Embed Size (px)

Citation preview

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 1 of 76

SNOWDONIA NATIONAL PARK AUTHORITY

STATEMENT OF ACCOUNTS

FOR THE YEAR ENDED 31ST MARCH 2016

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 2 of 76

SNOWDONIA NATIONAL PARK AUTHORITY

STATEMENT OF ACCOUNTS 2015/16

INDEX

Page(s)

Narrative Report 3-8

Statement of Responsibilities for the Statement of Accounts 9

Statement of Accounting Policies 10-19

The Accounting Statements:

- Comprehensive Income and Expenditure Statement 20-21

- Balance Sheet 22

- Movement in Reserves Statement 23-24

- Cash Flow Statement 25

Notes to the Accounts 26-59

Auditor’s Report 60-61

Annual Governance Statement 62-75

Glossary 76

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 3 of 76

NARRATIVE REPORT

1. INTRODUCTION

The narrative report provides a brief explanation of the more significant matters reported in the accounts and aims to add to and assist the interpretation of the accounting statements which are set out on pages 20 to 25 and consist of :-

The Comprehensive Income and Expenditure Statement consolidates all the gains and losses experienced by the Authority during the financial year. These gains and losses should reconcile to the overall movement in net worth.

The Balance Sheet setting out the financial position of the Authority as at 31st March 2016.

The Movement in Reserves Statement is a summary of the changes that have taken place in the bottom half of the balance sheet over the financial year.

The Cash Flow Statement which summarises the inflows and outflows of cash arising from transactions for revenue and capital purposes.

The accounts are supported by the Statement of Accounting Policies and explanatory

notes.

2. ESTABLISHMENT OF SNOWDONIA NATIONAL PARK AUTHORITY

Under the provision of Section 63 of the Environment Act 1995 and The National Park Authorities (Wales) Order 1995 the Secretary of State established the Snowdonia National Park Authority on 23rd November 1995

It has the following purposes as defined by the Act:

To conserve and enhance the natural beauty , wildlife and cultural heritage, and

To promote opportunities for the understanding and enjoyment of the special qualities of the (National) Park by the public.

The Authority has responsibility for planning, conservation, countryside management, access and recreation. Services such as schools, highways, social services and other Local Authority duties are carried out by the local Unitary Authority. The Act goes on to say that in pursuing National Park purposes, the National Park shall seek to foster the economic and social well being of local communities within its boundaries, and shall for that purpose co-operate with local Authorities and public bodies whose functions include the promotion of economic and social development within the area of the Park. The Authority is a local planning Authority under the Environment Act 1995 for the whole of the National Park, and is responsible for the production of the Local Development Plan and for the determination of planning applications.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 4 of 76

The National Park covers 2,139 square km of varied countryside including mountain, moorland, woodland and coast. About 25,702 (2011 census) people live in the National Park which receives an estimated 9.7 million visitor days each year.

Approximately 59% of the residents of the National Park are Welsh speaking. 3. APPROVED REVENUE EXPENDITURE

In determining the amount of the National Park Grant, the Welsh Government also

determines, in accordance with the National Park Authorities (Levies)(Wales) Regulations 1995 as amended, the minimum amount that can be raised by the National Park Authority for the financial year by way of levies to be borne by constituent Councils (billing authorities).

The Grant represents 75% of the total net revenue expenditure deemed appropriate by the Welsh Government for the National Park, while the remaining 25% is raised by way of the levies. A comparison of budgeted expenditure with the actual for 2015/16 is as follows:

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 5 of 76

2015/16 REVENUE ACCOUNT

`

Revised

Budget

2015/2016

Actual

2015/2016 Variance

£ £ £

Conservation and Natural Environment 638,278 579,399 58,879

Conservation and Cultural Heritage 576,618 467,452 109,166

Understanding 1,581,561 1,491,097 90,464Recreation Management & Traffic and

Transport 472,212 314,608 157,604

Wardens, Estate Workers and Volunteers 1,274,236 1,223,193 51,043

Development Control 611,399 529,695 81,704

Forward Planning and Communities 721,955 622,524 99,431

Corporate & Democratic 674,682 619,082 55,600

Non Distributable Cost 16,000 16,000 -

NET COST OF SERVICES 6,566,941 5,863,050 703,891

Gains & losses on disposals - 44,073

Interest Earned - 17,067Net interest (Pensions adjustment) 286,000Capital grants and contributions - 578,364

NET OPERATING EXPENDITURE 5,509,546

Items debited/credited to the Authority Fund Balance - 239,600

5,269,946

FUNDED FROM

National Park Grant - 3,952,460

Levies to Constituent Councils - 1,317,486

- 5,269,946

4. REVENUE EXPENDITURE 2015/16 The Authority’s net expenditure is arrived at after deducting from gross

expenditure fees and charges, service specific grants and making other various deductions as detailed in the Income and Expenditure Account on pages 20-21.

The variance on the 2015/16 Revenue Account of £703,891 corresponds to the variance on service budget lines before transfers to/from reserves of £710,406 as reported in the “Revenue & Capital Outturn Report 2015/16” to the Authority on the 8 June 2016. The difference of -£6,515 consists of -£9,636 (removal of income on disposals to “Gains & losses on disposals”), +£12,745 (adjustment to Plas Tan y Bwlch income) and -£9,624 (accrual for redundancy cost).

5. SUSTAINABLE DEVELOPMENT FUND Following the change in the Welsh Government settlement arrangements, the

Authority stipulated that for 2015/16, £157,000 of the National Park Grant be ring fenced to directly support partnership projects that develop and test ways of achieving a more sustainable way of living in Snowdonia. During the year expenditure from the

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 6 of 76

grant-aided scheme, locally promoted as the Cronfa Arbrofol Eryri, was £124,354. (2014/15: £169,438).

6. MATERIAL ASSETS ACQUIRED AND LIABILITIES INCURRED

Assets acquired in 2015/16 were vehicles for the Planning and Land Management directorate, and items relating to the annual I.T. replacement programme. No material liabilities were incurred during the 2015/16 financial year other than the capital commitment referred to in note 11 to the Financial Statements.

7. PENSION LIABILITY Snowdonia National Park Authority is a member of the Gwynedd Pension Fund. The

accounts fully incorporate the requirements of International Accounting Standard 19 (IAS 19).

The policy reflects the commitment in the long-term to increase contributions to make

up any shortfall in attributable net assets in the pension fund. The net pension liability in the balance sheet reduces the net worth of the Authority

by £5.753m as at 31 of March 2016.

According to the Gwynedd Pension Fund’s Actuary the decrease of £3.097m in the pension liability is because of the increase in real bond yield rates. The bond rate is the discount rate used to calculate the present value of the pension benefits which will be paid in the future. If these rates fall in subsequent years the liability will increase.

8. UNUSUAL CHARGE OR CREDIT IN THE ACCOUNTS

The main credit of significance in the 2015/16 accounts relates to the decrease in pension liability as identified in note 7 above. There is a net capital receipt of £74,440 resulting from the sale of land at Aberangell.

9. CHANGE IN ACCOUNTING POLICIES The only significant change in accounting policy is that surplus assets are now valued at fair (market) value.

10. CHANGE IN STATUTORY FUNCTIONS

There have been no changes in statutory functions during 2015-16.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 7 of 76

11. CAPITAL EXPENDITURE 2015/16

Capital expenditure is expenditure on the acquisition of a fixed asset or expenditure which adds to and not merely maintains the value of the existing fixed asset.

Capital expenditure in the year amounted to £901k. Details of expenditure within each service area are shown in note 36. The expenditure was financed by grants and contributions from other bodies (£564k) and direct revenue financing (£337k).

All planned capital expenditure will be funded from revenue, external grants and reserves held for one off spends.

The main scheme in which the Authority was involved as at 31/3/2016 was the development of the Ysgwrn property currently estimated at a cost of circa £3.1m

12. CAPITAL FUNDING

All capital expenditure of the Authority, since being established on 23rd November 1995, has been funded by capital grants and contributions from the Government, European Community and other sources of grants, from capital receipts applied and from the Authority’s revenue resources. As at 31 March 2016 the Authority had no outstanding debts, and as such will continue to be regarded for treasury management purposes a debt-free authority.

13. SIGNIFICANT PROVISIONS / CONTINGENCIES AND MATERIAL WRITE OFFS

The General Revenue Reserve target of £400,000 was reviewed and confirmed by the Authority in the meeting on 9 December 2015. The Authority has specific Usable Reserves totalling £2,832k and these are detailed in note 21 to the financial statements.

14. REVALUATION OF ASSETS

One revaluation of a surplus asset was required during 2015/16.

15. MATERIAL EVENTS AFTER THE REPORTING DATE

The contract value for the main contractor on the Ysgwrn scheme (part 2) was reduced by £150k.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 8 of 76

16. CHANGE IN CLASSIFICATION IN THE COMPREHENSIVE INCOME AND EXPENDITURE

STATEMENT

The lines relevant to the Ysgwrn have been moved from “Conservation and Natural Environment” to “Conservation and Cultural Heritage” on the basis of appropriateness.

17. IMPACT OF THE CURRENT ECONOMIC CLIMATE

The Authority has balanced its budget for 2016/17 with an £18k contribution from reserves to “bridge” consistent with the recommendations approved in March 2016. Whilst measures have been considered to mitigate a further budget cut in 2017/18, it was decided to postpone any further implementation until better clarity is available following the May 2016 elections.

FURTHER INFORMATION Further information about this Statement of Account is available from:

Emyr Roberts Head of Finance Snowdonia National Park Authority National Park Offices Penrhyndeudraeth Gwynedd LL48 6LF Tel: 01766 772 225 Email: [email protected]

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 9 of 76

THE STATEMENT OF RESPONSIBILITIES FOR THE STATEMENT OF ACCOUNTS

THE AUTHORITY’S RESPONSIBILITIES The Authority is required to:-

Make arrangements for the proper administration of its financial affairs and to secure that one of its officers has the responsibility for the administration of those affairs. For Snowdonia National Park Authority, that officer is the Chief Finance Officer;

Manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets;

Approve the statement of accounts. These accounts were approved by the Authority on 28 September 2016

THE CHIEF FINANCE OFFICER’S RESPONSIBILITIES The Chief Finance Officer is responsible for the preparation of the Authority’s statement of accounts in accordance with proper practices as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom (the CODE). In preparing this Statement of Accounts, the Chief Finance Officer has:-

Selected suitable accounting policies and then applied them consistently; Made judgements and estimates that were reasonable and prudent; Complied with the local authority CODE.

The Chief Financial Officer has also:-

Kept proper accounting records which were up to date; Taken reasonable steps for the prevention and detection of fraud and other

irregularities.

CHIEF FINANCE OFFICER’S CERTIFICATE

I certify that the Statement of Accounts has been prepared in accordance with the Local Government Accounts and Audit Regulations and gives a true and fair view of the financial position of the Authority at the accounting date and its income and expenditure for the year ended 31 March 2016. Signature 16 September 2016 DAFYDD L. EDWARDS - CHIEF FINANCE OFFICER

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 10 of 76

STATEMENT OF ACCOUNTING POLICIES

1. General Principles The accounts have been prepared in accordance with the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom (the CODE). The Code of Practice requires accounting policies to be applied consistently. The overriding requirement is that the Statement of Accounts “present a true and fair view” of the financial performance and position of the Authority.

2. Accounting Concepts The accounts have been prepared in accordance with the following fundamental (and pervasive) accounting principles and concepts:

Going concern

Relevance

Faithful representation

Comparability

Understandable

Materiality

Accruals

Primacy of legislative requirement These principles and concepts have been used in the selection and application of accounting policies and estimation techniques and in the exercise of professional judgement.

3. Accruals of Expenditure and Income The revenue and capital accounts of the Authority are maintained on an accruals basis. All sums due to the Authority are set up in the accounts at the time they are due.

The Debtors appearing in the balance sheet are the balances of those sums outstanding at 31st March 2016. Creditors are the amounts which are charged in the accounts for goods and services consumed or received, for which invoices had not been paid at 31st March 2016.

4. Acquired operations

No such items are applicable to the 2015/16 accounts

5. Cash and Cash Equivalents These consist of the Authority’s imprest and float accounts and cash held on “call” or short term deposit with banks where the monies are repayable without penalty on notice of not more than 24 hours.

6. Exceptional Items No such items are applicable to the 2015/16 accounts

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 11 of 76

7. Prior period adjustments, changes in accounting policies and estimates and errors

There are no relevant material adjustments or changes impacting on the 2015/16 accounts.

8. Charges to revenue for non-current assets Services, support services and trading accounts are debited with the following amounts to record the cost of holding fixed assets during the year:

depreciation attributable to the assets used by the relevant service.

revaluation and impairment losses on assets used by the service where there are no accumulated gains in the Revaluation Reserve against which the losses can be written off.

amortisation of intangible fixed assets attributable to the service. These sums are not chargeable against the Authority’s General Fund and as such are therefore reversed out through an adjusting transaction with the Capital Adjustment Account as shown in the Movement in Reserves Statement.

9. Discontinued Operations No such items are applicable to the 2015/16 accounts (other than closure of one Information Centre at Dolgellau).

10. Employee Benefits Benefits Payable During Employment : Short-term employee benefits are those due to be settled within 12 months of the year-end. They include such benefits as wages and salaries, paid annual leave and paid sick leave, bonuses and non-monetary benefits (eg cars) for current employees and are recognised as an expense for services in the year in which employees render service to the Authority. Termination Benefits : Termination benefits are amounts payable as a result of a decision by the Authority to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy and are charged on an accruals basis to the Non Distributed Costs line in the Comprehensive Income and Expenditure Statement when the Authority is demonstrably committed to the termination of the employment of an officer or group of officers or making an offer to encourage voluntary redundancy.

11. Events After the Balance Sheet Date Events after the Balance Sheet date are those events, both favourable and unfavourable, that occur between the end of the reporting period and the date when the Statement of Accounts is authorised for issue. Two types of events can be identified:

those that provide evidence of conditions that existed at the end of the reporting period – the Statement of Accounts is adjusted to reflect such events

those that are indicative of conditions that arose after the reporting period – the Statement of Accounts is not adjusted to reflect such events, but where a category of events would have a material effect, disclosure is

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 12 of 76

made in the notes of the nature of the events and their estimated financial effect.

Events taking place after the date of authorisation for issue are not reflected in the Statement of Accounts.

12. Financial Instruments Financial Liabilities The Authority is a debt-free Authority in that it has no borrowings. Financial Assets Financial assets are classified into two types:

loans and receivables – assets that have fixed or determinable payments but are not quoted in an active market. Such instruments relevant to the Authority are car loans made to employees (however the sums are deemed not to be material enough for inclusion).

available-for-sale assets – assets that have a quoted market price and/or do not have fixed or determinable payments. The Authority has one such asset.

13. Foreign Currency translation

Income and expenditure arising from any transactions denominated in a foreign currency is translated to £ sterling.

14. Government Grants and other Contributions Whether paid on account, by instalments or in arrears, government grants and third party contributions and donations are recognised as due to the Authority when there is reasonable assurance that:

the Authority will comply with the conditions attached to the payments, and

the grants or contributions will be received. Amounts recognised as due to the Authority are not credited to the Comprehensive Income and Expenditure Statement until conditions attached to the grant or contribution have been satisfied. Conditions are stipulations that specify that the future economic benefits or service potential embodied in the asset acquired using the grant or contribution are required to be consumed by the recipient as specified, or future economic benefits or service potential must be returned to the transferor. Monies advanced as grants and contributions for which conditions have not been satisfied are carried in the Balance Sheet as creditors. When conditions are satisfied, the grant or contribution is credited to the relevant service line (attributable revenue grants and contributions) or Taxation and Non-Specific Grant Income (non-ring fenced revenue grants and all capital grants) in the Comprehensive Income and Expenditure Statement. Where capital grants are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance in the Movement in Reserves Statement.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 13 of 76

Where the grant has yet to be used to finance capital expenditure, it is posted to the Capital Grants Unapplied reserve. Where it has been applied, it is posted to the Capital Adjustment Account. Amounts in the Capital Grants Unapplied reserve are transferred to the Capital Adjustment Account once they have been applied to fund capital expenditure.

15. Heritage Assets Heritage assets are those assets preserved in trust for future generations because of their cultural, environmental or historic associations i.e. they have historical, artistic, scientific, geophysical or environmental qualities. They are maintained by the Authority principally for their contribution to knowledge and culture, but are not utilised by the Authority in its normal course of business. Depreciation of heritage assets, where appropriate, is in line with the Authority’s general policy on depreciation.

16. Intangible Assets Purchased intangible assets in the form of software licences are accounted for as part of the Information Technology replacement programme, and are written off to revenue in line with depreciation charges.

17. Interests in Companies and Other Entities The Authority has an interest in a Limited Liability Partnership set up jointly by the 15 UK National Park Authorities for the purpose of generating income mainly from sponsorship.

18. Inventories and Long Term Contracts Stocks are brought into account at cost price for bar stocks, goods for resale and general provisions at Plas Tan y Bwlch, Study Centre, and for goods for resale at the Authority’s Information Centres. This is consistent with the policy adopted in previous years. Recommended practice requires stocks to be shown at the lower of actual cost or net realisable value but the difference in this case is not considered to be material.

19. Investment Property The Authority does not hold any such property.

20. Jointly controlled Property and Jointly Controlled Assets Following the end of the Snowdonia Uplands Footpaths Scheme, the assets acquired under that scheme are recorded in the accounts of Snowdonia National Park Authority but a proportion of these assets are in use by the National Trust. This was in lieu of the condition on the European grant funding awarded that the assets purchased are continued to be used by the partners in work related to that of the scheme. The condition has now lapsed and arrangements in place to formally transfer ownership of relevant assets to the National Trust.

21. Leases (Finance) As at 31/3/2016 the Authority has no finance lease arrangements.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 14 of 76

22. Leases (Operational) The Authority manages operating leases for:

Vehicles,

Photocopiers and snacks & drinks machines.

Land and buildings Lease payments are charged in full according to date payable on a straight line basis, ensuring an equal annual charge to service revenue accounts throughout the life of the lease. The Authority rents a number of properties in support of its services, and also receives rental income from a number of owned properties. The owned properties are held as fixed assets in the balance sheet. The lease income is accounted for on a straight line basis.

23. Overheads and Support Services

The costs of overheads and support services are charged to those that benefit from the supply or service in accordance with the costing principles of the CIPFA Best Value Accounting Code of Practice 2015/16 (BVACOP). The total absorption costing principle is used – the full cost of overheads and support services are shared between users in proportion to the benefits received, with the exception of:

Corporate and Democratic Core – costs relating to the Authority’s status as a multifunctional, democratic organisation.

Non Distributed Costs – past service costs relating to the Pension Fund. These two cost categories are defined in BVACOP and accounted for as separate headings in the Comprehensive Income and Expenditure Statement, as part of Net Expenditure on Continuing Services.

24. Property, Plant and Equipment Assets that have physical substance and are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes and that are expected to be used during more than one financial year are classified as Property, Plant and Equipment. Recognition: Expenditure on the acquisition, creation or enhancement of Property, Plant and Equipment is capitalised on an accruals basis, provided that it is probable that the future economic benefits or service potential associated with the item will flow to the Authority and the cost of the item can be measured reliably. Expenditure that maintains but does not add to an asset’s potential to deliver future economic benefits or service potential (ie repairs and maintenance) is charged as an expense when it is incurred. Measurement: Assets are initially measured at cost, comprising: the purchase price any costs attributable to bringing the asset to the location and condition

necessary for it to be capable of operating in the manner intended by management (the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located.)

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 15 of 76

The cost of assets acquired other than by purchase is deemed to be its fair value, unless the acquisition does not have commercial substance (i.e. it will not lead to a variation in the cash flows of the Authority). In the latter case, where an asset is acquired via an exchange, the cost of the acquisition is the carrying amount of the asset given up by the Authority. Where gains are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance to the Capital Adjustment Account in the Movement in Reserves Statement. Assets are then carried in the Balance Sheet using the following measurement bases:

infrastructure, community assets and assets under construction – depreciated historical cost where known

Non-operational assets (surplus assets) - measured at fair (market) value.

all other assets – service potential at existing use value (EUV), determined as the amount that would be paid for the asset in its existing use.

Where there is no market-based evidence of fair value or existing use value because of the specialist nature of an asset, depreciated replacement cost (DRC) is used as an estimate of the value.

Where non-property assets that have short useful lives or low values (or both), depreciated historical cost basis is used as a proxy for fair value. Other than for information systems equipment, a de minimis level of £10,000 has been used for the recognition of non-current assets. Assets included in the Balance Sheet at fair value are revalued sufficiently regularly to ensure that their carrying amount is not materially different from their fair value at the year-end, but as a minimum every five years. Increases in valuations are matched by credits to the Revaluation Reserve to recognise unrealised gains. [Exceptionally, gains might be credited to the Comprehensive Income and Expenditure Statement where they arise from the reversal of a loss previously charged to a service.] Where decreases in value are identified, they are accounted for by: o where there is a balance of revaluation gains for the asset in the Revaluation

Reserve, the carrying amount of the asset is written down against that balance (up to the amount of the accumulated gains)

o where there is no balance in the Revaluation Reserve or an insufficient balance, the carrying amount of the asset is written down against the relevant service line(s) in the Comprehensive Income and Expenditure Statement.

The Revaluation Reserve contains revaluation gains recognised since 1 April 2007 only, the date of its formal implementation. Gains arising before that date have been consolidated into the Capital Adjustment Account.

Componentisation :The Authority has applied the componentisation principle to those assets valued at £150,000 or over and where the difference in depreciation cost is identified as being material. This principle is applied in order that those elements of a property that have different operational lives and thereby differing rates of depreciation are recognised and accounted for.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 16 of 76

Impairment: Assets are assessed at each year-end as to whether there is any indication that an asset may be impaired. Where indications exist and any possible differences are estimated to be material, the recoverable amount of the asset is estimated and, where this is less than the carrying amount of the asset, an impairment loss is recognised for the shortfall. Where impairment losses are identified, they are accounted for by:

where there is a balance of revaluation gains for the asset in the Revaluation Reserve, the carrying amount of the asset is written down against that balance (up to the amount of the accumulated gains)

where there is no balance in the Revaluation Reserve or an insufficient balance, the carrying amount of the asset is written down against the relevant service line(s) in the Comprehensive Income and Expenditure Statement.

Where an impairment loss is reversed subsequently, the reversal is credited to the relevant service line(s) in the Comprehensive Income and Expenditure Statement, up to the amount of the original loss, adjusted for depreciation that would have been charged if the loss had not been recognised. Depreciation: Depreciation is provided for on all Property, Plant and Equipment assets by the systematic allocation of their depreciable amounts over their useful lives. An exception is made for assets without a determinable finite useful life (i.e. freehold land and certain Community Assets) and assets that are not yet available for use (i.e. assets under construction). Neither investment assets nor assets held for sale are depreciated. Deprecation is calculated on the following bases:

buildings – straight-line allocation over the useful life of the property as estimated by the valuer

vehicles, plant, furniture and equipment – a percentage of the value of each class of assets in the Balance Sheet, as advised by a suitably qualified officer

Where an item of Property, Plant and Equipment asset has major components whose cost is significant in relation to the total cost of the item, the components are depreciated separately. Revaluation gains are also depreciated, with an amount equal to the difference between current value depreciation charged on assets and the depreciation that would have been chargeable based on their historical cost being transferred each year from the Revaluation Reserve to the Capital Adjustment Account. Disposals and Non-current Assets Held for Sale When it becomes probable that the carrying amount of an asset will be recovered principally through a sale transaction rather than through its continuing use, it is reclassified as an Asset Held for Sale. The asset is revalued immediately before reclassification and then carried at the lower of this amount and fair value less costs to sell. Where there is a subsequent decrease to fair value less costs to sell, the loss is posted to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement. Gains in fair value are recognised only up to the amount of any previously losses recognised in the Surplus or Deficit on Provision of Services.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 17 of 76

If assets no longer meet the criteria to be classified as Assets Held for Sale, they are reclassified back to non-current assets and valued at the lower of their carrying amount before they were classified as held for sale; adjusted for depreciation, amortisation or revaluations that would have been recognised had they not been classified as Held for Sale, and their recoverable amount at the date of the decision not to sell. Assets that are to be abandoned or scrapped are not reclassified as Assets Held for Sale. When an asset is disposed of or decommissioned, the carrying amount of the asset in the Balance Sheet (whether Property, Plant and Equipment or Assets Held for Sale) is written off to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement as part of the gain or loss on disposal. Receipts from disposals (if any) are credited to the same line in the Comprehensive Income and Expenditure Statement also as part of the gain or loss on disposal (i.e. netted off against the carrying value of the asset at the time of disposal). Any revaluation gains accumulated for the asset in the Revaluation Reserve are transferred to the Capital Adjustment Account. Amounts received for a disposal in excess of £10,000 are categorised as capital receipts. The balance of receipts is required to be credited to the Capital Receipts Reserve, and can then only be used for new capital investment [or set aside to reduce the Authority’s underlying need to borrow (the capital financing requirement)]. Receipts are appropriated to the Reserve from the General Fund Balance in the Movement in Reserves Statement. The written-off value of disposals is not a charge against the General Fund. These amounts are appropriated to the Capital Adjustment Account from the General Fund Balance in the Movement in Reserves Statement.

25. Provisions, contingent liabilities and contingent assets Provisions are made where an event has taken place that gives the Authority a legal or constructive obligation that probably requires settlement by a transfer of economic benefits or service potential, and a reliable estimate can be made of the amount of the obligation. For instance, the Authority may be involved in a court case that could eventually result in the making of a settlement or the payment of compensation. Provisions Provisions are charged as an expense to the appropriate service line in the Comprehensive Income and Expenditure Statement in the year that the Authority becomes aware of the obligation, and are measured at the best estimate at the balance sheet date of the expenditure required to settle the obligation, taking into account relevant risks and uncertainties.

Contingent Liabilities A contingent liability arises where an event has taken place that gives the Authority a possible obligation whose existence will only be confirmed by the

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 18 of 76

occurrence or otherwise of uncertain future events not wholly within the control of the authority. Contingent liabilities also arise in circumstances where a provision would otherwise be made but either it is not probable that an outflow of resources will be required or the amount of the obligation cannot be measured reliably. Contingent liabilities are not recognised in the Balance Sheet but disclosed in a note to the accounts. Contingent Assets A contingent asset arises where an event has taken place that gives the Authority a possible asset whose existence will only be confirmed by the occurrence or otherwise of uncertain future events not wholly within the control of the authority. Contingent assets are not recognised in the Balance Sheet but disclosed in a note to the accounts where it is probable that there will be an inflow of economic benefits or service potential.

26. Reserves The Authority sets aside specific amounts as reserves for future policy purposes or to cover contingencies. Reserves are created by appropriating amounts out of the General Fund Balance in the Movement in Reserves Statement. When expenditure to be financed from a reserve is incurred, it is charged to the appropriate service in that year to score against the Surplus or Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement. The reserve is then appropriated back into the General Fund Balance in the Movement in Reserves Statement so that there is no net charge against the General Fund for the expenditure. Certain reserves are kept to manage the accounting processes for non-current assets, financial instruments, retirement and employee benefits and do not represent usable resources for the Authority – these reserves are explained in the relevant policies.

27. Revenue Expenditure Funded From Capital Under Statute Expenditure incurred during the year that may be capitalised under statutory provisions but that does not result in the creation of a non-current asset has been charged as expenditure to the relevant service in the Comprehensive Income and Expenditure Statement in the year. Where the Authority has determined to meet the cost of this expenditure from existing capital resources or by borrowing, a transfer in the Movement in Reserves Statement from the General Fund Balance to the Capital Adjustment Account then reverses out the amounts charged so that there is no impact on the General Fund Balance.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 19 of 76

28. Value Added Tax VAT payable is included as an expense only to the extent that it is not recoverable from Her Majesty’s Revenue and Customs. VAT receivable is excluded from income. The Authority supplies :

Some services which are exempt of VAT (e.g. providing educational courses at Plas Tan y Bwlch, renting out land & buildings without opting to tax etc.,), and

Other goods and services which are not exempt of VAT (e.g. bar sales at Plas Tan y Bwlch, sale of trees etc.,)

The Authority, therefore, falls within the scope of VAT Partial Exemption regulations (including at present the capital goods scheme). As such the Authority is unable to recover all the input tax incurred. It is the Authority’s practice to include all input tax which cannot be recovered from H.M. Revenue and Customs within the costs of relevant services.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 20 of 76

THE COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT This statement shows the accounting cost in the year of providing services in accordance with generally accepted accounting practices.

2014/15

Gross

Expenditure

£'000

2014/15

Gross

Income

£'000

2014/15

Net

Expenditure

£'000

2015/16

Gross

Expenditure

£'000

2015/16

Gross

Income

£'000

2015/16

Net

Expenditure

£'000Conservation and Natural

Environment

214 - 5 209

Natural Environment and

Forestry 0 0 0

900 - 351 549

Conservation and

Agriculture 737 -158 579

1,114 -356 758 737 -158 579

Conservation and Cultural

Heritage

258 0 258 Built Environment 367 -29 338

266 -162 104 THI Dolgellau 0 0 0

95 -10 85 Archaeology 104 -12 92

19 -4 15 Ysgwrn 71 -8 63

13 -6 7 Ysgwrn (HLF scheme part1) 0 0 0

17 -19 -2 Ysgwrn (HLF scheme part2) 105 -132 -27

6 0 6 Bwrlwm Eryri 1 0 1

674 -201 473 648 -181 467

Understanding

1,346 -544 802 Study Centre 1,297 -673 624

509 -8 501 Information & Education 585 -28 557

433 -135 298 Information Centres 444 -134 310

2,288 - 687 1,601 2,326 - 835 1,491

Recreation Management &

Traffic and Transport

367 -133 234 Access 498 -36 462

266 -149 117 General Visitor Facilities 309 -147 162

0 0 0 Hafod Eryri 7 0 7

196 -483 -287 Car Parks 195 -502 -307

72 -57 15 Llyn Tegid Management 33 -55 -22

11 0 11 Litter Collection 13 0 13

2 0 2 Tourism Projects 0 0 0

914 - 822 92 1,055 - 740 315

4,990 -2,066 2,924 Net Cost of Service c/fd 4,766 -1,914 2,852

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 21 of 76

THE COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT (CONTINUED)

2014/15

Gross

Expenditure

£'000

2014/15

Gross

Income

£'000

2014/15

Net

Expenditure

£'000

2015/16

Gross

Expenditure

£'000

2015/16

Gross

Income

£'000

2015/16

Net

Expenditure

£'000

4,990 -2,066 2,924 Net Cost of Service b/fd 4,766 -1,914 2,852

Wardens, Estate Workers &

Volunteers

789 -3 786 Wardens (and volunteers) 860 -3 857

461 -36 425 Estate Workers 381 -15 366

1,250 - 39 1,211 1,241 - 18 1,223

697 - 206 491 Development Control 755 - 225 530

Forward Planning and

Communities

420 - 40 380 Strategic Plans and Policy 378 0 378

280 0 280

Community and Environment

(incl. CAE) 245 0 245

700 - 40 660 623 0 623

593 -3 590 Corporate & Democratic 622 -3 619

82 0 82 Non-distributable Costs 16 0 16

8,312 - 2,354 5,958 Net Cost of Service 8,023 - 2,160 5,863

-1

Other Operating Expenditure

(note 8) -44

224

Financing and Investment

Income and Expenditure

(note 9) 269

-5,505

Non-specific grant income

(note 10) -5,848

676

Surplus (-) / Deficit on

Provision of Services for

the year 240

-9

Net surplus on revaluation of

fixed assets and impairment

losses charged to the

revaluation reserve (note 22) 57

3,153

Actuarial gains / losses on

pension assets/liabilities

(note 44) -3,598

3,144

Other Comprehensive

Income and Expenditure -3,541

3,820

Total Comprehensive

Income and Expenditure -3,301

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 22 of 76

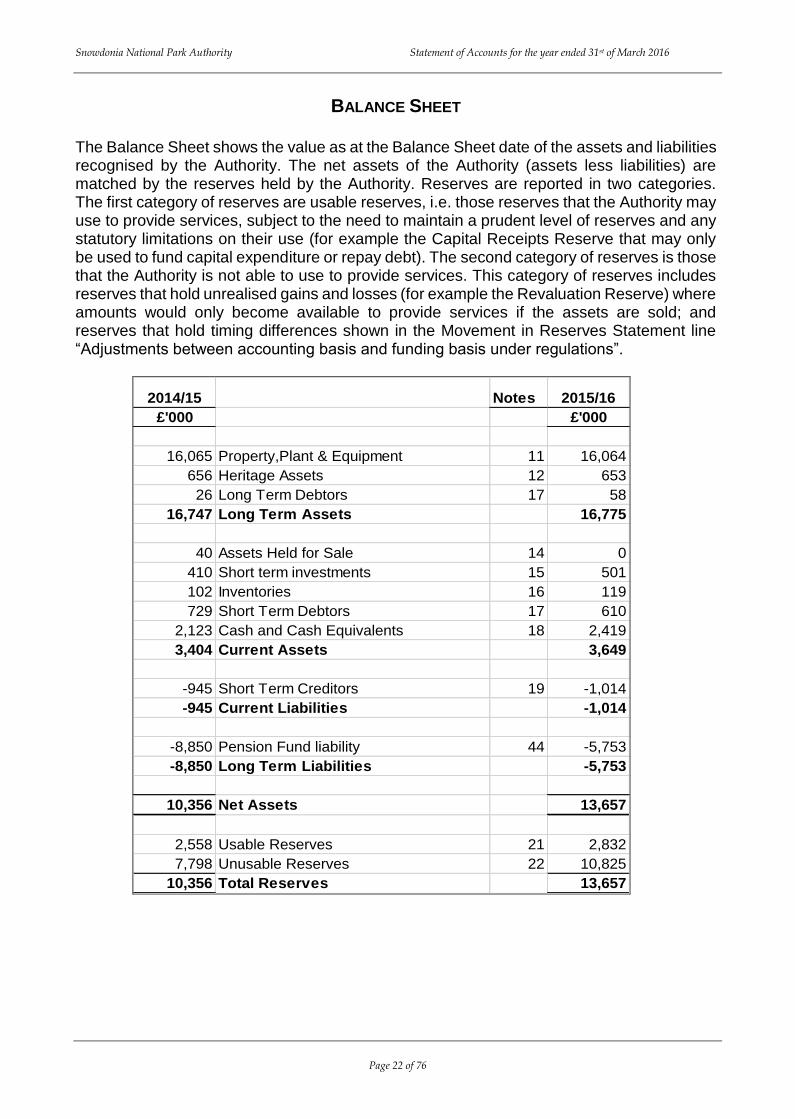

BALANCE SHEET The Balance Sheet shows the value as at the Balance Sheet date of the assets and liabilities recognised by the Authority. The net assets of the Authority (assets less liabilities) are matched by the reserves held by the Authority. Reserves are reported in two categories. The first category of reserves are usable reserves, i.e. those reserves that the Authority may use to provide services, subject to the need to maintain a prudent level of reserves and any statutory limitations on their use (for example the Capital Receipts Reserve that may only be used to fund capital expenditure or repay debt). The second category of reserves is those that the Authority is not able to use to provide services. This category of reserves includes reserves that hold unrealised gains and losses (for example the Revaluation Reserve) where amounts would only become available to provide services if the assets are sold; and reserves that hold timing differences shown in the Movement in Reserves Statement line “Adjustments between accounting basis and funding basis under regulations”.

2014/15 Notes 2015/16

£'000 £'000

16,065 Property,Plant & Equipment 11 16,064

656 Heritage Assets 12 653

26 Long Term Debtors 17 58

16,747 Long Term Assets 16,775

40 Assets Held for Sale 14 0

410 Short term investments 15 501

102 Inventories 16 119

729 Short Term Debtors 17 610

2,123 Cash and Cash Equivalents 18 2,419

3,404 Current Assets 3,649

-945 Short Term Creditors 19 -1,014

-945 Current Liabilities -1,014

-8,850 Pension Fund liability 44 -5,753

-8,850 Long Term Liabilities -5,753

10,356 Net Assets 13,657

2,558 Usable Reserves 21 2,832

7,798 Unusable Reserves 22 10,825

10,356 Total Reserves 13,657

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 23 of 76

THE MOVEMENT IN RESERVES STATEMENT This statement shows the movement in the year on the different reserves held by the Authority, analysed into “Usable reserves” (i.e. those that can be applied to fund expenditure) and other reserves. The Surplus (+) or Deficit (-) on the Provision of Services line shows the true economic cost of providing the Authority’s services, more details of which are shown in the Comprehensive Income and Expenditure Statement. These are different from the statutory amounts required to be charged to the General Fund Balance. The Net Increase/Decrease before Transfers to Earmarked Reserves line shows the statutory General Fund Balance before any discretionary transfers to or from earmarked reserves undertaken by the Authority.

Movement in Reserves

during 2014/15

Genera

l Fund

Bala

nce

Earm

ark

ed

Reserv

es

Capita

l

Receip

ts

Reserv

e

Capita

l Gra

nts

Unapplie

d

Reserv

e

To

tal U

su

ab

le

Reserv

es

Unusable

Reserv

es

To

tal

Au

tho

rity

Reserv

es

£'000 £'000 £'000 £'000 £'000 £'000 £'000

Balance as at 31 March

2014 brought forward 400 1,884 24 0 2,309 11,867 14,176

Surplus or (deficit) on the

provision of service -676 0 0 0 -676 0 -676

Other Comprehensive

Income and Expenditure 0 0 0 0 0 -3,144 -3,144

Total Comprehensive

Income and Expenditure -676 0 0 0 -676 -3,144 -3,820

Adjustments between

accounting basis &

funding basis under

regulations (note 6) 736 0 95 94 925 -925 0

Net Increase/Decrease

before transfers to

Earmarked Reserves 60 0 95 94 249 -4,069 -3,820

Transfers to/from

earmarked reserves (Note

7) -60 60 0 0 0 0 0

Increase / Decrease in

2014/15 0 60 95 94 249 -4,069 -3,820

Balance as at 31 March

2015 carried forward 400 1,944 119 94 2,558 7,798 10,356

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 24 of 76

MOVEMENT IN RESERVES STATEMENT (CONTINUED)

Movement in Reserves

during 2015/16

Genera

l F

und

Bala

nce

Earm

ark

ed

Reserv

es

Capital

Receip

ts

Reserv

e

Capital G

rants

Unapplie

d

Reserv

e

To

tal U

su

ab

le

Reserv

es

Unusable

Reserv

es

To

tal

Au

tho

rity

Reserv

es

£'000 £'000 £'000 £'000 £'000 £'000 £'000

Balance as at 31 March

2015 brought forward 400 1,944 119 94 2,558 7,798 10,356

Surplus or (deficit) on the

provision of service -240 0 0 0 -240 0 -240

Other Comprehensive

Income and Expenditure 0 0 0 0 0 3,541 3,541

Total Comprehensive

Income and Expenditure -240 0 0 0 -240 3,541 3,301

Adjustments between

accounting basis & funding

basis under regulations

(note 6) 423 0 75 16 514 -514 0

Net Increase/Decrease

before transfers to

Earmarked Reserves 183 0 75 16 274 3,027 3,301

Transfers to/from

earmarked reserves (Note

7) -183 183 0 0 0 0 0

Increase / Decrease in

2015/16 0 183 75 16 274 3,027 3,301

Balance as at 31 March

2016 carried forward 400 2,127 194 110 2,832 10,825 13,657

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 25 of 76

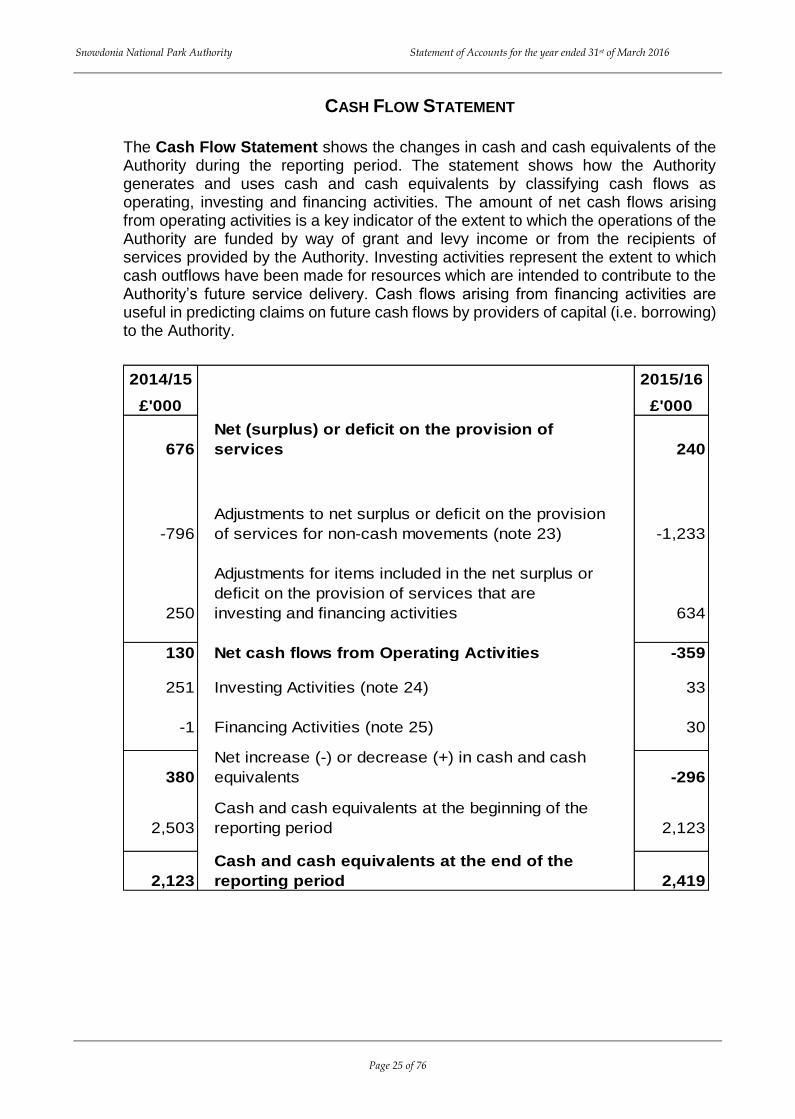

CASH FLOW STATEMENT

The Cash Flow Statement shows the changes in cash and cash equivalents of the Authority during the reporting period. The statement shows how the Authority generates and uses cash and cash equivalents by classifying cash flows as operating, investing and financing activities. The amount of net cash flows arising from operating activities is a key indicator of the extent to which the operations of the Authority are funded by way of grant and levy income or from the recipients of services provided by the Authority. Investing activities represent the extent to which cash outflows have been made for resources which are intended to contribute to the Authority’s future service delivery. Cash flows arising from financing activities are useful in predicting claims on future cash flows by providers of capital (i.e. borrowing) to the Authority.

2014/15 2015/16

£'000 £'000

676

Net (surplus) or deficit on the provision of

services 240

-796

Adjustments to net surplus or deficit on the provision

of services for non-cash movements (note 23) -1,233

250

Adjustments for items included in the net surplus or

deficit on the provision of services that are

investing and financing activities 634

130 Net cash flows from Operating Activities -359

251 Investing Activities (note 24) 33

-1 Financing Activities (note 25) 30

380

Net increase (-) or decrease (+) in cash and cash

equivalents -296

2,503

Cash and cash equivalents at the beginning of the

reporting period 2,123

2,123

Cash and cash equivalents at the end of the

reporting period 2,419

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 26 of 76

NOTES TO THE FINANCIAL STATEMENTS

1. ACCOUNTING STANDARDS THAT HAVE BEEN ISSUED BUT HAVE NOT YET BEEN ADOPTED The Code of Practice on Local Authority Accounting in the United Kingdom (the Code) requires the disclosure of information relating to the expected impact of an accounting change that will be required by a new standard that has been issued but not yet adopted. This applies to the adoption of the following new or amended standards within the 2016/17 Code which could impact upon the Authority.

Amendments to IAS19 Employee Benefits (Defined Benefit Plans : Employee Contributions)

Annual Improvements to IFRSs 2010-2012

Amendment to IFRS 11 Joint Arrangements (Accounting for Acquisitions of Interests in Joint operations)

Amendment to IAS16 Property, Plant & Equipment and IAS 38 Intangible Assets Annual Improvements to IFRSs 2012-2014

Amendment to IAS1 Presentation of Financial Statements (Disclosure Initiative)

The Changes to the format of the Comprehensive Income and Expenditure Statement, the Movement in Reserves Statement and the Introduction of the New Expenditure and Funding Analysis

The Changes to the format of the Pension Fund Account and the Net Assets Statement.

The Code does not anticipate that the above amendments will have a material impact on the information provided in local authority financial statements i.e. there is unlikely to be a change in reported information in the reported net cost of services or the Surplus or Deficit on the Provision of Services. However, in the 2016/17 year the comparator 2015/16 Comprehensive Income and Expenditure Statement and the Movement in Reserves Statement must reflect the new formats and reporting requirements as a result of the Telling the Story review of the presentation of local authority financial statements.

2. CRITICAL JUDGEMENTS IN APPLYING ACCOUNTING POLICIES None, other than disclosed elsewhere in these notes.

3. ASSUMPTIONS MADE ABOUT THE FUTURE AND OTHER MAJOR SOURCES OF ESTIMATION

UNCERTAINTY

The Statement of Accounts contains estimated figures that are based on assumptions made by the Authority about the future or that are otherwise uncertain. Estimates are made taking into account historical experience, current trends and other relevant factors. However, because balances cannot be determined with certainty, actual results could be materially different from the assumptions and estimates.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 27 of 76

Those assumptions made by the Actuary relating to the pension fund are disclosed in note 44.

4. MATERIAL ITEMS OF INCOME AND EXPENSE There is an decrease of £3.097m in the pension liability due to the change in financial assumptions (further detail in note 44).

5. EVENTS AFTER THE BALANCE SHEET DATE

The only event of note relevant to the 2015/16 accounts is that the value of the contract with the main contractor on the Ysgwrn (part 2) scheme has been reduced by £150k.

6. ADJUSTMENTS BETWEEN ACCOUNTING BASIS AND FUNDING BASIS UNDER REGULATIONS

This note details the adjustments that are made in the total comprehensive income and expenditure recognised by the Authority in the year in accordance with proper accounting practice to the resources that are specified by statutory provisions as being available to the Authority to meet future capital and revenue expenditure.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 28 of 76

Gen

era

l F

un

d

Bala

nce

Earm

ark

ed

Reserv

es

Cap

ital

Receip

ts

Reserv

es

Cap

ital

Gra

nts

Un

ap

pli

ed

Reserv

e

Mo

vem

en

t in

Un

usab

le

Reserv

es

£'0

00

£'0

00

£'0

00

£'0

00

£'0

00

ADJUSTMENTS PRIMARILY INVOLVING THE CAPITAL ADJUSTMENT ACCOUNT

Reversal of items debited or credited to the

Comprehensive Income and Expenditure

Statement

Charges for depreciation, impairment and

revaluation losses on non-current assets 524 0 0 0 -524

Capital grants and contributions applied -30 0 0 0 30

Revenue Expenditure funded from capital under

statute 184 0 0 0 -184Amounts of non-current assets written off on

disposal or sale as part of the gain/loss on disposal

to the Comprehensive Income and Expenditure

Statement 210 0 0 0 -210

Insertion of items not debited or credited to the

Comprehensive Income and Expenditure

Statement

Capital expenditure charges against the General

Fund -167 0 0 0 167

ADJUSTMENT PRIMARILY INVOLVING THE CAPITAL GRANTS UNAPPLIED ACCOUNT

Capital Grants and Contributions Unapplied credited

to the Comprehensive Income and Expenditure

Statement -94 94 0

ADJUSTMENT PRIMARILY INVOLVING THE CAPITAL RECEIPTS RESERVE

Transfer of cash sale proceeds credited as part of

the gain/loss on disposal to the CIES -205 205 0

Use of the Capital Receipts reserve to finance new

capital expenditure 0 0 -110 0 110

ADJUSTMENTS PRIMARILY INVOLVING THE PENSION RESERVE

Reversal of items relating to retirement benefits

debited or credited to the Comprehensive Income

and Expenditure Statement 1069 0 0 0 -1069

Employers Pension contributions and direct

payments to pensioners payable in the year. -756 0 0 0 756

ADJUSTMENT PRIMARILY INVOLVING THE ACCUMULATED ABSENCES ACCOUNT

Amount by which officer remuneration charged to

the Comprehensive Income and Expenditure

Statement on an accruals basis is different from

remuneration chargeable in the year in accordance

with statutory requirements 1 0 0 0 -1

TOTAL ADJUSTMENTS 736 0 95 94 -925

Usable Reserves

2014/15

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 29 of 76

Gen

era

l F

un

d

Bala

nce

Earm

ark

ed

Reserv

es

Cap

ital

Receip

ts

Reserv

es

Cap

ital

Gra

nts

Un

ap

pli

ed

Reserv

e

Mo

vem

en

t in

Un

usab

le

Reserv

es

£'0

00

£'0

00

£'0

00

£'0

00

£'0

00

ADJUSTMENTS PRIMARILY INVOLVING THE CAPITAL ADJUSTMENT ACCOUNT

Reversal of items debited or credited to the

Comprehensive Income and Expenditure

Statement

Charges for depreciation, impairment and

revaluation losses on non-current assets 491 0 0 0 -491

Capital grants and contributions applied -468 0 0 0 468

Revenue Expenditure funded from capital under

statute 346 0 0 0 -346Amounts of non-current assets written off on

disposal or sale as part of the gain/loss on disposal

to the Comprehensive Income and Expenditure

Statement 49 0 0 0 -49

Insertion of items not debited or credited to the

Comprehensive Income and Expenditure

Statement

Capital grant received in 2014/15 and used in

2015/16 -94 94

Capital expenditure charges against the General

Fund -337 0 0 0 337

ADJUSTMENT PRIMARILY INVOLVING THE CAPITAL GRANTS UNAPPLIED ACCOUNT

Capital Grants and Contributions Unapplied credited

to the Comprehensive Income and Expenditure

Statement -110 110 0

ADJUSTMENT PRIMARILY INVOLVING THE CAPITAL RECEIPTS RESERVE

Transfer of cash sale proceeds credited as part of

the gain/loss on disposal to the CIES -75 75 0

ADJUSTMENTS PRIMARILY INVOLVING THE PENSION RESERVE

Reversal of items relating to retirement benefits

debited or credited to the Comprehensive Income

and Expenditure Statement 1205 0 0 0 -1205

Employers Pension contributions and direct

payments to pensioners payable in the year. -704 0 0 0 704

ADJUSTMENT PRIMARILY INVOLVING THE ACCUMULATED ABSENCES ACCOUNT

Amount by which officer remuneration charged to

the Comprehensive Income and Expenditure

Statement on an accruals basis is different from

remuneration chargeable in the year in accordance

with statutory requirements 26 0 0 0 -26

TOTAL ADJUSTMENTS 423 0 75 16 -514

Usable Reserves

2015/16

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 30 of 76

7. TRANSFERS TO/FROM EARMARKED RESERVES

Bala

nce a

t

31 M

arc

h

2015

Tra

nsfe

rs o

ut

2015/1

6

Tra

nsfe

rs in

2015/1

6

Bala

nce a

t

31 M

arc

h

2016

£'000 £'000 £'000 £'000

Earmarked reserve 359 -359 516 516

Specific Risks reserve 401 -122 114 393

Capital projects reserve 168 -35 0 133

Self-Insurance reserve 13 -13 0 0

Planning reserve 200 0 0 200

Match funding reserve 450 -76 45 419

Match funding reserve (NRW) 9 0 0 9

Revenue Grants reserve 9 0 68 77

Bequest reserve 30 0 0 30

Pen y Pass Income reserve 126 0 5 131

Section 106 reserve 115 0 40 155

Car Park income reserve 28 0 0 28

Green Key reserve 36 0 0 36

1,944 -605 788 2,127

8. OTHER OPERATING EXPENDITURE

2014/15 2015/16

£’000 £’000

-1 Gains/losses on disposal of non-current assets

-44

9. FINANCING AND INVESTMENT INCOME AND EXPENDITURE

2014/15 2015/16

£’000 £’000

233 Net interest on the net defined benefit liability (asset)

286

-14 Interest receivable and similar income -17

5 Disposal costs on Porth Gwyn 0

224 Total 269

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 31 of 76

10. NON-SPECIFIC GRANT INCOME

2014/15 2015/16

£’000 £’000

-4,110 National Park Grant -3,952

-1,365 Levies on Constituent Authorities

-1,318

-30 Capital Grants and Contributions

-578

-5,505 Total -5,848

11. PROPERTY PLANT AND EQUIPMENT

Movement on Balances

2014/15

La

nd

an

d

Bu

ild

ing

s

Ve

hic

les,

Pla

nt

& E

qu

ipm

en

t

Co

mm

un

ity

Su

rplu

s A

sse

ts

Ass

ets

un

de

r

Co

nst

ruct

ion

To

tal

£'000 £'000 £'000 £'000 £'000 £'000

Cost or valuation

At 1 April 2014 17,309 1,794 142 67 0 19,312

Additions 48 75 0 0 0 123

Disposals 0 -42 0 0 0 -42Revaluation to CIES 0 0 0 1 0 1Revaluation to Rev.

Reserve 0 0 0 39 0 39Other movements 0 -53 0 -40 0 -93

At 31 March 2015 17,357 1,774 142 67 0 19,340`

Accumulated Depreciation and Impairments

At 1 April 2014 -1,359 -1,424 -34 -1 0 -2,818

Depreciation Charge -365 -130 0 0 0 -495

Derecognition - Disposals 0 42 0 0 0 42Other movements in

Depreciation and

Impairment 0 44 0 0 0 44write back on revaluation

- to revaluation reserve -30 0 0 0 0 -30- to surplus/deficit on

provision of services -18 0 0 0 0 -18

At 31 March 2015 -1,772 -1,468 -34 -1 0 -3,275

Net BookValue at March

2015 15,585 306 108 66 0 16,065

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 32 of 76

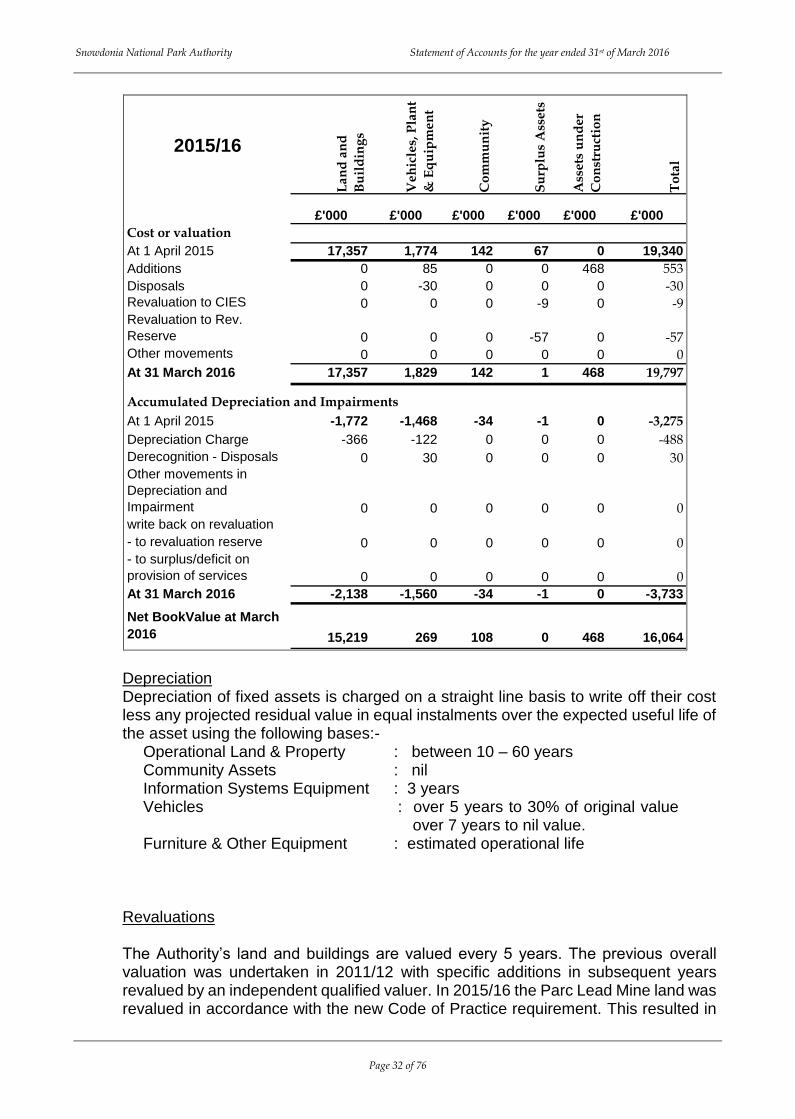

2015/16

La

nd

an

d

Bu

ild

ing

s

Ve

hic

les,

Pla

nt

& E

qu

ipm

en

t

Co

mm

un

ity

Su

rplu

s A

sse

ts

Ass

ets

un

de

r

Co

nst

ruct

ion

To

tal

£'000 £'000 £'000 £'000 £'000 £'000

Cost or valuation

At 1 April 2015 17,357 1,774 142 67 0 19,340

Additions 0 85 0 0 468 553

Disposals 0 -30 0 0 0 -30Revaluation to CIES 0 0 0 -9 0 -9Revaluation to Rev.

Reserve 0 0 0 -57 0 -57Other movements 0 0 0 0 0 0

At 31 March 2016 17,357 1,829 142 1 468 19,797`

Accumulated Depreciation and Impairments

At 1 April 2015 -1,772 -1,468 -34 -1 0 -3,275

Depreciation Charge -366 -122 0 0 0 -488

Derecognition - Disposals 0 30 0 0 0 30Other movements in

Depreciation and

Impairment 0 0 0 0 0 0write back on revaluation

- to revaluation reserve 0 0 0 0 0 0- to surplus/deficit on

provision of services 0 0 0 0 0 0

At 31 March 2016 -2,138 -1,560 -34 -1 0 -3,733

Net BookValue at March

2016 15,219 269 108 0 468 16,064

Depreciation Depreciation of fixed assets is charged on a straight line basis to write off their cost less any projected residual value in equal instalments over the expected useful life of the asset using the following bases:- Operational Land & Property : between 10 – 60 years Community Assets : nil Information Systems Equipment : 3 years Vehicles : over 5 years to 30% of original value

over 7 years to nil value. Furniture & Other Equipment : estimated operational life

Revaluations

The Authority’s land and buildings are valued every 5 years. The previous overall valuation was undertaken in 2011/12 with specific additions in subsequent years revalued by an independent qualified valuer. In 2015/16 the Parc Lead Mine land was revalued in accordance with the new Code of Practice requirement. This resulted in

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 33 of 76

deleting a book value of £66,500, with £9,250 of that cost going to Visitor Facilities and £57,250 showing against “Net deficit on revaluation of fixed assets and impairment losses charged to the revaluation reserve” in the Comprehensive Income and Expenditure Statement. The Authority has the following capital commitments on tendered contracts as at 31/3/2016 budgeted to cost £1,813k (corresponding commitments at 31/3/2015 were worth £377k) :

Management Fee re Ysgwrn HLF scheme £146k Main contractor on Phase I works – Ysgwrn HLF scheme £302k

(including retention of £8,454) Main contractor on Phase 2 works – Ysgwrn HLF scheme £1,366k

(There was a reduction in the value of £150k on the contract with the main contractor on phase 2 works of the Ysgwrn scheme after 31/3/16 to come to the figure £1,366k)

12. HERITAGE ASSETS The Authority’s classification of tangible heritage assets relates to :

Ynys y Pandy Slate Mill - a listed building with no operational use, and removed from the land and buildings valuation in 2011/12 due to being below the de-minimis level.

Craig Yr Aderyn - a Site of Special Scientific Interest and retained for its environmental qualities.

Yr Ysgwrn - home of the poet Hedd Wyn having been purchased to protect its cultural heritage. (Although there has been building work on the site during 2015/16, no building has been demolished and none completed by 31/3/2016).

All Heritage Assets have been valued at existing use value.

There have been no revaluations during 2015/16.

Ynys y Pandy

Slate Mill

Craig yr

Aderyn Ysgwrn Total

(£'000) (£'000) (£'000) (£'000)

Cost or valuation

31 March 2014 0 13 646 659

Depreciation charge 0 0 -3 -3

31 March 2015 0 13 643 656

Depreciation charge 0 0 -3 -3

31 March 2016 0 13 640 653

13. INTANGIBLE FIXED ASSETS

Purchased intangible assets in the form of software licences are accounted for as part of the Information Technology replacement programme, and are written off to revenue in line with depreciation charges. The value of these intangible assets is

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 34 of 76

deemed such that a disclosure separate from Vehicles, Plant and Equipment is unwarranted.

14. ASSETS HELD FOR SALE

As at 31/3/2016 there are no assets held for sale. (On 31/3/2015 Aberangell amenity site was held for sale).

15. SHORT TERM INVESTMENTS

As at 31/3/2016 all of the Authority’s deposits are repayable on demand and without loss of interest apart from £501k on a 95 day deposit with Santander UK. (£410k as at 31/3/2015).

16. INVENTORIES Stocks are brought into account at cost price. Stocks held on 31st March 2016

consisted of :-

Inform.

Centres Access Access Admin. Total

Goods for

resale

Snowdon

Maps Bar

Goods

for

resale

Catering

&

Cleaning

Stones &

heli-bags

Protective

Clothing

£'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000

Balance as at

31/3/2015 64 0 4 2 4 23 5 102

Purchases 87 12 12 9 88 0 9 217

Recognised as

an expense in

the year -72 -4 -13 -2 -89 -10 -10 -200

Balance as at

31/3/2016 79 8 3 9 3 13 4 119

Plas Tan y Bwlch

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 35 of 76

17. DEBTORS

2014/15 2015/16

£'000 £'000

Amounts falling due within one year :413 Central Government Bodies 289

16 Other local authorities 402 Public corporations & trading funds 0

298 Other entities and individuals 281729 610

LONG TERM DEBTORS (amounts falling due after one year)

26 Car Loans to Employees 5826 58

18. CASH AND CASH EQUIVALENTS The balance of Cash and Cash Equivalents is made up of the following elements :

31 March 2015

31 March 2016

£’000 £’000

8 Cash held by the Authority 12

893 Bank current accounts 652

1,222 Short-term deposits with banks 1,755

2,123 Total Cash and Cash Equivalents 2,419

19. CREDITORS

2014/15 2015/16

£'000 £'000

-108 Central Govt. Bodies -99

-145 Other local authorities -155

-692 Other entities & individuals -760

-945 -1,014 20. PROVISIONS

The Authority has no such items as at 31/3/2016.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 36 of 76

21. USABLE RESERVES Movements in the Authority’s usable reserves are as noted in the Movement in Reserves Statement.

2014/15 2015/16

£'000 £'000

Revenue

359

Earmarked Revenue & Capital reserves

(Amount approved as earmarked revenue and

capital expenditure)

516

401 Specific Risks Reserve (to meet probable

budget pressures )393

168 Capital projects reserve (to fund one -off capital

committments)133

200 Planning Reserve

(To meet costs of Public Inquiry)200

450 Match Funding Revenue Reserve

(For Convergence Fund Purposes)419

9 Match Funding Reserve - NRW

(For Convergence Fund purposes)9

13 Insurance Reserve

(To meet self-insured liabilities)0

115 Section 106 Reserve 155

30 Bequest 30

126 Pen y Pass Income Reserve 131

28 Car Park Income Reserve 28

36 Green Key Reserve 36

9 Revenue grants (rec'd in advance) Reserve 77

1944 2127

400 General reserve 400

2,344 2,527

Capital

94 Capital Grants Unapplied 110

120 Usable Capital Receipts Reserves : 195

2,558 2,832

22. UNUSABLE RESERVES

2014/15 2015/16

£'000 £'000

7,943 Revaluation Reserve 7,713

8,826 Capital Adjustments Account 9,012

-8,850 Pensions Reserve -5,753

-121 Accumulated Absences Account -147

7,798 10,825

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 37 of 76

THE REVALUATION RESERVE

The Revaluation Reserve contains the gains made by the Authority arising from increases in the value of its Property, Plant and Equipment (and Intangible Assets). The balance is reduced when assets with accumulated gains are:

Revalued downwards or impaired and the gains are lost,

Used in the provision of services and the gains are consumed through depreciation, or

Disposed of and the gains are realised The reserve contains only revaluation gains accumulated since 1 April 2007, the date that the Reserve was created. Accumulated gains arising before that date are consolidated into the balance on the Capital Adjustment Account.

2014/15 2015/16

£'000 £'000

8,080 Balance at 1st April 7,943

39 Upward revaluation of assets 0

-30

Downward revaluation of assets and

impairment losses not charged to the

Surplus / Deficit on the Provision of

Services

-57

9 Surplus or deficit on revaluation of non-

current assets not posted to the

Surplus or Deficit on the Provision of

Services

-57

-13 Revaluation losses written off to the

Capital Adjustment Account

-39

-133 Depreciation on revaluation gains

written off to the Capital Adjustment

-134

7,943 Balance at 31st March 7,713

CAPITAL ADJUSTMENT ACCOUNT

The Capital Adjustment Account absorbs the timing differences arising from the different arrangements for accounting for the consumption of non-current assets and for financing the acquisition, construction or enhancement of those assets under statutory provisions. The Account is debited with the cost of acquisition, construction or enhancement as depreciation, impairment losses and amortisations are charged to the Comprehensive Income and Expenditure Statement (with reconciling postings from the Revaluation Reserve to convert fair value figures to a historical cost basis). The Account is credited with the amounts set aside by the Authority as finance for the costs of acquisition, construction and enhancement. The Account contains accumulated gains and losses on Investment Properties and gains recognised on donated assets that have yet to be consumed by the Authority.

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 38 of 76

The Account also contains revaluation gains accumulated on Property, Plant and Equipment before 1 April 2007, the date that the Revaluation reserve was created to hold such gains. Note 6 provides details of the source of all the transactions posted to the Account, apart from those involving the Revaluation reserve.

2014/15 2015/16

£'000 £'000

9,291 Balance at 1st April 8,826

Reversal of items relating to capital

expenditure debited or credited to the

Comprehensive Income and Expenditure

Statement :-515 Charges for depreciation and impairment of

non-current assets

-491

13 Revaluation gains / losses on Property, Plant

and Equipment

0

-184 Revenue Expenditure Funded from capital

under statute -346

-210 Amount of investment property value written

off on disposal 0

-9 Amounts of non-current assets written off on

disposal or sale as part of the gain/loss on

disposal to the Comprehensive Income and

Expenditure Statement

-49

8,386 7,940

Adjusting amounts written out of the

Revaluation Reserve

0 remaining value of Aberangell amenity land 39

133 Depreciation adjustment 134

8,519 Net written out amount of the cost of non-

current assets consumed in the year

8,113

Capital financing applied in the year :

110 Use of 2014/15 capital receipts to finance

new capital expenditure

0

30 Capital grants and contributions credited to

the Comprehensive Income and Expenditure

Statement that have been applied to capital

financing

468

0 Application of grants to capital financing from

the Capital Grants Unapplied Account

94

167 Capital expenditure charged against the

General Fund balances

337

8,826 Balance at 31st March 9,012

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 39 of 76

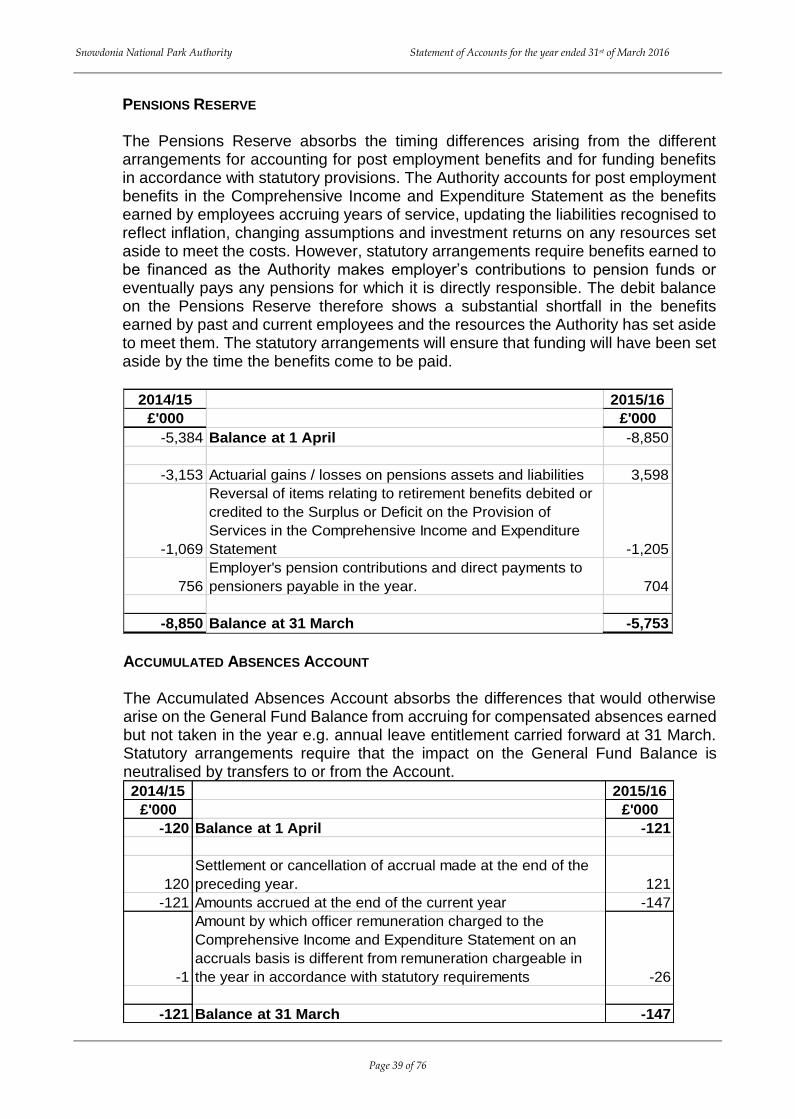

PENSIONS RESERVE

The Pensions Reserve absorbs the timing differences arising from the different arrangements for accounting for post employment benefits and for funding benefits in accordance with statutory provisions. The Authority accounts for post employment benefits in the Comprehensive Income and Expenditure Statement as the benefits earned by employees accruing years of service, updating the liabilities recognised to reflect inflation, changing assumptions and investment returns on any resources set aside to meet the costs. However, statutory arrangements require benefits earned to be financed as the Authority makes employer’s contributions to pension funds or eventually pays any pensions for which it is directly responsible. The debit balance on the Pensions Reserve therefore shows a substantial shortfall in the benefits earned by past and current employees and the resources the Authority has set aside to meet them. The statutory arrangements will ensure that funding will have been set aside by the time the benefits come to be paid.

2014/15 2015/16

£'000 £'000

-5,384 Balance at 1 April -8,850

-3,153 Actuarial gains / losses on pensions assets and liabilities 3,598

-1,069

Reversal of items relating to retirement benefits debited or

credited to the Surplus or Deficit on the Provision of

Services in the Comprehensive Income and Expenditure

Statement -1,205

756

Employer's pension contributions and direct payments to

pensioners payable in the year. 704

-8,850 Balance at 31 March -5,753 ACCUMULATED ABSENCES ACCOUNT

The Accumulated Absences Account absorbs the differences that would otherwise arise on the General Fund Balance from accruing for compensated absences earned but not taken in the year e.g. annual leave entitlement carried forward at 31 March. Statutory arrangements require that the impact on the General Fund Balance is neutralised by transfers to or from the Account.

2014/15 2015/16

£'000 £'000

-120 Balance at 1 April -121

120

Settlement or cancellation of accrual made at the end of the

preceding year. 121

-121 Amounts accrued at the end of the current year -147

-1

Amount by which officer remuneration charged to the

Comprehensive Income and Expenditure Statement on an

accruals basis is different from remuneration chargeable in

the year in accordance with statutory requirements -26

-121 Balance at 31 March -147

Snowdonia National Park Authority Statement of Accounts for the year ended 31st of March 2016

Page 40 of 76

23. CASH FLOW STATEMENT – OPERATING ACTIVITIES

The “adjustments to net surplus or deficit on the provision of services for non cash movements” comprises of :

2014/15 2015/16

£'000 £'000

-498 Depreciation -491

-18 Impairment 0

-218 Other movements related to asset values -49

305 Movement in creditors 2

1 Movement in short term investments 0

-65 Movement in debtors -211

10 Movement in stock 17

-313 Provision of Services costs for post employment benefits -501

-796 -1,233

The cash flows for operating activities includes bank interest received of £14k (£13k in 2014/15).

24. CASH FLOW STATEMENT – INVESTING ACTIVITIES

2014/15 2015/16

£'000 £'000

103

Purchase of property,plant and Equipment,

investment property and intangible assets 94

409

Purchase of short term and long term

investments 500

107 Other payments for investing activities 405

-220

Proceeds from the sale of property, plant and

equipment, investment property and intangible

assets -84

0

Proceeds from short term and long term