Embed Size (px)

Citation preview

Social Security,Medicare andPensions 20th Edition

CPE EditionDistributed by The CPE Store

www.cpestore.com1-800-910-2755

Joseph Matthews

Social Security, Medicare and Pensions

20th Edition

Attorney Joseph L. Matthews

Copyright © 2015 by Nolo and The CPE Store, Inc. All rights reserved. This book includes the full text of “Social Security, Medicare & Government Pensions,” written by attorney Joseph Matthews, and reprinted with permission from Nolo, which owns the copyright. The Course Information, Learning Objectives, Review Questions and Review Answers are written by The CPE Store, Inc., which owns the copyrights, thereto. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the Publisher. Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher nor author shall be liable for any loss of profit or any other commercial damages, including but not limited to special, incidental, consequential, or other damages. Printed in the United States of America

Course Information Course Title: Social Security, Medicare and Pensions Learning Objectives:

Recognize the basic categories of Social Security benefits that are paid based upon earnings Identify a general requirement everyone must meet to receive Social Security benefits Ascertain what a PIA is Determine what term is used by Social Security to indicate eligible retirement benefits Identify the earliest age at which retirement benefits can be claimed Pinpoint how many years of an individual’s highest earnings are used to determine Social Securi-

ty retirement benefits Ascertain what applies during the 12 months you are approaching full retirement age if you are

already receiving retirement benefits Recognize the qualifications for a disabled widower to receive disability benefits when there are

not enough work credits to qualify Select the absolute rule regarding disability Recognize an unlikely scenario to qualify for disability benefits Identify what cannot be collected at the same time as Social Security disability benefits Discern how a Special Needs Trust can help you Recognize who qualifies for Social Security Dependents Benefits Identify the maximum family benefit percentage Discern what may be subject to a reduction in Social Security dependents benefits, called the

government pension offset Recognize situations which would be eligible for survivors benefits Pinpoint the family benefits limit for a surviving spouse and children Ascertain the significance of the break-even point when claiming Social Security Benefits Determine what method of undoing an early claim involves Social Security recalculating benefits Recognize justifiable reasons for claiming early retirement benefits Identify a requirement for receiving Supplemental Security Income Determine the income limits for qualifying for SSI Discern the types of income counted toward the SSI limits Recognize assets or resources counted by SSI Recognize methods of initiating the filing of Social Security claims for benefits Pinpoint the recommended time to sign up for Social Security benefits Select the best time to file an application for disability benefits Ascertain what the DDS will rely on in determining the nature and extent of a disability Identify the most important part of filling out the Request for Reconsideration form Choose which procedure applies if your claim for SSI benefits was denied for nonmedical reasons Ascertain what should be addressed during initial reconsideration of your benefits claim Discern the best chance of reversing Social Security’s decision when denying benefits Recognize the approved fees lawyers or other representatives can collect during the course of the

Social Security appeal process Ascertain the minimum years worked in order to qualify for a pension with the federal govern-

ment as a civilian employee Select an accurate statement regarding the CSRS retirement system Recognize contribution rules regarding the CSRS worker’s TSP account Determine what applies to FERS-covered workers Identify which office makes decisions about both CSFS and FERS benefit claims

Select which organization requires at least 90 days of active duty service in order to qualify for veterans benefits

Ascertain what determines the amount of disability compensation to which a veteran is entitled Recognize what the A&A benefit is Discern what is considered to be “Priority Group 4” by the VA Identify which supplemental insurance policy pays much of what Medicare does not Choose what type of plans limit the health care providers a patient can use Select what daily skilled nursing care service Medicare covers Pinpoint what home health care services are covered by Medicare Determine what qualifies a prescription drug payment as a TrOOP Pinpoint the name of the gap within which Medicare beneficiaries must personally pay all of the

cost of their prescription drugs Select what Medicare requires all Part D plans to include Discern when an applicant applying for Medicare would be eligible for Part B coverage Identify a situation which requires paying the difference between what Medicare pays and the full

amount of the doctor’s bill Ascertain who makes the initial Medicare approval of whether treatment must be as an inpatient Choose who will mediate disputes between the patient and the hospital Recognize what is vital for successfully appealing a plan’s rule or decision Recognize a gap in Medicare Part B Identify the basic benefit that is included in all standard Medigap policies Choose which type of supplemental insurance is partly fee-for service and partly managed care Determine what type of policies base premiums entirely on age Recognize what all plans must cover under federal law Pinpoint one of the main customer objections to managed care Identify what makes some Medicare Advantage HMOs more attractive and more expensive than

standard HMO plans Recognize disadvantages of Medicare Advantage Fee-for-Service Plans Identify what qualifies an enrollee as categorically needy Choose the term that is used to define the process of subtracting actual medical bills from income

and assets Recognize what is considered in deciding your Medicaid eligibility Identify expenses which are 100% covered by Medicaid

Subject Area: Administrative Practice Prerequisites: None Program Level: Overview Program Content: Help your clients get the most retirement and pension income and the best medical coverage. Find out what benefits are available and how to claim them as quickly and easily as possible. Learn how to qualify for Medicare and Medicaid. Find out exactly how much your benefits will be at the age you plan to claim them; time your retirement to claim your benefits at the best time for you; appeal any denied claims; learn how to fill out and file every important document. Advance Preparation: None Recommended CPE Credit: 20 hours

Table of Contents Introduction ............................................................................................................................................ i

Locating Chapters That Fit Your Needs................................................................................................. i If You Are 60 to 62 and Not Yet Retired ............................................................................................ i If You Are Within Six Months of Your 65th Birthday .......................................................................... ii If You Are 65 or Older ...................................................................................................................... ii If You Are Within Six Months of Your 66th Birthday .......................................................................... ii If You Can Work Very Little or Not at All Because of a Physical or Mental Condition ......................... ii If You Are a Surviving Spouse or Former Spouse of a Worker Who Is Retirement Age .....................iii If You Are Age 60 or Older and Are Considering Getting Married .....................................................iii

Chapter 1 – Social Security: The Basics .............................................................................................. 1

Learning Objectives ............................................................................................................................. 1 Introduction.......................................................................................................................................... 1 History of Social Security ..................................................................................................................... 1

The Beginning of Social Security ...................................................................................................... 1 Benefits Now Provide Diminished Security ....................................................................................... 2 “Saving” Social Security ................................................................................................................... 2 What You Can Do ............................................................................................................................ 3

Social Security Defined ........................................................................................................................ 3 Retirement Benefits ......................................................................................................................... 3 Disability Benefits ............................................................................................................................ 3 Dependents Benefits ........................................................................................................................ 4 Survivors Benefits ............................................................................................................................ 4

Eligibility for Benefits ............................................................................................................................ 4 Earning Work Credits ....................................................................................................................... 4 Coverage for Specific Workers ......................................................................................................... 5

Earning Work Credits ........................................................................................................................... 7 Determining Your Benefit Amount ........................................................................................................ 7

How Your Earnings Average Is Computed ....................................................................................... 8 Benefit Formula ............................................................................................................................... 8 Taxes on Your Benefits .................................................................................................................... 9

Your Social Security Earnings Record .................................................................................................. 9 U.S. Citizens’ Rights to Receive Benefits While Living Abroad ........................................................... 10 Receiving Benefits as a Noncitizen .................................................................................................... 10

Noncitizens Living in the United States ........................................................................................... 10 Non-U.S. Citizens Living Abroad .................................................................................................... 10

Review Questions .............................................................................................................................. 11 Review Answers ................................................................................................................................ 12

Chapter 2 – Social Security Retirement Benefits ............................................................................... 14

Learning Objectives ........................................................................................................................... 14 Introduction........................................................................................................................................ 14 Work Credits Required ....................................................................................................................... 14

Checking Your Earnings Record .................................................................................................... 14 Benefits for Employees of Nonprofits.............................................................................................. 15

Timing Your Retirement Benefits Claim .............................................................................................. 16 If You Claim Benefits Before Full Retirement Age ........................................................................... 16 Your Break-Even Point................................................................................................................... 16 Full Retirement Age ....................................................................................................................... 17 If You Claim Benefits After Full Retirement Age.............................................................................. 18 “Suspending” Benefits Procedure for Delaying Retirement ............................................................. 19 Reversing Suspension of Benefits and Collecting a Lump Sum ...................................................... 19

The Amount of Your Retirement Check .............................................................................................. 20 Increases for Cost of Living ............................................................................................................ 20

Table of Contents

ii

Reductions for Government Pensions ............................................................................................ 21 Working After Claiming Early Retirement Benefits .............................................................................. 21

Limits on Earned Income If Claiming Early Benefits ........................................................................ 21 Special Rule as You Approach Full Retirement Age ....................................................................... 22

Review Questions .............................................................................................................................. 24 Review Answers ................................................................................................................................ 25

Chapter 3 – Social Security Disability Benefits .................................................................................. 26

Learning Objectives ........................................................................................................................... 26 Introduction........................................................................................................................................ 26 Who Is Eligible ................................................................................................................................... 26

Work Credits Required ................................................................................................................... 26 Requirement of Recent Work ......................................................................................................... 27 Young Workers .............................................................................................................................. 28 Blind Workers ................................................................................................................................ 28 Disabled Widows and Widowers .................................................................................................... 28

What Is a Disability? .......................................................................................................................... 28 Conditions That May Qualify .......................................................................................................... 28 Listed Impairments......................................................................................................................... 29 Must Be Expected to Last One Year .............................................................................................. 30 No Substantial Gainful Activity ....................................................................................................... 30 Special Rules for Blindness ............................................................................................................ 31 Examples of Disability Determinations ............................................................................................ 31

Amount of Disability Benefit Payments ............................................................................................... 32 Estimating Benefit Amounts ........................................................................................................... 33 Cost-of-Living Increases ................................................................................................................ 33

Collecting Additional Benefits ............................................................................................................. 34 Disability and Earned Income ......................................................................................................... 34 Other Social Security Benefits ........................................................................................................ 34 Other Disability Benefits ................................................................................................................. 34 Workers’ Compensation ................................................................................................................. 34 Medicare ........................................................................................................................................ 35 Medicaid and SSI ........................................................................................................................... 35

Continuing Eligibility Review .............................................................................................................. 36 When Your Eligibility Will Be Reviewed .......................................................................................... 36 The Review Process ...................................................................................................................... 36

Returning to Work .............................................................................................................................. 36 Trial Work Period ........................................................................................................................... 36 Extended Eligibility for Benefits ...................................................................................................... 37 Quick Restart of Benefits ............................................................................................................... 37 Continuing Medicare Coverage ...................................................................................................... 37

Review Questions .............................................................................................................................. 38 Review Answers ................................................................................................................................ 39

Chapter 4 – Social Security Dependents Benefits ............................................................................. 42

Learning Objectives ........................................................................................................................... 42 Introduction........................................................................................................................................ 42 Who Is Eligible ................................................................................................................................... 42

Individuals Who Qualify .................................................................................................................. 42 Effect of Marriage and Divorce ....................................................................................................... 43

Calculating Dependents Benefits ....................................................................................................... 44 One Dependent ............................................................................................................................. 44 Family Benefits .............................................................................................................................. 45

Eligibility for More Than One Benefit .................................................................................................. 45 Working While Receiving Benefits ...................................................................................................... 45 Government Pension Offset ............................................................................................................... 46

Table of Contents

iii

Review Questions .............................................................................................................................. 48 Review Answers ................................................................................................................................ 49

Chapter 5 – Social Security Survivors Benefits ................................................................................. 50

Learning Objectives ........................................................................................................................... 50 Introduction........................................................................................................................................ 50 Work Credits Required for Eligibility ................................................................................................... 50

Number of Work Credits Required .................................................................................................. 50 Credits Earned Just Before Death .................................................................................................. 50

Who Is Eligible ................................................................................................................................... 51 Length of Marriage Rule ................................................................................................................. 51 Effect of Remarrying ...................................................................................................................... 51

Amount of Survivors Benefits ............................................................................................................. 52 Percentage of Benefits Awarded .................................................................................................... 52 Estimating Benefit Amounts ........................................................................................................... 54

Eligibility for More Than One Benefit .................................................................................................. 54 Working While Receiving Benefits ...................................................................................................... 55 Government Pension Offset ............................................................................................................... 55 Review Questions .............................................................................................................................. 57 Review Answers ................................................................................................................................ 58

Chapter 6 – When to Claim Social Security Benefits, and Which One to Claim ............................... 60

Learning Objectives ........................................................................................................................... 60 Introduction........................................................................................................................................ 60 Considerations for All Beneficiaries .................................................................................................... 60

Your Lifetime Total: The Break-Even Point ..................................................................................... 60 Factors to Consider........................................................................................................................ 61 Immediate Financial Need.............................................................................................................. 61 Continuing to Earn Before Full Retirement Age .............................................................................. 62 Life Expectancy ............................................................................................................................. 62 Availability of Other Benefits .......................................................................................................... 62

Considerations for Specific Situations ................................................................................................ 62 Unmarried, Divorced, or Widowed .................................................................................................. 62 With No Benefits From Anyone Else’s Work Record ....................................................................... 63 With Other Benefits From a Former Spouse’s Work Record ........................................................... 63 Married Couples ............................................................................................................................ 63 Worker With Minor Child ................................................................................................................ 65

Review Questions .............................................................................................................................. 66 Review Answers ................................................................................................................................ 67

Chapter 7 – Supplemental Security Income ....................................................................................... 69

Learning Objectives ........................................................................................................................... 69 Introduction........................................................................................................................................ 69 Who Is Eligible ................................................................................................................................... 69

Blind or Disabled ............................................................................................................................ 69 Citizens or Longtime Residents ...................................................................................................... 70 Income Limits ................................................................................................................................ 70 Asset Limits ................................................................................................................................... 72

Benefit Amounts ................................................................................................................................ 73 States With Federally Administered Supplements .......................................................................... 73 States With Their Own Supplements .............................................................................................. 74

Reductions to Benefits ....................................................................................................................... 74 Limit on Earned Income ................................................................................................................. 74 Limit on Unearned Income ............................................................................................................. 75 Limit on Outside Support ................................................................................................................ 75 Limit on Working Couples .............................................................................................................. 75

Table of Contents

iv

Review Questions .............................................................................................................................. 76 Review Answers ................................................................................................................................ 77

Chapter 8 – Applying for Benefits....................................................................................................... 79

Learning Objectives ........................................................................................................................... 79 Introduction........................................................................................................................................ 79 Retirement, Dependents, and Survivors Benefits ............................................................................... 79

When to Claim Benefits .................................................................................................................. 79 How and Where to File Your Claim ................................................................................................ 79 Help on the Internet ....................................................................................................................... 80 Documents You’ll Need .................................................................................................................. 81 At the Social Security Office ........................................................................................................... 83 Withdrawing a Benefits Application ................................................................................................ 83

Disability Benefits .............................................................................................................................. 83 When to File Your Claim ................................................................................................................ 84 Documents You’ll Need .................................................................................................................. 84 How Your Eligibility Is Determined .................................................................................................. 85

Supplemental Security Income (SSI) .................................................................................................. 86 Proof of Income and Assets ........................................................................................................... 86 Proof of Age If 65 or Older ............................................................................................................. 87 Proof of Blindness or Disability ....................................................................................................... 87 Proof of Citizenship or Qualifying Legal Residence ........................................................................ 87

Finding Out What Happens to Your Claim .......................................................................................... 87 Notification of Eligibility .................................................................................................................. 87 Methods of Receiving Payment ...................................................................................................... 88

Review Questions .............................................................................................................................. 90 Review Answers ................................................................................................................................ 91

Chapter 9 – Appealing a Social Security Decision ............................................................................. 93

Learning Objectives ........................................................................................................................... 93 Introduction........................................................................................................................................ 93 Reconsideration of Decision .............................................................................................................. 94

Requesting Reconsideration of Decision on Initial Benefits Claim ................................................... 94 Completing the Request for Reconsideration Form ........................................................................ 95 The Reconsideration Process ........................................................................................................ 97 Requesting Reconsideration of SSI Decision.................................................................................. 97

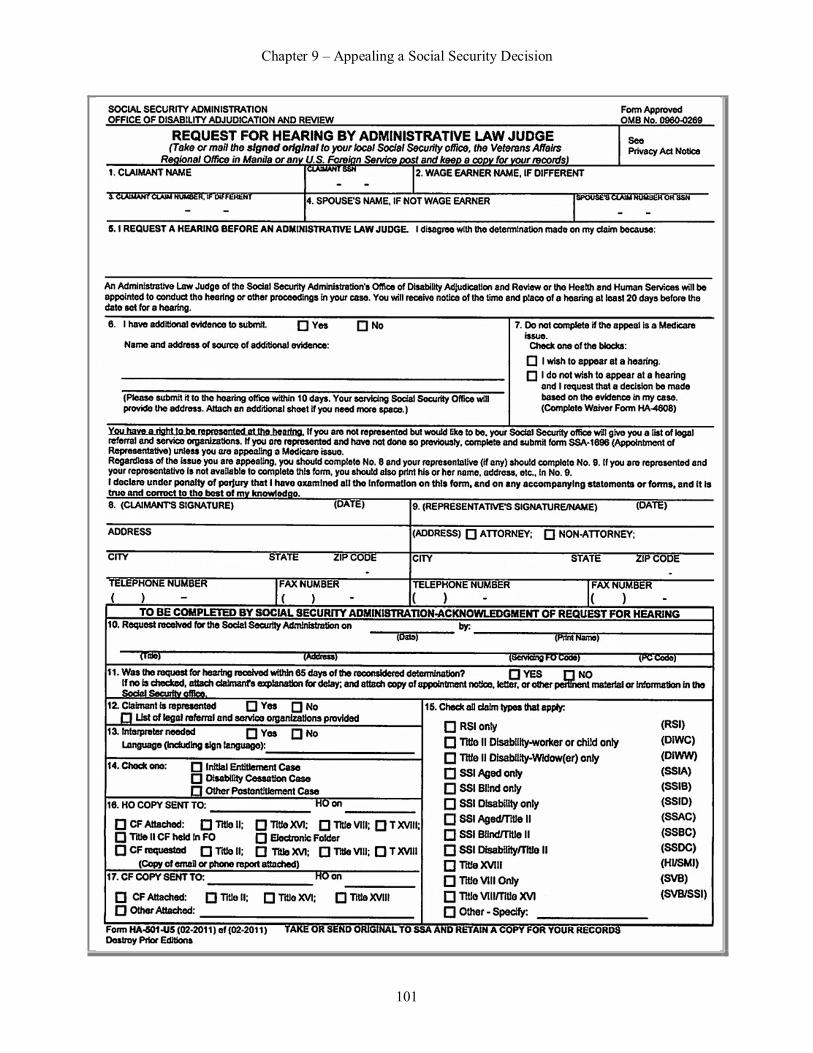

Administrative Hearing ....................................................................................................................... 98 Requesting a Hearing .................................................................................................................... 98 Completing the Request for Hearing by Administrative Law Judge Form ........................................ 99 Preparing for the Hearing ............................................................................................................. 100 The Hearing ................................................................................................................................. 100

Appeal to the National Appeals Council ........................................................................................... 102 Completing the Form ................................................................................................................... 102 Appeal Procedure ........................................................................................................................ 102

Lawsuit in Federal Court .................................................................................................................. 104 Lawyers and Other Assistance ......................................................................................................... 104

Deciding Whether You Need Assistance ...................................................................................... 104 Where to Find Assistance ............................................................................................................ 105 Legal Limits on Lawyers’ Fees ..................................................................................................... 106

Review Questions ............................................................................................................................ 108 Review Answers .............................................................................................................................. 109

Chapter 10 – Federal Civil Service Retirement Benefits .................................................................. 111

Learning Objectives ......................................................................................................................... 111 Introduction...................................................................................................................................... 111 Two Retirement Systems: CSRS and FERS .................................................................................... 112 Retirement Benefits ......................................................................................................................... 112

Table of Contents

v

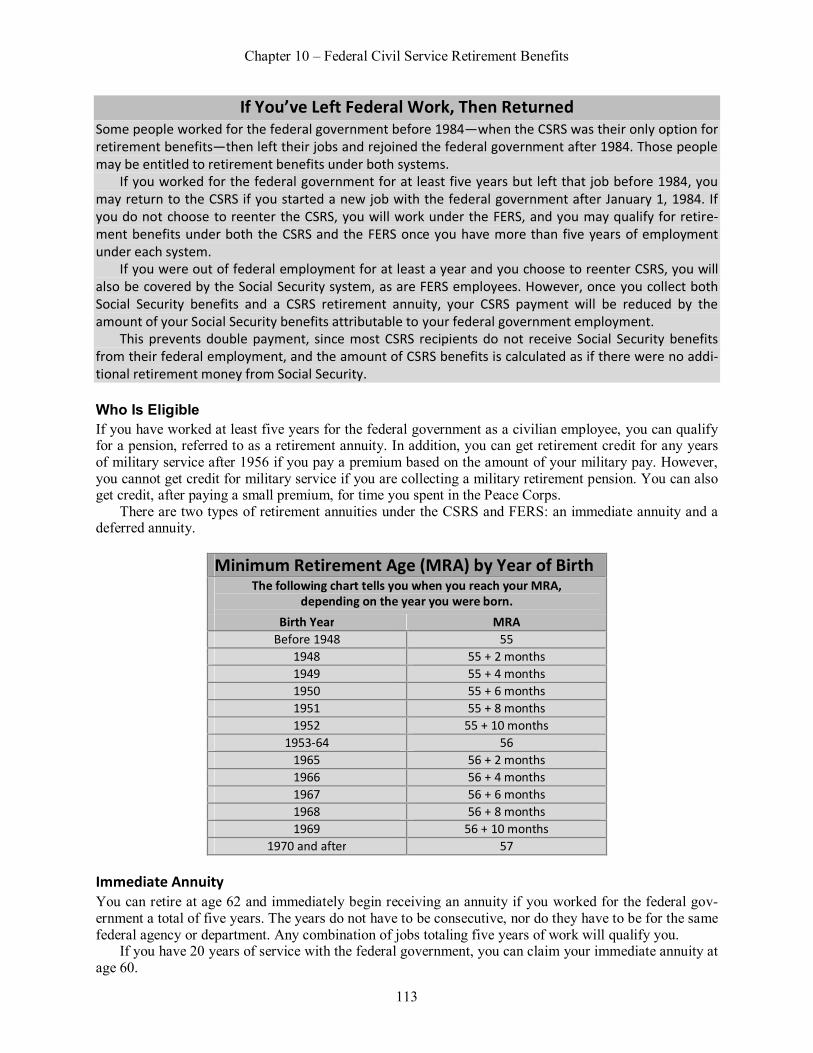

Who Is Eligible ............................................................................................................................. 113 Calculating Benefits ..................................................................................................................... 115 Survivors Benefits ........................................................................................................................ 117 Thrift Savings Plan ....................................................................................................................... 119

Disability Benefits to Federal Workers .............................................................................................. 120 Who Is Eligible ............................................................................................................................. 120 Definition of Disability ................................................................................................................... 120 Review of Disability Status ........................................................................................................... 121 Amount of Benefits....................................................................................................................... 121

Payments to Surviving Family Members........................................................................................... 122 Who Is Eligible ............................................................................................................................. 122 Amount of Benefits....................................................................................................................... 122

Applying for CSRS or FERS Benefits ............................................................................................... 123 Review Questions ............................................................................................................................ 124 Review Answers .............................................................................................................................. 126

Chapter 11 – Veterans Benefits ........................................................................................................ 128

Learning Objectives ......................................................................................................................... 128 Introduction...................................................................................................................................... 128 Types of Military Service Required ................................................................................................... 128

Active Duty .................................................................................................................................. 128 Active Duty for Training ................................................................................................................ 128

Compensation for Service-Connected Disability ............................................................................... 128 Who Is Eligible ............................................................................................................................. 129 Amount of Benefits....................................................................................................................... 129 Changes to Your Rating ............................................................................................................... 130

Pension Benefits for Financially Needy Disabled Veterans ............................................................... 131 Survivors Benefits ............................................................................................................................ 131

Dependency and Indemnity Compensation .................................................................................. 132 Wartime Service Pension ............................................................................................................. 132 Aid and Attendance...................................................................................................................... 132

Medical Treatment ........................................................................................................................... 133 Getting Information and Applying for Benefits ................................................................................... 134 Review Questions ............................................................................................................................ 135 Review Answers .............................................................................................................................. 136

Chapter 12 – Medicare ....................................................................................................................... 138

Learning Objectives ......................................................................................................................... 138 Introduction...................................................................................................................................... 138 The Medicare Maze ......................................................................................................................... 139 Medicare: The Basics ...................................................................................................................... 140

Medicare and Medicaid: A Comparison ........................................................................................ 141 Part A Hospital Insurance ................................................................................................................ 142

Who Is Eligible ............................................................................................................................. 142 Types of Care Covered ................................................................................................................ 144 Medicare-Approved Facility or Agency ......................................................................................... 145 Facility Review Panel Approval .................................................................................................... 145 Foreign Hospital Stays ................................................................................................................. 145 Skilled Nursing Facilities .............................................................................................................. 146 Home Health Care ....................................................................................................................... 147 Hospice Care ............................................................................................................................... 149

How Much Medicare Part A Pays ..................................................................................................... 150 Benefit Period or Spell of Illness ................................................................................................... 150 Hospital Bills ................................................................................................................................ 150 Psychiatric Hospitals .................................................................................................................... 152 Skilled Nursing Facilities .............................................................................................................. 152 Home Health Care ....................................................................................................................... 153

Table of Contents

vi

Hospice Care ............................................................................................................................... 154 Part B Medical Insurance ................................................................................................................. 154

Eligibility and Premiums ............................................................................................................... 154 Types of Services Covered .......................................................................................................... 155 Services Not Covered by Medicare Part B .................................................................................... 159

How Much Medicare Part B Pays ..................................................................................................... 160 Deductible Amounts ..................................................................................................................... 160 80% of Approved Charges ........................................................................................................... 160 100% of Approved Charges for Some Services ............................................................................ 160 Payments for Outpatient Therapies .............................................................................................. 161 Legal Limit on Amounts Charged ................................................................................................. 162 Assignment of Medicare-Approved Amount .................................................................................. 162 Different Payment Structure for Hospital Outpatient Charges ....................................................... 162

Part D Prescription Drug Coverage .................................................................................................. 163 Eligibility ...................................................................................................................................... 165 Premiums, Deductibles, Copayments, and Coverage Gaps .......................................................... 166 Restrictions on Coverage ............................................................................................................. 172 Deciding on a Part D Plan ............................................................................................................ 175

Review Questions ............................................................................................................................ 180 Review Answers .............................................................................................................................. 182

Chapter 13 – Medicare Procedures: Enrollment, Claims, and Appeals .......................................... 186

Learning Objectives ......................................................................................................................... 186 Introduction...................................................................................................................................... 186 Enrolling in Part A Hospital Insurance .............................................................................................. 186

Those Who Receive Social Security Benefits ............................................................................... 186 Those Who Do Not Receive Social Security Benefits ................................................................... 187 Appealing Denial of Coverage ...................................................................................................... 188

Enrolling in Part B Medical Insurance ............................................................................................... 188 Those Who Receive Social Security Benefits ............................................................................... 188 Those Who Do Not Receive Social Security Benefits ................................................................... 189 Delayed Enrollment...................................................................................................................... 189

Medicare’s Payment of Your Medical Bills ........................................................................................ 189 Inpatient and Home Care Bills ...................................................................................................... 190 Outpatient and Doctor Bills........................................................................................................... 190

Paying Your Share of the Bill ........................................................................................................... 193 How to Read a Medicare Summary Notice ....................................................................................... 193

Date of the Notice ........................................................................................................................ 193 Medicare Intermediary ................................................................................................................. 193 Type of Claim .............................................................................................................................. 193 Services Provided ........................................................................................................................ 193 Division of the Bills ....................................................................................................................... 194 Sample Forms ............................................................................................................................. 194

Appealing the Denial of a Claim ....................................................................................................... 197 Decisions About Inpatient Care (Medicare Part A) ........................................................................ 197 Payment of Doctor and Other Medical Bills (Part B)...................................................................... 201

Medicare Part D: Enrollment, Exceptions, and Appeals .................................................................... 207 Enrollment ................................................................................................................................... 208 Exceptions ................................................................................................................................... 209 Appeals ....................................................................................................................................... 210

Switching Part D Plans .................................................................................................................... 211 When You May Switch Plans ....................................................................................................... 211 Plans You May Switch To ............................................................................................................ 212 How to Switch From One Plan to Another .................................................................................... 212

State Health Insurance Assistance Programs (SHIPs)...................................................................... 212 Review Questions ............................................................................................................................ 214 Review Answers .............................................................................................................................. 215

Table of Contents

vii

Chapter 14 – Medigap Insurance ...................................................................................................... 218 Learning Objectives ......................................................................................................................... 218 Introduction...................................................................................................................................... 218 Gaps in Medicare............................................................................................................................. 219

Gaps in Part A Hospital Insurance................................................................................................ 219 Gaps in Part B Medical Insurance ................................................................................................ 219

Standard Medigap Benefit Plans ...................................................................................................... 220 Basic Benefits Included in All Medigap Plans ............................................................................... 221 Descriptions of the Standard Medigap Plans ................................................................................ 222

Terms and Conditions of Medigap Policies ....................................................................................... 227 Premium Increases ...................................................................................................................... 227 Eligibility and Enrollment .............................................................................................................. 228 Preexisting Illness Exclusion ........................................................................................................ 230

Finding the Best Medicare Supplement ............................................................................................ 231 Using an Insurance Agent ............................................................................................................ 231 Senior Associations ..................................................................................................................... 231 Only One Medigap Policy Required .............................................................................................. 232 Replacement Policies .................................................................................................................. 233

Review Questions ............................................................................................................................ 234 Review Answers .............................................................................................................................. 236

Chapter 15 – Medicare Part C: Medicare Advantage Plans ............................................................. 239

Learning Objectives ......................................................................................................................... 239 Introduction...................................................................................................................................... 239 Medicare Advantage Managed Care Plans ...................................................................................... 240

Health Maintenance Organization (HMO) ..................................................................................... 241 HMO With Point-of-Service (POS) Option .................................................................................... 242 Preferred Provider Organization (PPO) ........................................................................................ 242 Provider Sponsored Organization (PSO) ...................................................................................... 242

Medicare Advantage Fee-for-Service Plans ..................................................................................... 243 How Most Medicare Advantage Fee-for-Service Plans Work ........................................................ 244 Fee-for-Service Plans With Tiered Payment ................................................................................. 244 Disadvantages of Medicare Advantage Fee-for-Service Plans ...................................................... 244

Choosing a Medicare Advantage Plan ............................................................................................. 244 Choice of Doctors and Other Providers ........................................................................................ 245 Access to Specialists and Preventive Care ................................................................................... 246 Prescription Drug Coverage ......................................................................................................... 247 Extent of Service Area ................................................................................................................. 247 Other Plan Features ..................................................................................................................... 248

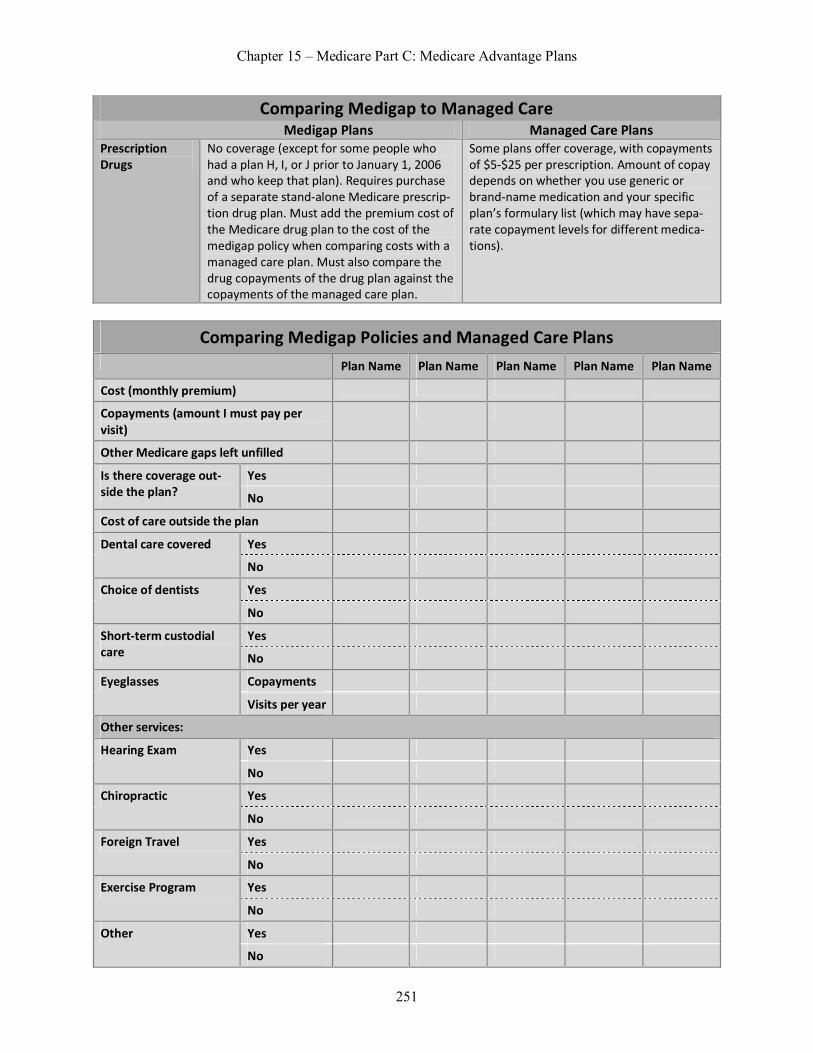

Comparing Medigap and Medicare Advantage Plans ....................................................................... 249 Your Rights When Joining, Leaving, or Losing a Medicare Advantage Plan ...................................... 252

Joining in the First Six Months After Enrolling in Medicare ............................................................ 252 Joining During a Plan’s Open Enrollment Period .......................................................................... 252 Leaving the Plan .......................................................................................................................... 252 Joining When Dropped From Another Medicare Advantage Plan .................................................. 252 Joining When Moving to a New Geographic Area ......................................................................... 252

Review Questions ............................................................................................................................ 254 Review Answers .............................................................................................................................. 255

Chapter 16 – Medicaid and State Supplements to Medicare ........................................................... 257

Learning Objectives ......................................................................................................................... 257 Introduction...................................................................................................................................... 257 Medicaid Defined ............................................................................................................................. 257 Who Is Eligible ................................................................................................................................. 257

Categorically Needy ..................................................................................................................... 258 Medically Needy .......................................................................................................................... 258 Determining Couples’ Income and Assets .................................................................................... 259

Table of Contents

viii

Financial Help From Friends or Family ......................................................................................... 260 Medical Costs Covered by Medicaid ................................................................................................ 260

Services Covered in Every State .................................................................................................. 260 Optional Services ......................................................................................................................... 261

Requirements for Coverage ............................................................................................................. 262 Care Must Be Prescribed by Doctor ............................................................................................. 262 Provider Must Be Participating in Medicaid ................................................................................... 262 Treatment Must Be Medically Necessary...................................................................................... 263

Cost of Medicaid Coverage .............................................................................................................. 263 No Payments to Medical Providers ............................................................................................... 263 Fees to State Medicaid Agency for Services................................................................................. 263

Other State Assistance .................................................................................................................... 264 Qualified Medicare Beneficiary (QMB) .......................................................................................... 264 Specified Low-Income Medicare Beneficiary (SLMB) and Qualifying Individual (QI) ...................... 265

Applying for Medicaid, QMB, SLMB, or QI ........................................................................................ 265 Where to File ............................................................................................................................... 265 Required Documents and Other Information................................................................................. 265 Application Procedure .................................................................................................................. 266 Retroactive Benefits ..................................................................................................................... 266 Review of Eligibility ...................................................................................................................... 266

What to Do If You Are Denied Coverage .......................................................................................... 267 Review Questions ............................................................................................................................ 268 Review Answers .............................................................................................................................. 269

Glossary ............................................................................................................................................. 271 Index .................................................................................................................................................. 275

Introduction Are you approaching retirement, or are you disabled? Do you help support someone who is?

If so, you may be facing a series of problems for which you are unprepared: getting the most retire-ment and pension income and obtaining the broadest medical coverage you can afford. People in their retirement years may have access to a wide variety of programs to help with financial support and medi-cal care. But many people are unaware of the extent of such programs, or are unable to wade through the programs’ rules and regulations, and so do not receive all the benefits they could.

For people who are or soon will be on fixed incomes, an unnecessary loss of benefits can cause criti-cal problems. This book is intended to help you get all the benefits to which you are entitled: Social Secu-rity (both retirement and disability based), Supplemental Security Income, veterans benefits, and civil service benefits.

Most people want the broadest possible medical coverage they can afford, because a serious medical problem can cost a fortune. Almost everyone is aware that Medicare is available, but few people under-stand how it works and what it does and does not cover. This book carefully, completely, and in plain language explains Medicare rules and regulations. It also explains how the holes in Medicare can be filled by medigap private insurance, Medicare Advantage health plans, Medicaid, and veterans benefits. Locating Chapters That Fit Your Needs Each chapter in this book explains a different benefit program or set of laws designed to protect the rights of older Americans. It explains how each particular program works, and how it may relate to the other programs discussed in the book. Not all of these benefits will apply to you. But, even if you don’t think you are eligible for a particular benefit, take a look at the general requirements discussed in that chapter. You may be surprised to find that a program, or some part of it, applies to you in ways you had not previ-ously realized. Pay special attention to explanations of how your income, or your participation in one benefit program, might affect your rights in another program.

You have earned these benefits. A key word in this book is “entitled.” Almost all of the bene-fits discussed here are paid to you because you worked for them, paying contributions into the system throughout your working life. If you are an older American facing retirement and a

fixed income, you need all the financial support these programs are supposed to provide. And you are entitled to it.

RESOURCE Private pensions and 401(k) deferred benefit plans are far more complex than can be cov-ered in a book of this breadth. We recommend that you consult IRAs, 401(k)s & Other Re-tirement Plans: Taking Your Money Out, by Twila Slesnick and John C. Suttle (Nolo).

Depending on your age and stage of life, there are a number of major issues you should consider as

you first scan through the book.

If You Are 60 to 62 and Not Yet Retired Find out how soon (at what age) you will become eligible for Social Security retirement, depend-

ents, or survivors benefits. (See “Timing Your Retirement Benefits Claim” in Chapter 2.) Learn how much your Social Security retirement benefits will be reduced if you retire early or in-

creased if you retire later. (See “Timing Your Retirement” and “The Amount of Your Retirement Check” in Chapter 2.)

Explore when would be the best time to claim your benefits, and which benefits to claim. (See Chapter 6.)

Introduction

ii

Find out how much income you can earn without affecting your Social Security benefits if you claim them before full retirement age. (See “Working After Claiming Early Retirement Benefits” in Chapter 2.)

See whether you can claim civil service retirement benefits if you have ever worked for the feder-al, state, or local government or any public agency or institution—such as a school system, li-brary, or public health facility. (See Chapter 10.)

Check the rules of your private pension plan—if you worked for any private company that had a pension plan, or if you belonged to any union—including whether your pension will be affected by your Social Security benefits. (Private pension plans are outside the scope of this book.)

This Book Provides Ongoing Help to Caregivers

People in their 60s must make initial decisions about Social Security, Medicare, and other benefit pro-grams. But over the years, people will also have to make new decisions, concerning how they receive their Medicare coverage, choose medigap insurance or prescription drug plans, qualify for long-term care insurance benefits, and determine eligibility for Medicaid and other programs for people with low incomes. This book serves as a guide for caregivers, such as adult children, who may not have been in-volved in original choices about these matters, but who now must help loved ones make ongoing deci-sions over time. If You Are Within Six Months of Your 65th Birthday

If you have not already claimed retirement benefits, obtain a current estimate of the benefits you could receive from your civil service retirement system, the private pension plan of any company where you’ve worked for at least three years, and the Department of Veterans Affairs if you are a veteran. (See Chapters 10 and 11.)

Be ready to claim your Medicare coverage as soon as you become eligible. (See Chapter 12.) Look into ways to supplement your Medicare coverage, including medigap insurance, a Medicare

Advantage plan, and a Medicare drug coverage plan. (See Chapters 12, 14, and 15.) If you have low income and few assets, check into your eligibility to receive assistance with med-

ical bills from Medicaid. (See Chapter 16.) If You Are 65 or Older

If you have a low income and few assets, see whether you can get financial assistance from the Supplemental Security Income (SSI) program. (See Chapter 7.)

Arrange for your access to medical treatment, after reading about the Medicare rules as well as those of your Medicare Advantage or medigap insurance plan. (See Chapters 13, 14, 15, and 16.)

If you have low income and few assets other than your home, see whether you are eligible for Medicaid or for expanded Medicare coverage for prescription drugs. (See “Part D Prescription Drug Coverage” in Chapter 12; and Chapter 16.)

If you were in the military, see whether you can claim financial or medical benefits from the De-partment of Veterans Affairs (VA). (See Chapter 11.)

If You Are Within Six Months of Your 66th Birthday If you have not already claimed Social Security retirement benefits, obtain a current estimate of the bene-fits you could receive when you reach full retirement age, which is now 66. (See Chapter 1.) If You Can Work Very Little or Not at All Because of a Physical or Mental Condition

Look into whether you might qualify for Social Security disability benefits. (See Chapter 3.) If you have low income and few assets, see whether you might qualify for Supplemental Security

Income (SSI). (See Chapter 7.)

Introduction

iii

If you were in the armed forces and your physical condition is in any way related to your time in the service, investigate the qualification rules for veterans disability benefits and medical care. (See Chapter 11.)

If You Are a Surviving Spouse or Former Spouse of a Worker Who Is Retirement Age

Learn whether you’re eligible for Social Security or civil service survivors and dependents bene-fits. (See Chapters 4 and 5.)

Obtain an estimate of your own retirement benefits, and compare them to estimates of survivors or dependents benefits.

Check the rules of the pension plan of any company or government entity for which your spouse worked for more than three years. (See Chapter 10 for government pensions.)

If you or your spouse were in the military, look into whether you are entitled to any veterans ben-efits. (See Chapter 11.)

If You Are Age 60 or Older and Are Considering Getting Married

Find out what effect marriage would have on your right and your intended spouse’s right to col-lect Social Security retirement, survivors, and dependents or disability benefits, and on the amount of those benefits. (See “The Amount of Your Retirement Check” in Chapter 2; Chapters 4 and 5.)

Determine what effect marriage would have on your and your intended’s eligibility for Supple-mental Security Income (SSI) and Medicaid. (See Chapters 7 and 16.)

A Note for Same-Sex Spouses The United States Supreme Court has recently struck down parts of the federal Defense of Marriage Act, which had previously refused federal benefits to same-sex spouses. Now, some federal benefits—including Social Security and veterans benefits—are available to some same-sex spouses, depending on the marital laws in the state they live in or were married in. For rules concerning particular benefits for same-sex married couples, refer to the chapters in this book that explain those benefits.

Living Together: Unofficial Marriages and Benefit Programs Your eligibility for certain benefits and the amount of those benefits may depend on your marital status. Although Social Security and other programs provide a number of benefits to the spouse of a worker, they do not provide for people who live together without being married even if they are registered do-mestic partners or have entered into a civil union under their state’s laws.

On the other hand, your eligibility for some benefits may depend on the combined amount of in-come and assets of you and your spouse. If you are not married, your partner’s income and assets won’t be considered, so you are more likely to be eligible for benefits.

Many people who live together believe they have a common law marriage—a legally recognized marriage—even though they never went through a formal ceremony, took out a marriage license, or filed a marriage certificate.

In fact, common law marriages are recognized only in Alabama, Colorado, District of Columbia, Iowa, Kansas, Montana, Oklahoma, Rhode Island, South Carolina, Texas, and Utah. In Georgia, Idaho, Ohio, and Pennsylvania, common law marriages are recognized only if they were formed before a certain date. If you do not live in one of these states and meet your state’s particular requirements, you do not have a common law marriage.

If you do live in one of these states, you will be considered to have a common law marriage only if you and a person of the opposite sex intend to be considered as married. You can show this in a number of ways—including living together as husband and wife for several years, using the same last name, re-

Introduction

iv

ferring to yourselves as married, having children together and giving them the family name you share, and owning property together. You can even write out an agreement that says you regard yourselves as being in a common law marriage. However, there is no one thing you can count on to absolutely prove the existence of your common law marriage. And nothing guarantees that Social Security or other pro-grams will consider you married when making a decision about your benefits.

Finally, if either you or the person with whom you live is still lawfully married to someone else, there can be no common law marriage.

Online Help on Social Security, Medicare, and Other Government Programs The Internet has greatly increased public access to information about government programs. But not all this information is created equal. Plenty of information on the Web is helpful, but there is also a lot of confusing or misleading material. The government’s own websites—like Social Security’s www.ssa.gov and Medicare’s www.medicare.gov—contain a huge amount of material, but the sites themselves can be hard to navigate.

This book will point you to some of the most useful Internet tools and information from government websites covering retirement, pension, and medical benefits programs. If you find information on your own from nongovernment Web sources, make sure to confirm its accuracy on an official site before you use it to make a decision. Get Updates to This Book and More on Nolo.com When there are important changes to the information in this book, we’ll post updates online, on a page dedicated to this book: www.nolo.com/back-of-book/SOA.html. You’ll find other useful information there, too, including author blogs, podcasts, and videos.

About the Author Joseph L. Matthews has been an attorney since 1971. From 1975 to 1977 he taught at the law school of the University of California at Berkeley (Boalt Hall). Mr. Matthews is a senior editor at www.caring.com and also the author of Long-Term Care: How to Plan & Pay for It, How to Win Your Personal Injury Claim, and The Lawsuit Survival Guide, all published by Nolo.

Chapter 1

Social Security: The Basics Learning Objectives

Recognize the basic categories of Social Security benefits that are paid based upon earnings Identify a general requirement everyone must meet to receive Social Security benefits Ascertain what a PIA is

Introduction Social Security is the general term that describes a number of related programs—retirement, disability, dependents, and survivors benefits. These programs operate together to provide workers and their families with some monthly income when their normal flow of income shrinks because of the retirement, disabil-ity, or death of the person who earned that income.

The Social Security system was initially intended to provide financial security for older Americans. It was meant to help compensate for limited job opportunities available to older people in our society. And it was intended to help bridge the financial gaps created by the disappearance of the multigenerational family household—a breakup caused in large measure by the need for American workers to move around the country to find decent employment.

Unfortunately, this goal of providing financial security is today increasingly remote. The combination of rapidly rising living costs, stagnation of benefit amounts, and penalties for older people who continue to work has made the amount of support offered by Social Security less adequate with each passing year. This shrinking of the Social Security safety net makes it that much more important that you get the max-imum benefits to which you are entitled.