Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

07 January 2015

Americas/United States

Equity Research

Biotechnology (SMID Cap Biotechnology (US))

SMID Cap Biotechnology INDUSTRY PRIMER

Credit Suisse 2015 Question Prep Pack

We have prepared a list of key questions for our covered companies. We

believe these questions are relevant for the near-term and long-term catalysts

for the respective companies and are intended to help investors prep for

meetings with management in Q1.

The important themes in 2015 for our coverage include:

■ Antibiotics – How will the pending legislation impact companies developing

/ marketing antibiotics; will consolidation continue; and how well will recently

approved antibiotics launch?

■ Duchenne muscular dystrophy (DMD) – How will the pending clinical /

regulatory events impact the DMD therapeutic landscape; specifically, how

will FDA and EMA handle applications for drugs that do not have positive

Phase 3 results?

■ Cholesterol lowering agents – How will the pending PCSK9 approvals

impact the LDL lowering market, how will these agents be priced, will recent

pricing concerns in HCV impact the PCSK9 market dynamics, will the market

be evenly split or will a leader emerge, will FDA provide a path forward to

new oral agents (ETC-1002)?

■ CAR-T cell therapy – How will the efficacy and safety profiles for CAR-T

therapies evolve over 2015, and how many new players will enter the field

through collaboration or acquisition?

■ Oral lymphoma drugs – Will clinical results and new approvals alter the

trajectory of Imbruvica, will Zydelig gain significant commercial traction, will

new combinations emerge, and will there be consolidation in the space?

■ Acute myeloid leukemia (AML) – Which drugs will emerge as viable

contenders? Will FDA change its stance on a survival benefit in the primary

analysis of a Phase III trial?

.

Research Analysts

Jason Kantor, PhD

415 249 7942

Jeremiah Shepard, PhD

415 249 7933

Ravi Mehrotra PhD

212 325 3487

Anuj Shah

212 325 6931

07 January 2015

SMID Cap Biotechnology 2

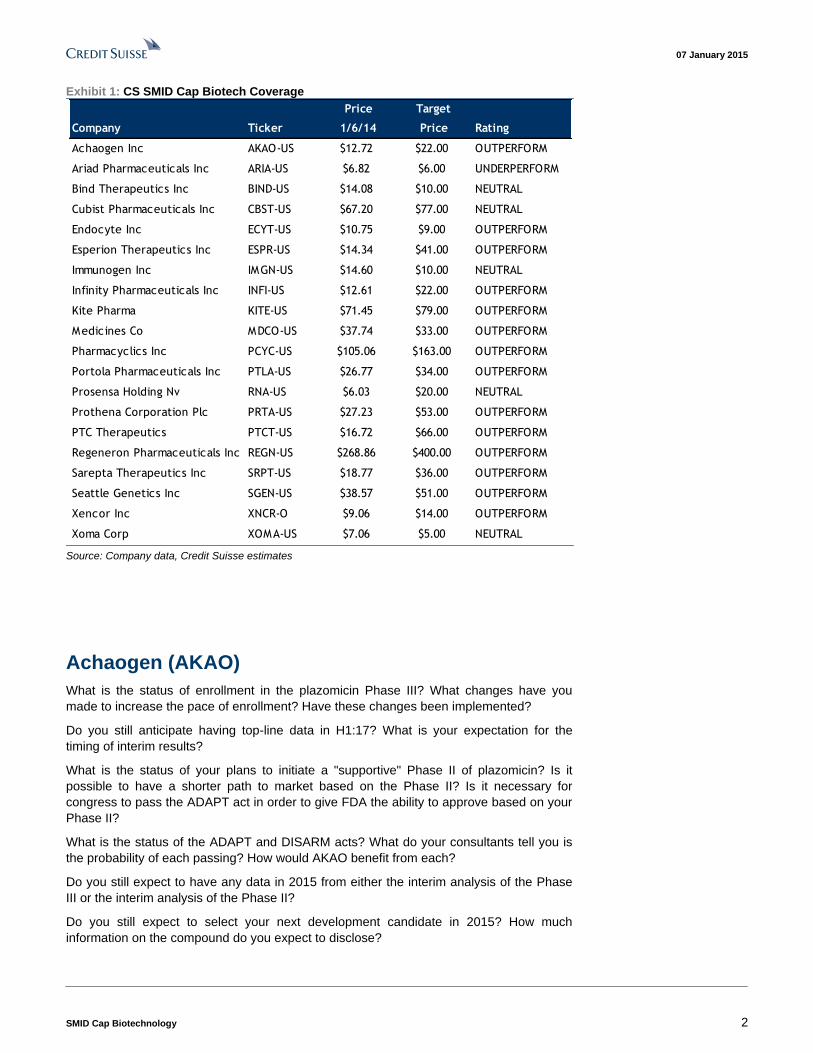

Exhibit 1: CS SMID Cap Biotech Coverage

Price Target

Company Ticker 1/6/14 Price Rating

Achaogen Inc AKAO-US $12.72 $22.00 OUTPERFORM

Ariad Pharmaceuticals Inc ARIA-US $6.82 $6.00 UNDERPERFORM

Bind Therapeutics Inc BIND-US $14.08 $10.00 NEUTRAL

Cubist Pharmaceuticals Inc CBST-US $67.20 $77.00 NEUTRAL

Endocyte Inc ECYT-US $10.75 $9.00 OUTPERFORM

Esperion Therapeutics Inc ESPR-US $14.34 $41.00 OUTPERFORM

Immunogen Inc IMGN-US $14.60 $10.00 NEUTRAL

Infinity Pharmaceuticals Inc INFI-US $12.61 $22.00 OUTPERFORM

Kite Pharma KITE-US $71.45 $79.00 OUTPERFORM

Medicines Co MDCO-US $37.74 $33.00 OUTPERFORM

Pharmacyclics Inc PCYC-US $105.06 $163.00 OUTPERFORM

Portola Pharmaceuticals Inc PTLA-US $26.77 $34.00 OUTPERFORM

Prosensa Holding Nv RNA-US $6.03 $20.00 NEUTRAL

Prothena Corporation Plc PRTA-US $27.23 $53.00 OUTPERFORM

PTC Therapeutics PTCT-US $16.72 $66.00 OUTPERFORM

Regeneron Pharmaceuticals Inc REGN-US $268.86 $400.00 OUTPERFORM

Sarepta Therapeutics Inc SRPT-US $18.77 $36.00 OUTPERFORM

Seattle Genetics Inc SGEN-US $38.57 $51.00 OUTPERFORM

Xencor Inc XNCR-O $9.06 $14.00 OUTPERFORM

Xoma Corp XOMA-US $7.06 $5.00 NEUTRAL

Source: Company data, Credit Suisse estimates

Achaogen (AKAO)

What is the status of enrollment in the plazomicin Phase III? What changes have you

made to increase the pace of enrollment? Have these changes been implemented?

Do you still anticipate having top-line data in H1:17? What is your expectation for the

timing of interim results?

What is the status of your plans to initiate a "supportive" Phase II of plazomicin? Is it

possible to have a shorter path to market based on the Phase II? Is it necessary for

congress to pass the ADAPT act in order to give FDA the ability to approve based on your

Phase II?

What is the status of the ADAPT and DISARM acts? What do your consultants tell you is

the probability of each passing? How would AKAO benefit from each?

Do you still expect to have any data in 2015 from either the interim analysis of the Phase

III or the interim analysis of the Phase II?

Do you still expect to select your next development candidate in 2015? How much

information on the compound do you expect to disclose?

07 January 2015

SMID Cap Biotechnology 3

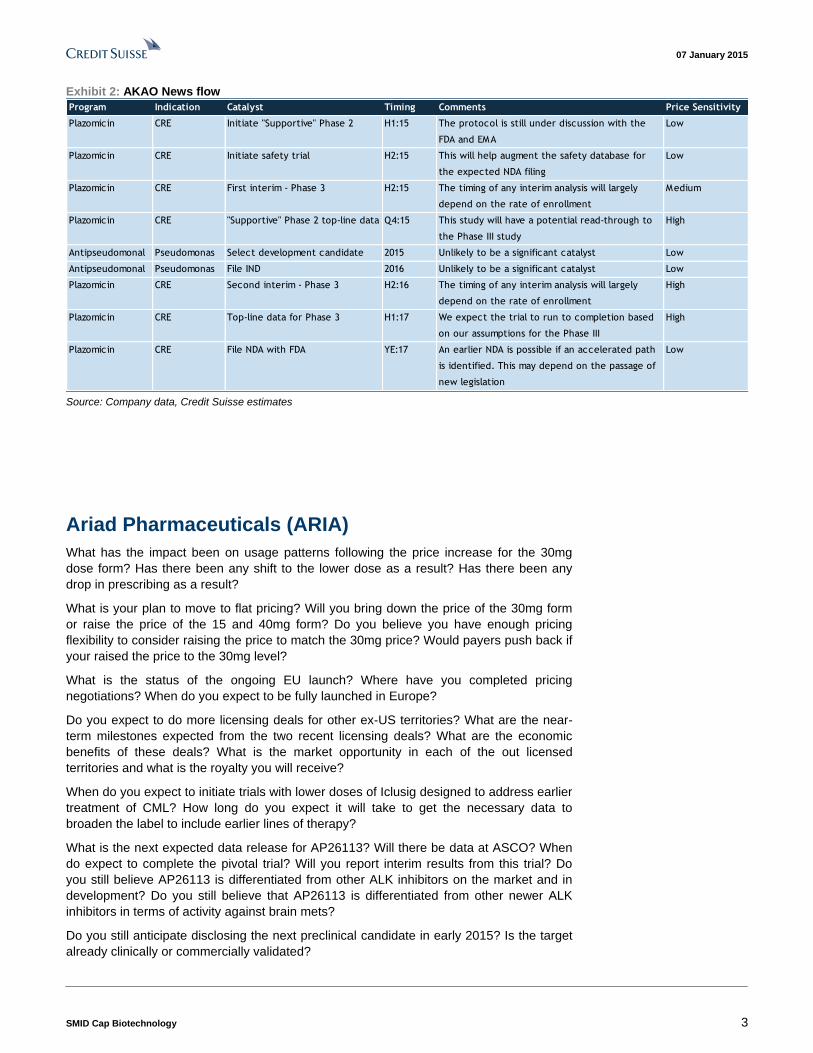

Exhibit 2: AKAO News flow

Program Indication Catalyst Timing Comments Price Sensitivity

Plazomicin CRE Initiate "Supportive" Phase 2 H1:15 The protocol is still under discussion with the

FDA and EMA

Low

Plazomicin CRE Initiate safety trial H2:15 This will help augment the safety database for

the expected NDA filing

Low

Plazomicin CRE First interim - Phase 3 H2:15 The timing of any interim analysis will largely

depend on the rate of enrollment

Medium

Plazomicin CRE "Supportive" Phase 2 top-line data releaseQ4:15 This study will have a potential read-through to

the Phase III study

High

Antipseudomonal Pseudomonas Select development candidate 2015 Unlikely to be a significant catalyst Low

Antipseudomonal Pseudomonas File IND 2016 Unlikely to be a significant catalyst Low

Plazomicin CRE Second interim - Phase 3 H2:16 The timing of any interim analysis will largely

depend on the rate of enrollment

High

Plazomicin CRE Top-line data for Phase 3 H1:17 We expect the trial to run to completion based

on our assumptions for the Phase III

High

Plazomicin CRE File NDA with FDA YE:17 An earlier NDA is possible if an accelerated path

is identified. This may depend on the passage of

new legislation

Low

Source: Company data, Credit Suisse estimates

Ariad Pharmaceuticals (ARIA)

What has the impact been on usage patterns following the price increase for the 30mg

dose form? Has there been any shift to the lower dose as a result? Has there been any

drop in prescribing as a result?

What is your plan to move to flat pricing? Will you bring down the price of the 30mg form

or raise the price of the 15 and 40mg form? Do you believe you have enough pricing

flexibility to consider raising the price to match the 30mg price? Would payers push back if

your raised the price to the 30mg level?

What is the status of the ongoing EU launch? Where have you completed pricing

negotiations? When do you expect to be fully launched in Europe?

Do you expect to do more licensing deals for other ex-US territories? What are the near-

term milestones expected from the two recent licensing deals? What are the economic

benefits of these deals? What is the market opportunity in each of the out licensed

territories and what is the royalty you will receive?

When do you expect to initiate trials with lower doses of Iclusig designed to address earlier

treatment of CML? How long do you expect it will take to get the necessary data to

broaden the label to include earlier lines of therapy?

What is the next expected data release for AP26113? Will there be data at ASCO? When

do expect to complete the pivotal trial? Will you report interim results from this trial? Do

you still believe AP26113 is differentiated from other ALK inhibitors on the market and in

development? Do you still believe that AP26113 is differentiated from other newer ALK

inhibitors in terms of activity against brain mets?

Do you still anticipate disclosing the next preclinical candidate in early 2015? Is the target

already clinically or commercially validated?

07 January 2015

SMID Cap Biotechnology 4

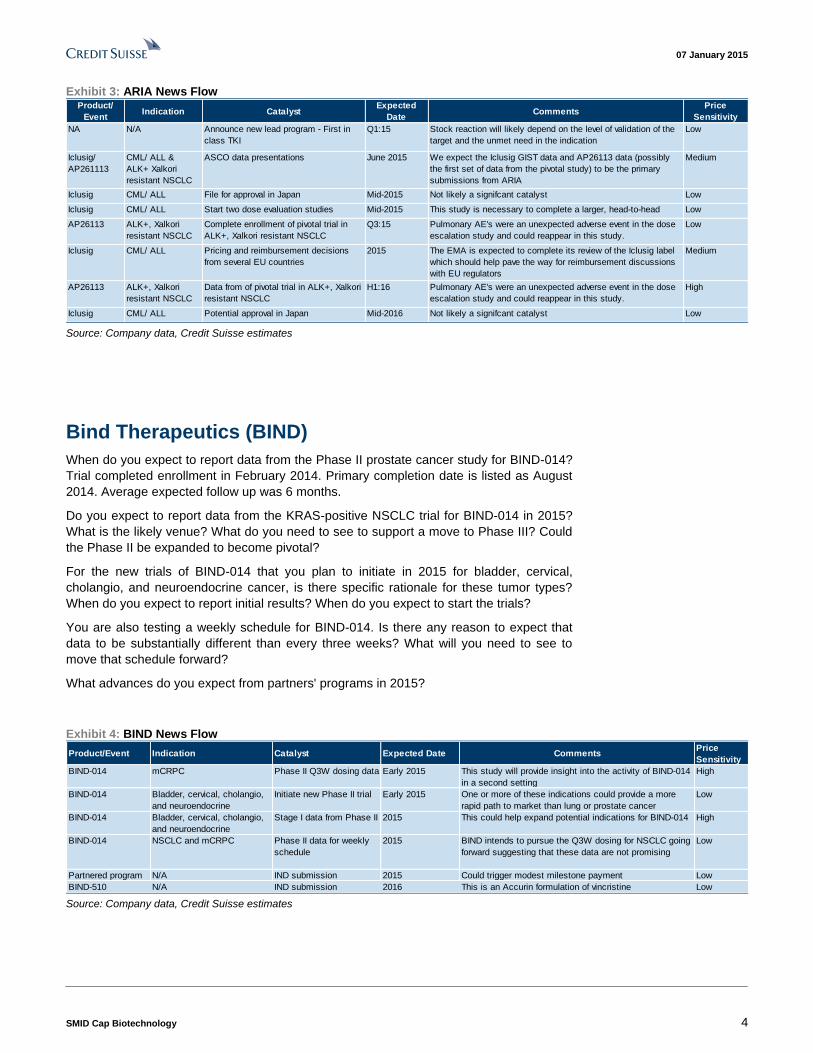

Exhibit 3: ARIA News Flow Product/

EventIndication Catalyst

Expected

DateComments

Price

Sensitivity

NA N/A Announce new lead program - First in

class TKI

Q1:15 Stock reaction will likely depend on the level of validation of the

target and the unmet need in the indication

Low

Iclusig/

AP261113

CML/ ALL &

ALK+ Xalkori

resistant NSCLC

ASCO data presentations June 2015 We expect the Iclusig GIST data and AP26113 data (possibly

the first set of data from the pivotal study) to be the primary

submissions from ARIA

Medium

Iclusig CML/ ALL File for approval in Japan Mid-2015 Not likely a signifcant catalyst Low

Iclusig CML/ ALL Start two dose evaluation studies Mid-2015 This study is necessary to complete a larger, head-to-head

study with another approved TKI

Low

AP26113 ALK+, Xalkori

resistant NSCLC

Complete enrollment of pivotal trial in

ALK+, Xalkori resistant NSCLC

Q3:15 Pulmonary AE's were an unexpected adverse event in the dose

escalation study and could reappear in this study.

Low

Iclusig CML/ ALL Pricing and reimbursement decisions

from several EU countries

2015 The EMA is expected to complete its review of the Iclusig label

which should help pave the way for reimbursement discussions

with EU regulators

Medium

AP26113 ALK+, Xalkori

resistant NSCLC

Data from of pivotal trial in ALK+, Xalkori

resistant NSCLC

H1:16 Pulmonary AE's were an unexpected adverse event in the dose

escalation study and could reappear in this study.

High

Iclusig CML/ ALL Potential approval in Japan Mid-2016 Not likely a signifcant catalyst Low

Source: Company data, Credit Suisse estimates

Bind Therapeutics (BIND)

When do you expect to report data from the Phase II prostate cancer study for BIND-014?

Trial completed enrollment in February 2014. Primary completion date is listed as August

2014. Average expected follow up was 6 months.

Do you expect to report data from the KRAS-positive NSCLC trial for BIND-014 in 2015?

What is the likely venue? What do you need to see to support a move to Phase III? Could

the Phase II be expanded to become pivotal?

For the new trials of BIND-014 that you plan to initiate in 2015 for bladder, cervical,

cholangio, and neuroendocrine cancer, is there specific rationale for these tumor types?

When do you expect to report initial results? When do you expect to start the trials?

You are also testing a weekly schedule for BIND-014. Is there any reason to expect that

data to be substantially different than every three weeks? What will you need to see to

move that schedule forward?

What advances do you expect from partners' programs in 2015?

Exhibit 4: BIND News Flow

Product/Event Indication Catalyst Expected Date CommentsPrice

Sensitivity

BIND-014 mCRPC Phase II Q3W dosing data Early 2015 This study will provide insight into the activity of BIND-014

in a second setting

High

BIND-014 Bladder, cervical, cholangio,

and neuroendocrine

Initiate new Phase II trial Early 2015 One or more of these indications could provide a more

rapid path to market than lung or prostate cancer

Low

BIND-014 Bladder, cervical, cholangio,

and neuroendocrine

Stage I data from Phase II 2015 This could help expand potential indications for BIND-014 High

BIND-014 NSCLC and mCRPC Phase II data for weekly

schedule

2015 BIND intends to pursue the Q3W dosing for NSCLC going

forward suggesting that these data are not promising

Low

Partnered program N/A IND submission 2015 Could trigger modest milestone payment Low

BIND-510 N/A IND submission 2016 This is an Accurin formulation of vincristine Low Source: Company data, Credit Suisse estimates

07 January 2015

SMID Cap Biotechnology 5

Endocyte (ECYT)

When do you expect to report initial data from the Phase I of EC1169 (PSMA-tubulysin) in

prostate cancer? Primary completion on ClinicalTrials.gov is listed as June 2015; is ASCO

the likely venue?

When do you expect updated Phase I data for EC1456 (FR-tubulysin) in solid tumors?

Primary completion is listed as June 2015; is ASCO the likely venue? When do you expect

to have data from expansion cohorts from the Phase I trial?

What do you need to see from the final OS data in lung cancer to make a "go" decision for

vintafolide? When do you expect to have the data to make a decision on vintafolide? What

would make you choose vintafolide over EC1456 for future development?

Do you expect to partner either the technology or any of your product candidates in 2015?

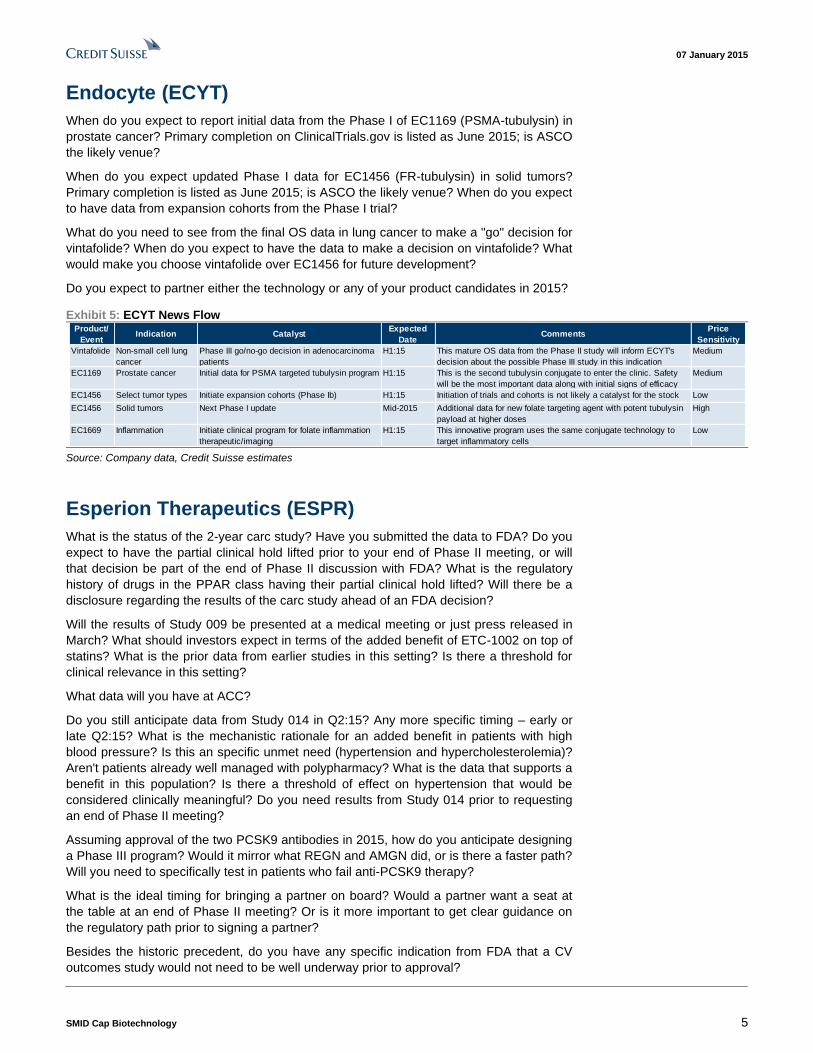

Exhibit 5: ECYT News Flow

Product/

EventIndication Catalyst

Expected

DateComments

Price

Sensitivity

Vintafolide Non-small cell lung

cancer

Phase III go/no-go decision in adenocarcinoma

patients

H1:15 This mature OS data from the Phase II study will inform ECYT's

decision about the possible Phase III study in this indication

Medium

EC1169 Prostate cancer Initial data for PSMA targeted tubulysin program H1:15 This is the second tubulysin conjugate to enter the clinic. Safety

will be the most important data along with initial signs of efficacy

Medium

EC1456 Select tumor types Initiate expansion cohorts (Phase Ib) H1:15 Initiation of trials and cohorts is not likely a catalyst for the stock Low

EC1456 Solid tumors Next Phase I update Mid-2015 Additional data for new folate targeting agent with potent tubulysin

payload at higher doses

High

EC1669 Inflammation Initiate clinical program for folate inflammation

therapeutic/imaging

H1:15 This innovative program uses the same conjugate technology to

target inflammatory cells

Low

Source: Company data, Credit Suisse estimates

Esperion Therapeutics (ESPR)

What is the status of the 2-year carc study? Have you submitted the data to FDA? Do you

expect to have the partial clinical hold lifted prior to your end of Phase II meeting, or will

that decision be part of the end of Phase II discussion with FDA? What is the regulatory

history of drugs in the PPAR class having their partial clinical hold lifted? Will there be a

disclosure regarding the results of the carc study ahead of an FDA decision?

Will the results of Study 009 be presented at a medical meeting or just press released in

March? What should investors expect in terms of the added benefit of ETC-1002 on top of

statins? What is the prior data from earlier studies in this setting? Is there a threshold for

clinical relevance in this setting?

What data will you have at ACC?

Do you still anticipate data from Study 014 in Q2:15? Any more specific timing – early or

late Q2:15? What is the mechanistic rationale for an added benefit in patients with high

blood pressure? Is this an specific unmet need (hypertension and hypercholesterolemia)?

Aren't patients already well managed with polypharmacy? What is the data that supports a

benefit in this population? Is there a threshold of effect on hypertension that would be

considered clinically meaningful? Do you need results from Study 014 prior to requesting

an end of Phase II meeting?

Assuming approval of the two PCSK9 antibodies in 2015, how do you anticipate designing

a Phase III program? Would it mirror what REGN and AMGN did, or is there a faster path?

Will you need to specifically test in patients who fail anti-PCSK9 therapy?

What is the ideal timing for bringing a partner on board? Would a partner want a seat at

the table at an end of Phase II meeting? Or is it more important to get clear guidance on

the regulatory path prior to signing a partner?

Besides the historic precedent, do you have any specific indication from FDA that a CV

outcomes study would not need to be well underway prior to approval?

07 January 2015

SMID Cap Biotechnology 6

Exhibit 6: ESPR News Flow

Product/Event Indication CatalystExpected

DateComments

Price

Sensitivity

ETC-1002

(regulatory)

LDL-C lowering 2-year carc. study in

animals

Early

2015

The results were collected in late 2014, and we expect ESPR

will announce that the results are positive and supportive of

lifting the partial clinical hold.

Medium

ETC-1002 LDL-C lowering- Residual risk,

statin add-on

Phase IIb trial readout

(Study-009)

March,

2015

The largest portion of the market is for patients not adquately

controlled on statins. We expect ETC-1002 will provide a

modest and statistically significant reduction of LDL-C on top

of statins

High

ETC-1002 LDL-C lowering Lifting of partial clinical

hold

H1:15 The partial clinical hold limits human testing to a 6 month

duration until full animal toxicity data is available, including 2-

year carcinogenicity studies. Lifting the partial hold is

essential for starting Phase III testing.

High

ETC-1002 LDL-C lowering - both

hypercholesterolemia and

hypertension

Phase IIb data (Study-

014)

Q2:15 ETC-1002 has shown modest blood pressure lowering and

may have added benefit in patients that have high blood

pressure on top of their high cholesterol.

Medium

ETC-1002 LDL-C lowering End of Phase II meeting Mid-2015 The most important question(s) to be answered in this meeting

include (1) the design and size of the Phase III program, and

(2) will a cardiovascular outcome study be required prior to

approval.

High

ETC-1002 LDL-C lowering Start Phase III study Q4:15 The Phase III trial start will already be assumed and in the

stock price if all other events in 2015 are positive.

Low

Source: Company data, Credit Suisse estimates

Immunogen (IMGN)

How does the failure of the MARIANNE trial change your view of the Kadcyla opportunity?

Does this have a negative read through to adjuvant?

Does the failure of the MARIANNE trial change your internal spending plans in any way?

What data do you expect to have at ASCO this year? IMGN853? IMGN289?

What do you need to see from IMGN853 to determine to move it forward?

What is the evidence that IMGN289 does not cause skin toxicity? Other EGFR antibodies

are known to cause skin toxicity?

How is IMGN779 differentiated from SGEN's SGN-CD33A? Is there a development

strategy that could potentially move that drug faster than SGEN's.

What are the next steps for IMGN529 in non-Hodgkin's lymphoma? Where does that drug

fit in, given the very competitive landscape in NHL?

Which partnered programs do you expect will generate new clinical data in 2015?

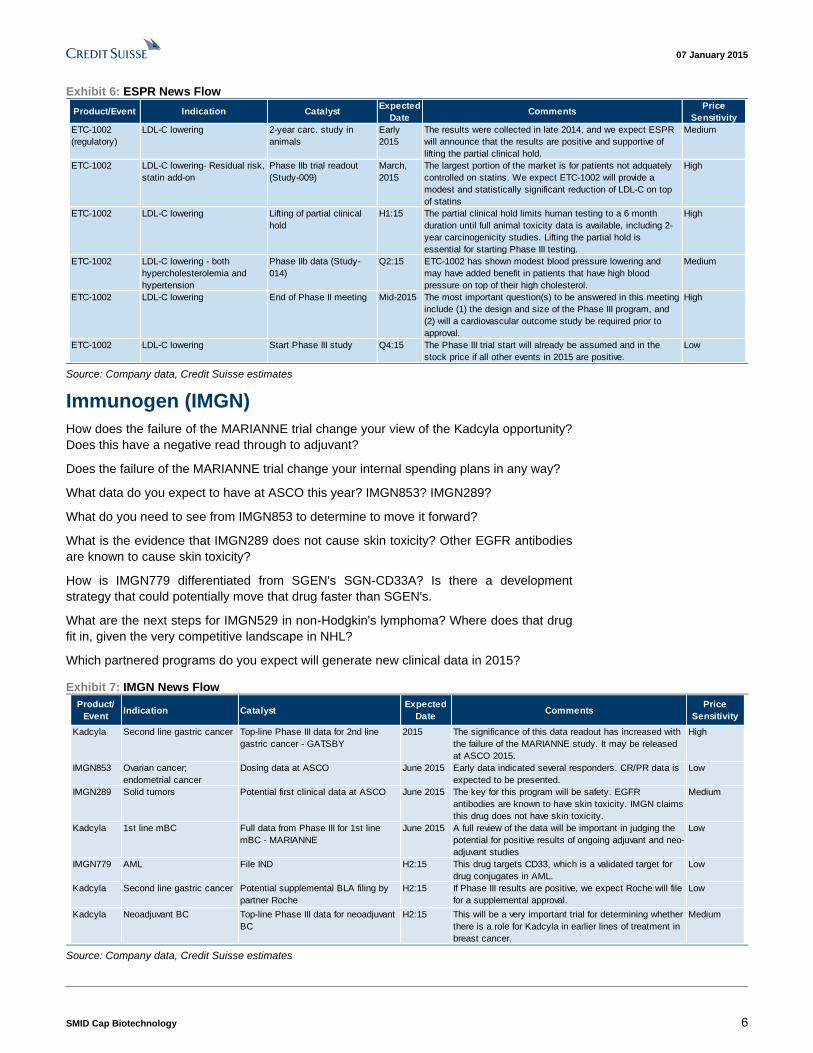

Exhibit 7: IMGN News Flow

Product/

EventIndication Catalyst

Expected

DateComments

Price

Sensitivity

Kadcyla Second line gastric cancer Top-line Phase III data for 2nd line

gastric cancer - GATSBY

2015 The significance of this data readout has increased with

the failure of the MARIANNE study. It may be released

at ASCO 2015.

High

IMGN853 Ovarian cancer;

endometrial cancer

Dosing data at ASCO June 2015 Early data indicated several responders. CR/PR data is

expected to be presented.

Low

IMGN289 Solid tumors Potential first clinical data at ASCO June 2015 The key for this program will be safety. EGFR

antibodies are known to have skin toxicity. IMGN claims

this drug does not have skin toxicity.

Medium

Kadcyla 1st line mBC Full data from Phase III for 1st line

mBC - MARIANNE

June 2015 A full review of the data will be important in judging the

potential for positive results of ongoing adjuvant and neo-

adjuvant studies

Low

IMGN779 AML File IND H2:15 This drug targets CD33, which is a validated target for

drug conjugates in AML.

Low

Kadcyla Second line gastric cancer Potential supplemental BLA filing by

partner Roche

H2:15 If Phase III results are positive, we expect Roche will file

for a supplemental approval.

Low

Kadcyla Neoadjuvant BC Top-line Phase III data for neoadjuvant

BC

H2:15 This will be a very important trial for determining whether

there is a role for Kadcyla in earlier lines of treatment in

breast cancer.

Medium

Source: Company data, Credit Suisse estimates

07 January 2015

SMID Cap Biotechnology 7

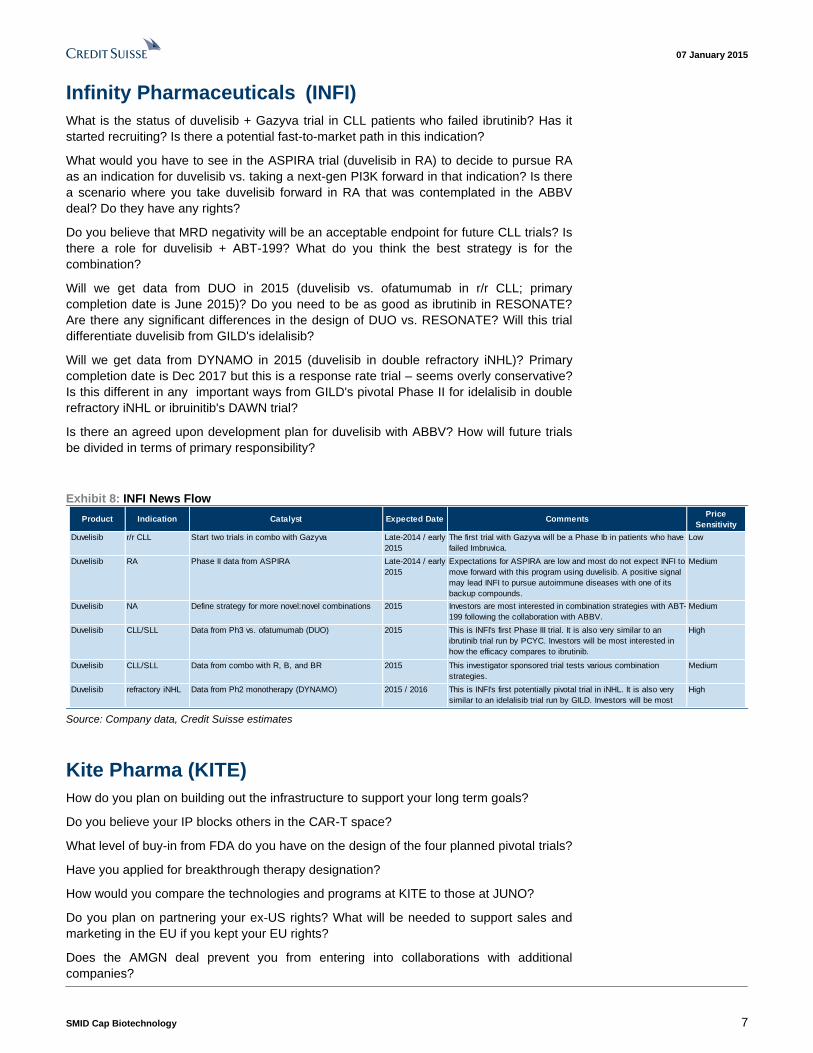

Infinity Pharmaceuticals (INFI)

What is the status of duvelisib + Gazyva trial in CLL patients who failed ibrutinib? Has it

started recruiting? Is there a potential fast-to-market path in this indication?

What would you have to see in the ASPIRA trial (duvelisib in RA) to decide to pursue RA

as an indication for duvelisib vs. taking a next-gen PI3K forward in that indication? Is there

a scenario where you take duvelisib forward in RA that was contemplated in the ABBV

deal? Do they have any rights?

Do you believe that MRD negativity will be an acceptable endpoint for future CLL trials? Is

there a role for duvelisib + ABT-199? What do you think the best strategy is for the

combination?

Will we get data from DUO in 2015 (duvelisib vs. ofatumumab in r/r CLL; primary

completion date is June 2015)? Do you need to be as good as ibrutinib in RESONATE?

Are there any significant differences in the design of DUO vs. RESONATE? Will this trial

differentiate duvelisib from GILD's idelalisib?

Will we get data from DYNAMO in 2015 (duvelisib in double refractory iNHL)? Primary

completion date is Dec 2017 but this is a response rate trial – seems overly conservative?

Is this different in any important ways from GILD's pivotal Phase II for idelalisib in double

refractory iNHL or ibruinitib's DAWN trial?

Is there an agreed upon development plan for duvelisib with ABBV? How will future trials

be divided in terms of primary responsibility?

Exhibit 8: INFI News Flow

Product Indication Catalyst Expected Date CommentsPrice

Sensitivity

Duvelisib r/r CLL Start two trials in combo with Gazyva Late-2014 / early

2015

The first trial with Gazyva will be a Phase Ib in patients who have

failed Imbruvica.

Low

Duvelisib RA Phase II data from ASPIRA Late-2014 / early

2015

Expectations for ASPIRA are low and most do not expect INFI to

move forward with this program using duvelisib. A positive signal

may lead INFI to pursue autoimmune diseases with one of its

backup compounds.

Medium

Duvelisib NA Define strategy for more novel:novel combinations 2015 Investors are most interested in combination strategies with ABT-

199 following the collaboration with ABBV.

Medium

Duvelisib CLL/SLL Data from Ph3 vs. ofatumumab (DUO) 2015 This is INFI's first Phase III trial. It is also very similar to an

ibrutinib trial run by PCYC. Investors will be most interested in

how the efficacy compares to ibrutinib.

High

Duvelisib CLL/SLL Data from combo with R, B, and BR 2015 This investigator sponsored trial tests various combination

strategies.

Medium

Duvelisib refractory iNHL Data from Ph2 monotherapy (DYNAMO) 2015 / 2016 This is INFI's first potentially pivotal trial in iNHL. It is also very

similar to an idelalisib trial run by GILD. Investors will be most

interested in how the efficacy compares to idelalisib.

High

Source: Company data, Credit Suisse estimates

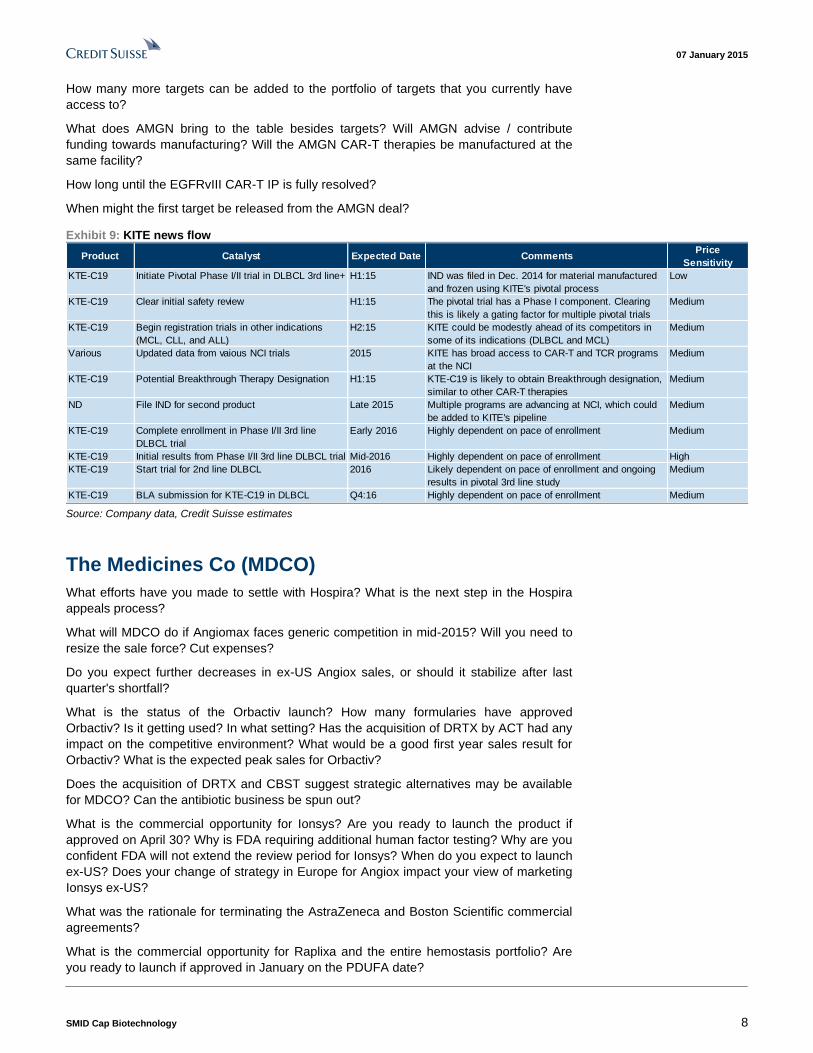

Kite Pharma (KITE)

How do you plan on building out the infrastructure to support your long term goals?

Do you believe your IP blocks others in the CAR-T space?

What level of buy-in from FDA do you have on the design of the four planned pivotal trials?

Have you applied for breakthrough therapy designation?

How would you compare the technologies and programs at KITE to those at JUNO?

Do you plan on partnering your ex-US rights? What will be needed to support sales and

marketing in the EU if you kept your EU rights?

Does the AMGN deal prevent you from entering into collaborations with additional

companies?

07 January 2015

SMID Cap Biotechnology 8

How many more targets can be added to the portfolio of targets that you currently have

access to?

What does AMGN bring to the table besides targets? Will AMGN advise / contribute

funding towards manufacturing? Will the AMGN CAR-T therapies be manufactured at the

same facility?

How long until the EGFRvIII CAR-T IP is fully resolved?

When might the first target be released from the AMGN deal?

Exhibit 9: KITE news flow

Product Catalyst Expected Date CommentsPrice

Sensitivity

KTE-C19 Initiate Pivotal Phase I/II trial in DLBCL 3rd line+ H1:15 IND was filed in Dec. 2014 for material manufactured

and frozen using KITE's pivotal process

Low

KTE-C19 Clear initial safety review H1:15 The pivotal trial has a Phase I component. Clearing

this is likely a gating factor for multiple pivotal trials

Medium

KTE-C19 Begin registration trials in other indications

(MCL, CLL, and ALL)

H2:15 KITE could be modestly ahead of its competitors in

some of its indications (DLBCL and MCL)

Medium

Various Updated data from vaious NCI trials 2015 KITE has broad access to CAR-T and TCR programs

at the NCI

Medium

KTE-C19 Potential Breakthrough Therapy Designation H1:15 KTE-C19 is likely to obtain Breakthrough designation,

similar to other CAR-T therapies

Medium

ND File IND for second product Late 2015 Multiple programs are advancing at NCI, which could

be added to KITE's pipeline

Medium

KTE-C19 Complete enrollment in Phase I/II 3rd line

DLBCL trial

Early 2016 Highly dependent on pace of enrollment Medium

KTE-C19 Initial results from Phase I/II 3rd line DLBCL trial Mid-2016 Highly dependent on pace of enrollment High

KTE-C19 Start trial for 2nd line DLBCL 2016 Likely dependent on pace of enrollment and ongoing

results in pivotal 3rd line study

Medium

KTE-C19 BLA submission for KTE-C19 in DLBCL Q4:16 Highly dependent on pace of enrollment Medium Source: Company data, Credit Suisse estimates

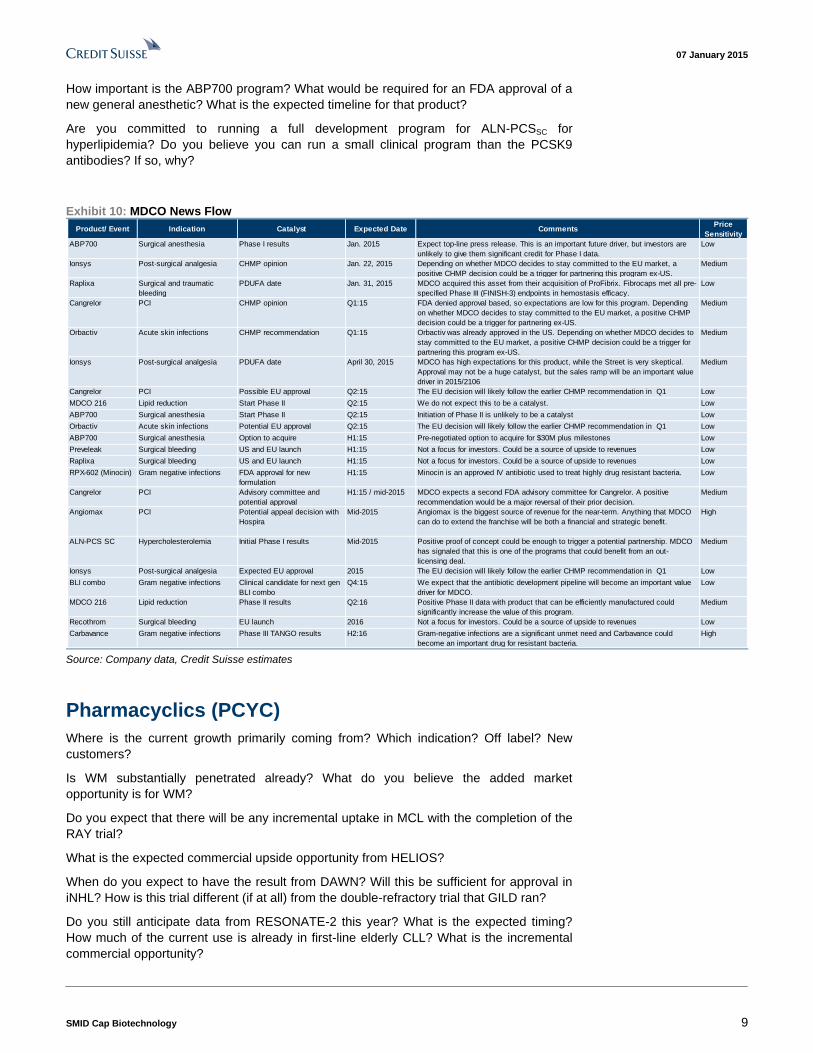

The Medicines Co (MDCO)

What efforts have you made to settle with Hospira? What is the next step in the Hospira

appeals process?

What will MDCO do if Angiomax faces generic competition in mid-2015? Will you need to

resize the sale force? Cut expenses?

Do you expect further decreases in ex-US Angiox sales, or should it stabilize after last

quarter's shortfall?

What is the status of the Orbactiv launch? How many formularies have approved

Orbactiv? Is it getting used? In what setting? Has the acquisition of DRTX by ACT had any

impact on the competitive environment? What would be a good first year sales result for

Orbactiv? What is the expected peak sales for Orbactiv?

Does the acquisition of DRTX and CBST suggest strategic alternatives may be available

for MDCO? Can the antibiotic business be spun out?

What is the commercial opportunity for Ionsys? Are you ready to launch the product if

approved on April 30? Why is FDA requiring additional human factor testing? Why are you

confident FDA will not extend the review period for Ionsys? When do you expect to launch

ex-US? Does your change of strategy in Europe for Angiox impact your view of marketing

Ionsys ex-US?

What was the rationale for terminating the AstraZeneca and Boston Scientific commercial

agreements?

What is the commercial opportunity for Raplixa and the entire hemostasis portfolio? Are

you ready to launch if approved in January on the PDUFA date?

07 January 2015

SMID Cap Biotechnology 9

How important is the ABP700 program? What would be required for an FDA approval of a

new general anesthetic? What is the expected timeline for that product?

Are you committed to running a full development program for ALN-PCSSC for

hyperlipidemia? Do you believe you can run a small clinical program than the PCSK9

antibodies? If so, why?

Exhibit 10: MDCO News Flow

Product/ Event Indication Catalyst Expected Date CommentsPrice

Sensitivity

ABP700 Surgical anesthesia Phase I results Jan. 2015 Expect top-line press release. This is an important future driver, but investors are

unlikely to give them significant credit for Phase I data.

Low

Ionsys Post-surgical analgesia CHMP opinion Jan. 22, 2015 Depending on whether MDCO decides to stay committed to the EU market, a

positive CHMP decision could be a trigger for partnering this program ex-US.

Medium

Raplixa Surgical and traumatic

bleeding

PDUFA date Jan. 31, 2015 MDCO acquired this asset from their acquisition of ProFibrix. Fibrocaps met all pre-

specified Phase III (FINISH-3) endpoints in hemostasis efficacy.

Low

Cangrelor PCI CHMP opinion Q1:15 FDA denied approval based, so expectations are low for this program. Depending

on whether MDCO decides to stay committed to the EU market, a positive CHMP

decision could be a trigger for partnering ex-US.

Medium

Orbactiv Acute skin infections CHMP recommendation Q1:15 Orbactiv was already approved in the US. Depending on whether MDCO decides to

stay committed to the EU market, a positive CHMP decision could be a trigger for

partnering this program ex-US.

Medium

Ionsys Post-surgical analgesia PDUFA date April 30, 2015 MDCO has high expectations for this product, while the Street is very skeptical.

Approval may not be a huge catalyst, but the sales ramp will be an important value

driver in 2015/2106

Medium

Cangrelor PCI Possible EU approval Q2:15 The EU decision will likely follow the earlier CHMP recommendation in Q1 Low

MDCO 216 Lipid reduction Start Phase II Q2:15 We do not expect this to be a catalyst. Low

ABP700 Surgical anesthesia Start Phase II Q2:15 Initiation of Phase II is unlikely to be a catalyst Low

Orbactiv Acute skin infections Potential EU approval Q2:15 The EU decision will likely follow the earlier CHMP recommendation in Q1 Low

ABP700 Surgical anesthesia Option to acquire H1:15 Pre-negotiated option to acquire for $30M plus milestones Low

Preveleak Surgical bleeding US and EU launch H1:15 Not a focus for investors. Could be a source of upside to revenues Low

Raplixa Surgical bleeding US and EU launch H1:15 Not a focus for investors. Could be a source of upside to revenues Low

RPX-602 (Minocin) Gram negative infections FDA approval for new

formulation

H1:15 Minocin is an approved IV antibiotic used to treat highly drug resistant bacteria. Low

Cangrelor PCI Advisory committee and

potential approval

H1:15 / mid-2015 MDCO expects a second FDA advisory committee for Cangrelor. A positive

recommendation would be a major reversal of their prior decision.

Medium

Angiomax PCI Potential appeal decision with

Hospira

Mid-2015 Angiomax is the biggest source of revenue for the near-term. Anything that MDCO

can do to extend the franchise will be both a financial and strategic benefit.

High

ALN-PCS SC Hypercholesterolemia Initial Phase I results Mid-2015 Positive proof of concept could be enough to trigger a potential partnership. MDCO

has signaled that this is one of the programs that could benefit from an out-

licensing deal.

Medium

Ionsys Post-surgical analgesia Expected EU approval 2015 The EU decision will likely follow the earlier CHMP recommendation in Q1 Low

BLI combo Gram negative infections Clinical candidate for next gen

BLI combo

Q4:15 We expect that the antibiotic development pipeline will become an important value

driver for MDCO.

Low

MDCO 216 Lipid reduction Phase II results Q2:16 Positive Phase II data with product that can be efficiently manufactured could

significantly increase the value of this program.

Medium

Recothrom Surgical bleeding EU launch 2016 Not a focus for investors. Could be a source of upside to revenues Low

Carbavance Gram negative infections Phase III TANGO results H2:16 Gram-negative infections are a significant unmet need and Carbavance could

become an important drug for resistant bacteria.

High

Source: Company data, Credit Suisse estimates

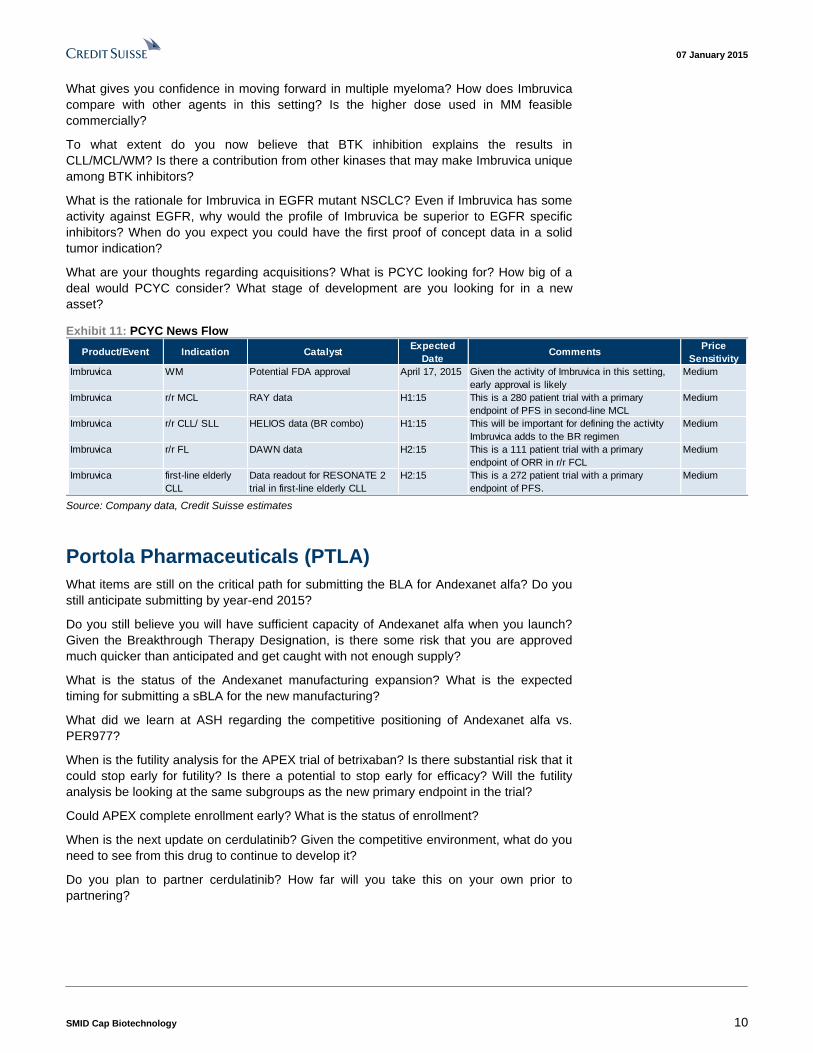

Pharmacyclics (PCYC)

Where is the current growth primarily coming from? Which indication? Off label? New

customers?

Is WM substantially penetrated already? What do you believe the added market

opportunity is for WM?

Do you expect that there will be any incremental uptake in MCL with the completion of the

RAY trial?

What is the expected commercial upside opportunity from HELIOS?

When do you expect to have the result from DAWN? Will this be sufficient for approval in

iNHL? How is this trial different (if at all) from the double-refractory trial that GILD ran?

Do you still anticipate data from RESONATE-2 this year? What is the expected timing?

How much of the current use is already in first-line elderly CLL? What is the incremental

commercial opportunity?

07 January 2015

SMID Cap Biotechnology 10

What gives you confidence in moving forward in multiple myeloma? How does Imbruvica

compare with other agents in this setting? Is the higher dose used in MM feasible

commercially?

To what extent do you now believe that BTK inhibition explains the results in

CLL/MCL/WM? Is there a contribution from other kinases that may make Imbruvica unique

among BTK inhibitors?

What is the rationale for Imbruvica in EGFR mutant NSCLC? Even if Imbruvica has some

activity against EGFR, why would the profile of Imbruvica be superior to EGFR specific

inhibitors? When do you expect you could have the first proof of concept data in a solid

tumor indication?

What are your thoughts regarding acquisitions? What is PCYC looking for? How big of a

deal would PCYC consider? What stage of development are you looking for in a new

asset?

Exhibit 11: PCYC News Flow

Product/Event Indication CatalystExpected

DateComments

Price

Sensitivity

Imbruvica WM Potential FDA approval April 17, 2015 Given the activity of Imbruvica in this setting,

early approval is likely

Medium

Imbruvica r/r MCL RAY data H1:15 This is a 280 patient trial with a primary

endpoint of PFS in second-line MCL

Medium

Imbruvica r/r CLL/ SLL HELIOS data (BR combo) H1:15 This will be important for defining the activity

Imbruvica adds to the BR regimen

Medium

Imbruvica r/r FL DAWN data H2:15 This is a 111 patient trial with a primary

endpoint of ORR in r/r FCL

Medium

Imbruvica first-line elderly

CLL

Data readout for RESONATE 2

trial in first-line elderly CLL

H2:15 This is a 272 patient trial with a primary

endpoint of PFS.

Medium

Source: Company data, Credit Suisse estimates

Portola Pharmaceuticals (PTLA)

What items are still on the critical path for submitting the BLA for Andexanet alfa? Do you

still anticipate submitting by year-end 2015?

Do you still believe you will have sufficient capacity of Andexanet alfa when you launch?

Given the Breakthrough Therapy Designation, is there some risk that you are approved

much quicker than anticipated and get caught with not enough supply?

What is the status of the Andexanet manufacturing expansion? What is the expected

timing for submitting a sBLA for the new manufacturing?

What did we learn at ASH regarding the competitive positioning of Andexanet alfa vs.

PER977?

When is the futility analysis for the APEX trial of betrixaban? Is there substantial risk that it

could stop early for futility? Is there a potential to stop early for efficacy? Will the futility

analysis be looking at the same subgroups as the new primary endpoint in the trial?

Could APEX complete enrollment early? What is the status of enrollment?

When is the next update on cerdulatinib? Given the competitive environment, what do you

need to see from this drug to continue to develop it?

Do you plan to partner cerdulatinib? How far will you take this on your own prior to

partnering?

07 January 2015

SMID Cap Biotechnology 11

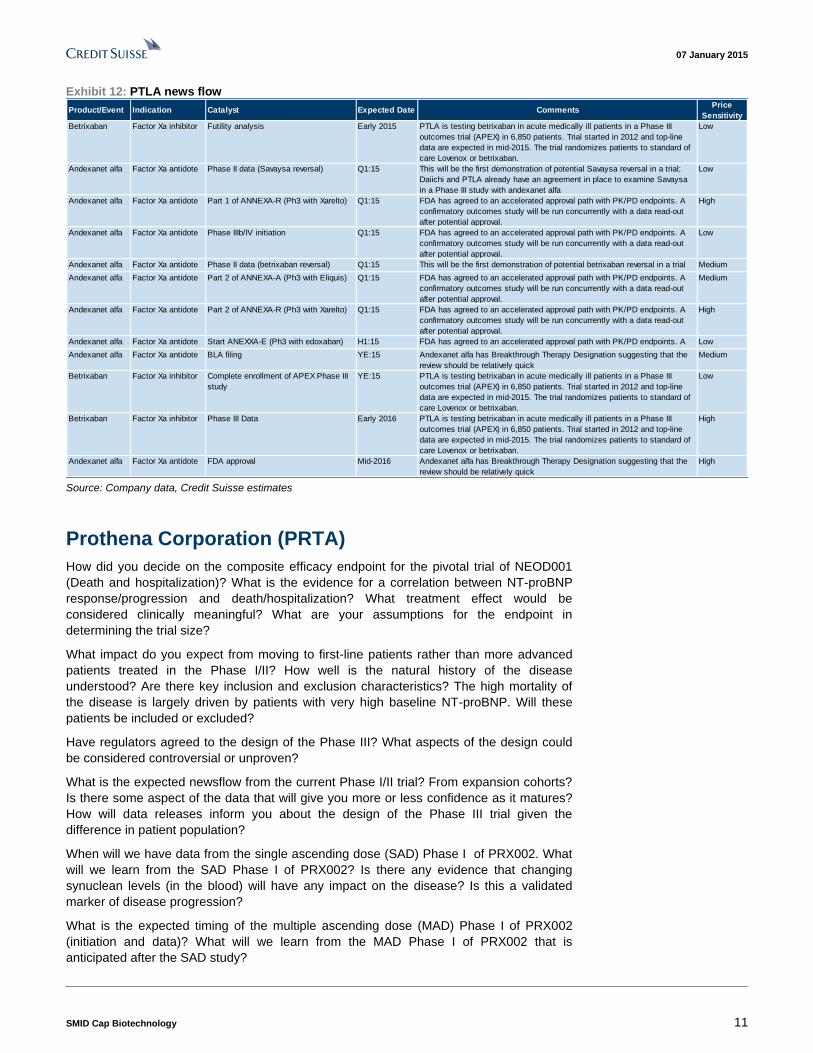

Exhibit 12: PTLA news flow

Product/Event Indication Catalyst Expected Date CommentsPrice

Sensitivity

Betrixaban Factor Xa inhibitor Futility analysis Early 2015 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

Low

Andexanet alfa Factor Xa antidote Phase II data (Savaysa reversal) Q1:15 This will be the first demonstration of potential Savaysa reversal in a trial;

Daiichi and PTLA already have an agreement in place to examine Savaysa

in a Phase III study with andexanet alfa

Low

Andexanet alfa Factor Xa antidote Part 1 of ANNEXA-R (Ph3 with Xarelto) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

High

Andexanet alfa Factor Xa antidote Phase IIIb/IV initiation Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

Low

Andexanet alfa Factor Xa antidote Phase II data (betrixaban reversal) Q1:15 This will be the first demonstration of potential betrixaban reversal in a trial Medium

Andexanet alfa Factor Xa antidote Part 2 of ANNEXA-A (Ph3 with Eliquis) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

Medium

Andexanet alfa Factor Xa antidote Part 2 of ANNEXA-R (Ph3 with Xarelto) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

High

Andexanet alfa Factor Xa antidote Start ANEXXA-E (Ph3 with edoxaban) H1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

Low

Andexanet alfa Factor Xa antidote BLA filing YE:15 Andexanet alfa has Breakthrough Therapy Designation suggesting that the

review should be relatively quick

Medium

Betrixaban Factor Xa inhibitor Complete enrollment of APEX Phase III

study

YE:15 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

Low

Betrixaban Factor Xa inhibitor Phase III Data Early 2016 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

High

Andexanet alfa Factor Xa antidote FDA approval Mid-2016 Andexanet alfa has Breakthrough Therapy Designation suggesting that the

review should be relatively quick

High

Source: Company data, Credit Suisse estimates

Prothena Corporation (PRTA)

How did you decide on the composite efficacy endpoint for the pivotal trial of NEOD001

(Death and hospitalization)? What is the evidence for a correlation between NT-proBNP

response/progression and death/hospitalization? What treatment effect would be

considered clinically meaningful? What are your assumptions for the endpoint in

determining the trial size?

What impact do you expect from moving to first-line patients rather than more advanced

patients treated in the Phase I/II? How well is the natural history of the disease

understood? Are there key inclusion and exclusion characteristics? The high mortality of

the disease is largely driven by patients with very high baseline NT-proBNP. Will these

patients be included or excluded?

Have regulators agreed to the design of the Phase III? What aspects of the design could

be considered controversial or unproven?

What is the expected newsflow from the current Phase I/II trial? From expansion cohorts?

Is there some aspect of the data that will give you more or less confidence as it matures?

How will data releases inform you about the design of the Phase III trial given the

difference in patient population?

When will we have data from the single ascending dose (SAD) Phase I of PRX002. What

will we learn from the SAD Phase I of PRX002? Is there any evidence that changing

synuclean levels (in the blood) will have any impact on the disease? Is this a validated

marker of disease progression?

What is the expected timing of the multiple ascending dose (MAD) Phase I of PRX002

(initiation and data)? What will we learn from the MAD Phase I of PRX002 that is

anticipated after the SAD study?

07 January 2015

SMID Cap Biotechnology 12

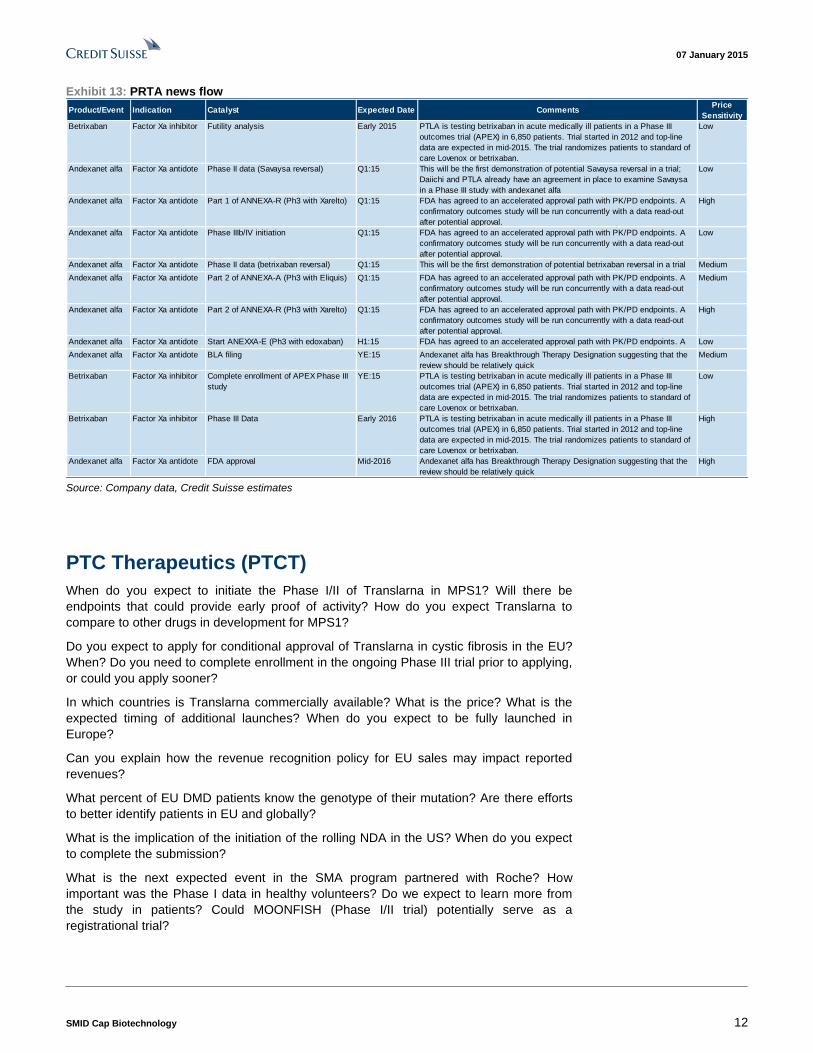

Exhibit 13: PRTA news flow

Product/Event Indication Catalyst Expected Date CommentsPrice

Sensitivity

Betrixaban Factor Xa inhibitor Futility analysis Early 2015 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

Low

Andexanet alfa Factor Xa antidote Phase II data (Savaysa reversal) Q1:15 This will be the first demonstration of potential Savaysa reversal in a trial;

Daiichi and PTLA already have an agreement in place to examine Savaysa

in a Phase III study with andexanet alfa

Low

Andexanet alfa Factor Xa antidote Part 1 of ANNEXA-R (Ph3 with Xarelto) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

High

Andexanet alfa Factor Xa antidote Phase IIIb/IV initiation Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

Low

Andexanet alfa Factor Xa antidote Phase II data (betrixaban reversal) Q1:15 This will be the first demonstration of potential betrixaban reversal in a trial Medium

Andexanet alfa Factor Xa antidote Part 2 of ANNEXA-A (Ph3 with Eliquis) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

Medium

Andexanet alfa Factor Xa antidote Part 2 of ANNEXA-R (Ph3 with Xarelto) Q1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

after potential approval.

High

Andexanet alfa Factor Xa antidote Start ANEXXA-E (Ph3 with edoxaban) H1:15 FDA has agreed to an accelerated approval path with PK/PD endpoints. A

confirmatory outcomes study will be run concurrently with a data read-out

Low

Andexanet alfa Factor Xa antidote BLA filing YE:15 Andexanet alfa has Breakthrough Therapy Designation suggesting that the

review should be relatively quick

Medium

Betrixaban Factor Xa inhibitor Complete enrollment of APEX Phase III

study

YE:15 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

Low

Betrixaban Factor Xa inhibitor Phase III Data Early 2016 PTLA is testing betrixaban in acute medically ill patients in a Phase III

outcomes trial (APEX) in 6,850 patients. Trial started in 2012 and top-line

data are expected in mid-2015. The trial randomizes patients to standard of

care Lovenox or betrixaban.

High

Andexanet alfa Factor Xa antidote FDA approval Mid-2016 Andexanet alfa has Breakthrough Therapy Designation suggesting that the

review should be relatively quick

High

Source: Company data, Credit Suisse estimates

PTC Therapeutics (PTCT)

When do you expect to initiate the Phase I/II of Translarna in MPS1? Will there be

endpoints that could provide early proof of activity? How do you expect Translarna to

compare to other drugs in development for MPS1?

Do you expect to apply for conditional approval of Translarna in cystic fibrosis in the EU?

When? Do you need to complete enrollment in the ongoing Phase III trial prior to applying,

or could you apply sooner?

In which countries is Translarna commercially available? What is the price? What is the

expected timing of additional launches? When do you expect to be fully launched in

Europe?

Can you explain how the revenue recognition policy for EU sales may impact reported

revenues?

What percent of EU DMD patients know the genotype of their mutation? Are there efforts

to better identify patients in EU and globally?

What is the implication of the initiation of the rolling NDA in the US? When do you expect

to complete the submission?

What is the next expected event in the SMA program partnered with Roche? How

important was the Phase I data in healthy volunteers? Do we expect to learn more from

the study in patients? Could MOONFISH (Phase I/II trial) potentially serve as a

registrational trial?

07 January 2015

SMID Cap Biotechnology 13

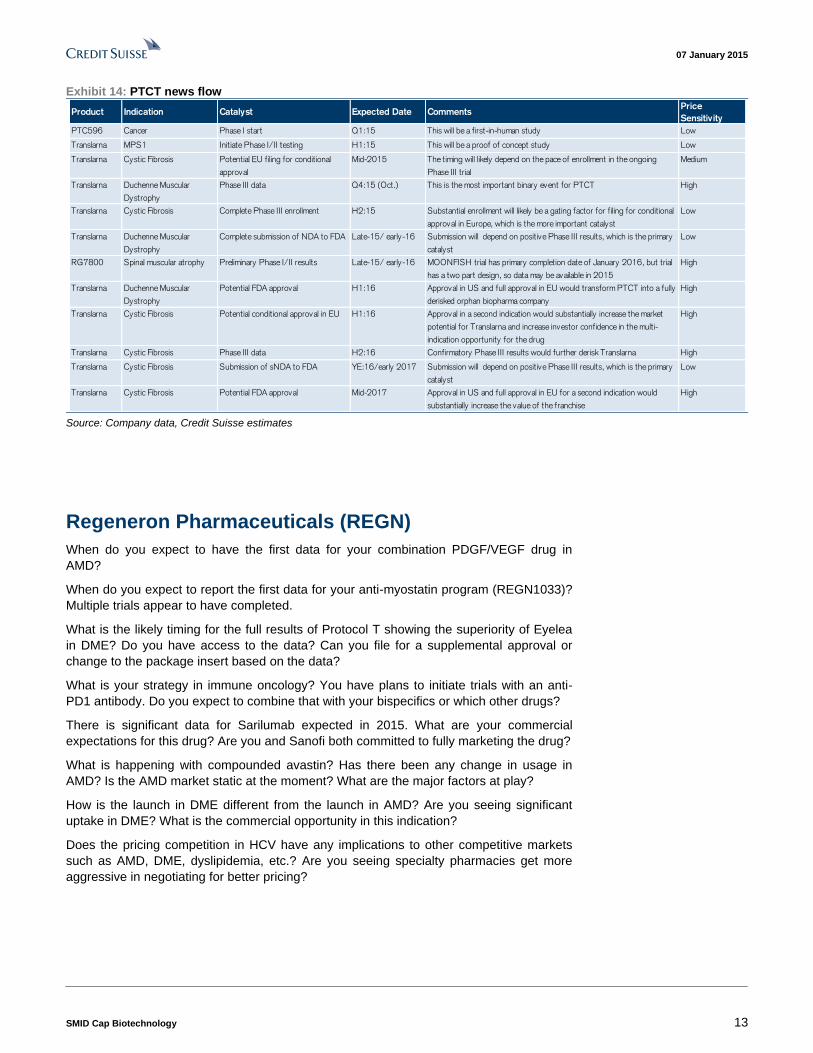

Exhibit 14: PTCT news flow

Product Indication Catalyst Expected Date CommentsPrice

Sensitivity

PTC596 Cancer Phase I start Q1:15 This will be a first-in-human study Low

Translarna MPS1 Initiate Phase I/II testing H1:15 This will be a proof of concept study Low

Translarna Cystic Fibrosis Potential EU filing for conditional

approval

Mid-2015 The timing will likely depend on the pace of enrollment in the ongoing

Phase III trial

Medium

Translarna Duchenne Muscular

Dystrophy

Phase III data Q4:15 (Oct.) This is the most important binary event for PTCT High

Translarna Cystic Fibrosis Complete Phase III enrollment H2:15 Substantial enrollment will likely be a gating factor for filing for conditional

approval in Europe, which is the more important catalyst

Low

Translarna Duchenne Muscular

Dystrophy

Complete submission of NDA to FDA Late-15/ early-16 Submission will depend on positive Phase III results, which is the primary

catalyst

Low

RG7800 Spinal muscular atrophy Preliminary Phase I/II results Late-15/ early-16 MOONFISH trial has primary completion date of January 2016, but trial

has a two part design, so data may be available in 2015

High

Translarna Duchenne Muscular

Dystrophy

Potential FDA approval H1:16 Approval in US and full approval in EU would transform PTCT into a fully

derisked orphan biopharma company

High

Translarna Cystic Fibrosis Potential conditional approval in EU H1:16 Approval in a second indication would substantially increase the market

potential for Translarna and increase investor confidence in the multi-

indication opportunity for the drug

High

Translarna Cystic Fibrosis Phase III data H2:16 Confirmatory Phase III results would further derisk Translarna High

Translarna Cystic Fibrosis Submission of sNDA to FDA YE:16/early 2017 Submission will depend on positive Phase III results, which is the primary

catalyst

Low

Translarna Cystic Fibrosis Potential FDA approval Mid-2017 Approval in US and full approval in EU for a second indication would

substantially increase the value of the franchise

High

Source: Company data, Credit Suisse estimates

Regeneron Pharmaceuticals (REGN)

When do you expect to have the first data for your combination PDGF/VEGF drug in

AMD?

When do you expect to report the first data for your anti-myostatin program (REGN1033)?

Multiple trials appear to have completed.

What is the likely timing for the full results of Protocol T showing the superiority of Eyelea

in DME? Do you have access to the data? Can you file for a supplemental approval or

change to the package insert based on the data?

What is your strategy in immune oncology? You have plans to initiate trials with an anti-

PD1 antibody. Do you expect to combine that with your bispecifics or which other drugs?

There is significant data for Sarilumab expected in 2015. What are your commercial

expectations for this drug? Are you and Sanofi both committed to fully marketing the drug?

What is happening with compounded avastin? Has there been any change in usage in

AMD? Is the AMD market static at the moment? What are the major factors at play?

How is the launch in DME different from the launch in AMD? Are you seeing significant

uptake in DME? What is the commercial opportunity in this indication?

Does the pricing competition in HCV have any implications to other competitive markets

such as AMD, DME, dyslipidemia, etc.? Are you seeing specialty pharmacies get more

aggressive in negotiating for better pricing?

07 January 2015

SMID Cap Biotechnology 14

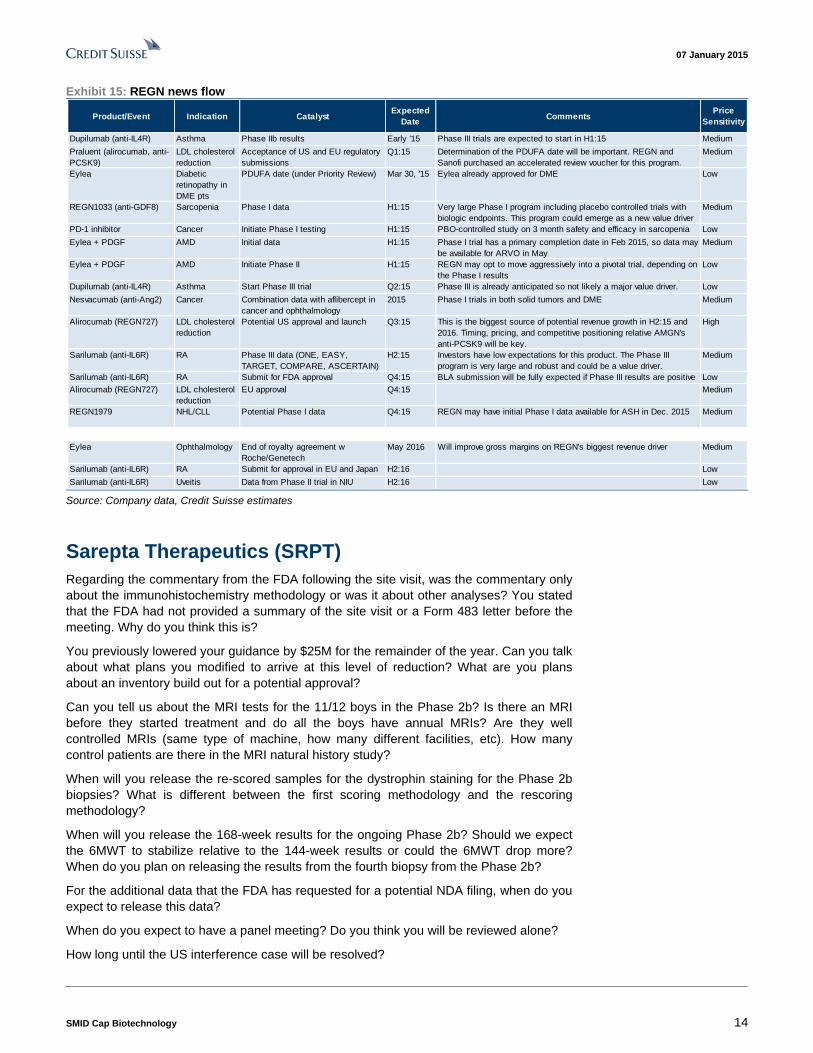

Exhibit 15: REGN news flow

Product/Event Indication CatalystExpected

DateComments

Price

Sensitivity

Dupilumab (anti-IL4R) Asthma Phase IIb results Early '15 Phase III trials are expected to start in H1:15 Medium

Praluent (alirocumab, anti-

PCSK9)

LDL cholesterol

reduction

Acceptance of US and EU regulatory

submissions

Q1:15 Determination of the PDUFA date will be important. REGN and

Sanofi purchased an accelerated review voucher for this program.

Medium

Eylea Diabetic

retinopathy in

DME pts

PDUFA date (under Priority Review) Mar 30, '15 Eylea already approved for DME Low

REGN1033 (anti-GDF8) Sarcopenia Phase I data H1:15 Very large Phase I program including placebo controlled trials with

biologic endpoints. This program could emerge as a new value driver

Medium

PD-1 inhibitor Cancer Initiate Phase I testing H1:15 PBO-controlled study on 3 month safety and efficacy in sarcopenia Low

Eylea + PDGF AMD Initial data H1:15 Phase I trial has a primary completion date in Feb 2015, so data may

be available for ARVO in May

Medium

Eylea + PDGF AMD Initiate Phase II H1:15 REGN may opt to move aggressively into a pivotal trial, depending on

the Phase I results

Low

Dupilumab (anti-IL4R) Asthma Start Phase III trial Q2:15 Phase III is already anticipated so not likely a major value driver. Low

Nesvacumab (anti-Ang2) Cancer Combination data with aflibercept in

cancer and ophthalmology

2015 Phase I trials in both solid tumors and DME Medium

Alirocumab (REGN727) LDL cholesterol

reduction

Potential US approval and launch Q3:15 This is the biggest source of potential revenue growth in H2:15 and

2016. Timing, pricing, and competitive positioning relative AMGN's

anti-PCSK9 will be key.

High

Sarilumab (anti-IL6R) RA Phase III data (ONE, EASY,

TARGET, COMPARE, ASCERTAIN)

H2:15 Investors have low expectations for this product. The Phase III

program is very large and robust and could be a value driver.

Medium

Sarilumab (anti-IL6R) RA Submit for FDA approval Q4:15 BLA submission will be fully expected if Phase III results are positive Low

Alirocumab (REGN727) LDL cholesterol

reduction

EU approval Q4:15 Medium

REGN1979 NHL/CLL Potential Phase I data Q4:15 REGN may have initial Phase I data available for ASH in Dec. 2015 Medium

Eylea Ophthalmology End of royalty agreement w

Roche/Genetech

May 2016 Will improve gross margins on REGN's biggest revenue driver Medium

Sarilumab (anti-IL6R) RA Submit for approval in EU and Japan H2:16 Low

Sarilumab (anti-IL6R) Uveitis Data from Phase II trial in NIU H2:16 Low Source: Company data, Credit Suisse estimates

Sarepta Therapeutics (SRPT)

Regarding the commentary from the FDA following the site visit, was the commentary only

about the immunohistochemistry methodology or was it about other analyses? You stated

that the FDA had not provided a summary of the site visit or a Form 483 letter before the

meeting. Why do you think this is?

You previously lowered your guidance by $25M for the remainder of the year. Can you talk

about what plans you modified to arrive at this level of reduction? What are you plans

about an inventory build out for a potential approval?

Can you tell us about the MRI tests for the 11/12 boys in the Phase 2b? Is there an MRI

before they started treatment and do all the boys have annual MRIs? Are they well

controlled MRIs (same type of machine, how many different facilities, etc). How many

control patients are there in the MRI natural history study?

When will you release the re-scored samples for the dystrophin staining for the Phase 2b

biopsies? What is different between the first scoring methodology and the rescoring

methodology?

When will you release the 168-week results for the ongoing Phase 2b? Should we expect

the 6MWT to stabilize relative to the 144-week results or could the 6MWT drop more?

When do you plan on releasing the results from the fourth biopsy from the Phase 2b?

For the additional data that the FDA has requested for a potential NDA filing, when do you

expect to release this data?

When do you expect to have a panel meeting? Do you think you will be reviewed alone?

How long until the US interference case will be resolved?

07 January 2015

SMID Cap Biotechnology 15

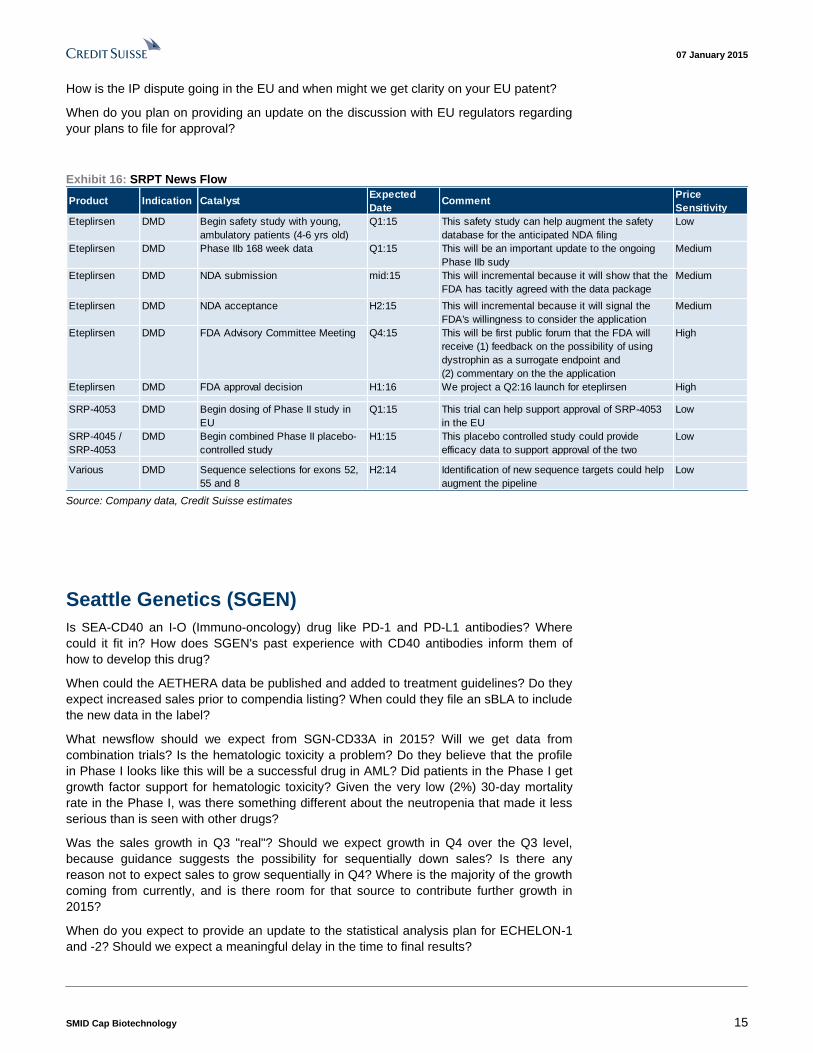

How is the IP dispute going in the EU and when might we get clarity on your EU patent?

When do you plan on providing an update on the discussion with EU regulators regarding

your plans to file for approval?

Exhibit 16: SRPT News Flow

Product Indication CatalystExpected

DateComment

Price

Sensitivity

Eteplirsen DMD Begin safety study with young,

ambulatory patients (4-6 yrs old)

Q1:15 This safety study can help augment the safety

database for the anticipated NDA filing

Low

Eteplirsen DMD Phase IIb 168 week data Q1:15 This will be an important update to the ongoing

Phase IIb sudy

Medium

Eteplirsen DMD NDA submission mid:15 This will incremental because it will show that the

FDA has tacitly agreed with the data package

Medium

Eteplirsen DMD NDA acceptance H2:15 This will incremental because it will signal the

FDA's willingness to consider the application

Medium

Eteplirsen DMD FDA Advisory Committee Meeting Q4:15 This will be first public forum that the FDA will

receive (1) feedback on the possibility of using

dystrophin as a surrogate endpoint and

(2) commentary on the the application

High

Eteplirsen DMD FDA approval decision H1:16 We project a Q2:16 launch for eteplirsen High

SRP-4053 DMD Begin dosing of Phase II study in

EU

Q1:15 This trial can help support approval of SRP-4053

in the EU

Low

SRP-4045 /

SRP-4053

DMD Begin combined Phase II placebo-

controlled study

H1:15 This placebo controlled study could provide

efficacy data to support approval of the two

Low

Various DMD Sequence selections for exons 52,

55 and 8

H2:14 Identification of new sequence targets could help

augment the pipeline

Low

Source: Company data, Credit Suisse estimates

Seattle Genetics (SGEN)

Is SEA-CD40 an I-O (Immuno-oncology) drug like PD-1 and PD-L1 antibodies? Where

could it fit in? How does SGEN's past experience with CD40 antibodies inform them of

how to develop this drug?

When could the AETHERA data be published and added to treatment guidelines? Do they

expect increased sales prior to compendia listing? When could they file an sBLA to include

the new data in the label?

What newsflow should we expect from SGN-CD33A in 2015? Will we get data from

combination trials? Is the hematologic toxicity a problem? Do they believe that the profile

in Phase I looks like this will be a successful drug in AML? Did patients in the Phase I get

growth factor support for hematologic toxicity? Given the very low (2%) 30-day mortality

rate in the Phase I, was there something different about the neutropenia that made it less

serious than is seen with other drugs?

Was the sales growth in Q3 "real"? Should we expect growth in Q4 over the Q3 level,

because guidance suggests the possibility for sequentially down sales? Is there any

reason not to expect sales to grow sequentially in Q4? Where is the majority of the growth

coming from currently, and is there room for that source to contribute further growth in

2015?

When do you expect to provide an update to the statistical analysis plan for ECHELON-1

and -2? Should we expect a meaningful delay in the time to final results?

07 January 2015

SMID Cap Biotechnology 16

How do you expect PD-1 inhibitors to impact the market opportunity for Adcetris? If PD-1

inhibitors are approved in relapsed/refractory HL, do you expect Adcetris sales to suffer?

How much? Is there a scientific rationale for the combination of Adcetris with a PD-1

inhibitor? Do you expect to start trials in 2015 testing the combination of Adcetris with a

PD-1 inhibitor?

Do you anticipate that the planned randomized Phase II trial of SGN-CD19A in second line

DLBCL could serve as a registrational trial? What is the expected combination for that

trial? When would you expect to have data?

When in 2015 do you expect to have the ALCANZA data (relapsed CTCL)? What is the

upside to sales based on positive results?

When could we see data from SGN-LIV1A? ASCO?

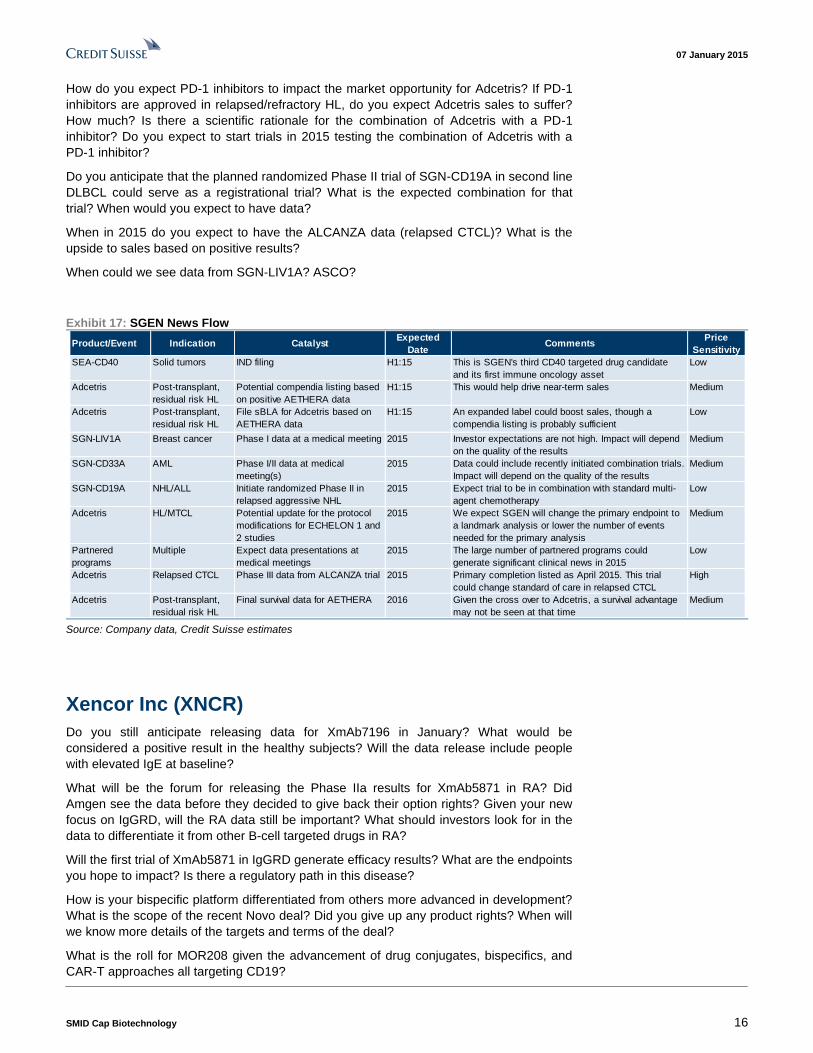

Exhibit 17: SGEN News Flow

Product/Event Indication CatalystExpected

DateComments

Price

Sensitivity

SEA-CD40 Solid tumors IND filing H1:15 This is SGEN's third CD40 targeted drug candidate

and its first immune oncology asset

Low

Adcetris Post-transplant,

residual risk HL

Potential compendia listing based

on positive AETHERA data

H1:15 This would help drive near-term sales Medium

Adcetris Post-transplant,

residual risk HL

File sBLA for Adcetris based on

AETHERA data

H1:15 An expanded label could boost sales, though a

compendia listing is probably sufficient

Low

SGN-LIV1A Breast cancer Phase I data at a medical meeting 2015 Investor expectations are not high. Impact will depend

on the quality of the results

Medium

SGN-CD33A AML Phase I/II data at medical

meeting(s)

2015 Data could include recently initiated combination trials.

Impact will depend on the quality of the results

Medium

SGN-CD19A NHL/ALL Initiate randomized Phase II in

relapsed aggressive NHL

2015 Expect trial to be in combination with standard multi-

agent chemotherapy

Low

Adcetris HL/MTCL Potential update for the protocol

modifications for ECHELON 1 and

2 studies

2015 We expect SGEN will change the primary endpoint to

a landmark analysis or lower the number of events

needed for the primary analysis

Medium

Partnered

programs

Multiple Expect data presentations at

medical meetings

2015 The large number of partnered programs could

generate significant clinical news in 2015

Low

Adcetris Relapsed CTCL Phase III data from ALCANZA trial 2015 Primary completion listed as April 2015. This trial

could change standard of care in relapsed CTCL

High

Adcetris Post-transplant,

residual risk HL

Final survival data for AETHERA 2016 Given the cross over to Adcetris, a survival advantage

may not be seen at that time

Medium

Source: Company data, Credit Suisse estimates

Xencor Inc (XNCR)

Do you still anticipate releasing data for XmAb7196 in January? What would be

considered a positive result in the healthy subjects? Will the data release include people

with elevated IgE at baseline?

What will be the forum for releasing the Phase IIa results for XmAb5871 in RA? Did

Amgen see the data before they decided to give back their option rights? Given your new

focus on IgGRD, will the RA data still be important? What should investors look for in the

data to differentiate it from other B-cell targeted drugs in RA?

Will the first trial of XmAb5871 in IgGRD generate efficacy results? What are the endpoints

you hope to impact? Is there a regulatory path in this disease?

How is your bispecific platform differentiated from others more advanced in development?

What is the scope of the recent Novo deal? Did you give up any product rights? When will

we know more details of the targets and terms of the deal?

What is the roll for MOR208 given the advancement of drug conjugates, bispecifics, and

CAR-T approaches all targeting CD19?

07 January 2015

SMID Cap Biotechnology 17

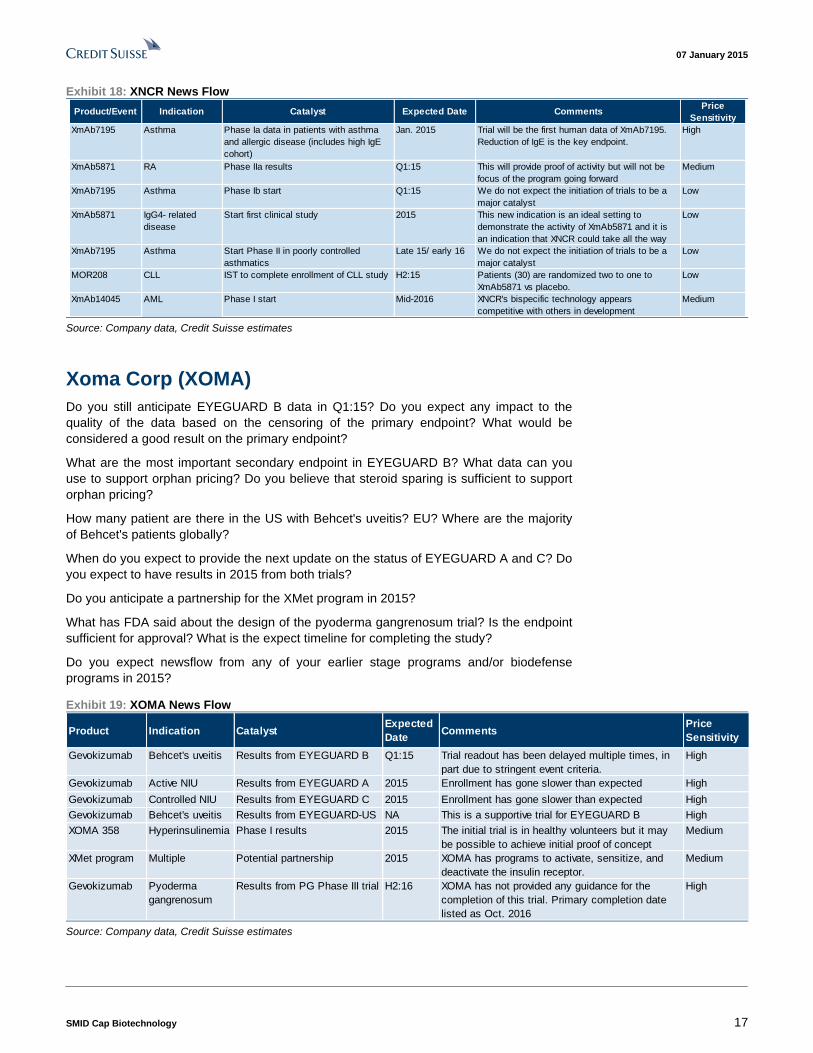

Exhibit 18: XNCR News Flow

Product/Event Indication Catalyst Expected Date CommentsPrice

Sensitivity

XmAb7195 Asthma Phase Ia data in patients with asthma

and allergic disease (includes high IgE

cohort)

Jan. 2015 Trial will be the first human data of XmAb7195.

Reduction of IgE is the key endpoint.

High

XmAb5871 RA Phase IIa results Q1:15 This will provide proof of activity but will not be

focus of the program going forward

Medium

XmAb7195 Asthma Phase Ib start Q1:15 We do not expect the initiation of trials to be a

major catalyst

Low

XmAb5871 IgG4- related

disease

Start first clinical study 2015 This new indication is an ideal setting to

demonstrate the activity of XmAb5871 and it is

an indication that XNCR could take all the way

Low

XmAb7195 Asthma Start Phase II in poorly controlled

asthmatics

Late 15/ early 16 We do not expect the initiation of trials to be a

major catalyst

Low

MOR208 CLL IST to complete enrollment of CLL study H2:15 Patients (30) are randomized two to one to

XmAb5871 vs placebo.

Low

XmAb14045 AML Phase I start Mid-2016 XNCR's bispecific technology appears

competitive with others in development

Medium

Source: Company data, Credit Suisse estimates

Xoma Corp (XOMA)

Do you still anticipate EYEGUARD B data in Q1:15? Do you expect any impact to the

quality of the data based on the censoring of the primary endpoint? What would be

considered a good result on the primary endpoint?

What are the most important secondary endpoint in EYEGUARD B? What data can you

use to support orphan pricing? Do you believe that steroid sparing is sufficient to support

orphan pricing?

How many patient are there in the US with Behcet's uveitis? EU? Where are the majority

of Behcet's patients globally?

When do you expect to provide the next update on the status of EYEGUARD A and C? Do

you expect to have results in 2015 from both trials?

Do you anticipate a partnership for the XMet program in 2015?

What has FDA said about the design of the pyoderma gangrenosum trial? Is the endpoint

sufficient for approval? What is the expect timeline for completing the study?

Do you expect newsflow from any of your earlier stage programs and/or biodefense

programs in 2015?

Exhibit 19: XOMA News Flow

Product Indication Catalyst

Expected

DateComments

Price

Sensitivity

Gevokizumab Behcet's uveitis Results from EYEGUARD B Q1:15 Trial readout has been delayed multiple times, in

part due to stringent event criteria.

High

Gevokizumab Active NIU Results from EYEGUARD A 2015 Enrollment has gone slower than expected High

Gevokizumab Controlled NIU Results from EYEGUARD C 2015 Enrollment has gone slower than expected High

Gevokizumab Behcet's uveitis Results from EYEGUARD-US NA This is a supportive trial for EYEGUARD B High

XOMA 358 Hyperinsulinemia Phase I results 2015 The initial trial is in healthy volunteers but it may

be possible to achieve initial proof of concept

Medium

XMet program Multiple Potential partnership 2015 XOMA has programs to activate, sensitize, and

deactivate the insulin receptor.

Medium

Gevokizumab Pyoderma

gangrenosum

Results from PG Phase III trial H2:16 XOMA has not provided any guidance for the

completion of this trial. Primary completion date

listed as Oct. 2016

High

Source: Company data, Credit Suisse estimates

07 January 2015

SMID Cap Biotechnology 18

Companies Mentioned (Price as of 06-Jan-2015)

Achaogen (AKAO.OQ, $12.72) Ariad Pharmaceuticals, Inc. (ARIA.OQ, $6.51) BIND Therapeutics (BIND.OQ, $5.38) Endocyte, Inc. (ECYT.OQ, $6.11) Esperion Therapeutics (ESPR.OQ, $43.37) ImmunoGen, Inc. (IMGN.OQ, $6.5) Infinity Pharmaceuticals, Inc. (INFI.OQ, $16.08) Kite Pharma (KITE.OQ, $71.45) PTC Therapeutics, Inc (PTCT.OQ, $51.07) Pharmacyclics, Inc. (PCYC.OQ, $119.85) Portola Pharmaceuticals (PTLA.OQ, $27.06) Prosensa Holding N.V. (RNA.OQ, $18.75) Prothena Corp (PRTA.OQ, $19.05) Regeneron Pharmaceutical (REGN.OQ, $396.89) Sarepta Therapeutics (SRPT.OQ, $14.11) Seattle Genetics (SGEN.OQ, $31.45) The Medicines Company (MDCO.OQ, $25.27) XOMA Corporation (XOMA.OQ, $3.51) Xencor, Inc (XNCR.OQ, $16.48)

Disclosure Appendix

Important Global Disclosures

Jason Kantor, PhD, Jeremiah Shepard, PhD and Ravi Mehrotra PhD each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractiv e, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin Ame rican and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiv eness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, 12 -month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10 -15% and -10-15% levels in the Neutral stock rating definition, respectively. Prior to 10th December 2012, Japanese ratings were based on a stock’s total return relative to the average total return of the relevant country or regional benchmark.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

07 January 2015

SMID Cap Biotechnology 19

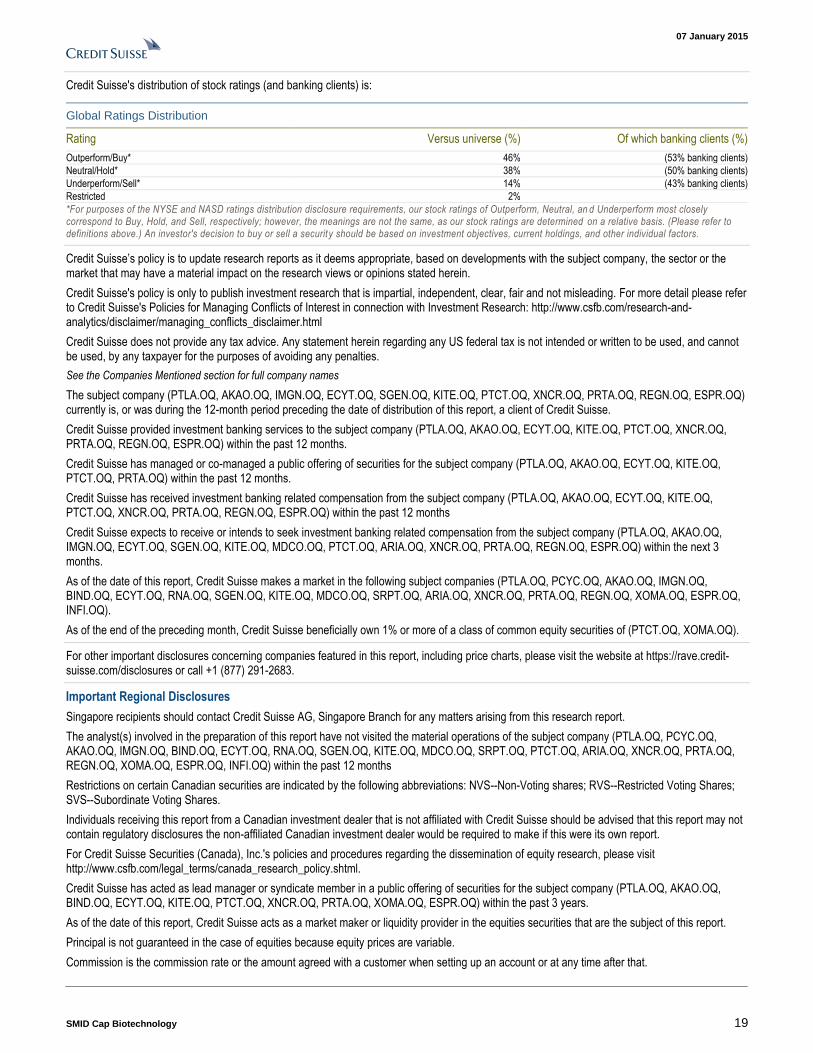

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 46% (53% banking clients)

Neutral/Hold* 38% (50% banking clients)

Underperform/Sell* 14% (43% banking clients)

Restricted 2%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

See the Companies Mentioned section for full company names

The subject company (PTLA.OQ, AKAO.OQ, IMGN.OQ, ECYT.OQ, SGEN.OQ, KITE.OQ, PTCT.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, ESPR.OQ) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (PTLA.OQ, AKAO.OQ, ECYT.OQ, KITE.OQ, PTCT.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, ESPR.OQ) within the past 12 months.

Credit Suisse has managed or co-managed a public offering of securities for the subject company (PTLA.OQ, AKAO.OQ, ECYT.OQ, KITE.OQ, PTCT.OQ, PRTA.OQ) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (PTLA.OQ, AKAO.OQ, ECYT.OQ, KITE.OQ, PTCT.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, ESPR.OQ) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (PTLA.OQ, AKAO.OQ, IMGN.OQ, ECYT.OQ, SGEN.OQ, KITE.OQ, MDCO.OQ, PTCT.OQ, ARIA.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, ESPR.OQ) within the next 3 months.

As of the date of this report, Credit Suisse makes a market in the following subject companies (PTLA.OQ, PCYC.OQ, AKAO.OQ, IMGN.OQ, BIND.OQ, ECYT.OQ, RNA.OQ, SGEN.OQ, KITE.OQ, MDCO.OQ, SRPT.OQ, ARIA.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, XOMA.OQ, ESPR.OQ, INFI.OQ).

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (PTCT.OQ, XOMA.OQ).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (PTLA.OQ, PCYC.OQ, AKAO.OQ, IMGN.OQ, BIND.OQ, ECYT.OQ, RNA.OQ, SGEN.OQ, KITE.OQ, MDCO.OQ, SRPT.OQ, PTCT.OQ, ARIA.OQ, XNCR.OQ, PRTA.OQ, REGN.OQ, XOMA.OQ, ESPR.OQ, INFI.OQ) within the past 12 months

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit http://www.csfb.com/legal_terms/canada_research_policy.shtml.

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (PTLA.OQ, AKAO.OQ, BIND.OQ, ECYT.OQ, KITE.OQ, PTCT.OQ, XNCR.OQ, PRTA.OQ, XOMA.OQ, ESPR.OQ) within the past 3 years.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

07 January 2015

SMID Cap Biotechnology 20

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

07 January 2015

SMID Cap Biotechnology 21