Embed Size (px)

Citation preview

Snohomish County Assessor’s Office

Gail S. Rauch

Snohomish County AssessorCindy S. Portmann - Chief Deputy Assessor

Chuck Sessler – Appraisal Manager

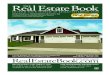

Legislative

Council*

Executive* Judicial

Courts & Judges*

Administrative

Assessor* Airport Human Resources

Auditor* BRB/BOE Human Services

Clerk* Corrections Information Services

Prosecutor* Facilities Medical Examiner

Sheriff* Finance Parks & Recreation

Treasurer* Hearing Examiner

Planning & Development Srvs

Public Works

Snohomish County Voters

What is the Assessor’s job?

• Washington State law requires that Assessors– Assess all real and personal property in the

county at 100% of true and fair market value in money, unless specifically exempted by law

– Fair market value or true value is the amount that a willing and unobligated buyer is willing to pay a willing and unobligated seller

Scope

• The listing of all taxable real and personal property within the geographic boundaries of Snohomish County are within the office’s jurisdiction, including property within incorporated cities.

Real Property

• Includes land, improvements to land, structures and certain equipment fixed to structures

• Assessor values property using one or more of the following methods– Market or sales comparison– Cost Approach– Income

Personal Property

• The primary characteristic of personal property is mobility

• Personal property includes furnishings, machinery and equipment, fixtures, supplies and tools

• Most personal property owned by individuals is specifically exempt.

• If these items are used in a business, personal property tax applies

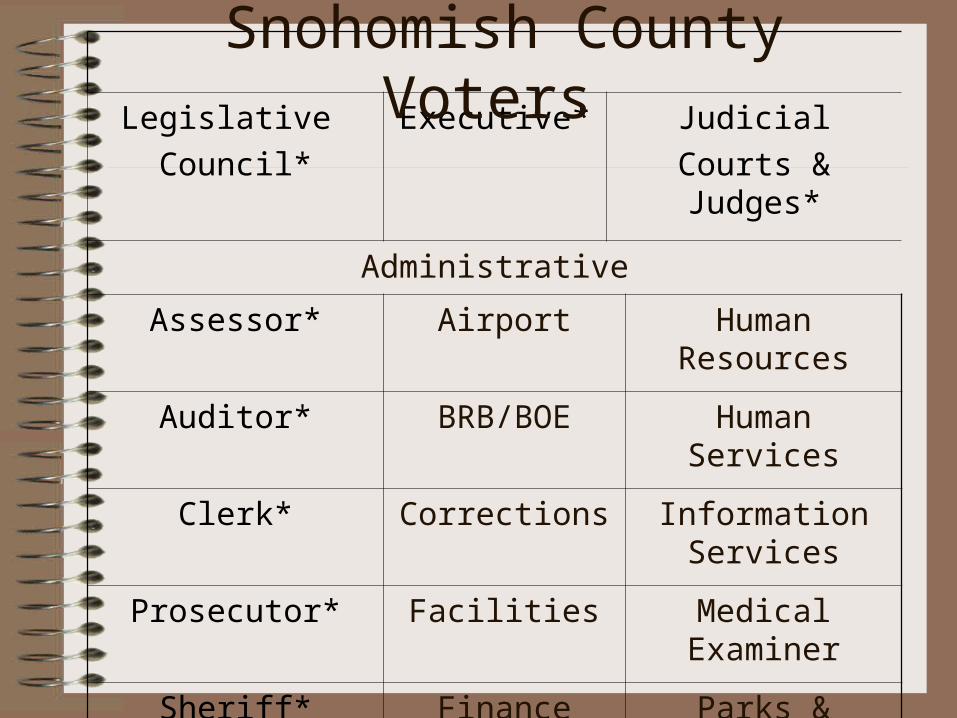

What else is the Assessor’s office responsible for?

• Administration of exemption programs such as senior citizen and non-profit

• Administration of special programs – Open Space

• (Farm & Agricultural, Timber, and General)

– Forest land– Historical Restoration

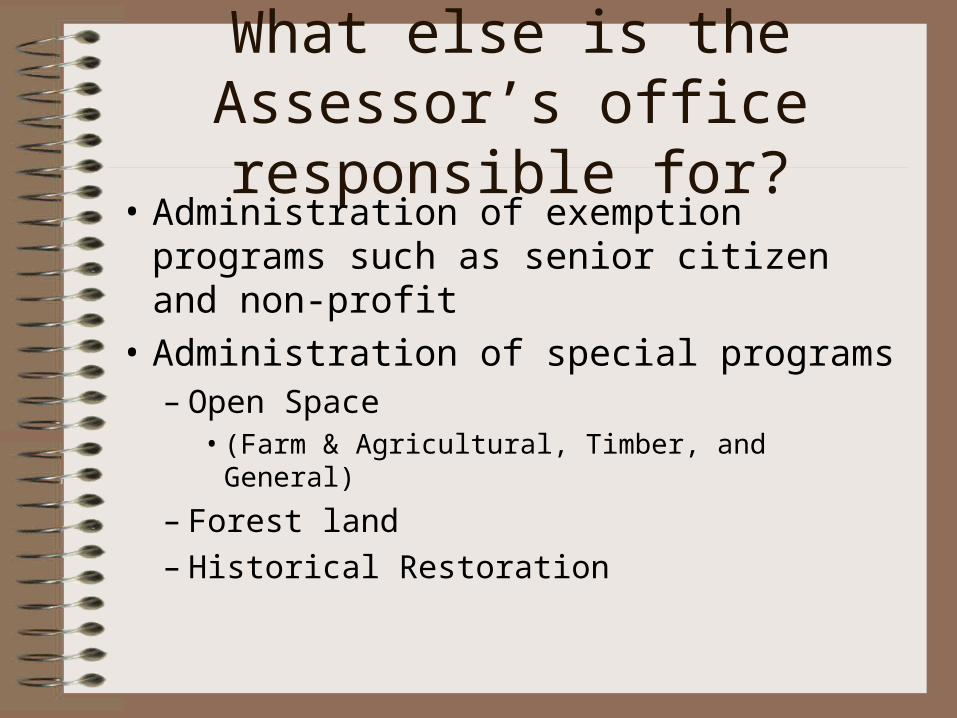

Workload Indicators

• 250,000 real property parcels to assess• 13,500 personal property accounts• 49.3 billion in assessed value• 1 billion + added for new construction

each year for the past 5 years• 9,000 senior exemptions• 28,500 phone calls (main customer service

line only)

Why do we have property tax?

• Taxing districts levy taxes to deliver services that taxpayers want and authorize

• Also used to pay for special voter-approved levies such as school maintenance and operation levies and bonds, and emergency medical levies

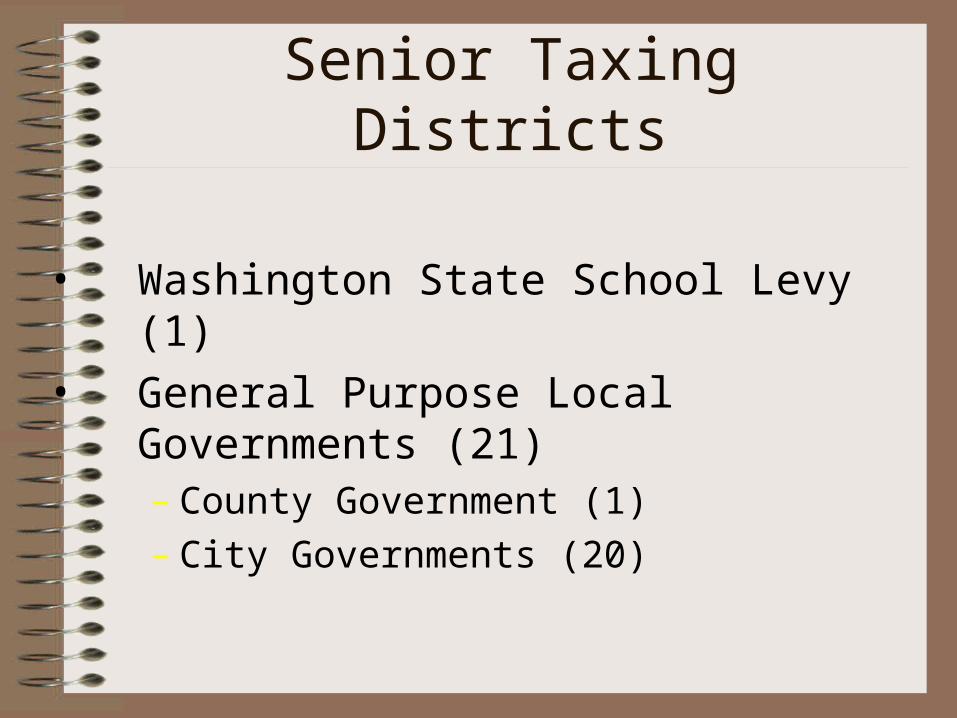

Senior Taxing Districts

• Washington State School Levy (1)

• General Purpose Local Governments (21)– County Government (1)– City Governments (20)

Junior Taxing Jurisdictions• Junior Taxing Jurisdictions (59)

– School Districts (15)

– Fire Districts (24)

– Health District (1)

– Library Districts (1)

– Water-7 & Sewer-3 Districts (10)

– Ports Districts (2)

– Hospital Districts (3)

– Transit (3)– Other: Recreation, Convention, Diking, PUD

Property Tax Distribution

Which local governments receive property taxes?Which local governments receive property taxes?

5.6¢ Fire Districts

10.8¢ General Uses

4.0¢ Ports &

Hospitals13.2¢ Cities &

Towns

60.4¢ School Distr

icts

6.0¢ County Roads

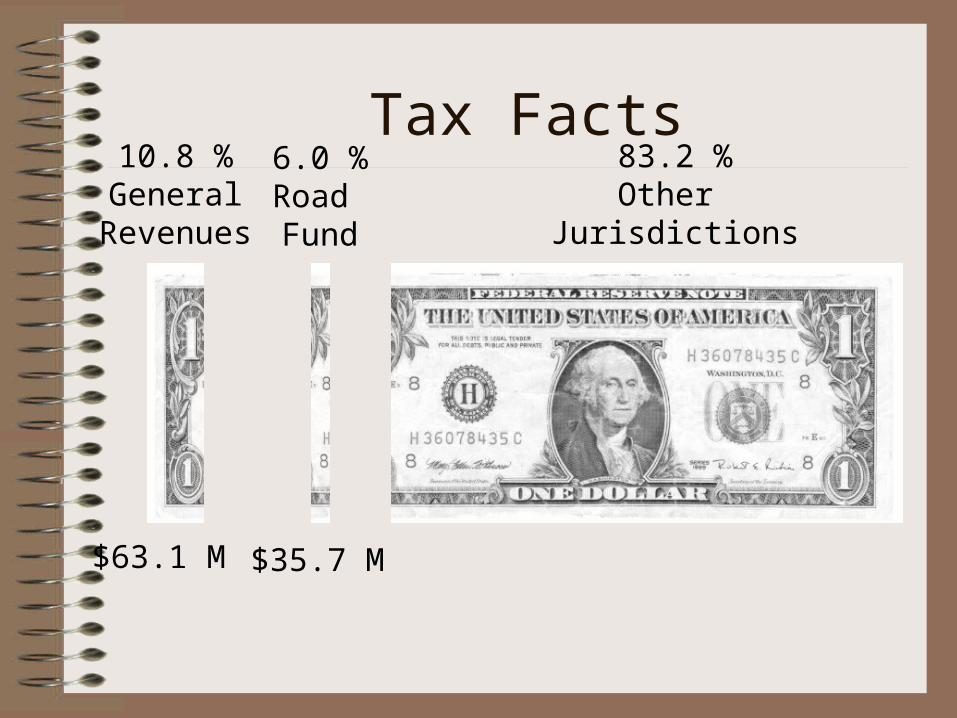

Tax Facts10.8 %General

Revenues

6.0 %Road Fund

83.2 %Other

Jurisdictions

$63.1 M $35.7 M

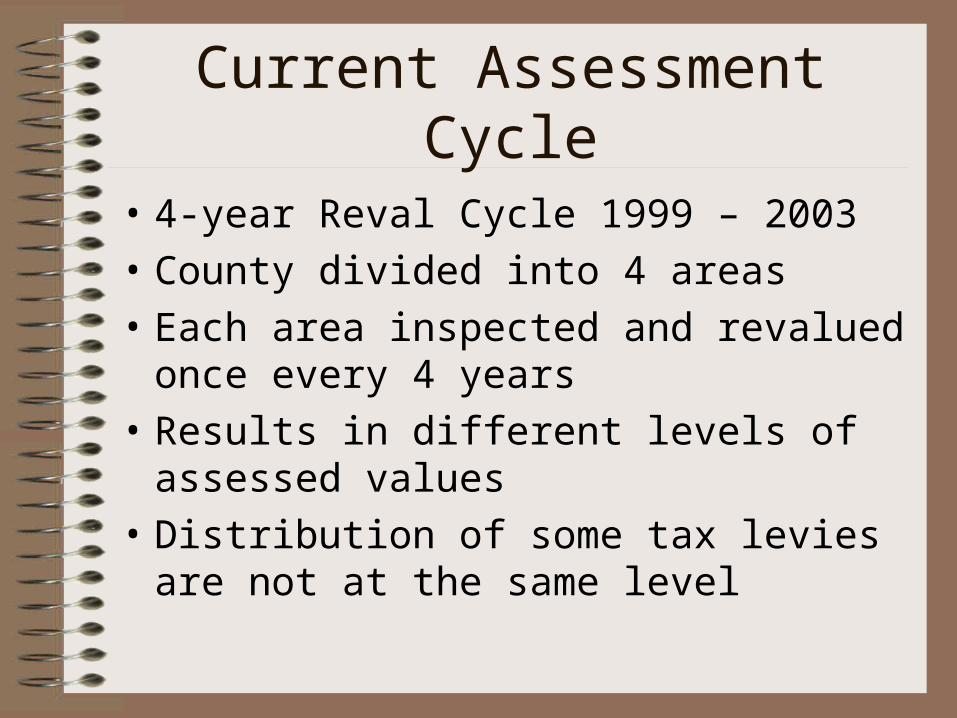

Current Assessment Cycle

• 4-year Reval Cycle 1999 – 2003

• County divided into 4 areas

• Each area inspected and revalued once every 4 years

• Results in different levels of assessed values

• Distribution of some tax levies are not at the same level

Iniative 747

• I-747 limited the amount a taxing district may levy, but did not affect assessed values

• Some taxing districts may have “banked levy capacity” that allows them to increase their budgets more than 1%

• Voter approved special levies are not affected by the $5.90 limit, 1% limit and I-747

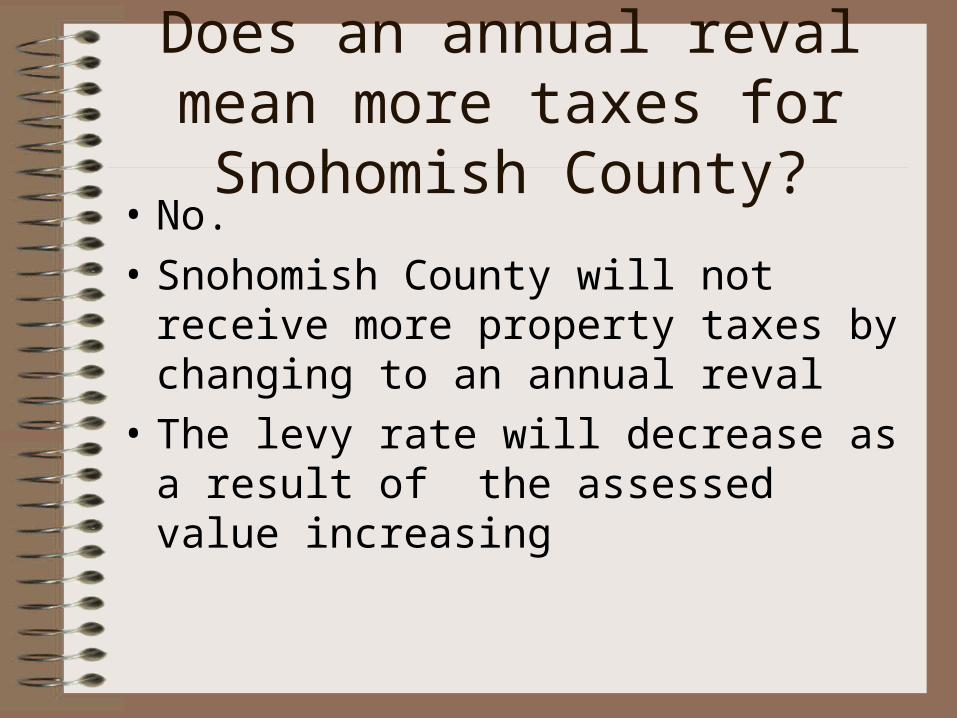

Does an annual reval mean more taxes for Snohomish County?

• No.

• Snohomish County will not receive more property taxes by changing to an annual reval

• The levy rate will decrease as a result of the assessed value increasing

Annual Reval – A goal we have been working towards

• Standards, Accountability & Reorganization

• Using technology– GIS– CAMA– Ascend– Tablet computers for field appraisers– Working with Planning & Development

Annual Reval Plan

• Starting in 2004 - revaluation will be done annually

• 1/6 of property in the county will be physically inspected and updated to market value

• All property that is not physically inspected must be statistically updated annually

• New 2004 assessed value used to calculate taxes owing in 2005

Benefits of an Annual Reval

• Uniformity– All property is closer to market value

• Level of assessment– Tax burden distributed more equitably

• Predictability– Helps taxpayers and taxing districts

Uniformity

• All property is assessed every year at market value

• Particularly important if market values begin to decline

• Assessed values are not “fixed” for 4 years

Level of Assessment

• Tax burden is distributed more equitably

• Particularly important for county-wide levies such as the:– state school levy– county levies – other levies that cross area boundaries

Predictability

• Large increases in assessed values that result from a 4-year cycle are:– difficult for taxpayers to accept– misunderstood (40% increase in A/V must

equal 40% increase in taxes)– result in the area that has just been revalued

carrying a larger share of some taxes than the other 3 areas

Advances in Technology

Resulted in Increases in Efficiency • In 1975 the office had 118 employees

• In 2002 there were 71 FTEs

• In 2003 we will have 69.85 FTEs

• More than a 40% decrease in staff

• In 1973 there were 147,500 parcels

• In 2003 we will have over 250,000 parcels

• More than a 69% increase in workload

Exemption Programs andSpecial Classifications

• Open Space Classification

• Improvement Exemption

• Destroyed Property Claims

• Designated Forest Land

• Historical Restoration Exemption

• Non-Profit Organizations

• Senior Citizen/Disabled Person Exemption