Embed Size (px)

Citation preview

Snowdon & Associates Inc.

Shifts in Income Sources and the Impact on Internal Resource Allocation Policies

CAUBO Conference “Adjusting the Sails”Halifax, June 21-24

Ken SnowdonHigher Education Consultant

Snowdon & Associates Inc.

Outline

Changing fiscal environment - revenue changes

Characteristics of revenue change and implications

Responses to the changing fiscal environment

Resource Allocation ModelsLessons…….

Snowdon & Associates Inc.

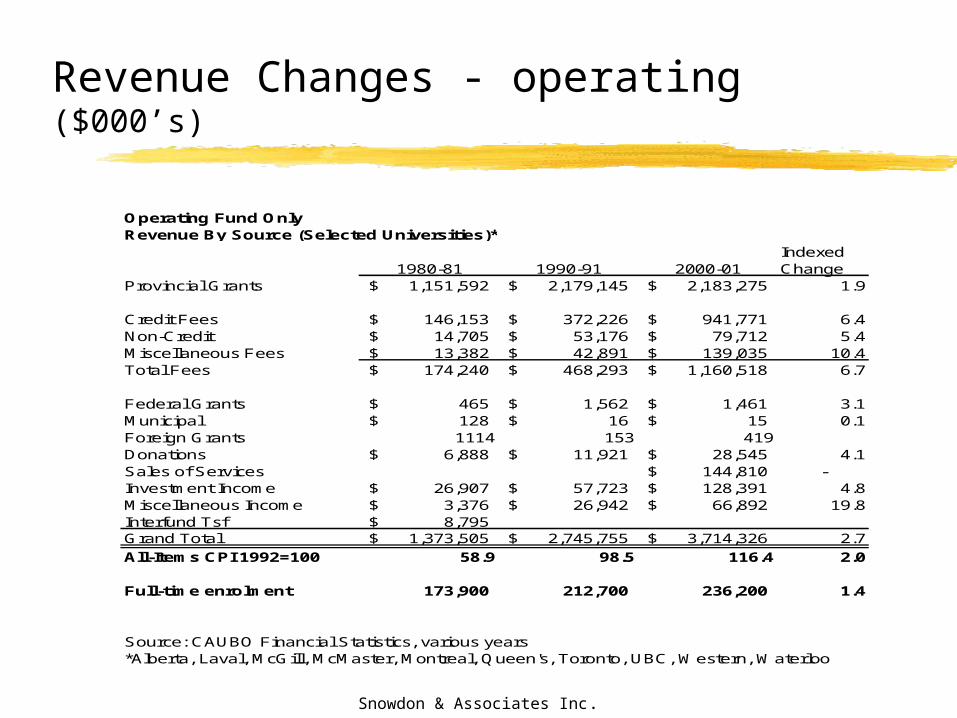

Revenue Changes - operating ($000’s)

Operating Fund OnlyRevenue By Source (Selected Universities)*

Indexed1980-81 1990-91 2000-01 Change

Provincial Grants 1,151,592$ 2,179,145$ 2,183,275$ 1.9

Credit Fees 146,153$ 372,226$ 941,771$ 6.4Non-Credit 14,705$ 53,176$ 79,712$ 5.4Miscellaneous Fees 13,382$ 42,891$ 139,035$ 10.4Total Fees 174,240$ 468,293$ 1,160,518$ 6.7

Federal Grants 465$ 1,562$ 1,461$ 3.1Municipal 128$ 16$ 15$ 0.1Foreign Grants 1114 153 419Donations 6,888$ 11,921$ 28,545$ 4.1Sales of Services 144,810$ -Investment Income 26,907$ 57,723$ 128,391$ 4.8Miscellaneous Income 3,376$ 26,942$ 66,892$ 19.8Interfund Tsf 8,795$ Grand Total 1,373,505$ 2,745,755$ 3,714,326$ 2.7

All-Items CPI 1992=100 58.9 98.5 116.4 2.0

Full-time enrolment 173,900 212,700 236,200 1.4

Source: CAUBO Financial Statistics, various years*Alberta, Laval, McGill, McMaster, Montreal, Queen's, Toronto, UBC, Western, Waterloo

Snowdon & Associates Inc.

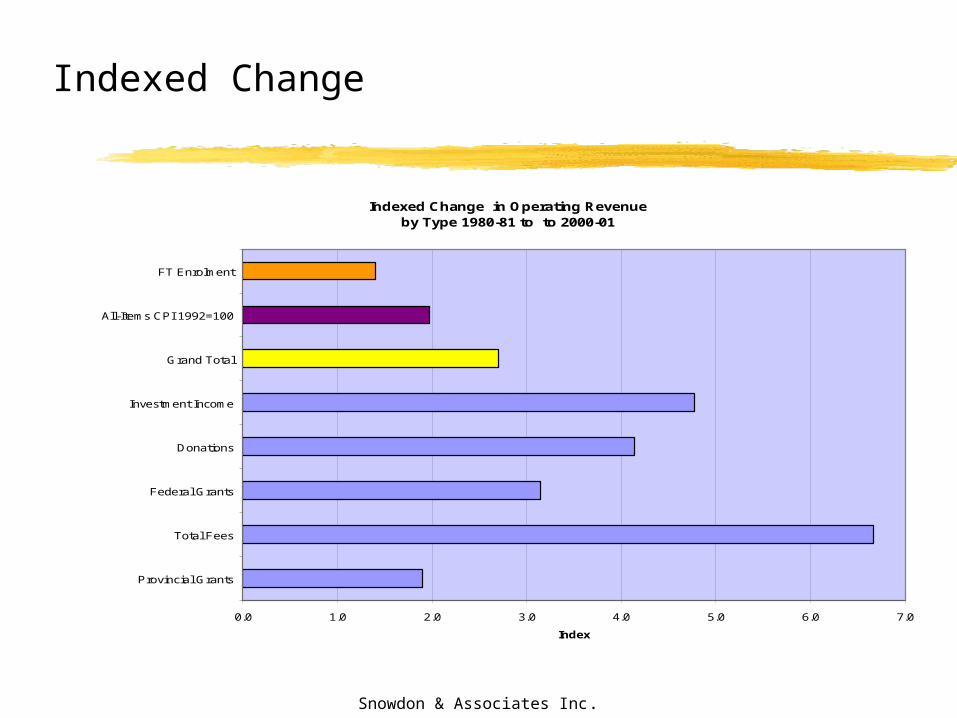

Indexed Change

Indexed Change in Operating Revenue by Type 1980-81 to to 2000-01

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

Provincial Grants

Total Fees

Federal Grants

Donations

Investment Income

Grand Total

All-Items CPI 1992=100

FT Enrolment

Index

Snowdon & Associates Inc.

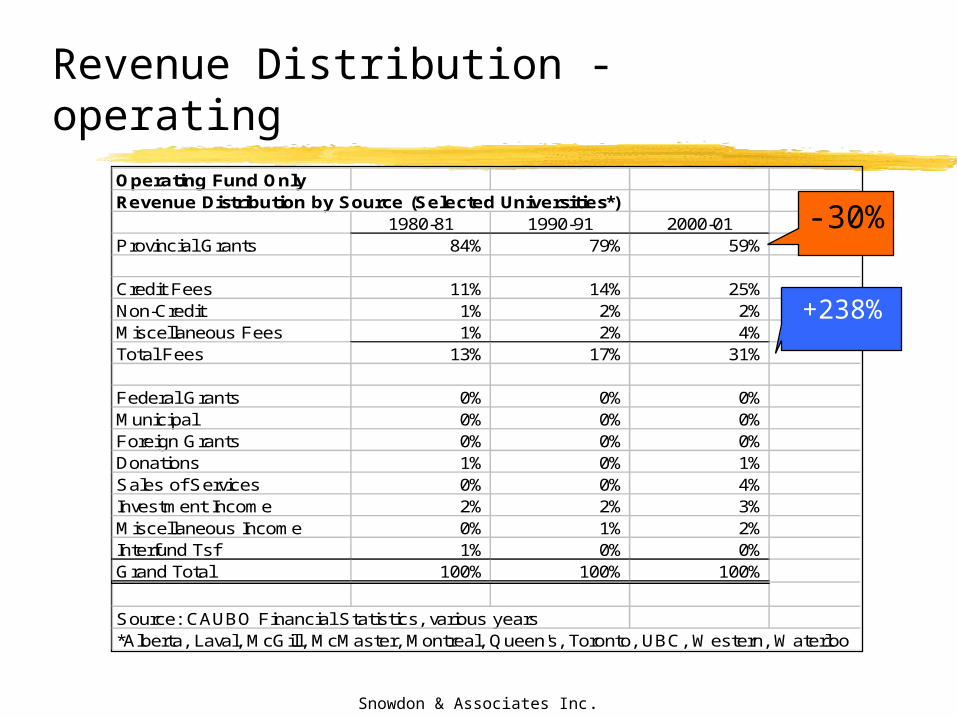

Revenue Distribution - operatingOperating Fund OnlyRevenue Distribution by Source (Selected Universities*)

1980-81 1990-91 2000-01Provincial Grants 84% 79% 59%

Credit Fees 11% 14% 25%Non-Credit 1% 2% 2%Miscellaneous Fees 1% 2% 4%Total Fees 13% 17% 31%

Federal Grants 0% 0% 0%Municipal 0% 0% 0%Foreign Grants 0% 0% 0%Donations 1% 0% 1%Sales of Services 0% 0% 4%Investment Income 2% 2% 3%Miscellaneous Income 0% 1% 2%Interfund Tsf 1% 0% 0%Grand Total 100% 100% 100%

Source: CAUBO Financial Statistics, various years*Alberta, Laval, McGill, McMaster, Montreal, Queen's, Toronto, UBC, Western, Waterloo

-30%

+238%

Snowdon & Associates Inc.

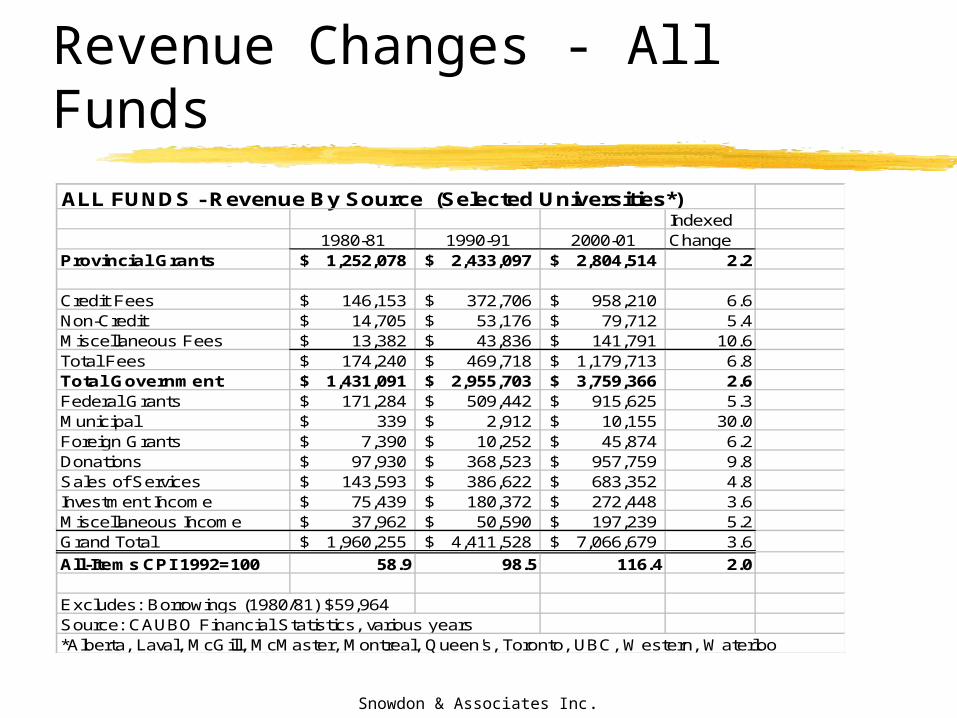

Revenue Changes - All FundsALL FUNDS - Revenue By Source (Selected Universities*)

Indexed1980-81 1990-91 2000-01 Change

Provincial Grants 1,252,078$ 2,433,097$ 2,804,514$ 2.2

Credit Fees 146,153$ 372,706$ 958,210$ 6.6Non-Credit 14,705$ 53,176$ 79,712$ 5.4Miscellaneous Fees 13,382$ 43,836$ 141,791$ 10.6Total Fees 174,240$ 469,718$ 1,179,713$ 6.8Total Government 1,431,091$ 2,955,703$ 3,759,366$ 2.6Federal Grants 171,284$ 509,442$ 915,625$ 5.3Municipal 339$ 2,912$ 10,155$ 30.0Foreign Grants 7,390$ 10,252$ 45,874$ 6.2Donations 97,930$ 368,523$ 957,759$ 9.8Sales of Services 143,593$ 386,622$ 683,352$ 4.8Investment Income 75,439$ 180,372$ 272,448$ 3.6Miscellaneous Income 37,962$ 50,590$ 197,239$ 5.2Grand Total 1,960,255$ 4,411,528$ 7,066,679$ 3.6

All-Items CPI 1992=100 58.9 98.5 116.4 2.0

Excludes: Borrowings (1980/81) $59,964Source: CAUBO Financial Statistics, various years*Alberta, Laval, McGill, McMaster, Montreal, Queen's, Toronto, UBC, Western, Waterloo

Snowdon & Associates Inc.

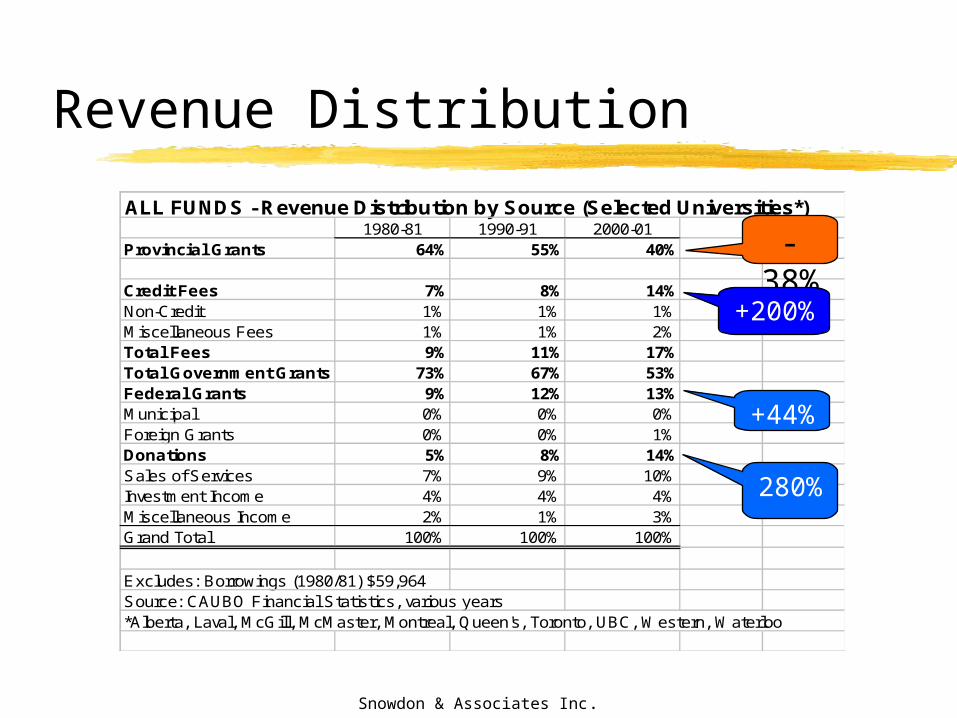

Revenue Distribution

ALL FUNDS - Revenue Distribution by Source (Selected Universities*)1980-81 1990-91 2000-01

Provincial Grants 64% 55% 40%

Credit Fees 7% 8% 14%Non-Credit 1% 1% 1%Miscellaneous Fees 1% 1% 2%Total Fees 9% 11% 17%Total Government Grants 73% 67% 53%Federal Grants 9% 12% 13%Municipal 0% 0% 0%Foreign Grants 0% 0% 1%Donations 5% 8% 14%Sales of Services 7% 9% 10%Investment Income 4% 4% 4%Miscellaneous Income 2% 1% 3%Grand Total 100% 100% 100%

Excludes: Borrowings (1980/81) $59,964Source: CAUBO Financial Statistics, various years*Alberta, Laval, McGill, McMaster, Montreal, Queen's, Toronto, UBC, Western, Waterloo

-38%

+200%

+44%

280%

Snowdon & Associates Inc.

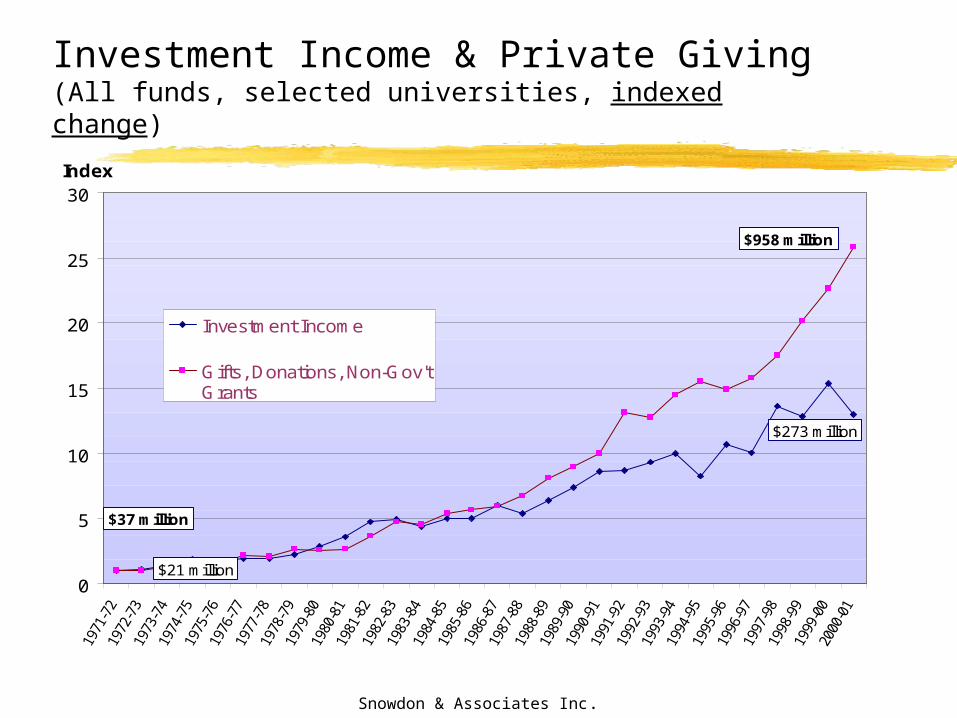

Investment Income & Private Giving (All funds, selected universities, indexed change)

0

5

10

15

20

25

30Index

Investment Income

Gifts, Donations, Non-Gov'tGrants

$273 million

$958 million

$37 million

$21 million

Snowdon & Associates Inc.

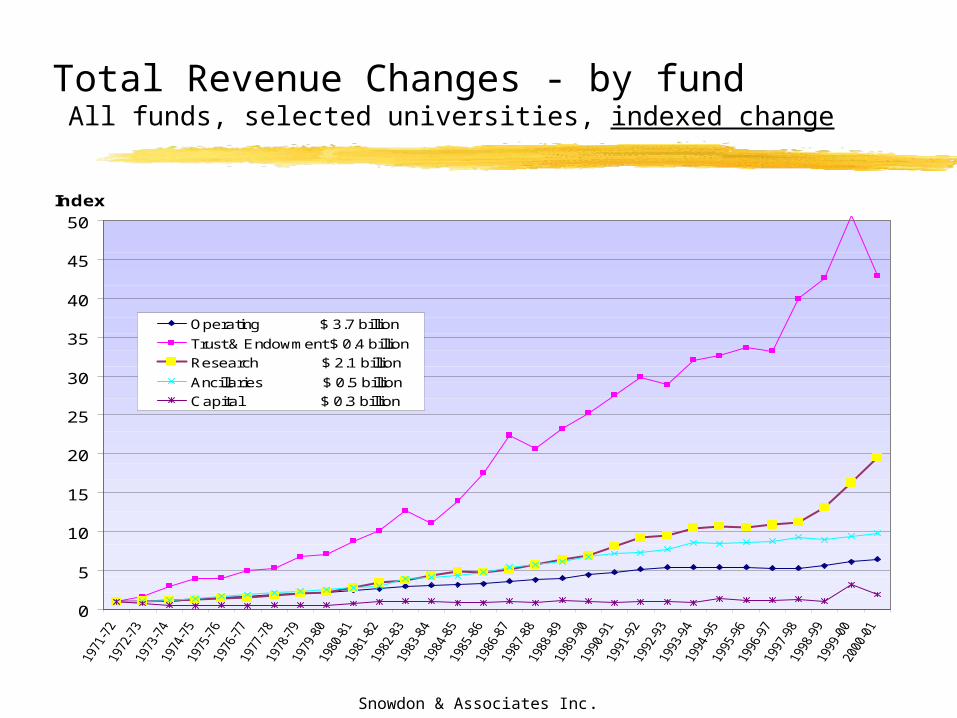

Total Revenue Changes - by fund All funds, selected universities, indexed change

0

5

10

15

20

25

30

35

40

45

50

Index

Operating $ 3.7 billion

Trust & Endowment $ 0.4 billion

Research $ 2.1 billion

Ancillaries $ 0.5 billion

Capital $ 0.3 billion

Snowdon & Associates Inc.

Characteristics of Funding Changes

External restrictions - earmarked funds Sometimes ‘matching’ requirements Workload - tuition policy, student assistance, research, private giving,

earmarked grants, preparing proposals, regulations, accountability, stewardship,….

Complexity - linking various sources of income Uneven in terms of campus impacts (ie. de-regulated fees,

research, private giving) Sometimes leads to costs in other areas - research (indirect costs),

capital (operating costs), subsidizaton of enrolment expansion in certain programs, student assistance with fee increases

Snowdon & Associates Inc.

Financial Planning Issues

Cash management / investment strategy trying to be ‘transparent’ with increasing complex array of

funding sources financial planning in a more complex environment recognizing ‘real costs’ of new ventures and opportunity costs internal resource allocation - budget subsidies and subsidization mechanisms links to academic planning, fund-raising, capital planning

Snowdon & Associates Inc.

Responding to a changing fiscal environment

Snowdon & Associates Inc.

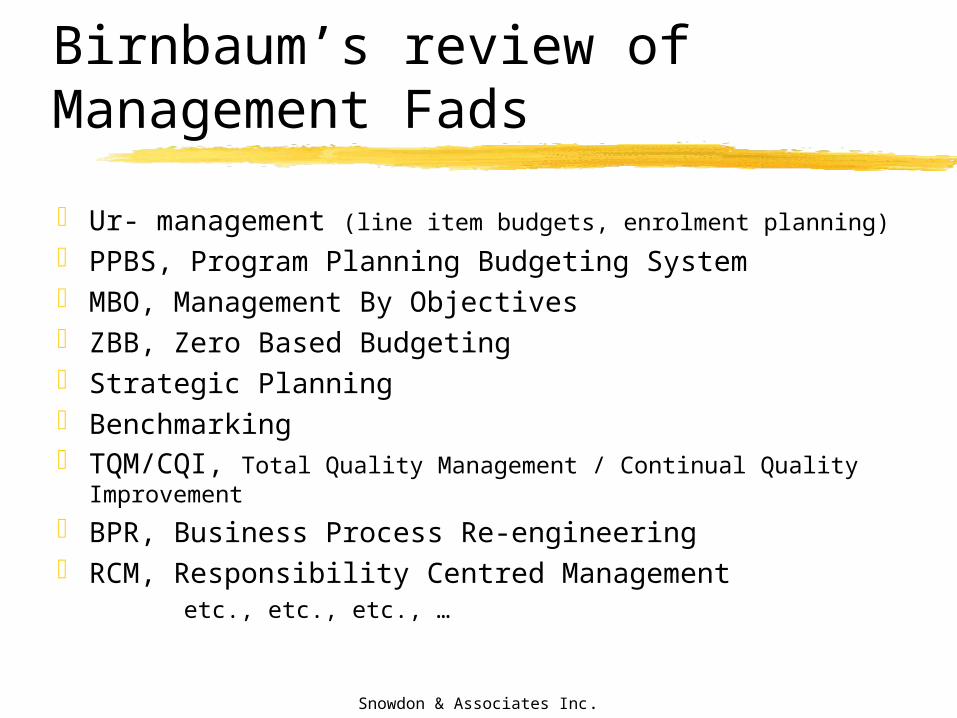

Birnbaum’s review of Management Fads

Ur- management (line item budgets, enrolment planning)

PPBS, Program Planning Budgeting System MBO, Management By Objectives ZBB, Zero Based Budgeting Strategic Planning Benchmarking TQM/CQI, Total Quality Management / Continual Quality Improvement

BPR, Business Process Re-engineering RCM, Responsibility Centred Management

etc., etc., etc., …

Snowdon & Associates Inc.

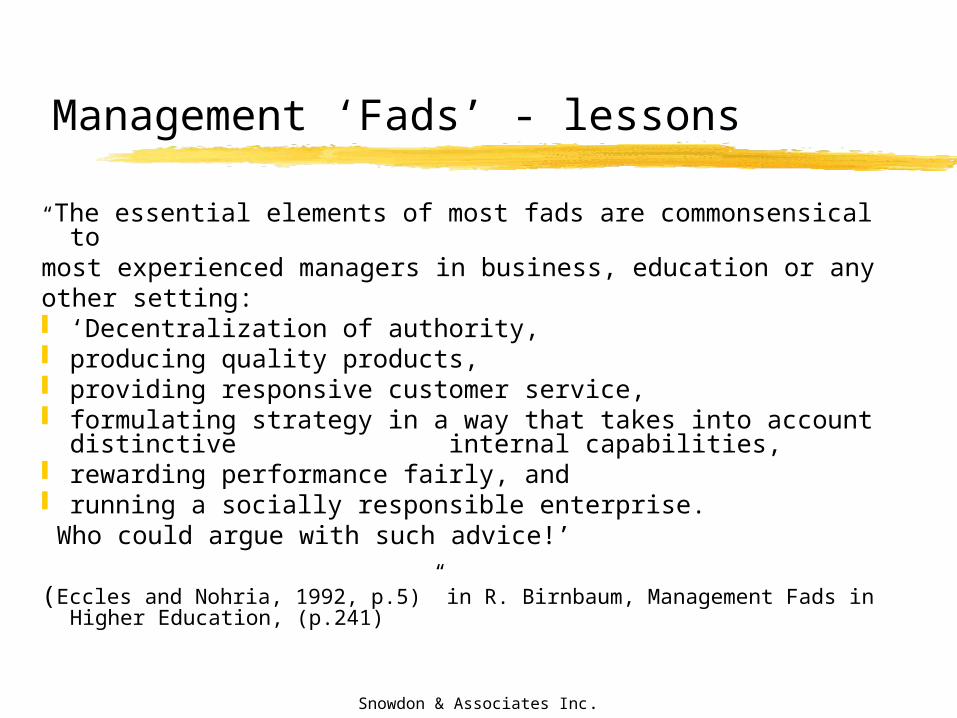

Management ‘Fads’ - lessons

“The essential elements of most fads are commonsensical to most experienced managers in business, education or any other setting: ‘Decentralization of authority, producing quality products, providing responsive customer service, formulating strategy in a way that takes into account distinctive

internal capabilities, rewarding performance fairly, and running a socially responsible enterprise. Who could argue with such advice!’

(Eccles and Nohria, 1992, p.5)” in R. Birnbaum, Management Fads in Higher Education, (p.241)

Snowdon & Associates Inc.

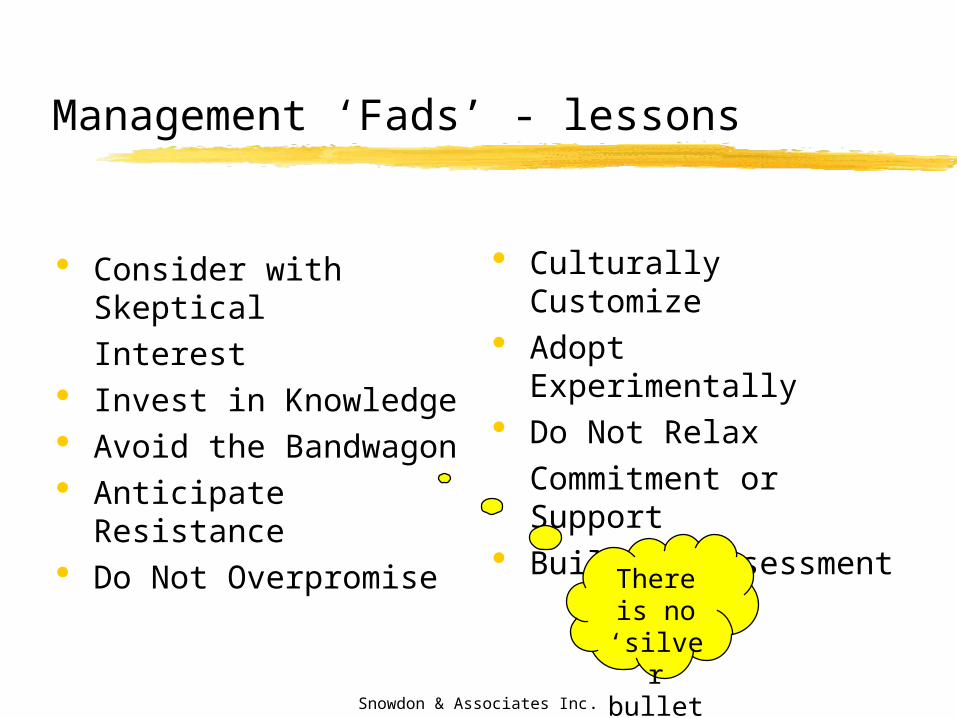

Management ‘Fads’ - lessons

Consider with Skeptical Interest

Invest in Knowledge Avoid the Bandwagon Anticipate Resistance Do Not Overpromise

Culturally Customize Adopt Experimentally Do Not Relax

Commitment or Support

Build in Assessment

There is no ‘silver

bullet’

Snowdon & Associates Inc.

Management ‘Fads’ - lessons

“Higher education does not need more management techniques. It needs more good managers.” (p.239)

Snowdon & Associates Inc.

Current issues in budget planning

incentives for management of fiscal resourcesdecentralized / centralizedcomprehensive (operating, capital, trust, vs.

operating only)definitions of ‘operating’multi-year (rolling budget, long-term budget)

vs. annual

Snowdon & Associates Inc.

U of T - Provost Review

people and organization structure philosophy - guiding principles role of Deans & Principals academic planning

budget, capital, advancement

Specific issues / policies Academic Priorities Fund (APF) multi-year financial plans revenue diversification

Snowdon & Associates Inc.

Specific allocation issues

Year-end balance carry-forward policies Sharing of ‘base’ revenue (and expense) Sharing of incremental revenue (and expense) Accounting for ALL costs (direct & indirect) Subsidies “Tax backs” Allocation of “tax backs”

flexibility funds, reinvestment funds, academic priority funds, innovation funds

Snowdon & Associates Inc.

Related issues…

“Haves and HaveNots” Funding Advancement/Development Faculty/Departmental Development Plans Accountability – reporting, stewardship of funds Complexity of budgeting

Multiple funding sources Processes

Institutional management of the funding ‘story’ Operating, capital, fund-raising, research

Snowdon & Associates Inc.

Summary

Major shifts in sources of revenue Changes in internal resource policies Greater reliance on decentralized approach Need for well developed Faculty / Institutional goals Retention of ‘institutional’ goals through central funds /

central direction the optimum approach changes over time depending on the

many factors influencing funding and institutional circumstances

Snowdon & Associates Inc.

Lessons…

There is No ‘silver bullet’….But, there some key characteristics of well developed

approaches Institutional Plan with objectives Multi-year fiscal plan Balance between ‘centralization vs. de-centralization’ Measurement indicators Public accountability