Embed Size (px)

Citation preview

SME Digital Capability and E-Commerce: What do we know?

Michelle Harrison and Drew Hird, BIS Enterprise Analysis

October 2015

1

SME Digital Capability and E-Commerce

2

• Why digital capability matters

• Key ONS and BIS data

• Exploring the issues through the BIS Small Business Survey

• So what do we really know and what else do we need?

3

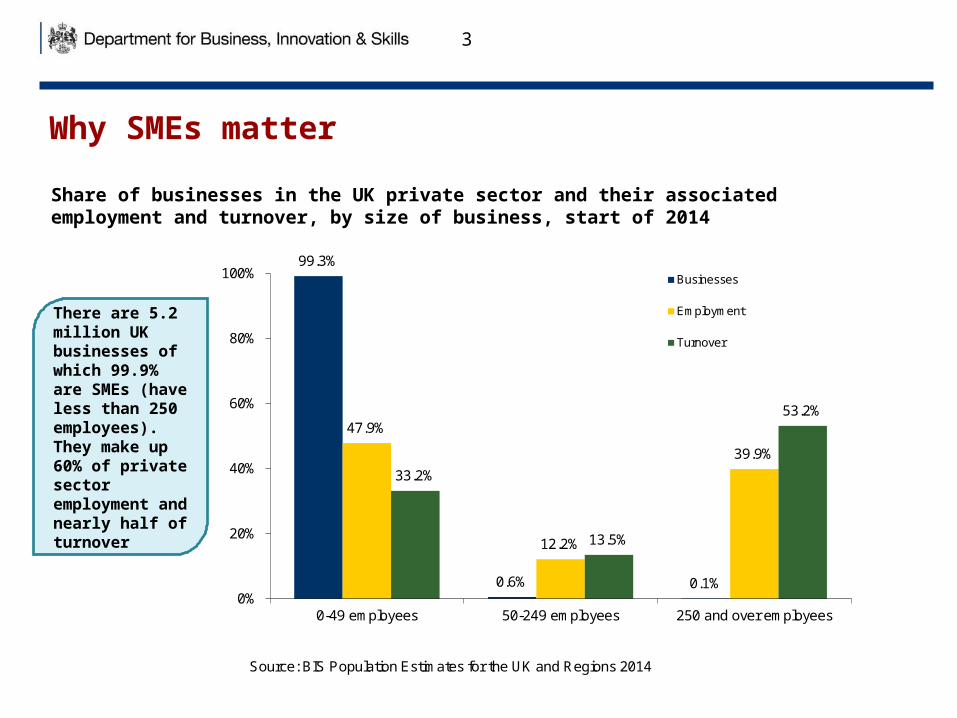

Share of businesses in the UK private sector and their associated employment and turnover, by size of business, start of 2014

99.3%

0.6% 0.1%

47.9%

12.2%

39.9%

33.2%

13.5%

53.2%

0%

20%

40%

60%

80%

100%

0-49 employees 50-249 employees 250 and over employees

Businesses

Employment

Turnover

Source: BIS Population Estimates for the UK and Regions 2014

There are 5.2 million UK businesses of which 99.9% are SMEs (have less than 250 employees). They make up 60% of private sector employment and nearly half of turnover

Why SMEs matter

Digital isn’t just the future

Digital is an important factor for a competitive UK economy

•Many growth sectors already rely heavily on digital capability, e.g.

• ICT Content and Media - over the last 10 years the sector has grown over three times as fast as the whole economy

• Assisted living – the UK is the largest market in Europe

• Creative industries: 1.68 m jobs in 2012, grew by 9% over 2011-12

• Total website sales, for businesses with more than 10 employees, were over £193bn in 2013

•Trading online can increase revenues in domestic and international markets

4

Some contextual evidence

5

“This is for Everyone” – The Case for Universal Digitisation, Booz & Company (2012) Lloyds Bank UK Business Digital Index 2015,

Lloyds, Accenture and Go-On UK (March 2015)

Reduced costs:

Argued that UK SMEs are lagging internationally, and could reduce their cost base by up to 20% by digitising. “The 2015 Index indicates a clear link between

digital maturity and organisational success. So again, once SMEs and charities recognise the benefits of being online and invest the time and money to do so, they will clearly reap the rewards.”

Increased turnover:

Suggested “digital technology can enable SMEs to unlock as much as £18.8 billion in incremental revenue”

A simple framework for looking at SME digital capability

• General idea is that further to the right along this activity scale businesses are the more capable they are

– Are they connected?

– Do they have an online presence to promote themselves?

– Are they selling their goods/services online?

• But we do have to remember different businesses have different circumstances, so it’s only a general indication

6

Not connected

Connected but not

promoting or selling online

Promoting online but not

sellingSelling online

Digital capability may enable growth

Digital capability can provide improved access to new markets and may be associated with higher growth

• 83% of ‘growth’ businesses have a website

• compared to 69% of those with stable performance, and 59% of those whose employment or turnover has shrunk (SBS 2014)

• Some SMEs begin exporting “by accident” through their website

• 33% of exporters use e-commerce through their own website, compared to 6% non-exporters (BIS 2015)

• Around 80% of individuals buy online, yet nearer 20% of firms sell online (ONS)

• But is this actually a problem…?

7

ONS data shows growth in market/appetite of consumers

8

In 2012, around 19% of UK enterprises were selling online, and nearly 80% of individuals had bought online.

• UK has a high rate of individuals purchasing online• But not a particularly high rate of firms selling online

• But value of online sales is going up fairly quickly• So do SMEs need to do anything to keep up?

Value of e-commerce sales over a website has increased significantly.

£billion

A word about differences between BIS and ONS data

• Small Business Survey is BIS’s key evidence source on small businesses

• used to give insight into characteristics and activities of SMEs

• Two key differences between ONS e-commerce data and the BIS data

• BIS covers non-employing and micro businesses (so all <10 employees)

• BIS is capturing a broader definition of selling online

• Comparison of 2012 data for similar questions

9

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

No employees Micro Small Medium All SMEs

share of businesses

No business internet connection Internet connection but not selling or promoting goods and services

Promoting but not selling goods and services Selling goods and services

BIS Small Business Survey – hierarchy of activity

10

BIS 2014 Small Business Survey

• Extent to which firms use the internet clearly related to size• Larger firms more likely to sell online• Smaller firms more likely to be connected but with no real presence• Smaller firms also more likely to not be connected at all

BIS Digital Re-survey

• Involved 803 former SBS 2014 respondents, with 249 employees or less. March – May 2015

• Wanted to find out more about SMEs digital capabilities• Developed questions to explore e-commerce at detailed

level – to develop a clearer picture of SME digital activity.• Full findings available: Digital capabilities in SMEs

11

Objectives….

• Which businesses, if any, were maximising digital opportunities and the outcomes.

• How many businesses were engaged in e-commerce?

• If not, why not? • Is this a sector story? • Issues for future digital planning.

12

Sector concerns on not having a website vary…

13

• Across all sectors, businesses without a website do not see them as necessary• OR is it that they just do not realise that they are necessary? • Internet security is a concern in the retail sector – does this reflect concern about taking

payment?• Paying someone to create a website is considered expensive, particularly in construction

and other services.

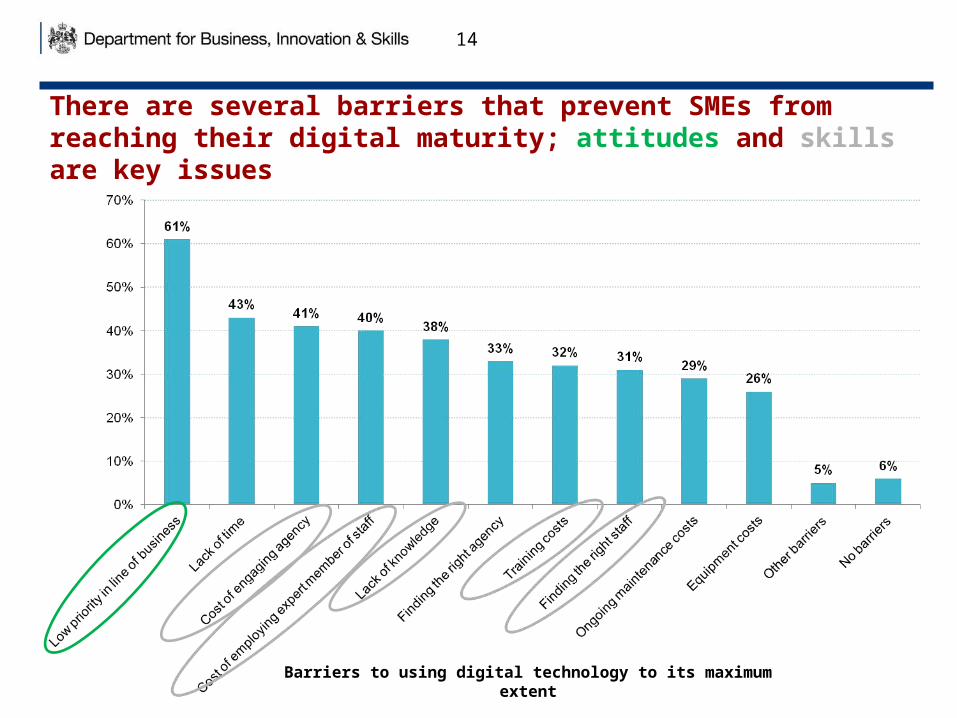

There are several barriers that prevent SMEs from reaching their digital maturity; attitudes and skills are key issues

14

Barriers to using digital technology to its maximum extent

E-commerce

15

11% bookings

and orders via

own website

11% e-commerce via a third

party website

E-commerce by sector

16

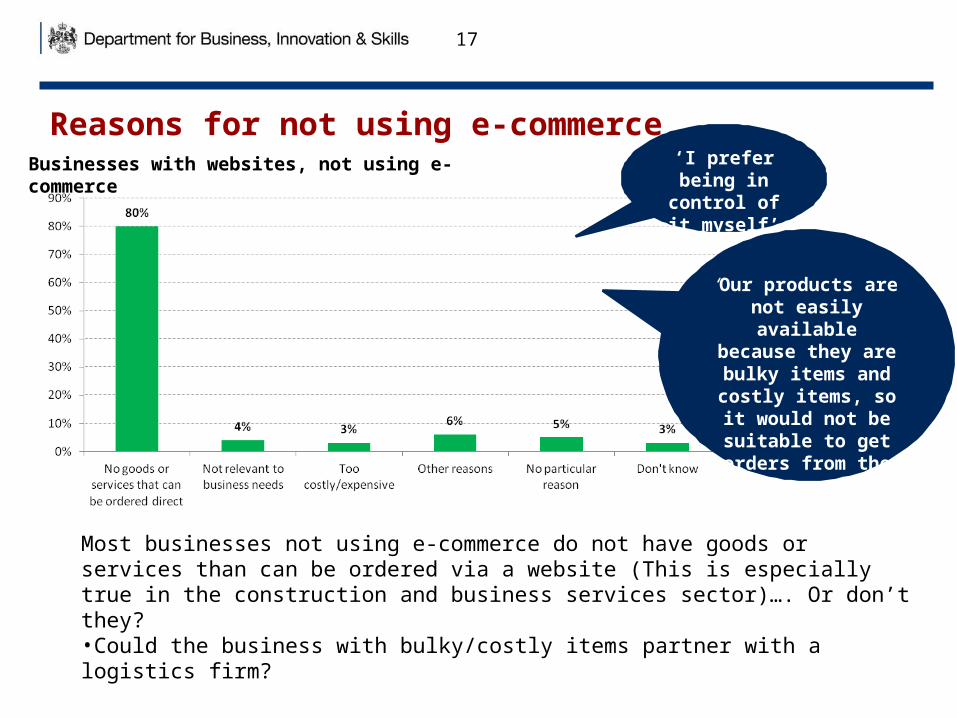

Reasons for not using e-commerce

17

‘I prefer being in control of

it myself’

‘Our products are not easily available because they are bulky items and

costly items, so it would not be

suitable to get orders from the all over the country’

Most businesses not using e-commerce do not have goods or services than can be ordered via a website (This is especially true in the construction and business services sector)…. Or don’t they?•Could the business with bulky/costly items partner with a logistics firm?

Businesses with websites, not using e-commerce

Plans to engage in e-commerce vary by sector

18

responding to consumer demand.

attracting new customers and following the trend.

cost savings, making more money and responding to consumer demand.

Transport:

Construction:

Retail:

So what do we actually know?

• Evidence to date doesn’t point to an overriding market failure for SMEs

• There are obvious differences between some firms

• But that might just be nature of the market they’re in or who they sell to

– it will be good to start to understand more

• Businesses are time poor, so they will only do more on digital if it’s more important to them than all the other things they need to do.

• Firms need the right information to make good decisions about what’s right for them

– so they can stay up to date and compete

19

And what else do we need to find out?

• Longitudinal Small Business Survey will give us more analytical power

– 15,000 businesses and opportunity to track and follow up groups of interest

– 5 year process means questions need to be right – improvements made

• Hope to establish whether performance differences between otherwise similar businesses that do digital to different extents

– and perhaps explore choices of different performance groups

• Also need to keep developing information on size of digital market

– and where digital sales of both goods and services are growing

• So maybe more from BIS and ONS looking at sectors and size in combination

• Can we start to understand goods and services more distinctly?

– to understand any differences

– but also to communicate importance of digital for both

20

Questions

• For the floor…

• But also interested in your views about what’s important here

• And on what other information and evidence is needed

21