Embed Size (px)

Citation preview

SMV Updating and General Revisionand General Revision

of Real Property Assessments

FUNCTIONS OF BLGF UNDER E.O. NO. 292FUNCTIONS OF BLGF UNDER E.O. NO. 292 ADMINISTRATIVE CODE OF 1987

Sec. 33, Title II, Chapter 4Sec. 33, Title II, Chapter 4“(1) Assist in the formulation and implementation

of policies on local government revenueof policies on local government revenue administration and fund management.

“(2) Exercise administrative and technical(2) Exercise administrative and technical supervision and coordination over the treasury and assessment operations of localand assessment operations of local governments.”

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 200. Administration of the Real PropertySec. 200. Administration of the Real Property Tax“The provinces and cities includingThe provinces and cities including

municipalities within the Metropolitan Manila Area, shall be primarily responsible for the , p y pproper, efficient and effective administration of the real property tax.”

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 201. Appraisal of Real PropertySec. 201. Appraisal of Real Property“All real property, whether taxable or exempt,

shall be appraised at the current and fairshall be appraised at the current and fair market value prevailing in the locality where the property is situated. The Department of p p y pFinance shall promulgated the necessary and regulations for the classification, appraisal, and assessment of real property pursuant to the provisions of this Code.”

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 219. General Revision of AssessmentsSec. 219. General Revision of Assessments and Property Classification“The Provincial city or municipal assessor shallThe Provincial, city or municipal assessor shall

undertake a general revision of real property assessment within two (2) years after the ( ) yeffectivity of this Code and every three (3) years thereafter.”

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 219. General Revision of AssessmentsSec. 219. General Revision of Assessments and Property ClassificationArt. 310. General Revision of Assessments andArt. 310. General Revision of Assessments and

Property Classification(a) The provincial, city and municipal assessor shall ( ) p y p

undertake a general revision of real property assessment within two (2) years after the effectivity of the Code and every three (3) yearseffectivity of the Code and every three (3) years thereafter.

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 219. General Revision of AssessmentsSec. 219. General Revision of Assessments and Property ClassificationArt. 310. General Revision of Assessments andArt. 310. General Revision of Assessments and

Property Classification(b) For this purpose, the provincial assessors, the city

assessors, and the municipal assessors of MMA shall prepare the schedule of fair market values for the different kinds and classes of real propertythe different kinds and classes of real property located within the territorial jurisdiction of the province, city or municipality within one (1) year from the effectivity of the Code in accordance with such rules and regulations issued by DOF.

SECTIONS 200, 201 & 219SECTIONS 200, 201 & 219 LOCAL GOVERNMENT CODE OF 1991

Sec. 219. General Revision of AssessmentsSec. 219. General Revision of Assessments and Property ClassificationArt. 310. General Revision of Assessments andArt. 310. General Revision of Assessments and

Property Classification(c) The general revision of assessments and property

classification shall commence upon the enactment of the schedule of fair market values but not later than two (2) years from the effectivity of the Codethan two (2) years from the effectivity of the Code. Thereafter, the provincial, city or municipal assessor shall undertake the general revision of real property assessments and property classification once every three (3) years.

MRPAAO & PVSMRPAAO & PVSDOF ISSUANCES

Manual on Real Property Appraisal andManual on Real Property Appraisal and Assessment Operations (MRPAAO) under Local Assessment Regulations No. 1-04 issued by the DOF on Oct. 1, 2004.

Department Order No. 37-09 issued by the DOF p yon Oct. 19, 2009, prescribing the Philippine Valuation Standards (PVS 1st Edition: Adoption of the IVSC Valuation Standards under Philippine setting

WHAT IS A SCHEDULE OF MARKET VALUES?WHAT IS A SCHEDULE OF MARKET VALUES?SMV

It is an approved schedule of unit base marketIt is an approved schedule of unit base market values for different classes of real property used by the provincial, city or municipal assessors as basis for the appraisal and assessment of real properties in their respective territorial j i di ti f l t t tijurisdictions for real property taxation purposes.

Sections 199 (e) and (f) of the LGC provide:Sections 199 (e) and (f) of the LGC provide:(e) “Appraisal” is the act or process of

determining the value of property as of adetermining the value of property as of a specific date for a specific purpose.

(f) “Assessment” is the act or process of(f) Assessment is the act or process of determining the value of a property, or proportion thereof subject to tax, including the p p j , gdiscovery, listing, classification, and appraisal of properties.

Real Estate – the physical and tangible thing.Real Estate the physical and tangible thing.Real Property – All the rights, interests, and

benefits related to the ownership of real estate.benefits related to the ownership of real estate.Market Value – estimated amount for which a

property should exchange on the date of p p y gvaluation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsioncompulsion.

Why revise the SMV?y

• Mandated by law (Section 219 R.A. No. 7160).S k t fl t t k t l l f ti• Seeks to reflect true market levels of properties based on the updated base unit values.

• Rationalizes the real property tax base• Rationalizes the real property tax base.• To promote transparency and accuracy in the

property market to entice investors.p p y• To provide equitable and fair distribution of tax

burden.

PREPARATION OF THE SMVPREPARATION OF THE SMV

Before any General Revision of Real Property Before any General Revision of Real Property Assessment is made, there shall be prepared a SMV by the Provincial, City and the Municipality of MMA for the different classes of real property situated in their respective LGUs for enactment of an ordinance b th S i dby the Sanggunian concerned.

WHAT IS THE GENERAL REVISION OFWHAT IS THE GENERAL REVISION OF PROPERTY ASSESSMENTS?

The General Revision of real property assessments is the updating of all real property records of the LGU p g p p yonce every three (3) years using the revised Schedule of Market Values (SMV).

Why Conduct General Revision?Why Conduct General Revision?

General Revision serves two important purposes i dditi t it i f li i din addition to its primary purpose of equalizing and updating valuation. These are:

1) T di l ti th t h1) To rediscover real properties that have been “lost” from the tax rolls,

2) To enable the assessor to purge the rolls of double assessments of properties that have accumulated through the years andaccumulated through the years, and

3) To reclassify properties based on its Highest and Best Use (HABU)Highest and Best Use (HABU).

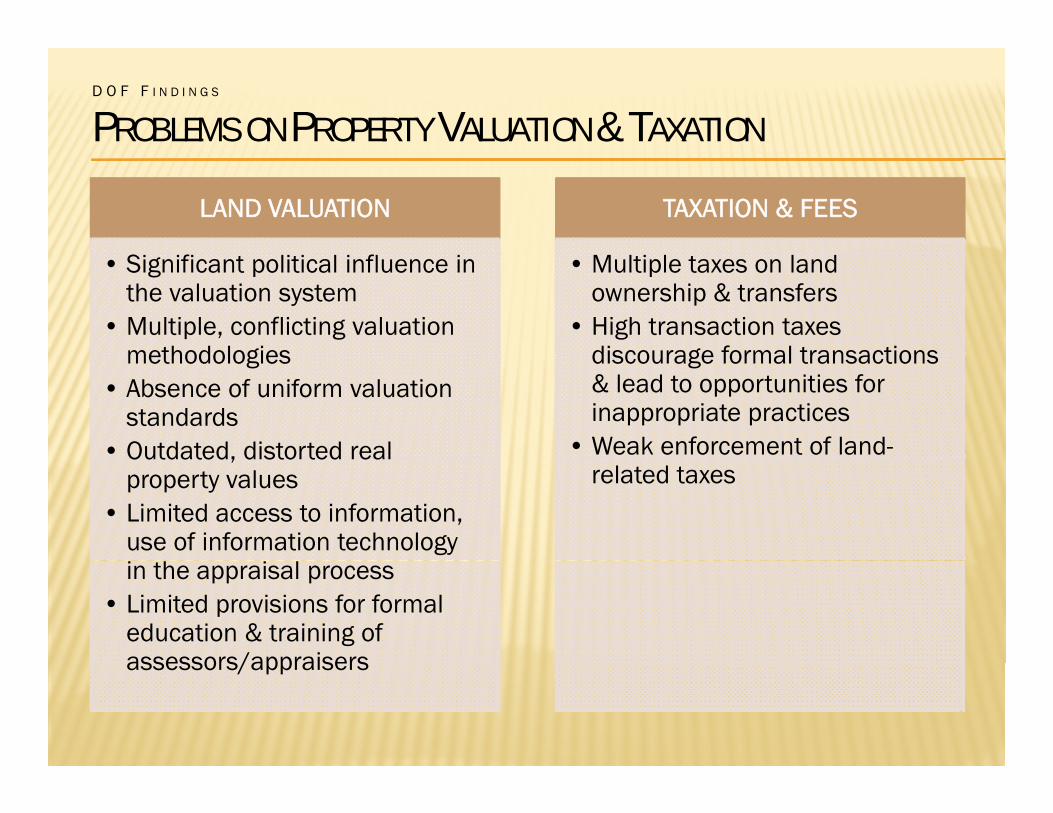

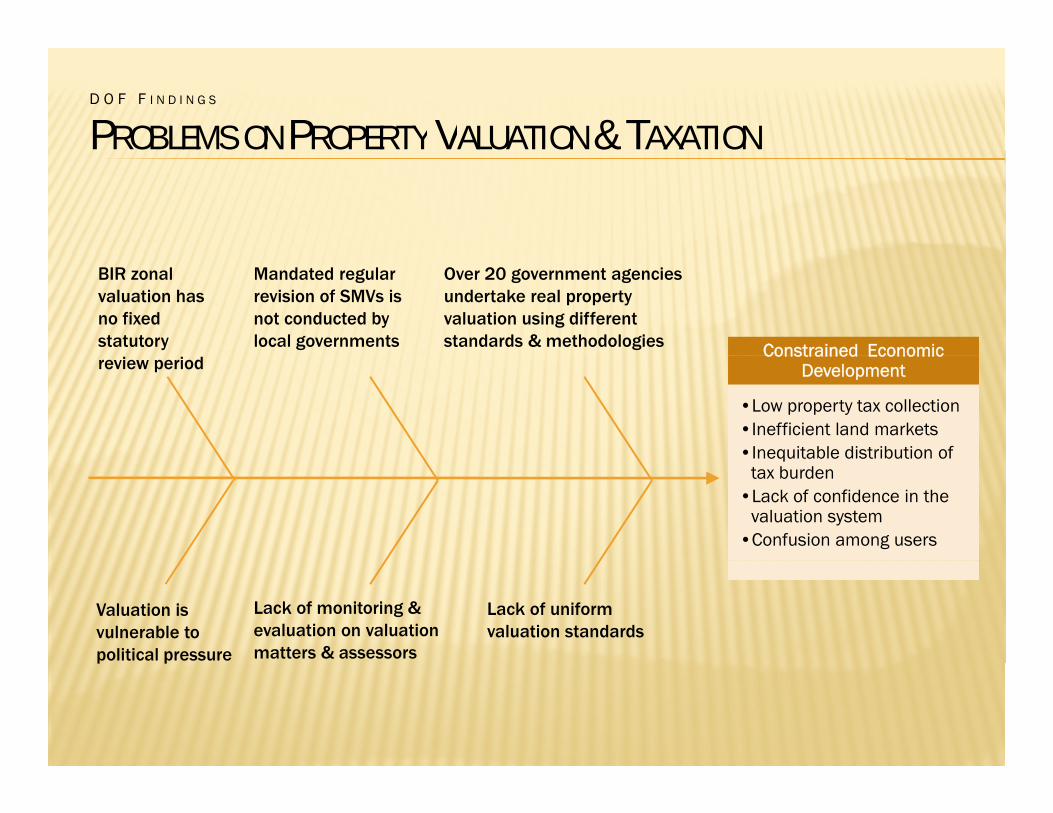

D O F F I N D I N G S

PROBLEMS ON PROPERTY VALUATION & TAXATION

LAND VALUATION TAXATION & FEES

• Significant political influence in the valuation system

• Multiple, conflicting valuation methodologies

• Multiple taxes on land ownership & transfers

• High transaction taxes discourage formal transactions methodologies

• Absence of uniform valuation standards

• Outdated, distorted real

discourage formal transactions & lead to opportunities for inappropriate practices

• Weak enforcement of land-Outdated, distorted real property values

• Limited access to information, use of information technology

related taxes

in the appraisal process• Limited provisions for formal

education & training of assessors/appraisersassessors/appraisers

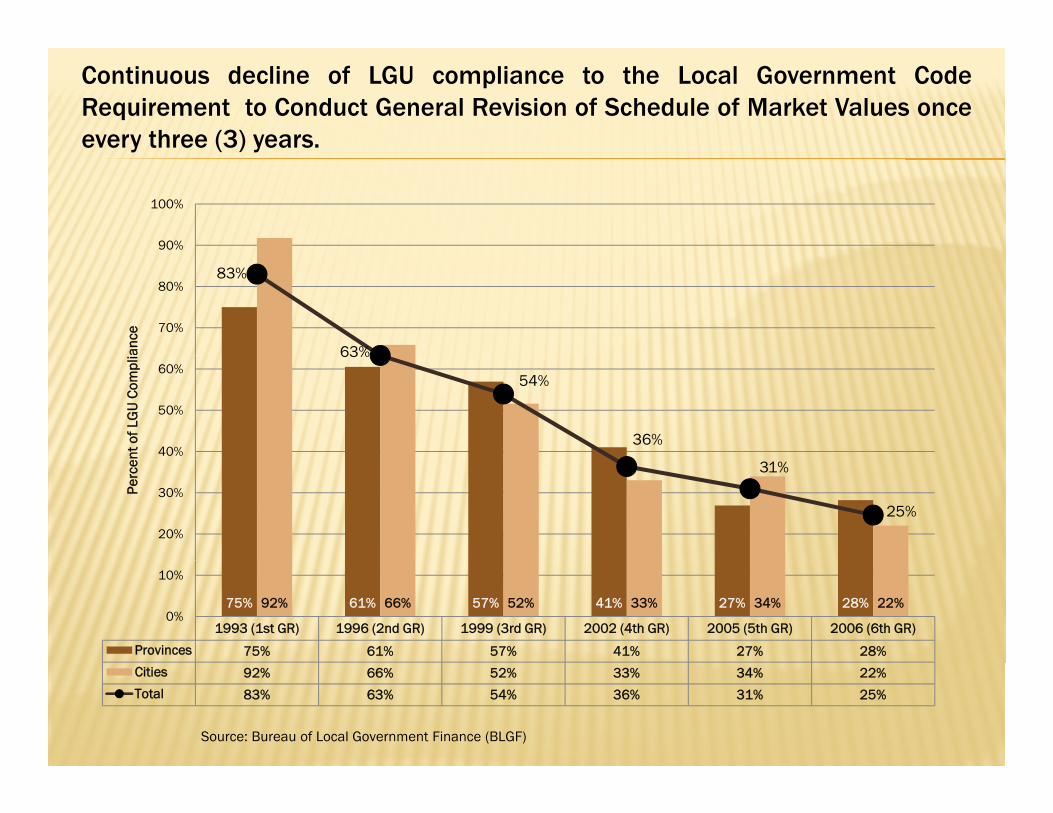

Continuous decline of LGU compliance to the Local Government CodeRequirement to Conduct General Revision of Schedule of Market Values onceevery three (3) years.

90%

100%

y ( ) y

83%

63%

70%

80%

ance

63%

54%

36%40%

50%

60%

nt o

f LG

U C

ompl

i

31%

25%20%

30%Perc

en

1993 (1st GR) 1996 (2nd GR) 1999 (3rd GR) 2002 (4th GR) 2005 (5th GR) 2006 (6th GR)

Provinces 75% 61% 57% 41% 27% 28%

75% 61% 57% 41% 27% 28%92% 66% 52% 33% 34% 22%0%

10%

Cities 92% 66% 52% 33% 34% 22%

Total 83% 63% 54% 36% 31% 25%

Source: Bureau of Local Government Finance (BLGF)

D O F F I N D I N G S

PROBLEMS ON PROPERTY VALUATION & TAXATION

Constrained Economic

Over 20 government agencies undertake real property valuation using different standards & methodologies

BIR zonal valuation has no fixed statutory

Mandated regular revision of SMVs is not conducted by local governments Constrained Economic

Development

•Low property tax collection•Inefficient land markets•Inequitable distribution of

review period

Inequitable distribution of tax burden

•Lack of confidence in the valuation system

•Confusion among users

Valuation is vulnerable to political pressure

Lack of monitoring & evaluation on valuation matters & assessors

Lack of uniform valuation standards

p p

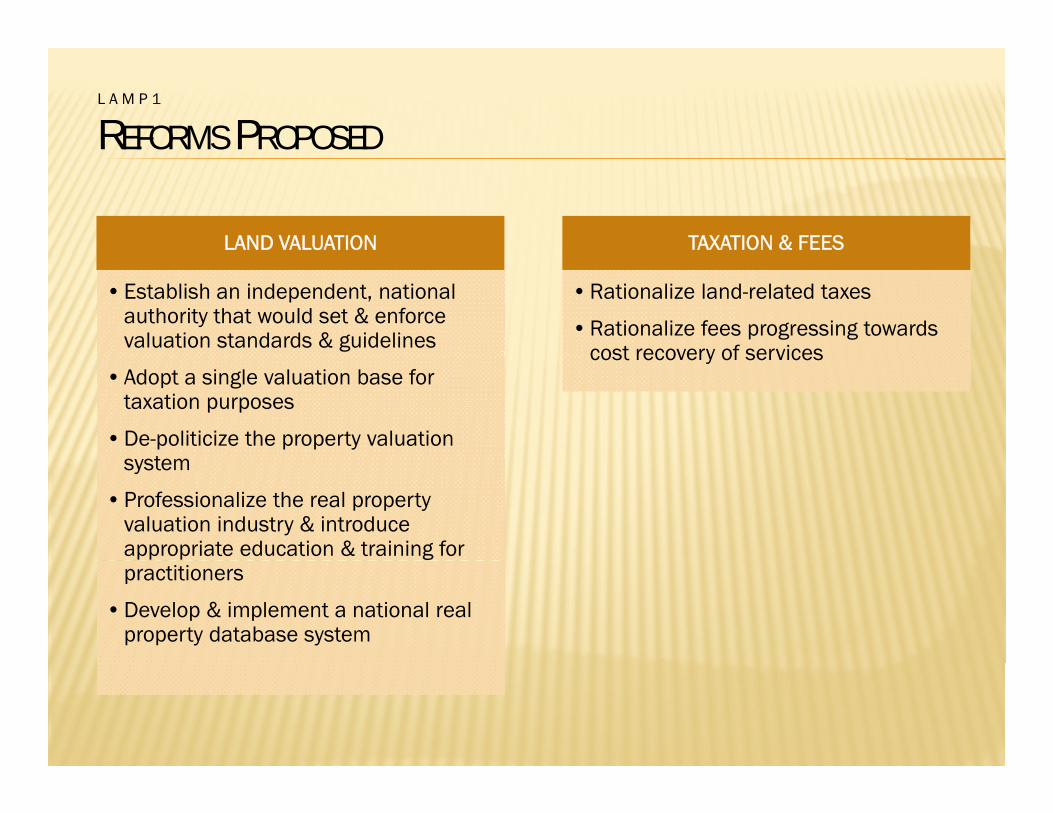

L A M P 1

REFORMS PROPOSED

LAND VALUATION TAXATION & FEES

• Establish an independent, national authority that would set & enforce valuation standards & guidelines

• Rationalize land-related taxes

• Rationalize fees progressing towards cost recovery of services

• Adopt a single valuation base for taxation purposes

• De-politicize the property valuation t

cost recovery of services

system

• Professionalize the real property valuation industry & introduce appropriate education & training for practitioners

• Develop & implement a national real property database system

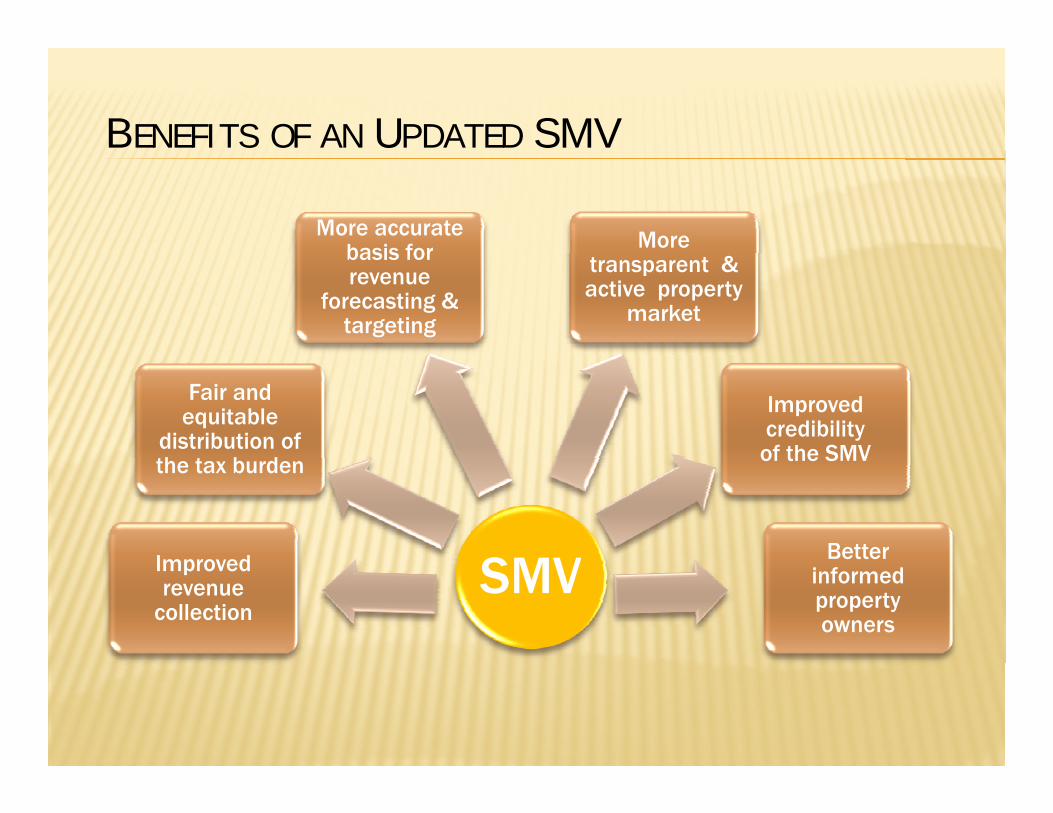

B E N E F I T S O F A N U P D A T E D S M V

More accurate basis for More basis for revenue

forecasting & targeting

transparent & active property

market

Fair and equitable

distribution of h b d

Improved credibility

of the SMV

SMVImproved

the tax burden of the SMV

Better

SMVImproved revenue

collection

informed property owners

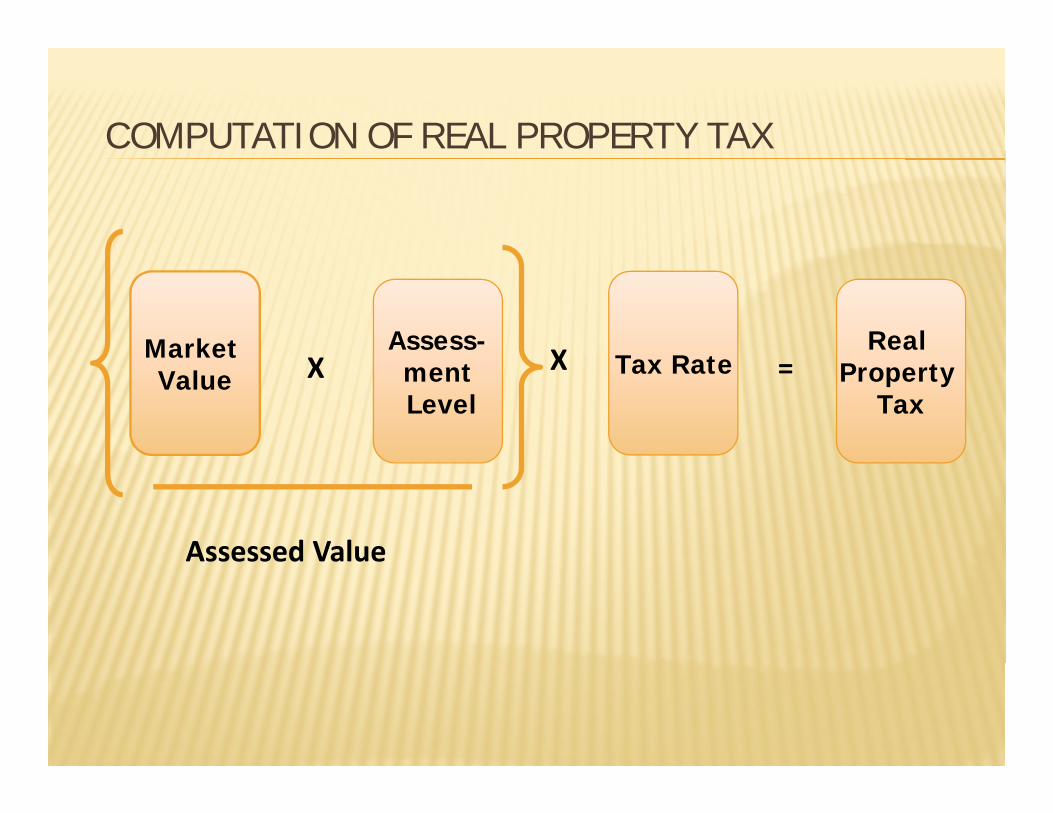

C O M P U TAT I O N O F R E A L P R O P E R T Y TA X

Market Assess-T R tX

Real Market Value ment

LevelTax RateX X Property

Tax=

Assessed ValueAssessed Value

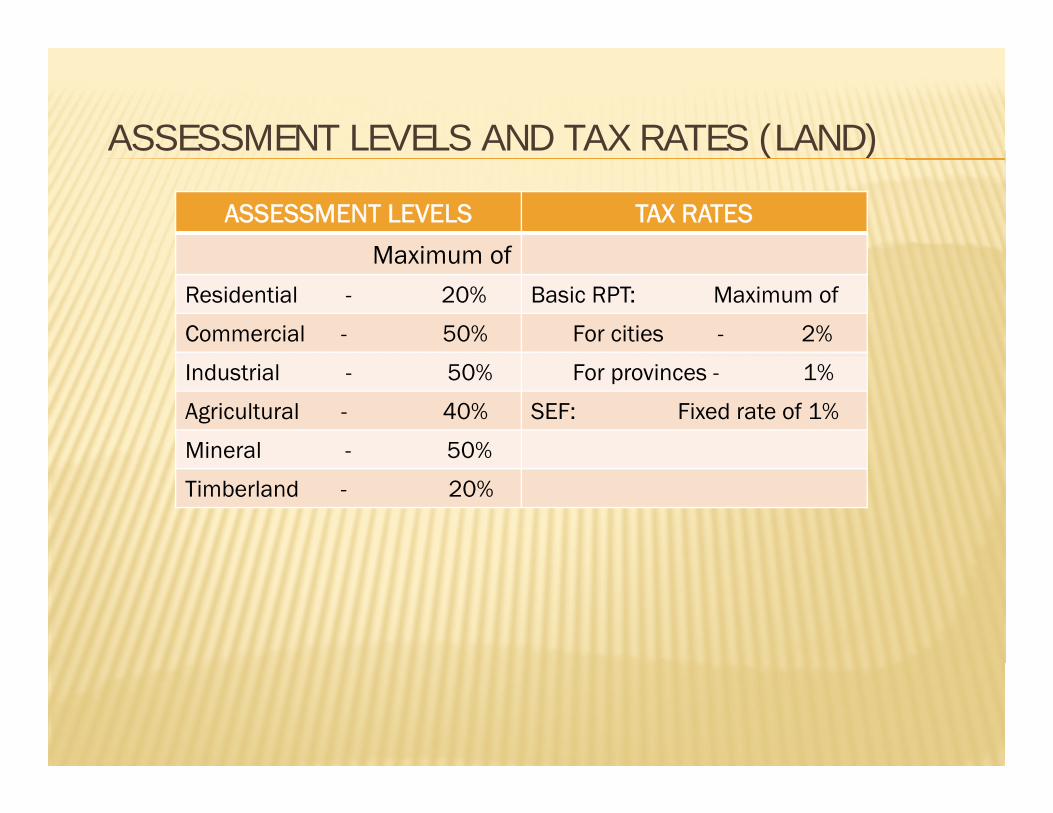

A S S E S S M E N T L E V E L S A N D TA X R AT E S ( L A N D )A S S E S S M E N T L E V E L S A N D TA X R AT E S ( L A N D )

ASSESSMENT LEVELS TAX RATES

Maximum of Maximum of

Residential - 20% Basic RPT: Maximum of

Commercial - 50% For cities - 2%

Industrial - 50% For provinces - 1%

Agricultural - 40% SEF: Fixed rate of 1%

Mineral - 50%e a 50%

Timberland - 20%

How will the revised SMV improve our RPT collection?

Real Property Tax (RPT) is dependent on three elements:1) M k V l1) Market Value;2) Assessment Level; and3) Tax Rate.

An increase in the market values of real properties will lead to an increase in RPT.

However, the LGU should also consider the taxpayer’s ability to pay the taxes. This, the LGU may opt to lower the assessment level or the tax rates as provided in the LGC. This will improve the LGU’s revenue and lessen the taxpayer’s burden as well.taxpayer s burden as well.

What is the Joint-Memorandum Circular No. 2010-01?

• The Joint-Memorandum Circular No.2010-01 is a i d f h D f Fi (DOF) d reminder from the Department of Finance (DOF) and

Department of Interior and Local Government (DILG) for LGUs to comply with the provisions of the Local for LGUs to comply with the provisions of the Local Government Code regarding appraisal and assessment of properties and to conduct general

i i f SMV revision of SMV.

• The JMC 1 also prescribes the use of Philippine V l ti St d d (DOF D t O d N 37 09) d Valuation Standards (DOF Dept. Order No.37-09) and Mass Appraisal Guidebook (DOF Dept. Order No.2010-10).)

For inquiries, contact the JMC Task Force Secretariat at:

JMC Task Force – Department of Finance (DOF)Bureau of Local Government Finance, Department of Finance8/F EDPC Building, Bangko Sentral ng Pilipinas Complex,Roxas Blvd ManilaRoxas Blvd., ManilaTelefax: (02) 524-6324/(02)522-8770

JMC Task Force – Department of the Interior and Local Government (DILG)Bureau of Local Government DevelopmentDepartment of the Interior and Local Government4/F, A. Francisco Gold Condominium II, EDSA, corner MapagmahalSt., Diliman, Quezon CitySt., Diliman, Quezon CityTel.: (02) 929-9235Fax: (02)927-7852

- END -HAVE A NICE DAYHAVE A NICE DAY

![SMV [McMillan 93]](https://img.pdfslide.us/doc/110x75/5681572a550346895dc4c47a/smv-mcmillan-93.jpg)