Embed Size (px)

DESCRIPTION

Social Security Essentials for Ohio Public Employees. Earning Credits. 40 Credits for retirement Maximum 4 credits in 1 year $1,120 earnings = 1 credit in 2011 ($4,480). Worker Reduced benefits as early as age 62 Full benefits at age 65-67 - PowerPoint PPT Presentation

Citation preview

Social Security Social Security Essentials Essentials

for Ohio for Ohio

Public EmployeesPublic Employees

Earning CreditsEarning Credits

40 Credits for retirement40 Credits for retirement

Maximum 4 credits in 1 yearMaximum 4 credits in 1 year

$1,120 earnings = 1 credit in 2011 ($4,480) $1,120 earnings = 1 credit in 2011 ($4,480)

WorkerWorker

Reduced benefits as early as age 62 Reduced benefits as early as age 62

Full benefits at age 65-67Full benefits at age 65-67

Increased benefits after full retirement age (FRA)Increased benefits after full retirement age (FRA)

Wife or HusbandWife or Husband

As early as age 62As early as age 62

At any age if caring for child under age 16 or disabledAt any age if caring for child under age 16 or disabled

Divorced spouses may qualify if married at least 10 yearsDivorced spouses may qualify if married at least 10 years

ChildChild

Unmarried and up to age 18 or 19 if still in high schoolUnmarried and up to age 18 or 19 if still in high school

Any age if disabled before age 22Any age if disabled before age 22

Retirement BenefitsRetirement Benefits

Full Retirement Age &Full Retirement Age &

Age 62 ReductionAge 62 Reduction

Year of BirthYear of Birth Full Retirement AgeFull Retirement Age % at Age 62% at Age 62

1943-1954 1943-1954 66 66 75 %75 % 19551955 66 & 2 months 66 & 2 months 74.2 %74.2 % 19561956 66 & 4 months 66 & 4 months 73.3 %73.3 % 1957 1957 66 & 6 months 66 & 6 months 72.5 %72.5 % 19581958 66 & 8 months 66 & 8 months 71.7 %71.7 % 1959 1959 66 & 10 months 66 & 10 months 70.8 %70.8 % 1960 & later 1960 & later 67 67 70 %70 %

Reduction is Permanent! Reduction is Permanent!

Benefits for Dependent SpousesBenefits for Dependent Spouses

Spouse may receive up to 50% of a worker’s Spouse may receive up to 50% of a worker’s fullfull Social Security benefit—Social Security benefit—howeverhowever,,

A spouse benefit is reduced by amount equal A spouse benefit is reduced by amount equal toto fullfull retirement benefit the spouse earned retirement benefit the spouse earned on his/her own work recordon his/her own work record

Reduced if started early (before FRA) Reduced if started early (before FRA)

Survivor BenefitsSurvivor Benefits

Widow(er)Widow(er)Reduced benefits as early as age 60 or, if disabled, Reduced benefits as early as age 60 or, if disabled, age 50 age 50

At any age if caring for child of worker under age 16 At any age if caring for child of worker under age 16 or disabled before age 22or disabled before age 22

Divorced widow(er) may qualify if married at least Divorced widow(er) may qualify if married at least 10 years 10 years

Remarriage @ age 60 or later does not end benefitRemarriage @ age 60 or later does not end benefit

Benefit at full retirement age is Benefit at full retirement age is usuallyusually the same as the same as what worker was receiving at his death or would what worker was receiving at his death or would have received at full retirement age have received at full retirement age

Survivor Benefits Survivor Benefits (cont)(cont)

ChildChild

Under age 18 or 19 if still in high schoolUnder age 18 or 19 if still in high school

Any age if disabled before age 22Any age if disabled before age 22

UnmarriedUnmarried****

$255 Lump Sum Death Benefit$255 Lump Sum Death Benefit

Surviving spouse or minor/disabled children onlySurviving spouse or minor/disabled children only

Social Security Benefits While WorkingSocial Security Benefits While Working

What is work?What is work?

Wages from PERS, FICA, anywhereWages from PERS, FICA, anywhere

May be self employmentMay be self employment

Work is Work is NOTNOT income from private pensions, income from private pensions, rental properties, investments, 401k or deferred rental properties, investments, 401k or deferred comp, etc.comp, etc.

Work Before Full Retirement AgeWork Before Full Retirement Age

Work Work beforebefore full retirement age often reduces or full retirement age often reduces or eliminates Social Security cash benefitseliminates Social Security cash benefits

Earnings from work may affect both retirement Earnings from work may affect both retirement and dependent/survivor benefitsand dependent/survivor benefits

Online Retirement Earnings Test Calculator at Online Retirement Earnings Test Calculator at www.ssa.gov/planners/morecalculators.htm www.ssa.gov/planners/morecalculators.htm computes how work may affect benefitscomputes how work may affect benefits

How Work Affects Your Benefit How Work Affects Your Benefit pamphletpamphlet

OPERS and Social SecurityOPERS and Social Security

When your pension is from work not covered When your pension is from work not covered by Social Security, two laws may affect your by Social Security, two laws may affect your Social Security benefit:Social Security benefit:

Government Pension Offset (GPO)Government Pension Offset (GPO)

Windfall Elimination Provision (WEP)Windfall Elimination Provision (WEP)

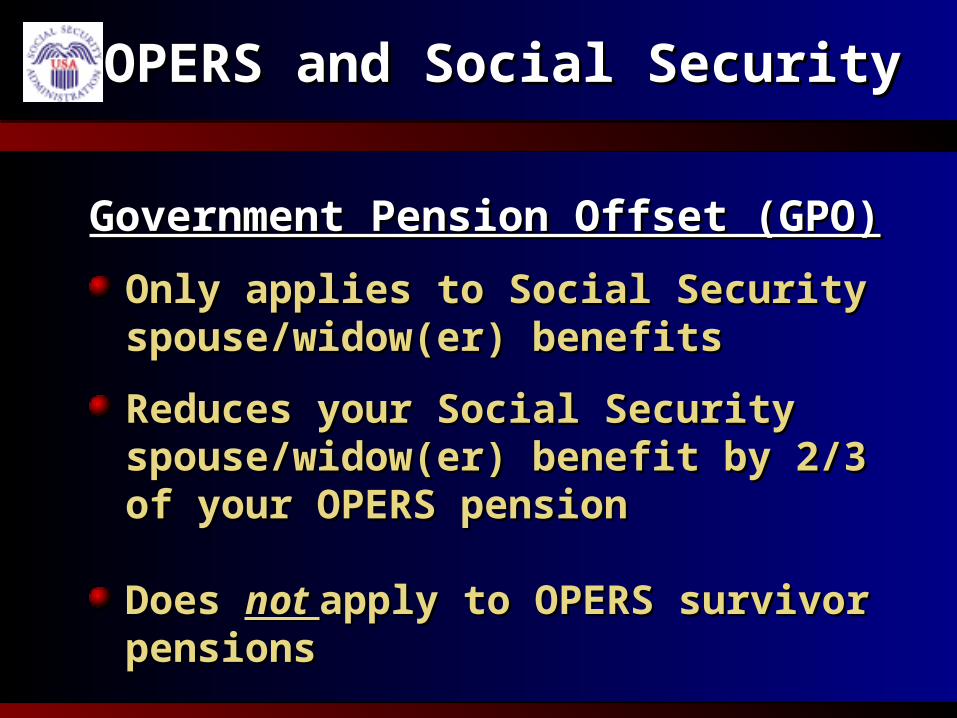

OPERS and Social SecurityOPERS and Social Security

Government Pension Offset (GPO)Government Pension Offset (GPO)

Only applies to Social Security Only applies to Social Security spouse/widow(er) benefitsspouse/widow(er) benefits

Reduces your Social Security Reduces your Social Security spouse/widow(er) benefit by 2/3 of your spouse/widow(er) benefit by 2/3 of your OPERS pensionOPERS pension

Does Does not not apply to OPERS survivor pensionsapply to OPERS survivor pensions

Spouse Benefit ComputationSpouse Benefit Computation

Fred and Alice both paid FICA. Fred receives Fred and Alice both paid FICA. Fred receives $2,366/month Social Security benefit at Full $2,366/month Social Security benefit at Full Retirement AgeRetirement Age

Alice receives $1,400 Alice receives $1,400 Social Security benefitSocial Security benefit at at Full Retirement AgeFull Retirement Age

Spouse 50% rate = $1,183Spouse 50% rate = $1,183

Alice cannot get spouse benefits because her own Alice cannot get spouse benefits because her own Social Security benefit is greaterSocial Security benefit is greater

Alice’s own benefit offsets spouse benefit!Alice’s own benefit offsets spouse benefit!

GPO Example: Spouse GPO Example: Spouse

Tom’s Social Security benefit at Full Retirement Tom’s Social Security benefit at Full Retirement Age is $2,366/monthAge is $2,366/month

Ann’s spouse benefit from Tom at her Full Ann’s spouse benefit from Tom at her Full Retirement Age Retirement Age = $1,183= $1,183

2/3 of Ann’s $2,100 OPERS = $1,4002/3 of Ann’s $2,100 OPERS = $1,400

Ann’s Social Security spouse benefit = $ 0Ann’s Social Security spouse benefit = $ 0

Ann’s OPERS benefit offsets the spouse benefitAnn’s OPERS benefit offsets the spouse benefitjust as her own Social Security benefit would just as her own Social Security benefit would

offset the spouse benefit. offset the spouse benefit.

GPO Example: Widow(er)GPO Example: Widow(er)

Tom diesTom dies

Ann’s widow benefit Ann’s widow benefit = $2,366 = $2,366

2/3 of Ann’s $2,100 OPERS 2/3 of Ann’s $2,100 OPERS = $1,400 = $1,400

Ann’s Social Security widow benefit = $ 966Ann’s Social Security widow benefit = $ 966

If OPERS pension is $4,685 or more, 2/3 isIf OPERS pension is $4,685 or more, 2/3 is

more than highest possible spouse/widow benefit more than highest possible spouse/widow benefit

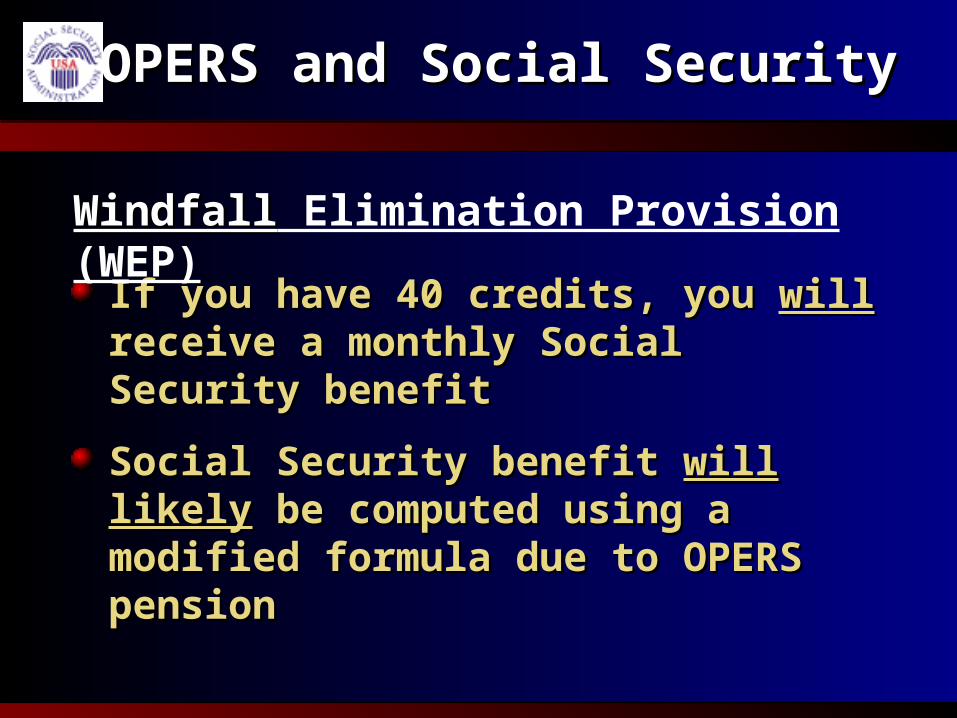

OPERS and Social SecurityOPERS and Social Security

If you have 40 credits, you If you have 40 credits, you willwill receive a receive a monthly Social Security benefitmonthly Social Security benefit

Social Security benefit Social Security benefit will likelywill likely be be computed using a modified formula due to computed using a modified formula due to OPERS pensionOPERS pension

WindfallWindfall Elimination Provision (WEP)

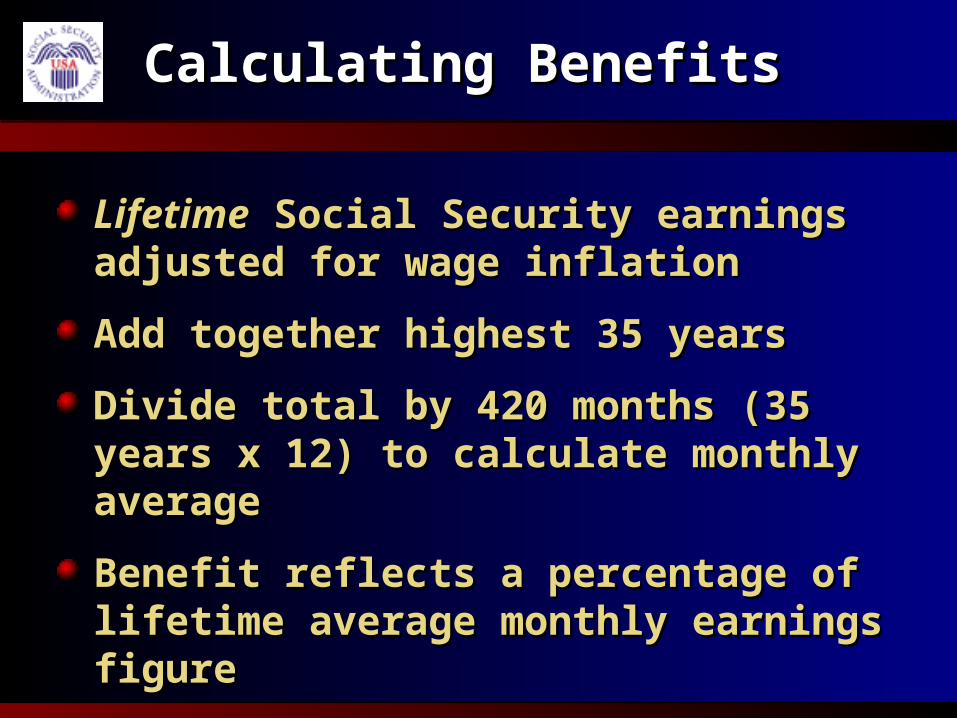

Calculating BenefitsCalculating Benefits

LifetimeLifetime Social Security earnings adjusted for Social Security earnings adjusted for wage inflation wage inflation

Add together highest 35 years Add together highest 35 years

Divide total by 420 months (35 years x 12) to Divide total by 420 months (35 years x 12) to calculate monthly average calculate monthly average

Benefit reflects a percentage of lifetime average Benefit reflects a percentage of lifetime average monthly earnings figure monthly earnings figure

The higher your average lifetime Social The higher your average lifetime Social Security earnings, the higher your benefitSecurity earnings, the higher your benefit

Lower-paid workers receive larger Lower-paid workers receive larger benefits in relation to their earnings than benefits in relation to their earnings than higher-paid workershigher-paid workers

Calculating BenefitsCalculating Benefits

Replacement Rates Replacement Rates (Approximate)(Approximate)

Low Income Worker Low Income Worker

$20,800annual avg. $20,800annual avg. ($10/hr)($10/hr)

$989/month benefit at full age$989/month benefit at full age

Middle Income WorkerMiddle Income Worker

$41,600 annual avg. $41,600 annual avg. ($20.00/hr)($20.00/hr)

$1,543/month benefit at full age$1,543/month benefit at full age

Higher Income WorkerHigher Income Worker

$84,032annual avg.$84,032annual avg. ($40.00/hr)($40.00/hr)

$2,241/month benefit at full age$2,241/month benefit at full age

% o

f ea

rnin

gs%

of

earn

ings

57%

44.5%

32%

Why Windfall Provision?Why Windfall Provision?

Years with 0 earnings under Social Security Years with 0 earnings under Social Security reduce average lifetime earnings figurereduce average lifetime earnings figure

The result: Your average FICA earnings are The result: Your average FICA earnings are low and you look like a low-income worker low and you look like a low-income worker even if your PERS earnings are high(er)even if your PERS earnings are high(er)

Windfall reduces the higher replacement % Windfall reduces the higher replacement % intended for low income workersintended for low income workers

Windfall RulesWindfall Rules

Recognizes the more years a worker has Recognizes the more years a worker has paid Social Security taxes on substantial paid Social Security taxes on substantial earnings, the closer that person should be to earnings, the closer that person should be to the standard benefit formula.the standard benefit formula.

30+ years 30+ years = WEP doesn = WEP doesn’’t applyt apply

21-29 years21-29 years = modified WEP = modified WEP

20 or fewer years 20 or fewer years = full WEP = full WEP

WEP & Your Benefit EstimateWEP & Your Benefit Estimate

Your Your Social Security StatementSocial Security Statement estimates don estimates don’’t t figure WEPfigure WEP

If your full benefit estimate in 2011 is If your full benefit estimate in 2011 is

- $750/month or more, subtract $374- $750/month or more, subtract $374- $749/month or less, multiply by .445- $749/month or less, multiply by .445

Online WEP Calculator and chart atOnline WEP Calculator and chart at www.socialsecurity.gov/gpo-wepwww.socialsecurity.gov/gpo-wep

Social Security Benefits & Income Tax

Are Social Security benefits taxable? Are Social Security benefits taxable? MaybeMaybe

If the sum of other income and Social Security If the sum of other income and Social Security benefits exceeds:benefits exceeds:

- $25,000 for an individual- $25,000 for an individual- $32,000 for a married couple- $32,000 for a married couple

Then you may have to pay income tax on part of Then you may have to pay income tax on part of your Social Security benefits.your Social Security benefits.

For more information, call 1-800-829-3676 or visit www.irs.gov IRS Pub. 915

MedicareMedicare

65 and older

Receiving Social Security Disability benefits at least 24 months (exception: Lou Gehrig’s disease)

Permanent kidney failure

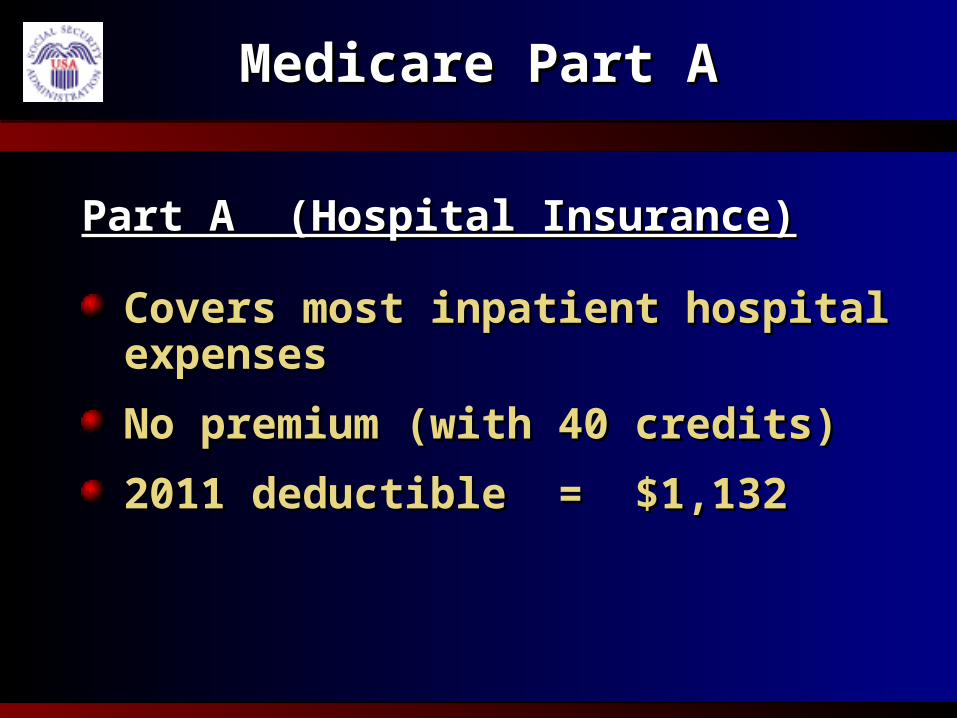

Medicare Part AMedicare Part A

Part A (Hospital Insurance)Part A (Hospital Insurance)

Covers most inpatient hospital expenses Covers most inpatient hospital expenses

No premium (with 40 credits)No premium (with 40 credits)

2011 deductible = $1,1322011 deductible = $1,132

Medicare CoverageMedicare Coverage

Part B ( Supplemental Medical Insurance)Part B ( Supplemental Medical Insurance)

Covers 80% doctor bills and outpatient Covers 80% doctor bills and outpatient medical expenses after $162 calendar year medical expenses after $162 calendar year deductibledeductible

2011 Monthly Premium = $115.402011 Monthly Premium = $115.40****

Defined Enrollment Periods (Defined Enrollment Periods (or penalties!)or penalties!)

Filing for MedicareFiling for Medicare

Automatic if you are getting Social Security Automatic if you are getting Social Security benefits at 65benefits at 65

Contact SSA at age 65 if you are not getting Contact SSA at age 65 if you are not getting benefitsbenefits

May apply on own Social Security record May apply on own Social Security record (many OPERS employees pay Medicare tax) (many OPERS employees pay Medicare tax) or the record of a spouse -living, deceased, or the record of a spouse -living, deceased, disabled, or divorceddisabled, or divorced

May file even if deferring cash paymentsMay file even if deferring cash payments

Paying the Part B PremiumPaying the Part B Premium

Deducted from SS benefits - Deducted from SS benefits - alwaysalways

Monthly/Quarterly billing if not entitled to Monthly/Quarterly billing if not entitled to benefits or benefits less than premiumbenefits or benefits less than premium

- Pay by check or credit card- Pay by check or credit card

- Medicare - Medicare EasyEasy PayPay Monthly Direct DebitMonthly Direct Debit

- Request by calling 1 800 Medicare- Request by calling 1 800 Medicare

Medicare ResourcesMedicare Resources

1-800-Medicare 1-800-Medicare

www.medicare.govwww.medicare.gov

Ohio Senior Health Insurance Ohio Senior Health Insurance Information Program (OSHIIP) Information Program (OSHIIP)

1-800-686-1578 1-800-686-1578

www.insurance.ohio.govwww.insurance.ohio.gov

How to FileHow to FileVia the Internet at Via the Internet at www.socialsecurity.govwww.socialsecurity.gov

In the office or over the telephoneIn the office or over the telephone

For an appointment, call 1-800-772-1213For an appointment, call 1-800-772-1213

When to Contact Social SecurityWhen to Contact Social SecurityUp to 3 months before you retire or attain age 62Up to 3 months before you retire or attain age 62

If over age 62, review your work plans before If over age 62, review your work plans before Feb. 1 to determine when benefits could startFeb. 1 to determine when benefits could start

Filing for BenefitsFiling for Benefits

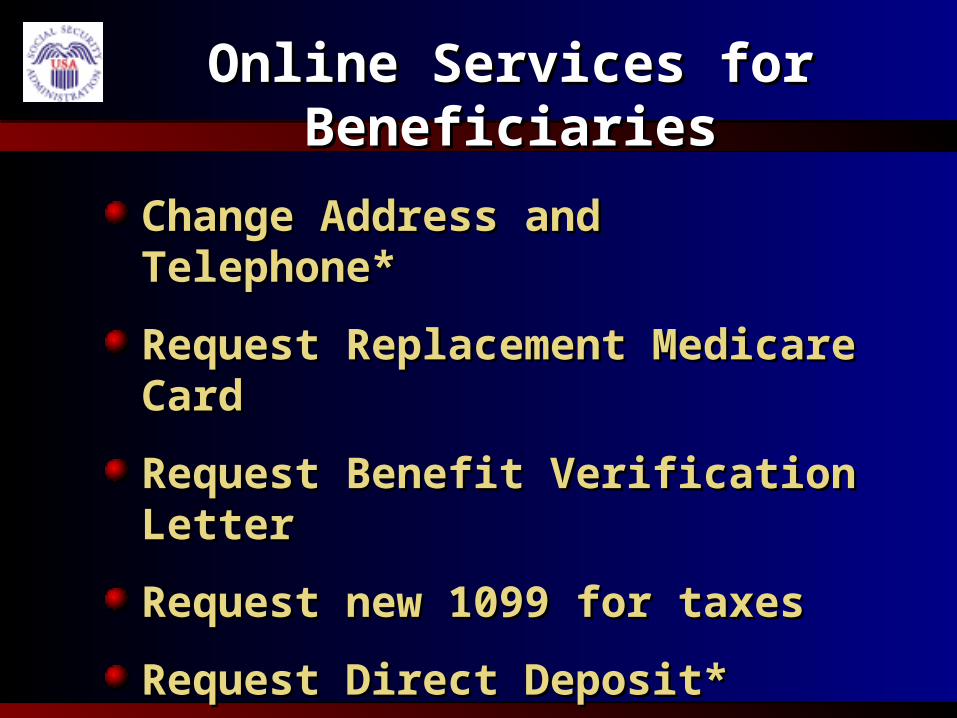

Online Services for BeneficiariesOnline Services for Beneficiaries

Change Address and Telephone* Change Address and Telephone*

Request Replacement Medicare CardRequest Replacement Medicare Card

Request Benefit Verification LetterRequest Benefit Verification Letter

Request new 1099 for taxesRequest new 1099 for taxes

Request Direct Deposit*Request Direct Deposit*

*Request Password*Request Password

Government Employees

34

Thank You !Thank You !