Embed Size (px)

Citation preview

Presented by: Michael Wayne

Small Caps -“Old World versus New Age”

GENERAL ADVICE DISCLAIMER

The information provided by Medallion Financial Group Pty Ltd (CAR 1257237) (hereafter referred to as Medallion Financial Group) to you does not constitute personal financial product advice. The information provided is of a general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

Medallion Financial Group recommends that you obtain your own independent professional advice before making any decision in relation to your particular requirements or circumstances.

Medallion Financial Group does not warrant he accuracy, completeness or currency of the information provided. Past performance of any product discussed is not indicative of future performance (We urge that caution should be exercised in assessing past performance. All financial products are subject to market forces and unpredictable events that may adversely affect their future performance).

We may at times refer to third parties. Details of these third parties have been provided solely for you to obtain further information about other relevant products and entities in the market. Medallion Financial has no control over the information third parties have, or the products or services offered, and therefore make no representations regarding the accuracy or suitability of such information, products or services. You are advised to make your own enquiries in relation to third parties. Our inclusion of any third-party content is not an endorsement of that content or the third party.

At your request, we can refer you to a comprehensive financial planning advice provider. The Financial planner will then be in a position to consider your individual objectives, your current financial situation and needs before recommending a suitable strategy that meets your specific requirements.

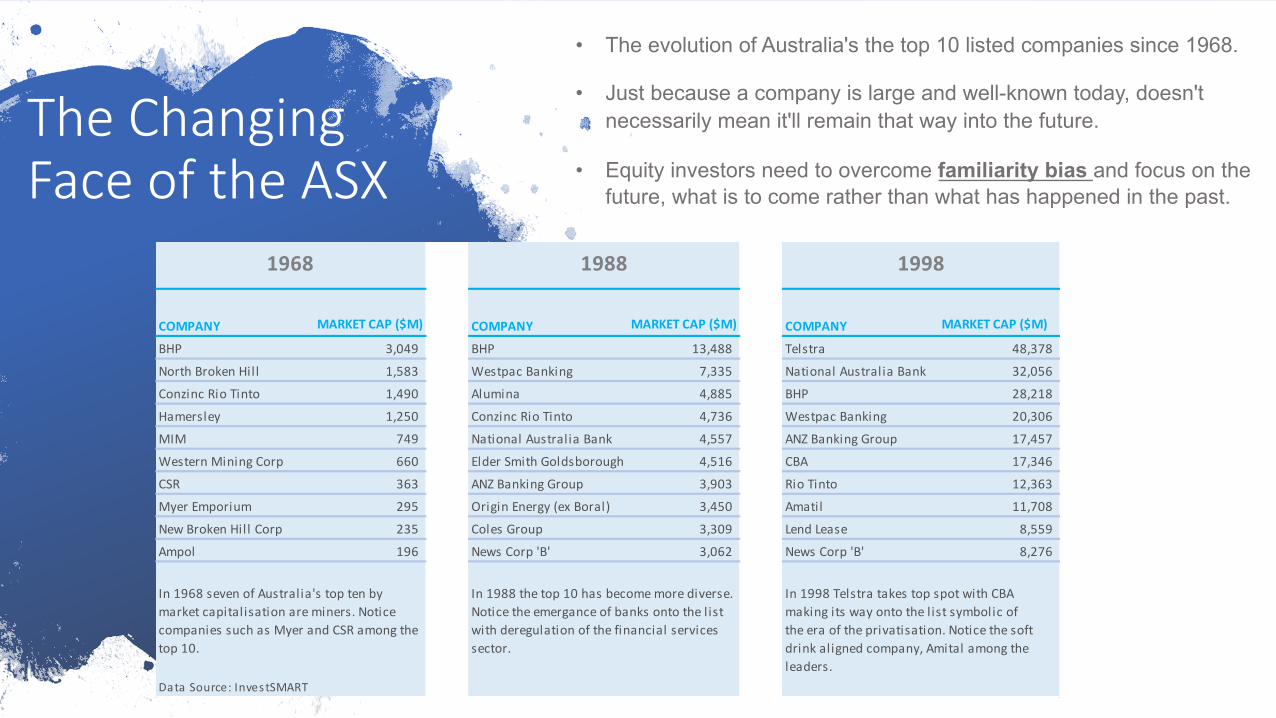

The Changing Face of the ASX

• The evolution of Australia's the top 10 listed companies since 1968.

• Just because a company is large and well-known today, doesn't necessarily mean it'll remain that way into the future.

• Equity investors need to overcome familiarity bias and focus on the future, what is to come rather than what has happened in the past.

COMPANY MARKET CAP ($M) COMPANY MARKET CAP ($M) COMPANY MARKET CAP ($M)

BHP 3,049 BHP 13,488 Telstra 48,378

North Broken Hill 1,583 Westpac Banking 7,335 National Australia Bank 32,056

Conzinc Rio Tinto 1,490 Alumina 4,885 BHP 28,218

Hamersley 1,250 Conzinc Rio Tinto 4,736 Westpac Banking 20,306

MIM 749 National Australia Bank 4,557 ANZ Banking Group 17,457

Western Mining Corp 660 Elder Smith Goldsborough 4,516 CBA 17,346

CSR 363 ANZ Banking Group 3,903 Rio Tinto 12,363

Myer Emporium 295 Origin Energy (ex Boral) 3,450 Amatil 11,708

New Broken Hill Corp 235 Coles Group 3,309 Lend Lease 8,559

Ampol 196 News Corp 'B' 3,062 News Corp 'B' 8,276

Data Source: InvestSMART

1968 1988 1998

In 1968 seven of Australia's top ten by market capitalisation are miners. Notice companies such as Myer and CSR among the top 10.

In 1988 the top 10 has become more diverse. Notice the emergance of banks onto the list with deregulation of the financial services sector.

In 1998 Telstra takes top spot with CBA making its way onto the list symbolic of the era of the privatisation. Notice the soft drink aligned company, Amital among the leaders.

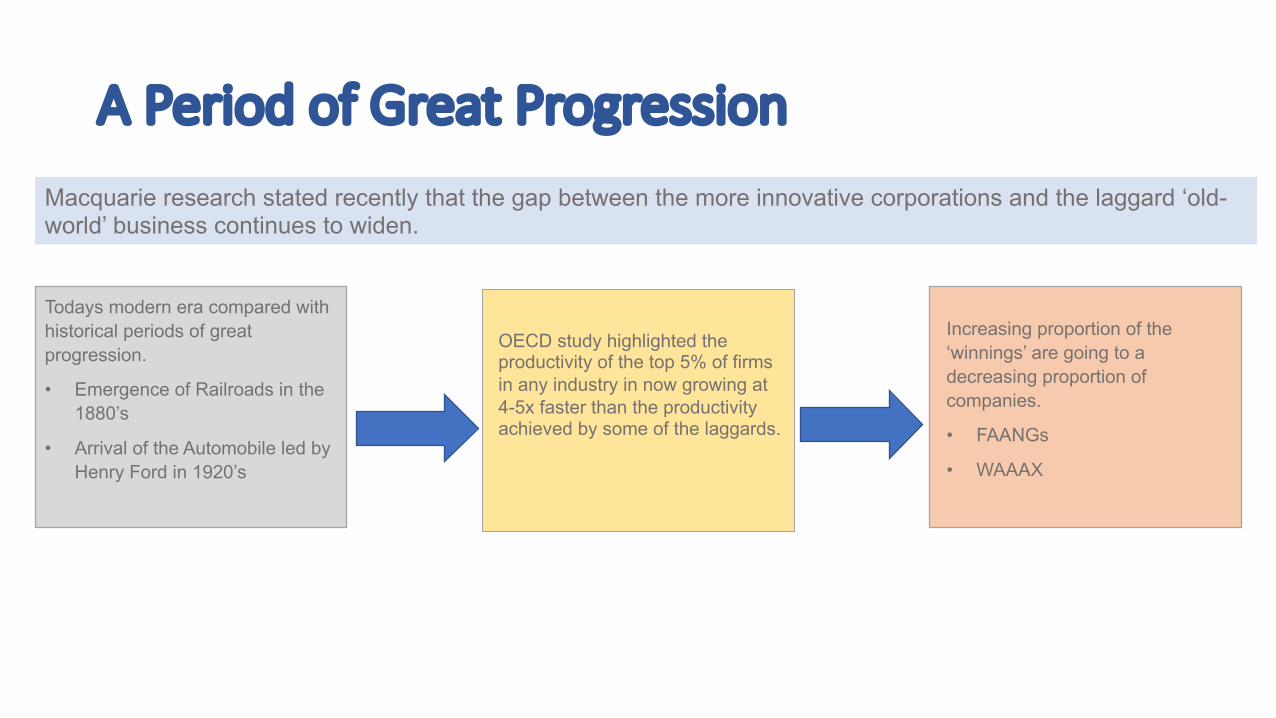

A Period of Great Progression Macquarie research stated recently that the gap between the more innovative corporations and the laggard ‘old-world’ business continues to widen.

Todays modern era compared with historical periods of great progression.

• Emergence of Railroads in the 1880’s

• Arrival of the Automobile led by Henry Ford in 1920’s

OECD study highlighted the productivity of the top 5% of firms in any industry in now growing at 4-5x faster than the productivity achieved by some of the laggards.

Increasing proportion of the ‘winnings’ are going to a decreasing proportion of companies.

• FAANGs

• WAAAX

Small Caps - Defined

• All those companies that sit outside of the largest ASX 100

• Companies in this index generally have a market cap of less than $3 billion

• Not all small caps are the same…

• Would you consider old world businesses CSR, MTS, PPT as small caps?

Small Caps - Reasons to Invest

• Significantly larger opportunity set outside of the top 100 companies

• Relatively higher growth rates, although Risk can be higher

• Successful individual stock stories

• APT, FMG etc

• Small or Large Cap Investments should be subject to the same rational review as any investment opportunity

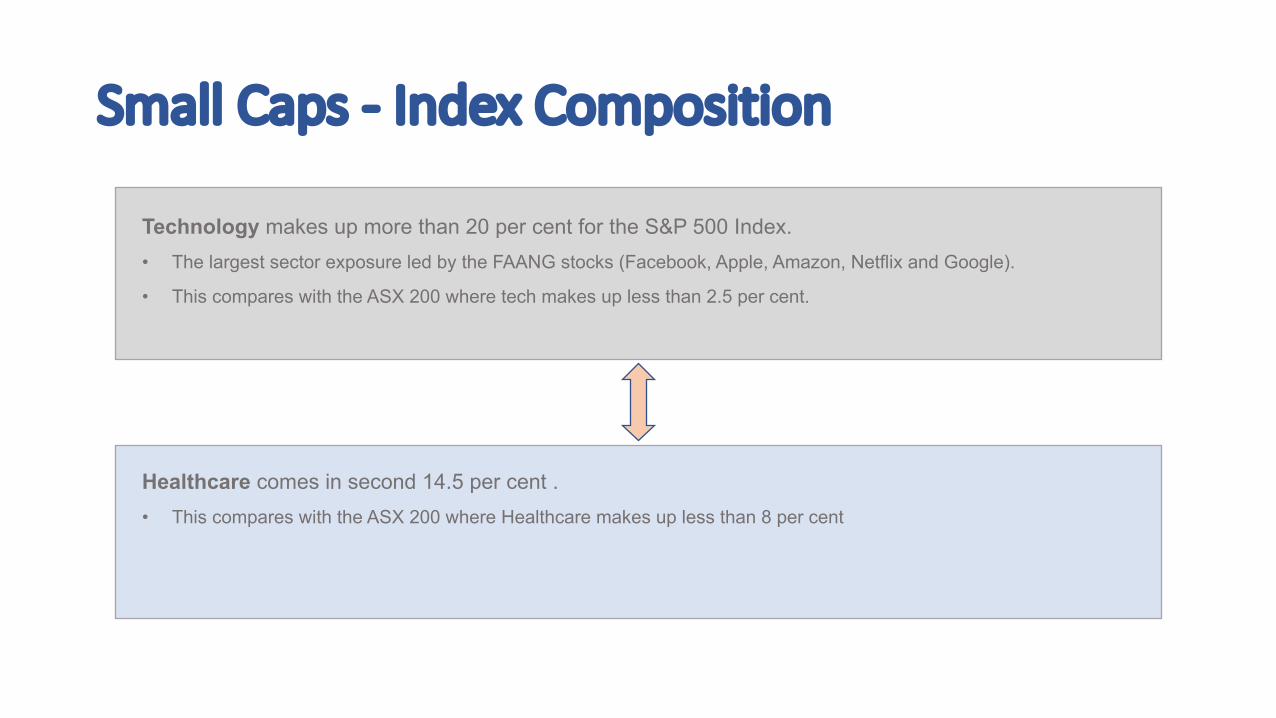

Small Caps - Index Composition

Technology makes up more than 20 per cent for the S&P 500 Index.• The largest sector exposure led by the FAANG stocks (Facebook, Apple, Amazon, Netflix and Google).

• This compares with the ASX 200 where tech makes up less than 2.5 per cent.

Healthcare comes in second 14.5 per cent .• This compares with the ASX 200 where Healthcare makes up less than 8 per cent

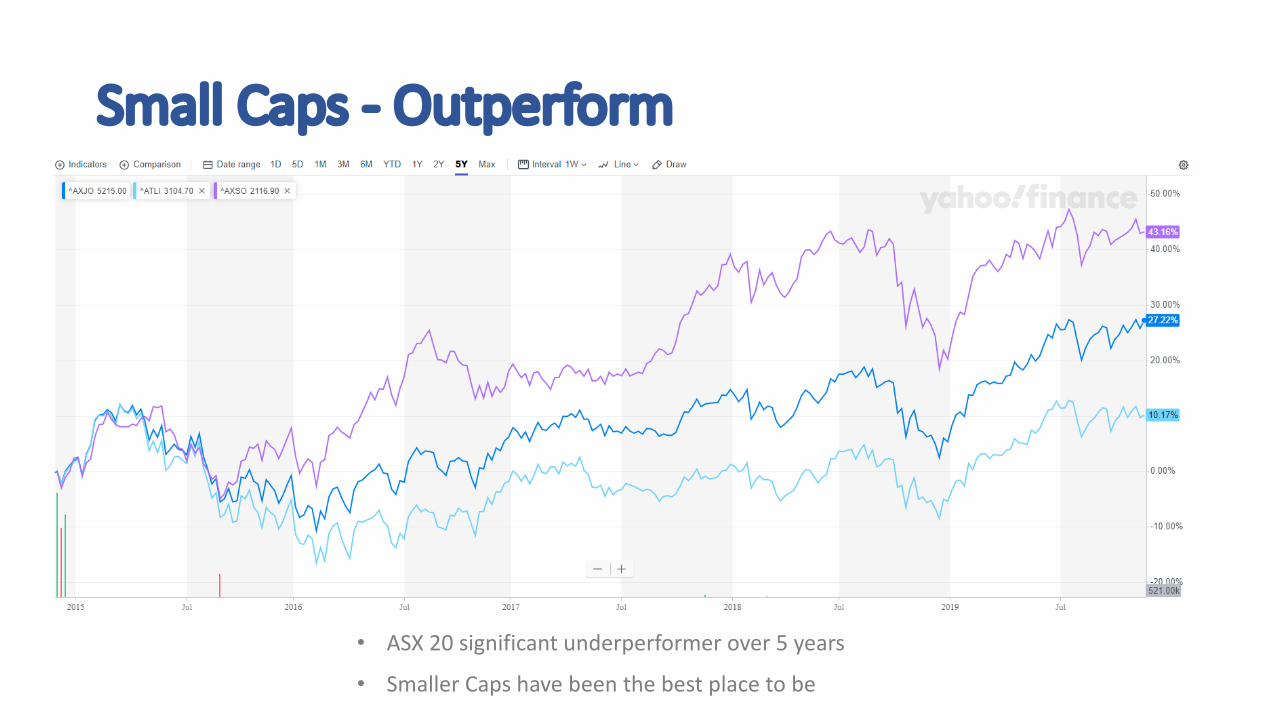

Small Caps - Outperform

• ASX 20 significant underperformer over 5 years

• Smaller Caps have been the best place to be

Small Caps - WAAAX On!

• As a basket, the WAAAX (WiseTech, Appen, Afterpay, Altium and Xero) have increased 401% in price over the last two years

o Yet only comprises less than 3.0% of the S&P/ASX All Ordinaries Index.

• In comparison, the FAANGs (Facebook, Apple, Amazon, Netflix and Alphabet (own Google)) are up just 39% o Comprise more than 20% of the S&P 500 Index.

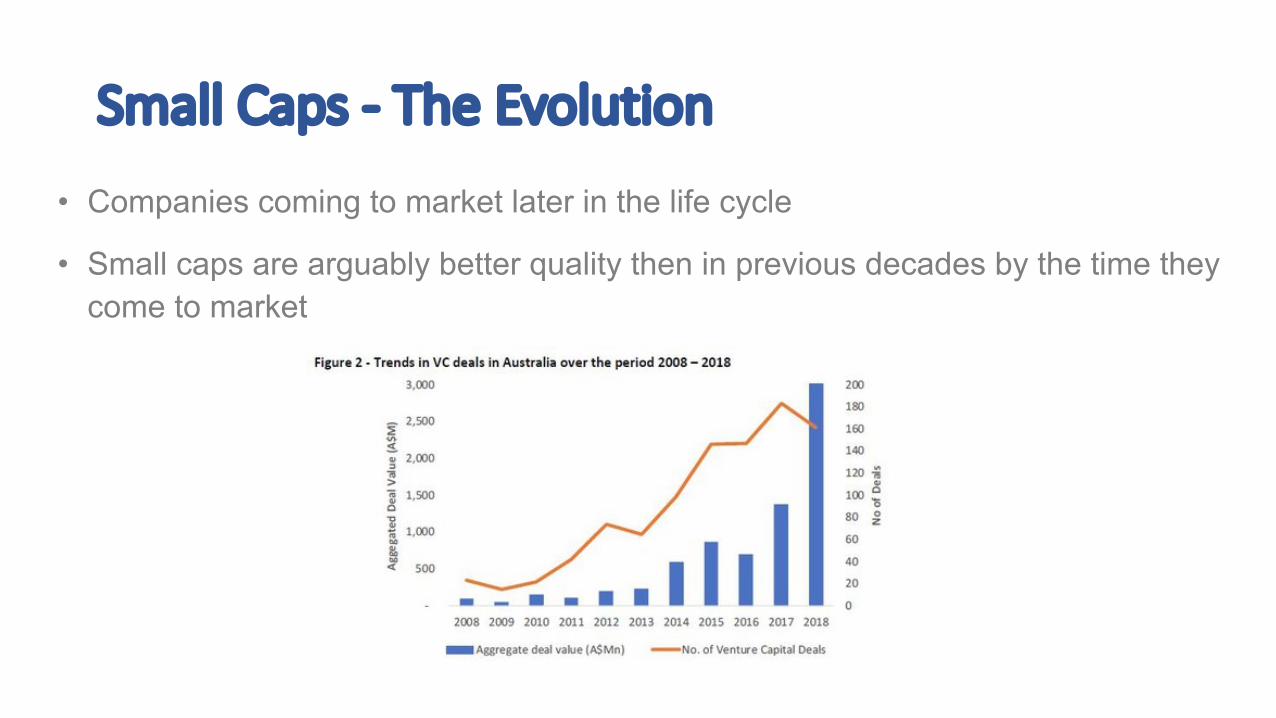

Small Caps - The Evolution

• Historically dominated by highly speculative mining companies

• Absence of an established venture capital industry

• The Australian Small Cap market built around, at times, a large number of non-revenue or profit generating companies

• These days the situation has evolved into something different

Small Caps - The Evolution

• Companies coming to market later in the life cycle

• Small caps are arguably better quality then in previous decades by the time they come to market

“Turnover is vanity; Profit is sanity; and Cash Flow is reality”

• Capital Light

• Intangible Assets

• Low Churn

• High Margins

• Free Cash Flow Generation

• Sacrifice Profitability for Growth

Traits of Quality Small Caps

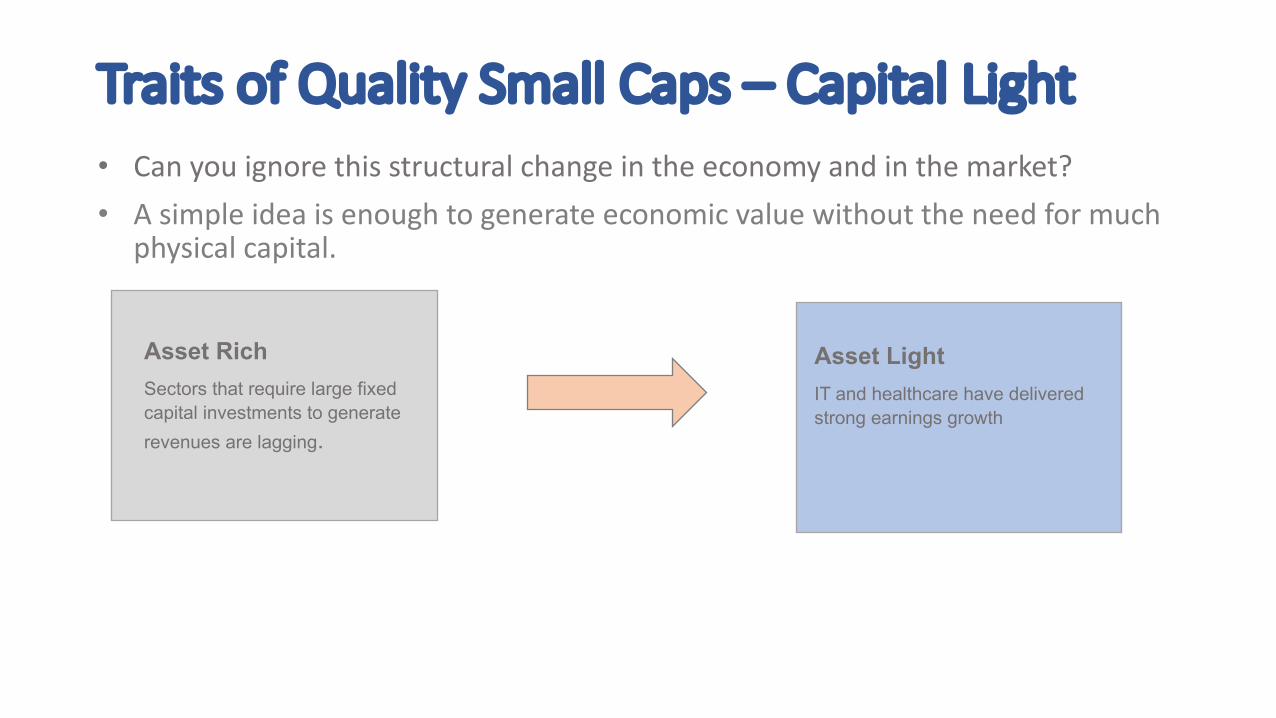

Traits of Quality Small Caps – Capital Light • Can you ignore this structural change in the economy and in the market?• A simple idea is enough to generate economic value without the need for much

physical capital.

Asset RichSectors that require large fixed capital investments to generate revenues are lagging.

Asset LightIT and healthcare have delivered strong earnings growth

Traits of Quality Small Caps – Intangible Assets• Companies with intangible assets have almost doubled their earnings and

their market cap has followed

• The market cap is unchanged for those without intangible assets

• Negative earnings growth was attributed to companies not investing early enough in intellectual capital

o Includes intangible items such as human capital and Intellectual property.

Traits of Quality Small Caps – Low Churn

• Customer churn is the scenario where a customer ceases their relationship

• The lower the churn rate the better for any business

• Negative churn rates are ideal

oWhen a company loses customers, yet the additional revenue generated from the existing customers collectively increases by more than the amount lost from to the departing customers

Traits of Quality Small Caps – High Margins

• A common trait of quality high growth businesses is that they exhibit high gross margins

• Capital light businesses with low levels of tangible assets typically have high margins

• Businesses often operate on slim margins which in the event of an economic downturn can rapidly see profits evaporate should top-line revenues compress

Traits of Quality Small Caps – Free Cash Flow

• As a result of businesses moving increasingly toward capital-light business models there has been a sizable jump in the amount of free cash flow (FCF) generation and return of capital (ROC) in the form of dividends and buybacks.

• As a general rule overtime,

Dividends & buybacks = Free Cash Flow

Traits of Quality Small Caps – Sacrifice Profitability• High-quality small caps often sacrifice profitability for growth

• Obvious example is Research and Development (R&D) or Marketing

• None of this is investment reflected on the balance sheet immediately often distorting investor perceptions of value as benefits transpire over time

• What use is a P/E ratio when earnings are depressed intentionally?

Traits of Quality Small Caps – Sacrifice Profitability• Investing money today to capture customers for the indefinite future is an

entirely rational strategy.

o Though this shows up in historic financials as increasing losses in the short term.

o The key is to determine the “profit” opportunities from those that generate only revenue.

• E.g. Software-as-a-service (Saas) firms

o When a new user signs up, they have limited immediate impact on a company's income statement, balance sheet, or cash flow.

o Yet that user may pay $15 a month for a decade, and even be willing to pay higher and higher prices overtime.

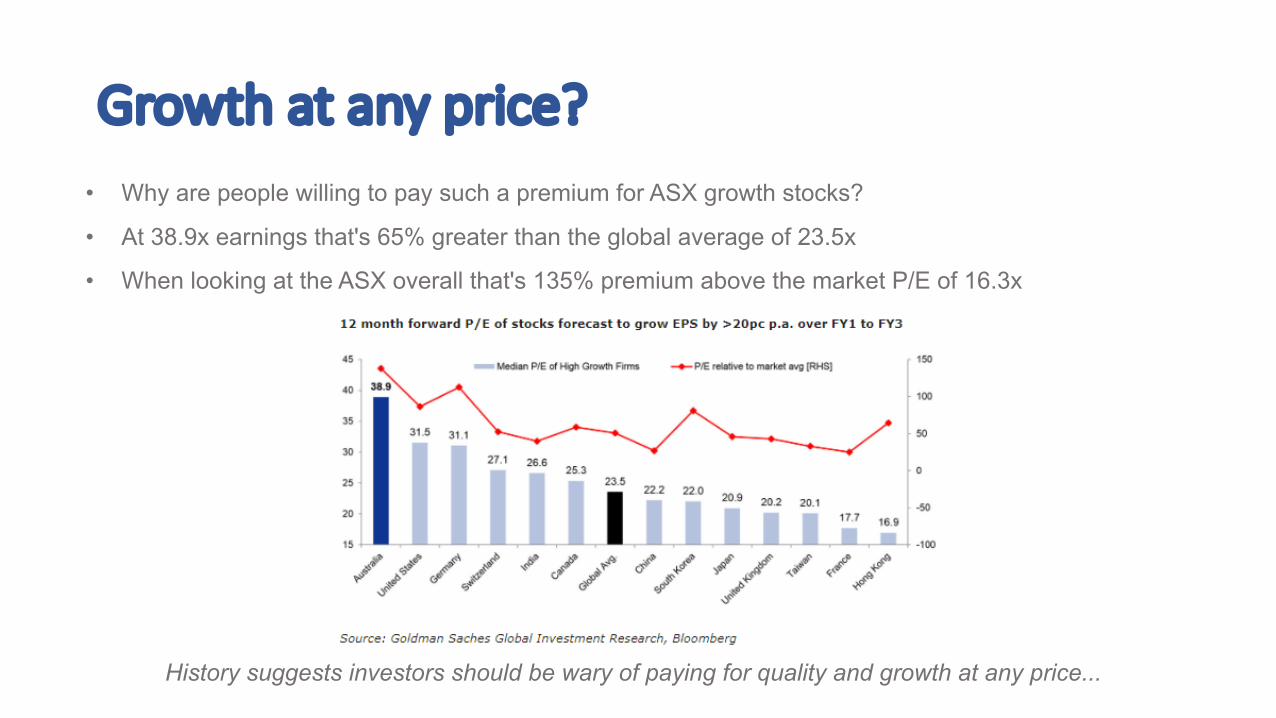

Growth at any price?• Why are people willing to pay such a premium for ASX growth stocks?

• At 38.9x earnings that's 65% greater than the global average of 23.5x

• When looking at the ASX overall that's 135% premium above the market P/E of 16.3x

History suggests investors should be wary of paying for quality and growth at any price...

Medallion’s Opinion• In summary, we are “long innovation and short incumbency” across client portfolios.

• We prefer companies that sell globally.

• At Medallion our investment decisions will continue to be guided by the undeniable trends.

• We will continue to focus our attention on the those ‘New-age’ sectors that we believe will offer the greatest chances of success.

• We believe quality businesses in growing sectors have a better probability of delivering reliable revenue, earnings, & dividend income growth overtime.

• We will continue to look for growth at a reasonable price.

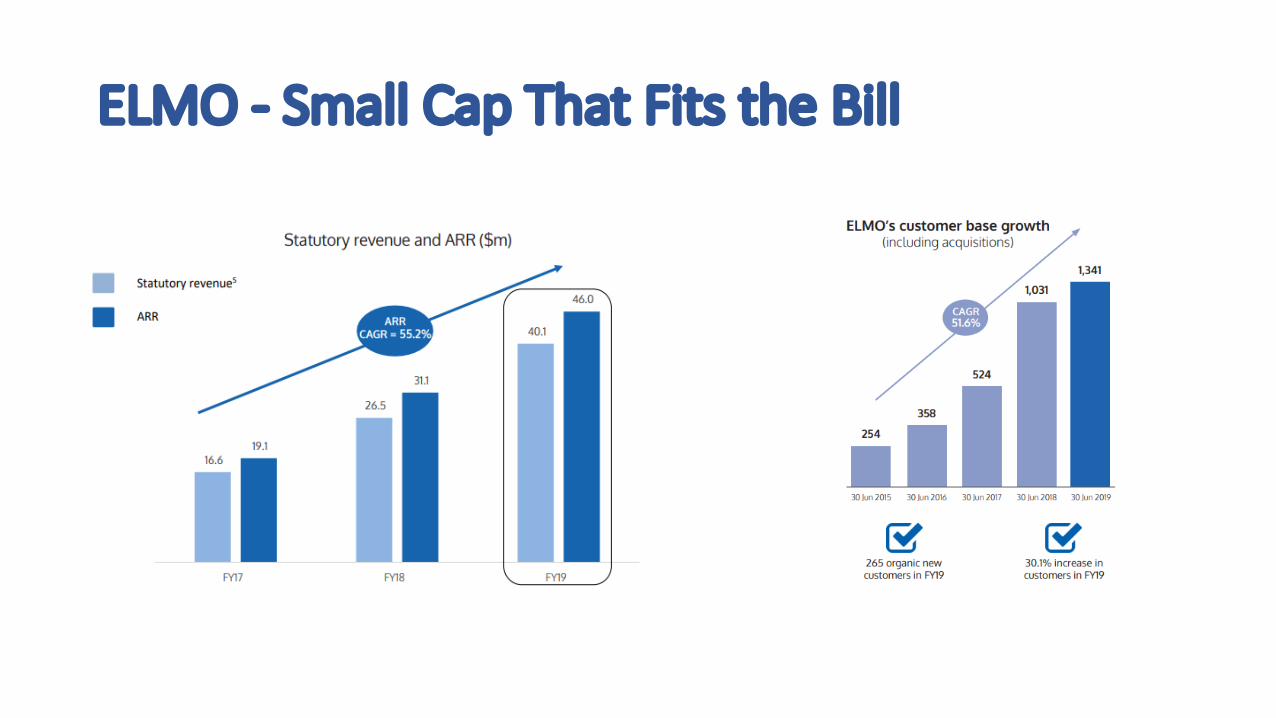

ELMO - Small Cap That Fits the Bill• Elmo is a rapidly growing HR Tech company providing cloud HR,

payroll, rostering and attendance management technology to more than 1100 companies primarily throughout Australia & NZ

• Large addressable market opportunity• Management team with ‘skin in the game’ • Low churn rate

o 110.8% customer dollar retention

• Gross profit margins of 86.6%• Organic Growth and growth through acquisition

ELMO - Small Cap That Fits the Bill