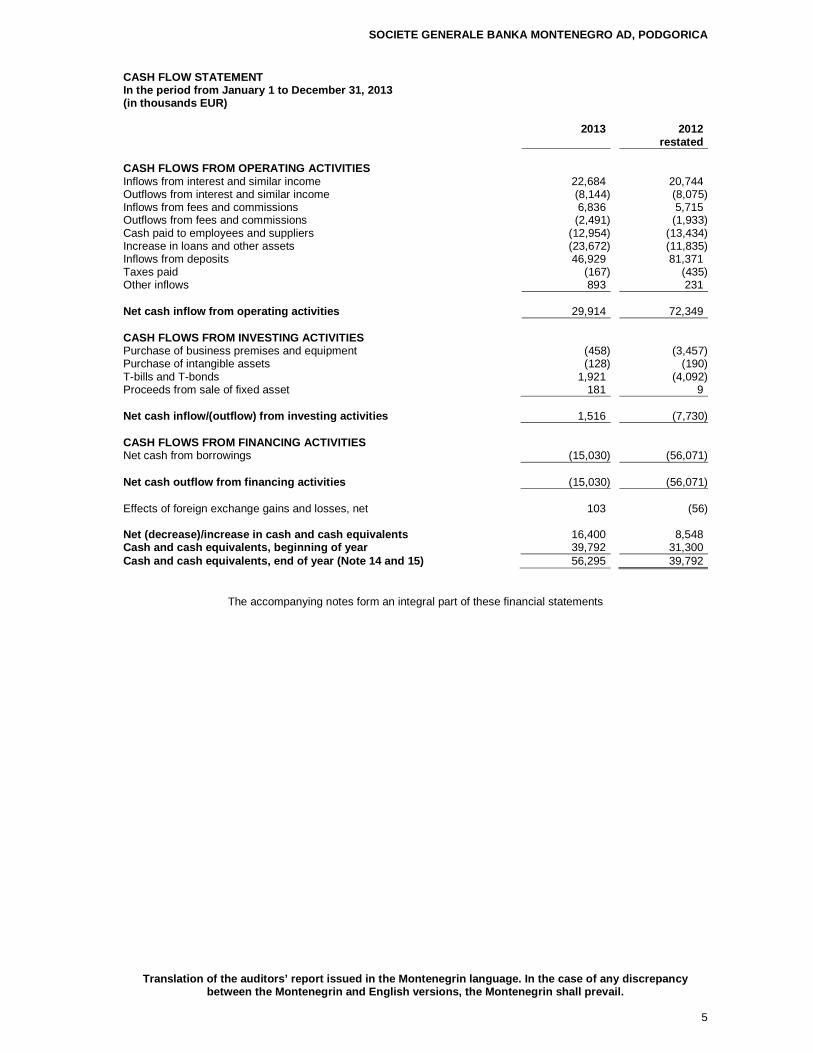

CASH FLOW STATEMENT In the period from January 1 to December 31, 2013 (in thousands EUR)

2013 2012

restated

CASH FLOWS FROM OPERATING ACTIVITIES Inflows from interest and similar income 22,684 20,744 Outflows from interest and similar income (8,144) (8,075)Inflows from fees and commissions 6,836 5,715 Outflows from fees and commissions (2,491) (1,933)Cash paid to employees and suppliers (12,954) (13,434)Increase in loans and other assets (23,672) (11,835)Inflows from deposits 46,929 81,371 Taxes paid (167) (435)Other inflows 893 231 Net cash inflow from operating activities 29,914

72,349

CASH FLOWS FROM INVESTING ACTIVITIES Purchase of business premises and equipment (458) (3,457)Purchase of intangible assets (128) (190)T-bills and T-bonds 1,921 (4,092)Proceeds from sale of fixed asset 181 9 Net cash inflow/(outflow) from investing activities 1,516

(7,730)

CASH FLOWS FROM FINANCING ACTIVITIES Net cash from borrowings (15,030) (56,071) Net cash outflow from financing activities (15,030) (56,071) Effects of foreign exchange gains and losses, net 103 (56) Net (decrease)/increase in cash and cash equivalent s 16,400 8,548 Cash and cash equivalents, beginning of year 39,792 31,300 Cash and cash equivalents, end of year (Note 14 and 15) 56,295 39,792

The accompanying notes form an integral part of these financial statements

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

6

1. FOUNDATION AND BUSINESS ACTIVITY

Podgorička Banka AD, Podgorica was established by separating from Montenegrobanka D.D., Podgorica in the course of 1992. On November 21, 2001, the Central Bank of Montenegro issued an approval enabling the bank to continue its operations pursuant to Decision 27. Following the aforementioned privatization process that took place in 2005, the majority interest in the bank is held by Societe Generale, Paris, France. On September 26, 2006, the bank was inscribed in the Central Register of the Commercial Court in Podgorica under the registration number 4-0000880/019, operating the activities as Podgorička Banka Societe Generale Group AD, Podgorica. Under registration number 4-0000880/41 on May 7, 2012, the bank was inscribed in Central Register of the Commercial Court in Podgorica as Societe Generale banka Montenegro AD. The bank is licensed to perform credit, depositary and guarantee operations, as well as foreign payments transactions, depo transaction, to provide safekeeping services, issuance, processing and recording of payment instruments (including credit cards, travellers’ and banks’ cheques). The bank is headquartered in Bulevar Revolucije 17, Podgorica. As of December 31, 2013, the bank was comprised of a Central Office located in Podgorica and 20 branch offices located throughout Montenegro. As of December 31, 2013, the bank has 268 employees (December 31, 2012: 275 employees).

2. BASIS FOR PREPARATION AND PRESENTATION OF THE FI NANCIAL STATEMENTS 2.1. Basis for preparation and presentation of the financial statements

The Bank is obligated to maintain its accounting records and prepare its statutory financial statements in conformity with the Accounting and Auditing Law of Montenegro (Official Gazette of Montenegro, nos. 69/2005, 80/2008 and 32/2011) entailing the application of International Accounting Standards (“IAS”) and decisions of the Central bank of Montenegro governing the financial reporting of banks.

The financial statements are prepared in accordance with the Decision on the Contents, Deadlines and Manner of Preparation and Submission of the financial Statements of Banks (Official Gazette of Montenegro, nos. 15/12 and 18/13). Comparative information for 2012 was reclassified in order to be comparable to the reporting format effective for the year 2013 (Notes 2.3 and 4). In the presented financial statements, reclassifications were made within the balance sheet as of December 31, 2012 for the effects of postings the Bank made as of January 1, 2013 in accordance with the Guidleines on the Manner of Forming Provisions for Potential Losses, Impairment Allowances and Written-Off Balance Sheet Assets (Official Gazette of Montenegro, no. 61/12). In preparation of these financial statements the Bank applied policies in conformity with the regulations of the Central Bank of Montenegro, which however, in the part regarding recording receivables eligible for derecognition from the Bank's balance sheet, in the format for presentation of the financial statements and in interest calculation for receivables over 90 days past due, depart from the requirements of IFRS and IAS effective as of December 31, 2013. Due to the potentially significant effects of the above described matters on the accuracy and fair presentation of the financial statements, these financial statements cannot be described as having been prepared in accordance with International Financial Reporting Standards and International Accounting Standards.

In the preparation of the accompanying financial statements, the Bank has adhered to the accounting policies described in Note 3, which are in conformity with the accounting, banking and tax regulations prevailing in Montenegro.

The official currency in Montenegro and the Bank’s functional and presentation currency is Euro (EUR).

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

7

2. BASIS FOR PREPARATION AND PRESENTATION OF THE FI NANCIAL STATEMENTS (continued) 2.2. Use of estimates

The presentation of financial statements requires the bank’s management to make best estimates and reasonable assumptions that affect the assets and liabilities’ amounts, as well as the disclosure of contingent liabilities and assets as of the date of the preparation of the financial statements, and the income and expenses arising during the accounting period. These estimations and assumptions are based on information available as of the date of preparation of the financial statements. However, actual outcome may vary from the estimated values. The most important estimates were performed on the following balance sheet positions:

• Provisions on loans and interest receivables • Provisions on deposits placed in other banks • Provision on equity investments • Provisions on off - balance sheet items • Provisions on employee benefits • Provisions on litigations and claims • Useful life of intangible and tangible assets

Bank's financial statements include provisions, calculated by an actuary, based on the estimated present value of retirement benefits and jubilee awards to employees upon vesting in respective rights, using of Projected Unit Credit method. However, the bank’s future operating results may vary from the estimated values.

2.3. Changes in the regulations of the Central Bank of Montenegro

Decision on Minimum Standards for Credit Risk Management in Banks (Official Gazette of Montenegro, no. 22/12, 55/12 and 57/13.) (hereinafter the Decision), stipulates the application of International Accounting Standards in valuation of balance sheet assets and off-balance sheet items and presentation in accordance with International Financial Reporting Standards. The Bank has adopted the methodology for assessment of balance sheet assets’ impairment and probable loss per off-balance items according to the Decision. The Bank is consistent in methodology application, reviews it annually and updates it as appropriate, and adjusts the assumptions underlying the methodology. The Guidleines on the Manner of Forming Provisions for Potential Losses, Impairment Allowances and Writte-Off of Balance Sheet Assets in determining the opening balances in the Bank’s records for 2013 (Official Gazette of Montenegro, no. 61/12) defines the following:

• Accoiunting for receivables classified in the classification category E - loss, • Calculation and accounting for interest on non-performing assets, • Accounting for provisions for potential losses according to the regulatory requirement and

allowances according to IAS, • Accounting for provisions for potential losses in accordance with the Decision effective at the time

of transition to the new Chart of Accounts (opening balance of the balance sheet), • Recording of impaired loans at the moment of transition to the new Chart of Accounts (opening

balance of the balance sheet), • Calculation and booking of allowances on impaired loans under IAS and provisions according to

the Decision from January 1, 2013 (in balance sheet and income statement).

In accordance with the Guidlelines, the Bank reclassified balance sheet and off-balance sheet items, calculated the impairment allowances under IAS and regulatory provisions, and credited the net effect of changes in the method of estimating provisions to the shortfall missing reserves for credit losses. In accordance with these regulatory requirements the Bank did not maKe adjustments to the Income statement for the comparative period.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

8

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES 3.1. Interest and fees income and expense

Interest income and expense are recognized in the income statement for all instruments measured at amortized value using the effective interest method. The effective interest method is a method of calculating the amortized cost of a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that discounts estimated future cash payments or receipts over the expected life of a financial instrument or, where appropriate, a shorter period, to the net carrying amount of the financial asset or financial liability. When calculating the effective interest rate, the bank estimates cash flows considering all contractual terms of the financial instrument (i.e. prepayment options) but does not consider future credit losses. The calculations include all fees and commissions paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts. Interest income and interest expense, including penalty interest and operating income and expenses related to interest-bearing assets and liabilities are accounted for on an accrual basis. Fees for banking services and fee and commission expenses are recorded when due, i.e., when realized. Income and expenses arising from loan and guarantee origination are accounted for on an accrual basis using effective interest method.

3.2. Foreign Exchange Translation

Transactions denominated in foreign currencies are translated in Euros using official average exchange rates determined on the Interbank Market effective on date of each transaction. Assets and liabilities denominated in foreign currencies are translated in Euros by applying the official average exchange rates, as determined on the Interbank Market, effective on the balance sheet date. Net foreign exchange gains or losses arising from transactions in foreign currencies and from translation of balance sheet items denominated in foreign currencies are credited or charged to the income statement. Commitments and contingent liabilities denominated in foreign currencies are translated in Euros by applying the official average exchange rates, as determined on the Interbank Market, effective on the balance sheet date.

3.3. Leasing

The leases entered into by the Bank are operating leases. The payments made under operating leases are charged to operating expenses in the income statement on a straight-line basis over the period of the lease agreement duration.

3.4. Taxes and Contributions

Income Taxes

Current income taxes

Income taxes are calculated and paid in conformity with Article 28 of the Corporate Income Tax Law (Official Gazette of the Republic of Montenegro, nos. 65/01, 80/04 and Official Gazette of Montenegro, nos. 40/08, 86/09, 40/11 and 14/12). The income tax rate is a proportionate rate of 9% applied to the tax base. A taxpaying entity’s taxable income is determined based on the income stated in its statutory statements of comprehensive income following certain adjustments to its income and expenses performed in accordance with the Montenegrin Income Tax Law (Articles 8 and 9 for income adjustment and Articles 10 to 20 for expense adjustment) and the Decision on the New Chart of accounts for Bank Central Bank of Montenegro (Official Gazette of Montenegro no. 55/12). Capital losses may be set off against capital gains earned in the same year. In case there are outstanding capital losses even after the set-off of capital losses against capital gains earned in the same year, these outstanding losses are available for carryforward in the ensuing 5 years. Montenegrin tax regulations do not envisage that any tax losses of the current period be used to recover taxes paid within a specific carryback period. However, any current year losses reported in the annual corporate income tax returns may be carried forward and used to reduce or eliminate taxes to be paid in future accounting periods, but only for a period of a maximum of five ensuing years.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

9

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont inued) 3.4. Taxes and Contributions (continued)

Deferred income taxes

Deferred income tax is determined using the balance sheet liability method, for the temporary differences arising between the tax bases of assets and liabilities, and their carrying values in the stand alone financial statements. The currently-enacted tax rates at the balance sheet date are used to determine the deferred income tax amount. Deferred tax liabilities are recognized for all taxable temporary differences. Deferred tax assets are recognized for the deductible temporary differences, and the tax effects of income tax losses and credits available for carry forward, to the extent that it is probable that future taxable profit will be available against which deferred tax assets may be utilized. Taxes, contributions and other duties not related t o operating results

Taxes, contributions and other duties that are not related to the bank’s operating result, include property taxes and other various taxes and contributions paid pursuant to republic and municipal regulations.

3.5. Cash and Cash Equivalents

Cash and cash equivalents comprise cash (EUR and foreign currencies) and balances with the Central Bank of Montenegro and other banks.

3.6. Loans

Loans approved by the bank are recorded in the books when funds are transferred to the loan beneficiary’s account. Loans are stated in the balance sheet in the amount of amount approved increased by invoiced and accrued interest, as decreased by the principal and interest repaid and allowance for impairment which is based on the assessment of risk inherent in certain placements and risks which have been historically identified in the credit portfolio. The bank’s management applies the methodology prescribed by the Central Bank of Montenegro in its evaluation of the risks, which is disclosed in Note 3.7.

3.7. Allowances for Impairment and Provisions for P otential Losses

The Decision issued by the Central Bank of Montenegro regarding minimal standards for management of credit risks in banks (Official Gazette of Montenegro, no. 22/12, 55/12 and 57/2013) prescribessets forth the following: elements of credit risk management, minimum criteria and manner of classifying assets and off-balance sheet items which render the bank is exposed to credit risk and the manner of determining the minimum provisions for potential losses arising from credit risk exposure. The bank's risk-weighted assets, within the meaning of this Decision, are comprised of loans, interest, fees and commissions, lease receivables, deposits with banks, advances and all other items included in the balance sheet exposing the bank to default risk, as well as guarantees issued, other sureties, effectuated letters of credit and approved, but undrawn loan facilities, as well as all other off-balance sheet items being the bank's contingent liabilities. In accordance with the Decision on Minimum standards for credit risk management in banks (Official Gazette of Montenegro, no.22/12, 55/12 and 57/2013 ) the bank shall perform at least once in quarter impairment assessment (for balance sheet items) and/or assessment of probable loss (for off-balance sheet items) for balance sheet assets and off-balance sheet items based on which it is exposed to credit risk and classify them into appropriate classification categories. According to IAS 39 the bank is also required to establish a methodology for assessing impairment of balance sheet assets and probable losses related to off-balance sheet items.

Starting from January 1, 2013 and for the purpose of calculation of credit risk provisions, the bank prepared methodology for assessment of asset impairment and probable loss for off-balance items which is compliant with the methodology of Societe Generale Group. Bank on a quarterly basis estimates whether there is an objective reason for the devaluation of exposure or group of exposures.If the bank assess that an event which has a negative effect on expected cash flows has occurred, exposure is reclassified from healthy in defaulted loans/exposures.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

10

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont inued) 3.7. Allowances for Impairment and Provisions for P otential Losses (continued)

There is an objective evidence of impairment if: - Debtor’s financial standing indicates that there are significant problems in his business; - There is data on unsettled obligations, on frequent delays in repayment of principle and/or interest,

or about unsettlement of other obligations over 90 days without chances for recent recovery (for public company, regional or local self-governments days of delay may be up to 180 days); or

- It is evident that at debtor will be initiated bankruptcy process, reorganization process or some similar process.

If there is an objective evidence of impairment, impairment test is performed and in case of need recognition of impairment loss for balance sheet items and probable loss for off balance sheet items. The objective is to present financial assets of the bank at fair value and to recognize expected losses as a result of partial or complete lack of debt collection. Impairment or a loss should be recognized in the period when it is determined that receivable will not be fully collected. The bank has a policy that on the day of impairment calculation for all loans for which there are uncollected interest receivables older than 90 days are classified under the category of receivables for which each subsequent calculation of the interest will be booked in internal records and do not affect receivables and interest income positions. These receivables are recognised in income only if collectioned from client. Impairment loss is equal to difference between gross exposure and discounted expected cash flows. Gross exposure includes: - Remaining exposure, i.e. collectible principle increased for unpaid interest till the day when

receivable is classified as defaulted. - and IAS interest i.e. interest calculated on impaired amount of receivables. Assessment of future cash flows is performed based on days of delay, client’s financial situation and collateral and direct selling costs of collateral.

Corporate loans

In accordance with Methodology for assessment of asset impairment and probable loss for off-balance items for corporate loans in default without mortgage minimum impairment from principal and interest exposure at the time the loan became defaulted are presented in accordance with days of delay, as follows:

- 91 to 180 days - 25% - 181 to 270 days the - 75% - over 270 days - 100%

For corporate loans in default fully covered with mortgage minimum impairment amounts are presented in accordance with days in delay, as follows:

- 91 to 180 days - 20% -181 to 270 days - 25% - over 270 days - 30%

For every subsequent calculation of impairment on this amount is added IAS interest calculated for pervious account period.

Retail loans

In accordance with Methodology for assessment of asset impairment and probable loss for off-balance items for retail loans in default without mortgage minimum impairment from principal and interest exposure at the time the loan became defaulted are presented in accordance with days of delay, as follows: - 91 to 150 days - 25% - 151 to 180 days - 50% - 181 to 270 days -75% - over 270 days - 100%

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

11

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont inued) 3.7. Allowances for Impairment and Provisions for P otential Losses (continued)

For every subsequent calculation of impairment on this amount is added IAS interest calculated for pervious account period. For retail loans fully covered with mortgage, only when delay is over 270 days, mortgage covers 70% of exposure, i.e. the applied percentage of impairment is 30%. Exposure can be impaired or loss can be expected, even If delay is less that 90 days, if the bank estimates that the client will become defaulted, or it requires special consideration because of confirmed or expected deterioration of credit rating. In those cases the impairment is calculated by applying percantage of 12.5% on total exposure of the client. At least quarterly, the bank is required to classify balance sheet assets and off-balance sheet items in respect of which it is exposed to credit risk and to calculate allowances for expected losses. In accordance with the Decision on Minimum standards for credit risk management in banks, loans and other risk bearing assets are classified into the following categories: • A category (“Good”) – including assets assessed as collectible in full pursuant to the agreement; • B category (“Special Mention”) – with B subcategory including items for which there is low probability of loss, but which, still the same, require special attention, as the potential risk, if not adequately monitored, could diminish their collectability; • C category (“Substandard assets”) – with C1, C2 and C3 subcategories for which there is high probability of loss, due to the clearly identified collectability issues; • D category (“Doubtful assets”) – including items the collection of which is, given the creditworthiness of loan beneficiaries, value and marketability of collaterals, highly unlikely; • E category (“Loss”) – including the items which are uncollectible in full, or will be collectible in an insignificant amount On monthly bases, based on the performed classification the bank is required to calculate the allowances for losses related to the balance sheet and off-balance sheet items, applying percentages in the following table:

As at December 31, 2013 As at December 31, 2012

%

%

Risk

category Provisions Days of delay Provisions Days of delayA - <30 - <30

B1 2 31-60 3 31-90 B2 7 61-90 C1 20 91-150 15 91-150 C2 40 151-270 30 151-210 C3 - - 50 211-270 D 70 271-365 75 271-365 E 100 >365 100 >365

The bank shall determine the difference between the amount of loan loss provisions calculated in accordance with the above given table and the sum of the amount of allowances for impairment losses and provisionings for off-balance sheet items calculated in accordance with the provisions of Decision regulating the manner of valuation of asset items by applying International Accounting Standards. The positive difference between the amount of calculated loan loss provisions and the sum of the amount of allowances for impairment andimpairment losses and provisionsing for off-balance sheet items represents necessary reserves for estimated losses. At the time of adoption of the annual financial statements the bank is required to transfer amount of necessary reserves for estimated losses from the profit in the current year or retained earnings from previous years to the account of reserves for estimated losses on regulatory requirements.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

12

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont inued) 3.8. Securities available for sale

Securities available-for-sale include securities which cannot be classified as trading financial assets or as held to maturity and are comprised of equity investments in other legal entities and investment in five-year bonds issued by the Ministry of Finance of Montenegro. Equity instruments of legal entities that do not have a quoted market price in an active market and for which other methods of reasonably estimating fair value are inappropriate and unworkable, are measured at cost, less any allowance for impairment. Investments in Plantaže AD, Podgorica, Lovćen AD Podgorica, CG broker-diler AD and investments in bonds issued by the Ministry of Finance of Montenegro are recorded at fair value. After initial recognition, unrealized gains and losses arising from changes in the fair value of available-for-sale financial assets are recognized directly in equity (revaluation reserves), until the financial asset is derecognized or impaired at which time the cumulative gain or loss previously recognized in equity should be recognized in profit or loss. Dividends on available for sale equity instruments are recognized in the income statement when the entity’s right to receive payment is established. After initial recognition, securities available for sale are recorded at fair value. Unrealized gains and losses on securities available for sale are recorded within unrealized gains and losses in equity, until the securities are sold, collected or otherwise realised or until such securities are impaired. When securities available for sale are sold or when their value is impaired, the accumulated fair value adjustments, previously recognised in equity, are recognised in the income statement. Interest income on securities is calculated and accrued monthly.

3.9. Held to maturity securities

Held to maturity securities relates to purchase of Treasury bills with maturity of 182 days, which are issued by the Government of Montenegro. Income is recognized on a monthly bases based on approved (contracted) discount. Part of the T-bills was funded from obligatory reserve, which the bank holds with the Central Bank of Montenegro. In accordance with Article 8 and 17a of “The decision on reserve requirements for banks to be Held with the Central Bank of Montenegro” (Official Gazette of Montenegro no. 35/2011 dated July 27, 2011 and no. 22/2012 and 61/2012) the bank can hold up to 35% of the bank’s obligatory reserve requirements in the form of treasury bills issued by the Government of Montenegro.

3.10. Business Premises, Other Property and Equipme nt and Intangible Assets

Business premises, other property, equipment and intangible assets on December 31, 2012 2013 are recorded at cost less accumulated depreciation and/or amortisation. Purchase value represents the prices billed by suppliers together with all costs incurred in bringing the respective asset to the location and condition necessary for its intended use. Depreciation and/or amortization are calculated on a straight-line basis on cost of business premises and other property, equipment and intangible assets in order to write them off over their expected useful lives. Depreciation and/or amortization are calculated using the following prescribed annual rates: Rate % Business premises

3.3 Computer equipment 25.0 Furniture and other equipment 15.0 Air conditioning system 10.0 Vehicles 15.0 Intangible assets 30.0

The calculation of depreciation and/or amortization commences when asset is placed into use. Pursuant to the Article 13, paragraph 6 of the Income Tax Law ("Official Gazette of Montenegro" no. 80/2004, 40/2008, 86/2009 and 14/2012) value of buildings for tax purposes is calculated using the proportional method and value of equipment and application software by applying digressive method for the entire period, regardless the date of activation. Business premises belong to the group I forto which is applied rate is of 5%, while the remaining fixed asset, equipment and softwares, are arranged in groups II to V, for which is applied rates are in range of 15% to 30%.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

13

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont inued) 3.11. Impairment of tangible and intangible assets

On each balance sheet date, the bank’s management reviews the carrying amounts of the bank’s tangible and intangible assets. If there is any indication that such assets have been impaired, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss. If the recoverable amount of an asset is estimated to be less than its carrying value, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognised as an expense of the current period and is recorded under other operating expenses. Where impairment loss subsequently reverses, the carrying amount of the asset is increased up to the revised estimate of its recoverable value. However, this is performed so that the increased carrying amount does not exceed the carrying value that would have been determined had no impairment loss been recognised for the asset in prior years.

3.12. Provisions

Provisions are recognised when the bank has a present legal or constructive obligation as a result of past events, and when it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of the obligation can be made.

3.13. Employee Benefits

Employee Taxes and Contributions for Social Securit y In accordance with the current regulations in Montenegro, the bank has an obligation to pay contributions to various State’s social security funds. These obligations involve the payment of contributions on behalf of the employee, by the employer in an amount calculated by applying the specific, legally-prescribed rates. The bank is also legally obligated to withhold contributions from gross salaries to employees, and on behalf of the employees, to transfer the withheld portions directly to government funds. These contributions payable on behalf of the employee and employer are charged to expenses in the period in which they arise.

Retirement benefits and other long term employee be nefits In accordance with the Collective Bargaining Agreement, the bank has an obligation to disburse an employment retirement benefit to a retiree, in an amount equal to six average net salaries effective in the bank in the month prior to the employee’s retirement. In addition, employees are entitled to receive jubilee awards at their 10th, 20th and 30th employment anniversaries with the bank as follows: - for 10 years of service – one minimal salary in the bank, - for 20 years of service – two minimal salaries in the bank, - for 30 years of service – three minimal salaries in the bank The bank's financial statements as of December 31, 2013 include provisions calculated by an actuary based on the estimated present value of retirement benefits and jubilee awards to employees upon vesting in respective rights, using of projected unit credit method.

3.14. Financial Liabilities – Borrowings Borrowings are initially recognised at fair value less transaction costs. Subsequently, borrowings are carried at their amortized value; all differences between the realized inflows (less transaction costs) and the amounts repaid are carried through profit and loss over the period of using the amounts borrowed by applying the effective interest rate method.

3.15. Fair Value

In accordance with International Financial Reporting Standards the fair value of financial assets and liabilities should be disclosed in the Notes to the Financial Statements. For these purposes, the fair value is defined as an amount at which an asset can be exchanged, or a liability settled, between knowledgeable willing parties in an arm’s-length transaction. The bank should disclose the fair value information of those components of assets and liabilities for which published market information is readily available, and for which their fair value is materially different from their recorded amounts. In Montenegro, sufficient market experience, stability and liquidity do not exist for the purchase and sale of receivables, investments and other financial assets or liabilities, for which published market information is presently not available. Fair value cannot readily be determined in the absence of active capital and financial markets, as generally required under the provisions of IFRS/IAS. According to the opinion of the management of the bank, the reported carrying amounts are the most valid and useful reporting values under the present market conditions and accounting regulations of Montenegro and Central Bank’s regulations for financial reporting. In the amount of the identified estimated risk that the carrying value will not be realized, a provision is recognised based on a relevant decision of the bank’s management.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

14

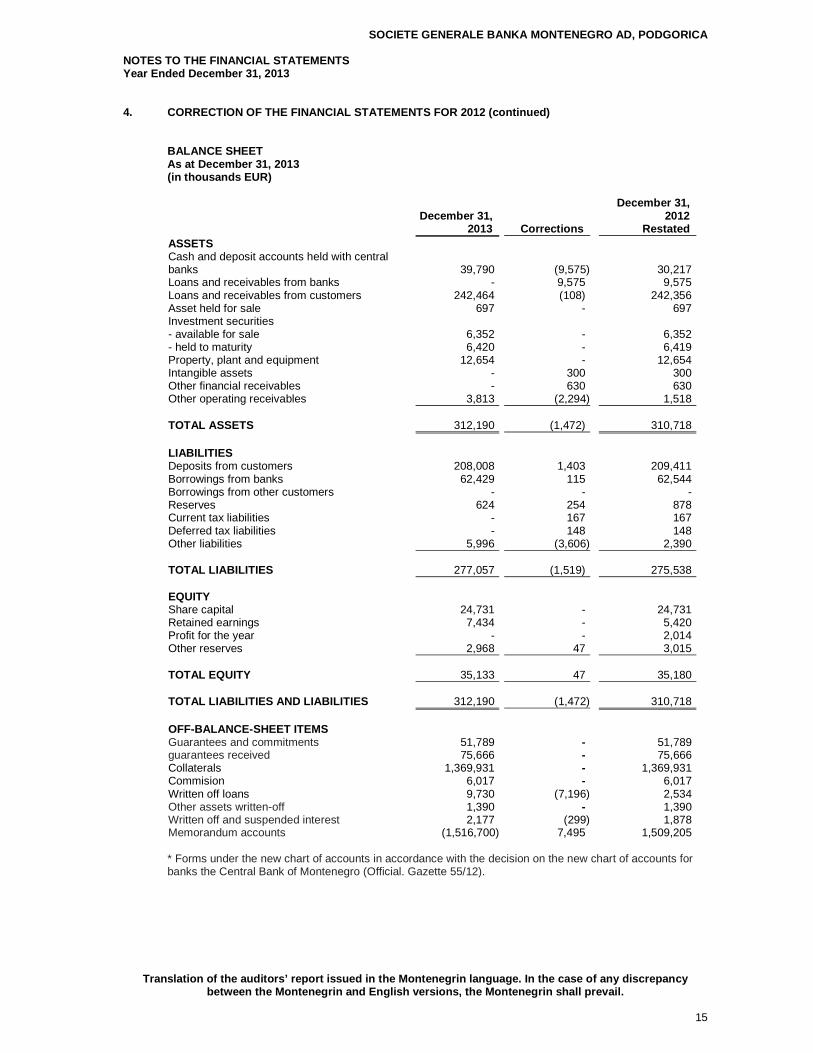

4. CORRECTION OF THE FINANCIAL STATEMENTS FOR 2012

The bank has made certain adjustments of balance sheet and off-balance sheet items as at December 31, 2012, as well as the reclassification of balance sheet and income statement for the purpose of comparability with the financial statements for the 2013 which are by January 1, 2013 modified in accordance with the Decision on the contents, terms and method of preparation and submission of financial statements of banks ("Off. Gazette of Montenegro", no. 15/2012 and 18/2013), the decision of the Chart of Accounts for Banks ("Off. Gazette of above "55/12), Decision on minimum Standards for Credit Risk Management in Banks (" Off. Gazette of Montenegro ", 22/12, 55/12 and 57/13) and the Guidelines on the method of recording reserves for potential credit losses, corrections values and amortizable assets in the balance sheet items of the initial conditions in the books of banks for 2013th ("Official. Gazette of Montenegro", no. 61/12), as disclosed in Note 2.3 and ordered the tables below:

INCOME STATEMENT In the period from January 1 to December 31, 2013 (in thousands EUR)

2012 before correction* Corrections

2012. restated

Interest income 20,832 (157) 20,675 Interest expense (8,152) - (8,152)NET INTEREST INCOME 12,680 (157) 12,523 Income from dividends - 56 56 Impairment losses (3,222) 276 (2,946)Provisions - (119) (119)Fee and commission income 5,760 - 5,760 Fee and commission expense (2,001) - (2,001)NET FEE AND COMMISSION INCOME 3,759 - 3,759 Net gains from foreign exchange differences 58 - 58 Personnel expenses (6,430) - (6,430)General and administrative expenses (3,631) - (3,631)Depreciation (968) - (968)Other expenses (216) - (216)Other income 198 (56) 142 OPERATING PROFIT 2,228 - 2,228 Income taxes (214) - (214) NET PROFIT 2,014 - 2,014

* Forms under the new chart of accounts in accordance with the decision on the new chart of accounts for banks the Central Bank of Montenegro (Official. Gazette 55/12).

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

15

4. CORRECTION OF THE FINANCIAL STATEMENTS FOR 2012 (continued)

BALANCE SHEET As at December 31, 2013 (in thousands EUR)

December 31,

2013

Corrections

December 31, 2012

Restated ASSETS Cash and deposit accounts held with central banks 39,790 (9,575) 30,217 Loans and receivables from banks - 9,575 9,575 Loans and receivables from customers 242,464 (108) 242,356 Asset held for sale 697 - 697 Investment securities - available for sale 6,352 - 6,352 - held to maturity 6,420 - 6,419 Property, plant and equipment 12,654 - 12,654 Intangible assets - 300 300 Other financial receivables - 630 630 Other operating receivables 3,813 (2,294) 1,518 TOTAL ASSETS 312,190 (1,472)

310,718

LIABILITIES Deposits from customers 208,008 1,403 209,411 Borrowings from banks 62,429 115 62,544 Borrowings from other customers - - - Reserves 624 254 878 Current tax liabilities - 167 167 Deferred tax liabilities - 148 148 Other liabilities 5,996 (3,606) 2,390 TOTAL LIABILITIES 277,057 (1,519) 275,538 EQUITY Share capital 24,731 - 24,731 Retained earnings 7,434 - 5,420 Profit for the year - - 2,014 Other reserves 2,968 47 3,015 TOTAL EQUITY 35,133 47 35,180 TOTAL LIABILITIES AND LIABILITIES 312,190 (1,472) 310,718 OFF-BALANCE-SHEET ITEMS Guarantees and commitments 51,789 - 51,789 guarantees received 75,666 - 75,666 Collaterals 1,369,931 - 1,369,931 Commision 6,017 - 6,017 Written off loans 9,730 (7,196) 2,534 Other assets written-off 1,390 - 1,390 Written off and suspended interest 2,177 (299) 1,878 Memorandum accounts (1,516,700) 7,495 1,509,205

* Forms under the new chart of accounts in accordance with the decision on the new chart of accounts for banks the Central Bank of Montenegro (Official. Gazette 55/12).

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

16

5. FINANCIAL INSTUMENTS

5.1. Risk management

Bank is exposed in its operation to a various risks, including the most important:

• credit risk; • market risk; • liqidity risk; • operational risk.

The risk management procedures are designed to identify and analyze risks, to define limits and controls required for risk management and to monitor Bank’s exposure to each individual risk. Procedures for risk management are subject to regular control in order to adequately respond to the changes in the market, products and services. Risk department is responsible for monitoring Bank’s exposure to a certain risks which is reported to Board of Directors on a monthly basis. In addition, monitoring of Bank’s exposure to a certain risks is the resposnsibility of Committee for credit risk , Committee of operational risk and Committe on asset and liability management.

5.2. Credit risk

Banks is exposed to credit risk which is a riks that counterparty will be unable to pay full amount due to the bank and on time. Bank is creating provisions for imapairment losses, related to losses expected on reporting date. Significan changes in the economic environment or certain industries included in bank’s loan portfolio could result in losses that are different from the losses provided for in the statement of financial position. Therefore, management carefully manages bank’s exposure to credit risk.

5.2.1. Credit risk managemnt Credit risk exposure is a risk of financial loss which is a result of borrowers being unable to fulfill contractual obligations to the bank. The bank manages credit risk by placing the limits with respect to large loans, individual borrowers and related parties. Those risks are continuously monitored and are subject of constant control.

In accordance to the limits prescribed by the Central Bank of Montenegro, sector concentration is constantly monitored. Credit risk management is performed by regular analyses of the ability of borrowers and potential borrowers to repay obligations in respect of interest and principal. Credit Related Commitments and Contingent Liabiliti es The primary purpose of those instruments is to ensure that funds are available to a customer as required. Guarantees and letters of credit represent irrevocable assurances that the bank will make payments in the event that a customer can not meet its obligations to third parties, and therefore carry the same credit risk as loans. Documentary and commercial letters of credit - which are written undertakings by the bank on behalf of the client, which authorizes a third party to draw bills of exchange on the bank up to a stipulated amount under specific conditions – are secured by the underlying goods deliveries to which they relate and therefore carry less risk than a loan.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

17

5. FINANCIAL INSTRUMENS (continued) 5.2. Credit risk (continued)

5.2.2. Provisions for Impairment Losses in Accorda nce with Requirements of IAS 39

On the balance sheet date bank assesses if there is any objective evidence for impairment of financial asset or a group of financial assets, in accordance to IAS 39. If the bank determines that an event occured which will negatively affect expected cash flows, exposure is reclasified from healthy to bad loans/exposures. Bank is obliged at least on a quarterly basis to assess quality of its assets, and to determine if there is an objective evidence of impairment for balance sheet assets or probable losses related to off balance sheet items. There is an objective evidence of impairment if: - Debtor’s financial standing indicates that there are significant problems in his business; - There is data on unsettled obligations, on frequent delays in repayment of principle and/or interest,

or about unsettlement of other obligations over 90 days without chances for recent recovery (for public company, regional or local self-governments days of delay may be up to 180 days); or

- It is evident that at debtor will be initiated bankruptcy process, reorganization process or some similar process.

If there is an objective evidence of impairment, impairment test is performed and in case of need recognition of impairment loss for balance sheet items and probable loss for off balance sheet items. The objective is to present financial assets of the bank at fair value and to recognize expected losses as a result of partial or complete lack of debt collection. Impairment or a loss should be recognized in the period when it is determined that receivable will not be fully collected. Exposure can be impaired or loss can be expected, even If delay is less that 90 days, if the bank estimates that the client will become defaulted, or it requires special consideration because of confirmed or expected deterioration of credit rating. In those cases the impairment is calculated by applying percantage of 12,5% on total exposure of the client.

5.2.3. Maximum exposure to credit risk for balance sheet and off balance sheet items

In thousands EUR 2013. 2012.

Balance sheet items Loans and receivables from banks 9,296 9,575 Loans and receivables from clients 265,214 241,780 Interest and other receivables 661 576 Securities – available for sale 5,237 6,352 Securities – held tu maturity 5,541 6,419

285,949 264,702 Off balance sheet items Payment guaranties 23,076 20,534 Performance guarantiees 9,442 8,375 Letters of credit 2,637 1,077 Undrawn credit facilities 21,216 21,749

56,371 51,735 Total exposure to credit risk 342,320 316,437

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

18

5. FINANCIAL INSTRUMENS (continued) 5.2. Credit risk (continued)

5.2.3. Maximum exposure to credit risk for balance sheet and off balance sheet items (continued)

Exposure to credit risk is partially controlled by obtaining collateral and guaranties of legal entities and individuals. In addition, all individuals are required to receive their monthly salary through a current account with the bank in order to reduce credit risk. Types of securing the loans:

• Deposits; • Pledges placed against industrial machines, securities, inventories and vehicles; • Mortgages and fiduciarytransfer of ownership; • Bills of exchange; • Authorizations; • Administrative injunctions; • Guarantors and • insurance.

5.2.4. Loans and Advances

Loans and advances are presented in the following tables:

In thousands EUR

Neither Past due nor

Impaired Past Due but not Impaired

Individua-lly

Impaired Total, Gross

Individual Allowance for

Impairment Total, net exposure

31.Decembe r 2013 Housing loans 25,354 3,276 430 29,060 (235) 28,825 Customer loans 65,980 6,361 3,243 75,584 (2,861) 72,723 Cards 1,044 1,942 291 3,277 (232) 3,045 Special purpose loans 333 15 2 350 (2) 348 Other loans to individuals covered by mortgage 21,075

4,455

305

25,835

(190)

25,645

Loans to micro and small enterprises 14,826 7,205 3,144 25,175 (1,635) 23,540 Loans to medium and large enterprises 74,425 9,940 16,703 101,068 (5,899) 95,169 Lons to Government and municipalities 14,623 1,293 - 15,916 - 15,916 Loans to financial institutions - 3 5 8 (5) 3

217,660

34,490

24,123

276,273

(11,059)

265,214

In thousands EUR

Neither Past due nor

Impaired Past Due but not Impaired

Individually Impaired Total, Gross

Individual Allowance for

Impairment Total, net exposure

31.Decembe r 2012 Housing loans 17,840 2,647 224 20,711 (188) 20,523 Customer loans 52,125 5,798 4,912 62,835 (4,294) 58,541 Cards 1,181 1,685 426 3,292 (266) 3,026 Special purpose loans 304 15 - 319 - 319 Other loans to individuals covered by mortgage 19,042

3,232

190

22,464

(141)

22,323

Loans to micro and small enterprises 13,696 5083 2,767 21,546 (1,382) 20,164 Loans to medium and large enterprises 84,541 9,079 12,891 106,511 (4,101) 102,410 Lons to Government and municipalities 13,000 1,474 14,474 - 14,474 Loans to financial institutions - - 5 5 (5) -

201,729

29,013

21,415 252,157

(10,377)

241,780

Loans and advances neither past due nor impaired in u 2013 and 2012 are all ranked under the satisfactory risk category.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

19

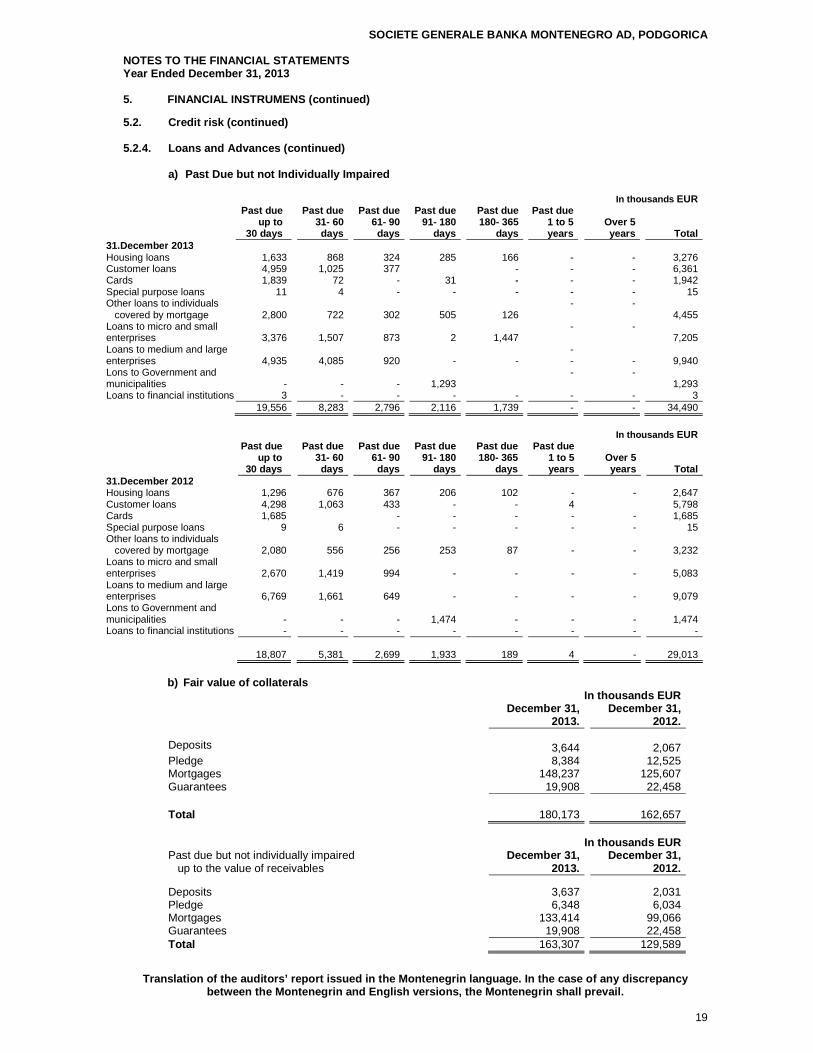

5. FINANCIAL INSTRUMENS (continued) 5.2. Credit risk (continued) 5.2.4. Loans and Advances (continued)

a) Past Due but not Individually Impaired

In thousands EUR Past due

up to 30 days

Past due 31- 60 days

Past due 61- 90

days

Past due 91- 180

days

Past due 180- 365

days

Past due 1 to 5 years

Over 5 years

Total

31.Decembe r 2013 Housing loans 1,633 868 324 285 166 - - 3,276 Customer loans 4,959 1,025 377 - - - 6,361 Cards 1,839 72 - 31 - - - 1,942 Special purpose loans 11 4 - - - - - 15 Other loans to individuals covered by mortgage 2,800

722

302 505

126

- - 4,455

Loans to micro and small enterprises 3,376

1,507

873 2

1,447

- - 7,205

Loans to medium and large enterprises 4,935

4,085

920 -

-

- -

-

9,940

Lons to Government and municipalities -

-

- 1,293

- - 1,293

Loans to financial institutions 3 - - - - - - 3 19,556 8,283 2,796 2,116 1,739 - - 34,490

In thousands EUR

Past due up to

30 days

Past due 31- 60

days

Past due 61- 90

days

Past due 91- 180

days

Past due 180- 365

days

Past due 1 to 5 years

Over 5 years Total

31.Decembe r 2012 Housing loans 1,296 676 367 206 102 - - 2,647 Customer loans 4,298 1,063 433 - - 4 5,798 Cards 1,685 - - - - - 1,685 Special purpose loans 9 6 - - - - - 15 Other loans to individuals covered by mortgage 2,080

556

256 253

87

-

-

3,232

Loans to micro and small enterprises 2,670

1,419

994 -

-

-

-

5,083

Loans to medium and large enterprises 6,769

1,661

649 -

-

-

-

9,079

Lons to Government and municipalities -

-

- 1,474 - -

- 1,474

Loans to financial institutions - - - - - - - -

18,807

5,381

2,699 1,933

189

4 -

29,013

b) Fair value of collaterals In thousands EUR December 31,

2013. December 31,

2012. Deposits

3,644

2,067

Pledge 8,384 12,525 Mortgages 148,237 125,607 Guarantees 19,908 22,458 Total 180,173 162,657

In thousands EUR

Past due but not individually impaired up to the value of receivables

December 31, 2013.

December 31, 2012.

Deposits 3,637 2,031 Pledge 6,348 6,034 Mortgages 133,414 99,066 Guarantees 19,908 22,458 Total 163,307 129,589

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

20

5. FINANCIAL INSTRUMENS (continued) 5.2. Credit risk (continued) 5.2.4. Loans and advances (continued)

b) Fair value of collaterals (continued)

In thousands EUR

Individually impaired up to the value of receivables December 31,

2013. December 31,

2012. Deposits 7 36 Pledge 2,036 6,491 Mortgages 14,823 26,541 Total 16,866 33,068

As collateral, the Bank accepts mortgages against immovables the fair value of which, pursuant to the certified appraiser’s valuations, exceeds the minimum 25% for the exposures to the individuals, and 50% for the exposures to corpoarte clients, of total loan, except if some other decisions do not define this differentlly. Properties used as collateral are housing premises, apartment buildings, business buildings and premises, as well as land depending on its location and future use. c) Restructured Loans and Advances

The Bank restructured a loan to the borrower due to a decline in the borrower’s creditworthiness, if it has:

a. Extended the principal and interest maturity, b. Decreased the interest rate on the loan approved, c. Reduced the amount of debt, principal or interest or d. Made other concessions which place the borrower in a better financial position.

Upon restructuring of the loan, the Bank performs financial analysis of the borrower and assesses its capacitates to realize cash flows necessary for the repayment of the loan principal, as well as the corresponding interest once the loan is restructured. During 2013 the Bank restructured loans in the amount of EUR 27,494 thousand (2012: EUR 27,322 thousand). d) Geographic Concentration

Geographic concentration of the Bank’s exposure to the credit risk, exclusive of the allowance for

impairment is as follows: In thousands EUR European USA and Montenegro Union Canada Other Total Loans and advances to banks -

6,757

2,435

104 9,296

Loans and advances to customers 276,257

13

-

3 276,273

Secutities - available for sale 5,215 - - 22 5,237 Securities held to maturity 5,541 - - - 5,541 December 31, 2013 287,013

6,770

2,435

129 296,347

December 31, 2012 264,908 6,792 2,620 183 274,503

SOCIETE GENERALE BANKA MONTENEGRO A.D., PODGORICA NAPOMENE UZ FINANSIJSKE IZVJEŠTAJE 31. decembar 2013. godine

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the Montenegrin shall prevail.

21

5. FINANCIAL INSTRUMENTS (continued) 5.2. Credit risk (continued) 5.2.4. Loans and advances (continued)

e) Industry Concentration Industry concentration of the Bank’s exposure to the credit risk, exclusive of the allowance for impairment is as follows:

Finance

Transportation, Traffic and

Tele- communication

Services, Tourism,

Hotel Mana- gement

Trading

Civil Engineering

Electrical power

industry

Mining Admini stration

Real Estate

Agriculture

Hunting and

Fishing Manu-

facturing Other Retail

Customers

Loans and advances to banks 9,296

-

-

-

-

-

-

- -

- -

-

9,296 Loans and advances to customers 8 6,945 3,181 72,345 15,111 6,023 16,829 27 9,121 8,980 3,980 133,723

276,273

Secutities - available for sale 2,742

-

- -

- -

-

-

-

- 2,482 13 -

5,237

Securities held to maturity 5,541

-

-

-

-

-

- -

- -

-

5,541

December 31, 2013 17,587 6,945 3,181 72,345 15,111 6,023 16,829 27 9,121 11,462 3,993 133,723 296,347

December 31, 2012 19,163 7,683 2,832 75,239 15,470 6,009 15,380 28 7,610 12,632 3,353 109,104 274,503

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

22

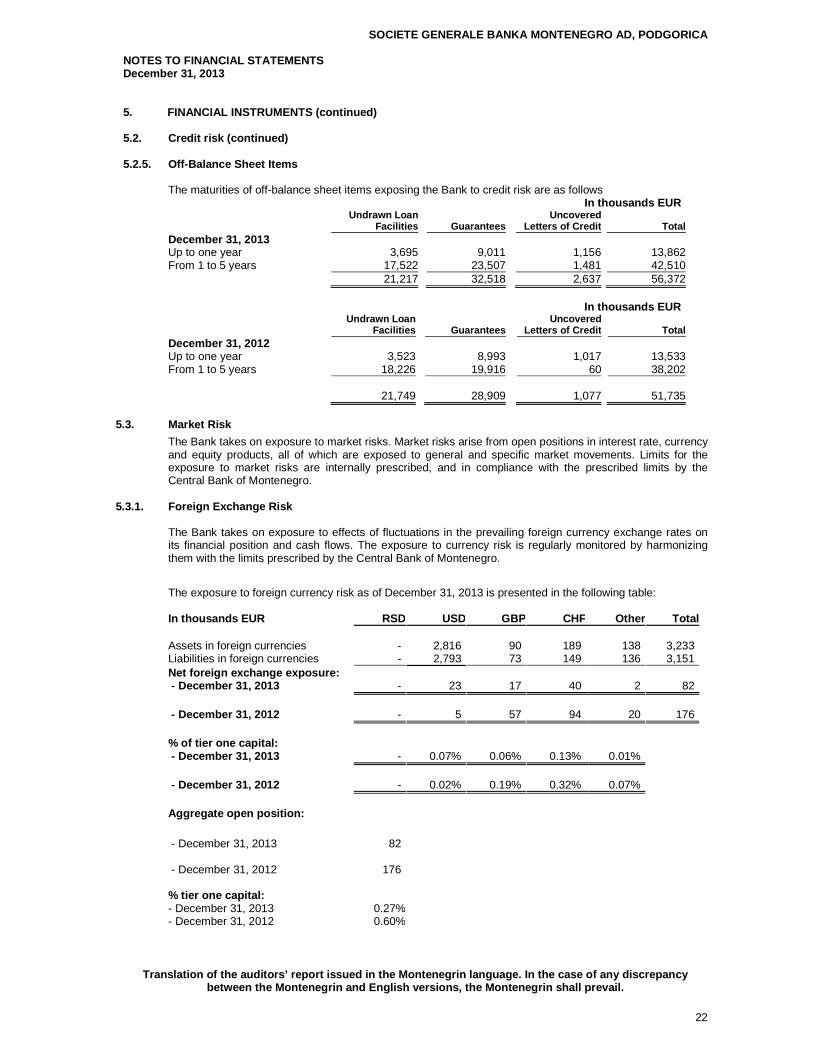

5. FINANCIAL INSTRUMENTS (continued) 5.2. Credit risk (continued) 5.2.5. Off-Balance Sheet Items The maturities of off-balance sheet items exposing the Bank to credit risk are as follows

In thousands EUR Undrawn Loan

Facilities Guarantees Uncovered

Letters of Credit Total December 31, 2013 Up to one year 3,695 9,011 1,156 13,862From 1 to 5 years 17,522 23,507 1,481 42,510

21,217 32,518 2,637 56,372

In thousands EUR

Undrawn Loan

Facilities Guarantees Uncovered

Letters of Credit Total December 31, 2012 Up to one year 3,523 8,993 1,017 13,533From 1 to 5 years 18,226 19,916 60 38,202 21,749 28,909 1,077 51,735

5.3. Market Risk

The Bank takes on exposure to market risks. Market risks arise from open positions in interest rate, currency and equity products, all of which are exposed to general and specific market movements. Limits for the exposure to market risks are internally prescribed, and in compliance with the prescribed limits by the Central Bank of Montenegro.

5.3.1. Foreign Exchange Risk

The Bank takes on exposure to effects of fluctuations in the prevailing foreign currency exchange rates on its financial position and cash flows. The exposure to currency risk is regularly monitored by harmonizing them with the limits prescribed by the Central Bank of Montenegro.

The exposure to foreign currency risk as of December 31, 2013 is presented in the following table: In thousands EUR RSD USD GBP CHF Other Total

- 2,816 90 189 138 3,233 Assets in foreign currencies Liabilities in foreign currencies - 2,793 73 149 136 3,151 Net foreign exchange exposure: - December 31, 2013 - 23 17 40 2 82 - December 31, 2012 - 5 57 94 20 176 % of tier one capital: - December 31, 2013 - 0.07% 0.06% 0.13% 0.01% - December 31, 2012 - 0.02% 0.19% 0.32% 0.07% Aggregate open position:

- December 31, 2013 82 - December 31, 2012 176 % tier one capital: - December 31, 2013 0.27% - December 31, 2012 0.60%

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

23

5. FINANCIAL INSTRUMENTS (continued) 5.3. Market Risk (continued) 5.3.1. Foreign Exchange Risk (continued)

Cash flow interest rate risk is the risk that the future cash flows of a financial instrument will fluctuate because of changes in market interest rates. Fair value interest rate risk is the risk that the value of a financial instrument will fluctuate because of changes in market interest rates. The Bank takes on exposure to the effects of fluctuations in the prevailing levels of market interest rates on both its fair value and cash flow risks. Interest margins may increase as a result of such changes but may reduce or create losses in the event that unexpected movements arise. The interest rates are based on market rates and the Bank regularly performs repricing. The following table presents the Bank’s interest bearing and non-interest bearing assets and liabilities as of December 31, 2013: In thousands EUR

Interest Bearing

Non-Interest Bearing Total

ASSETS Cash and balances with the Central Bank 3,595 43,404 46,999 Loans and advances to banks 2,363 6,933 9,296 Loans and advances to customers 265,875 - 265,875 Secutities - available for sale 2,570 2,667 5,237 Securities held to maturity 5,541 - 5,541 Total assets 279,944 53,004 332,948 LIABILITIES Due to customers 239,635 16,907 256,542 Other borrowed funds 47,383 - 47,383 Other liabilities 113 - 113 Total liabilities 287,131 16,907 304,038 Interest Sensitive Gap: - December 31, 2013 (7,187) 36,097 28,910 - December 31, 2012 13,026 13,370 26,396

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

24

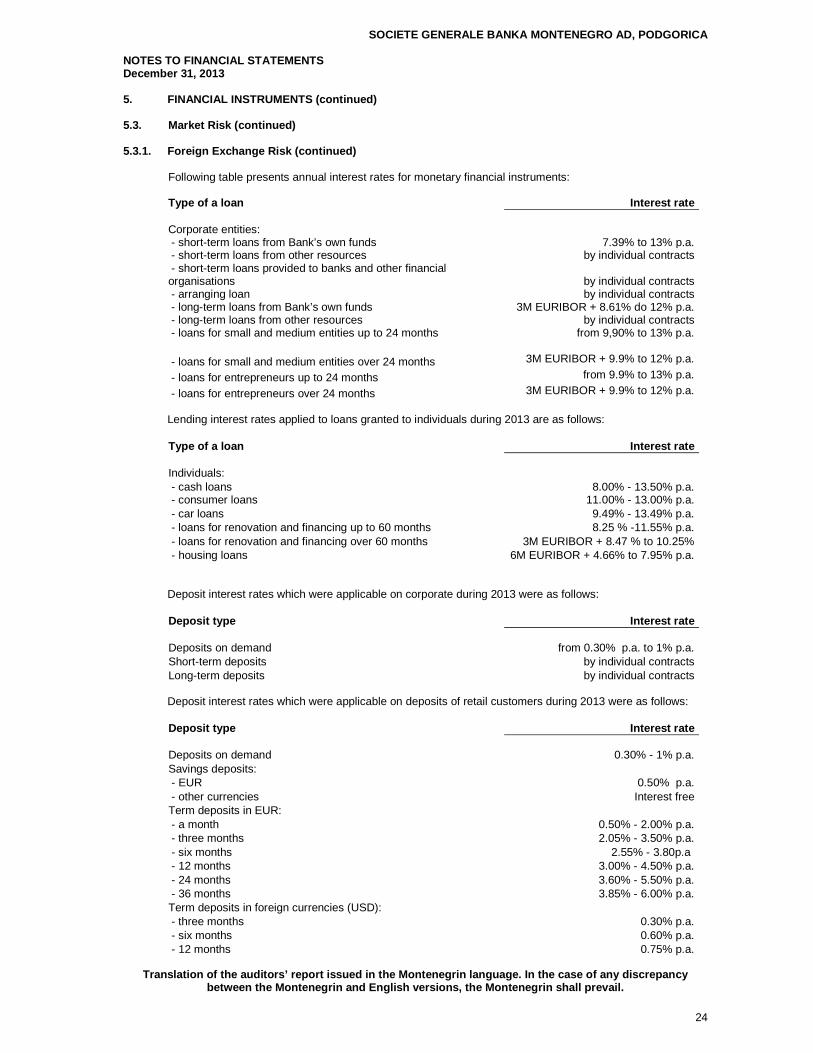

5. FINANCIAL INSTRUMENTS (continued) 5.3. Market Risk (continued) 5.3.1. Foreign Exchange Risk (continued)

Following table presents annual interest rates for monetary financial instruments: Type of a loan Interest rate Corporate entities:

- short-term loans from Bank’s own funds 7.39% to 13% p.a. - short-term loans from other resources by individual contracts - short-term loans provided to banks and other financial organisations by individual contracts - arranging loan by individual contracts - long-term loans from Bank’s own funds 3M EURIBOR + 8.61% do 12% p.a. - long-term loans from other resources by individual contracts - loans for small and medium entities up to 24 months from 9,90% to 13% p.a. - loans for small and medium entities over 24 months 3M EURIBOR + 9.9% to 12% p.a.

- loans for entrepreneurs up to 24 months from 9.9% to 13% p.a.

- loans for entrepreneurs over 24 months 3M EURIBOR + 9.9% to 12% p.a. Lending interest rates applied to loans granted to individuals during 2013 are as follows:

Type of a loan Interest rate Individuals:

- cash loans - consumer loans

8.00% - 13.50% p.a. 11.00% - 13.00% p.a.

- car loans 9.49% - 13.49% p.a. - loans for renovation and financing up to 60 months 8.25 % -11.55% p.a. - loans for renovation and financing over 60 months 3M EURIBOR + 8.47 % to 10.25% - housing loans 6M EURIBOR + 4.66% to 7.95% p.a. Deposit interest rates which were applicable on corporate during 2013 were as follows:

Deposit type Interest rate Deposits on demand

from 0.30% p.a. to 1% p.a.

Short-term deposits by individual contracts Long-term deposits by individual contracts

Deposit interest rates which were applicable on deposits of retail customers during 2013 were as follows:

Deposit type Interest rate Deposits on demand

0.30% - 1% p.a.

Savings deposits: - EUR 0.50% p.a. - other currencies Interest free Term deposits in EUR: - a month 0.50% - 2.00% p.a. - three months 2.05% - 3.50% p.a. - six months 2.55% - 3.80p.a - 12 months 3.00% - 4.50% p.a. - 24 months 3.60% - 5.50% p.a. - 36 months 3.85% - 6.00% p.a. Term deposits in foreign currencies (USD): - three months 0.30% p.a. - six months 0.60% p.a. - 12 months 0.75% p.a.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

25

5. FINANCIAL INSTRUMENTS (continued) 5.3. Market Risk (continued) 5.3.1. Foreign Exchange Risk (continued)

The table below shows the Bank’s exposure to interest rate risk as of December 31, 2013:

In thousands EUR

Interest rate sensitive assets Up to one

monthFrom 1 to 3

monthFrom 3 to 6

mon thFrom 6 to 12

month Over 1 year Total Interest-bearing deposits in other institutions 5,958 - - -

- 5,958

Securities held to maturity - 5,000 541 5,541 Loans and other receivables from clients 155,871 27,350 16,206 20,618

56,227 276,273

Other sensitive assets - - - 725 1,918 2,643 Total: 161,829 32,350 16,747 21,343 58,145 290,415

55.72% 11.14% 5.77% 7.35% 20.02% 100% % of total interest-bearing assets Interest rate sensitive liabilities Interest bearing deposits 110,485 15,206 40,732 52,279 20,933 239,635 Interest-bearing borrowings 20,002 14,290 10,006 11 3,089 47,398 Total: 130,487 29,496 50,738 52,290 24,022 287,033

45.46% 10.28% 17.68% 18.22% 8.37% 100% % of total interest-bearing liabilities

Interest rate exposure: - December 31, 201 3 31,342 2,854 (33,991) (30,947) 34,123 3,381 - December 31, 201 2 47,662 (26,445) (14,128) (24,110) 22,282 5,261 Cumulative GAP:

- December 31, 201 3 31,342 34,196 205 (30,742) 3,381 - December 31, 201 2 47,662 21,217 7,089 (17,021) 5,261

5.4. Liquidity Risk

Liquidity risk includes both the risk of being unable to provide cash to settle liabilities at appropriate maturities and the risk of being unable to liquidate an asset at a reasonable price and in an appropriate time frame.

5.4.1. Liquidity Risk Management The matching and controlled mismatching between the maturities and interest rates of assets and of liabilities is fundamental to the management of the Bank. It is unusual for banks ever to be completely matched since business transacted is often of uncertain term and of different types. An unmatched position potentially enhances profitability, but also increases the risk of losses. The maturities of assets and liabilities and the ability of the Bank to replace, at an acceptable cost, interest-bearing liabilities as they mature, are important factors in assessing the liquidity of the Bank and its exposure to changes in interest rates and exchange rates. Liquidity requirements to support calls under guarantees and standby letters of credit are considerably less than the amount of the commitment because the Bank does not generally expect the third party to draw funds under the agreement. The total outstanding contractual amount of commitments to extend credit does not necessarily represent future cash requirements, since many of these commitments will expire or terminate without being funded.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

26

5. FINANCIAL INSTRUMENTS (continued)

5.4. Liquidity Risk (continued) 5.4.1. Liquidity Risk Management (continued)

The Bank is exposed to daily calls on its available cash resources which influence the available cash held on the current accounts or as deposits. The Bank does not maintain cash to meet all of these needs since historical experience demonstrates that a minimum level of reinvestment of maturing funds can be predicted with a high degree of certainty. The expected maturities of the Bank’s asset and liability components as of December 31, 2013 were as follows:

In thousands EUR

Up to one month

From 1 t o 3 months

From 3 to 6months

From 6 to 12months

From 1 to 5years

Over 5 years Total

Financial assets Cash balances and deposit accounts with depository institutions 46,999 - - - - - 46,999 Loans and deposits to banks 9,296 - - - - 9,296 Loans and other receivables form clients 22,550 19,306 27,122 45,132 108,750 53,412 276,273 Securities available for sale - - - 653 4,584 5,237 Securities held to maturity - 5,000 541 - - - 5,541 Other financial assets, including investments in shares 917 2,045 - - - - 2,962 Total: 79,762 26,351 27,663 45,785 113,334 53,412 346,307 Financial liabilities Deposits 45,235 19,702 46,832 65,164 79,524 87 256,544 Borrowings from banks and other clients 100 3,575 6 16,010 27,805 - 47,496 Other financial liabilities 2,560 - - 285 11 - 2,856 Total: 47,895 23,277 46,838 81,459 107,340 87 306,896 Maturity gap: - December 31, 201 3 31,867 3,074 (19,175) (35,674) 5,994 53,325 39,411 - December 31, 201 2 20,377 (26,099) 3,469 (16,967) 4,217 39,279 24,276 Cumulative GAP: - December 31, 201 3 31,867 34,941 15,766 (9,908) (13,914) 39,411 - December 31, 2012 20,377 (5,722) (2,253) (19,220) (15,003) 24,276 % of total funds : - December 31, 201 3 10.38% 11.39% 5.14% -6.49% -4.50% 12.84% - December 31, 201 2 7.38% -2.07% -0.82% -6.96% -5.43% 8.79%

The structure of the Bank’s financial assets and liabilities as classified into their relevant maturities as of December 31, 2013 indicates the existence of a liquidity gap in the period from 3 months up to 1 year. The Bank’s liquidity, characterised by its ability to settle its due obligation, depends on one hand on the balance sheet structure, and on the other hand, on the matching between cash inflows and outflows. At December 31, 2013, demand deposits in the above table are presented by the expected maturity which is calculated using the Societe Generale Group model based on historical data from the Bank. The Bank applies this approach for liquidity management as of December 31, 2012.

SOCIETE GENERALE BANKA MONTENEGRO AD, PODGORICA

NOTES TO FINANCIAL STATEMENTS December 31, 2013

Translation of the auditors’ report issued in the M ontenegrin language. In the case of any discrepancy between the Montenegrin and English versions, the M ontenegrin shall prevail.

27

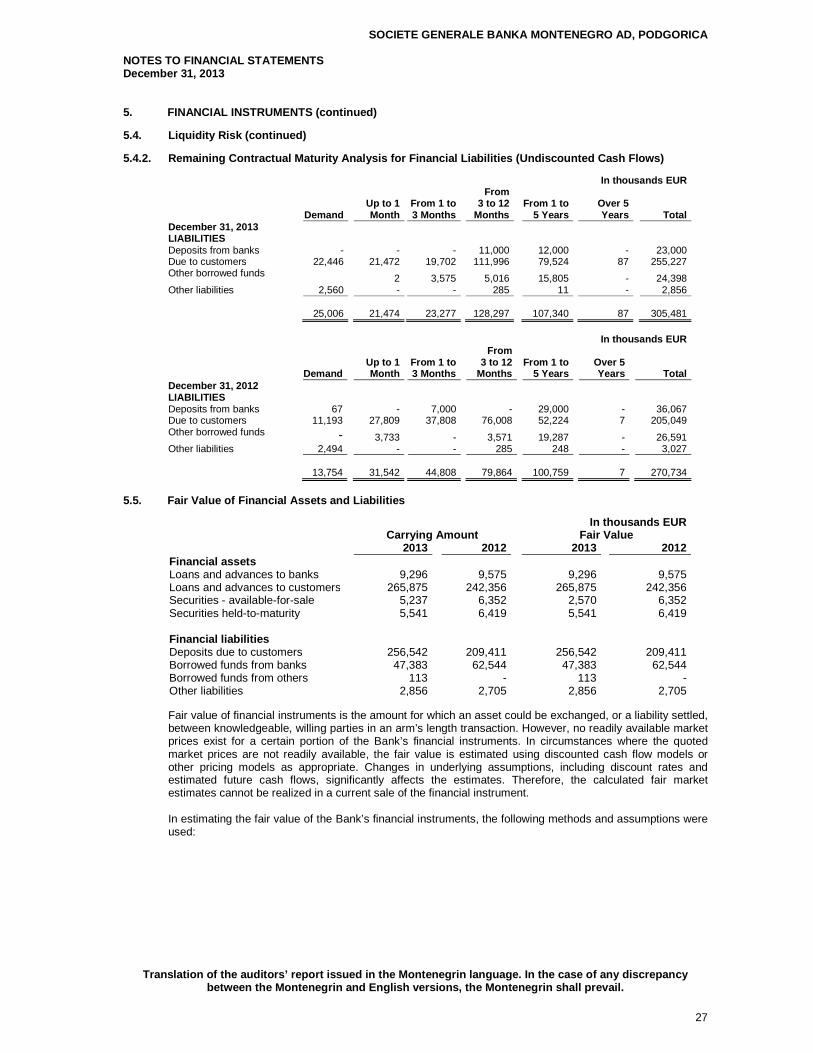

5. FINANCIAL INSTRUMENTS (continued)

5.4. Liquidity Risk (continued) 5.4.2. Remaining Contractual Maturity Analysis for F inancial Liabilities (Undiscounted Cash Flows)

In thousands EUR

Demand

Up to 1 Month

From 1 to 3 Months

From 3 to 12

Months

From 1 to

5 Years

Over 5 Years

Total December 31, 201 3

LIABILITIES Deposits from banks - - - 11,000 12,000 - 23,000 Due to customers 22,446 21,472 19,702 111,996 79,524 87 255,227 Other borrowed funds 2 3,575 5,016 15,805 - 24,398 Other liabilities 2,560 - - 285 11 - 2,856

25,006 21,474 23,277 128,297 107,340 87 305,481

In thousands EUR

Demand

Up to 1 Month

From 1 to 3 Months

From 3 to 12

Months

From 1 to

5 Years

Over 5 Years