Embed Size (px)

Citation preview

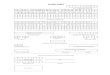

SOCIAL SECURITY SYSTEM

(All amounts in Philippine peso unless otherwise stated)

Statement of financial position

At 31 December Increase/(decrease)

Note 2015 2014

ASSETS

Current assets

Cash and cash equivalents 4 19,112,368,217 14,083,905,111 5,028,463,106

Held-to-maturity investments 5 23,447,522,042 17,133,909,303 6,313,612,739

Held-for-trading financial assets 6 4,295,367,446 3,926,486,365 368,881,082

Loans & receivables 7 548,782,374 698,177,807 (149,395,433)

Other receivables 8 7,663,422,547 10,178,110,135 (2,514,687,588)

Other current assets 9 300,476,320 165,314,848 135,161,472

55,367,938,946 46,185,903,568 9,182,035,378

Non-current assets

Financial assets 10 358,376,203,072 354,840,305,711 3,535,897,361

Investment property 11 19,488,937,709 17,956,117,270 1,532,820,439

Property and equipment 12 4,414,892,489 3,155,817,281 1,259,075,208

Intangible assets 13 141,272,896 127,447,442 13,825,454

Non-current assets held for sale 14 4,386,197,083 4,331,335,842 54,861,241

Other non-current assets 15 2,223,852,256 567,996,129 1,655,856,127

389,031,355,505 380,979,019,674 8,052,335,831

Total assets 444,399,294,451 427,164,923,243 17,234,371,209

LIABILITIES

Current liabilities

Accounts payable and accrued expenses 16 4,060,149,416 3,935,637,573 124,511,843

Funds held in trust 17 765,881,517 601,712,695 164,168,822

Deferred income 18 47,346,854 40,414,297 6,932,557

Other current liabilities 19 2,018,275,378 2,412,024,481 (393,749,102)

6,891,653,165 6,989,789,045 (98,135,879)

Non-current liabilities

Accrued retirement benefits 20 1,501,493,327 1,498,874,327 2,619,000

Rent payable 21 18,455,690 8,667,336 9,788,354

Deferred income 22 463,314,857 351,067,005 112,247,852

1,983,263,875 1,858,608,669 124,655,206

Total liabilities 8,874,917,040 8,848,397,714 26,519,326

RESERVES 23 435,524,377,411 418,316,525,529 17,207,851,882

Total liabilities and reserves 444,399,294,451 427,164,923,243 17,234,371,209

The notes on pages 9 to 41 form part of these financial statements

Book1 5

SOCIAL SECURITY SYSTEM

(All amounts in Philippine peso unless otherwise stated)

Statement of profit or loss and other comprehensive income

Year ended 31 December Increase/(decrease)

Note 2015 2014

Revenues

Members' contribution 132,615,001,628 120,650,176,296 11,964,825,332

Investment and other income 24 29,486,866,665 34,530,627,499 (5,043,760,834)

162,101,868,293 155,180,803,795 6,921,064,498

Expenditures

Benefit payments 25

Retirement 63,084,598,735 56,086,469,443 6,998,129,292

Death 34,793,885,370 33,530,284,836 1,263,600,534

Maternity 5,213,138,153 4,416,251,890 796,886,262

Disability 4,152,579,448 3,762,793,935 389,785,512

Funeral grant 3,073,285,313 2,914,563,179 158,722,135

Sickness 2,226,135,701 1,870,977,839 355,157,862

Medical services 15,973,343 16,739,338 (765,995)

Rehabilitation services 1,224,384 655,594 568,790

112,560,820,447 102,598,736,055 9,962,084,392

Operating expenses

Personnel services 26 5,755,113,244 5,467,378,561 287,734,683

Maintenance and other operating expenses 27 3,091,267,562 2,646,243,286 445,024,275

8,846,380,806 8,113,621,848 732,758,958

Total expenditures 121,407,201,253 110,712,357,903 10,694,843,350

Net revenue/profit for the year 40,694,667,040 44,468,445,892 (3,773,778,852)

Other comprehensive income/(loss)

Items that may be reclassified subsequently to profit or loss

Available-for-sale financial assets

Reclassification adjustments (167,841,422) (1,837,245,940) 1,669,404,517

Net gain/(loss) on fair value adjustment (24,362,335,815) 4,092,599,826 (28,454,935,641)

Net gain on revaluation of land 1,122,325,680 - 1,122,325,680

(23,407,851,557) 2,255,353,886 (25,663,205,443)

Total comprehensive income for the year 17,286,815,483 46,723,799,778 (29,436,984,295)

The notes on pages 9 to 41 form part of these financial statements

Book1 6

SOCIAL SECURITY SYSTEM

(All amounts in Philippine peso unless otherwise stated)

Statement of changes in reserves

Investments Flexi-fund PESO fund Property

revaluation members' members' revaluation Contingent Donated

Reserve fund reserve equity equity reserve surplus property Total reserves

Balance at 1 January 2014 359,919,929,240 9,626,545,031 391,855,049 1,763,625,900 7,040,647 11,391,980 371,720,387,847

Changes in reserves for the year

Corporate operating budget of:

Employees' Compensation Commission (69,876,100) - - - - - (69,876,100)

Occupational Safety and Health Center (106,198,152) - - - - - (106,198,152)

Contribution - - 77,521,804 - - - 77,521,804

Withdrawal - - (29,628,291) - - - (29,628,291)

Guaranteed income - - 5,337,786 - - - 5,337,786

Management cost of investment - - (4,015,106) - - - (4,015,106)

Annual incentive benefit (8,040,386) - 7,236,347 - - - (804,039)

Total comprehensive income/(loss) for the year 44,468,445,892 2,255,353,886 - - - - 46,723,799,778

Balance at 31 December 2014 404,204,260,495 11,881,898,917 448,307,590 - 1,763,625,900 7,040,647 11,391,980 418,316,525,529

Balance at 1 January 2015 404,204,260,495 11,881,898,917 448,307,590 - 1,763,625,900 7,040,647 11,391,980 418,316,525,529

Changes in reserves for the year

Corporate operating budget of:

Employees' Compensation Commission (71,150,494) (71,150,494)

Occupational Safety and Health Center (83,518,400) (83,518,400)

Contribution 93,820,752 6,484,000 100,304,752

Withdrawal (26,870,360) (26,870,360)

Guaranteed income 8,218,450 8,218,450

Management cost of investment (4,538,514) (4,538,514)

Annual incentive benefit (14,090,344) 12,681,310 (1,409,034)

Reclassification of PE-land to investment property 6,863,225 (6,863,225) -

Total comprehensive income/(loss) for the year 40,694,667,040 (24,530,177,237) 1,122,325,680 17,286,815,483

Balance at 31 December 2015 444,737,031,522 (12,648,278,320) 531,619,227 6,484,000 2,879,088,354 7,040,647 11,391,980 435,524,377,411

The notes on pages 9 to 41 form part of these financial statements

Book1 7

SOCIAL SECURITY SYSTEM

(All amounts in Philippine peso unless otherwise stated)

Statement of cash flows

Year ended 31 December

2015 2014

Cash flows from operating activities

Members' contribution 132,615,001,628 120,650,176,296

Investment and other income 24,006,657,657 22,157,725,784

Payments to members and beneficiaries (112,560,881,711) (102,605,612,680)

Payments for operations (8,515,355,684) (8,038,970,506)

Operating income before changes in operating assets and liabilities 35,545,421,890 32,163,318,893

(Increase)/decrease in operating assets

Held-for-trading financial assets (1,867,431,032) 463,458,484

Receivables 1,269,801,216 (1,526,259,637)

Other operating assets (1,864,776,543) 189,054,633

Increase/(decrease) in operating liabilities

Funds held in trust 164,168,822 100,746,300

Other current liabilities (393,749,102) (4,054,619,104)

Net cash generated by operating activities 32,853,435,251 27,335,699,569

Cash flows from investing activities

Loan releases and other investment purchases, net (27,356,719,765) (30,753,904,779)

Acquisition of property and equipment, net (309,599,740) (299,270,675)

Acquisition of intangible assets, net (79,689,038) (20,816,850)

Net cash used in investing activities (27,746,008,544) (31,073,992,304)

Cash flows from financing activities

Corporate operating budget of:

Employees' Compensation Commission (71,150,494) (69,876,100)

Occupational Safety and Health Center (83,518,400) (106,198,152)

Flexi-fund equity

Contribution 93,820,752 77,521,804

Withdrawal (26,870,360) (29,628,291)

Guaranteed income 8,218,450 5,337,786

Management cost of investment (4,538,514) (4,015,106)

Annual incentive benefit (1,409,034) (804,039)

PESO fund equity

Contribution 6,484,000 -

Net cash used in financing activities (78,963,601) (127,662,097)

Net increase/(decrease) in cash and cash equivalents 5,028,463,106 (3,865,954,832)

Cash and cash equivalents at beginning of the year 14,083,905,111 17,949,859,943

Cash and cash equivalents at end of the year 19,112,368,217 14,083,905,111

The notes on pages 9 to 41 form part of these financial statements

Book1 8

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 9

1. REPORTING ENTITY The Social Security System (SSS) administers social security protection to workers in the private sector. Social security provides replacement income for workers in times of death, disability, sickness, maternity and old age. On 1 September 1957, the Social Security Act of 1954 was implemented. Thereafter, the coverage and benefits given by SSS have been expanded and enhanced through the enactment of various laws. On 1 May 1997, Republic Act (RA) No. 8282, otherwise known as the “Social Security Act of 1997”, was enacted to further strengthen the SSS. Under this Act, the government accepts general responsibility for the solvency of the SSS and guarantees that prescribed benefits shall not be diminished. Section 16 of the Social Security Act of 1954 as amended by RA 8282 (SS Law) exempts the SSS and all its benefit payments from all kinds of taxes, fees or charges, customs or import duty. The SSS is a financial institution in the Philippines. Its principal office is in East Avenue, Quezon City. The financial statements include the accounts of Employees’ Compensation and State Insurance Fund, which is being administered by the SSS, as provided for by Presidential Decree No. 626, as amended. All inter-fund accounts have been eliminated. The accompanying financial statements were approved and authorized for issue by the Social Security Commission (SSC) on __________________.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies that have been used in the preparation of these financial statements are summarized below. These policies have been consistently applied to all the years presented, unless otherwise stated. 2.1 Basis of preparation

a. Statement of compliance

The financial statements of the SSS have been prepared in accordance with Philippine Financial Reporting Standards (PFRS), where practicable. PFRS includes all applicable PFRS, Philippine Accounting Standards (PAS) and Philippine Interpretations issued by the Financial Reporting Standards Council (FRSC).

b. Basis of measurement

The financial statements have been prepared on the historical cost basis except for the following items:

financial assets at fair value through profit or loss are measured at fair value

marketable securities classified as available-for-sale are measured at fair value

investment properties are measured at fair value

land under property and equipment are measured at revalued amount

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 10

c. Estimates and judgments

The preparation of the financial statements requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, revenue and expenses. However, uncertainty about these assumptions and estimates could result in outcomes that could require a material adjustment to the carrying amount of the affected asset or liability in the future

Judgments, estimates and assumptions are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

d. Segment reporting

For management purposes, financial statements are prepared based on the funds managed by the Social Security System (SSS) as follows:

Social Security Fund

Under Section 9 of RA No. 8282, coverage in the SSS shall be compulsory upon all private employees not over sixty (60) years of age and their employers, household-helpers earning at least P1,000 a month, and self-employed persons, regardless of trade, business or occupation, with an income of at least P1,000 a month. It also allows voluntary coverage of separated members, overseas Filipino workers (OFWs) and non-working spouses of SSS members. It is mandatory for the covered employees and employers, household helpers and their employers, and self-employed persons to pay their monthly contributions in accordance with the SSS Contribution Schedule and to remit the same to the SSS on the payment deadline applicable. The Social Security program is a defined-benefit program, which simply means that the contribution rate is based on a specified benefit package. The funding method of the SSS uses the Scaled Premium Method; meaning, an earning-related contribution rate is set such that over a certain period of time, the fund is able to cumulate reserves. Under Section 26-B of RA No. 8282, the SSS, as part of its investment operations, acts as insurer of all or part of its interest on SSS properties mortgaged to the SSS, or lives of mortgagors whose properties are mortgaged to the SSS. For this purpose, a separate account known as the “Mortgagors’ Insurance Account” (MIA) was established wherein all amounts received by the SSS in connection with the aforesaid insurance operations are placed in the said account. Under Section 4.a.2 of RA No. 8282, a voluntary provident fund for overseas Filipino workers was authorized. The supplementary benefit program known as the “Flexi-Fund” was established and approved by the Social Security Commission (SSC) under Resolution No. 288 dated 18 April 2001 and by the President of the Philippines on 17 September 2001.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 11

Membership to the Flexi-Fund is on a voluntary basis for those with at least P16,000 monthly earnings either covered under existing program or new entrant with requirement of initial contributions to the SSS program. Voluntary membership starts upon first payment of contribution to the supplementary program. Another voluntary provident fund program is the Personal Equity and Savings Option (PESO) Fund which was established and approved by the SSC on 16 March 2011 under Resolution No. 349-s.2011, and by the President of the Philippines on 06 June 2011. It is offered exclusively to SSS members in addition to the regular SSS program. It aims to provide SSS members the opportunity to receive additional benefits based on their capacity to contribute more. Membership to the PESO Fund is open to all employees, self employed, voluntary and OFW members who have met the following qualifications: (a) below 55 years of age; (b) have paid contributions in the regular SSS program for at least six (6) consecutive months within the 12-month period immediately prior to the month of enrollment; (c) should be paying the maximum amount of contributions under the regular SSS program; and (d) have not filed claim under the regular SSS program. Membership begins with the payment of the first contribution to the PESO Fund. Each member shall be allowed a maximum contribution of P100,000 per annum and a minimum of P1,000 per contribution. A seed capital of P50 million to fund the initial investment activities of the PESO Fund was approved by the SSC under Resolution No. 79 dated 21 January 2015.

Employees’ Compensation and State Insurance Fund

The Employees’ Compensation Commission (ECC), a government corporation, is attached to the Department of Labor and Employment for policy coordination and guidance. It was created in November 01, 1974 by virtue of PD 442 or the Labor Code of the Philippines. It, however, became fully operational with the issuance of PD 626 which took effect January 01, 1975. It is a quasi-judicial corporate entity created to implement the Employees’ Compensation Program (ECP). The ECP provides a package of benefits for public and private sector employees and their dependents in the event of work-connected contingencies such as sickness, injury, disability or death. The State Insurance Fund (SIF) is established to provide funding support to the ECP. It is generated from the employers’ contributions collected by both GSIS and SSS from public and private sector employers, respectively. Coverage in the SIF shall be compulsory upon all employers and their employees not over sixty (60) years of age. Provided, that an employee who is over sixty years of age and paying contributions to qualify for the retirement of life insurance benefit administered by the System shall be subject to compulsory coverage.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 12

2.2 New standards, interpretations and amendments to published standards

a. Effective for reporting periods beginning or after 1 January 2018

a.1 PFRS 9 Financial Instruments PFRS 9 requires an entity to classify financial assets as subsequently measured at either amortised cost or fair value on the basis of both the entity’s business model for managing the financial assets and the contractual cash flow characteristics of the financial asset. A financial asset shall be measured at amortised cost if both of the following conditions are met: (a) The asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows and (b) The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. At initial recognition, an entity may irrevocably designate a financial asset as measured at fair value through profit or loss if doing so eliminates or significantly reduces a measurement or recognition inconsistency (sometimes referred to as an ‘accounting mismatch’) that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases. A financial asset shall be measured at fair value unless it is measured at amortised cost. A gain or loss on a financial asset that is measured at fair value shall be recognized in profit or loss. However, at initial recognition an entity may make an irrevocable election to present in other comprehensive income subsequent changes in the fair value of an investment in an equity instrument that is not held for trading. If an entity makes the election, it shall recognise in profit or loss dividends from that investment when the entity’s right to receive payment of the dividend is established. The SSS is yet to assess PFRS 9’s full impact and it is not practicable to provide a reasonable estimate of the effect until a detailed review has been completed.

2.3 Financial assets

a. Date of recognition

The SSS initially recognizes loans and receivables and deposits on the date that they are originated. All other financial assets are recognized initially on the trade date at which the SSS becomes a party to the contractual provisions of the instrument.

b. Initial recognition

The SSS initially recognizes a financial asset at fair value. Transaction costs are included in the initial measurement, except for financial assets measured at fair value through profit or loss.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 13

c. Determination of fair value

The fair value of investments that are actively traded in organized financial markets is determined by reference to quoted market bid prices. When current bid prices are not available, the price of the most recent transaction provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction.

For investments where there is no active market, fair value is determined using valuation techniques. Such techniques include using recent arm’s-length market transactions, reference to the current market value of another instrument, which is substantially the same, discounted cash flow analysis and option pricing models.

d. Classification

The SSS has the following non-derivative financial assets: financial assets at fair value through profit or loss, held-to-maturity financial assets, loans and receivables and available-for-sale financial assets.

d.1 Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss consist of held-for-trading financial assets. Held-for-trading financial assets are financial assets acquired or held for the purpose of selling in the short term or for which there is a recent pattern of short-term profit taking. Upon initial recognition, attributable transaction costs are recognized in profit or loss as incurred. Financial assets at fair value through profit or loss are measured at fair value and changes therein are recognized in profit or loss.

d.2 Held-to-maturity financial assets

Held-to-maturity financial assets are non-derivative financial assets with fixed or determinable payments and fixed maturity for which there is the positive intention and ability to hold to maturity. They are recognized initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition held-to-maturity investments are measured at amortized cost using the effective interest method, less any impairment in value.

Gains and losses are recognized in profit or loss when the held-to-maturity financial assets are derecognized or impaired, as well as through the amortization process.

d.3 Loans and receivables

Loans and receivables are financial assets with fixed or determinable payments that are not quoted in an active market. Such assets are carried at cost or amortized cost less impairment in value.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 14

A loan or receivable is deemed impaired when it is considered that it will probably not be possible to recover all the amounts due according to the contractual terms, or equivalent value. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy and default or delinquency in payments are considered indicators that such loans and receivables are impaired.

d.4 Available-for-sale financial assets

Available-for-sale financial assets are non-derivative financial assets that are designated as available-for-sale and that are not classified in any of the other categories. Subsequent to initial recognition, available-for-sale financial assets are carried at fair value in the statement of financial position. Changes in the fair value of such assets are recognized in other comprehensive income and presented within reserves in the unrealized gain or loss on available-for-sale financial assets portion. When an available-for-sale financial asset is derecognized, the cumulative gains or losses are transferred to profit or loss and presented as a reclassification adjustment within the statement of comprehensive income. Dividends on available-for-sale equity instruments are recognized in profit or loss when the right to receive payments is established. If an available-for-sale financial asset is impaired, an amount comprising the difference between its cost (net of any principal payment and amortization) and its current fair value, less any impairment loss previously recognized in profit or loss, is transferred from reserves to profit or loss and presented as a reclassification adjustment within the statement of comprehensive income. Reversals in respect of equity instruments classified as available-for-sale are not recognized in profit or loss.

e. Derecognition of financial assets

Financial assets are derecognized when the rights to receive cash flows from the asset have expired or have been transferred and the SSS either has transferred substantially all risks and rewards of ownership or has neither transferred nor retained substantially all the risks and rewards of ownership, but has transferred control of the asset.

f. Derivative financial instrument

The SSS enters into a derivative financial instrument to manage its exposure to foreign exchange risk. Derivatives are initially recognized at fair value at the date the derivative contract is entered into and is subsequently remeasured to their fair value at the end of each reporting period.

2.4 Cash equivalents

Cash equivalents comprise short-term, highly liquid investments that are readily convertible to known amounts of cash with original maturities of 90 days or less and are subject to an insignificant risk of change in value.

2.5 Supplies and materials

Supplies and materials are valued at cost using the weighted average cost method.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 15

2.6 Investment property

Investment property account consists of property held to earn rentals and/or for capital appreciation.

An investment property is initially measured at cost, including transaction costs. Such cost should not include start-up costs, abnormal waste, or initial operating losses incurred before the investment property achieves the planned level of occupancy. After initial recognition, it is measured at fair value with any change therein recognized in profit or loss.

Transfers to or from investment property are made when there is a change in use, evidenced by:

commencement of owner-occupation

end of owner-occupation

commencement of an operating lease to another party

2.7 Property and equipment

Property and equipment, except land, are stated at cost less accumulated depreciation, amortization and any impairment in value. Land is carried at revalued amount. Increase in value as a result of revaluation is credited to reserves under property valuation reserve unless it represents the reversal of a revaluation decrease of the same asset previously recognized as an expense, in which case it is recognized as income. On the other hand, a decrease arising as a result of a revaluation is recognized as an expense to the extent that it exceeds any amount previously credited to property valuation reserve relating to the same asset. Cost includes all costs necessary to bring the asset to working condition for its intended use. This would include not only its original purchase price but also costs of site preparation, delivery and handling, installation, related professional fees for architects and engineers, and the estimated cost of dismantling and removing the asset and restoring the site.

The cost of replacing a part of an item of property and equipment is recognized in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the SSS, and its cost can be measured reliably. The carrying amount of the replaced part is derecognized. The costs of the day-to-day servicing of property and equipment are recognized in profit or loss as incurred. Depreciation is calculated over the depreciable amount less its residual value. It is recognized in profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property and equipment. The estimated useful lives of property and equipment are as follows:

Building/building improvements 10-30 years Furniture and equipment/computer hardware 5-10 years Land improvements 10 years Transportation equipment 7 years Leasehold improvements 10-30 years or the term of lease

whichever is shorter

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 16

Property and equipment except land have residual value equivalent to 10 per cent of the acquisition/appraised value.

Construction in progress (CIP) represents building and building/leasehold improvements under construction and is stated at cost. CIP is not depreciated until such time the relevant assets are completed and put into operational use.

2.8 Intangible assets

Acquired computer software/licenses are capitalized on the basis of the costs incurred to acquire and bring to use the specific software. Computer software/licenses with finite lives are amortized on a straight-line basis over their estimated useful lives, while those with indefinite useful lives or those used perpetually or for as long as there are computers compatible with them are carried at cost and tested annually for impairment.

2.9 Non-current assets held for sale

Non-current assets are classified as held for sale if their carrying amount will be recovered through a sale transaction rather than through continuing use. This condition is regarded as met when the sale is highly probable and the asset is available for immediate sale in its present condition.

Assets classified as held for sale are measured at the lower of carrying amount and fair value less costs to sell. Any excess of carrying amount over fair value less costs to sell is an impairment loss. No depreciation is recognized for these assets while classified as held for sale. Non-current assets held for sale include real and other properties acquired (ROPA) in settlement of contribution and member/housing/other loan delinquencies through foreclosure or dation in payment. They are initially booked at the carrying amount of the contribution/loan delinquency plus transaction costs incurred upon acquisition. When the booked amount of ROPA exceeds the appraised value of the acquired property, an allowance for impairment loss equivalent to the excess of the amount booked over the appraised value is set up.

2.10 Impairment of non-financial assets

The carrying amount of non-financial assets, other than investment property and non-current assets held for sale is assessed to determine whether there is any indication of impairment or an impairment previously recognized may no longer exist or may have decreased. If any such indication exists, then the asset’s recoverable amount is estimated. Recoverable amount is the higher of an asset's fair value less costs to sell and its value in use.

Impairment loss is recognized if the carrying amount of an asset exceeds its estimated recoverable amount. The carrying amount of the asset is reduced through the use of an allowance account and the amount of loss is recognized in profit or loss unless it relates to a revalued asset where the value changes are recognized in other comprehensive income/loss and presented within reserves in the property valuation reserve portion. Depreciation and amortization charge for future periods is adjusted.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 17

An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized in prior years.

2.11 Revenue recognition

Revenue is recognized to the extent that it is probable that the economic benefits will flow to the SSS and the amount of revenue can be reliably measured. The following specific recognition criteria must also be met before revenue is recognized:

a. Member’s contribution

Revenue is recognized upon collection.

b. Interest income

Revenue is recognized as the interest accrues, taking into account the effective yield on the asset. Excluded are interest income from member and housing loans which are recognized upon collection.

c. Dividend income

Dividend income is recognized at the time the right to receive the payment is established.

d. Rental income

Rental income is recognized on a straight-line basis over the lease term. 2.12 Expense recognition

Expenses are recognized in the statement of comprehensive income upon utilization of the service or at the date they are incurred.

2.13 Operating Leases

The determination of whether an arrangement is, or contains a lease is based on the substance of the arrangement at inception date of whether the fulfillment of the arrangement is dependent on the use of a specific asset or assets and the arrangement conveys a right to use the asset.

a. SSS as lessee

Leases which do not transfer to the SSS substantially all the risks and benefits of ownership of the asset are classified as operating leases. Operating lease payments are recognized as expense on a straight-line basis over the lease term.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 18

b. SSS as lessor

Leases where the SSS does not transfer to the lessee substantially all the risk and benefits of ownership of the asset are classified as operating leases. Lease income from operating leases is recognized as income on a straight-line basis over the lease term.

3. SEGMENT INFORMATION

The table below shows the Statement of Financial Position of all the funds as at 31 December 2015.

SSS EC-SIF Total

Assets

Investments 378,064,120,818 28,092,691,826 406,156,812,644

Cash and cash equivalent 14,386,598,574 4,725,769,643 19,112,368,217

Receivables 7,365,149,746 298,272,801 7,663,422,547

Property and equipment 4,556,165,385 - 4,556,165,385

Others 6,903,133,660 7,391,998 6,910,525,658

Total Assets 411,275,168,183 33,124,126,268 444,399,294,451

Liabilities 8,663,098,455 211,818,585 8,874,917,040

Reserves 402,612,069,728 32,912,307,683 435,524,377,411

Total Liabilities & Reserves 411,275,168,183 33,124,126,268 444,399,294,451

The table below shows the Statement of Comprehensive Income for all the funds for the year ended 31 December 2015.

SSS EC-SIF Total

Revenues

Members' contribution 130,786,300,137 1,828,701,491 132,615,001,628

Investment and other income 28,459,868,383 1,026,998,283 29,486,866,666

159,246,168,520 2,855,699,774 162,101,868,294

Expenditures

Benefit payments 111,489,161,124 1,071,659,324 112,560,820,448

Operating expenses 8,762,340,188 84,040,618 8,846,380,806

120,251,501,312 1,155,699,942 121,407,201,254

Profit for the year 38,994,667,208 1,699,999,832 40,694,667,040

Other comprehensive income/(loss)

Net unrealized gain/(loss) on AFSFA (24,482,724,968) (47,452,269) (24,530,177,237)

Net gain on revaluation of land 1,122,325,680 - 1,122,325,680

(23,360,399,288) (47,452,269) (23,407,851,557)

Total comprehensive income 15,634,267,920 1,652,547,563 17,286,815,483

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 19

4. CASH AND CASH EQUIVALENTS

2015 2014

Cash on hand and in banks 4,856,248,305 4,012,866,416

Term deposits 14,256,119,912 10,071,038,695

19,112,368,217 14,083,905,111

Cash in banks earn interest at the respective bank deposit rates. Time and special savings deposits are made for varying periods of up to 90 days depending on the immediate cash requirements of SSS and earn interest at the prevailing time and special savings deposit rates. In consideration of the banks’ making their deposit pick up facility available to the SSS, the latter agreed to maintain an average daily balance of P1 million in a non-drawing interest bearing current account/savings account (CASA) with each of the banks’ servicing branches. As of 31 December 2015, P95 million is being maintained in several banks for such purpose. Interest income earned from cash in banks and term deposits amounted to P291.84 million and P233.12 million as at 31 December 2015 and 2014, respectively (see Note 24).

5. HELD-TO-MATURITY INVESTMENTS

2015 2014

Short-term money placements 4,812,861,865 7,168,909,303

Government bonds 15,645,200,000 8,765,000,000

Corporate notes 2,989,460,177 700,000,000

Corporate bonds - 500,000,000

23,447,522,042 17,133,909,303

Short-term money placements are short-term investments with original maturities of more than 90 days. Interest income earned recorded under current investment income - held to maturity (see Note 24) as at 31 December 2015 and 2014 amounted to P349.03 million and P159.45 million, respectively.

6. HELD-FOR-TRADING FINANCIAL ASSETS The cost of held-for-trading financial assets as at 31 December 2015 and 31 December 2014 are P4,336.94 million and P2,446.40. million, respectively.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 20

7. LOANS AND RECEIVABLE

2015 2014

Loan to National Home Mortgage Finance Corporation 457,526,254 481,114,295

Commercial and industrial loans 60,861,093 189,096,497

Loan to other government agencies - UP-PGH 22,334,251 21,850,812

Sales contract receivable - investment property 8,060,776 6,116,204

548,782,374 698,177,808

8. OTHER RECEIVABLES

2015 2014

Collecting banks/agents/bayad center 3,684,297,011 4,945,953,675

Interest receivable 3,359,823,217 3,430,217,011

Other receivables 619,302,320 1,801,939,449

7,663,422,548 10,178,110,135

9. OTHER CURRENT ASSETS

2015 2014

Supplies and materials inventory 286,341,614 147,181,971

Prepaid expenses 12,466,871 16,536,839

Revolving fund 1,499,947 1,160,758

Advances-officials and employees 167,888 435,279

300,476,320 165,314,847

Supplies and materials used for consumption as at 31 December 2015 and 2014 amounted to P170.86 million and P113.91 million, respectively (see Note 26). Obsolete inventory for employer (ER) registration plates and stickers amounting P7.82 million was writen-off in December 2015.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 21

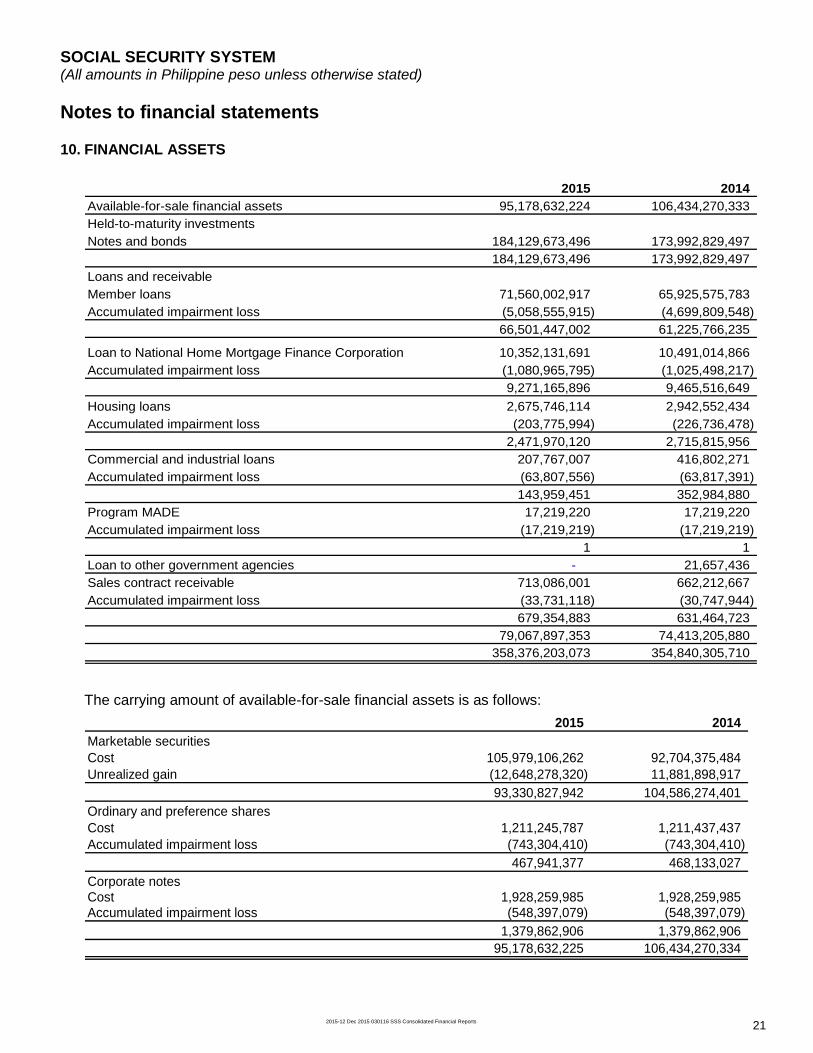

10. FINANCIAL ASSETS

2015 2014

Available-for-sale financial assets 95,178,632,224 106,434,270,333

Held-to-maturity investments

Notes and bonds 184,129,673,496 173,992,829,497

184,129,673,496 173,992,829,497

Loans and receivable

Member loans 71,560,002,917 65,925,575,783

Accumulated impairment loss (5,058,555,915) (4,699,809,548)

66,501,447,002 61,225,766,235

Loan to National Home Mortgage Finance Corporation 10,352,131,691 10,491,014,866

Accumulated impairment loss (1,080,965,795) (1,025,498,217)

9,271,165,896 9,465,516,649

Housing loans 2,675,746,114 2,942,552,434

Accumulated impairment loss (203,775,994) (226,736,478)

2,471,970,120 2,715,815,956

Commercial and industrial loans 207,767,007 416,802,271

Accumulated impairment loss (63,807,556) (63,817,391)

143,959,451 352,984,880

Program MADE 17,219,220 17,219,220

Accumulated impairment loss (17,219,219) (17,219,219)

1 1

Loan to other government agencies - 21,657,436

Sales contract receivable 713,086,001 662,212,667

Accumulated impairment loss (33,731,118) (30,747,944)

679,354,883 631,464,723

79,067,897,353 74,413,205,880

358,376,203,073 354,840,305,710

The carrying amount of available-for-sale financial assets is as follows:

2015 2014

Marketable securities

Cost 105,979,106,262 92,704,375,484

Unrealized gain (12,648,278,320) 11,881,898,917

93,330,827,942 104,586,274,401

Ordinary and preference shares

Cost 1,211,245,787 1,211,437,437

Accumulated impairment loss (743,304,410) (743,304,410)

467,941,377 468,133,027

Corporate notesCost 1,928,259,985 1,928,259,985 Accumulated impairment loss (548,397,079) (548,397,079)

1,379,862,906 1,379,862,906

95,178,632,225 106,434,270,334

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 22

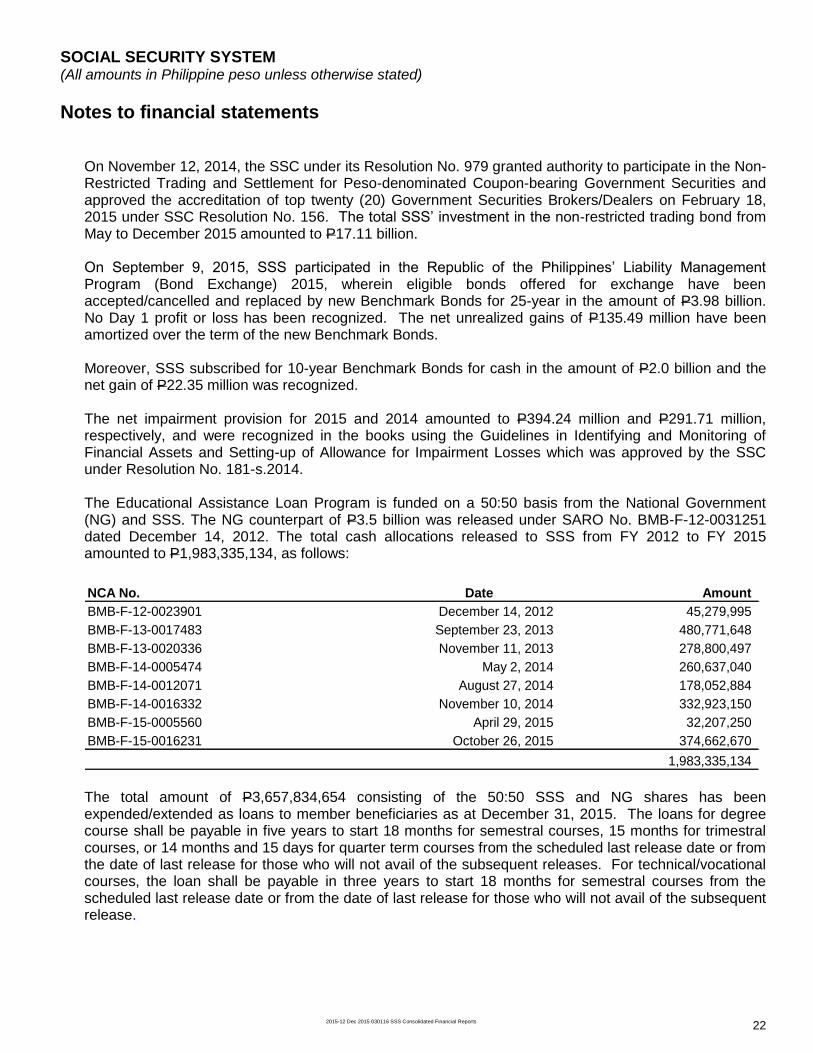

On November 12, 2014, the SSC under its Resolution No. 979 granted authority to participate in the Non-Restricted Trading and Settlement for Peso-denominated Coupon-bearing Government Securities and approved the accreditation of top twenty (20) Government Securities Brokers/Dealers on February 18, 2015 under SSC Resolution No. 156. The total SSS’ investment in the non-restricted trading bond from May to December 2015 amounted to P17.11 billion. On September 9, 2015, SSS participated in the Republic of the Philippines’ Liability Management Program (Bond Exchange) 2015, wherein eligible bonds offered for exchange have been accepted/cancelled and replaced by new Benchmark Bonds for 25-year in the amount of P3.98 billion. No Day 1 profit or loss has been recognized. The net unrealized gains of P135.49 million have been amortized over the term of the new Benchmark Bonds. Moreover, SSS subscribed for 10-year Benchmark Bonds for cash in the amount of P2.0 billion and the net gain of P22.35 million was recognized. The net impairment provision for 2015 and 2014 amounted to P394.24 million and P291.71 million, respectively, and were recognized in the books using the Guidelines in Identifying and Monitoring of Financial Assets and Setting-up of Allowance for Impairment Losses which was approved by the SSC under Resolution No. 181-s.2014. The Educational Assistance Loan Program is funded on a 50:50 basis from the National Government (NG) and SSS. The NG counterpart of P3.5 billion was released under SARO No. BMB-F-12-0031251 dated December 14, 2012. The total cash allocations released to SSS from FY 2012 to FY 2015 amounted to P1,983,335,134, as follows:

NCA No. Date Amount

BMB-F-12-0023901 December 14, 2012 45,279,995

BMB-F-13-0017483 September 23, 2013 480,771,648

BMB-F-13-0020336 November 11, 2013 278,800,497

BMB-F-14-0005474 May 2, 2014 260,637,040

BMB-F-14-0012071 August 27, 2014 178,052,884

BMB-F-14-0016332 November 10, 2014 332,923,150

BMB-F-15-0005560 April 29, 2015 32,207,250

BMB-F-15-0016231 October 26, 2015 374,662,670

1,983,335,134 The total amount of P3,657,834,654 consisting of the 50:50 SSS and NG shares has been expended/extended as loans to member beneficiaries as at December 31, 2015. The loans for degree course shall be payable in five years to start 18 months for semestral courses, 15 months for trimestral courses, or 14 months and 15 days for quarter term courses from the scheduled last release date or from the date of last release for those who will not avail of the subsequent releases. For technical/vocational courses, the loan shall be payable in three years to start 18 months for semestral courses from the scheduled last release date or from the date of last release for those who will not avail of the subsequent release.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 23

11. INVESTMENT PROPERTY

Land Building

Development

Cost Total

Fair value, 1 January 2015 13,940,407,657 4,006,023,775 9,685,838 17,956,117,270

Adjustements - 2,315,329 - 2,315,329

Disposals - (1,000,000) - (1,000,000)

Fair value gain/(loss) 1,536,767,519 (5,262,409) 1,531,505,110

Fair value, 31 December 2015 15,477,175,176 4,002,076,695 9,685,838 19,488,937,709

Fair value, 31 December 2014 13,940,407,657 4,006,023,775 9,685,838 17,956,117,270

The cost of investment property as at 31 December 2015 and 2014 remains at P7.55 billion. The fair value of investment property is determined based on valuations performed by independent appraisers. The following amounts are recognized in the statement of profit or loss and other comprehensive income:

2015 2014

Rental income 507,811,127 463,041,527

Penalty on rentals 1,282,336 2,797,268

Gain/(loss) on fair value adjustment 1,531,505,110 889,650,789

Gain/(loss) on sale/disposal 72,000 (446,820)

Direct operating expenses (83,892,499) (82,730,037)

1,956,778,074 1,272,312,727

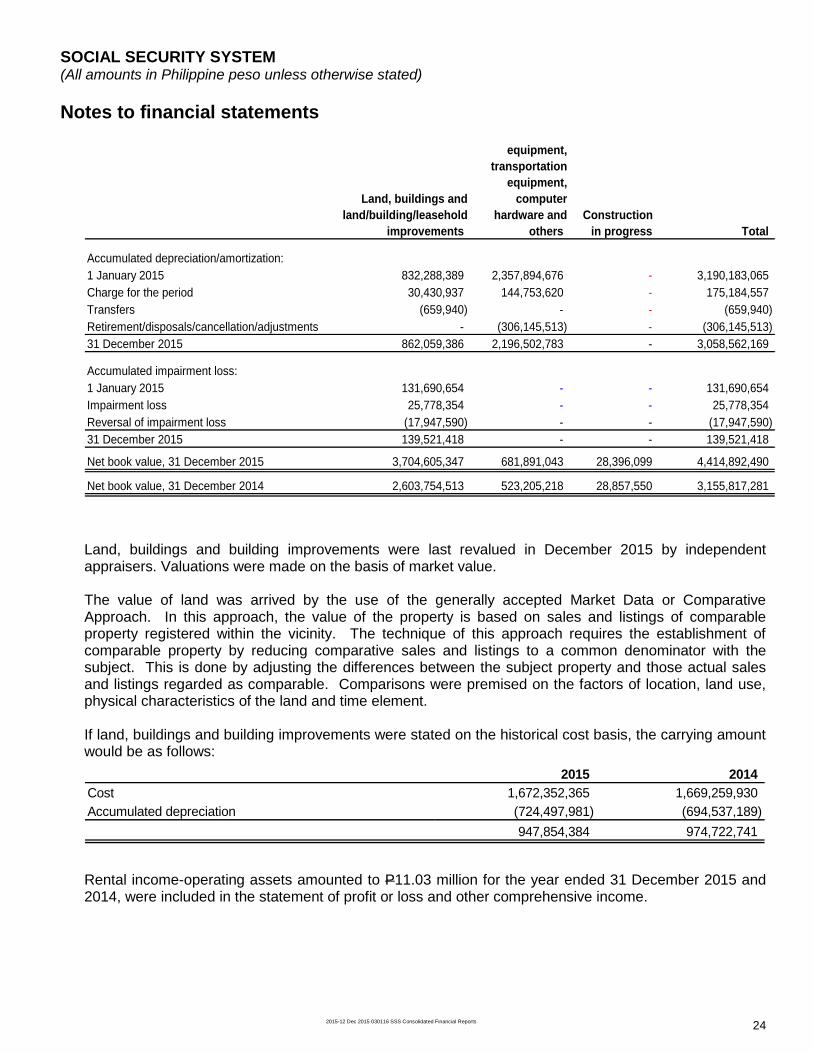

12. PROPERTY AND EQUIPMENT

Furniture and

equipment,

transportation

equipment,

Land, buildings and computer

land/building/leasehold hardware and Construction

improvements others in progress Total

Gross carrying amount:

1 January 2015 3,567,733,556 2,881,099,894 28,857,550 6,477,691,000

Additions - 306,179,823 4,458,870 310,638,693

Transfers 2,887,595 - (4,920,321) (2,032,726)

Net revaluation increase/(decrease) 1,135,565,000 - - 1,135,565,000

Retirement/disposals/cancellation/adjustments - (308,885,891) - (308,885,891)

31 December 2015 4,706,186,151 2,878,393,826 28,396,099 7,612,976,076

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 24

equipment,

transportation

equipment,

Land, buildings and computer

land/building/leasehold hardware and Construction

improvements others in progress Total

Accumulated depreciation/amortization:

1 January 2015 832,288,389 2,357,894,676 - 3,190,183,065

Charge for the period 30,430,937 144,753,620 - 175,184,557

Transfers (659,940) - - (659,940)

Retirement/disposals/cancellation/adjustments - (306,145,513) - (306,145,513)

31 December 2015 862,059,386 2,196,502,783 - 3,058,562,169

Accumulated impairment loss:

1 January 2015 131,690,654 - - 131,690,654

Impairment loss 25,778,354 - - 25,778,354

Reversal of impairment loss (17,947,590) - - (17,947,590)

31 December 2015 139,521,418 - - 139,521,418

Net book value, 31 December 2015 3,704,605,347 681,891,043 28,396,099 4,414,892,490

Net book value, 31 December 2014 2,603,754,513 523,205,218 28,857,550 3,155,817,281

Land, buildings and building improvements were last revalued in December 2015 by independent appraisers. Valuations were made on the basis of market value. The value of land was arrived by the use of the generally accepted Market Data or Comparative Approach. In this approach, the value of the property is based on sales and listings of comparable property registered within the vicinity. The technique of this approach requires the establishment of comparable property by reducing comparative sales and listings to a common denominator with the subject. This is done by adjusting the differences between the subject property and those actual sales and listings regarded as comparable. Comparisons were premised on the factors of location, land use, physical characteristics of the land and time element. If land, buildings and building improvements were stated on the historical cost basis, the carrying amount would be as follows:

2015 2014

Cost 1,672,352,365 1,669,259,930

Accumulated depreciation (724,497,981) (694,537,189)

947,854,384 974,722,741

Rental income-operating assets amounted to P11.03 million for the year ended 31 December 2015 and 2014, were included in the statement of profit or loss and other comprehensive income.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 25

13. INTANGIBLE ASSETS

2015 2014

Cost

Balance at the beginning of the year 534,246,358 513,429,508

Additions 79,837,753 20,816,850

Transfers - -

Retirement/disposals/cancellation (20,652,225) -

Balance at end of year 593,431,886 534,246,358

Accumulated amortizationBalance at the beginning of the year 330,970,690 281,961,267 Amortization charge for the year 46,258,115 49,009,423

Transfers - -

Retirement/disposals/cancellation (898,042) -

Balance at end of year 376,330,763 330,970,690

Accumulated impairment loss

Balance at the beginning of the year 75,828,227 75,828,227

Retirement/disposals/cancellation - -

Balance at end of year 75,828,227 75,828,227

Net book value 141,272,896 127,447,441

The carrying amount of intangible assets with indefinite lives as at 31 December 2015 amounted to P60.70 million.

14. NON-CURRENT ASSETS HELD FOR SALE

Acquired asset/

Land Building reqistered Total

Carrying amount, 1 January 2015 3,771,824,760 164,816,285 404,033,116 4,340,674,161

Accumulated impairment loss (2,475,762) (2,744,503) (4,118,055) (9,338,320)

Net carrying amount, 1 January 2015 3,769,348,998 162,071,782 399,915,061 4,331,335,841

Additions - - 207,025,522 207,025,522

Transfer/Adjsustments 1,386,810 (30,510) - 1,356,300

Disposals (3,243,690) - (144,557,916) (147,801,606)

Impairment (loss)/reversal (426,786) (567,444) (4,724,745) (5,718,975)

Fair value, 31 December 2015 3,767,065,332 161,473,828 457,657,922 4,386,197,082

Fair value, 31 December 2014 3,769,348,998 162,071,782 399,915,062 4,331,335,842

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 26

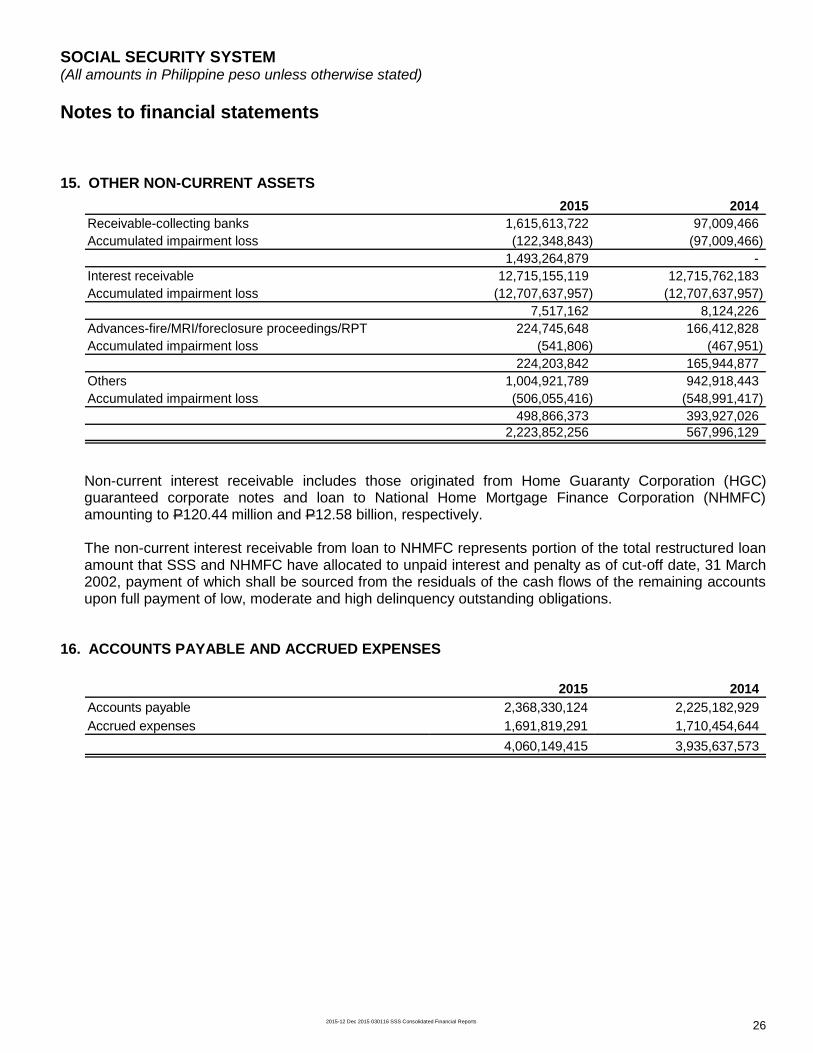

15. OTHER NON-CURRENT ASSETS

2015 2014

Receivable-collecting banks 1,615,613,722 97,009,466

Accumulated impairment loss (122,348,843) (97,009,466)

1,493,264,879 -

Interest receivable 12,715,155,119 12,715,762,183

Accumulated impairment loss (12,707,637,957) (12,707,637,957)

7,517,162 8,124,226

Advances-fire/MRI/foreclosure proceedings/RPT 224,745,648 166,412,828

Accumulated impairment loss (541,806) (467,951)

224,203,842 165,944,877

Others 1,004,921,789 942,918,443

Accumulated impairment loss (506,055,416) (548,991,417)

498,866,373 393,927,026

2,223,852,256 567,996,129

Non-current interest receivable includes those originated from Home Guaranty Corporation (HGC) guaranteed corporate notes and loan to National Home Mortgage Finance Corporation (NHMFC) amounting to P120.44 million and P12.58 billion, respectively.

The non-current interest receivable from loan to NHMFC represents portion of the total restructured loan amount that SSS and NHMFC have allocated to unpaid interest and penalty as of cut-off date, 31 March 2002, payment of which shall be sourced from the residuals of the cash flows of the remaining accounts upon full payment of low, moderate and high delinquency outstanding obligations.

16. ACCOUNTS PAYABLE AND ACCRUED EXPENSES

2015 2014

Accounts payable 2,368,330,124 2,225,182,929

Accrued expenses 1,691,819,291 1,710,454,644

4,060,149,415 3,935,637,573

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 27

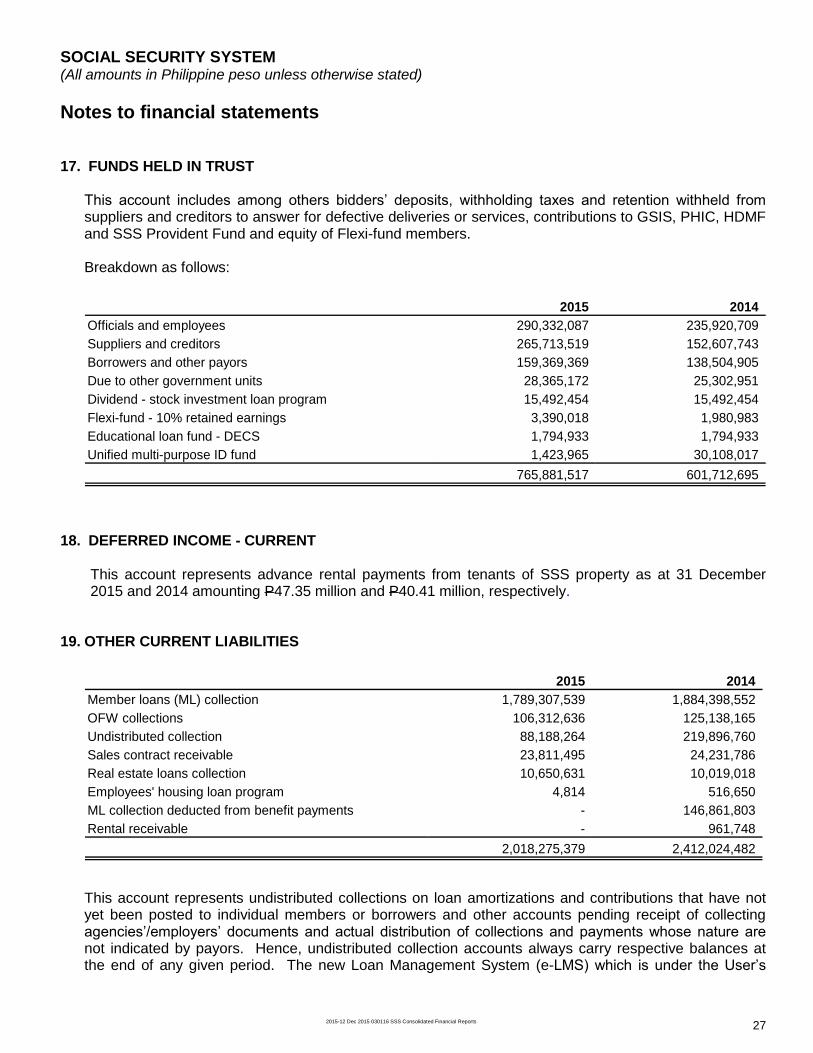

17. FUNDS HELD IN TRUST

This account includes among others bidders’ deposits, withholding taxes and retention withheld from suppliers and creditors to answer for defective deliveries or services, contributions to GSIS, PHIC, HDMF and SSS Provident Fund and equity of Flexi-fund members. Breakdown as follows:

2015 2014

Officials and employees 290,332,087 235,920,709

Suppliers and creditors 265,713,519 152,607,743

Borrowers and other payors 159,369,369 138,504,905

Due to other government units 28,365,172 25,302,951

Dividend - stock investment loan program 15,492,454 15,492,454

Flexi-fund - 10% retained earnings 3,390,018 1,980,983

Educational loan fund - DECS 1,794,933 1,794,933

Unified multi-purpose ID fund 1,423,965 30,108,017

765,881,517 601,712,695

18. DEFERRED INCOME - CURRENT

This account represents advance rental payments from tenants of SSS property as at 31 December 2015 and 2014 amounting P47.35 million and P40.41 million, respectively.

19. OTHER CURRENT LIABILITIES

2015 2014

Member loans (ML) collection 1,789,307,539 1,884,398,552

OFW collections 106,312,636 125,138,165

Undistributed collection 88,188,264 219,896,760

Sales contract receivable 23,811,495 24,231,786

Real estate loans collection 10,650,631 10,019,018

Employees' housing loan program 4,814 516,650

ML collection deducted from benefit payments - 146,861,803

Rental receivable - 961,748

2,018,275,379 2,412,024,482

This account represents undistributed collections on loan amortizations and contributions that have not yet been posted to individual members or borrowers and other accounts pending receipt of collecting agencies’/employers’ documents and actual distribution of collections and payments whose nature are not indicated by payors. Hence, undistributed collection accounts always carry respective balances at the end of any given period. The new Loan Management System (e-LMS) which is under the User’s

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 28

Acceptance Testing, will fully automate the process of Loans Granting, Billing and Collection. This will also facilitate posting to ensure that borrowers’ accounts reflect the correct loan balances, including the corresponding charge, such as interest and penalties

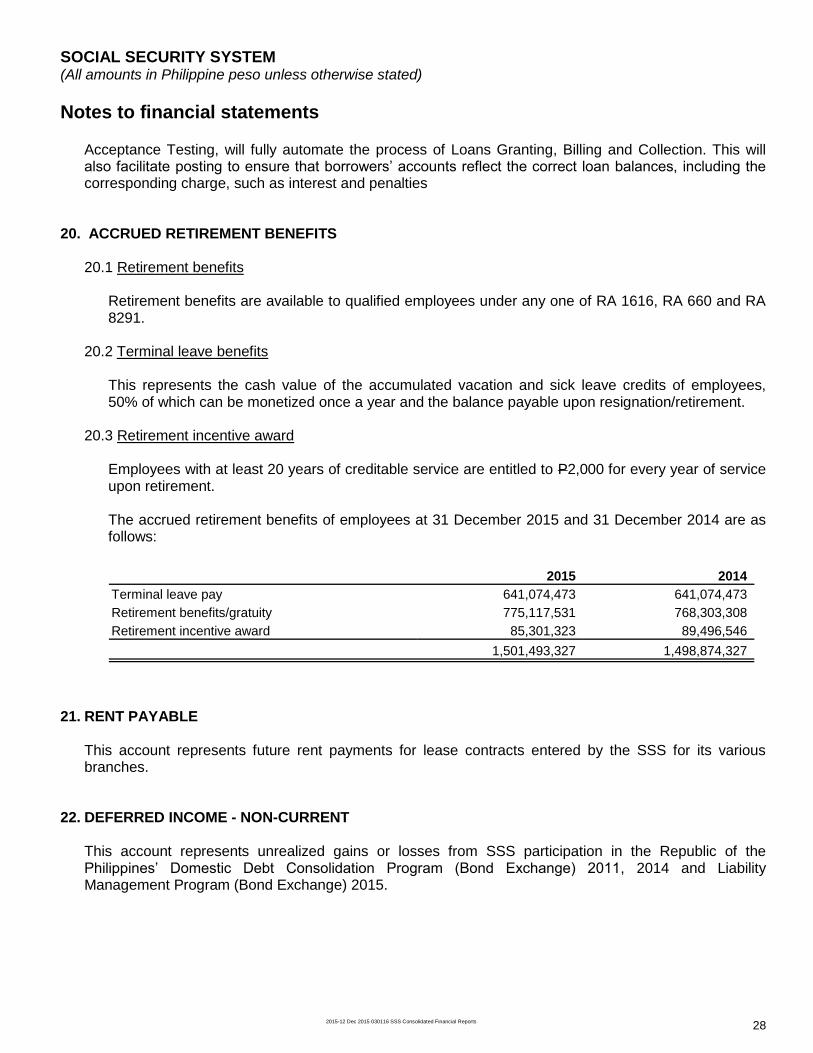

20. ACCRUED RETIREMENT BENEFITS

20.1 Retirement benefits Retirement benefits are available to qualified employees under any one of RA 1616, RA 660 and RA 8291.

20.2 Terminal leave benefits This represents the cash value of the accumulated vacation and sick leave credits of employees, 50% of which can be monetized once a year and the balance payable upon resignation/retirement.

20.3 Retirement incentive award

Employees with at least 20 years of creditable service are entitled to P2,000 for every year of service upon retirement. The accrued retirement benefits of employees at 31 December 2015 and 31 December 2014 are as follows:

2015 2014

Terminal leave pay 641,074,473 641,074,473

Retirement benefits/gratuity 775,117,531 768,303,308

Retirement incentive award 85,301,323 89,496,546

1,501,493,327 1,498,874,327

21. RENT PAYABLE

This account represents future rent payments for lease contracts entered by the SSS for its various branches.

22. DEFERRED INCOME - NON-CURRENT

This account represents unrealized gains or losses from SSS participation in the Republic of the Philippines’ Domestic Debt Consolidation Program (Bond Exchange) 2011, 2014 and Liability Management Program (Bond Exchange) 2015.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 29

23. RESERVES

23.1 Investment reserve fund (IRF) All revenues of the SSS that are not needed to meet the current administrative and operational expenses are accumulated in the reserve fund. Such portion of the reserve fund as are not needed to meet the current benefit obligations is known as the IRF which the SSC manages and invests with the skill, care, prudence and diligence necessary under the circumstances then prevailing that a prudent man acting in like capacity and familiar with such matters would exercise in the conduct of an enterprise of a like character and with similar aims, subject to prescribed ceilings under Section 26 of the SS Law. No portion of the IRF or income thereof shall accrue to the general fund of the National Government or to any of its agencies or instrumentalities, including government-owned or controlled corporations, except as may be allowed under the SS Law. It also provides that no portion of the IRF shall be invested for any purpose or in any instrument, institution or industry over and above the prescribed cumulative ceilings as follows: 40% in private securities, 35% in housing, 30% in real estate related investments, 10% in short and medium-term member loans, 30% in government financial institutions and corporations, 30% in infrastructure projects, 15% in any particular industry and 7.5% in foreign-currency denominated investments. In its Resolution No. 402 s. 2007, the SSC, adopted the use of acquisition cost of shares of stock as the basis for computing the 30% limit in equity investments, based on the opinion dated 25 June 2007 of the Legal and Adjudication Sector of COA.

23.2 Actuarial valuation of the reserve fund of the SSS The SS Law requires the Actuary of the System to submit a valuation report every four years, or more frequently as may be necessary, to determine the actuarial soundness of the reserve fund of the SSS and to recommend measures on how to improve its viability. The reserve fund is affected by (a) changes in demographic factors (such as increased life expectancy, ageing of population, declining fertility level and delay in retirement) and (b) the economic conditions of the country. Economic factors on which assumptions are made include interest rates, inflation rates and salary wage increases. With these and other assumptions, and taking into account the uncertainty of future events, the life of the fund is projected. In the 1999 Actuarial Valuation, the Social Security Fund (SSF) was projected to last only until 2015. Since then, parametric measures (e.g. increases in the contribution rate from 8.4% to 9.4% in March 2003, increase in the maximum salary base for contributions from P12,000 to P15,000 and the redefinition of Credited Years of Service) and operational developments (e.g. Tellering System, more accounts officers, cost saving measures, improved investment portfolio and management, etc.) were implemented to strengthen the SSF. The System’s concerted efforts have resulted in improved actuarial soundness. Results of the 2003 Actuarial Valuation indicate an extension on the life of the fund by sixteen years, from 2015 to 2031.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 30

An update of the 2003 Actuarial Valuation was later undertaken, to include the effect of the increase in the contribution rate to 10.4% effective January 2007, and the grant of 10% across-the-board increases in pension effective September 2006 and September 2007. This update showed that the actuarial life of the SSF has extended further to 2036. The 2007 Actuarial Valuation was later conducted, which projected the fund lasting until 2039. The SSF life extended further to 2043 in the conduct of 2011 Actuarial Valuation, which considered the Reform Agenda items implemented on January 1, 2014, particularly the increase in contribution rate to 11%, and the increase in Monthly Salary Credit (MSC) ceiling to P16,000. The 2011 Actuarial Valuation was then updated to consider the 5% across-the-board pension increase implemented in June 2014. This update showed a reduction of the fund life by one year to 2042. The summary of results of the 2011 Valuation, as well as the original 2007 Valuation results, are presented in the table below. There are two columns under 2011 Valuation: (1) the original results as published in the 2011 Actuarial Valuation report; and (2) the updated results that take into consideration the 5% across-the board pension increase.

Actuarial Valuation Comparison of Key Projection Results 2011 Valuation versus 2007 Valuation

Under the Baseline Scenario

Key Projection Results 2007 Valuation

2011 Valuation

Original * Updated **

No future Across-the-Board Increase in Pensions

Year Fund Will Last 2039 2043 2042

Year Net Revenue Becomes Negative

2030 2035 2034

* As published in the 2011 Actuarial Valuation report ** Updated results upon considering the effect of the 5% across-the-board pension increase effective June 2014

Both original and updated 2011 Valuation results show an improvement of the fund life by four and three years, respectively, when compared to the original 2007 Valuation results. Despite these improvements, the SSS, like most defined-benefit social security schemes, is faced with the reality of a less-than-ideal actuarial fund life, and a considerable level of unfunded liabilities (UL). The unfunded liability arises when the liability, or the difference between the present value of future benefits and operating expenses, present value of future contributions, less reserve fund, is positive. From the 2007 Valuation results, the unfunded liability was valued at P748.99 billion, which has then increased to P1.19 trillion based on the original 2011 Valuation results, and further increased to P1.22 trillion based on the updated 2011 Valuation results.

This current UL and fund life situation was caused in part by a structural imbalance, brought about by the mismatch of the increases in pension relative to the monthly salary credit (MSC) ceiling and contribution rate. While pensions were increased 22 times since 1980 through across-the-board pension increases of up to 20% and increases in the minimum pension amount through Republic Act No. 8282, and the MSC ceiling was increased 12 times, the contribution rate, on the other hand, was only increased three times during the same period, from 8.4% to 9.4% in 2003, then to 10.4% in 2007, and finally to 11% in 2014.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 31

The effect of demographic change on the fund should also be recognized, as there may not be enough contributors remitting to pay all the expenses and benefits of the growing number of pensioners due to declining population growth rate and lengthening life spans.

To address these and other issues on the viability of the reserve fund, actuarial valuations and other studies are continuously conducted, which shall be the basis of recommendations for policy reforms. The recommendations mentioned in the valuations include, but not limited to, raising the contribution rate, raising the maximum monthly salary credit (MSC), initially raising the required contributing years to be entitled to retirement pension to 15 years, and raising the retirement age. Further reform packages and other measures shall be formulated which simultaneously address the interest of the stakeholders of SSS: benefit adequacy for current pensioners, and financial sustainability for future pensioners, who are now active contributors of the SSS.

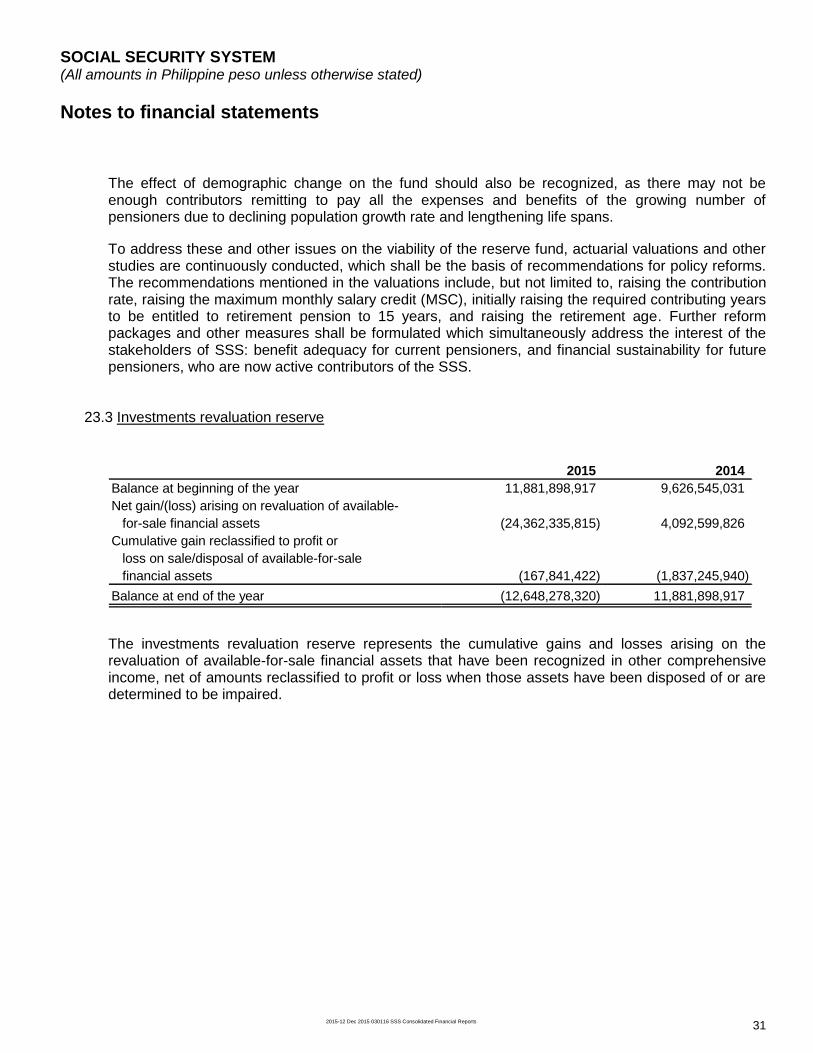

23.3 Investments revaluation reserve

2015 2014

Balance at beginning of the year 11,881,898,917 9,626,545,031

Net gain/(loss) arising on revaluation of available-

for-sale financial assets (24,362,335,815) 4,092,599,826

Cumulative gain reclassified to profit or

loss on sale/disposal of available-for-sale

financial assets (167,841,422) (1,837,245,940)

Balance at end of the year (12,648,278,320) 11,881,898,917

The investments revaluation reserve represents the cumulative gains and losses arising on the revaluation of available-for-sale financial assets that have been recognized in other comprehensive income, net of amounts reclassified to profit or loss when those assets have been disposed of or are determined to be impaired.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 32

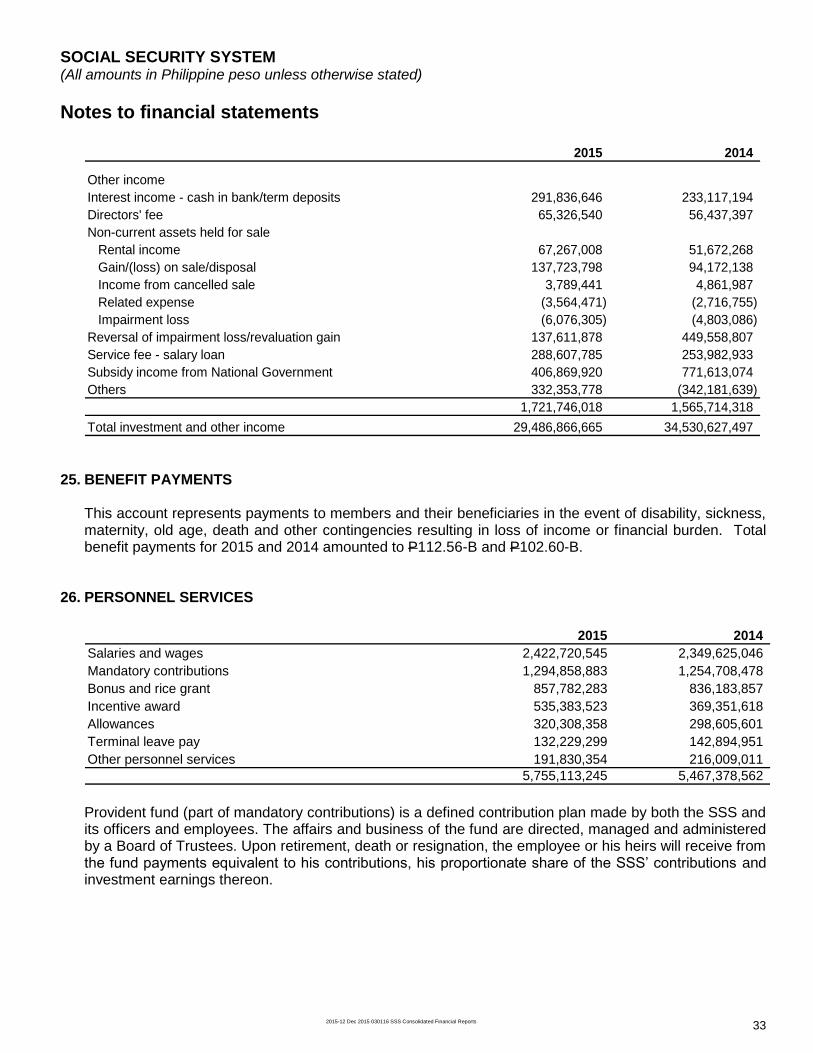

24. INVESTMENT AND OTHER INCOME

2015 2014

Investment income

Income from current investments

Held-to-maturity investments

Interest income 349,030,439 159,449,283

Held-for-trading financial assets

Dividend income 168,700,037 29,934,425

Gain/(loss) on fair value adjustment (1,498,549,951) 69,000,800

Gain/(loss) on sale/disposal 404,818,118 326,283,640

Investment expense (37,387,834) (24,781,476)

(962,419,630) 400,437,389

Total income from current investments (613,389,191) 559,886,672

Income from non-current investments

Available-for-sale financial assets

Dividend income 3,164,431,467 3,564,468,259

Gain/(loss) on sale/disposal 5,868,817,041 10,751,671,374

Investment expense (7,737,934) (7,415,565)

9,025,510,574 14,308,724,068

Held-to-maturity investments

Interest income 12,449,067,682 11,986,173,216

Penalty on overdue amortization - 6,788

Gain/(loss) on sale/disposal 23,237,721 21,075,007

Penalty on pre-payment/pre-termination - 3,687,500

Investment expense (811,678) -

12,471,493,725 12,010,942,511

Loans and receivable

Interest income 3,413,717,785 3,481,185,826

Penalty on overdue amortization 1,968,370,253 1,640,679,554

Realized gain/(loss) on foreclosure - -

Investment expense (117,133) (174,713)

Impairment loss (457,243,439) (308,643,465)

4,924,727,466 4,813,047,202

Investment property 1,956,778,073 1,272,312,726

Total income from non-current investments 28,378,509,838 32,405,026,507

27,765,120,647 32,964,913,179

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 33

2015 2014

Other income

Interest income - cash in bank/term deposits 291,836,646 233,117,194

Directors' fee 65,326,540 56,437,397

Non-current assets held for sale

Rental income 67,267,008 51,672,268

Gain/(loss) on sale/disposal 137,723,798 94,172,138

Income from cancelled sale 3,789,441 4,861,987

Related expense (3,564,471) (2,716,755)

Impairment loss (6,076,305) (4,803,086)

Reversal of impairment loss/revaluation gain 137,611,878 449,558,807

Service fee - salary loan 288,607,785 253,982,933

Subsidy income from National Government 406,869,920 771,613,074

Others 332,353,778 (342,181,639)

1,721,746,018 1,565,714,318

Total investment and other income 29,486,866,665 34,530,627,497

25. BENEFIT PAYMENTS

This account represents payments to members and their beneficiaries in the event of disability, sickness, maternity, old age, death and other contingencies resulting in loss of income or financial burden. Total benefit payments for 2015 and 2014 amounted to P112.56-B and P102.60-B.

26. PERSONNEL SERVICES

2015 2014

Salaries and wages 2,422,720,545 2,349,625,046

Mandatory contributions 1,294,858,883 1,254,708,478

Bonus and rice grant 857,782,283 836,183,857

Incentive award 535,383,523 369,351,618

Allowances 320,308,358 298,605,601

Terminal leave pay 132,229,299 142,894,951

Other personnel services 191,830,354 216,009,011

5,755,113,245 5,467,378,562

Provident fund (part of mandatory contributions) is a defined contribution plan made by both the SSS and its officers and employees. The affairs and business of the fund are directed, managed and administered by a Board of Trustees. Upon retirement, death or resignation, the employee or his heirs will receive from the fund payments equivalent to his contributions, his proportionate share of the SSS’ contributions and investment earnings thereon.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 34

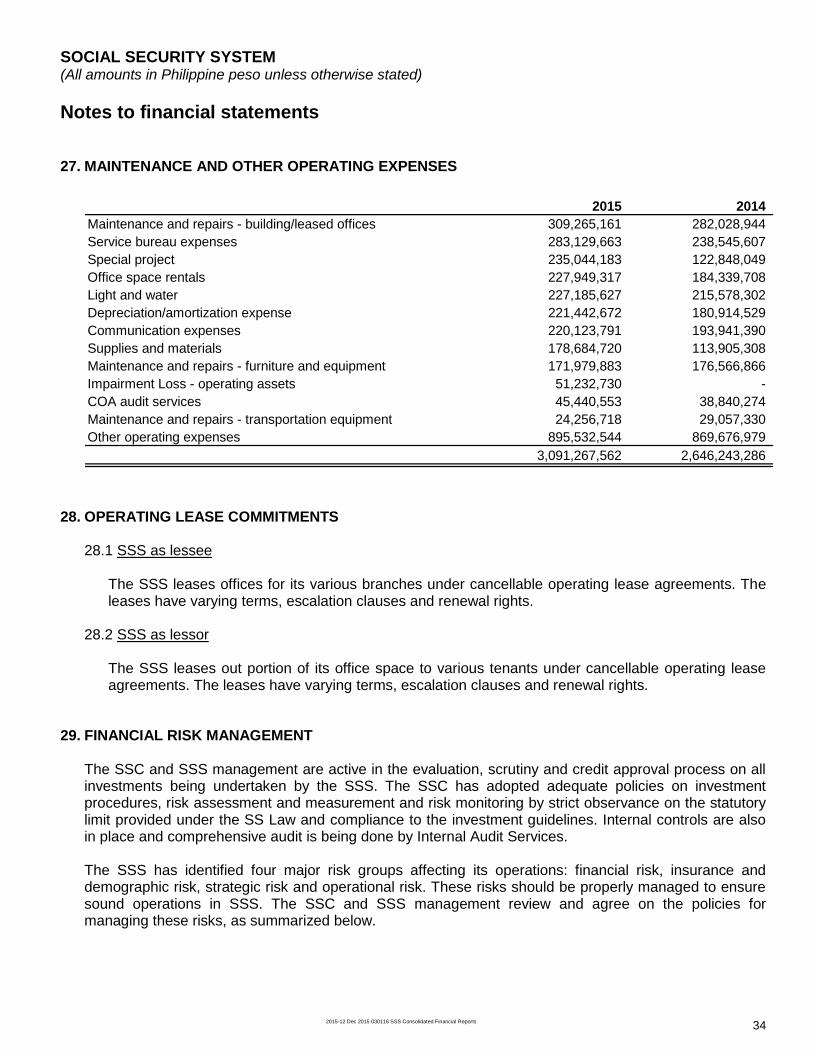

27. MAINTENANCE AND OTHER OPERATING EXPENSES

2015 2014

Maintenance and repairs - building/leased offices 309,265,161 282,028,944

Service bureau expenses 283,129,663 238,545,607

Special project 235,044,183 122,848,049

Office space rentals 227,949,317 184,339,708

Light and water 227,185,627 215,578,302

Depreciation/amortization expense 221,442,672 180,914,529

Communication expenses 220,123,791 193,941,390

Supplies and materials 178,684,720 113,905,308

Maintenance and repairs - furniture and equipment 171,979,883 176,566,866

Impairment Loss - operating assets 51,232,730 -

COA audit services 45,440,553 38,840,274

Maintenance and repairs - transportation equipment 24,256,718 29,057,330

Other operating expenses 895,532,544 869,676,979

3,091,267,562 2,646,243,286

28. OPERATING LEASE COMMITMENTS 28.1 SSS as lessee

The SSS leases offices for its various branches under cancellable operating lease agreements. The leases have varying terms, escalation clauses and renewal rights.

28.2 SSS as lessor

The SSS leases out portion of its office space to various tenants under cancellable operating lease agreements. The leases have varying terms, escalation clauses and renewal rights.

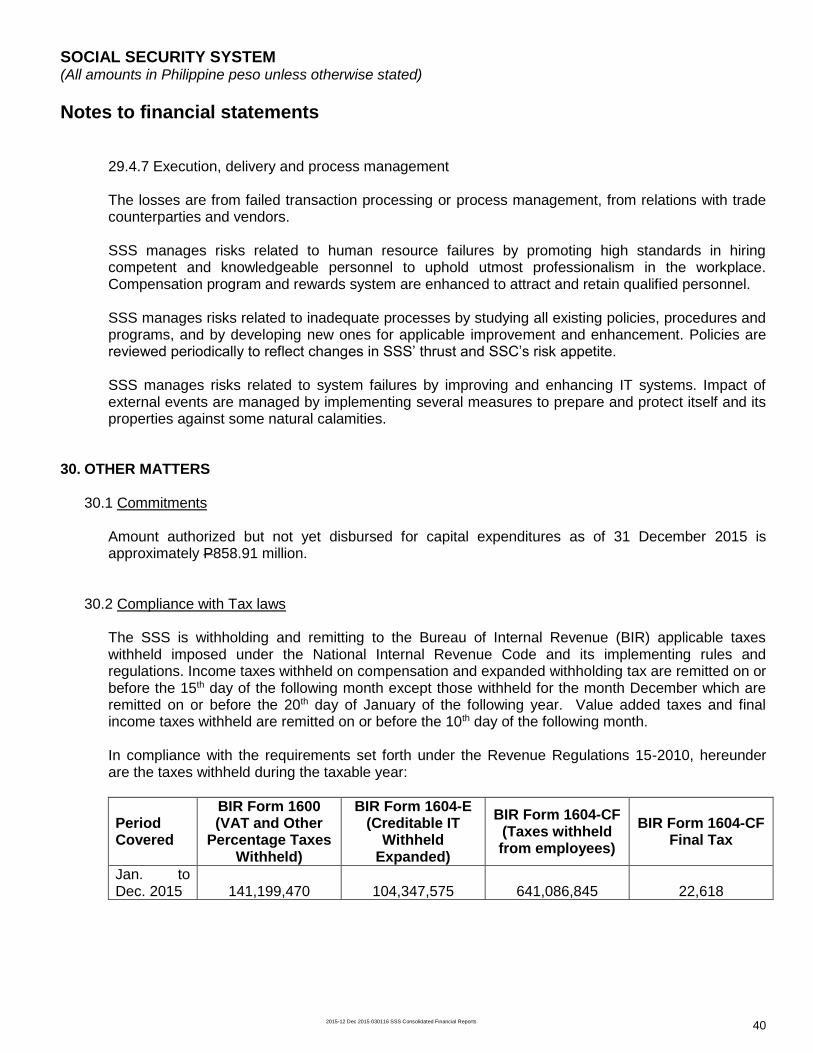

29. FINANCIAL RISK MANAGEMENT The SSC and SSS management are active in the evaluation, scrutiny and credit approval process on all investments being undertaken by the SSS. The SSC has adopted adequate policies on investment procedures, risk assessment and measurement and risk monitoring by strict observance on the statutory limit provided under the SS Law and compliance to the investment guidelines. Internal controls are also in place and comprehensive audit is being done by Internal Audit Services. The SSS has identified four major risk groups affecting its operations: financial risk, insurance and demographic risk, strategic risk and operational risk. These risks should be properly managed to ensure sound operations in SSS. The SSC and SSS management review and agree on the policies for managing these risks, as summarized below.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 35

29.1 Financial risk

This is the risk that results from unexpected changes in external markets, prices, rates and liquidity supply and demand.

29.1.1 Market risk Market risk is the SSS’ exposure to potential loss due to unexpected changes in external markets, prices or rates related to general market movements or a specific asset on the balance sheet. This risk arises from (a) fluctuations in market prices of equities due to changes in demand and supply for the securities (Equity Risk), (b) volatility in the absolute level of interest rates (Interest Rate Risk), and (c) fluctuations in exchange rates due to changes in global and local economic conditions and political developments that affect the value of SSS’ foreign-denominated investments (Foreign Currency Risk). SSS manages market risk by monitoring the daily changes in the market price of the investments. Also, the SSS Equities Portfolio is subject to Stop-Loss/Cut-Loss Program (Selling at a Loss) to limit SSS loss on a position in a security. SSS strictly adheres to the provisions of Section 26 of the SS Law, which states that the funds invested in various corporate notes/bonds, loan exposures and other financial instruments shall earn an annual income not less than the average rates of treasury bills or any acceptable market yield indicator. Currently, the SSS has achieved a mix of financial investments with interest rates that are within acceptable level. Significant investments in said instruments have fixed interest rates while repricing rates of investments in corporate notes/bond that carry floating interest rates are always based on acceptable yield (i.e. prevailing 3 months Philippine Dealing system Transaction-Fixing Rate plus a spread of not less than 0.50%). 29.1.2 Credit risk This refers to the risk of loss arising from failure of SSS’ counterparty to perform contractual obligations in a timely manner. This includes risk due to (a) failure of a counterparty to make required payments on their obligations when due (Default Risk) and (b) default of a counterparty before any transfer of securities or funds or once final transfer of securities or funds has begun but not been completed (Settlement Risk). SSS implements structured and standardized evaluation guidelines, credit ratings and approval processes. Investments undergo technical evaluation to determine their viability/acceptability. Due diligence process (i.e. credit analysis, evaluation of the financial performance of the issuer/borrower to determine financial capability to pay obligations when due, etc.) and information from third party (e.g. CIBI Information, Inc. banks and other institutions) are used to determine if counterparties are credit-worthy.

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 36

With respect to stockbrokers, the SSS has adopted the following mitigating measures: a. Evaluation of stockbrokers, at the minimum, is based on the stockbroker’s (i) good standing in the

Exchange, (ii) minimum capitalization, (iii) profitability, and (iv) positive track record of service.

b. Transactions of a stockbroker must (i) on a daily basis, not exceed a certain percentage of the

stockbroker capitalization/stockholder’s equity; (ii) in terms of total transaction, not exceed a

certain percentage of total SSS transaction except for negotiated block transaction, and (iii) within

a year of accreditation, not exceed a certain percentage of its total market transactions to ensure

that the stockbroker does not rely heavily on SSS for its business.

To avoid significant concentrations of exposures to specific industries or group of issuers and

borrowers, SSS investments are regularly monitored to ensure that it is always within the prescribed

cumulative ceilings specified in Section 26 of the SS Law. To further ensure compliance to Section 26

of SS Law, Policies and Guidelines in Determining and Managing Exposure Limits to Debt and Equity

were established.

The following table shows the latest aging analysis of some financial assets:

Neither

past due

nor

impaired 3-12 13-36 37-48 49-60 Over 60 Expired Impaired Total

Held-for-trading financial assets 4,295 - - - - - - - 4,295

Available-for-sale financial assets 95,179 - - - - - - 1,292 96,471

Held-to-maturity investments

Short-term money placements 4,813 - - - - - - - 4,813

Corporate notes and bonds 32,761 - - - - - - - 32,761

Government notes and bonds 169,966 - - - - - - - 169,966

Loans and receivable

National Home Mortgage Finance Corporation9,729 - - - - - - 1,081 10,810

Commercial and industrial loans 190 - - - - 2 12 64 268

Program MADE - - - - - - - 17 17

Other government agencies 22 - - - - - - - 22

316,955 - - - - 2 12 2,454 319,423

2015

Past due but not impaired (Age in months)

(In Millions)

SOCIAL SECURITY SYSTEM (All amounts in Philippine peso unless otherwise stated)

Notes to financial statements

2015-12 Dec 2015 030116 SSS Consolidated Financial Reports 37

Neither

past due

nor

impaired 3-12 13-36 37-48 49-60 Over 60 Expired Impaired Total

Held-for-trading financial assets 3,926 - - - - - - - 3,926

Available-for-sale financial assets 106,434 - - - - - - 1,292 107,726

Held-to-maturity investments

Short-term money placements 7,169 - - - - - - - 7,169

Corporate notes and bonds 24,875 - - - - - - - 24,875

Government notes and bonds 159,082 - - - - - - - 159,082

Loans and receivable

National Home Mortgage Finance Corporation9,947 - - - - - - 1,025 10,972

Commercial and industrial loans 513 - - - - 2 12 64 591

Program MADE - - - - - - - 17 17

Other government agencies 44 - - - - - - - 44

311,990 - - - - 2 12 2,398 314,402

2014

Past due but not impaired (Age in months)

(In Millions)

29.1.3 Liquidity risk

This refers to the risk of loss, though solvent, due to insufficient financial resources to cover for

liabilities as they fall due. It also involves the risk of excessive costs in securing such resources. This

risk also refers to (a) unanticipated changes in liquidity supply and demand that may affect the

organization through untimely sale of assets, inability to meet contractual obligations or default

(Funding Liquidity Risk) and (b) asset illiquidity or the risk of loss arising from inability to realize the

value of assets, without significant reduction in price, due to bad market conditions (Market Liquidity

Risk).

SSS manages this risk through daily monitoring of cash flows in consideration of future payment due dates and daily collection amounts. The SSS also maintains sufficient portfolio of highly marketable assets that can easily be liquidated as protection against unforeseen interruption to cash flow. To manage this risk in SSS equity investments, liquidity requirements are included in SSS’ Stock Accreditation Guidelines.

29.2 Insurance and demographic risk