Embed Size (px)

Citation preview

Helping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestBy Hervé ConanEdited by Charles T. Andrews and Almud Weitz

SmallPipedWaterNetworks

ADB S E

R

I E

S

S E

R

I E

S

S E

R

I E

S

S E

R

I E

S

S E

R

I E

S

1313131313

Helping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to InvestHelping Local Entrepreneurs to Invest

SmallPipedWaterNetworks

© Asian Development Bank

All rights reserved

The findings, interpretations, and conclusions expressed in this documentdo not necessarily represent the views of the Asian Development Bank (ADB)or the views of its member governments. ADB does not guarantee theaccuracy of the data included in this publication and accepts no responsibilityfor any consequences of their use.

AbbreviationsAbbreviationsAbbreviationsAbbreviationsAbbreviations

ADB Asian Development BankDCC Dhaka City CorporationDWASA Dhaka Water Supply and Sanitation AuthorityGDP gross domestic productHC house connectionHCMC Ho Chi Minh CityHH householdhr hourkm2 square kilometerl literm3 cubic meterMCWD Metro Cebu Water DistrictMDG Millennium Development GoalNGO nongovernment organizationNRW nonrevenue waterO&M operation and maintenancePVC poly vinyl chlorideRETA regional technical assistanceSSPWP small-scale private water providerWHO World Health OrganizationWSP Water and Sanitation Program (World Bank)WTP willingness to payWSS water supply and sanitationWU water utilityWWF World Water Forum

Note: $ values in this publication are local currency equivalents in US dollars.

11111 INTRODUCTIONResearch objectivesMethodology

77777 SMALL-SCALE PRIVATE WATER PROVIDERSSSPWPs as defined by the researchHow SSPWPs supply waterSSPWP users

1212121212 SCOPE AND SCALE OF SSPWPs IN ASIAN CITIESSSPWPs and their niche marketsNon-SSPWP alternative sourcesSSPWP activities differUser charges by SSPWP type

2727272727 A CLOSER LOOK AT SMALL PIPED WATER NETWORKSHow networks get startedThe water network entrepreneurNetwork investmentsNetwork technologiesNetworks and utilities: Similarities and differencesSmall piped water networks: The realitiesDifficulties resulting from informal status

3636363636 POLICIES AND ACTIONS TO SUPPORT SMALL PIPED WATER NETWORKSWhy support small piped water networksHelping local entrepreneurs to invest

Contents

Foreword

This book is about small-scale private water providers in Asian cities and theentrepreneurial potential of small piped network operators. It proposes that cityofficials, city water utilities, and local banks should work with small networkentrepreneurs who can bring water supplies to the poor and disadvantagedimmediately, on an agreed interim basis until the water utility is able to.

Published Asian Development Bank (ADB) studies on water in Asian cities in1993, 1997, and 2004 track the generally disappointing performance of waterutilities. Most water utilities in South Asia provide a very intermittent watersupply throughout the entire city, whereas water utilities in Southeast Asia typicallyprovide a better quality service, but only to part of the city—leaving many millionsof residents entirely unserved. This book reports on the findings of an ADBstudy examining the role of small water providers in filling these service gaps.

Survey results from the study show that from city to city, 20–50% of residentsare customers in informal water markets—they buy all or some of their waterfrom small-scale water providers. The cart-pushing water vendor, the water tankeroperator, the neighbor selling water from her well or reselling water from herutility connection, the engineer-turned small piped network operator, and theseller of bottled and barreled water—these are the familiar face of the informalwater market in our cities. These local providers are here as long as city waterutilities fail in their core mandate to provide continuous 24-hour supplies ofclean water by piped connection to every house and business in the city. Thesurvey results show that small providers are not profiteers—they do not exploit.But neither are they efficient and innovative, nor good at quality control. Andthey mostly do not deliver what people want most and are willing to pay for—acontinuous supply to the house. Small private piped water networks are theexception.

The study examines small piped networks through case studies: how and whostarts these operations; who they supply, with what, at what cost, and using whattechnologies; their business and risk management approaches; and what hinderstheir development. Their relationships with city hall, the city water utility, andthe local banks are examined—and are shown to be difficult and limiting. Mostimportant, the case studies show that it is the poor who benefit most when local

entrepreneurs invest risk capital and build and operate piped networks in unservedurban slums and low-income neighborhoods that have been failed by the citywater utility.

The study finds strongly in favor of small piped networks, as short- and medium-term providers until the city water utility can expand services to the area.

The book offers practical recommendations to city governments and utilities forgetting local water network entrepreneurs to invest. Small piped networks shouldbe included in city development strategies, utilities should work with localentrepreneurs, small networks should be “formalized” with licensing and exitstrategies and takeout agreements, minimum standards should recognize riskand pay-back requirements, enabling legal and contractual conditions should becreated, and small operators should be integrated into the water supply chain tothe extent possible. ADB will join with two or three cities to test and refine theserecommendations during 2005–2006.

Jan P. M. van HeeswijkDirector GeneralRegional and SustainableDevelopment Department

Acknowledgments

The Asian Development Bank wishes to thank the small-scale water providerswho furnished information to make this publication possible, including PhucDoan and Hiep An companies of Ho Chi Minh City (Viet Nam); FernandoMiñoza and Virgie Zafra of Cebu and Inpart Engineering of Manila (Philippines);the tankers’ association of Kathmandu Valley (Nepal); the pushcart waterdistributors of Delhi (India); and the independent water bottlers of Shanghai(People’s Republic of China).

We are grateful for the support of local consultants in the surveyed cities whocollected information and prepared reports on their local informal water markets.

We give special thanks to former ADB staff Maria Paniagua, who initiated anddefined this study, and to Marc Vezina for his guidance on approach andmethodology.

Charles T. AndrewsPrincipal Water Supply andSanitation SpecialistAgriculture and Natural Resourcesand Social Sectors Division

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

1

Small Piped Water Networks:Helping Local Entrepreneurs

to InvestBackgroundIntroduction This publication presents findings and recommendations from field research

funded by the Asian Development Bank (ADB). Researching small-scaleprivate water providers (SSPWPs) was part of a wider study on “Water in

Asian Cities”.1 The SSPWP research investigated and analyzed the role of smallproviders in eight Asian cities, namely Cebu (Philippines), Delhi (India), Dhaka(Bangladesh), Ho Chi Minh City or HCMC (Viet Nam), Jakarta (Indonesia),Kathmandu (Nepal), Shanghai (People’s Republic of China), and Ulaanbaatar(Mongolia).2 Additionally, one SSPWP in Manila (Philippines) was studied.

Research objectivesThe objectives of the SSPWP research were to (i) provide an overview of urbanwater suppliers beyond formal water utilities, (ii) increase the knowledge aboutthe type of services provided by SSPWPs, (iii) define the profile of the mostsignificant SSPWPs, and (iv) assess the main constraints and potential forSSPWPs.

MethodologyUnder the supervision of ADB and a consultant team coordinator, a team ofeight local consultants conducted field surveys on the scope and scale of SSPWPsin the eight selected cities.

The study started in mid-August 2002 and field surveys were finished in earlyJanuary 2003. The field surveys included a household survey to define the waterprofile of each city. The surveys considered not just SSPWPs but all water services,including utilities, traditional water points, and other water providers set up bycommunity organizations, nongovernment organizations (NGOs), and privateoperators. Case studies were also undertaken to get in-depth information onspecific services provided by selected SSPWPs.

1 The main study collected and analyzed data on the performance of water utilities in 18 Asian cities (Chengdu, Colombo,Delhi, Dhaka, Ho Chi Minh City, Hong Kong, Jakarta, Karachi, Kathmandu, Kuala Lumpur, Manila, Osaka, PhnomPenh, Seoul, Shanghai, Tashkent, Ulaanbaatar, and Vientiane). ADB published the findings in Water in Asian Cities:Utilities’ Performance and Civil Society Views. The views of civil society were also collected and synthesized, and areappended to the publication..

2 The studies were funded under Regional Technical Assistance 6031: Promoting Effective Water Management Policiesand Practices, 26 April 2002.

Introduction

2

Cebu Delhi Dhaka HCMC Jakarta Kathmandu Shanghai Ulaanbaatar Region SEA South Asia South Asia GMS SEA South Asia East Asia Central Asia Country Philippines India Bangladesh Viet Nam Indonesia Nepal PRC Mongolia Population (in million)

0.655 13.8 10.5 5.3 8.35 1 13 0.74

Growth rate (%) 1.6 3.8 4.2 1.3 2.4 6 < 0 4.5 Surface area (km²) 326 1,483 360 2,095 660 100 6,340 3,450 Population density (p/km2)

9.26 9,300 95.3 2,520 12,620 17.57 2,050 13.3

Average GDP ($/y/cap.)

400 810 630 720 366 573 2,000 440

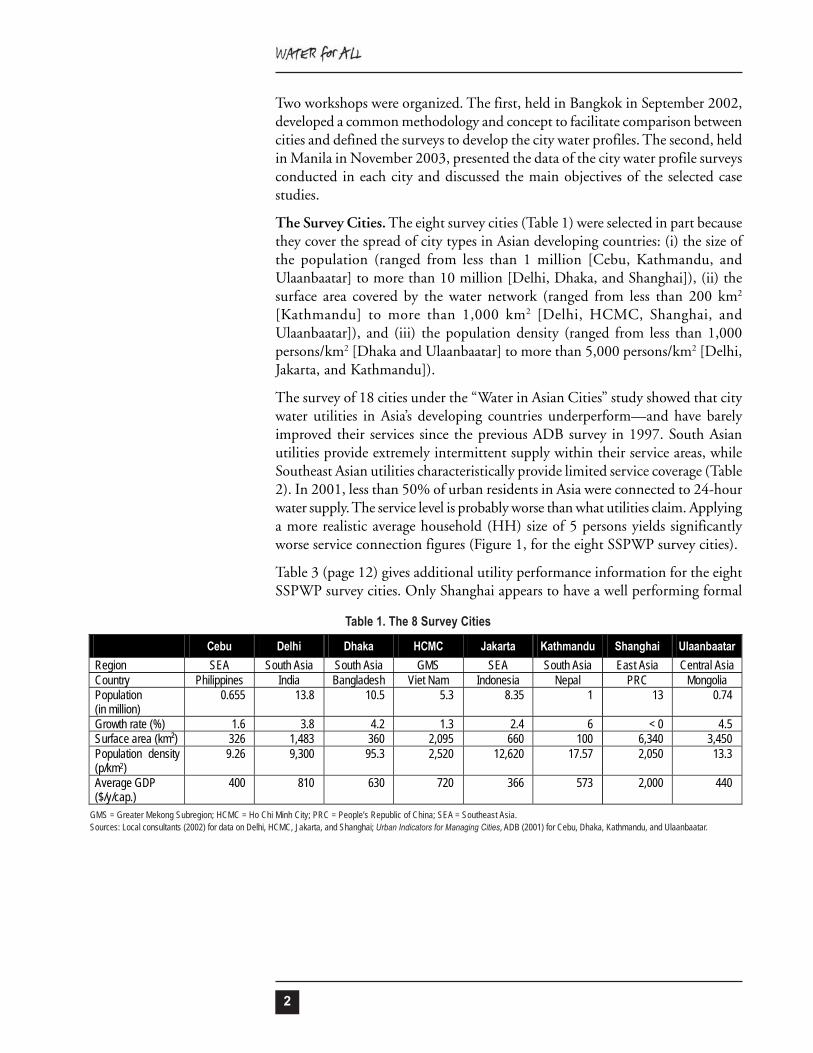

Two workshops were organized. The first, held in Bangkok in September 2002,developed a common methodology and concept to facilitate comparison betweencities and defined the surveys to develop the city water profiles. The second, heldin Manila in November 2003, presented the data of the city water profile surveysconducted in each city and discussed the main objectives of the selected casestudies.

The Survey Cities. The eight survey cities (Table 1) were selected in part becausethey cover the spread of city types in Asian developing countries: (i) the size ofthe population (ranged from less than 1 million [Cebu, Kathmandu, andUlaanbaatar] to more than 10 million [Delhi, Dhaka, and Shanghai]), (ii) thesurface area covered by the water network (ranged from less than 200 km2

[Kathmandu] to more than 1,000 km2 [Delhi, HCMC, Shanghai, andUlaanbaatar]), and (iii) the population density (ranged from less than 1,000persons/km2 [Dhaka and Ulaanbaatar] to more than 5,000 persons/km2 [Delhi,Jakarta, and Kathmandu]).

The survey of 18 cities under the “Water in Asian Cities” study showed that citywater utilities in Asia’s developing countries underperform—and have barelyimproved their services since the previous ADB survey in 1997. South Asianutilities provide extremely intermittent supply within their service areas, whileSoutheast Asian utilities characteristically provide limited service coverage (Table2). In 2001, less than 50% of urban residents in Asia were connected to 24-hourwater supply. The service level is probably worse than what utilities claim. Applyinga more realistic average household (HH) size of 5 persons yields significantlyworse service connection figures (Figure 1, for the eight SSPWP survey cities).

Table 3 (page 12) gives additional utility performance information for the eightSSPWP survey cities. Only Shanghai appears to have a well performing formal

Table 1. The 8 Survey Cities

GMS = Greater Mekong Subregion; HCMC = Ho Chi Minh City; PRC = People’s Republic of China; SEA = Southeast Asia.Sources: Local consultants (2002) for data on Delhi, HCMC, Jakarta, and Shanghai; Urban Indicators for Managing Cities, ADB (2001) for Cebu, Dhaka, Kathmandu, and Ulaanbaatar.

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

3

Figure 1. Percentage of Households Connected to Water Utility Network

HCMC = Ho Chi Minh City.Source: ADB. Water in Asian Cities (RETA 6031).

020406080

100

CebuDe lhi

DhakaHCMC

Jakarta

Ka thmandu

Shangha i

U laanbaa tar

% o

f hou

seho

lds

Table 2. Coverage and Water Availability in 18 Asian Cities (2001)

a Percentage of connections served with 24-hour continuous supply.b This does not include about 151,860 people served by 2,531 public taps in tenement gardens.Source: National GDP. World Bank website. Water Services: Water in Asian Cities.

Country National GDP ($/capita) City Coverage

(%) Supply Continuitya

(%) Central and East Asia Japan 33,550 Osaka 100 100 People’s Republic of China 960 Shanghai 100 100 People’s Republic of China 960 Chengdu 83 100 People’s Republic of China 24,750 Hong Kong 100 100 Uzbekistan 460 Tashkent 99 100 Southeast Asia Malaysia 3,540 Kuala Lumpur 100 100 Republic of Korea 9,930 Seoul 100 100 Philippines 1,020 Manila 58 88 Indonesia 710 Jakarta 51 92 Mekong Region Viet Nam 430 Ho Chi Minh City 84 75 Lao People’s Democratic Republic 310 Vientiane 63 50

Cambodia 280 Phnom Penh 84 100 South Asia Sri Lanka 840 Colombo 69b 60 Pakistan 410 Karachi 58 0 India 440 Delhi 69 1 Bangladesh 360 Dhaka 72 0 Nepal 230 Kathmandu 83 0

4

Tabl

e 3. L

evel

of S

ervic

e Pro

vided

by W

ater

Util

ities

in th

e 8 S

elect

ed C

ities

HCMC

= H

o Ch

i Minh

City

, HH

= ho

useh

old.

a The

situ

ation

in U

laanb

aata

r is q

uite

uniqu

e wi

th co

llecti

ve m

eter

s for

buil

dings

in th

e cit

y and

stan

dpipe

s in

low-in

come

fring

e ar

eas.

b Bas

ed o

n loc

al co

nsult

ants’

not

es (2

002)

; see

Table

2.

c Fro

m As

ian W

ater

Sup

plies

: Rea

ching

the U

rban

Poo

r, App

endix

1: C

ity W

ater

Pro

files a

nd S

umma

ry F

inding

s. AD

B an

d Int

erna

tiona

l Wat

er A

ssoc

iation

. 200

3 (ex

cept

for

Cebu

case

stud

ies).

d Tra

dition

al te

nt d

wellin

g of

Mon

golia

n no

mads

.So

urce

: ADB

. 200

3. W

ater

in A

sian

Citie

s: Ut

ilities

’ Per

form

ance

and

Civi

l Soc

iety V

iews (

exce

pt C

ebu,

% o

f HH

conn

ectio

ns, a

nd a

s not

ed).

Ce

bu

Delh

i Dh

aka

HCMC

Ja

karta

Ka

thm

andu

Sh

angh

ai Ul

aanb

aata

ra

Popu

lation

b 72

0,000

13

,800,0

00

10,50

0,000

5,3

00,00

0 8,3

50,00

0 1,0

00,00

0 13

,000,0

00

740,0

00

Name

of w

ater u

tility

Metro

Ceb

u Wate

r Di

strict

(MCW

D)

Delhi

Jal B

oard

(D

JB)

Dhak

a Wate

r Su

pply

and

Sewe

rage

Au

thority

(DW

ASA)

Ho C

hi Mi

nh W

ater

Supp

ly Co

mpan

y

Pam

Lyon

naise

Ja

ya

& Th

ames

Pam

Ja

ya

Nepa

l Wate

r Su

pply

Corp

orati

on(N

WSC

) --

Wate

r Utili

ty Co

mpan

y of

Ulaa

nbaa

tar C

ity

(USA

G)

Statu

s Go

vern

ment

Corp

orati

on

Gove

rnme

nt Co

mpan

y Go

vern

ment

Corp

orati

on

Prov

incial

Co

mpan

y Pr

ivate

Com

panie

s Go

vern

ment

Corp

orati

on

Munic

ipal: 2

Di

strict

: 39

Town

: 152

St

ate E

nterp

rise

Nonr

even

ue w

ater (

%)

n/a

53%

40

38

51

37

16

36

Staff

per 1

,000 c

onne

ction

s n/a

20

11

3.5

5.3

15

5.7

82

3

% of

surfa

ce w

ater

Low

83%

2

58

100

62

70

0

% of

HHs

that

have

acce

ss

to pip

ed sy

stem

n/a

69%

72

84

51

83

10

0 49

% of

HH

conn

ectio

n

35%

65%

10

57

54

71

10

0 53

No. o

f con

necti

ons

51

,730

1,3

75,00

0 18

5,000

33

0,000

61

0,000

12

3,000

3,0

00,00

0 1,4

00

Wate

r ava

ilabil

ity (h

ours)

18–2

4

2–4

16

24

18

2–4

24

21

% of

HHs

with

24-h

servi

ce

n/a

1%

0%

75

92

0 10

0 48

Socia

l tariff

($)c

0.24

0.03

0.06–

0.08

0.11

0.04

0.08

0.12

0.19 d

ownto

wn

0.5 in

gerd a

rea

Aver

age c

onne

ction

fee

($)

100

2 29

53

9–

38

20

83

450

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

5

water market. Interestingly, this is achieved with a metro total of 193 separatewater utilities. The case of Jakarta shows how difficult it will be to pull backwater supply (let alone sanitation) service deficits in low-income cities (Box 1).

Household Survey. To better appreciate the scope and scale of SSPWPs in Asiancities, a common customers’ survey was implemented by national consultants ineach of the eight selected cities. Around 500 households in each city (exceptShanghai3) were selected randomly for the sample to represent the different watersupply situations present at city scale, within and beyond the area covered by thewater utility. The different water supply situations are defined by services providedboth by the city water utility and traditional water points. In areas served by thewater utility, the main services provided are household connections, standpipes,and tanker services. In areas not served, the main existing services are wells (openand tube wells) where groundwater sources are available.

Representative areas for the survey were selected for each situation, and the sizeof the sample in each selected area was defined according to the percentage ofpopulation living in such areas. Box 2 (next page) shows the approach forKathmandu.

The survey questionnaire was developed by the project team and adapted by thelocal consultants to take into account the specificities of their water situation.Due to the limited size of the sample compared with the population living in theeight cities (0.7–14 million), the results are not statistically representative, butprovide an estimate of the scope and scale of SSPWPs.

3 No household survey was carried out in Shanghai where the whole population is connected to pipe systems managedby water utilities. The field survey in Shanghai instead focused on remote and migrant living areas to check possibleinvolvement of SSPWPs. However, no SSPWPs were found.

Based on data provided by the Jakarta Water SupplyRegulatory Body for the Water in Asian Cities study (ADB 2003),there are 602,000 individual connections serving a population ofaround 4,580,000 in metro Jakarta (yielding an unlikely 7.6persons/connection). Metro Jakarta’s population is around 10million.

With a yearly population growth of around 2.5% and aprogram to connect each year around 50,000 new customers(10% more than achieved annually during the last 5 years), thepercentage of people who will not have an individual connectionin 2015 will be 31% compared with 54% in 2002.

In real terms, this means that around 4.3 million metro Jakartaresidents in 2015 will still be without water connection comparedwith 5.4 million today.

Box 1. Jakarta: More than 4 Million PeopleStill Without House Connection in 2015

202530354045505560

2002 20152,000,000 2,500,000 3,000,000 3,500,000 4,000,000 4,500,000 5,000,000 5,500,000 6,000,000

% of population without house connection

No. of people without house connection

% o

f pop

ulat

ion

No.

of p

eopl

e

6

Box 2. Survey Structure for Kathmandu

TRIBHUW AN A IRPORT

Pa sh u p a tinath

BUD HANATH

M AHARAJGU NJ

TRIBHUW AN

K A T H M A N D U M E T R O P O L I T A N C I T YBAN ESW OR

SW AYAM BHU NATH

N AGARJUN BAN

U NIVERSITY

KA

NTI

RAJ

PATH

BASBARIGAGABU

N EPALTAR

RAN IBAN

BAL AJU

N AYABAJARHARIGAU

C ABAHIL

TRIPU RESW AR

RABI BHAW AN

KOPUN DOLTHAPATHALI

M IN BHAW AN

THANAGAU

L AL ITPUR

HOSPITAL

JAU LAKHEL

OKHTHANKHU M ALTAR

D HAPAKHEL

GOTHATAR

VOC ATIONALTRAIN IN G CENTRE

KOTESW AR

BARAL GAU

N AIKAP

KAL AN KITHAN

(P. BHANJYANG)

16

29

3

4

26

5

7

8

9

34

10

32

3331

11

30

17

15

132019

18 282726

25 24

2221

23

12

14

35

2 110

22

162120 18 11

6

1219

5

13

4

1514

39

8

7

1

17

5

KATHMANDU & LALITPUR MUNICIPALITY

ICHHANGU

D HAPASI

L A L I T P U R S U B M E T R O P O L I T A N

Kat

hman

du C

ore

Kat

hman

du C

entra

l

Kat

hman

du N

orth

Kat

hman

du W

est

Kat

hman

du E

ast

15

10

3

4

21

6

9

7

8

Lal

itpur

Ext

ensi

on

Lal

itpur

Ext

ensi

on

Lalitpur Extension

CoreLalitpur

8

C I T Y

Kathmandu and Lalitpur have 57 wards distributed in 8 mainareas.

For the survey, 15 wards were selected to represent thedifferent city areas:

(a) Kathmandu Metropolitan Corporation (12):- Kathmandu Core, 3- Kathmandu Central, 2- Kathmandu North, 2- Kathmandu West, 2- Kathmandu East, 3

(b) Lalitpur Sub Metropolitan Corporation (3):- Lalitpur Core, 1- Lalitpur North, 1- Lalitpur South, 1

The selected wards cover around 70,000 people. A total of540 households (HHs) were surveyed.

Methodology followed to select HHs to be surveyed:1. Enumerator approached the selected ward office.2. With the support of ward officials, enumerator selected

five different categories of areas covered by the utility.3. Enumerator selected in each of these areas the required

numbers of HHs belonging to four income categories andexecuted the survey.

Due to the very low percentage of HHs surveyed (4% of theselected wards and around 0.3% of total population), 15 focusgroups were organized (one in each selected ward) tocomplement the information collected through interviews.

Source: Local consultant.

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

7

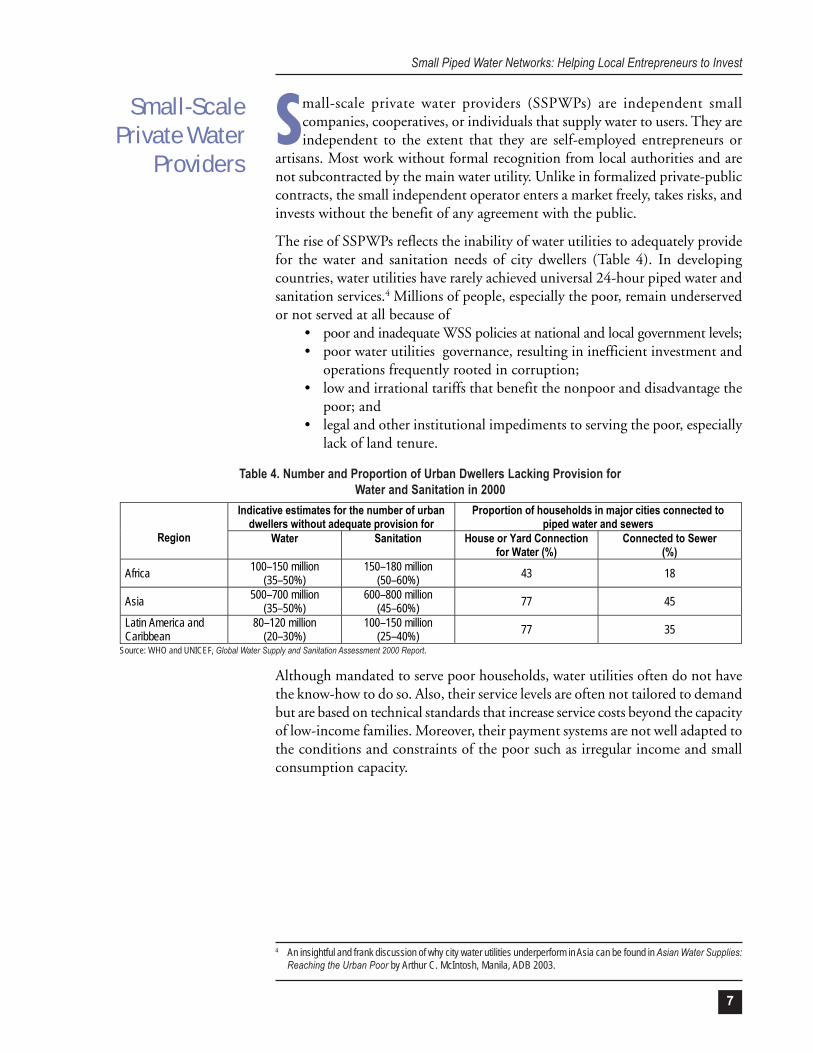

Small-scale private water providers (SSPWPs) are independent smallcompanies, cooperatives, or individuals that supply water to users. They areindependent to the extent that they are self-employed entrepreneurs or

artisans. Most work without formal recognition from local authorities and arenot subcontracted by the main water utility. Unlike in formalized private-publiccontracts, the small independent operator enters a market freely, takes risks, andinvests without the benefit of any agreement with the public.

The rise of SSPWPs reflects the inability of water utilities to adequately providefor the water and sanitation needs of city dwellers (Table 4). In developingcountries, water utilities have rarely achieved universal 24-hour piped water andsanitation services.4 Millions of people, especially the poor, remain underservedor not served at all because of

• poor and inadequate WSS policies at national and local government levels;• poor water utilities governance, resulting in inefficient investment and

operations frequently rooted in corruption;• low and irrational tariffs that benefit the nonpoor and disadvantage the

poor; and• legal and other institutional impediments to serving the poor, especially

lack of land tenure.

Small-ScalePrivate Water

Providers

Although mandated to serve poor households, water utilities often do not havethe know-how to do so. Also, their service levels are often not tailored to demandbut are based on technical standards that increase service costs beyond the capacityof low-income families. Moreover, their payment systems are not well adapted tothe conditions and constraints of the poor such as irregular income and smallconsumption capacity.

4 An insightful and frank discussion of why city water utilities underperform in Asia can be found in Asian Water Supplies:Reaching the Urban Poor by Arthur C. McIntosh, Manila, ADB 2003.

Indicative estimates for the number of urban dwellers without adequate provision for

Proportion of households in major cities connected to piped water and sewers

Region Water Sanitation House or Yard Connection for Water (%)

Connected to Sewer (%)

Africa 100–150 million (35–50%)

150–180 million (50–60%) 43 18

Asia 500–700 million (35–50%)

600–800 million (45–60%) 77 45

Latin America and Caribbean

80–120 million (20–30%)

100–150 million (25–40%) 77 35

Table 4. Number and Proportion of Urban Dwellers Lacking Provision forWater and Sanitation in 2000

Source: WHO and UNICEF, Global Water Supply and Sanitation Assessment 2000 Report.

8

International experience shows that SSPWPs, in comparison with water utilities,can be more dynamic in filling the gap between supply and demand and havemore incentives to grow and expand their services (Box 3). Be they vendors,tanker truck operators, or managers of small-scale distribution networks, SSPWPsprovide a competitive and appropriate service to households that have no accessto utility connection.5 This is evident in Africa, Asia, and Latin America whereSSPWPs serve large urban populations. (See Paraguay example, Box 4.)

Profit orientation strengthens SSPWPs. Sustained and motivated by profits,SSPWPs may be longer lasting and more expansionary than cooperatives, NGOs,and other not-for-profit providers.

5 Findings of this research have been summarized in the following papers: Competition in Water and Sanitation:TheRole of Small Scale Entrepreneurs (Tova, Maria Solo, Private Sector Viewpoint, Note No. 165, December, 1998, TheWorld Bank); Independent Water and Sanitation Providers in African Cities: Full Report of a Ten-Country Study (BernardCollignon and Marc Vezina, 2000).

An estimated one third of the water connections made in the past 20 years in Asuncion andCiudad del Este have been provided by aguateros. (A typical aguateria system supplies a cluster ofhouses and consists of a well, a pump house, and heavy polyethylene hosing. The system is relativelyinexpensive and simple to install.) There are 350–600 independent aguaterias currently operating.Theyserve about half a million persons and represent an investment of some $30 million, at roughly $250/household.

Development is completely private. The aguatero makes the full investment and assumes allthe risks. The customer must pay a connection fee, which is in fact the aguatero’s principal incomefor amortizing the investment. The installations’ precarious nature and legal insecurity in the mediumterm means that the investment must have a short payback, generally within 3 years.Source: Torayno, Fernando.Small Scale Water Providers in Paraguay. Water and Sanitation Program, The WorldBank, Working Paper Series, January 1999.

Box 4. Small-Scale Water Providers in Paraguay

The operational efficiency of small private operators compares well with that of large utilities. Astudy of Haiti and four West African countries reported virtually no water losses among the privateoperators. It further showed the private firms to have an employee-client ratio of 1:500, one that anyutility company would envy. The study in Guatemala compared two private operators of aqueductand sanitation systems with the state water company. The study found that the investment costs ofthe two private operators per new customer were lower than the state utility’s—20% and 60%,respectively. The private firms’ operating costs were also lower, 72% and 77%, and administrativecosts again lower, 92% and 95%, respectively.Source: Tova, Maria Solo. December 1998. Competition in Water and Sanitation: The Role of Small ScaleEntrepreneurs. Private Sector Viewpoint Note No. 165. The World Bank.

Box 3. Competition in Water and Sanitation:Efficient Small-Scale Suppliers

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

9

SSPWPs as defined by the researchFor the purpose of the SSPWP research, the project team defined “small-scaleprivate water provider” as having all of the following characteristics:

Small in scale. The provider’s infrastructure or installation is not city-wide andcovers only a single neighborhood or a part of it. The business has a staff of lessthan 100 and is, more often than not, owner-managed.

Independent. The provider does not receive any public subsidies or supportfrom NGOs.

Private. Capital investment comes from private sources. Providing water is themain livelihood of the people behind the venture. The business is not driven byexternal investors.

According to this characterization, community organizations and NGOs thatrely on volunteer work and receive financial aid from charities, other NGOs,and donor agencies are not considered SSPWPs.

How SSPWPs supply waterSSPWPs provide water by any of the following means: (i) having customers collectwater from the provider’s source, (ii) transporting water to customers’ homes, (iii)piping water to customers’ homes, and (iv) treating and selling water in bottles orbarrels.

Having customers collect water from the provider’s source. Customers areneighbors who collect water from the provider’s dug well, hand pump, or waterutility connection. Generally this enterprise requires only a small investment.Income from this is commensurately small and supplements other householdincome.

Transporting water to customers’ homes. From a point source, vendors transportwater by vehicle, ranging from a small pushcart to a large tanker truck. Customersprovide their own storage or containers. Carters can deliver relatively smallvolumes (20–200 liters) while trucks can distribute several cubic meters at atime. The required investment varies: from a few dollars for a cart to $10,000 for atanker truck.

Piping water to customers’ homes. Operators of such systems (also called“pioneers”) build and run small piped networks with individual connections tocustomers’ homes. The operators either produce the water themselves or buy itin bulk from the water utility. If customers cannot afford a piped connection,the operators can also supply water by hose. Small network operators invest largeamounts ($5,000–100,000) for fixed installations. Quality of service is high andmatches the expectations of urban users.

Treating and selling water in bottles or barrels. Operators sell potable bottledor barreled water in shops and markets and can also deliver directly to customers’homes. Such operators account for only a small quantity of water supplied to

10

users. Investment in this type of operation may range from $5,000 to $100,000,depending on the quality of raw water and the technology used to treat it.

SSPWP usersFor the purpose of the research, a user is considered to be served by an SSPWP ifhe or she hires or pays for SSPWP services on a regular basis at least during thedry season when other sources (utility or natural) cannot fill the daily waterneeds.

Many surveys have shown that water users, including low-income users, willreadily pay for

Convenience. Users do not have to travel long distances or waste time queuingfor water.Reliability. They are assured of continuous (uninterrupted) service or, if notcontinuous, on a regular basis (same time every day); this facilitateshousekeeping.Quantity. They are assured of enough water to cover their needs for dailyhouse chores.Quality. They are assured of “safe” drinking water and “clean” water forcooking, dishwashing, bathing, and laundry.Affordability. According to surveys, low-income families are willing to spendaround 3–5% of their income on water; they also prefer to pay in smallamounts (daily or every few days) and pay connection fees by installment.

Different types of SSPWPs satisfy these demand characteristics to varying degrees(Figure 2). Surveys further show that poorly served households prefer a houseconnection as their first choice, a private well as their second choice if conditionsallow, and a shared connection or community-based model as their third choicedepending on the type of management involved.6 These preferences usually exceedthe service available to them (Box 5).

In Cebu (Philippines), residents living in areas not served by the water utilityand who get water from vendors or standpipes stated in a survey7 their criteriafor satisfaction: accessibility (> 80%), quality (78%), and affordability (55%).This shows that even among the poor, the top criteria is not affordability but acompromise between accessibility and quality.

6 Survey in Phialat (Lao People’s Democratic Republic), AsiaUrbs Project, BURGEAP, 2001.7 The survey was undertaken by V. Verdeil in 2001 as part of a research thesis, Local Water Markets: Practices and

Territory of the Water Supply in Metro Cebu, March 2003.

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

11

A field survey carried out during October–December 2001 covered about 2,900 households inrural areas with different water availability situations (high and low water table, coastal area, arsenicissues, etc.). Whatever the water and socioeconomic situations, there is a strong demand for pipedwater. Willingness to pay (WTP) is around taka (Tk)50 ($0.9)/month for public standpipes comparedwith Tk90 ($1.5)/month for domestic connections. For the initial capital cost the ratio is around thesame with a WTP of $16 for standpipe and $30 for domestic connection.

The estimated mean WTP of all households taken together exceeds the actual operation andmaintenance (O&M) costs of supplying piped water. Even the WTP of poor households is on averagemore than the O&M cost of piped water supply, both for public standpipes and domestic connection.Source: The World Bank’s Water and Sanitation Program, South Asia Region, Field Note, December 2002.

Box 5. Willingness to Pay for Safe Drinking Waterin Rural Bangladesh

Figure 2. Demand-Response Characteristics of SSPWP Types

Note: Representations in this Figure were prepared by the study team.

TYPE OF SERVICE Pushcart CRITERIA RESPONSE

Quantity Low volume per service (maximum = 200 liters)

Quality Depends on water source. Generally water quality deteriorates during transportation.

Reliability and Convenience

Service is provided at home, generally on request. 0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability

Retail water is generally expensive, but actual amounts paid are low due to low quantity served at each time.

Standpipe

Quantity

People who fetch water from a point source or standpipe consume less water than those with a house connection (20–30 l/p/d compared to 50 l/p/d)

Quality Water from tap is usually safe. Contamination occurs during transport to house.

Reliability and Convenience

Point source can be located at some distance from home. Standpipes are not open all the time (8–12 hours/day) and users may have to queue. Area around tap is often muddy.

0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability

Though cost of having a standpipe attendant inflates the volumetric cost of water, amounts paid remain low due to low volumes.

House Connection

Quantity Users consume as much water as they want if service is reliable.

Quality Quality will depend on the source and effectiveness of treatment.

Reliability/ Convenience

Service design ranges from 24 hours continuous to intermittent (but regular, depending on reliability of electricity supply).

0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability

Connection fees range from $15 to $100. Tariffs are generally lower for people connected to a piped system than for those not connected.

12

Around 20% of residents in the selected cities (except Shanghai) regularlyget their water from SSPWPs either to (i) supplement unreliable water utilityservices or groundwater sources during the dry season, or (ii) cover all their

water needs.

Figure 3 shows how water utilities in the survey cities respond to the demandcharacteristics introduced in Figure 2. These significant differences in demand-response characteristics have resulted in a spread of SSPWP opportunities andresponses in the eight survey cities.

Scope and Scaleof SSPWPs in

Asian Cities

Figure 3. Demand-Response Characteristics of UtilitiesCITY

Delhi (similar for Dhaka and Kathmandu) CRITERIA RESPONSE

Quantity Low volume partly due to limited water resources.

Quality Water quality is variable due to intermittent supply.

Reliability and convenience

Only 1% of the population has access to 24-hour service and 70% of households get water for less than 4 hours per day regardless of their income level.

0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability Water tariff is very low: $0.03/m3 and $2 for connection.

Ho Chi Minh City (similar for Jakarta and Cebu)

Quantity Households connected to network generally get the expected quantity of water.

Quality The water quality generally seems good but is at risk due to high levels of leakage

Reliability and convenience

Around 75% of customers have 24-hour water supply.

0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability Water tariff: $0.11/m3 Average connection fee: $53

Shanghai

Quantity Households connected to network get the expected quantity of water.

Quality Water quality is generally good. Reliability and convenience

100% of customers have 24-hour water supply. 0

0.5

1Quantity

Quality

Affordability

Reliability

Affordability Water tariff: $0.12/m3 Average connection fee: $83, but has been cancelled recently.

Note: Ulaanbaatar was not included as its situation differs substantially from the other cities—all houses and apartmentsare connected to the network, and informal settlements are served by water kiosks (standpipe).

Table 5. Various Water Situations in the 8 Survey CitiesWater

Situation Cities Utility Coverage

Reliability of Service

Alternative Sources

Income vs. Service Cost Niche Market for SSPWP

1 Shanghai High High Low High No niche market except for bottled water

Delhi Medium Low High High Dhaka Medium Low High Medium 2

Kathmandu Medium Low High High

Competitive market to supplement the low service provided by water utility (WU)

Cebu Low High Medium Low Ho Chi Minh

City Low High Medium Low 3

Jakarta Low High Medium Low

Supplementary market for low- income HHs in areas served by WU Big market opportunities in areas not served by WU

4 Ulaanbaatar Low Low Low Low Low market opportunities in ger areas due to low accessibility to water resources

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

13

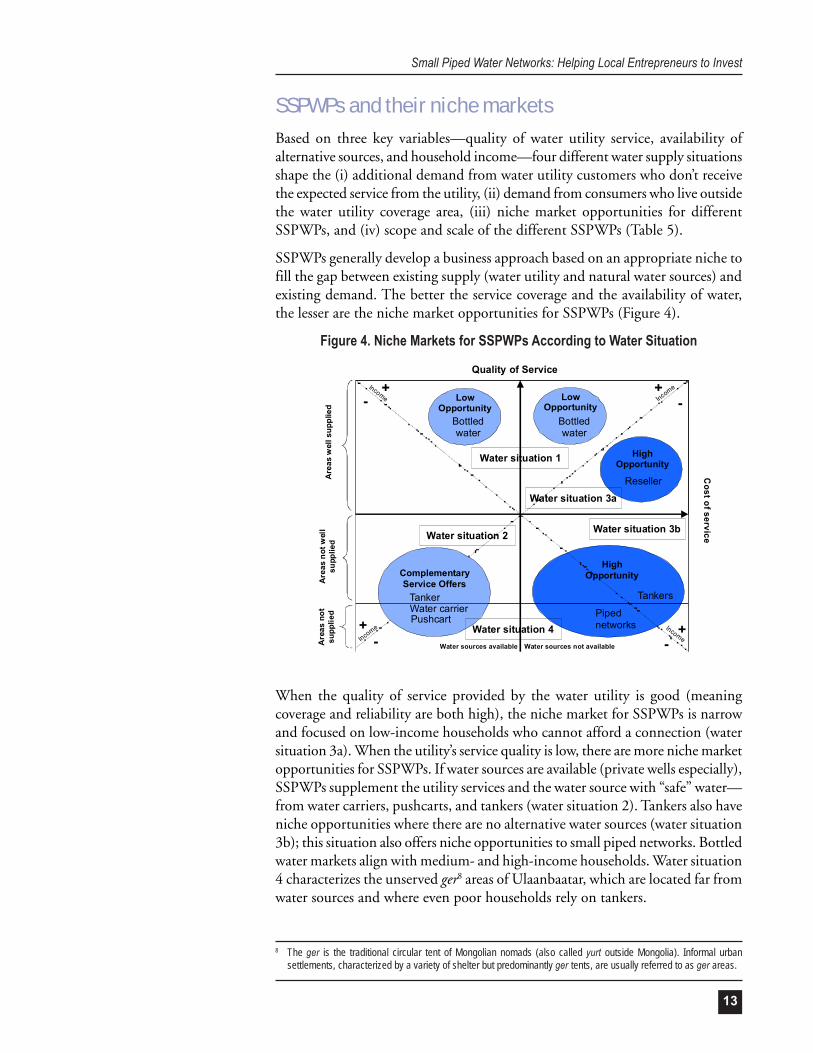

SSPWPs and their niche marketsBased on three key variables—quality of water utility service, availability ofalternative sources, and household income—four different water supply situationsshape the (i) additional demand from water utility customers who don’t receivethe expected service from the utility, (ii) demand from consumers who live outsidethe water utility coverage area, (iii) niche market opportunities for differentSSPWPs, and (iv) scope and scale of the different SSPWPs (Table 5).

SSPWPs generally develop a business approach based on an appropriate niche tofill the gap between existing supply (water utility and natural water sources) andexisting demand. The better the service coverage and the availability of water,the lesser are the niche market opportunities for SSPWPs (Figure 4).

When the quality of service provided by the water utility is good (meaningcoverage and reliability are both high), the niche market for SSPWPs is narrowand focused on low-income households who cannot afford a connection (watersituation 3a). When the utility’s service quality is low, there are more niche marketopportunities for SSPWPs. If water sources are available (private wells especially),SSPWPs supplement the utility services and the water source with “safe” water—from water carriers, pushcarts, and tankers (water situation 2). Tankers also haveniche opportunities where there are no alternative water sources (water situation3b); this situation also offers niche opportunities to small piped networks. Bottledwater markets align with medium- and high-income households. Water situation4 characterizes the unserved ger8 areas of Ulaanbaatar, which are located far fromwater sources and where even poor households rely on tankers.

8 The ger is the traditional circular tent of Mongolian nomads (also called yurt outside Mongolia). Informal urbansettlements, characterized by a variety of shelter but predominantly ger tents, are usually referred to as ger areas.

Figure 4. Niche Markets for SSPWPs According to Water Situation

Costofservice

Quality of Service

Are

asw

ells

uppl

ied

Are

asno

twel

lsu

pplie

dA

reas

not

supp

lied

Water sources available Water sources not available

IncomeIncome+

+ +

+

Income Income

--

--

LowOpportunity

LowOpportunity

Bottledwater

Water situation 3b

PushcartWater carrierTanker

ComplementaryService Offers

HighOpportunity

HighOpportunity

Bottledwater

Reseller

Pipednetworks

Tankers

Water situation 4

Water situation 2

Water situation 3a

Water situation 1

14

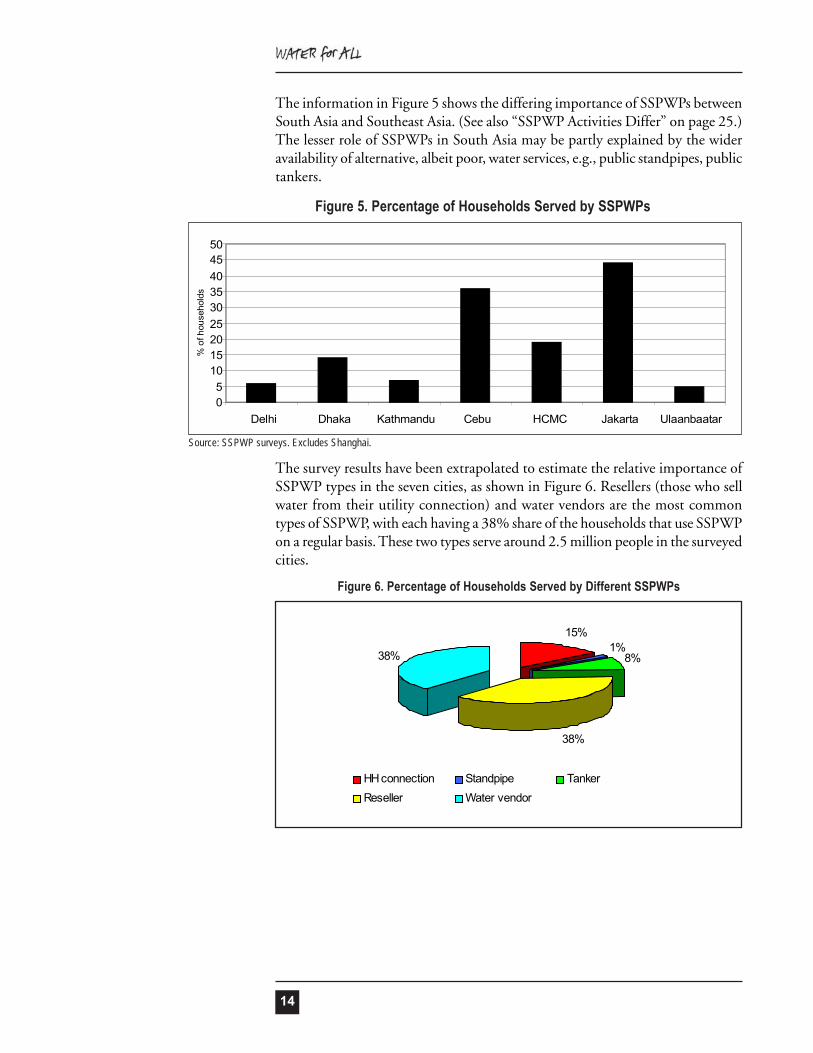

The information in Figure 5 shows the differing importance of SSPWPs betweenSouth Asia and Southeast Asia. (See also “SSPWP Activities Differ” on page 25.)The lesser role of SSPWPs in South Asia may be partly explained by the wideravailability of alternative, albeit poor, water services, e.g., public standpipes, publictankers.

15%1%

8%

38%

38%

HH connection Standpipe TankerReseller Water vendor

Figure 6. Percentage of Households Served by Different SSPWPs

The survey results have been extrapolated to estimate the relative importance ofSSPWP types in the seven cities, as shown in Figure 6. Resellers (those who sellwater from their utility connection) and water vendors are the most commontypes of SSPWP, with each having a 38% share of the households that use SSPWPon a regular basis. These two types serve around 2.5 million people in the surveyedcities.

Figure 5. Percentage of Households Served by SSPWPs

Source: SSPWP surveys. Excludes Shanghai.

05

101520253035404550

Delhi Dhaka Kathmandu Cebu HCMC Jakarta Ulaanbaatar

% o

f hou

seho

lds

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

15

Because of the increasing demand for potable water, bottlers of drinking waterhave also become important players. The bottled water business has grown rapidlyin the survey cities, particularly in Shanghai (Box 6). Bottled water markets areusually characterized by (i) uncertain quality of the utility’s water, (ii) higherincome levels of the population, and (iii) increased health awareness. Around 5–20% of residents in the surveyed cities drink bottled water. Bottlers in the surveycities number from 10 to a few hundred and produce around 5–10 m3 per dayper enterprise. These small enterprises use various treatment technologies (fromUV ozonation to reverse osmosis) and package their water in containers rangingin size from 1 to 20 liters. They generally sell the bottled water directly to customersnear their bottling premises.

Non-SSPWP alternative sourcesAside from SSPWPs, private wells and community systems are also importantalternative water sources.

Private Wells (Own Source). Data from the household surveys highlight theimportance of private wells (open or equipped with a manual or electric pump)for city households, particularly in areas not served by water utilities. In theseven selected cities, an average 24% of households use wells to cover their dailyneeds at least partially. In South Asia, well water is readily accessible and is oftenused by people connected to the utility piped system to supplement poor service.

It is estimated that around 700,000 m3 of water are bottled or barreled in Shanghai every year.Typically, bottled water comes in containers less than 10 liters in capacity and barreled water incontainers 10–20 liters in capacity. Shanghai’s consumption of bottled and barreled water is muchhigher than its production since surrounding provinces also supply the city with such water. Bottledand barreled water is mainly consumed by offices and about 40% of households in Shanghai. Demandcontinues to rise.

There were approximately 100 bottled water suppliers and 300 barreled water suppliers inShanghai in 2001. Large-scale producers accounted for almost all the bottled water production whilesmall-scale producers accounted for 70–80% of the barreled water production. Typically, small-scaleproducers have a capacity of less than 30 m3/d and do only barreling. They account for less than10% of market share and merely supplement the production of large-scale bottlers.

Small-scale producers offer lower prices than large-scale producers. Small producers reducecosts by avoiding advertising, transporting their product over short distances, and benefiting fromgovernment tax breaks. They mainly serve low- to medium-income families. Small bottlers haveproliferated because of low investment requirements, easy technology and operation, and limitedgovernment supervision.

Quality control by small producers is poorer than that of large producers. Stricter governmentsupervision and control may expel some poorly operated bottlers and barrelers from the market.

Example of a typical small-scale producer in Shanghai:· Capacity: 0.6–1 m3/d · Households served: 300–500· Working staff: 3–4 persons · Gross value: $12–15/m3

· Investment: $6,000 · Net value: $7–10/m3

· Shipment: bicycle or tricycleSource: Zhang Windy, ERM Shanghai.

Box 6. Small-Scale Bottled and BarreledWater Suppliers in Shanghai

16

In Southeast Asia, wells are used mainly by people living in areas not served bywater utilities.

Community Systems. People in the survey cities also get their water fromcommunity systems: 55% of Dhaka residents access systems developed by NGOsand communities, 15% of Cebu’s population get their water from systems builtby community organizations, and 22% of Kathmandu’s inhabitants fetch waterfrom traditional stone spouts.

In Dhaka, NGOs have developed water supply projects aimed at providing betterservice in low-income informal settlements which make up around 30% ofDhaka’s population. These settlements fall under the jurisdiction of the DhakaWater Supply and Sewerage Authority (DWASA) which has a strict policy onwater connections: it only provides connections to applicants on presentation ofa “holding number” confirming landownership. Since most slum dwellers aresquatters on government land, they cannot fulfill this requirement and are forcedto rely mainly on illegal connections established by those who control slumhousing. The NGO initiative involved negotiating with the Dhaka CityCorporation (DCC) to obtain permission for road cutting and situating waterpoints on DCC land. Under the project design, NGOs are the formal customersof the water utility and generally implement extensions from the main pipe systemto the slum areas where they provide water through specific water points.9 Theresponsibility for running the services is delegated to a community associationwho has to pay the DWASA water bills and reimburse the NGOs the cost ofsetting up the water points (around $750 each). The water tariff to cover chargesis around $0.46/m3, while the official DWASA rate is $0.13/m3. So far, NGOshave helped set up some 150 water points serving 17,500 families, or 110,000people. For low-income areas too far for the DWSA network to reach, NGOshave implemented boreholes equipped with hand pumps.

In Kathmandu, the traditional urban water supply system of dhunge dharas is theprimary alternative to the municipal piped supply. The spouts provide an essentialsource of water for the city’s middle- and low-income residents. The existence ofthis readily accessible public supply alters the dynamics of a water-scarce city,changing it from an environment of drastic inequality to one of varied access forall. Depending on where they live in the city, people spend up to 45 minuteswalking to the nearest dhunge dharas, often waiting in line for 6 or more hours.Water for the most part is free but the community may charge small fees for thespouts’ maintenance and improvement. However, the lack of effective institutionsand resources to undertake this threatens the spouts’ sustainability.

9 Comprising a 3 m3 underground tank with two suction hand pumps on top, and with separate bathing and washingplatforms.

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

17

SSPWP activities differThere are marked differences in the level of SSPWP activity between South Asiaand Southeast Asia, as well as between cities and among neighborhoods adequatelyserved and underserved/unserved by water utilities.

Between South Asia and Southeast Asia. In South Asia SSPWPs play a relativelyminor role (5–15%). In Delhi, Dhaka, and Kathmandu, SSPWPs co-existalongside utilities which provide irregular water at low pressure. They also haveto compete with alternative sources like utility standpipes and tankers (Delhi),open wells, tube wells with hand pumps, and community standpipes (Dhaka),or traditional stone waterspouts (Kathmandu).

People in these cities develop coping strategies between the different alternativesand diversify their water sources, shifting between suppliers depending on thetime of year, cost, reliability, and water quality and quantity to fill their dailyneeds. Table 6 and Figure 7 show the coping strategies in Kathmandu.

Table 6. Water Dynamics in KathmanduSource Available Household

Income NWSC Tanker Private Well Community Well Dhunge Dharaa

High X X X Rare Rare

High middle X X X Rare Rare

Middle X X X Rare X

Low middle X X X X X

Low X Rare X X

a Public waterspout.Source: Yarror Moench, 2001–ISET/NWCF.

Figure 7. Water Supplies Used in Dry Season in Kathmandu

0

10

20

30

40

50

60

70

80

NWSC HHconnection

NWSCstandpipe

NWSC tanker Neighbors'connection

Private tanker Communitysystem

Well

% o

f hou

seho

lds

HH = household, NWSC = Nepal Water Supply Corporation.Source: Household survey under ADB SSPWP study, K. K. Jha, October 2002.

18

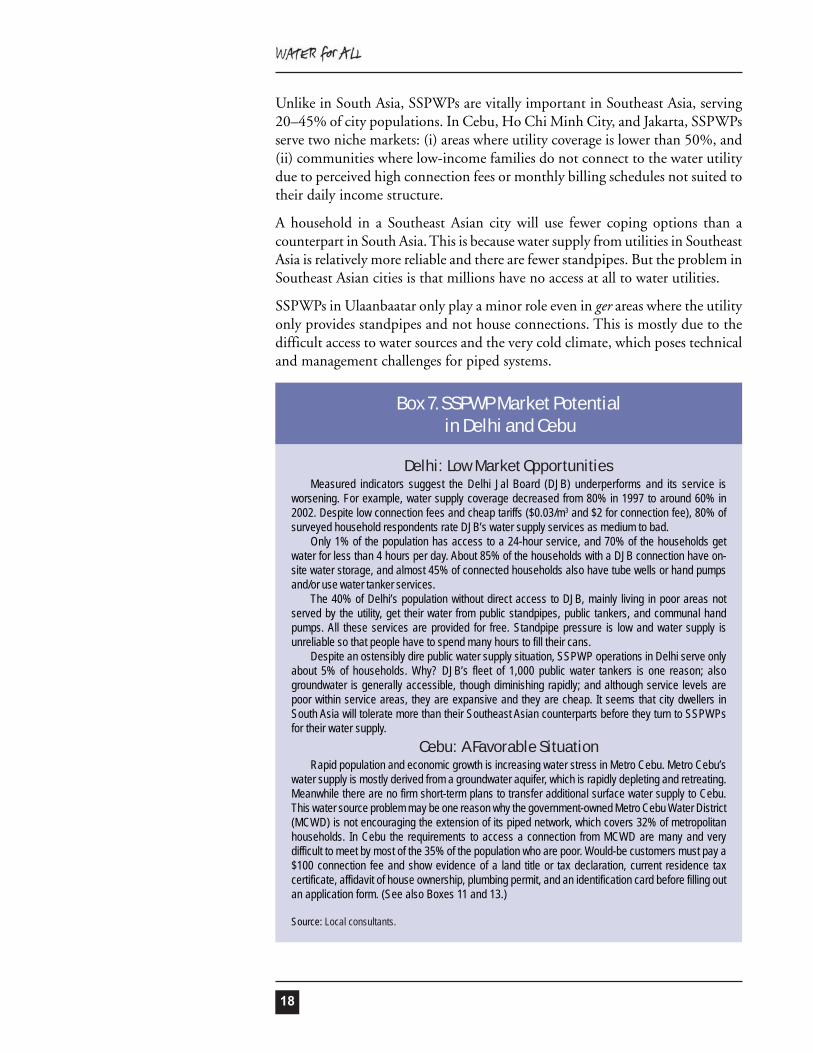

Unlike in South Asia, SSPWPs are vitally important in Southeast Asia, serving20–45% of city populations. In Cebu, Ho Chi Minh City, and Jakarta, SSPWPsserve two niche markets: (i) areas where utility coverage is lower than 50%, and(ii) communities where low-income families do not connect to the water utilitydue to perceived high connection fees or monthly billing schedules not suited totheir daily income structure.

A household in a Southeast Asian city will use fewer coping options than acounterpart in South Asia. This is because water supply from utilities in SoutheastAsia is relatively more reliable and there are fewer standpipes. But the problem inSoutheast Asian cities is that millions have no access at all to water utilities.

SSPWPs in Ulaanbaatar only play a minor role even in ger areas where the utilityonly provides standpipes and not house connections. This is mostly due to thedifficult access to water sources and the very cold climate, which poses technicaland management challenges for piped systems.

Delhi: Low Market OpportunitiesMeasured indicators suggest the Delhi Jal Board (DJB) underperforms and its service is

worsening. For example, water supply coverage decreased from 80% in 1997 to around 60% in2002. Despite low connection fees and cheap tariffs ($0.03/m3 and $2 for connection fee), 80% ofsurveyed household respondents rate DJB’s water supply services as medium to bad.

Only 1% of the population has access to a 24-hour service, and 70% of the households getwater for less than 4 hours per day. About 85% of the households with a DJB connection have on-site water storage, and almost 45% of connected households also have tube wells or hand pumpsand/or use water tanker services.

The 40% of Delhi’s population without direct access to DJB, mainly living in poor areas notserved by the utility, get their water from public standpipes, public tankers, and communal handpumps. All these services are provided for free. Standpipe pressure is low and water supply isunreliable so that people have to spend many hours to fill their cans.

Despite an ostensibly dire public water supply situation, SSPWP operations in Delhi serve onlyabout 5% of households. Why? DJB’s fleet of 1,000 public water tankers is one reason; alsogroundwater is generally accessible, though diminishing rapidly; and although service levels arepoor within service areas, they are expansive and they are cheap. It seems that city dwellers inSouth Asia will tolerate more than their Southeast Asian counterparts before they turn to SSPWPsfor their water supply.

Cebu: A Favorable SituationRapid population and economic growth is increasing water stress in Metro Cebu. Metro Cebu’s

water supply is mostly derived from a groundwater aquifer, which is rapidly depleting and retreating.Meanwhile there are no firm short-term plans to transfer additional surface water supply to Cebu.This water source problem may be one reason why the government-owned Metro Cebu Water District(MCWD) is not encouraging the extension of its piped network, which covers 32% of metropolitanhouseholds. In Cebu the requirements to access a connection from MCWD are many and verydifficult to meet by most of the 35% of the population who are poor. Would-be customers must pay a$100 connection fee and show evidence of a land title or tax declaration, current residence taxcertificate, affidavit of house ownership, plumbing permit, and an identification card before filling outan application form. (See also Boxes 11 and 13.)

Source: Local consultants.

Box 7. SSPWP Market Potential in Delhi and Cebu

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

19

SSPWPs seek and serve niche markets, as illustrated earlier in Figure 4. Whereutility service is good and cheap or where there are alternative water sources, theniche market for SSPWPs is small. The scope for SSPWP involvement becomesgreater when the utility’s service is poor or relatively expensive in an environmentwith limited alternative sources. The different water situations in Delhi and Cebuhave a strong impact on SSPWP market share (Box 7).

Figure 9. SSPWP Services in the Survey Cities (within and outside utility service areas)

HH = household, HCMC = Ho Chi Minh CityNote: Total SSPWP market shares vary from city to city, e.g., 36% in Cebu,6% in Delhi, and 3% in Ulaanbaatar.

Between Cities and Among Neighborhoods. The type and scope of services alsodiffer between and within cities in the same region (Figure 8). Based on thehousehold surveys, a distinction can be made between (i) services provided withinareas served by water utilities and (ii) services provided outside these areas. Thedistinction contributes at least partially to the different patterns of SSPWP servicesin the survey cities (Figure 9).

HH connection Standpipe TankerReseller Water vendor

0

20

40

60

80

100

Dehli

Dhaka

Kathman

duCeb

uHCMC

Jaka

rta

Ulaanba

atarSh

are

ofSS

PWP

Mar

ket

%

Figure 8. Different Water Sources Used at City Level

0

20

40

60

80

100

Delhi

Dhaka

Kathman

duCeb

uHCMC

Jaka

rta

Ulaanb

aatar

Shangh

ai

Water Utility Own Source Others SSPWP

% o

f HH

s us

ing

serv

ice

HCMC = Ho Chi Minh City

20

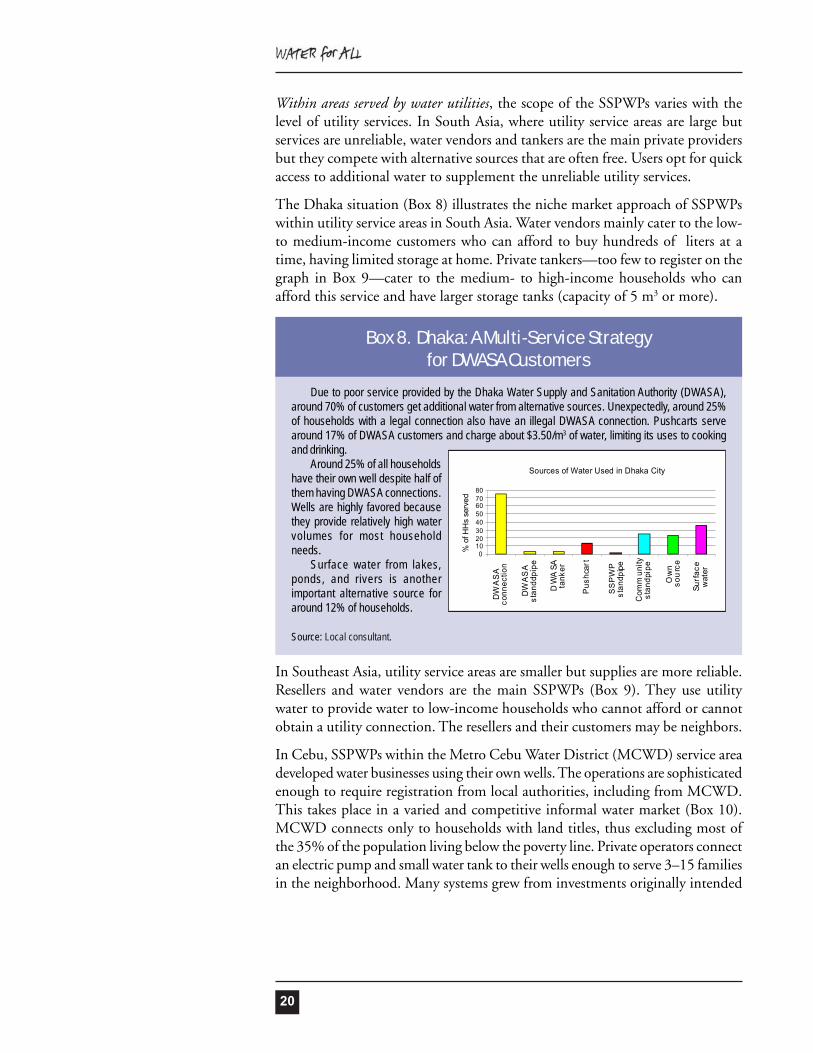

Within areas served by water utilities, the scope of the SSPWPs varies with thelevel of utility services. In South Asia, where utility service areas are large butservices are unreliable, water vendors and tankers are the main private providersbut they compete with alternative sources that are often free. Users opt for quickaccess to additional water to supplement the unreliable utility services.

The Dhaka situation (Box 8) illustrates the niche market approach of SSPWPswithin utility service areas in South Asia. Water vendors mainly cater to the low-to medium-income customers who can afford to buy hundreds of liters at atime, having limited storage at home. Private tankers—too few to register on thegraph in Box 9—cater to the medium- to high-income households who canafford this service and have larger storage tanks (capacity of 5 m3 or more).

In Southeast Asia, utility service areas are smaller but supplies are more reliable.Resellers and water vendors are the main SSPWPs (Box 9). They use utilitywater to provide water to low-income households who cannot afford or cannotobtain a utility connection. The resellers and their customers may be neighbors.

In Cebu, SSPWPs within the Metro Cebu Water District (MCWD) service areadeveloped water businesses using their own wells. The operations are sophisticatedenough to require registration from local authorities, including from MCWD.This takes place in a varied and competitive informal water market (Box 10).MCWD connects only to households with land titles, thus excluding most ofthe 35% of the population living below the poverty line. Private operators connectan electric pump and small water tank to their wells enough to serve 3–15 familiesin the neighborhood. Many systems grew from investments originally intended

Due to poor service provided by the Dhaka Water Supply and Sanitation Authority (DWASA),around 70% of customers get additional water from alternative sources. Unexpectedly, around 25%of households with a legal connection also have an illegal DWASA connection. Pushcarts servearound 17% of DWASA customers and charge about $3.50/m3 of water, limiting its uses to cookingand drinking.

Around 25% of all householdshave their own well despite half ofthem having DWASA connections.Wells are highly favored becausethey provide relatively high watervolumes for most householdneeds.

Surface water from lakes,ponds, and rivers is anotherimportant alternative source foraround 12% of households.

Source: Local consultant.

Box 8. Dhaka: A Multi-Service Strategyfor DWASA Customers

Sources of Water Used in Dhaka City

01020304050607080

DW

AS

Aco

nnec

tion

DW

AS

Ast

andd

pipe

DW

ASA

tank

er

Pus

hcar

t

stan

dpip

e

Com

mun

ityst

andp

ipe

Ow

nso

urc

e

Surf

ace

wat

er

SS

PW

P

% o

f HH

s se

rved

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

21

Around 12% of urban residents get their water from resellers. Customers are predominantlymedium low-income households (70%) who either cannot afford the connection fee or do not haveaccess to the piped system.

Resellers serve 3–5 neighbors through a secondary meter (locally made at $5–10). They arebilled according to the quantity of water used.The average quantity of water bought by the reseller’scustomers is around half the average consumption of utility customers (17.5 m3/month comparedwith 36 m3/month). The water tariff paid to the resellers is between $0.13 and $0.5/m3. Averaging$0.25/m3, this is around twice the utility’s social tariff of $0.11/m3. Ho Chi Minh Water Supply Company(HCMWSC) has developed the following block tariff system based on consumption per capita:

Consumption/month/capita Tariff/m3

< 4 m3 $0.114–6 m3 $0.176–10 m3 $0.21> 10 m3 $0.27

The utility’s block tariff system affects the reseller’s tariff, depending on the quantity of waterresold. With an average consumption of 36 m3 and 5 persons/household for those connected toHCMWSC, the consumption per capita is around 7.2 m3/month at a monthly unit tariff of $0.21/m3. Ifthis customer resells water to 3 neighbors who have a monthly consumption of around 17 m3, thetotal monthly consumption is 87 m3 corresponding to 17 m3/capita/month. Thus, the water tariff is$0.27/m3. Even with a small margin of a few cents per cubic meter, the water tariff for resellers’customers will be three times more than the social tariff.

Source: Local consultant.

Box 9. Resellers in Ho Chi Minh City

Barangay Labangon, a community of 5,500 households, is located in an areaserved by the Metro Cebu Water District (MCWD). Because of connection constraints(household too far from pipe, land title issues, etc.), many private and communitysystems have been developed and compete against each other. Households in thebarangay can freely choose from among various types of water sources: householdconnection, standpipe (private or communal), and reseller.

• 4 SSPWPs provide household connectionsservicing from 3–16 households each;

• 14 SSPWPs each serve 5–30 householdsthrough private taps;

• 21 resellers each serve 3–30 householdsthrough taps; and

• 4 communal standpipes each serve between35–45 households.

Altogether they serve around 20% of thehouseholds in the barangay.

Box 10. Merry Mix of Water Suppliers and Sources for Cebu Community

Source: Survey by University of San Carlos (Cebu), December 2002.

22

to improve only the well owner’s water supply. Generally, the operator does notcharge a connection fee. Customers pay for plumbing services, water meter, andgalvanized iron piping from their house to the operator’s house. The averagetotal cost of the materials is approximately $60. Customers pay their bills weeklyor monthly.

Outside areas served by water utilities, tankers and water vendors are the mostcommon private providers. Tankers serve mainly high-income households(example in Kathmandu, Box 11). In South Asia, water vendors get their waterfrom free sources (standpipes, traditional waterspouts, or tube wells). In SoutheastAsia, many water vendors get their water from standpipes managed by waterutilities and pay for the water they fetch. Tankers generally get their water froma natural water source (spring or river).

The field surveys revealed the emergence of local private entrepreneurs developingsmall piped networks outside utility service areas. SSPWPs build and finance thenetworks themselves and provide direct connections to households. They aremost active in Cebu (Box 12), Delhi, Dhaka and Ho Chi Minh City, and serveapproximately 750,000–1 million people in the survey cities. The approaches ofthese private operators are different in each city and are summarized in Table 7.

Municipal supply has increasingly struggled to meet the water needs of this city. Becauseresidents have become accustomed to house connection, private tankers have moved in to providedoor-to-door water delivery especially when supply from the water utility is low. The tankers mainlyserve institutions and high-income households due to their relatively high-priced water ($1.30/m3

compared with $0.08/m3 from the piped system) and the need for large capacity storage on the partof customers. Their clientele is broken down as follows: industries (33%), residences (24%), mineralwater plants (13%), hotels/restaurants (11%), hospitals and schools (10%), and offices (9%).

There are at present 35 private tanker operators with 65 tanker trucks doing business in theKathmandu valley. They supply around 775,000 m3/year, representing a $1 million turnover at about10% profit. Medium- and low-income households with little storage capacity are served by smallertankers (5 m3). All tanker operators came from the transport sector. As tankers, none of them isregistered with the government and thus not subject to price or quality regulations. The leadingcompanies among them have organized themselves into a tankers’ association and establishedwater quality standards for the private market but some customers still doubt the quality of theirwater because of their poor hygiene practices.Source: Kishore Kumar Jha (Multidisciplinary Consultants Ltd.).

Box 11. Kathmandu: Private Tankers ServeIndustries and High-Income Households

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

23

Fernando Miñoza, an engineer and entrepreneur with diverse local business interests, developeda small-scale water system in Barangay Barayan. The system started to operate in July 2002.

The owner built the system in response to requests from his employees and their immediateneighbors to provide water to their households. The design of the distribution network and technicalstandards are similar to those implemented by the Metro Cebu Water District (MCWD) in low-incomeareas. A 15-m high water reservoir with a capacity of 20 m3 serves 24 hrs/day water through a maindistribution line (a 2-inch, 400-m long galvanized iron pipe). This line is equipped with a series of 1-inch stub-outs to which 1/2-inch metered pipelines are connected. Mr. Minoza obtained the necessarypermits from the barangay (community), a business permit from the city, and a license from theNational Water Resources Board.

In the beginning, the operator encountered problems with some lot owners who refused to granthim right-of-way for the distribution pipes. However, the users themselves managed to convince thelot owners to allow the installation of pipelines at no cost on condition that these be installedunderground or only in designated areas.

The owner invested $6,000 to set up the system, inclusive of a water tank. Seventy customerswere using the system after a few months. Now, three sitios in Bacayan are served by this system.

Responding to demand, Mr Minoza plans to build another reservoir at Upper Bacayan, and, inthe near future, build another system in Pulangbato, a barangay approximately 3 kilometers fromBacayan that is not within the coverage area of MCWD.

The water tariff is $0.75/m3, and the customer is responsible for making the house connection.The customer can either purchase the needed materials (e.g., pipe, meter) from any hardware store,or from the hardware store owned by the operator himself. On average, the total cost of materials isestimated to be $60. The operator does not require any legal or administrative documentation.

Four part-time caretakers oversee the day-to-day operation of the system each servicingapproximately 17 clients. The operator believes that, at the moment, the current setup is adequate.

Monthly bills are sent to households who are required to make their payments at the office of theoperator, which is located nearby. Those who cannot settle their accounts on time are given a 2-month grace period, after which they are disconnected. But this has never happened.

Randomly-selected consumers, who were asked to comment on the services provided by theoperator, all expressed satisfaction. They said that before the system was in place, they had toqueue to fetch water from nearby public wells, which was inconvenient and time-consuming.

Customers perceived the operator’s tariff to be higher than that of the utility but said that this issomething that they would have to live with in the absence of an efficient and adequate water supplysystem. Nevertheless, they said that they hoped the operator would make an effort to make thewater safe and palatable.Source: Survey done under the direction of Fiscalino Amadora Nolasco, University of San Carlos (Cebu), 2002.

Box 12. Cebu Piped Network Operator FillsUrban Villagers’ Water Needs

Table 7. Main Characteristics of Small Piped NetworksCity Status Water Source Level of Service

Provided Water

Quality Average No.

of HHs Served

Approx. No. of Networks in the City

Cebu Legal Groundwater - HH connection 24 hrs/day - Hose connection 3–4

days/week

Untreated 75–100 5

Delhi Illegal Groundwater - HH connection 1–1.5 hrs/day

Untreated 50–700 > 100

Dhaka Illegal DWASA (illegal connection)

- Standpipe (99%) - HH connection (1%)

Untreated 9,000 1

Ho Chi Minh City

Legal Groundwater - HH connection 24 hrs/day

Treated 100–500 > 20

DWASA = Dhaka Water Supply and Sanitation Authority, HH = household

24

The study’s surveys show a correlation between SSPWP niche operations andthe city or neighborhood’s utility service and water sources. In areas where thecost of services provided by the water utility is affordable and/or alternative sourcesare readily available, water vendors and tanker trucks are not present. Relativelywell-off households buy bottled water even when the distribution networkprovides adequate coverage at a reasonable price. In cities where the cost of utilityservice is high and alternative water sources are not readily available, water vendors,resellers, and piped system operators compete with or supplement the water utility.Figure 10 slots the eight survey cities into the model introduced in Figure 4.

Figure 10. SSPWP Niche Markets in the 8 Cities

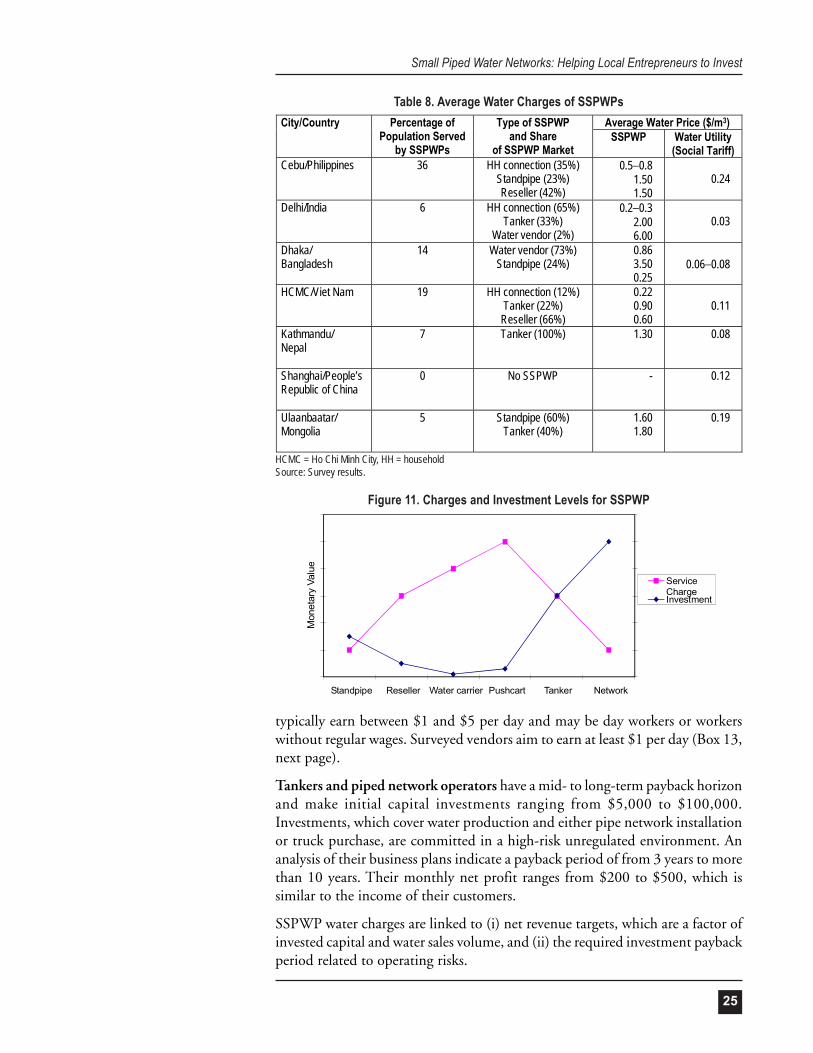

User charges by SSPWP typeSSPWP water user charges vary widely in the survey cities. However, surveyresults show that this does not indicate profiteering or exploitation on the part ofthe SSPWPs. SSPWP charges are typically higher than the social tariffs chargedby the water utility, which is to be expected given that utilities subsidize theirsocial tariffs with revenues from customers paying higher block tariffs (Table 8).Vendors (pushcart or water carrier) and tankers generally charge the most, duepartly to the small volume of water supplied. SSPWPs who have a more efficientratio of investment to volume of water sold charge less (Figure 11). Piped networkoperators, who have the highest level of investment, also supply the highestvolumes of water.

Vendors and resellers operate with short-term investment horizons, hence theirinvestments are small (< $150) and their payback periods short (< 3 months),which is based on daily payments from low-income customers. Their customers

HCMCJakarta

Cebu

DelhiKathmandu

Dhaka

Costofservice

Quality of ServiceAr

eas

wel

lsup

plie

dAr

eas

notw

ell

supp

lied

Are

asno

tsu

pplie

d

Water sources available Water sources not available

IncomeIncome+

+ +

+

Income Income

--

--

Shanghai

Ulaan-baatar

Bottled water

Water vendorsResellers

Piped networks

TankersWater vendors

HCMC = Ho Chi Minh City

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

25

typically earn between $1 and $5 per day and may be day workers or workerswithout regular wages. Surveyed vendors aim to earn at least $1 per day (Box 13,next page).

Tankers and piped network operators have a mid- to long-term payback horizonand make initial capital investments ranging from $5,000 to $100,000.Investments, which cover water production and either pipe network installationor truck purchase, are committed in a high-risk unregulated environment. Ananalysis of their business plans indicate a payback period of from 3 years to morethan 10 years. Their monthly net profit ranges from $200 to $500, which issimilar to the income of their customers.

SSPWP water charges are linked to (i) net revenue targets, which are a factor ofinvested capital and water sales volume, and (ii) the required investment paybackperiod related to operating risks.

Table 8. Average Water Charges of SSPWPsAverage Water Price ($/m3) City/Country Percentage of

Population Served by SSPWPs

Type of SSPWP and Share

of SSPWP Market SSPWP Water Utility

(Social Tariff) Cebu/Philippines 36 HH connection (35%)

Standpipe (23%) Reseller (42%)

0.5–0.8 1.50 1.50

0.24

Delhi/India 6 HH connection (65%) Tanker (33%)

Water vendor (2%)

0.2–0.3 2.00 6.00

0.03

Dhaka/ Bangladesh

14 Water vendor (73%) Standpipe (24%)

0.86 3.50 0.25

0.06–0.08

HCMC/Viet Nam 19 HH connection (12%) Tanker (22%) Reseller (66%)

0.22 0.90 0.60

0.11

Kathmandu/ Nepal

7 Tanker (100%) 1.30 0.08

Shanghai/People’s Republic of China

0 No SSPWP - 0.12

Ulaanbaatar/ Mongolia

5 Standpipe (60%) Tanker (40%)

1.60 1.80

0.19

HCMC = Ho Chi Minh City, HH = householdSource: Survey results.

Standpipe Reseller Water carrier Pushcart Tanker Network

ServiceChargeInvestment

Mon

etar

y Va

lue

Figure 11. Charges and Investment Levels for SSPWP

26

Network operators offer a better service at a lower price than vendors and resellers,but at a higher price than utilities. SSPWP (all types) water supply charges rangefrom $0.2 to $3.5/m3 whereas water charges of small piped networks in thesurvey cities range from $0.2 to $0.8/m3. SSPWPs’ charges in Ho Chi MinhCity (Figure 12) are significantly lower than in other cities.

(Box 14)with table info

A pushcart operation is generally a family business engaging three to four family members.Since the water pressure at the standpipe is generally high only at night, one member from eachprovider’s family works all through the night to fill water, and in the morning another takes over.Other family members transport water to the client households. Water is also filled during the daybut filling is slow due to low water pressure. Pushcarts charge $5–6 equivalent per cubic meter. Onthe face of it, this is expensive water compared with the “free” water from the public standpipe. Butonly small quantities of water are involved—1–2 m3 per day per pushcart—and participants in thefamily pushcart business may earn only $1–3 for each 10-hour plus working day.

Box 13. Operational Details of Pushcart Providers in Delhi

Figure 12. Average SSPWP Water Charges in Ho Chi Minh City

0.5

0.6

0.9

0.220.11

00.10.20.30.40.50.60.70.80.9

1

Pushcart Reseller Tanker Network Water Utility

Wat

er ta

riff (

in $

/m)3

a 4 hours in the morning and 4 hours in the evening.b Depends on the transport distance.c These are generally family enterprises engaging at least three members of a family.Source: Usha Raghupathi, National Institute of Urban Affairs.

1st Provider 2nd Provider 3rd Provider Area Okhla Vihar Batlahouse Ext. A.F. Enclave Size of settlement (no. of HHs) 800–1,000 1,500– 2,000 2,000–2,500 Age of settlement 18 years 15 years 18 years Provider living in the locality or not No, living nearby Yes Yes Since when providing service Last 10 years Last 2 years Last 6 years No. of clients (HHs) 40 30 50–60 Source of water Standpipe Standpipe Standpipe Hours of water availability at source/day 8 hoursa 8 hoursa 10 hours Provider's hours of work/day 12–14 hours 8–10 hours 12–14 hours Quantity of water delivered/day 1,600 to 1,800 liters 1,200 to 1,500 liters About 2,000 liters Chargesb (for 25–40-liter can) $ 0.17–20/day $ 0.12 to 0.17/day $ 0.12 to 0.2/day Type of vehicle used Tricycle Tricycle Tricycle Investment $30 $30 $30 Source of funds Own funds Loan Own funds

Average monthly earnings $ 200–300c (< $100/pers) $100–200 $200–300

Small Piped Water Networks: Helping Local Entrepreneurs to Invest

27