Embed Size (px)

Citation preview

1

Smart Grid Research from a

Utility Perspective

TCIPG Seminar – May 2, 2014

Richard Smith

Director – Research and Development

Ameren Corporation

Outline

2

• Introduction

• Ameren Overview - A representative U.S. utility

• Industry Context

• Smart Grid Technology – Business Perspective

• Ameren Smart Grid Activities

• R&D Needs

3

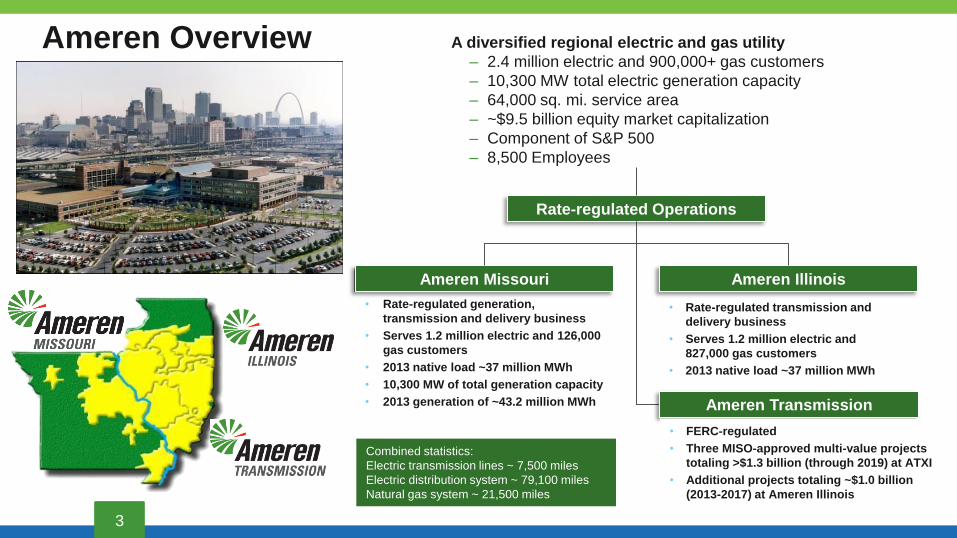

Ameren Overview A diversified regional electric and gas utility

– 2.4 million electric and 900,000+ gas customers

– 10,300 MW total electric generation capacity

– 64,000 sq. mi. service area

– ~$9.5 billion equity market capitalization

– Component of S&P 500

– 8,500 Employees

Combined statistics:

Electric transmission lines ~ 7,500 miles

Electric distribution system ~ 79,100 miles

Natural gas system ~ 21,500 miles

• Rate-regulated generation,

transmission and delivery business

• Serves 1.2 million electric and 126,000

gas customers

• 2013 native load ~37 million MWh

• 10,300 MW of total generation capacity

• 2013 generation of ~43.2 million MWh

Ameren Missouri Ameren Illinois

• Rate-regulated transmission and

delivery business

• Serves 1.2 million electric and

827,000 gas customers

• 2013 native load ~37 million MWh

Rate-regulated Operations

Ameren Transmission

• FERC-regulated

• Three MISO-approved multi-value projects

totaling >$1.3 billion (through 2019) at ATXI

• Additional projects totaling ~$1.0 billion

(2013-2017) at Ameren Illinois

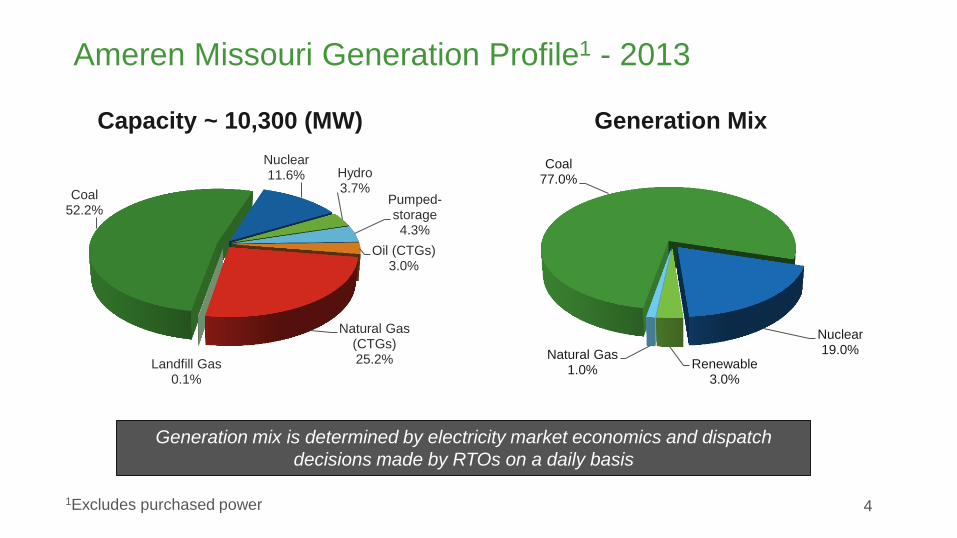

Ameren Missouri Generation Profile1 - 2013

Capacity ~ 10,300 (MW) Generation Mix

Generation mix is determined by electricity market economics and dispatch

decisions made by RTOs on a daily basis

4

Coal 52.2%

Nuclear 11.6% Hydro

3.7% Pumped-storage 4.3%

Oil (CTGs) 3.0%

Natural Gas (CTGs) 25.2% Landfill Gas

0.1%

Coal 77.0%

Nuclear 19.0%

Renewable 3.0%

Natural Gas 1.0%

1Excludes purchased power

Outline

5

• Introduction

• Ameren Overview - A representative U.S. utility

• Industry Context

• Smart Grid Technology – Business Perspective

• Ameren Smart Grid Activities

• R&D Needs

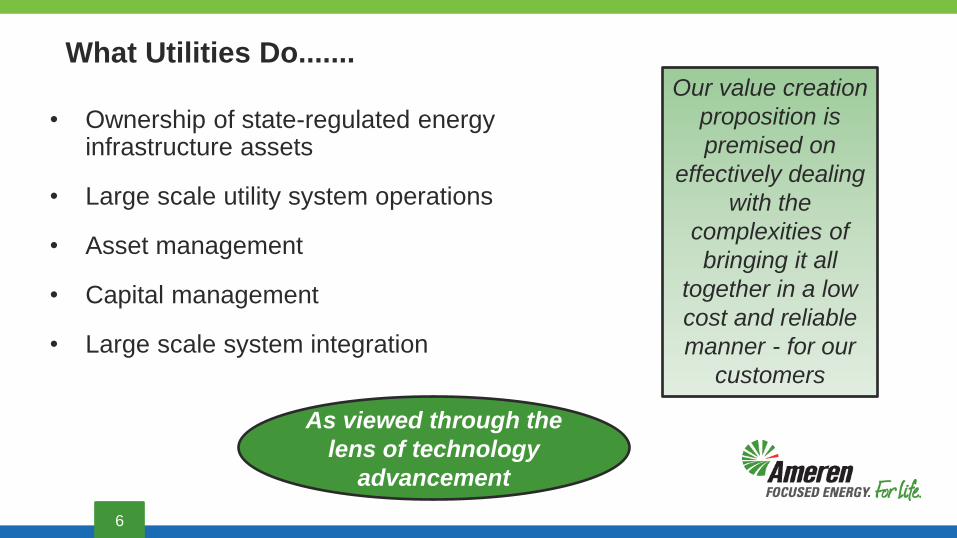

What Utilities Do.......

6

• Ownership of state-regulated energy infrastructure assets

• Large scale utility system operations

• Asset management

• Capital management

• Large scale system integration

Our value creation

proposition is

premised on

effectively dealing

with the

complexities of

bringing it all

together in a low

cost and reliable

manner - for our

customers

As viewed through the

lens of technology

advancement

Key Utility Industry Drivers

7

Capital Markets & Desired

Investment Returns

Government Ideology & Policy

Economic Growth

Environmental Regulations

Natural Gas Prices

Reliability

Technology Advancement

KEY

DRIVERS

Climate & Environmental Policy

Nuclear

The Future of Coal

Natural Gas

Renewable Energy

The Economy

Transmission

Power Prices

Technology

Customer of the Future

What are the

implications

for

customers

and smart

grid?

Achieving Balance – Utility Priorities

8

How does investment in smart grid help with these priorities?

Customers and Communities

• Reliable and affordable

• Quality service

Environment

• Cleaner generation and renewable

energy

• Reduce environmental impacts

Workforce

• Safe working environment

• Preferred employer

Shareholders

• Predictable returns and earnings

growth

• Solid financial management

Outline

9

• Introduction

• Ameren Overview - A representative U.S. utility

• Industry Context

• Smart Grid Technology – Business Perspective

• Ameren Smart Grid Activities

• R&D Needs

10

Potentially Transformative

NATURAL GAS

EXTRACTION

• Fracking and

directional drilling

• Recovery of

methane hydrates

NUCLEAR

• Small

modular

nuclear

reactors

DISTRIBUTED

GENERATION

• Solar technologies

• Energy storage

systems

• Small scale

natural gas fueled

NONTRADITIONAL

ENERGY SYSTEMS

• Microgrids

• Net-zero energy

buildings

ADVANCED

COMPUTING

& GRID

AUTOMATION

• Smart

grid/analytics

• Automation

Technologies that could prove “transformative”

to the traditional utility system in the long-term:

Technical and Business Case Uncertainties

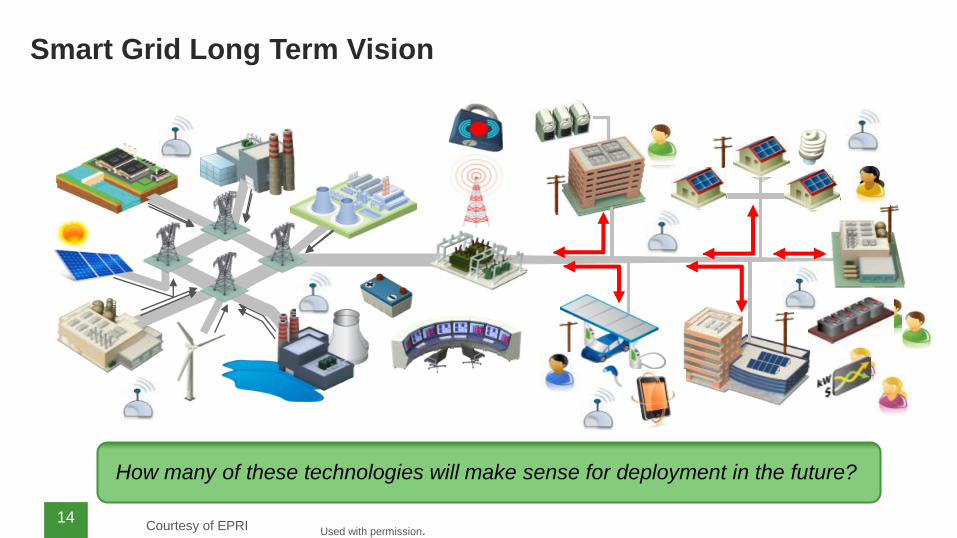

A Transformed Electrical System that is Highly Flexible, Resilient and

Connected and Optimizes Energy Resources - EPRI

Used with permission. Courtesy of EPRI 11

Smart Grid Long Term Vision

Technological “Grid Parity” = Utility Customer Price

12

0

5

10

15

20

¢/K

Wh

Average Residential Electricity Prices1

1 Source: Bureau of Labor Statistics and “2013 EEI Typical Bills and Average Rates" report. 2 DER = Distributed Energy Resources, e.g. DG, Community Energy Storage, PV, etc.

Will a modern

“grid” with DER2

be price

competitive in

the future?

What will utility

customers be

willing to pay?

Price and

reliability – the

top two customer

issues.

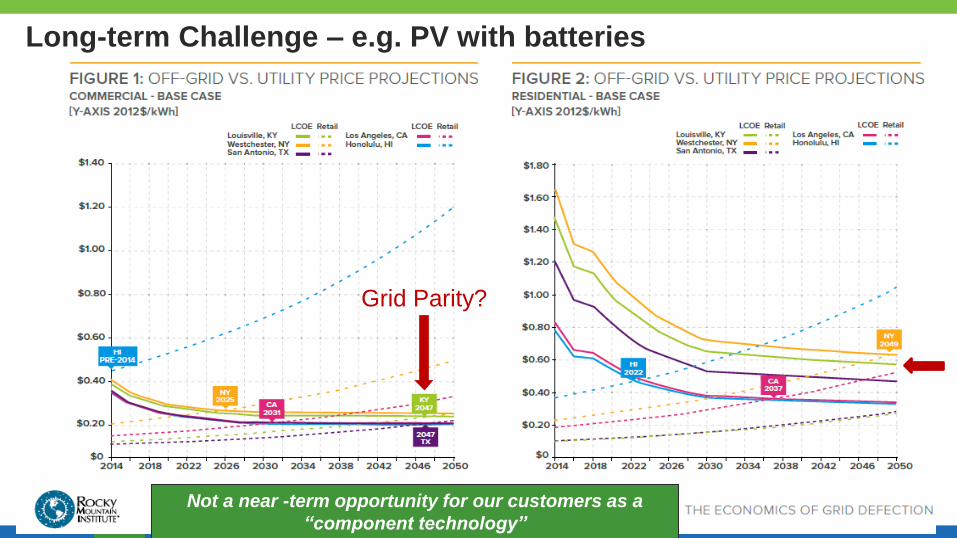

Long-term Challenge – e.g. PV with batteries

Not a near -term opportunity for our customers as a

“component technology”

Grid Parity?

How many of these technologies will make sense for deployment in the future?

Used with permission. Courtesy of EPRI 14

Smart Grid Long Term Vision

• Avalanche of perspectives: • Journals, magazines and newsletters related to emergence of all

kinds of technologies from generation to delivery, to customer end

use. What is real? What has real business value?

• “Hard Trend” - technology is changing • With and/or without utilities

• Which technologies matter? Which ones will be at a scale that

matters at reasonable cost?

• Convergence of information, operation, and

communication technologies • provides an architecture or platform for the future

• Component technologies improving

• Need for standards based approaches

• A call for cleaner generation is still being heard

• How can utilities leverage the technologies to benefit

customers?

15

Technology Challenges/Opportunities

• Will smart grid technologies continue to improve and will costs

decline enough?

• What will be the pace of technological change and timing of

market development?

• Can investor owned utilities earn a return on investing in smart

grid and extensions like “community power” systems?

• How should we think about breaking “the grid” into smaller

operating segments? (to what extent a “grid of grids”?)

• Will smart grid technology applied to the distribution system

provide a good platform for greater amounts of cleaner

generation in the future?

• Will utility customers choose to take advantage of emerging

technologies?

• What will regulators promote or allow in the future?

16

Key Business Questions

In the long run, will customers be willing to pay for grid improvements and migration

to a more interactive, cleaner operation based on advanced technologies?

Outline

17

• Introduction

• Ameren Overview - A representative U.S. utility

• Industry Context

• Smart Grid Technology – Business Perspective

• Ameren Smart Grid Activities

• R&D Needs

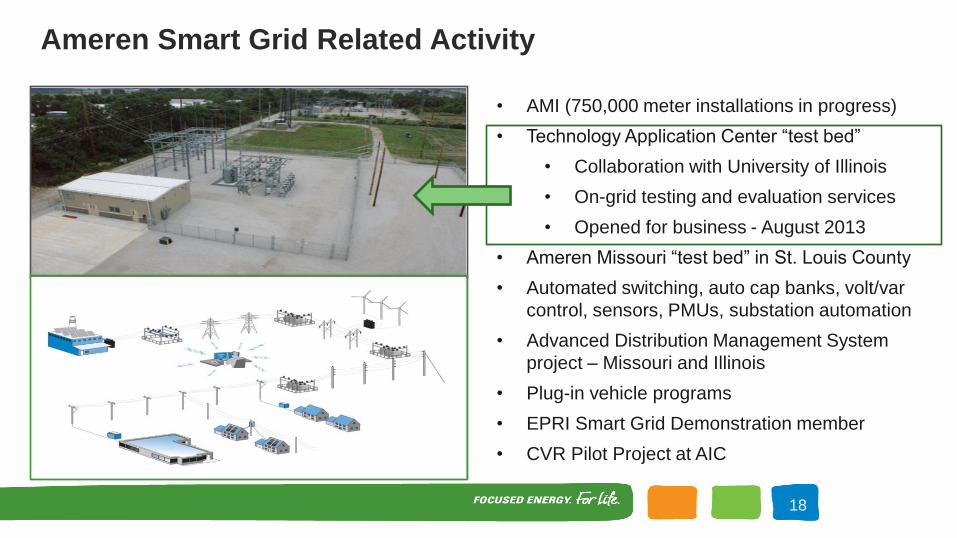

Ameren Smart Grid Related Activity

18

• AMI (750,000 meter installations in progress)

• Technology Application Center “test bed”

• Collaboration with University of Illinois

• On-grid testing and evaluation services

• Opened for business - August 2013

• Ameren Missouri “test bed” in St. Louis County

• Automated switching, auto cap banks, volt/var

control, sensors, PMUs, substation automation

• Advanced Distribution Management System

project – Missouri and Illinois

• Plug-in vehicle programs

• EPRI Smart Grid Demonstration member

• CVR Pilot Project at AIC

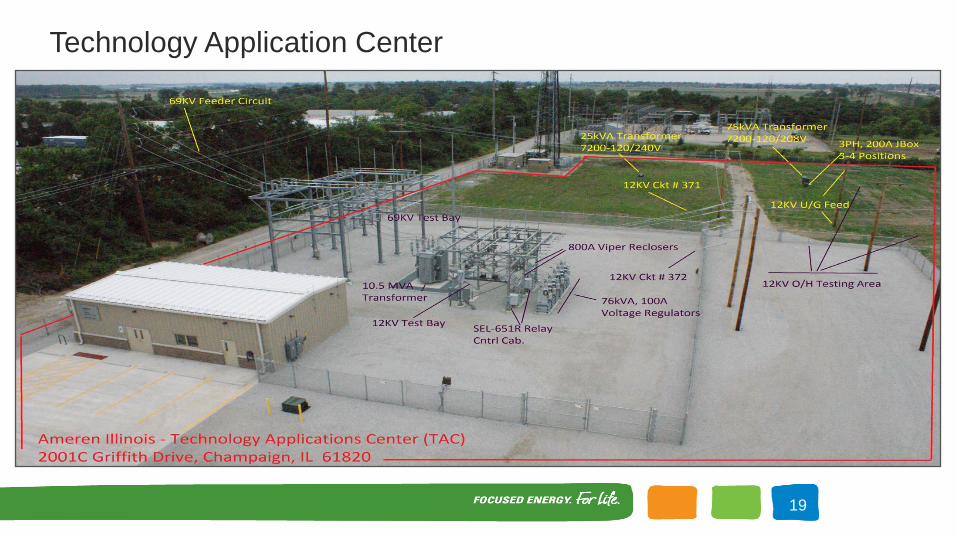

Technology Application Center

19

20

Technology Application Center – Equipment Examples Testing Equipment Platform

Relay Panels

Distribution

SCADA Panel

AMI Metering Bank

Smart Appliances

Voltage Regulators

Selected Ameren R&D Projects

21

• Participant in EPRI’s Smart Grid Demonstration Project Initiative

• Ameren Illinois CVR Pilot

• Energy Efficiency Demo - LED Lighting Ballwin, Missouri

EPRI Rover

Cove

www.epri.com

EPRI smart grid

updates available at:

%MW / %∆𝐕

CVRf = 0.97

Ameren Microgrid, DG Pilot Projects

22

3 MW Brookside Substation Fuel Cell

Demo Project – Delmarva/EPRI

Missouri S&T Solar Village

Microgrid Project

• Rooftop Solar PV

• A123 Li-ion Battery

System

• ClearEdge 5kW Fuel Cell

(community power)

Bloom Energy

• Lewis & Clark Community

College

ClearEdge

5 kW Unit

Outline

23

• Introduction

• Ameren Overview - A representative U.S. utility

• Industry Context

• Smart Grid Technology – Business Perspective

• Ameren Smart Grid Activities

• R&D Needs

Currently Available Technology is Enabling:

24

Sensors Automation Applications

Transformers:

• Bushings

• Temperature

• Dissolved gasses

Remote Voltage Regulator Control Conservation Voltage Reduction

• How to prioritize circuits for CVR

deployment

Electric Distribution Lines:

• Faulted circuit indicators

• Remote voltage

Remote Capacitor Control Software

• Software defined networking

• Intrusion detection

Relays (sense, control, some

diagnostics)

Remotely Operated or Automated

Switches

Automated:

• Circuit isolation

• Switching

• Fault locating

AMI with multiple functionalities:

• Read

• Connect and disconnect

• Voltage

• Theft detection, etc.

Distributed Resources:

• Some degree of control and

coordination of DR

• System operating with some

distributed generation

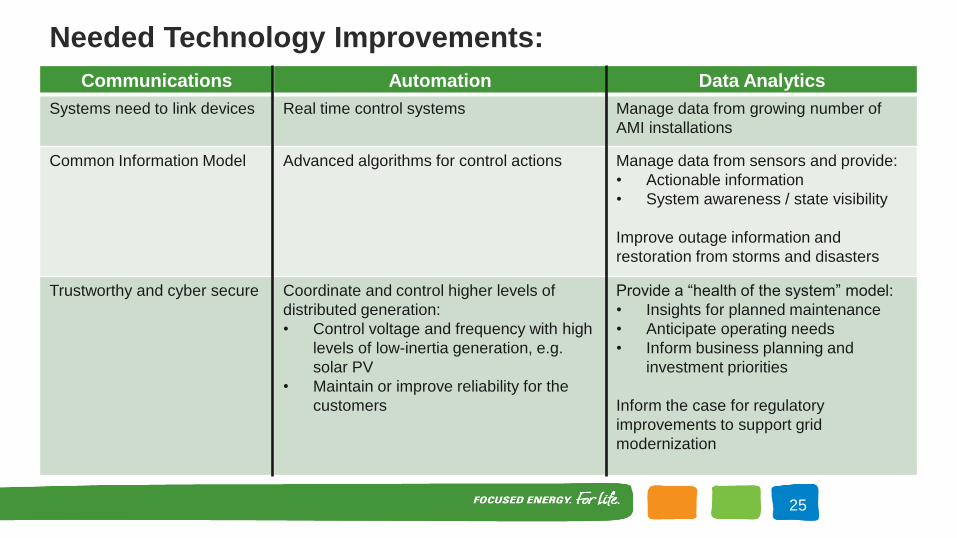

Needed Technology Improvements:

25

Communications Automation Data Analytics

Systems need to link devices Real time control systems Manage data from growing number of

AMI installations

Common Information Model Advanced algorithms for control actions Manage data from sensors and provide:

• Actionable information

• System awareness / state visibility

Improve outage information and

restoration from storms and disasters

Trustworthy and cyber secure Coordinate and control higher levels of

distributed generation:

• Control voltage and frequency with high

levels of low-inertia generation, e.g.

solar PV

• Maintain or improve reliability for the

customers

Provide a “health of the system” model:

• Insights for planned maintenance

• Anticipate operating needs

• Inform business planning and

investment priorities

Inform the case for regulatory

improvements to support grid

modernization

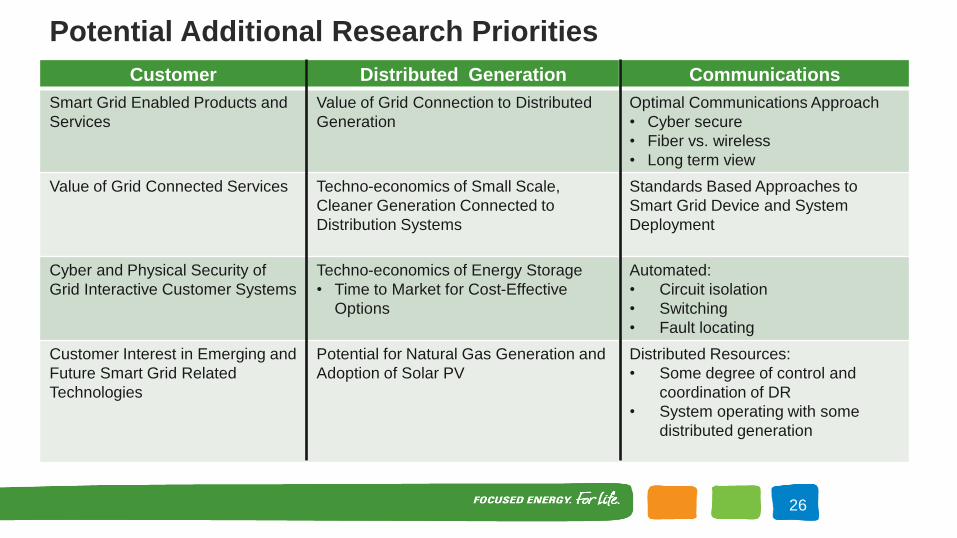

Potential Additional Research Priorities

26

Customer Distributed Generation Communications

Smart Grid Enabled Products and

Services

Value of Grid Connection to Distributed

Generation

Optimal Communications Approach

• Cyber secure

• Fiber vs. wireless

• Long term view

Value of Grid Connected Services Techno-economics of Small Scale,

Cleaner Generation Connected to

Distribution Systems

Standards Based Approaches to

Smart Grid Device and System

Deployment

Cyber and Physical Security of

Grid Interactive Customer Systems

Techno-economics of Energy Storage

• Time to Market for Cost-Effective

Options

Automated:

• Circuit isolation

• Switching

• Fault locating

Customer Interest in Emerging and

Future Smart Grid Related

Technologies

Potential for Natural Gas Generation and

Adoption of Solar PV

Distributed Resources:

• Some degree of control and

coordination of DR

• System operating with some

distributed generation

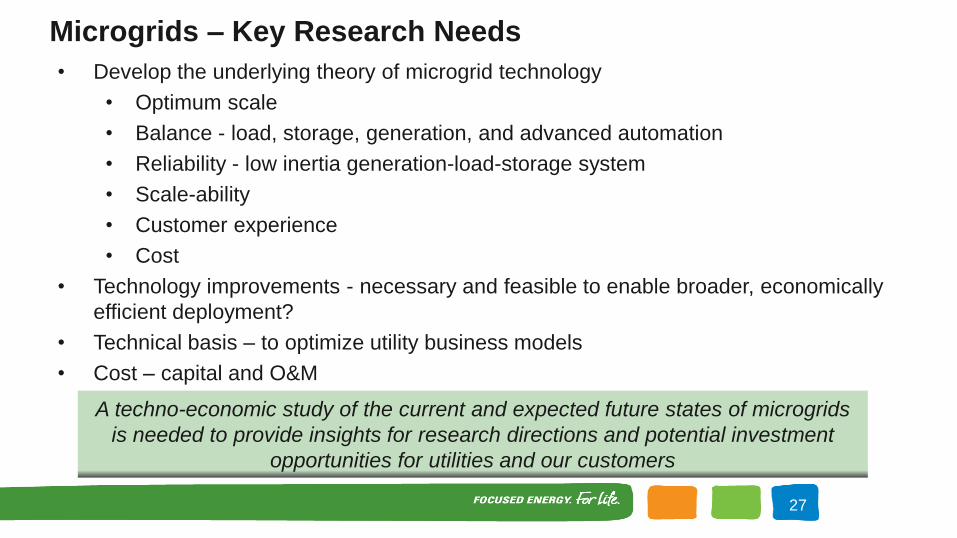

• Develop the underlying theory of microgrid technology

• Optimum scale

• Balance - load, storage, generation, and advanced automation

• Reliability - low inertia generation-load-storage system

• Scale-ability

• Customer experience

• Cost

• Technology improvements - necessary and feasible to enable broader, economically

efficient deployment?

• Technical basis – to optimize utility business models

• Cost – capital and O&M

27

A techno-economic study of the current and expected future states of microgrids

is needed to provide insights for research directions and potential investment

opportunities for utilities and our customers

Microgrids – Key Research Needs

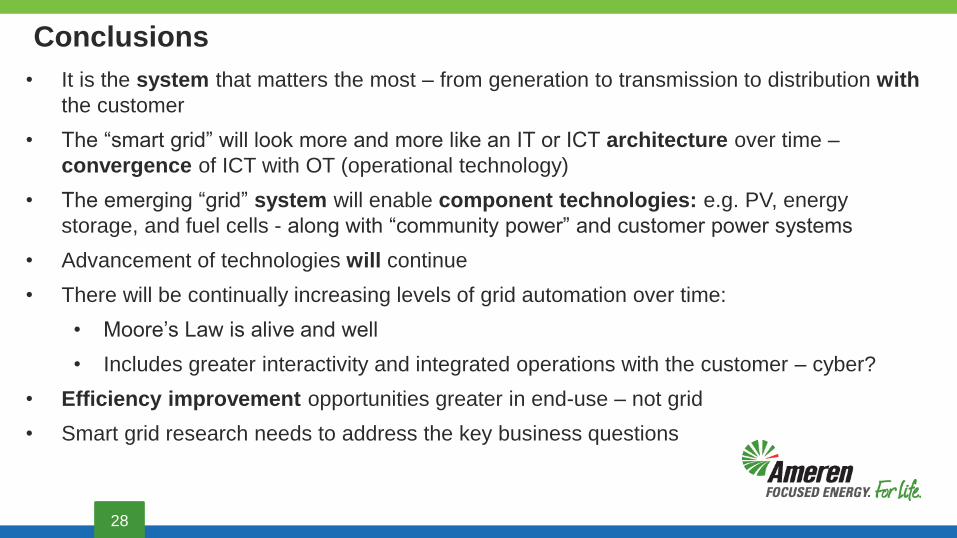

Conclusions

28

• It is the system that matters the most – from generation to transmission to distribution with

the customer

• The “smart grid” will look more and more like an IT or ICT architecture over time –

convergence of ICT with OT (operational technology)

• The emerging “grid” system will enable component technologies: e.g. PV, energy

storage, and fuel cells - along with “community power” and customer power systems

• Advancement of technologies will continue

• There will be continually increasing levels of grid automation over time:

• Moore’s Law is alive and well

• Includes greater interactivity and integrated operations with the customer – cyber?

• Efficiency improvement opportunities greater in end-use – not grid

• Smart grid research needs to address the key business questions

Contact info:

Richard Smith

Office: 314.554.3531

email: [email protected]

Technology Application Center:

Rod Hilburn

Office: 217.424.6638

email: [email protected]